1 Chapter 14: Pass-Through Entities Page 209-227 14: Pass-Through Entities

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Chapter 14: Pass-Through Entities

Page 209-227

14: Pass-Through Entities

Upon completion of this seminar, participants should be able to—

Learning Objectives

2

• Summarize K-1 reporting for Forms 1065, 1120S and 1041.

• Calculate basis, at-risk basis and other loss limitations.• Consider “best practices” when entering a client’s

Schedule K-1 information

Page 209-227

14: Pass-Through Entities

3

Key Developments

• Information on a gateway for K-1 tax packages, which frequently will have an earlier delivery than the paper package. Page 211

• Dealing with debt basis for LLCs. Page 215• There have been numerous regulation updates for S

Corporation debt basis that need to be reviewed. Page 225

Page 209-227

14: Pass-Through Entities

II. Schedule K-1 Overview

Page 209

Partnerships, S Corporations and Trusts/Estates are flow thru entities that pass:1. A net result of trade

or business operations and

2. All other specially allocated items

Books

Flow Thru

Entities

Non-Separate

14: Pass-Through Entities4

Some of the concepts:Except for “operation’s income” other items such as investments, sale of assets, contributions, etc. will retain their identity on the owner’s tax return.There will need to be an identification of :

Basis At Risk (IRC 465) Material Participation (IRC 469)

II. Schedule K-1 Overview

Page 209

14: Pass-Through Entities5

What if the provider of the K-1 gets it wrong?There is a provision which provides for the taxpayer to indicate items that have not been reported consistent with Form K-1.

II. Schedule K-1 Overview

Page 209

14: Pass-Through Entities6

Correctness standard – Regs.Math Error Authority

The question, can the taxpayer use estimates when reporting flow thru income? Yes, but must have some

kind of reliable basis for those estimates.

If there is a K-1 provided the procedures of Form 8082 should be followed.

II. Schedule K-1 Overview

Page 209-210

14: Pass-Through Entities7

Not all activities of the flow thru entity are equal:A taxpayer may have:1. Basis, records and computations should be kept,

the records of the entity for basis do not necessarily reflect a correct amount.

2. At risk, determination of at risk amounts are frequently made at entity level and generally must be respected.

3. Participation under the rules of IRC 469, each activity of the entity must be measured for determination of passive versus non-passive.

II. Schedule K-1 Overview

Page 210

14: Pass-Through Entities8

Expenses paid in connection with owner’s participation of the flow thru entity:2. Partnerships – UPE – However,

they must be provided for in the partnership agreement.

3. S Corporations – Employee business expense, but not the expenses of the company.

II. Schedule K-1 Overview

Page 210

14: Pass-Through Entities9

The must dos of flow thru entity tax preparation on the owner’s return.

Maintain records of basis of partner/shareholder.Computations of basis must be attached to S Corporation shareholders return if a loss.It is perfectly okay to rely on a third party that may have prepared the return, but issues cannot be ignored that do not appear to be “logical”.

II. Schedule K-1 Overview

Page 211

14: Pass-Through Entities10

III. Publically Traded andMaster Limited Partnerships

Waiting for the K-1 is often one of the greatest challenges of preparing a return for a taxpayer with a PTP or MLP.Solution - taxpackagesupport.com/

Page 211

14: Pass-Through Entities11

III. Publically Traded andMaster Limited Partnerships

Waiting for the K-1 is often one of the greatest challenges of preparing a return for a taxpayer with a PTP or MLP.Solution - taxpackagesupport.com/

Page 211

14: Pass-Through Entities12

III. Publically Traded andMaster Limited Partnerships

Waiting for the K-1 is often one of the greatest challenges of preparing a return for a taxpayer with a PTP or MLP.Solution - taxpackagesupport.com/

Page 211

14: Pass-Through Entities13

III. Publically Traded andMaster Limited Partnerships

G. A myriad of issues will apply to the sale:

1. Hot assets, IRC 751 gains.2. Recapture of Depreciation3. Suspended Losses released

at sale4. Differences of AMT to

Regular Tax Basis5. Section 754 disclosures

Page 212

14: Pass-Through Entities14

III. Publically Traded andMaster Limited Partnerships

What might it look like:

Page 212

Description Transactions 1099-B Adj.

