Chapter 4: Leverage Analysis 2015 1 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College) Advanced Financial Management Bachelors of Business (Specialized in Finance) – Study Notes & Tutorial Questions Chapter 4: Leverage Analysis

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 4: Leverage Analysis 2015

1 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Advanced Financial Management

Bachelors of Business (Specialized in

Finance) – Study Notes & Tutorial

Questions

Chapter 4: Leverage Analysis

Chapter 4: Leverage Analysis 2015

2 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

INTRODUCTION

Financial decision is one of the integral and important parts of financial management in any kind

of business concern. A sound financial decision must consider the board coverage of the

financial mix (Capital Structure), total amount of capital (capitalization) and cost of capital (Ko).

Capital structure is one of the significant things for the management, since it influences the debt

equity mix of the business concern, which affects the shareholder’s return and risk. Hence,

deciding the debt-equity mix plays a major role in the part of the value of the company and

market value of the shares. The debt equity mix of the company can be examined with the help

of leverage.

The concept of leverage is discussed in this part. Types and effects of leverage are discussed in

the part of EBIT and EPS.

Meaning of Leverage

The term leverage refers to an increased means of accomplishing some purpose. Leverage is

used to lifting heavy objects, which may not be otherwise possible. In the financial point of view,

leverage refers to furnish the ability to use fixed cost assets or funds to increase the return to its

shareholders.

Definition of Leverage

James Horne has defined leverage as, “the employment of an asset or fund for which the firm

pays a fixed cost or fixed return.

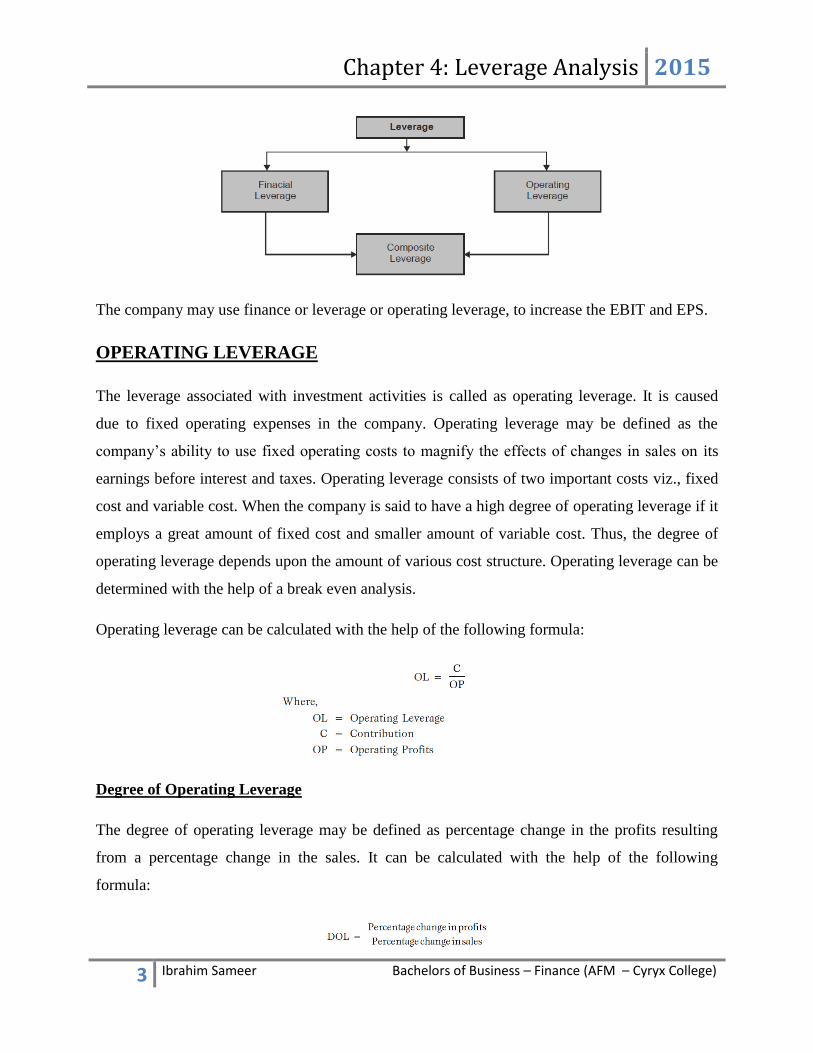

Types of Leverage

Leverage can be classified into three major headings according to the nature of the finance mix

of the company.

