Chapter 10 Chapter 10 Accounting Accounting for Long-Term for Long-Term Liabilities Liabilities

Chapter 10 Accounting for Long-Term Liabilities. BOND FINANCING Projects that demand large amounts of money are funded from bond issuances For-profit,

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 10 Chapter 10

Accounting for Accounting for Long-Term Long-Term LiabilitiesLiabilities

BOND FINANCING

• Projects that demand large amounts of money are funded from bond issuances

• For-profit, nonprofit, and governments issue bonds

• A bond is its issuer’s written promise to pay an amount identified as the par value with interest

• The issuer usually makes semiannual interest payments

Advantages of Bonds

• Bonds do not affect owner control – this is debt capital NOT equity capital

• The interest paid to bondholders is tax deductible – dividends are not tax deductible

• Companies can earn a higher return with borrowed funds than it pays in interest on those funds - See Exhibit 10.1

Disadvantages of Bonds• Bonds can decrease return on equity

– When a company earns a lower return with borrowed funds than it pays in interest

• Bonds require payment of both periodic interest and the par value at maturity– These required cash payments may be difficult if

a company faces tight cash flows

A company must weigh the risks and returns of the disadvantages and advantages of bond financing when deciding whether to issue bonds to finance operations

Bond Trading

• Bonds are securities that can be readily bought and sold

• After bonds are issued, they are often bought and sold by investors

• They are traded on the NYSE and American Stock exchanges

• A bond will have a number of owners before it matures

• Since bonds are bought and sold in the market, they have a market value or price

• Bonds always have a par value of $1,000

Bond Trading

• For convenience bond market values are expressed as a percent of their par value

Example: A bond might be trading at 103 ½ meaning they can be bought or sold at 103.5% of their par value A bond trading at 95 can be bought and sold below par value at 95%

Bond market Bond market values are values are

expressed as a expressed as a percent of their percent of their

par value.par value.

Bond-Issuing Procedures• State and federal laws govern bond issuances• The legal document identifying the rights and

obligations of both the bondholders and the issuer is called bond indenture

• The bond indenture is the legal contract between the issuer and the bondholder

• A bondholder may also receive a bond certificate as evidence as the company’s debt

• A bond certificate includes: issuer’s name, par value, contract interest rate, maturity date

Issuing Bonds at Par

K i n g C o . i s s u e s t h e f o l l o w i n g b o n d s o n J a n u a r y 1 , 2 0 0 8P a r V a l u e = $ 1 , 0 0 0 , 0 0 0S t a t e d I n t e r e s t R a t e = 1 0 %I n t e r e s t D a t e s = 6 / 3 0 a n d 1 2 / 3 1B o n d D a t e = J a n . 1 , 2 0 0 8M a t u r i t y D a t e = D e c . 3 1 , 2 0 2 7 ( 2 0 y e a r s )

K i n g C o . i s s u e s t h e f o l l o w i n g b o n d s o n J a n u a r y 1 , 2 0 0 8P a r V a l u e = $ 1 , 0 0 0 , 0 0 0S t a t e d I n t e r e s t R a t e = 1 0 %I n t e r e s t D a t e s = 6 / 3 0 a n d 1 2 / 3 1B o n d D a t e = J a n . 1 , 2 0 0 8M a t u r i t y D a t e = D e c . 3 1 , 2 0 2 7 ( 2 0 y e a r s )

I s s u i n g B o n d s a t P a r

D R C RJ a n . 1 C a s h 1 , 0 0 0 , 0 0 0

B o n d s p a y a b l e 1 , 0 0 0 , 0 0 0 I s s u e d b o n d s a t p a r

P 1

King Company issues bonds at par value. This means that the stated interest rate on the bond and the market interest rate on the bond are equal. King’s bonds have a par value of one million dollars, a stated interest rate of ten percent with interest payable on June 30th and December 31st. The bonds are dated January 1, 2008 and mature twenty years later on December 31, 2027.

On the issue date, King would debit Cash and credit Bonds Payable for one million dollars. The Bonds Payable account is always credited for the par value, or maturity value, of the bonds.

