Chapter 5 Chapter 5 ORGANIZATION AND FUNCTIONING OF SECURITIES MARKETS

Chapter 5 ORGANIZATION AND FUNCTIONING OF SECURITIES MARKETS.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 5Chapter 5

ORGANIZATION AND FUNCTIONING OF SECURITIES MARKETS

1.2Investments Chapter 5

Chapter 5 Questions

What is the purpose and function of a market? What are the characteristics that determine the quality of a

market? What is the difference between a primary and secondary

capital market and how do these two markets support each other?

What is the typical underwriting organization structure for corporate stock issues?

1.3Investments Chapter 5

Chapter 5 Questions

For secondary equity markets, what are the two basic trading systems?

What are the major primary listing markets in the United States and how do they differ?

What are call markets and when are they typically used in U.S. markets?

1.4Investments Chapter 5

Chapter 5 Questions

How are national exchanges around the world linked and what is meant by “passing the book”?

What is Nasdaq and how has its growth and influence impacted the securities market?

What are the regional exchanges and what securities do they trade?

What is the third market?

1.5Investments Chapter 5

Chapter 5 Questions

What are Electronic Communications Networks (ECNs) and alternative trading systems (ATSs) and how do they differ from the primary listing markets?

What are the major types of orders available to investors and market makers?

What are the major functions of the specialist on the NYSE?

1.6Investments Chapter 5

Chapter 5 Questions

What new trading systems on the NYSE and Nasdaq have made it possible to handle the growth in U.S. trading volume?

What are the three recent innovations that contribute to competition within the U.S. equity market?

1.7Investments Chapter 5

What is a market?

The means through which buyers and sellers are brought together to aid in the transfer of goods and services

Does not require a physical location “The market” itself does not have to own the goods

and services involved Buyers and sellers benefit from the market

1.8Investments Chapter 5

Characteristics of a Good Market

Availability of past transaction informationmust be timely and accurate

Liquidity: sell quickly at a good pricemarketabilityprice continuitydepth

Transaction cost are low (Internal efficiency) Prevailing market prices reflect all relevant information

(External efficiency)

1.9Investments Chapter 5

Decimal Pricing

The movement to decimal pricing is a case study in making a market better

Benefits:Ease of understanding prices for investorsReduction in minimum bid-ask spreadsLower transaction costs through enhanced global

competition

1.10Investments Chapter 5

Organization of the Securities Market

Primary marketsNew issues

Secondary marketsOutstanding securities are bought and sold

1.11Investments Chapter 5

Primary Capital Markets : Government Bonds

Sold regularly through auctions Treasury bills: one year maturity or less Treasury notes: maturities of two to ten years Treasury bonds: original maturities of more than

