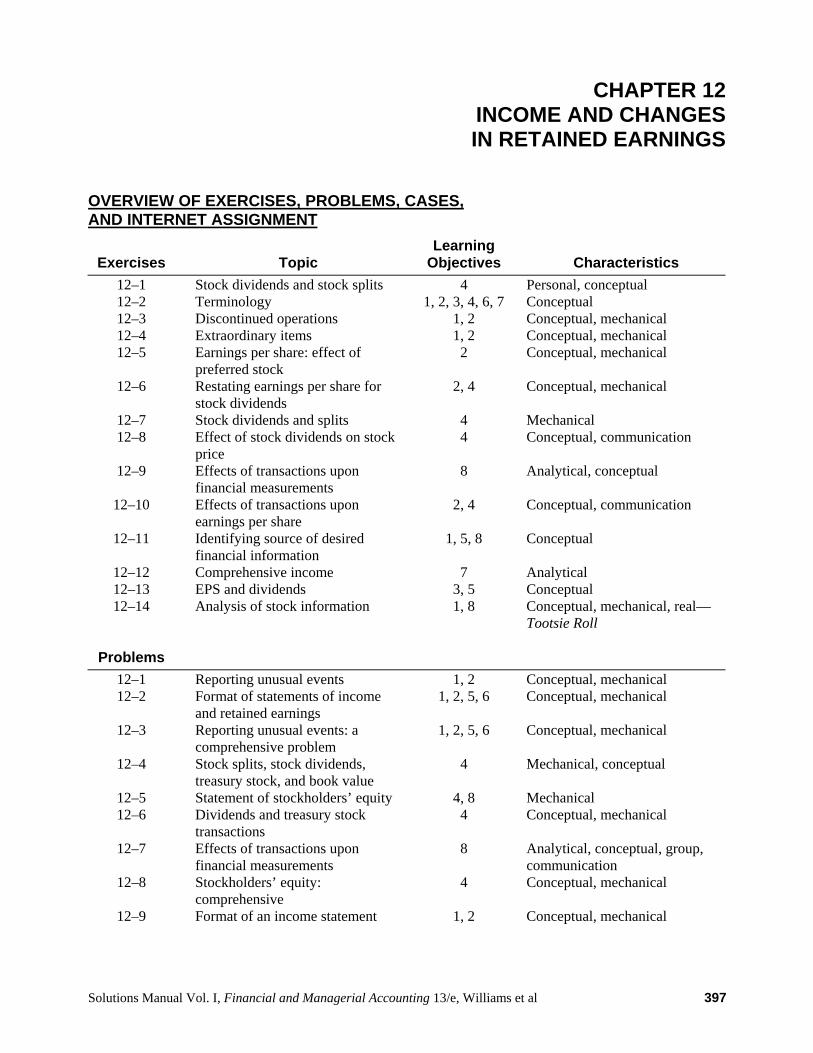

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 397 CHAPTER 12 INCOME AND CHANGES IN RETAINED EARNINGS OVERVIEW OF EXERCISES, PROBLEMS, CASES, AND INTERNET ASSIGNMENT Exercises Topic Learning Objectives Characteristics 12–1 Stock dividends and stock splits 4 Personal, conceptual 12–2 Terminology 1, 2, 3, 4, 6, 7 Conceptual 12–3 Discontinued operations 1, 2 Conceptual, mechanical 12–4 Extraordinary items 1, 2 Conceptual, mechanical 12–5 Earnings per share: effect of preferred stock 2 Conceptual, mechanical 12–6 Restating earnings per share for stock dividends 2, 4 Conceptual, mechanical 12–7 Stock dividends and splits 4 Mechanical 12–8 Effect of stock dividends on stock price 4 Conceptual, communication 12–9 Effects of transactions upon financial measurements 8 Analytical, conceptual 12–10 Effects of transactions upon earnings per share 2, 4 Conceptual, communication 12–11 Identifying source of desired financial information 1, 5, 8 Conceptual 12–12 Comprehensive income 7 Analytical 12–13 EPS and dividends 3, 5 Conceptual 12–14 Analysis of stock information 1, 8 Conceptual, mechanical, real— Tootsie Roll Problems 12–1 Reporting unusual events 1, 2 Conceptual, mechanical 12–2 Format of statements of income and retained earnings 1, 2, 5, 6 Conceptual, mechanical 12–3 Reporting unusual events: a comprehensive problem 1, 2, 5, 6 Conceptual, mechanical 12–4 Stock splits, stock dividends, treasury stock, and book value 4 Mechanical, conceptual 12–5 Statement of stockholders’ equity 4, 8 Mechanical 12–6 Dividends and treasury stock transactions 4 Conceptual, mechanical 12–7 Effects of transactions upon financial measurements 8 Analytical, conceptual, group, communication 12–8 Stockholders’ equity: comprehensive 4 Conceptual, mechanical 12–9 Format of an income statement 1, 2 Conceptual, mechanical

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 397

CHAPTER 12 INCOME AND CHANGES IN RETAINED EARNINGS

OVERVIEW OF EXERCISES, PROBLEMS, CASES, AND INTERNET ASSIGNMENT

Exercises

Topic

LearningObjectives

Characteristics

12–1 Stock dividends and stock splits 4 Personal, conceptual 12–2 Terminology 1, 2, 3, 4, 6, 7 Conceptual 12–3 Discontinued operations 1, 2 Conceptual, mechanical 12–4 Extraordinary items 1, 2 Conceptual, mechanical 12–5 Earnings per share: effect of

preferred stock 2 Conceptual, mechanical

12–6 Restating earnings per share for stock dividends

2, 4 Conceptual, mechanical

12–7 Stock dividends and splits 4 Mechanical 12–8 Effect of stock dividends on stock

price 4 Conceptual, communication

12–9 Effects of transactions upon financial measurements

8 Analytical, conceptual

12–10 Effects of transactions upon earnings per share

2, 4 Conceptual, communication

12–11 Identifying source of desired financial information

1, 5, 8 Conceptual

12–12 Comprehensive income 7 Analytical 12–13 EPS and dividends 3, 5 Conceptual 12–14 Analysis of stock information 1, 8 Conceptual, mechanical, real—

Tootsie Roll

Problems

12–1 Reporting unusual events 1, 2 Conceptual, mechanical 12–2 Format of statements of income

and retained earnings 1, 2, 5, 6 Conceptual, mechanical

12–3 Reporting unusual events: a comprehensive problem

1, 2, 5, 6 Conceptual, mechanical

12–4 Stock splits, stock dividends, treasury stock, and book value

4 Mechanical, conceptual

12–5 Statement of stockholders’ equity 4, 8 Mechanical 12–6 Dividends and treasury stock

transactions 4 Conceptual, mechanical

12–7 Effects of transactions upon financial measurements

8 Analytical, conceptual, group, communication

12–8 Stockholders’ equity: comprehensive

4 Conceptual, mechanical

12–9 Format of an income statement

1, 2 Conceptual, mechanical

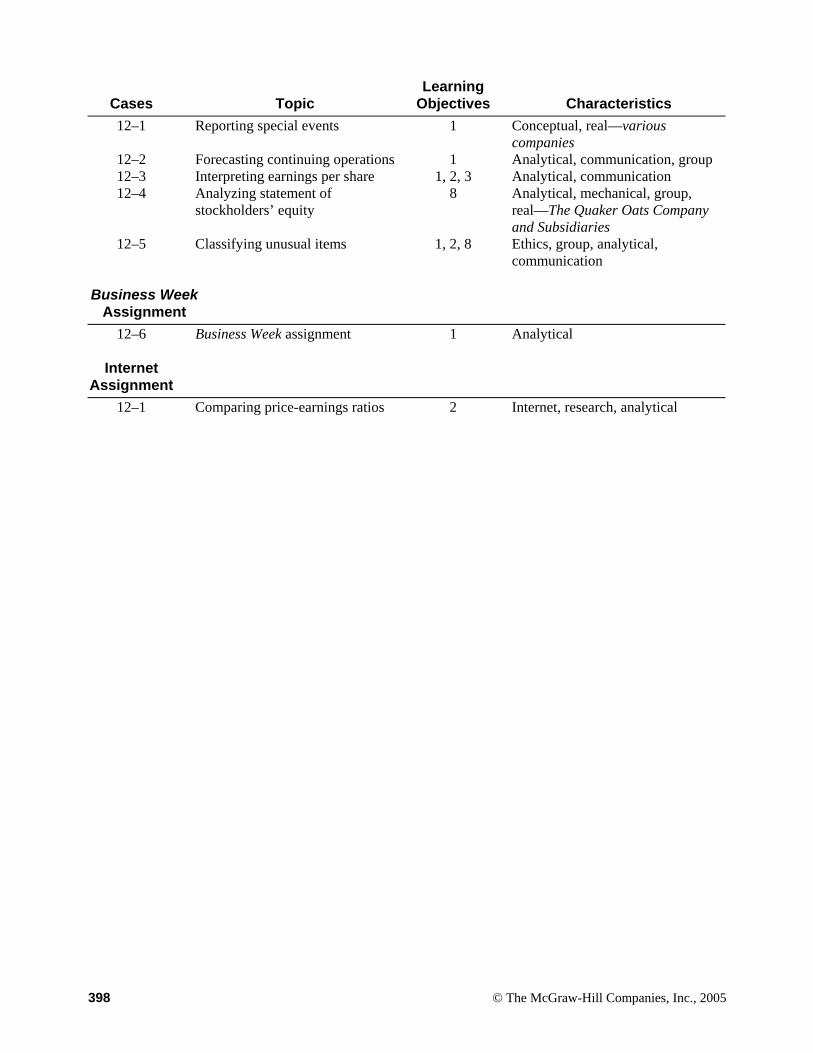

398 © The McGraw-Hill Companies, Inc., 2005

Cases

Topic

LearningObjectives

Characteristics

12–1 Reporting special events 1 Conceptual, real—various companies

12–2 Forecasting continuing operations 1 Analytical, communication, group 12–3 Interpreting earnings per share 1, 2, 3 Analytical, communication 12–4 Analyzing statement of

