Chapter 10: The Basics Of Capital Budgeting

Chapter 10: The Basics Of Capital Budgeting. 2 The Basics Of Capital Budgeting :

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 10:

The Basics Of Capital Budgeting

2

The Basics Of Capital Budgeting :

3

Chapter Outline: Introduction. Capital Budgeting Decision Rules:

Payback Period.Discounted payback Period. Net Present Value (NPV).Internal Rate of Return (IRR).Profitability Index (PI).

4

Capital Budgeting:

The process of planning expenditures on assets whose cash flows are expected to extend beyond one year.

5

Capital Budgeting:

Analysis of potential additions to fixed assets.

Long-term decisions; involve large expenditures.

Very important to firm’s future.

6

Steps to Capital Budgeting:

1. Estimate Cash Flow (inflows & outflows).

2. Assess riskiness of CFs.

3. Determine the appropriate cost of capital.

4. Find NPV and/or IRR.

5. Accept if NPV > 0 and/or IRR > WACC.

7

Payback Period:

The number of years required to recover a project’s cost, or “How long does it take to get our money back?”

8

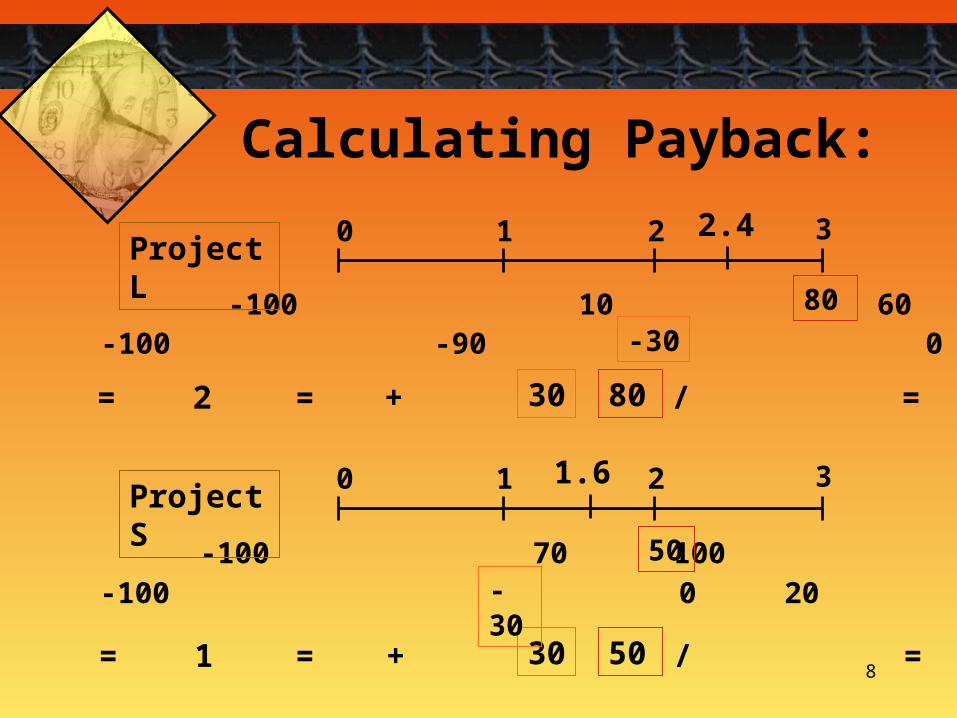

Calculating Payback:

