8/28/2019 1 Chapter 18 Process Costing Chapter 18 Learning Objectives 1. Describe the flow of costs through a process costing system 2. Calculate equivalent units of production for direct materials and conversion costs 18-2 © 2018 Pearson Education, Inc. 1 2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/28/2019

1

Chapter 18Process Costing

Chapter 18 Learning Objectives

1. Describe the flow of costs through a process costing system

2. Calculate equivalent units of production for direct materials and conversion costs

18-2© 2018 Pearson Education, Inc.

1

2

8/28/2019

2

Chapter 18 Learning Objectives

3. Prepare a production cost report for the first department using the weighted-average method

4. Prepare a production cost report for subsequent departments using the weighted-average method

18-3© 2018 Pearson Education, Inc.

Chapter 18 Learning Objectives

5. Prepare journal entries for a process costing system

6. Use a production cost report to make decisions

7. Prepare a production cost report using the first-in, first-out method (Appendix 18A)

18-4© 2018 Pearson Education, Inc.

3

4

8/28/2019

3

Learning Objective 1

Describe the flow of costs through a process costing system

18-5© 2018 Pearson Education, Inc.

HOW DO COSTS FLOW THROUGH A PROCESS COSTING SYSTEM?

• Job order costing system– Allocates costs by job– Used by companies that manufacture unique

products or provide specialized services• Process costing system

– Allocates costs by process– Used by companies that manufacture identical

units– Focuses on a process, one of the steps in

manufacturing production

18-6© 2018 Pearson Education, Inc.

5

6

8/28/2019

4

Job Order Costing Versus Process Costing

18-7© 2018 Pearson Education, Inc.

Flow of Costs Through a Process Costing System

18-8© 2018 Pearson Education, Inc.

7

8

8/28/2019

5

Flow of Costs Through a Process Costing System

Suppose the company’s production costs incurred to make 50,000 puzzles and the costs per puzzle are as follows:

18-9© 2018 Pearson Education, Inc.

Flow of Costs Through a Process Costing System

• Companies use process costing to determine the per unit cost in order to:– Control costs– Set sales prices– Calculate account balances for

• Work-in-Process Inventory• Finished Goods Inventory• Cost of Goods Sold

18-10© 2018 Pearson Education, Inc.

9

10

8/28/2019

6

18-11© 2018 Pearson Education, Inc.

Learning Objective 2

Calculate equivalent units of production for direct materials and conversion costs

18-12© 2018 Pearson Education, Inc.

11

12

8/28/2019

7

WHAT ARE EQUIVALENT UNITS OF PRODUCTION, AND HOW ARE THEY

CALCULATED?

18-13© 2018 Pearson Education, Inc.

• Companies may have products still in process at the end of the accounting period.

• The total production costs incurred in each process must be split between the following:– The units that have been completed in that

process and transferred to the next process.– The units not completed and remaining in

Work-in-Process Inventory.

WHAT ARE EQUIVALENT UNITS OF PRODUCTION, AND HOW ARE THEY

CALCULATED?

18-14© 2018 Pearson Education, Inc.

13

14

8/28/2019

8

Equivalent Units of Production

• Equivalent units of production (EUP)– Measures the amount of materials added to or

work done on partially completed units during a period

– Expressed in terms of fully complete units of output

• Conversion costs are the sum of direct labor and manufacturing overhead costs and represent the cost to convert direct materials into finished goods.

18-15© 2018 Pearson Education, Inc.

Equivalent Units of Production

• Assume Puzzle Me has 40,000 units that the Assembly Department completed and transferred out.

• Therefore, for units complete and transferred out the equivalent units would be 40,000 units (40,000 units * 100% complete) for both direct materials and conversion costs.

18-16© 2018 Pearson Education, Inc.

15

16

8/28/2019

9

Equivalent Units of Production

• Puzzle Me has 10,000 units in ending Work-in-Process Inventory that are 100% complete with respect to direct materials cost and 25% completed with respect to conversion costs.

• The equivalent units in ending Work-in-Process Inventory in terms of direct materials:

• The equivalent units in ending Work-in-Process Inventory in terms of conversion costs:

18-17© 2018 Pearson Education, Inc.

Learning Objective 3

Prepare a production cost report for the first department using the weighted-average method

18-18© 2018 Pearson Education, Inc.

17

18

8/28/2019

10

HOW IS A PRODUCTION COST REPORT PREPARED FOR THE FIRST DEPARTMENT?