Issuing Bonds at Par

• The bond issuer pays the interest rate specified in the indenture – the contract rate is also called the coupon rate

• The annual interest paid is determined by multiplying the bond par value by the contract rate

• Contract rate is stated on an annual basis – but interest is paid semiannually

$ 1 , 0 0 0 , 0 0 0 × 1 0 % × ½ y e a r = $ 5 0 , 0 0 0T h i s e n t r y i s m a d e e v e r y s i x m o n t h s u n t i l

t h e b o n d s m a t u r e .

$ 1 , 0 0 0 , 0 0 0 $ 1 , 0 0 0 , 0 0 0 ×× 1 0 % 1 0 % ×× ½½ y e a r = $ 5 0 , 0 0 0y e a r = $ 5 0 , 0 0 0T h i s e n t r y i s m a d e e v e r y s i x m o n t h s u n t i l

t h e b o n d s m a t u r e .

I s s u i n g B o n d s a t P a r

T h e e n t r y o n J u n e 3 0 , 2 0 0 8 , t o r e c o r d t h e f i r s t s e m i a n n u a l i n t e r e s t p a y m e n t i s . . .

T h e e n t r y o n J u n e 3 0 , 2 0 0 8 , t o r e c o r d t h e f i r s t s e m i a n n u a l i n t e r e s t p a y m e n t i s . . .

D R C RJ u n e 3 0 B o n d i n t e r e s t e x p e n s e 5 0 , 0 0 0

C a s h 5 0 , 0 0 0 P a i d s e m i - a n n u a l i n t e r e s t

P 1

• On the first interest payment date, King would debit Bond Interest Expense and credit Cash for fifty thousand dollars. The interest was calculated as Par value times stated rate times months outstanding.

• King will actually make this entry every six months until the maturity date.

• Problem, bonds RARELY sell on the open market at par. Conditions in the market cause them to trade above or below par.

• Concert ticket example here!

• Just like demand for a performer can spike up ticket prices, differences in interest rates between what the bond pays and market expects can lead a bond to trade at a discount or premium.

Bond Discount or Premium

Contract Rate is: Bonds Sells:

Above market rate At a premium

Equal to market rate

At par value

Below market rate At a discount

In almost all cases, the stated (contract) rate and the market rate of interest will not agree. When these two interest rates are different, it might make sense to you for us to just change our stated rate to equal the market rate and then everything would be fine. Well, we can’t do that. Remember that the bond certificate lists all of the specifics about the bond including the interest rate. Because we have to print the bond certificates in advance, we are stuck having to pay the interest printed on the bond certificate.

The only thing that is not printed on the bond certificate is the selling price. So, the issuing company and the bond investors come to an agreement on the selling price that incorporates the difference in the stated interest rate and the market interest rate.

