CHAPTER ONE GENERAL INTRODUCTION 1.0 BACKGROUND OF THE STUDY Lending constitutes one of the core activities in the operations of any bank. To this end, Ghana Association of Bankers in collaboration with PriceWaterHouseCoopers (2010) observed that net loans and advances remained the most significant component of operating assets of the banks in Ghana. It however noted that the growth rate in loans and advances of 7.5% in 2009 was lower than the 45% in 2008. The Financial Stability Report (FSR, April 2010) of the Bank of Ghana (BoG), lends credence to the above observation by stating that net loans and advances for February 2010 amounted to GH¢ 6.2 billion, representing a growth rate of 6.3% compared with a growth of 45.3% recorded a year earlier. Many people in Ghana save part of their income in a particular bank primarily with the hope of accessing some form of credit from the bank in the future. As is required by standards, banks solicit a certain level of information from their customers in order to decide on whether or not to grant them credit of any kind. However, since the information between banks (as lenders) and borrowers is asymmetric, lending is a risky activity. In this regard, banks have developed robust and time tested credit management systems that seek to reduce or eliminate the incidence of non – performing loans. These involve credit application processes that scrutinize the background of loan applicants to determine their credit worthiness. In spite of all these efforts, many banks still have very large amounts of non – performing loans in their books. The 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER ONE

GENERAL INTRODUCTION

1.0 BACKGROUND OF THE STUDY

Lending constitutes one of the core activities in the operations of any bank.

To this end, Ghana Association of Bankers in collaboration with

PriceWaterHouseCoopers (2010) observed that net loans and advances remained the

most significant component of operating assets of the banks in Ghana. It

however noted that the growth rate in loans and advances of 7.5% in 2009 was

lower than the 45% in 2008. The Financial Stability Report (FSR, April 2010) of

the Bank of Ghana (BoG), lends credence to the above observation by stating

that net loans and advances for February 2010 amounted to GH¢ 6.2 billion,

representing a growth rate of 6.3% compared with a growth of 45.3% recorded a

year earlier. Many people in Ghana save part of their income in a particular

bank primarily with the hope of accessing some form of credit from the bank in

the future. As is required by standards, banks solicit a certain level of

information from their customers in order to decide on whether or not to grant

them credit of any kind.

However, since the information between banks (as lenders) and borrowers is

asymmetric, lending is a risky activity. In this regard, banks have developed

robust and time tested credit management systems that seek to reduce or

eliminate the incidence of non – performing loans. These involve credit

application processes that scrutinize the background of loan applicants to

determine their credit worthiness. In spite of all these efforts, many banks

still have very large amounts of non – performing loans in their books. The

1

Bank of Ghana, in its Financial Stability Report of April, 2010 noted that

although the banking sector showed continued strong asset growth on account of

significant increases in deposits and net worth, the continued increase in non

– performing loans is impacting on banks’ ability to deliver credit.

The IMF country report (January, 2011) noted that the banking industry across

the world has been the worst hit by the global financial crisis and the

hitherto profitable institutions suddenly reported massive losses with some

even folding up. The report also noted that paramount among the reasons for

this trend is the limited role of risk management in the granting of loans by

banks to their customers leading to unprecedented levels of loan defaults.

Related to this, the McKinsey Quarterly: an Online Business Journal (2002)

noted that the issue of Non – Performing Loans, also known as Non –

Performing Assets (NPA) has been a major concern for banks years before the

Global financial crisis. It said that, European banks were owed $900 billion of

non – performing loans as at the end of the third quarter of 2002 and that

dealing with bad loans has become so worrying for banks that some of them are

now specializing in debt recovery. So profound is the problem that, just as the

crisis seems to be over, an article written by Jack Ewing and published on

http://www.dealbook.nytimes.com/austrian-banks-reflect-eastern-europe’s-pain/

June 6, 2010, states that about $2.6 trillion represents the amount that banks

and other financial institutions have lent in Europe as of May, 2010. Expert

opinion from both analysts and investors show that more than half of this

amount may never be paid.

2

In response to several criticisms relating to the lack of due diligence on the

part of banks especially in the area of credit provision, many banks have put

in place measures to streamline their credit application and recovery

processes. These streamlined processes have impacted on the way banks have

approached the provision of credit to their customers. Popov and Udell (2010)

observed that as a result of the crisis, loan applications especially in Europe

have been discouraged because of very high interest rates and unfavourable

collateral requirements. In their view, the banks have adopted these measures

in order to minimize losses arising from default.

The issue of problem loans is not only peculiar to Europe. The West Africa sub

region faces a similar situation. There are three identifiable reasons that

make the situation very serious. These are:

The growing number of banks and other lending institutions

The development of financial markets and stock exchanges and

The weaknesses in the Banking Supervision roles of Central Banks in the

region

A lot of banks and other financial institutions have sprung up in recent years.

The IMF country report number 11/8 (January, 2011) notes that the number of

banks in the West African Economic and Monetary Union rose from 64 in 2000 to

66 in 2002 and to 86 as of 2010. There is evidence that the growing number of

banks will result in increased competition that leads to a rise in credit

extension. In such heightened competition, more money will be lent with a

moderate adherence to banks’ credit policies. This occurrence will include the

creation of problem loans.

3

The growth of lending activities among non – bank financial institutions, whose

number has also seen significant increases over the years has heightened the

competition in the lending sector and then made the credit conditions more

flexible. Since the number of borrowers had increased due to decrease in credit

requirements, the likelihood for banks to lend to bad borrowers has also

increased. In that situation, prudent credit risk management systems and

ability to manage problem loans becomes critical success factors.

To add to the above, the deepening of the West African Financial Markets

through the creation of stock exchanges in the region has given investors an

alternative means of investment. Banks’ shareholders will now require higher

returns on their equity or shift their investments to the stock exchanges. This

will constitute a fresh pressure on banks to, among other things, grow their

loan books for higher profitability, and hopefully increased shareholders’

value.

Finally, the weaknesses and inefficiencies in the operations of the Central

Banks reflect in the relatively poor quality of the performance of their

banking supervision function. As a result of this the West African Economic and

Monetary Union (2010) observed that 64 banks in the union did not comply with

the risk management coverage ratio and 23 banks exceeded the limits of loans to

managers and personnel of the bank in 2009.

The issue of problem loans is not new to Ghanaian banks. Data from the Bank of

Ghana shows that the ratio of non – performing loans to total loans has, on the

average, been above 10% for the past decade. According to the Financial

Stability Report (FSR, May 2005) of the BoG, the percentage stood at 12.8% and

4

11.9% in 1999 and 2000 respectively. Just after that marginal decline, the non

– performing loan ratio increased to 19.6% in 2001 and further to 22.7% by

December 2002. It however dropped to 17.9% in December 2003. In a November 20,

2009 press release by the Monetary Policy Committee (MPC) of the Bank of Ghana,

the percentage of non – performing loans to total loans stood at 13.2% as at

September 2009, rising from 7.6% for the same period in 2008.

It is obvious that the up and down movements depicted by these figures is an

indication that the menace of problem loans still represent a major problem

Ghanaian banks are still struggling to contend with. The effect this will have

on the credit application and recovery processes among banks cannot be

overlooked.

Ecobank Ghana Limited (EGH) is one of the thirty-one (31) subsidiaries of the

Ecobank Group. Ecobank Ghana Limited was chosen for this study for several

reasons. First is its reputation of being among the best four banks in Ghana

(Ghana Banking Survey, 2010). The bank was also ranked 15th on the prestigious

Ghana Club 100 listing in 2008 with a 45% Return on Equity (ROE). It is also

listed on the Ghana Stock Exchange and therefore has its financial and other

regulatory reports published. It has also won several banking awards within the

industry including the coveted “Bank of the Year” award for the sixth time in

2009. According to the 2010 Banking Survey Report released by

PricewaterhouseCoopers Ghana in collaboration with the Ghana Association of

Bankers, EGH is ranked the fourth largest bank in terms of total assets

contributing 10.1% to total assets of the banking industry. The bank was the

third largest contributor to both industry deposits and gross loans and

advances with 10.5% and 7.7% respectively, according to the report.

