73 Chapter - 3 Theoretical Background, Conceptual Framework and Research Design

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

73

Chapter - 3

Theoretical Background,

Conceptual Framework

and Research Design

74

Chapter - 3

Theoretical Background,Conceptual Framework and Research Design

Section – A

Theoretical Background and Conceptual Framework of the Study

3.1 Introduction

3.2 Theoretical Background

3.3 Conceptual Framework

Section – B

Research Methodology

3.4 Research Design

3.5 Sample Design

3.6 Summary

75

Section – A

Theoretical Background and Conceptual Framework of the Study

3.1 Introduction

This chapter explains about the theoretical background of the present study. This

section gives the significance of ICT in the Banking Industry and acceptability and

adaptability of the new technology by both customers and employees of

Banks. Technology innovation and economic development are positively correlated.

Invention of technology has become popular and useful for financial services. Old

fashioned Banks have now jumped into the platform of modern technological

environment. Before introducing ICT in the banking sector,ledgers were being

maintained, brick and mortar system was accepted and each transaction was both time

and energy consuming, but now with the advent of technology in this sector the work has

been speeded up and a single card swiping in the machine can shower money.

3.2 Theoretical Background of the Study

Anywhere and anytime Banking has become a feature of the modern financial

system. Electronic funds transfers and E- Banking services have made globe into a small

village and have eliminated the geographical constraints. Technology is identified as an

important factor by many economists. Since decades, in this background this section

reviews various theories related to the present study. Innovation Diffusion Theory was

developed by Roger in 1983. This theory investigates the characteristics of technology

adopters who accept innovative technology. This theory is based on five important

factors such as

Relative advantage: Observing the comparative advantage over new technology

with available technology

Triability : Before adopting new technology in routine life just taking trial and

error

Observability : Clearly observing technology's outputs and its gains

Complexity: Understanding its ease of use

Compatibility: Accepting new technology without problems or conflict

76

Researchers namely Tan and Teo (2000), Gerrard and Cunningham (2003) and

Md Nor and Pearson (2008) have tested this theory on E-Banking services. In this

background the present research study also tests the reasons for opting E-Payments and

E- Banking service by both customers and employees in the study area. The present study

has taken the following factors such as

Chart . No -3.1 Reasons for Accepting Technology Based Services by Employees

(Self created chart)

77

Chart . No -3.2 Reasons for Accepting Technology Based Services by Customers

(Self created chart)

The study has listed above factors and asked respondents to answer the reasons for

accepting or adopting new technology in Banking transactions.

Adam smith, Father of economics in his ‘Wealth of Nations’ had discussed about

the division of labour and varieties of machines and opined that inventions of machines

encourage labour force to produce more output with good productivity.

John Schumpeter (1883 – 1950) in his theory of innovation, stated that anything stagnated

in the state does not yield any profit, but when innovation takes place it disturbs steady

state and brings profit.

78

Chart . No -3.3 Innovation and Growth

(Self created chart)

Innovation economists opined that a key driver of economic growth in today’s

knowledge based economy is not Capital but it is Technology. According to them

technological spill overs create a competitive environment. They also found the inter -

linkage between innovation and market growth.

Chart. No -3.4 Schumpeter’ Economic Growth

(Self created chart)

Schumpeter in his book Theory of Economic Development which was published

in 1912 wrote that any economy to be on the path of economic development needs

healthy and well developed Banking sector. Set of Innovations or Research and

development activities pave the way for technological development and create a new

product for organization. Eventually, it leads to long term growth in the economy. Robert

Solow (1950) formulated a theory of economic growth and stressed the importance of

79

technology. He stated that a tremendous increase in gross output per hour of work in the

USA economy between 1909 and 1949 was the outcome of technological advancement.

He also examined that increased use of capital assured 12.5 percent in per capita output

and it left 87.5percent residual that was attributed by technology development.

During the initial revolution (1750 – 1850) undoubtedly people saw improvements

in their lifestyle and growth of the economy. Wealth increased in the economy of England

but it led to the concentration of wealth in a few hands. The poor became much poorer

and rich dominated the economy. This situation led to the birth of utopian socialism. It

became prominent in the beginning of the 19th century. Saint Simon, Charles Fourier,

Robert Own and others gave importance to equal distribution of wealth and income.

Robert Own (1771 – 1850) contributed greatly to the utopian socialism and he advocated

the establishment of ‘Villages of Cooperation’. He promoted cooperative community

model and encouraged only a fixed rate of interest.

R. C. Dutt (1849 – 1909) in his books economic history of India and famines of

India (two volumes) stated that the poverty in India was the outcome of unsound and

ineffective financial institutions. Peasants and Artisans were not able to face high

competition from British products due to lack of Capital. Sidney Webb (1859 – 1947)

was in favour of Consumers’ Cooperatives. He encouraged cooperative societies for

consumer groups for mutual help and voluntary work. He also stated that producers

cooperative had become a puppet in the hands of capitalism. They were acting as per the

instructions of the Capitalists. Therefore, he emphasized on setting up of consumers’

cooperatives.