ten years

1.12Investments Chapter 5

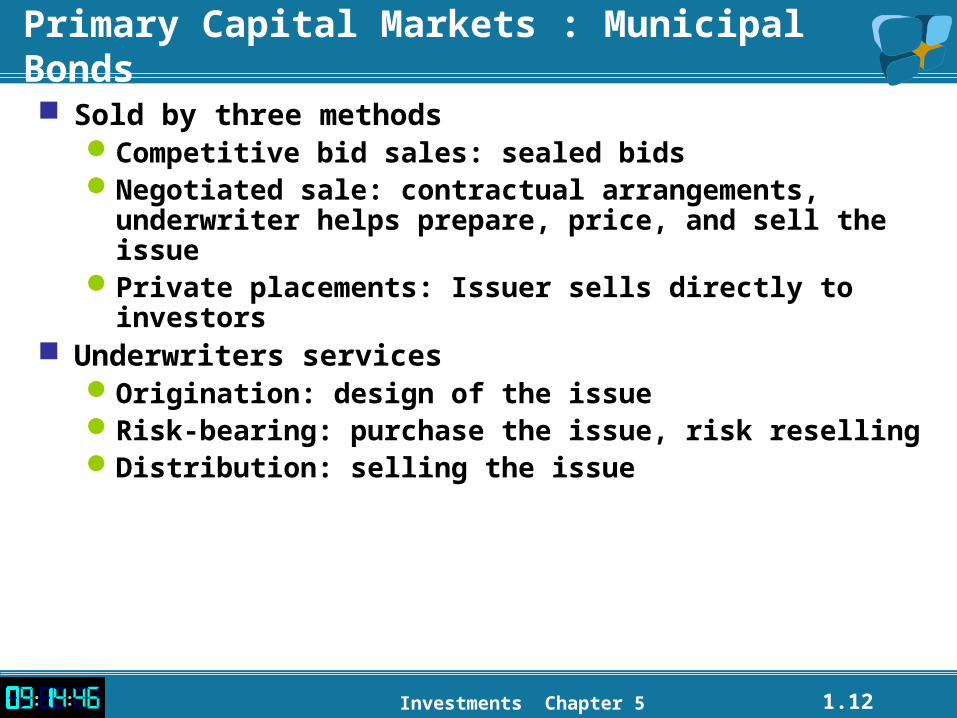

Primary Capital Markets : Municipal Bonds

Sold by three methodsCompetitive bid sales: sealed bidsNegotiated sale: contractual arrangements, underwriter

helps prepare, price, and sell the issuePrivate placements: Issuer sells directly to investors

Underwriters servicesOrigination: design of the issueRisk-bearing: purchase the issue, risk resellingDistribution: selling the issue

1.13Investments Chapter 5

Primary Capital Markets: Corporate Bonds

Negotiated arrangement with an investment banking firm who maintains a relationship with the issuing firm

Underwriting firm often organizes a syndicate for distribution

1.14Investments Chapter 5

Primary Capital Markets : Common Stock

New issues are divided into two groupsSeasoned new issues

New shares offered by firms that already have stock outstanding

Initial public offerings (IPOs)Firms selling their stock to the public for the first time

New issues normally underwritten by investment banking firms

1.15Investments Chapter 5

Relationships with Investment Bankers

1. NegotiatedMost commonFull services of underwriter

2. Competitive bidsCorporation specifies securities offered, then seeks

bidsReduced costs but also reduced services of

underwriter3. Best-efforts

Investment banker acts as broker, selling all it can at a specified price

The underwriting of corporate issues typically takes three forms:

1.16Investments Chapter 5

Introduction of Rule 415

Shelf registration: Allows firms to register securities and sell them

piecemeal over the next two years Increased flexibility for timing issues Reduces registration fees and expenses Mostly used for bond sales

1.17Investments Chapter 5

Private Placements and Rule 144A

Firms sells to a small group of institutional investors, with some assistance of an investment banker

Lower issuing costs than public offering Extensive registration not required Issues can trade among large, sophisticated

investors

1.18Investments Chapter 5

Secondary Markets

Involves the trading of issues that are already outstanding

Provide a means obtaining cash for sellers

Provide buyers with more investment choices

1.19Investments Chapter 5

Why Secondary Markets Are Important

Provide liquidity to investors who acquire securities in the primary marketHelps issuers raise needed funds in the primary market

since investors want liquidity

Help determine market pricing for new issues

1.20Investments Chapter 5

Secondary Bond Markets

Secondary market for U.S. government and municipal bondsU.S. government bonds traded by bond dealers who

specialize in these issuesBanks and investment firms make markets in municipal bond

issues Secondary corporate bond market

Traded in an OTC market by bond dealersA much more limited market than for stock issues

1.21Investments Chapter 5

Financial Futures

Bond futures contracts allow the holder to either buy or sell a specific bond issue at a specific price on a future date

Bond futures are traded in separate marketsChicago Board of Trade (CBOT)Chicago Mercantile Exchange (CME)

1.22Investments Chapter 5

Secondary Equity Markets

Basic Trading SystemsPure auction market

Buyers “bid” and sellers “ask”Buy and sell orders are matched at a central locationPrice driven market: trades are made by determining the highest

bid and the lowest ask

Dealer marketDealers buy shares (at the bid price) and sell shares (at the ask

price) from their own inventoryDealers compete against each other

1.23Investments Chapter 5

Call Versus Continuous Markets

Call markets trade individual stocks at specified times to gather all orders and determine a single price to satisfy the most ordersUsed for opening prices on NYSE if orders build up

overnight or after trading is suspended Continuous markets trade any time the market is

open

1.24Investments Chapter 5

Classification of U.S. Secondary Equity Markets Primary Market Listings Regional Stock Exchanges The Third Market Alternative Trading Systems

