Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending CHAPTER 18 CONSUMER LOANS, CREDIT CARDS, AND REAL ESTATE LENDING Goal of This Chapter : To learn about the different types of loans lenders make to consumers (individuals and families) and to real estate borrowers, and to understand the factors that influence the profitability and risk of these loans. Additionally, the chapter also examines how consumer and real estate loan rates may be determined and the options a loan officer has today in pricing the loans extended to individuals and families. Key Topics in This Chapter Types of Loans for Individuals and Families Unique Characteristics of Consumer Loans Dodd-Frank, the Consumer Protection Bureau, and CARD Evaluating a Consumer Loan Request Credit Cards and Credit Scoring Disclosure Rules and Discrimination Consumer Loan Pricing and Refinancing Chapter Outline I. Introduction II. Types of Loans Granted to Individuals and Families A. Residential Mortgage Loans B. Nonresidential Loans 1. Installment Loans 2. Noninstallment Loans C. Credit Card Loans and Revolving Credit D. New Credit Card Regulations E. New Consumer Regulations: Dodd-Frank, CARD Act, and the New Consumer Protection Bureau 1. Tricks and Traps—The CARD Act and Revised Regulation Z Appear 2. Dodd-Frank Reforms and Protections Push the Rules Farther Down the Road F. Debit Cards: A Partial Substitute for Credit Cards? G. Rapid Consumer Loan Growth: Rising Debt-to-Income Ratios 18-1

Chap 018

Dec 08, 2015

Banking operations Managemet

Solution Manual

Solution Manual

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

CHAPTER 18

CONSUMER LOANS, CREDIT CARDS, AND REAL ESTATE LENDING

Goal of This Chapter: To learn about the different types of loans lenders make to consumers (individuals and families) and to real estate borrowers, and to understand the factors that influence the profitability and risk of these loans. Additionally, the chapter also examines how consumer and real estate loan rates may be determined and the options a loan officer has today in pricing the loans extended to individuals and families.

Key Topics in This Chapter

Types of Loans for Individuals and Families Unique Characteristics of Consumer Loans Dodd-Frank, the Consumer Protection Bureau, and CARD Evaluating a Consumer Loan Request Credit Cards and Credit Scoring Disclosure Rules and Discrimination Consumer Loan Pricing and Refinancing

Chapter Outline

I. IntroductionII. Types of Loans Granted to Individuals and Families

A. Residential Mortgage LoansB. Nonresidential Loans

1. Installment Loans2. Noninstallment Loans

C. Credit Card Loans and Revolving CreditD. New Credit Card RegulationsE. New Consumer Regulations: Dodd-Frank, CARD Act, and the New Consumer Protection Bureau

1. Tricks and Traps—The CARD Act and Revised Regulation Z Appear2. Dodd-Frank Reforms and Protections Push the Rules Farther Down the Road

F. Debit Cards: A Partial Substitute for Credit Cards?G. Rapid Consumer Loan Growth: Rising Debt-to-Income Ratios

III. Characteristics of Consumer LoansIV. Evaluating a Consumer Loan Application

A. Character and PurposeB. Income LevelsC. Deposit BalancesD. Employment and Residential StabilityE. Pyramiding of DebtF. How to Qualify for a Consumer LoanG. The Challenge of Consumer Lending

V. Example of a Consumer Loan Application

18-1

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

VI. Credit Scoring Consumer Loan ApplicationsA. The FICO Scoring System

VII. Laws and Regulations Applying to Consumer LoansA. Customer Disclosure RequirementsB. Outlawing Credit DiscriminationC. Predatory Lending and Subprime Loans

VIII. Real Estate LoansA. Differences between Real Estate Loans and Other LoansB. Factors in Evaluating Applications for Real Estate LoansC. Home Equity LendingD. The Most Controversial of Home Mortgage Loans: Interest-Only and Adjustable Mortgages and the Recent Mortgage Crisis

IX. A Revised Federal Bankruptcy Code as Bankruptcy Filings SoarX. Pricing Consumer and Real Estate Loans: Determining the Rate of Interest and Other Loan Terms

A. The Interest Rate Attached to Nonresidential Consumer Loans1. The Cost-Plus Model2. Annual Percentage Rate3. Simple Interest4. The Discount Rate Method5. The Add-On Loan Rate Method6. Rule of 78s

B. Interest Rates on Home Mortgage Loans1. Fixed-Rate Mortgages (FRMs)2. Adjustable-Rate Mortgages (ARMs)3. Charging the Customer Mortgage Points

XI. Summary of the Chapter

Concept Checks

18-1. What are the principal differences among residential loans, nonresidential installment loans, noninstallment loans, and credit card or revolving loans?

