1 CHAPTER 3 Equity Markets A. Investment Banking and Primary Equity Markets An investment bank is an institution whose traditional role is to assist corporations in the issue and sale of securities to the general public. This issue of new securities can be referred to as a primary offering or primary distribution. The market in which the primary distribution occurs is referred to as the primary market as opposed to the secondary market where previously issued securities are sold. The secondary market's function can be described as "providing liquidity for the primary market" and includes transactions on the exchanges and in the so-called "over the counter markets." If new corporate stock is being sold to the public for the first time, it is said that the corporation is making an initial public offering of its stock. If the firm is raising money to start its operations, it is said to be raising venture capital. The firm can also issue securities via a private placement, selling share directly to a small group of institutional and high net worth investors. SEC Rule 144A enables firms to forgo high placement costs by permitting private placements to small groups of qualified private investors. The investment bank assists the corporation in making the primary offering by first providing advice and counsel and then acting as a "middleman" in the sale of the new securities. This "middleman" function is served by the investment banker acting either as a broker selling the securities on a "best efforts" basis or by underwriting the new issue. If the investment banker acts as an underwriter, it purchases the new securities from the issuing corporation and attempts to resell them at a profit, in a sense, acting as a wholesaler or dealer. This underwriting operation, through negotiation with the investment banking institution, in effect, insures the issuing corporation against the risk of being unable to make its primary distribution at a satisfactory price. The investment bank can also act as a broker, selling the new securities for the corporation or other investment banks on a commission or best efforts basis. Investment bankers specialize in the selling of newly issued securities; they are better equipped to handle a primary offering than is the issuing corporation. Often, an underwriting institution engages other investment banks and brokers to assist in the sale of the new securities. Thus, typically, an investment banker does not underwrite a primary offering alone; it forms with other investment banking institutions an underwriting syndicate. This enables the managing underwriter (originating investment banker dealing directly with the issuing corporation) to decrease its risk by engaging other members of the syndicate to purchase and resell securities. The underwriting syndicate also allows the managing underwriter to improve its selling or marketing ability and to more easily raise the funds necessary to underwrite the issue. Often, the underwriting syndicate employs a selling group to distribute the new issues. This selling syndicate brokers shares of the new issue for the underwriting syndicate on a best efforts basis. A study of 1028 IPOs from 1977-1982 found that approximately 35% were brought to market on a best efforts basis. Almost half of these best efforts IPOs failed; that is, the issuer was not able to sell a sufficient number of shares of the issue to make the new issue viable. However, average returns for best efforts offerings were 48%, compared to 15% for underwritten (also

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

CHAPTER 3 Equity Markets

A. Investment Banking and Primary Equity Markets

An investment bank is an institution whose traditional role is to assist corporations in the issue and sale of securities to the general public. This issue of new securities can be referred to as a primary offering or primary distribution. The market in which the primary distribution occurs is referred to as the primary market as opposed to the secondary market where previously issued securities are sold. The secondary market's function can be described as "providing liquidity for the primary market" and includes transactions on the exchanges and in the so-called "over the counter markets." If new corporate stock is being sold to the public for the first time, it is said that the corporation is making an initial public offering of its stock. If the firm is raising money to start its operations, it is said to be raising venture capital. The firm can also issue securities via a private placement, selling share directly to a small group of institutional and high net worth investors. SEC Rule 144A enables firms to forgo high placement costs by permitting private placements to small groups of qualified private investors. The investment bank assists the corporation in making the primary offering by first providing advice and counsel and then acting as a "middleman" in the sale of the new securities. This "middleman" function is served by the investment banker acting either as a broker selling the securities on a "best efforts" basis or by underwriting the new issue. If the investment banker acts as an underwriter, it purchases the new securities from the issuing corporation and attempts to resell them at a profit, in a sense, acting as a wholesaler or dealer. This underwriting operation, through negotiation with the investment banking institution, in effect, insures the issuing corporation against the risk of being unable to make its primary distribution at a satisfactory price. The investment bank can also act as a broker, selling the new securities for the corporation or other investment banks on a commission or best efforts basis. Investment bankers specialize in the selling of newly issued securities; they are better equipped to handle a primary offering than is the issuing corporation. Often, an underwriting institution engages other investment banks and brokers to assist in the sale of the new securities. Thus, typically, an investment banker does not underwrite a primary offering alone; it forms with other investment banking institutions an underwriting syndicate. This enables the managing underwriter (originating investment banker dealing directly with the issuing corporation) to decrease its risk by engaging other members of the syndicate to purchase and resell securities. The underwriting syndicate also allows the managing underwriter to improve its selling or marketing ability and to more easily raise the funds necessary to underwrite the issue. Often, the underwriting syndicate employs a selling group to distribute the new issues. This selling syndicate brokers shares of the new issue for the underwriting syndicate on a best efforts basis. A study of 1028 IPOs from 1977-1982 found that approximately 35% were brought to market on a best efforts basis. Almost half of these best efforts IPOs failed; that is, the issuer was not able to sell a sufficient number of shares of the issue to make the new issue viable. However, average returns for best efforts offerings were 48%, compared to 15% for underwritten (also

2

called firm commitment) offerings over this period.1 This "IPO underpricing" phenomena will be discussed in detail later. Issuing firms often select an underwriter based on its experience taking similar firms public. Having a well-known analyst in the same industry is usually a strong selling point for the investment bank as is a willingness to make a market for the new issue. Many industrial corporations maintain an ongoing relationship with an investment bank. In some instances, there will be a sharing of directors of the investment bank and its client. This investment bank may be in a particularly good position to provide competent advice and counsel given its close working relationship with its client. Contractual arrangements in these cases are usually negotiated between the investment bank and the issuing corporation. In most instances, publicly regulated utilities and municipalities are required to submit their primary offerings for competitive bidding among prospective underwriters. The general process of a typical common stock underwriting operation might be as follows: 1. The issuing firm and investment bank discuss the issuing firm's need for funds

and various means of raising them. A specific issue or group of issues is decided upon and the investment banker determines the legal and other technical implications of the flotation. The function of the investment bank at this stage is to provide advice and counsel. In addition, the investment bank will conduct a due diligence investigation of the issuer. Terms of the underwriting agreement are negotiated between the issuing firm and the underwriter. Generally as noted above, railroad and utility firms and states and municipalities are required to accept competitive bids for underwriting.

2. A registration statement containing a prospectus with audited financial statements detailing relevant business and financial information regarding the issuing firm's condition and prospects is filed with the SEC (the Securities and Exchange Commission), as required by law. The types and quantity of information to be included in this registration statement will depend on the size and age of the firm along with the amount of money being raised. IPOs from certain regulated industries such as banking will be required to fulfill additional disclosure requirements as will firms from industries with histories of securities markets abuses (such as and oil, gas and mining). The SEC will require approximately 20 days to analyze this statement for omissions. The underwriters assists in this registration process and may not offer the securities for sale during this period; however, they may print a preliminary prospectus (sometimes referred to as a red herring) with all relevant information except for the price of the securities.

3. The originating underwriter may invite other investment banking institutions to join the operation, forming an underwriting syndicate. In most cases, it will invite other investment banks and brokers to form a selling group to assist in selling shares.

4. Setting the price for a seasoned issue (an issue which is substantially the same as 1Ritter [1987]

3

a previous issue which is publicly traded) is fairly straightforward. The market price of currently traded securities will provide useful information for pricing the seasoned issue. However, the price setting process is most difficult for an initial public offering. The investment bank is likely to perform an appraisal based on the issuing firm's accounting statements and other relevant information. Also, the investment bank will present the new issue to prospective purchasers in "dog and pony shows" or “road shows” in its efforts to create interest in the issue. The underwriter will canvas its clientele to solicit bids to purchase shares in the new issue within a price range (the bookbuilding process). Although these preliminary bids are not binding, they do indicate the strength of the interest in the new issue. If the new issue is oversubscribed, the offer price may be set at a level that exceeds the high end of the preliminary range. If interest in the new issue seems week, the offer price may be reduced below the range or the offering may be withdrawn altogether.

5. The price of the securities is often determined just before they are to be sold. The IPO is said to be effective and the shares are then offered for sale to the public, a process known as opening the books on the new issue. The managing underwriter may attempt to stabilize, manipulate or control the security price through a price-pegging operation.2 In the price-pegging operation, the managing underwriter attempts to prevent members of the underwriting syndicate from undercutting an agreed upon sale price for the securities. This operation typically has the managing underwriter placing a buy order in secondary markets at a price just below the syndicate price for the new issue. If syndicate members attempt to undercut the syndicate price by selling for less than this secondary market buy order price, investors will rush to buy from the "syndicate cheater" to sell to the managing underwriter at the higher price. The typical price pegging operation lasts for approximately two to four days and its costs are shared by the underwriting syndicate. The prospectus must state that there will be a price-pegging operation if one is planned. Some evidence suggests that these operations are often ineffective and their legality has been challenged - though not successfully - in the court system.3 In addition, this price stabilization process provides protection to participants in the market for the security, improving the market's acceptance of the new issue. Price pegging may also contribute to the IPO underpricing phenomena discussed below. Price supports and stabilization also seem to enhance underwriters' reputations with issuers and clients.