Chapter 4: Leverage Analysis 2015

3 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

The company may use finance or leverage or operating leverage, to increase the EBIT and EPS.

OPERATING LEVERAGE

The leverage associated with investment activities is called as operating leverage. It is caused

due to fixed operating expenses in the company. Operating leverage may be defined as the

company’s ability to use fixed operating costs to magnify the effects of changes in sales on its

earnings before interest and taxes. Operating leverage consists of two important costs viz., fixed

cost and variable cost. When the company is said to have a high degree of operating leverage if it

employs a great amount of fixed cost and smaller amount of variable cost. Thus, the degree of

operating leverage depends upon the amount of various cost structure. Operating leverage can be

determined with the help of a break even analysis.

Operating leverage can be calculated with the help of the following formula:

Degree of Operating Leverage

The degree of operating leverage may be defined as percentage change in the profits resulting

from a percentage change in the sales. It can be calculated with the help of the following

formula:

Chapter 4: Leverage Analysis 2015

4 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Uses of Operating Leverage

Operating leverage is one of the techniques to measure the impact of changes in sales which lead

for change in the profits of the company. If any change in the sales, it will lead to corresponding

changes in profit. Operating leverage helps to identify the position of fixed cost and variable

cost. Operating leverage measures the relationship between the sales and revenue of the company

during a particular period.

Operating leverage helps to understand the level of fixed cost which is invested in the operating

expenses of business activities. Operating leverage describes the overall position of the fixed

operating cost.

Chapter 4: Leverage Analysis 2015

5 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

FINANCIAL LEVERAGE

Leverage activities with financing activities is called financial leverage. Financial leverage

represents the relationship between the company’s earnings before interest and taxes (EBIT) or

operating profit and the earning available to equity shareholders.

Financial leverage is defined as “the ability of a firm to use fixed financial charges to magnify

the effects of changes in EBIT on the earnings per share”. It involves the use of funds obtained at

a fixed cost in the hope of increasing the return to the shareholders.

“The use of long-term fixed interest bearing debt and preference share capital along with share

capital is called financial leverage or trading on equity”.

Financial leverage may be favourable or unfavourable depends upon the use of fixed cost funds.

Favourable financial leverage occurs when the company earns more on the assets purchased with

the funds, then the fixed cost of their use. Hence, it is also called as positive financial leverage.

Unfavourable financial leverage occurs when the company does not earn as much as the funds

cost. Hence, it is also called as negative financial leverage.

Financial leverage can be calculated with the help of the following formula:

Degree of Financial Leverage

Degree of financial leverage may be defined as the percentage change in taxable profit as a result

of percentage change in earnings before interest and tax (EBIT). This can be calculated by the

following formula

Chapter 4: Leverage Analysis 2015

6 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Alternative Definition of Financial Leverage

According to Gitmar, “financial leverage is the ability of a firm to use fixed financial changes to

magnify the effects of change in EBIT and EPS”.

Uses of Financial Leverage

Financial leverage helps to examine the relationship between EBIT and EPS. Financial leverage

measures the percentage of change in taxable income to the percentage change in EBIT.

Financial leverage locates the correct profitable financial decision regarding capital structure of

the company. Financial leverage is one of the important devices which is used to measure the

fixed cost proportion with the total capital of the company.

If the firm acquires fixed cost funds at a higher cost, then the earnings from those assets, the

earning per share and return on equity capital will decrease. The impact of financial leverage can

be understood with the help of the following exercise.

Chapter 4: Leverage Analysis 2015

7 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

DISTINGUISH BETWEEN OPERATING LEVERAGE AND FINANCIAL

LEVERAGE

EBIT - EPS Break even chart for three different financing alternatives

Chapter 4: Leverage Analysis 2015

8 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Financial BEP

It is the level of EBIT which covers all fixed financing costs of the company. It is the level of

EBIT at which EPS is zero.

Indifference Point

It is the point at which different sets of debt ratios (percentage of debt to total capital employed

in the company) gives the same EPS.

COMBINED LEVERAGE

When the company uses both financial and operating leverage to magnification of any change in

sales into a larger relative changes in earning per share. Combined leverage is also called as

composite leverage or total leverage.

Combined leverage express the relationship between the revenue in the account of sales and the

taxable income.

