Copyright © 2009 Pearson Prentice Hall. All rights reserved. Chapter 15 Capital Structure

Chapter 15: Capital Structures

Oct 19, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2009 Pearson Prentice Hall. All rights reserved.

Chapter 15

Capital Structure

15-

Chapter Outline

15.1 Capital Structure Choices 15.2 Capital Structure in Perfect Capital Markets15.3 Debt and Taxes15.4 Costs of Bankruptcy and Financial Distress15.5 Optimal Capital Structure: The Tradeoff Theory15.6 Additional Consequences of Leverage: Agency Costs

and Information15.7 Capital Structure: Putting It All Together

15-

Learning Objectives

• Examine how capital structures vary across industries and companies• Understand why investment decisions, rather than financing decisions, fundamentally

determine the value and cost of capital of the firm• Describe how leverage increases the risk of the firm’s equity• Demonstrate how debt can affect firm value through taxes and bankruptcy costs• Show how the optimal mix of debt and equity trades off the costs (including financial

distress costs) and benefits (including the tax advantage) of debt• Analyze how debt can alter the incentives of managers to choose different projects and

can be used as a signal to investors• Weigh the many costs and benefits to debt that a manager must balance when deciding

how to finance the firm’s investments

15-

15.1 Capital Structure Choices

• The collection of securities a firm issues to raise capital from investors is called the firm’s capital structure.

• When raising funds from outside investors, a firm must choose what type of security to issue and what capital structure to have.

15-

15.1 Capital Structure Choices

• Firms consider whether the securities issued:w Will receive a fair price in the market

w Have tax consequences

w Entail transactions costs

w Change its future investment opportunities

15-

15.1 Capital Structure Choices

• A firm’s debt-to-value ratio D / (E+D) is the fraction of the firm’s total value that

corresponds to debt

Figure 15.1 Debt-to-Value Ratio [D/(E + D)] for Select Industries

15-

Figure 15.2 Capital Structures of Blockbuster and Netflix

15-

15.2 Capital Structure in Perfect Capital Markets

• A perfect capital market is a market in which:w Securities are fairly priced

w No tax consequences or transactions costs

w Investment cash flows are independent of financing choices

15-

15.2 Capital Structure in Perfect Capital Markets

• Unlevered equity: equity in a firm with no debt• Levered equity: equity in a firm that has debt