Investment banks also tend to be active in secondary markets for stocks they underwrite. In addition to the price stabilization role discussed above, investment banks also develop and maintain closer relationships with clients by participating in secondary markets. These improved relationships make it easier for underwriters to place their new offerings. Furthermore, their participation in secondary markets improve liquidity for securities they underwrite. In addition, 2According to Hess and Frost [1982], 57% of 274 seasoned issues between January 1, 1975 and March 1 1977, had price supports.

3Securities Exchange Commission Rule 10b-7 permits underwriter price supports because it reduces underwriter losses due to temporary downward price pressure during IPO selling periods.

4

secondary markets participation provides opportunities to realize profits. Taking a firm public is a costly activity for a firm. Auditing, legal and auditing fees along with substantial management time are among the costs of taking the firm public. Several studies (e.g., Chen and Ritter [2000]) have observed a remarkable similarity among underwriting fees, which seem to be concentrated around 7% of the issue amount. Furthermore, most IPOs are underpriced (This will be discussed in detail later). IPOs occur with the expectation that the issued securities will develop liquid markets. This enhanced liquidity may reduce the firm's cost of capital and bring added attention to the firm’s products. There are a few alternatives to using underwriters in the IPO process. For example, Spring Street Brewing Company used web-based documents, prospectuses and solicitations to offer its IPO. WitCapital (later merged with Soundview Technology Group) was formed for the purpose of providing web-based IPOs. Google, in its widely publicized IPO 2004 offering, structured a Dutch auction process to sell 25.8 million shares of its stock, suggesting bids in the range of $108 to $135 per share. This Dutch auction will search bids for a clearing price that enables it to sell its 25.8 million shares. Lead underwriters, Morgan Stanley and CS First Boston collected a 3% commission on this offering rather than the standard 7% fee. Some observers opined that, if successful, the Google IPO could lead to a transfer of power and fees away from underwriters in favor if issuing firms. W.R. Hambrecht & Co., a smaller investment bank marketing primarily to individual investors, uses a web-based auction process to offer securities for its clients. Some observers believe that these nontraditional approaches to offering IPOs will improve prices received by issuing firms and allow smaller retail investors to participate in IPO markets that they are generally shut out of.

5

B. The IPO Anomalies IPO anomalies refer to three unusual pricing patterns associated with Initial Public offerings of equities: 1. Short-term IPO returns are abnormally high. 2. IPOs seem to under-perform the market in the long run. 3. IPO under-performance seems to be cyclical. The most dramatic pattern is that Initial Public Offerings (IPOs) have been shown to generate significant abnormally high short-term returns. These returns are most substantial on the day of the new issue. For example, in December 1999, stock in VA Linux was offered in an IPO at $30 per share. By the end of its first day of trading, the stock had traded at $239.25 per share. While the VA Linux example is rather extreme, significant abnormal IPO returns typically exist after adjusting for risk.4 Thus, it seems that unseasoned offerings with no trading histories do generate abnormally high short-term returns. Such offerings seem underpriced even when there is substantially greater interest among investors than shares available of the IPO. Although many of these studies have found that IPOs tend to be riskier than other investments empirical studies indicate that abnormally high offer date returns simply cannot be explained by IPO risk. Additional evidence suggests that "favored" clients of the underwriting firm frequently are the beneficiaries of this apparent underpricing. Given that this underpricing phenomenon may seem to raise the cost of capital to issuing firms, there is substantial interest in both the academic and investing communities in finding an explanation for this persistent phenomenon. On the other hand, we note that the evidence regarding longer-term IPO returns is not clear. Longer term returns on IPO's do not seem nearly so high; in fact, several studies report IPO returns to be negative over the period 20 days to two years after the IPO (See, for example, Ritter [1991]). Some evidence exists which suggests that these IPO returns are due to the provision of useful price-setting information by IPO market participants and by price supports in the IPO aftermarket. There exist a number of theories intended to explain the underpricing phenomena. For example, one might expect that underwriters and issuers of IPOs along with each of the individual investors would have different sets of information regarding to the value of the issue. Many of the underpricing theories contend that underpricing is a form of compensation for the risk that a particular party bears because of an assumed informational advantage of one of the parties over another, and other theories propose underpricing is compensation for providing information to other participants. Baron [1982] suggests that the underwriter simply uses its superior information access and processing to price the issue to the advantage of its investing clients and itself, at the expense of the issuing firm. Issuing firms accept this "exploitation" because the underwriter still markets the new issue better than the issuing firm could. However, Muscarella and Vetsuypens [1989] 4See, for example McDonald and Fisher [1972], Ibbotson [1975] and Ritter [1984]

6

cast doubt on this conclusion based on their finding that issuers act as their own underwriters experience as much IPO underpricing as issuers employing underwriters. Myers and Majluf [1984] argue that a firm uses its informational advantage over investors and will issue stock only when it is overpriced. Hence, managers will use their inside information to ensure that their employers will issue stock only when investors should not wish to buy. This is the “lemon problem.” Rock [1986] argues that underpricing is a result of the risk assumed by uninformed investors because of the informational advantage of issuer, underwriter and informed investors. Underpricing of IPOs is necessary to induce uninformed investors to participate in a market where they can be exploited by more informed investors. In Rock's model, informed investors do not have enough capital to take up the entirety of any new issue. Thus, participation in IPO markets is required of uninformed investors. Informed investors participate only in underpriced offerings and earn higher than normal returns. Uninformed investors, unable to distinguish between underpriced IPOs and overpriced IPOs, participate in all new offerings. Thus, on average, IPOs must be underpriced for uninformed investors to earn normal returns and ensure their participation. Koh and Walter [1989] find empirical evidence supporting the Rock model. Greenblatt and Hwang [1989] claim that underpricing is a signal by a more informed issuer to indicate firm value and the variance of expected returns to less informed investors.5 Beatty and Ritter [1986] extend Rock's model and find that underpricing is an increasing function of the ex-ante uncertainty of the issue. Carter and Manaster [1990] develop another extension of Rock's model demonstrating that as the risk of an issue increases, informed demand will increase, exacerbating the adverse selection problem and the required underpricing. Low risk firms can not creditably distinguish themselves from high risk firms. However, they can employ high reputation investment banks to certify that they are low risk firms, which allows them to underprice by less. Booth and Smith [1986 hypothesize that the underwriter stakes its reputational capital as a bond that securities' prices reflect all potential negative inside information about the expected performance of the firm. Underpricing provides both protection and compensation for the use of the underwriter's reputational capital. Numerous other studies have found that issues underwritten by low-prestige investment banks have higher initial returns than high-prestige banks. Among these are McDonald and Fischer (1972), Logue (1973), Neuberger and Hammond (1974), Block and Stanley (1980), and Neuberger and LaChapelle (1983), and Johnson and Miller (1987). Tinic [1988] argues that underpricing is a form of insurance to protect underwriters against potential due diligence legal liabilities. The Securities Act of 1933 requires all parties to an offering to perform "due diligence" and requires that parties attempt to include all relevant information in the prospectus. If any party neglects its "due diligence", it may be subject to criminal and/or civil prosecution. Tinic (1988) hypothesizes "that underpricing serves as a form of insurance against legal liability and the associated damages to the reputations of investment bankers." Tinic's theory of underpricing focuses on the role of due diligence requirements on the underwriting process. If an issue is overpriced, the investment bank may be subjected to legal

5Welch (1989) and Allen and Faulhaber (1989) also develop signalling models where underpricing is a direct signal to the market about the value of a firm.

