1 Chapter 10 Introduction to Government Finance

CHAPTER 10- INTRODUCTION TO GOVERNMENT FINANCE

Nov 17, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Chapter 10

Introduction to Government Finance

2

Federal, State, and Local Revenue

Sources: Taxes:

Payroll Income (Corporate and Personal) Property Sales and Excise Estate Tariffs

Fees Tuition Licenses

$3 trillion annually

3

Purpose and Consequences of

Government Finance

Political Equilibrium

Market Equilibrium and Its Efficiency

The Distribution of Income

4

Taxes

Taxes are compulsory payments to government

5

Tax Basics Tax Base

The item or activity that is to be taxed A general tax is one that taxes all of the components of the

economic base, with no exclusions, exemptions, or deductions from the tax base.

A selective tax is one that taxes only certain portions of the tax base, or it might allow exemptions and deductions from the general tax base. An excise tax is a selective tax on the manufacture or sale of a particular good or service.

Tax Rate Structure The relationship between the amount that is

to be paid in tax and the tax base for a given accounting period

6

Tax Basics (Continued)Marginal Tax Rate

The amount by which the tax increases when the tax base increases

BaseTaxtheofValue

PaidTaxesTotalMTR

BaseTaxtheofValue

PaidTaxesTotalATR

Average Tax RateThe total amount of tax divided by the total amount of the tax base

Tax bracketThe range of the tax base in which the marginal rate is constant

7

Descriptors of the Tax Rate Structure A Progressive Tax has a structure where the

marginal tax rate is increasing and greater than the average tax rate.

A Proportional Tax has a structure where the marginal tax rate is constant and equal to the average tax rate. (Sometimes called a Flat Tax)

A Regressive Tax has a structure where the marginal tax rate is decreasing and less than the average tax rate.

8

Figure 10.1 A Proportional Tax Rate Structure

Ta

x R

ate

(P

erc

en

t)

Tax Base (Dollars per Year) 0

t ATR = MTR

9

Figure 10.2 A Progressive Tax Rate StructureT

ax

Ra

te (

Pe

rce

nt)

Tax Base (Dollars of Taxable Income per Year)

0

35

25

15

MTR

ATR

4,000 29,000 70,000

10

Figure 10.3 An Example of a Regressive Tax StructureT

ax

Ra

te (

Pe

rce

nt)

Annual Labor Earnings per Worker

0

15.30

12.35

2.9

$100,000 MTR

ATR

$76,200

11

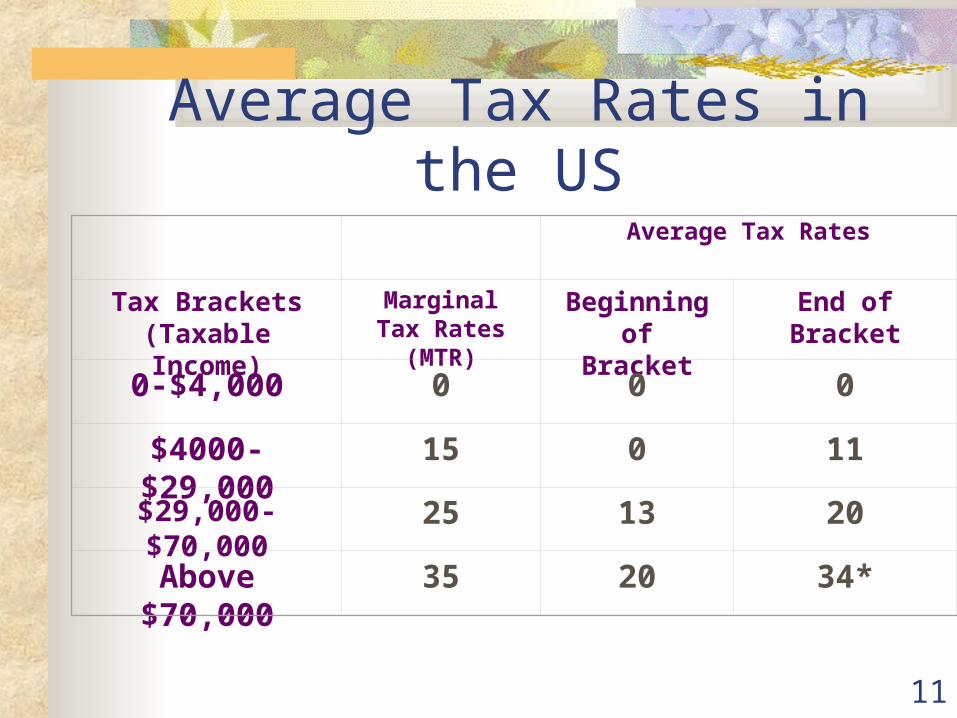

Average Tax Rates

Tax Brackets(Taxable Income)

