Copyright Copyright ©2009 Pearson Education, Inc. Publishing as 2009 Pearson Education, Inc. Publishing as Prentice Hall Prentice Hall 1 Chapter 14 Equity Financing Chapter 14 Equity Financing Sources of Equity Financing

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 11Chapter 14 Equity FinancingChapter 14 Equity Financing

Sources of Equity

Financing

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 22Chapter 14 Equity FinancingChapter 14 Equity Financing

The “Secrets” to The “Secrets” to Successful FinancingSuccessful Financing1. Choosing the right sources of capital 1. Choosing the right sources of capital

is a decision that will influence a is a decision that will influence a company for a lifetimecompany for a lifetime

2. The money is out there; the key is 2. The money is out there; the key is knowing where to lookknowing where to look

3. Creativity counts. Entrepreneurs have 3. Creativity counts. Entrepreneurs have to be as creative in their searches for to be as creative in their searches for capital as they are in developing their capital as they are in developing their business ideasbusiness ideas

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 33Chapter 14 Equity FinancingChapter 14 Equity Financing

The “Secrets” to The “Secrets” to Successful FinancingSuccessful Financing4. The World Wide Web puts at 4. The World Wide Web puts at

entrepreneur’s fingertips vast entrepreneur’s fingertips vast resources of information that can lead resources of information that can lead to financing to financing

5. Be thoroughly prepared before 5. Be thoroughly prepared before approaching lenders and investors approaching lenders and investors

6. Looking for “smart” money is more 6. Looking for “smart” money is more important than looking for “easy” important than looking for “easy” money money

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 44Chapter 14 Equity FinancingChapter 14 Equity Financing

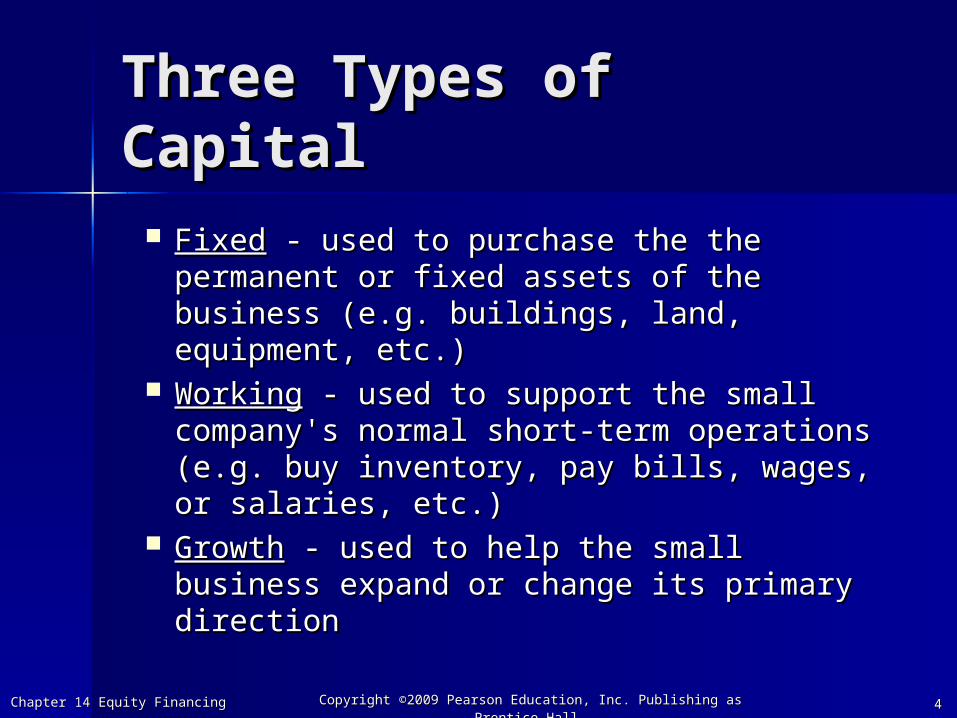

Three Types of Three Types of CapitalCapital

FixedFixed - used to purchase the the - used to purchase the the permanent or fixed assets of the permanent or fixed assets of the business (e.g. buildings, land, business (e.g. buildings, land, equipment, etc.)equipment, etc.)

WorkingWorking - used to support the small - used to support the small company's normal short-term operations company's normal short-term operations (e.g. buy inventory, pay bills, wages, or (e.g. buy inventory, pay bills, wages, or salaries, etc.)salaries, etc.)

GrowthGrowth - used to help the small business - used to help the small business expand or change its primary directionexpand or change its primary direction