stockholders’ equity 8 Analytical, mechanical, group,

real—The Quaker Oats Company and Subsidiaries

12–5 Classifying unusual items

1, 2, 8 Ethics, group, analytical, communication

Business Week

Assignment

12–6 Business Week assignment 1 Analytical

Internet Assignment

12–1 Comparing price-earnings ratios 2 Internet, research, analytical

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 399

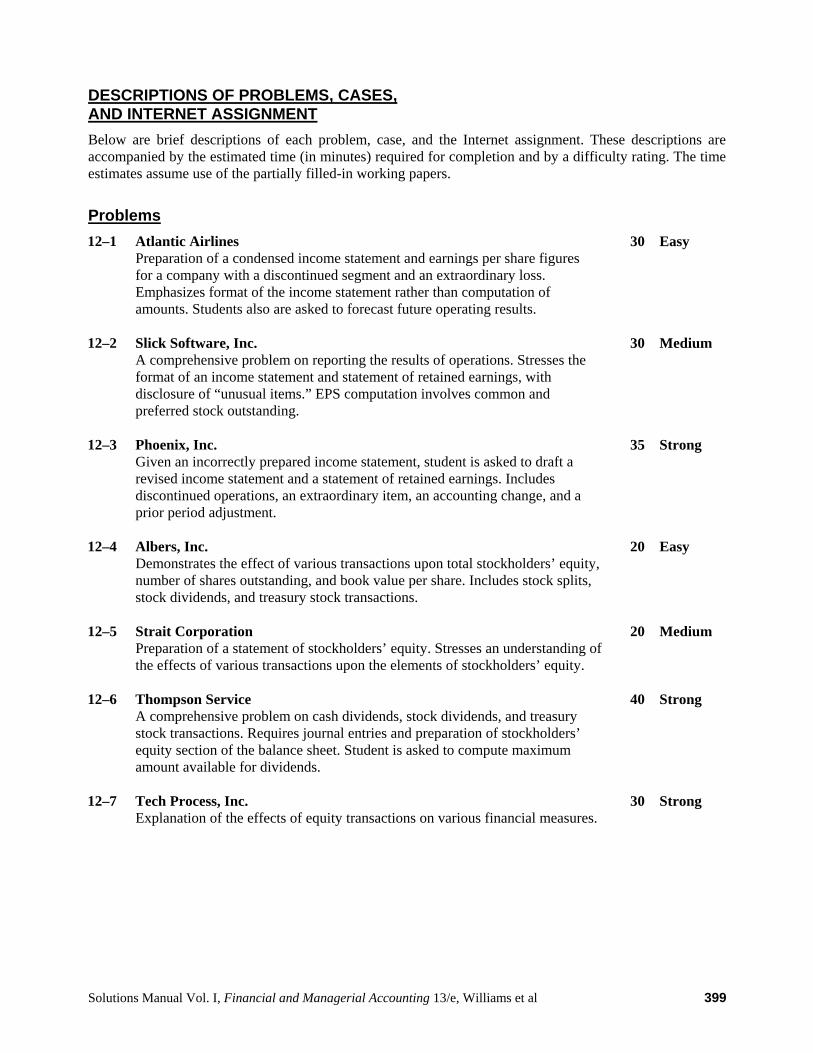

DESCRIPTIONS OF PROBLEMS, CASES, AND INTERNET ASSIGNMENT Below are brief descriptions of each problem, case, and the Internet assignment. These descriptions are accompanied by the estimated time (in minutes) required for completion and by a difficulty rating. The time estimates assume use of the partially filled-in working papers.

Problems 12–1 Atlantic Airlines

Preparation of a condensed income statement and earnings per share figures for a company with a discontinued segment and an extraordinary loss. Emphasizes format of the income statement rather than computation of amounts. Students also are asked to forecast future operating results.

30 Easy

12–2 Slick Software, Inc. A comprehensive problem on reporting the results of operations. Stresses the format of an income statement and statement of retained earnings, with disclosure of “unusual items.” EPS computation involves common and preferred stock outstanding.

30 Medium

12–3 Phoenix, Inc. Given an incorrectly prepared income statement, student is asked to draft a revised income statement and a statement of retained earnings. Includes discontinued operations, an extraordinary item, an accounting change, and a prior period adjustment.

35 Strong

12–4 Albers, Inc. Demonstrates the effect of various transactions upon total stockholders’ equity, number of shares outstanding, and book value per share. Includes stock splits, stock dividends, and treasury stock transactions.

20 Easy

12–5 Strait Corporation Preparation of a statement of stockholders’ equity. Stresses an understanding of the effects of various transactions upon the elements of stockholders’ equity.

20 Medium

12–6 Thompson Service A comprehensive problem on cash dividends, stock dividends, and treasury stock transactions. Requires journal entries and preparation of stockholders’ equity section of the balance sheet. Student is asked to compute maximum amount available for dividends.

40 Strong

12–7 Tech Process, Inc. Explanation of the effects of equity transactions on various financial measures.

30 Strong

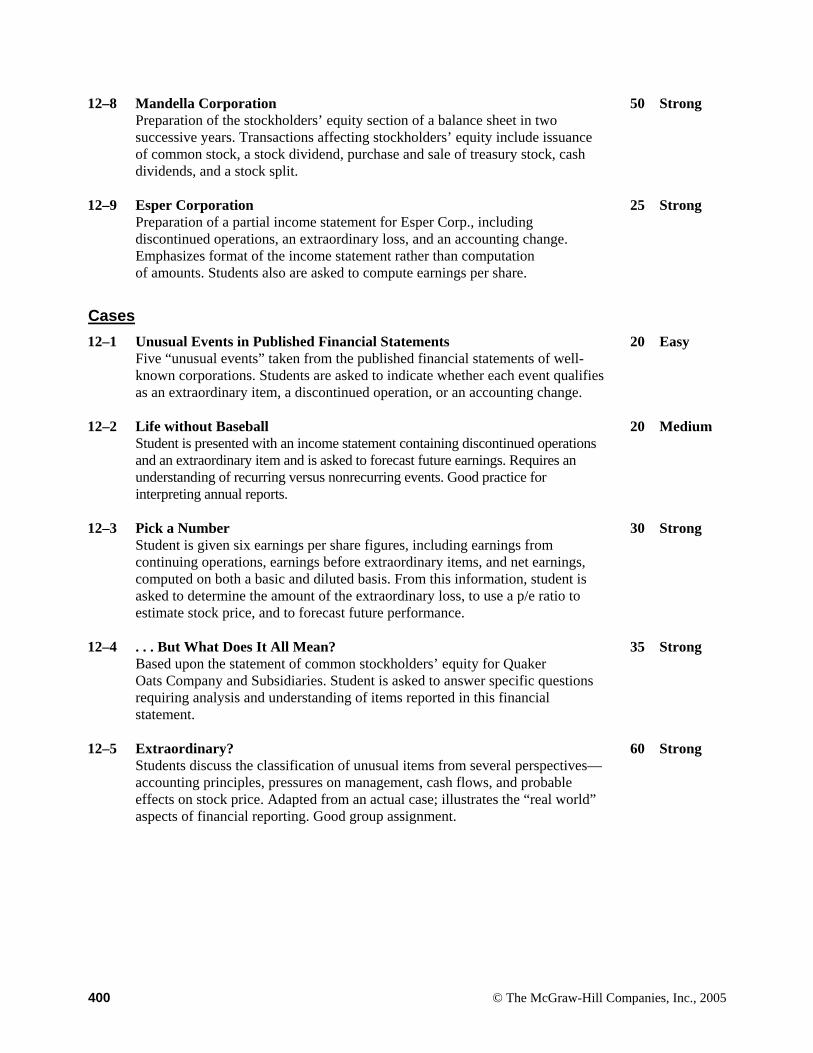

400 © The McGraw-Hill Companies, Inc., 2005

12–8 Mandella Corporation

Preparation of the stockholders’ equity section of a balance sheet in two successive years. Transactions affecting stockholders’ equity include issuance of common stock, a stock dividend, purchase and sale of treasury stock, cash dividends, and a stock split.

50 Strong

12–9 Esper Corporation Preparation of a partial income statement for Esper Corp., including discontinued operations, an extraordinary loss, and an accounting change. Emphasizes format of the income statement rather than computation of amounts. Students also are asked to compute earnings per share.

25 Strong

Cases 12–1 Unusual Events in Published Financial Statements

Five “unusual events” taken from the published financial statements of well-known corporations. Students are asked to indicate whether each event qualifies as an extraordinary item, a discontinued operation, or an accounting change.

20 Easy

12–2 Life without Baseball Student is presented with an income statement containing discontinued operations and an extraordinary item and is asked to forecast future earnings. Requires an understanding of recurring versus nonrecurring events. Good practice for interpreting annual reports.

20 Medium

12–3 Pick a Number Student is given six earnings per share figures, including earnings from continuing operations, earnings before extraordinary items, and net earnings, computed on both a basic and diluted basis. From this information, student is asked to determine the amount of the extraordinary loss, to use a p/e ratio to estimate stock price, and to forecast future performance.

30 Strong

12–4 . . . But What Does It All Mean? Based upon the statement of common stockholders’ equity for Quaker Oats Company and Subsidiaries. Student is asked to answer specific questions requiring analysis and understanding of items reported in this financial statement.

35 Strong

12–5 Extraordinary? Students discuss the classification of unusual items from several perspectives—accounting principles, pressures on management, cash flows, and probable effects on stock price. Adapted from an actual case; illustrates the “real world” aspects of financial reporting. Good group assignment.

60 Strong

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 401

Business Week Assignment 12–6 Business Week Assignment

Students are asked to consider the difficulty of defining events in a way that results in consistent financial reporting.

15 Medium

Internet Assignment 12–1 Price-Earnings Ratios

Students are to obtain information on the Internet about a Fortune 500 company and an emerging company. They are to compare p/e ratios and speculate on the reasons for the differences.

30 Easy

402 © The McGraw-Hill Companies, Inc., 2005

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS 1. The purpose of presenting subtotals such as Income from Continuing Operations and Income before

Extraordinary Items is to assist users of the income statement in making forecasts of future earnings. By excluding the operating results of discontinued operations and the effects of unusual and nonrecurring transactions, these subtotals indicate the amount of income derived from the company’s ongoing, normal operations.

2. The discontinued operations classification is used in the income statement only when a business discontinues an entire segment of its activities. Frank’s has two business segments—pizza parlors and the baseball team. Only if one of these segments is discontinued in its entirety will the company report discontinued operations. The sale or closure of a few parlors does not represent the disposal of the pizza parlor segment of the company’s business activities.

3. Extraordinary items are gains and losses that are unusual in nature and not expected to recur in the foreseeable future.

Separate line-item presentation should be made for items that are unusual in nature or infrequent in occurrence, but not both. While these items are disclosed separately via their separate presentation, a subtotal for income before and after them is not presented as is done for extraordinary items.

4. The restructuring charges should be combined and presented as a line item in the company’s income statement in determining operating income.

In predicting future earnings for the company, the charges generally should not be considered to be costs that will be incurred in the future. In fact, if the program of downsizing is successful, operating results in the future could be expected to improve as a result of having incurred the restructuring charges.

5. In determining the cumulative effect of a change in accounting principle, the income of prior periods is recomputed under the assumption that the new accounting principle has always been in use. The difference between this recomputed past income and the income actually reported represents the cumulative effect of the change on the income of prior periods and is reported as a separate item in the income statement.