Bond Discount or Premium

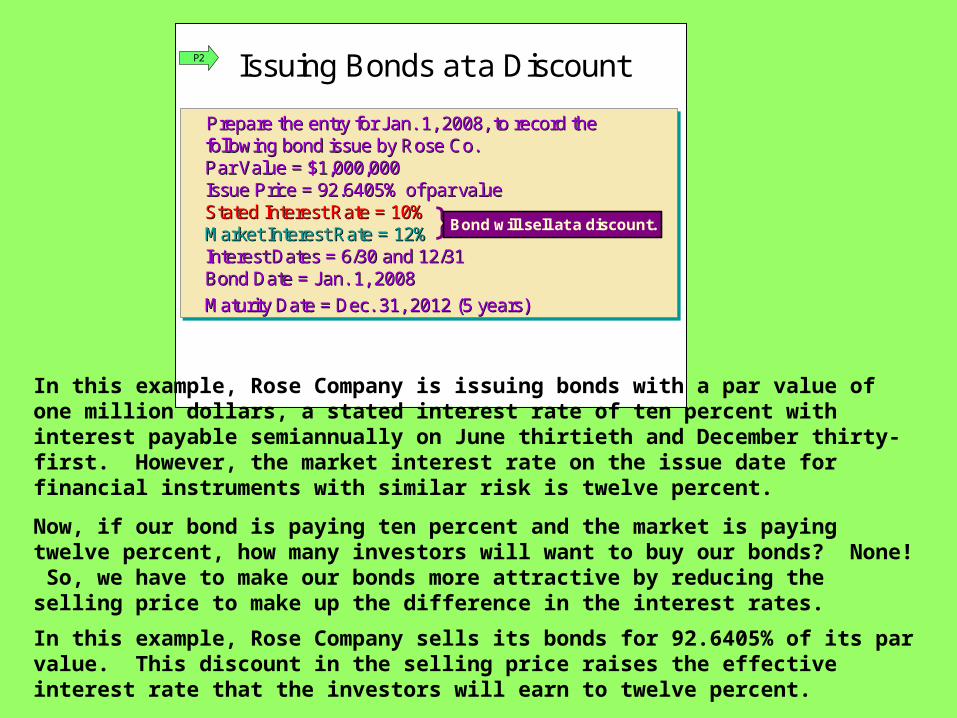

Prepare the entry for Jan. 1, 2008, to record the following bond issue by Rose Co. Par Value = $1,000,000Issue Price = 92.6405% of par valueStated Interest Rate = 10%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2008

Maturity Date = Dec. 31, 2012 (5 years)

Prepare the entry for Jan. 1, 2008, to record the Prepare the entry for Jan. 1, 2008, to record the following bond issue by Rose Co. following bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 92.6405% of par valueIssue Price = 92.6405% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 12%Market Interest Rate = 12%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2008 Bond Date = Jan. 1, 2008

Maturity Date = Dec. 31, 2012 (5 years)Maturity Date = Dec. 31, 2012 (5 years)

Issuing Bonds at a Discount

} Bond will sell at a discount.

P2

In this example, Rose Company is issuing bonds with a par value of one million dollars, a stated interest rate of ten percent with interest payable semiannually on June thirtieth and December thirty-first. However, the market interest rate on the issue date for financial instruments with similar risk is twelve percent.

Now, if our bond is paying ten percent and the market is paying twelve percent, how many investors will want to buy our bonds? None! So, we have to make our bonds more attractive by reducing the selling price to make up the difference in the interest rates.

In this example, Rose Company sells its bonds for 92.6405% of its par value. This discount in the selling price raises the effective interest rate that the investors will earn to twelve percent.

D R C R J a n . 1 C a s h 9 2 6 , 4 0 5

D i s c o u n t o n b o n d s p a y a b l e 7 3 , 5 9 5 B o n d s p a y a b l e 1 , 0 0 0 , 0 0 0

S o l d b o n d s a t a d i s c o u n t o n i s s u e d a t e

C o n t r a - L i a b i l i t yA c c o u n t

C o n t r aC o n t r a -- L i a b i l i t yL i a b i l i t yA c c o u n tA c c o u n t

O n J a n . 1 , 2 0 0 8 , R o s e C o . w o u l d r e c o r d t h e b o n d i s s u e a s f o l l o w s .

O n J a n . 1 , 2 0 0 8 , R o s e C o . w o u l d r e c o r d t h e O n J a n . 1 , 2 0 0 8 , R o s e C o . w o u l d r e c o r d t h e b o n d i s s u e a s f o l l o w s . b o n d i s s u e a s f o l l o w s .

I s s u i n g B o n d s a t a D i s c o u n tP 2

• On the issue date, Rose will debit Cash for the amount of the cash proceeds, credit Bonds Payable for the par value of the bonds issued, and debit Discount on Bonds Payable for the difference between the two.

• Discount on Bonds Payable is a contra-liability account and has a normal debit balance.

P a r t i a l B a l a n c e S h e e t a s o f J a n . 1 , 2 0 0 8

L o n g - t e r m L i a b i l i t i e s : D R C R B o n d s P a y a b l e 1 , 0 0 0 , 0 0 0$ L e s s : D i s c o u n t o n B o n d s P a y a b l e 7 3 , 5 9 5 9 2 6 , 4 0 5$

M a t u r i t y V a l u eM a t u r i t y V a l u eM a t u r i t y V a l u e

C a r r y i n g V a l u eC a r r y i n g V a l u eC a r r y i n g V a l u e

I s s u i n g B o n d s a t a D i s c o u n t

U s i n g t h e s t r a i g h t - l i n e m e t h o d , t h e d i s c o u n t a m o r t i z a t i o n w i l l b e $ 7 , 3 6 0

e v e r y s i x m o n t h s .

$ 7 3 , 5 9 5 ÷ 1 0 p e r i o d s = $ 7 , 3 6 0 * * ( r o u n d e d )

U s i n g t h e s t r a i g h tU s i n g t h e s t r a i g h t -- l i n e m e t h o d , t h e l i n e m e t h o d , t h e d i s c o u n t a m o r t i z a t i o n w i l l b e $ 7 , 3 6 0 d i s c o u n t a m o r t i z a t i o n w i l l b e $ 7 , 3 6 0

e v e r y s i x m o n t h s . e v e r y s i x m o n t h s .

