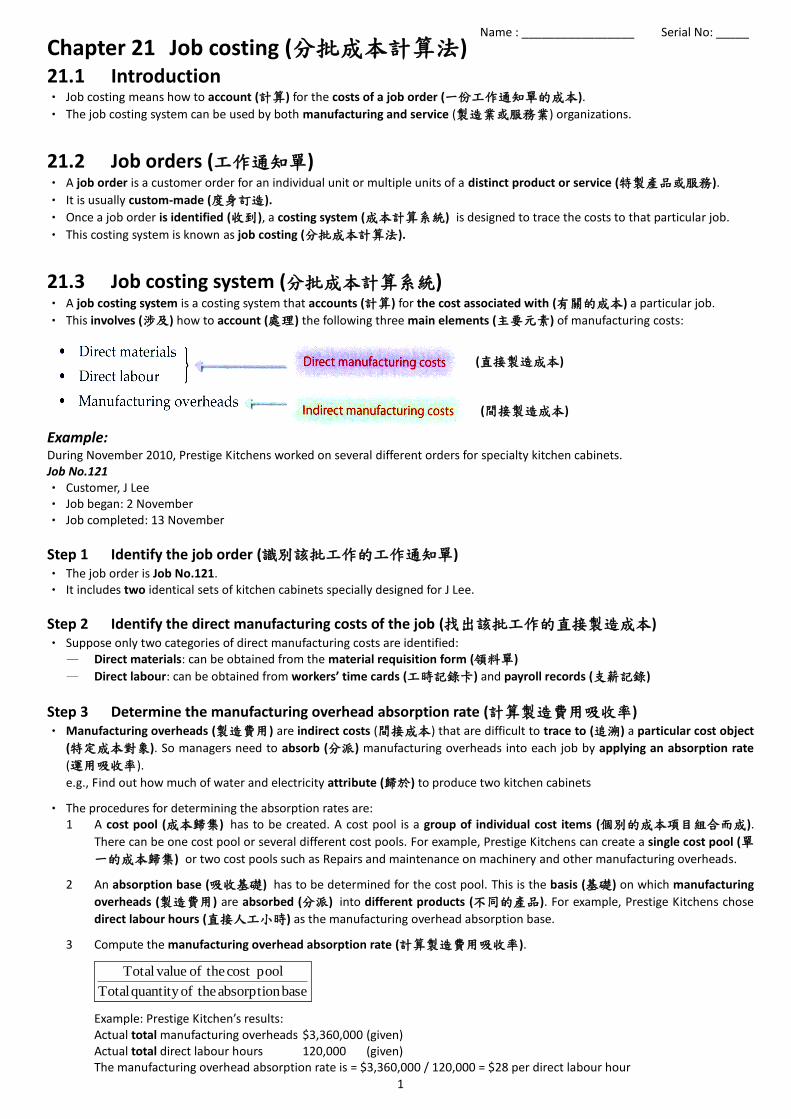

1 Chapter 21 Job costing (分批成本計算法) 21.1 Introduction • Job costing means how to account (計算) for the costs of a job order (一份工作通知單的成本). • The job costing system can be used by both manufacturing and service (製造業或服務業) organizations. 21.2 Job orders (工作通知單) • A job order is a customer order for an individual unit or multiple units of a distinct product or service (特製產品或服務). • It is usually custom-made (度身訂造). • Once a job order is identified (收到), a costing system (成本計算系統) is designed to trace the costs to that particular job. • This costing system is known as job costing (分批成本計算法). 21.3 Job costing system (分批成本計算系統) • A job costing system is a costing system that accounts (計算) for the cost associated with (有關的成本) a particular job. • This involves (涉及) how to account (處理) the following three main elements (主要元素) of manufacturing costs: Example: During November 2010, Prestige Kitchens worked on several different orders for specialty kitchen cabinets. Job No.121 • Customer, J Lee • Job began: 2 November • Job completed: 13 November Step 1 Identify the job order (識別該批工作的工作通知單) • The job order is Job No.121. • It includes two identical sets of kitchen cabinets specially designed for J Lee. Step 2 Identify the direct manufacturing costs of the job (找出該批工作的直接製造成本) • Suppose only two categories of direct manufacturing costs are identified: — Direct materials: can be obtained from the material requisition form (領料單) — Direct labour: can be obtained from workers’ time cards (工時記錄卡) and payroll records (支薪記錄) Step 3 Determine the manufacturing overhead absorption rate (計算製造費用吸收率) • Manufacturing overheads (製造費用) are indirect costs (間接成本) that are difficult to trace to (追溯) a particular cost object (特定成本對象). So managers need to absorb (分派) manufacturing overheads into each job by applying an absorption rate (運用吸收率). e.g., Find out how much of water and electricity attribute (歸於) to produce two kitchen cabinets • The procedures for determining the absorption rates are: 1 A cost pool (成本歸集) has to be created. A cost pool is a group of individual cost items (個別的成本項目組合而成). There can be one cost pool or several different cost pools. For example, Prestige Kitchens can create a single cost pool (單 一的成本歸集) or two cost pools such as Repairs and maintenance on machinery and other manufacturing overheads. 2 An absorption base (吸收基礎) has to be determined for the cost pool. This is the basis (基礎) on which manufacturing overheads (製造費用) are absorbed (分派) into different products (不同的產品). For example, Prestige Kitchens chose direct labour hours (直接人工小時) as the manufacturing overhead absorption base. 3 Compute the manufacturing overhead absorption rate (計算製造費用吸收率). base absorption the of quantity Total pool cost the of value Total Example: Prestige Kitchen’s results: Actual total manufacturing overheads $3,360,000 (given) Actual total direct labour hours 120,000 (given) The manufacturing overhead absorption rate is = $3,360,000 / 120,000 = $28 per direct labour hour Name : _________________ Serial No: _____ (直接製造成本) (間接製造成本)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Chapter 21 Job costing (分批成本計算法) 21.1 Introduction • Job costing means how to account (計算) for the costs of a job order (一份工作通知單的成本).

• The job costing system can be used by both manufacturing and service (製造業或服務業) organizations.

21.2 Job orders (工作通知單) • A job order is a customer order for an individual unit or multiple units of a distinct product or service (特製產品或服務).

• It is usually custom-made (度身訂造).

• Once a job order is identified (收到), a costing system (成本計算系統) is designed to trace the costs to that particular job.

• This costing system is known as job costing (分批成本計算法).

21.3 Job costing system (分批成本計算系統) • A job costing system is a costing system that accounts (計算) for the cost associated with (有關的成本) a particular job.

• This involves (涉及) how to account (處理) the following three main elements (主要元素) of manufacturing costs:

Example: During November 2010, Prestige Kitchens worked on several different orders for specialty kitchen cabinets. Job No.121 • Customer, J Lee • Job began: 2 November • Job completed: 13 November

Step 1 Identify the job order (識別該批工作的工作通知單) • The job order is Job No.121. • It includes two identical sets of kitchen cabinets specially designed for J Lee.

Step 2 Identify the direct manufacturing costs of the job (找出該批工作的直接製造成本) • Suppose only two categories of direct manufacturing costs are identified:

— Direct materials: can be obtained from the material requisition form (領料單)

— Direct labour: can be obtained from workers’ time cards (工時記錄卡) and payroll records (支薪記錄)

Step 3 Determine the manufacturing overhead absorption rate (計算製造費用吸收率) • Manufacturing overheads (製造費用) are indirect costs (間接成本) that are difficult to trace to (追溯) a particular cost object

(特定成本對象). So managers need to absorb (分派) manufacturing overheads into each job by applying an absorption rate

(運用吸收率).

e.g., Find out how much of water and electricity attribute (歸於) to produce two kitchen cabinets

• The procedures for determining the absorption rates are: 1 A cost pool (成本歸集) has to be created. A cost pool is a group of individual cost items (個別的成本項目組合而成).

There can be one cost pool or several different cost pools. For example, Prestige Kitchens can create a single cost pool (單

一的成本歸集) or two cost pools such as Repairs and maintenance on machinery and other manufacturing overheads. 2 An absorption base (吸收基礎) has to be determined for the cost pool. This is the basis (基礎) on which manufacturing

overheads (製造費用) are absorbed (分派) into different products (不同的產品). For example, Prestige Kitchens chose

direct labour hours (直接人工小時) as the manufacturing overhead absorption base. 3 Compute the manufacturing overhead absorption rate (計算製造費用吸收率).

base absorption theofquantity Total

poolcost theof valueTotal

Example: Prestige Kitchen’s results: Actual total manufacturing overheads $3,360,000 (given) Actual total direct labour hours 120,000 (given)

The manufacturing overhead absorption rate is = $3,360,000 / 120,000 = $28 per direct labour hour

Name : _________________ Serial No: _____

(直接製造成本)

(間接製造成本)

2

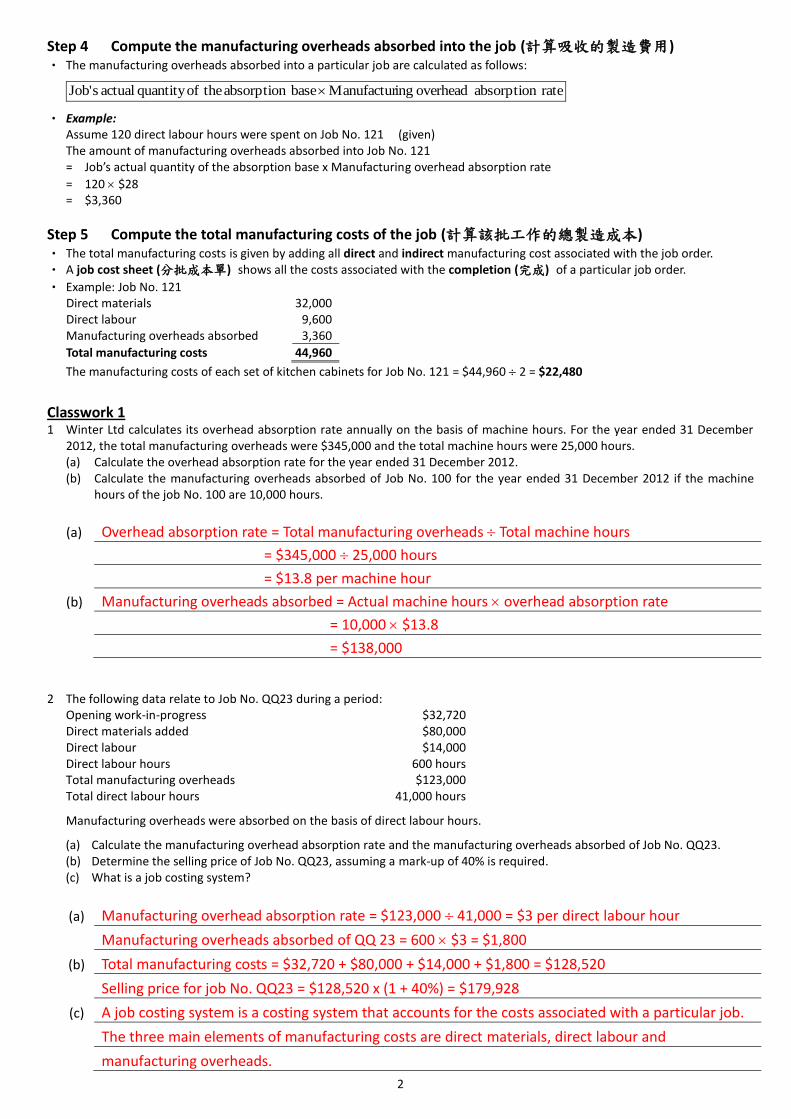

Step 4 Compute the manufacturing overheads absorbed into the job (計算吸收的製造費用) • The manufacturing overheads absorbed into a particular job are calculated as follows:

rate absorption overhead ingManufacturbase absorption theofquantity actual sJob'

• Example:

Assume 120 direct labour hours were spent on Job No. 121 (given) The amount of manufacturing overheads absorbed into Job No. 121 = Job’s actual quantity of the absorption base x Manufacturing overhead absorption rate

= 120 $28 = $3,360

Step 5 Compute the total manufacturing costs of the job (計算該批工作的總製造成本) • The total manufacturing costs is given by adding all direct and indirect manufacturing cost associated with the job order. • A job cost sheet (分批成本單) shows all the costs associated with the completion (完成) of a particular job order.

• Example: Job No. 121 Direct materials 32,000 Direct labour 9,600 Manufacturing overheads absorbed 3,360

Total manufacturing costs 44,960

The manufacturing costs of each set of kitchen cabinets for Job No. 121 = $44,960 2 = $22,480

Classwork 1 1 Winter Ltd calculates its overhead absorption rate annually on the basis of machine hours. For the year ended 31 December

2012, the total manufacturing overheads were $345,000 and the total machine hours were 25,000 hours. (a) Calculate the overhead absorption rate for the year ended 31 December 2012. (b) Calculate the manufacturing overheads absorbed of Job No. 100 for the year ended 31 December 2012 if the machine

hours of the job No. 100 are 10,000 hours.

