Chapter 12 1 CHAPTER 12 CONSUMER AND SMALL BUSINESS LENDING

Chapter 121 CHAPTER 12 CONSUMER AND SMALL BUSINESS LENDING.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 12 1

CHAPTER 12

CONSUMER AND SMALL BUSINESS LENDING

Chapter 12 2

LEARNING OBJECTIVES

The markets for and importance of small-business lending, consumer installment lending, residential mortgages, and home-equity lines of credit

The credit analysis, pricing, and risks of small-business, consumer, and residential-mortgage lending

Credit scoring for consumers and small businesses and how it can be misused

The importance and growth of subprime lending and the outcry about “predatory practices” and attempts to regulate them

The future of consumer and small-business lending

TO UNDERSTAND…

Chapter 12 3

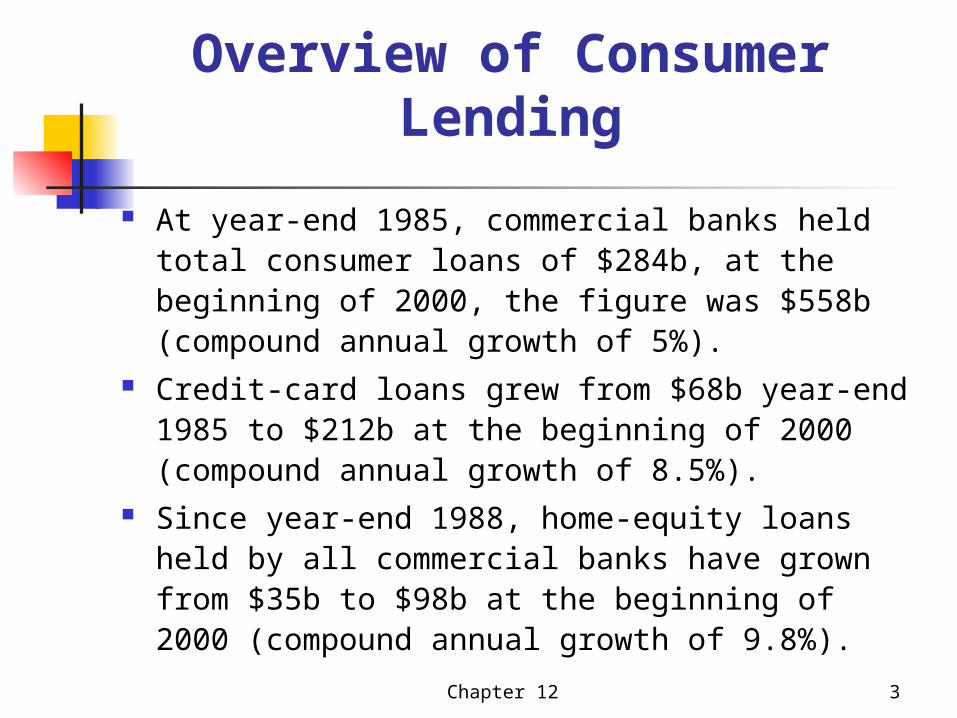

Overview of Consumer Lending

At year-end 1985, commercial banks held total consumer loans of $284b, at the beginning of 2000, the figure was $558b (compound annual growth of 5%).

Credit-card loans grew from $68b year-end 1985 to $212b at the beginning of 2000 (compound annual growth of 8.5%).

Since year-end 1988, home-equity loans held by all commercial banks have grown from $35b to $98b at the beginning of 2000 (compound annual growth of 9.8%).