Mahatma Gandhi (1869 – 1948) stressed village welfare and was in favour of self –

sufficient and self – reliant villages. He dreamt about prosperous villages. According to

him “Real India Was to be Found in Villages and not in Towns and Cities” So he inspired

the villagers to organize cooperative groups for mutual financial help. He also advocated

desi products and sale of Svadeshi items in the domestic market with cooperative

societies. Rognar Nurkse (1952) explained the causes of the vicious circle of poverty.

According to his study.

80

Low savings

Low Income

Low Production

They were the causes of deep rooted poverty. The above factors led to poor

performance of the economy. Therefore, he advocated credit facilities at lower rate of

interest. In that way it would help poor to come out of the vicious circle of poverty.

Gunnar Myrdal (1957) in his ‘Economic Theory and under developed Regions’,

Explained spread effect, backwash effect and Increasing inequalities in underdeveloped

countries. According to him circular and cumulative process, i.e. a vicious circle of

poverty leads to inequality. Production, Banking, Extravagant shopping and other

activities in a free economy lead to unequal distribution. Herrod (1957) in his growth

model stated that low savings and chronic inflation are the main features of UDCs,

Expansion of Bank credit through the best financial institutional setup enables the

economy to stimulate growth process.

Prof, Mohammed Yunus (1975) a Noble Laureate advocated the group based credit

approach to reduce poverty in the economy. He had developed the ‘Grameena Bank

model’ to ensure timely credit facilities to needy people. He became successful in his

attempt. It was recognized all over the world and the he was awarded very prestigious

award i.e. Noble Award.Corrigan (1982) argued that Banks have special role in the

economy and have provided variety of transactional services.

Banks Administer payment system in the Nations

They provide liquidity backup to the economy

They are transmitters of monetary policy

The Banking sector has greatly changed the lifestyle of people and also banking

transaction business has witnessed many changes. The banking sector is considered to be

the nervous system of any economy.

Technology Acceptance Model was coined by Davis in 1989. This theory is one of

the best theories of this modern era. This theory explains how a person accepts

technology when it is introduced in his working environment or when it is to be opted by

him. It explains about the attitude, perception and intention to make use of that advanced

81

technology. It can be easily explained with the help of the following chart when people

are offered with a new technology, Many such factors influence them to decide about

How to use new technology

and

When to use new technology.

Chart . No -3.5 Technology Acceptance Model

(Self created chart)

The first intention of accepting technology is that perceived usefulness that

means using technology would enhance his or her job performance or increase his

happiness". The present study in this background is going to study the perception of both

customers and employees in accepting technology in the Banking organization. By

accepting technology in working place employees would enhance their job performance

and customers may get more utility.

The second intention of embracing advanced technology is to perceive ease of use

meaning that the person believes that using a technology would be free from effort”.

Usually people develop positive attitudes towards advanced technology due to belief and

its propagation.

Davis Originally developed this model to test the acceptance of word-processor

technology. Later on it has been extended to database management systems, email, voice

mail, personal computers, telemedicine technology and so on.

82

The present study wants to analyse the perception of employees and customers.

Following are the main features of the model. It was developed to give an adequate

explanation about actual behavior, attitude and behavioral intention of people about IT-

related services

This model has a strong theoretical base and uses psychometric measurement

scales

It is based on strong empirical study

Explains the behavior of end-user computing technologies.

The theory explains the person’s attitude towards acceptance of technology and

his perception pertaining to its usefulness. It also highlights that person believes that the

new technology brings him pleasure only on that belief he starts to embrace it.

Chart . No -3.6 Risk involved in E-Banking Services

(Self created chart)

The technology adoption lifecycle model (2003) is an extension of the diffusion

model of Joe M. Bohlen, and developed by Neal C. Gross and Bryce Ryan. They found

that people easily do not want to face risks in their life. Therefore the present study is

going to test whether customers and employees of selected commercial Banks and UCBs

are risk lovers or risk averters. Innovators are more educated and risk lovers, rich and

ready to take challenges in their life, early adopters are young generation highly educated,

though they are less prosperous than the first group lead the community. The Early

majority group consists of conservative minds people, but they are ready to accept new

83

ideas. The late majority group comprises old generation, less educated and highly

conservative in their nature. Laggards are very conservative and least educated.

Griliche and Jogerson (1961 – 1973) with this formula Yt = F (Kt, It, t) stated that

economic growth is function of capital, labour and technological progress. Here,

technology is considered as one of the important factors of economic growth. Simon

Kuznets (1966) opined that the technological developments in underdeveloped countries

contributed to the progress in different sectors of the economy. Technology up gradation

ensures research and development programmes, increases skilled labour force and

introduces capable entrepreneurs.Akio Mortia, The chairmen of Sony Corporation in

1992 opined that the introduction of technology alone is not a great achievement but the

creativity and optimum use of this technology make a wider sense. Organisation with

magical wand i.e. Technology can bring maximum benefits. Vernon (1993) in his product

cycle hypothesis stated that underdeveloped countries to improve their economic

conditions should import a package of technology from other well developed countries

and these technology capabilities encourage them to enhance market size. The product

cycle is based on the idea that the production process passes through several stages and

technology development is one of the stages in the product cycle hypothesis. Endogenous

growth theories also recommended the introduction and up gradation of technology in

different sectors of the economy. They also supported the investment on human capital,

knowledge and technology to reap maximum benefits.