outstanding• Leverage will increase the risk of the firm’s

equity and raise its equity cost of capital

15-

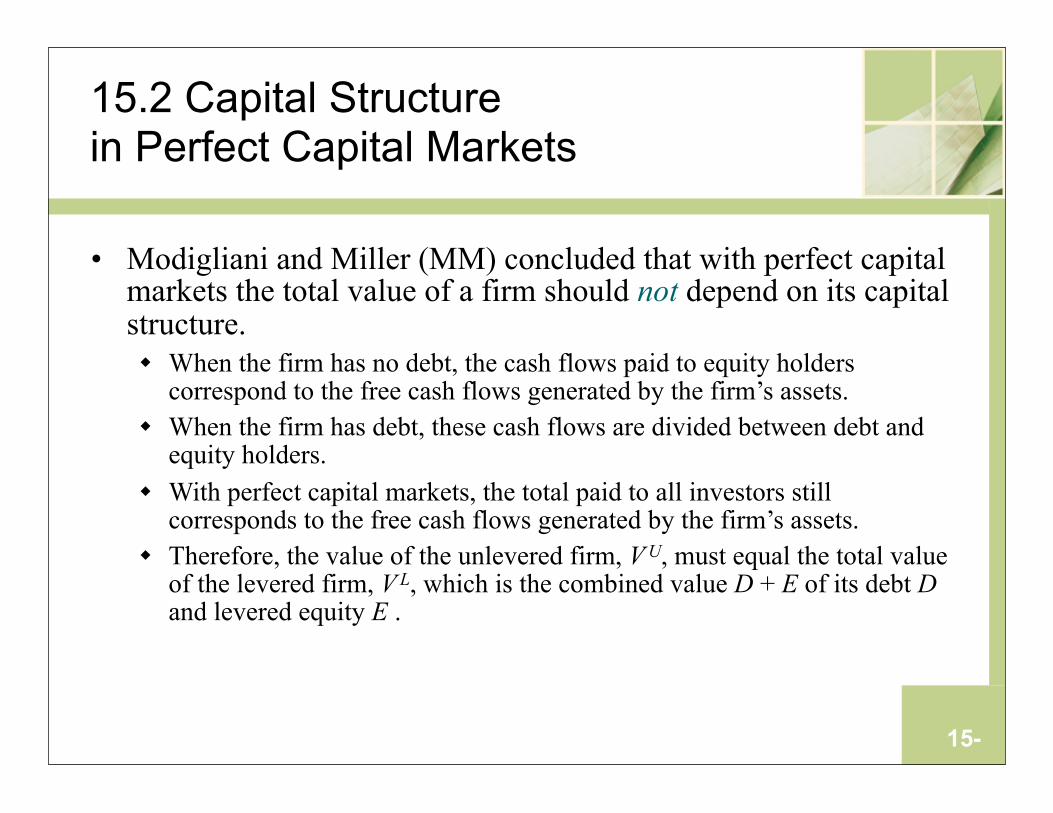

15.2 Capital Structure in Perfect Capital Markets

• Modigliani and Miller (MM) concluded that with perfect capital markets the total value of a firm should not depend on its capital structure.w When the firm has no debt, the cash flows paid to equity holders

correspond to the free cash flows generated by the firm’s assets. w When the firm has debt, these cash flows are divided between debt and

equity holders. w With perfect capital markets, the total paid to all investors still

corresponds to the free cash flows generated by the firm’s assets. w Therefore, the value of the unlevered firm, V U, must equal the total value

of the levered firm, V L, which is the combined value D + E of its debt D and levered equity E .

15-

Figure 15.3 Unlevered Versus Levered Cash Flows with Perfect Capital Markets

15-

MM Proposition I

• MM Proposition I: In a perfect capital market, the total value of a firm is equal to the market value of the free cash flows generated by its assets and is not affected by its choice of capital structure.w We can write this result in an equation:

V L= E + D =V U (Eq. 15.1)