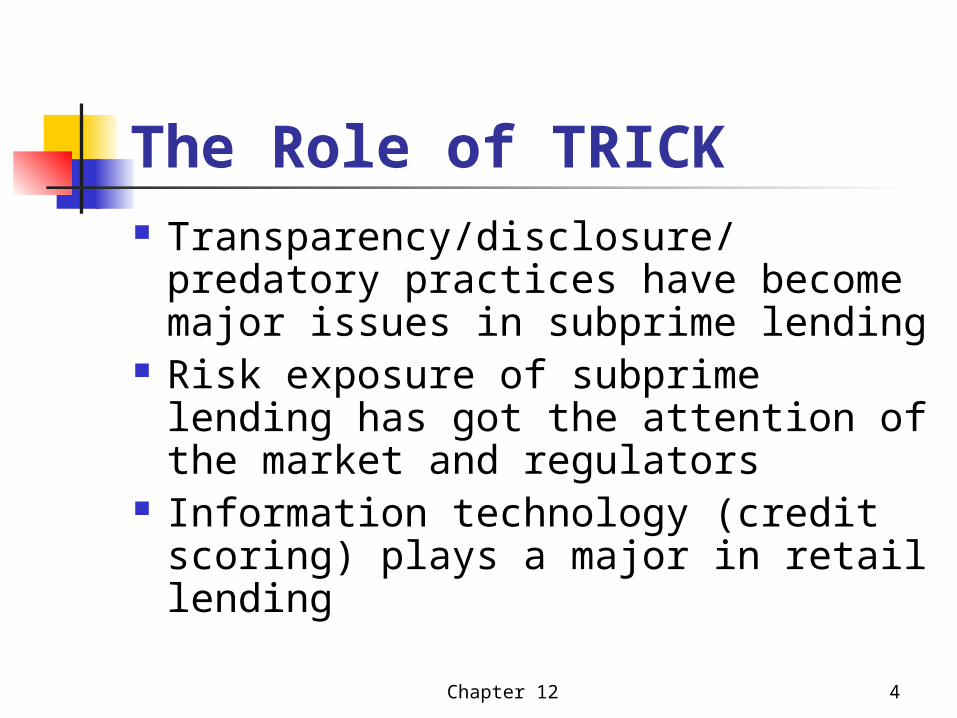

Chapter 12 4

The Role of TRICK Transparency/disclosure/predatory

practices have become major issues in subprime lending

Risk exposure of subprime lending has got the attention of the market and regulators

Information technology (credit scoring) plays a major in retail lending

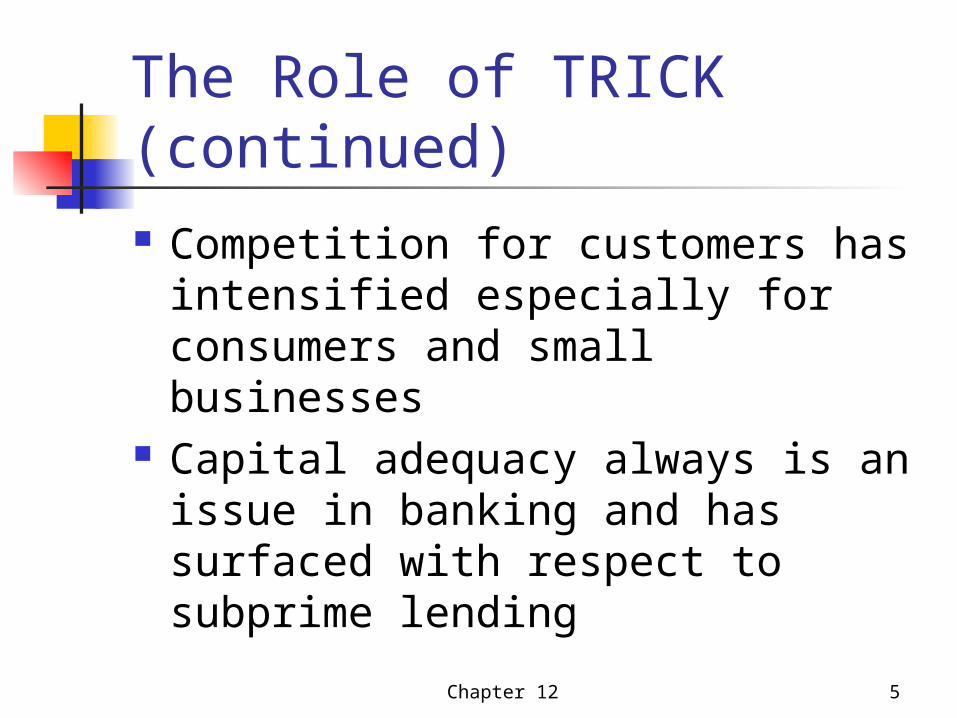

Chapter 12 5

The Role of TRICK (continued) Competition for customers has

intensified especially for consumers and small businesses

Capital adequacy always is an issue in banking and has surfaced with respect to subprime lending

Chapter 12 6

Securitization Started with government-

sponsored enterprises (GSEs such as Ginnie Mae, Fannie Mae, and Freddie Mac) and the residential-mortgage market