Combined leverage can be calculated with the help of the following formulas:

Degree of Combined Leverage

The percentage change in a firm’s earning per share (EPS) results from one percent change in

sales. This is also equal to the firm’s degree of operating leverage (DOL) times its degree of

financial leverage (DFL) at a particular level of sales.

Chapter 4: Leverage Analysis 2015

9 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

WORKING CAPITAL LEVERAGE

One of the new models of leverage is working capital leverage which is used to locate the

investment in working capital or current assets in the company.

Working capital leverage measures the sensitivity of return in investment of charges in the level

of current assets.

………………… END………………...

Chapter 4: Leverage Analysis 2015

10 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

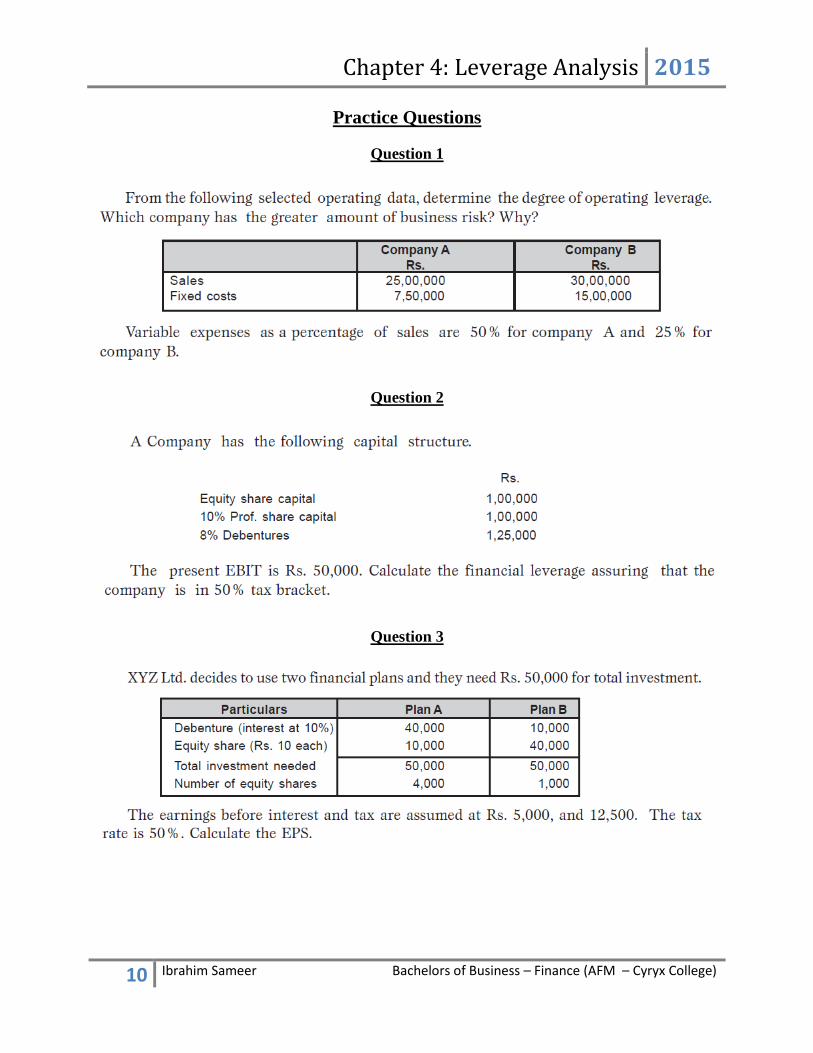

Practice Questions

Question 1

Question 2

Question 3

Chapter 4: Leverage Analysis 2015

11 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

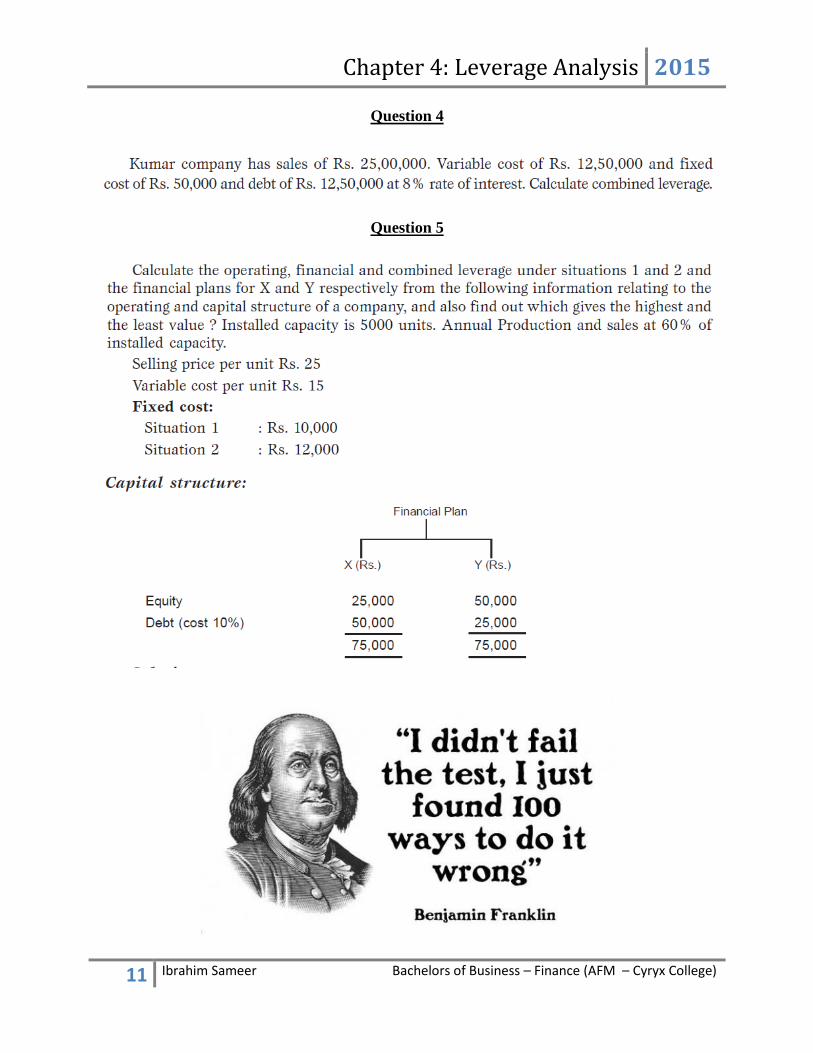

Question 4

Question 5

Chapter 4: Leverage Analysis 2015

12 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 6

Question 7

Chapter 4: Leverage Analysis 2015

13 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

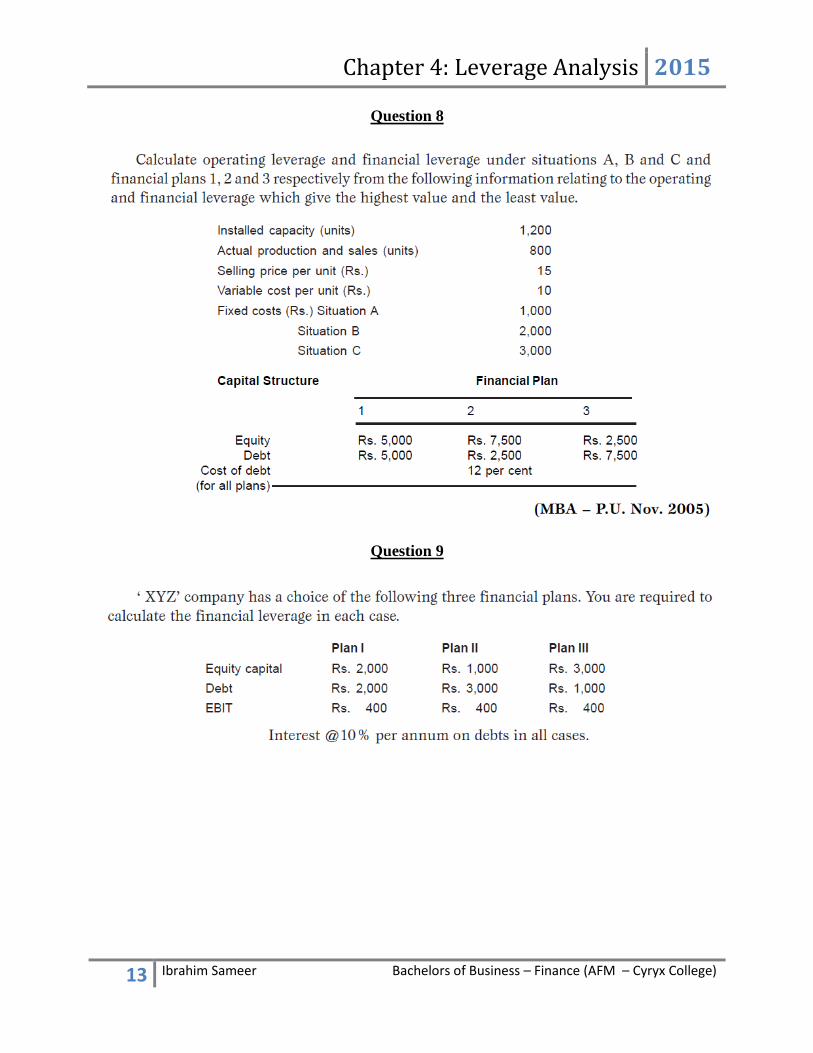

Question 8

Question 9

Chapter 4: Leverage Analysis 2015

