Chapter 1: Market Indexes, Financial Time Series and their Characteristics • What is time series (TS) analysis? Observe the following two data sets: Hang Seng 12877 12850 13023 ··· Index Date 30.8.04 31.8.04 01.9.04 ··· Student’s 130kg 200kg 45kg ··· Weights Students A B C ··· What is the difference between these two data sets? • Definition: A time series (TS) is a sequence of random variables labeled by time t. Time series data are observations of TS. 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 1: Market Indexes, Financial Time

Series and their Characteristics

• What is time series (TS) analysis?

Observe the following two data sets:

Hang Seng 12877 12850 13023 · · ·IndexDate 30.8.04 31.8.04 01.9.04 · · ·

Student’s 130kg 200kg 45kg · · ·WeightsStudents A B C · · ·

What is the difference between these two data

sets?

• Definition:

A time series (TS) is a sequence of random

variables labeled by time t.

Time series data are observations of TS.

1

TSA History

• Linear TSA: The beginning/babyhood 1927

• George Udny Yule (1871-1951), a British statis-

tician.

• Eugen Slutsky (1880-1948), a Russian/Soviet

mathematical statistician, economist and po-

litical economist.

• Herman Ole Andreas Wold ( 1908– 1992)

• Peter Whittle (1927-) (ARMA model)

• Linear TSA in 1970’s

• George Edward Pelham Box (1919–2013), a

British statistician (quality control, TSA, de-

sign of experiments, and Bayesian inference).

He has been called “one of the great statistical

minds of the 20th century”.

• Sir Ronald Aylmer Fisher (1890 –1962)

• Box & Jenkins (1976) Time Series Analysis:

Forecasting and Control

• Nonlinear TSA in 1950’s

• Patrick Alfred Pierce Moran (1917–1988), an

Australian statistician (probability theory, pop-

ulation and evolutionary genetics).

• Peter Whittle (1927-, New Zealand), stochas-

tic nets, optimal control, time series analysis,

stochastic optimisation and stochastic dynam-

ics.

• Nonlinear TSA in 1980’s

• Howell Tong (1944–, in Hong Kong) (TAR

model).

• Robert Fry Engle III (1942–) is an American

economist and the winner of the 2003 Nobel

Memorial Prize.

• What is financial time series (FTS)?

Examples

1. Daily log returns of Hang Sang Index .

2. Monthly log return of exchange rates of

Japan-USA.

3. China life daily stock data.

4. HSBC daily stock data.

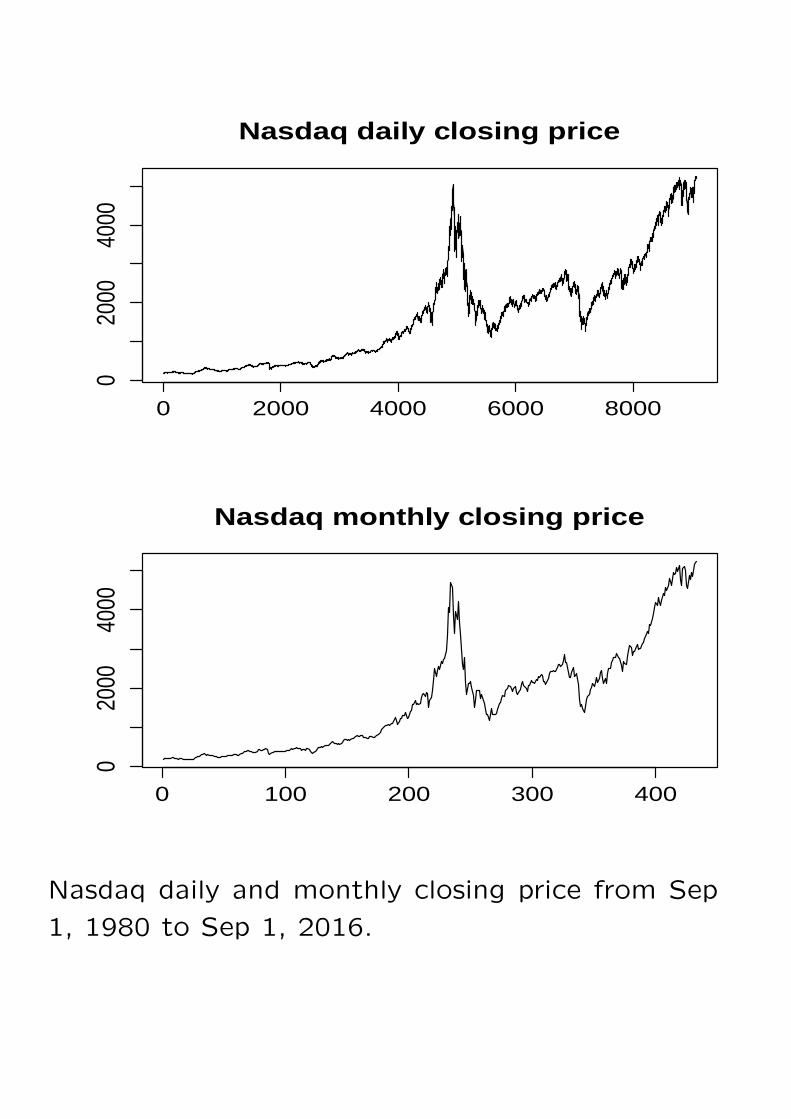

0 2000 4000 6000 8000

020

0040

00Nasdaq daily closing price

0 100 200 300 400

020

0040

00

Nasdaq monthly closing price

Nasdaq daily and monthly closing price from Sep

1, 1980 to Sep 1, 2016.

Special features of FTS

1. Theory and practice of asset valuation over

time.

2. Added more uncertainty. For example, FTS

must deal with the changing business and eco-

nomic environment and the fact that volatility is

not directly observed.

General objective of the course

to provide some basic knowledge of financial time

series data

to introduce some statistical tools and economet-

ric models useful for analyzing these series.

to gain empirical experience in analyzing FTS

to study methods for assessing market risk

to analyze high-dimensional asset returns.

Special objective of the course

Past data =⇒TS r.v. Zt=⇒ future of TS.

(a) E(Zn+l|Z1, · · · , Zn

),

(b) P (a ≤ Zn+l ≤ b|Z1, · · · , Zn) for some a < b.

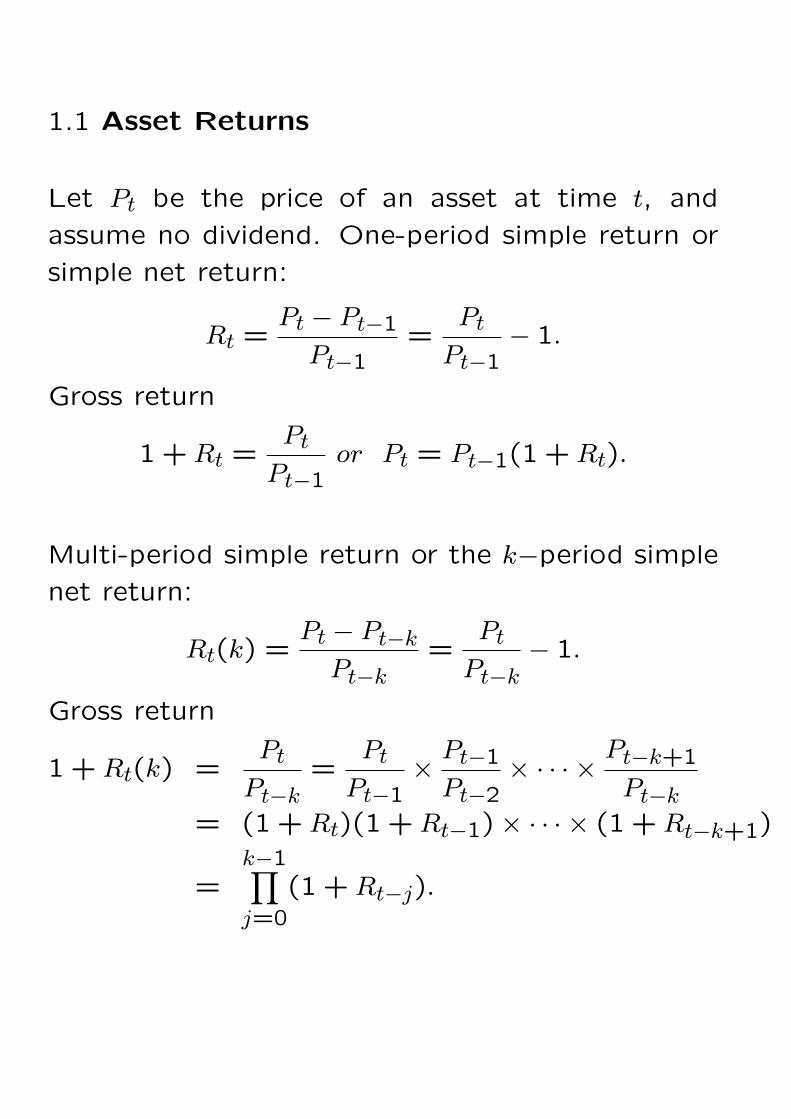

1.1 Asset Returns

Let Pt be the price of an asset at time t, and

assume no dividend. One-period simple return or

simple net return:

Rt =Pt − Pt−1

Pt−1=

Pt

Pt−1− 1.

Gross return

1 +Rt =Pt

Pt−1or Pt = Pt−1(1 +Rt).

Multi-period simple return or the k−period simple

net return:

Rt(k) =Pt − Pt−k

Pt−k=

Pt

Pt−k− 1.

Gross return

1 +Rt(k) =Pt

Pt−k=

Pt

Pt−1×

Pt−1

Pt−2× · · · ×

Pt−k+1

Pt−k

= (1+Rt)(1 +Rt−1)× · · · × (1 +Rt−k+1)

=k−1∏j=0

(1 +Rt−j).