Residential loans are credit to finance the purchase of a home or fund improvements on a private residence. Nonresidential loans to individuals and families include installment loans and noninstallment loans. Short-term to medium-term loans, repayable in two or more consecutive payments (usually monthly or quarterly), are known as installment loans. Installment loans are paid off gradually over time, whereas short-term loans that individuals and families draw upon for immediate cash needs and are repayable in a lump sum at the end of the loan are known as noninstallment loans.

Installment loans usually finance large-ticket purchases, such as automobiles or household furniture, whereas noninstallment loans usually are directed at current living expenses. Installment loans help the bank recover funds that can be reloaned more quickly but they generally require a more intensive credit investigation by the bank. Bank credit cards offer convenience and a revolving line of credit that customers can access whenever the need arises.

18-2

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

18-2. Why do interest rates on consumer loans typically average higher than on most other kinds of loans?

Interest rates on consumer loans are typically higher than on most other kinds of loans since they are among the most costly as well as risky to make per dollar of loanable funds committed. Consumer loans also tend to be cyclically sensitive. Moreover, demand for consumers loans tend to be relatively inelastic to changes in interest rates.

18-3. What features of a consumer loan application should a loan officer examine most carefully?

A loan officer should examine character and income level of the borrower, purpose of the loan, employment and residential stability of the borrower, and pyramiding of debt when evaluating a consumer loan application.

18-4. How do credit-scoring systems work?

Credit-scoring systems use statistical techniques (usually multiple discriminant analysis) to evaluate the loan applications they receive from consumers. Credit-scoring systems are usually based on discriminant models or related techniques, such as logit or probit analysis or neural networks, in which several variables are used jointly to establish a numerical score for each credit applicant. If the applicant’s score exceeds a critical cutoff level, he or she is likely to be approved for credit in the absence of other damaging information. On the contrary, if the applicant’s score falls below the cutoff level, credit is likely to be denied in the absence of other mitigating factors.

18-5. What are the principal advantages to a lending institution of using a credit-scoring system?

The credit scoring method has the advantage of being objective, requiring less loan officer judgment, possibly reducing loan losses, reducing operating costs, and quicker evaluation of applications when a large volume of consumer loans is being processed.

18-6. Are there any significant disadvantages to a credit-scoring system?

A credit-scoring system assumes that the same factors that separated good from bad loans in the past will, with an acceptable risk of error, separate good from bad loans in the future. Clearly, this underlying assumption can be wrong if the economy or other factors change abruptly. Also, from a lending institution’s perspective, it runs the risk of alienating those customers who feel the lending institution has not fully considered their financial situation and the special circumstances that may have given rise to their loan request. There is also the danger of being sued by a customer under antidiscrimination laws if race, gender, marital status, or other discriminating factors prohibited by statute or court rulings are used in a scoring system.