5

1.1 STATEMENT OF THE PROBLEM

The major operating activity of banks is the provision of credit to borrowers.

This activity exposes them to credit risk. Credit risk arises due to the

uncertainty in a borrower’s ability to repay. The incidence of problem loans is

highly associated with credit risk. In the banking industry, a problem loan is

one of two things; it can be a commercial loan that is at least 90 days past

due or a consumer loan that is at least 180 days past due. This type of loan is

also referred to as non-performing loan/asset.

The International Monetary Fund (IMF 2011) reveals that the average level of

non-performing loans (NPLs) in Ghana is around 25% of total loans. Similarly,

the Bank of Ghana in its Financial Stability Report of May 2005 estimated the

NPL ratio at 15.7%. Ecobank Transnational Incorporated (September, 2008)

reveals that total non-performing loans of the Group stood at $186.09 million;

which represents 16.18% of total loans.

Clearly, the issue of problems as a component of credit is a major challenge

facing many banks and as long as the core of the banking business remains the

provision of credit, one has to admit that it is a problem that will remain a

major challenge which will require a lot of work to surmount.

1.2 OBJECTIVES OF THE STUDY

The purpose of this study is to assess the credit risk profile and the loan

application and recovery processes of Ecobank Ghana Limited.

Critical related objectives are as follows:

6

To assess the credit risk profile and management processes of the bank.

To assess existing credit application and recovery processes & problem

loans management systems of the Bank.

1.3 RESEARCH QUESTIONS

The above stated objectives can be achieved by answering the followingquestions:

What is the credit application and recovery processes of the Bank?

What are the credit risk profile and management processes of the Bank?

What measures are taken to prevent the creation of problem loans?

1.4 SIGNIFICANCE OF THE STUDY

An assessment of EGH‘s credit risk management framework will unearth the bank‘s

ability to handle the inherent risks in its operations. Also deviations from

international best practices would also be identified and alternatives

recommended. The bank‘s ability to deal with significant shocks and avoid

losses during crisis periods would also be tested.

Since there is not much structural and operational difference amongst the banks

in Ghana, it is hoped that this study will provide an indication of how the

credit risk management landscape looks like in Ghana‘s banking sector. In

addition, it will provide a guide for further studies on risk management in the

industry.

7

1.5 LIMITATION OF THE STUDY

In conducting a credit risk assessment of Ecobank Ghana Limited, information

was mainly gathered from financial statements and other disclosures contained

in the bank‘s annual reports. In this regard, annual reports of a three year

period (2010, 2009, and 2008) will be considered.

Additionally, the problem loans management system at Ecobank Ghana Limited is

analyzed and compared with standard problem loans management practices

recommended by the World Bank, International Monetary Fund and The West African

Monetary Union. This is to establish if the bank’s practices in this regard

conforms to the set standards.

Finally, common issues in credit risk management like adverse selections, moral

hazards and credit concentration are discussed. Ecobank’s financial statements’

analysis highlights the level of the bank’s loan concentration by the various

economic sectors such as energy, construction and mining.

1.6 ORGANISATION OF THE STUDY

The study is structured as follows:

Chapter one (1) provides a general introduction of the study

Chapter two (2) gives an in depth overview of Ecobank Ghana Limited (EGH). It

summarizes key information about the banks’ history and development, management

structure, product and service offerings among others.

8

The chapter also summarizes the literature on credit in general, the credit

application and recovery processes of the bank as well as issues on problem

loans.

Ecobank credit risk management processes is also discussed.

Chapter Three (3) presents the data collection and tools of analysis used and

interpretation of findings.

The data collected is analyzed and interpreted in Chapter Four (4).

Chapter Five (5) presents recommendations to improve the credit application and

recovery processes, the credit risk management and how to lower loan losses.

The conclusion ends the study with key deductions.

9

CHAPTER TWO

LITERATURE REVIEW

2.1 PROFILE OF ECOBANK GHANA LIMITED

2.1.1 History and Development

Ecobank Ghana Limited (“Ecobank” or “the bank”) commenced business On February,

1990, as a 92.2% owned subsidiary of Ecobank Transnational Incorporated (ETI).

Ecobank Transnational Incorporated is a pan-African banking group with a

presence in more African countries than any other bank. It is the leading

independent regional banking Group in West and Central Africa, serving

wholesale and retail customers. It is a Public Limited Liability Company

established as a bank holding company in 1985 under a private sector initiative

spearheaded by the Federation of West African Chambers of Commerce and Industry

with the support of ECOWAS. In the early 1980’s; prior to its formation, the

banking industry in West Africa was dominated by foreign and state-owned banks.

ETI was founded with the objective of filling this vacuum. The Group mission is

“to be perceived by our customers as providing convenient, accessible and

reliable banking products and services” with a vision “to become a world class

African banking group.”

According to the Global Credit Rating Company (2009), Ecobank became the first

bank to obtain a universal banking license in Ghana; clearing the way for it to10

move from being a wholesale (merchant) bank to one with retail focused

operations in 2003. The 2009 annual report of the bank states that, true to its

reputation as a pacesetter; Ecobank became the first bank to be granted a

universal banking license by the Bank of Ghana. The report also confirms that,

the bank got listed on the Ghana Stock Exchange (GSE) in July 2006; a feat that

underpins its consistent growth to become one of the leading banks in Ghana.

The Ghana Banking Survey report 2010 establishes that, as at the end of 2009,

Ecobank was Ghana’s fourth largest bank in terms of industry assets and fourth

in terms of deposits, making it the industry’s most systematically important

and fastest growing. Ecobank Ghana Limited currently operates a network of

approximately 52 branches across the country.

Until recently, large corporate bodies formed a major component of Ecobank’s

customers. However, in view of the limited scope of growth in the Ghanaian

corporate market, Ecobank has expanded its product offerings to include retail

banking and micro financing. The bank aims to penetrate these markets by

attracting the contractors, service providers and distributors of its corporate

clients, small and medium enterprises (SMEs) as well as employees of the

corporate companies.

In the area of micro-financing, it has entered into a joint venture with ACCION

International, a micro-financing specialist firm, to achieve that objective. In

addition to ACCION International, Ecobank has three other wholly owned

corporate affiliates: Ecobank Investment Managers Limited, Ecobank Leasing

Company Limited and Ecobank Venture Capital Limited which help it to offer

retail banking services, wholesale banking services, trade finance, advisory

services and wealth management services. The bank also offers non-bank

financial services to the general public. The most recent service in this

11

regard is the establishment of the U.S. visa application services to collect

visa fees on behalf the United States of America Embassy.

The table below summarizes the services offered by each of Ecobank’s corporate

affiliates.

Table 2.0 - Service Offering of Ecobank’s Corporate Affiliates

Corporate Affiliate Forms of servicesECOBANK INVESTMENT MANAGERS LIMITED Management of InvestmentsECOBANK LEASING COMPANY LIMITED Providing of finance lease

facilitiesECOBANK VENTURE CAPITAL COMPANY LIMITED Provision of venture capitalEB ACCION SAVINGS & LOANS COMPANY LIMITED Provision of micro-finance

services

Source: Own Construction Based on Information from 2009 EGH Annual Report

2.1.2 Management Structure

Ecobank Ghana Limited has a management structure that is made up of the Board

of Directors at the apex, followed by an Executive committee (EXCOM) composed

of the Managing Director, Executive Director, the group Executive Head and

three Business Heads.

The Managing Director is the chairman of the EXCOM which is the responsible for

the day-to-day administration of the bank.

Next in line is the management committee which is made up of all Departmental

Heads and Branch Managers, followed by the officer and non-officer level staff.

2.1.3 Specialized Corporate Subsidiaries

12

Ecobank Ghana Limited has two specialized corporate subsidiaries: Ecobank

Development Corporation (EDC) and eProcess International (eProcess). EDC was

incorporated with a broad mandate to develop the banks investment banking and

advisory businesses throughout the countries where Ecobank Operates.