(a) Overhead absorption rate = Total manufacturing overheads Total machine hours

= $345,000 25,000 hours

= $13.8 per machine hour

(b) Manufacturing overheads absorbed = Actual machine hours overhead absorption rate

= 10,000 $13.8

= $138,000 2 The following data relate to Job No. QQ23 during a period:

Opening work-in-progress $32,720 Direct materials added $80,000 Direct labour $14,000 Direct labour hours 600 hours Total manufacturing overheads $123,000 Total direct labour hours 41,000 hours

Manufacturing overheads were absorbed on the basis of direct labour hours.

(a) Calculate the manufacturing overhead absorption rate and the manufacturing overheads absorbed of Job No. QQ23. (b) Determine the selling price of Job No. QQ23, assuming a mark-up of 40% is required. (c) What is a job costing system?

(a) Manufacturing overhead absorption rate = $123,000 41,000 = $3 per direct labour hour

Manufacturing overheads absorbed of QQ 23 = 600 $3 = $1,800

(b) Total manufacturing costs = $32,720 + $80,000 + $14,000 + $1,800 = $128,520

Selling price for job No. QQ23 = $128,520 x (1 + 40%) = $179,928

(c) A job costing system is a costing system that accounts for the costs associated with a particular job.

The three main elements of manufacturing costs are direct materials, direct labour and

manufacturing overheads.

3

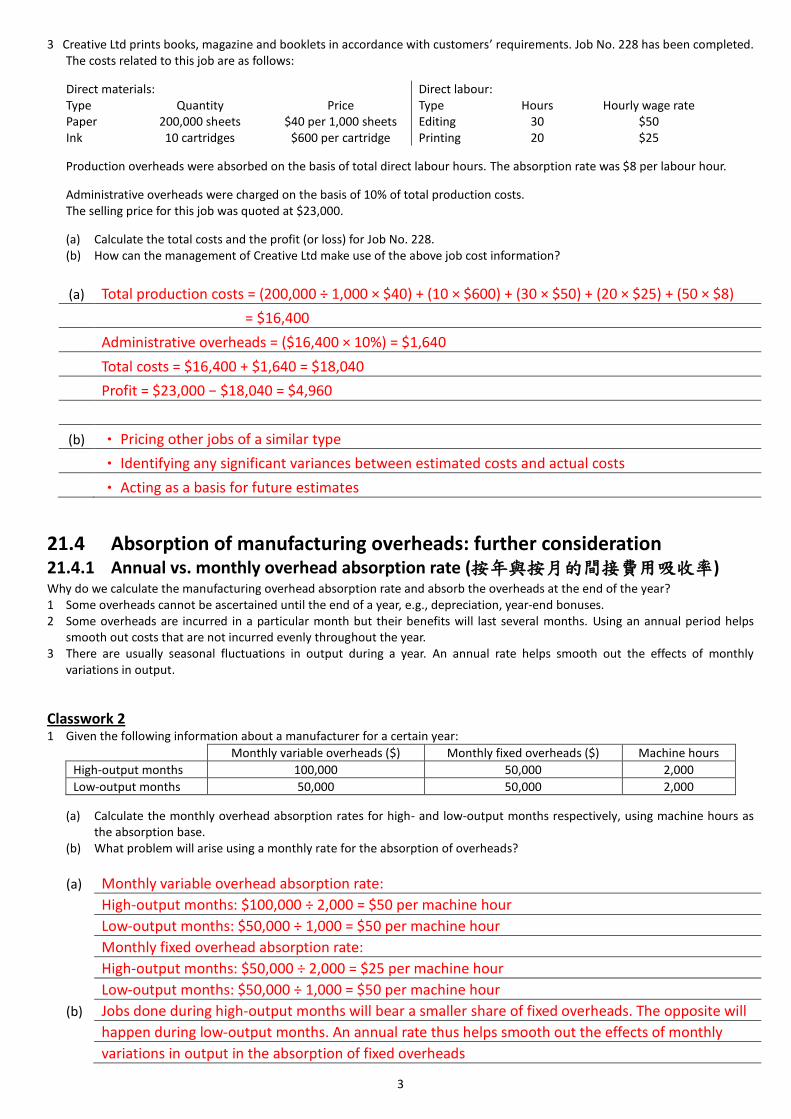

3 Creative Ltd prints books, magazine and booklets in accordance with customers’ requirements. Job No. 228 has been completed. The costs related to this job are as follows: Direct materials: Direct labour: Type Quantity Price Type Hours Hourly wage rate Paper 200,000 sheets $40 per 1,000 sheets Editing 30 $50 Ink 10 cartridges $600 per cartridge Printing 20 $25

Production overheads were absorbed on the basis of total direct labour hours. The absorption rate was $8 per labour hour.

Administrative overheads were charged on the basis of 10% of total production costs. The selling price for this job was quoted at $23,000.

(a) Calculate the total costs and the profit (or loss) for Job No. 228. (b) How can the management of Creative Ltd make use of the above job cost information?

(a) Total production costs = (200,000 ÷ 1,000 × $40) + (10 × $600) + (30 × $50) + (20 × $25) + (50 × $8)

= $16,400

Administrative overheads = ($16,400 × 10%) = $1,640

Total costs = $16,400 + $1,640 = $18,040

Profit = $23,000 − $18,040 = $4,960

(b) • Pricing other jobs of a similar type

• Identifying any significant variances between estimated costs and actual costs

• Acting as a basis for future estimates

21.4 Absorption of manufacturing overheads: further consideration 21.4.1 Annual vs. monthly overhead absorption rate (按年與按月的間接費用吸收率) Why do we calculate the manufacturing overhead absorption rate and absorb the overheads at the end of the year? 1 Some overheads cannot be ascertained until the end of a year, e.g., depreciation, year-end bonuses. 2 Some overheads are incurred in a particular month but their benefits will last several months. Using an annual period helps

smooth out costs that are not incurred evenly throughout the year. 3 There are usually seasonal fluctuations in output during a year. An annual rate helps smooth out the effects of monthly

variations in output.

Classwork 2 1 Given the following information about a manufacturer for a certain year:

Monthly variable overheads ($) Monthly fixed overheads ($) Machine hours

High-output months 100,000 50,000 2,000

Low-output months 50,000 50,000 2,000

(a) Calculate the monthly overhead absorption rates for high- and low-output months respectively, using machine hours as the absorption base.

(b) What problem will arise using a monthly rate for the absorption of overheads?

(a) Monthly variable overhead absorption rate:

High-output months: $100,000 ÷ 2,000 = $50 per machine hour

Low-output months: $50,000 ÷ 1,000 = $50 per machine hour

Monthly fixed overhead absorption rate:

High-output months: $50,000 ÷ 2,000 = $25 per machine hour

Low-output months: $50,000 ÷ 1,000 = $50 per machine hour

(b) Jobs done during high-output months will bear a smaller share of fixed overheads. The opposite will

happen during low-output months. An annual rate thus helps smooth out the effects of monthly

variations in output in the absorption of fixed overheads

4

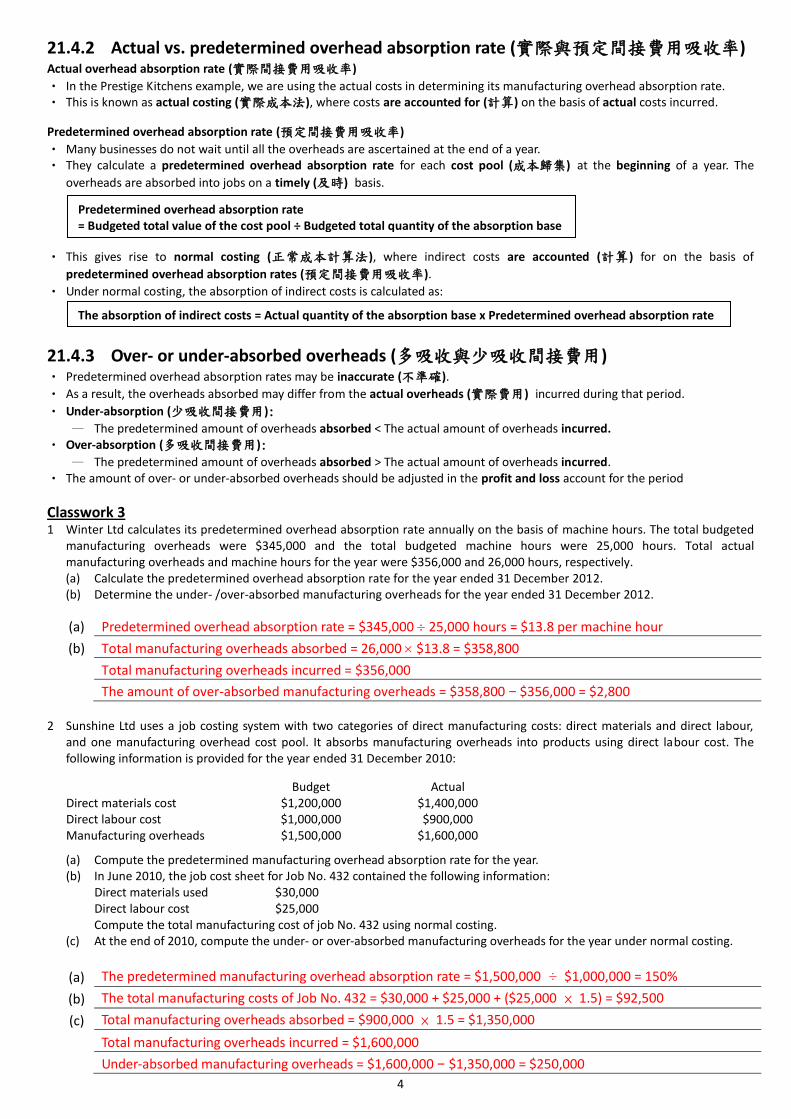

21.4.2 Actual vs. predetermined overhead absorption rate (實際與預定間接費用吸收率) Actual overhead absorption rate (實際間接費用吸收率)

• In the Prestige Kitchens example, we are using the actual costs in determining its manufacturing overhead absorption rate. • This is known as actual costing (實際成本法), where costs are accounted for (計算) on the basis of actual costs incurred. Predetermined overhead absorption rate (預定間接費用吸收率)

• Many businesses do not wait until all the overheads are ascertained at the end of a year. • They calculate a predetermined overhead absorption rate for each cost pool (成本歸集) at the beginning of a year. The

overheads are absorbed into jobs on a timely (及時) basis.

• This gives rise to normal costing (正常成本計算法), where indirect costs are accounted (計算) for on the basis of

predetermined overhead absorption rates (預定間接費用吸收率).

• Under normal costing, the absorption of indirect costs is calculated as:

21.4.3 Over- or under-absorbed overheads (多吸收與少吸收間接費用) • Predetermined overhead absorption rates may be inaccurate (不準確).

• As a result, the overheads absorbed may differ from the actual overheads (實際費用) incurred during that period.

• Under-absorption (少吸收間接費用):

— The predetermined amount of overheads absorbed < The actual amount of overheads incurred. • Over-absorption (多吸收間接費用):

— The predetermined amount of overheads absorbed > The actual amount of overheads incurred. • The amount of over- or under-absorbed overheads should be adjusted in the profit and loss account for the period

Classwork 3 1 Winter Ltd calculates its predetermined overhead absorption rate annually on the basis of machine hours. The total budgeted

manufacturing overheads were $345,000 and the total budgeted machine hours were 25,000 hours. Total actual manufacturing overheads and machine hours for the year were $356,000 and 26,000 hours, respectively. (a) Calculate the predetermined overhead absorption rate for the year ended 31 December 2012. (b) Determine the under- /over-absorbed manufacturing overheads for the year ended 31 December 2012.

(a) Predetermined overhead absorption rate = $345,000 25,000 hours = $13.8 per machine hour

(b) Total manufacturing overheads absorbed = 26,000 $13.8 = $358,800

Total manufacturing overheads incurred = $356,000

The amount of over-absorbed manufacturing overheads = $358,800 − $356,000 = $2,800 2 Sunshine Ltd uses a job costing system with two categories of direct manufacturing costs: direct materials and direct labour,

and one manufacturing overhead cost pool. It absorbs manufacturing overheads into products using direct labour cost. The following information is provided for the year ended 31 December 2010: Budget Actual Direct materials cost $1,200,000 $1,400,000 Direct labour cost $1,000,000 $900,000 Manufacturing overheads $1,500,000 $1,600,000

(a) Compute the predetermined manufacturing overhead absorption rate for the year. (b) In June 2010, the job cost sheet for Job No. 432 contained the following information:

Direct materials used $30,000 Direct labour cost $25,000

Compute the total manufacturing cost of job No. 432 using normal costing. (c) At the end of 2010, compute the under- or over-absorbed manufacturing overheads for the year under normal costing.