18-19© 2018 Pearson Education, Inc.

• A production cost report shows the calculations for the physical flows and the cost flows of the products.

• Preparing this report involves four steps:

1. Summarize the flow of physical units.2. Compute output in terms of equivalent units of

production.3. Compute the cost per equivalent unit of production.4. Assign costs to units completed and units in process.

18-20© 2018 Pearson Education, Inc.

HOW IS A PRODUCTION COST REPORT PREPARED FOR THE FIRST DEPARTMENT?

19

20

8/28/2019

11

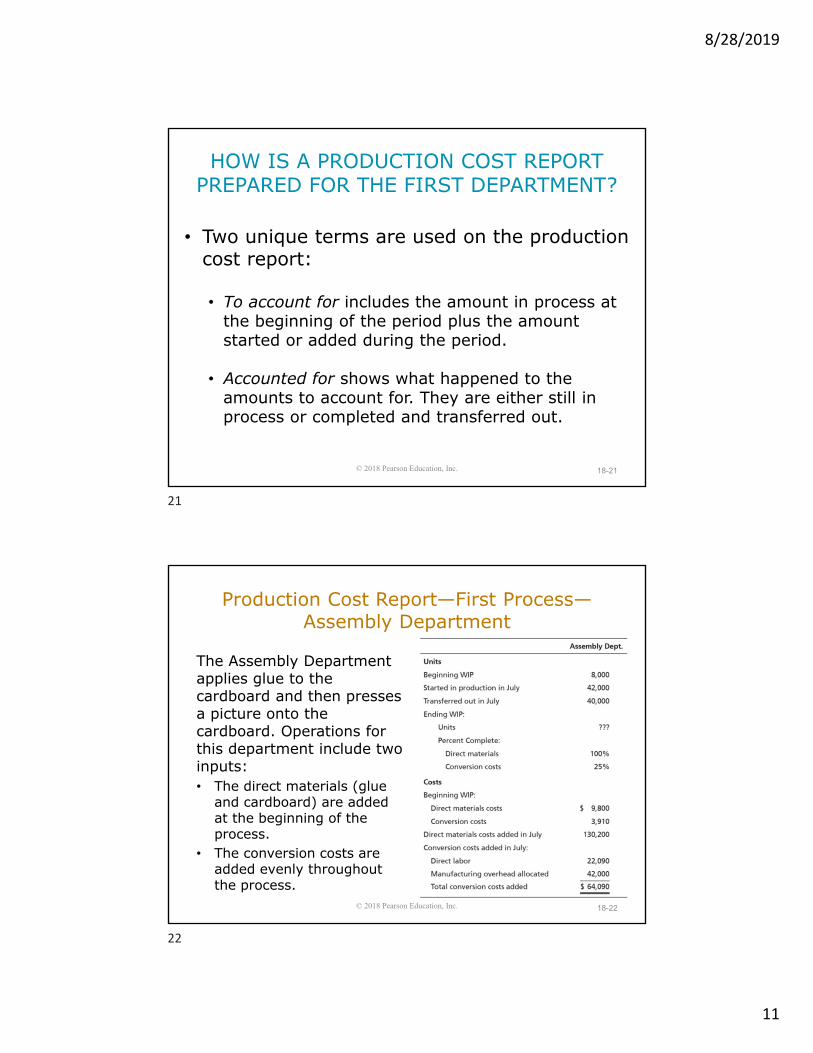

• Two unique terms are used on the production cost report:

• To account for includes the amount in process at the beginning of the period plus the amount started or added during the period.

• Accounted for shows what happened to the amounts to account for. They are either still in process or completed and transferred out.

18-21© 2018 Pearson Education, Inc.

HOW IS A PRODUCTION COST REPORT PREPARED FOR THE FIRST DEPARTMENT?

18-22© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

The Assembly Department applies glue to the cardboard and then presses a picture onto the cardboard. Operations for this department include two inputs:• The direct materials (glue

and cardboard) are added at the beginning of the process.

• The conversion costs are added evenly throughout the process.

21

22

8/28/2019

12

18-23© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 1: Summarize the Flow of Physical Units The physical units are the actual units that the company will account for during the period. The Assembly Department had 8,000 units in process on July 1 and started 42,000 units during the month.

18-24© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

23

24

8/28/2019

13

18-25© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 2: Compute Output in Terms of Equivalent Units of Production The Assembly Department adds all direct materials at the beginning of the process.