A prior period adjustment represents a correction of an error in the amount of income reported in a prior period. Prior period adjustments are shown in the statement of retained earnings (or statement of stockholders’ equity) as an adjustment to the balance of retained earnings at the beginning of the period in which the error is identified.

6. The cumulative effect of an accounting change is the difference between the income reported in past years and the income that would have been reported had the new accounting method always been in use. King, Inc. had been using an accelerated depreciation method, and, therefore, reported more depreciation expense and lower net income than would have resulted from use of the straight-line method. The company will report this retroactive increase in the income of prior years as the cumulative effect of the accounting change. Thus, the change will increase the net income reported in the current year.

7. a. The current-year preferred dividend is deducted from net income to determine the earnings allocable to the common stockholders. (If the preferred stock is noncumulative, the preferred dividend is deducted only if declared; the preferred dividend on cumulative preferred stock is always deducted.)

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 403

b. The par value of all preferred stock outstanding and the amount of all dividends in arrears on

preferred stock are deducted from total stockholders’ equity to determine the aggregate book value allocable to the common stockholders.

8. No, the number of common shares used in computing earnings per share may be different from that used to determine book value per share. In computing earnings per share, earnings allocable to the common stockholders is divided by the weighted-average number of common shares outstanding throughout the period. In computing book value per share at a specified date, stockholders’ equity allocable to the common stockholders is divided by the number of common shares actually outstanding on that date. If the number of common shares outstanding has not changed during the period, the weighted-average number of common shares outstanding during the period will be equal to the number of common shares outstanding on a particular date.

9. a. The price-earnings ratio is computed by dividing the market price of a share of common stock by the annual earnings per share.

b. The amount of basic earnings per share is computed by dividing the net income available for common stock by the weighted-average number of common shares outstanding during the year.

c. The amount of diluted earnings per share is computed by dividing net income by the maximum potential number of shares outstanding after convertible securities are assumed to have been converted.

10. a. Shares used in computing basic earnings per share: Common shares outstanding throughout the year............................................................. 3,000,000

b. Shares used in computing diluted earnings per share: Common shares outstanding throughout the year............................................................. 3,000,000 Additional common shares that would exist if preferred stock had

been converted at the beginning of the year (150,000 × 2) ............................................ 300,000

Total shares used in diluted earnings computation ........................................................... 3,300,00011. The analyst should recognize the risk that the outstanding convertible securities may be converted into

additional shares of common stock, thereby diluting (reducing) basic earnings per share in future years. If any of the convertible securities are converted, basic earnings per share probably will increase at a slower rate than net income. In fact, if enough dilution occurs, basic earnings per share could actually decline while net income continues to increase.

12. Date of declaration is the day the obligation to pay a dividend comes into existence by action of the board of directors. Date of record is the day on which the particular stockholders who are entitled to receive a dividend is determined. Persons listed in the corporate records as owning stock on this day will receive the dividend. Date of payment is the day the dividend is distributed by the corporation. Ex-dividend date (usually three business days prior to the date of record) is the day on which the right to receive a recently declared dividend no longer attaches to shares of stock. As a result, the market price of the shares usually falls by the amount of the dividend.

13. The purpose of a stock dividend is to make a distribution of value to stockholders as a representation of the profitability of the company while, at the same time, conserving cash.

404 © The McGraw-Hill Companies, Inc., 2005

14. A stock split occurs when there is a relatively large increase in the number of shares issued without any

change in the total amount of stated capital (because the par value per share is reduced proportionately to the increase in the number of shares).

A stock dividend occurs when there is a relatively small increase in the number of shares issued, with no change in the net assets of the company but a transfer from retained earnings to the paid-in capital section of the balance sheet. The par value of stock remains the same.

The distinction in the accounting treatment of a stock dividend and a stock split stems directly from the difference in the effect on stated (legal) capital and retained earnings. There is no difference in the probable effect on per-share market price of a stock dividend and a stock split of equal size, although stock splits are usually much larger than stock dividends.

15. Prior period adjustments are entries made in the accounting records to correct material errors in the net income reported in prior years.

In the year in which a prior period adjustment is recorded, it should appear in the statement of retained earnings (or statement of stockholders’ equity) as an adjustment to the balance of retained earnings at the beginning of the year.

16. Three items that may be shown in a statement of retained earnings as causing changes in the balance of retained earnings are:

(1) Net income or net loss for the period (2) Dividends declared (both cash dividends and stock dividends) (3) Prior period adjustments 17. If the price of the stock declines in proportion to the distribution of shares in a stock dividend, at the

time of that distribution the stockholder does not benefit. He/she holds exactly the same percentage of the outstanding shares, and the value per share has declined in proportion to the increased number of shares. Often, however, the value does not drop in proportion to the increased number of shares, meaning that the recipient of the shares has an immediate benefit. For example, if an investor who held 2,000 shares of stock that had a market value of $10 each received a 10% stock dividend, and the market price only declined 5%, the following would result:

Market value before stock dividend: 2,000 shares @ $10 ............................................................................................................. $20,000 Market value after stock dividend: (2,000 shares × 110%) × ($10 × 95%)................................................................................. $20,900

The investor has benefited by $900. He/she could sell about 95 shares [$900/($10 × 95%)] at $9.50 and still have a stock investment equal to the value before the stock dividend, although the investor would own a smaller percentage of the company after the sale.

18. A liquidating dividend is a return of the investment made in the company to the investor, in contrast to a non-liquidating dividend which is a return on the investment in the company. A liquidating dividend occurs when dividends are distributed in excess of a company’s retained earnings.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 405

19. The student is right in one sense—both stock splits and stock dividends are distributions of a

company’s shares to existing stockholders with the company receiving no payment in return. The student is incorrect, however, in stating that the two are exactly the same. The primary difference is one of magnitude and, thus, the impact on market value. A stock dividend is usually relatively small—5% to 20% of the outstanding shares. A stock split, on the other hand, is usually some multiple of the number of outstanding shares, like a 2:1 split (100% increase) or a 3:1 split (200% increase). The market price reacts strongly to a distribution as large as a stock split while stock dividends are often unnoticed in the stock price.

20. The statement of retained earnings shows for the Retained Earnings account the beginning balance, changes in the account balance during the period, and the ending balance. A statement of stockholders’ equity provides the same information, but includes every category of stockholders’ equity account (including retained earnings). Therefore, a statement of stockholders’ equity may appropriately be described as an expanded statement of retained earnings.

406 © The McGraw-Hill Companies, Inc., 2005

SOLUTIONS TO EXERCISES

Ex. 12–1 a. 1,440 shares = [(200 × 2) × 120%] × 3 $17,280 = 1,440 × $12.

b. Since Smiley is a small and growing corporation, the board of directors probablydecided that cash from operations was needed to finance the company’s expanding operations.

c. You are probably better off because of the board’s decision not to declare cashdividends. Wiley was obviously able to invest the funds to earn a high rate of return, asevidenced by the value of your investment, which has grown from $1,000 to $17,280.

Ex. 12–2 a. Extraordinary item b. None (Treasury stock is not an asset; it represents shares that have been reacquired by

the company, not shares that have not yet been issued.) c. Stock dividend d. Additional paid-in capital e. Prior period adjustment f. P/e ratio (Market price divided by earnings per share.) g. Discontinued operations (Showing the discontinued operations in a separate section of

the income statement permits presentation of the subtotal, Income from Continuing Operations.)

h. Diluted earnings per share i. Comprehensive income

Ex. 12–3 a. SPORTS+, INC. Income Statement

For the Year Ended December 31, 20__ Net sales.............................................................................................................$12,500,000 Costs and expenses (including applicable income taxes) .............................. 8,600,000 Income from continuing operations ...............................................................$ 3,900,000 Discontinued operations: Operating loss from tennis shops (net of income tax

benefit) .....................................................................................

$192,000 Loss on sale of tennis shops (net of income tax benefit)......... 348,000 (540,000) Net income ........................................................................................................ $3,360,000

Earnings per share: Earnings from continuing operations ($3,900,000 ÷ 182,000 shares) ...... $21.43 Loss from discontinued operations ($540,000 ÷ 182,000) ......................... (2.97) Net earnings ($3,360,000 ÷ 182,000 shares) ............................................... $18.46

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 407

b. The $21.43 earnings per share figure from continuing operations (part a) is probably the most useful one for predicting future operating results for Sports+, Inc. Earningsper share from continuing operations represents the results of continuing and ordinary business activity, which is expected to continue in the future. Discontinued operationsand extraordinary items are not likely to recur in the future.

Ex. 12–4 a. GLOBAL EXPORTS Income Statement

For the Year Ended December 31, 20__ Net sales............................................................................................................... $ 7,750,000 Less: Costs and expenses (including income taxes)......................................... 6,200,000 Income before extraordinary items .................................................................. 1,550,000 Extraordinary gain, net of income taxes .......................................................... 420,000 Net income .......................................................................................................... $ 1,970,000

Earnings per share of common stock: Earnings before extraordinary items ($1,550,000 ÷ 910,000 shares)......... $1.70 Extraordinary gain ($420,000 ÷ 910,000 shares)......................................... .46 Net earnings ($1,970,000 ÷ 910,000 shares) ................................................. $2.16

b. The $1.70 earnings per share before extraordinary items is the figure used to computethe price-earnings ratio for Global Exports. If a company reports an extraordinarygain or loss, the price-earnings ratio is computed using the per-share earnings before the extraordinary item.

Ex. 12–5 a. 1. Net income (all applicable to common stock)............................................ $ 1,920,000 Shares of common stock outstanding throughout the year...................... 400,000 Earnings per share ($1,920,000 ÷ 400,000 shares).................................... $4.80

2. Net income.................................................................................................... $ 1,920,000 Less: Preferred stock dividend (100,000 × 8% × $100) ............................ 800,000 Earnings available for common stock........................................................ $ 1,120,000 Shares of common stock outstanding throughout the year...................... 300,000 Earnings per share ($1,120,000 ÷ 300,000 shares).................................... $3.73

b. The earnings per share figure computed in part a (2) is a basic EPS figure. Although the company has outstanding both common and preferred stock, the preferred stockmust be convertible into common stock in order to result in a diluted computation ofearnings per share. The potential conversion of preferred stock into common stock iswhat necessitates disclosure of diluted EPS. Because the preferred stock in this exerciseis not convertible, the EPS computation is basic.