1.25Investments Chapter 5

Primary Market Listings

Large number of listed securities Listing often seen as a sign of prestige Wide geographic dispersion of listed firms Diverse clientele of buyers and sellers Firms wanting to list must meet listing

requirements

1.26Investments Chapter 5

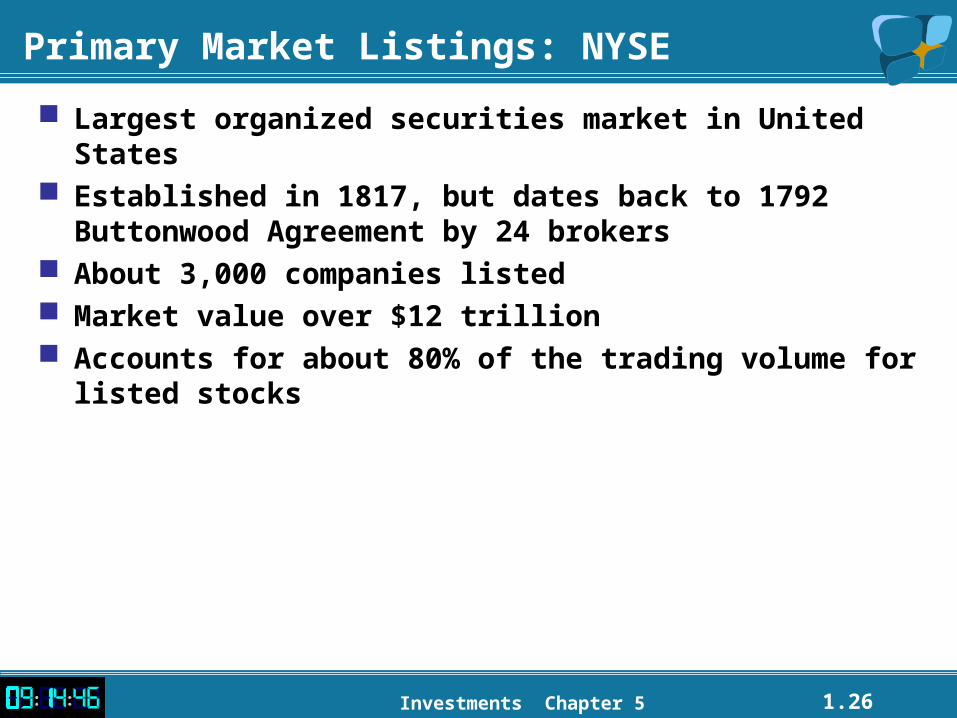

Primary Market Listings: NYSE

Largest organized securities market in United States Established in 1817, but dates back to 1792 Buttonwood

Agreement by 24 brokers About 3,000 companies listed Market value over $12 trillion Accounts for about 80% of the trading volume for listed