Equivalent Units of Production for Direct Materials:

18-26© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 2: Compute Output in Terms of Equivalent Units of Production The Assembly Department incurs conversion costs evenly throughout the process.

Equivalent Units of Production for Conversion Costs:

25

26

8/28/2019

14

18-27© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

18-28© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 3: Compute the Cost per Equivalent Unit of ProductionThe Assembly Department has to account for costs associated with the following:• Work done last month on the 8,000 partially

completed units (beginning work-in-process)• Work done this month to complete the 8,000 partially

completed units• Work done this month on the 42,000 units that were

started into production

27

28

8/28/2019

15

18-29© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 3: Compute the Cost per Equivalent Unit of Production• The weighted-average method combines the

beginning work-in-process costs and the costs added during the period into one cost pool.

• A cost pool is an accumulation of individual costs. • The total costs to be accounted for include direct

materials and conversion costs and will be calculated as beginning work-in-process costs plus costs added during the period.

18-30© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 3: Compute the Cost per Equivalent Unit of Production

29

30

8/28/2019

16

18-31© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 3: Compute the Cost per Equivalent Unit of Production

18-32© 2018 Pearson Education, Inc.

31

32

8/28/2019

17

18-33© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 4: Assign Costs to Units Completed and Units in ProcessThe costs must be divided between two outputs:• The 40,000 completed puzzle boards that have been

transferred out to the Cutting Department.• The 10,000 partially completed puzzle boards

remaining in the Assembly Department’s ending Work-in-Process Inventory.

This is accomplished by multiplying the cost per equivalent unit of production (Step 3) by the equivalent units of production (Step 2).

18-34© 2018 Pearson Education, Inc.

Production Cost Report—First Process—Assembly Department

Step 4: Assign Costs to Units Completed and Units in Process

33

34

8/28/2019

18

18-35© 2018 Pearson Education, Inc.

Learning Objective 4

Prepare a production cost report for subsequent departments using the weighted-average method

18-36© 2018 Pearson Education, Inc.

35

36

8/28/2019

19

• The Cutting Department receives the puzzle boards from the Assembly Department and cuts the boards into puzzle pieces before inserting the pieces into the box at the end of the process. – Glued puzzle boards with pictures are transferred

in from the Assembly Department at the beginning of the Cutting Department’s process.

– The Cutting Department’s conversion costs are added evenly throughout the process.

– The Cutting Department’s direct materials are added at the end of the process.

18-37© 2018 Pearson Education, Inc.

Production Cost Report—Second Process—Cutting Department

18-38© 2018 Pearson Education, Inc.

Production Cost Report—

Second Process—Cutting Department

Transferred in costs are costs that were incurred in a previous process and brought into a later process as part of the product’s cost.

37

38

8/28/2019

20

18-39© 2018 Pearson Education, Inc.

Step 1: Summarize the Flow of Physical Units The Cutting Department has 5,000 units in process on July 1 and receives 40,000 units during the month from the Assembly Department.

The Cutting Department completes the cutting and boxing process on 38,000 of the 45,000 units to account for and transfers those units to Finished Goods Inventory.

Production Cost Report—Second Process—Cutting Department

18-40© 2018 Pearson Education, Inc.

Production Cost Report—Second Process—Cutting Department

39

40

8/28/2019

21

18-41© 2018 Pearson Education, Inc.

Step 2: Compute Output in Terms of Equivalent Units of Production The Cutting Department starts with the units transferred in from the Assembly Department. The equivalent units of production for transferred in are always 100%.

Equivalent Units of Production for Transferred In:

Production Cost Report—Second Process—Cutting Department

18-42© 2018 Pearson Education, Inc.

Step 2: Compute Output in Terms of Equivalent Units of Production The Cutting Department adds direct materials at the end of the process.

Equivalent Units of Production for Direct Materials:

Production Cost Report—Second Process—Cutting Department

41

42

8/28/2019

22

18-43© 2018 Pearson Education, Inc.

Step 2: Compute Output in Terms of Equivalent Units of Production The Cutting Department incurs conversion costs evenly throughout the process.

Equivalent Units of Production for Conversion Costs:

Production Cost Report—Second Process—Cutting Department

18-44© 2018 Pearson Education, Inc.

Production Cost Report—Second Process—Cutting Department

43

44

8/28/2019

23

18-45© 2018 Pearson Education, Inc.

