Chapter 15 Principles Principles of of Corporate Corporate Finance Finance Tenth Edition How Corporations Issue Securities Slides by Matthew Will Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved McGraw Hill/Irwin

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 15 PrinciplesPrinciples

ofof

CorporateCorporate

FinanceFinance

Tenth Edition

How Corporations Issue Securities

Slides by

Matthew Will

Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved

McGraw Hill/Irwin

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 2

McGraw Hill/Irwin

Topics Covered

Venture CapitalThe Initial Public OfferingOther New-Issue ProceduresSecurity Sales by Public Companies

– Rights Issue

Private Placements and Public Issues

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 3

McGraw Hill/Irwin

Venture Capital

Since success of a new firm is highly dependent on the effort of the managers, restrictions are placed on management by the venture capital company and funds are usually dispersed in stages, after a certain level of success is achieved.

Venture Capital

Money invested to finance a new firm

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 4

McGraw Hill/Irwin

Venture Capital

2.0Value2.0Value

1.0equity originalYour 1.0assetsOther

1.0capital venturefromequity New 1.0equitynew from Cash

Equityand sLiabilitieAssets

($mil)Sheet BalanceValue Market StageFirst

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 5

McGraw Hill/Irwin

Venture Capital

14.0Value14.0Value

5.0equity originalYour 9.0assetsOther

5.0stage1st fromEquity 1.0assets Fixed

4.0stage 2nd fromequity New 4.0equitynew from Cash

Equityand sLiabilitieAssets

($mil)Sheet BalanceValue Market Stage Second

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 6

McGraw Hill/Irwin

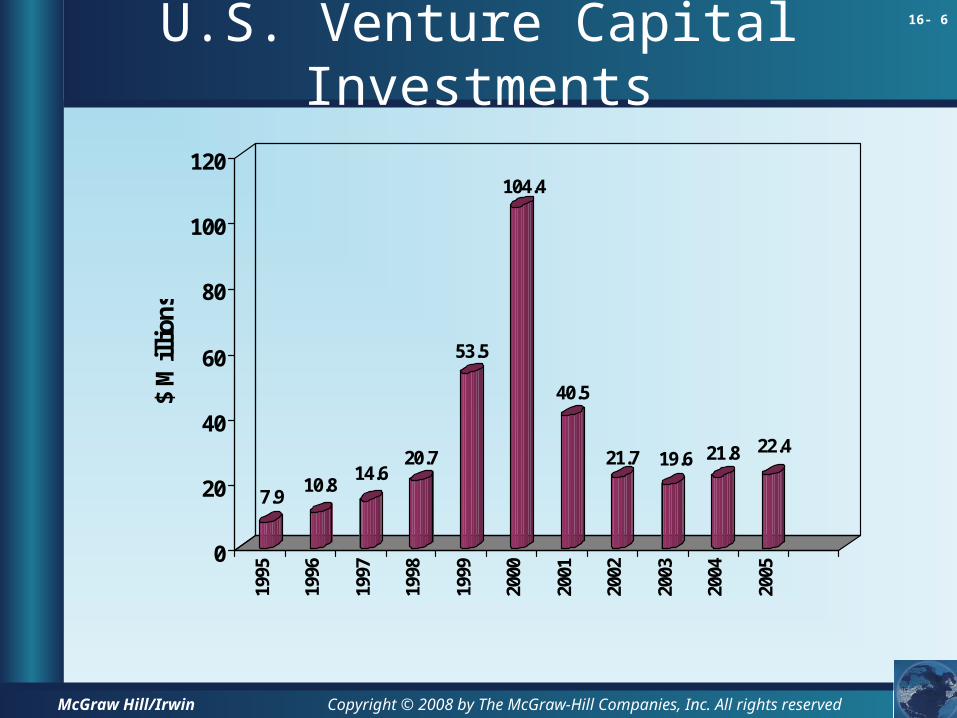

U.S. Venture Capital Investments

7.910.8

14.620.7

53.5

104.4

40.5

21.7 19.6 21.8 22.4

0

20

40

60

80

100

120$

Mil

lion

s

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 7

McGraw Hill/Irwin

Initial Offering

Initial Public Offering (IPO) - First offering of stock to the general public.