$ 7 3 , 5 9 5 ÷ 1 0 p e r i o d s = $ 7 , 3 6 0 * $ 7 3 , 5 9 5 ÷ 1 0 p e r i o d s = $ 7 , 3 6 0 * * ( r o u n d e d )* ( r o u n d e d )

P 2

• On the balance sheet, the amount of the unamortized discount is subtracted from the par value of the bonds to arrive at the current carrying value of the bonds.

• Using the straight-line method to amortize the discount, Rose will divide the amount of the discount by the number of interest payment periods during the bond’s life. Since this is a 5 year bond and it pays interest semiannually, there are 10 interest payment periods. This calculation determines that the discount amortization will be seven thousand, three hundred sixty dollars at every interest payment date.

D R C R J u n e 3 0 B o n d i n t e r e s t e x p e n s e 5 7 , 3 6 0

D i s c o u n t o n b o n d s p a y a b l e 7 , 3 6 0 C a s h 5 0 , 0 0 0

P a i d s e m i - a n n u a l i n t e r e s t a n d a m o r t i z e d d i s c o u n t

$ 7 3 , 5 9 5 ÷ 1 0 p e r i o d s = $ 7 , 3 6 0 ( r o u n d e d )

$ 1 , 0 0 0 , 0 0 0 × 1 0 % × ½ = $ 5 0 , 0 0 0

$ 7 3 , 5 9 5 ÷ 1 0 p e r i o d s = $ 7 , 3 6 0 ( r o u n d e d )

$ 1 , 0 0 0 , 0 0 0 × 1 0 % × ½ = $ 5 0 , 0 0 0

M a k e t h e f o l l o w i n g e n t r y e v e r y s i x m o n t h s t o r e c o r d t h e c a s h i n t e r e s t p a y m e n t a n d t h e

a m o r t i z a t i o n o f t h e d i s c o u n t .

M a k e t h e f o l l o w i n g e n t r y e v e r y s i x m o n t h s t o M a k e t h e f o l l o w i n g e n t r y e v e r y s i x m o n t h s t o r e c o r d t h e c a s h i n t e r e s t p a y m e n t a n d t h e r e c o r d t h e c a s h i n t e r e s t p a y m e n t a n d t h e

a m o r t i z a t i o n a m o r t i z a t i o n o f t h e d i s c o u n t .o f t h e d i s c o u n t .