18-3

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

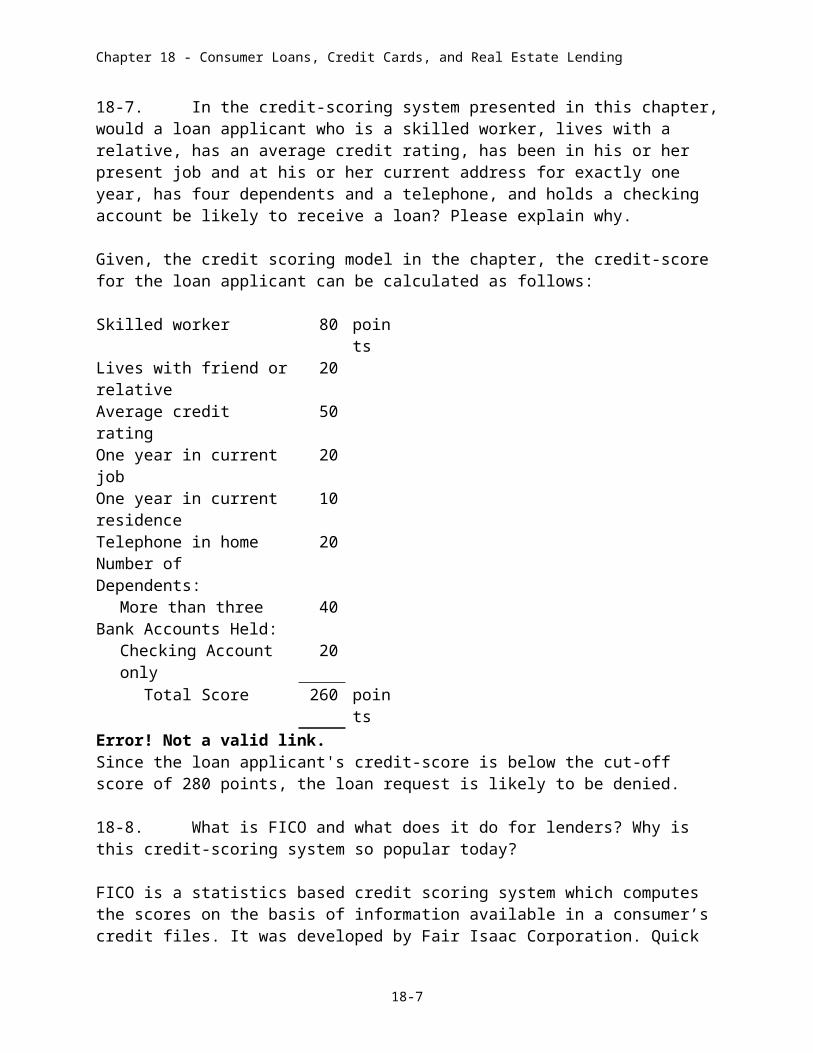

18-7. In the credit-scoring system presented in this chapter, would a loan applicant who is a skilled worker, lives with a relative, has an average credit rating, has been in his or her present job and at his or her current address for exactly one year, has four dependents and a telephone, and holds a checking account be likely to receive a loan? Please explain why.

Given, the credit scoring model in the chapter, the credit-score for the loan applicant can be calculated as follows:

Skilled worker 80 pointsLives with friend or relative 20Average credit rating 50One year in current job 20One year in current residence 10Telephone in home 20Number of Dependents:

More than three 40Bank Accounts Held:

Checking Account only 20Total Score 260 points

Error! Not a valid link.Since the loan applicant's credit-score is below the cut-off score of 280 points, the loan request is likely to be denied.

18-8. What is FICO and what does it do for lenders? Why is this credit-scoring system so popular today?

FICO is a statistics based credit scoring system which computes the scores on the basis of information available in a consumer’s credit files. It was developed by Fair Isaac Corporation. Quick and easy access to objective and impartial credit scores makes it very useful tool for lending institutions. In addition to being widely accepted, presence of a FICO score simulator allows individuals to estimate what would happen to their FICO score if certain changes were made in their personal financial profile has made the score popular.

18-9. What laws exist today to give consumers fuller disclosure about the terms and risks of taking on credit?

The following federal laws give consumers who are borrowing money fuller disclosure about the terms and risks of taking on credit:

a. Truth-in-Lending Act, 1968b. Fair Credit Reporting Act c. Fair Credit Billing Act, 1974d. Fair Credit and Charge-Card Disclosure Acte. Fair Debt Collection Practices Act

18-4

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

The Truth-in-Lending Act mandates that lenders must provide their customers with information on all loan charges and associated risks in a disclosure statement. The Fair Credit Reporting Act gives individuals easier access to their credit-bureau records, the right to challenge information contained therein, and to insist on the prompt correction of errors. The Fair Credit Billing Act gives consumers the right to dispute billing errors and have those errors corrected. The Fair Credit and Charge-Card Disclosure requires that customers applying for credit cards be given early written notice (usually before a credit card is used for the first time) about required fees to open or renew a credit account. Also, if a fee for renewal is charged, the customer must receive written notice in advance. The Fair Debt Collection Practices Act limits how far a creditor or credit collection agency can go in pressing that customer to pay up.

18-10. What legal protections are available today to protect borrowers against discrimination? Against predatory lending?

The Equal Credit Opportunity Act outlaws discrimination in lending based on race, age, sex, religious preference, receipt of public assistance, or any other irrelevant factors. The Community Reinvestment Act requires banks and other lending institutions to make an affirmative effort to serve all segments of their designated market areas without discriminating against certain neighborhoods.

Predatory lending is an abusive practice among some lenders that involves making loans to borrowers with below-average credit rating and then charging them excessive fees and interest rates, thereby increasing the risk of default. In 1994 Congress passed the Home Ownership and Equity Protection Act, which was aimed to protect home owners from loan agreements they could not afford. Loans with annual percentage rates (APR) of 10 percentage points or more above the yield on comparable maturity U.S. Treasury securities and closing fees above 8 percent of the loan amount are defined as “abusive.” Consumers have 6 days (three days before plus three days after a home loan closing) in which to decide whether or not to proceed with the loan. Also, credit granting institutions must fully disclose all fees, risks and prohibitory conditions associated with the loan, failing which, a borrower has up to 3 years to rescind the transaction, and lenders might be liable for all damages that occur.

18-11. In your opinion, are any additional laws needed in these areas?