408 © The McGraw-Hill Companies, Inc., 2005

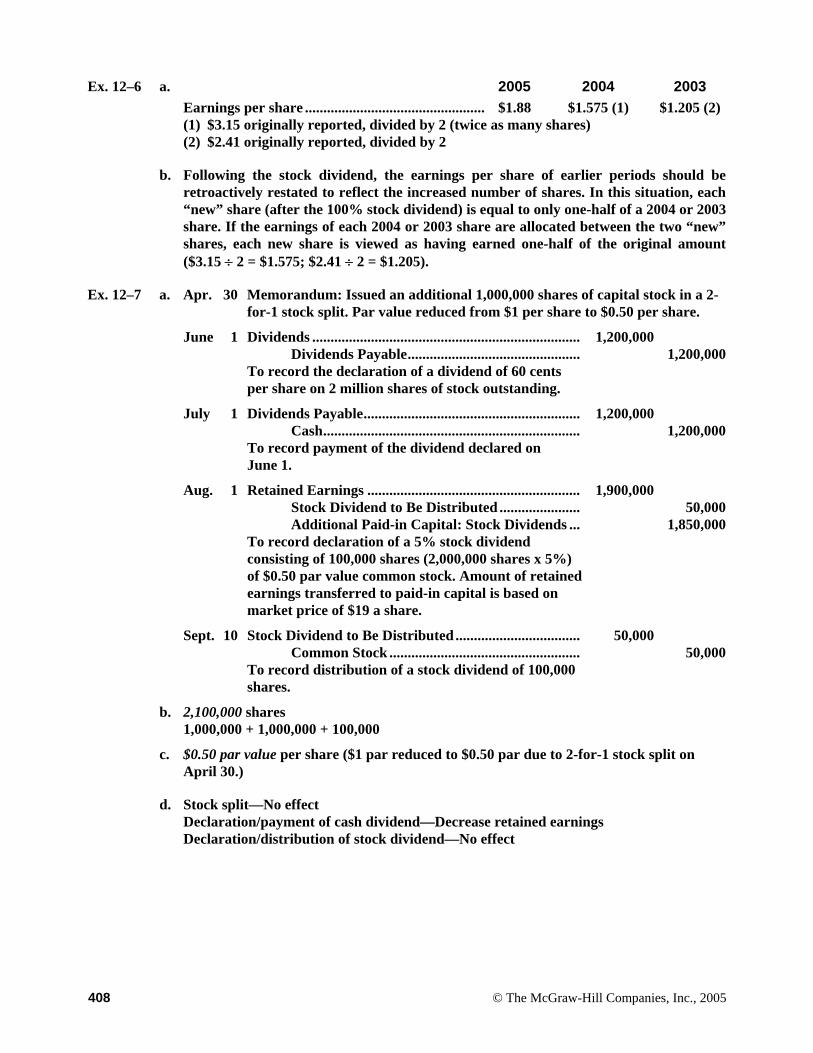

Ex. 12–6 a. 2005 2004 2003 Earnings per share ................................................. $1.88 $1.575 (1) $1.205 (2) (1) $3.15 originally reported, divided by 2 (twice as many shares) (2) $2.41 originally reported, divided by 2

b. Following the stock dividend, the earnings per share of earlier periods should beretroactively restated to reflect the increased number of shares. In this situation, each“new” share (after the 100% stock dividend) is equal to only one-half of a 2004 or 2003 share. If the earnings of each 2004 or 2003 share are allocated between the two “new”shares, each new share is viewed as having earned one-half of the original amount ($3.15 ÷ 2 = $1.575; $2.41 ÷ 2 = $1.205).

Ex. 12–7 a. Apr. 30 Memorandum: Issued an additional 1,000,000 shares of capital stock in a 2-for-1 stock split. Par value reduced from $1 per share to $0.50 per share.

June 1 Dividends ......................................................................... 1,200,000 Dividends Payable............................................... 1,200,000 To record the declaration of a dividend of 60 cents

per share on 2 million shares of stock outstanding.

July 1 Dividends Payable........................................................... 1,200,000 Cash...................................................................... 1,200,000 To record payment of the dividend declared on

June 1.

Aug. 1 Retained Earnings .......................................................... 1,900,000 Stock Dividend to Be Distributed ...................... 50,000 Additional Paid-in Capital: Stock Dividends ... 1,850,000 To record declaration of a 5% stock dividend

consisting of 100,000 shares (2,000,000 shares x 5%) of $0.50 par value common stock. Amount of retained earnings transferred to paid-in capital is based on market price of $19 a share.

Sept. 10 Stock Dividend to Be Distributed .................................. 50,000 Common Stock .................................................... 50,000 To record distribution of a stock dividend of 100,000

shares.

b. 2,100,000 shares 1,000,000 + 1,000,000 + 100,000

c. $0.50 par value per share ($1 par reduced to $0.50 par due to 2-for-1 stock split on April 30.)

d. Stock split—No effect Declaration/payment of cash dividend—Decrease retained earnings Declaration/distribution of stock dividend—No effect

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 409

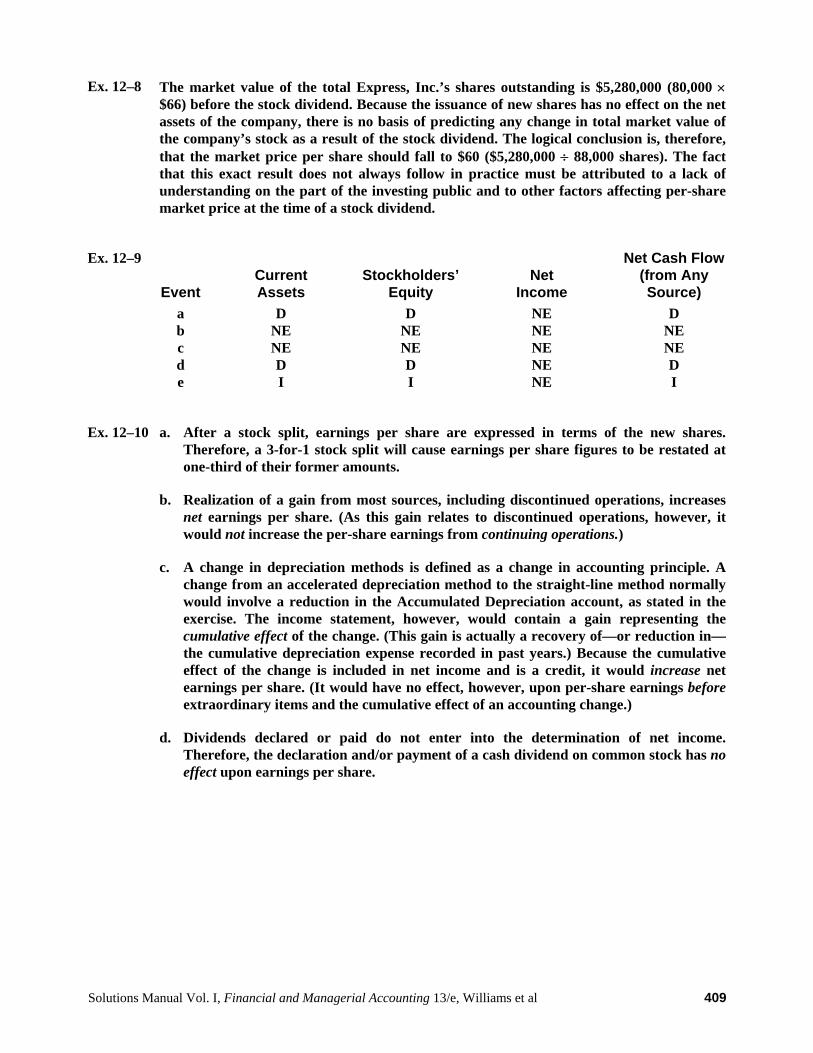

Ex. 12–8 The market value of the total Express, Inc.’s shares outstanding is $5,280,000 (80,000 ×$66) before the stock dividend. Because the issuance of new shares has no effect on the netassets of the company, there is no basis of predicting any change in total market value ofthe company’s stock as a result of the stock dividend. The logical conclusion is, therefore,that the market price per share should fall to $60 ($5,280,000 ÷ 88,000 shares). The fact that this exact result does not always follow in practice must be attributed to a lack ofunderstanding on the part of the investing public and to other factors affecting per-sharemarket price at the time of a stock dividend.

Ex. 12–9

Event

Current Assets

Stockholders’

Equity

Net

Income

Net Cash Flow(from Any Source)

a b c d e

D NE NE D I

D NE NE D I

NE NE NE NE NE

D NE NE D I

Ex. 12–10

a.

After a stock split, earnings per share are expressed in terms of the new shares.Therefore, a 3-for-1 stock split will cause earnings per share figures to be restated atone-third of their former amounts.

b. Realization of a gain from most sources, including discontinued operations, increases net earnings per share. (As this gain relates to discontinued operations, however, itwould not increase the per-share earnings from continuing operations.)

c. A change in depreciation methods is defined as a change in accounting principle. A change from an accelerated depreciation method to the straight-line method normally would involve a reduction in the Accumulated Depreciation account, as stated in theexercise. The income statement, however, would contain a gain representing thecumulative effect of the change. (This gain is actually a recovery of—or reduction in—the cumulative depreciation expense recorded in past years.) Because the cumulativeeffect of the change is included in net income and is a credit, it would increase netearnings per share. (It would have no effect, however, upon per-share earnings beforeextraordinary items and the cumulative effect of an accounting change.)

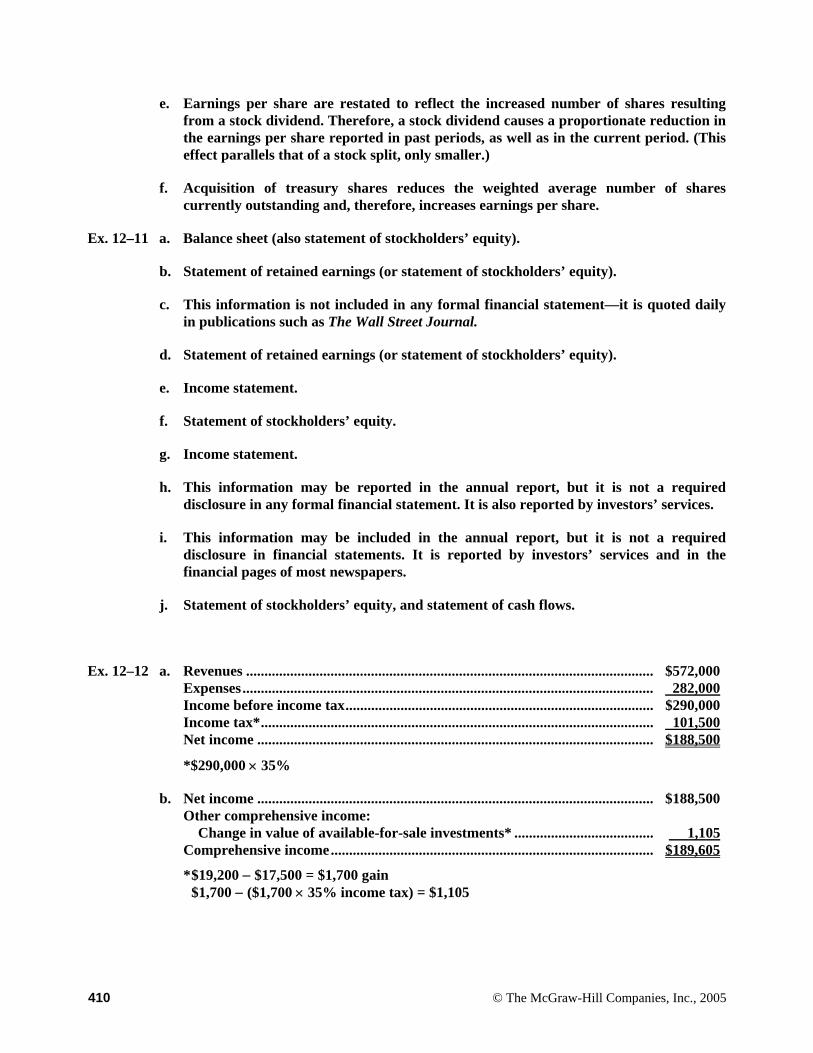

d. Dividends declared or paid do not enter into the determination of net income.Therefore, the declaration and/or payment of a cash dividend on common stock has no effect upon earnings per share.