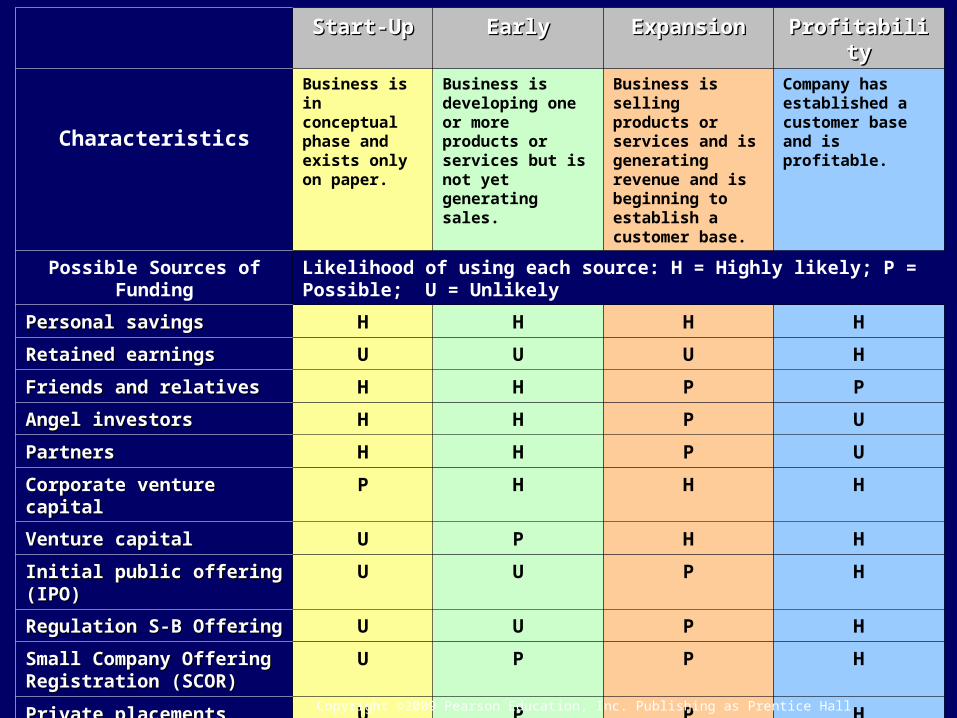

Start-UpStart-Up EarlyEarly ExpansionExpansion ProfitabilityProfitability

Characteristics

Business is in conceptual phase and exists only on paper.

Business is developing one or more products or services but is not yet generating sales.

Business is selling products or services and is generating revenue and is beginning to establish a customer base.

Company has established a customer base and is profitable.

Possible Sources of Funding Likelihood of using each source: H = Highly likely; P = Possible; U = Unlikely

Personal savingsPersonal savings H H H H

Retained earningsRetained earnings U U U H

Friends and relativesFriends and relatives H H P P

Angel investorsAngel investors H H P U

PartnersPartners H H P U

Corporate venture capitalCorporate venture capital P H H H

Venture capitalVenture capital U P H H

Initial public offering (IPO)Initial public offering (IPO) U U P H

Regulation S-B OfferingRegulation S-B Offering U U P H

Small Company Offering Small Company Offering Registration (SCOR)Registration (SCOR)

U P P H

Private placementsPrivate placements U P P H

Intrastate offerings (Rule 147)Intrastate offerings (Rule 147) U P P H

Regulation ARegulation A U P P H

Chapter 14 Equity Financing Copyright ©2009 Pearson Education, Inc. Publishing as Prentice Hall 5

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 66Chapter 14 Equity FinancingChapter 14 Equity Financing

Equity Equity CapitalCapital

Represents the personal investment Represents the personal investment of the owner(s) in the businessof the owner(s) in the business

Is called Is called risk capital risk capital because because investors assume the risk of losing investors assume the risk of losing their money if the business failstheir money if the business fails

Does Does notnot have to be repaid with have to be repaid with interest like a loan doesinterest like a loan does

Means that an entrepreneur must Means that an entrepreneur must give up some ownership in the give up some ownership in the company to outside investorscompany to outside investors

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 77Chapter 14 Equity FinancingChapter 14 Equity Financing

Sources of Equity Sources of Equity FinancingFinancing Personal savingsPersonal savings Friends and family membersFriends and family members AngelsAngels PartnersPartners CorporationsCorporations Venture capital companiesVenture capital companies Public stock salePublic stock sale

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 88Chapter 14 Equity FinancingChapter 14 Equity Financing

Personal Personal SavingsSavings The The firstfirst place an entrepreneur place an entrepreneur

should look for money should look for money The most common source of equity The most common source of equity

capital for starting a businesscapital for starting a business GEM study: GEM study:

Average cost to start a business in Average cost to start a business in U.S. is $70,200U.S. is $70,200

Typical entrepreneur provides 67.9% Typical entrepreneur provides 67.9% of the initial capital requirement of the initial capital requirement

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 99Chapter 14 Equity FinancingChapter 14 Equity Financing

Friends and Family Friends and Family MembersMembers After emptying her own pockets, an After emptying her own pockets, an

entrepreneur should turn to those most entrepreneur should turn to those most likely to invest in the business - friends likely to invest in the business - friends and family membersand family members

GEM study: GEM study: Across the globe, the average amount Across the globe, the average amount

family and friends invest in start-up family and friends invest in start-up businesses is $3,000 businesses is $3,000

In U.S., average amount is $27,715 for a In U.S., average amount is $27,715 for a total of $100 billion per year total of $100 billion per year

Careful!!! Inherent dangers lurk in Careful!!! Inherent dangers lurk in family/friendly business deals, family/friendly business deals, especiallyespecially those that flop those that flop

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1010Chapter 14 Equity FinancingChapter 14 Equity Financing

Guidelines for family and friendship Guidelines for family and friendship financing deals:financing deals: Consider the impact of the investment Consider the impact of the investment

on everyone involvedon everyone involved Keep the arrangement “strictly Keep the arrangement “strictly

business”business” Educate “naïve” investors Educate “naïve” investors Settle the details up frontSettle the details up front Never accept more than the investor Never accept more than the investor

can afford to losecan afford to lose

Friends and Family Friends and Family MembersMembers

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1111Chapter 14 Equity FinancingChapter 14 Equity Financing