1,000 units +$30,000 $30,000

Cash Dist. -$2,500 $27,500

Income K-1 +$2,000 $29,500

Depr K-1 -$1,500 $28,000

Sale of Units -$32,000 +$4,000

+$30,000

-$2,500

-$32,000

+$4,500

+$2,000

-$1,500

+$4,000

Reported Gain/Loss on Form 1099-B

Adjusted Net +Gain/-Loss

14: Pass-Through Entities15

C. A K-1 is not simply about entering the numbers in the tax software. The limitations on differing items are numerous.To deduct a loss:1. Determine Outside Basis.2. Determine what amounts are at risk.3. Determine the applicability of IRC 469

limitations4. Other loss limitations

IV. Partnerships - Partner’s Basis forClaiming Losses on K-1s

Page 212-213

14: Pass-Through Entities16

4. Each item of flow thru from the 1065 K-1 will need to be analyzed to determine its affect on:

a. A NOLb. A Net Capital Lossc. A Net Section 1231 lossd. Is there in a fact a hobby loss.

IV. Partnerships - Partner’s Basis for Claiming Losses on K-1s

Page 213

14: Pass-Through Entities17

The steps of basis, a statutory procedure:1. Beginning Outside Basis2. Plus additional contributions3. Plus share of all positive adjustments (income)4. Plus additional liabilities attributed to partner5. Less share of losses and deductions6. Less distributions to partner7. Less reduction in share of liabilities8. Equals – Tax Capital Account – Year End Basis

V. Partnerships – Partners Outside Basis[IRS Sec. 704(D)] “The First Test”

Page 213

14: Pass-Through Entities18

V. Partnerships – Partners Outside Basis[IRS Sec. 704(D)] “The First Test”

Stuff your software will do if you let it

Page 213

14: Pass-Through Entities19

B. What might have occurred to cause a variance between the partnership books and partner:1. Acquisition on interest other than directly

from the partnership.2. Distribution recognition3. Lack of loss basis in a prior year.4. The partner may have used estimates due to

lack of information

Page 213-214

14: Pass-Through Entities20

V. Partnerships – Partners Outside Basis[IRS Sec. 704(D)] “The First Test”

C. Basis from liabilities Increases – Treated

as a cash contribution by partner.

Decreases –Treated as a cash distribution to the partner.

Page 214

14: Pass-Through Entities21

V. Partnerships – Partners Outside Basis[IRS Sec. 704(D)] “The First Test”

4. Debt Rules:a. Recourse DebtAny debt of which the partner bears some kind of personal responsibility, however be careful of special allocations of loss (Zero Value Liquidation)b. Non-Recourse DebtA debt of which the partnership (or some other related person) but the partner will not be liable in the event of default.

Page 214

14: Pass-Through Entities22

V. Partnerships – Partners Outside Basis[IRS Sec. 704(D)] “The First Test”

V. Partnerships – Partners Outside Basis[IRS Sec. 704(D)] “The First Test”

Be cautious of LLCs including the disregarded entity (such as a Schedule C taxpayer).

At risk issues are present in an LLC by definition a member is not “at risk” for debts of an LLC unless

they have “guaranteed” the debt.

Page 215

14: Pass-Through Entities23

Be cautious of LLCs including the disregarded entity (such as a Schedule C taxpayer).

If a loss Form 6198 is required.

At risk issues are present in an LLC by definition a member is not “at risk” for debts of an LLC unless

they have “guaranteed” the debt (Exculpatory).

Page 215

14: Pass-Through Entities24

V. Partnerships – Partners Outside Basis[IRS Sec. 704(D)] “The First Test”

At risk of loss rules are complicated, but the concept is will the partner/member have to dig into their personal pocketbook without a right of recovery (guarantee) by some other individual or entity.

VI. Partnerships - Partners At-Risk Rules[IRC Sec. 465]- The Second Test

Page 215

14: Pass-Through Entities25

Qualified Non-Recourse loans are applied:To those organizations that were formed for the purpose of investing in real estate andNo individual partner are at risk for the debt andThe loan is from a qualifying lending agency, i.e. not related.

While all non-recourse debt increases basis QNRD will also be considered at risk, i.e. allow the partner to use losses from QNRD activities.

Page 215-216

14: Pass-Through Entities26

VI. Partnerships - Partners At-Risk Rules[IRC Sec. 465]- The Second Test

How it works and the issues associated with non-recourse debt

Page 216

14: Pass-Through Entities27

VI. Partnerships - Partners At-Risk Rules[IRC Sec. 465]- The Second Test

While the partner has basis from the NRD they fail the at risk rules.

Therefor the $20,000 loss is limited to Shelly’s at risk amount of $14,000 suspend the rest.