7

liabilities. Therefore, underpricing reduces the probability that investment banks will be sued for lack of due diligence. Tinic provides empirical support for his hypothesis by showing that underpricing seems to be a post-Depression phenomenon, when securities laws were in effect. On the other hand, Keloharju [1993] demonstrates that the IPO effect prevails in Finland, despite the fact that class action lawsuits are rarely filed. Contrasting the above theories proposing that underpricing is related to private information that the firm has which is not available to investors, Benveniste and Spindt [1990] suggest that informed investors reveal their information to the underwriter by their preliminary interest and orders before the offering price is set. Underwriters use this preliminary indication of interest to help determine the actual offer price of the IPO. Underpricing is regarded as compensation to informed investors for the information that they convey to the underwriter through their preliminary offers that will be used in the price-setting process. Several other theories explaining IPO underpricing also rely on informational asymmetries. For example, Chemmanur [1989] argues that underpricing is intended to encourage information production and dissemination by investors so that the issuer can receive higher prices for subsequent issues of securities. Sherman [1992] argues that in best efforts offerings, issuers maintain an option to withdraw from the market their securities if demand for them is low. Issuers pay for this option by accepting reduced prices for the securities that they offer. Providing support for the information theories of IPO underpricing are empirical studies on closed-end fund IPOs. For example, Peavy (1990) examined 41 closed-end fund IPOs going public during 1986 and 1987 and finds that their returns are not significantly different from zero, contrasting to the overwhelming empirical evidence that non-fund IPOs are significantly underpriced. Clearly, the asymmetric information between the issuer, underwriter and investor for closed-end funds (which are typically portfolios of securities) is less than for nonfund IPOs. Weiss (1989) analyzed 67 closed end funds that went public between 1985 and 1987 and obtained results similar to those of Peavy. Muscarella and Vetsuypens (1989) also found support for the asymmetric information theory. They argued that the information asymmetry should be significantly reduced for IPOs of companies that were once public, then taken private. Supporting the information hypothesis, they found that for the 74 IPOs in their sample which had previously been public, then taken private, underpricing was significantly less than for other IPOs. Ruud [1993], Schultz and Zaman [1994], Hanley, Kumar and Seguin [1993] and others find evidence that IPO returns are due, at least in part, to underwriter price supports in the aftermarket. For example, Ruud finds that approximately one fourth of 463 IPOs from 1982 and 83 have first day returns equal to zero and that the distribution of IPO returns is skewed to the right. Approximately two thirds of those IPOs with zero first day returns have zero or negative returns over the following week. This suggests that underwriters are providing price supports for "cold" IPOs early in the aftermarket, delaying drops in market prices for at least one week. Schultz and Zaman suggest that underwriters provide price support for IPOs by placing purchase orders for new issues in a manner described above. At the same time, they secure an over-allotment option enabling them to purchase additional shares from the issuer at a specified

8

price. They oversell (short) the offering, knowing that if the price rises, underwriters can exercise their over-allotment options. If the issue price falls, they cover short positions with the shares purchased as a result of the price support. Thus, if the IPO is hot (its market price increased), additional shares will be sold to investors due to the over-allotment option. It has been well established that IPO returns tend to be extremely high on issue dates; it also seems that many small investors lack access to this lucrative market, particular for the spectacular performers. However, a paper by Krigman, Shaw and Womack finds that IPOs which perform well (up between 10% and 60%), but not spectacularly (up by more than 60%) on the issue date tend to be better long-term performers, by 14% over the first year. Ritter suggests that underwriters attempt to underprice IPOs by 15% to 30%, and those IPOs that substantially outperform this range are overbid by investors. In addition, those IPOs that are sold (flipped) on the issue date by their original purchasers tend to be outperformed over the longer term by IPOs that are held beyond their original purchasers on the issue date. The lessons here for the small investor who must purchase the IPO after its date of issue are to avoid the particularly hot issues and those which have been flipped by their original purchasers. Many observers note that IPO underpricing transfers wealth from original owners of the firm going public to its new owners; that is, the underwriter is “leaving money on the table.” For example, Ritter [1998] notes that the August 1995 Netscape IPO of 5.75 million shares at $28.00 per share left $174 million on the table due to its increase to $58.25 on its first day of trading. Shouldn’t Netscape’s original owners have been incensed at its underwriter for this “loss” of $174 million? Apparently, they were not. Perhaps the original owners actually originally expected a much lower payment for its shares. Netscape’s preliminary prospectus listed an anticipated offer price range of $12-14 per share for 3,500,000 shares (plus a 15% overallotment option). Clearly, they must have been pleased at the increase of this offer price, which the underwriter undoubtedly attributed to its strong marketing efforts. Yet, it appears that Netscape didn’t insist on its shares being marketed at an even higher price. So, original shareholders, purchasers of the IPO and the underwriter seem all to be quite happy with such an IPO result. Negative long-term returns for IPOs have a number of possible explanations. Some observers have noted that the initial buyers into the IPO, who were most optimistic about the IPO prospects, sell into a market with less optimistic buyers. Furthermore, the most successful marketing and pricing efforts for an IPO are likely to be those with the most successful unsubstantiated hype. Survey results suggest that perhaps as many as one-fourth of buyers of IPO shares do not perform proper fundamental analyses. In addition, IPOs brought to market during hot market cycles might be expected to draw less enthusiasm during later cooler market cycles when they are sold.

9

C. Exchange Markets Secondary markets are markets for previously issued shares. Secondary markets provide liquidity for primary market participants. The pricing of securities in secondary markets also provides important information evaluating firm performance and opportunities as well as for the pricing of securities in primary markets. Secondary markets have been traditionally classified into first markets (exchanges), second markets (Over the Counter Markets), third markets (broker assisted off-floor [or OTC] markets for exchange listed issues) and fourth markets (non-broker assisted off-floor markets for exchange listed issues) through electronic communication networks (ECN, a computer facility to trade financial products outside of exchanges). However, these sorts of distinctions are dwindling due to massive changes in market structures. The following paragraphs describe some of the secondary securities market architectures that have been developed over the years. However, in recent years, exchanges and other markets have engaged in cutthroat competition with one another, leaving the market in a state of flux and likely soon to be quite different from these descriptions. An exchange is traditionally defined as a physical meeting place drawing together brokers and dealers to facilitate the buying and selling of securities. More recently, this definition has been extended to include electronic facilities. In the United States, exchange transactions are executed through an auction process. Exchanges in the United States are intended to provide for orderly, liquid and continuous markets for the securities they trade. A continuous market provides for transactions may be executed at any time for a price that might be expected to differ little from the prior transaction price for the same security. In addition, exchanges serve as self-regulatory organizations (SROs) for their members, regulating and policing their behavior with respect to a variety of rules and requirements.

As of May 2007, NYSE Euronext, the world’s largest exchange and its first global exchange, operates six equities exchanges and six derivatives exchanges in five countries. NYSE Euronext was launched on April 4, 2007 by a merger between the New York Stock Exchange Gorup and Euronext, NV. The New York Stock Exchange Group, formed by the 2006 merger of the New York Stock Exchange and the Archipelago Exchange, operates the New York Stock Exchange (NYSE) with its now diminishing physical trading floor, the Archipelago Exchange (NYSE Arca), an electronic exchange, and the Pacific Exchange. NYSE Euronext is a public company whose shares are listed on the New York Stock Exchange. Traditionally, the New York Stock Exchange (NYSE) and the American Exchange (ASE or AMEX) have been regarded as the two national exchanges in the U.S. Other exchanges still function, and are sometimes known as regional exchanges. These might include those in Chicago (formerly the Midwest Exchange), Boston and Philadelphia, but again, even this terminology and definitions are in flux. The Pacific Exchange, with trading floors in San Francisco and Los Angeles, was owned by Archipelago, which has since merged with the New York Stock Exchange to form the New York Stock Exchange Group. These regional exchanges list stocks that would not qualify for national exchange listing as well as provide local or competing markets for a number of national exchange listed securities. In some instances, either lower transactions costs or better prices can be obtained for clients for dual-listed securities on the regional exchanges; to some extent, competition provided by these regional exchanges may

10

provide lower transactions costs for investors. There also exist a number of exchanges for other securities such as the Chicago Board of Trade (CBT - for futures contracts), The Chicago Board Options Exchange (CBOE), the Kansas City Board of Trade and the Commodities Exchange (COMEX). Finally, there are several exchanges without actual trading floors, including the National Exchange (formerly the Cincinnati Exchange that is currently located in Chicago) and the International Securities Exchange (ISE). These exchanges operations are based entirely on electronic platforms. As of 2006, the New York Stock Exchange, which traditionally has maintained the most stringent listing requirements, listed securities of approximately 3000 companies with a combined market value of over $22.6 trillion. During the same year, AMEX listed about 1000 stocks with a combined value of $126 billion. NASD divested itself of NASDAQ in 2000/01, whose listings have grown to approximately 3300 stocks. Larger companies whose stocks were traded on NASDAQ as of December 2004 included Microsoft (market capitalization $290 billion), Intel, Cisco Systems, Dell (all over $100 billion), Amgen, eBay and Oracle. The National Association of Security Dealers (NASD) described above as the self-regulated agency cooperating with the S.E.C. is empowered by the S.E.C. to regulate, police and discipline its members. The S.E.C. maintains authority to overrule the NASD. The Way it Was Stock markets have until recently evolved rather slowly over the centuries, hanging on to their traditions, rules and regulations. Much of their current structures and idiosyncrasies owe from this evolution. Understanding how they functioned in the past is helpful in understanding their current structures, policies and procedures. Precursors to stock exchanges may have existed in Egypt as early as the 11th century, where it is believed that Jewish and Islamic brokers traded a variety of credit-related instruments. 13th century Bruges (Belgium) commodity traders assembled in the van der Beurse family home (and inn), ultimately becoming the “Brugse Beurse.” Additional bourses later opened elsewhere in Flanders and Amsterdam. The Amsterdam Stock Exchange opened in the early 17th century, trading shares of the Dutch East India Company. The exchange continues to operate as a unit of Euronext. The first securities exchange to operate in the United States was in Philadelphia, opening operations in 1791. The New York Stock Exchange began operations outdoors after the 1792 signing of the “Buttonwood Agreement.” This contract, signed under a buttonwood tree, fixed brokerage commissions among its signors and prohibited off-board trading (i.e., traders and brokers were to trade only with each other). In earlier days, exchanges often operated outdoors so that brokers could call out their orders from their office windows to the street where transactions actually took place. In 1865, the New York Stock Exchange adopted its current name. The American Stock Exchange, previously known as the New York Curb Exchange, did not move indoors until 1921. For most of its history, NASDAQ was not considered to be an exchange because it did not have a physical trading floor. Founded in 1971 by the National Association of Securities Dealers (NASD), NASDAQ, formerly known as the National Association of Security Dealers Automated Quotation System (NASDAQ), has served as an