Trickled down to credit cards and auto loans

Chapter 12 7

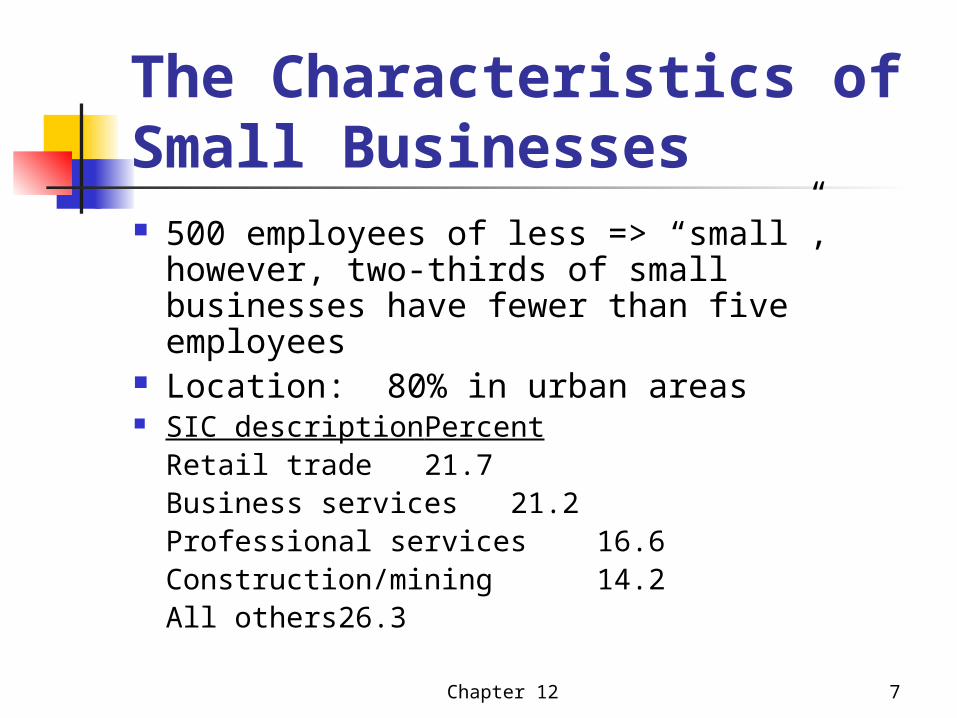

The Characteristics of Small Businesses 500 employees of less => “small”,

however, two-thirds of small businesses have fewer than five employees

Location: 80% in urban areas SIC description Percent

Retail trade 21.7Business services 21.2Professional services 16.6Construction/mining 14.2All others 26.3