(a) The predetermined manufacturing overhead absorption rate = $1,500,000 ÷ $1,000,000 = 150%

(b) The total manufacturing costs of Job No. 432 = $30,000 + $25,000 + ($25,000 × 1.5) = $92,500

(c) Total manufacturing overheads absorbed = $900,000 × 1.5 = $1,350,000

Total manufacturing overheads incurred = $1,600,000

Under-absorbed manufacturing overheads = $1,600,000 − $1,350,000 = $250,000

Predetermined overhead absorption rate = Budgeted total value of the cost pool ÷ Budgeted total quantity of the absorption base

The absorption of indirect costs = Actual quantity of the absorption base x Predetermined overhead absorption rate

5

21.4.4 Single vs. multiple overhead absorption rates (單一與多個間接費用吸收率) Single absorption rates (單一費用吸收率)

• We used a single rate (blanket rate or plant-wide rate) (單一,全廠吸收率) in the example of Prestige Kitchens.

Multiple overhead absorption rates (多個間接費用吸收率)

• Some businesses use multiple overhead absorption rates by creating various cost pools (建立多個成本歸集) and selecting (選

取) their appropriate absorption bases (合適的吸收基礎) or cost driver (成本動因).

• This helps generate (有助獲取) more accurate (準確) costing information.

• However, the greater the number of cost pools and overhead absorption rates, the more time and resources will be required to build up (建立) the cost pools and work out (計算) the absorption rates. Example: Suppose Prestige Kitchens has created two cost pools for manufacturing overheads:

Cost pool Cost driver 1. Repairs and maintenance on machinery Machine hours 2. Other manufacturing overheads Direct labour hours

Given the following information budgeted at 1 Jan 2010:

Repairs and maintenance on machinery $1,400,000 Other manufacturing overheads $1,600,000 Direct labour hours 100,000 Machine hours 20,000

The predetermined overhead absorption rates are:

Cost pool Predetermined overhead absorption rate

1. Repairs and maintenance on machinery $1,400,000 ÷ 20,000 = $70 per machine hour

2. Other manufacturing overheads $1,600,000 ÷ 100,000 = $16 per direct labour hour

Assume 100 machine hours and 120 direct labour hours were incurred on Job No. 121, this job would absorb the following manufacturing overheads:

Repairs and maintenance on machinery (100 $70) $7,000

Other manufacturing overheads (120 $16) $1,920

Total manufacturing overheads $8,920

Classwork 4 1 Data of a firm for the past period are as follows:

Total machine hours 8,000 Number of material requisitions 350 Number of purchase orders 200 Number of production runs 200

Production overheads: $ Cost drivers:

Short run variable costs 560,000 Machine hours Production scheduling costs 600,000 Production runs Stores receiving costs 50,000 Purchase orders executed Materials handling costs 70,000 Requisitions raised

(a) Calculate the cost driver rate for each of the four production overheads activities. (b) Assume 6,000 machine hours, 50 production runs, 100 purchase orders and 200 material requisitions were incurred on

product P1, calculate the production overheads for P1.

(a) Cost driver rates:

Short run variable costs per machine hour ($560,000 ÷ 8,000) = $70 per machine hour

Production scheduling costs per production run ($600,000 ÷ 200) = $3,000 per production runs

Stores receiving costs per purchase order ($50,000 ÷ 200) = $250 per purchase orders

Materials handling costs per requisition ($70,000 ÷ 350) = $200 per material requisitions

(b) The production overheads absorbed for P1

= 6,000 x $70 + 50 x $3,000 + 100 x $250 + 200 x $200

= $635,000

6

21.5 More than one production department (多於一個生產部門) If the job order involves (涉及) several production departments, a separate manufacturing overhead absorption rate (個別製造

費用吸收率) has to be created (建立) for each production department (每個生產部門). This requires the apportionment of

manufacturing overheads (分派製造費用) between the various production departments (不同的生產部門). After apportioning

the overheads among departments, we can find the total manufacturing overhead absorbed by the job. Process of finding the total manufacturing overhead absorbed by the job: 1 The apportionment of overheads among departments (把費用攤派到不同部門)

If there is more than one manufacturing overhead, we need to apportion (攤派) the overheads between the production

departments before calculating the overhead absorption rate (費用吸收率) for each production department.

(a) An appropriate basis of apportionment has to be selected for each type of overhead (為每種類型製造費用選取一個合

適的費用攤派基礎). The basis of apportionment (攤派基礎) must be a strong cost driver (合適成本動因) of the

overhead. For example, Manufacturing overheads: Basis of apportionment Factory rent Factory area occupied Repairs and maintenance on machinery Machine value

(b) Find out the total manufacturing overheads for each production department according to the basis of apportionment.

2 Calculate the predetermined overhead absorption rate among departments (計算不同部門預定間接費用吸收率) 3 Calculate the total manufacturing overhead to be absorbed by the job (計算工作總製造成本) Example 1 One manufacturing overhead for two or more production department (一個製造費用於多個生產部門) J Hui operates a plant producing custom-made shoes. There are two manufacturing departments: cutting and assembly. The budgeted manufacturing overheads and levels of activity for the year ended 31 December 2010 were as follows:

Cutting department Assembly department Manufacturing overheads $250,000 $320,000 Machine hours 1,000,000 200,000 Direct labour hours 160,000 800,000 Job No. 334 was completed during the year. It consumed 5,000 and 850 machine hours in the cutting and assembly departments, respectively, and 760 and 3,600 direct labour hours in the cutting and assembly departments, respectively. (a) Absorb the manufacturing overheads into Job No. 334, using a plant-wide (全廠) predetermined overhead absorption rate

based on direct labour hours. (b) Absorb the manufacturing overheads into Job No. 334, using departmental (部門) predetermined overhead absorption rates

for each manufacturing department. The absorption base for cutting and assembly department is machine hours and direct labour hours respectively.

(c) During 2010, the record for Job No. 334 showed the following information: Cutting Assembly department department

Direct materials consumed $18,000 $1,200 Direct manufacturing labour costs $2,000 $800

Calculate the total manufacturing cost of Job No. 334.

Answer:

(a) Plant-wide predetermined overhead absorption rate

= ($250,000 + $320,000) ÷ (160,000 + 800,000) = $0.59375 per direct labour hour

Manufacturing overheads absorbed into Job No. 334 = $0.59375 × (760 + 3,600) = $2,588.75

(b) Departmental predetermined overhead absorption rate for the cutting department

= $250,000 ÷ 1,000,000 = $0.25 per machine hour

Departmental predetermined overhead absorption rate for the assembly department

= $320,000 ÷ 800,000 = $0.4 per direct labour hour

Manufacturing overheads absorbed into Job No. 334 = (5,000 × $0.25) + (3,600 × $0.4) = $2,690

(c) Total manufacturing costs of Job No. 334 = ($18,000 + $2,000) + ($1,200 + $800) + $2,690 = $24,690

7

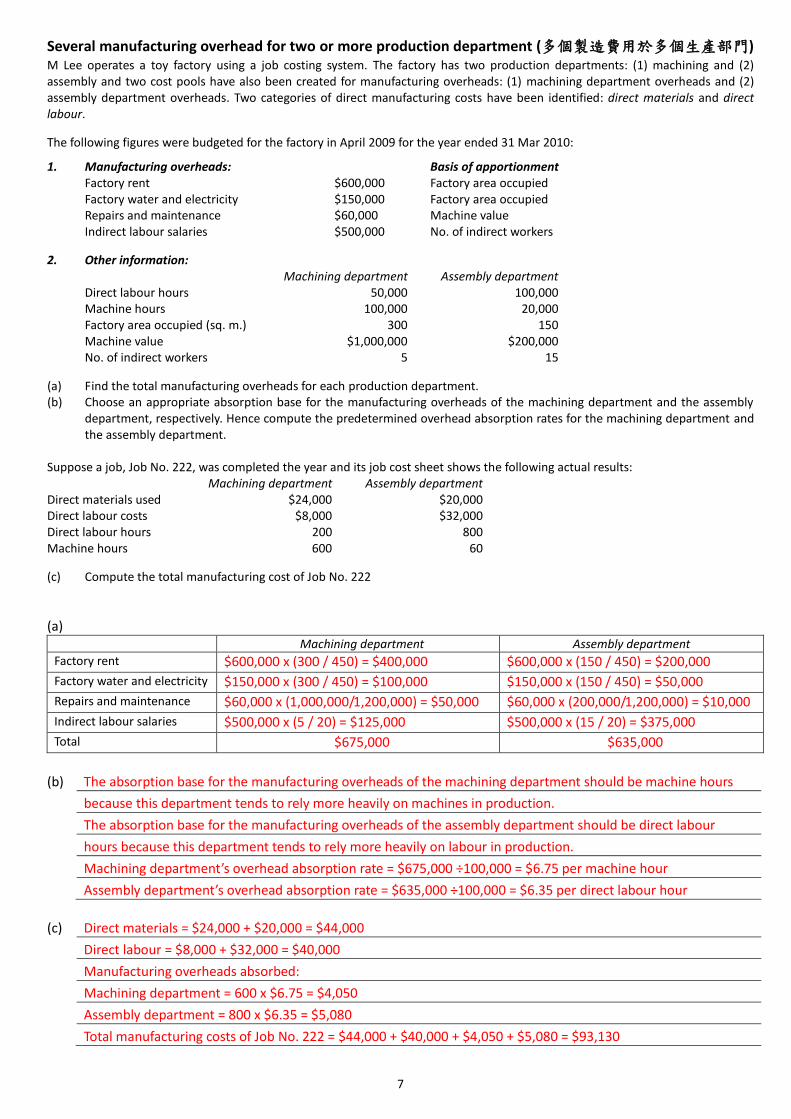

Several manufacturing overhead for two or more production department (多個製造費用於多個生產部門) M Lee operates a toy factory using a job costing system. The factory has two production departments: (1) machining and (2) assembly and two cost pools have also been created for manufacturing overheads: (1) machining department overheads and (2) assembly department overheads. Two categories of direct manufacturing costs have been identified: direct materials and direct labour. The following figures were budgeted for the factory in April 2009 for the year ended 31 Mar 2010:

1. Manufacturing overheads: Basis of apportionment Factory rent $600,000 Factory area occupied Factory water and electricity $150,000 Factory area occupied Repairs and maintenance $60,000 Machine value Indirect labour salaries $500,000 No. of indirect workers 2. Other information:

Machining department Assembly department Direct labour hours 50,000 100,000 Machine hours 100,000 20,000 Factory area occupied (sq. m.) 300 150 Machine value $1,000,000 $200,000 No. of indirect workers 5 15

(a) Find the total manufacturing overheads for each production department. (b) Choose an appropriate absorption base for the manufacturing overheads of the machining department and the assembly

department, respectively. Hence compute the predetermined overhead absorption rates for the machining department and the assembly department.

Suppose a job, Job No. 222, was completed the year and its job cost sheet shows the following actual results:

Machining department Assembly department Direct materials used $24,000 $20,000 Direct labour costs $8,000 $32,000 Direct labour hours 200 800 Machine hours 600 60 (c) Compute the total manufacturing cost of Job No. 222

(a) Machining department Assembly department

Factory rent $600,000 x (300 / 450) = $400,000 $600,000 x (150 / 450) = $200,000

Factory water and electricity $150,000 x (300 / 450) = $100,000 $150,000 x (150 / 450) = $50,000

Repairs and maintenance $60,000 x (1,000,000/1,200,000) = $50,000 $60,000 x (200,000/1,200,000) = $10,000

Indirect labour salaries $500,000 x (5 / 20) = $125,000 $500,000 x (15 / 20) = $375,000

Total $675,000 $635,000

(b) The absorption base for the manufacturing overheads of the machining department should be machine hours

because this department tends to rely more heavily on machines in production.

The absorption base for the manufacturing overheads of the assembly department should be direct labour

hours because this department tends to rely more heavily on labour in production.

Machining department’s overhead absorption rate = $675,000 ÷100,000 = $6.75 per machine hour

Assembly department’s overhead absorption rate = $635,000 ÷100,000 = $6.35 per direct labour hour

(c) Direct materials = $24,000 + $20,000 = $44,000

Direct labour = $8,000 + $32,000 = $40,000

Manufacturing overheads absorbed:

Machining department = 600 x $6.75 = $4,050

Assembly department = 800 x $6.35 = $5,080

Total manufacturing costs of Job No. 222 = $44,000 + $40,000 + $4,050 + $5,080 = $93,130

8

Classwork 5 1 Pitt Smith Ltd uses a job costing system in its plant in Tai Po. The company has two production departments: the wiring

department and the polishing department. The company has selected machine hours as the absorption base for the wiring department and direct manufacturing labour costs as the absorption base for the polishing department.