Guidelines for family and friendship Guidelines for family and friendship financing deals:financing deals: Create a written contractCreate a written contract Treat the money as “bridge financing” Treat the money as “bridge financing” Develop a payment schedule that Develop a payment schedule that

suits both parties suits both parties Have an exit planHave an exit plan Keep everyone informed Keep everyone informed

Friends and Family Friends and Family MembersMembers

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1212Chapter 14 Equity FinancingChapter 14 Equity Financing

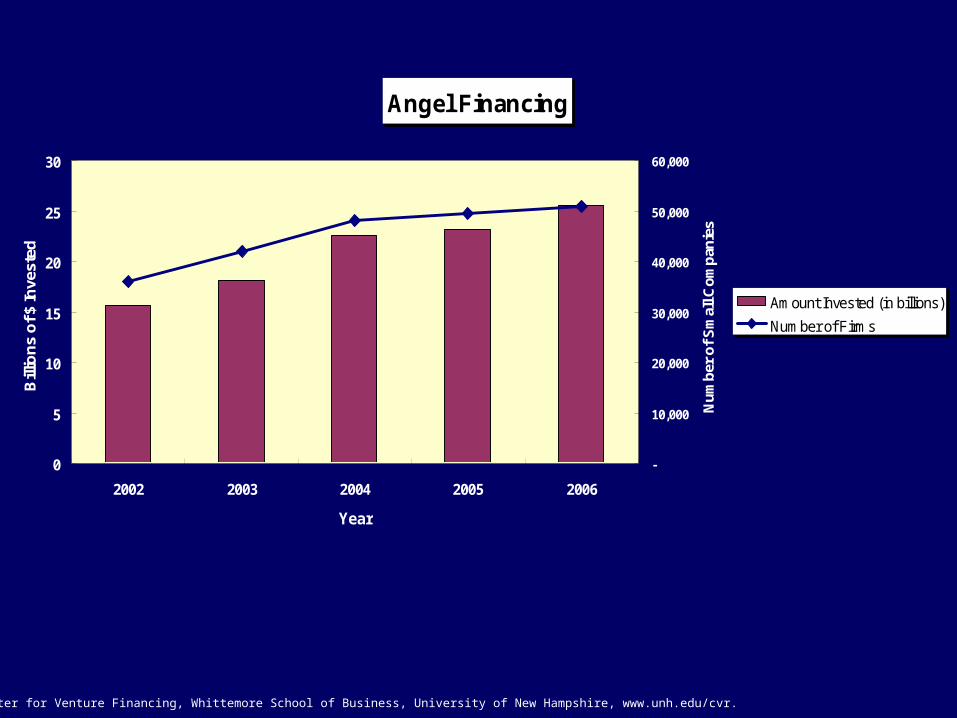

AngelsAngels Private investors who invest in Private investors who invest in

emerging business start-ups in emerging business start-ups in exchange for equity stakes in the exchange for equity stakes in the companycompany

Fastest growing segment of the Fastest growing segment of the small business capital market small business capital market

Center for Venture Research study: Center for Venture Research study: 234,000 angels invest $25.6 billion 234,000 angels invest $25.6 billion a year in 51,000 small companiesa year in 51,000 small companies

Angel Financing

0

5

10

15

20

25

30

2002 2003 2004 2005 2006

Year

Bill

ions

of $

Inve

sted

-

10,000

20,000

30,000

40,000

50,000

60,000

Num

ber o

f Sm

all C

ompa

nies

Amount Invested (in billions)Number of Firms

Source: Center for Venture Financing, Whittemore School of Business, University of New Hampshire, www.unh.edu/cvr.

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1414Chapter 14 Equity FinancingChapter 14 Equity Financing

AngelsAngels

Ideal source of financing for Ideal source of financing for companies that have outgrown companies that have outgrown the capacity of friends and family the capacity of friends and family members but are still too small to members but are still too small to attract the interest of venture attract the interest of venture capital companies capital companies

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1515Chapter 14 Equity FinancingChapter 14 Equity Financing

Most likely to finance deals in the Most likely to finance deals in the $10,000 to $2 million range $10,000 to $2 million range

Key: finding them! Key: finding them! Angels almost always invest their Angels almost always invest their

money locally and can be found money locally and can be found through networkingthrough networking

Another avenue: Angel capital Another avenue: Angel capital networks on the World Wide Webnetworks on the World Wide Web

AngelsAngels

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1616Chapter 14 Equity FinancingChapter 14 Equity Financing

Typical angel accepts 12% of the Typical angel accepts 12% of the proposals presented and has proposals presented and has invested an average of $80,000 invested an average of $80,000 in 3.5 businesses in 3.5 businesses

An excellent source of “patient An excellent source of “patient money” for investors needing money” for investors needing relatively small amounts of relatively small amounts of capital – often less than $500,000capital – often less than $500,000

AngelsAngels

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1717Chapter 14 Equity FinancingChapter 14 Equity Financing

Corporate Venture Corporate Venture CapitalCapital About 300 large corporations across the About 300 large corporations across the

globe invest in start-up companiesglobe invest in start-up companies 19% of all venture capital investments 19% of all venture capital investments

come from corporationscome from corporations Average CVC investment = $2.97 millionAverage CVC investment = $2.97 million