11

electronic stock market allowing brokers and dealers to efficiently transmit bid, offer and close prices for securities. Since the New York Stock Exchange has been the largest exchange in the world, we will first emphasize its structure and organization, first past and then present. Until 2006, the NYSE was a sort of hybrid corporation/partnership whose members faced unlimited liability.6 At the same time, the NYSE structure was unaffected by the death of one of its 1366 members. Only members who owned or leased seats had trading privileges and there number four types of members. Each member was an individual and most were sponsored by or associated with a brokerage firm or other organization (typically called a member firm). A membership is often referred to as a seat, which was purchased (for as much as $4 million in 2005, and last sold on December 29, 2005 for $3,505,000) through a competitive market process. Full membership was limited to 1366 seats, though there have been special limited trading permits issued as well. Now, one can join the 1366 members by purchasing a license that permits the member to trade for one year. As of July 2006, the annual fee for a license was $54,219. The four types of memberships are as follows:

House Broker: also known as a commission broker executes orders on behalf of clients submitting orders through brokerage firms. Until 2006, approximately half of the members on the floor were commission brokers. Independent Broker: also called a two-dollar broker, executes orders on behalf of commission brokers when activity is high. Alternatively, sometimes commission brokers executing orders on behalf of off-floor clients are referred to as floor brokers. Floor Trader: execute orders on their own trading accounts. As of 1992, there were approximately 40 floor traders on the NYSE and this number continued to decline. Specialist: is charged with the responsibility for maintaining a continuous, liquid, orderly market for the securities in which he specializes. He also keeps the book (records) for unexecuted transactions and buys and sells on his own account. As of 1992, there were approximately 400 specialists on the NYSE. Specialists are typically selected on the basis of their performance as specialists for other securities. Specialists were involved in approximately 20% of NYSE transactions as a principal. Because of his dual roles as running the market for securities on behalf of the exchange and as trader buying and selling those securities at a profit, the specialist's role is particularly interesting. The specialist is expected to fulfill his obligation to maintain a continuous, orderly and liquid market; this role may conflict with his desire to earn a profit from trading those securities. Trading activity for the shares of approximately 2779 listed firms (prior to 2006)

center about trading posts located around the floor throughout various rooms. Brokers and traders would congregate about these posts and specialists who oversee trading activity. Clerks employed by the exchanges record trading activities and relayed records to systems that disseminated data to the investing public. 6 Many exchanges (worldwide), including the American Stock Exchange (until 2007) still maintain this hybrid “partnership” type of structure.

12

Over the years, exchanges have dramatically increased their ability to handle increasing

transactions volume (averaging over 1.5 billion million shares per day in 2005, with over 3 billion on June 24th alone) due to improved technology. Some exchanges had permitted all or most of their orders to be routed and executed electronically while others provide electronic routing and execution only for specific types of orders. For example, the Super DOT (Designated Order Turnaround) computerized routing and trading system employed by the New York Stock Exchange has permitted small orders (generally defined as less than 30,099 shares) to be routed electronically to the specialist by a brokerage firm. Most program trades were also submitted through the Super Dot system as well, accounting for over 10% of all orders. Overall, the SuperDOT system has executed approximately 99% of all NYSE orders. For these SuperDOT orders, the brokerage firm need not have the order presented at the trading post by a commission broker. This means that the order can be executed faster. The Post Execution Reporting System used by the AMEX and the Small Order Execution System used by NASDAQ (The National Association of Securities Dealers Automated Quotations System to be discussed shortly) perform functions similar to SuperDOT. When the NYSE opens at 9:30 EST, orders of up to 30,099 shares which have accumulated in the Opening Automated Report Service (OARS) are matched and the specialist attempts to establish a market clearing price. The specialist will attempt to open the security at a price that deviates as little as possible from the prior day's close at 4:00 PM. Transforming the NYSE On April 20, 2005, the New York Stock Exchange dropped a bombshell on the investing public, announcing its intent to be taken over by Archipelago. In a single sweep, the NYSE would be merged, privatized, expanded into derivatives and have its springboard for the switch to electronic trading. Stock markets have traditionally emphasized roles of the specialists who conduct auction markets and maintain liquidity for off-floor brokers and traders. Since the founding of the NYSE in the late 1700's, exchange markets have brought together widely dispersed brokers, dealers and individual investors, creating highly organized, visible and regulated environments intended to facilitate trading and price discovery. The traditional floor-based stock exchange in the U.S. centered around a specialist with a regular "trading crowd" that focused its energies on a small number of stocks. Floor brokers enter the crowd with orders initiated by larger off-floor traders while smaller and routine orders are more likely to be routed electronically to the specialist through a system such as SuperDOT. However, the merger followed on the heals of the Richard Grasso compensation quagmire, the $6 billion deal granted the 1366 NYSE members about 64% of the combined firm's shares and the remainder to Archipelago shareholders (30%), NYSE top management (5%) and lower-level managers and employees (1%). Interestingly, the 5% granted to NYSE CEO John Thain and other top managers was valued at approximately $300,000,000, more than the disputed sums paid to Richard Grasso. A number of NYSE member-seat holders, notably Kenneth Langone, former Chairman of the NYSE Board of Directors complained about the price accepted by NYSE management. However, a seat on the NYSE sold for $960,000 in January 2005, $1,600,000 on April 20, 2005, shortly before the takeover announcement and for $3,000,000 in July 2005, shortly after the takeover announcement. By year-end, the price of a seat had risen to $4,000,000 before dropping to $3,505,000 at year-end. In addition, some NYSE

13

members complained about Thain's former employer, Goldman Sachs representing both sides in the deal. Furthermore, Goldman Sachs owned several seats on the NYSE and maintained substantial holdings of Archipelago shares. However, two other investment banks, Greenhill and Lazard did required due diligence for the deal. The deal was valued by these institutions at between $3 and $5 billion, a substantial discount below the value implied by the July 2005 market price of Archipelago shares.

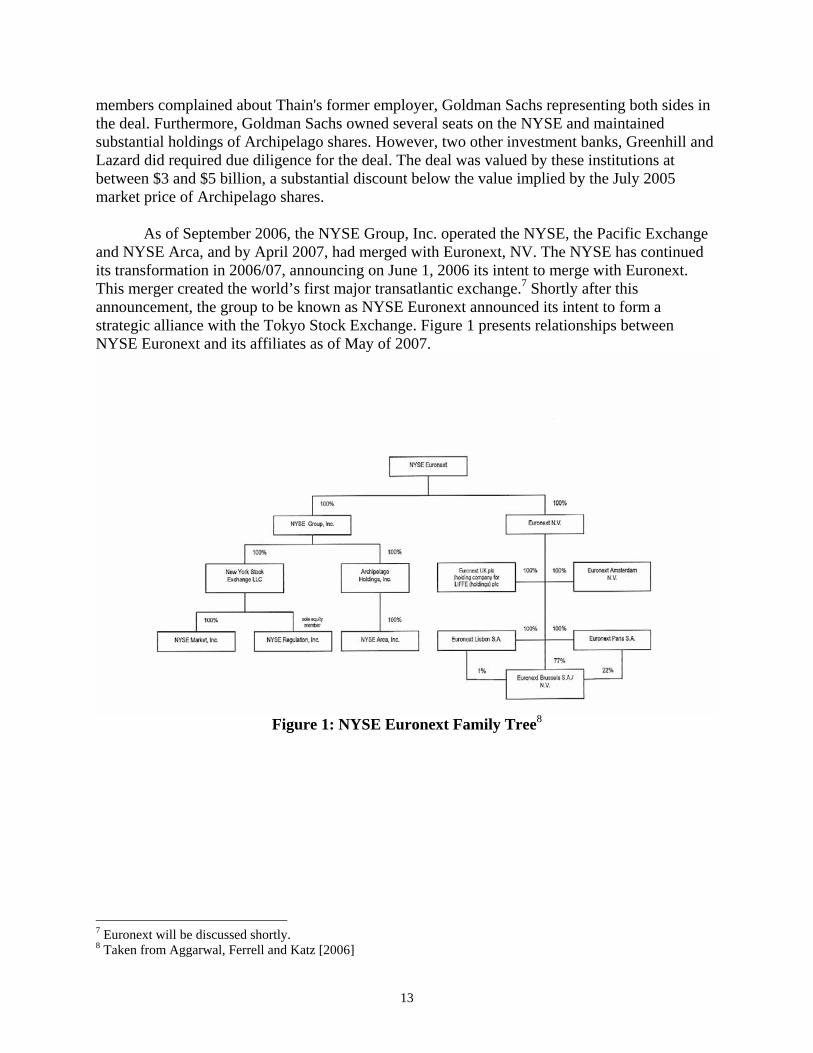

As of September 2006, the NYSE Group, Inc. operated the NYSE, the Pacific Exchange and NYSE Arca, and by April 2007, had merged with Euronext, NV. The NYSE has continued its transformation in 2006/07, announcing on June 1, 2006 its intent to merge with Euronext. This merger created the world’s first major transatlantic exchange.7 Shortly after this announcement, the group to be known as NYSE Euronext announced its intent to form a strategic alliance with the Tokyo Stock Exchange. Figure 1 presents relationships between NYSE Euronext and its affiliates as of May of 2007.