Depending on one's point of view, a case can be made, both for and against the requirement of more regulation to protect a consumer’s interest. Most, if not all, bankers and bank trade associations, as well as many of the regulatory agencies, tend to agree that there are enough existing laws and regulations in these areas. On the contrary, consumer groups and some elected officials may argue that consumers, particularly in certain economic groups or communities, need more legislations and/or regulation to protect their interests.

18-12. In what ways is a real estate loan unique compared to other kinds of bank loans?

Real estate loans differ from any other kind of loan in several aspects. The average size of a mortgage loan is usually much higher than that of any other loan. Also, the duration of these loans tends to be much longer, typically between 15 to 30 years. Both these factors also

18-5

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

significantly increase the associated risks—including adverse changes in economic conditions, interest rates, value of the collateral, and the health of the borrower—for a lending institution.

18-13. What factors should a lender consider in evaluating real estate loan applications?

Some of the important factors to be considered in evaluating a real estate loan application are:

1. The amount of down payment planned by the borrower as a percentage of the purchase price of the property—a critical factor in determining the safety level for a lending institution.

2. Potential future business that can be gained as a result of providing a mortgage loan.3. Amount and stability of the borrower’s income—a determinant of the borrower’s

capacity to service the debt as and when it becomes due.4. The outlook for real estate sales in the local market area.5. The outlook for interest rates in the economy

18-14. What is home equity lending, and what are its advantages and disadvantages for banks and other consumer lending institutions?

Loans involving a borrowing base of the residual market value of a home (value over and above the amount of any outstanding liens against the home), being drawn upon as collateral is known as home equity lending. Borrowers can secure home equity loans for second mortgage, college tuition, or any other financial needs that they may have. Usually these loans carry a lower rate of interest than consumer loans. It is advantageous for the lending institutions since these loans are secured against the equity value of the property.However, these loans are made on the premise that housing prices will not fall significantly. This may not always be a correct assumption. If the housing market slows down and property prices decline, the borrower may default. The banks will likely be forced to foreclose in such situations. It may also face difficulty in selling the property in an already depressed market. Also, there is always a risk of the bank’s reputation being harmed in the event of foreclosures. Moreover, regulations prohibit the lending institutions from arbitrarily cancelling any home equity loans.

18-15. How is the changing age structure of the population likely to affect consumer loan programs? What other forces are reshaping household lending today?

As people grow older, especially beyond the age of 40 or 45, they tend to make less use of credit and to pay down outstanding debt obligations. This suggests that the total demand for consumer credit per capita may fall, forcing banks and other consumer lenders to fight hard for profitable consumer loan accounts. However, economic prosperity and higher disposable income has allowed many young people to afford housing loans earlier than ever before. Some of the important factors that shape the household lending industry include high consumer demand, effective regulations, and innovations of the financial products that allow institutions to reduce risks on their books and secure more capital, among others.

18-6

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

18-16. What challenges have U.S. bankruptcy laws provided for consumers and those lending money to them?

Recent changes in U.S. bankruptcy laws present serious challenges to consumer lending institutions. Congress passed the Bankruptcy Reform Act in 1978, amending a federal bankruptcy code that had stood since the turn of the century. While amendments in 1984 tightened up some of the loopholes in the 1978 law, the most recent reforms tipped the legal scales substantially in favor of individuals filing bankruptcy petitions and more severely limited the amount and kinds of debtors' assets that could be converted into cash for distribution to banks and other creditors. However, the Bankruptcy Abuse Prevention and Consumer Protection Act was signed in April of 2005. This law is likely to make it more difficult, expensive and time consuming to file for bankruptcy. Consumers must complete a credit counseling program before becoming eligible for filing bankruptcy. Also, a ‘means test’ must be undertaken by consumers to determine whether they are eligible to file for Chapter 7 bankruptcy—which wipes out most debt—or whether they will have to file Chapter 13—which requires them to have a court approved repayment plan for their outstanding debt. Overall, the revised bankruptcy code is expected to eventually reduce the cost of credit for the average borrower because it may tend to reduce the incidence of bad loans. For the banks though, it may result in slow growth of credit card and instalment loans as consumers become more cautious about running up too much debt and shift more of their borrowing into housing-related loans because a bankrupt’s home (depending on the laws in the borrower’s home state) may be protected from seizure by creditors.

18-17. What options does a loan officer have in pricing consumer loans?