410 © The McGraw-Hill Companies, Inc., 2005

e. Earnings per share are restated to reflect the increased number of shares resulting

from a stock dividend. Therefore, a stock dividend causes a proportionate reduction in the earnings per share reported in past periods, as well as in the current period. (Thiseffect parallels that of a stock split, only smaller.)

f. Acquisition of treasury shares reduces the weighted average number of sharescurrently outstanding and, therefore, increases earnings per share.

Ex. 12–11 a. Balance sheet (also statement of stockholders’ equity).

b. Statement of retained earnings (or statement of stockholders’ equity).

c. This information is not included in any formal financial statement—it is quoted daily in publications such as The Wall Street Journal.

d. Statement of retained earnings (or statement of stockholders’ equity).

e. Income statement.

f. Statement of stockholders’ equity.

g. Income statement.

h. This information may be reported in the annual report, but it is not a requireddisclosure in any formal financial statement. It is also reported by investors’ services.

i. This information may be included in the annual report, but it is not a required disclosure in financial statements. It is reported by investors’ services and in thefinancial pages of most newspapers.

j. Statement of stockholders’ equity, and statement of cash flows.

Ex. 12–12 a. Revenues ............................................................................................................... $572,000 Expenses................................................................................................................ 282,000 Income before income tax.................................................................................... $290,000 Income tax*........................................................................................................... 101,500 Net income ............................................................................................................ $188,500

*$290,000 × 35%

b. Net income ............................................................................................................ $188,500 Other comprehensive income: Change in value of available-for-sale investments* ...................................... 1,105 Comprehensive income........................................................................................ $189,605

* $19,200 − $17,500 = $1,700 gain $1,700 − ($1,700 × 35% income tax) = $1,105

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 411

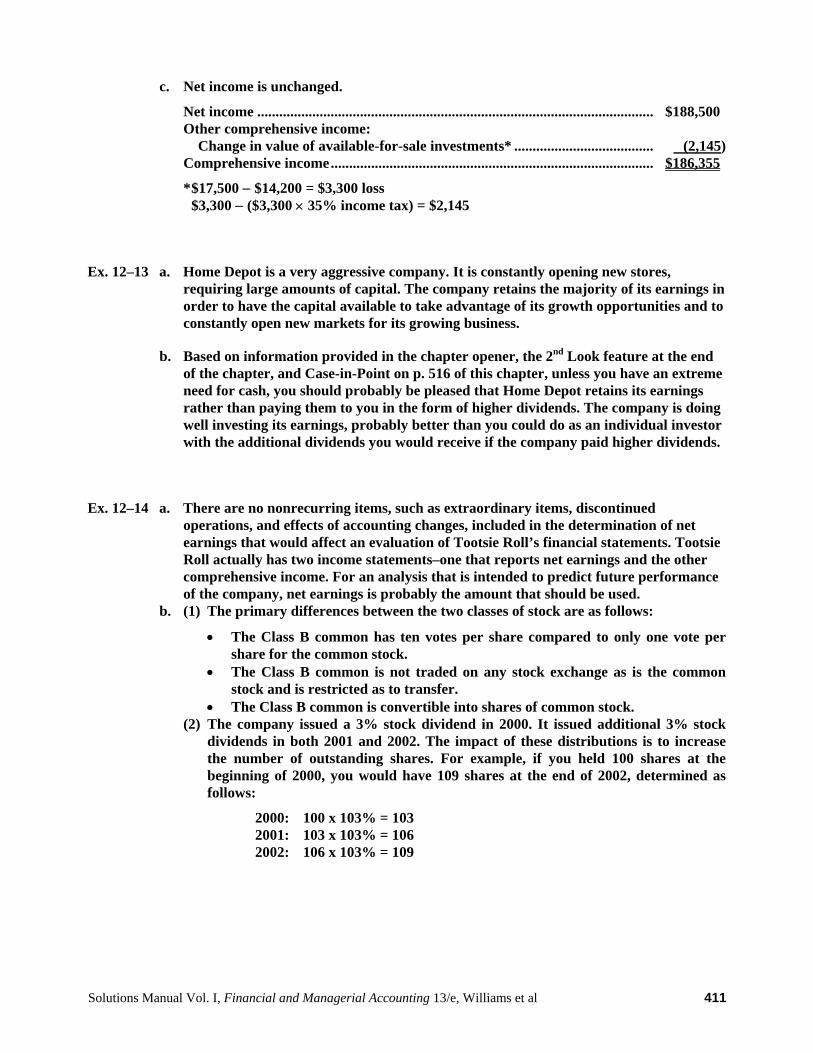

c. Net income is unchanged.

Net income ............................................................................................................ $188,500 Other comprehensive income: Change in value of available-for-sale investments* ...................................... (2,145) Comprehensive income........................................................................................ $186,355

* $17,500 − $14,200 = $3,300 loss $3,300 − ($3,300 × 35% income tax) = $2,145

Ex. 12–13 a. Home Depot is a very aggressive company. It is constantly opening new stores, requiring large amounts of capital. The company retains the majority of its earnings in order to have the capital available to take advantage of its growth opportunities and to constantly open new markets for its growing business.

b. Based on information provided in the chapter opener, the 2nd Look feature at the end of the chapter, and Case-in-Point on p. 516 of this chapter, unless you have an extreme need for cash, you should probably be pleased that Home Depot retains its earnings rather than paying them to you in the form of higher dividends. The company is doing well investing its earnings, probably better than you could do as an individual investor with the additional dividends you would receive if the company paid higher dividends.

Ex. 12–14 a. There are no nonrecurring items, such as extraordinary items, discontinued operations, and effects of accounting changes, included in the determination of net earnings that would affect an evaluation of Tootsie Roll’s financial statements. Tootsie Roll actually has two income statements–one that reports net earnings and the other comprehensive income. For an analysis that is intended to predict future performance of the company, net earnings is probably the amount that should be used.

b. (1) The primary differences between the two classes of stock are as follows:

• The Class B common has ten votes per share compared to only one vote pershare for the common stock.

• The Class B common is not traded on any stock exchange as is the commonstock and is restricted as to transfer.

• The Class B common is convertible into shares of common stock. (2) The company issued a 3% stock dividend in 2000. It issued additional 3% stock

dividends in both 2001 and 2002. The impact of these distributions is to increasethe number of outstanding shares. For example, if you held 100 shares at the beginning of 2000, you would have 109 shares at the end of 2002, determined asfollows:

2000: 100 x 103% = 103 2001: 103 x 103% = 106 2002: 106 x 103% = 109

412 © The McGraw-Hill Companies, Inc., 2005

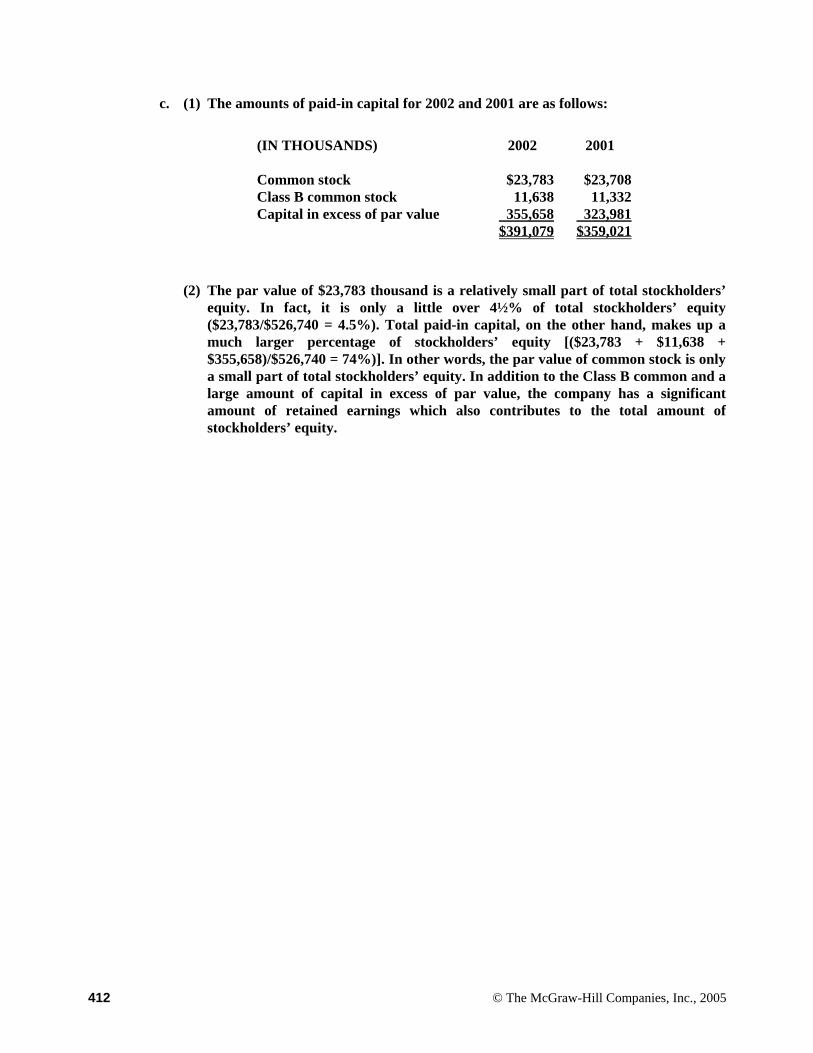

c. (1) The amounts of paid-in capital for 2002 and 2001 are as follows:

(IN THOUSANDS) 2002 2001 Common stock $23,783 $23,708 Class B common stock 11,638 11,332 Capital in excess of par value 355,658 323,981 $391,079 $359,021

(2) The par value of $23,783 thousand is a relatively small part of total stockholders’

equity. In fact, it is only a little over 4½% of total stockholders’ equity($23,783/$526,740 = 4.5%). Total paid-in capital, on the other hand, makes up a much larger percentage of stockholders’ equity [($23,783 + $11,638 + $355,658)/$526,740 = 74%)]. In other words, the par value of common stock is onlya small part of total stockholders’ equity. In addition to the Class B common and alarge amount of capital in excess of par value, the company has a significantamount of retained earnings which also contributes to the total amount ofstockholders’ equity.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 413

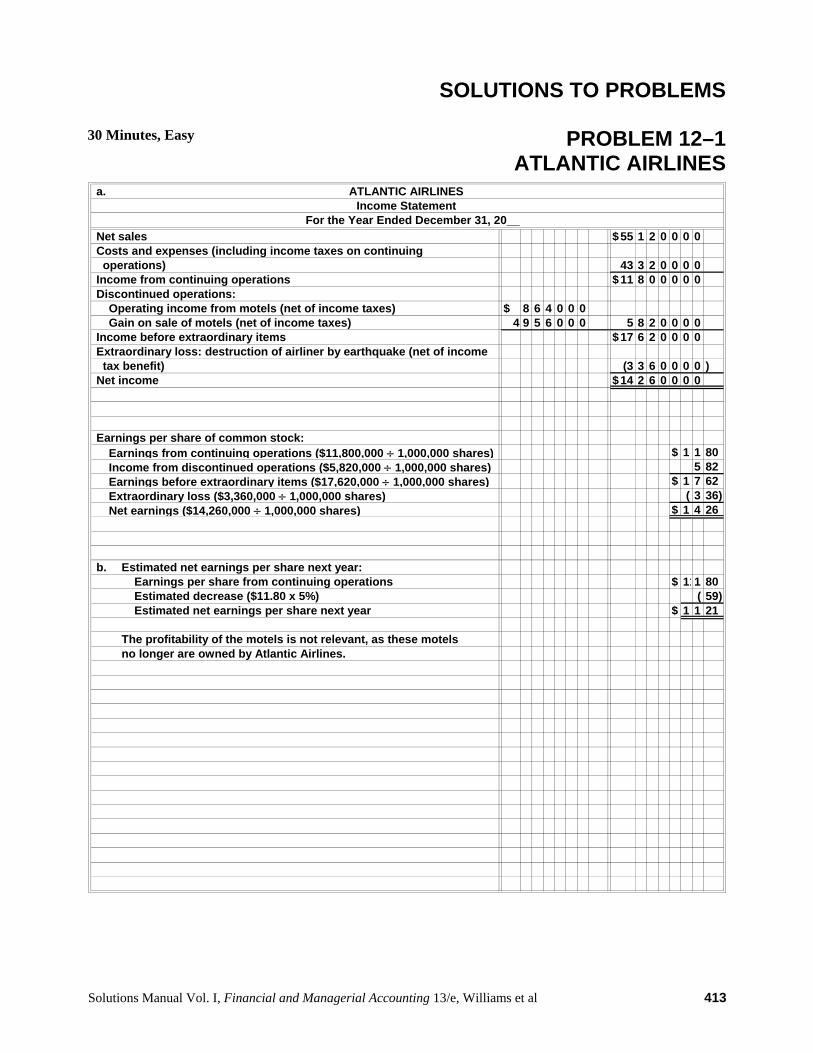

SOLUTIONS TO PROBLEMS

30 Minutes, Easy PROBLEM 12–1ATLANTIC AIRLINES

a. ATLANTIC AIRLINESIncome Statement

For the Year Ended December 31, 20__ Net sales $55 1 2 0 0 0 0 Costs and expenses (including income taxes on continuing operations) 43 3 2 0 0 0 0 Income from continuing operations $11 8 0 0 0 0 0 Discontinued operations:

Operating income from motels (net of income taxes) $ 8 6 4 0 0 0Gain on sale of motels (net of income taxes) 4 9 5 6 0 0 0 5 8 2 0 0 0 0

Income before extraordinary items $17 6 2 0 0 0 0 Extraordinary loss: destruction of airliner by earthquake (net of income tax benefit) (3 3 6 0 0 0 0 ) Net income $14 2 6 0 0 0 0

Earnings per share of common stock:Earnings from continuing operations ($11,800,000 ÷ 1,000,000 shares) $ 1 1 80Income from discontinued operations ($5,820,000 ÷ 1,000,000 shares) 5 82Earnings before extraordinary items ($17,620,000 ÷ 1,000,000 shares) $ 1 7 62Extraordinary loss ($3,360,000 ÷ 1,000,000 shares) ( 3 36)Net earnings ($14,260,000 ÷ 1,000,000 shares) $ 1 4 26

b. Estimated net earnings per share next year:Earnings per share from continuing operations $ 111 80Estimated decrease ($11.80 x 5%) ( 59)Estimated net earnings per share next year $ 1 1 21

The profitability of the motels is not relevant, as these motelsno longer are owned by Atlantic Airlines.

414 © The McGraw-Hill Companies, Inc., 2005

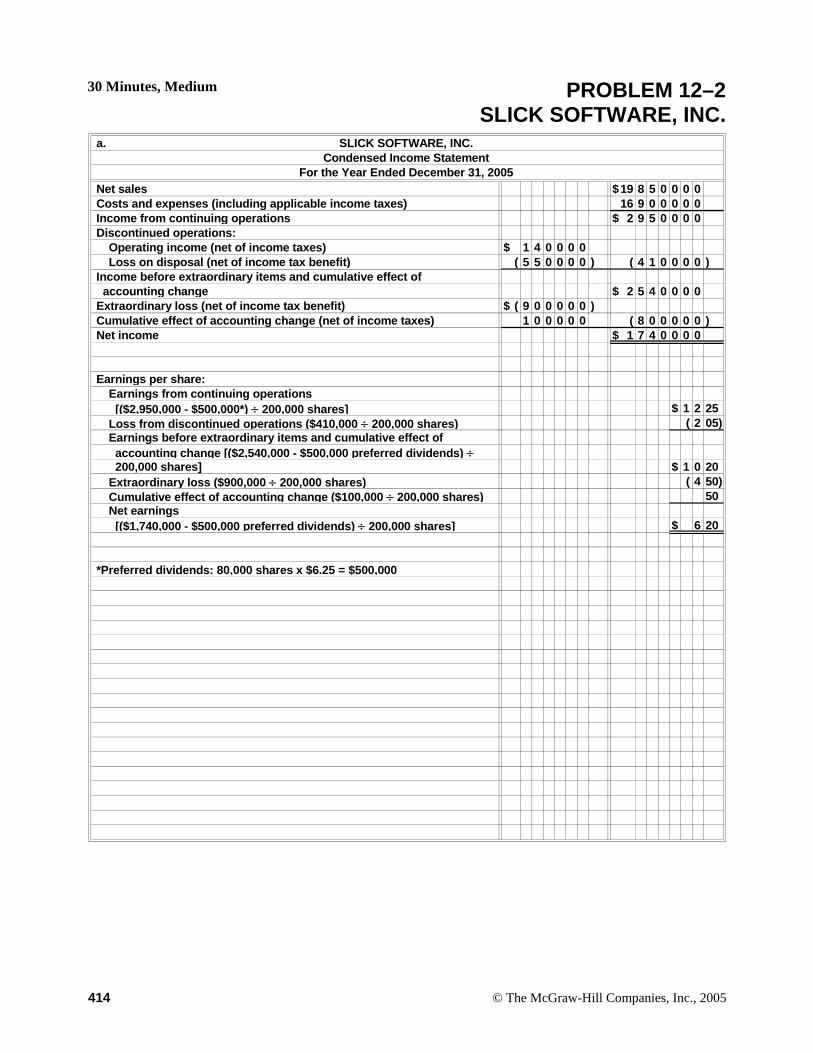

30 Minutes, Medium PROBLEM 12–2SLICK SOFTWARE, INC.

a. SLICK SOFTWARE, INC.Condensed Income Statement

For the Year Ended December 31, 2005 Net sales $19 8 5 0 0 0 0 Costs and expenses (including applicable income taxes) 16 9 0 0 0 0 0 Income from continuing operations $ 2 9 5 0 0 0 0 Discontinued operations:

Operating income (net of income taxes) $ 1 4 0 0 0 0Loss on disposal (net of income tax benefit) ( 5 5 0 0 0 0 ) ( 4 1 0 0 0 0 )

Income before extraordinary items and cumulative effect of accounting change $ 2 5 4 0 0 0 0 Extraordinary loss (net of income tax benefit) $ ( 9 0 0 0 0 0 ) Cumulative effect of accounting change (net of income taxes) 1 0 0 0 0 0 ( 8 0 0 0 0 0 ) Net income $ 1 7 4 0 0 0 0

Earnings per share:Earnings from continuing operations [($2,950,000 - $500,000*) ÷ 200,000 shares] $ 1 2 25Loss from discontinued operations ($410,000 ÷ 200,000 shares) ( 2 05)Earnings before extraordinary items and cumulative effect of accounting change [($2,540,000 - $500,000 preferred dividends) ÷ 200,000 shares] $ 1 0 20Extraordinary loss ($900,000 ÷ 200,000 shares) ( 4 50)Cumulative effect of accounting change ($100,000 ÷ 200,000 shares) 50Net earnings [($1,740,000 - $500,000 preferred dividends) ÷ 200,000 shares] $ 6 20

