Financial Accounting Environment Balance Sheet (Financial Position) ▪ Income Statement (Statement of Operations) ▪ Statement of Cash Flows ▪ Statement of Shareholders' Equity ▪ Financial Statements provided are; ○ Primary Focus of financial accounting is on the information needs of investors and creditors. - Financial Reporting: Process of providing financial statement information to external users. - Capital Markets: Mechanisms that foster the allocation of resources efficiently. - Corporation: The dominate form of business organization that acquires capital from investors in exchange for ownership interest and from creditors by borrowing. - Initial Market Transactions: Provide for new cash by the issuance of stocks and bonds by the corporation. - Secondary Market Transactions: Provide for the transfer of stocks and bonds among individuals and institutions. - What information do investors and creditors need when determining which companies will receive capital? The Investment-Credit Decision -- A Cash Flor Perspective: Investors and creditors are interested in earning a fair return on the resources they provide, the expected rate of return and the uncertainty, or risk, of that return are key variables in the investment decision. - Rate of Return: (Dividends + Share Price Appreciation) / Initial investment = RATE OF RETURN. - A company will be able to provide a return to investors and creditors only if it can generate a profit from selling goods/services. - The objective of financial accounting is to provide investors and creditors with useful information for decision making. - Cash vs Accrual Accounting: This is the best model to predict future cash flows. ○ Accrual Accounting: Measurement of the entity's accomplishments and resource sacrifices during the period, regardless of when cash is received or paid. - Produces a measure called net operating cash flow, this measure is the difference between cash receipts and cash payments from transactions. ○ Net Operating cash flow is the difference between cash receipts and cash disbursements from providing goods/services. ○ A variable of concern, over short periods of time operating cash flows may not be indicative of the company's long run cash generating ability. ○ Cash Basis Accounting: - At the beginning of the first year, Carter prepaid $60,000 for three years' rent on the facilities. The company also incurred utility costs of $10,000 per year over the period. However, during the first year only $5,000 actually was paid, with the remainder being paid the second year. Employee salary costs of $50,000 were paid in full each year. Is net operating cash flow for year 1 (negative $65,000) an accurate indicator of future cash-generating ability? Clearly not, given that the next two years show positive net cash flows. Is the three-year pattern of net operating cash flows indicative of the company's year-by-year performance? No, because the years in which Carter paid for rent and utilities are not the same as the years in which Carter actually consumed those resources. Accrual Accounting: Net income is considered a better indicator of future operating cash flows than is current net operating cash flow: - Revenue for year 1 is the $100,000 sales. Given that sales eventually are collected in cash, the year 1 revenue of $100,000 is a better measure of the inflow of resources from company operations than is the $50,000 cash collected from customers. Also, net income of $20,000 for year 1 appears to be a reasonable predictor of the company's cash-generating ability, as total net operating cash flow for the three-year period is a positive $60,000. Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018 8:54 PM Intermediate Accounting I Page 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial Accounting Environment

Balance Sheet (Financial Position)▪

Income Statement (Statement of Operations)▪

Statement of Cash Flows▪

Statement of Shareholders' Equity ▪

Financial Statements provided are;○

Primary Focus of financial accounting is on the information needs of investors and creditors.-

Financial Reporting: Process of providing financial statement information to external users.-

Capital Markets: Mechanisms that foster the allocation of resources efficiently.-

Corporation: The dominate form of business organization that acquires capital from investors in exchange for ownership interest and from creditors by borrowing.-

Initial Market Transactions: Provide for new cash by the issuance of stocks and bonds by the corporation.-

Secondary Market Transactions: Provide for the transfer of stocks and bonds among individuals and institutions.-

What information do investors and creditors need when determining which companies will receive capital?

The Investment-Credit Decision -- A Cash Flor Perspective:

Investors and creditors are interested in earning a fair return on the resources they provide, the expected rate of return and the uncertainty, or risk, of that return are key variables in the investment decision.

