CHAPTER 3: LEARNINGS AND EXPERIENCE Internship programme was of great help to me. It helped me to understand the practical application of Income tax in real life. Internship programme gave me the much needed exposure which I was looking for. During my training session my main focus was on The following key areas • Assessment of Individuals, Firms and Companies • Filing of returns and Forms of Returns • Payment of advance Tax and TDS It was not easy to cover the entire portion of the above mentioned subject within the given duration of one month. My main focus was to understand the basic aspect of the above mentioned subject and also to know how these concepts were used in real life. The internship programme threw in a lot challenge for me. The greatest challenge for me was to adapt to the new situation (The corporate life) initially, I founded it very difficult to cope with it, but as the days went by I was able to gain the much needed confidence to perform my task. This programme has installed in me the much needed confidence to face the real challenges in a working environment. It was surely a wonderful experience for me personally because I feel at present I am ready to face any new Challenges thrown at me. I was also able to understand that there is a glaring difference between learning a subject and practical application.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER 3: LEARNINGS AND EXPERIENCE

Internship programme was of great help to me. It helped me to understand the practical

application of Income tax in real life. Internship programme gave me the much needed

exposure which I was looking for. During my training session my main focus was on

The following key areas

• Assessment of Individuals, Firms and Companies

• Filing of returns and Forms of Returns

• Payment of advance Tax and TDS

It was not easy to cover the entire portion of the above mentioned subject within the given

duration of one month. My main focus was to understand the basic aspect of the above

mentioned subject and also to know how these concepts were used in real life. The internship

programme threw in a lot challenge for me. The greatest challenge for me was to adapt to the

new situation (The corporate life) initially, I founded it very difficult to cope with it, but as the

days went by I was able to gain the much needed confidence to perform my task. This

programme has installed in me the much needed confidence to face the real challenges in a

working environment. It was surely a wonderful experience for me personally because I feel at

present I am ready to face any new Challenges thrown at me. I was also able to understand

that there is a glaring difference between learning a subject and practical application.

Assessment of Individuals

In the training programme I went through the main 5 heads of Incomes

• Income from salary

• Income from House property

• Income from capital gains

• Income from Business and Profession

• Income from other sources

An individual, firms and companies earn from the above mentioned Heads of income

Income from salary

Any person employed gets compensated by the way of remuneration for the services

rendered. It is received in cash or in kind by the way of amenities benefits and perquisites.

Every payment made by an employer to his employee for services rendered would be

chargeable to tax as income from salary.

Taxability allowances: These are allowances that are fully taxable without any exemptions

1) Basic Salary

2) Dearness allowances

3) Advance salary

4) Arrears of salary

5) Bonus

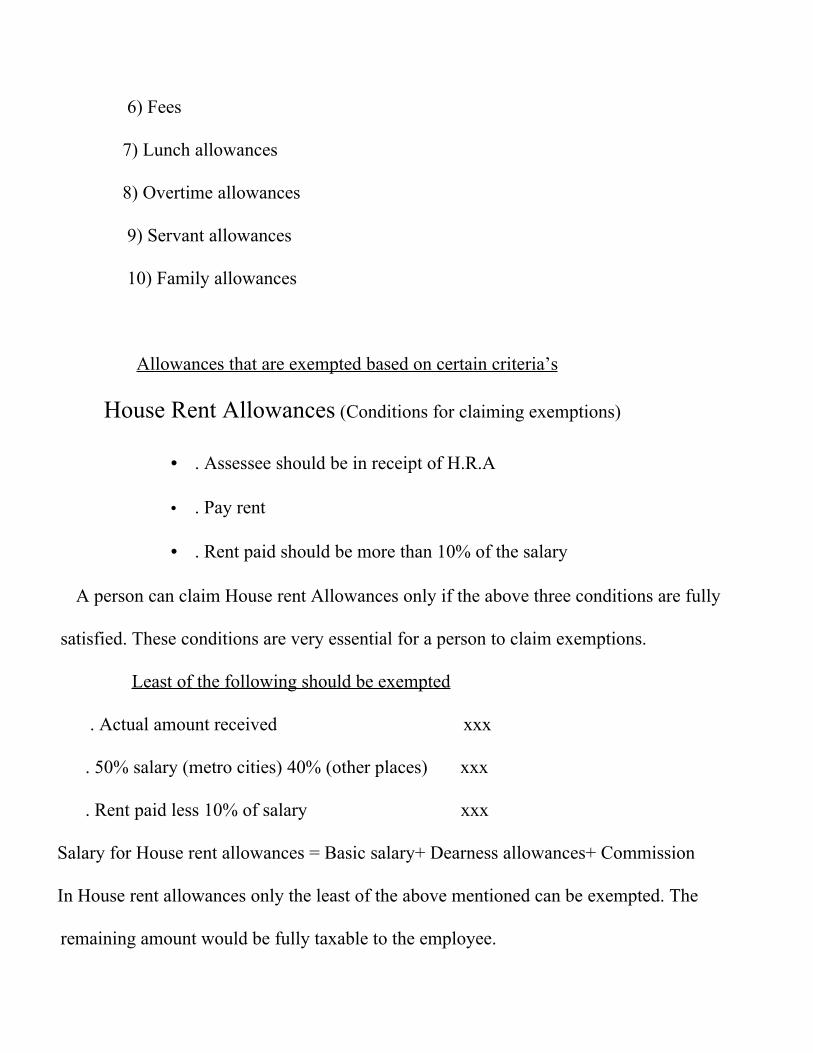

6) Fees

7) Lunch allowances

8) Overtime allowances

9) Servant allowances

10) Family allowances

Allowances that are exempted based on certain criteria’s

House Rent Allowances (Conditions for claiming exemptions)

• . Assessee should be in receipt of H.R.A

• . Pay rent

• . Rent paid should be more than 10% of the salary

A person can claim House rent Allowances only if the above three conditions are fully

satisfied. These conditions are very essential for a person to claim exemptions.

Least of the following should be exempted

. Actual amount received xxx

. 50% salary (metro cities) 40% (other places) xxx

. Rent paid less 10% of salary xxx

Salary for House rent allowances = Basic salary+ Dearness allowances+ Commission

In House rent allowances only the least of the above mentioned can be exempted. The

remaining amount would be fully taxable to the employee.

Leave Travel Assistance (LTA)

Any individual can avail the benefit of leave travel assistance offered by his employer twice

in a block of four years. Leave Travel Assistance is provided by the employer to employee

and his entire family. Leave travel assistance is provided for following reasons

• . In connection with his proceeding on leave to any place in India, while in service

• . Proceed to any place in India after retirement or termination from service.

Leave Travel Assistance is taxable only if it is

1) Encashed without performing journey is fully taxable

2) Expenses reimbursed other than fare like boarding or Lodging is fully taxable

3) Amount received from employer in excess of cost of traveling on the shortest route

In Leave Travel Assistance only boarding or lodging fare is reimbursed. The remaining

amount is fully taxable. Traveling expenses is not taxable but any amount in excess of

traveling through the shortest route is fully taxable under Leave Travel Assistance. In short

only boarding, lodging, and traveling expenses are not taxable under Leave Travel

Assistance. The remaining amount is fully taxable. Leave travel Assistance cannot be

claimed every year. It can be claimed only twice in a block of four years, Example between

1998 and 2002 Leave travel assistance can be claimed only two times. If an employee

Encashes money and does not commence journey the entire amount of money claimed is

fully taxable.