Step 3: Compute the Cost per Equivalent Unit of ProductionThe Cutting Department has three inputs and therefore must make three calculations for cost per equivalent unit of production.

Production Cost Report—Second Process—Cutting Department

18-46© 2018 Pearson Education, Inc.

Step 3: Compute the Cost per Equivalent Unit of Production

Production Cost Report—Second Process—Cutting Department

45

46

8/28/2019

24

18-47© 2018 Pearson Education, Inc.

Step 3: Compute the Cost per Equivalent Unit of Production

Production Cost Report—Second Process—Cutting Department

18-48© 2018 Pearson Education, Inc.

47

48

8/28/2019

25

18-49© 2018 Pearson Education, Inc.

Step 4: Assign Costs to Units Completed and Units in ProcessThe $233,040 total costs accounted for by the Cutting Department should be assigned to the following:• The 38,000 completed puzzles that have been

transferred out to Finished Goods Inventory• The 7,000 partially completed puzzle boards

remaining in the Cutting Department’s ending Work-in-Process Inventory

Production Cost Report—Second Process—Cutting Department

18-50© 2018 Pearson Education, Inc.

Step 4: Assign Costs to Units Completed and Units in Process

Production Cost Report—Second Process—Cutting Department

49

50

8/28/2019

26

18-51© 2018 Pearson Education, Inc.

Learning Objective 5

Prepare journal entries for a process costing system

18-52© 2018 Pearson Education, Inc.

51

52

8/28/2019

27

WHAT JOURNAL ENTRIES ARE REQUIRED IN A PROCESS COSTING SYSTEM?

• Costs flow through the process costing system in four steps:1. Accumulate2. Assign3. Allocate4. Adjust

• Costs flow from one Work-in-Process Inventory account to the next and eventually to Finished Goods Inventory and Cost of Goods Sold.

18-53© 2018 Pearson Education, Inc.

Transaction 1—Raw Materials Purchased

18-54

During July, the company purchases materials on account for $175,000.

© 2018 Pearson Education, Inc.

53

54

8/28/2019

28

Transaction 2—Raw Materials Used in Production

18-55

During July, Puzzle Me assigns direct materials to the two production departments: $130,200 to the Assembly Department and $19,000 to the Cutting Department; $2,000 in indirect materials is accumulated in Manufacturing Overhead.

© 2018 Pearson Education, Inc.

Transaction 3—Labor Costs Incurred

18-56

During the month, Puzzle Me assigns $22,090 in direct labor costs to the Assembly Department and $3,840 in direct labor costs to the Cutting Department. $1,500 in indirect labor costs are accumulated in Manufacturing Overhead.

© 2018 Pearson Education, Inc.

55

56

8/28/2019

29

Transaction 4—Additional Manufacturing Costs Incurred

18-57

Puzzle Me incurs $30,000 in machinery depreciation and $19,000 in indirect costs that were paid in cash. These costs are accumulated in the Manufacturing Overhead account.

© 2018 Pearson Education, Inc.

Transaction 5—Allocation ofManufacturing Overhead

18-58

Puzzle Me uses a predetermined overhead allocation rate to allocate indirect costs to the departments: $42,000 to the Assembly Department and $11,000 to the Cutting Department.

© 2018 Pearson Education, Inc.

57

58

8/28/2019

30

Transaction 6—Transfer from the Assembly Department to the Cutting Department

18-59

At the end of July, when the production cost report for the Assembly Department is prepared, Puzzle Me assigns $176,000 to the 40,000 units transferred from the Assembly Department to the Cutting Department.

© 2018 Pearson Education, Inc.

Transaction 7—Transfer from Cutting Department to Finished Goods Inventory

18-60

At the end of July, when the production cost report for the Cutting Department is prepared, Puzzle Me assigns $201,400 to the 38,000 units transferred from the Cutting Department to Finished Goods Inventory. This is the cost of goods manufactured.

© 2018 Pearson Education, Inc.

59

60

8/28/2019

31

Transaction 8—Puzzles SoldDuring July, Puzzle Me sells 35,000 puzzles. The total production cost of manufacturing a puzzle is $5.30. The cost of 35,000 puzzles is $185,500 (35,000 puzzles × $5.30 per puzzle). The puzzles are sold on account for $8.00 each, which is a total of $280,000 (35,000 puzzles × $8.00 per puzzle).