-

Rate of Return: (Dividends + Share Price Appreciation) / Initial investment = RATE OF RETURN.-

A company will be able to provide a return to investors and creditors only if it can generate a profit from selling goods/services.-

The objective of financial accounting is to provide investors and creditors with useful information for decision making.-

Cash vs Accrual Accounting:

This is the best model to predict future cash flows.○

Accrual Accounting: Measurement of the entity's accomplishments and resource sacrifices during the period, regardless of when cash is received or paid.-

Produces a measure called net operating cash flow, this measure is the difference between cash receipts and cash payments from transactions.○

Net Operating cash flow is the difference between cash receipts and cash disbursements from providing goods/services.○

A variable of concern, over short periods of time operating cash flows may not be indicative of the company's long run cash generating ability.○

Cash Basis Accounting: -

At the beginning of the first year, Carter prepaid $60,000 for three years' rent on the facilities. The company also incurred utility costs of $10,000 per year over the period. However, during the first year only $5,000 actually was paid, with the remainder being paid the second year. Employee salary costs of $50,000 were paid in full each year.

Is net operating cash flow for year 1 (negative $65,000) an accurate indicator of future cash-generating ability? Clearly not, given that the next two years show positive net cash flows. Is the three-year pattern of net operating cash flows indicative of the company's year-by-year performance? No, because the years in which Carter paid for rent and utilities are not the same as the years in which Carter actually consumed those resources.

Accrual Accounting: Net income is considered a better indicator of future operating cash flows than is current net operating cash flow:-

Revenue for year 1 is the $100,000 sales. Given that sales eventually are collected in cash, the year 1 revenue of $100,000 is a better measure of the inflow of resources from company operations than is the $50,000 cash collected from customers. Also, net income of $20,000 for year 1 appears to be a reasonable predictor of the company's cash-generating ability, as total net operating cash flow for the three-year period is a positive $60,000.

Chapter 1 Environment and Theoretical Structure of Financial Accounting:Monday, May 21, 2018 8:54 PM

Intermediate Accounting I Page 1

Development of Financial Accounting and Reporting Standards:

Generally Accepted Accounting Principles (GAAP): Set of both broad and specific guidelines that companies should follow when measuring and reporting the information in their financial statements and related notes.

-

Mandates accounting and disclosure requirements for initial offerings of securities.○

Committee on Accounting Procedure (CAP) - initial committee of Accountants that issued Bulletins from 1938 to 1959 which dealt with specific accounting problems.

▪

Accounting Principles Board (APB) Replaced the cap through 1973 issued 31 Bulletins▪

Developed Conceptual framework - Deals with theoretical and conceptual issues and provides an underlying structure for current and future accounting and reporting standards.

□

Financial Accounting Standards Board (FASB) 1973 - Present, there are more full time members and represent various constituencies concerned with standards.

▪

The SEC has the authority to set accounting standards for companies, but has delegated the task to the private sector.○

International Financial Reporting Standards (IFRSs) - developed by the IASB and used by more than 100 countries. ▪

International Accounting Standards Board (IASB) - Helps to develop a single set of high-quality. Understandable global accounting standards, to promote the use of those standards, and to bring about the convergence of national accounting standards.

○

Securities and Exchange Commission (SEC) - created in 1933 & 1934 by Congress.-

Serves as an independent intermediary to help ensure that management has in fact appropriately applied GAAP in preparing the company's financial statements. "Offer credibility to financial statements."

○

In mores states only CPAs can represent that the financial statements have been audited in accordance with generally accepted auditing standards.

▪

Auditors express an opinion on the compliance of financial statements with GAAP○

The Role of Auditor:-

Collapse of Enron 2001○

Dismantling of international public accounting firms Arthur Andersen in 2002○

Sarbanes-Oxley: applies to public securities issuing entities, provides for the regulation of auditors and types of services they furnish to clients, increases accountability of corporate executives, addresses conflicts of interests for analysts and provides stiff penalties for violators.

○

Financial Reporting Reform-

Principles based approach to standard setting stresses professional judgement as opposed to following a list of rules. ▪

Argument made that the absence of detailed rules opens the door to even more abuse because management can use the latitude provided to justify their means.

□Focuses on professional judgement means there are few rules to sidestep, more likely to arrive at appropriate accounting treatment.▪

Detailed rules help auditors withstand pressure from clients who want a more favorable accounting treatment, and help companies ensure that they are complying with GAAP to avoid litigation or SEC inquiry.

▪

Principles-based (Objectives-oriented) vs Rules-based○

A Move Away from Rules-Based Standards-

Encouraging High-Quality Financial Reporting:

Ethics in Accounting

Ethical dilemma is a situation which individual or group is faced with decisions that test this code.○

Ethics: refers to a code or moral system that provides criteria for evaluating right and wrong. -

Accountants are faced with ethical dilemmas, some which are complex and difficult to resolve.-

Codes of Ethics for those in the accounting profession○

Public Accounting has achieved widespread recognition.○

Institute of Management Accounts (IMA)○

Institute of Internal Auditors○

Ethics and Professionalism.-

7 Steps: Determine facts, identify ethical issue and stakeholders, identify values related to situation, specify the alternative courses, evaluate the courses of action specified in step 4 in terms of their consistency with values identified in step 3, identify the consequences of each possible course of action, make your decision and take any actions.