Page 216

14: Pass-Through Entities28

VI. Partnerships - Partners At-Risk Rules[IRC Sec. 465]- The Second Test

So the amounts on the 1065 K-1 are incorrect whose problem is this.

Page 217

14: Pass-Through Entities29

VI. Partnerships - Partners At-Risk Rules[IRC Sec. 465]- The Second Test

Chapter 15 in our text specifically addresses the rules of IRC 469 Chapter 11 NIIT address the issues associated with the determination of whether the pass-thru is subject to the 3.8% surcharge

VII. Partnerships – Passive Activities(IRC 469) “The Third Test”

Page 217

14: Pass-Through Entities30

So what does this tell us about the “outside basis” of the partner: If all capital transactions and values are equal

between partnership and partner everything but If there are any transactions the partnership was

not party to, very little.

Page 217

14: Pass-Through Entities31

VII. Partnerships – Passive Activities(IRC 469) “The Third Test”

VII. Partnerships – Passive Activities(IRC 469) “The Third Test”

The tax basis on the 1065 does not yield the partners basis in all cases

Chapter 17: Partnership (or LLC) Operations

10401065

Page 217

There should be no W-2 for a partner: However some organizations continue to treat a

partner as an employee in error. This practice MUST be stopped by 12/31/2016

due to a recent IRS attempt to discontinue this practice.

Payments made to a partner without regard to a profits interest will generally be a guaranteed payment reported on Line 4 this includes health insurance.

VIII. Other Reportable Items by Partner

Page 217

14: Pass-Through Entities33

Does the partner have expenses they are “required” to pay themselves for partnership business, this error can be fixed if necessary, normally March 15th

now.

VIII. Other Reportable Items by Partner

Page 220

14: Pass-Through Entities34

Does the partner have expenses they are “required” to pay themselves for partnership business:

Action Item – Review partnership agreement to determine requirement to pay. Do not get trapped by the Hines case.

VIII. Other Reportable Items by Partner

Page 220

14: Pass-Through Entities35

For the preparer of the 1040:1. Obtaining a copy of the partnership agreement is

a best practice

2. No agreement no UPE

VIII. Other Reportable Items by Partner

Page 220

14: Pass-Through Entities36

The criticality of basis:

A. Controversy between IRS and taxpayers continue. Why – Taxpayers continue to deduct losses without basis records.

D. Tracking basis is the responsibility of the shareholder, not the corporation.

E. The basis of each share is calculated separately.

IX. S Corporations – Shareholder’sStock Basis

Page 220-221

14: Pass-Through Entities37

Records should be kept to understand how and what was “paid” to acquire the stock.

Purchase – What was paid for it.IRC 351 Incorporation – Basis of property contributed to the corporation.Electing C Corporation – Basis of stock at time of election.Gift – Yuck, it depends based on transaction.Inheritance – FMV on DODServices – FMV of stock received on date of services

X. S Corporations-Initial Basis

Page 221

14: Pass-Through Entities38

Discussion:Purchase of additional shares – Problem basis of new shares differs from older shares – What does the minutes reflect regarding that “transaction”? Or opportunity to take distributions that are partly taxable.

Additional Paid in Capital – Capital required by shareholders to allow company to continue to function – Not new shares, simply an increase in the cost basis of prior shares.

X. S Corporations-Initial Basis

Page 221

14: Pass-Through Entities39

Basis Equals:The beginning amount +Positive Adjustments –Distributions –Losses, Deductions and CreditsIt is a must if you miss it your chance to deduct a loss is gone forever.In Barnes v. Comm. The court found that there is NO tax benefit rule, losses are deductible when they occur, unless suspended by basis, at risk or PAL when released they are deductible and only then.

XII. S Corporations-Order and TimingOf Basis Adjustments

Page 223

14: Pass-Through Entities40

Any activity will be accounted for prior to the sale of stock:

The Math is $10,000 + $25,000 = $35,000 in basisThe Outcome is$35,000 ordinary income not $40,000 in CG.

XII. S Corporations-Order and TimingOf Basis Adjustments

Page 223

14: Pass-Through Entities41

Another Issue – The order of things

The shareholder will be required to suspend his losses as the non-deductibles have reduced his basis to $ 9,500 after apply the non-deductible loss.

XII. S Corporations-Order and TimingOf Basis Adjustments

Page 224

14: Pass-Through Entities42

Warning An election that many taxpayers have found enticing is the election to flip the order to have non-deductible items consume basis last.Benefit – Deductible losses will be allowed currently if after distributions there is basis availableProblem – Any non-deductible losses not absorbed will be carried forward until consumed by available basis.