stocks

1.27Investments Chapter 5

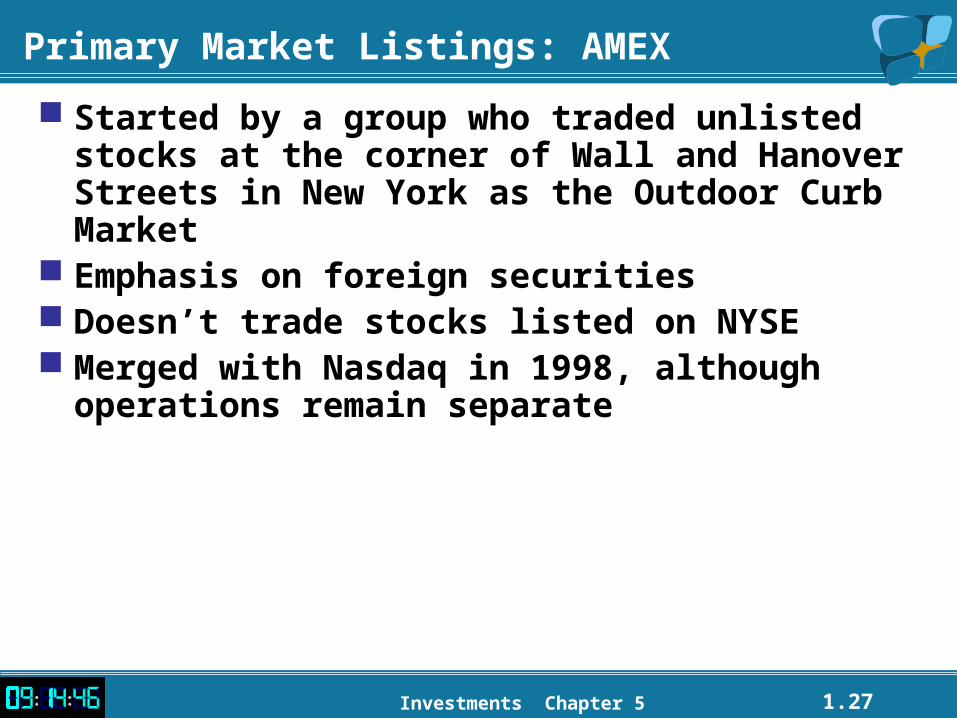

Primary Market Listings: AMEX

Started by a group who traded unlisted stocks at the corner of Wall and Hanover Streets in New York as the Outdoor Curb Market

Emphasis on foreign securities Doesn’t trade stocks listed on NYSE Merged with Nasdaq in 1998, although operations

remain separate

1.28Investments Chapter 5

Primary Market Listings: Global Stock Exchanges

Tokyo Stock Exchange (TSE) London Stock Exchange (LSE) Other National Exchanges

Frankfurt, Toronto, Paris

New exchanges in emerging countriesRussia, Poland, China, Hungary, Peru, Sri Lanka

1.29Investments Chapter 5

Primary Market Listings: Global Stock Exchanges

Trend toward consolidation of exchanges Economies of scale, especially in terms of the required

technologyLiquidity is enhanced with more firms trading

Larger firms dual-listed on a U.S. exchangeMust meet listing requirements of both

Strong exchanges abroad enable continuous global trading for firms

1.30Investments Chapter 5

The Global Twenty-four Hour Market

Investment firms “pass the book” around the world to maintain nearly continuous trading by utilizing markets at Tokyo, London, and New York

This means that the markets are increasingly interrelated, moving toward a single world market