Brynjolfsson and Hitt (2000) pointed out that ICT has a positive impact on the

performance of any organizations. They proved in their study that ICT capital has a major

share of 81% marginal increase in the output of an organization but capita which is not

backed up by Information Technology contributes only 6%. in their study, they have also

illustrated that employees who are provided ICT infrastructure are as productive twice

more than as conventional professionals.The present study is going to analyse the

performance, productivity and profitability of Banks with regard to ICT tools to test

whether the banking sector in India is influenced by ICT adoption.

84

3.3 Conceptual Framework

ICT strategy in the Banking sector is recognised as an important step by the RBI.

Because in India more than 65 percent of the total population is either under banked or

unbanked. E-Banking services are a powerful tool to reach the doorsteps of unreached

community to bring them to the mainstream of the economy and also to help them to

access Banking services. No doubt that today’s banking business environment has

become dynamic and has undergone rapid changes because of the introduction and up

gradation of technological tools.

Concept of ICT

ICT is a combination of computer technology and telecommunication technology.

21st Century is directly controlled by multiple communication channels like verbal

communication, writing, audio- visual and electronic media. Communication and

technology are widely used in all aspects of life and increasingly applied to all the sectors

of the economy.

ICT is a Combination of

Chart. No -3.7 Concept of ICT

(Self created chart)

ICT can be described as

Information -> Processed data

Communication -> Exchange of Information from one point to another, either

electronically or Non-electronically.

85

Technology -> Specific scientific knowledge used in a practical way with

advanced tools.

Concept of Banking Technology

ICT has sprinkled miraculous water on the economy. It is hatching golden eggs

and boosting the economy to achieve double digit growth. ICT strategy by bringing

transparency and increasing efficiency is helping the Banking sector to have a sound

financial performance.

Chart. No -3.8 E-Payment Services in Banks

(Self created chart)

I. Real Time Gross Settlement

RTGS helps customers to transfer their funds from one Bank to another Bank. It

is operated and managed by the Reserve Bank of India. With this E-Channel a Bank can

transfer funds fast and reach the beneficiary within two hours. The only core banking

solution enables Banks to go to these facilities. It is an online system for quick

transactions settlement in the Banking field.

II. National Electronic Fund Transfer

NEFT facilitates individuals, firms and comparators to transfer funds

electronically from any branch to another account. RBI has introduced NEFT in 2005.

There is no minimum or maximum limit on transferring funds before sending money.

86

Customers should give accurate and essential details of the receiver’s name, account,

number, branch etc.

III. Electronic Clearing Service

ECS helps to transfer funds from one Bank to another. This service facilitates

credit and debit transactions directly linked to customer's account. Through ECS

customers can pay electronically, such as Bills like mobile bills, telephone bills and other

utility bills. It helps customers to avoid late payments and multiple cheques.

IV. Magnetic Ink Character Recognition

MICR facilitates the faster process of cheque clearing. Traditional way of cheque

clearing method was delaying the cheque clearing transactions. With MICR method

cheque collection and clearing can be done at a faster rate. MICR cheque leaves have

(8x3 2/3) standardised size. Bank branch code and account type are printed on this.

Magnetic Ink character recognition is used on cheques and deposit slips. It detects those

characters and converts them into digital data.

V. Point of Sale Terminal

Point of sale terminal deals with computerised information files of customers.

POS is a swipe machine which is provided to a merchant establishment customer without

paying cash by swiping their magnetic plastic card which buys goods and services.

Chart . No -3.9 E-Banking Services

(Self created chart)

87

Core Banking Solution helps customers to transfer funds, to operate accounts and

avail all Banking transactions from any branch of a Bank. It creates a network among all

branches of a Bank. CBS is used in many ways.

To get a statement of accounts

To transfer funds

To make payments in any branch

To get demand drafts in any branch

The core banking solution aims at providing efficient and transparent quality services.

I. ATM service

ATM is also noted as Automated Teller Machine or Automatic Teller Machine

and it is also simply said in commoners’ language as any time money. It is an electronic

communication device installed in the premises of a particular or established outside the

area of the Bank to help customers to do their transactions without the need of Bank staff.

Customers have to insert card with magnetic strip which contains their Bank’s

information and enter the PIN code to perform financial transactions.

II. Email, Voicemail and SMS alerts

The customers are provided with E-mail option. Banks send mails regarding

passbook statements and E-Banking services. Customers can also contact managers when

they face security and transaction related aspects. Customers with a touch tone phone can

directly call concerned department. The automatic Voice recorder is used for queries if

the call is not answered. Customers can leave a message to them. This is called Voice

mail service. Foreign Banks in India have become successful in providing this service to

their customers when customers withdraw or deposit money or repay loans, Banks send

automated SMS alerts for confirmation of registered mobile numbers. It is regarded as

SMS alert services. It is also a type of mobile Banking.

III. Mobile Banking

RBI issued guidelines for Banks to start mobile Banking transaction in 2008.