PaybackL = 2 + / = 2.375 years

CFt -100 10 60 100Cumulative -100 -90 0 50

0 1 2 3

=

2.4

30 80

80

-30

Project L

PaybackS = 1 + / = 1.6 years

CFt -100 70 100 20Cumulative -100 0 20 40

0 1 2 3

=

1.6

30 50

50-30

Project S

9

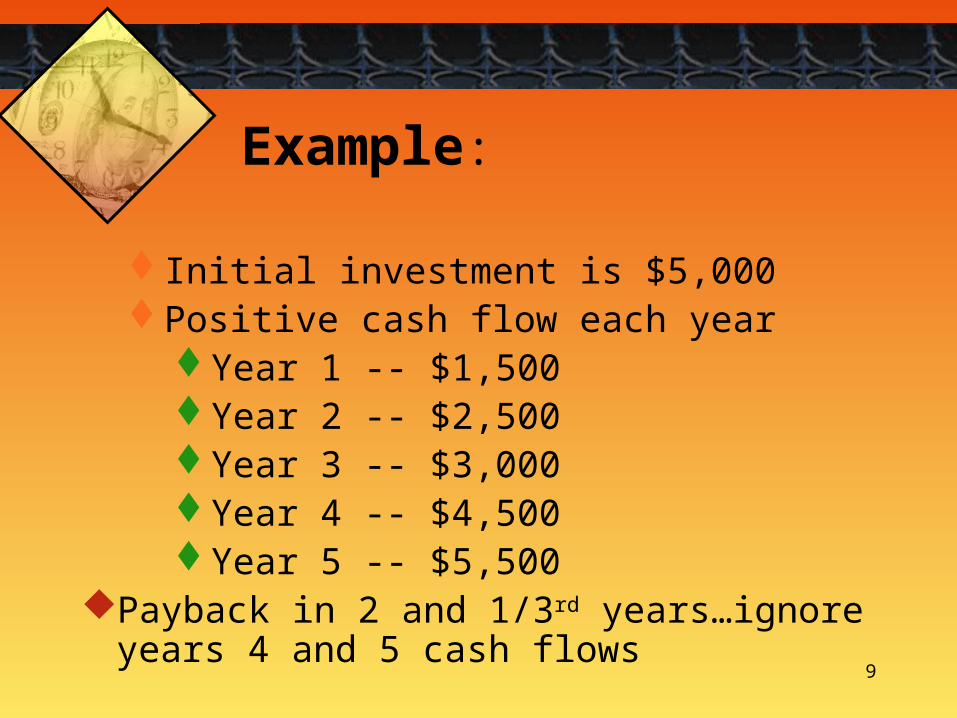

Example:

Initial investment is $5,000Positive cash flow each year

Year 1 -- $1,500Year 2 -- $2,500Year 3 -- $3,000Year 4 -- $4,500Year 5 -- $5,500

Payback in 2 and 1/3rd years…ignore years 4 and 5 cash flows

10

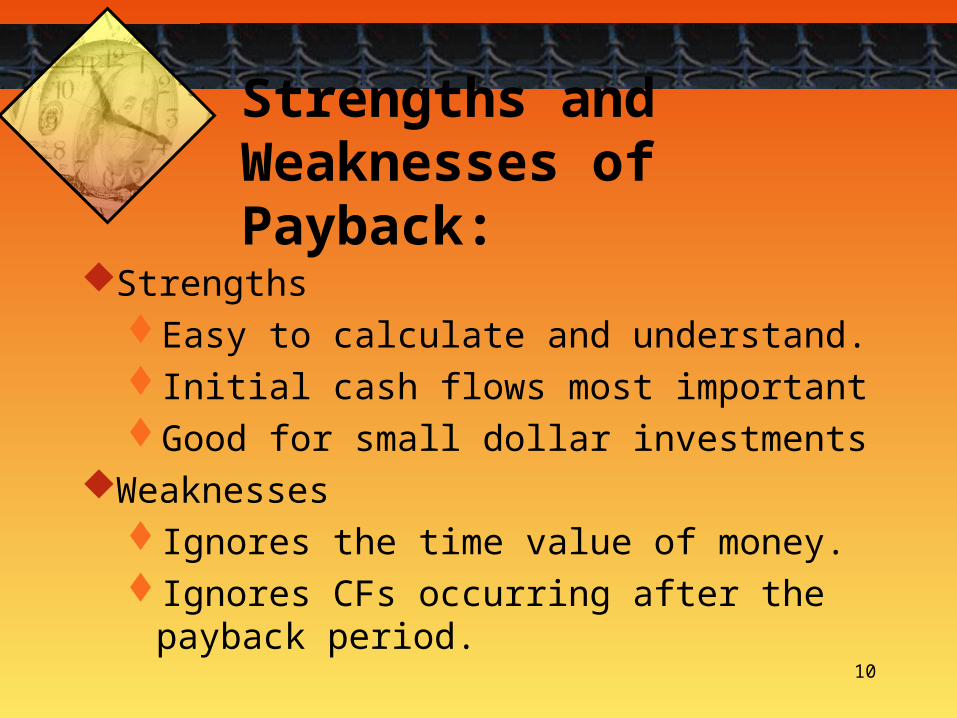

Strengths and Weaknesses of Payback:

StrengthsEasy to calculate and understand.Initial cash flows most importantGood for small dollar investments

WeaknessesIgnores the time value of money.Ignores CFs occurring after the payback

period.

11

Discounted Payback Period:

Attempt to correct one flaw of Payback Period…time value of money

Discount cash flow to present and see if the discount cash flow are sufficient to cover initial cost within cutoff time period

Careful in consistencyDiscounting means cash flow at end of periodAppropriate discount rate for cash flow

12

Discounted payback period:

Uses discounted cash flows rather than raw CFs.

Disc PaybackL = 2 + / = 2.7 years

CFt -100 10 60 80

Cumulative -100 -90.91 18.79

0 1 2 3

=

2.7

60.11

-41.32

PV of CFt -100 9.09 49.59

41.32 60.11

10%

13

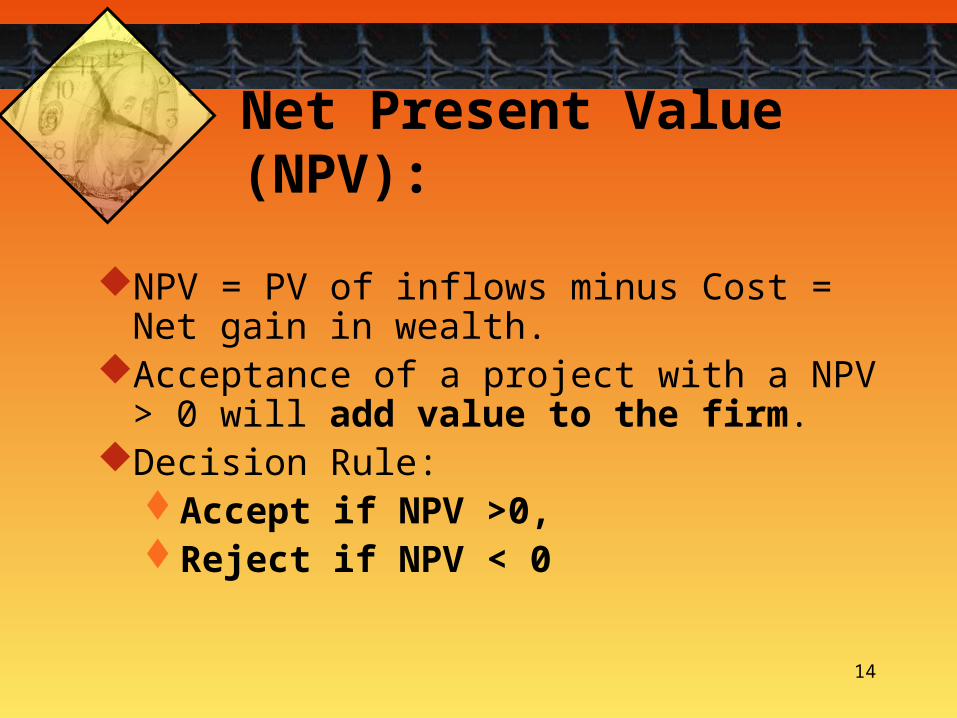

Net Present Value (NPV):

Correction to discounted cash flowIncludes all cash flow in decisionChanges decision (go vs. no-go) to

dollars, not arbitrary cutoff period Need all cash flow Need appropriate discount rate

14

Net Present Value (NPV):

NPV = PV of inflows minus Cost = Net gain in wealth.