Underwriter - Firm that buys an issue of securities from a company and resells it to the public.

Spread - Difference between public offer price and price paid by underwriter.

Prospectus - Formal summary that provides information on an issue of securities.

Underpricing - Issuing securities at an offering price set below the true value of the security.

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 8

McGraw Hill/Irwin

Motives For An IPO

Percent of CFOs who strongly agree with the reason for an IPO

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 9

McGraw Hill/Irwin

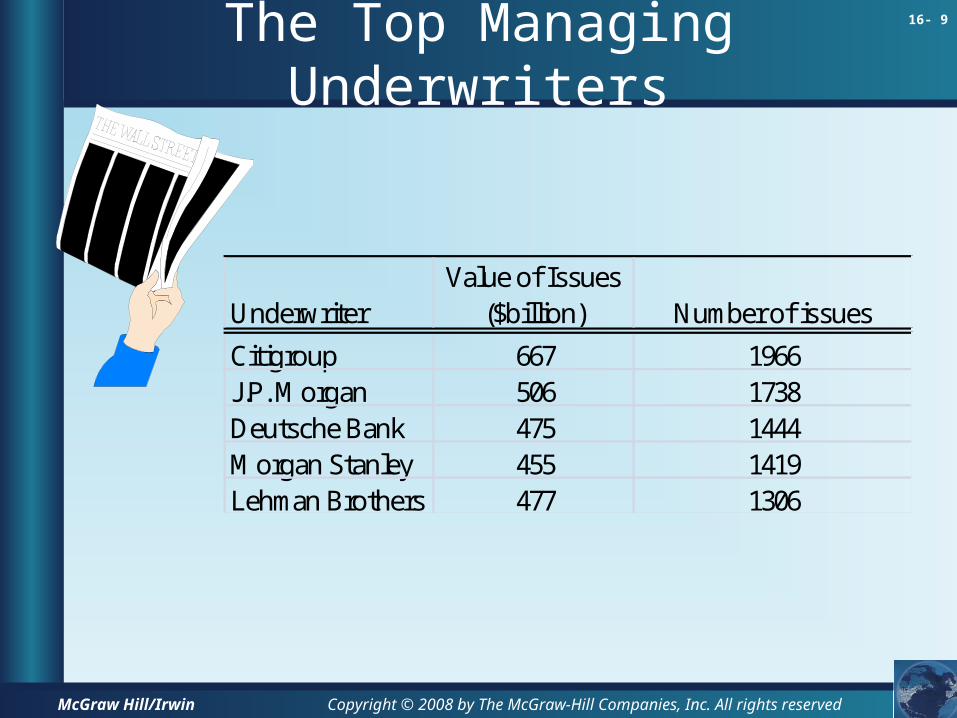

The Top Managing Underwriters

UnderwriterValue of Issues

($billion) Number of issues

Citigroup 667 1966J.P. Morgan 506 1738Deutsche Bank 475 1444Morgan Stanley 455 1419Lehman Brothers 477 1306

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 10

McGraw Hill/Irwin

Average Initial IPO Returns

0 20 40 60 80 100

return (percent)

DenmarkCanadaNetherlandsSpainTurkeyFranceAustraliaNorwayHong KongUKUSAItalyJapanSingaporeSwedenTaiwanGermanySwitzerlandKoreaBrazilIndiaChina