I s s u i n g B o n d s a t a D i s c o u n tP 2

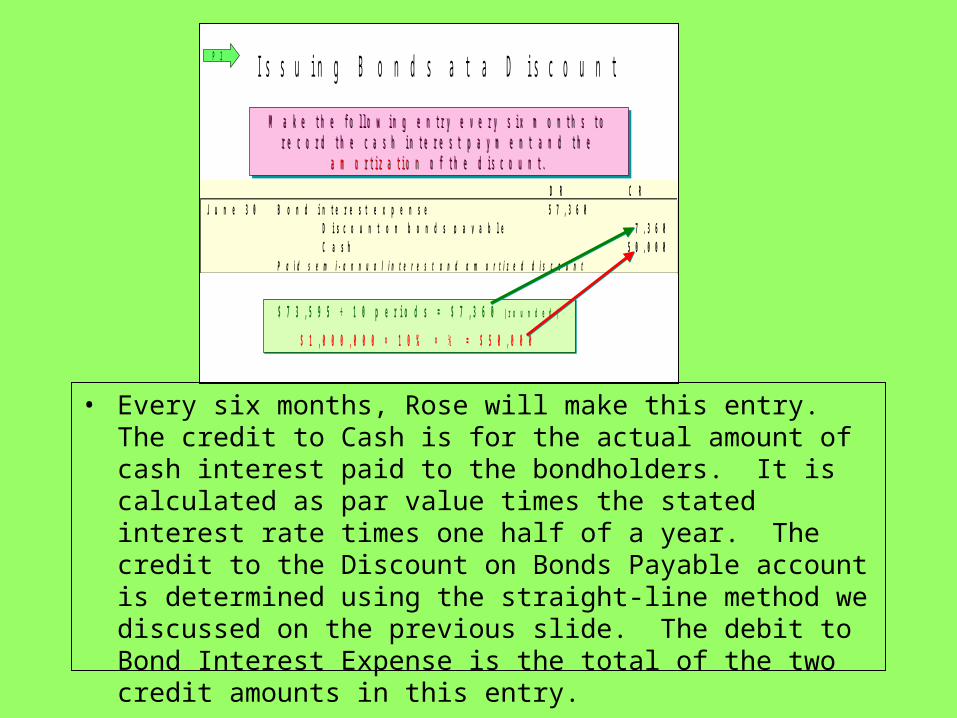

• Every six months, Rose will make this entry. The credit to Cash is for the actual amount of cash interest paid to the bondholders. It is calculated as par value times the stated interest rate times one half of a year. The credit to the Discount on Bonds Payable account is determined using the straight-line method we discussed on the previous slide. The debit to Bond Interest Expense is the total of the two credit amounts in this entry.

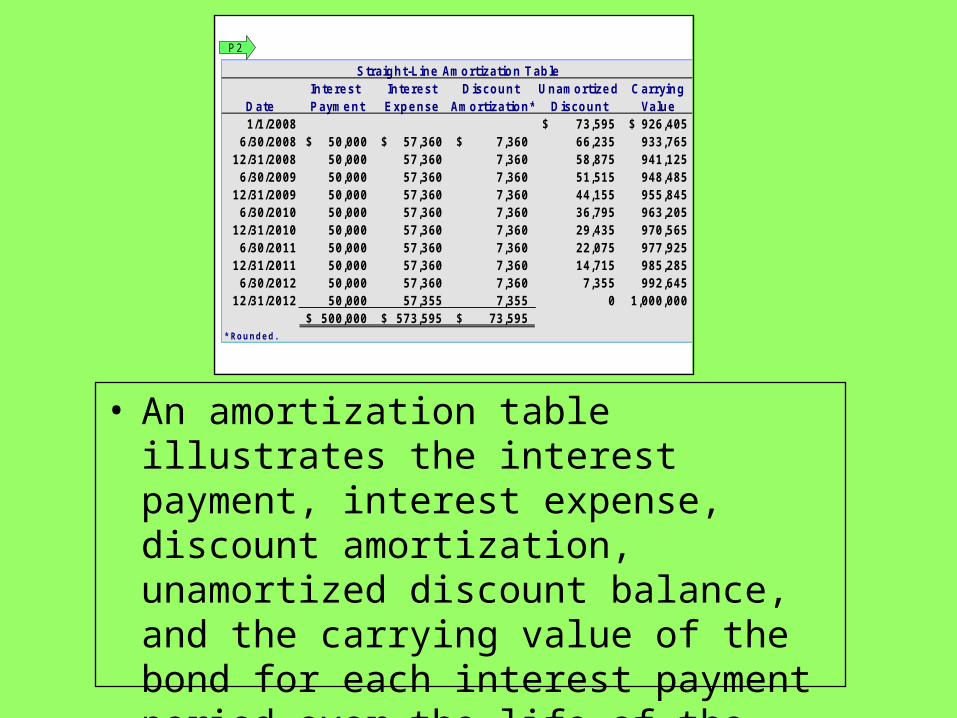

• An amortization table illustrates the interest payment, interest expense, discount amortization, unamortized discount balance, and the carrying value of the bond for each interest payment period over the life of the bond.

S tra ig h t-L in e Amo rtiz atio n T ab leIn te re st In te re st D isco u n t U n amo rtiz e d C arryin g

D ate P ayme n t E xp e n se Amo rtiz atio n * D isco u n t Valu e1/1 /2008 73,595$ 926,405$

6 /30/2008 50,000$ 57 ,360$ 7 ,360$ 66 ,235 933,765 12 /31/2008 50,000 57 ,360 7 ,360 58 ,875 941,125

6 /30/2009 50,000 57 ,360 7 ,360 51 ,515 948,485 12 /31/2009 50,000 57 ,360 7 ,360 44 ,155 955,845

6 /30/2010 50,000 57 ,360 7 ,360 36 ,795 963,205 12 /31/2010 50,000 57 ,360 7 ,360 29 ,435 970,565

6 /30/2011 50,000 57 ,360 7 ,360 22 ,075 977,925 12 /31/2011 50,000 57 ,360 7 ,360 14 ,715 985,285

6 /30/2012 50,000 57 ,360 7 ,360 7 ,355 992,645 12 /31/2012 50,000 57 ,355 7 ,355 0 1 ,000,000

500,000$ 573,595$ 73 ,595$ * Ro u n d e d .