Chapter 12 8

Financial Services Usedby Small Businesses

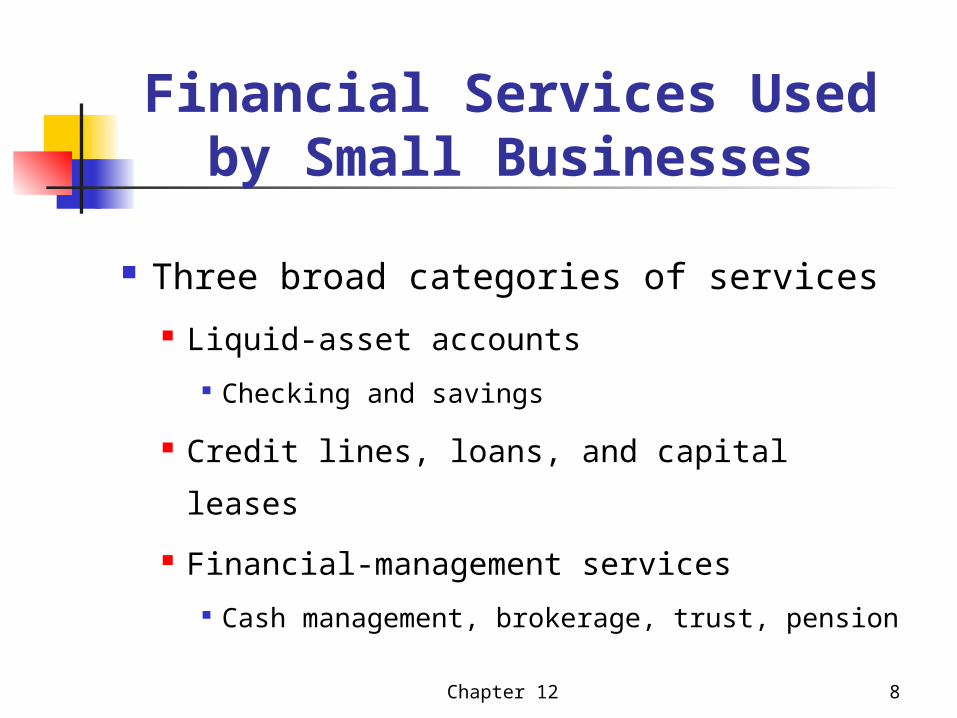

Three broad categories of services

Liquid-asset accounts Checking and savings

Credit lines, loans, and capital leases

Financial-management services Cash management, brokerage, trust,

pension

Chapter 12 9

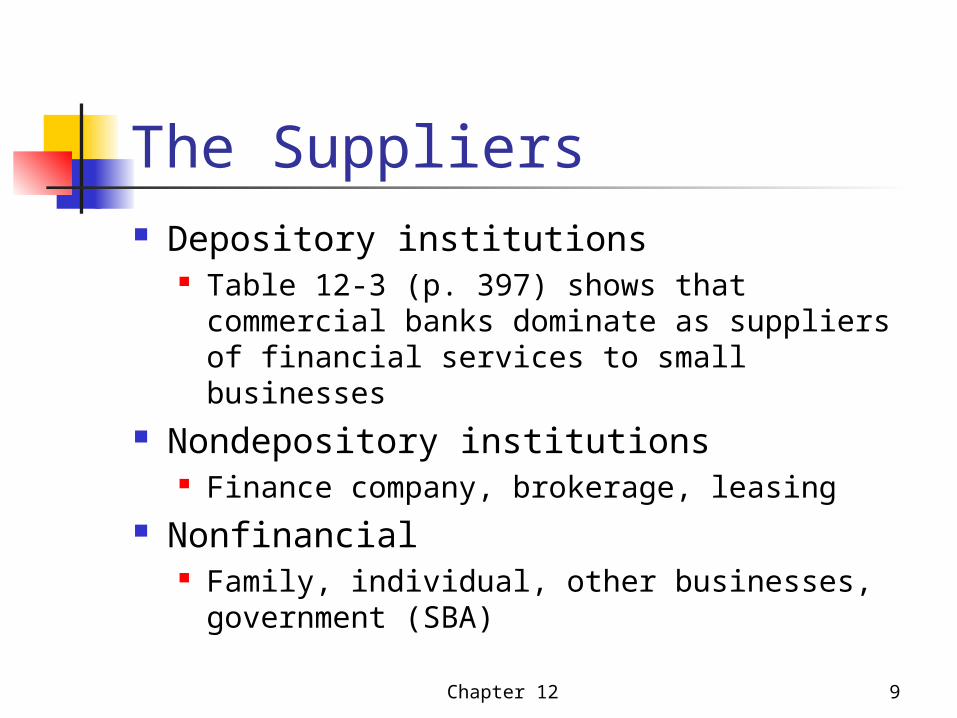

The Suppliers Depository institutions

Table 12-3 (p. 397) shows that commercial banks dominate as suppliers of financial services to small businesses

Nondepository institutions Finance company, brokerage, leasing

Nonfinancial Family, individual, other businesses,

government (SBA)

Chapter 12 10

Credit Analysis and Credit Scoring Evolution from the 5Cs to credit scoring

for consumers Small businesses stand on the far left-

hand side of the borrower-information continuum (Ch. 10) – scare information that is costly to obtain

Fewer than five employees => 5Cs approach might be best, especially character

Chapter 12 11

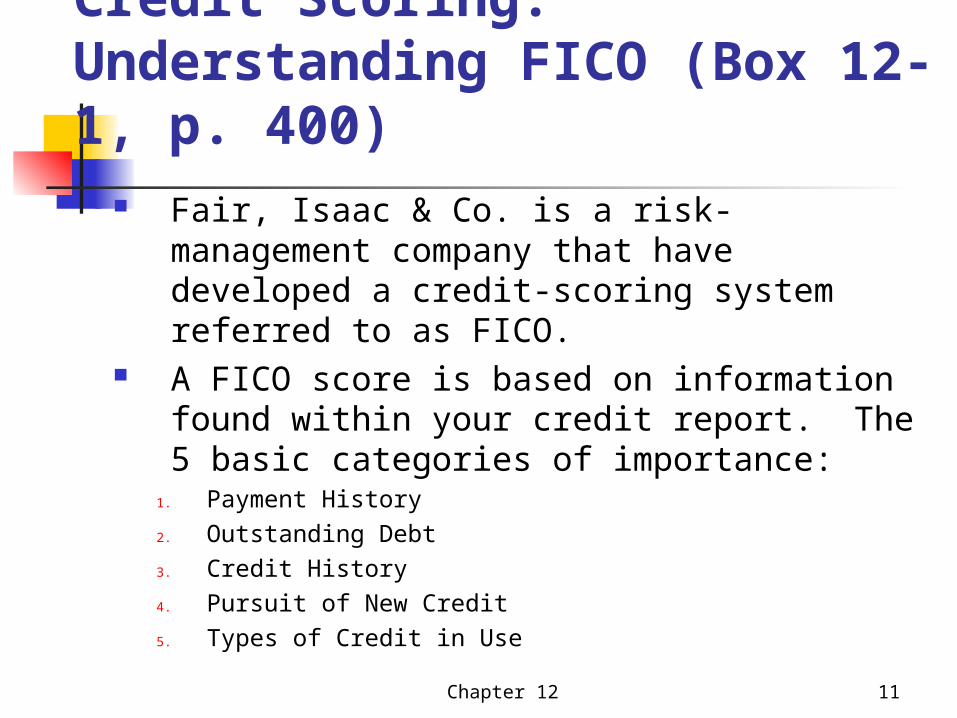

Credit Scoring: Understanding FICO (Box 12-1, p. 400)

Fair, Isaac & Co. is a risk-management company that have developed a credit-scoring system referred to as FICO.