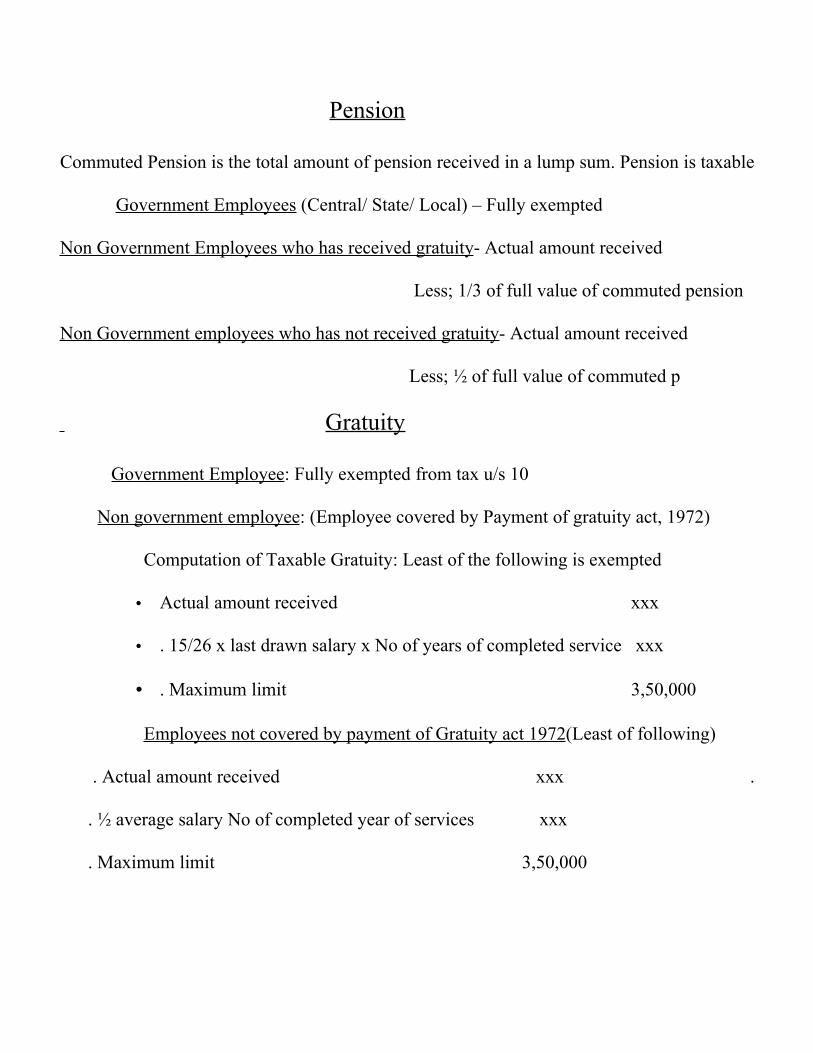

Pension

Commuted Pension is the total amount of pension received in a lump sum. Pension is taxable

Government Employees (Central/ State/ Local) – Fully exempted

Non Government Employees who has received gratuity- Actual amount received

Less; 1/3 of full value of commuted pension

Non Government employees who has not received gratuity- Actual amount received

Less; ½ of full value of commuted p

Gratuity

Government Employee: Fully exempted from tax u/s 10

Non government employee: (Employee covered by Payment of gratuity act, 1972)

Computation of Taxable Gratuity: Least of the following is exempted

• Actual amount received xxx

• . 15/26 x last drawn salary x No of years of completed service xxx

• . Maximum limit 3,50,000

Employees not covered by payment of Gratuity act 1972(Least of following)

. Actual amount received xxx .

. ½ average salary No of completed year of services xxx

. Maximum limit 3,50,000

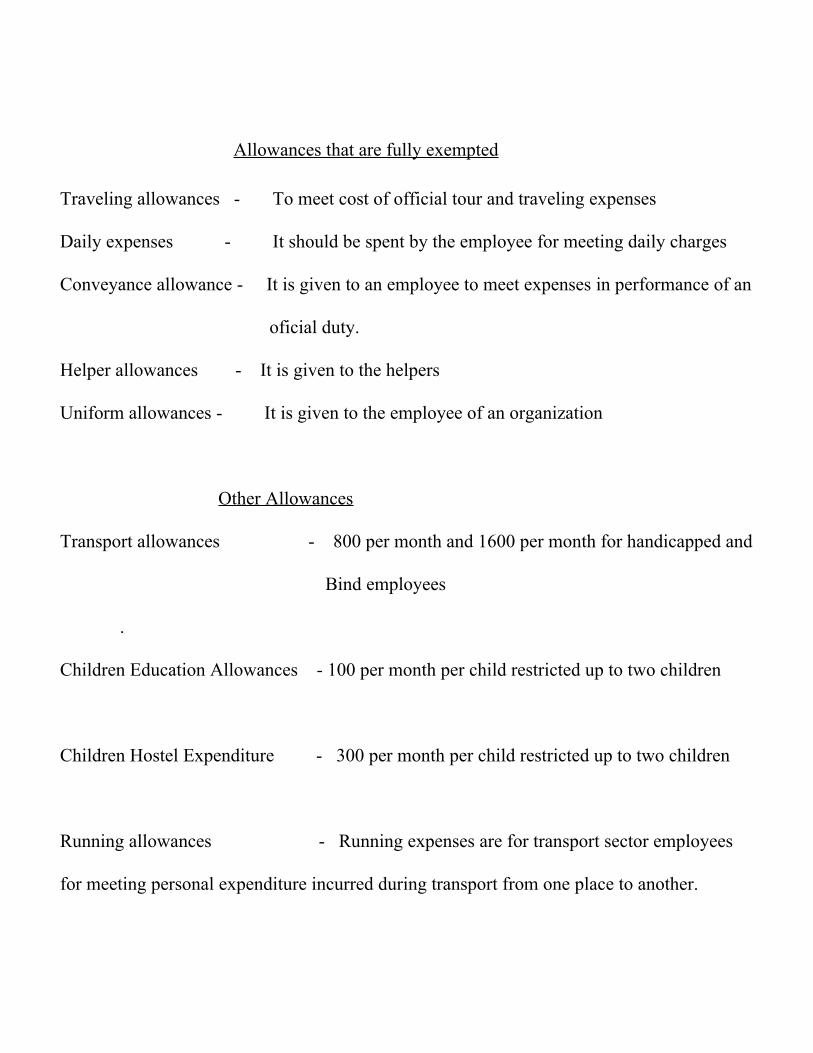

Allowances that are fully exempted

Traveling allowances - To meet cost of official tour and traveling expenses

Daily expenses - It should be spent by the employee for meeting daily charges

Conveyance allowance - It is given to an employee to meet expenses in performance of an

oficial duty.