Capital infusions are just one benefit; Capital infusions are just one benefit; corporate partners may share corporate partners may share marketing and technical expertise marketing and technical expertise

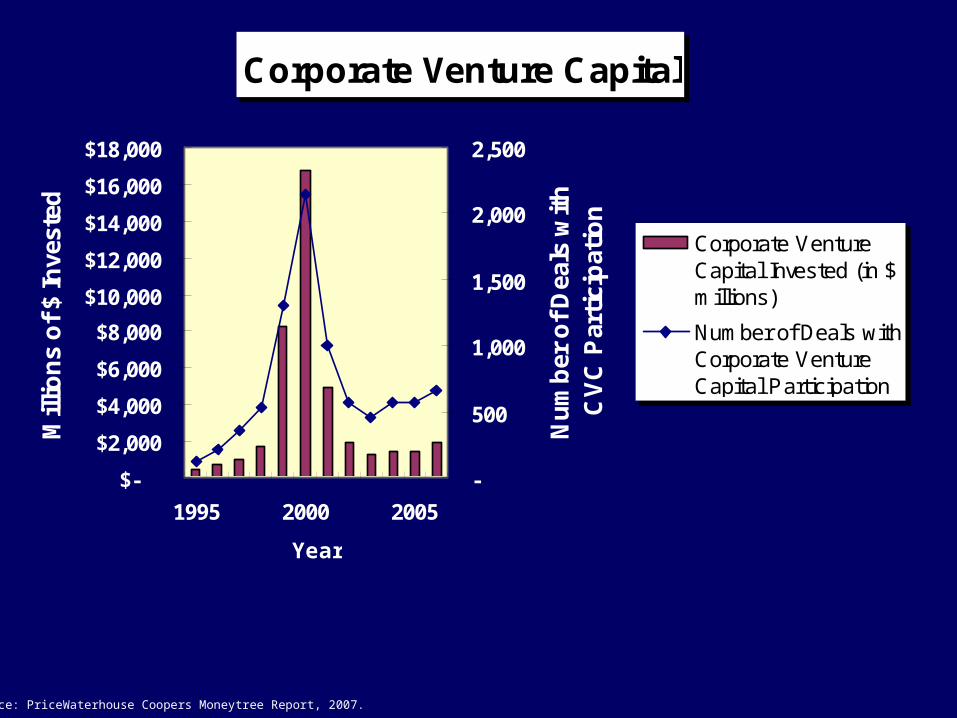

Corporate Venture Capital

$-$2,000$4,000$6,000$8,000

$10,000$12,000$14,000$16,000$18,000

1995 2000 2005

Year

Mill

ions

of $

Inve

sted

-

500

1,000

1,500

2,000

2,500

Num

ber o

f Dea

ls w

ith

CVC

Par

ticip

atio

n

Corporate VentureCapital Invested (in $millions)

Number of Deals withCorporate VentureCapital Participation

Source: PriceWaterhouse Coopers Moneytree Report, 2007.

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 1919Chapter 14 Equity FinancingChapter 14 Equity Financing

Venture Capital Venture Capital CompaniesCompanies More than 1,300 venture capital More than 1,300 venture capital

firms operate across the U.S. firms operate across the U.S. Most venture capitalists seek Most venture capitalists seek

investments in the $3,000,000 to investments in the $3,000,000 to $10,00,000 range in companies $10,00,000 range in companies with high-growth and high-profit with high-growth and high-profit potential potential Average VC investment = $7.4 million Average VC investment = $7.4 million

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 2020Chapter 14 Equity FinancingChapter 14 Equity Financing

Venture Capital Venture Capital CompaniesCompanies Business plans are subjected to Business plans are subjected to

an extremely rigorous review - an extremely rigorous review - less than 1% acceptedless than 1% accepted

GEM study: Only 1 in 10,000 GEM study: Only 1 in 10,000 entrepreneurs worldwide entrepreneurs worldwide receives VS funding at start-up receives VS funding at start-up