Figure 1: NYSE Euronext Family Tree8

7 Euronext will be discussed shortly. 8 Taken from Aggarwal, Ferrell and Katz [2006]

14

D. Over the Counter Markets The over the counter markets have traditionally been defined as the non-exchange markets. Securities that do not trade in the exchange markets are said to trade in the over the counter markets. The over the counter markets are made up of broker-dealer houses that execute transactions on behalf of client accounts as well as their own. Almost all federal, municipal and corporate bonds are traded in the over the counter markets as well as stocks of smaller corporations. Brokers and dealers in the over the counter markets belong to the National Association of Securities Dealers (NASD), a self-regulated agency cooperating with the SEC. As of 2006, over 5100 broker/dealer firms and over 657,800 registered representatives were members of NASD. NASD also operates the largest securities dispute resolution forum in the world, processing over 8,000 arbitrations and 1,000 mediations per year. Sometimes references are made to so-called third and fourth markets. Third markets exist for listed securities traded between brokers off any exchange. Fourth markets exist when institutions trade securities directly among themselves in the so-called upstairs market. This market is frequently used by institutions for block trades (transactions for more than 10,000 shares or $200,000 of a security), particularly when such a transaction might pose liquidity problems on an exchange. The upstairs markets accounts for approximately one half of all stock transactions volume. The largest of the electronic communication networks (ECN’s) include Instinet and Archipeligo which provide electronic forums for linking dealers with each other and with institutional investors and match and cross trades in the upstairs market (fourth market). Instinet was founded in 1969, became a wholly owned subsidiary of Reuters in 1987, took its shares through an IPO in 2001 and merged with Island shortly afterwards before going private again in 2005. The focus of Instinet’s activities is block trading (10,000 or more shares). In addition, many institutions maintain a block executions department. Other ECNs include Bloomberg TradeBook, BATS Trading, Track Data and have included BRUT (purchased by Nasdaq) and Island (merged into Instinet). Sometimes, these markets third and fourth markets are referred to as being part of the over the counter markets. Alternative Trading Systems Most Alternative Trading Systems (ATS) are Internet-based. However, as we will see shortly, this distinction between floor-based and Internet-based systems is not entirely clear. Some observers have simply defined the ATS as an electronic proprietary market or “fourth market” that is maintained by a third party with a limited SRO (Self-regulatory Organization) function. The SEC defines an Alternative Trading System (ATS) to be an automated system that centralizes, displays, crosses, matches or otherwise executes trading interest, but is not currently registered with the Commission as national security exchanges or operated by a registered securities association. However, the SEC later redefined the term “exchange” to include “any organization, association, or group of persons that: (1) Brings together the orders of multiple buyers and sellers; and (2) uses established non-discretionary methods (whether by providing a trading facility or by setting rules) under which such orders interact with each other, and the buyers and sellers entering such orders agree to the terms of a trade.” Under this new definition, at least several ATSs might be considered to be exchanges, even if they are not traditional "brick and mortar" exchanges.

15

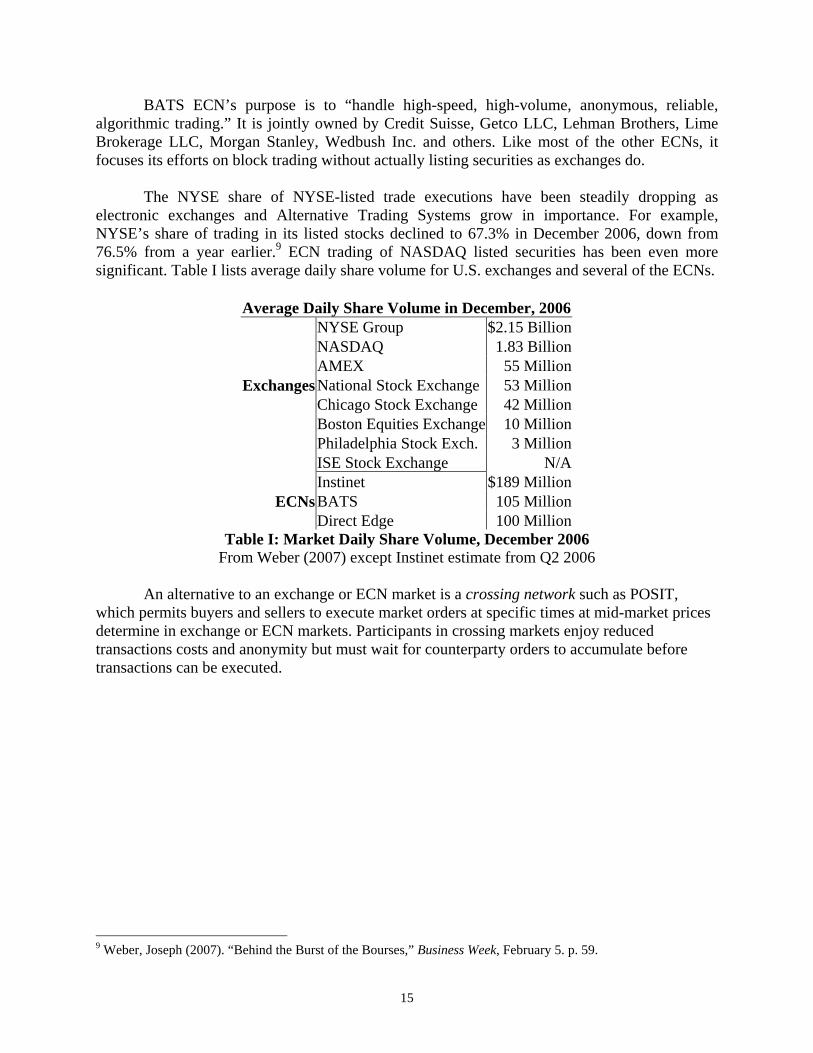

BATS ECN’s purpose is to “handle high-speed, high-volume, anonymous, reliable, algorithmic trading.” It is jointly owned by Credit Suisse, Getco LLC, Lehman Brothers, Lime Brokerage LLC, Morgan Stanley, Wedbush Inc. and others. Like most of the other ECNs, it focuses its efforts on block trading without actually listing securities as exchanges do. The NYSE share of NYSE-listed trade executions have been steadily dropping as electronic exchanges and Alternative Trading Systems grow in importance. For example, NYSE’s share of trading in its listed stocks declined to 67.3% in December 2006, down from 76.5% from a year earlier.9 ECN trading of NASDAQ listed securities has been even more significant. Table I lists average daily share volume for U.S. exchanges and several of the ECNs.

Average Daily Share Volume in December, 2006 NYSE Group $2.15 Billion NASDAQ 1.83 Billion AMEX 55 Million

Exchanges National Stock Exchange 53 Million Chicago Stock Exchange 42 Million Boston Equities Exchange 10 Million Philadelphia Stock Exch. 3 Million ISE Stock Exchange N/A Instinet $189 Million

ECNs BATS 105 Million Direct Edge 100 Million

Table I: Market Daily Share Volume, December 2006 From Weber (2007) except Instinet estimate from Q2 2006

An alternative to an exchange or ECN market is a crossing network such as POSIT, which permits buyers and sellers to execute market orders at specific times at mid-market prices determine in exchange or ECN markets. Participants in crossing markets enjoy reduced transactions costs and anonymity but must wait for counterparty orders to accumulate before transactions can be executed.