The 2005 budget for the Tai Po plant was as follows:

Wiring Polishing department department

Manufacturing overheads $13,000,000 $10,600,000 Direct manufacturing labour costs $2,080,000 $5,800,000 Direct manufacturing labour hours 42,000 hrs 210,000 hrs Machine hours 340,000 hrs 42,500 hrs

The actual figures at the end of 2005 were as follows:

Wiring Polishing department department

Manufacturing overheads $13,400,000 $10,800,000 Direct manufacturing labour costs $2,400,000 $5,950,000 Machine hours 365,000 hrs 40,500 hrs

(a) Calculate the predetermined overhead recovery rates for the two departments for 2005. (b) Calculate the under-or over-absorbed manufacturing overhead for each department. (c) During 2005, the record card for Job T44 showed the following information:

Wiring Polishing department department

Direct materials consumed $124,300 $15,800 Direct manufacturing labour costs $60,000 $4,600 Direct manufacturing labour hours 3,200 hrs 150 hrs Machine hours 250 hrs 40 hrs

Given the information in other parts of this question, calculate the total manufacturing overhead to be absorbed by Job T44.

(d) Given the information in other parts of this question, calculate the total production cost and unit product cost of Job T44 if there were 500 units of output produced under the job.

(a) Predetermined overhead recovery rates for Wiring department:

= $13,000,000 ÷ 340,000 = $38.24 per machine hour

Predetermined overhead recovery rates for Polishing department:

= $10,600,000 ÷ $5,800,000 = 182.76%

(b) Manufacturing overhead incurred for Wiring department = $13,400,000

Manufacturing overhead absorbed for Wiring department = 365,000 x $38.24 = $13,957,600

Over-absorption for Wiring department = $13,957,600 − $13,400,000 = $557,600

Manufacturing overhead incurred for Polishing department = $10,800,000

Manufacturing overhead absorbed for Polishing department = $5,950,000 x 182.76% = $10,874,220

Over-absorption for Polishing department = $10,874,220 − $10,800,000 = $74,220

(c) Manufacturing overhead absorbed for Wiring department = 250 x $38.24 = $9,560.00

Manufacturing overhead absorbed for Polishing department = $4,600 x 182.76% = $8,406.96

Total manufacturing overhead absorbed by Job T44 = $9,560.00 + $8,406.96 = 17,966.96

(d) Total job cost = ($124,300 + $15,800) + ($60,000 + $4,600) + 17,966.96 = $222,666.96

Unit product cost = $222,666.96 ÷500 = $445.33

9

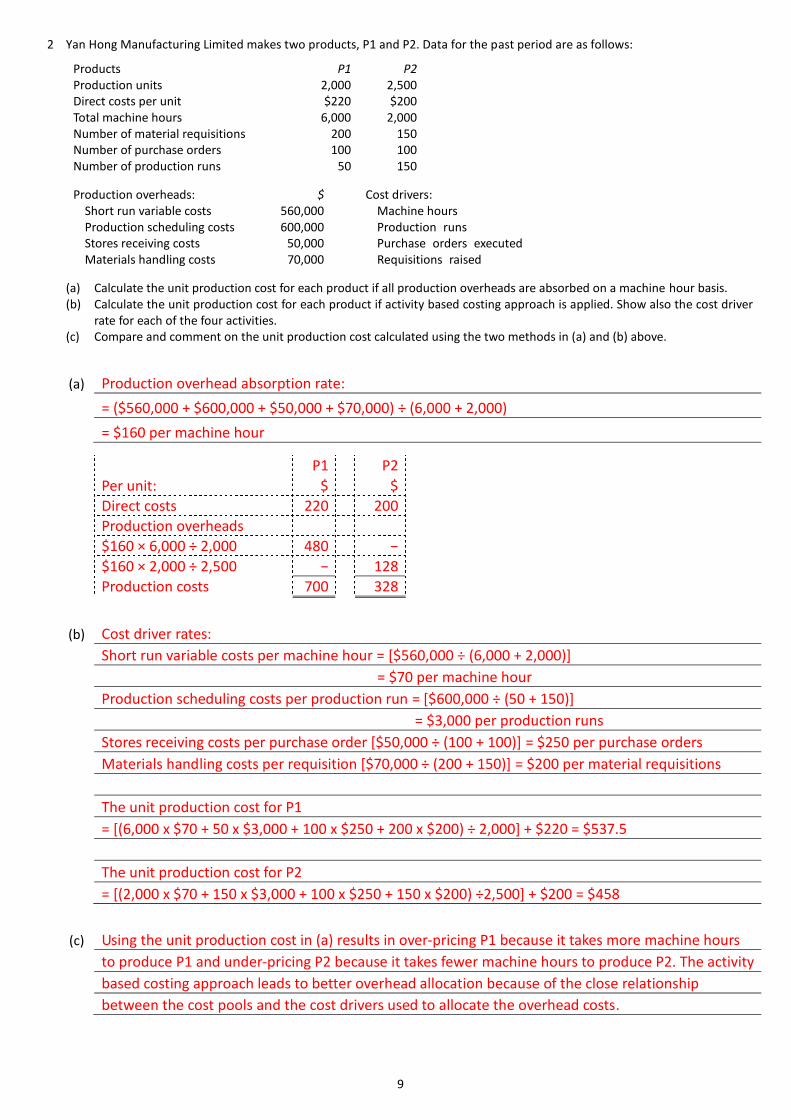

2 Yan Hong Manufacturing Limited makes two products, P1 and P2. Data for the past period are as follows:

Products P1 P2 Production units 2,000 2,500 Direct costs per unit $220 $200 Total machine hours 6,000 2,000 Number of material requisitions 200 150 Number of purchase orders 100 100 Number of production runs 50 150

Production overheads: $ Cost drivers:

Short run variable costs 560,000 Machine hours Production scheduling costs 600,000 Production runs Stores receiving costs 50,000 Purchase orders executed Materials handling costs 70,000 Requisitions raised

(a) Calculate the unit production cost for each product if all production overheads are absorbed on a machine hour basis. (b) Calculate the unit production cost for each product if activity based costing approach is applied. Show also the cost driver

rate for each of the four activities. (c) Compare and comment on the unit production cost calculated using the two methods in (a) and (b) above.

(a) Production overhead absorption rate:

= ($560,000 + $600,000 + $50,000 + $70,000) ÷ (6,000 + 2,000)

= $160 per machine hour

P1 P2

Per unit: $ $

Direct costs 220 200

Production overheads

$160 × 6,000 ÷ 2,000 480 −

$160 × 2,000 ÷ 2,500 − 128

Production costs 700 328

(b) Cost driver rates:

Short run variable costs per machine hour = [$560,000 ÷ (6,000 + 2,000)]

= $70 per machine hour

Production scheduling costs per production run = [$600,000 ÷ (50 + 150)]

= $3,000 per production runs

Stores receiving costs per purchase order [$50,000 ÷ (100 + 100)] = $250 per purchase orders

Materials handling costs per requisition [$70,000 ÷ (200 + 150)] = $200 per material requisitions

The unit production cost for P1

= [(6,000 x $70 + 50 x $3,000 + 100 x $250 + 200 x $200) ÷ 2,000] + $220 = $537.5

The unit production cost for P2

= [(2,000 x $70 + 150 x $3,000 + 100 x $250 + 150 x $200) ÷2,500] + $200 = $458

(c) Using the unit production cost in (a) results in over-pricing P1 because it takes more machine hours

to produce P1 and under-pricing P2 because it takes fewer machine hours to produce P2. The activity

based costing approach leads to better overhead allocation because of the close relationship

between the cost pools and the cost drivers used to allocate the overhead costs.

10

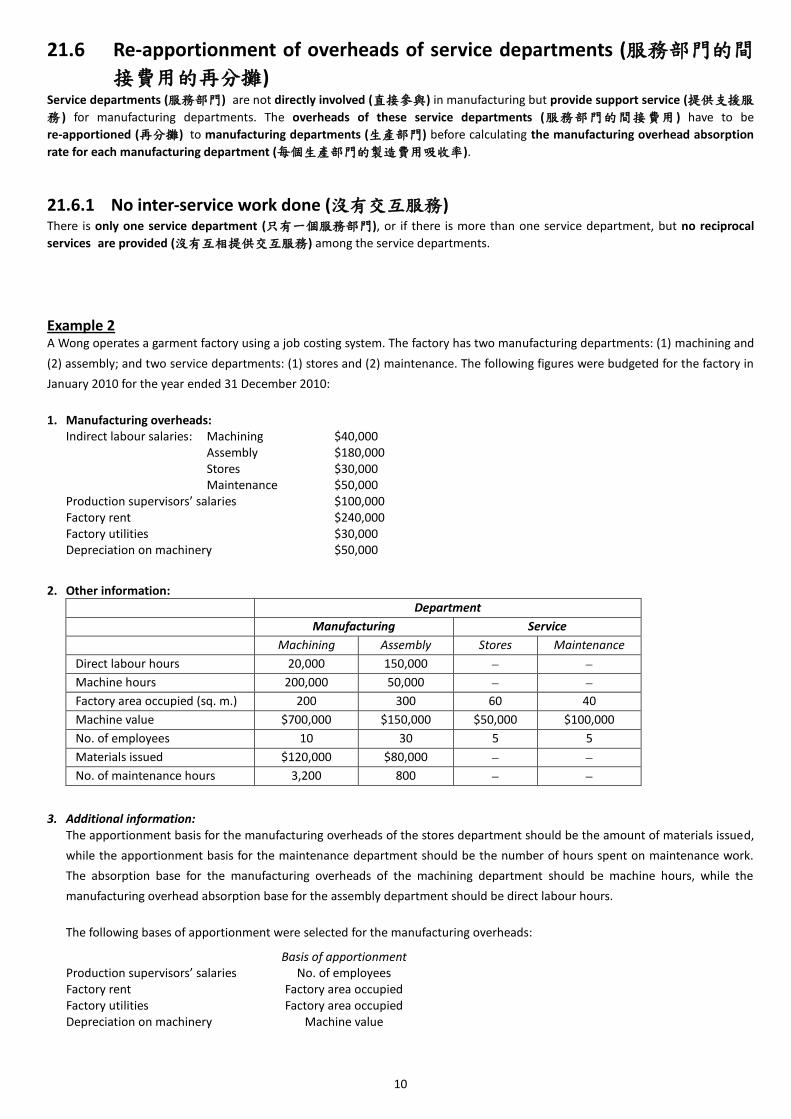

21.6 Re-apportionment of overheads of service departments (服務部門的間

接費用的再分攤) Service departments (服務部門) are not directly involved (直接參與) in manufacturing but provide support service (提供支援服

務 ) for manufacturing departments. The overheads of these service departments (服務部門的間接費用 ) have to be

re-apportioned (再分攤) to manufacturing departments (生產部門) before calculating the manufacturing overhead absorption

rate for each manufacturing department (每個生產部門的製造費用吸收率).

21.6.1 No inter-service work done (沒有交互服務) There is only one service department (只有一個服務部門), or if there is more than one service department, but no reciprocal

services are provided (沒有互相提供交互服務) among the service departments.

Example 2 A Wong operates a garment factory using a job costing system. The factory has two manufacturing departments: (1) machining and

(2) assembly; and two service departments: (1) stores and (2) maintenance. The following figures were budgeted for the factory in

January 2010 for the year ended 31 December 2010:

1. Manufacturing overheads: Indirect labour salaries: Machining $40,000 Assembly $180,000 Stores $30,000 Maintenance $50,000

Production supervisors’ salaries $100,000 Factory rent $240,000 Factory utilities $30,000 Depreciation on machinery $50,000 2. Other information:

Department

Manufacturing Service

Machining Assembly Stores Maintenance

Direct labour hours 20,000 150,000

Machine hours 200,000 50,000

Factory area occupied (sq. m.) 200 300 60 40

Machine value $700,000 $150,000 $50,000 $100,000

No. of employees 10 30 5 5

Materials issued $120,000 $80,000

No. of maintenance hours 3,200 800 3. Additional information:

The apportionment basis for the manufacturing overheads of the stores department should be the amount of materials issued,

while the apportionment basis for the maintenance department should be the number of hours spent on maintenance work.

The absorption base for the manufacturing overheads of the machining department should be machine hours, while the

manufacturing overhead absorption base for the assembly department should be direct labour hours.