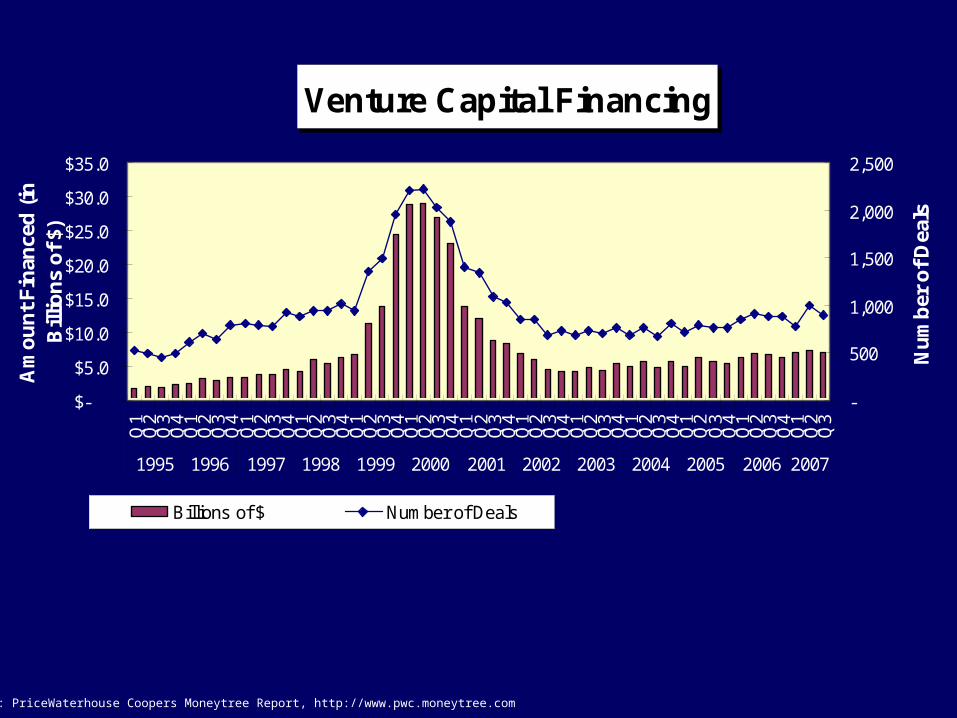

Venture Capital Financing

$-

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Am

ount

Fin

ance

d (in

B

illio

ns o

f $)

-

500

1,000

1,500

2,000

2,500

Num

ber o

f Dea

ls

Billions of $ Number of Deals

Source: PriceWaterhouse Coopers Moneytree Report, http://www.pwc.moneytree.com

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 2222Chapter 14 Equity FinancingChapter 14 Equity Financing

Venture Capital Venture Capital CompaniesCompanies Usually take an active role in managing Usually take an active role in managing

the companies in which they investthe companies in which they invest Focus their investments in specific Focus their investments in specific

industries with which they are familiarindustries with which they are familiar Invest in a company across several Invest in a company across several

stages Most common stages:stages Most common stages: ExpansionExpansion Later-stageLater-stage Early-stageEarly-stage

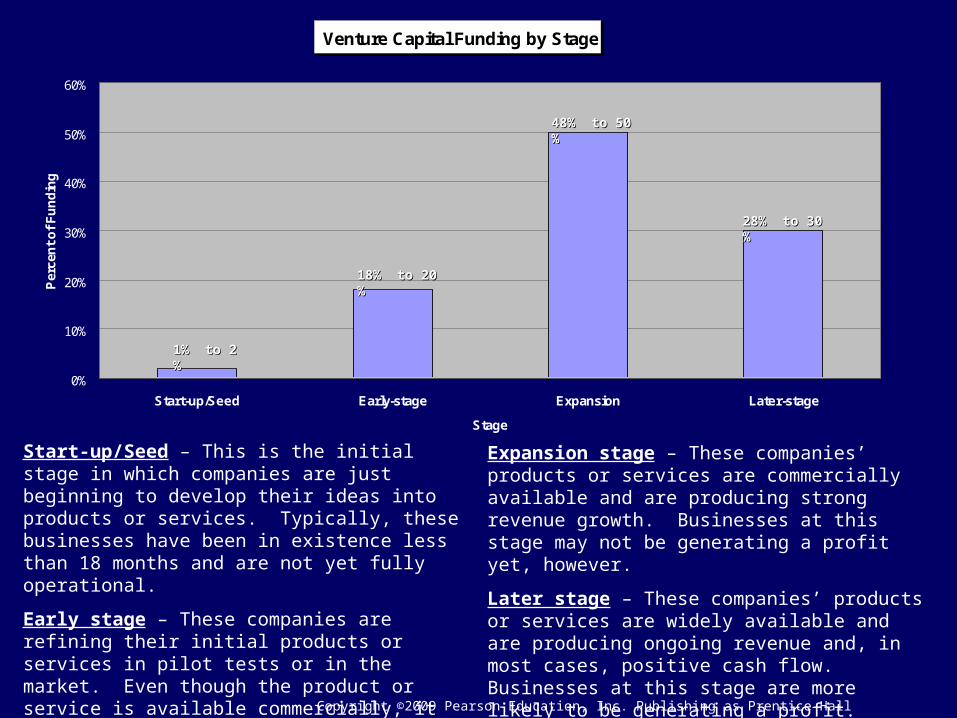

Venture Capital Funding by Stage

0%

10%

20%

30%

40%

50%

60%

Start-up/Seed Early-stage Expansion Later-stage

Stage

Perc

ent o

f Fun

ding

Start-up/Seed – This is the initial stage in which companies are just beginning to develop their ideas into products or services. Typically, these businesses have been in existence less than 18 months and are not yet fully operational.

Early stage – These companies are refining their initial products or services in pilot tests or in the market. Even though the product or service is available commercially, it typically generates little or no revenue. These companies have been in business less than three years.

1% to 2 %1% to 2 %

18% to 20 %18% to 20 %

28% to 30 %28% to 30 %

48% to 50 %48% to 50 %

Expansion stage – These companies’ products or services are commercially available and are producing strong revenue growth. Businesses at this stage may not be generating a profit yet, however.

Later stage – These companies’ products or services are widely available and are producing ongoing revenue and, in most cases, positive cash flow. Businesses at this stage are more likely to be generating a profit. Sometimes these businesses are spin-offs of already established successful private companies.

Chapter 14 Equity Financing Copyright ©2009 Pearson Education, Inc. Publishing as Prentice Hall 23

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 2424Chapter 14 Equity FinancingChapter 14 Equity Financing

What Do Venture What Do Venture CapitalCapitalCompanies Look For?Companies Look For?