9 Weber, Joseph (2007). “Behind the Burst of the Bourses,” Business Week, February 5. p. 59.

16

E. The Decline of Brick and Mortar? The natural monopoly power associated with exchange-based open outcry stock markets owes its early existence to a nearly complete absence of technology and communications systems. Investors were far too dispersed to conduct unaided securities transactions and security traders required a central physical meeting site. This site, or exchange enabled large networks of local broker offices to execute securities transactions on behalf of these widely dispersed investors. New York's Wall Street district provided an excellent venue for this purpose and the individual exchanges filled specific niches in the securities markets. As telecommunication technology advanced in the early decades of the 20th century offering market access to millions of investors, U.S. securities markets nearly self-destructed, only to be salvaged by regulatory authorities and intense efforts by exchanges to curb market abuse. Exchanges now facilitate monitoring for regulatory compliance in much the same manner that they had facilitated trading. Exchanges were private mutual organizations owned by members representing brokerage firms and investment institutions and were regulated by individual states prior to passage of the Securities Exchange Act of 1934. Shortly after passage of this Act, the SEC gained authority over the exchanges that, in turn, monitored and regulated their members. Until the mid-1970’s, brokerage firms maintained their monopoly with a system of fixed transactions fees. All of their transactions were routed through the principle exchanges and off-floor markets. Exchanges had limited competition for securities listings. The primary sources of competition among securities brokers were in the arrays of services that they offered. After the price controls were lifted, the market saw formation of a number of discount brokerage houses that unbundled non-transactions services such as research and were able to offer drastically reduced execution costs. The market segmented to an extent, with some firms offering only transaction executions and others offering the full array of brokerage house services. However, the vast majority of transactions were still routed through the principle exchanges and off-floor markets. More recent technological developments in telecommunications, wireless communications and the Internet have imposed enormous competitive pressures on U.S. securities exchanges. With the electronic NASDAQ system beginning in 1971, competition from foreign fully-automated exchanges trading U.S. Securities (e.g., Eurex), development of fully automated exchanges in the U.S. (e.g., the ISE) and ECNs such as the Instinet, Island and Posit systems that allow direct trading between institutions, exchanges have been forced to accept and even innovate technological development to survive. The natural monopoly enjoyed by traditional “brick and mortar” markets has been enhanced by a number of barriers to entry. Overhead outlays are required for large investments in office facilities, communications equipment, fixed exchange fees and memberships, broker training and licensing and building client bases. Each of these overhead outlays are accompanied by significant time lags, increasing times required for recapturing initial investments. In addition, traditional brokerage offices experience significant returns to scale (see Stigler [1961]), making it almost impossible for smaller and newer firms to compete against larger better-established firms. Each of these barriers to entry into the securities brokerage business applies to the creation of overhead-intensive “brick and mortar” securities exchanges and markets. For example, in the

17

late 1990’s, the Chicago Board of Trade and the New York Mercantile Exchanges constructed new futures pits that cost $180 and $228 million, respectively. However, recent electronic and other technological developments, particularly the Internet substantially relieve these barriers to entry. First, the majority of prospective clients already have Internet access and usage skills. Transactions costs are substantially reduced through use of equipment already installed in client homes. Whereas the typical U.S. customer stock transaction executed through a phone call has a variable cost of about $1, its cost is reduced to just $0.02 executed online. Similar disparities exist in open-outcry and electronic markets. For example, the open outcry LIFFE charged about $1.50 per for long and short positions on the Bund futures contract in the late 1990’s; its electronic German competitor DTB charged only $0.66 for the same contract. Open outcry exchanges in the United States charge fees of approximately $1.50 contract (see Cavaletti [1997]).

More significantly, overhead expenses for Internet brokers run approximately 1 percent of assets, as opposed to 2-3 percent for brick-and mortar offices. Time required for Internet brokerage firm start-ups is substantially reduced relative to brick and mortar start-ups. In addition, the Internet and other technological advances have reduced economies of scale for brokerage firms. For example, as the Internet has replaced “cold-calling,” the fixed costs of seeking and soliciting the business of small clients have dropped significantly. Furthermore, clients of electronic brokers trade far more frequently than those of full-service brokers, with some estimates ranging to 10-25 times as frequent (Varian [1998]). Hence, smaller individual investors are able to play larger roles in securities markets at smaller costs. The increased participation of smaller investors enables them to replace specialists and market makers, at least to some extent, in the provision of liquidity to the market. In addition, the reduction of scale economies has increased competition among brokerage firms, in large part because so many of their services (e.g., advice, loans and cash management) could be unbundled and commoditized through automation. Some of these services require very little initial capital outlays and no unique technology.

Reduced brokerage commissions substantially increased competition in the brokerage

industry as reduced costs of service provision have softened barriers to entry. Brokerage commissions and fees have fallen from an average of $52.89 per trade in early 1996 to $15.67 in mid-1998. By 2000, a few online brokerage services had temporarily reduced their commissions to zero. This particular scenario is interesting and quite controversial because it seems to be a direct result of order flow payments, where brokerage firms receive their compensation from electronic exchanges and ATSs in payment for order flow. Many Internet brokerage firms currently maintain commission levels below $10 per transaction. Barriers to entry based on ownership of physical facilities are disappearing, and existing firms are being forced vary their product lines and to merge into other institutions.

Combinations, alliances and mergers between exchanges have also enabled smaller and

less efficient markets to compete against larger ones. These combinations have enabled exchanges and markets to mutually benefit from one another’s technological resources. Some of these combinations have been domestic such as OneChicago, LLC, an alliance created by the Chicago Board Options Exchange and Chicago Mercantile Exchange to trade equity futures contracts and the Pacific Exchange and the Archipelago Exchange merger. On the international

18

scene, the New York Mercantile Exchange opened a satellite open-outcry trading floor in Dublin for trading in a Brent crude oil futures contract and mergers among exchanges in other countries such as Euronext (formed by combining bourses in Amsterdam/Brussels/Paris/LIFFE/BVLP) and Eurex (combining the Deutsche Börse AG/SWX Swiss Exchange. Each of these latter combinations offered improvements in investors’ abilities to trade on a global basis.

Which trading and brokerage platforms result in lower trading costs? In an interesting

study, Bakos et al. [2000], with $60,000 provided by the Salomon Brothers Center at New York University, opened a series of accounts at various full-service, discount and electronic securities brokers. Their commissions for 100-share lots averaged $7.50 for electronic brokers and $47 for full-service voice brokers. They found that full-service brokers were more likely to route orders to the principle exchanges than electronic brokers and that such orders were more likely to be improved. However, for smaller orders, these price improvement advantages are more than offset by the higher brokerage commissions. Hence, specialists and market makers on exchanges were able to provide better order executions while brokers using electronic markets charged smaller commissions. It appeared that smaller investors fared better with discount electronic brokers while larger transactions resulted in better after-commission executions on the principle exchanges.

One of the more troubling aspects of electronic brokerage transactions is that customers

do not normally have a say in order routings and that orders need not necessarily be routed to the markets with the best prices. Many electronic markets have agreements with particular exchanges and markets to route transactions through them. These exchanges and market makers pay for order flow that might result in worse prices for clients. For example, in 1999, the Knight/Trimark Group paid $138.7 million for order flow, with over 10% of this sum received from Ameritrade, a large electronic brokerage firm (Bakos et al. [2000]). Specialists and market makers resent this controversial practice of order flow payment and many discount brokerage clients seem unaware of it. Demutualization of Exchanges Accompanying the increase of technology in trading has been a trend to demutualize exchanges. Euronext, the Australian and London Exchanges were among the first to demutualize in 1997, 1998 and 1999, following the Stockholm Exchange in 1993. NASDAQ demutualized in 2000 and the NYSE in 2006. Most exchanges justified restructuring to for-profit institutions based on their needs to raise capital to finance their technology and infrastructure expenses. Exchange self-regulation and other regulatory issues remain important concerns for these restructured institutions. To avoid conflicts of interest, the NYSE Group created a not-for-profit corporation, NYSE Regulation, Inc., with the New York Stock Exchange LLC as its sole equity member. This new corporation performs all the SRO (self-regulatory organization – to be discussed later) regulatory responsibilities currently conducted by the NYSE.