Mobile Banking technology is a system that allows customers who have smart phones to

perform their Banking transaction. It includes

88

a. Checking Bank statements

b. Monitoring term deposits

c. Accessing to mutual fund and Equity statements

d. Accessing to loan statements

e. Transferring funds

f. Paying bills, etc.

Therefore, it is said that Mobile Banking is an E - Banking service provided by

Bank to do transactions in the physical absence of the customer.

IV. Internet Banking

Internet Banking is a convenient E-Banking service provided by the Banks to their

customers. With this service, customers can do Banking transaction anywhere or at home

or office. Internet Banking service provides the following services

To check account information

To open fixed deposits

To recharge prepaid mobile or DTH

To pay utility bills

To transfer funds

To open or close accounts

With net Banking transaction customers can avail various services online even

after office hours.

V. Card Based Transactions in Banks

Banks issue credit, debit and smart cards to their customers. Debit cards are

provided by Banks to help customers to withdraw money anytime and anywhere. They

are considered as plastic money. With these cards they can also purchase goods and

services without paying cash. ATM machines are established in different areas for home

Bank to help customers. These cards are provided with personal identified number (PIN)

to check Bank statements, to withdraw money or to make cash payments in shopping

centers. Banks also provide smart cards to customers. They are built in microprocessor

used for financial transaction. They have unique identity solution. The smart card

contains the name of the account holder, card number, photo of the card holder and

89

others. They are used as electronic wallets and considered to be secure. Banks also

provide credit card facilities to their customers. It helped the account holder to purchase

goods and services in shopping centers without paying money at that time, but they have

to repay that amount with interest to the concerned Bank within a specified period.

Chart. No -3.10 Communication Networks

(Self created chart)

Communication networks in Banks facilitate to share and exchange messages with

other member Banks. They avoid language barriers and interpretation problems and

provide 24x7 communication facility.

BANKNET was introduced by RBI in 1991 to transfer Inter-Bank and Intra-Bank

messages within a country by public sector Banks that have membership in this network.

COMET has given facility to send messages from minimum 8 lines consisting of 48

characters. Indian Financial Network (INFINET) is satellite based using network, i.e.

VSAT (Very Small Aperture Terminal) was introduced by RBI in 1999. It is considered

as a backbone for the Indian Banking sector. It consists of 950 VSATs in 127 cities of this

country. Society for worldwide Interbank Financial Telecommunication (SWIFT) is a

code recognized as a Banks identifier code. Each Bank has its own unique codes. This

code comprises 8 – 11 characters. It facilitates Bank to exchange messages with other

Banks. The message delivery is very fast.

90

Each Bank aspires to adopt the best possible strategy to improve performance and

to achieve predetermined goals. To this background ICT has become an important tool in

redefining and redesigning the Banking sector. This development has assured timeless

and placeless Banking business by dismantling significance of the physical structure of

Banks.

Table No -3.1 ICT Services in Indian Banking Sector

ICT Services offered by Banks

Year of Introduction Credit card 1981

ATM service 1987

MICR 1987

BANKNET 1991

SWIFT 1991

EFT 1995

Internet Banking 1996

INFINET 1999

RTGS 2004

NEFT 2005

Mobile Banking 2006

Cheque truncation system 2008

Source-collected information from RBI

ICT based services help Banks to come out of loopholes of manual system of

traditional Banking environment. Today Banks have realised the benefits of this latest

technology

Technological development in the Indian Banking sector started in the year 1962

when the RBI introduced unit record machine to process statistical data. In the year 1967

RBI and the State Bank of India brought computers to their banking operation to maintain

branch transaction. The RBI appointed a working group to highlight the importance of

computerization of the banking business in 1970. In 1983 The Indian Bank Association

(IBA) made an agreement with the National Confederation of Bank Employees (NCBE)

and All India Bank Employees Association (AIBEA) to start the computerisation process

at branches and head office level of Banks. Computers in the Banking sector were used at

that time for the following reasons

91

For investment management

To maintain ledger accounts

To maintain branch information

For remittance purpose

For foreign exchange dealings

Computerization in the banking business included

Microprocessor

Electronic legal posting machines (ELPM)

Main frame computers

Accounting machines

Those machines allowed installing in 2500 branches, including the head offices of

Banks. RBI also insisted Banks to take the assistance from software vendors Viz, CMC

Limited, Combol, Unify database and Unix OS. RBI also formed Rangarajan Committee,

which was the first committee, which highlighted the importance of computerization in

Indian Banks. In 1982 RBI appointed working group on MICR for cheque processing

under the chairmen ship of Dr. Y B Dhamle to introduce MICR technology in important

cities like Delhi, Chennai, Mumbai and Calcutta. T. N. Iyer committee in 1987 also

recommended BANKNET, establishment of electronic data processing cells and SWIFT

implementation during this period. The Second Rangarajan Committee in 1988 suggested

to go for 900 mini computers at all levels of Banks all over India and insisted to automate

2500 branches of Banks in India before entering the year 1994.

In 1983 Indian Banks Association made an agreement with all India Bank

Employees' Association (AIBEA). As per agreement Banks has to follow the following

instructions

Banks who have less than 500 branches should computerise at least 3 branches

every year.

Banks who have more than 500 branches should computerise at least 5 branches

every year.