Most consumer loans, like most business loans, are priced off some base or cost rate, with a profit margin and compensation for risk added on. This is known as cost plus model. Some of the other pricing mechanisms followed in pricing a consumer loans are:Annual percentage rate: The annual percentage rate is the internal rate of return (annualized) that equates expected total payments for the lender with the amount of the loan.Simple interest: This method computes the repayment amount by adding a flat rate of interest to the borrowed amount adjusted for the length of time of borrowing.The discount rate method: This method requires the customer to pay interest up front. Under this approach, interest is deducted upfront and the customer receives the loan amount less any interest owed.The add-on rate method: This method of pricing involves adding up the entire interest cost to the principal amount upfront before determining the instalments for the borrower.Rule of 78s: This method determines the amount of interest income a lender is entitled to accrue at any point in time from a loan that is being paid out in monthly installments.Most installments and lump-sum payment loans are made with fixed interest rates. However, due to increasing volatility in interest rates a large number of floating rate consumer loans have also gained popularity.

18-18. Suppose a customer is offered a loan at a discount rate of 8 percent and pays $75 in interest at the beginning of the term of the loan. What net amount of credit did this customer receive? Suppose you are told that the effective rate on this loan is 12 percent. What is the average loan amount the customer has available during the year?

18-7

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

The amount of net credit received by the customer will be:

An effective rate of 12 percent implies an interest cost of 12 percent on the available funds to the

borrower. Since the interest paid is $75, the average funds available will be:

18-19. See if you can determine what APR you are charging a consumer loan customer if you grant the customer a loan for five years payable in monthly installments, and the customer must pay a finance charge of $42.74 per $100.

Assuming a borrowed amount of $100, the total amount to be repaid will be $142.74.

Since the loan period is five years, the monthly installment will be:

Using the following equation for present value of an annuity ($2.379 in this case) and solving for will give us a monthly rate of 1.25%

Therefore, the APR charged on the loan will be 18-20. If you quote a consumer loan customer an APR of 16 percent on a $10,000 loan with a term of four years that requires monthly installment payments, what finance charge must this customer pay?

Given an APR of 16 percent, the monthly rate of interest will be

The equated monthly installments for the loan can be calculated as:

Thus, the total amount paid by the borrower will be:

Therefore, finance charges on the loan equals;

18-21. What differences exist between ARMs and FRMs?

An ARM or adjustable rate mortgage is a mortgage whose interest rate changes over time, usually based upon changes in some base or reference rate that reflects the cost of funds to the lending institutions. An FRM or fixed rate mortgage is a mortgage whose interest rate does not change throughout the tenure of the loan.

18-22. How is the loan rate figured on a home mortgage loan? What are the key factors or variables?

18-8

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

A home mortgage loan rate is usually based on the market rate of interest plus a premium based on the amount of perceived credit risk of the borrower. It can either be a fixed rate or a floating rate mortgage. One way to figure out the affordability of a home mortgage loan is to calculate the required monthly mortgage payment to be paid by the borrower. This is a time value of money calculation and the payment depends upon the loan principal, the interest rate, and the length of the mortgage loan. An amount where both, the borrower and the lender, agree with each other can be used to set the rate on the mortgage.

18-23. What are points? What is their function?

Often, home loan borrowers are required to pay an additional charge upfront called points. Each point is equivalent to one percentage point. Total amount needed to be paid by the borrower equals these points multiplied by the mortgage amount. Usually these extra charges are levied by a lending institution to be able to earn a higher effective interest rate.

Problems and Projects

18-1. The Childress family has applied for a $5,000 loan for home improvements, especially to install a new roof and add new carpeting. Bob Childress is a welder at Ford Motor Co., the first year he has held that job, and his wife sells clothing at Wal-Mart. They have three children. The Childresses own their home, which they purchased six months ago, and have an average credit rating, with some late bill payments. They have a telephone, but hold only a checking account with a bank and a few savings bonds. Mr. Childress has a $35,000 life insurance policy with a cash surrender value of $1,100. Suppose the lender uses the credit scoring system presented in this chapter and denies all credit applications scoring fewer than 360 points. Is the Childress family likely to get their loan? What is the family’s credit score? (Hint: For the occupation factor take the average for the husband’s and wife’s occupations.)

The credit-scoring system presented in Chapter 18 is assumed here to have a cutoff point of 360 with credit requests denied when an applicant’s score is below 360. The Childress family would score approximately as follows under the scoring system in the chapter:

Occupation (for skilled or clerical workers) 75 points (average of 70 and 80)Housing Status (own home) 60Credit Rating 50Time in Job (one year or less) 20Time at Current Address (one year or less) 10Telephone 20Number of Dependents:More than three 40Bank Accounts Held:Checking Account only 20Total 295 points

This credit request, in the absence of other mitigating factors, would be denied.