© 2018 Pearson Education, Inc. 18-61

Transaction 9—Adjust Manufacturing Overhead

The actual manufacturing overhead costs incurred are $50,500. The amount of manufacturing overhead allocated to the two departments is $53,000.

© 2018 Pearson Education, Inc. 18-62

61

62

8/28/2019

32

Transaction 9—Adjust Manufacturing Overhead

© 2018 Pearson Education, Inc. 18-63

© 2018 Pearson Education, Inc. 18-64

WHAT JOURNAL ENTRIES ARE REQUIRED IN A PROCESS COSTING SYSTEM?

63

64

8/28/2019

33

Learning Objective 6

Use a production cost report to make decisions

18-65© 2018 Pearson Education, Inc.

HOW CAN THE PRODUCTION COST REPORT BE USED TO MAKE DECISIONS?

• Controlling costs• Evaluating performance• Pricing products• Identifying the most profitable products• Preparing the financial statements

18-66© 2018 Pearson Education, Inc.

65

66

8/28/2019

34

Learning Objective 7

Prepare a production cost report using the first-in, first-out method (Appendix 18A)

18-67© 2018 Pearson Education, Inc.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

• Equivalent unit of production cost methods:– Weighted-average method– First-in, first-out

• The first-in, first-out method (for Process Costing) determines the cost of equivalent units by accounting for beginning inventory separately.

18-68© 2018 Pearson Education, Inc.

67

68

8/28/2019

35

18-69© 2018 Pearson Education, Inc.

HOW IS A PRODUCTION COST REPORT

PREPARED USING THE FIFO METHOD?

The data related to Puzzle Me’s Assembly Department is shown to the left.

18-70© 2018 Pearson Education, Inc.

Step 1: Summarize the Flow of Physical Units The Assembly Department has 8,000 units in process on July 1 and starts 42,000 units during the month. Therefore, to account for is 50,000 units. This is the same as in the weighted-average method.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

69

70

8/28/2019

36

18-71© 2018 Pearson Education, Inc.

Step 1: Summarize the Flow of Physical UnitsIf 40,000 units are completed and transferred, this includes the 8,000 units in beginning inventory plus another 32,000 units started in July. We must account for 50,000 units. If 40,000 are transferred out, then that leaves 10,000 still in process at the end of July.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

18-72© 2018 Pearson Education, Inc.

Step 1: Summarize the Flow of Physical Units

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

71

72

8/28/2019

37

18-73© 2018 Pearson Education, Inc.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

18-74© 2018 Pearson Education, Inc.

Step 2: Compute Output in Terms of Equivalent Units of ProductionThe Assembly Department adds direct materials at the beginning of the process.

Equivalent Units of Production for Direct Materials:

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

73

74

8/28/2019

38

18-75© 2018 Pearson Education, Inc.

Step 2: Compute Output in Terms of Equivalent Units of ProductionThe Assembly Department incurs conversion costs evenly throughout the process.

Equivalent Units of Production for Conversion Costs:

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

18-76© 2018 Pearson Education, Inc.

Step 2: Compute Output in Terms of Equivalent Units of Production

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

75

76

8/28/2019

39

18-77© 2018 Pearson Education, Inc.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

18-78© 2018 Pearson Education, Inc.

Step 3: Compute the Cost per Equivalent Unit of ProductionThe Assembly Department has $208,000 of costs to account for.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

77

78

8/28/2019

40

18-79© 2018 Pearson Education, Inc.

Step 3: Compute the Cost per Equivalent Unit of Production

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

18-80© 2018 Pearson Education, Inc.

79

80

8/28/2019

41

18-81© 2018 Pearson Education, Inc.

Step 4: Assign Costs to Units Completed and Units in ProcessThe $208,000 total costs must be assigned to:• The 8,000 puzzle boards from beginning inventory

that have now been completed and transferred to the Cutting Department.

• The 32,000 started and completed puzzle boards that have also been transferred to Cutting Department.

• The 10,000 partially completed puzzle boards remaining in the Assembly Department’s ending Work-in-Process Inventory.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

18-82© 2018 Pearson Education, Inc.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

81

82

8/28/2019

42

18-83© 2018 Pearson Education, Inc.

18-84© 2018 Pearson Education, Inc.

83

84

8/28/2019

43

Comparison of Weighted-Average and FIFO Methods

Notice the differences in the completed and transferred out costs and ending work-in-process costs under each method.

18-85© 2018 Pearson Education, Inc.

18-86© 2018 Pearson Education, Inc.

85

86

Related Documents