The mandate of eProcess is to manage the Groups information technology function

with a view to ultimately centralizing the bank’s middle and back office

operations to improve efficiency, service standards and reduce costs.

An efficient eProcess function has propelled the bank in generating earnings

growth in an increasingly competitive environment characterized by declining

margins through efficient usage of ICT and the introduction of various

electronic banking products such as VISA electron cards, electronic payment and

collection platform to its clients, as well as being part of E-card personal

debit card consortium. Ecobank has also secured a main agent status for Western

Union Money Transfer Services. As a result of a solid ICT platform, Ecobank, in

July, 2007 launched the first electronic Credit Card in Ghana.

2.1.4 Forms of Services and Products

Ecobank Ghana Limited, with its subsidiaries, provides corporate banking,

investment banking and retail banking services in Ghana to individuals, small

and medium scale companies, local and regional corporate, public sector

companies and multi-national companies. The bank’s deposits products include

current, savings and deposit accounts. Its loan portfolio comprises personal

loans, car and motor loans, mortgage loans and business loans.

It also offers cards, letter of credits and bills for collections, transfer

payments, foreign exchange and Western Union Money Transfer Services. In13

addition, the bank engages in finance leasing, venture capital and micro-

finance services as well as provision of Automated Teller Machines (ATM)

services, internet banking and telephone banking services.

2.2 CREDIT POLICY OF ECOBANK GHANA LIMITED

The word credit comes from the Latin word “Credo” meaning “I believe”. It is a

lender’s trust in a borrower’s ability or potential ability and intention to

repay. In other words, credit is the ability to command goods or services of

another in return for promise to pay for such goods or services at some

specified time in the future. For a Bank, it is the main source of profit.

However, the wrong use of credit would bring disaster not only for the bank but

also for the economy as a whole.

The objective of credit management is to maximize performing assets and

minimize the non-performing assets as well as ensuring the optimal point of

loan and advances and their efficient management. Credit management is a

dynamic field where a certain standard of long-range planning is needed to

allocate the fund in diverse fields and to minimize the risk and maximizing the

return on the invested fund. Continuous supervision, monitoring and follow-ups

are highly required for ensuring the timely repayment and minimizing the

default rate. Actually, the credit portfolio is not only constituted by the

bank’s asset structure but also a vital factor of the bank’s success.

The provision of credit is the major function of every commercial bank. A

greater portion of its funds is used for this purpose and this is also the

major source of the bank’s income. Saunders (1997) describes a commercial bank

14

as a bank that focuses on the provision of credit to various parties for

profit.

The overall success in credit management depends on the bank’s credit policy,

portfolio of credit, monitoring, supervision and follow-ups on the loans and

advances. Therefore, while analyzing the credit management of Ecobank, it is

required to analyze its credit policy, credit application procedure, the

recovery process and its credit risk management processes.

One of the most important ways, a bank can make sure its loans meet

organizational and regulatory standards and that they are profitable is to

establish a loan policy. Such a policy gives loan managers a specific guideline

in making individual loan decisions and in shaping the bank’s overall loan

portfolio. In Ecobank Ghana Limited, the credit policy as enshrined in the

Group Credit Policy and Procedure Manual (GCPPM, Version 11) is well designed

to shape the banks’ lending procedures towards ensuring the timely provision of

credit to its cherished customers but at the same time minimizing their credit

risk exposures.

To safeguard its interest over the entire period of the advance, Ecobank

generally lays emphasis on a comprehensive review of the capital adequacy of

the borrower, integrity of the borrower; which includes credit history, nature

of collateral security, compliance with all legal formalities, and completion

of all documentation and finally a constant watch on the loan account. Where

advances are granted against the guarantee of a third party, that guarantor

must be subjected to the same credit assessment as made for the principal

15

borrower. The basis of collateral security valuations is: expert third party

assessments, current market price and forced sale value.

In making lending decisions, the bank pays particular attention to the analysis

of credit proposals received from heavily leveraged Companies and those dealing

in non-essential consumer goods, taking special care about their debt servicing

abilities. Besides, the bank also applies the following sound credit

principles:

Credit advancement shall focus on the development and enhancement of

customer relationship.

Credit extension shall focus on the present and future business

potentiality for optimum deployment of Bank's fund to increase return on

assets.

Loans and advances shall normally be financed from customer’s deposit and

not out of temporary funds or borrowing from other banks.

The bank shall provide suitable credit services for the markets in which

it operates.

It should be provided to those customers who can make best use of them.

The conduct and administration of the loan portfolio should be within the

defined risk limitation for the achievement of profitable growth and

superior return on bank capital.

Interest rate of various lending categories will depend on the level of

risk and types of security offered.

16

All credit extension must comply with the requirements of Bank’s

Memorandum and Article of Association, Ghana Banking Act, Bank of Ghana

Regulations and other rules and regulations as amended from time to time.

2.3 RISK ASSET CLASSIFICATION OF ECOBANK GHANA LIMITED

Credit facilities that are extended to customers by the bank make up its risk

assets. Based on the Group Credit Policy and Procedure Manual, Ecobank risk

asset process is the flow of planned, identifiable and sequential events

involved in the booking of individual credit transactions and the management of

those assets to full recovery.

Credit facilities extended to customers may be short term (up to one year),

medium term (one to three years), or long term (over three years) in tenor.

Additionally, facilities may be of a direct or indirect nature.

2.3.1 Direct Facilities

Direct facilities are those where the Bank actually disburses funds to a

borrower, in the form of a loan or other advance, or creates an arrangement

whereby the customer may himself draw funds on credit at his volition up to an

agreed limit. Examples of direct facilities are Advances in Current Account

Demand Loans, Term Loans, Bill discounting, advances under Letters of Credit

and Temporary Overdrafts.

2.3.2 Indirect Facilities

Indirect (or contingent) obligations are created when the Bank enters into a

contractual obligation to pay a third party at a future date, or upon the

occurrence of a certain event, against the indemnity of a customer (who is the

17

direct obligor). Examples of indirect obligations are Opening and/or

confirmation of letters of credit, Issuance of guarantees (e.g. to customs,

immigration), Issuance of bid/performance/advance payment bonds, and Issuance

of standby letters of credits.

A collection of all credit facilities extended by the Bank to its customers

(both direct and indirect) make up its risk asset portfolio.

2.4 CREDIT APPLICATION PROCESS OF ECOBANK GHANA LIMITED

Prior to the extension of any credit facility, whether direct or contingent, it

must be recommended and approved by means of a Credit Application (CA). Such CA

will incorporate analysis and evaluation of all risk inherent in the

transaction. Ecobank’s credit policy and procedure manual proposes three types

of credit applications.

The first credit application is known as the initial review. This proposes a

new credit relationship for the bank. It is actually a comprehensive review of

a first time credit application by a customer.

To reach a decision to lend, the Bank undertakes several activities in line

with a credit application just to make predictions about the future and how it

will affect the borrower’s ability to repay the loan. Therefore when the Bank

decides to lend, it is because it has judged that it will get repaid at an

agreed future date.

The length of a Credit Application (CA) is dependent upon the complexity of the

credit and whether it is an initial, interim or annual CA. The initial credit

application is generally subjected to a series of analysis in order for the

18

bank to reach a decision. The initial credit application process of Ecobank

consists of the following:

2.4.1 Credit Application (CA) Face

According to the Group Credit Policy and Procedure Manual (Version 11), the CA

face is the way in which the bank presents facilities to be approved to a

borrower. An application for credit is mostly made at the account holding

branch of the customer. The branch Manager facilitates the process and seeks

approval from Board of Directors whenever necessary. For a business entity, the

bank requires that it submits a letter of application for the facility together

with a written resolution on its official letter head and signed by the Board

of Directors of the entity; if it is a Limited Liability Company (LLC) stating

clearly their intention to obtain credit from the bank.

The next stage is legal documentation in support of the Credit Application.

