Chapter 19: Learning Objectives OTHER DEPOSITORY INSITUTIONS & FINANCIAL INSTITUTIONS What are “Near-Banks”? A Brief History of “Near-Banks” Types: Trusts, MLC, and Credit Unions Other depository institutions Performance

Chapter 19: Learning Objectives OTHER DEPOSITORY INSITUTIONS & FINANCIAL INSTITUTIONS What are “Near-Banks”? A Brief History of “Near-Banks” Types: Trusts,

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 19:Learning Objectives OTHER DEPOSITORY INSITUTIONS & FINANCIAL

INSTITUTIONS What are “Near-Banks”? A Brief History of “Near-Banks” Types:

Trusts, MLC, and Credit Unions Other depository institutions

Performance

Learning Objectives (CONT’D)

Other Financial Institutions: What Are They?

Insurance Industry: General Characteristics

Mutual Funds & Pension Funds: General Overview

Government Programs & Incentives

What are the Near Banks?

Trust & Mortgage Loan Cos. Credit Unions and Caisses Populaires Provincially based depository

institutions

Trust & Mortgage Loan Cos.

Offer typical banking type services Estate, Trust, and Agency function

remains most important distinguishing characteristic vis-à-vis Chartered banks

A bit of history: filling the gap left by the Chartered banks

What do their operations look like?

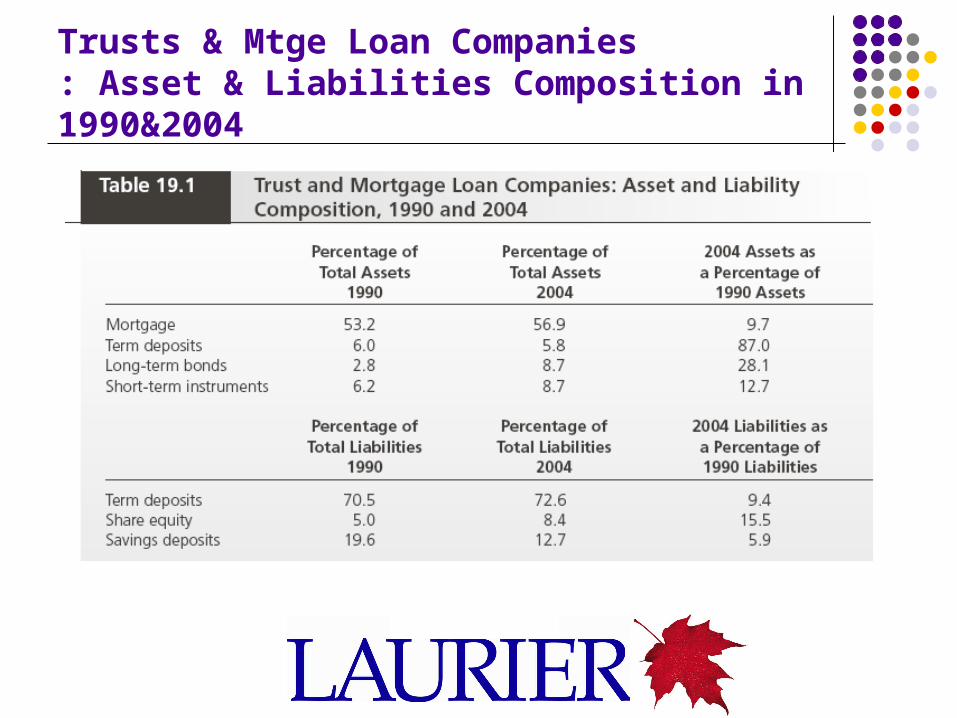

Trusts & Mtge Loan Companies: Asset & Liabilities Composition in 1990&2004

Trust & Mortgage Loans Cos

Credit Unions & Caisses Populaires

Primarily savings type institutions offering a “smorgasboard” of financial and non-financial services

Depositors are also the shareholders A little history: the need to generate a pool of savings in

a community Big changes are underway to merge with other

institutions and to bring in non depositing shareholders

Credit Unions: Asset & Liabilities Composition in 1990 & 2004

Credit Unions: Balance Sheet 2004

Other Financial Institutions

Financial and Leasing Corporations Investment Dealers Government Financial Institutions Insurance Companies Mutual Funds Pension Funds