14 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

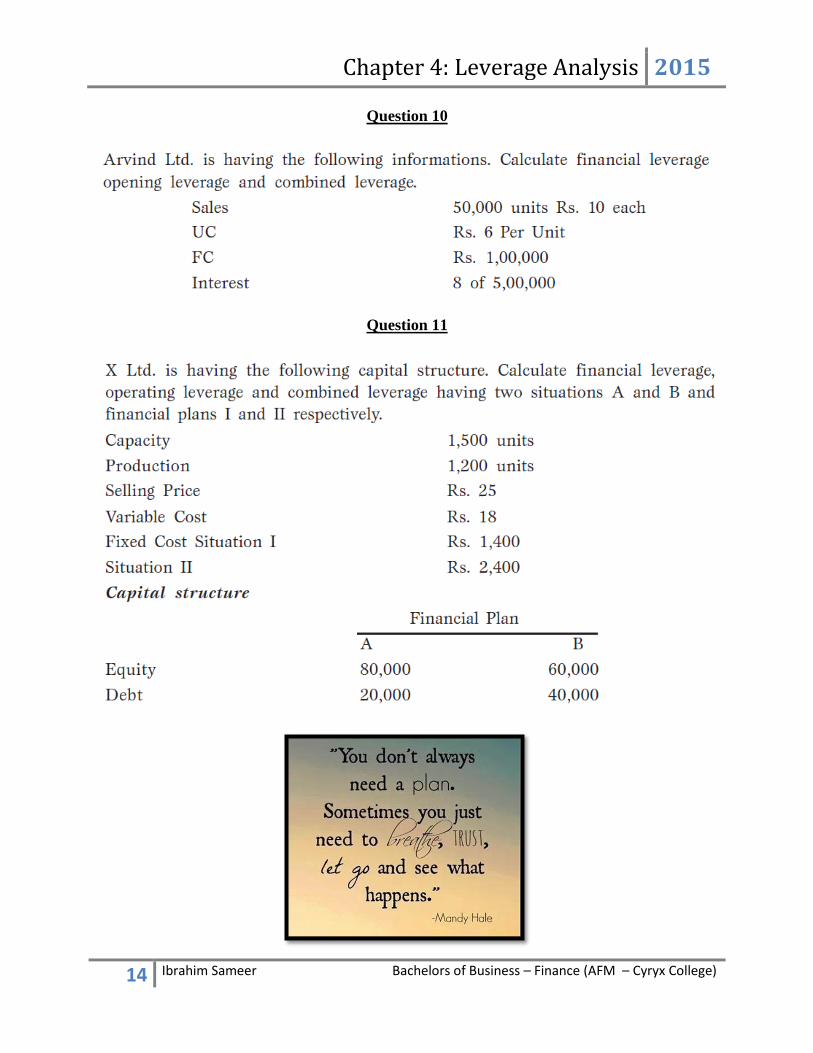

Question 10

Question 11

Chapter 4: Leverage Analysis 2015

15 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 12

Question 13

Question 14

Soma Autos employs debt financing, borrowing at a rate of 10%. The interest cost at this rate

equals MVR 65 billion. If 8 million cars, what is the degree of financial leverage (DFL) for

Soma given revenue per car is MVR 25,000, variable cost per car is MVR 14,000 and fixed costs

equal MVR 15 billion?

Chapter 4: Leverage Analysis 2015

16 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 15

Alpha and Beta both operate in the automobile sector with same degree of operating leverage.