Documentation requirements for each credit facility are decided by the Credit

committee in consultation with the minimum documentation requirements laid

clown by Legal Counsel. Legal Counsel must be consulted in all situations that

depart from the routine guidelines. From the Group perspective the minimum

documentation requirements are:

Borrower must be a current account holder and must have met the necessary

current account documentation requirements.

Borrower must also meet the general borrowing requirements and

additionally, depending on the product under consideration, meet the

specific requirements for each product.

19

The documentation requirements form a part of the credit package and no

disbursement of funds may take place until the Account Manager and Credit

Department Head have confirmed to the Credit Committee that all

documentation is obtained and in order.

Prior to being lodged for safekeeping, all documents must be

independently signature verified. They should also be pencil initialled

by the Account Manager and Credit Department Head and Legal Officer.

In situations where disbursements are made prior to completion of

documentation, a procedure in place in the Credit Administration

Department must be activated to enable the bank to continue following up

for the receipt of outstanding documentation by the agreed Target Date.

This requirement is in addition to the approvals required for deferral of

documentation.

Consequently, the legal documents that must be submitted in support of a CA are

Certificate of Incorporation, Certificate to Commence Business, Memorandum of

Association, Forms 3 and 4 of company’s registration and documentation covering

any property that is used as collateral security for the facility. Copies of

the company’s audited financial statements including Income Statement, Balance

Sheet and statement of cash flows must also be submitted to enable the bank to

conduct detailed financial analysis of the borrower. Finally, a guarantor’s

form (usually prepared by the bank) must be completed and duly signed by all

persons willing to act as guarantors of the borrower. Guarantees could be

personal, joint and several, cross company, parent company or third party. It

is important that the net worth of individuals and corporate entities

guaranteeing the obligation are estimated and indicated.

20

After an application for credit is received along with the necessary

documentation from a prospective borrower, the bank takes steps to put the

application together in line with its guidelines and requirements for the

necessary analysis to be carried out. This is what we referred to as the CA

Face. It indicates the following:

Whether the borrower is a Target Market name or not and its tier.

Exchange rates used for conversion of fine amounts to dollars.

Outstanding obligations (if any) against existing or proposed credit

lines.

Pricing for each facility.

A list of documentation requirements. The security documents should be

listed separately from the support documents as the two have different

legal implications on the credit. After listing, the credit officer

should include a statement that he has reviewed the documents and that

they are in order or otherwise. Where certain documents are being

deferred, appropriate credit committee approval should be obtained before

any drawdown is made.

2.4.2 Facility Listing

It is the continuation process of describing the nature of the facilities

applied for if it does not fit on the CA face. A detailed background is given

especially for initial reviews. There is also a description of the nature of

the relationship that exists between the bank and the client.

2.4.3 Credit Application (CA) Remarks

21

After the facility has been listed and a background provided, CA remarks are

made and they cover the following subject matter:

Purpose or line structure: the credit application (CA) face provides a

comprehensive analysis of what the purpose of the credit application is. In

this regard this section only provides a short statement about the purpose of

the CA (i.e. whether initial, interim or annual).

Management: this provides information on the assessment of the quality of

management’s capabilities if the loan will be used to run a company.

Significant changes during the past year and anticipated major changes in

Management are noted and discussed.

Financial Analysis: Based on the credit procedure manual, where a separate

financial memo is not prepared, this section gives the credit committee an in-

depth overall picture of the company's financial performance, its balance sheet

strengths and weaknesses and its cash generating capabilities. An element of

practical common sense is applied, which distinguishes regular features in

financial statements from either one time or irregular developments or/trends.

For instance, the borrower may have embarked on capital expenditure (CAPEX)

programme during the year under review. How this was financed, whether the

programme costs are on target, and the effects of depreciation, tax

liabilities, etc. are explained. Similarly, if the receivables or inventory

evidence a slip from past levels or if short term debt or payables show a

significant variation, they are explained. If margins have improved or worsened

(price controls, competition, one time rationalizing, restructuring of

expenses) they are also to be addressed. Where security for the loan is a

22

charge over the company's assets (floating, fixed or both), the analysis is

complemented with a liquidation analysis providing the realizable value of such

assets.

Future prospects or sensitivity: For larger CA’s, a paragraph covering future

prospects is included immediately after the financial analysis Section. This

section discusses the borrower's business and financial outlook over the next

12-18 months (or the life of the term loan if relevant). A critical assessment

of the company's business is then made by employing different basic assumptions

(adverse political changes, sudden curtailment of import licences for raw

material purchase, a shift in consumer demands, price decontrol, etc) and the

resultant impact on aspects such as cash, net income and the balance sheet. A

conclusion of this analysis indicates whether such an eventuality would result

in the bank working away from the relationship, reducing its exposure or

otherwise.

2.4.4 Circulation of the credit package for credit committee review

After the credit application remarks are completed, each credit committee

member reviews the CA documents and sets out any observations in a memo to the

accounts officer. The accounts officer then finalizes the package for approval

taking into account all points made and agreed upon by the credit committee

members.

The second form of credit application in Ecobank is known as the annual review.

Once a credit application is approved and funds are disbursed to the borrower

after an initial review, a credit relationship is established. This

relationship must be reviewed at regular intervals usually within twelve months

23

after the initial review or the last annual review. The interval could be less

than twelve months but not more.

The best practice is that, the review be timed to coincide with receipt of

borrower’s annual audited financial statements. This enables credit officers of

the Bank to, among other things; quickly respond to any signs of financial

distress which could hinder the borrowers’ ability to repay the facility.

Where there is the need for a facility to be increased or decreased or even

radically changed in a way, for instance, in the substitution of collateral

security, a third form of credit application is proposed and is known as

interim review. This is usually submitted between annual reviews.

Credit Applications (for all facilities both direct and contingent) must

incorporate total exposure to the customer/borrower and it is this aggregate

level of credit risk which determines the level of approval required.

2.5 CREDIT APPROVAL SYSTEM OF ECOBANK GHANA LIMITED

Credit approval authority is delegated to Management by the Board of Directors

of Ecobank Transnational Incorporated (ETI). Any extension of credit exceeding

the authority delegated is subject to approval by the Board of Directors of ETI

itself, following recommendation to the Board by Management.

For the approval of credit at the various affiliates of the Bank, approval

limits are delegated to the Managing Directors of affiliates (Local Managing

Director) by ETI. Any extension of credit at an affiliate exceeding such

delegated authority is also subject to approval by ETI, following the

24

recommendation by the affiliate. Additionally, extension of credit by the

affiliate may require further approval of the Board of Directors of the

affiliate, following recommendation by management of the affiliate and prior

approval by ETI as necessary.

In addition to the above, there are other general rules and regulations that

govern the extension of credit at Ecobank which are worth examining.

First among these regulations is approval and documentation. As required by the

principles in the credit policy and procedure manual of the bank, any written

commitment to extend credit must be executed by a Managing Director, unless

specific delegated authority has been granted to other credit officers for this

purpose.

Secondly, approval for all types of credit extension shall be evidenced on the

Credit Application or other authorised approval document by the signatures or

initials of each of the credit officers approving the credit. It sometimes

becomes necessary for the deferral of the receipt of documentation required

under credit arrangements, or otherwise essential to the granting of credit. In

such a case, the approval of the local Managing Director is required.

The general rules and regulations governing credit extension at Ecobank also

has at its core what is generally known as the “Three Initial System”. The

principle of this system is that credit is not extended on the judgement of one

officer alone.

Consequently, it requires that authority for credit extensions must have the

joint approval of at least three credit officers (collectively referred to as

25

"Credit Committee"), at least one of whom must have a personal designated

credit limit covering the amount of credit extension under consideration. The

rules also make it clear that, a specific title by itself will not be

sufficient to allow an officer to approve the extension of credit. As a result,

only those officers who have duties and responsibilities that involve the

approval of loans and other extensions of credit are "credit officers".