The following bases of apportionment were selected for the manufacturing overheads:

Basis of apportionment Production supervisors’ salaries No. of employees Factory rent Factory area occupied Factory utilities Factory area occupied Depreciation on machinery Machine value

11

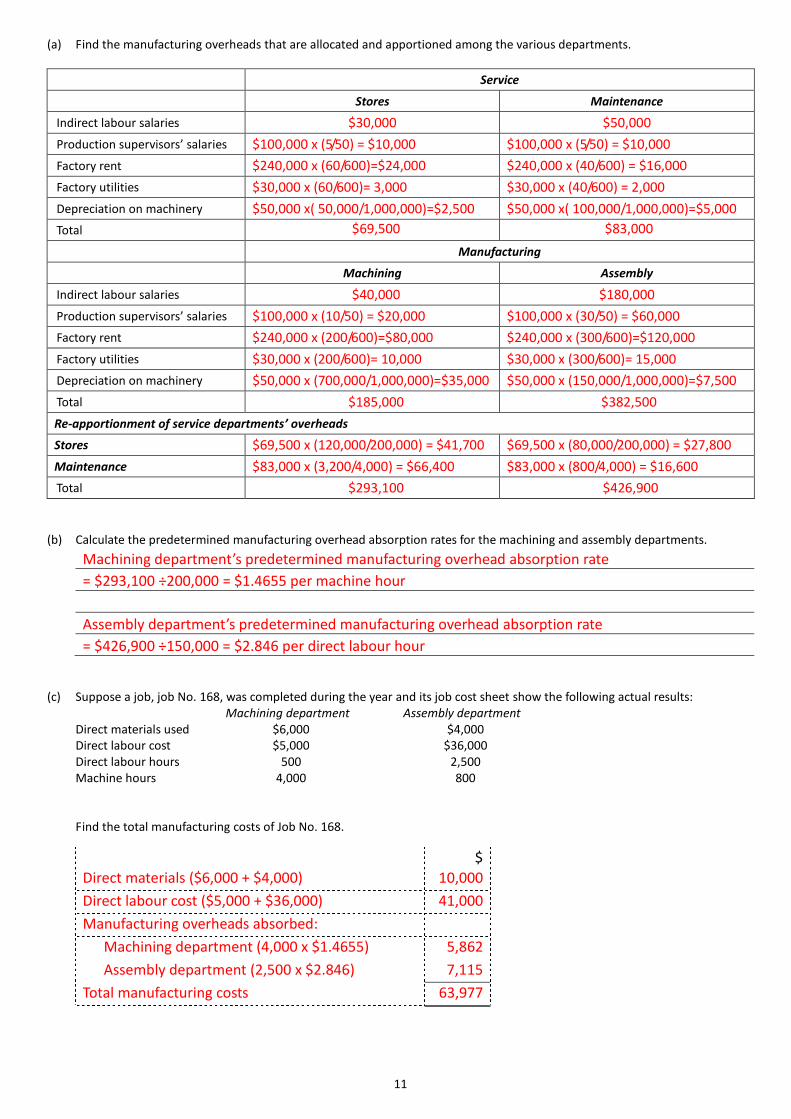

(a) Find the manufacturing overheads that are allocated and apportioned among the various departments.

Service

Stores Maintenance

Indirect labour salaries $30,000 $50,000

Production supervisors’ salaries $100,000 x (5/50) = $10,000 $100,000 x (5/50) = $10,000

Factory rent $240,000 x (60/600)=$24,000 $240,000 x (40/600) = $16,000

Factory utilities $30,000 x (60/600)= 3,000 $30,000 x (40/600) = 2,000

Depreciation on machinery $50,000 x( 50,000/1,000,000)=$2,500 $50,000 x( 100,000/1,000,000)=$5,000

Total $69,500 $83,000

Manufacturing

Machining Assembly

Indirect labour salaries $40,000 $180,000

Production supervisors’ salaries $100,000 x (10/50) = $20,000 $100,000 x (30/50) = $60,000

Factory rent $240,000 x (200/600)=$80,000 $240,000 x (300/600)=$120,000

Factory utilities $30,000 x (200/600)= 10,000 $30,000 x (300/600)= 15,000

Depreciation on machinery $50,000 x (700,000/1,000,000)=$35,000 $50,000 x (150,000/1,000,000)=$7,500

Total $185,000 $382,500

Re-apportionment of service departments’ overheads

Stores $69,500 x (120,000/200,000) = $41,700 $69,500 x (80,000/200,000) = $27,800

Maintenance $83,000 x (3,200/4,000) = $66,400 $83,000 x (800/4,000) = $16,600

Total $293,100 $426,900

(b) Calculate the predetermined manufacturing overhead absorption rates for the machining and assembly departments.

Machining department’s predetermined manufacturing overhead absorption rate

= $293,100 ÷200,000 = $1.4655 per machine hour

Assembly department’s predetermined manufacturing overhead absorption rate

= $426,900 ÷150,000 = $2.846 per direct labour hour (c) Suppose a job, job No. 168, was completed during the year and its job cost sheet show the following actual results:

Machining department Assembly department Direct materials used $6,000 $4,000 Direct labour cost $5,000 $36,000 Direct labour hours 500 2,500 Machine hours 4,000 800

Find the total manufacturing costs of Job No. 168.

$

Direct materials ($6,000 + $4,000) 10,000

Direct labour cost ($5,000 + $36,000) 41,000

Manufacturing overheads absorbed:

Machining department (4,000 x $1.4655) 5,862

Assembly department (2,500 x $2.846) 7,115

Total manufacturing costs 63,977

12

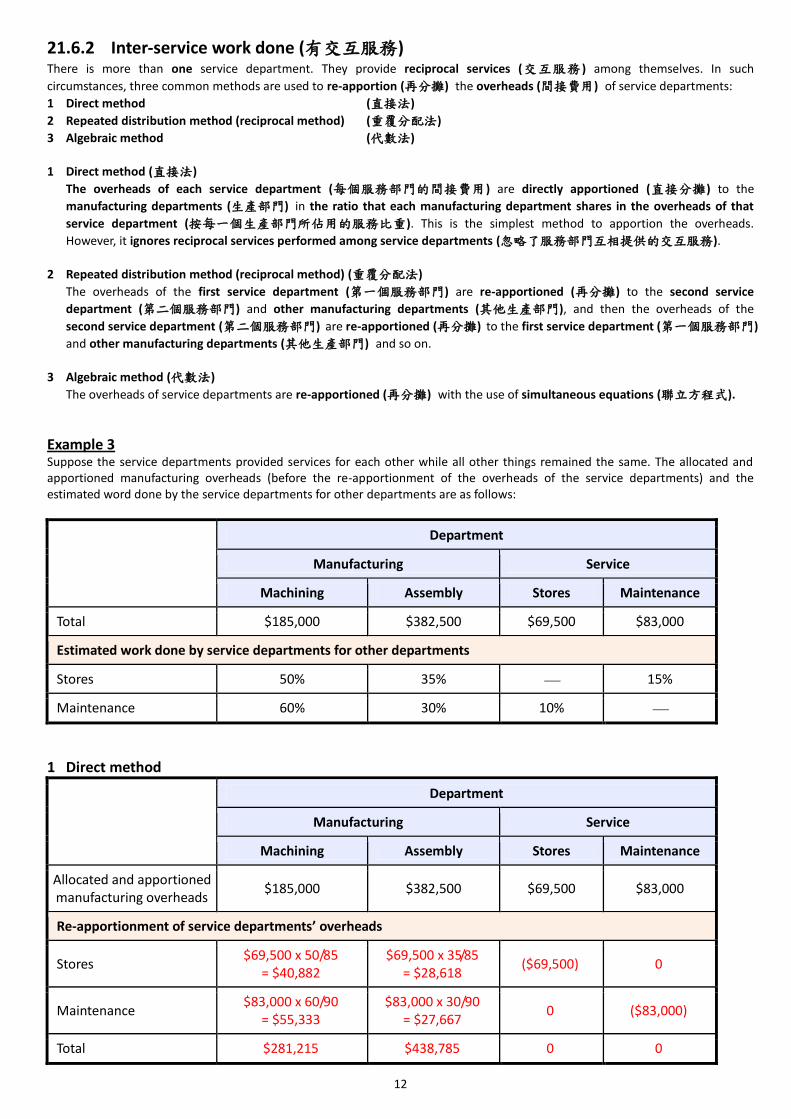

21.6.2 Inter-service work done (有交互服務) There is more than one service department. They provide reciprocal services (交互服務 ) among themselves. In such

circumstances, three common methods are used to re-apportion (再分攤) the overheads (間接費用) of service departments:

1 Direct method (直接法)

2 Repeated distribution method (reciprocal method) (重覆分配法)

3 Algebraic method (代數法)

1 Direct method (直接法)

The overheads of each service department (每個服務部門的間接費用) are directly apportioned (直接分攤) to the

manufacturing departments (生產部門) in the ratio that each manufacturing department shares in the overheads of that

service department (按每一個生產部門所佔用的服務比重). This is the simplest method to apportion the overheads.

However, it ignores reciprocal services performed among service departments (忽略了服務部門互相提供的交互服務).

2 Repeated distribution method (reciprocal method) (重覆分配法)

The overheads of the first service department (第一個服務部門) are re-apportioned (再分攤) to the second service

department (第二個服務部門) and other manufacturing departments (其他生產部門), and then the overheads of the

second service department (第二個服務部門) are re-apportioned (再分攤) to the first service department (第一個服務部門)

and other manufacturing departments (其他生產部門) and so on.

3 Algebraic method (代數法)

The overheads of service departments are re-apportioned (再分攤) with the use of simultaneous equations (聯立方程式).

Example 3 Suppose the service departments provided services for each other while all other things remained the same. The allocated and apportioned manufacturing overheads (before the re-apportionment of the overheads of the service departments) and the estimated word done by the service departments for other departments are as follows:

Department

Manufacturing Service

Machining Assembly Stores Maintenance

Total $185,000 $382,500 $69,500 $83,000

Estimated work done by service departments for other departments

Stores 50% 35% 15%

Maintenance 60% 30% 10%

1 Direct method

Department

Manufacturing Service

Machining Assembly Stores Maintenance

Allocated and apportioned manufacturing overheads

$185,000 $382,500 $69,500 $83,000

Re-apportionment of service departments’ overheads

Stores $69,500 x 50/85

= $40,882 $69,500 x 35/85

= $28,618 ($69,500) 0

Maintenance $83,000 x 60/90

= $55,333 $83,000 x 30/90

= $27,667 0 ($83,000)

Total $281,215 $438,785 0 0

13

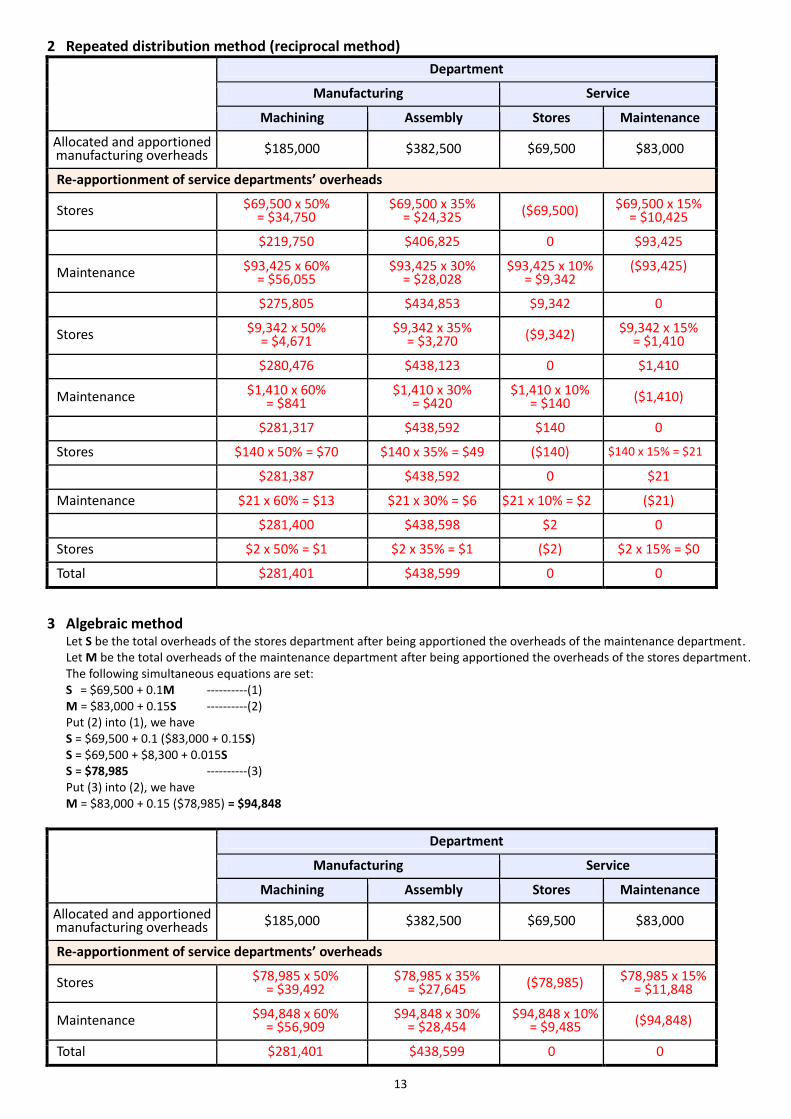

2 Repeated distribution method (reciprocal method)

Department

Manufacturing Service

Machining Assembly Stores Maintenance

Allocated and apportioned manufacturing overheads $185,000 $382,500 $69,500 $83,000