Banks should install ATMs gradually in all cities

Setting up pass book printers, note-counting machines, signature verification

equipment etc.

92

WS Saraf Committee in 1994 and Shere committee in 1995 recommended to start E –

Payment system. RBI considered technology as a key driver in the Banking business

management. RBI in 1998 under the chairmanship of Sri Narasmiham appointed a

committee to look into various issues concerned with Banking business. The committee

recommended to use E – Files and digital signature in Banks. In the same year the RBI

also recommended the technical assistance products of department for international

development. RBI in 1996 established IDRBT (Institute for development and research in

Banking industry) and research and development were encouraged. Vasudeva committee

in 1999 suggested to blend INFINET with satellites and microwave lines and to start up V

– SAT network for interBank and intra-Bank operations.

In 2001 Mithal committee concentrated on security issues in implementing ICT tools in

Banking transactions. The early 2000’s witnessed a tremendous growth of IT tools in

Banks computer and communication technologies like Internet, Mobile, ATM and others

have lots of potential to redesign the Indian Banking platform. According to the reports of

RBI, at the end of March 2011 nearly 97.8percent of public Banks were fully automated,

but private and foreign Banks were 100percent computerized in India.

Economic reforms in India opened new avenues to the Banking sector to the global

economy. Relaxed rules and regulations of Indian government provided an opportunity to

adopt electronic Banking. Especially Private Banks and Foreign Banks became efficient

in using ICT tools in their business operations. This trend brought pressure on

nationalized Banks to adopt technology enabled services. To maintain healthy

competition on the platform of Banking Sector, it has become inevitable for Banks to go

for advanced technology in their operations.

93

Section – B

Research Methodology

3.4 Introduction

Innovation of technology in the Banking sector is changing expectations of

customers and increasing awareness about advanced technology is the outcome of the

electronic age. The modern technology is saving time and providing quick services to

customers. In this background, the present study has made an attempt to analyse the

perceptions of customers in both Commercial Banks and Urban Cooperative Banks in the

Mysore city. The study is concerned with ICT practices in the banking sector in India.

With the introduction of ICT strategy in this sector considerable changes have been

achieved in Commercial Banks but UCBs need to rapidly sink into IT revolution. The

study is confined to both Commercial Banks and UCBs of India. Therefore performance

and ICT usages in Banking are analysed.

3.5 Research Design

The study is concerned with ICT practices in the banking sector in India. With the

introduction of ICT strategy in this sector considerable changes have been achieved in

Commercial Banks but UCBs need to rapidly sink into IT revolution. This section throws

light on the plan, structure and strategy of the present study. Here research design deals

with the following important aspects. The present study is based on both quantitative and

qualitative research approaches.

94

Chart. No -3.11 Overview of Study Design

The present study has chosen simple random sampling method. Customers and

Employees of both Commercial Banks and UCBs are selected randomly from the larger

population. The simple random sampling method is used to get a better representation of

the larger group of the study area. The simple random sampling method is one of the

95

types of probability sampling technique.to choose both Commercial Banks and UCBs

purposive sampling method has been adopted

Chart . No -3.12 Structure of the Study

96

3.6 Sample Design

Sample design consists of two elements they are,

I. Sampling Method: Sampling method shows what rules and procedures have

been adopted to draw samples of the population, such as data collection method,

sample size, study area and study period.Twelve parameters are taken in to

consideration for the analysis of trend and the impact of ICT on the performance

of Commercial Banks and UCBs

II. Data Analysis Method: This shows the estimation process for analyzing sample

statistics. In this study many different estimators have been used to analyse. A

simple random sampling method has been adapted to select customers and

employees of Banks and purposive sampling method is used to select Banks in the

study area. The study has used a simple percentage method, T –test, F-test,

dummy variable method, AAGR, graphical method and chi square test statistical

measures to analyse trend, impact of ICT on Banking sector and perception of

employees and customers about ICT based services of Banks.

a. Data Collection

The present study is based on both primary data and secondary data.

Chart. No -3.13 Primary data

Two methods are used to gather required information for the present study, Viz,

questionnaire, schedule and interview method.

Schedule used for the present study comprises two parts. The 1st part deals with the

demographic profile of selected 300 customers and 200 employees on the basis of

97

their age, education, gender and occupation. The second part deals with their

perception towards ICT services provided by Banks. The present study has used a

five point Likert type scales to get information from the respondents. They were

asked to rate from 1 to 5. if they rate it indicates that if they mark 1 it indicates that

they are highly satisfied. If they mark 5 it means they are highly dissatisfied. It can

be shown in a following way,

Chart . No -3.14 Five Point Likert Type Scale

Highly

Satisfied

Satisfied Do Not

Know

Not Satisfied Highly

Dissatisfied

1 2

3

4

5

Questionnaire method was used to take information from Bank managers regarding

E-Banking services of selected Commercial Banks and UCBs of Mysore city.

Chart . No -3.15 Secondary Data

The secondary data are collected from various published sources such as RBI

reports, NFFSCOB reports and reputed journals, books, newspapers and websites. It is an

explanatory as well as analytical research conducted to explain the behaviour and reaction

98

of both customers and employees of Commercial Banks and Urban Cooperative Banks of

Mysore city regarding ICT adoption in Banks.

b. Sample Size of Banks, Customers and Employees

Selecting samples for the study is an important step in research work. The

collected samples must be the best representatives of our study area.

