Chapter 1 Getting Started

Chapter 1 Getting Started. Chap 1 --- Getting Started We take value creation as a company’s objective, through its investments in real assets. On.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 1

Getting Started

Chap 1 --- Getting Started

We take value creation as a company’s objective, through its investments in real assets.

On the make-or-break investments that are strategic in nature.

We want it to be a useful tool that shows how to use Real Options Analysis ( ROA ) in enough detail that today’s managers, most of whom are familiar with the use of a personal computer, can work through a problem from start to finish and fully understand the results.

Estimating the NPV without flexibility, Modeling the uncertainties that drive

the value of the investment, Putting decision nodes into the event

tree that is built to reflect the uncertainties, and

Valuing the real options using a replicating portfolio approach

An analogy - Getting from here to there

Turnpike theorem, which says that it’s preferable to go a little out of your way to take advantage of higher speed paths.

Using your expected route – no detours, no traffic jams, no bad weather – no ability to respond to uncertainty.

There are at least five different types of managerial flexibility to respond to uncertainties.

Definition of a real option A real option is the right, but not the obligation, to take an action ( e.g., deferring,

expanding, contracting, or abandoning ) at a predetermined cost called the exercise price, for a predetermined period of time – the life of the option.

We would go so far as to say that NPV systematically undervalues every project. 1. The value of the underlying risky asset, a project, investment, or acquisition. 2. The exercise price. 3. The time to expiration of the option. 4. The standard deviation of the value of the underlying risky asset. 5. The risk-free rate of interest over the life of the option. The sixth variable is the dividends that may be paid out by the underlying asset :

the cash outflows or inflows over its life.

It seems that Thales read the tea leaves and interpreted them as forecasting a bountiful olive harvest that year.

The underlying risky asset was the rental value of the olive presses.

The driving cause of the uncertainty was the variability of the olive harvest, but the actual variable of interest ( the underlying risky asset ) was the standard derivation of the value of the rental fee on the olive presses.

The exercise price was the normal rental rate, a value that had been written into the contract.

The risk-free rate was, presumably, an observable market rate.

And the time to maturity was the time until the olive harvest.

The value of the option was the money that Thales paid to the owners of the presses – his life’s savings.

You have the opportunity to buy a toy bank that allows you to put in a dollar today and guarantees you $1.05 with absolute certainty a year later if you do. The offer is good for one year. However, interest rates at real bank are 10 percent right now. How much is the toy bank worth?

x1

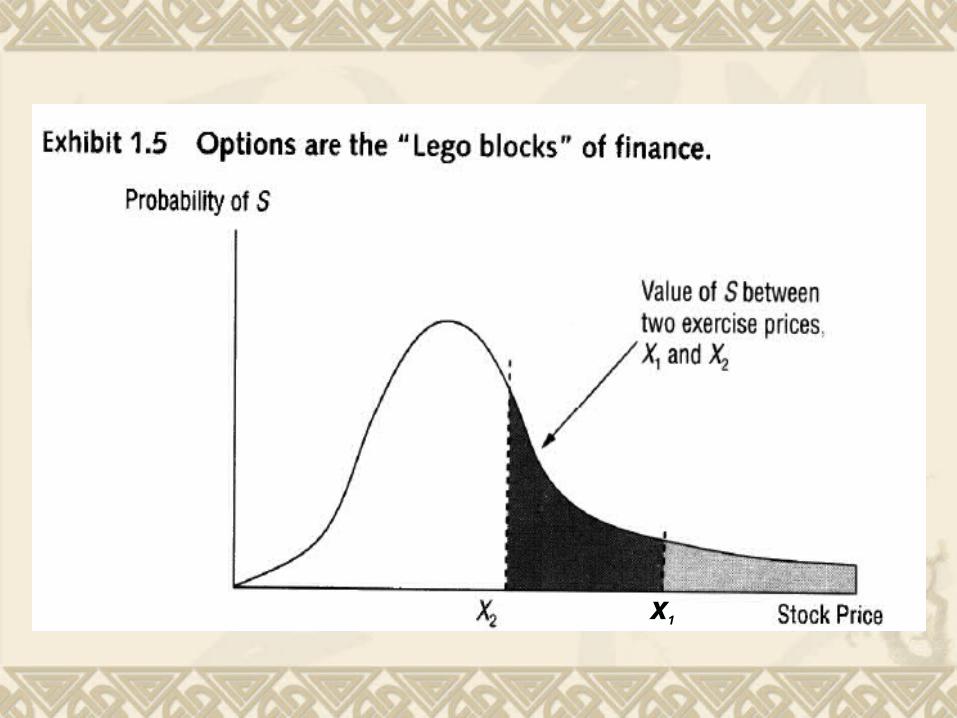

Real options dictionary

A call option where the price of the underlying is above the exercise price so that an immediate profit could be made by exercising the option is said to be in-the-money.