1.31Investments Chapter 5

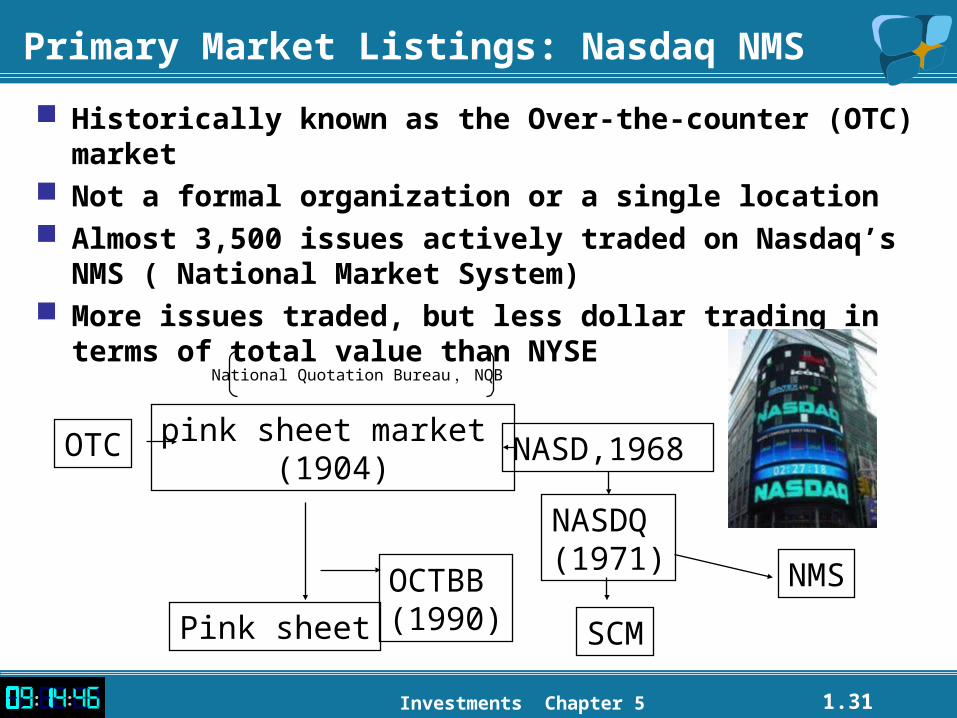

Primary Market Listings: Nasdaq NMS

Historically known as the Over-the-counter (OTC) market Not a formal organization or a single location Almost 3,500 issues actively traded on Nasdaq’s NMS

( National Market System) More issues traded, but less dollar trading in terms of total

value than NYSE

OTC NASD,1968

NASDQ(1971)

OCTBB(1990)

pink sheet market (1904)

National Quotation Bureau , NQB

NMS

SCMPink sheet

1.32Investments Chapter 5

Primary Market Listings: Nasdaq NMS

OperationsAny stock may be traded as long as it has a willing

market maker to act a dealerNasdaq is a negotiated market with investors

potentially dealing directly with dealers

1.33Investments Chapter 5

Primary Market Listings: Nasdaq NMS

The Nasdaq SystemNational Association of Security Dealers Automated

Quotation systemDealers may elect to make markets in stocksAverage of about 8 dealers per stock in 2003Three levels of quotations available

Level 1 shows a median representative quoteLevel 2 shows quotes by all market makersLevel 3 is for Nasdaq market makers to change their quotes shown

1.34Investments Chapter 5

Primary Market Listings: Nasdaq NMS

Listing Requirements for Nasdaq Two lists

National Market System (NMS)Regular Nasdaq

Must meet at least one standard for initial and continued listing See Exhibit 6.6

Making trades Broker determines which dealer has the best price (lowest

ask price/highest bid price)

1.35Investments Chapter 5

Primary Market Listings: Nasdaq

Other Nasdaq Market SegmentsThe Nasdaq Small-Cap Market (SCM)

More lenient listing requirements

The Nasdaq OTC Electronic Bulletin BoardReport service for smaller stocks

The National Quotation Bureau (NQB) Pink SheetsPrice quotation sheets for smaller stocks

1.36Investments Chapter 5

Regional Exchanges

Provide secondary markets for stocks not listed on a major exchangeListing requirements vary

Some regional exchanges list issues also listed on a national exchange

Regional Exchanges in United StatesChicago, Boston, Pacific (San Francisco/Los Angeles),

Philadelphia, Cincinnati

1.37Investments Chapter 5

Third Market

Dealer and broker trading of shares listed on an exchange away from the exchange

Mostly well known stocks May be important to investors particularly when the

exchange is closed or when trading is suspended on the exchange

Success depends on relative costs of transactions compared to the exchange

1.38Investments Chapter 5

Alternative Trading Systems (The Fourth Market) Area of great innovation Electronic Communication Networks (ECNs)

Buy and sell orders are matched via computer, mainly for retail and small institutional trading

Electronic Crossing Systems (ECSs)Electronic means for matching larger buy and sell

orders

1.39Investments Chapter 5

Detailed Analysis of Exchange Markets

Listed exchange markets have evolved into rather unique institutions; they can be described with a number of attributes:

Exchange Membership Major Types of Orders Exchange Market Makers

1.40Investments Chapter 5

Exchange Membership

Four categories of membership: Specialists

Maintain an orderly market in a stock Commission brokers

Member firm employees executing orders for clients of the firm

Floor brokersIndependent brokers who work for other brokers

Registered tradersMembers who buy and sell for their own accounts

1.41Investments Chapter 5

Major Types of Orders

Market ordersBuy or sell at the best current price

Limit ordersOrder specifies the buy or sell priceTime specifications for order may vary