*Preferred dividends: 80,000 shares x $6.25 = $500,000

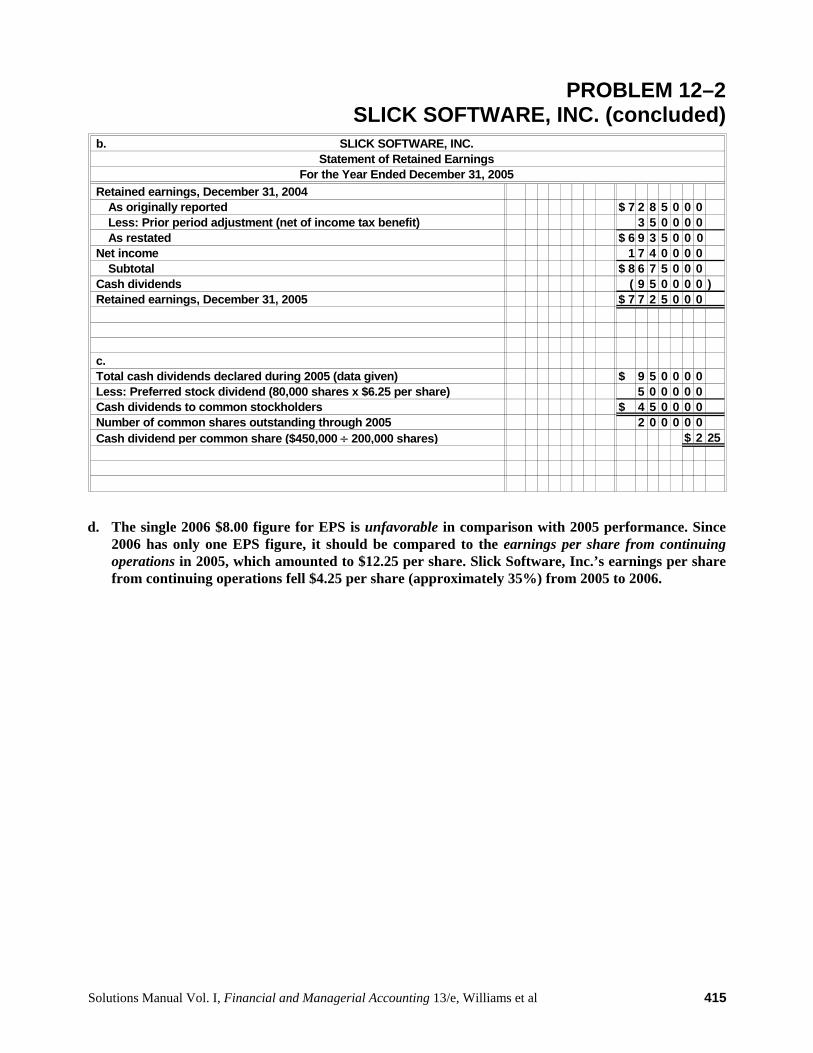

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 415

PROBLEM 12–2SLICK SOFTWARE, INC. (concluded)

b. SLICK SOFTWARE, INC.Statement of Retained Earnings

For the Year Ended December 31, 2005 Retained earnings, December 31, 2004

As originally reported $ 7 2 8 5 0 0 0Less: Prior period adjustment (net of income tax benefit) 3 5 0 0 0 0As restated $ 6 9 3 5 0 0 0

Net income 1 7 4 0 0 0 0Subtotal $ 8 6 7 5 0 0 0

Cash dividends ( 9 5 0 0 0 0 ) Retained earnings, December 31, 2005 $ 7 7 2 5 0 0 0

c. Total cash dividends declared during 2005 (data given) $ 9 5 0 0 0 0 Less: Preferred stock dividend (80,000 shares x $6.25 per share) 5 0 0 0 0 0 Cash dividends to common stockholders $ 4 5 0 0 0 0 Number of common shares outstanding through 2005 2 0 0 0 0 0 Cash dividend per common share ($450,000 ÷ 200,000 shares) $ 2 25

d. The single 2006 $8.00 figure for EPS is unfavorable in comparison with 2005 performance. Since

2006 has only one EPS figure, it should be compared to the earnings per share from continuing operations in 2005, which amounted to $12.25 per share. Slick Software, Inc.’s earnings per sharefrom continuing operations fell $4.25 per share (approximately 35%) from 2005 to 2006.

416 © The McGraw-Hill Companies, Inc., 2005

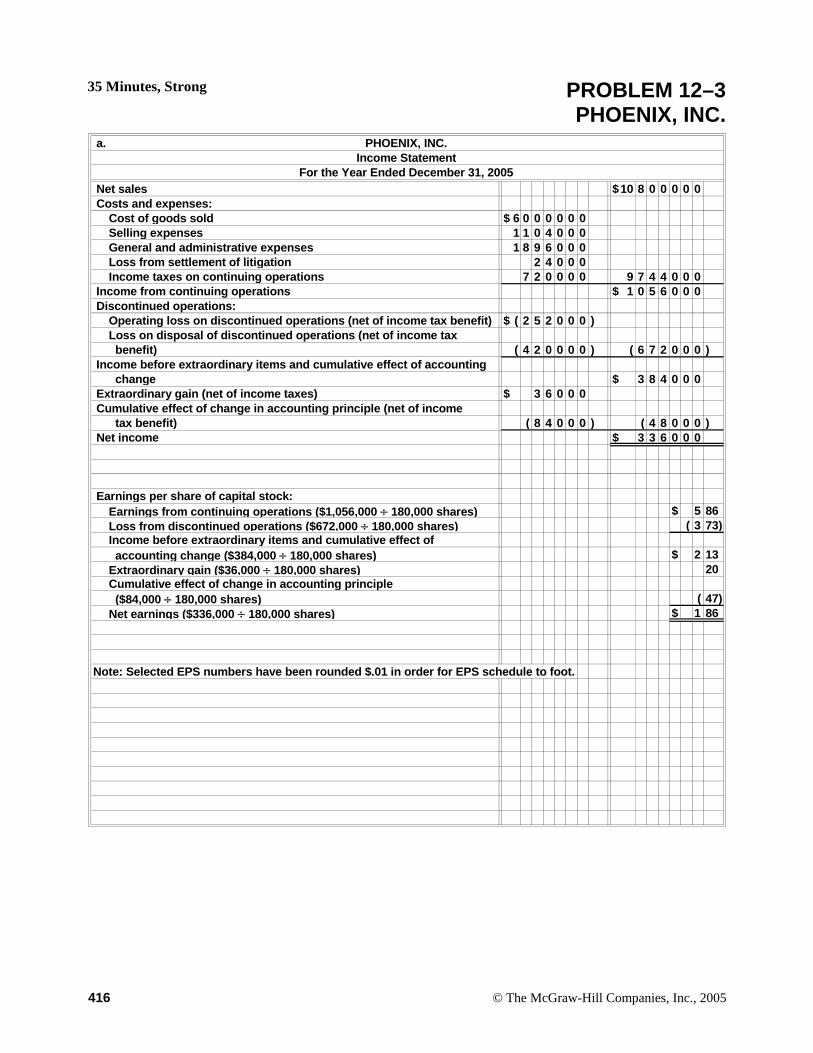

35 Minutes, Strong PROBLEM 12–3PHOENIX, INC.

a. PHOENIX, INC.Income Statement

For the Year Ended December 31, 2005 Net sales $10 8 0 0 0 0 0 Costs and expenses:

Cost of goods sold $ 6 0 0 0 0 0 0Selling expenses 1 1 0 4 0 0 0General and administrative expenses 1 8 9 6 0 0 0Loss from settlement of litigation 2 4 0 0 0Income taxes on continuing operations 7 2 0 0 0 0 9 7 4 4 0 0 0

Income from continuing operations $ 1 0 5 6 0 0 0 Discontinued operations:

Operating loss on discontinued operations (net of income tax benefit) $ ( 2 5 2 0 0 0 )Loss on disposal of discontinued operations (net of income tax benefit) ( 4 2 0 0 0 0 ) ( 6 7 2 0 0 0 )

Income before extraordinary items and cumulative effect of accounting change $ 3 8 4 0 0 0

Extraordinary gain (net of income taxes) $ 3 6 0 0 0 Cumulative effect of change in accounting principle (net of income

tax benefit) ( 8 4 0 0 0 ) ( 4 8 0 0 0 ) Net income $ 3 3 6 0 0 0

Earnings per share of capital stock:Earnings from continuing operations ($1,056,000 ÷ 180,000 shares) $ 5 86Loss from discontinued operations ($672,000 ÷ 180,000 shares) ( 3 73)Income before extraordinary items and cumulative effect of accounting change ($384,000 ÷ 180,000 shares) $ 2 13Extraordinary gain ($36,000 ÷ 180,000 shares) 20Cumulative effect of change in accounting principle ($84,000 ÷ 180,000 shares) ( 47)Net earnings ($336,000 ÷ 180,000 shares) $ 1 86

Note: Selected EPS numbers have been rounded $.01 in order for EPS schedule to foot.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 417

PROBLEM 12–3PHOENIX, INC. (concluded)

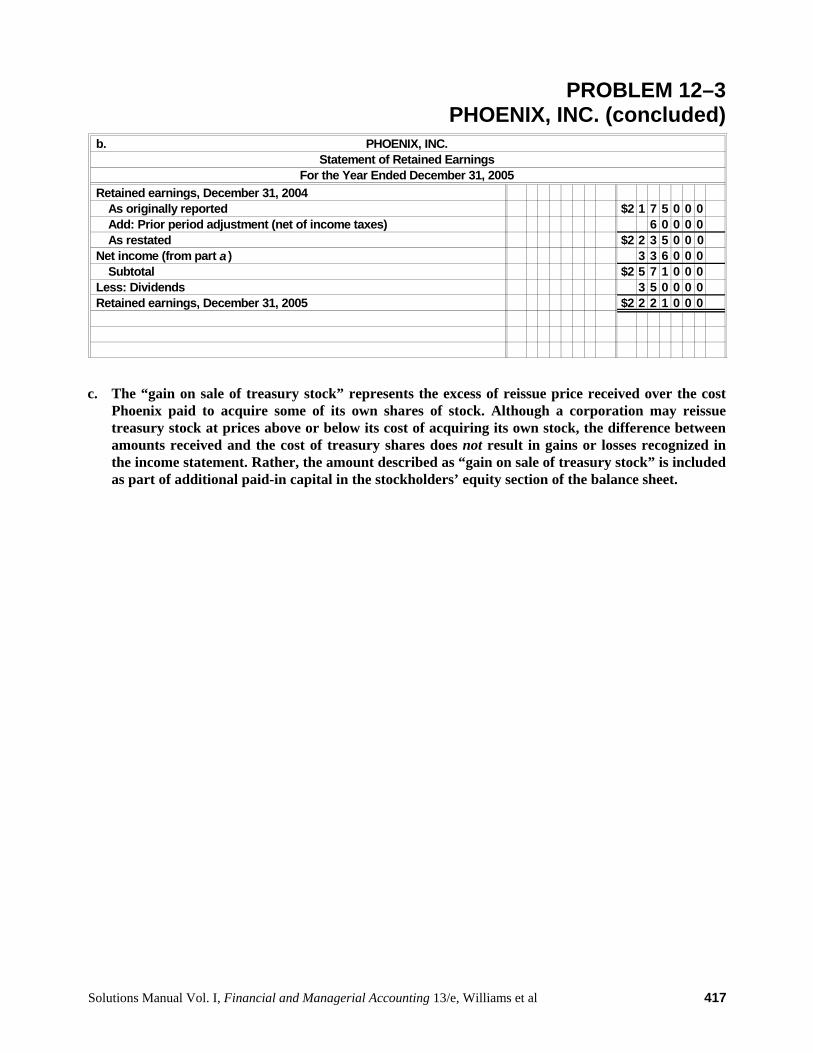

b. PHOENIX, INC.Statement of Retained Earnings

For the Year Ended December 31, 2005 Retained earnings, December 31, 2004

As originally reported $2 1 7 5 0 0 0Add: Prior period adjustment (net of income taxes) 6 0 0 0 0As restated $2 2 3 5 0 0 0

Net income (from part a ) 3 3 6 0 0 0 Subtotal $2 5 7 1 0 0 0 Less: Dividends 3 5 0 0 0 0 Retained earnings, December 31, 2005 $2 2 2 1 0 0 0

c. The “gain on sale of treasury stock” represents the excess of reissue price received over the cost

Phoenix paid to acquire some of its own shares of stock. Although a corporation may reissue treasury stock at prices above or below its cost of acquiring its own stock, the difference betweenamounts received and the cost of treasury shares does not result in gains or losses recognized in the income statement. Rather, the amount described as “gain on sale of treasury stock” is includedas part of additional paid-in capital in the stockholders’ equity section of the balance sheet.

