Chapter 14 & 15 Capital Markets and Investment Underwriting

Chapter 14 & 15 Capital Markets and Investment Underwriting.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 14 & 15

Capital Markets and Investment Underwriting

Agenda for today

By issuing financial instruments such as corporate bonds, common stock and preferred shares, a company may raise capital from the public.

Today’s agenda focus on

where and how to issue those financial instruments

Basic Knowledge

To issue financial instruments, we need to know about the followings:

1. Financial System

2. Market Efficiency

3. Underwriting

1. Financial System

Conceptually, a financial system consists of Providers of Capital - mainly householdsUsers of Capital - governments & businessesThe providers and users of capital are linked together by financial intermediaries such as commercial banks, trust companies, mutual funds, pension funds, insurance companies, etc

Role of Financial Intermediaries

Match supply and demand of Capital

Provide related services

Bank services - deposits, loans, currency exchange, international transfer of fund, etc

Trust company services - common stock transfer agent, handling dividend payments, managing clients’ assets, acting for bondholders, etc

Financial Market

A financial market is where the exchange between capital users and providers takes place. It may be classified into

Money market - short-term capital with maturity less than a year, e.g. T-bills, commercial papers, bankers’ acceptances

Capital market - long-term capital with maturity greater than a year, e.g. bonds, common stocks, preferred shares

Where is the Financial Market?

Wall Street in the States or Bay Street in Canada where the financial intermediaries gatherOrganized Exchanges - NYSE or TSX which facilitate the trading of various securities through a competitive auction mechanismOver The Counter Markets - OTC which is a network of brokers and dealers (big players)linked electronically for the trading of mainly bonds and money market securities (10 times the vol of OEs)

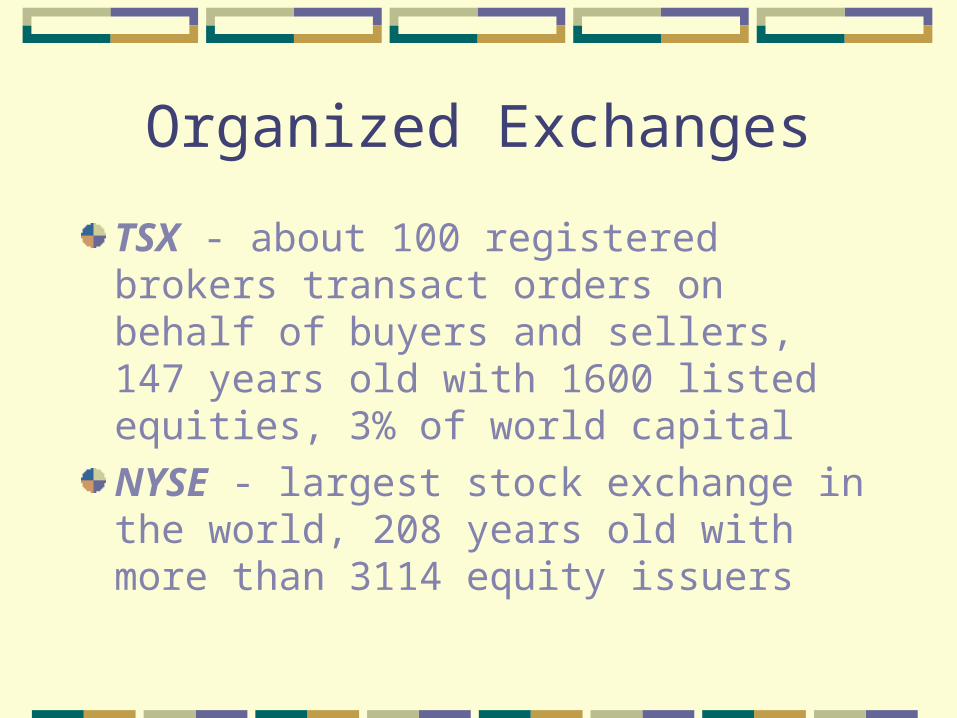

Organized Exchanges

TSX - about 100 registered brokers transact orders on behalf of buyers and sellers, 147 years old with 1600 listed equities, 3% of world capital

NYSE - largest stock exchange in the world, 208 years old with more than 3114 equity issuers

OTC Markets

Canadian Dealing Network

NASDAQ -the National Association of Securities Dealers Automated Quotation System

Is the market efficient enough?