Helper allowances - It is given to the helpers

Uniform allowances - It is given to the employee of an organization

Other Allowances

Transport allowances - 800 per month and 1600 per month for handicapped and

Bind employees

.

Children Education Allowances - 100 per month per child restricted up to two children

Children Hostel Expenditure - 300 per month per child restricted up to two children

Running allowances - Running expenses are for transport sector employees

for meeting personal expenditure incurred during transport from one place to another.

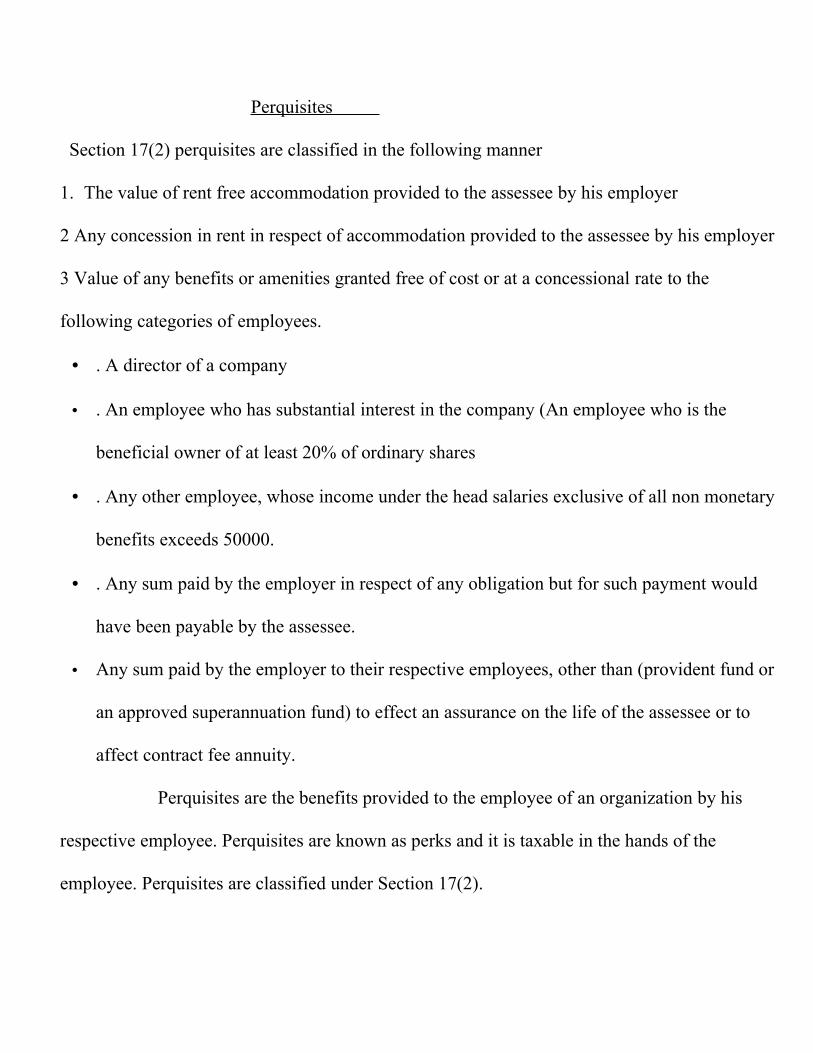

Perquisites

Section 17(2) perquisites are classified in the following manner

1. The value of rent free accommodation provided to the assessee by his employer

2 Any concession in rent in respect of accommodation provided to the assessee by his employer

3 Value of any benefits or amenities granted free of cost or at a concessional rate to the

following categories of employees.

• . A director of a company

• . An employee who has substantial interest in the company (An employee who is the

beneficial owner of at least 20% of ordinary shares

• . Any other employee, whose income under the head salaries exclusive of all non monetary

benefits exceeds 50000.

• . Any sum paid by the employer in respect of any obligation but for such payment would

have been payable by the assessee.

• Any sum paid by the employer to their respective employees, other than (provident fund or

an approved superannuation fund) to effect an assurance on the life of the assessee or to

affect contract fee annuity.

Perquisites are the benefits provided to the employee of an organization by his

respective employee. Perquisites are known as perks and it is taxable in the hands of the

employee. Perquisites are classified under Section 17(2).

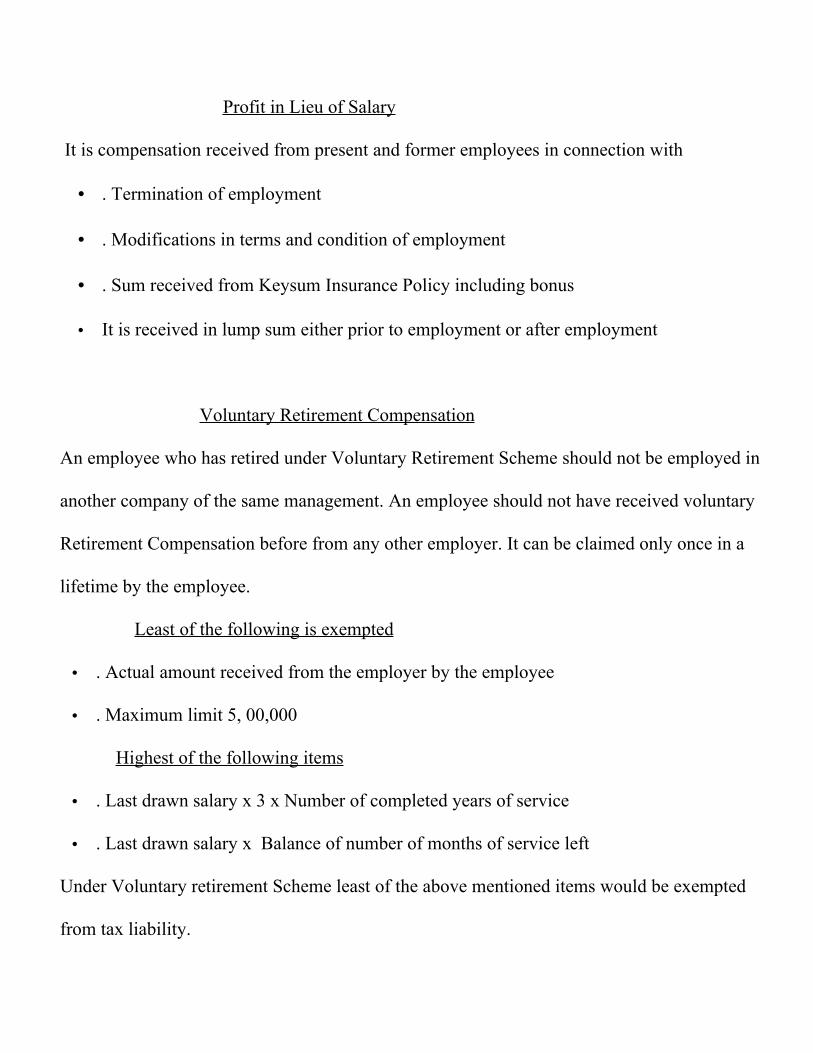

Profit in Lieu of Salary

It is compensation received from present and former employees in connection with

• . Termination of employment

• . Modifications in terms and condition of employment

• . Sum received from Keysum Insurance Policy including bonus

• It is received in lump sum either prior to employment or after employment

Voluntary Retirement Compensation

An employee who has retired under Voluntary Retirement Scheme should not be employed in

another company of the same management. An employee should not have received voluntary

Retirement Compensation before from any other employer. It can be claimed only once in a

lifetime by the employee.