A credit officer’s ability to approve credit extension depends, among other

things, on his credit approval level or credit limit. Specific personal

designated credit limits are delegated to credit officers by the Group Managing

Director on the recommendation of the Group Credit Officer, based on rank,

experience and proven ability. Such limits are advised to the ETI Board of

Directors. The minimum requirement for credit approvals are as follows:

Table 2.1 – Ecobank Credit Approval Levels

a) If aggregate amount is not inexcess of a ManagingDirector’s Limit:

Two credit officers and the ManagingDirector.

b) If aggregate amount ExceedsManaging Director’s limit butis not in excess of$1,000,000 :

As for (a) plus an officer with a personallimit of $1,000,000 or higher.

c) If aggregate amount exceeds$1,000,000 but is not inexcess of $2,500,000 :

As for (a) plus a Senior Credit Officer.

d) If aggregate amount

exceeds $2,500,000 but is notin excess of $5,000,000 :

As for (a) plus a Credit Officer with apersonal limit of $1,000,000 and oneSenior Credit Officer plus the ETI Boardof Directors, or such subcommittee as theBoard may appoint for credit approvalpurposes.

e) If aggregate amount exceeds$5,000,000 :

As for (a) plus two Senior Credit Officersplus the ETI Board of Directors, or suchsubcommittee as the Board may appoint forcredit approval purposes.

26

Source: Group Credit Policy and Procedure Manual (GCPPM, Version 11)

2.6 CREDIT RECOVERY PROCESSES

The Oesterreichische National Bank (Austria) in the 2004 edition of its

publication dubbed ‘the guidelines on credit risk management’ observed that

Banks were never as serious in their efforts to ensure timely recovery of loans

and consequent reduction of Non Performing Assets (NPAs) as in recent times.

This is attributable to the high incidence of losses that many banks have

suffered due to loan defaults. The publication highlighted the importance of

recovery management, be it fresh loans or old loans, as central to NPA

management. This management process needs to start at the loan initiating stage

itself.

Effective management of recovery and NPAs comprise two pronged strategies. The

first strategy relates to arresting of the defaults and the consequent creation

of problem loans. The second strategy relates to the handling of loan

delinquencies.

Further observations made by the bank in the publication includes the fact that

the creation of financial sector reforms by successive governments has helped

banks to develop effective loan recovery policies based on the premise that

they either perform or perish. In the view of the bank, the set of prudential

norms contained in the financial sector reforms has forced the banks to look

into their asset quality with the ultimate focus on reducing the incidence of

loan defaults. The main elements of the bank credit recovery would generally

include:

27

Specific tasks to be accomplished e.g. the amount to be recovered from the

specified loan accounts in default and the broad time frame.

Credit Recovery Policy and Procedure of the bank.

Code of conduct in recovery process may include verbal and written

communication rules to be followed by bank’s credit officer responsible for

the collection of the debt.

The credit recovery policy and code of conduct in the recovery processes will

be regulations compliant, i.e. in accordance with the directives and guidelines

of the central bank (Bank of Ghana) issued from time to time.

For the majority of facilities that banks give, the primary source of repayment

will be sustainable cash flow generated by on-going trading activities

(Fuchita, 2004). Security provides a safety net for the Bank if a customer

cannot repay an advance as originally planned. Except where the disposal of a

specific asset is the source of repayment (e.g. a bridging loan) reliance on

security should always be a last resort.

According to Fuchita (2004), there are no rules governing what formula a bank

should use in any individual case or for any particular type of industry

regarding the recovery of the loan facility. However, the point to bear in mind

is that, there should be a formula to be used in order to recover a loan

facility. As often as it may be, banks in general amortize loan facilities to

customers and then recover the loan through the monthly payment of interest and

principal made by the customer.

The credit recovery processes as recommended in the Oesterreichische National

Bank’s publication (2004) on credit risk management guidelines are presented

below.

28

The first step in the credit recovery procedure is to make customer calls to

clients whose loan repayments are past due. This is done for two main reasons.

First, is to remind the customer of his obligation that is overdue and second,

to find out the reasons for the delay if any. In making customer calls, the

following guidelines must be followed:

The bank must ensure that calls are made from the same number to the

customer

The credit officer making the call must disclose his identity and

authority to the customer at first instance.

The officer must contact the customer between the hours of 07:00 hours

and 19:00 hours unless there is a special circumstance that requires the

bank to contact the customer at a different time. Under no circumstance

can the customer be called beyond 21:00 hours.

All calls when the customer becomes abusive or threatening should be

appropriately documented.

Customer’s questions should be answered in full. They should be provided

with information requested and given assistance in making the repayment.

The frequency of calls to the customer should be well regulated. As

indicated above, the purpose of a collection call is to bring to the

customer’s notice the obligation and to seek a commitment to pay on a

specified date. Once a promise is elicited, a call may be made to serve

as a reminder and for confirmation of payment.

29

If the customer is not available after a considerable number of calls

made by the officer, a message may be left to an adult family member. The

message should not indicate that the customer has an overdue amount.

The second stage of the credit recovery process is a visit to the customer. If

all attempts to get the customer to repay the loan through telephone contact

fail, then a visit to the customer becomes inevitable. The process is initiated

by the account officer and implemented by the credit recovery officers of the

bank. The following conditions must be satisfied before a customer is visited

for debt collection.

The customer has not paid the due amount within the days of grace and the

dues are still outstanding against him or her.

The customer has been notified of the amount due and also the name of the

credit officer.

The credit officer has taken an appointment from the customer for visit.

There are instances where deterioration in the financial position of a customer

may lead to a total failure of the loan repayment. In such situations, banks

resort to the possession of asset pledged as security in the case of default.

In general, the banks institute legal actions to enable them exercise their

right under the security arrangements.

Once the legal proceedings are complete, the banks appoint liquidators to help

in the valuation and disposal of the asset(s). The assets must be disposed off

to the exact loan amount outstanding.

2.6.1 Credit Recovery Processes of Ecobank Ghana Limited

30

The GCPPM (Version 11) outlines a series of activities in respect of recovering

loans that have been granted to the bank’s customers. These processes form part

of the credit administration function of the bank. Some of the administrative

functions are handled by the Credit Department, but the ultimate responsibility

for an overall acceptable process for each borrower lies with the Account

Manager.

All credit agreements entered into by the bank make specific provisions for the

repayment of principal and the payment of all interest due by the customer.

These repayment plans are structured to fit within a specific time frame which

is acceptable to both the bank and customer. There are times when the payments

of principal and accrued interests go according to plan. At other times the

reverse is the case. When the latter is the situation, then a problem occurs.

This calls for a proactive response by the bank to anticipate the problems

before they occur.

The most critical principle in the bank’s credit recovery process is problem

recognition. It is the ability of the bank to anticipate, detect, recognise,

and report as early as possible potential problems within an individual

borrower’s business or industry. The objective is to address problems while

there is still time for alternative corrective actions and revision of strategy

against the relationship.

One of the effective ways of the bank achieving an overall acceptable rating in

problem recognition is by continuous contact and information gathering, both

from the customer as well as the market; the Account or Credit Officers record

all negative signals and discuss these with the Credit Committee and

Management. The information gathered is then used to classify the credits in

31

order for specific provisions to be made regarding their collectability (See

Table 2.2 Below)

Ecobank’s credit recovery methods vary depending on the severity of the

classification. These involve dialogue between the Account Officer, Bank

Management and Legal Counsel in a classified ‘IA’ situation. The primary

responsibility rests with the Account Manager but close involvement of both

Management and Legal Counsel is required.

In a classified ‘II’ situation, the action plan calls for a prepayment of some

of the obligations, request for the client to find alternative Bankers, calls

under guarantees etc. Every step is documented and if results are not being

achieved, more serious steps (Legal action) are considered.

In a classified ‘III’ situation, the action plan calls for legal action to

enable the Bank to exercise its rights under the security arrangements, sale of

collateral, and appointment of a receiver or liquidator.

The action plans called for in this situation are very time-consuming and

involve several senior Bank Officers, and even outside Accountants or

Receivers. Legal action against any borrower, provided that such action is

recommended by Legal Counsel, must be approved by the Managing Director, and

confirmed by the local Board of Directors.