Instantaneous - “fill or kill”, part of a day, a full day, several days, a week, a month, or good until canceled (GTC)

1.42Investments Chapter 5

Major Types of Orders

Short salesSell overpriced stock that you don’t own and purchase

it back later (at a lower price)Borrow the stock from another investor (through your

broker)Can only be made on an uptick tradeMust pay any dividends to lenderMargin requirements apply

1.43Investments Chapter 5

Major Types of Orders

Special OrdersStop loss

Conditional market order to sell stock if it drops to a given price

Does not guarantee price you will get upon saleMarket disruptions can cancel such orders

Stop buy orderInvestor who sold short may want to limit loss if stock

increases in price

1.44Investments Chapter 5

Major Types of Orders

Buying on Margin: On any type order, instead of paying 100% cash, borrow a

portion of the transaction, using the stock as collateral Interest rate is based on the call money rate from a bank Regulations limit proportion borrowed and the investor’s

equity percentage (margin)Margin requirements are from 50% up

Changes in price affect investor’s equity

1.45Investments Chapter 5

Major Types of Orders

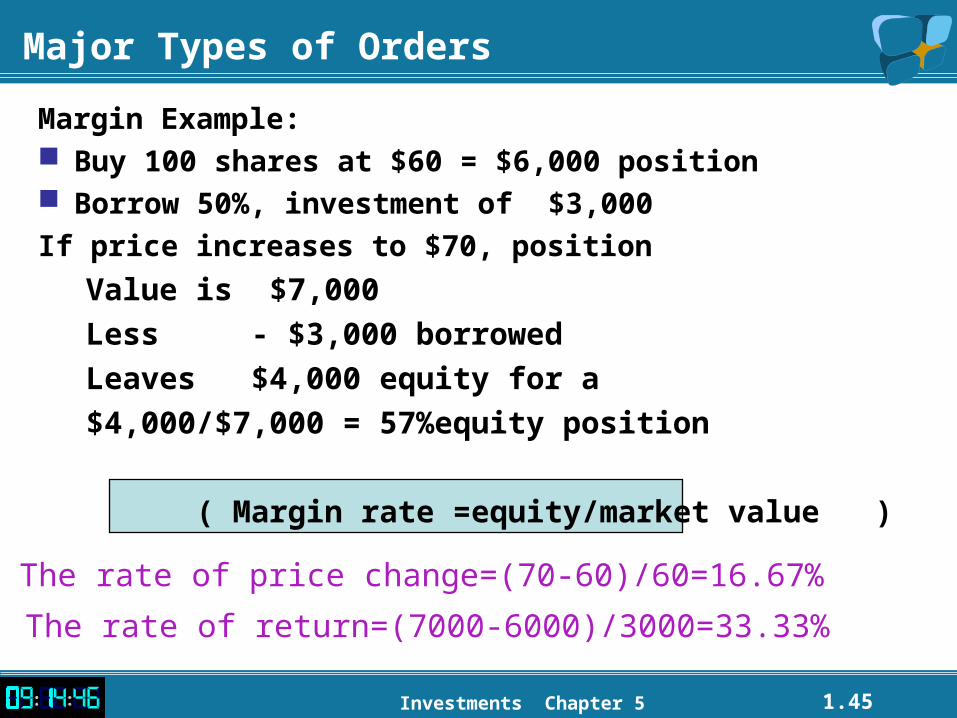

Margin Example: Buy 100 shares at $60 = $6,000 position Borrow 50%, investment of $3,000

If price increases to $70, position

Value is $7,000

Less - $3,000 borrowed

Leaves $4,000 equity for a

$4,000/$7,000 = 57%equity position

( Margin rate =equity/market value )