Conversely, if the price of the underlying is below the exercise price the option is out-of-the-money.

Options that can be exercise only on their maturity date are called European options. Those that can be exercised any time during their life are called American options.

There are also boundary conditions called caps and floors that bound the value of the underlying.

Taxonomy of real options Real options are classified primarily by the type of flexibility

that they offer. For example, an option is just what it seems to be - the

right, but not the obligation to invest in a project at a later date.

A deferral option is an American call option found in most projects where one has the right to delay the start of a project. Its exercise price is the money invested in getting the project started.

The option to abandon a project for a fixed price ( even that price decrease through time ) is formally an American put.

So is the option to contract ( scale back ) by selling a fraction of it for a fixed price.

The option to expand a project by paying more to scale up the operations is an exercise price is also an American call.

Switching options are portfolios of American call and put options that allow their owner to switch at a fixed cost ( or costs ) between two modes of operations.

There are also options on options, called compound options. Phased investments fit into this category.

Options that are driven by multiple sources of uncertainty are called rainbow options.

Most real options are affected by uncertainty regarding the price of a unit of output, the quantity that might be sold, and by uncertain interest rates that affect the present value of the project.

Many real-world applications require modeling as compound rainbow options.

Real options are everywhere – war stories

First, isn’t the option value of managerial flexibility always positive and consequently isn’t the use of real option just an attempt to justify projects that should be turned down?

First, the appropriate mind-set is to recognize that the net present value technique systematically undervalues everything because it fails to capture the value of flexibility.

And second, while the value of flexibility is always positive, the price that you have to pay for it often exceeds its value.

The second question is, when is the use of real options likely to change the answer a lot?

Real options have the greatest value when three factors come together.

When there is high uncertainty and when managers have flexibility to respond to it, real options are important. But the value of real options relative to NPV is large when the NPV is close to zero, in the gray area.

If the NPV is high, then most options that provide additional flexibility will have a very low probability of being exercised, and therefore have low relative value.

If the NPV is extremely negative, no amount of optionality can rescue the project.

Deferral call option

Having a deferral option, allowing them to postpone their development decision until the price of coal increased enough to make them relatively certain that they could recover their development costs before the price turned around and fell again.

Node that this example illustrates a fundamental difference between NPV and ROA that will be discussed in detail later on.

Real options analysis combines them into a single present value – a go or no go decision today – with a decision rule about when to develop the lease.

American put option : a cancelable operating lease

The lease could be canceled either redelivery or for a period of time after delivery of the aircraft – a walk-away option.

If he stopped offering the cancellation feature. Subsequently, we segmented the market into categories

based on the variability of estimated operating income, which in turn depends on the variability of passenger revenue miles.

The jet engine manufacturer decided to stop offering the cancellation feature to these airlines where the value of the cancellation feature was greatest, preferring to lose their business to competitors.

Opening and closing mines : switching options

Switching options are the right to close an operation that is currently open by paying fixed shutdown costs and the right to open it later for a different fixed cost to a common type of option, actually a portfolio of puts and calls.

Application of switching options in mining. Not only does the real options approach reveal the added value from the ability to close then reopen the mine, but it also provides rules of thumb about when to do so.

Real options approaches to this problem show that the flexibility to shut down and reopen adds value to the mine, adds more value if the switching costs are low, and tells the mining company exactly what trigger prices to use for optimal operation.

Phased investment in a chemical plant : a compound option

A real option approach viewed the project as a series of compound options – each option depending on the exercise of those that preceded it.

Thus Phase II is a call option that is contingent on Phase I.

Many executive decisions are made in phase without recommitment to undertake all phases regardless of how uncertainties that drive the value of the project might evolve.