The former has a capital structure of 40% debt and 60% equity, while the latter is financed

completely by equity. Which of the following statements is most accurate? Compared to the Beta

Company, Alpha has:

A. The same sensitivity of operating income to changes in unit sales

B. The same sensitivity of net income to changes in operating income.

C. A higher sensitivity of net income to changes in unit sales.

Question 16

Soomros now sell 1 million units at MVR 3,972 per unit. Fixed operating costs are MVR 1,960

million and variable operating costs are MVR 1,250 per unit. If the company pays MVR 376

million in interest, the levels of sales at the operating breakeven and breakeven points are,

respectively:

A. MVR 2,860,073,475 and MVR 3,408,740,632.

B. MVR 2,875,073,470 and MVR 3,428,740,630.

C. MVR 3,560,073,475 and MVR 4,105,740,632.

Question 17

Will firms in industries in which high levels of output are necessary for minimum efficient scale

tend to have substantial degrees of operating leverage?

Chapter 4: Leverage Analysis 2015

17 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 18

Operating leverage may be defined as:

a. the degree to which debt is used in financing the firm

b. the difference between price and variable costs

c. the extent to which capital assets and fixed costs are utilized

d. the difference between fixed costs and the contribution margin

Question 19

The conservative firm will utilize:

a. a high degree of operating leverage

b. a low degree of operating leverage

c. high fixed costs

d. a higher profit margin

Question 20

The more aggressive firm:

a. substitutes higher fixed costs for variable costs

b. substitutes lower fixed costs for variable costs

c. has lower potential profit above the break-even point

d. is normally more effectively managed

Chapter 4: Leverage Analysis 2015

18 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 21

Degree of operating leverage may be defined as:

a. the extent to which the firm utilizes debt in its financing plan

b. the percent change in operating income/percent change in unit volume

c. the percent change in operating income/percent change in sales

d. the percent change in net income/percent change in unit volume

Question 22

Financial leverage:

a. reflects the firm's commitment to fixed, financial assets

b. has no impact on the earning of the firm

c. reflects the amount of debt used in the capital structure of the firm

d. primarily affects the left side of the balance sheet

Chapter 4: Leverage Analysis 2015

19 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 23

The highly financially leverage firm will typically:

a. has a higher EPS figure than the conservative firm

b. has a lower EPS figure than the conservative firm

c. uses less debt than the conservative firm

d. will produce the same EPS figure as the conservative firm

Question 24

The degree of financial leverage may be defined as:

a. percent change in sales/percent change in volume

b. percent change in EPS/percent change in net income

c. percent change in EPS/percent change in EBIT

d. percent change in EPS/percent change in sales

Question 25

A high degree of financial leverage:

a. is a sign of astute financial management

b. will always decrease the cost of financing for the firm

c. will result in an increase of the firm's overall value in all cases

d. may increase the firm's risk and drive the price of the shares down

Chapter 4: Leverage Analysis 2015

20 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 26

A higher degree of financial leverage may be desirable for:

a. a stable firm, with positive growth, under favorable economic conditions

b. an unstable firm operating in an uncertain environment

c. a stable firm operating in an uncertain environment

d. neither the stable nor unstable firm under any circumstances

Question 27

Degree of combined leverage:

a. should be minimized by the financial manager

b. affects only balance sheet items

c. decreases the firm's operating profit

d. shows the impact of sales or volume changes on bottom line EPS

Chapter 4: Leverage Analysis 2015

21 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 28

Question 29

Chapter 4: Leverage Analysis 2015

22 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 30

Chapter 4: Leverage Analysis 2015

23 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 31

Question 32

Chapter 4: Leverage Analysis 2015

24 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 33

Chapter 4: Leverage Analysis 2015

25 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 34

Question 35

Question 36

Chapter 4: Leverage Analysis 2015

26 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 37

Question 38

Question 39

Question 40

Chapter 4: Leverage Analysis 2015

27 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 41

Chapter 4: Leverage Analysis 2015

28 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 42

Question 43

Chapter 4: Leverage Analysis 2015

29 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 44

Chapter 4: Leverage Analysis 2015

30 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 45

Question 46

Chapter 4: Leverage Analysis 2015

31 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 47

Chapter 4: Leverage Analysis 2015

32 Ibrahim Sameer Bachelors of Business – Finance (AFM – Cyryx College)

Question 48

Related Documents