P 2

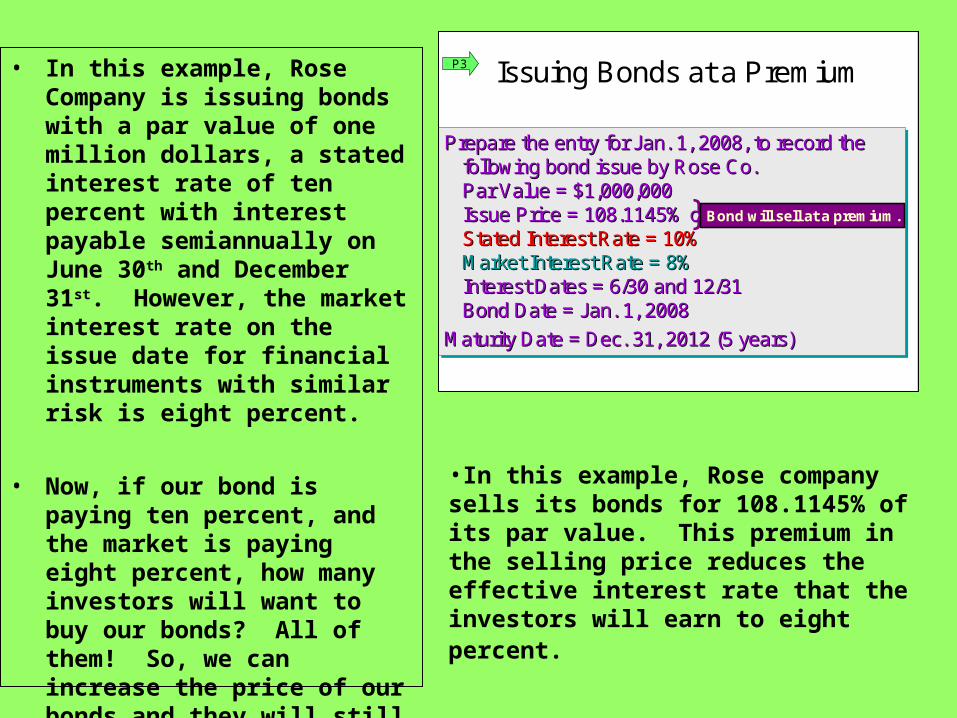

Prepare the entry for Jan. 1, 2008, to record the following bond issue by Rose Co. Par Value = $1,000,000Issue Price = 108.1145% of par valueStated Interest Rate = 10%Market Interest Rate = 8%Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2008

Maturity Date = Dec. 31, 2012 (5 years)

Prepare the entry for Jan. 1, 2008, to record the Prepare the entry for Jan. 1, 2008, to record the following bond issue by Rose Co. following bond issue by Rose Co. Par Value = $1,000,000Par Value = $1,000,000Issue Price = 108.1145% of par valueIssue Price = 108.1145% of par valueStated Interest Rate = 10%Stated Interest Rate = 10%Market Interest Rate = 8%Market Interest Rate = 8%Interest Dates = 6/30 and 12/31Interest Dates = 6/30 and 12/31Bond Date = Jan. 1, 2008Bond Date = Jan. 1, 2008

Maturity Date = Dec. 31, 2012 (5 years)Maturity Date = Dec. 31, 2012 (5 years)

Issuing Bonds at a Premium

} Bond will sell at a premium.

P3• In this example, Rose Company is issuing bonds with a par value of one million dollars, a stated interest rate of ten percent with interest payable semiannually on June 30th and December 31st. However, the market interest rate on the issue date for financial instruments with similar risk is eight percent.

• Now, if our bond is paying ten percent, and the market is paying eight percent, how many investors will want to buy our bonds? All of them! So, we can increase the price of our bonds and they will still be attractive to the bond investors.

•In this example, Rose company sells its bonds for 108.1145% of its par value. This premium in the selling price reduces the effective interest rate that the investors will earn to eight percent.