VL= value of the firm with leverageVU= value of the unlevered firm

unlevered levered

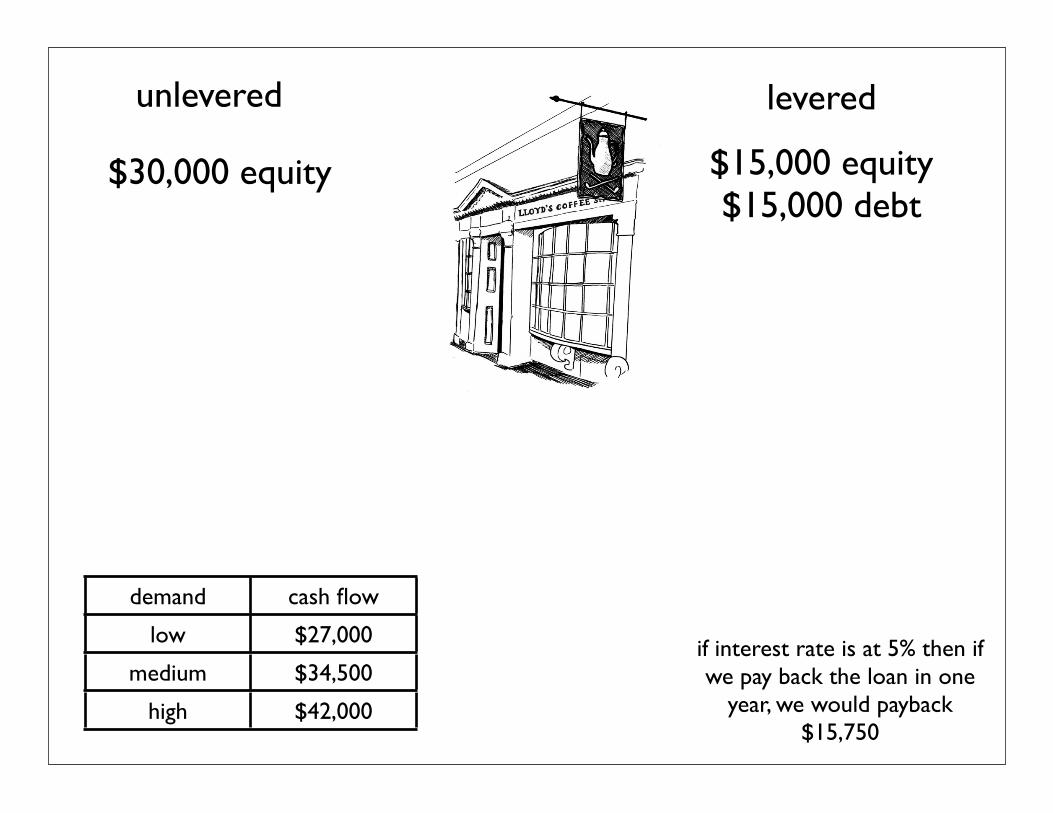

$30,000 down $15,000 down$15,000 borrowed

$30,000 equity$15,000 equity$15,000 debt

if interest rate is at 5% then if we pay back the loan in one

year, we would payback $15,750

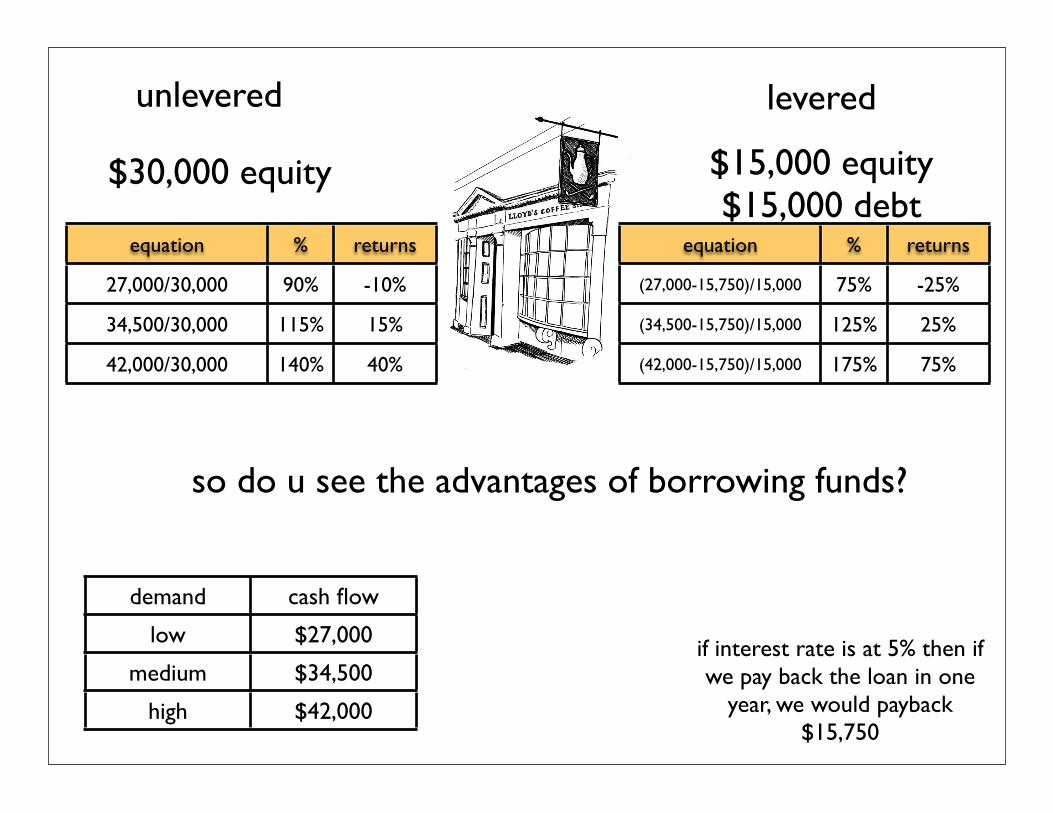

unlevered levered

$30,000 equity $15,000 equity$15,000 debt

if interest rate is at 5% then if we pay back the loan in one

year, we would payback $15,750

demand cash flow

low $27,000

medium $34,500

high $42,000

unlevered levered

$30,000 equity $15,000 equity$15,000 debt

if interest rate is at 5% then if we pay back the loan in one

year, we would payback $15,750

demand cash flow

low $27,000

medium $34,500

high $42,000

equation % returns

27,000/30,000 90% -10%

34,500/30,000 115% 15%

42,000/30,000 140% 40%

equation % returns

(27,000-15,750)/15,000 75% -25%

(34,500-15,750)/15,000 125% 25%

(42,000-15,750)/15,000 175% 75%

so do u see the advantages of borrowing funds?

15-

Table 15.1 Returns to Equity in Different Scenarios with and without Leverage

Assumptions for leverage: $15,000 borrowed to be paidback in one year at 5% interest, 15,000×1.05 = 15,750

=

++

Free cash flowsare given for thethree scenarios

If unlevered:$30,000 equity no debt

If levered:$15,000 equity$15,000 debt

+==

Equity risk premium:10% if unlevered20% if levered

15-

15.2 Capital Structure in Perfect Capital Markets

• Homemade leverage: when investors use leverage in their own portfolios to adjust the leverage choice made by the firm.

• Homemade leverage is a perfect substitute for the use of leverage by the firm in perfect capital markets.