Competent managementCompetent management Competitive edgeCompetitive edge Growth industryGrowth industry Viable exit strategyViable exit strategy ““Intangibles”Intangibles”

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 2525Chapter 14 Equity FinancingChapter 14 Equity Financing

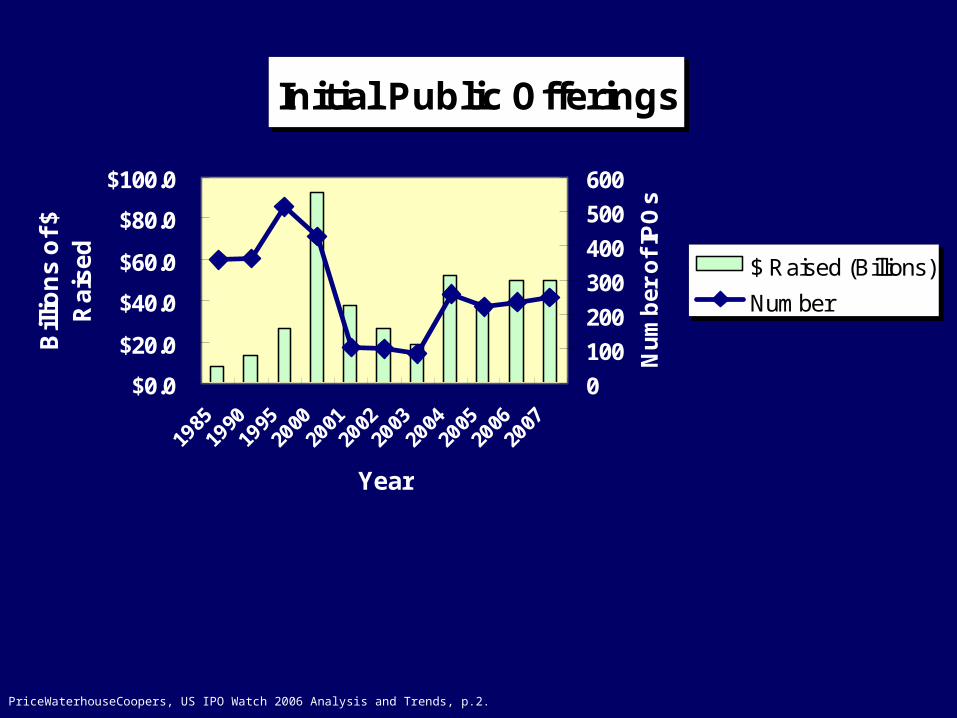

Going PublicGoing Public Initial public offering (IPO) - when Initial public offering (IPO) - when

a company raises capital by selling a company raises capital by selling shares of its stock to the public for shares of its stock to the public for the first time the first time

Since 2000, average number of Since 2000, average number of companies making IPOs is 211 companies making IPOs is 211

Few companies with annual sales Few companies with annual sales below $25 million make IPOs below $25 million make IPOs

Initial Public Offerings

$0.0$20.0

$40.0$60.0

$80.0$100.0

1985

1990

1995

2000

2001

2002

2003

2004

2005

2006

2007

Year

Bill

ions

of $

R

aise

d

0100200300400500600

Num

ber o

f IPO

s

$ Raised (Billions)Number

Source: PriceWaterhouseCoopers, US IPO Watch 2006 Analysis and Trends, p.2.

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 2727Chapter 14 Equity FinancingChapter 14 Equity Financing

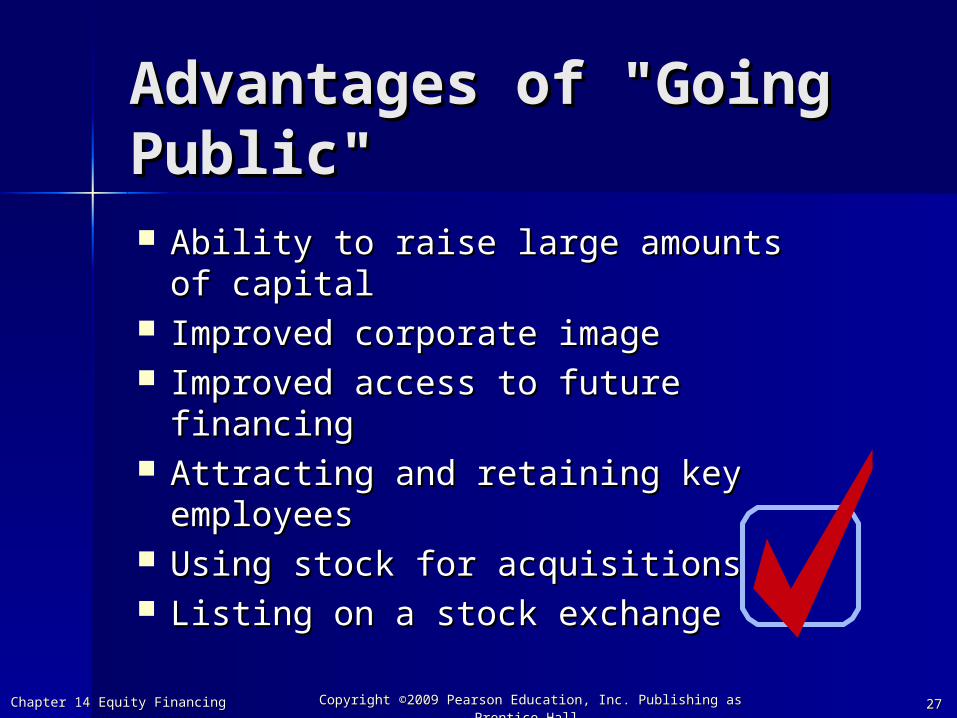

Advantages of "Going Advantages of "Going Public"Public" Ability to raise large amounts of Ability to raise large amounts of

capitalcapital Improved corporate imageImproved corporate image Improved access to future financingImproved access to future financing Attracting and retaining key Attracting and retaining key

employeesemployees Using stock for acquisitionsUsing stock for acquisitions Listing on a stock exchangeListing on a stock exchange