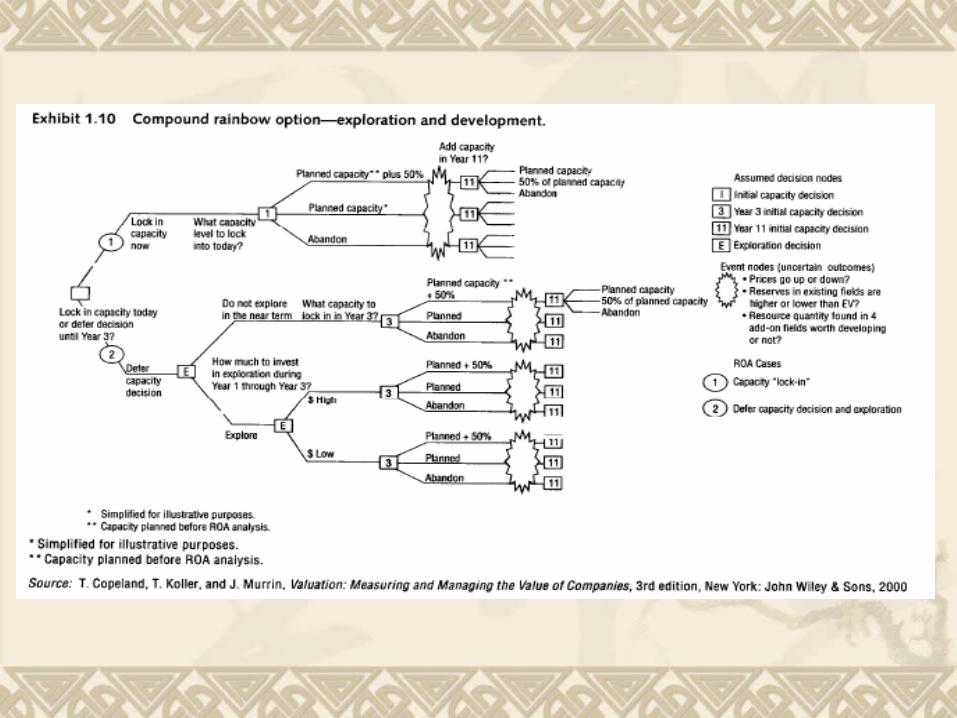

Exploration and development: A compound rainbow option

Compound rainbow options are perhaps the most realistic and the most complex real options that we will show you how to value.

But they cover a wide and important class of decision : In addition to exploration and development, they are useful for research and development, and new product development decisions.

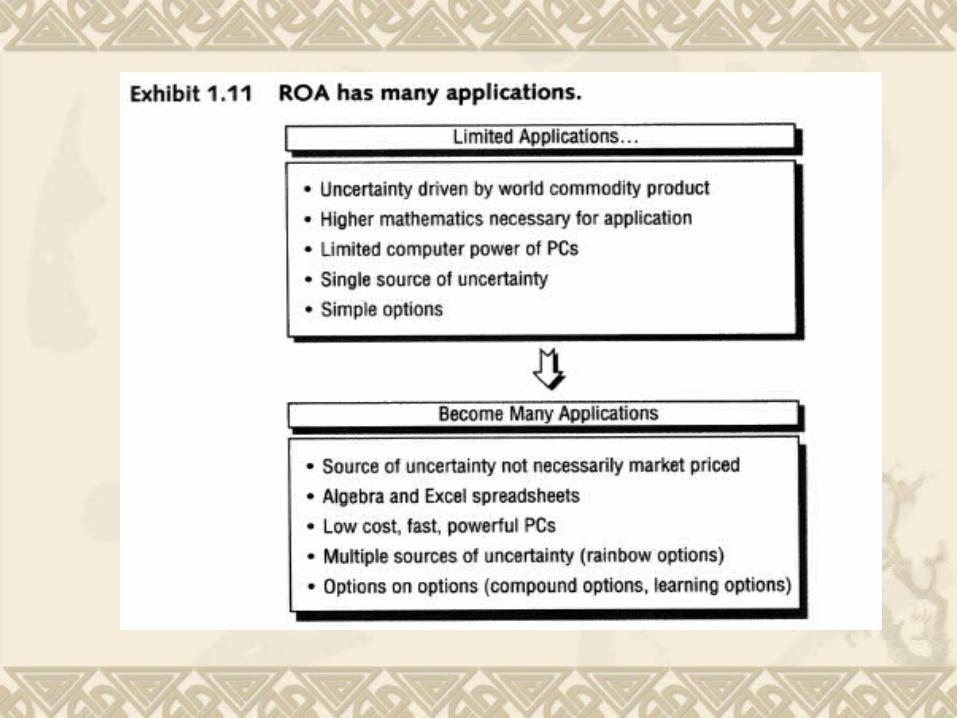

The speed and capacity of personal computers have advanced so rapidly that only recently have managers had at their disposal enough easy-to-access computer power to bring realism and transparency to the table.

Now we realize that real options can be applied to almost any situation where it is possible to estimate the understand and to value real options for many realistic applications including those that are compound options and that have multiple sources of uncertainty.

Conclusion

Real options analysis values the flexibility to respond to uncertain events – net present value techniques do not and consequently undervalue everything.

Related Documents

![Skaffold - storage.googleapis.com · [getting-started getting-started] Hello world! [getting-started getting-started] Hello world! [getting-started getting-started] Hello world! 5.](https://static.cupdf.com/doc/110x72/5ec939f2a76a033f091c5ac7/skaffold-getting-started-getting-started-hello-world-getting-started-getting-started.jpg)