Re-apportionment of service departments’ overheads

Stores $69,500 x 50% = $34,750

$69,500 x 35% = $24,325 ($69,500) $69,500 x 15%

= $10,425

$219,750 $406,825 0 $93,425

Maintenance $93,425 x 60% = $56,055

$93,425 x 30% = $28,028

$93,425 x 10% = $9,342

($93,425)

$275,805 $434,853 $9,342 0

Stores $9,342 x 50% = $4,671

$9,342 x 35% = $3,270 ($9,342) $9,342 x 15%

= $1,410

$280,476 $438,123 0 $1,410

Maintenance $1,410 x 60% = $841

$1,410 x 30% = $420

$1,410 x 10% = $140 ($1,410)

$281,317 $438,592 $140 0

Stores $140 x 50% = $70 $140 x 35% = $49 ($140) $140 x 15% = $21

$281,387 $438,592 0 $21

Maintenance $21 x 60% = $13 $21 x 30% = $6 $21 x 10% = $2 ($21)

$281,400 $438,598 $2 0

Stores $2 x 50% = $1 $2 x 35% = $1 ($2) $2 x 15% = $0

Total $281,401 $438,599 0 0

3 Algebraic method Let S be the total overheads of the stores department after being apportioned the overheads of the maintenance department. Let M be the total overheads of the maintenance department after being apportioned the overheads of the stores department. The following simultaneous equations are set: S = $69,500 + 0.1M ----------(1) M = $83,000 + 0.15S ----------(2) Put (2) into (1), we have S = $69,500 + 0.1 ($83,000 + 0.15S) S = $69,500 + $8,300 + 0.015S S = $78,985 ----------(3)

Put (3) into (2), we have M = $83,000 + 0.15 ($78,985) = $94,848

Department

Manufacturing Service

Machining Assembly Stores Maintenance

Allocated and apportioned manufacturing overheads $185,000 $382,500 $69,500 $83,000

Re-apportionment of service departments’ overheads

Stores $78,985 x 50% = $39,492

$78,985 x 35% = $27,645 ($78,985) $78,985 x 15%

= $11,848

Maintenance $94,848 x 60% = $56,909

$94,848 x 30% = $28,454

$94,848 x 10% = $9,485 ($94,848)

Total $281,401 $438,599 0 0

14

It is given that the machine hours of machining department are 200,000 and the direct labour hours of assembly department are 150,000. The absorption base for the manufacturing overheads of the machining department should be machine hours, while the manufacturing overhead absorption base for the assembly department should be direct labour hours. The predetermined manufacturing overhead absorption rates for the machining department and the assembly department are calculated as follows:

Machining department’s manufacturing overhead absorption rate = $281,401 ÷200,000 = $1.407 per machine hour

Assembly department’s manufacturing overhead absorption rate = $438,599 ÷150,000 = $2.924 per direct labour hour Suppose a job, job No. 168, was completed during the year and its job cost sheet show the following actual results: Machining department Assembly department Direct materials used $6,000 $4,000 Direct labour cost $5,000 $36,000 Direct labour hours 500 2,500 Machine hours 4,000 800 The total manufacturing costs of job No. 168 are calculated as follows:

$

Direct materials ($6,000 + $4,000) 10,000

Direct labour cost ($5,000 + $36,000) 41,000

Manufacturing overheads absorbed:

Machining department (4,000 x $1.407) 5,628

Assembly department (2,500 x $2.924) 7,310

Total manufacturing costs 63,938

Classwork 6 1 Ting Tang Co Ltd has two service departments (Service A and Service B) and two production departments (Prod. 1 and Prod. 2).

The direct costs and percentage of service costs consumed by the departments for the month June 2005 are as follows:

Percentage of service consumed

Department Cost Service A Service B Prod. 1 Prod. 2

Service A $160,000 20% 45% 35%

Service B $230,000 15% 35% 50%

Prod. 1 $880,000

Prod. 2 $1,000,000

Calculate the amount of service department costs that should be apportioned to production departments using: (a) the direct method; and (b) the reciprocal method.

(a)

Service department Cost to be allocated Prod. 1 Prod.2

A $160,000 $160,000 x 45/80 = $90,000 $160,000 x 35/80 = $70,000

B $230,000 $230,000 x 35/85 = $94,706 $230,000 x 50/85 = $135,294

(b)

Service department Cost to be allocated Prod. 1 Prod.2 Service A Service B

A $160,000 $72,000 $56,000 $32,000

B $262,000 $91,700 $131,000 $39,300 A $39,300 $17,685 $13,755 $7,860

B $7,860 $2,751 $3,930 $1,179 A $1,179 $531 $413 $235

B $235 $82 $118 $35 A $35 $16 $12 $7

B $7 $3 $4

15

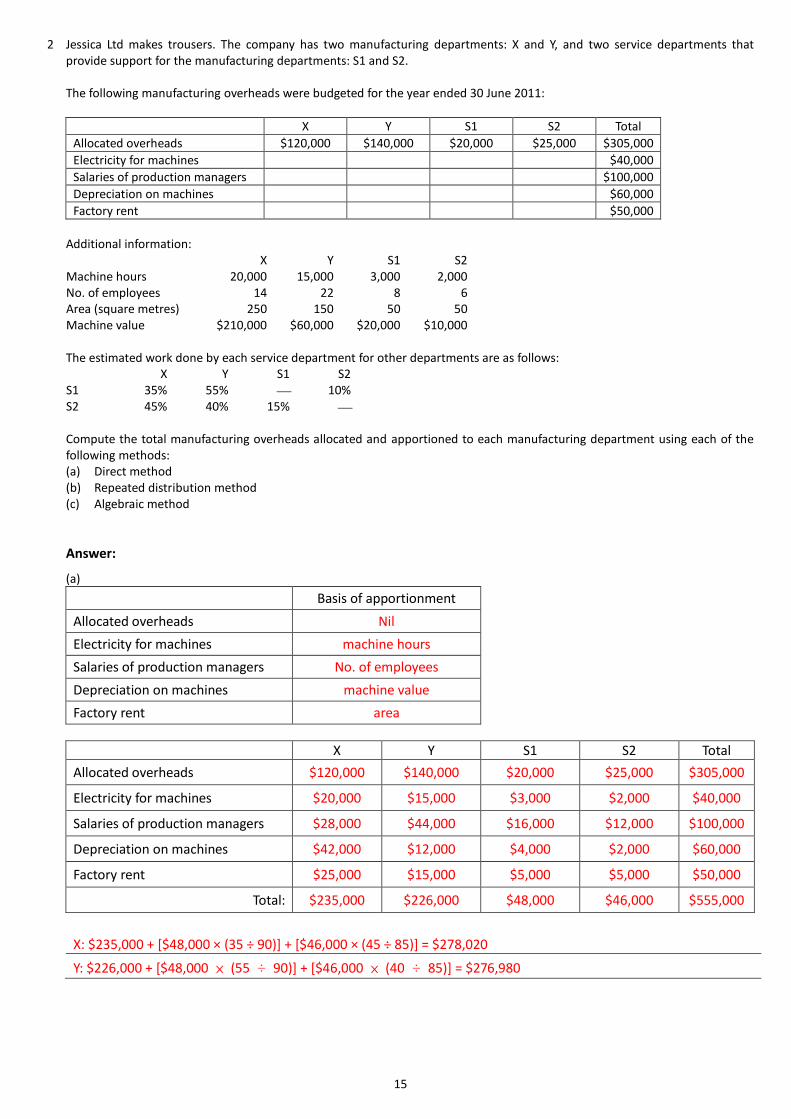

2 Jessica Ltd makes trousers. The company has two manufacturing departments: X and Y, and two service departments that provide support for the manufacturing departments: S1 and S2.

The following manufacturing overheads were budgeted for the year ended 30 June 2011:

X Y S1 S2 Total

Allocated overheads $120,000 $140,000 $20,000 $25,000 $305,000

Electricity for machines $40,000

Salaries of production managers $100,000

Depreciation on machines $60,000

Factory rent $50,000

Additional information:

X Y S1 S2 Machine hours 20,000 15,000 3,000 2,000 No. of employees 14 22 8 6 Area (square metres) 250 150 50 50 Machine value $210,000 $60,000 $20,000 $10,000

The estimated work done by each service department for other departments are as follows:

X Y S1 S2 S1 35% 55% 10% S2 45% 40% 15%

Compute the total manufacturing overheads allocated and apportioned to each manufacturing department using each of the

following methods: (a) Direct method (b) Repeated distribution method (c) Algebraic method

Answer: (a)

Basis of apportionment

Allocated overheads Nil

Electricity for machines machine hours

Salaries of production managers No. of employees

Depreciation on machines machine value

Factory rent area

X Y S1 S2 Total

Allocated overheads $120,000 $140,000 $20,000 $25,000 $305,000

Electricity for machines $20,000 $15,000 $3,000 $2,000 $40,000

Salaries of production managers $28,000 $44,000 $16,000 $12,000 $100,000

Depreciation on machines $42,000 $12,000 $4,000 $2,000 $60,000

Factory rent $25,000 $15,000 $5,000 $5,000 $50,000

Total: $235,000 $226,000 $48,000 $46,000 $555,000

X: $235,000 + [$48,000 × (35 ÷ 90)] + [$46,000 × (45 ÷ 85)] = $278,020

Y: $226,000 + [$48,000 × (55 ÷ 90)] + [$46,000 × (40 ÷ 85)] = $276,980

16

(b) Re-apportionment of service departments’ overheads

X Y S1 S2

Cost to be allocated $235,000 $226,000 $48,000 $46,000

S1 $48,000 $16,800 $26,400 ($48,000) $4,800

S2 $50,800 $22,860 $20,320 $7,620 ($50,800)

S1 $7,620 $2,667 $4,191 ($7,620) $762

S2 $762 $343 $305 $114 ($762)

S1 $114 $40 $63 ($114) $11

S2 $11 $5 $4 $2 ($11)

S1 $2 $1 $1 ($2) 0

Total: $277,716 $277,284 0 0

(c) Let S1 be the total overheads of the S1 department after being apportioned the overheads of the S2.

Let S2 be the total overheads of the S2 department after being apportioned the overheads of the S1.

S1 = $48,000 + 0.15S2 — (1)

S2 = $46,000 + 0.1S1 — (2)

Put equation (2) into equation (1):

S1 = $48,000 + 0.15($46,000 + 0.1S1)

= $48,000 + $6,900 + 0.015S1

= $55,736 — (3)

Put equation (3) into equation (2):

S2 = $46,000 + (0.1 × $55,736) = $51,574

X Y S1 S2 Total

Allocated and apportioned overheads $235,000 $226,000 $48,000 $46,000 $555,000

Re-apportionment of service departments’ overheads

S1 $55,736 $19,508 $30,654 ($55,736) $5,574

S2 $51,574 $23,208 $20,630 $7,736 ($51,574)

Total: $277,716 $277,284 0 0 $555,000

17

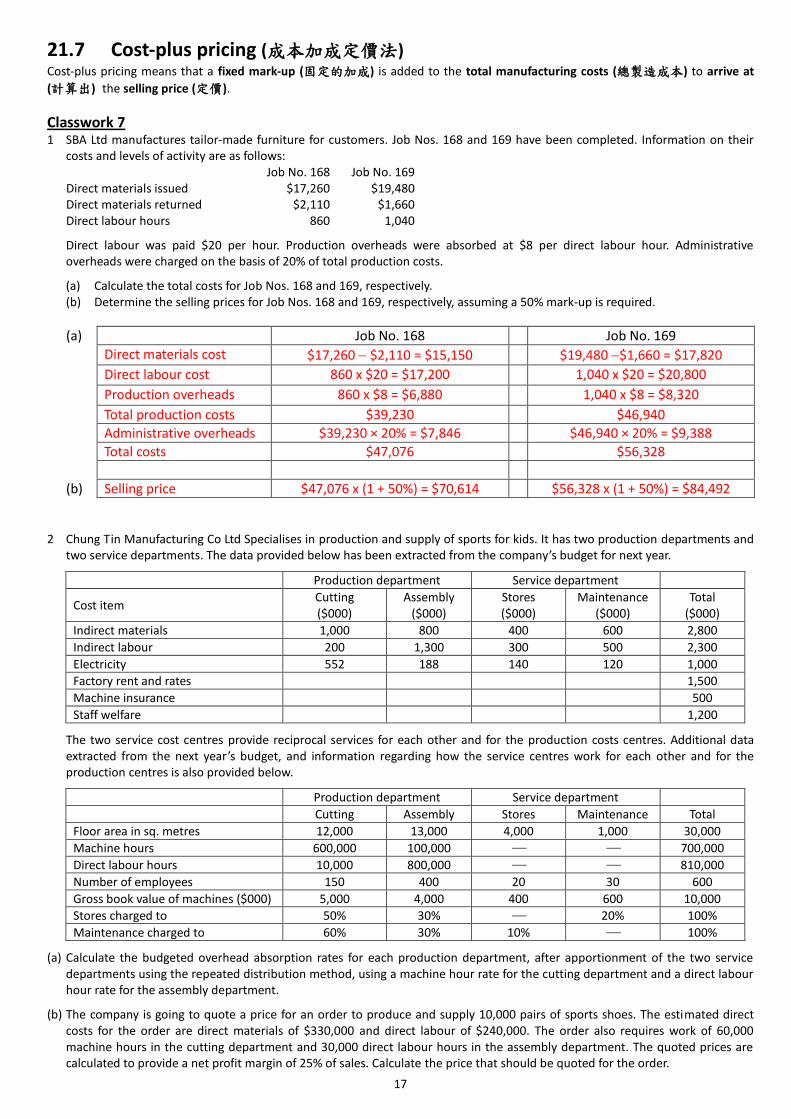

21.7 Cost-plus pricing (成本加成定價法) Cost-plus pricing means that a fixed mark-up (固定的加成) is added to the total manufacturing costs (總製造成本) to arrive at

(計算出) the selling price (定價).