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 2828Chapter 14 Equity FinancingChapter 14 Equity Financing

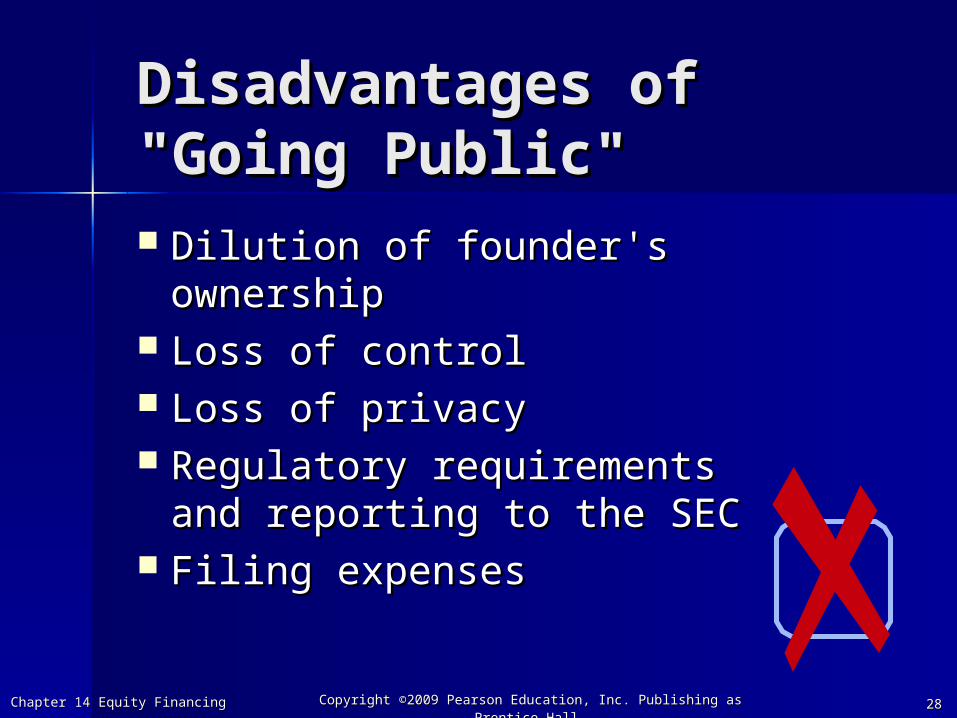

Disadvantages of Disadvantages of "Going Public""Going Public" Dilution of founder's Dilution of founder's

ownershipownership Loss of controlLoss of control Loss of privacyLoss of privacy Regulatory requirements Regulatory requirements

and reporting to the SECand reporting to the SEC Filing expensesFiling expenses

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 2929Chapter 14 Equity FinancingChapter 14 Equity Financing

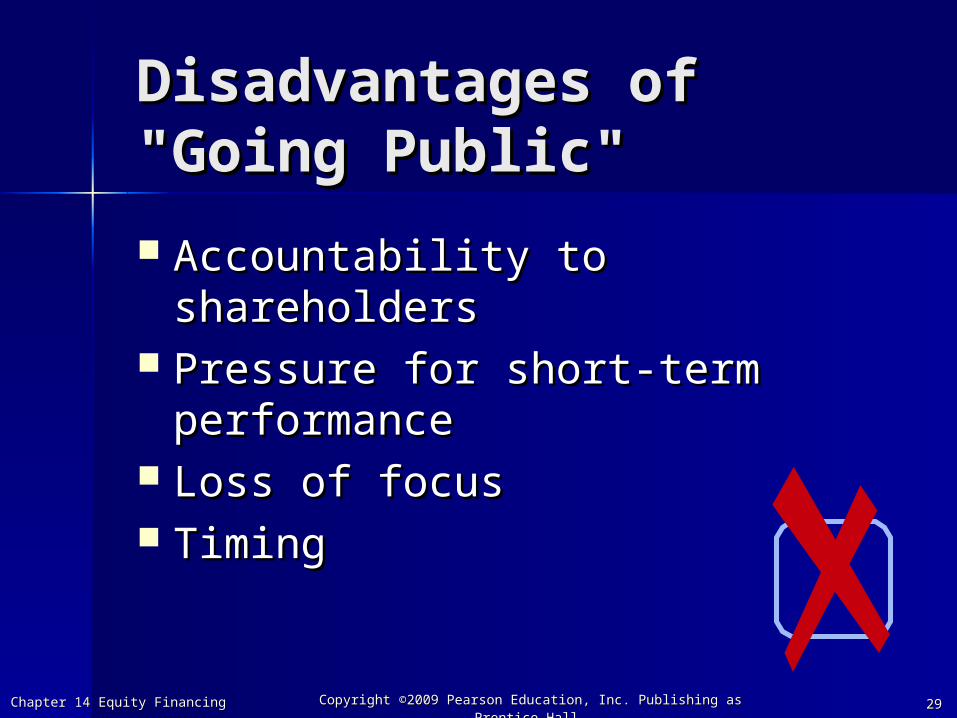

Disadvantages of Disadvantages of "Going Public""Going Public" Accountability to Accountability to

shareholdersshareholders Pressure for short-term Pressure for short-term

performanceperformance Loss of focusLoss of focus TimingTiming

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3030Chapter 14 Equity FinancingChapter 14 Equity Financing