With so many participants in the financial system, we will ask if the market is efficient enough to deal with them

By that, we mean the supply is able to meet the demand or vice versa and the price is a fair market price (i.e. no undue cost for capital users and no consistent abnormal returns for capital providers)

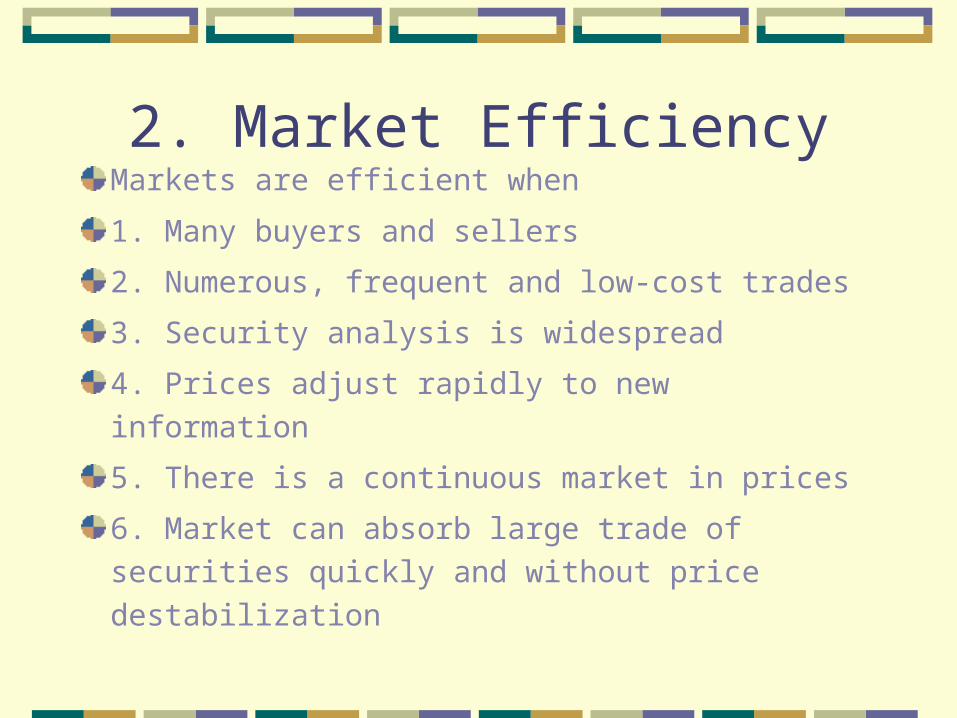

2. Market EfficiencyMarkets are efficient when

1. Many buyers and sellers

2. Numerous, frequent and low-cost trades

3. Security analysis is widespread

4. Prices adjust rapidly to new information

5. There is a continuous market in prices

6. Market can absorb large trade of securities

quickly and without price destabilization

Market Efficiency Hypothesis

Weak form - current market prices reflect all the information contained in past transactions (historic information), no abnormal return derived from “chartists”

Semi-strong form - security prices adjust rapidly and fully to reflect all publicly available information including historic, current and future information, no abnormal return derived from outsiders (the general public)

Market Efficiency Hypothesis cont’

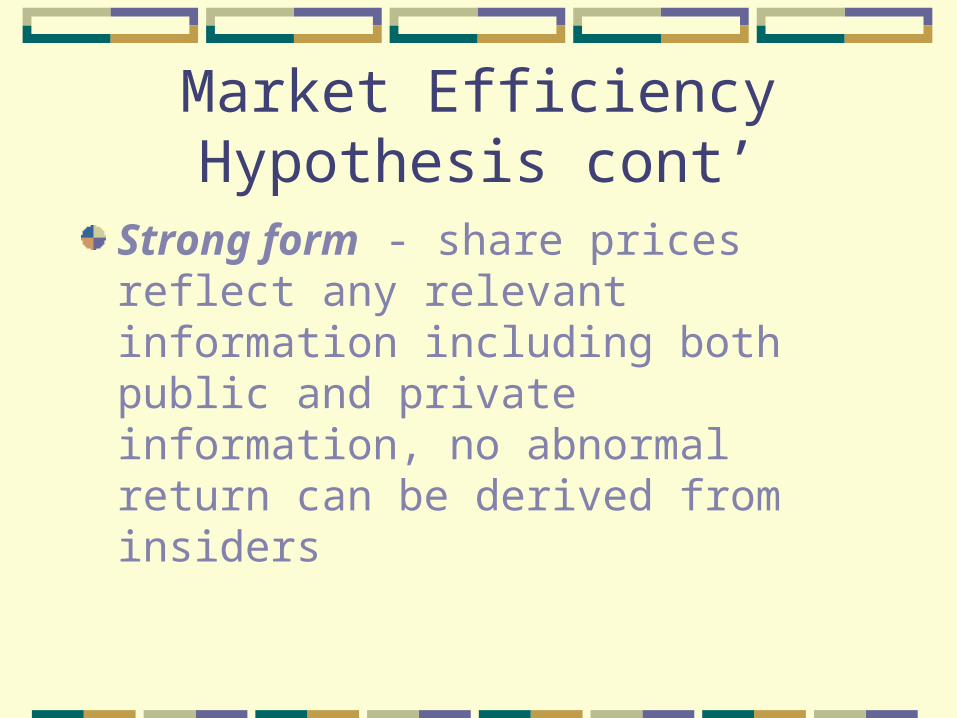

Strong form - share prices reflect any relevant information including both public and private information, no abnormal return can be derived from insiders