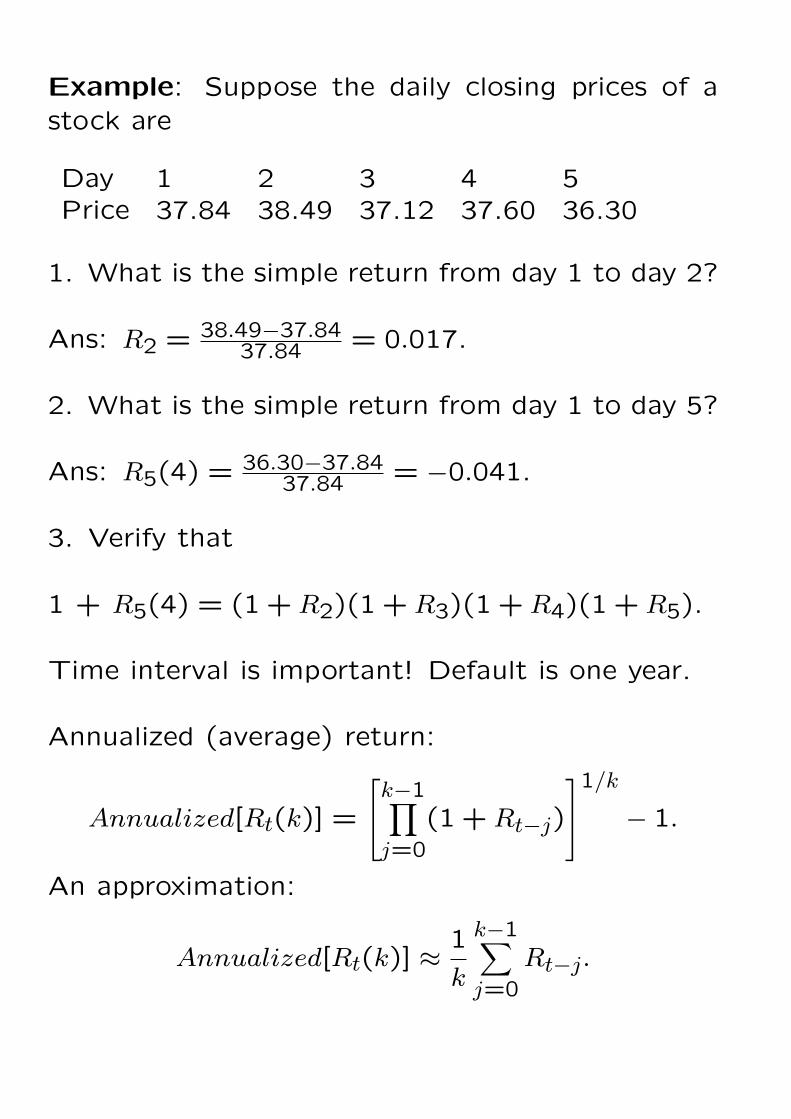

Example: Suppose the daily closing prices of astock are

Day 1 2 3 4 5Price 37.84 38.49 37.12 37.60 36.30

1. What is the simple return from day 1 to day 2?

Ans: R2 = 38.49−37.8437.84 = 0.017.

2. What is the simple return from day 1 to day 5?

Ans: R5(4) = 36.30−37.8437.84 = −0.041.

3. Verify that

1 + R5(4) = (1+R2)(1 +R3)(1 +R4)(1 +R5).

Time interval is important! Default is one year.

Annualized (average) return:

Annualized[Rt(k)] =

k−1∏j=0

(1 +Rt−j)

1/k − 1.

An approximation:

Annualized[Rt(k)] ≈1

k

k−1∑j=0

Rt−j.

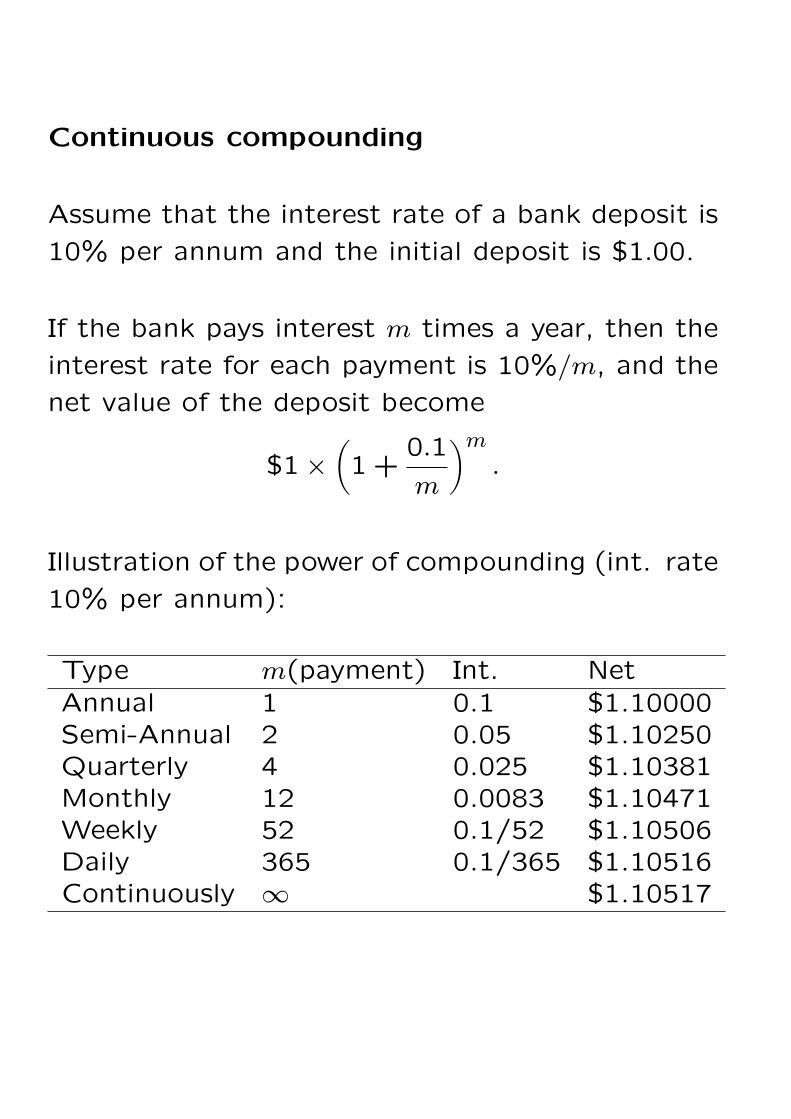

Continuous compounding

Assume that the interest rate of a bank deposit is

10% per annum and the initial deposit is $1.00.

If the bank pays interest m times a year, then the

interest rate for each payment is 10%/m, and the

net value of the deposit become

$1×(1+

0.1

m

)m.

Illustration of the power of compounding (int. rate

10% per annum):

Type m(payment) Int. NetAnnual 1 0.1 $1.10000Semi-Annual 2 0.05 $1.10250Quarterly 4 0.025 $1.10381Monthly 12 0.0083 $1.10471Weekly 52 0.1/52 $1.10506Daily 365 0.1/365 $1.10516Continuously ∞ $1.10517

In general, the net asset value A of the continuous

compounding is

A = C exp(r × n),

r is the interest rate per annum, C is the initial

capital, n is the number of years, and and exp is

the exponential function.

Present value:

C = A exp[−r × n].

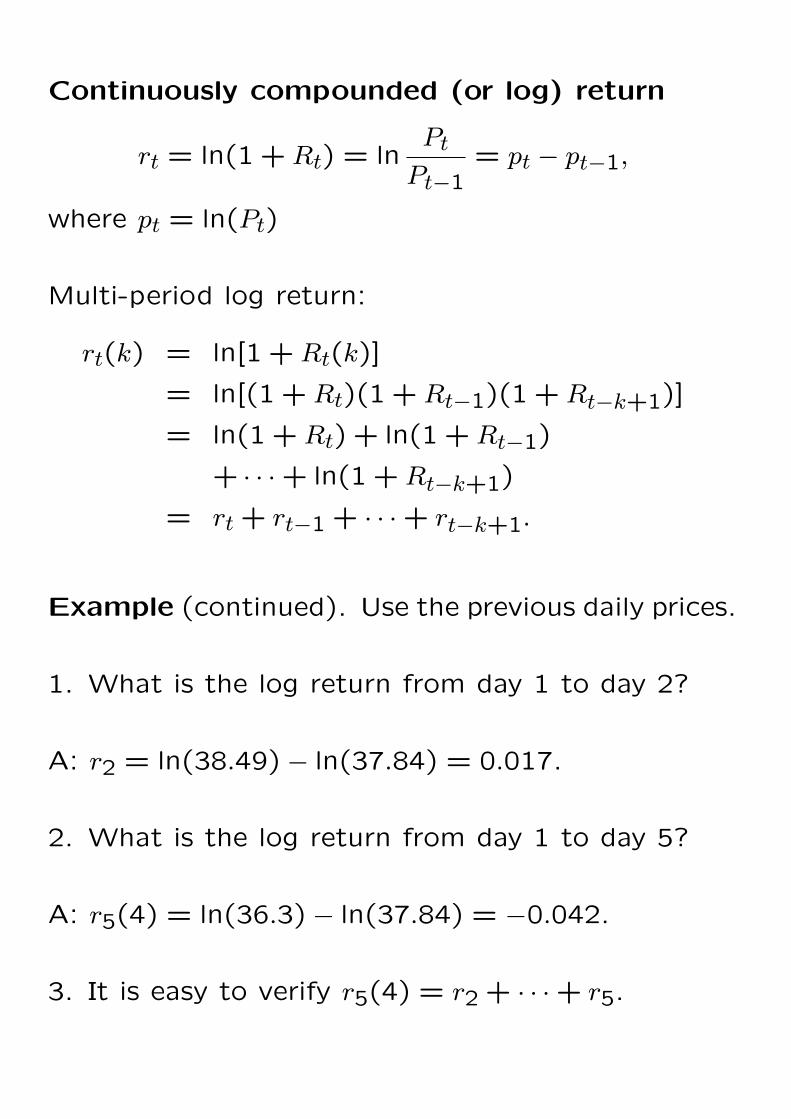

Continuously compounded (or log) return

rt = ln(1 +Rt) = lnPt

Pt−1= pt − pt−1,

where pt = ln(Pt)

Multi-period log return:

rt(k) = ln[1 +Rt(k)]

= ln[(1 +Rt)(1 +Rt−1)(1 +Rt−k+1)]

= ln(1 +Rt) + ln(1 +Rt−1)

+ · · ·+ ln(1 +Rt−k+1)

= rt + rt−1 + · · ·+ rt−k+1.