256 %

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 11

McGraw Hill/Irwin

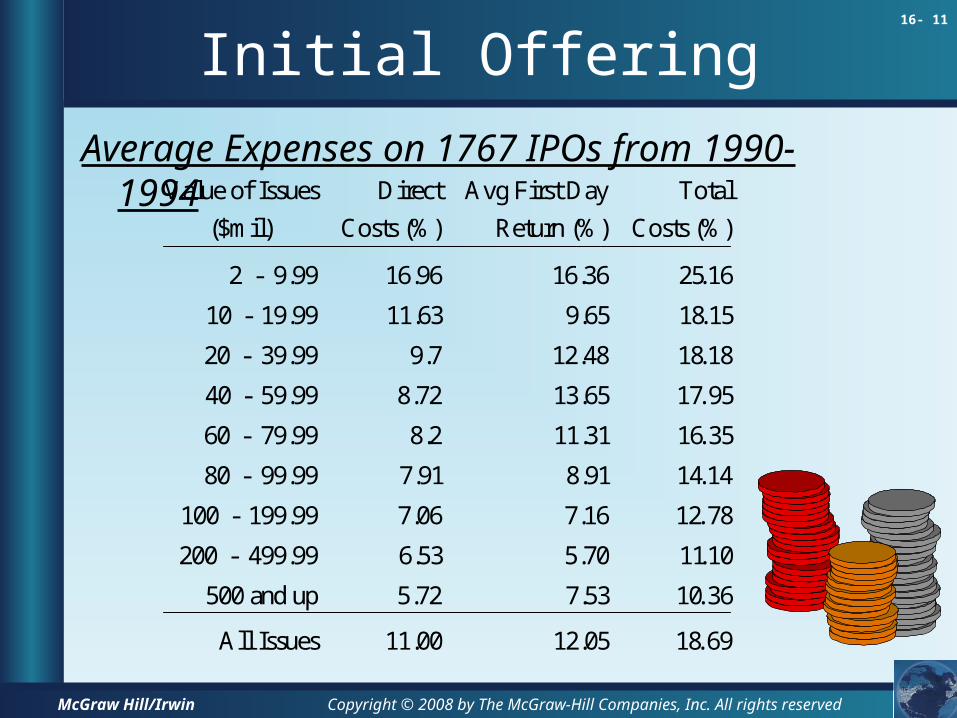

Initial Offering

Average Expenses on 1767 IPOs from 1990-1994Value of Issues

($mil)

Direct

Costs (%)

Avg First Day

Return (%)

Total

Costs (%)

2 - 9.99 16.96 16.36

10 - 19.99 11.63 9.65

20 - 39.99 9.7 12.48

40 - 59.99 8.72 13.65

60 - 79.99 8.2 11.31

80 - 99.99 7.91 8.91

100 - 199.99 7.06 7.16

200 - 499.99 6.53 5.70

500 and up 5.72 7.53

All Issues 11.00 12.05

25 16

18 15

18 18

17 95

16 35

14 14

12 78

11 10

10 36

18 69

.

.

.

.

.

.

.

.

.

.

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 12

McGraw Hill/Irwin

IPO Proceeds

IPO Proceeds and First Day Returns

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 13

McGraw Hill/Irwin

General Cash Offers

Seasoned Offering - Sale of securities by a firm that is already publicly traded.

General Cash Offer - Sale of securities open to all investors by an already public company.

Shelf Registration - A procedure that allows firms to file one registration statement for several issues of the same security.

Private Placement - Sale of securities to a limited number of investors without a public offering.