Classwork 7 1 SBA Ltd manufactures tailor-made furniture for customers. Job Nos. 168 and 169 have been completed. Information on their

costs and levels of activity are as follows: Job No. 168 Job No. 169 Direct materials issued $17,260 $19,480 Direct materials returned $2,110 $1,660 Direct labour hours 860 1,040

Direct labour was paid $20 per hour. Production overheads were absorbed at $8 per direct labour hour. Administrative overheads were charged on the basis of 20% of total production costs.

(a) Calculate the total costs for Job Nos. 168 and 169, respectively. (b) Determine the selling prices for Job Nos. 168 and 169, respectively, assuming a 50% mark-up is required.

(a) Job No. 168 Job No. 169

Direct materials cost $17,260 $2,110 = $15,150 $19,480 $1,660 = $17,820

Direct labour cost 860 x $20 = $17,200 1,040 x $20 = $20,800

Production overheads 860 x $8 = $6,880 1,040 x $8 = $8,320

Total production costs $39,230 $46,940

Administrative overheads $39,230 × 20% = $7,846 $46,940 × 20% = $9,388

Total costs $47,076 $56,328

(b) Selling price $47,076 x (1 + 50%) = $70,614 $56,328 x (1 + 50%) = $84,492 2 Chung Tin Manufacturing Co Ltd Specialises in production and supply of sports for kids. It has two production departments and

two service departments. The data provided below has been extracted from the company’s budget for next year.

Production department Service department

Cost item Cutting ($000)

Assembly ($000)

Stores ($000)

Maintenance ($000)

Total ($000)

Indirect materials 1,000 800 400 600 2,800

Indirect labour 200 1,300 300 500 2,300

Electricity 552 188 140 120 1,000

Factory rent and rates 1,500

Machine insurance 500

Staff welfare 1,200

The two service cost centres provide reciprocal services for each other and for the production costs centres. Additional data extracted from the next year’s budget, and information regarding how the service centres work for each other and for the production centres is also provided below.

Production department Service department

Cutting Assembly Stores Maintenance Total

Floor area in sq. metres 12,000 13,000 4,000 1,000 30,000

Machine hours 600,000 100,000 700,000

Direct labour hours 10,000 800,000 810,000

Number of employees 150 400 20 30 600

Gross book value of machines ($000) 5,000 4,000 400 600 10,000

Stores charged to 50% 30% 20% 100%

Maintenance charged to 60% 30% 10% 100% (a) Calculate the budgeted overhead absorption rates for each production department, after apportionment of the two service

departments using the repeated distribution method, using a machine hour rate for the cutting department and a direct labour hour rate for the assembly department.

(b) The company is going to quote a price for an order to produce and supply 10,000 pairs of sports shoes. The estimated direct

costs for the order are direct materials of $330,000 and direct labour of $240,000. The order also requires work of 60,000 machine hours in the cutting department and 30,000 direct labour hours in the assembly department. The quoted prices are calculated to provide a net profit margin of 25% of sales. Calculate the price that should be quoted for the order.

18

(c) If next year 500,000 machine hours were worked in the cutting department, 900,000 direct labour hours were worked in the assembly department, and the actual overheads for the cutting department and the assembly department were $3,500,000 and $5,600,000. Calculate any under or over absorption of overheads separately for the cutting and the assembly department.

(a)

Allocated and apportioned manufacturing overheads

Production department Service department

Cost item Basis of apportionment Cutting ($000)

Assembly ($000)

Stores ($000)

Maintenance ($000)

Total ($000)

Indirect materials 1,000 800 400 600 2,800

Indirect labour 200 1,300 300 500 2,300

Electricity 552 188 140 120 1,000

Factory rent and rates Floor area 600 650 200 50 1,500

Machine insurance Gross book value 250 200 20 30 500

Staff welfare Number of employees 300 800 40 60 1,200

Budgeted overheads before re-apportionment 2,902 3,938 1,100 1,360 9,300

Re-apportionment of service departments’ overheads

Cost item Cost to be allocated

Maintenance 1,360 816 408 136 (1,360)

Stores 1,236 618 371 (1,236) 247

Maintenance 247 148 74 25 (247)

Stores 25 13 7 (25) 5

Maintenance 5 3 2 0 (5)

Total Budgeted overhead 4,500 4,800 0 0

Cutting department’s budgeted overhead absorption rate = 4,500,000 ÷600,000 = $7.5 per machine hour

Assembly department’s budgeted overhead absorption rate = $4,800,000 ÷800,000 = $6 per direct labour hour

(b) Quoted price:

$

Direct materials 330,000

Direct labour 240,000

Manufacturing overheads absorbed:

Cutting department (60,000 x $7.5) 450,000

Assembly department (30,000 x $6) 180,000

Production costs 1,200,000

Profit margin (25%) 400,000

Quoted price (100%) 1,600,000

(c) Under- or over-absorption of overheads:

Cutting Assembly

Overheads absorbed 500,000 x $7.5 = $3,750,000 900,000 x $6 = $5,400,000

Overheads incurred ($3,500,000) ($5,600,000)

Over-/(Under-) absorption $250,000 ($200,000)

19

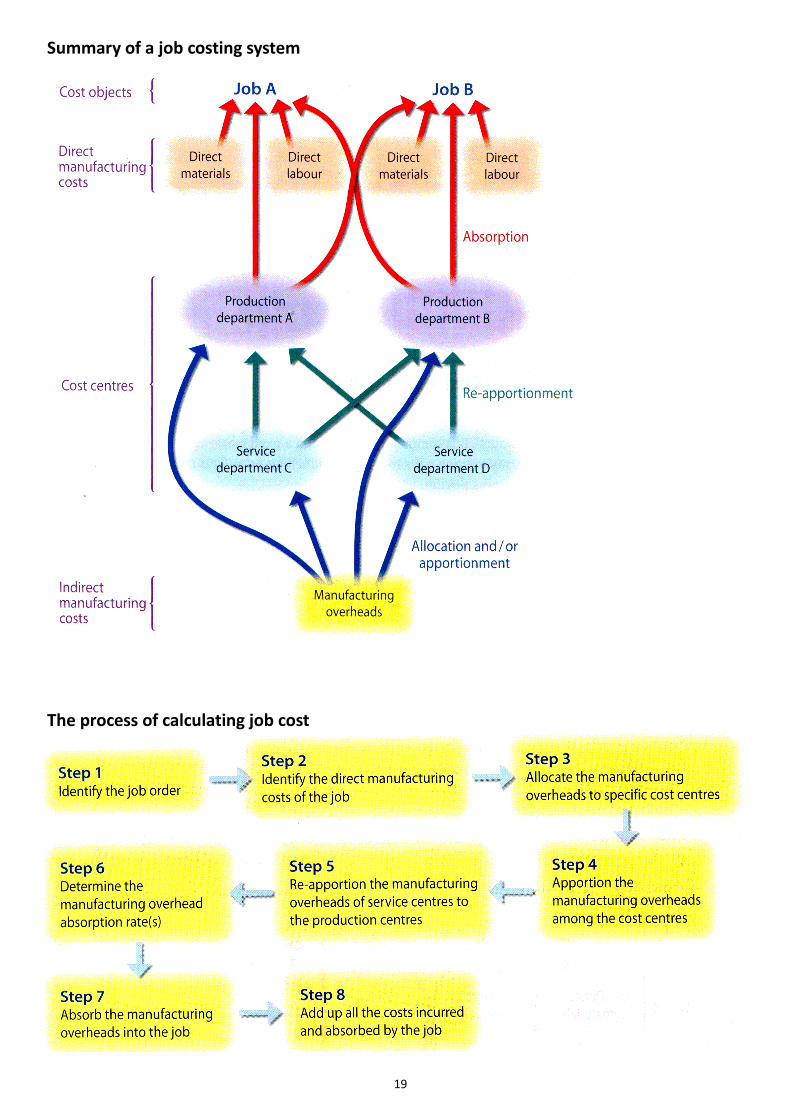

Summary of a job costing system

The process of calculating job cost

20

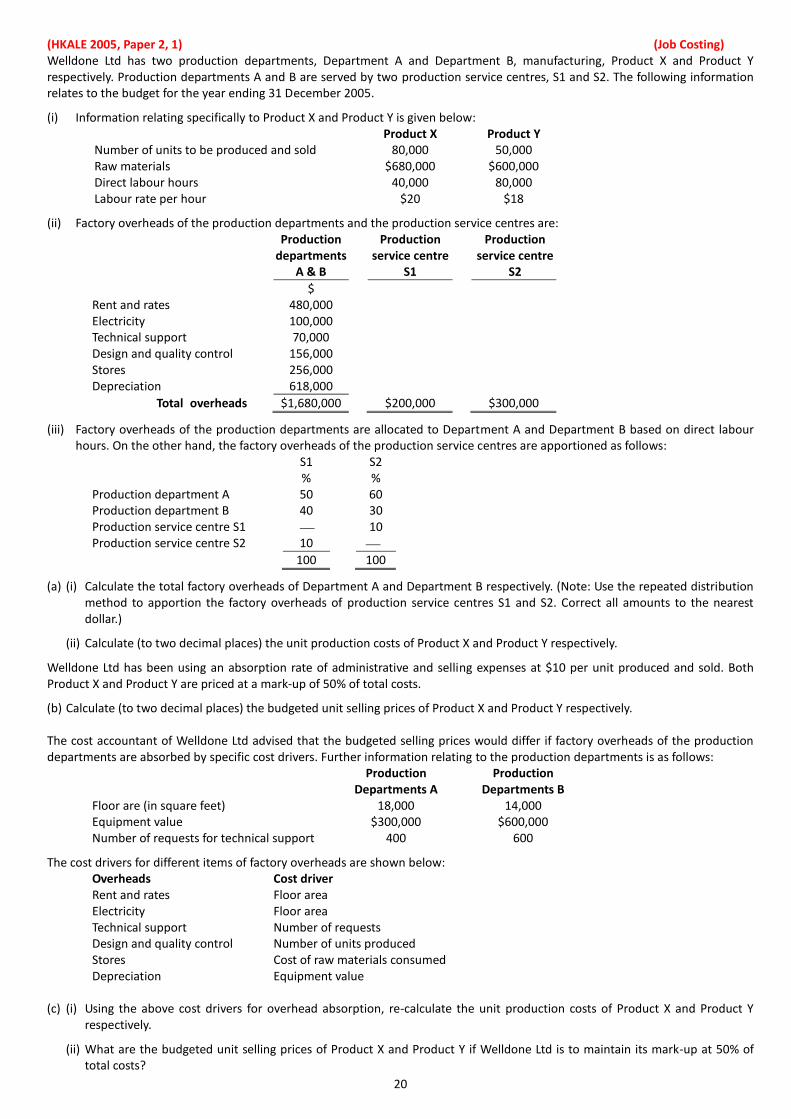

(HKALE 2005, Paper 2, 1) (Job Costing) Welldone Ltd has two production departments, Department A and Department B, manufacturing, Product X and Product Y respectively. Production departments A and B are served by two production service centres, S1 and S2. The following information relates to the budget for the year ending 31 December 2005. (i) Information relating specifically to Product X and Product Y is given below:

Product X Product Y Number of units to be produced and sold 80,000 50,000 Raw materials $680,000 $600,000 Direct labour hours 40,000 80,000 Labour rate per hour $20 $18

(ii) Factory overheads of the production departments and the production service centres are:

Production departments

A & B

Production service centre

S1

Production service centre

S2

$ Rent and rates 480,000 Electricity 100,000 Technical support 70,000 Design and quality control 156,000 Stores 256,000 Depreciation 618,000

Total overheads $1,680,000 $200,000 $300,000 (iii) Factory overheads of the production departments are allocated to Department A and Department B based on direct labour

hours. On the other hand, the factory overheads of the production service centres are apportioned as follows: S1 S2 % % Production department A 50 60 Production department B 40 30 Production service centre S1 10 Production service centre S2 10 100 100

(a) (i) Calculate the total factory overheads of Department A and Department B respectively. (Note: Use the repeated distribution

method to apportion the factory overheads of production service centres S1 and S2. Correct all amounts to the nearest dollar.)