The rate of return=(7000-6000)/3000=33.33%

The rate of price change=(70-60)/60=16.67%

1.46Investments Chapter 5

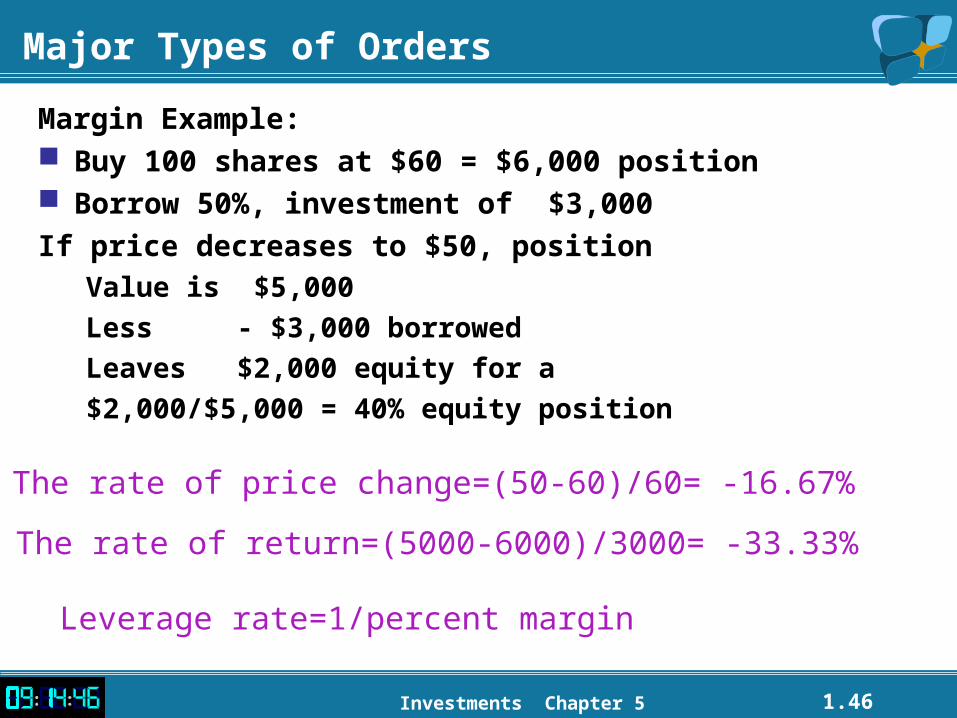

Major Types of Orders

Margin Example: Buy 100 shares at $60 = $6,000 position Borrow 50%, investment of $3,000