15-

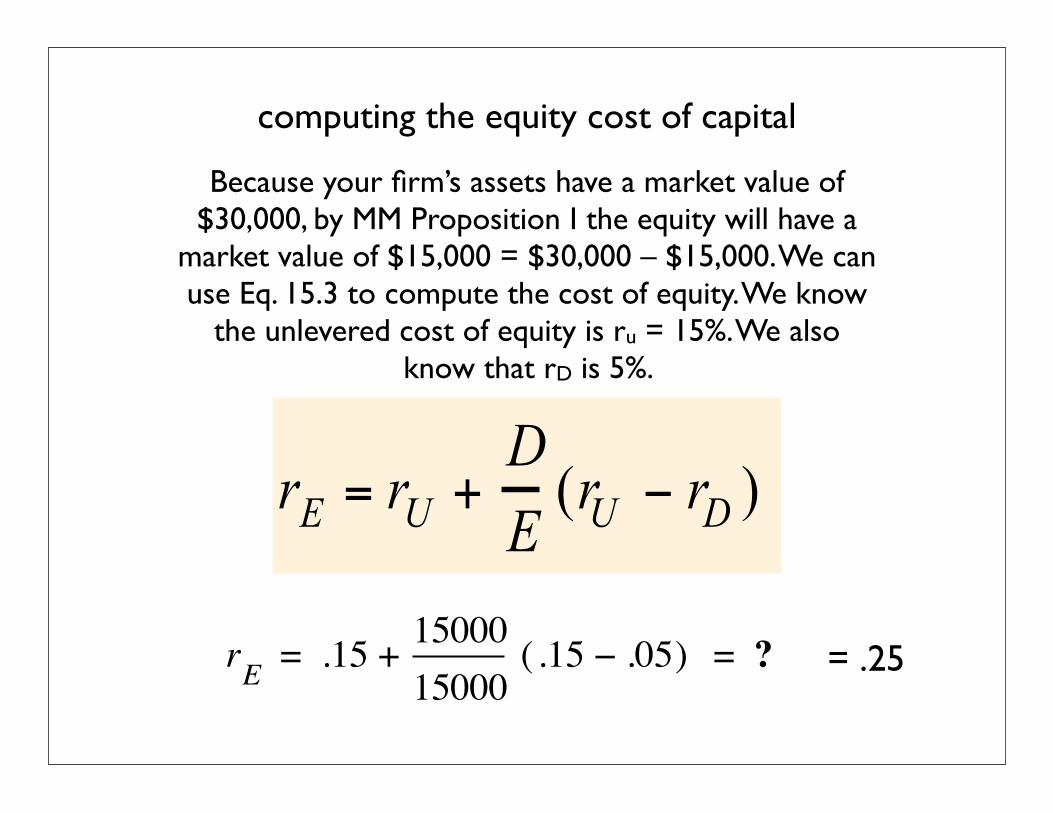

MM Proposition II: The Cost of Capital of Levered Equity

• MM Proposition II: The Cost of Capital of Levered Equity

(Eq. 15.3)

rE = expected return (cost of capita) of levered equity

computing the equity cost of capital

Because your firm’s assets have a market value of $30,000, by MM Proposition I the equity will have a

market value of $15,000 = $30,000 – $15,000. We can use Eq. 15.3 to compute the cost of equity. We know

the unlevered cost of equity is ru = 15%. We also know that rD is 5%.

rE .15 1500015000

.15 .05−( )+ ?= = = .25

unlevered levered

$30,000 equity $15,000 equity$15,000 debt

if interest rate is at 5% then if we pay back the loan in one

year, we would payback $15,750

demand cash flow

low $27,000

medium $34,500

high $42,000

equation % returns

27,000/30,000 90% -10%

34,500/30,000 115% 15%

42,000/30,000 140% 40%

equation % returns

(27,000-15,750)/15,000 75% -25%

(34,500-15,750)/15,000 125% 25%

(42,000-15,750)/15,000 175% 75%

so do u see the advantages of borrowing funds?

15-

15.3 Debt and Taxes

• In the real world, markets are imperfect, and these imperfections can create a role for the firm’s capital structure. A firm’s capital structure can affect the corporate taxes it must pay.w Corporations can deduct interest expenses from their taxable

income. w The deduction reduces the taxes paid which increases the

amount available to pay investors. w In doing so, the interest tax deduction increases the value of

the corporation.

15-

15.3 Debt and Taxes

• Consider the impact of interest expenses on taxes paid by Safeway, Inc., a grocery store chain.

• In 2006, Safeway had earnings before interest and taxes of $1.65 billion, and interest expenses of $400 million. Given a corporate tax rate of 35%, we can compare Safeway’s actual net income with what it would have been without debt.

15-

Table 15.2 Safeway’s Income with and without Leverage, 2006 ($ million)

15-

15.3 Debt and Taxes

• Interest Tax Shield: The gain to investors from the tax deductibility of interest payments