18-9

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

18-2. Mr. and Mrs. Napper are interested in funding their children's college education by taking out a home equity loan in the amount of $24,000. Eldridge National Bank is willing to extend a loan, using the Nappers’ home as collateral. Their home has been appraised at $110,000, and Eldridge permits a customer to use no more than 70 percent of the appraised value of a home as a borrowing base. The Nappers still owe $60,000 on the first mortgage against their home. Is there enough residual value left in the Nappers’ home to support their loan request? How could the lender help them meet their credit needs?

The maximum credit line available to the Nappers under the bank's current home-equity loan policy is:

This clearly is not a large enough borrowing base to cover the $24,000 loan requested. Many banks make adjustments in the permissible loan amount if the customer has an above-average level of income, other assets to pledge, relatively low mortgage debt obligations, and an excellent credit rating. Thus, the Nappers may be able to qualify for an additional $7,000 in loanable funds (perhaps by pledging other collateral) to make up the $24,000 they need.

18-3. Greg Lance has just been informed by a finance company that he can access a line of credit of no more than $75,000 based upon the equity value in his home. Lance still owes $180,000 on a first mortgage against his home and $25,000 on a second mortgage against the home, which was incurred last year to repair the roof and driveway. If the appraised value of Lance’s residence is $400,000, what percentage of the home's estimated market value is the lender using to determine Lance’s maximum available line of credit?Maximum credit line can be calculated as:

or,

Therefore,

The lender is using approximately 70% of market value of Greg’s home to determine his available credit line.

18-4. What term in the consumer lending field does each of the following statements describe?

a. Plastic card used to pay for goods and services without borrowing money – Debit card.

b. Loan to purchase an automobile and pay it off monthly – Installment loan.

c. If you fail to pay the lender seizes your deposit – Right of offset.

d. Numerical rating describing likelihood of loan repayment – Credit score.

e. Loans extended to low-credit-rated borrowers – Subprime loans.

18-10

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

f. Loan based on spread between a home’s market value and its mortgage balance – Home equity loans.

g. Method for calculating rebate borrower receives from retiring a loan early – Rule of 78s.

h. Lender requires excessive insurance fees on a new loan – Predatory lending.

i. Loan rate lenders must quote under the Truth in Lending Act – APR.

j. Upfront payment required as a condition for getting a home loan – Points.

18-5. Which federal law or laws apply to each of the situations described below?

a. A loan officer asks an individual requesting a loan about her race – This is prohibited by the Equal Credit Opportunity Act.

b. A bill collector called Jim Jones three times yesterday at his work number without first asking permission – This is prohibited by the Fair Debt Collection Practices Act.

c. Sixton National Bank has developed a special form to tell its customers the finance charges they must pay to secure a loan – Disclosure of all charges are required under Truth in Lending Act.

d. Consumer Savings Bank has just received an outstanding rating from federal examiners for its efforts to serve all segments of its community – Ratings are provided under the Community Reinvestment Act.

e. Presage State Bank must disclose once a year the areas in the local community where it has made home mortgage and home improvement loans – Disclosure required under the Home Mortgage Disclosure Act.

f. Reliance Credit Card Company is contacted by one of its customers in a dispute over the amount of charges the customer made at a local department store – This is a consumer’s right under Fair Credit Billing Act.

g. Amy Imed, after requesting a copy of her credit report, discovers several errors and demands a correction – This is a right under the Fair Credit Reporting Act.

18-6. James Smithern has asked for a $3,500 loan from Beard Center National Bank to repay some personal expenses. The bank uses a credit-scoring system to evaluate such requests, which contains the following discriminating factors along with their associated point weights in parentheses:

Credit Rating (excellent 3; average 2; poor or no record 0)Time in Current Job (five years or more, 6; one to five years, 3)

18-11

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

Time at Current Residence (more than 2 years, 4; one to two years, 2; less than one year, 1)Telephone in Residence (yes, 1; no, 0)Holds Account at Bank (yes, 2; no, 0)

The bank generally grants a loan if a customer scores 9 or more points. Mr. Smithern has an average credit rating, has been in his current job for three years and at his current residence for two years, has a telephone, but has no account at the bank. Is James Smithern likely to receive the loan he has requested?

The credit score for Mr. Smithem can be calculated as follows:

Credit rating: average 2 pointsTime in current job: one to five years 3 pointsTime in current residence: one to two years 2 pointsTelephone: Yes 1 pointHolds Bank Account: No 0 points

Mr. Smithern's total credit score is 8. Given, the bank grants loans to applicants with credit scores of 9 or more points, Mr. Smithern is not likely to receive a loan under this scoring system.