Example (continued). Use the previous daily prices.

1. What is the log return from day 1 to day 2?

A: r2 = ln(38.49)− ln(37.84) = 0.017.

2. What is the log return from day 1 to day 5?

A: r5(4) = ln(36.3)− ln(37.84) = −0.042.

3. It is easy to verify r5(4) = r2 + · · ·+ r5.

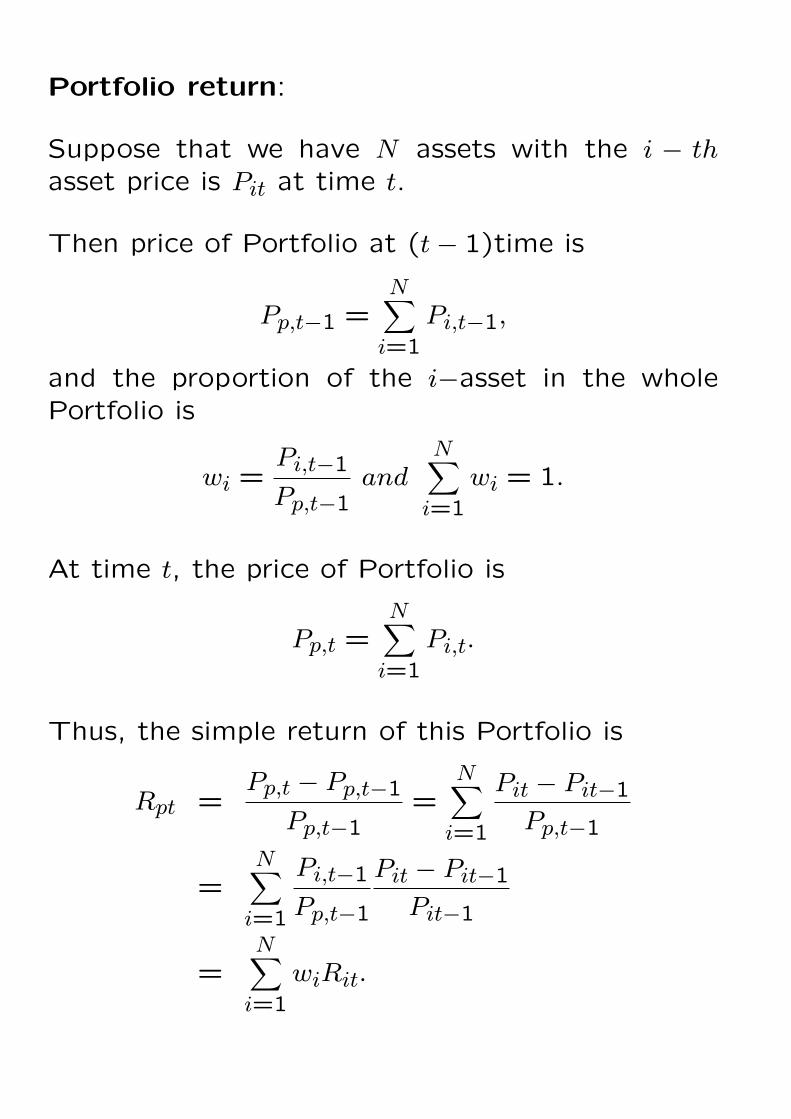

Portfolio return:

Suppose that we have N assets with the i − thasset price is Pit at time t.

Then price of Portfolio at (t− 1)time is

Pp,t−1 =N∑

i=1

Pi,t−1,

and the proportion of the i−asset in the wholePortfolio is

wi =Pi,t−1

Pp,t−1and

N∑i=1

wi = 1.

At time t, the price of Portfolio is

Pp,t =N∑

i=1

Pi,t.

Thus, the simple return of this Portfolio is

Rpt =Pp,t − Pp,t−1

Pp,t−1=

N∑i=1

Pit − Pit−1

Pp,t−1

=N∑

i=1

Pi,t−1

Pp,t−1

Pit − Pit−1

Pit−1

=N∑

i=1

wiRit.

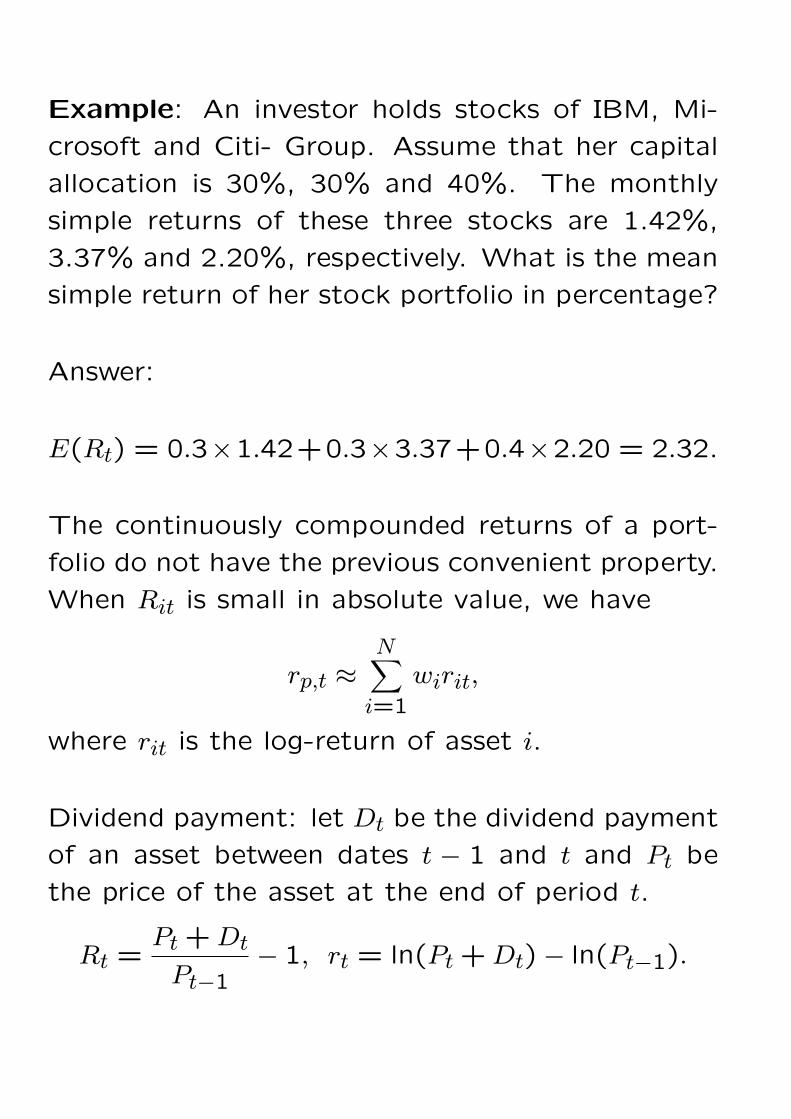

Example: An investor holds stocks of IBM, Mi-

crosoft and Citi- Group. Assume that her capital

allocation is 30%, 30% and 40%. The monthly

simple returns of these three stocks are 1.42%,

3.37% and 2.20%, respectively. What is the mean

simple return of her stock portfolio in percentage?

Answer:

E(Rt) = 0.3×1.42+0.3×3.37+0.4×2.20 = 2.32.

The continuously compounded returns of a port-

folio do not have the previous convenient property.

When Rit is small in absolute value, we have

rp,t ≈N∑

i=1

wirit,

where rit is the log-return of asset i.

Dividend payment: let Dt be the dividend payment

of an asset between dates t − 1 and t and Pt be

the price of the asset at the end of period t.

Rt =Pt +Dt

Pt−1− 1, rt = ln(Pt +Dt)− ln(Pt−1).