2.6.2 Compromise Settlements and Abandonment of Recovery Efforts

With some problem credits where a protracted work out is anticipated, where the

principal amount is wholly or partially reserved or likely to be reserved in

the near future, and when the legal, opportunity and carrying costs are high,

32

the bank considers it worthwhile to negotiate a compromise settlement with a

borrower. Such compromise settlements may include the foregoing of part or all

of interest and even part of principal.

The Board of Ecobank Ghana Limited (EGH) and Ecobank Transnational Incorporated

– Credit Policy Committee (ETI-CPC) are consulted for any such transaction in

excess of US$ 50,000 before a commitment is made. Similarly, for amounts in

excess of US$ 250,000, the Board of ETI is consulted. In either case, once

approved, the Audit Division of ETI is promptly advised.

Decision to abandon recovery efforts is taken by the Credit Committee,

including the Managing Director of EGH for amounts up to US$ 5,000. For amounts

exceeding US$ 5,000 but not US$ 50,000, approval by the Board of Directors of

EGH is obtained. Amounts in excess of US$ 50,000 but not exceeding US$ 250,000

are referred to ETI-CPC for approval and amounts in excess of $250,000 to the

Board of ETI.

2.7 CREDIT RISK MANAGEMENT PROCESSES

The risks associated with the provision of banking services differ by the type

of services rendered. Different authors have grouped these risks in various

ways to develop the framework for their analyses but the common ones are credit

risk, market risks (which includes liquidity risk, interest rate risk and

foreign exchange risk), and operational risks which sometimes include legal

risk and more recently, strategic risk. The focus of this study, however, is on

credit risk and its management.

Greuning and Bratanovic (2003) define credit risk as the chance that a debtor

or issuer of a financial instrument - whether an individual, a company, or a

33

country - will not repay principal and other investment-related cash flows

according to the terms specified in a credit agreement. Inherent to banking,

credit risk means that payments may be delayed or not made at all, which can

cause cash flow problems and affect a bank‘s liquidity. The goal of credit risk

management is to maximize a bank‘s risk-adjusted rate of return by maintaining

credit risk exposure within acceptable parameters. More than 70 percent of a

bank‘s balance sheet generally relates to credit risk and hence considered as

the principal cause of potential losses and bank failures. Time and again, lack

of diversification of credit risk has been the primary culprit for bank

failures. The dilemma is that banks have a comparative advantage in making

loans to entities with whom they have an ongoing relationship, thereby creating

excessive concentrations in geographic and industrial sectors. Credit risk

includes both the risk that a obligor or counterparty fails to comply with

their obligation to service debt (default risk) and the risk of a decline in

the credit standing of the obligor or counterparty.

While default triggers a total or partial loss of any amount lent to the

obligor or counterparty, a deterioration of the credit standing leads to the

increase of the possibility of default. In the market universe, a deterioration

of credit standing of a borrower does materialize into a loss because it

triggers an upward move of the required market yield to compensate the higher

risk and triggers a value decline (Bessis, 2010). Normally the financial

condition of the borrower as well as the current value of any underlying

collateral are of considerable interest to banks when evaluating the credit

risks of obligors or counterparties (Santomero, 1997). According to Greuning

and Bratanovic (2003), formal policies that are laid down by the Board of

34

Directors of a bank and implemented by management play a vital part in credit

risk management. As a matter of fact, a bank uses a credit or lending policy to

outline the scope and allocation of a bank‘s credit facilities and the manner

in which a credit portfolio is managed - that is, how investment and financing

assets are originated, appraised, supervised, and collected.

There are also minimum standards set by regulators for managing credit risk.

These cover the identification of existing and potential risks, the definition

of policies that express the bank‘s risk management philosophy, and the setting

of parameters within which credit risk will be controlled. There are typically

three kinds of policies related to credit risk management. The first set aims

to limit or reduce credit risk, which include policies on concentration and

large exposures, diversification, lending to connected parties, and

overexposure. The second set aims at classifying assets by mandating periodic

evaluation of the collectability of the portfolio of credit instruments. The

third set of policies aims to make provision for loss or make allowances at a

level adequate to absorb anticipated loss.

Problem loans are at the end of the credit channel. Before a loan becomes bad,

it needs to be granted. Moreover, the poor quality of a loan is sometimes due

to factors not attributable to the lending bank such as adverse selection and

moral hazard (Stiglitz and Weiss, 1981) or any other external shock that may

alter the borrower's ability to repay the loan (Minsky, 1982 & 1985).

Nevertheless, there are cases where the way banks grant and monitor credits can

be responsible for the bad loan portfolio. In other terms, weak credit risk

management systems can also be sources of problem loans (Nishimura et al,

2001).

35

2.7.1 Credit Risk Management Process at Ecobank Ghana Limited

Ecobank Ghana Limited credit management processes can be summarized into three

main stages: Credit Initiation, Documentation and Disbursement and Credit

Administration.

1. Credit Initiation: The credit initiation is a process that starts from a

market analysis and ends at the credit application approval. The steps of the

credit initiation are listed below:

a. Surveys and industry studies: Relationship Officers scan the market

and economic sectors to identify key players and potential business for the

Bank. In the same vein, industries with high potential of growth that can be

good business for the Bank are also listed.

b. Risk Asset Acceptance Criteria (RAAC): for each industry, criteria

are designed to guide the relation with both industry and clients in order to

limit the level of exposure at credit risk. RAACs applied to industries include

both quantitative and qualitative information such as net sales, net profit,

years of experience in the business and the quality of corporate governance.

c. Prospect lists: some prospects (companies and individual customers)

identified as the main role players are short listed in accordance with the

industry studies and the minimum risk criteria. This prospect list is ranked in

order of preference.

d. Customer solicitation: at that stage, although the primary source

of target is the prospect list, the initiation of a credit comes either at the

36

bank request in the frequent contact with existing customers or at the clients

request if they have a need for financing.

e. Negotiation: the relationship officer identifies the financing

needs of the borrower and gathers background information such as the latest

financial statements, project details, projections over the loan life. This

information will allow the officer to check whether the risk is bearable by the

Bank and its compliance with the bank's targets.

f. Presentation: the conformity of information given with the market

and industry analysis is the reliability of the information once again verified

by consulting other sources. A draft of the credit application (CA) is prepared

in conformity with the GCPPM and in consideration of the market and industry

analysis by the account officer based on information collected.

g. Credit committee approval: a copy of that CA is submitted to each

member of the credit committee. The members review and approve submission of

the final CA.

h. Control and reporting requirements: the final CA package is

submitted to the credit committee with highlights on the credit exposures of

the bank.

i. Advice to customers: once the credit is approved, the customer is

advised in writing with details concerning the terms and conditions and with

the statement that the credit can be subject to review, modification or

cancellation at the Bank’s option.

37

II. Documentation and Disbursement: The documentation and disbursement refers

to the compliance of documents provided with the law applicable and the

requirements of the Bank's legal department. Documentation provided must

satisfy the Bank's legal department and afford maximum protection to the Bank.

The documentation is periodically reviewed to keep them in tune with ever-

changing legal systems and practices. The Legal department is consulted before

making any compromises with the customer. Any amendments are done in

consultation with the legal department.

Once the credit application satisfies all these conditions, a thorough analysis

is done and if the application complies with the Bank's conditions, instruction

is given to the Credit administration for disbursement.

III. Credit Administration: The credit administration refers to the credit

support, control systems and other practices necessary for the effective

monitoring of credit risks taken by the Bank. Some of the important points of

the credit administration are:

Control of Credit files.

Safekeeping of credit and documentation files.

Follow-ups for expirations of essential documents like CA's and

insurance.

Control of availments and excesses over approved lines.

Monitoring of collateral inspections, site visits and customer calls.

Monitoring of repayments under term credits.

38

Reporting: the portfolio is periodically reviewed to make sure that the

names tiered are still complying with the risk acceptance criteria.