○

Analytical Model for Ethical Decisions.-

Conceptual framework: deals with theoretical and conceptual issues and provides an underlying structure for current and future accounting and reporting standards.

-

Does not prescribe GAAP. It provides an underlying foundation for accounting standards.○

The Conceptual Framework:

Objective of Financial Reporting-

Intermediate Accounting I Page 2

Provide financial information about companies that is useful to capital providers in making decisions. ○

Relevance & Faithful representation□Decision usefulness: the quality of being useful to decision making.▪

Relevance:▪

Must have predictive value and/or confirmatory value. Typically Both, example could be current-period net income can predict future cash flows, and can confirm if it helps investors confirm or change assessments regarding the company's cash flow generating abilities.

□

Financial information is material if omitting it or misstating it could affect users decision.□Professional Judgment determines what amount is material in each situation□

Faithful Representation:▪

Agreement between a description or measure that it represents. For example: inventory in balance sheet wouldn't include accounts receivables because its not agreed that its where A/R goes.

□

Complete - it includes all information necessary for faithful representation

Neutrality - Implies freedom from bias, high quality answers away from political/social pressures to produce favorable outcomes.

Free from Error - No errors or omissions, estimates are common and some inaccuracy is likely, but a good estimate that is represented faithfully is one that is clearly described and users are given enough information to understand that potential for inaccuracy.

Complete, Neutral, and free from error.□

Undermines representational faithfulness, but being inconsistent with neutrality.

It is an important consideration though in order to not overinflate companies that mislead investors.

Conservatism does not equal neutrality.□

What characteristics of financial reporting should have the most use?○

Enhancing Qualitative Characteristics.-

Accounting information should be comparable across different companies and over different time periods.○

Comparability helps users see similarities and differences between events and conditions.▪

Consistency: permits valid comparisons between different periods.▪

Verifiability implies that different knowledgeable and independent measures would reach consensus regarding whether info is a faithful representation.

▪

Timeliness, when information is available to users early enough to allow them to use it in their decision process.▪

Understandability, means that their users are able to comprehend the information within the context of the decision being made, user specific quality because users will differ in comprehension. (Reasonable understanding of business/economics)

▪

Cost Effectiveness: the perceived benefit of increased decision usefulness exceeds the anticipated cost of providing that information.○

Costs include gathering, processing, and disseminating information. Users pay a cost by interpreting information.▪

Also adverse costs of implementing accounting standards and information gathering.▪

Key Constraints: Cost Effectiveness.-

Elements of Financial Statements-

Economic entity○

Going concern

Underlying Assumptions to GAAP-

Intermediate Accounting I Page 3

Going concern○

Periodicity○

Monetary unit.○

All economic events can be identified with a particular economic entity.○

For example, if you were considering buying some ownership stock in Google, you would want information on the various operating units that constitute Google. You would need information not only about its United States operations but also about its European and other international operations. As well as the financial information of the various companies that Google owns a controlling interest (>50%)

○

For small businesses personal residences and other assets are not considered part of this because they are not assets of the business.○

Economic Entity-

We anticipate that a business entity will continue to operate indefinitely.○

Accountants realize that this assumption does not always hold true, but this assumption helps justify measuring any assets based on historical costs.

○

Financial statements of a company presume the business is a going concern.○

Going Concern Assumption.-

Allows the life of a company to be divided into artificial time periods to provide timely info.○

External users need this to make decisions, quarterly/annual statements. Financial statements often prepared monthly.○

Fiscal years can vary but as long as it's consistent to the external users it's okay.○

Periodicity Assumption-

Measurement scale used in financial statements and nominal units of money ○

US dollar, to euro in EU○

Monetary Unit Assumption-

Intermediate Accounting I Page 4

"The Basic Model"