A FICO score is based on information found within your credit report. The 5 basic categories of importance:

1. Payment History2. Outstanding Debt3. Credit History4. Pursuit of New Credit5. Types of Credit in Use

Chapter 12 12

Credit Scoring and Decision-Making Figure 12-1 (p. 401) illustrates the

trade-off at origination between credit score and the loan-to-value (LTV) ratio

Don’t short change the importance of human judgment

Chapter 12 13

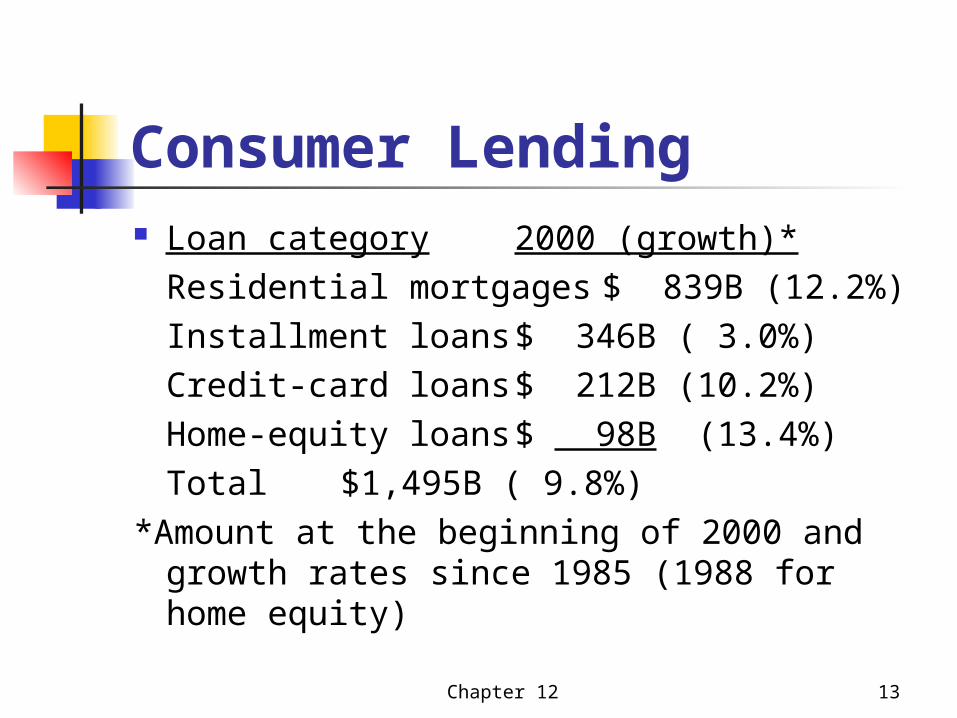

Consumer Lending Loan category 2000 (growth)*

Residential mortgages $ 839B (12.2%)Installment loans $ 346B ( 3.0%)Credit-card loans $ 212B (10.2%)Home-equity loans $ 98B (13.4%)Total $1,495B ( 9.8%)

*Amount at the beginning of 2000 and growth rates since 1985 (1988 for home equity)