(ii) Calculate (to two decimal places) the unit production costs of Product X and Product Y respectively. Welldone Ltd has been using an absorption rate of administrative and selling expenses at $10 per unit produced and sold. Both Product X and Product Y are priced at a mark-up of 50% of total costs. (b) Calculate (to two decimal places) the budgeted unit selling prices of Product X and Product Y respectively. The cost accountant of Welldone Ltd advised that the budgeted selling prices would differ if factory overheads of the production departments are absorbed by specific cost drivers. Further information relating to the production departments is as follows:

Production Departments A

Production Departments B

Floor are (in square feet) 18,000 14,000 Equipment value $300,000 $600,000 Number of requests for technical support 400 600

The cost drivers for different items of factory overheads are shown below:

Overheads Cost driver Rent and rates Floor area Electricity Floor area Technical support Number of requests Design and quality control Number of units produced Stores Cost of raw materials consumed Depreciation Equipment value

(c) (i) Using the above cost drivers for overhead absorption, re-calculate the unit production costs of Product X and Product Y

respectively. (ii) What are the budgeted unit selling prices of Product X and Product Y if Welldone Ltd is to maintain its mark-up at 50% of

total costs?

21

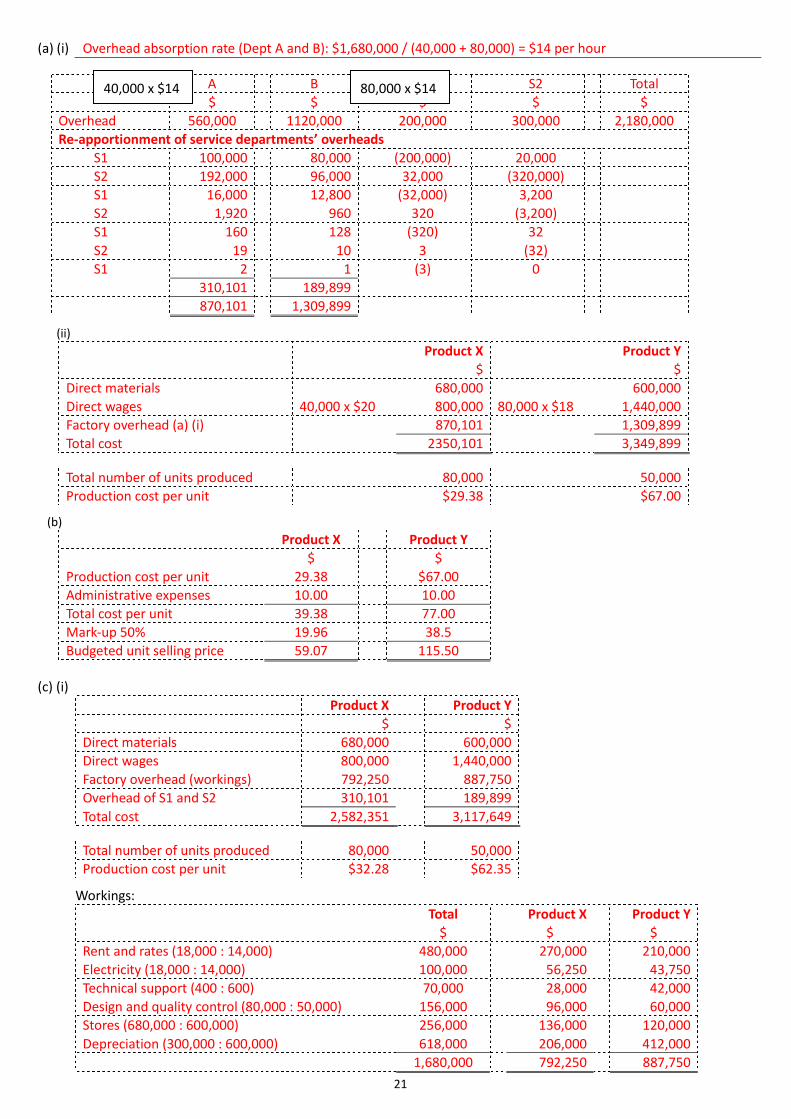

(a) (i) Overhead absorption rate (Dept A and B): $1,680,000 / (40,000 + 80,000) = $14 per hour

A B S1 S2 Total

$ $ $ $ $

Overhead 560,000 1120,000 200,000 300,000 2,180,000

Re-apportionment of service departments’ overheads

S1 100,000 80,000 (200,000) 20,000

S2 192,000 96,000 32,000 (320,000)

S1 16,000 12,800 (32,000) 3,200

S2 1,920 960 320 (3,200)

S1 160 128 (320) 32

S2 19 10 3 (32)

S1 2 1 (3) 0

310,101 189,899

870,101 1,309,899 (ii)

Product X Product Y

$ $

Direct materials 680,000 600,000

Direct wages 40,000 x $20 800,000 80,000 x $18 1,440,000

Factory overhead (a) (i) 870,101 1,309,899

Total cost 2350,101 3,349,899 Total number of units produced 80,000 50,000

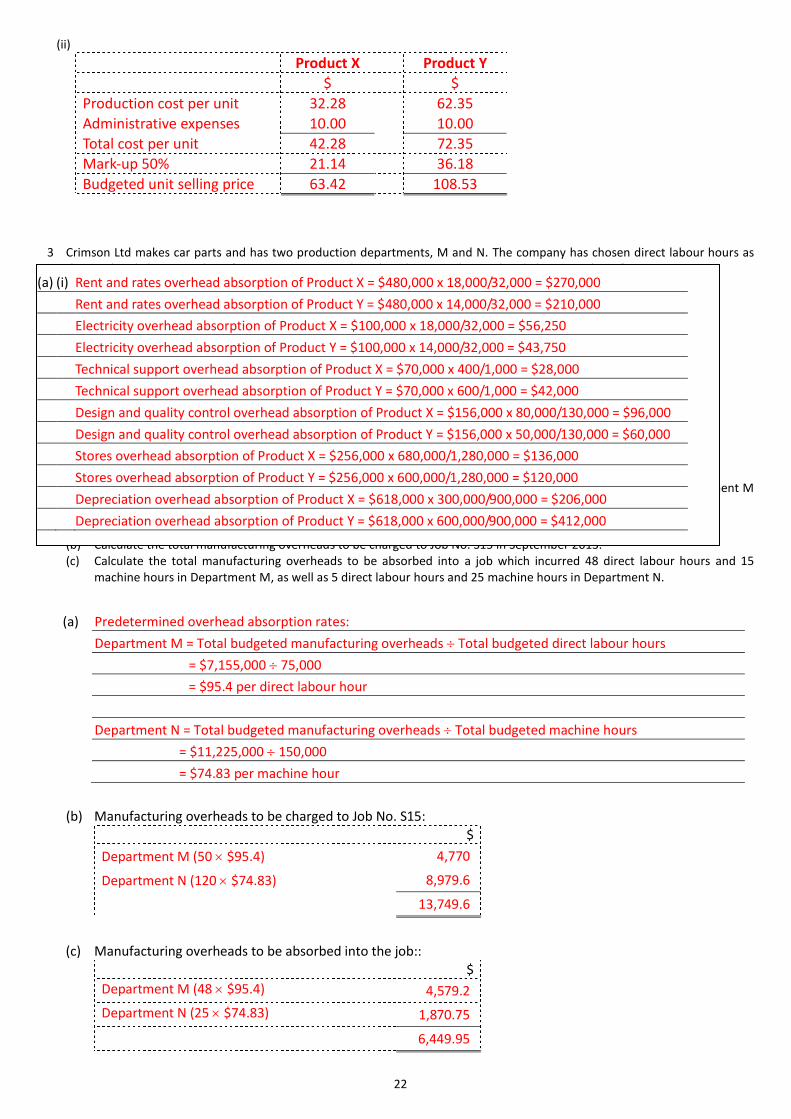

Production cost per unit $29.38 $67.00 (b)

Product X Product Y

$ $

Production cost per unit 29.38 $67.00

Administrative expenses 10.00 10.00

Total cost per unit 39.38 77.00

Mark-up 50% 19.96 38.5

Budgeted unit selling price 59.07 115.50

(c) (i)

Product X Product Y

$ $

Direct materials 680,000 600,000

Direct wages 800,000 1,440,000

Factory overhead (workings) 792,250 887,750

Overhead of S1 and S2 310,101 189,899

Total cost 2,582,351 3,117,649 Total number of units produced 80,000 50,000

Production cost per unit $32.28 $62.35

Workings:

Total Product X Product Y

$ $ $

Rent and rates (18,000 : 14,000) 480,000 270,000 210,000

Electricity (18,000 : 14,000) 100,000 56,250 43,750

Technical support (400 : 600) 70,000 28,000 42,000

Design and quality control (80,000 : 50,000) 156,000 96,000 60,000

Stores (680,000 : 600,000) 256,000 136,000 120,000

Depreciation (300,000 : 600,000) 618,000 206,000 412,000

1,680,000 792,250 887,750

40,000 x $14 80,000 x $14

22

(ii)

Product X Product Y

$ $

Production cost per unit 32.28 62.35

Administrative expenses 10.00 10.00

Total cost per unit 42.28 72.35

Mark-up 50% 21.14 36.18

Budgeted unit selling price 63.42 108.53 3 Crimson Ltd makes car parts and has two production departments, M and N. The company has chosen direct labour hours as

the overhead absorption base for Department M and machine hours as the overhead absorption base for Department N. Budget information at the beginning of the financial year ended 31 December 2013 is as follows:

Department M Department N Direct labour $6,000,000 $1,800,000 Manufacturing overheads $7,155,000 $11,225,000 Direct labour hours 75,000 hours 28,000 hours Machine hours 30,000 hours 150,000 hours

For the month of September 2013, the job cost records of Job No. S15 showed the following information:

Department M Department N Direct materials consumed $10,000 $50,000 Direct labour hours 50 hours 30 hours Machine hours 10 hours 120 hours

At the end of the financial year, the company ascertained that the actual manufacturing overheads incurred in Department M and Department N were $7,500,000 and $10,000,000, respectively.

(a) Calculate the predetermined overhead absorption rates for the production departments. (b) Calculate the total manufacturing overheads to be charged to Job No. S15 in September 2013. (c) Calculate the total manufacturing overheads to be absorbed into a job which incurred 48 direct labour hours and 15

machine hours in Department M, as well as 5 direct labour hours and 25 machine hours in Department N.

(a) Predetermined overhead absorption rates:

Department M = Total budgeted manufacturing overheads Total budgeted direct labour hours

= $7,155,000 75,000

= $95.4 per direct labour hour

Department N = Total budgeted manufacturing overheads Total budgeted machine hours

= $11,225,000 150,000

= $74.83 per machine hour

(b) Manufacturing overheads to be charged to Job No. S15:

$

Department M (50 $95.4) 4,770

Department N (120 $74.83) 8,979.6

13,749.6

(c) Manufacturing overheads to be absorbed into the job::

$

Department M (48 $95.4) 4,579.2

Department N (25 $74.83) 1,870.75

6,449.95

(a) (i) Rent and rates overhead absorption of Product X = $480,000 x 18,000/32,000 = $270,000

Rent and rates overhead absorption of Product Y = $480,000 x 14,000/32,000 = $210,000

Electricity overhead absorption of Product X = $100,000 x 18,000/32,000 = $56,250

Electricity overhead absorption of Product Y = $100,000 x 14,000/32,000 = $43,750

Technical support overhead absorption of Product X = $70,000 x 400/1,000 = $28,000

Technical support overhead absorption of Product Y = $70,000 x 600/1,000 = $42,000

Design and quality control overhead absorption of Product X = $156,000 x 80,000/130,000 = $96,000

Design and quality control overhead absorption of Product Y = $156,000 x 50,000/130,000 = $60,000

Stores overhead absorption of Product X = $256,000 x 680,000/1,280,000 = $136,000

Stores overhead absorption of Product Y = $256,000 x 600,000/1,280,000 = $120,000

Depreciation overhead absorption of Product X = $618,000 x 300,000/900,000 = $206,000

Depreciation overhead absorption of Product Y = $618,000 x 600,000/900,000 = $412,000

Related Documents