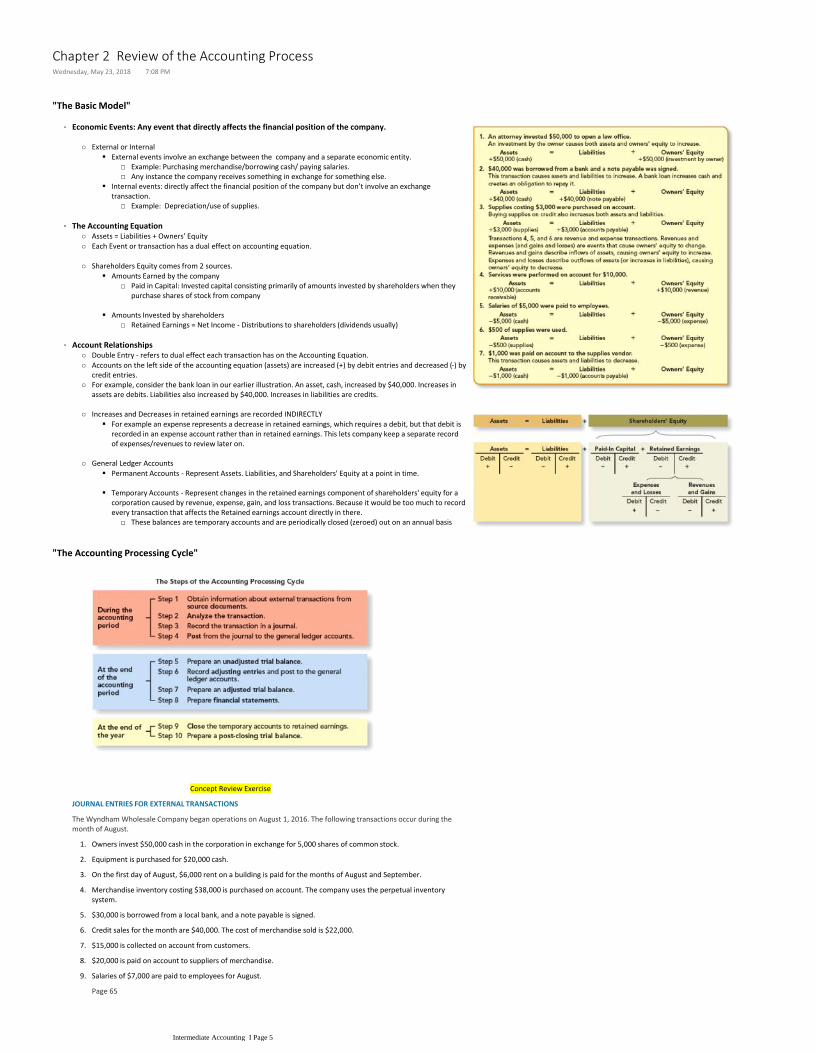

Economic Events: Any event that directly affects the financial position of the company.-

Example: Purchasing merchandise/borrowing cash/ paying salaries.□Any instance the company receives something in exchange for something else.□

External events involve an exchange between the company and a separate economic entity.▪

Example: Depreciation/use of supplies.□

Internal events: directly affect the financial position of the company but don’t involve an exchange transaction.

▪

External or Internal○

Assets = Liabilities + Owners' Equity○

Each Event or transaction has a dual effect on accounting equation.○

The Accounting Equation-

Paid in Capital: Invested capital consisting primarily of amounts invested by shareholders when they purchase shares of stock from company

□Amounts Earned by the company▪

Retained Earnings = Net Income - Distributions to shareholders (dividends usually)□Amounts Invested by shareholders▪

Shareholders Equity comes from 2 sources.○

Double Entry - refers to dual effect each transaction has on the Accounting Equation.○

Accounts on the left side of the accounting equation (assets) are increased (+) by debit entries and decreased (-) by credit entries.

○

For example, consider the bank loan in our earlier illustration. An asset, cash, increased by $40,000. Increases in assets are debits. Liabilities also increased by $40,000. Increases in liabilities are credits.

○

Account Relationships-

For example an expense represents a decrease in retained earnings, which requires a debit, but that debit is recorded in an expense account rather than in retained earnings. This lets company keep a separate record of expenses/revenues to review later on.

▪

Increases and Decreases in retained earnings are recorded INDIRECTLY○

Permanent Accounts - Represent Assets. Liabilities, and Shareholders' Equity at a point in time.▪

These balances are temporary accounts and are periodically closed (zeroed) out on an annual basis□

Temporary Accounts - Represent changes in the retained earnings component of shareholders' equity for a corporation caused by revenue, expense, gain, and loss transactions. Because it would be too much to record every transaction that affects the Retained earnings account directly in there.