Least of the following is exempted

• . Actual amount received from the employer by the employee

• . Maximum limit 5, 00,000

Highest of the following items

• . Last drawn salary x 3 x Number of completed years of service

• . Last drawn salary x Balance of number of months of service left

Under Voluntary retirement Scheme least of the above mentioned items would be exempted

from tax liability.

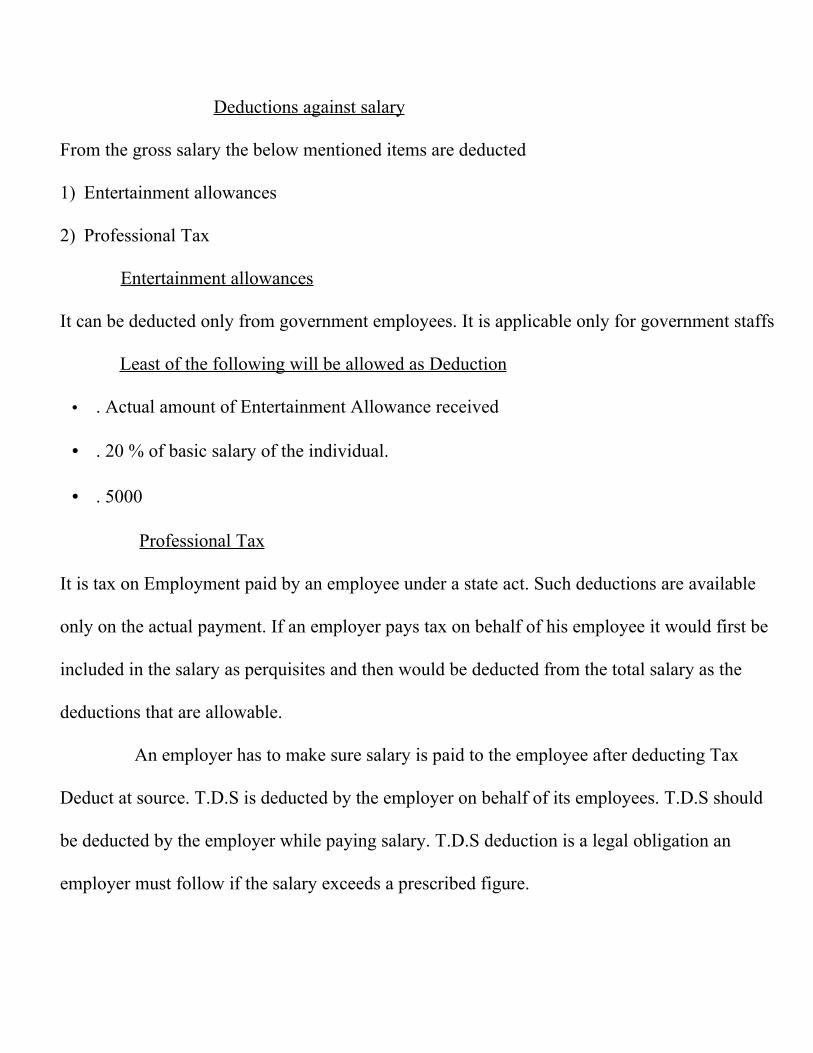

Deductions against salary

From the gross salary the below mentioned items are deducted

1) Entertainment allowances

2) Professional Tax

Entertainment allowances

It can be deducted only from government employees. It is applicable only for government staffs

Least of the following will be allowed as Deduction

• . Actual amount of Entertainment Allowance received

• . 20 % of basic salary of the individual.

• . 5000

Professional Tax

It is tax on Employment paid by an employee under a state act. Such deductions are available

only on the actual payment. If an employer pays tax on behalf of his employee it would first be

included in the salary as perquisites and then would be deducted from the total salary as the

deductions that are allowable.

An employer has to make sure salary is paid to the employee after deducting Tax

Deduct at source. T.D.S is deducted by the employer on behalf of its employees. T.D.S should

be deducted by the employer while paying salary. T.D.S deduction is a legal obligation an

employer must follow if the salary exceeds a prescribed figure.

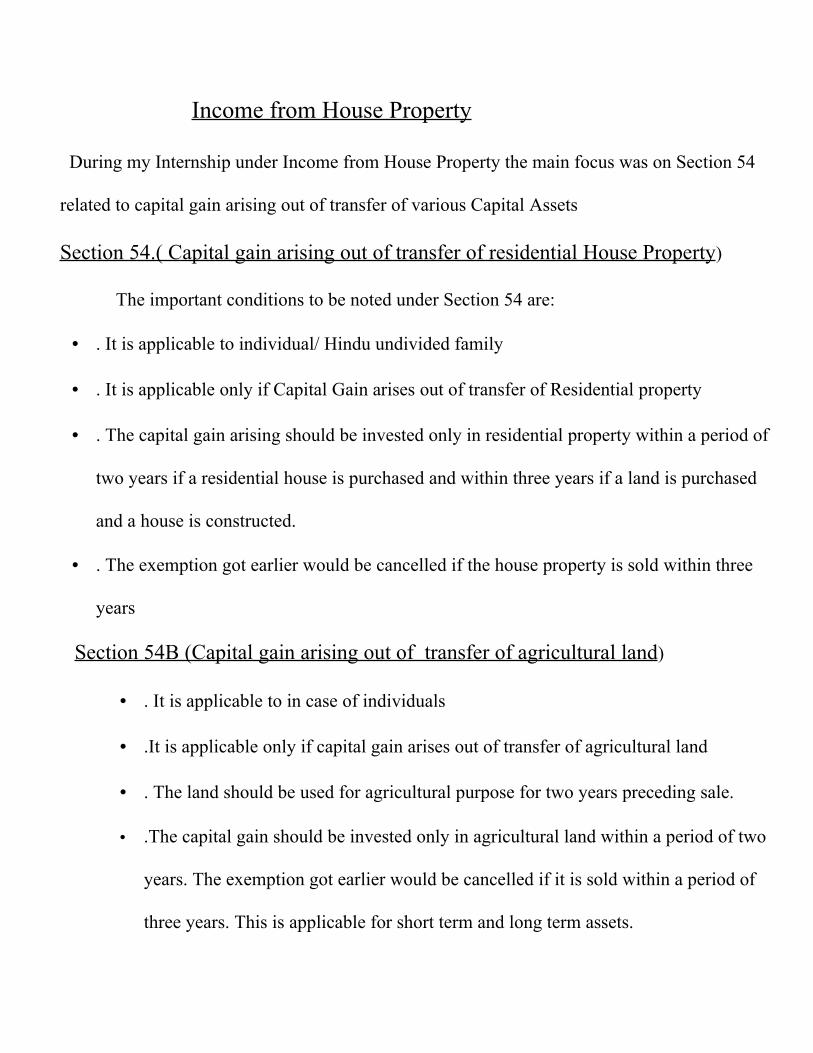

Income from House Property

During my Internship under Income from House Property the main focus was on Section 54

related to capital gain arising out of transfer of various Capital Assets

Section 54.( Capital gain arising out of transfer of residential House Property)

The important conditions to be noted under Section 54 are:

• . It is applicable to individual/ Hindu undivided family

• . It is applicable only if Capital Gain arises out of transfer of Residential property

• . The capital gain arising should be invested only in residential property within a period of

two years if a residential house is purchased and within three years if a land is purchased

and a house is constructed.