D R C RJ a n . 1 C a s h 1 , 0 8 1 , 1 4 5

P r e m i u m o n b o n d s p a y a b l e 8 1 , 1 4 5 B o n d s p a y a b l e 1 , 0 0 0 , 0 0 0

I s s u e d b o n d s a t a p r e m i u m o n i s s u e d a t e

C o n t r a - L i a b i l i t yA c c o u n t

C o n t r aC o n t r a -- L i a b i l i t yL i a b i l i t yA c c o u n tA c c o u n t

O n J a n . 1 , 2 0 0 8 , R o s e C o . w o u l d r e c o r d t h e b o n d i s s u e a s f o l l o w s .

O n J a n . 1 , 2 0 0 8 , R o s e C o . w o u l d r e c o r d t h e O n J a n . 1 , 2 0 0 8 , R o s e C o . w o u l d r e c o r d t h e b o n d i s s u e a s f o l l o w s . b o n d i s s u e a s f o l l o w s .

I s s u i n g B o n d s a t a P r e m i u mP 3

• On the issue date, Rose will debit Cash for the amount of the cash proceeds, credit Bonds Payable for the par value of the bonds issued, and credit Premium on Bonds Payable for the difference between the two.

• Premium on Bonds Payable is an contra-liability account and has a normal credit balance.

U s i n g t h e s t r a i g h t - l i n e m e t h o d , t h e p r e m i u m a m o r t i z a t i o n w i l l b e $ 8 , 1 1 5 e v e r y s i x m o n t h s .

$ 8 1 , 1 4 5 ÷ 1 0 p e r i o d s = $ 8 , 1 1 5 ( r o u n d e d )

U s i n g t h e s t r a i g h tU s i n g t h e s t r a i g h t -- l i n e m e t h o d , t h e p r e m i u m l i n e m e t h o d , t h e p r e m i u m a m o r t i z a t i o n w i l l b e $ 8 , 1 1 5 e v e r y s i x m o n t h s . a m o r t i z a t i o n w i l l b e $ 8 , 1 1 5 e v e r y s i x m o n t h s .

$ 8 1 , 1 4 5 ÷ 1 0 p e r i o d s = $ 8 , 1 1 5 ( r o u n d e d )$ 8 1 , 1 4 5 ÷ 1 0 p e r i o d s = $ 8 , 1 1 5 ( r o u n d e d )