2.7.2 Problem Loans Management at Ecobank Ghana Limited

When the time for repayment comes, two scenarios may occur:

1. The loan is repaid (principal and interest) under the pre-agreed terms and

conditions

2. The borrower fails to make the repayment of both or part of principal and

interest.

In such case the loan then becomes a problem loan and a new process is then

triggered. A loan can become a problem loan before its maturity due to the

disclosure of any information questioning the borrower's ability to repay (case

of cross default for example). In respect of the GCPPM, three main stages can

be defined in the bank's dealing with problem loans:

The Early Warning Systems

The Classification and Provisioning and

The Remedial Management

I. Early Warning Systems: They refer to the ability of the Bank to

anticipate, detect, recognize and report problems as early as possible so that

prompt corrective actions can be taken to avoid problem loans. In order to

achieve this objective, the Bank has built three main internal rating systems:

39

1. Obligor Risk Rating (ORR): the rating attributed to the obligor

applying for credit

2. Portfolio Risk Rating (PRR): the rating attributed to a related group

of companies, which has stakes in other companies. The PRR of a group is

derived from the ORR of the companies in its portfolio.

3. Facility Risk Rating (FRR): the structure, security and tenor of a

facility inform the assignment of an appropriate risk rating. This means that

the FRR is the rating given to the facility the obligor is applying for.

The GCPPM insists on the importance of continuous gathering of information on

the customer, market, industry and reporting to the Credit Committee and

Management. Among the warning signs that may draw the Bank's attention on the

borrower, we can mention:

Recurring casual overdrafts or line excesses that take a long time to

clear.

Frequent delays in repayment of principal or interest payments.

Inability to communicate with customer and failure to disclose

information.

Major management changes especially in financial area personnel and key

decision makers.

Negative market trends, Government directives, Legal suits and/or

bankruptcy threats by other creditors.

Deterioration of economic environment.

40

New competition in industry.

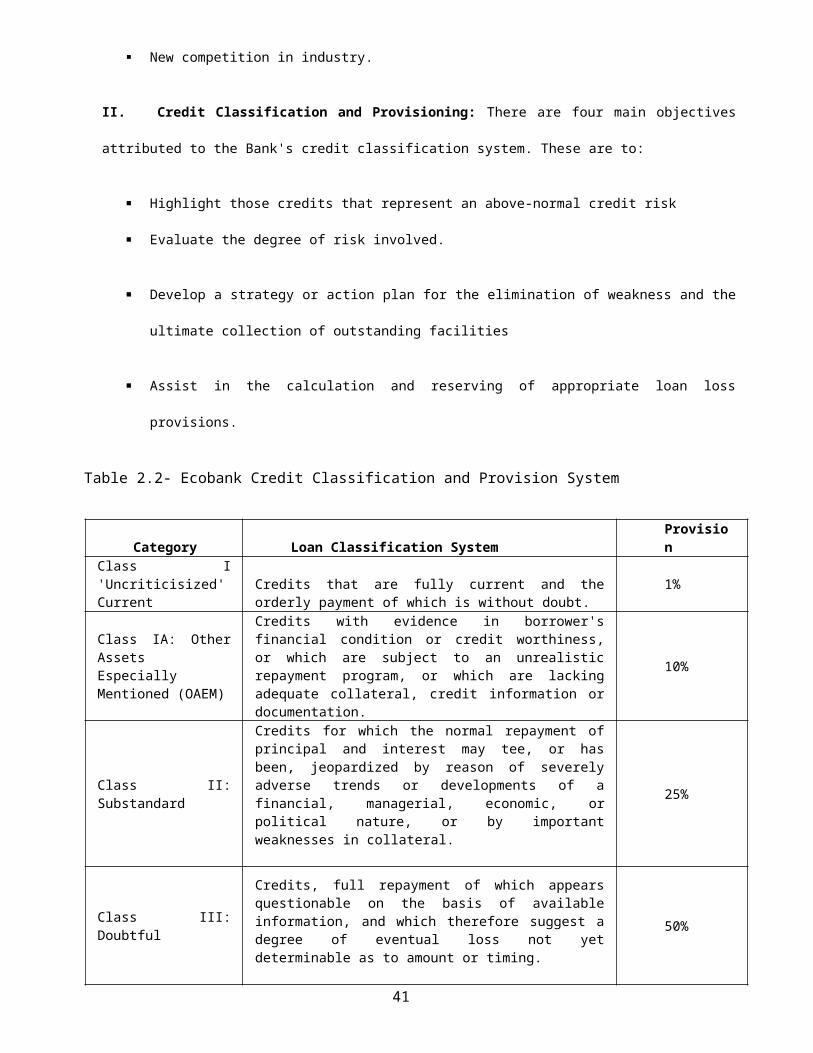

II. Credit Classification and Provisioning: There are four main objectives

attributed to the Bank's credit classification system. These are to:

Highlight those credits that represent an above-normal credit risk

Evaluate the degree of risk involved.

Develop a strategy or action plan for the elimination of weakness and the

ultimate collection of outstanding facilities

Assist in the calculation and reserving of appropriate loan loss

provisions.

Table 2.2- Ecobank Credit Classification and Provision System

Category Loan Classification SystemProvision

Class I'Uncriticisized'Current

Credits that are fully current and theorderly payment of which is without doubt.

1%

Class IA: OtherAssetsEspeciallyMentioned (OAEM)

Credits with evidence in borrower'sfinancial condition or credit worthiness,or which are subject to an unrealisticrepayment program, or which are lackingadequate collateral, credit information ordocumentation.

10%

Class II:Substandard

Credits for which the normal repayment ofprincipal and interest may tee, or hasbeen, jeopardized by reason of severelyadverse trends or developments of afinancial, managerial, economic, orpolitical nature, or by importantweaknesses in collateral.

25%

Class III:Doubtful

Credits, full repayment of which appearsquestionable on the basis of availableinformation, and which therefore suggest adegree of eventual loss not yetdeterminable as to amount or timing.

50%

41

Class IV: Loss

Credits that are regarded as uncollectible.Any amount so classified by accountmanagement, should be fully reserved, andpreviously accrued and unpaid interest mustbe reversed. A classification to IV doesnot mean that there is no potential foreventual recovery. Responsible units areexpected to continue a vigorous collectioneffort until it is decided that no furtherrepayment or recovery is possible.

100%

Source: Own Construction with Data Provided in Appendix C1

It is important to emphasis that some assets, though not worth classifying

require special attention. These are put in a "watch list" category. The watch

list is not a requirement but it is done with the aim to attract the bank's

attention to them. There is no provision made on them.

Another aspect of the classification is that an asset can move from class I to

IV without passing through classes IA, II or III. On the other hand, an asset

classified III can become I within a short period. This is quite understandable

because the overdue period of the loan is not the only criterion taken into

account for loans classification. A company can move from a healthy situation

to very bad one and vice versa.

III. Remedial Management: Remedial management refers to strategies used to

recover loans that are classified. These strategies are based on a case-by-case

analysis. Actions are taken according to the severity of the classification.

Nonetheless, the GCPPM gives some guidelines of objectives to achieve according

to the classification:

Class IA:

Reduction of total exposure.

42

Improvement of security margin by incremental collateral.

Review of the loan documents to ensure enforceability.

Class II:

Prepayment of some of the obligations.

Request for client to find alternative bankers.

Legal action.

Class III:

Legal action to enable the bank to exercise its rights under the security

arrangements

Appointment of a liquidator

Class IV:

Legal action to enable the bank to exercise its rights under the security

arrangements

Appointment of a liquidator

2.8 RECOMMENDED STANDARD PRACTICES OF PROBLEM LOANS MANAGEMENT

This section presents standard practices recommended by the World Bank, the

International Monetary Fund, the West African Monetary Union and the Bank of

Ghana for acceptable management of problem loans.