• . The exemption got earlier would be cancelled if the house property is sold within three

years

Section 54B (Capital gain arising out of transfer of agricultural land)

• . It is applicable to in case of individuals

• .It is applicable only if capital gain arises out of transfer of agricultural land

• . The land should be used for agricultural purpose for two years preceding sale.

• .The capital gain should be invested only in agricultural land within a period of two

years. The exemption got earlier would be cancelled if it is sold within a period of

three years. This is applicable for short term and long term assets.

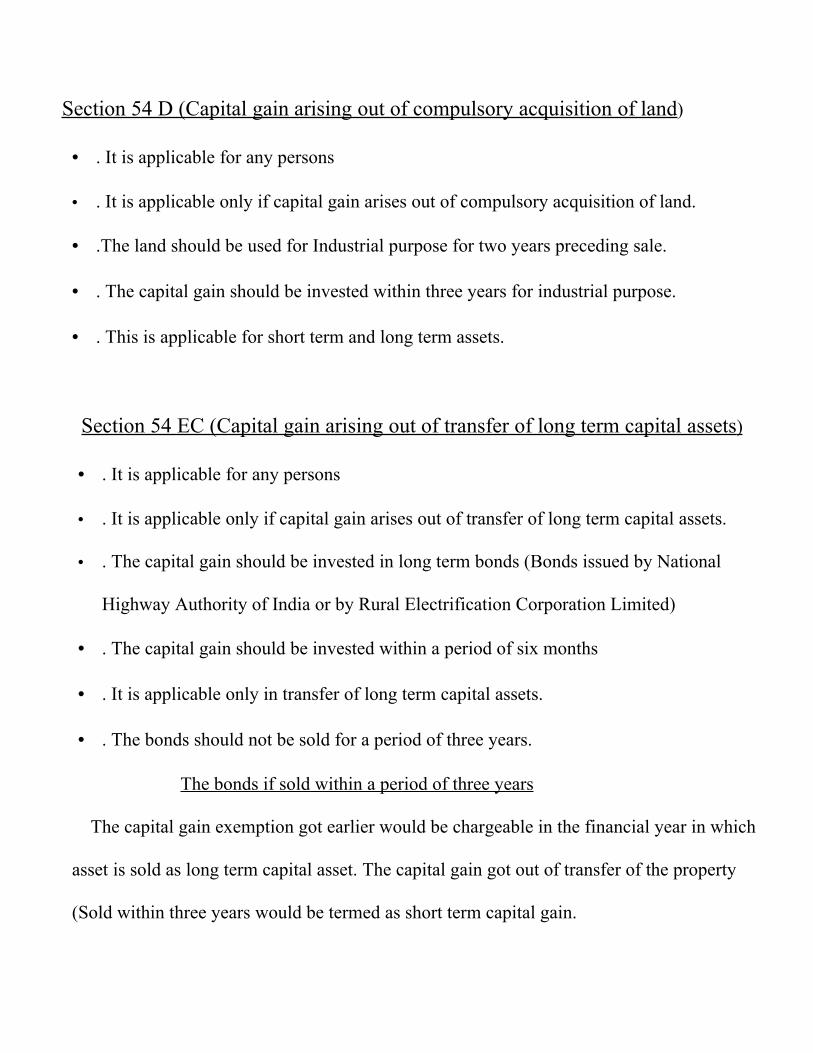

Section 54 D (Capital gain arising out of compulsory acquisition of land)

• . It is applicable for any persons

• . It is applicable only if capital gain arises out of compulsory acquisition of land.

• .The land should be used for Industrial purpose for two years preceding sale.

• . The capital gain should be invested within three years for industrial purpose.

• . This is applicable for short term and long term assets.

Section 54 EC (Capital gain arising out of transfer of long term capital assets )

• . It is applicable for any persons

• . It is applicable only if capital gain arises out of transfer of long term capital assets.

• . The capital gain should be invested in long term bonds (Bonds issued by National

Highway Authority of India or by Rural Electrification Corporation Limited)

• . The capital gain should be invested within a period of six months

• . It is applicable only in transfer of long term capital assets.

• . The bonds should not be sold for a period of three years.

The bonds if sold within a period of three years

The capital gain exemption got earlier would be chargeable in the financial year in which

asset is sold as long term capital asset. The capital gain got out of transfer of the property

(Sold within three years would be termed as short term capital gain.

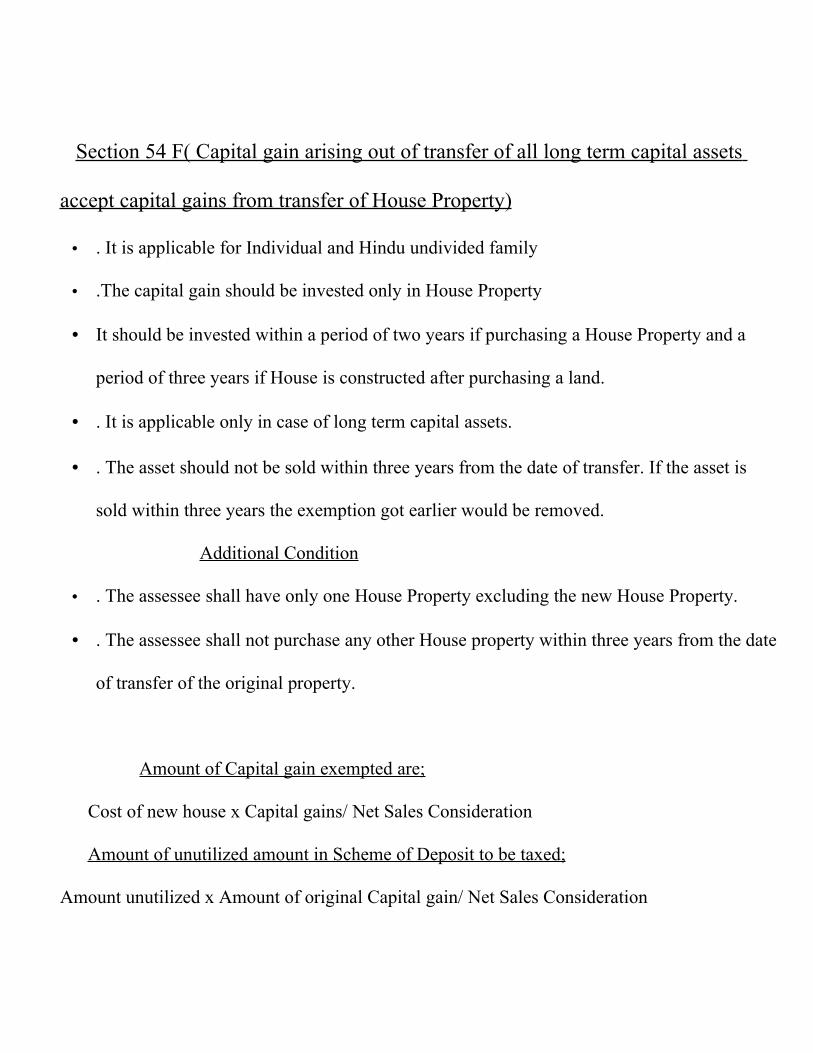

Section 54 F( Capital gain arising out of transfer of all long term capital assets