Interest Tax Shield = Corporate Tax Rate × Interest Payments

15-

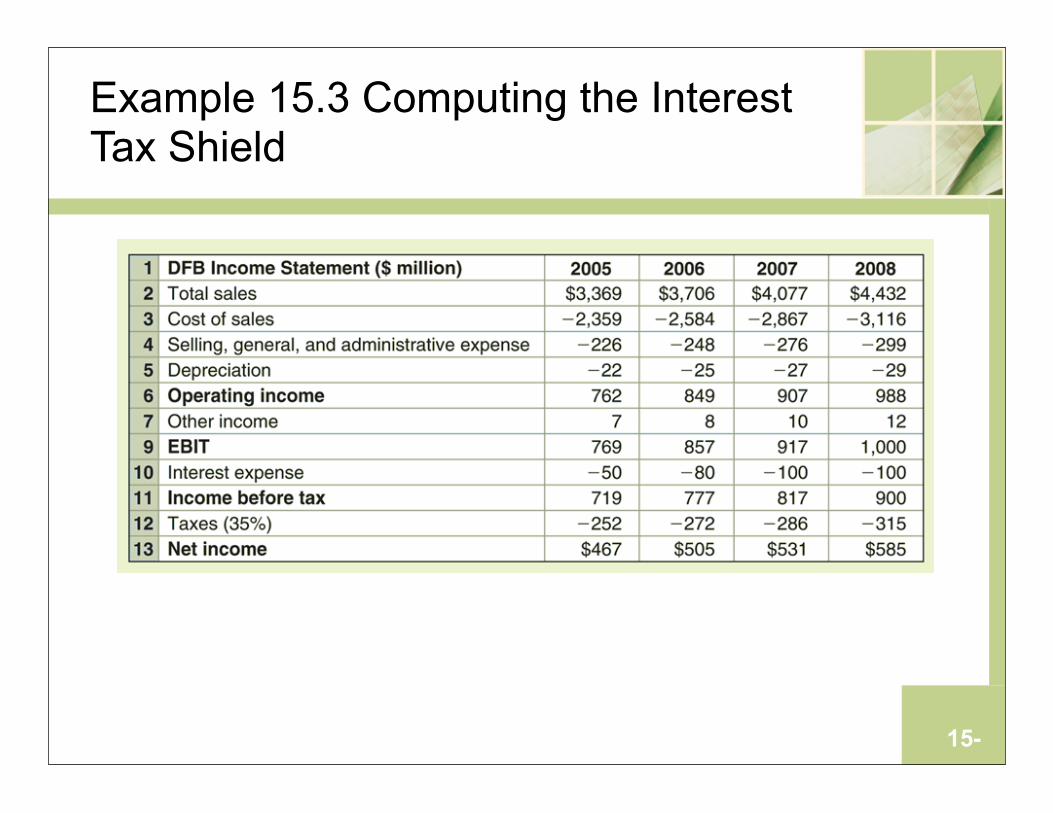

Example 15.3 Computing the Interest Tax Shield

Problem:• Shown on the next slide is the income statement

for D.F. Builders (DFB). Given its marginal corporate tax rate of 35%, what is the amount of the interest tax shield for DFB in years 2005 through 2008?

15-

Example 15.3 Computing the Interest Tax Shield

15-

Example 15.3 Computing the Interest Tax Shield

Solution:Plan:• From Eq. 15.4, the interest tax shield is the tax

rate of 35% multiplied by the interest payments in each year.