Marginal Tax Rates (MTR)

Beginning of Bracket

End of Bracket

0-$4,000 0 0 0

$4000-$29,000 15 0 11

$29,000-$70,000 25 13 20

Above $70,000 35 20 34*

Average Tax Rates in the US

12

Average Tax Rates Throughout the World

13

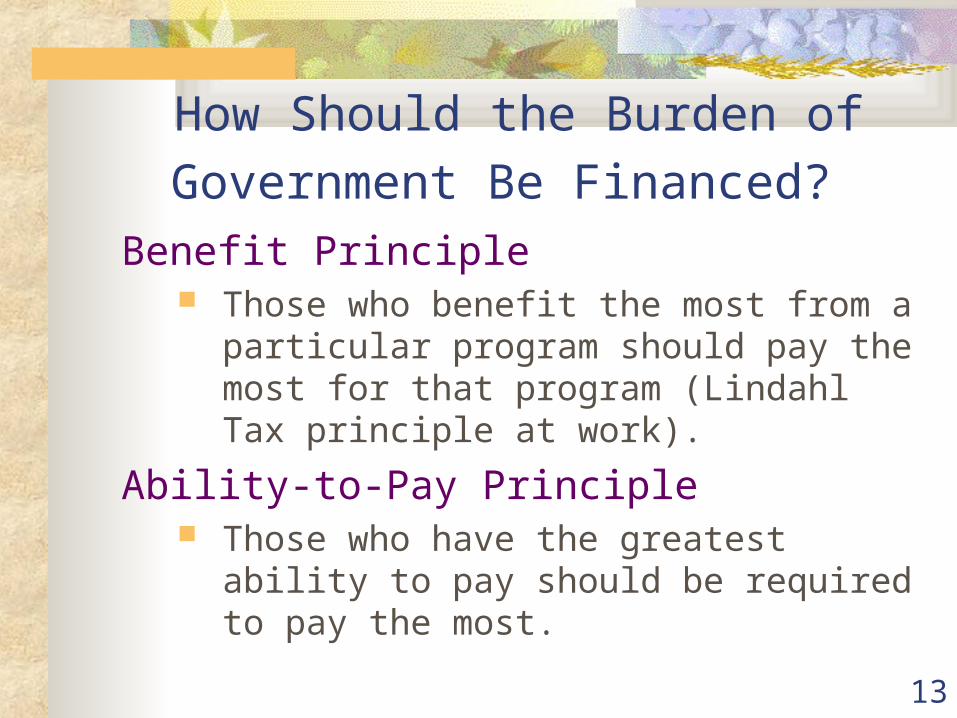

How Should the Burden of Government

Be Financed? Benefit Principle

Those who benefit the most from a particular program should pay the most for that program (Lindahl Tax principle at work).

Ability-to-Pay Principle Those who have the greatest ability to

pay should be required to pay the most.

14

Criteria for Evaluating Methods of Government Finance Equity

The distribution of the government finance burden should coincide with commonly held notions of fairness and ability-to-pay.

Efficiency The system of government finance should raise

revenues with the least loss in efficiency in the private sector.

Administrative ease A government finance system should be relatively

easy to administer consistently, without excessive costs to collect, enforce, and comply with taxes and tax laws.

15

Horizontal and Vertical Equity Horizontal equity is achieved when individuals of the

same economic capacity (measured, for example, by income) pay the same amount of taxes per year (or over their lifetimes).

Vertical equity is accomplished when individuals of differing economic ability pay annual tax bills that differ according to some collectively chosen notion of fairness.

Both concepts are subjective. “Economic capacity” is difficult to measure and

administer. “Ability to pay” requires value judgments on the

proper income distribution.

16

Tax Compliance, Avoidance and Evasion

Tax Evasion is the term for illegal ways to avoid paying taxes. It is typically the result of not declaring income or overstating otherwise legal deductions.

Tax Avoidance is the term for legal ways to avoid paying taxes, typically the result of avoiding activities that are taxed, delaying the time at which taxes are owed, or taking an action designed to lower a tax burden.

17

Figure 10.4 Reducing Tax Evasion

D*

A

MC

MB = MTR

Cos

t and

Ben

efit

Unreported Income per Year (Dollars)

0

E

MB2

E2

D*

Cos

t and

Ben

efit

Unreported Income per Year (Dollars)

0 D* 1

B

MC

1 E

MB1 = MTR1

2

MC2

E

D*

C MC1

Cos

t and

Ben

efit

Unreported Income per Year (Dollars)

0

MB = MTR

E1

D* 1 2

18

Alternatives to Taxation

Debt Finance is the means of financing expenditures by issuing bonds.