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 14

McGraw Hill/Irwin

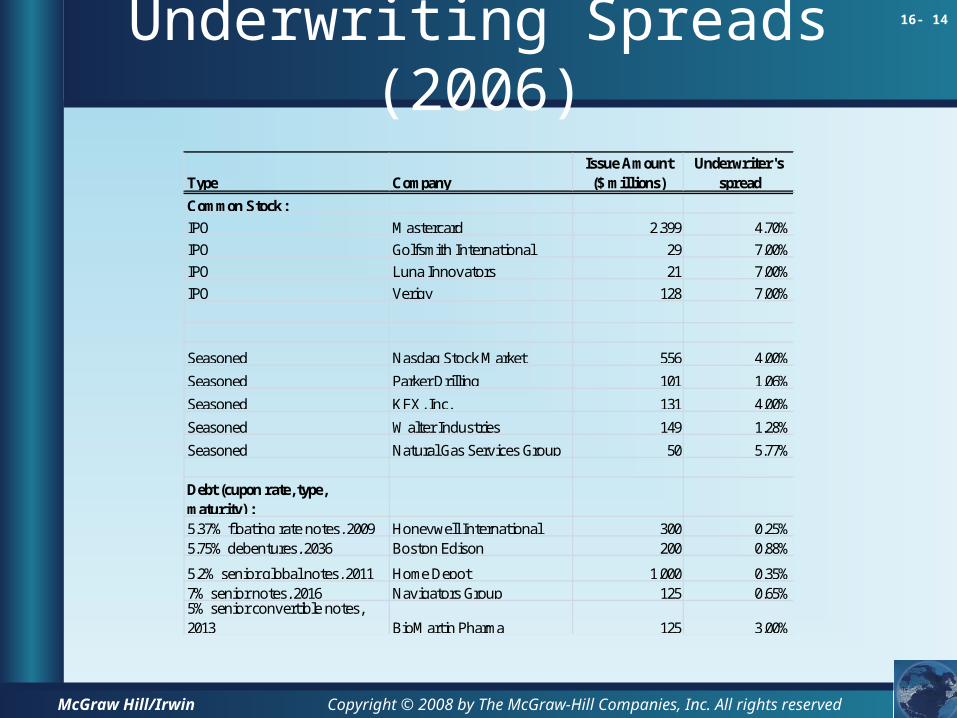

Underwriting Spreads (2006)

Type CompanyIssue Amount ($ millions)

Underwriter's spread

Common Stock:

IPO Mastercard 2,399 4.70%

IPO Golfsmith International 29 7.00%

IPO Luna Innovators 21 7.00%

IPO Verigy 128 7.00%

Seasoned Nasdaq Stock Market 556 4.00%

Seasoned Parker Drilling 101 1.06%

Seasoned KFX, Inc. 131 4.00%

Seasoned Walter Industries 149 1.28%

Seasoned Natural Gas Services Group 50 5.77%

Debt (cupon rate, type, maturity) :5.37% floating rate notes, 2009 Honeywell International 300 0.25%5.75% debentures, 2036 Boston Edison 200 0.88%

5.2% senior global notes, 2011 Home Depot 1,000 0.35%7% senior notes, 2016 Navigators Group 125 0.65%5% senior convertible notes, 2013 BioMartin Pharma 125 3.00%

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 15

McGraw Hill/Irwin

Rights Issue

Rights Issue - Issue of securities offered only to current stockholders.

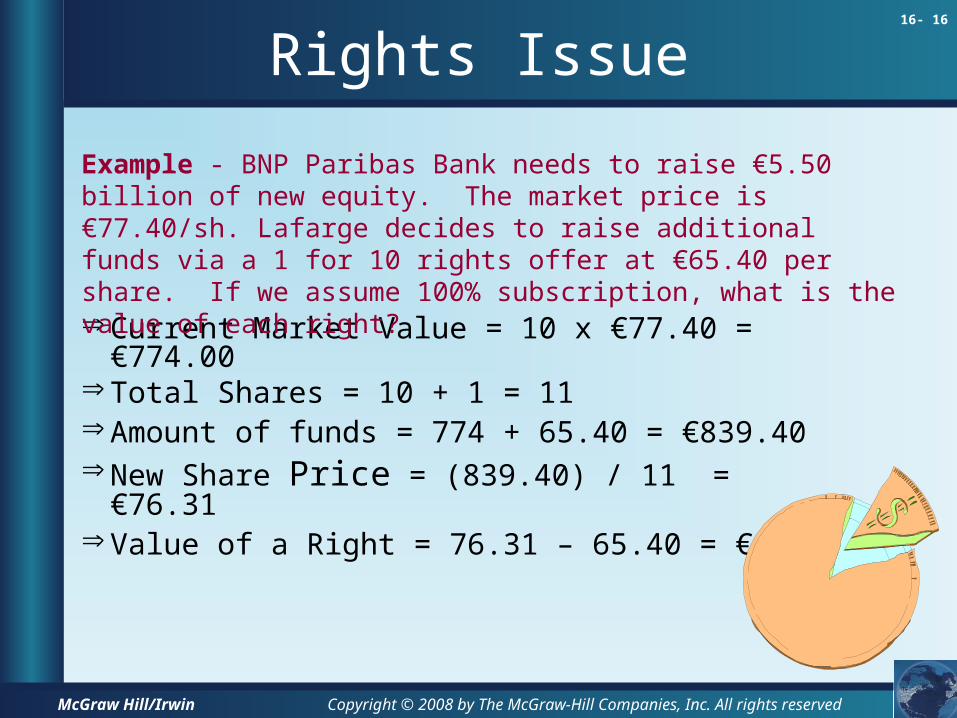

Example – BNP Paribas Bank needs to raise €5.50 billion of new equity. The market price is €77.40/sh. Lafarge decides to raise additional funds via a 1 for 10 rights offer at €65.40 per share. If we assume 100% subscription, what is the value of each right?