accept capital gains from transfer of House Property)

• . It is applicable for Individual and Hindu undivided family

• .The capital gain should be invested only in House Property

• It should be invested within a period of two years if purchasing a House Property and a

period of three years if House is constructed after purchasing a land.

• . It is applicable only in case of long term capital assets.

• . The asset should not be sold within three years from the date of transfer. If the asset is

sold within three years the exemption got earlier would be removed.

Additional Condition

• . The assessee shall have only one House Property excluding the new House Property.

• . The assessee shall not purchase any other House property within three years from the date

of transfer of the original property.

Amount of Capital gain exempted are;

Cost of new house x Capital gains/ Net Sales Consideration

Amount of unutilized amount in Scheme of Deposit to be taxed;

Amount unutilized x Amount of original Capital gain/ Net Sales Consideration

Income from other sources

The following items are covered under Income from other sources.

• . Winnings from lottery, crosswords puzzles

• . Income from ground rent

• . Income from royalties

• . Interest on bank deposits

• .Income from ground rent.

• . Income from interest on securities

Interest on securities would be assessed under this head only if they are not chargeable under

the head Profits and gains of the business.

Deductions under Income from other sources

The followings items can be deducted from Income from other sources

• . In respect of income in the nature of family pension a deduction of 33% of such income

• . Any other expenditure (not being in the nature of capital expenditure) laid out or

expended wholly for the purpose of making such Incomes.

• . Deprecation in respect of: buildings, machinery plant and furniture’s

• . Premium paid in respect of Insurance against risk of damage or destruction.

• . Amount paid on account of current repairs to premises, machinery, plant and furniture’s.

• . Benefits of: unabsorbed deprecations.

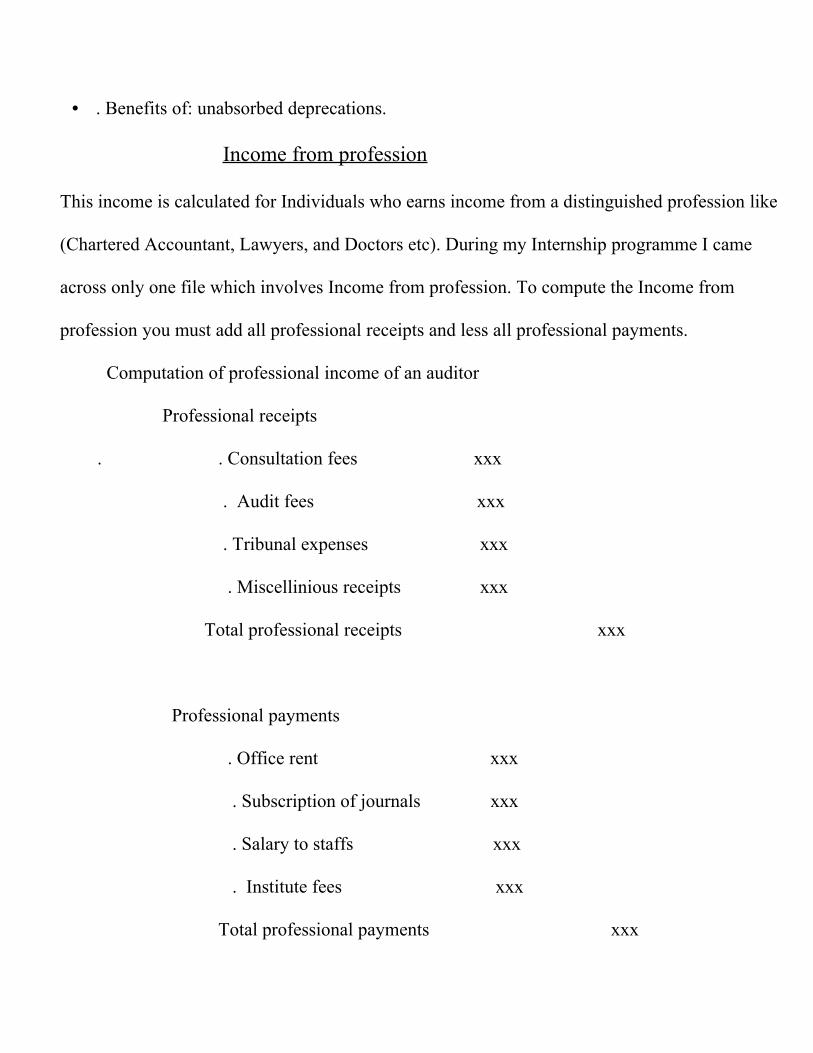

Income from profession

This income is calculated for Individuals who earns income from a distinguished profession like

(Chartered Accountant, Lawyers, and Doctors etc). During my Internship programme I came

across only one file which involves Income from profession. To compute the Income from

profession you must add all professional receipts and less all professional payments.

Computation of professional income of an auditor

Professional receipts

. . Consultation fees xxx

. Audit fees xxx

. Tribunal expenses xxx

. Miscellinious receipts xxx

Total professional receipts xxx

Professional payments

. Office rent xxx

. Subscription of journals xxx

. Salary to staffs xxx

. Institute fees xxx

Total professional payments xxx

Professional Income = Total Professional Receipts – Total Professional payments

Income from Business

During my Internship programme I noted that the auditing firm I worked in maintains a Profit

and loss account and a capital account. When asked on it they told me they prepare two separate

accounts to compute Income from business. Initially, I was confused with the capital account

because in college we never prepared a separate account for capital. The more I worked out

problems the more I came to learn about Income from Business. This is one incidence where I

realized theoretical study is completely different from real life practical application.