19

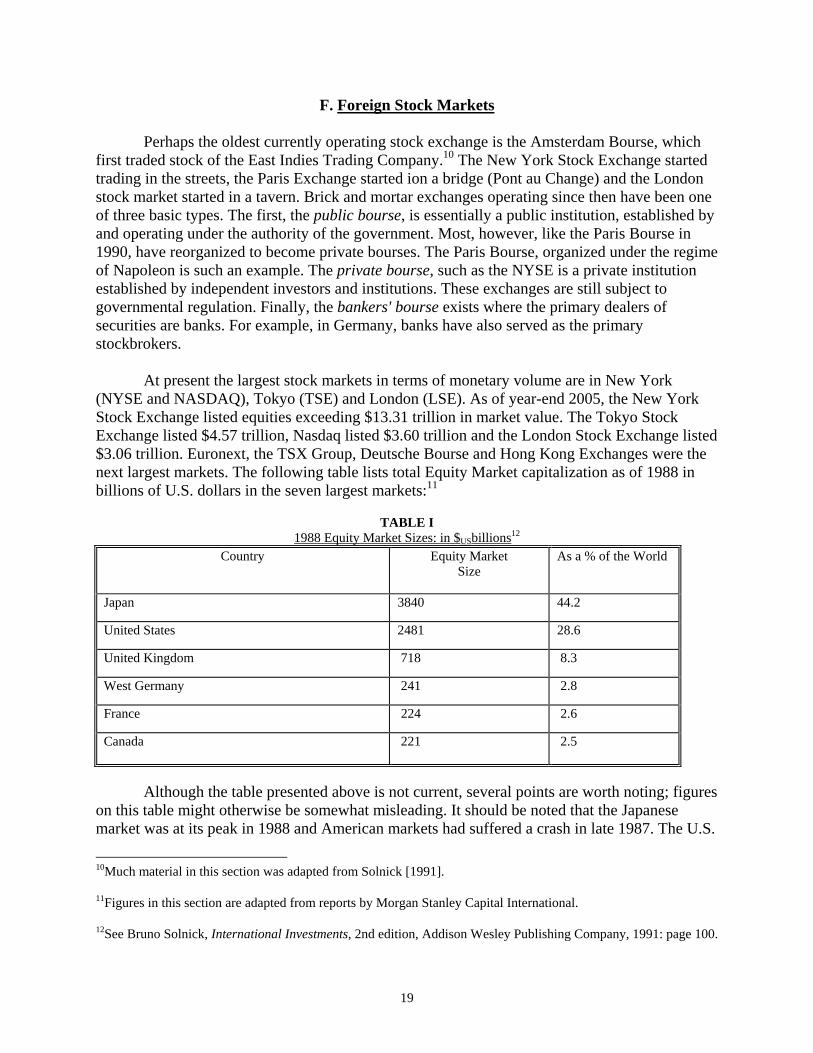

F. Foreign Stock Markets Perhaps the oldest currently operating stock exchange is the Amsterdam Bourse, which first traded stock of the East Indies Trading Company.10 The New York Stock Exchange started trading in the streets, the Paris Exchange started ion a bridge (Pont au Change) and the London stock market started in a tavern. Brick and mortar exchanges operating since then have been one of three basic types. The first, the public bourse, is essentially a public institution, established by and operating under the authority of the government. Most, however, like the Paris Bourse in 1990, have reorganized to become private bourses. The Paris Bourse, organized under the regime of Napoleon is such an example. The private bourse, such as the NYSE is a private institution established by independent investors and institutions. These exchanges are still subject to governmental regulation. Finally, the bankers' bourse exists where the primary dealers of securities are banks. For example, in Germany, banks have also served as the primary stockbrokers. At present the largest stock markets in terms of monetary volume are in New York (NYSE and NASDAQ), Tokyo (TSE) and London (LSE). As of year-end 2005, the New York Stock Exchange listed equities exceeding $13.31 trillion in market value. The Tokyo Stock Exchange listed $4.57 trillion, Nasdaq listed $3.60 trillion and the London Stock Exchange listed $3.06 trillion. Euronext, the TSX Group, Deutsche Bourse and Hong Kong Exchanges were the next largest markets. The following table lists total Equity Market capitalization as of 1988 in billions of U.S. dollars in the seven largest markets:11

TABLE I 1988 Equity Market Sizes: in $USbillions12

Country Equity Market Size

As a % of the World

Japan 3840 44.2

United States 2481 28.6

United Kingdom 718 8.3

West Germany 241 2.8

France 224 2.6

Canada 221 2.5

Although the table presented above is not current, several points are worth noting; figures on this table might otherwise be somewhat misleading. It should be noted that the Japanese market was at its peak in 1988 and American markets had suffered a crash in late 1987. The U.S.

10Much material in this section was adapted from Solnick [1991].

11Figures in this section are adapted from reports by Morgan Stanley Capital International.

12See Bruno Solnick, International Investments, 2nd edition, Addison Wesley Publishing Company, 1991: page 100.

20

dollar had weakened substantially against the yen as well as many other currencies. Furthermore, the table does not adjust for the more significant levels of cross-ownership of Japanese companies. In fact, approximately two-thirds of all Japanese equity is held by corporations (Osano [1996]. Thus, the Japanese figures are somewhat inflated due to the tendency for Japanese firms to hold stock in other firms. Much of this cross-ownership is due to formation of an informal Japanese institution known as a keiretsu. The keiretsu is a loosely organized family of closely related companies which is typically led and heavily financed by a main bank. Member firms are linked through business relationships and cross-ownership. We should as well note that as a percentage of overall economy size, more European capital is invested in privately held companies than in the United States. A study conducted by Booz, Allen Acquisition Services revealed that only 54% of the largest EC companies are traded, compared to 99% in the United States. Furthermore, European companies are more reliant on financing from banks, which frequently take equity positions in them. Thus, U.S. firms are more dependent on the public for financing. In addition, governments tend to play a larger role in European production than in U.S. production. The United Kingdom draws listings of more foreign companies than Germany due to taxes and transactions costs and German firms are more likely to be privately held than British firms. By 2001, the U.S. stock market had grown to about $13.9 trillion, over 55% of the world total, compared to $2.5 trillion for Japan and $2.3 trillion for the United Kingdom. The stock market capitalizations of Germany and France were over $1 trillion. Since 1974, China, India and the Pacific region have produced the largest growth rates in equity markets as a percentage of world equity markets. The combined proportions of these markets as a percentage of world markets has grown from 16% to 59% of world markets. Japan has been by far the most significant contributor to this figure. European equity markets as a percentage of the world total have increased from 22% to 26% of the world total. U.S. equity markets have remained fairly constant, declining from 57% to 55% of the world total. Over this 27-year period, the world equity market has grown from less than $900 billion to over $25 trillion as of 2001. ING Baring Securities reports that U.S. ownership of foreign stocks has increased from $41 billion in 1985 to $462 billion in 1995.13 This increased investment has been the product of a number of factors, including improved investing technology, reduced constraints on capital mobility, a greater appreciation for benefits of diversification and a belief in the potential for higher returns from foreign investment. Historically, European and Japanese investors have maintained higher levels of international investment. Market Micro-structure Market microstructure research is concerned with the efficiency and structures of the various securities markets. It is concerned with determining the best system for a given market. Generally, the best market is that which has the lowest transactions costs, results in the fairest prices, disseminates price information most efficiently and provides for the greatest liquidity. A 13See the Wall Street Journal, May 28, 1996, p.R23.

21

market is said to be liquid when prospective purchasers and sellers can transact on a timely basis with little cost or adverse price impact. One might argue that the exchange mandated responsibility of the specialist to provide liquidity in one-sided markets confers a liquidity advantage to the exchange while less-costly access might swing the advantage to the electronic market and its institutional participants. Bid-offer spreads are generally considered to be good indicators of liquidity, with narrow spreads indicating that price impacts of trading will not be severe. Many of the studies of electronic versus open-outcry trading have used on bid-offer spreads as a liquidity metric (e.g., Battalio, Greene and Jennings [1997] and Kumar and Shastri [1998]. Shyy and Lee [1995] found spreads to be wider in electronic markets than in open-outcry markets; Pirrong [1996] found the opposite. Pirrong argues that mis-communications and misunderstandings between trade participants reduce efficiency of open-outcry markets and that these issues are avoided in electronic markets. Several studies have found that the time to execute trades is certainly reduced in electronic markets. In addition, screen-based trading has facilitated after-hours markets. Now, a number of exchanges are offering investors opportunities to trade after normal business hours.

The evidence concerning the provision of liquidity by open-outcry exchange markets relative to electronic markets is both ambiguous and mixed (e.g., Pirrong (1996), Breedon and Holland (1997)). Some electronic systems have driven floor-based open outcry markets from contention. For example, Breedon and Holland describe how during 1997-‘98, the computerized Eurex drew practically 100% of the trading in German Bund futures from the open outcry LIFFE which had held a 70% market share. By 2000, LIFFE had abandoned open-outcry entirely for LIFFE CONNECT, a fully automated system. However, LIFFE did retain the bund options contracts, probably because of the more complicated strategies associated with them. In 1998, MATIF operated its open outcry and electronic systems simultaneously. Within two weeks, the computerized system had taken all volume from the open outcry markets that had to be closed. The Hong Kong Futures Exchange and the Sydney Futures Exchange both abandoned open-outcry during this same period. Frino et al. [2004] found that spreads narrowed on the Sydney and Hong Kong Exchanges; spreads widened on the LIFFE. In addition, according to Frino et al., bid-ask spreads on all three exchanges appear to widen in response to price volatility at a faster rate under electronic trading than with open-outcry trading, suggesting that the specialist-based system may offer better price continuity in periods of uncertainty.

On the other hand, open outcry markets have been particularly successful in the U.S. One

of the difficulties of screen-based trading is the ability to efficiently disseminate significant amounts of information concerning trades. While it is easy enough for screens to display bid and offer prices, most do not readily display order sizes. Open outcry participants are able to more easily communicate verbally order sizes, order types and combinations as well as other more complicated trade details. Such matters grow in importance when trade sizes are larger or when, for example, an options trader is attempting to leg into a spread or other position. While screen-based trading provides for a greater level of anonymity, many traders prefer a market where their counterparties can be identified. Furthermore, most markets are far more active during the conduct of open-outcry than during the after hours electronic periods. It is not clear the extent to which traders simply prefer to trade during “regular work hours.” In addition, Sarkar and Tozzi [1998] argue that open-outcry exchanges provide for more liquidity in more active markets while newer, less active issues are less likely to be found in open-outcry markets.