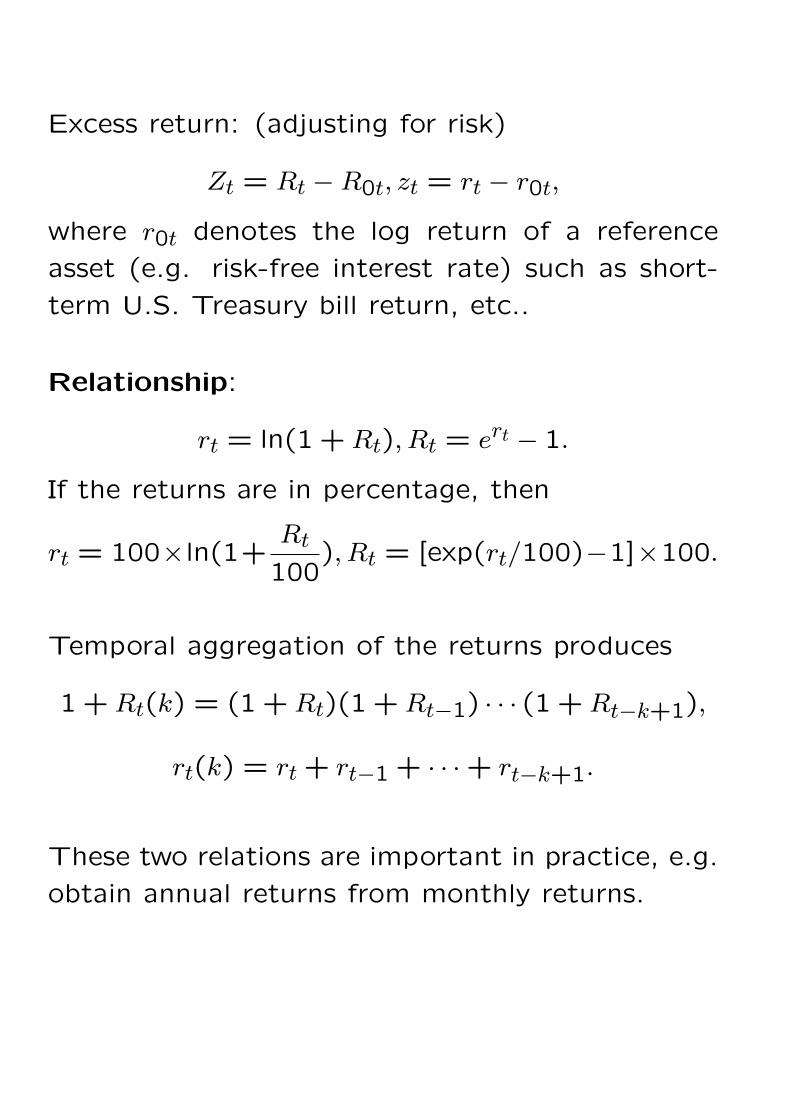

Excess return: (adjusting for risk)

Zt = Rt −R0t, zt = rt − r0t,

where r0t denotes the log return of a reference

asset (e.g. risk-free interest rate) such as short-

term U.S. Treasury bill return, etc..

Relationship:

rt = ln(1 +Rt), Rt = ert − 1.

If the returns are in percentage, then

rt = 100×ln(1+Rt

100), Rt = [exp(rt/100)−1]×100.

Temporal aggregation of the returns produces

1 +Rt(k) = (1+Rt)(1 +Rt−1) · · · (1 +Rt−k+1),

rt(k) = rt + rt−1 + · · ·+ rt−k+1.

These two relations are important in practice, e.g.

obtain annual returns from monthly returns.

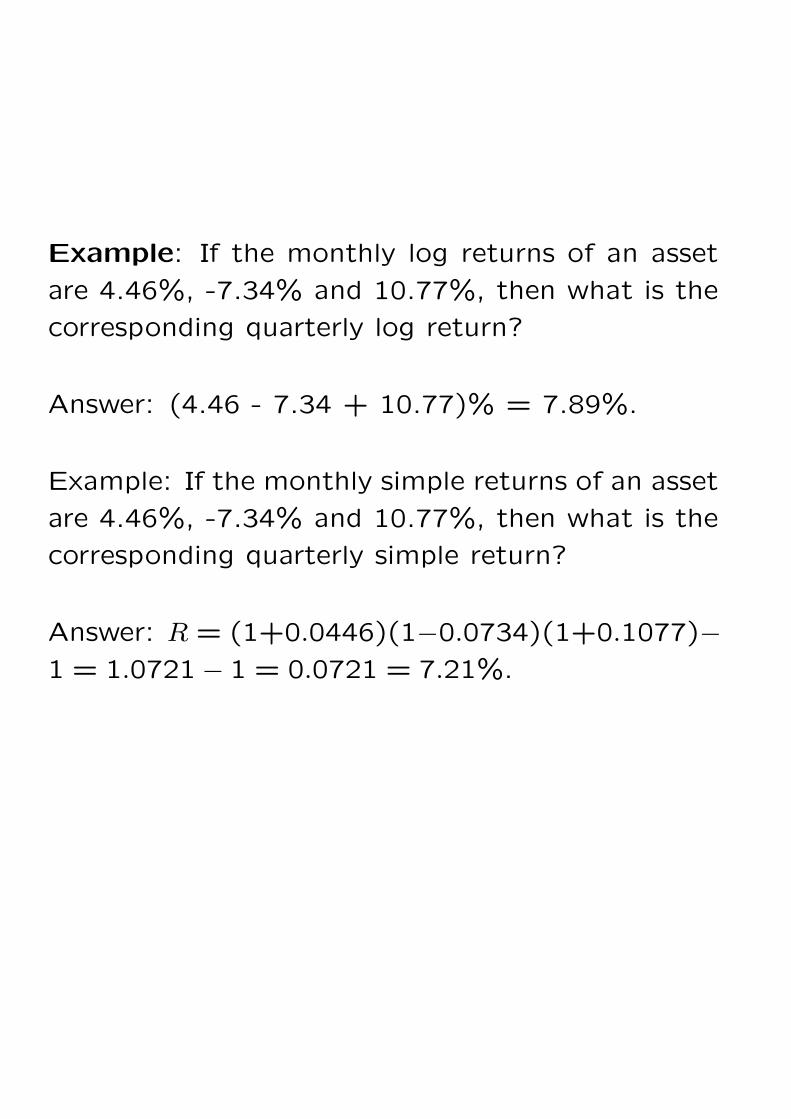

Example: If the monthly log returns of an asset

are 4.46%, -7.34% and 10.77%, then what is the

corresponding quarterly log return?

Answer: (4.46 - 7.34 + 10.77)% = 7.89%.

Example: If the monthly simple returns of an asset

are 4.46%, -7.34% and 10.77%, then what is the

corresponding quarterly simple return?

Answer: R = (1+0.0446)(1−0.0734)(1+0.1077)−1 = 1.0721− 1 = 0.0721 = 7.21%.

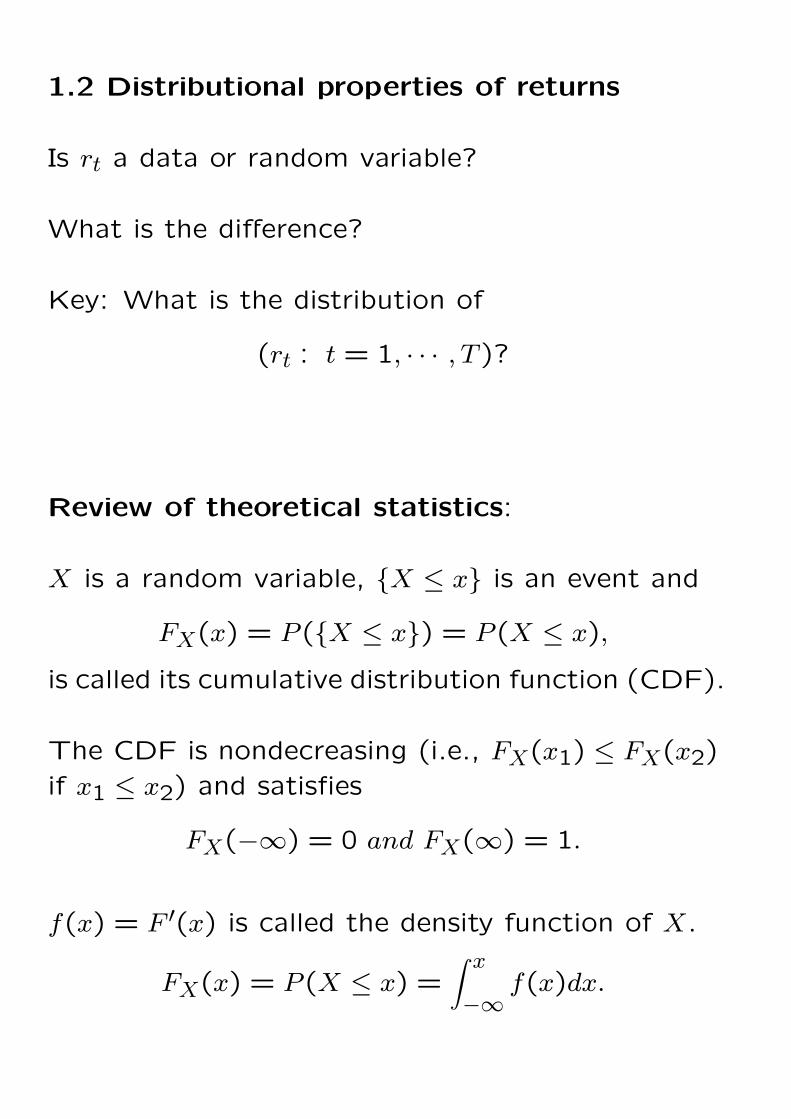

1.2 Distributional properties of returns

Is rt a data or random variable?

What is the difference?

Key: What is the distribution of

(rt : t = 1, · · · , T )?

Review of theoretical statistics:

X is a random variable, {X ≤ x} is an event and

FX(x) = P ({X ≤ x}) = P (X ≤ x),

is called its cumulative distribution function (CDF).

The CDF is nondecreasing (i.e., FX(x1) ≤ FX(x2)if x1 ≤ x2) and satisfies

FX(−∞) = 0 and FX(∞) = 1.

f(x) = F ′(x) is called the density function of X.

FX(x) = P (X ≤ x) =∫ x

−∞f(x)dx.