Computation of Income from Business

Net profit from the profit and loss account xxx

Add: Disallowable expenses (Examples of Disallowable expenses)

Capital expenses xxx

Reserves and provisions xxx

Less: Disallowable Income (Example of Disallowable Incomes)

Post office saving interest xxx

Bad debts recovered xxx

In my Internship training programme I was told to deduct items like Interest received,

commission received, and rent received from Net profit because they would be included under

Income from other sources. The other think which took my attention was adding and

subtracting deprecation to this they told me that, you add deprecation amount in the books of

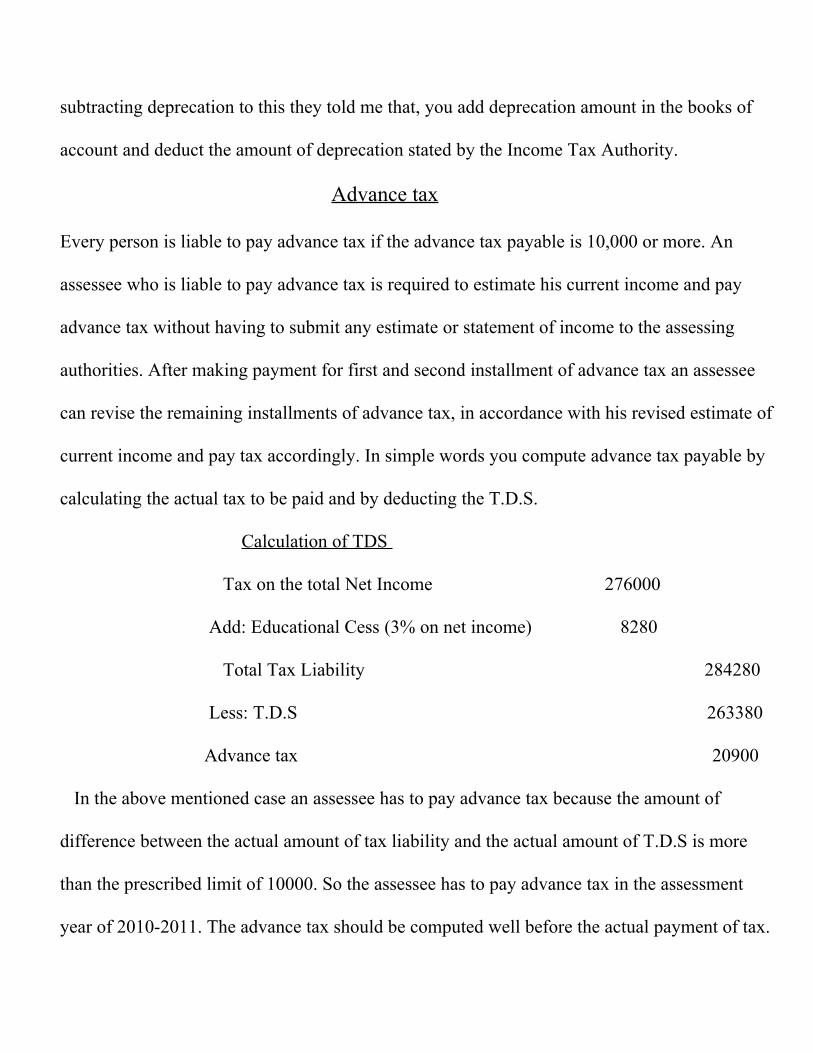

account and deduct the amount of deprecation stated by the Income Tax Authority.

Advance tax

Every person is liable to pay advance tax if the advance tax payable is 10,000 or more. An

assessee who is liable to pay advance tax is required to estimate his current income and pay

advance tax without having to submit any estimate or statement of income to the assessing

authorities. After making payment for first and second installment of advance tax an assessee

can revise the remaining installments of advance tax, in accordance with his revised estimate of

current income and pay tax accordingly. In simple words you compute advance tax payable by

calculating the actual tax to be paid and by deducting the T.D.S.

Calculation of TDS

Tax on the total Net Income 276000

Add: Educational Cess (3% on net income) 8280

Total Tax Liability 284280

Less: T.D.S 263380

Advance tax 20900

In the above mentioned case an assessee has to pay advance tax because the amount of

difference between the actual amount of tax liability and the actual amount of T.D.S is more

than the prescribed limit of 10000. So the assessee has to pay advance tax in the assessment

year of 2010-2011. The advance tax should be computed well before the actual payment of tax.

If the advance tax forecasted by the assessee is lesser than the actual amount of advance tax

payable then an assessee must pay penalty to the concerned Authority

Advance Tax Payment (Dates to be filed)

In case of corporate assessee

Due Date Tax to be paid

On or before June 15 15% of advance tax is payable

On or before September 15 30% of advance tax is payable

On or before December 15 30% of advance tax is payable

On or before March 15 25% of advance tax is payable

In case of non corporate assessee

On or before September 15 30% advance tax is payable

On or before December 15 30% advance tax is payable

On or before March 15 40% advance tax is payable

Any payment of advance tax which is made before March 31st is treated as advance tax that is

paid during the financial year. When the advance tax is payable by the virtue of notice of

demand issued by the assessing officer the whole amount or the appropriate part of advance tax

should be payable in the remaining installments. The assessing officer shall fine an interest on

the amount due or on the entire amount of advance tax assessed. Section 208 and 210 deals with

non payment of the advance tax. Advance tax payment is a must for all the assessee if the

difference between tax paid and TDS is more than the prescribed limit of 10000 or more. An

assessee is required to estimate his current income before computing advance tax.

Tax Deduct at Source (TDS)

Tax deduction at source is a must and it must be paid by the persons concerned within the given

period of time. When a person does not deduct tax at source or after deducting fails to pay

whole or any part of tax as required by the act, then such person would be liable for payment of

tax with interest and penalty. TDS is deducted in the following cases.

TDS in case of salary

• . It is paid by the employer of an organization

• . It is deducted from employee’s salary.

In case of salary TDS is deducted by the employer on behalf of its employees.

TDS in case of interest on securities

• . It is paid by any person issuing the securities

• . It should be deducted from any person receiving interest on securities.

TDS should be deducted only if a person receives interest of more than 10000 from securities.

Winnings from Horse race

• . It is paid by the company giving the winning sum.

• . It is deducted from any person.

• . Rate of 30%

TDS should be deducted only if a person receives more than 2500 from Horse race.

Rent received

. It is paid by any persons except Individual and Hindu undivided family.

. It is deducted from any person.

TDS should be deducted only if a person receives rent of 120000 or more.

Insurance Commission

. It is paid by any person who is giving the Insurance commission

. It can be deducted from any resident persons

TDS should be deducted only if a person receives Insurance Commission of 5000 or more

Interest other than interest on securities

. It is paid by any person other than individuals and HUF.

. It can be deducted from any resident in India

TDS should be deducted only if a person receives interest on securities exceeding 5000

in a year or 10000 in case of banking company or co-operative society, deposits with post

office. These are certain cases where TDS should be deducted by the respective persons. TDS

deducted should be deposited to the respective Authorities within the prescribed time. TDS is

deducted only if the amount received exceeds a certain limit. It is a must to deduct TDS if they

are not deducted properly a fine is levied on the person who is responsible for deductions.