Empirical Support

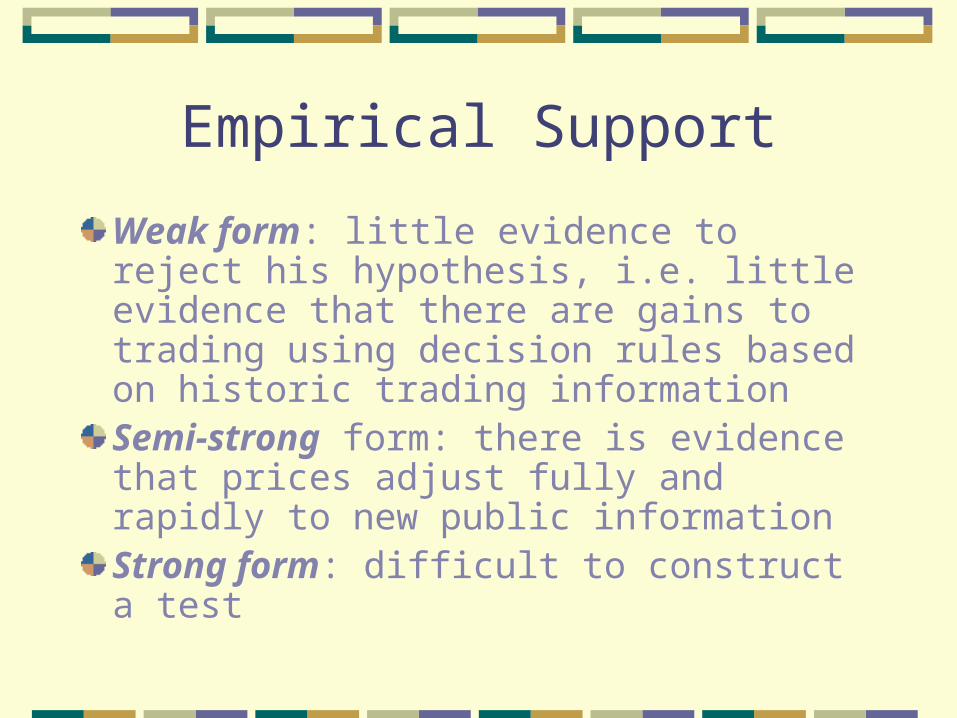

Weak form: little evidence to reject his hypothesis, i.e. little evidence that there are gains to trading using decision rules based on historic trading informationSemi-strong form: there is evidence that prices adjust fully and rapidly to new public informationStrong form: difficult to construct a test

What is the conclusion?

No definite conclusion has been made

A good topic for your Ph.D. thesis

Anyway, it seems that the markets are efficient in the semi-strong form

Underwriting

Now you know where to go to raise capital for your company and believe that the market is efficient enough

The second question is: how to raise capital

To answer this question, we need to know the underwriting mechanism

Investment Bankers

The financial intermediary between corporations and investors in general is the Investment BankersExamples: JP Morgan, Goldman SachsInvestment Bankers bring the two parties (capital users and providers) together by channeling money from one to the other

Functions of Investment Bankers

Underwriter function:- buying the security from the large corporate

issuers and reselling it to the public (Firm Commitment or Bought Deal)

- Selling security on commission basis (Best Effort - act as the agent of the issuers – small or new firms)

- Function being carried out by syndicate of investment bankers

Functions of Inv. Bankers cont’

Market maker function:- To create an available market by buying

and selling the security- To initiate trading of a new security- To inform the investors the issuance of

a new security through market trading

Functions of Inv. Bankers cont’

Advisor function:- advice on securities issues, mergers

and acquisitions, leveraged buyouts, corporate restructuring, etcBroker function:

- transact orders on behalf of buyers and sellers,

The Underwriting Process

Let’s focus on one specific area of raising capital – through IPO

Initial public offering refers to the sale of common shares to the public by the issuing firm for the first time

We say the issuing firm is ‘going public’

Advantages of going public

Greater availability of fundsPrestigeHigher liquidity for shareholders (buy and sell in the secondary market)Established price of public issues aids a shareholder’s estate planningEnables a firm to engage in merger activities more readily

Disadvantages of going public

Company information must be made public

Accumulating and disclosing information is expensive

Short-term pressure from security analysts

Embarrassment from public failure

High cost of going public (e.g. underwriting spread and flotation costs)

Underwriting Spread

Spread represents the compensation for those participating in the distribution of IPO

Spread = Public price – Issue offer price

It is shared among the participants

Spread on common stocks is greater than spread on bonds

Summary

In this class, we focus on where and how to issue financial instruments Where to go:

- Financial system consists of capital users, providers and financial intermediaries

- Markets seem to be efficient- How to issue:- Investment bankers and Underwriting

process

Related Documents