Acceptance of a project with a NPV > 0 will add value to the firm.

Decision Rule: Accept if NPV >0, Reject if NPV < 0

15

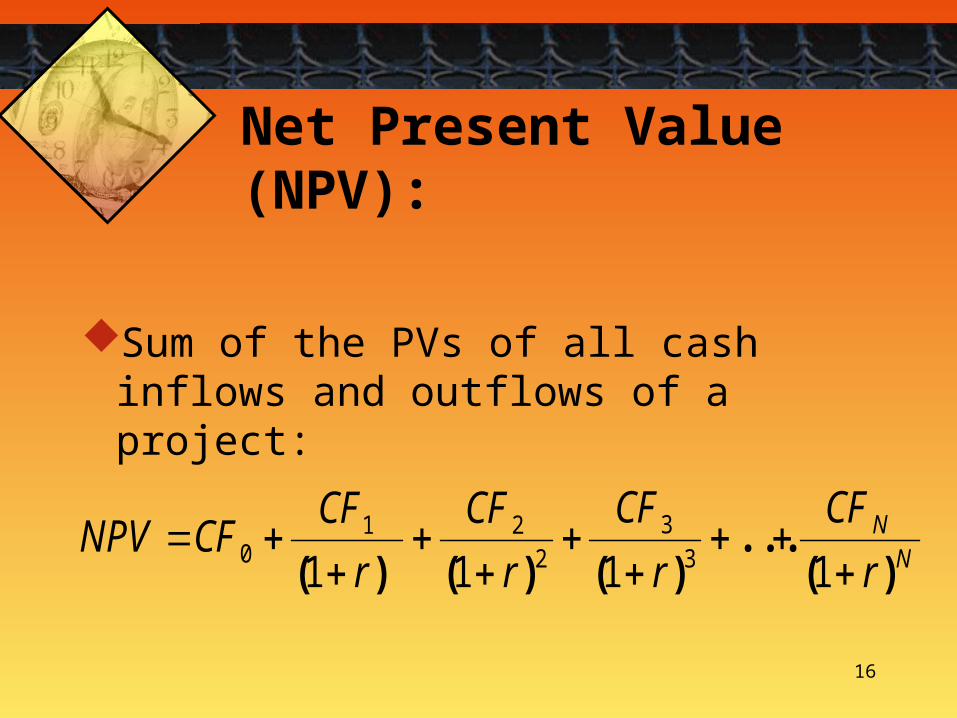

Net Present Value (NPV):

Sum of the PVs of all cash inflows and outflows of a project:

n

0tt

t

) k 1 (CF

NPV

16

Net Present Value (NPV):

Sum of the PVs of all cash inflows and outflows of a project:

NN

r

CF

r

CF

r

CF

r

CFCFNPV

)(...