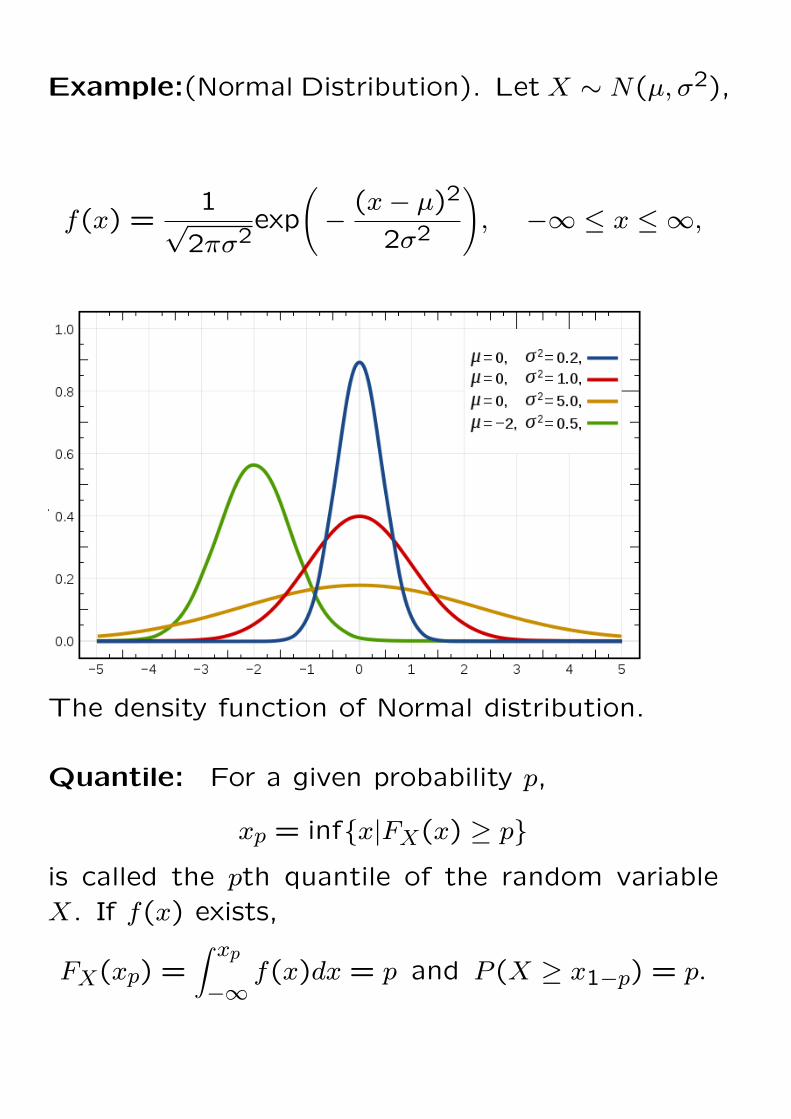

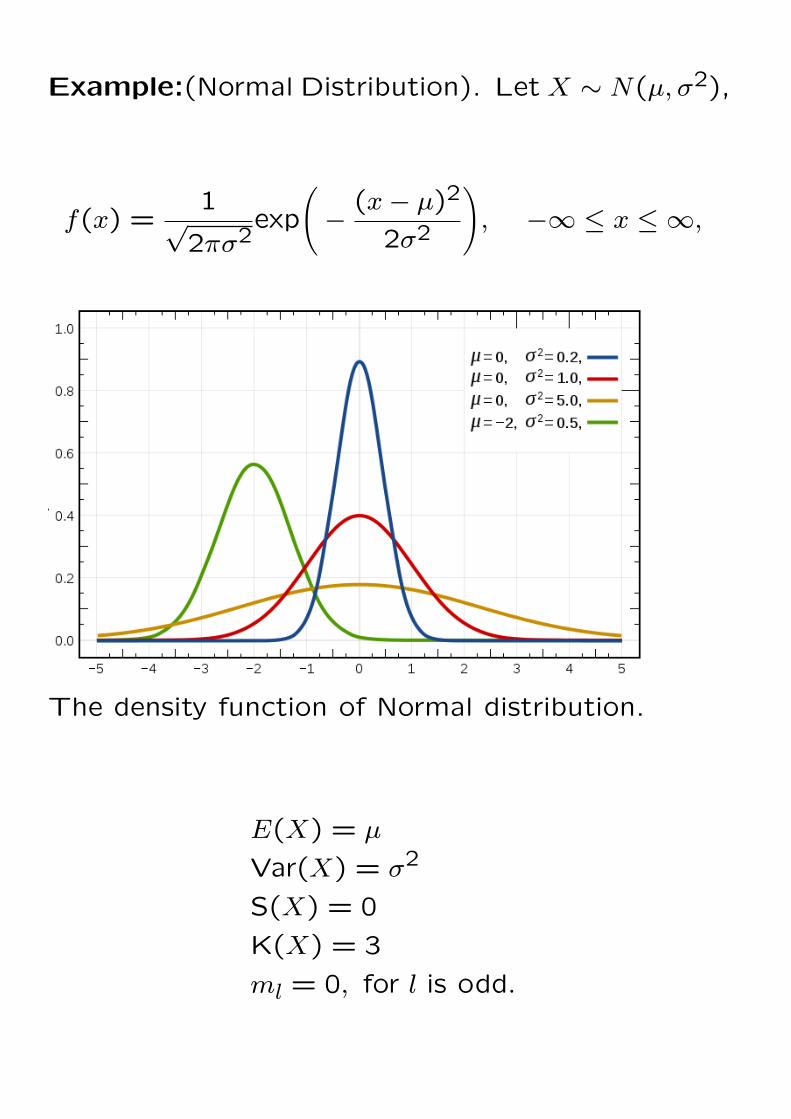

Example:(Normal Distribution). Let X ∼ N(µ, σ2),

f(x) =1√2πσ2

exp

(−

(x− µ)2

2σ2

), −∞ ≤ x ≤ ∞,

The density function of Normal distribution.

Quantile: For a given probability p,

xp = inf{x|FX(x) ≥ p}

is called the pth quantile of the random variableX. If f(x) exists,

FX(xp) =∫ xp

−∞f(x)dx = p and P (X ≥ x1−p) = p.

Moments of a random variable X:

Mean and variance:

µx = E(X) and σ2x = Var(X) = E(X − µx)2

Skewness (symmetry) and kurtosis (fat-tails)

S(x) = E(X − µx)3

σ3x, K(x) = E

(X − µx)4

σ4x.

K(x)− 3: Excess kurtosis.

The l−th moment and l−th central moment:

m′l = E(Xl) =

∫ ∞

−∞xlf(x)dx.

ml = E[(X − µx)l] =

∫ ∞

−∞(x− µx)

lf(x)dx,

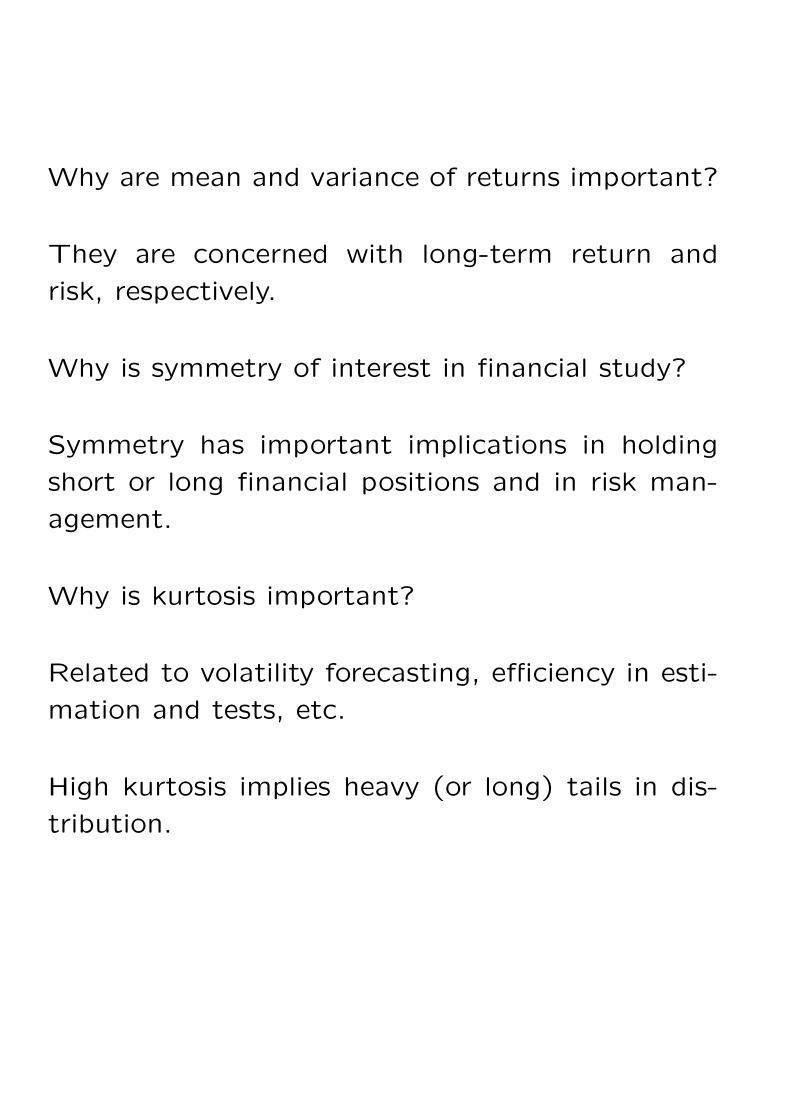

Why are mean and variance of returns important?

They are concerned with long-term return and

risk, respectively.

Why is symmetry of interest in financial study?

Symmetry has important implications in holding

short or long financial positions and in risk man-

agement.

Why is kurtosis important?

Related to volatility forecasting, efficiency in esti-

mation and tests, etc.