Computation of Income of Companies

Companies earn Income from three main sources of Income

• . Income from business

• Income from House Property

• . Income from Capital gains

For Companies the main source of Income would be from Income from Business. The Income

from Business starts with the Net profit. During my Internship training I came across items

which should be added and deducted from the Net profits. Items like rent received should be

deducted from the Net profits

Computation of Incomes of Firms

During my Internship training I noted that the auditor computed Income of the firm and the

partners together in one statement. I realized that’s a practice followed in almost all auditors

firm if both the firm and the partner are clients of the same auditor. The firm earns income from

• . Income from House Property

• . Income from Capital gains

• . Income from Business and Profession

For the firm though they receive Incomes from the other heads of Income, the main source of

Income would be Income from Business and profession.

CHAPTER 5: Conclusions

During Internship training my main focus was on to cover the topics as mentioned below.

• . Assessment of Individuals, Firms and Companies

• . Filing of returns and Forms of Returns

• . Payment of Advance Tax and TDS

It was not easy to cover the above mentioned Topics within the allotted time of 30 days. I tried

my level best to cover the above mentioned topics within the given time. It was a wonderful

experience working in an auditing firm. It gave me a real feel of the corporate world. It put be

into a group which was filled with real life performers, so I had to put in that extra bit of effort

to work with them. I was very lucky to work in such a reputed firm which had very rich

experience in the field of auditing. The most important think I learned during my training

session was that there is a glaring difference between what I learned and what I practiced.

This training period made me matured as an Individual and as a team member in the

organization. The real challenge for me was to adapt to the corporate environment. Initially, I

founded it very difficult to cope with it, but as the days went by I grew in confidence and was

ready to face new challenges thrown at me. The work environment was simply superb and it

gave me a chance to acquire new skills. I was also able to observe the manner in which each

client was treated in the organization. This programme has done a world of good to my

confidence and it has given me a wonderful experience of working in a top auditing firm.

Chapter 6: Feedback

The Internship programme was of great help to me as it gave me the much needed exposure to

face the challenges thrown in by the corporate world. I was not able to look into the topic given

in detail, because of the lack in duration in the training programme. I personally would like the

Internship training to be extended by a month. It gave me the much needed exposure to the

practical aspect of Income Tax. I was also able to pick up new traits from my auditor in relation

to handling of clients and building a good customer relationship.

It would be great, if we had a chance to do our Internship programme after studying

the theoretical aspect of Income Tax in full. I spent a majority of time in understanding the

concepts like TDS, Advance tax and computation of Incomes from different heads of Incomes.

The auditor told me I could work on various files only if I know such basic concepts. It took me

nearly two weeks to study these concepts, as a result of which time I did not have enough time

to practice all the above mentioned concepts. It would have been really good if our Internship

programme is extended by a month. Internship programme has a whole was excellent and I

really enjoyed this beautiful experience, which helped me a lot to develop personally and also to

live up to the expectations of my auditor. The stand out thing of this entire programme was it

gave all of us the much needed exposure and also a lot of scope to expand and develop our

skills, which would be very essential for us to face new challenges thrown at us. This training

programme was a real blessing to us. I would like to thank my College, teachers and the auditor

for their whole hearted support.

Income from House Property

. The auditor computes the gross annual value with the details given by the clients. From the

gross annual value municipal tax is been deducted and that would give you the Net annual

income of the House property. From the Net Annual value of the House property you deduct

30% as standard deductions. The next deduction available from the Net Annual income is

deduction on the Interest on loan borrowed and pre-construction interest..

An Illustration to explain Income from House Property (In case of let out House)

Gross Annual Income xxx

Less: Municipal tax paid xxx

Net Annual Income xxx

Less: Standard deductions xxx

Less; Interest on loan borrowed xxx

Less: Pre-construction interest xxx xxx

Total Income from House Property xxx

This is applicable only in case of House that are deemed to be let out. Gross annual value of

House that is self used is taken to be nil. Interest on loan borrowed and pre-construction interest

claimed should not be more than 30000. It can be raised provided three conditions are satisfied.

. Loan must be taken on or before 1.4.19

. Loan should be taken only for construction or for acquisition

. It must be repaid within three years from the end of financial year in which loan is taken.

Chapter 1.1: Introduction

Loyola College was established and owned by the Loyola College society. It was founded by

Rev.Fr. Francis Bertram and a band of dedicated Jesuits, who came to Chennai. The foundation

stone was laid on March 10th 1924 and the college started functioning in July of the following

year (1925) with seventy-five students on roll in undergraduate courses of Mathematics, History

and Economics. Loyola College is ranked as the Number one College in India by the top

magazines. Many eminent personalities of India have graduated from Loyola College and it is

surely any students dream and, I personally am very lucky to be a part of Loyola. The Internship

programme was mainly included in the curriculum to help the students understand the practical

application of Income tax in detail and also to give the students the much needed exposure.

During our Internship training our main focus was on

. Assessment of Income for Individuals

. Assessment of Income for Firms and Companies

. Tax Deduction at Source

. Advance tax payment

The other main purpose of this programme was to help the students understand the glaring

difference between theoretical study and practical application of various Income tax concepts.

Internship programme was very successful in fulfilling the objectives they were formed for. It

was a wonderful learning experience for me personally, as I was able to learn a lot of new

concepts in Income Tax which would be very useful for me.

Chapter 1.2: Profile of the Organization

The firm Kushal Raj and Co was formed in the year 1975 with a minimal number of two

employees. The firm at present has over thirty-five employees with a very rich experience in the

field of auditing for over thirty-five years. The firm’s office is situated in Sowcarpet; Chennai

opposite to Indian Overseas Branch (Parry’s branch). The firm deals with clients, who are from

various diversified Portfolio like

• . Manufacturing

• . Trading

• . Banking and Finance

• . Software

• . Publishing and Distribution

• . Hospitals

• . Advertising

• . Entertainment

The firm has grown in size on the audit and tax foundation, it is fairly very large in size and

very diverse. It provides internal audit service to a selected few companies and also offers

Project Management services to companies setting up Greenfield projects. The firm at present

has over hundred clients, which is been growing steadily every year. The firm is one of the

leading auditing firms in Chennai and has about five Interns who contribute immensely to the

growth of the firm.

Chapter 2: Profile of the work guide

Mr. Kushalraj:

He is a fellow member of the Institute of Chartered Accountancy and was also the youth wing

member of the forum for many years. He graduated from college in the year 1968 and also has

rich experience in the field of law. The firm was started by him in the year 1975. He holds an

F.C.A degree and has a very rich experience in the field of auditing for over thirty-five years.

His area of interest is

• . Project management

• . Tax advisory service

• . Compliance and Exchange control

• . Development system design

Mr. Anand Nahar:

He graduated from college in the year 1985. He joined the firm in the year 1993 and has a very

rich experience in the field of auditing for over twenty years. He holds an F.C.A degree and is

also a fellow member of the Institute of Chartered Accountancy. His area of Interest is

• . Project consultancy

• . Business planning

• . Development system Design

• . Tax advisory service

Chapter 4: Forms used in Income Tax procedure

Chapter: 1

1.1: Introduction

1.2: Profile of the firm

.

Chapter 2: Profile of the work guide

.

.

Chapter 3; Learning and Experience

Chapter 5: Conclusions

.

.

Chapter 6: Feedback

.

.

Related Documents