18-7. Yorktown Savings Bank, in reviewing its credit card customers, finds that of those customers who scored 40 points or less on its credit-scoring system, 30 percent (or a total of 7,665 credit customers) turned out to be delinquent credits, resulting in total loss. This group of bad credit card loans averaged $6,200 in size per customer account. Examining its successful credit accounts Yorktown finds that 12 percent of its good customers (or a total of 3,066 customers) scored 40 points or less on the bank’s scoring system. These low-scoring but good accounts generated about $1,000 in revenues each. If Yorktown’s credit card division follows the decision rule of granting credit cards only to those customers scoring more than 40 points and future credit accounts generate about the same average revenues and losses, about how much can the bank expect to save in net losses?

The total loss to the bank from delinquent customers is ($47,523,000 ($6,200 × 7,665). On the other hand, paying credit-card customers (amounting to 3,066 customers) averaged a score of 40 points or less, but successfully generated about $1,000 a piece in revenues, resulting in aggregate revenues of $3,066,000. By adopting a decision rule to grant credit-card privileges only to customers scoring more than 40 points (and given the same average revenues and losses) the bank will save $44,457,000 ($47,523,000 - $3,066,000) in net losses.

18-8 The Lathrop family needs some extra funds to put their two children through college starting this coming fall and to buy a new computer system for a part-time home business. They are not sure of the current market value of their home, though comparable four-bedroom homes are selling for about $395,000 in the neighborhood. The Monarch University Credit Union will loan 75 percent of the property’s appraised value, but the Lathrops still owe $235,000 on their home mortgage and a home improvement loan combined. What maximum amount of credit is available to this family should it elect to seek a home equity credit line?

18-12

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

Maximum credit line can be calculated as:or

Therefore, maximum amount of credit available to Lathrop family will be $61,250.

18-9 San Carlos Bank and Trust Company uses a credit-scoring system to evaluate most consumer loans that amount to more than $2,500. The key factors used in its scoring system are found at the conclusion of this problem.

The Mulvaney family has two wage earners who have held their present jobs for 18 months. They have lived at their current street address for one year, where they rent on a six month lease. Their credit report is excellent but shows only one previous charge. However, they are actively using two credit cards right now to help with household expenses. Yesterday, they opened an account at San Carlos and deposited $250. The Mulvaneys have asked for a $4,500 loan to purchase a used car and some furniture. The bank has a cutoff score in its scoring system of 30 points. Would you make this loan for two years as they have requested? Are there factors not included in the scoring system that you would like to know more about? Please explain.

Borrower’s length of employment in his/her Credit bureau report: present job: Excellent 8 points

More than one year 6 points Average 5 points Less than one year 3 points Below average or no record 2 points

Borrower’s length of time at current address: Credit cards currently active: More than 2 years 8 points One card 6 points One to two years 4 points Two cards 4 points Less than one year 2 points More than two cards 2 points

Borrower’s current home situation: Deposit account(s) with bank: Owns home 7 points Yes 5 points Rents home or apartment 4 points No 2 points Lives with friend or relative 2 points

The credit score for the Mulvaney family as per the credit-scoring system used by San Carlos Bank and Trust will be as follows:

Length of Employment: More than one year 6 pointsLength of time at Current Address: One to two years 4Current Home Situation: Rented home 4Credit Bureau Report: Excellent 8Credit Cards Currently Active: 2 Cards 4Deposit Accounts with Bank: Yes 5

Total 31 points

The Mulvaney family has a total credit score of 31. San Carlos Bank and Trust has a cutoff score of 30 points, so the Mulvaneys are likely to receive their loan. The credit-scoring system of the

18-13

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

bank, however, does not include the nature of employment of the borrower as a factor to consider in providing loans. This is very important since it can determine the sensitivity of the capacity of the borrower to repay to the funds to macro-economic variables.

18-10. Clyde Cook wants to start his own business. He has asked his bank for a $50,000 new-venture loan. The bank has a policy of making discount-rate loans in these cases if the venture looks good, but at an interest rate of prime plus 2. (The prime rate is currently posted at 4.25 percent.) If Mr. Cook’s loan is approved for the full amount requested, what net proceeds will he have to work with from this loan? What is the effective interest rate on this loan for one year?

Interest rate chargeable to Clyde is Therefore, interest amount charged upfront is: Hence, the net proceeds for Clyde will be

Thus, effective interest rate on the loan can be calculated as

18-11. The Michael family has asked for a 30-year mortgage in the amount of $325,000 to purchase a home. At a 5.25 percent loan rate, what is the required monthly payment?

Given an annual rate of 5.25 percent, monthly rate is

Therefore, the equated monthly payments on a 30-year mortgage at the rate of 5.25 percent per annum for an amount of $325,000 can be calculated as:

18-12. Barb Jones received a $5,000 loan last month with the intention of repaying the loan in 12 months. However, Jones now discovers she has cash to repay the loan after making just three payments. What percentage of the total finance charge is Jones entitled to receive as a rebate and what percentage of the loan's finance charge is the lender entitled to keep?