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 16

McGraw Hill/Irwin

Rights Issue

Current Market Value = 10 x €77.40 = €774.00 Total Shares = 10 + 1 = 11 Amount of funds = 774 + 65.40 = €839.40 New Share Price = (839.40) / 11 = €76.31 Value of a Right = 76.31 – 65.40 = €10.91

Example - BNP Paribas Bank needs to raise €5.50 billion of new equity. The market price is €77.40/sh. Lafarge decides to raise additional funds via a 1 for 10 rights offer at €65.40 per share. If we assume 100% subscription, what is the value of each right?

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 17

McGraw Hill/Irwin

Rights Issue

Slightly More Difficult Example

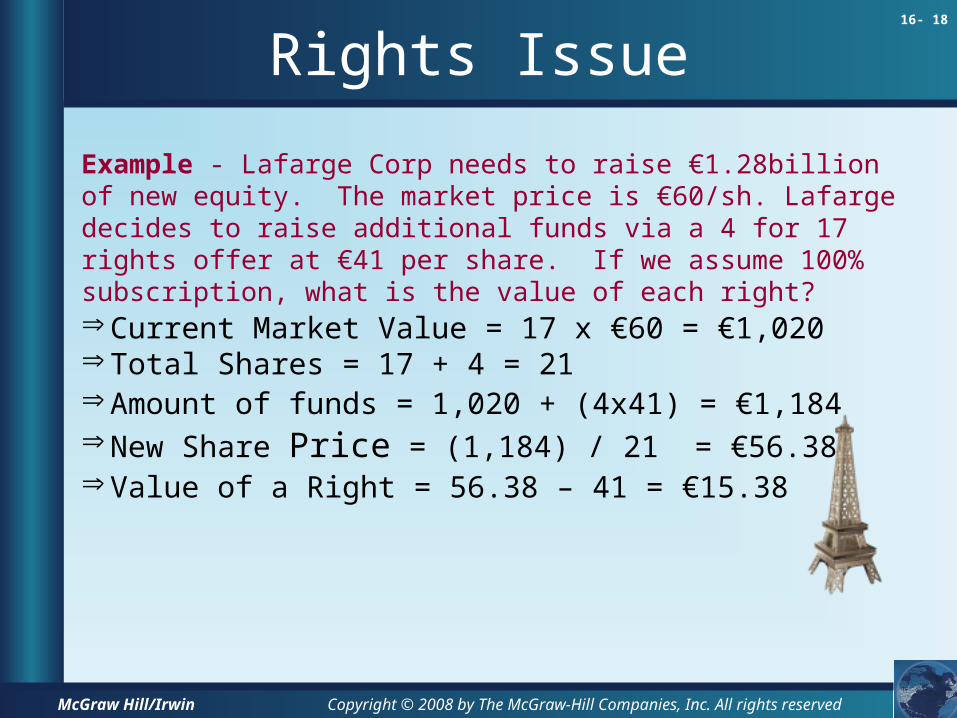

Lafarge Corp needs to raise €1.28billion of new equity. The market price is €60/sh. Lafarge decides to raise additional funds via a 4 for 17 rights offer at €41 per share. If we assume 100% subscription, what is the value of each right?

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 18

McGraw Hill/Irwin

Rights Issue

Current Market Value = 17 x €60 = €1,020 Total Shares = 17 + 4 = 21 Amount of funds = 1,020 + (4x41) = €1,184 New Share Price = (1,184) / 21 = €56.38 Value of a Right = 56.38 – 41 = €15.38

Example - Lafarge Corp needs to raise €1.28billion of new equity. The market price is €60/sh. Lafarge decides to raise additional funds via a 4 for 17 rights offer at €41 per share. If we assume 100% subscription, what is the value of each right?

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

16- 19

McGraw Hill/Irwin

Web Resources

www.redherring.com

www.nvca.org

www.evca.com

www.asianfn.com

www.ventureeconomics.com

www.pwcmoneytree.com

www.v1.com

www.vnpartners.com/primer.htm

Click to access web sitesClick to access web sites

Internet connection requiredInternet connection required

Related Documents