)()()(

1111 33

221

0

17

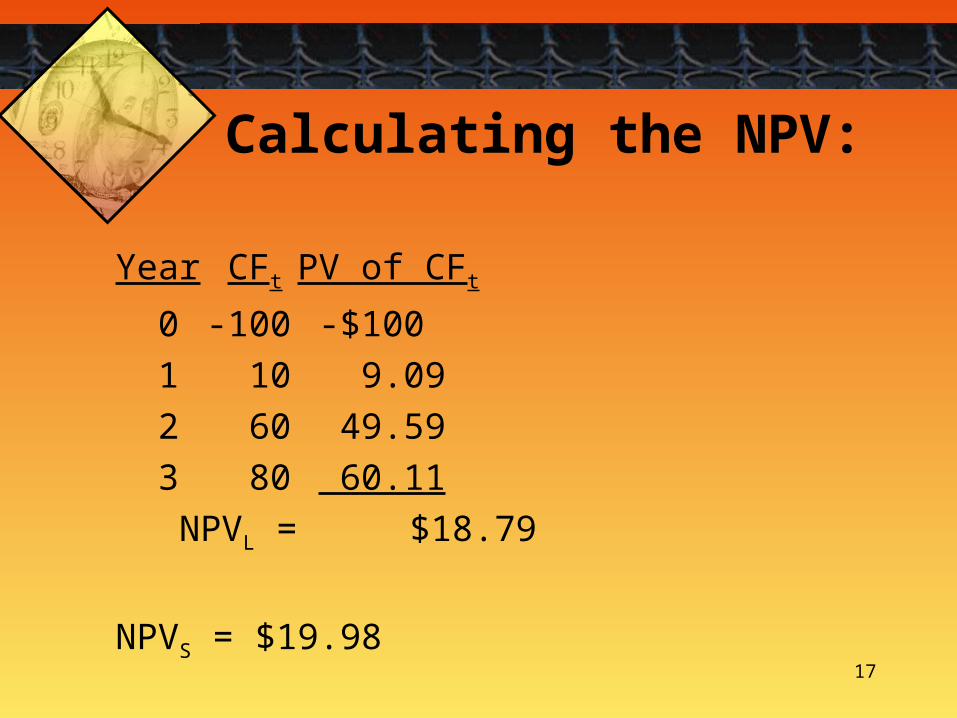

Calculating the NPV:

Year CFt PV of CFt

0 -100 -$100 1 10 9.09 2 60 49.59 3 80 60.11

NPVL = $18.79

NPVS = $19.98

18

Net Present Value (NPV):

The Decision ModelIncorporates risk and returnIncorporates time value of moneyIncorporates all cash flow

19

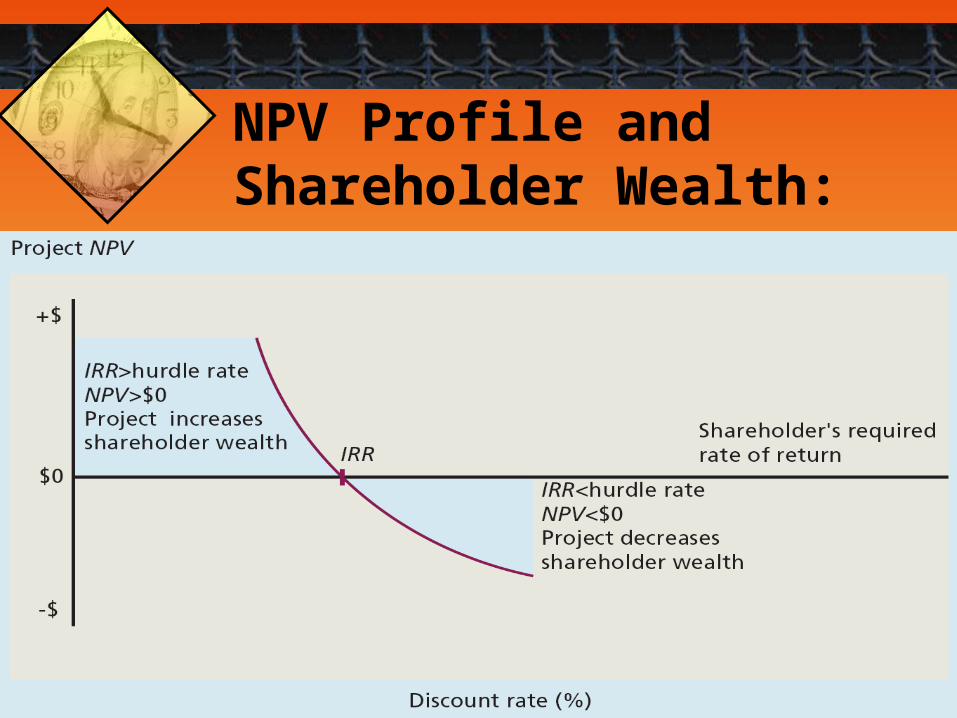

NPV Profile and Shareholder Wealth:

20

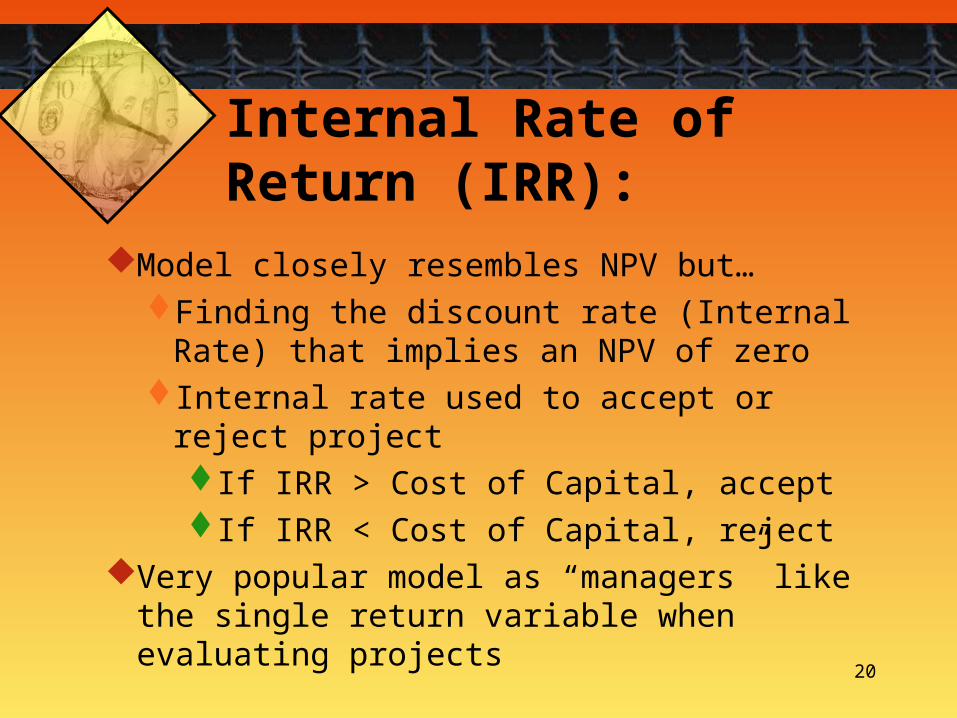

Internal Rate of Return (IRR):

Model closely resembles NPV but…Finding the discount rate (Internal Rate) that

implies an NPV of zeroInternal rate used to accept or reject project

If IRR > Cost of Capital, acceptIf IRR < Cost of Capital, reject

Very popular model as “managers” like the single return variable when evaluating projects

21

NN

r

CF

r

CF

r

CF

r

CFCFNPV

)(....

)()()(

11110

33

221

0

Internal Rate of Return (IRR):

22

Calculating the IRR:

23

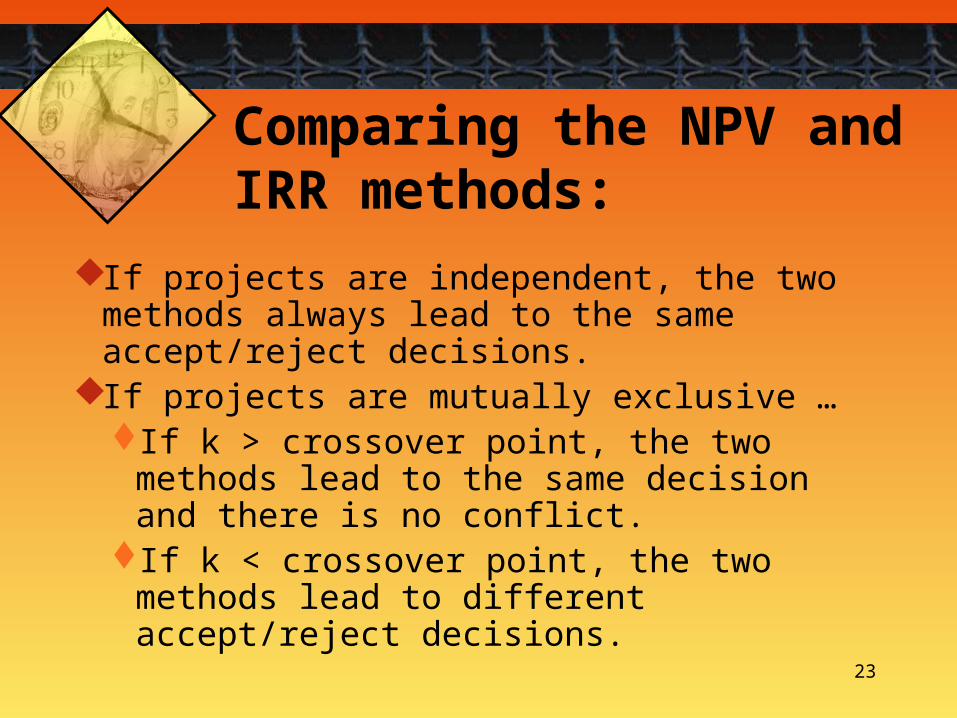

Comparing the NPV and IRR methods:

If projects are independent, the two methods always lead to the same accept/reject decisions.

If projects are mutually exclusive …If k > crossover point, the two methods

lead to the same decision and there is no conflict.

If k < crossover point, the two methods lead to different accept/reject decisions.

24

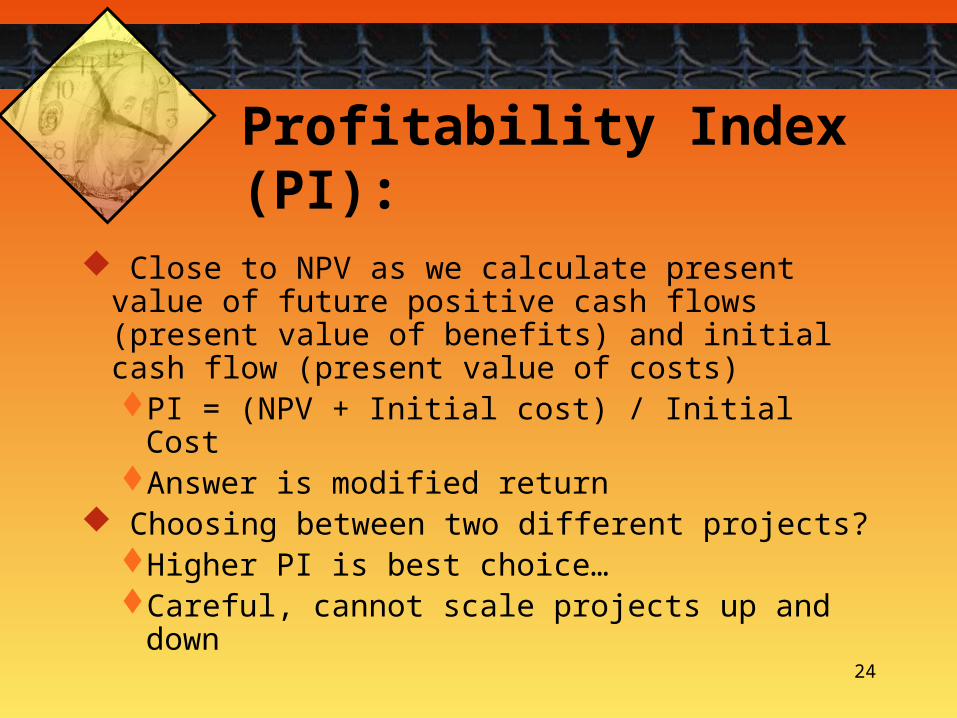

Profitability Index (PI):

Close to NPV as we calculate present value of future positive cash flows (present value of benefits) and initial cash flow (present value of costs)PI = (NPV + Initial cost) / Initial CostAnswer is modified return

Choosing between two different projects?Higher PI is best choice…Careful, cannot scale projects up and down

25

Profitability Index (PI):

Modified version of NPV Decision Criteria

PI > 1.0, accept projectPI < 1.0, reject project

26

Methods to generate, review, analyze, select, and implement long-term investment proposals:

Payback PeriodDiscounted payback periodNet Present Value (NPV)Internal rate of return (IRR)Profitability index (PI)

Capital Budgeting:

27

Related Documents