In cases of pre-payment of loans, the rebate on interest to the borrower can be computed using the Rule of 78s. Percentage of rebate that Barb Jones is entitled to receive will be:

of the total finance charges on the loan. The lender is entitled to keep percent of the finance charges associated with this loan.

18-14

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

18-13. The Bender family has been planning a vacation to Europe for the past two years. Tabb Savings agrees to advance a loan of $8,000 to finance the trip provided the Benders pay the loan back in 12 equal monthly installments. Tabb will charge an add-on loan rate of 5.75 percent. How much in interest will the Benders pay under the add-on rate method? What is the amount of each required monthly payment? What is the effective loan rate in this case?

The amount of interest cost for the Benders will be:

Thus, the equated monthly payments will be =

Since the average funds owned during the year will be $4,000 (approximately), the effective interest rate can be calculated as:

18-14. Jane Zahrley’s request for a five-year automobile loan for $39,000 has been approved. Reston Bank will require equal monthly installment payments for 60 months. The bank tells Jane that she must pay a total of $5,500 in finance charges. What is the loan’s APR?

Given finance charges of $5,500, the total amount to be repaid by Jane will be: .

Thus, the equated monthly payments to be made by her is: .

The monthly rate of interest can be calculated using a financial calculator or a spreadsheet. In this instance the monthly rate will be 0.44313%. Therefore, APR charged by Reston Bank is 5.32% (0.44313% × 12).

18-15. Susie Que has asked for a 25-year mortgage to purchase a home at Nag’s Head. The purchase price is $465,000, of which Susie must borrow $395,000 to be repaid in monthly installments. If Susie can get this loan for an APR of 5.50 percent, how much in total finance charges must she pay?

Monthly rate for the mortgage will be

The equated monthly installments that Susie will be required to pay can be calculated as:

Therefore, the total amount that she needs to repay is $727,693.68 ($2,425.65 × 300).Thus, total finance charges on the mortgage loan is $332,693.68 (727,693.68 - $395,000).

18-16. Mary Contrary is offered a $1,600 loan for a year to be paid back in equal quarterly principal installments of $400 each. If Mary is offered the loan at 6 percent simple interest, how much in total interest charges will she pay? Would Mary be better off (in terms of lower interest

18-15

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

cost) if she were offered the $1,600 at 5 percent simple interest with only one principal payment when the loan reaches maturity? What advantage would this second set of loan terms have over the first set of loan terms?

If the principal of $400 is repaid every quarter, Mary will pay the following in interest on her $1600 loan for one year at 6 percent simple interest:

First Quarter: I = Second Quarter: I = Third Quarter: I = Fourth Quarter: I = Therefore, total Interest owed =

However, if she was offered the $1,600 loan at a 5 percent simple interest rate and the loan is repaid in lump sum at maturity, she will end up paying a total interest of:$80 ($1,600 × 0.05). Therefore, purely from an interest cost point of view, Mary is better off borrowing using the first option. However, in the second option she would have the full amount of $1,600 available for use for one year.

18-17. Buck and Marie Rogers are negotiating with their local bank to secure a mortgage loan in order to buy their first home. With only a limited down payment available to them, Buck and Marie must borrow $300,000. Moreover, the bank has assessed them a half point on the loan. What is the dollar amount of points they must pay to receive this loan? How much home mortgage credit will they actually have available for their use?

The dollar amount of points that Buck and Marie are required to pay upfront is:

Thus, the amount of funds available to the Rogers will be:

18-18. Dryden Bank’s personal loan department quotes Lance Greg a finance charge of $3.75 for each $100 in credit the bank is willing to extend to him for a year (assuming the balance of the loan is to be paid off in 12 equal installments). What APR is the bank quoting Lance? How much would he save per $100 borrowed if he could retire the loan in six months?

Given the finance charge of $3.75, the total amount to be repaid by Lance is $103.75. Thus the

equated monthly payments required is . The monthly rate charged by the bank

can be calculated using a financial calculator or a spreadsheet. The rate charged by Dryden Bank on this loan is 0.571%. Thus, the APR will be: If the loan is repaid by lance in six months:The equated monthly payments at an APR of 6.852 percent can be calculated as:

18-16

Chapter 18 - Consumer Loans, Credit Cards, and Real Estate Lending

Thus, the total amount to be repaid in this case will be $102.008 ($17.002 × 12).Therefore, dollar amount saved on every $100 borrowed, if repaid in six months will be $1.742 ($103.75 - $102.008).

18-17

Related Documents