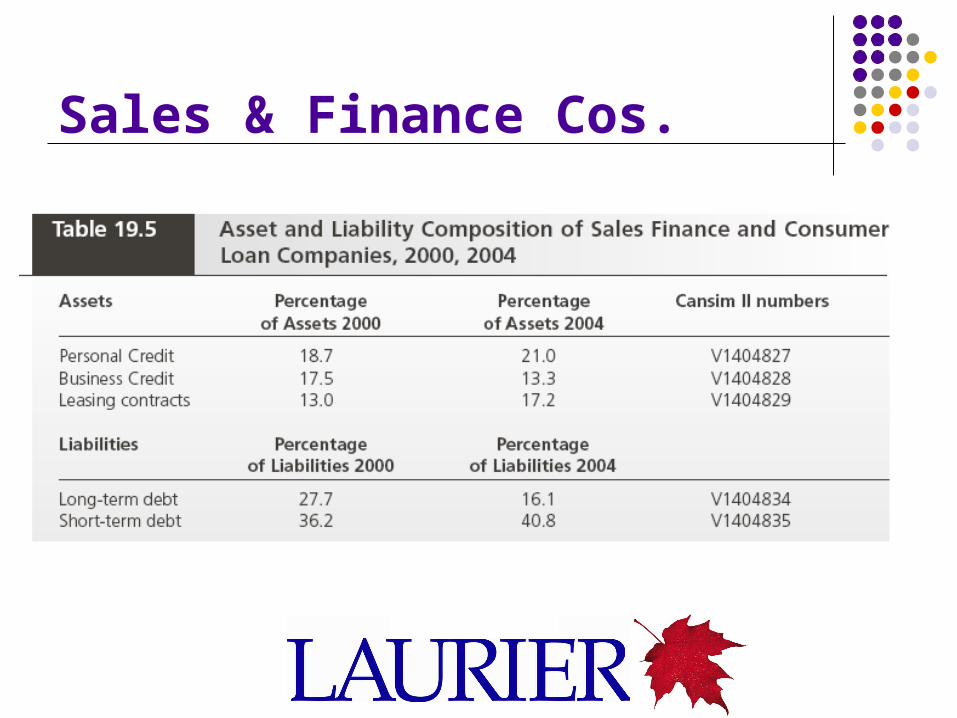

Sales & Finance Cos.

Investment Dealers

Underwrite securities Also act as primary market dealers Since the early 1990s have been largely

bought out by Chartered banks Serious regulatory issues have affected

the industry in the 1990s

Government Financial Institutions

In theory, fill in gaps left behind by the private market either because of risk or low profitability

Examples include: CMHC, FBDB, EDC, FCC

Insurance Companies

Most are federally regulated Separate Acts regulate domestic vs. foreign based

companies There are 2 types of cos.: Joint-stock (shareholder

owned) & mutual cos (policy holder owned). Assets must be sufficient to cover liabilities segregated fund component acts like an intermediary

by offering RRIFs They have their own “protection” fund that acts like

deposit insurance Demutualization is the dominant current trend

The Largest Insurance Cos.

Investment Funds & Cos

Mutual Funds Closed-end (fixed no. of shares) Open-end (no share limit) usually specialize (e.g., bonds, mortgages, etc.)

Mutual Funds and Market Timing

How much is your mutual fund worth? Depends on the time/date used in the calculation of Price X No. of shares If the price used is at 4pm Eastern time then the price is “stale”

by 4:01pm! Stock/bond trading is a 24 hour round the world phenomenon If prices rise in North America they tend to rise in Asia where its

later. There is, therefore, an arbitrage opportunity. How would the investor know that a shares sold between time t

and t+ would earn a profit without their knowledge? Estimates of the returns from market timing? 35 to 70%

annually Not everyone agrees with these estimates + there is also a risk

of loss from the same phenomenon!

Investment Funds & Cos

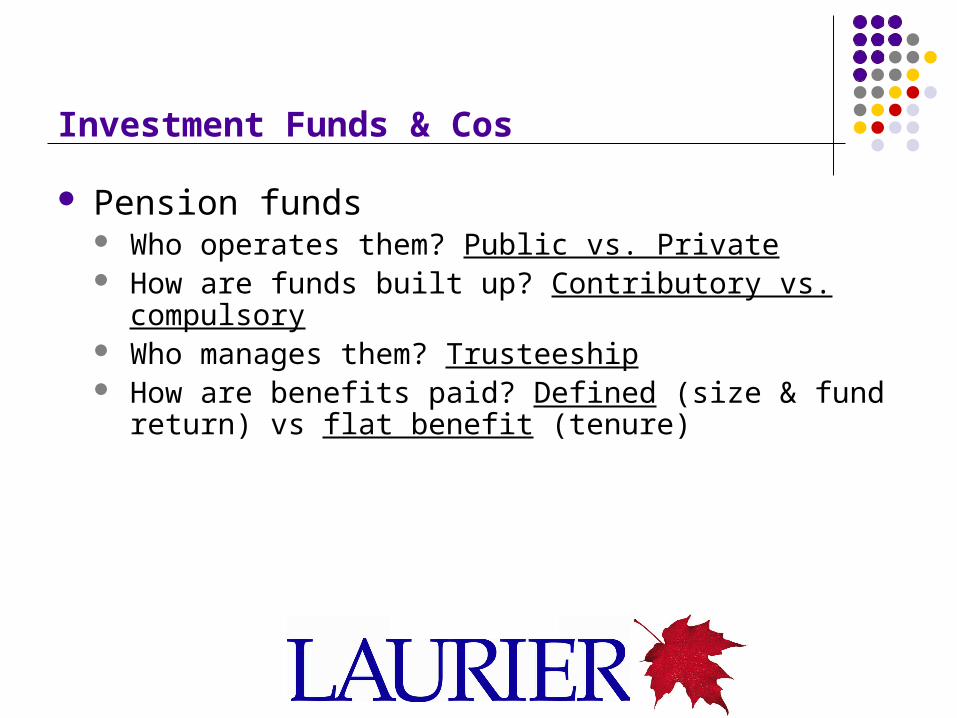

Pension funds Who operates them? Public vs. Private How are funds built up? Contributory vs. compulsory Who manages them? Trusteeship How are benefits paid? Defined (size & fund return)

vs flat benefit (tenure)

The CPP in 2004

Summary

There exist a large variety of public and private institutions which function as intermediaries but are not necessarily deposit-taking institutions

Public institutions attempt to fill a perceived void left by the private market either because risks are too high or anticipated profits too low

Other financial institutions include leasing cos., investment dealers, insurance companies, government financial institutions, mutual and pension funds

Other financial institutions have been termed “near banks” since they offer typical banking type services as well as other financial and non-financial services

The most important such institutions are the Trust&Mortgage Loan Cos. and Credit Unions

They emerged to fill the financial gap left by the Chartered banks but competition and technology are forcing them to change into institutions largely indistinguishable from the Chartered banks

Related Documents