Chapter 12 14

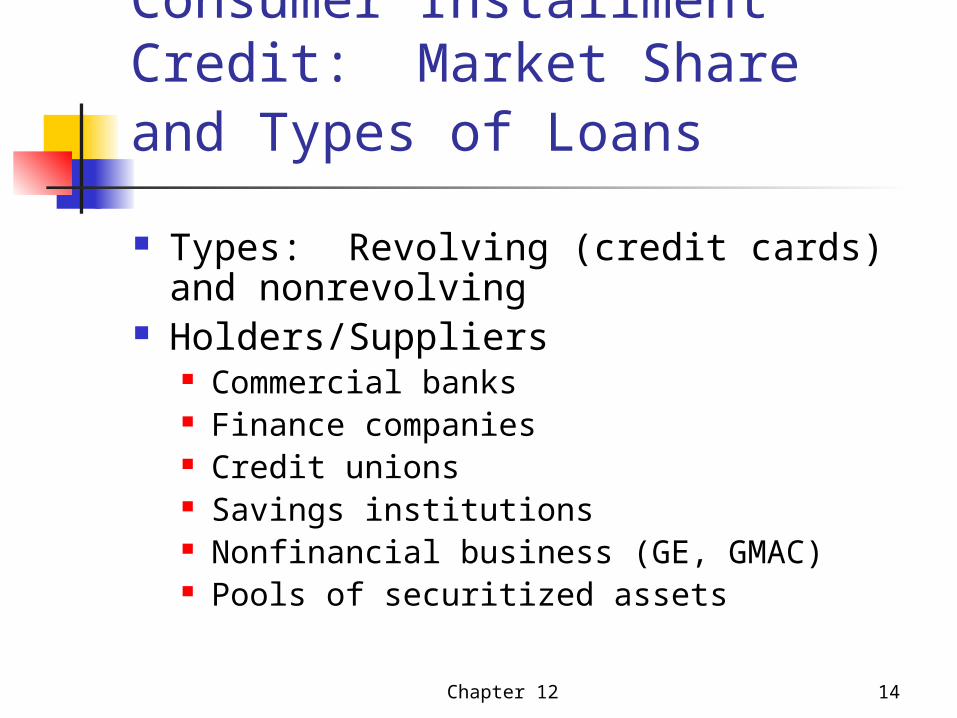

Consumer Installment Credit: Market Share and Types of Loans

Types: Revolving (credit cards) and nonrevolving

Holders/Suppliers Commercial banks Finance companies Credit unions Savings institutions Nonfinancial business (GE, GMAC) Pools of securitized assets

Chapter 12 15

The Cost of Making Consumer Loans (functional cost analysis)

Cost categories Office space Supplies Services Labor

Tables 12-9, 12-10, 12-11 (pp. 408-410) present FCA data

Chapter 12 16

Credit Analysis ForConsumer Lending

Five stages in the analysis of new customers:

1. Initial contact or introduction,

2. Credit application,

3. Review of the application,

4. Credit analysis or evaluation, and

5. Monitoring and control

Chapter 12 17

CAMPARI

An alternative to the five Cs of credit analysis is CAMPARI. In contrast to the five Cs, the CAMPARI framework is more specific with respect to the purpose and terms:

Character – the first of the five Cs Ability – in managing financial affairs Margin – interest rate, commission, and fees Purpose – of the loan Amount – of the loan Repayment – probability of Insurance – the collateral component of the five Cs

Chapter 12 18

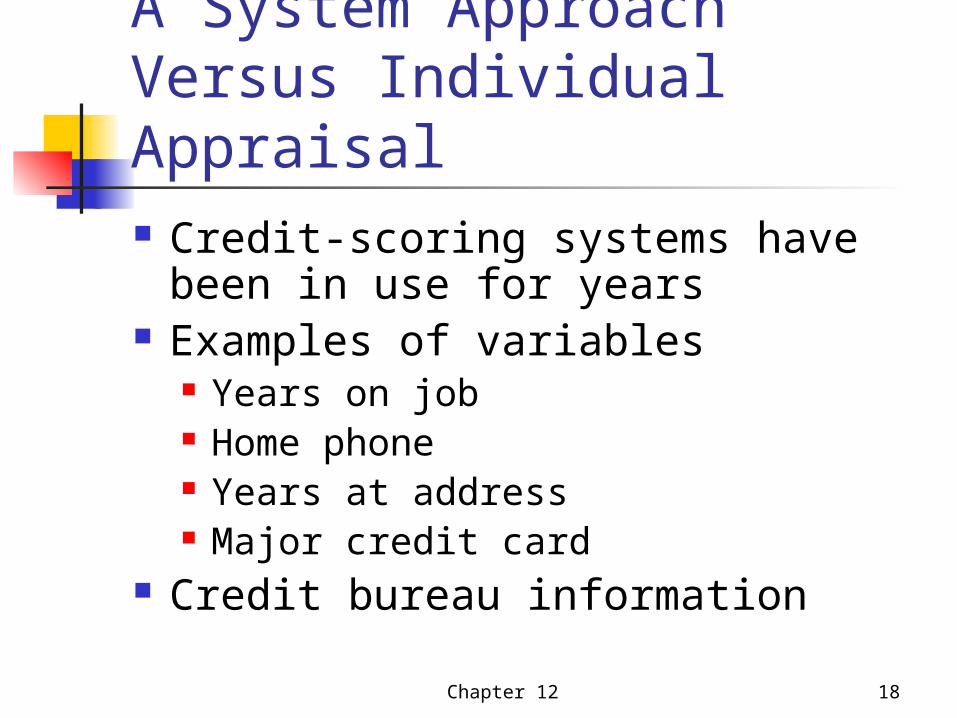

A System Approach Versus Individual Appraisal Credit-scoring systems have been

in use for years Examples of variables

Years on job Home phone Years at address Major credit card

Credit bureau information

Chapter 12 19

Predicting Personal Bankruptcy Research frameworks similar to

those used in predicting corporate bankruptcy (classification models, Ch. 11)

Three national credit bureaus predict personal bankruptcies Equifax Trans Union TRW

Chapter 12 20

Residential Real-Estate Lending:

Mortgages and Home-Equity Lines of Credit

One of the biggest changes in bank consumer lending has resulted from the restructuring of the savings-and-loan industry.