22

An important distinction between security trading systems concerns whether trading is

continuous. Stock exchanges in the U.S. and now, most exchanges elsewhere in the world permit continuous trading. These systems are called continuous markets. Transactions for securities in these markets can occur anytime the market is open. A number of markets, for example, the Frankfurt Stock Exchange, use a call system where a security is traded only once or a few times a day. In these markets, security orders are collected and bunched for execution at once when a clearing price is found. Call markets usually exist where trading is light or infrequent. Call markets can improve liquidity in less active markets by ensuring that interested traders congregate at the designated trading location at the designated time. Limit order prices in the typical call market are revealed only to the auctioneer. Trades executed in the same market are at the same price once the order accumulation is complete and the clearing price is established. Either a written or verbal call trading system may be used. The daily opening of the New York Stock Exchange might be characterized as a call auction. As with a number of other exchanges, the market reverts to continuous as the trading day progresses.

The Zurich Exchanges allowed for continuous trading after call market trading until

August 1996 when the system became electronic. Until the mid-1990's, the Paris bourse used a version of a call market known as the criée system where a clerk cried out a price for a given security to determine supply relative to demand. A variation of this system is still used for certain small issues. If there is an imbalance in this verbal call system, the clerk continues to cry out prices until it appears that the market will clear. The Madrid Exchange still uses a call system. The criée system may become obsolete as markets employ improved technology. However, the technologically advanced Tokyo Exchange still uses a form of the call system along with a continuous system for its most active issues.

Stock exchanges and markets vary with respect to how officials and members are

permitted to conduct their activities. The New York Stock Exchange permits its many of its members to act as both agents (brokers) and dealers. The Over the Counter Markets are dealer markets, where investors transact with dealers. The Tokyo Stock Exchange is exclusively an agency market. Fully automated systems such as the Toronto Stock Exchange do not necessarily require either a dealer or an agent to execute transactions. There have been a number of studies on the relative merits of specialist versus dealer markets. For example, Christie and Schultz [1994] argue that NASDAQ collaborated with one another in the setting of bid-offer spreads, increasing the costs of transactions.

Euronext N.V., formed in 2000 by the merger and integration of the Amsterdam, Brussels

and Paris stock exchanges, relies on electronic the trading system NSC (Nouveau Systeme de Cotation). In 2002, it expanded to include the London International Financial Futures and Options Exchange (LIFFE) and the Portuguese exchange BVLP.

The "Big Bang" of October 1986 brought several important changes in London Stock

Exchange practices. First, minimum brokerage commissions were abolished. Dual function market makers were permitted, enabling certain market participants to act as both broker and dealer. Membership requirements were substantially relaxed. Since this major event, the London Exchange has employed an electronic trading system similar to NASDAQ. The Stock Exchange

23

Automated Quotations (SEAQ) permits competing brokers and dealers access to each others' quotes. As a result of these very important changes, exchange listings have risen dramatically. Most transactions of shares involving larger companies are now executed using SETS (The Stock Exchange Trading Service) while larger block transactions are still executed through SEAQ.

The Tokyo Exchange (TSE) employs similar facilities known as the Computer-assisted

Order Routing and Execution System (CORES) which routes, executes and reports transactions for the majority of shares. The Floor Order Routing and Execution System (FORES) for the 150 most active Japanese stocks where floor trading remains dominant. Whereas in the U.S., the specialist may buy and sell shares, the saitori (TSE order taker) merely monitors trading and maintains the limit order books. The Toronto Exchange, with its Computer Assisted Trading System (CATS), provides an excellent example of use of computer technology in trading.

ADRs

American Depository Receipts (ADRs) are shares issued by banks evidencing ownership of shares of foreign company stock that are held by the bank. ADRs are the American version of a more general security known as an IDR, International Depository Receipt. Many ADRs are traded over-the-counter, but some meeting various regulatory and reporting requirements are exchange listed. Among the ADRs listed on the NYSE are Telefonos de Mexico, Glaxo, British Telecom and Royal Dutch Petroleum, all of which are among the most active securities on the exchange. These are level three ADRs, meaning that they conform to U.S. accounting standards and file 20-F statements (similar to 10-K reports) in English with the SEC. Other ADRs, such as Nestlé and Volkswagen, are level one, which trade over the counter and do not comply with U.S. accounting standards.

ADRs were originally developed by J.P. Morgan in 1927 to facilitate U.S. investment in

Selfridge's, a British retailer. ADRs are priced in dollars, though the underlying shares are still subject to currency risk. Over 1400 ADRs from more than 69 countries trade in U.S. markets as of 1999.

ADRs offer American investors opportunities to invest in foreign equity issues that are

traded on U.S. stock exchanges. This allows for some level of international diversification while maintaining the high level of liquidity associated with U.S. markets. These investments are denominated in dollars and may pay dividends converted into dollars. These dividends are usually not subject to the same stringent tax collection procedures as are many stock dividends in non-U.S. countries.

Sponsored ADRs are those whose creation has been facilitated by the underlying

company. Sometimes, these ADRs are referred to as ADS, or American Depository Shares. Foreign companies may wish to cross-list their securities in the U.S. to create a broader secondary market and improve liquidity for existing shares, particularly for American investors. ADRs may also increase visibility among the company's customers, suppliers and creditors. The empirical evidence on the impact of cross listing of is mixed. For example, Alexander, Eun and Janakiramanan [JFQA 1988] found that foreign firms cross-listing in the U.S. experienced positive returns. Howe and Kelm [FM 1987] found negative returns associated with U.S. firms cross-listing outside of the U.S.

24

In non-U.S. markets, other types international depository receipts offer investors opportunities similar to those provided by ADRs to American investors. The London Exchange offers Global Depository Receipts and the Singapore Stock Exchange trades Singapore Depository Receipts.

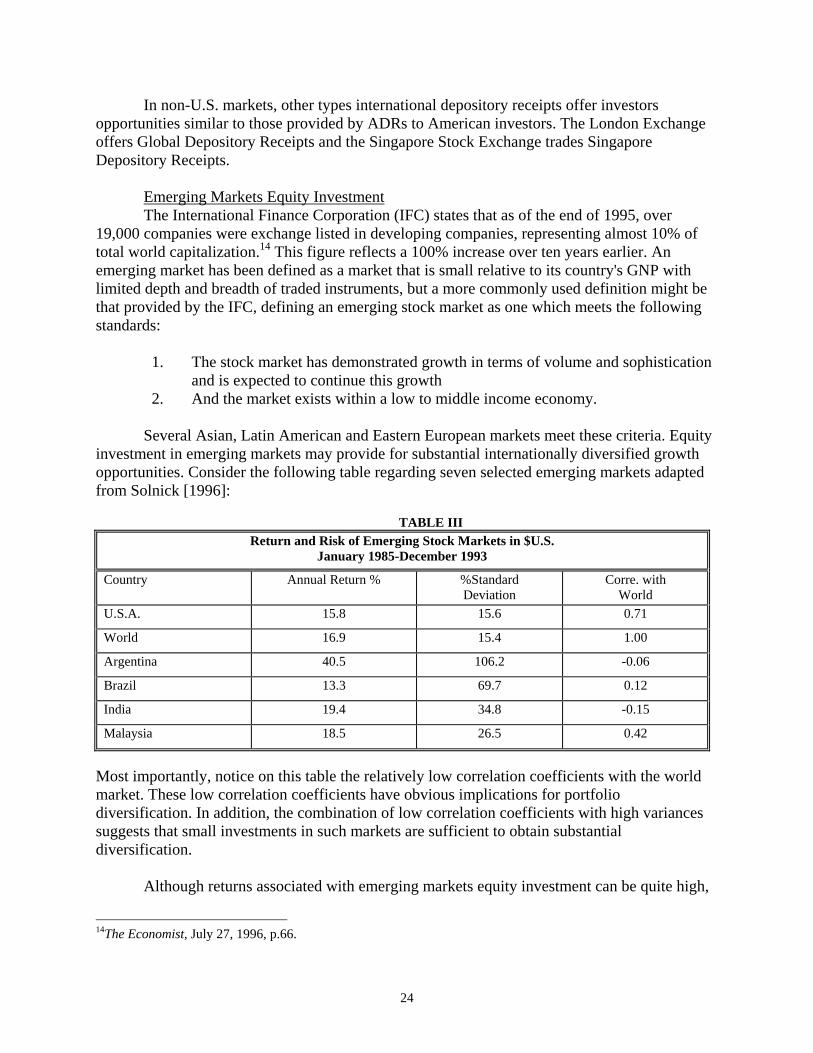

Emerging Markets Equity Investment The International Finance Corporation (IFC) states that as of the end of 1995, over

19,000 companies were exchange listed in developing companies, representing almost 10% of total world capitalization.14 This figure reflects a 100% increase over ten years earlier. An emerging market has been defined as a market that is small relative to its country's GNP with limited depth and breadth of traded instruments, but a more commonly used definition might be that provided by the IFC, defining an emerging stock market as one which meets the following standards:

1. The stock market has demonstrated growth in terms of volume and sophistication

and is expected to continue this growth 2. And the market exists within a low to middle income economy. Several Asian, Latin American and Eastern European markets meet these criteria. Equity