High kurtosis implies heavy (or long) tails in dis-

tribution.

Example:(Normal Distribution). Let X ∼ N(µ, σ2),

f(x) =1√2πσ2

exp

(−

(x− µ)2

2σ2

), −∞ ≤ x ≤ ∞,

The density function of Normal distribution.

E(X) = µ

Var(X) = σ2

S(X) = 0

K(X) = 3

ml = 0, for l is odd.

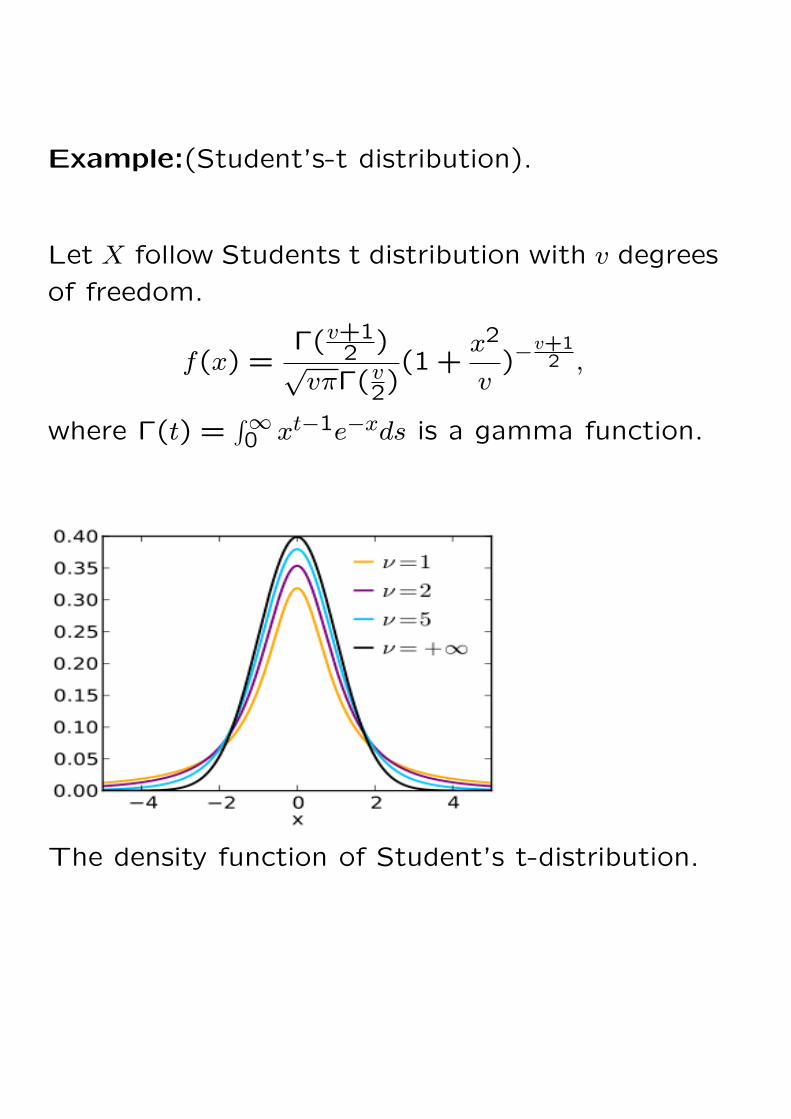

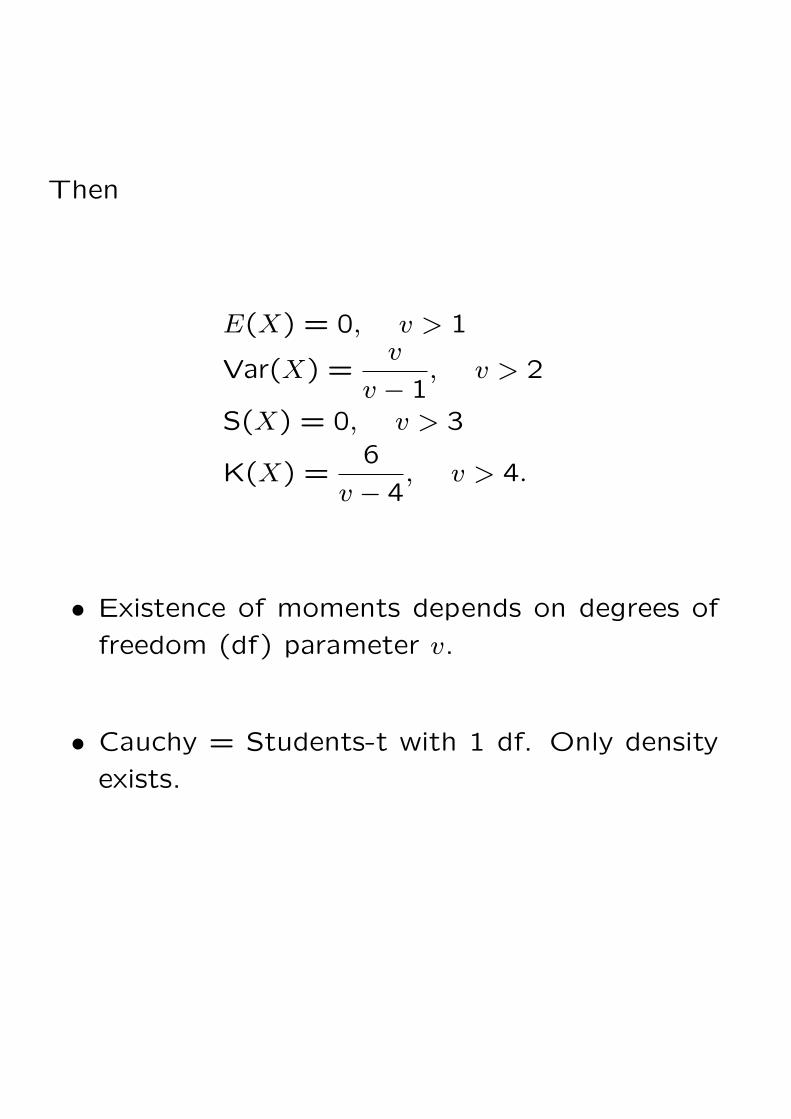

Example:(Student’s-t distribution).

Let X follow Students t distribution with v degrees

of freedom.

f(x) =Γ(v+1

2 )√vπΓ(v2)

(1 +x2

v)−

v+12 ,

where Γ(t) =∫∞0 xt−1e−xds is a gamma function.

The density function of Student’s t-distribution.

Then

E(X) = 0, v > 1

Var(X) =v

v − 1, v > 2

S(X) = 0, v > 3

K(X) =6

v − 4, v > 4.

• Existence of moments depends on degrees of

freedom (df) parameter v.

• Cauchy = Students-t with 1 df. Only density

exists.

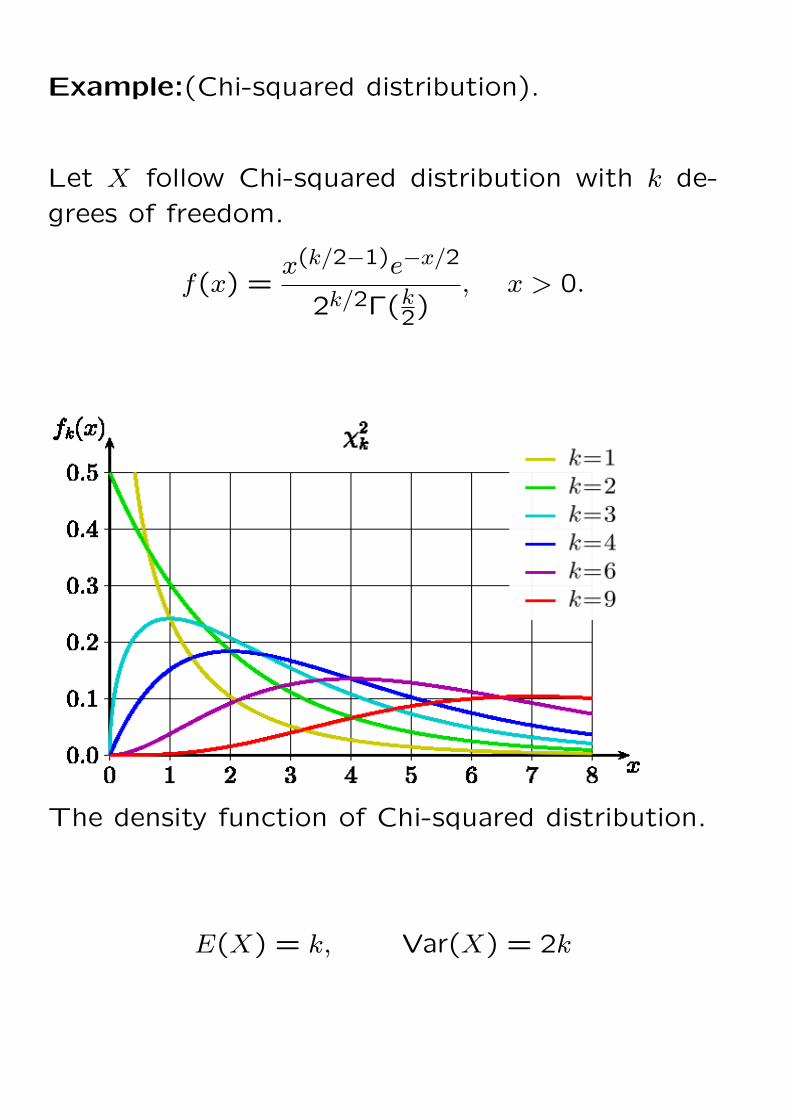

Example:(Chi-squared distribution).