XII. S Corporations-Order and TimingOf Basis Adjustments

Page 224

14: Pass-Through Entities43

There is no such thing as less than ZERO, distributions made in excess of basis are taxable.

Basis at beginning of year $100,000 +Distributable Earnings $ 20,000 +Distributions $150,000 –Basis $ 30,000 -

Taxable Portion of Distribution $ 30,000 +Basis $ 0

XIII. S Corporations-Distributions inExcess of Basis

Page 224

14: Pass-Through Entities44

A shareholder in a S Corporation can obtain basis for losses from direct loans to the corporation.

Stock Basis comes first.Losses can be applied to loan “basis” until the loan “basis” becomes ZERO.Distributable income will first restore loan basis to face amount. Loan guarantees are not direct debt until the shareholder actually make a payment under the guarantee.

XIV. S Corporations-Deducting ShareholderLosses Against Debt Basis

Page 224

14: Pass-Through Entities45

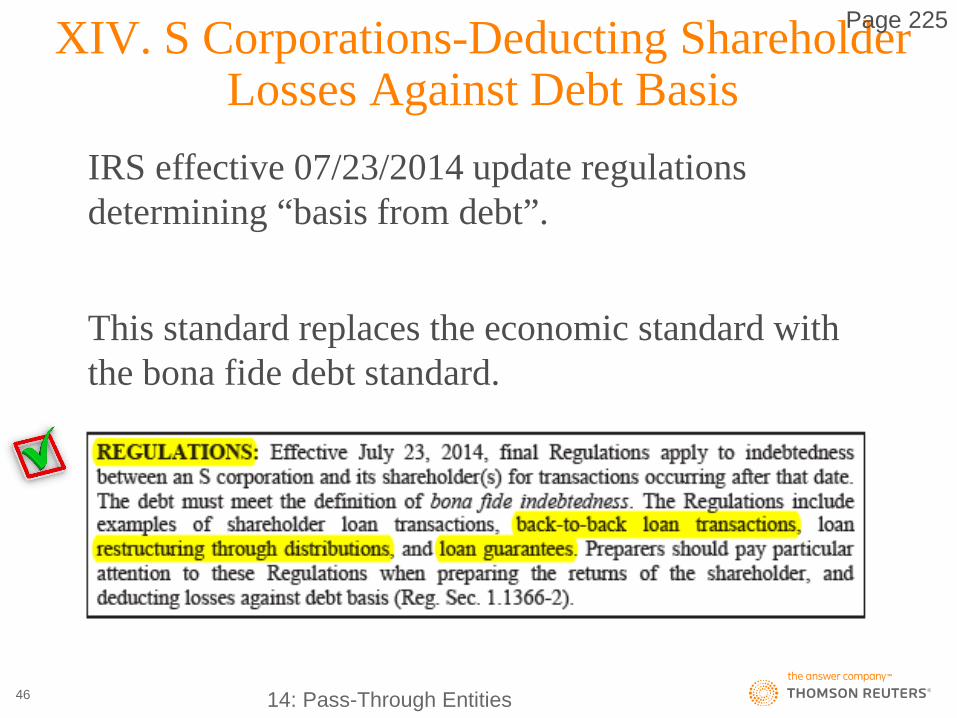

XIV. S Corporations-Deducting ShareholderLosses Against Debt Basis

IRS effective 07/23/2014 update regulations determining “basis from debt”.

This standard replaces the economic standard with the bona fide debt standard.

Page 225

14: Pass-Through Entities46

It was wonderful, your taxpayer deducted their S Corporation losses using direct loans as basis, but:

XV. S Corporations - Repayment of Reduced-Basis Shareholder Debt

Page 225

14: Pass-Through Entities47

Some good news and not so good news: Shareholder is able to deduct ordinary losses

from debt basis. Loans can only be restored by S Corp income. Repayment of debt with a basis of less than face

can result in a capital gain.

All this stuff requires vigilance and good records, your tax software is likely up to the task.

XV. S Corporations - Repayment of Reduced-Basis Shareholder Debt

Page 226

14: Pass-Through Entities48

Understand the rules of partnerships and you will understand the rules of trusts and estates easily.

The critical difference:The final year of the trust estate may lead to a distribution of “corpus” amounts.Excess deductions that were not allowed during the time of operation will go to Schedule ACapital Loss carryovers will go to Schedule D

XVI. Trusts and Estates

Page 227

14: Pass-Through Entities49

Related Documents