Table -3.2 Selected Banks for the Study

Sl. No

Category of Banks

No. Of Banks

1 Public Sector / Nationalized Banks 6

2 Private Banks 3

3 Foreign Banks 1

4 Urban Cooperative Banks 10

Total 20

Source : Field Work

The Sample for this study is limited to Mysore city of Karnataka State, India. Ten

Commercial Banks and ten UCBs of Mysore city have been selected for the study (1/4th

of the total Banks in the city). A purposive sampling method has been used to select

Commercial Banks and UCBs in the study area. As compared to private and foreign

Banks Public Sector / Nationalized Banks are more in number therefore six Banks are

drawn from that category. Three Private Sector Banks and one Foreign Bank have been

chosen for the study and out of 14 UCBs 10 Urban Cooperative Banks which are using

fully or partially the E-Payment and E-Banking methods in Mysore city have been

selected.

99

Chart . No. -3.16 Public Sector Banks (Selected for the Study)

Chart . No -3.17

Private Banks (Selected for the Study)

100

Chart . No -3.18 Foreign Bank (Selected for the Study)

Chart .No -3.19 Urban Cooperative Banks (Selected for the Study)

101

Table -3.3 Customers and Employees of Selected Banks for the Study

Sl. No Category of Banks No. of customers No. of Employees

1 Commercial Banks 150 100

2 UCBs 150 100

3 Total 300 200

Source : Field Work

For the Present study 150 customers from Commercial Banks and 150 customers

of UCBs of Mysore city and 100 employees of Commercial Banks and 100 employees of

UCBs of the same study area are selected on simple random sampling method. As

compared to the number of customers of Banks the number of employees is less,

therefore, the present study has taken 300 customers and 200 employees into an account

and 20 Banks are chosen for the study.

Parameters to measure Performance of Banks

Indian Banks now a days are making heavy expenditure on ICT tools. In this

background, the present study has analysed the impact of advanced technology on the

performance, productivity and profitability of Commercial Banks as well as Urban

Cooperative Banks in India. Following are the various performance indicators selected for

the study.

Chart. No -3.20 Indicators used to Measure the Performance Of Banks

102

The Study has analysed the financial performance of both Commercial Banks and

UCBs in India with the help of four indicators such as total deposits, total advances, total

investment and the total business.

Total Deposits

Total deposits are shown in the balance sheet of a Bank. Customers place their

money in their Banks to get the benefits of the rate of interest provided by the Bank. Total

deposits include various types of deposits such as demand deposits, term deposits and

others.

Total Advances

Total advance refers to the credit facility provided by a Bank. Banks may grant

short term as well as long term advances for various productive and domestic purposes.

Total Investments

Total investment is of two types a) investments from offices in India: it includes

Indian government securities, domestic securities, bonds, shares and foreign securities. b)

Investments by foreign offices of Indian Banks: it includes Indian securities, foreign

countries securities and other investments.

Total Business

Total business is the sum of all deposits, advances and investments of the Bank.it

is the best possible measure of analyzing the performance of any Bank.