Let X follow Chi-squared distribution with k de-

grees of freedom.

f(x) =x(k/2−1)e−x/2

2k/2Γ(k2), x > 0.

The density function of Chi-squared distribution.

E(X) = k, Var(X) = 2k

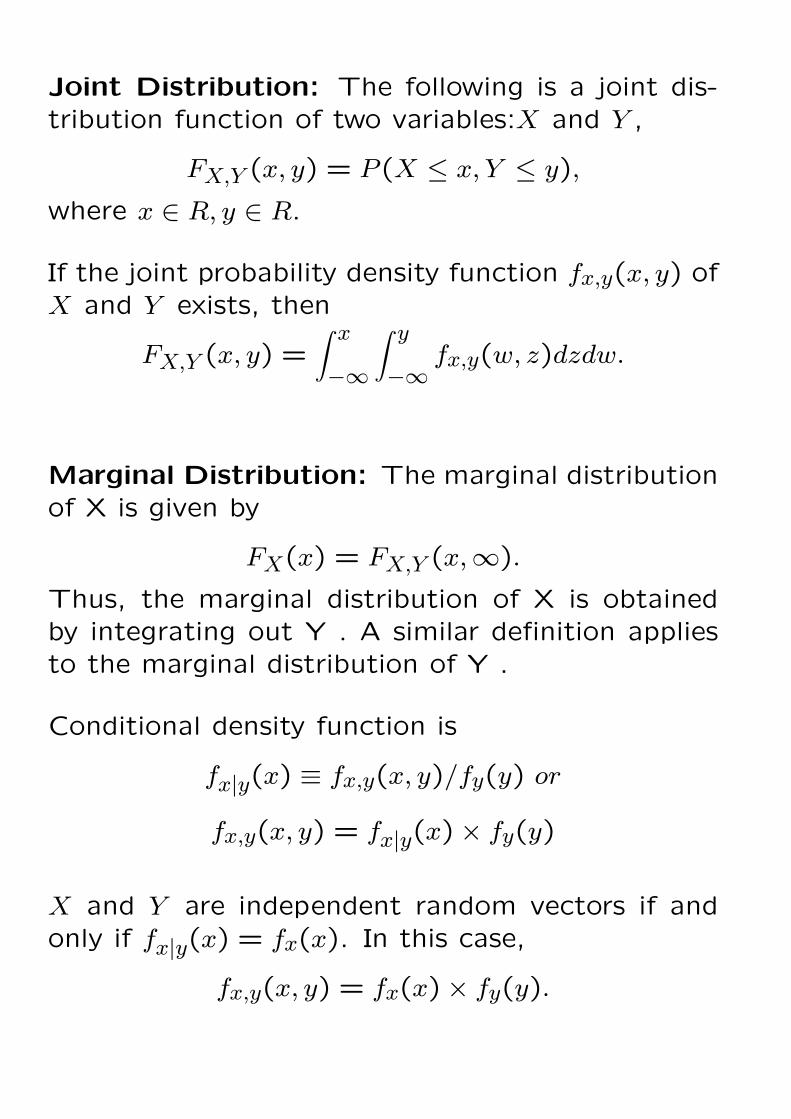

Joint Distribution: The following is a joint dis-tribution function of two variables:X and Y ,

FX,Y (x, y) = P (X ≤ x, Y ≤ y),

where x ∈ R, y ∈ R.

If the joint probability density function fx,y(x, y) ofX and Y exists, then

FX,Y (x, y) =∫ x

−∞

∫ y

−∞fx,y(w, z)dzdw.

Marginal Distribution: The marginal distributionof X is given by

FX(x) = FX,Y (x,∞).

Thus, the marginal distribution of X is obtainedby integrating out Y . A similar definition appliesto the marginal distribution of Y .

Conditional density function is

fx|y(x) ≡ fx,y(x, y)/fy(y) or

fx,y(x, y) = fx|y(x)× fy(y)

X and Y are independent random vectors if andonly if fx|y(x) = fx(x). In this case,

fx,y(x, y) = fx(x)× fy(y).

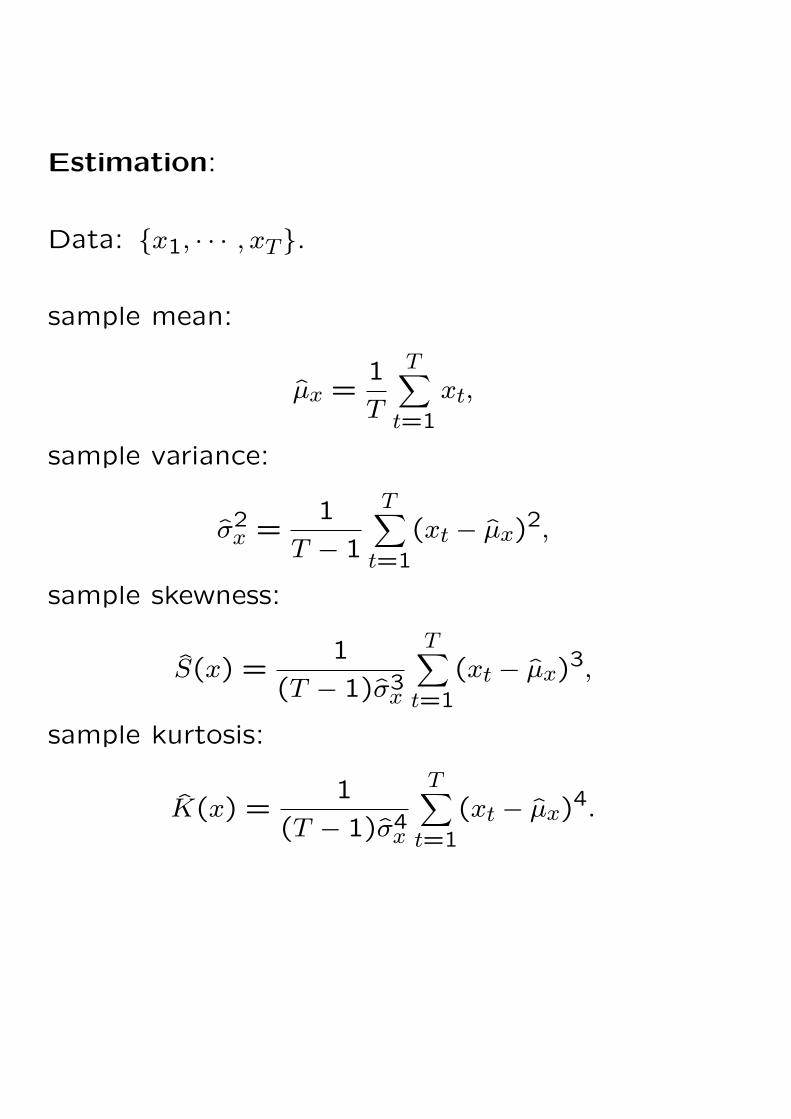

Estimation:

Data: {x1, · · · , xT}.

sample mean:

µx =1

T

T∑t=1

xt,

sample variance:

σ2x =1

T − 1

T∑t=1

(xt − µx)2,

sample skewness:

S(x) =1

(T − 1)σ3x

T∑t=1

(xt − µx)3,

sample kurtosis:

K(x) =1

(T − 1)σ4x

T∑t=1

(xt − µx)4.

Random sample: {x1, · · · , xT}.

µx, σ2x, S(x) and K(x) are random.

If Xi’s are iid N(µ, σ2), we can show that

S(x) ∼ N(0,6

T), K(x)− 3 ∼ N(0,

24

T).

Some simple tests for normality (for large T ).

1. Test for H0: symmetry v.s. H1: asymmetry:

S∗ =S(x)√6/T

∼ N(0,1)

if normality holds.

Decision rule: Reject H0 of a symmetric distribu-tion if |S∗| > Zα/2 or p-value is less than α.

2. Test for

H0 : K(x) = 3(thick tail) v.s. H1 : K(x) = 3.

K∗ =K(x)− 3√

24/T∼ N(0,1)

if normality holds.

Decision rule: Reject H0 of normal tails if |K∗| >Zα/2 or p-value is less than α

3. A joint test (Jarque-Bera test):

JB = (K∗)2 + (S∗)2 ∼ χ22,

if normality holds, where χ22 denotes a chi-squared

distribution with 2 degrees of freedom.

H0 : X ∼ N(µ, σ2) v.s.H1 : X ∼ N(µ, σ2).

Decision rule: Reject H0 of normality if JB >

χ22(α) or p-value is less than α.

Goodness-of-Fit Tests in SAS

Assume r1, · · · , rn are i.i.d with a common dis-

tribution function F(x). Order {r1, · · · , rn} from

smallest to largest as r(1), ..., r(n). The empirical

distribution function, Fn(x), is defined as

Fn(x) =1

n

n∑t=1

I{rt ≤ x} =1

n

n∑i=1

I{r(i) ≤ x}

=

0 if x < r(1)in if r(i) ≤ x < r(i+1), i = 1, · · · , n− 11 if x ≥ r(n).

Fn(x) is an estimator of F (x) and Fn(x) ≈ F (x).

PROC UNIVARIATE provides three EDF tests:

Kolmogorov-Smirnov (D)

Anderson-Darling (A− sq)

Cramr-von Mises (W − sq)

Kolmogorov D Statistic:

Dn = supx

|Fn(x)− F (x)|.