15-

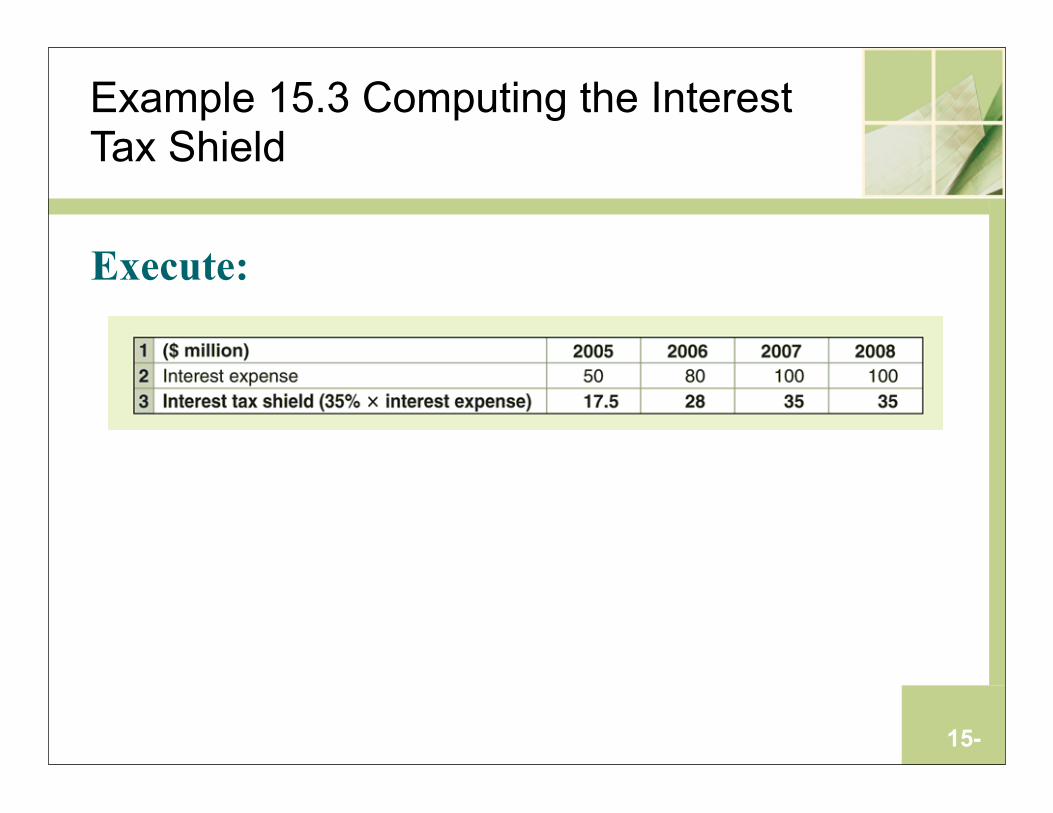

Example 15.3 Computing the Interest Tax Shield

Execute:

15-

Example 15.3 Computing the Interest Tax Shield

Evaluate:• By using debt, DFB is able to reduce its taxable

income and therefore decreased its total tax payments by $115.5 million over the four-year period. Thus the total amount of cash flows available to all investors (debtholders and equity holders) is $115.5 million higher over the four-year period.

15-

Example 15.3a Computing the Interest Tax Shield

Problem:• Shown on the next slide is the income statement

for Invite Only, an invitation/card company. Given its marginal corporate tax rate of 40%, what is the amount of the interest tax shield for Invite Only in years 2006 through 2008?

15-

Example 15.3a Computing the Interest Tax Shield

Invite Only Income Statement ($ million)

2006 2007 2008

Total sales $4,750 $5,350 $6,177Cost of sales –2,543 –2,428 –3,114Selling, general, and administrative expense

–446 –399 –470

Depreciation –32 –29 –35

Operating Income 1,729 2,494 2,558

Other income 14 12 16EBIT 1,743 2,506 2,574Interest expense –100 –110 –115Income before tax 1,643 2,396 2,459

Taxes (40%) –657 –958 –984Net income $986 $1,438 $1,475

15-

Example 15.3a Computing the Interest Tax Shield

Solution:Plan:• From Eq. 15.4, the interest tax shield is the tax

rate of 40% multiplied by the interest payments in each year.

15-

Example 15.3a Computing the Interest Tax Shield

Execute:

($ million) 2006 2007 2008

Interest expense –100 –110 –115Interest tax shield (40% × interest expense)

40 44 46

15-

Example 15.3a Computing the Interest Tax Shield

Evaluate:• By using debt, Invite Only is able to reduce its

taxable income and decrease its total tax payments. Therefore, the total amount of cash flows available to all investors (debtholders and equity holders) is $130 million higher over the three-year period.

15-

15.3 Debt and Taxes

• When a firm uses debt, the interest tax shield provides a corporate tax benefit each year. To determine the benefit of leverage for the value of the firm, we must compute the present value of the stream of future interest tax shields the firm will receive.

15-

Figure 15.6 The Cash Flows of the Unlevered and Levered Firm

15-

15.3 Debt and Taxes

• The graph shows that by increasing the cash flows paid to debtholders through interest payments, a firm reduces the amount paid in taxes.

• The increase in total cash flows paid to investors is the interest tax shield.

15-

Value of the Interest Tax Shield

• Cash flows of the levered firm are equal to the sum of the cash flows from the unlevered firm plus the interest tax shield. By the Valuation Principle the same must be true for the present values of these cash flows.

• Here’s the change to MM Proposition I with the presence of taxes:

The total value of the levered firm exceeds the value of the firm without leverage due to the present value of the tax savings from debt:

VL = VU + PV(Interest Tax Shield) (Eq. 15.5)

Related Documents