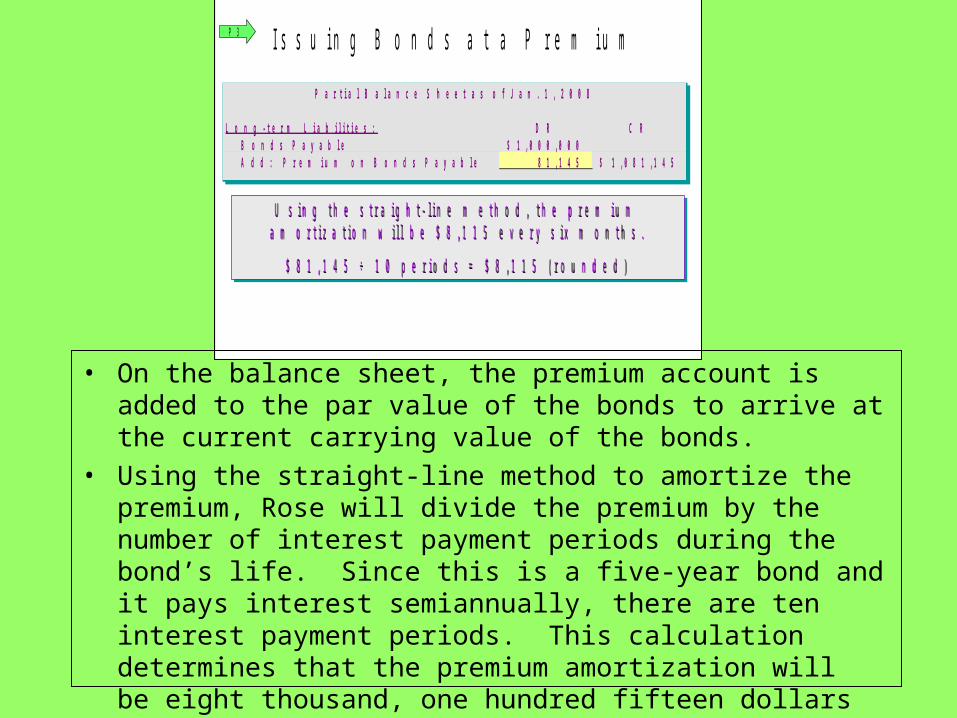

P a r t i a l B a l a n c e S h e e t a s o f J a n . 1 , 2 0 0 8

L o n g - t e r m L i a b i l i t i e s : D R C R B o n d s P a y a b l e 1 , 0 0 0 , 0 0 0$ A d d : P r e m i u m o n B o n d s P a y a b l e 8 1 , 1 4 5 1 , 0 8 1 , 1 4 5$

I s s u i n g B o n d s a t a P r e m i u mP 3

• On the balance sheet, the premium account is added to the par value of the bonds to arrive at the current carrying value of the bonds.

• Using the straight-line method to amortize the premium, Rose will divide the premium by the number of interest payment periods during the bond’s life. Since this is a five-year bond and it pays interest semiannually, there are ten interest payment periods. This calculation determines that the premium amortization will be eight thousand, one hundred fifteen dollars at every interest payment date.

D R C R J u n e 3 0 B o n d i n t e r e s t e x p e n s e 4 1 , 8 8 5

P r e m i u m o n b o n d s p a y a b l e 8 , 1 1 5 C a s h 5 0 , 0 0 0

P a i d s e m i - a n n u a l i n t e r e s t a n d a m o r t i z e d p r e m i u m

$ 8 1 , 1 4 5 ÷ 1 0 p e r i o d s = $ 8 , 1 1 5 ( r o u n d e d )

$ 1 , 0 0 0 , 0 0 0 × 1 0 % × ½ = $ 5 0 , 0 0 0

$ 8 1 , 1 4 5 ÷ 1 0 p e r i o d s = $ 8 , 1 1 5 ( r o u n d e d )

$ 1 , 0 0 0 , 0 0 0 × 1 0 % × ½ = $ 5 0 , 0 0 0

T h i s e n t r y i s m a d e e v e r y s i x m o n t h s t o r e c o r d t h e c a s h i n t e r e s t p a y m e n t a n d t h e

a m o r t i z a t i o n o f t h e p r e m i u m .

T h i s e n t r y i s m a d e e v e r y s i x m o n t h s t o T h i s e n t r y i s m a d e e v e r y s i x m o n t h s t o r e c o r d t h e c a s h i n t e r e s t p a y m e n t a n d t h e r e c o r d t h e c a s h i n t e r e s t p a y m e n t a n d t h e

a m o r t i z a t i o n o f t h e p r e m i u m .a m o r t i z a t i o n o f t h e p r e m i u m .

I s s u i n g B o n d s a t a P r e m i u mP 3

• Every six months, Rose will make this entry. The credit to Cash is for the actual amount of cash interest paid to the bondholders. It is calculated as par value times the stated interest rate times one half of a year. The debit to the Premium on Bonds Payable account is determined using the straight-line method we discussed on the previous slide. The debit to Bond Interest Expense is amount of the cash credit less the bond premium amortization.

Straight-Line Amortization T ableInte re st Inte re st Pre mium U namortize d C arrying

D ate Payme nt Expe nse Amortization* Pre mium Value1/1/2008 81,145$ 1,081,145$

6/30/2008 50,000$ 41,885$ 8,115$ 73,030 1,073,030 12/31/2008 50,000 41,885 8,115 64,915 1,064,915

6/30/2009 50,000 41,885 8,115 56,800 1,056,800 12/31/2009 50,000 41,885 8,115 48,685 1,048,685

6/30/2010 50,000 41,885 8,115 40,570 1,040,570 12/31/2010 50,000 41,885 8,115 32,455 1,032,455

6/30/2011 50,000 41,885 8,115 24,340 1,024,340 12/31/2011 50,000 41,885 8,115 16,225 1,016,225

6/30/2012 50,000 41,885 8,115 8,110 1,008,110 12/31/2012 50,000 41,890 8,110 0 1,000,000

500,000$ 418,855$ 81,145$ * Ro u n d e d .

P 3

• An amortization table illustrates the interest payment, interest expense, premium amortization, unamortized premium balance, and the carrying value of the bond for each interest payment period over the life of the bond.

Related Documents