2.8.1 The World Bank

43

The World Bank (April, 1999) recommends five basic systems that a bank must

have in order to successfully deal with problem loans:

A validated and properly functioning system of credit quality control and

asset classification

The needed reserves to write off all portions of the identified losses

The removal of these assets from the line organization which underwrote

them and their transfer to a specially trained group of collectors

The usage of a well-functioning legal system to help force collection

The stoppage of making, or renewing, bad loans

Table 2.3 - World Bank Credit Classification and Provision System

Classification Loan Classification SystemProvisionRequirement

Standard, orPass

When debt service capacity is consideredbeyond any doubt. Loans and other assetsfully secured by cash or cash-substitutesare usually classified as standard.

General LossReserve, ifdisclosed1-2%

SpeciallyMentioned, orWatch

Credit given through an inadequate loanagreement, a lack of control overcollateral, or without properdocumentation. Loans to borrowers operatingunder economic and market conditions thatnegatively affect the borrower in thefuture should receive this classification.

SpecificProvision5-10%

Substandard

Well-defined credit weaknesses in the debtservice capacity, in particular when theprimary sources of repayment are inadequateand when the bank must consider othersources of repayment such as collateral,the sale of a fixed asset, refinancing, orfresh capital. NPAs that are at least 90days overdue are normally classified assubstandard.

SpecificProvision10-30%

Doubtful Such assets have the same weaknesses as thesubstandard assets, but their collection infull is questionable on the basis ofexisting facts. The possibility of loss is

SpecificProvision50-75%

44

present, but certain events that maystrengthen the asset defer itsclassification as loss until a more exactstatus may be determined.

LossAssets that are considered uncollectible.Partial recovery may be possible in thefuture though.

SpecificProvision100%

Source: Own Construction with Data Provided in Appendix C2

2.8.2 The International Monetary Fund (IMF)

Salas & Saurina (2002) observed that the IMF emphasizes the existence of both

financial and non-financial early warning systems as important mechanisms in

problem loans management since they may prevent the bank from losses if actions

are taken in time to develop a remedial strategy. In addition, loan documents

must contain clauses that allow the bank to examine the books of the borrower.

There are two essential work-out strategies recommended depending on the

assessment of the problem:

If the problem area can be corrected, banks are encouraged to restructure

the loan by increasing collateral, revising repayment and/or changing

management.

If the problem area cannot be corrected, banks must exit the business by

selling collateral and taking legal action.

The loan classification of the IMF is similar to that of the World Bank

but with the following classes: Sound, Weak, Substandard, Doubtful and

Loss.

2.8.3 The West African Monetary Union (WAMU)

45

The WAMU Banking Commission (2001) defines impaired loans as all loans that are

not repaid under the pre-agreed terms and conditions. It recommends that such

loans must be clearly identified and isolated from the bank's books for a

specific treatment. All loans with either high or low risks of non-recovery

must be watched and an internal reporting system to the Managing Director must

be initiated. This will foster Senior Management involvement and guidance in

the close monitoring and management of the stressed accounts to lessen the

financial effects on the bank.

Their Loans classification system and provision requirements differ as the case

may be:

Direct risks or signatory commitments taken on the State and its fellows:

optional provision.

Risks guaranteed by the State: it is suggested, but not demanded, to make

provisions up to the amount of the guaranteed debt (principal and

interest) over a maximum period of 5 years, if the risks covered are not

taken into account in the State budget.

Private risks not guaranteed by the State: the following table summarizes

the loans classification and provision requirements of WAMU.

Table 2.4 – WAMU Credit Classification and Provision System

Loan Classification SystemProvisionRequirements

Unpaid debtsDebts overdue for a period notexceeding 6 months and that have notbeen extended or renewed.

Optional

46

Immobilized debts

Debts overdue for a period notexceeding 6 months and the repaymentis unlikely due to reasons beyond theborrower's control.

Optional

Doubtful orContentious debts

Debts overdue or not but presentingprobable or certain risks of part orfull non-recovery. Debts that haveregistered at least one unpaid of atleast 6 months. Debit accounts withoutany creditor movement for a periodover 3 months. Debit accounts withoutany significant creditor movement fora period over 6 months.

Asset notsecured: 100%provisioningAsset secured bycollateral:optionalprovision for 2years, 50 % the3rd year, 100%the 4th year.

Uncollectibledebts

Assets considered uncollectible afterthe bank has given up all effortseither amicably or legally.

Uncollectibledebts areaccounted aslosses for theirfull amount.

Country risk

Off-balance sheet debts andundertakings on public and privatedebtors

Provisioning isleft at thediscretion ofbanks butinterests must befully provisionedif due over 3months

Source: Own Construction with Data Provided in Appendix C3

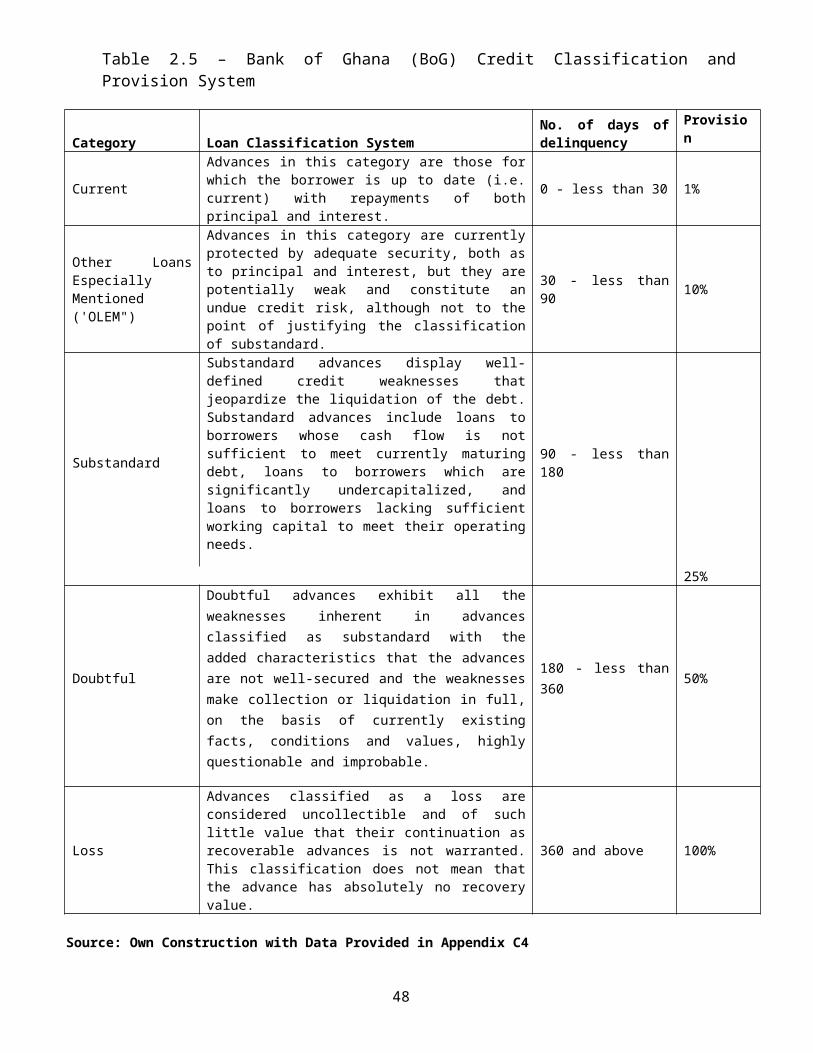

2.8.4 The Bank of Ghana (BoG)

The Bank of Ghana guidelines concerning loan classifications as contained inthe

‘Guideline on Classification of Non-Performing Loans and Provision for

Substandard, Bad and Doubtful Debts’ (December, 1997) are summarized in the

table below.

47

Table 2.5 – Bank of Ghana (BoG) Credit Classification andProvision System

Category Loan Classification SystemNo. of days ofdelinquency

Provision

Current

Advances in this category are those forwhich the borrower is up to date (i.e.current) with repayments of bothprincipal and interest.

0 - less than 30 1%

Other LoansEspeciallyMentioned('OLEM")

Advances in this category are currentlyprotected by adequate security, both asto principal and interest, but they arepotentially weak and constitute anundue credit risk, although not to thepoint of justifying the classificationof substandard.

30 - less than90 10%

Substandard