At the end of 1985, all commercial banks held $188b in loans backed by one-to-four family residential property. In 1999, it was $767b or annual growth of 10.6%.

Chapter 12 21

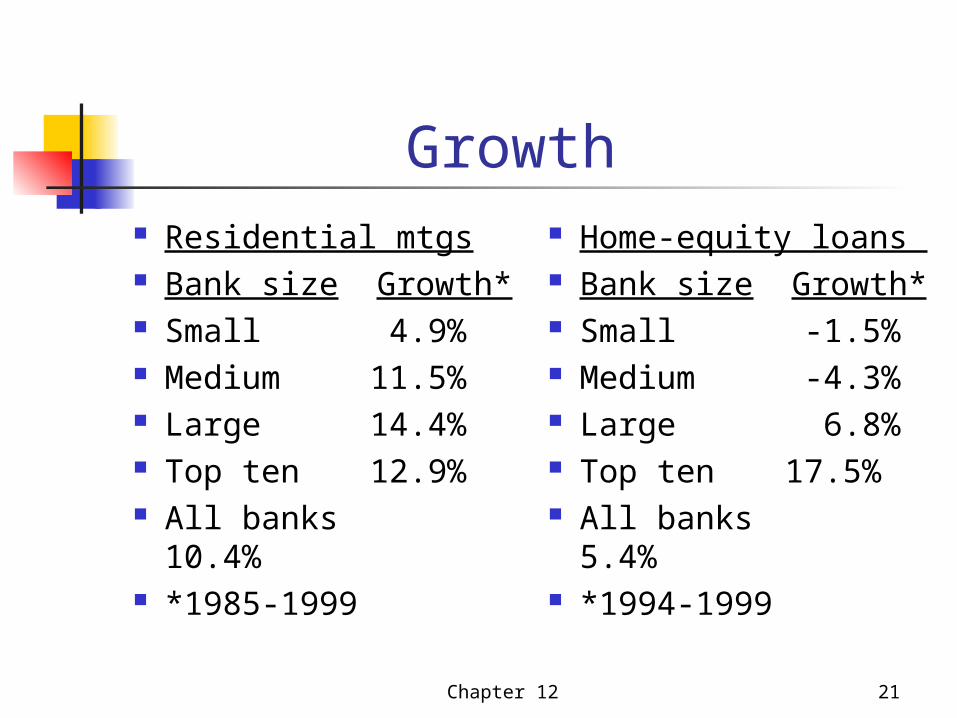

Growth Residential mtgs Bank size Growth* Small 4.9% Medium 11.5% Large 14.4% Top ten 12.9% All banks 10.4% *1985-1999

Home-equity loans Bank size Growth* Small -1.5% Medium -4.3% Large 6.8% Top ten 17.5% All banks 5.4% *1994-1999

Chapter 12 22

The Restructuring of Residential Lending Fragmentation of the mortgage-

lending process (securitization steps) Origination Funding/underwriting Selling Servicing Investor

Chapter 12 23

Subprime Lending

Subprime portfolios are those made up of loans to borrowers with higher-risk characteristics defined to include:

A FICO score of 660 or lower Two or more 30-day delinquencies in the

past year Bankruptcy in the last five years A debt-to-income ratio of 50% or higher A foreclosure, repossession, or charge-off