If price decreases to $50, positionValue is $5,000

Less - $3,000 borrowed

Leaves $2,000 equity for a

$2,000/$5,000 = 40% equity position

Leverage rate=1/percent margin

The rate of return=(5000-6000)/3000= -33.33%

The rate of price change=(50-60)/60= -16.67%

1.47Investments Chapter 5

Major Types of Orders

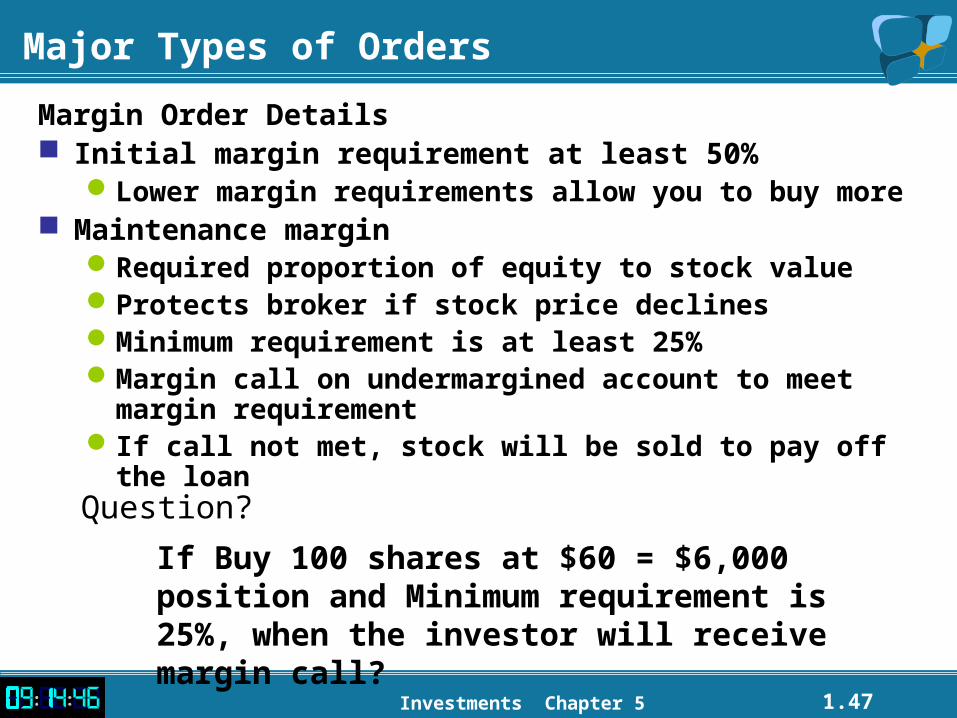

Margin Order Details Initial margin requirement at least 50%

Lower margin requirements allow you to buy more Maintenance margin

Required proportion of equity to stock valueProtects broker if stock price declinesMinimum requirement is at least 25%Margin call on undermargined account to meet margin

requirementIf call not met, stock will be sold to pay off the loan

If Buy 100 shares at $60 = $6,000 position and Minimum requirement is 25%, when the investor will receive margin call?

Question?

1.48Investments Chapter 5

Exchange Market Makers

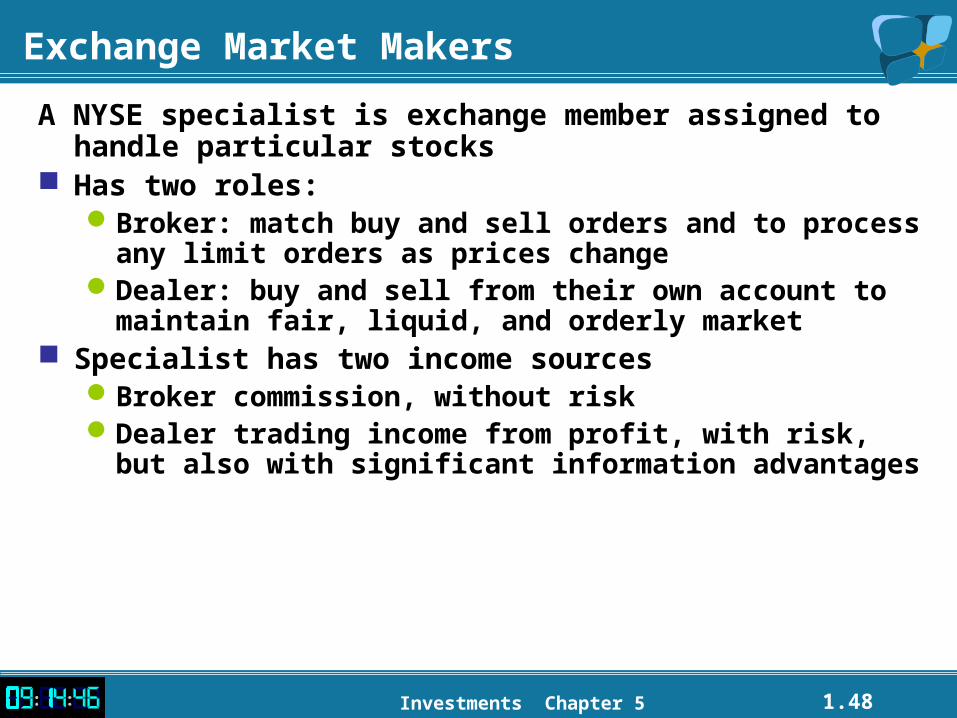

A NYSE specialist is exchange member assigned to handle particular stocks

Has two roles:Broker: match buy and sell orders and to process any limit

orders as prices changeDealer: buy and sell from their own account to maintain fair,

liquid, and orderly market Specialist has two income sources

Broker commission, without riskDealer trading income from profit, with risk, but also with

significant information advantages

Related Documents