The Registration The Registration ProcessProcess

Choose the underwriterChoose the underwriter Negotiate a letter of intentNegotiate a letter of intent

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3131Chapter 14 Equity FinancingChapter 14 Equity Financing

Letter of IntentLetter of Intent Two types of underwriting agreements:Two types of underwriting agreements:

Firm commitmentFirm commitment Best effortsBest efforts

Minimum number of shares offered is Minimum number of shares offered is usually 400,000 to 500,000usually 400,000 to 500,000

Total offering is usually at least $8 to Total offering is usually at least $8 to $15 million$15 million

Initial share price is usually between Initial share price is usually between $10 and $20 per share$10 and $20 per share

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3232Chapter 14 Equity FinancingChapter 14 Equity Financing

The Registration The Registration ProcessProcess Choose the underwriterChoose the underwriter Negotiate a letter of intentNegotiate a letter of intent Prepare the registration Prepare the registration

statementstatement File with the SECFile with the SEC Wait to “go effective” and road Wait to “go effective” and road

showshow Meet state requirementsMeet state requirements

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3333Chapter 14 Equity FinancingChapter 14 Equity Financing

Simplified Simplified RegistrationsRegistrationsand Exemptionsand Exemptions

Regulation S-BRegulation S-B S-B-1: Transitional registration for S-B-1: Transitional registration for

companies making offerings of less companies making offerings of less than $10 million over 12 monthsthan $10 million over 12 months

S-B-2: Registration for companies S-B-2: Registration for companies making offerings of more than $10 making offerings of more than $10 million over 12 monthsmillion over 12 months

Regulation D: Rule 504 - Small Regulation D: Rule 504 - Small Company Offering Registration Company Offering Registration (SCOR)(SCOR)

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3434Chapter 14 Equity FinancingChapter 14 Equity Financing

SCOR OfferingsSCOR Offerings Ceiling is $1 millionCeiling is $1 million Share price must be at least $5 per Share price must be at least $5 per

shareshare Must file Form U-7, a standardized Must file Form U-7, a standardized

disclosure statementdisclosure statement Can issue almost any kind of security Can issue almost any kind of security

through SCORthrough SCOR Cost is usually less than $25,000Cost is usually less than $25,000

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3535Chapter 14 Equity FinancingChapter 14 Equity Financing

Regulation D: Rule 505 and 506Regulation D: Rule 505 and 506 Private placementsPrivate placements

Section 4 (6)Section 4 (6) Rule 147 (Intrastate offerings)Rule 147 (Intrastate offerings) Regulation ARegulation A

Offerings up to $5 million over 12 Offerings up to $5 million over 12 monthsmonths

Typical cost: $80,000 to $120,000Typical cost: $80,000 to $120,000

Simplified Simplified RegistrationsRegistrationsand Exemptionsand Exemptions

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3636Chapter 14 Equity FinancingChapter 14 Equity Financing

Direct Stock Offerings Direct Stock Offerings Go straight to Main Street instead of Go straight to Main Street instead of

through underwriters on Wall Streetthrough underwriters on Wall Street World Wide Web (usually either World Wide Web (usually either

Regulation A or Regulation D offerings)Regulation A or Regulation D offerings) Typically generate between $300,000 Typically generate between $300,000

and $4 million for companyand $4 million for company Foreign Stock MarketsForeign Stock Markets

Simplified Simplified RegistrationsRegistrationsand Exemptionsand Exemptions

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3737Chapter 14 Equity FinancingChapter 14 Equity Financing

Web SitesWeb Sites PriceWaterhouseCoopers Money PriceWaterhouseCoopers Money

Tree SurveyTree Surveyhttp://www.pwcmoneytree.com/http://www.pwcmoneytree.com/

Hoover’s Online IPO CentralHoover’s Online IPO Central

http://www.hoovers.com/global/ipochttp://www.hoovers.com/global/ipoc/index.xhtml/index.xhtml

Active CapitalActive Capitalhttp://activecapital.org/http://activecapital.org/

Copyright Copyright ©©2009 Pearson Education, Inc. Publishing as Prentice Hall2009 Pearson Education, Inc. Publishing as Prentice Hall 3838Chapter 14 Equity FinancingChapter 14 Equity Financing

All rights reserved. No part of this publication may All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, electronic, mechanical, photocopying, recording, or otherwise, without the prior written or otherwise, without the prior written permission of the publisher. Printed in the United permission of the publisher. Printed in the United States of America.States of America.

Copyright ©2009 Pearson Education, Copyright ©2009 Pearson Education, Inc. Publishing as Prentice HallInc. Publishing as Prentice Hall

Related Documents