Inflationary Finance is the means of financing expenditures through the printing of money.

19

Figure 10.5 Inflationary Finance

T'

T G

un

s p

er

Ye

ar

Butter per Year 0 B2

G2 C

G1 A

B1

I

20

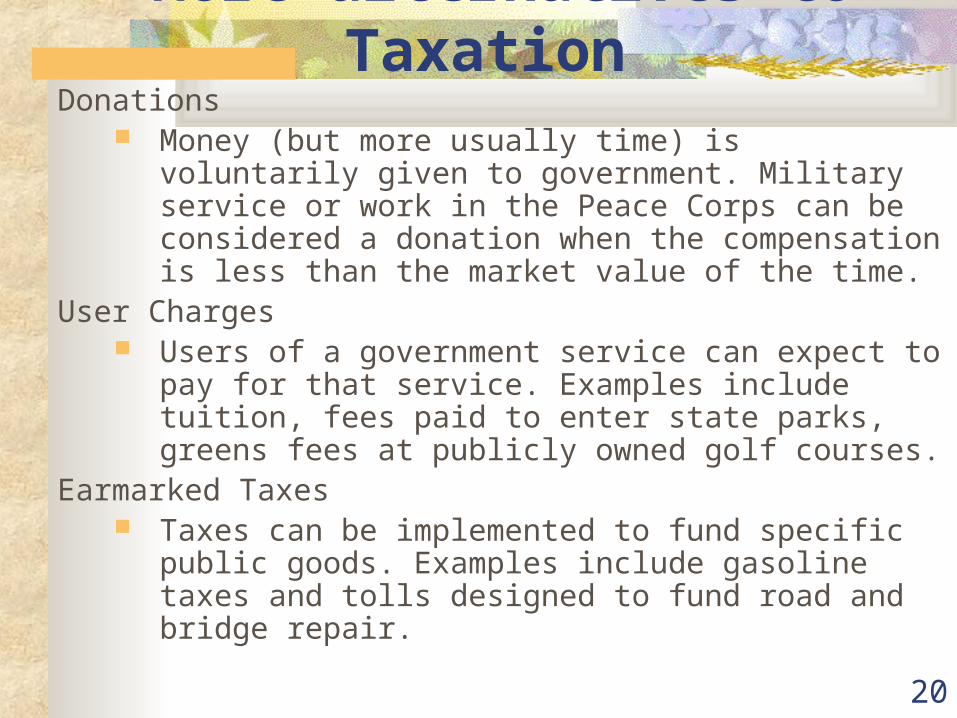

More alternatives to Taxation Donations

Money (but more usually time) is voluntarily given to government. Military service or work in the Peace Corps can be considered a donation when the compensation is less than the market value of the time.

User Charges Users of a government service can expect to pay for

that service. Examples include tuition, fees paid to enter state parks, greens fees at publicly owned golf courses.

Earmarked Taxes Taxes can be implemented to fund specific public

goods. Examples include gasoline taxes and tolls designed to fund road and bridge repair.

21

Figure 10.6 User Charges and Efficiency

MSB = MPB + MEB

MPB

MSC C

ha

rge

s

Trash Pickups per Year 0

C*

C* + S* Z*

Q*

S*

Z

22

User Charges and the Transportation Infrastructure

Economists argue that voters demand better roads and airports in part because the price to use them (usually zero) is less than the true marginal cost (which should include congestion costs.)

23

User Charges and Efficiency Roads and Bridges wear out when too much

weight is concentrated on too few axles.

Tolls motivate the wrong behavior in that they tax per axle rather than on pounds per axle.

Estimates suggest that taxing pounds per axle and using the revenue to create stronger roads would pay for itself more than eight-fold.

24

Figure 10.7 User Charges for a Congestible Government-Supplied Service

0

Us

er

Ch

arg

es

(C

en

ts p

er

Mile

)

Vehicles per Mile per Hour

E1

D1 = MSB1

80

E2

150

20

D2 = MSB2

120

E*

MSC

100

N*

25

Government Enterprise Local Utilities

Lotteries

26

State Lotteries 38 states run or participate in lotteries.

State Lotteries account for more than 3% of state revenues.

People of varying incomes spend approximately the same amount on lotteries, which suggests that the lottery system is a regressive means of creating government revenue.

Lotteries pay out a smaller portion of revenue to winners than other forms of gaming (horse racing, casinos, etc.).

Related Documents