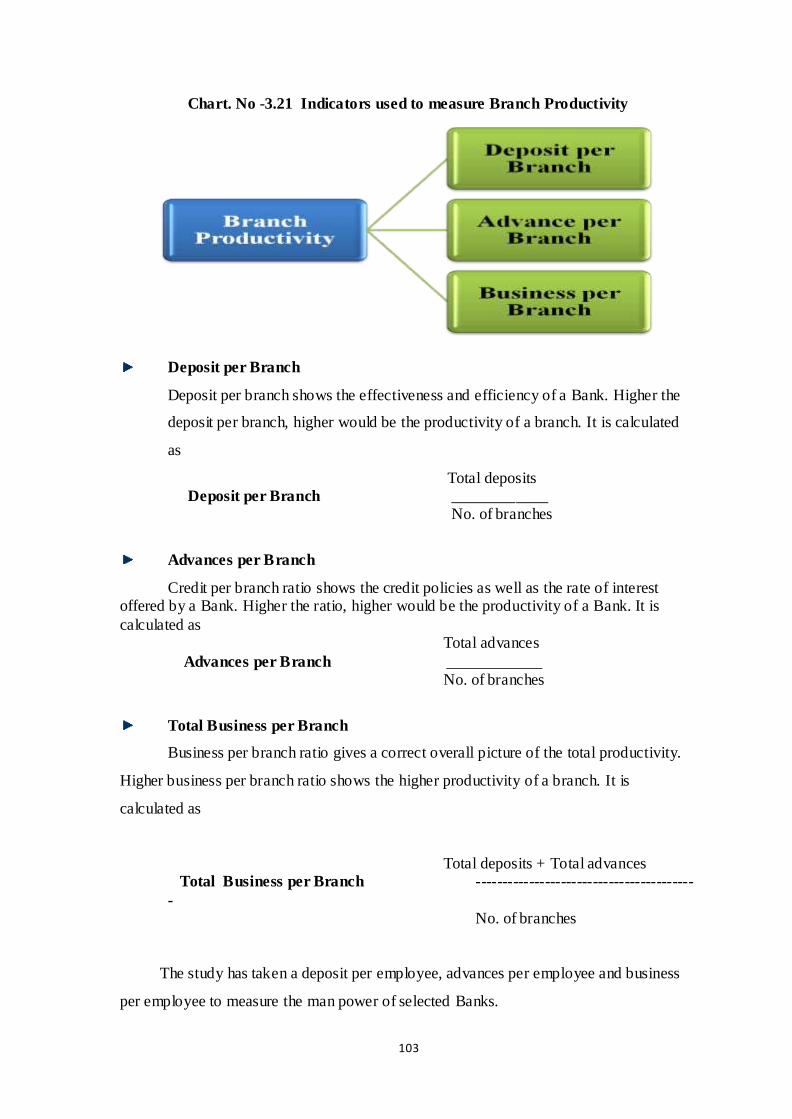

Indicators used to measure Branch Productivity

The study considers deposit per branch, advance per branch and total business per

branch to analyse the branch productivity of selected Banks

103

Chart. No -3.21 Indicators used to measure Branch Productivity

Deposit per Branch

Deposit per branch shows the effectiveness and efficiency of a Bank. Higher the

deposit per branch, higher would be the productivity of a branch. It is calculated

as

Total deposits Deposit per Branch ____________

No. of branches

Advances per Branch

Credit per branch ratio shows the credit policies as well as the rate of interest offered by a Bank. Higher the ratio, higher would be the productivity of a Bank. It is

calculated as Total advances

Advances per Branch ____________ No. of branches

Total Business per Branch

Business per branch ratio gives a correct overall picture of the total productivity.

Higher business per branch ratio shows the higher productivity of a branch. It is

calculated as

Total deposits + Total advances Total Business per Branch -----------------------------------------

- No. of branches

The study has taken a deposit per employee, advances per employee and business

per employee to measure the man power of selected Banks.

104

Chart. No -3.22 Indicators used to measure Labour Productivity

Labour Productivity

Labour productivity plays an important role in analyzing the total productivity of a

Bank. This part of the study deals with the deposit per employee, advances per employee

and Business per employee.

Deposit per Employee:

This ratio shows the capacity of employee in collecting the deposit in a branch.

When deposit per employee is higher it is an indication of higher productivity per

employee. It is calculated as

Deposits Per Employee = Total Deposits

_____________

No. of employees

Advances per Employee:

This ratio shows the skills of employees to convince customers to avail the credit

facilities of Banks. Higher the advances per employee ratio, the higher the productivity

per employee. It is calculated as

Advances per Employee = Total Advances

_____________ No. of employees

105

Total Business per Employee:

Business per employee reflects the total deposits collected and loans disbursed by

a Bank. When the business per employee ratio is higher the productivity of employees is

also higher in the Bank. It is calculated as

Total deposits + Total advances

Total Business per Employee ------------------------------------------

No. of branches

The study has taken an important indicator, i.e. return on investment to measure

the profitability of Banks.

Chart. No -3.23 Indicators used to measure Profitability of Banks

Profitability of Banks

Like all business organizations, banks also purely do their business to earn

maximum profit. Though social justice is a main concern, profit plays a major role. The

profitability of a bank is measured with return on investment.

Return on Investment:

This shows that whether a company is utilizing its available resources in an

efficient manner. Higher the returns the profitability of a Bank would be more. Return of

investment is calculated with the formula-

Net profit

_________ x 100

Investment

106

It is also helpful to evaluate the efficiency of an investment in a Bank.

Chart. No -3.24 Parameters Selected to analyse Perception of Customers and

Employees

Modern Banking sector today is providing a variety of E-Banking services. The

present study has taken the following E- Banking Services to analyse the perception of

customers.(explanation is given in 3rd chapter).

Chart. No -3.25 Parameters used to analyse the Satisfaction Level of Employees

107

Chart. No -3.26 Parameters used to analyse the Satisfaction Level of Customers

Indian Banks now a days are spending a maximum amount on ICT tools in their

Banking activities to attract more customers and to increase the productivity of

employees. In this background the present study has analysed satisfaction of customers of

Commercial Banks as well as Urban Cooperative Banks in the study area. The above are

the various performance indicators selected for the study to analyse the satisfaction level

of both customers and employees.

c. Study Period

The time period for the present study has been taken from 2003 – 04 to2012- 13.

The entire study period is divided into two parts.

Chart. No -3.27 Division of Study Period

108

Though ICT services were encouraged during the 90’s in Indian Banking Sector,

the big step was taken to introduce E – Banking services at a maximum level only after

the year 2002 – 03. RBI appointed a Committee on Internet Banking under the

chairmanship of Sri Mittal in 2001.Banks started to use RTGS and NEFT after 2003.

RTGS and NEFT actually started a new era in the banking field in this background study

period has been started from 2003-04.