▪

General Ledger Accounts○

Concept Review Exercise

JOURNAL ENTRIES FOR EXTERNAL TRANSACTIONS

Owners invest $50,000 cash in the corporation in exchange for 5,000 shares of common stock.1.

Equipment is purchased for $20,000 cash.2.

On the first day of August, $6,000 rent on a building is paid for the months of August and September.3.

Merchandise inventory costing $38,000 is purchased on account. The company uses the perpetual inventory system.

4.

$30,000 is borrowed from a local bank, and a note payable is signed.5.

Credit sales for the month are $40,000. The cost of merchandise sold is $22,000.6.

$15,000 is collected on account from customers.7.

$20,000 is paid on account to suppliers of merchandise.8.

Salaries of $7,000 are paid to employees for August.9.

Page 65A bill for $2,000 is received from the local utility company for the month of August.10.

The Wyndham Wholesale Company began operations on August 1, 2016. The following transactions occur during the month of August.

"The Accounting Processing Cycle"

Chapter 2 Review of the Accounting ProcessWednesday, May 23, 2018 7:08 PM

Intermediate Accounting I Page 5

A bill for $2,000 is received from the local utility company for the month of August.10.

$20,000 cash is loaned to another company, evidenced by a note receivable.11.

The corporation pays its shareholders a cash dividend of $1,000.12.

Prepare a journal entry for each transaction.1.

Prepare an unadjusted trial balance as of August 31, 2016.2.

Required:

The issuance of common stock for cash increases both cash and shareholders' equity (common stock).1.

The purchase of equipment increases equipment and decreases cash.2.

The payment of rent in advance increases prepaid rent and decreases cash.3.

The purchase of merchandise on account increases both inventory and accounts payable.4.

Borrowing cash and signing a note increases both cash and note payable.5.

The sale of merchandise on account increases both accounts receivable and sales revenue. Also, cost of goods sold increases and inventory decreases.

6.

The collection of cash on account increases cash and decreases accounts receivable.7.

The payment to suppliers on account decreases both accounts payable and cash.8.

Page 66The payment of salaries for the period increases salaries expense (decreases retained earnings) and decreases cash.

9.

The receipt of a bill for services rendered increases both an expense (utilities expense) and accounts payable. The expense decreases retained earnings.

10.

The lending of cash to another entity and the signing of a note increases note receivable and decreases cash.11.

Cash dividends paid to shareholders reduce both retained earnings and cash.12.

Prepare a journal entry for each transaction.1.

Prepare an unadjusted trial balance as of August 3l, 2016.2.

Account Title Debits Credits

Cash 21,000

Accounts receivable 25,000

Prepaid rent 6,000

Inventory 16,000

Note receivable 20,000

Equipment 20,000

Accounts payable 20,000

Note payable 30,000

Common stock 50,000

Retained earnings 1,000

Sales revenue 40,000

Cost of goods sold 22,000

Salaries expense 7,000

Utilities expense 2,000

Totals 140,000 140,000

Solution:

"Adjusting Entries"

Good Example of an internal event, there is not another party involved, and are not initiated by a Source Document.-

You might think of adjusting entries as a method of bringing the company's financial information up to date before preparing the financial statements.

-

Intermediate Accounting I Page 6

preparing the financial statements.

Prepayments○

Accruals○

Estimates○

Needed for 3 Situations-

Prepayments-

Company buys supplies in one period but uses them in a later period▪

Company may receive cash from customer in one period but provides the customer with good or service in the future. (Magazine Subscriptions for example)

▪

Cash flow precedes either expense or revenue recognition○

Prepaid Expenses○

Whenever cash is paid and it is not to satisfy a liability or pay a dividend or return capital to owners it must be determined whether or not the payment creates future benefits only the current period.

▪

The first asset that requires adjustment is supplies, $2,000 of which were purchased during July. This transaction created an asset as the supplies will be used in future periods. The company could either track the supplies used or simply count the supplies at the end of the period and determine the dollar amount of supplies remaining. Assume that Dress Right determines that at the end of July, $1,200 of supplies remain. The following adjusting journal entry is required.

• LO2–5

To record the cost of supplies used during the month of July.

Page 68After this entry is recorded and posted to the ledger accounts, the supplies (asset) account is reduced to a $1,200 debit balance, and the supplies expense account will have an $800 debit balance.

The next prepaid expense requiring adjustment is rent. Recall that at the beginning of July, the company paid $24,000 to its landlord representing one year's rent in advance. As it is reasonable to assume that the rent services provided each period are equal, the monthly rent is $2,000. At the end of July 2016, one month's prepaid rent has expired and must be recognized as expense.