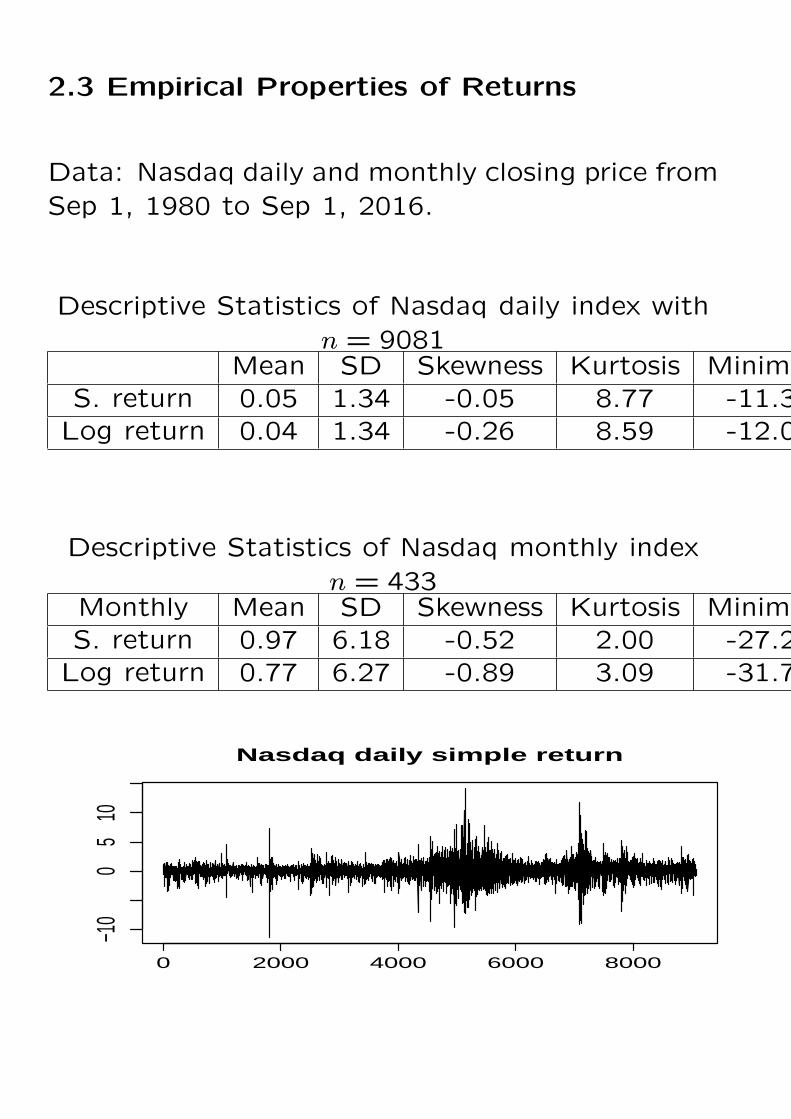

2.3 Empirical Properties of Returns

Data: Nasdaq daily and monthly closing price fromSep 1, 1980 to Sep 1, 2016.

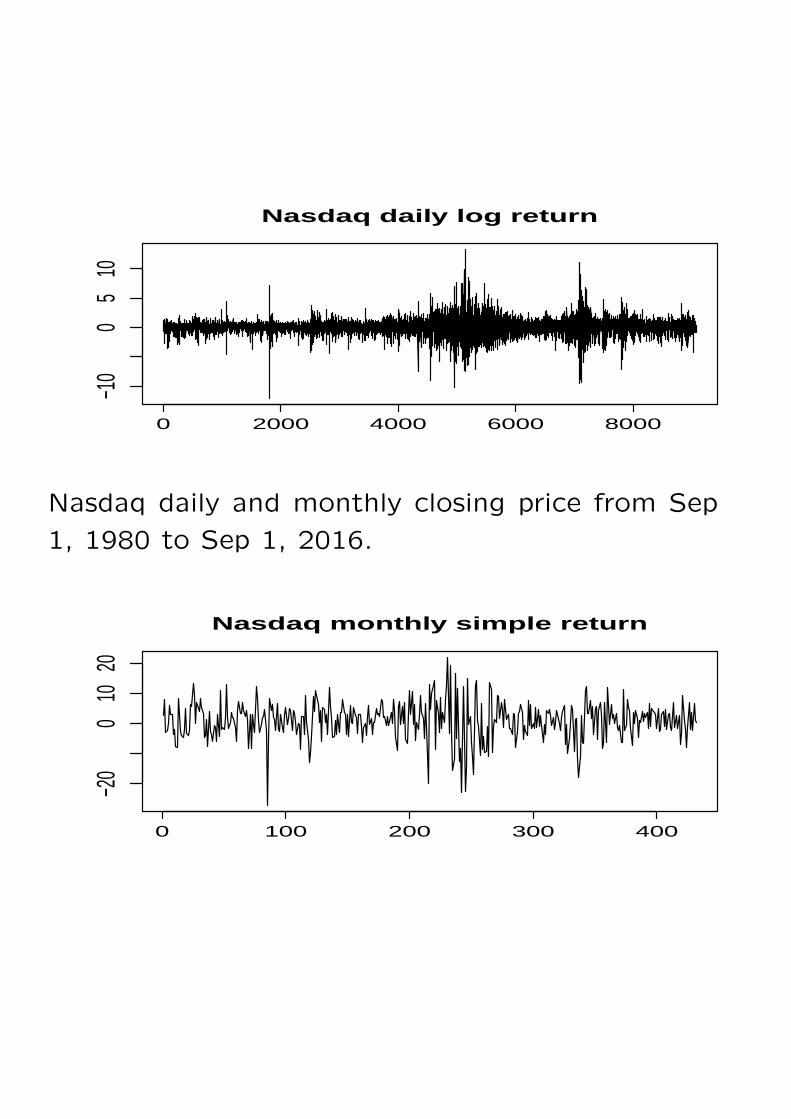

Descriptive Statistics of Nasdaq daily index withn = 9081

Mean SD Skewness Kurtosis Minimum MaximumS. return 0.05 1.34 -0.05 8.77 -11.35 14.17Log return 0.04 1.34 -0.26 8.59 -12.04 13.25

Descriptive Statistics of Nasdaq monthly indexn = 433

Monthly Mean SD Skewness Kurtosis Minimum MaximumS. return 0.97 6.18 -0.52 2.00 -27.23 21.98Log return 0.77 6.27 -0.89 3.09 -31.79 19.87

0 2000 4000 6000 8000

−10

05

10

Nasdaq daily simple return

0 2000 4000 6000 8000

−10

05

10

Nasdaq daily log return

Nasdaq daily and monthly closing price from Sep

1, 1980 to Sep 1, 2016.

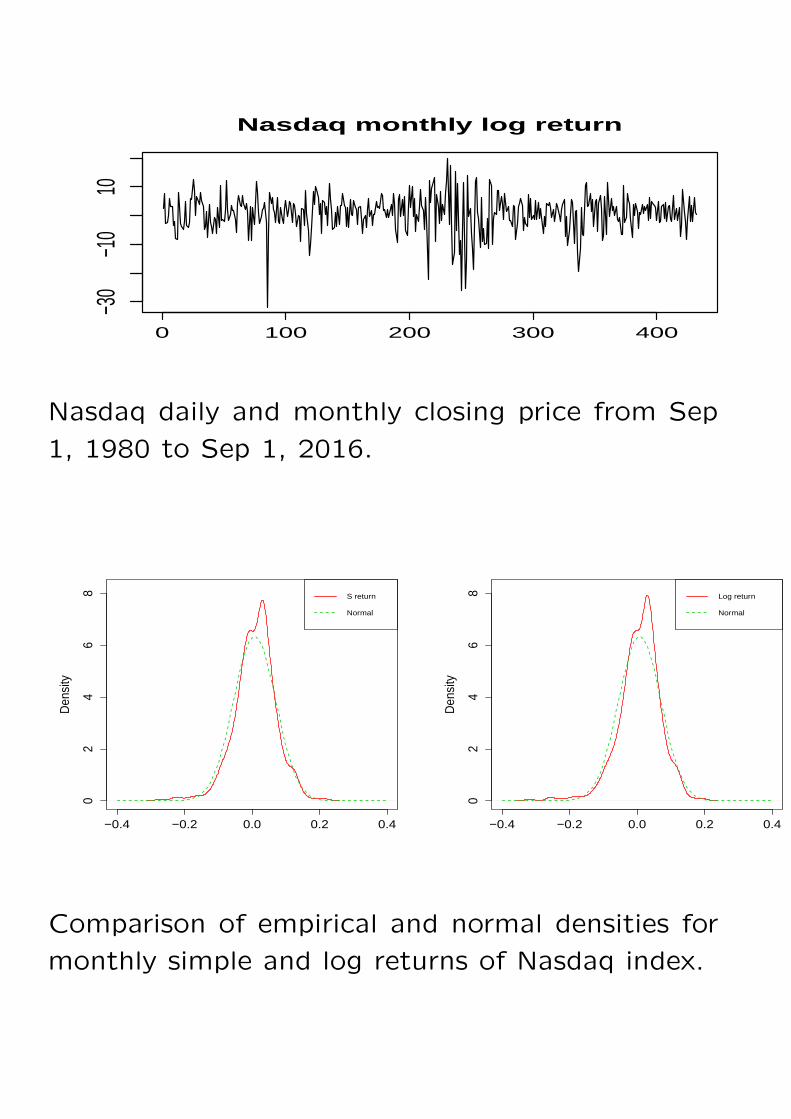

0 100 200 300 400

−20

010

20

Nasdaq monthly simple return

0 100 200 300 400

−30

−10

10Nasdaq monthly log return

Nasdaq daily and monthly closing price from Sep

1, 1980 to Sep 1, 2016.

−0.4 −0.2 0.0 0.2 0.4

02

46

8

Den

sity

S return

Normal

−0.4 −0.2 0.0 0.2 0.4

02

46

8

Den

sity

Log return

Normal

Comparison of empirical and normal densities for

monthly simple and log returns of Nasdaq index.

Related Documents