After introducing internet Banking E- Banking gained momentum and Banks

started to sink into E- Banking revolution. Financial Sector Technology Vision Document

2008 of RBI stressed 100 percent computerization and advised to complete the

implementation of Core Banking Systems by Banks. Mittal Committee which was

appointed by RBI in 2001 also recommended Commercial Banks to adopt E-Banking

services in their branches and also advised them to provide secured services to their

customers. Till 2008 there was no any committee to suggest ICT based services in UCBs

but under the chairmanship of Sri. R. Gandhi RBI appointed a working group on IT

support for UCBs in Jan 2008. This Committee advised that

Small and weak UCBs should be supported by RBI for their IT efforts

The core banking solution must be adopted by all UCBs

The Committee also suggested that to adopt IT tools UCBs need to be provided

interest free loan repayable in 7 years by RBI.

In this background the study period is divided into two parts to know the impact

of ICT before the formation of the working group on IT support for Urban Cooperative

Banks [2008] and after 2008 to till 2013.In this context study has taken the time period

from 2003-04 to 2012-13. The study period is divided into two distinct parts.

d . Profile of the Study Area

The Survey of business today 2011 found that Mysore occupied the 5 th place in

the list of Best cities in India in the field of business and third largest city in the state.

Mysore is an important center of tourism, trade, yoga, Industries and research centers.

Mysore city is also called as a capital city of Yoga. This city has reputed educational

institutions for study. World renewed research institutions such as central food

109

technological research institute (CFTRI), Central Sericulture Research and Training

Institute, Central Institute of Plastic Engineering and Technological Research Institute,

All India Institute of Speech and Hearing, Defense Food Research Lab rotary, New

Security Note Printing Press, Bharath Earth Movers Limited and National Daily

Development Board.

Mysore city has given place to major industries such as Karnataka Industrial

Areas Development Board (KIADB), TVS Motor Company Ltd, Automotive Axles Ltd,

Karnataka Silk Industries Corporation (KSIC), Nestle India Ltd, AT & S India Private

Ltd, VKC Sandals, JK Tires, Falken Tires and Mysore Sandal Wood Oil Factory etc.

The cultural city, Mysore attracts millions of people every year. During the

financial year 2013 –14 32, 47, 746 tourists visited Mysore to see more than 72 places in

and around Mysore city. This city is also becoming IT hub next to Silicon city Bangalore.

This city is regarded as 2nd software exporter in Karnataka. It has well equipped technical

training center of Infosys Ltd, Global Service Management Centre of Wipro Technologies

and other major IT companies such as software paradigms, WEP Peripherals Ltd, Lorsen

and Toubro InfoTech (L & T), Comat Technologies, Theorem India Pvt Ltd, Excel soft

Technologies etc. There are more than 70 companies are located in this city, software

exports from Mysore city is 4percent of the total IT exports of Karnataka State i.e. Rs

1.35 crore.

This city has also a large number of reputed, Nationalised, Private, Foreign and

Urban Cooperative Banks. All Banks have got good business due to the developmental

activities in the economy of Mysore. Mysore is a rapidly growing city next to Bangalore

in Karnataka and has more UCBs in South Karnataka next to Bangalore. Banks are

playing vital role in meeting the needs of customers and also seeking better opportunities

to enhance their business activities. In this background the present study has taken

Mysore city as a Case study.

II. Data Analysis Method

The present study has adopted the following advanced statistical tools to analyse

the data. They are as follows,

110

Table. No -3. 4 Data Analysis Method

Statistical Tools Analysis of data

Graphical Method To trace the trend in E- Payment and E-

Banking services, financial performance of

Banks

AAGR (average annual growth

rate) Method

To compare the growth between Commercial

Banks and UCBs in India

F-Test To find the significant difference in variance

between the period of technology up

gradation and Period of rapid usage of

technology.

T-Test To find the significant difference in mean

value between the period of technology up

gradation and Period of rapid usage of

technology.

Dummy Variable Analysis To estimate the impact of ‘time period’ i.e.

Period of technology up gradation and Period

of rapid usage of technology on the

performance, productivity and profitability of

Banks

Chi-square Test To find the significant association between

Bank type and satisfaction level of customers

as we as employees on E- Payment and E-

Banking services in study area i.e. Mysore city

111

3.7 Summary

Technology stands as a key given to run the economy to reap maximum benefits.

It is advocated by many economists all over the world. Technology led theories also

emphasised the role of technology based economic models. Sigfried Giedion, Leslie

White, Lynn White JR, Harold Innis and Marshall Maluhan who are considered as

technology push theorists stated that technology advancement in the economy brings a

wide range of fruitful results. Lynn White in his book ‘Medieval Technology and Social

Change’ stated that technological innovation quickly leads to development in the modern

world. Christopher Evans, one of the technological determinants said that computer

technology would bring wonderful transformation in the society at all levels. Mysore City

being one of the growing cities next to Bangalore has attracted and put red carpet

welcome to reputed IT companies. Easy traffic, excellent connectivity of roadways and

railways, aircraft landing facilities, reputed research centers, educational institutions,

attractive tourism places and well equipped banking business centers have posed plenty of

opportunities foreign investors to select this city. As business activities are increasing

there is large scope for Banking industry, Commercial Banks have well equipped

buildings and are offering technology based services to their customers. On the other

hand UCBs in majority are on traditional Banking method, but few UCBs are offering

variety of services to their customers.

Related Documents