To record the cost of expired rent for the month of July.

Deferred Revenues○

To illustrate a deferred revenue transaction, assume that during the month of June a magazine publisher received $24 in cash for a 24-month subscription to a monthly magazine. The subscription begins in July. On receipt of the cash, the publisher records a liability, deferred subscription revenue, of $24. Subsequently, revenue of $1 is recognized as each monthly magazine is published and mailed to the customer. An adjusting entry is required each month to increase shareholders' equity (revenue) to recognize the $1 in revenue and to decrease the liability. Assuming that the cash receipt entry included a credit to a liability, the adjusting entry for deferred revenues, therefore, is a debit to a liability, in this case deferred subscription revenue, and a credit to revenue.

▪

Accruals○

Company often uses the services of another entity in one period and pays them for subsequent period.□Accruals involve transactions where the cash outflow or inflow takes place in a period subsequent to expense or revenue recognition.

□

Cash flow comes after either expense or revenue recognition.▪

To record accrued salaries at the end of July.□

Accrued Liabilities▪

Accrued receivables involve situations when the revenue is recognized in a period prior to the cash receipt.

□

For example, assume that Dress Right loaned another corporation $30,000 at the beginning of August, evidenced by a note receivable. Terms of the note call for the payment of principal, $30,000, and

□

Accrued Receivables:▪

Interest rates always are stated as the annual rate. Therefore, the above calculation uses this annual rate multiplied by the principal amount multiplied by the amount of time outstanding, in this case one month or one-twelfth of a year

Intermediate Accounting I Page 7

Accrued receivables involve situations when the revenue is recognized in a period prior to the cash receipt.

□

For example, assume that Dress Right loaned another corporation $30,000 at the beginning of August, evidenced by a note receivable. Terms of the note call for the payment of principal, $30,000, and interest at 8% in three months. An external transaction records the cash disbursement—a debit to note receivable and a credit to cash of $30,000.

□

What adjusting entry would be required at the end of August? Dress Right needs to record the interest revenue earned but not yet received along with the corresponding receivable . Interest receivable increases and interest revenue (shareholders' equity) also increases. The adjusting entry for accrued receivables always includes a debit to an asset, a receivable, and a credit to revenue. In this case, at the end of August Dress Right recognizes $200 in interest revenue ($30,000 × 8% × 1/12) and makes the following adjusting entry. If this entry is not recorded, net income, assets, and shareholders' equity (retained earnings) will be understated.

□

Accrued Receivables:▪

Estimates○

Examples could be calculation of depreciation expense requires an estimate of expected useful life of the asset.

□Accountants often must make estimates of future events to comply with the accrual accounting model.▪

Accounting for bad debts requires a company to estimate the amount of Accounts Receivables that will ultimately be uncollectible and to reduce accounts receivables by that estimated amount.

▪

" Preparing the Financial Statements"

Summarize the profit-generating activities of a company that occurred during a particular period of time.○

Items are grouped in according to common characteristics (like Operating expenses)○

Reported in two ways; a single statement or in two separate but consecutive statements.▪

The Statement of Comprehensive Income - Reports any changes in shareholders' equity during the period that were not a result of transactions with owners. (referred to as OCI)

○

The Income Statement-

Present the financial position of the company on a particular date.○

Unlike Income Statement which is a change statements reporting events that occurred during a period of time○

There is a split up of Assets/Liabilities between Current and Long term. 1 year and less or 1 year and longer.▪

Items are grouped in common characteristics just like the Income Statement.○

The Balance Sheet-

Lists the paid-in capital portion of equity (common stock) and retained earnings. Notice that the income statement ties into the balance sheet through retained earnings.

○

Shareholders' Equity Statement -

Operating Activities - inflows and Outflows of cash related to transactions entering into the determination of net income.

▪

Investing Activities - nonoperating investment assets.▪

Financing Activities - involve cash inflows and outflows from transactions with creditors and owners.▪

Similar to income statement, it’s a change statement, report the events that caused cash to change during the period. Broken up into three parts;

○

The Statement of Cash Flows-

Also a change statement, it discloses the sources of the changes in various permanent shareholders' equity accounts that occurred during the period from investment by owners, distributions to owners, net income, and other comprehensive income.

○

The Statement of Shareholders' Equity -

Intermediate Accounting I Page 8

Related Documents