in the preceding 24 months

Chapter 12 24

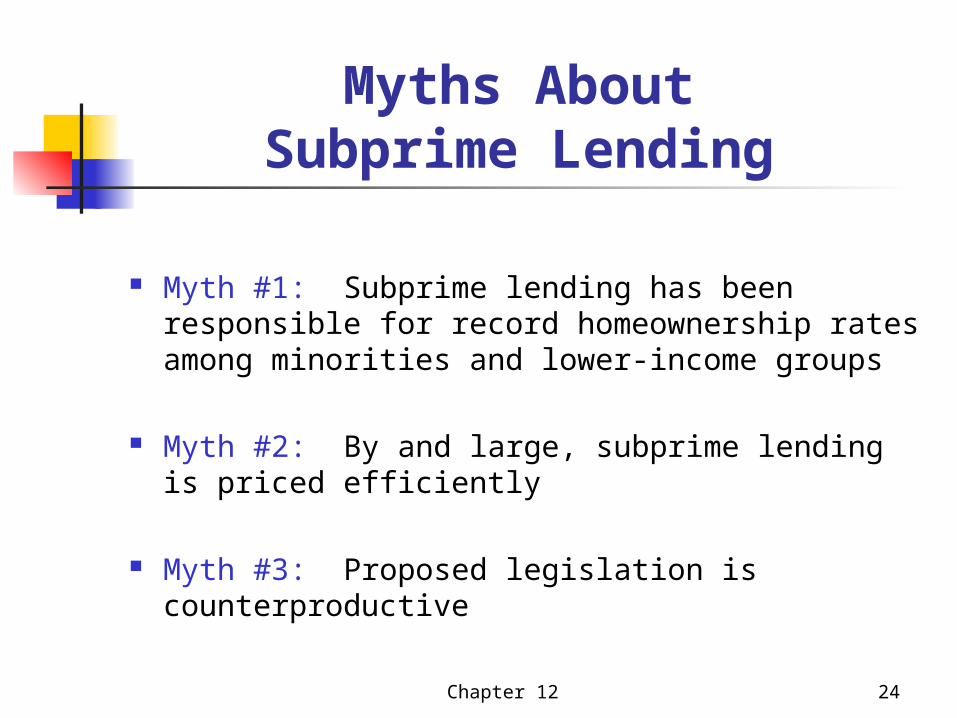

Myths AboutSubprime Lending

Myth #1: Subprime lending has been responsible for record homeownership rates among minorities and lower-income groups

Myth #2: By and large, subprime lending is priced efficiently

Myth #3: Proposed legislation is counterproductive

Chapter 12 25

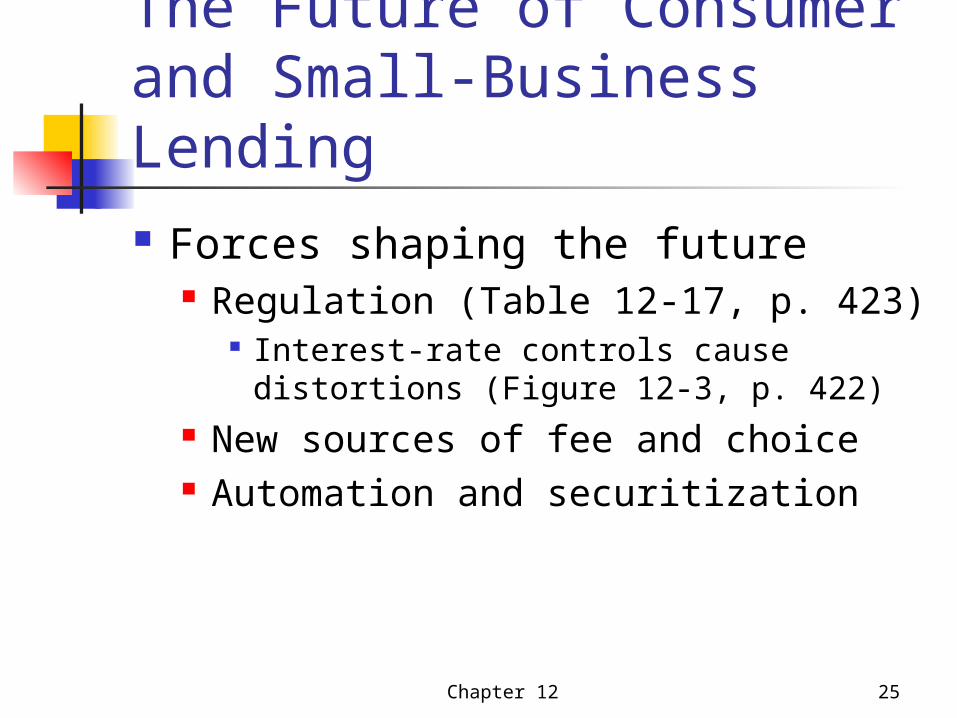

The Future of Consumer and Small-Business Lending Forces shaping the future

Regulation (Table 12-17, p. 423) Interest-rate controls cause distortions

(Figure 12-3, p. 422) New sources of fee and choice Automation and securitization

Chapter 12 26

Consumer Banking Innovations

Credit and debit cards

ATMs that permit cash advances

(loans)

Systems approaches to lending

Home-equity loans

On-line banking

Chapter 12 27

CHAPTER SUMMARY Consumer and small-business

lending Installment loans (credit cards) Residential mortgages Home-equity lines of credit Loans and financial services for small

businesses Credit scoring and securitization Subprime lending

Related Documents