418 © The McGraw-Hill Companies, Inc., 2005

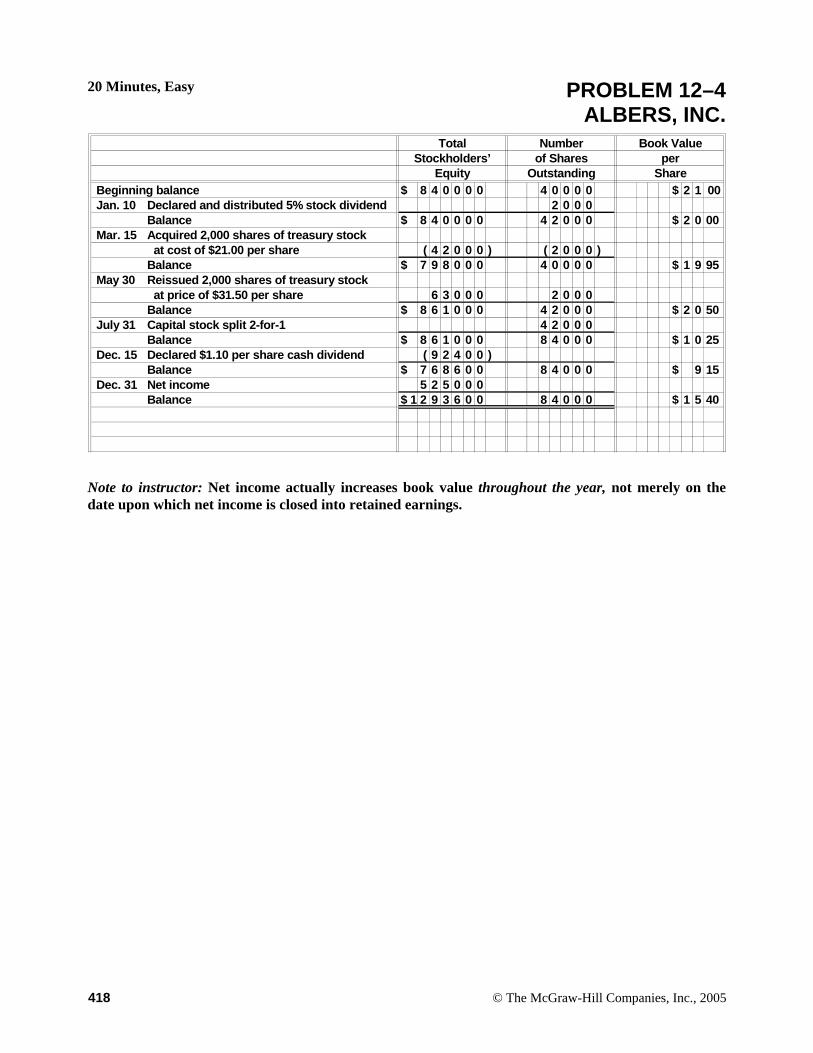

20 Minutes, Easy PROBLEM 12–4ALBERS, INC.

Total Number Book ValueStockholders’ of Shares per

Equity Outstanding Share Beginning balance $ 8 4 0 0 0 0 4 0 0 0 0 $ 2 1 00 Jan. 10 Declared and distributed 5% stock dividend 2 0 0 0

Balance $ 8 4 0 0 0 0 4 2 0 0 0 $ 2 0 00 Mar. 15 Acquired 2,000 shares of treasury stock

at cost of $21.00 per share ( 4 2 0 0 0 ) ( 2 0 0 0 )Balance $ 7 9 8 0 0 0 4 0 0 0 0 $ 1 9 95

May 30 Reissued 2,000 shares of treasury stock at price of $31.50 per share 6 3 0 0 0 2 0 0 0Balance $ 8 6 1 0 0 0 4 2 0 0 0 $ 2 0 50

July 31 Capital stock split 2-for-1 4 2 0 0 0Balance $ 8 6 1 0 0 0 8 4 0 0 0 $ 1 0 25

Dec. 15 Declared $1.10 per share cash dividend ( 9 2 4 0 0 )Balance $ 7 6 8 6 0 0 8 4 0 0 0 $ 9 15

Dec. 31 Net income 5 2 5 0 0 0Balance $ 1 2 9 3 6 0 0 8 4 0 0 0 $ 1 5 40

Note to instructor: Net income actually increases book value throughout the year, not merely on the date upon which net income is closed into retained earnings.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al

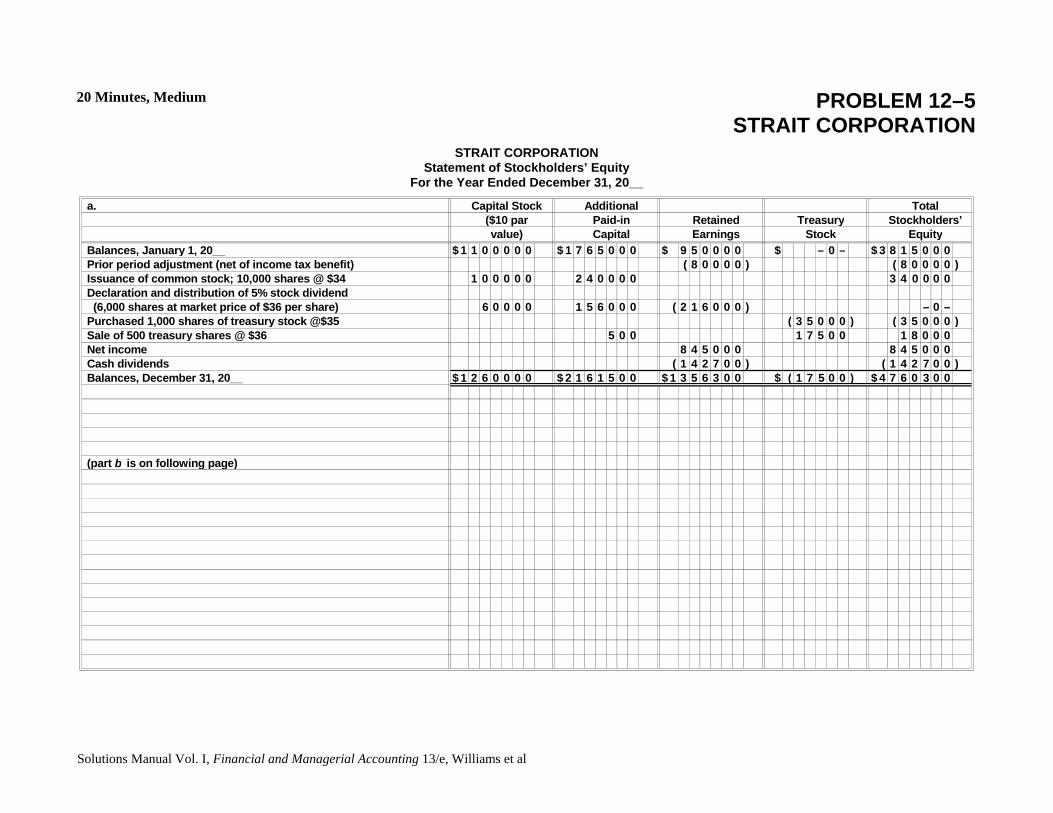

20 Minutes, Medium PROBLEM 12–5STRAIT CORPORATION

STRAIT CORPORATION Statement of Stockholders’ Equity

For the Year Ended December 31, 20__

a. Capital Stock Additional Total($10 par Paid-in Retained Treasury Stockholders’value) Capital Earnings Stock Equity

Balances, January 1, 20__ $ 1 1 0 0 0 0 0 $ 1 7 6 5 0 0 0 $ 9 5 0 0 0 0 $ – 0 – $ 3 8 1 5 0 0 0 Prior period adjustment (net of income tax benefit) ( 8 0 0 0 0 ) ( 8 0 0 0 0 ) Issuance of common stock; 10,000 shares @ $34 1 0 0 0 0 0 2 4 0 0 0 0 3 4 0 0 0 0 Declaration and distribution of 5% stock dividend (6,000 shares at market price of $36 per share) 6 0 0 0 0 1 5 6 0 0 0 ( 2 1 6 0 0 0 ) – 0 – Purchased 1,000 shares of treasury stock @$35 ( 3 5 0 0 0 ) ( 3 5 0 0 0 ) Sale of 500 treasury shares @ $36 5 0 0 1 7 5 0 0 1 8 0 0 0 Net income 8 4 5 0 0 0 8 4 5 0 0 0 Cash dividends ( 1 4 2 7 0 0 ) ( 1 4 2 7 0 0 ) Balances, December 31, 20__ $ 1 2 6 0 0 0 0 $ 2 1 6 1 5 0 0 $ 1 3 5 6 3 0 0 $ ( 1 7 5 0 0 ) $ 4 7 6 0 3 0 0

(part b is on following page)

420 © The McGraw-Hill Companies, Inc., 2005

PROBLEM 12–5STRAIT CORPORATION (concluded)

b. Declaration/distribution of a 5% stock dividend has no effect on total stockholders’ equity.Declaration of a cash dividend reduces total stockholders’ equity by the amount of the dividend.

The two types of dividends do not have the same impact upon stockholders’ equity. A cashdividend is a distribution of a corporation’s assets (cash) to stockholders and, as such, causes adecrease in stockholders’ equity. A stock dividend is simply issuing more stock certificates to theexisting group of shareholders with no accompanying increase or outflow of assets; acorporation’s own stock is not an asset of the corporation. With both small and large stock dividends, stockholders’ equity is adjusted to reflect the increased number of shares outstanding,but there is no additional equity created and no decrease in equity.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 421

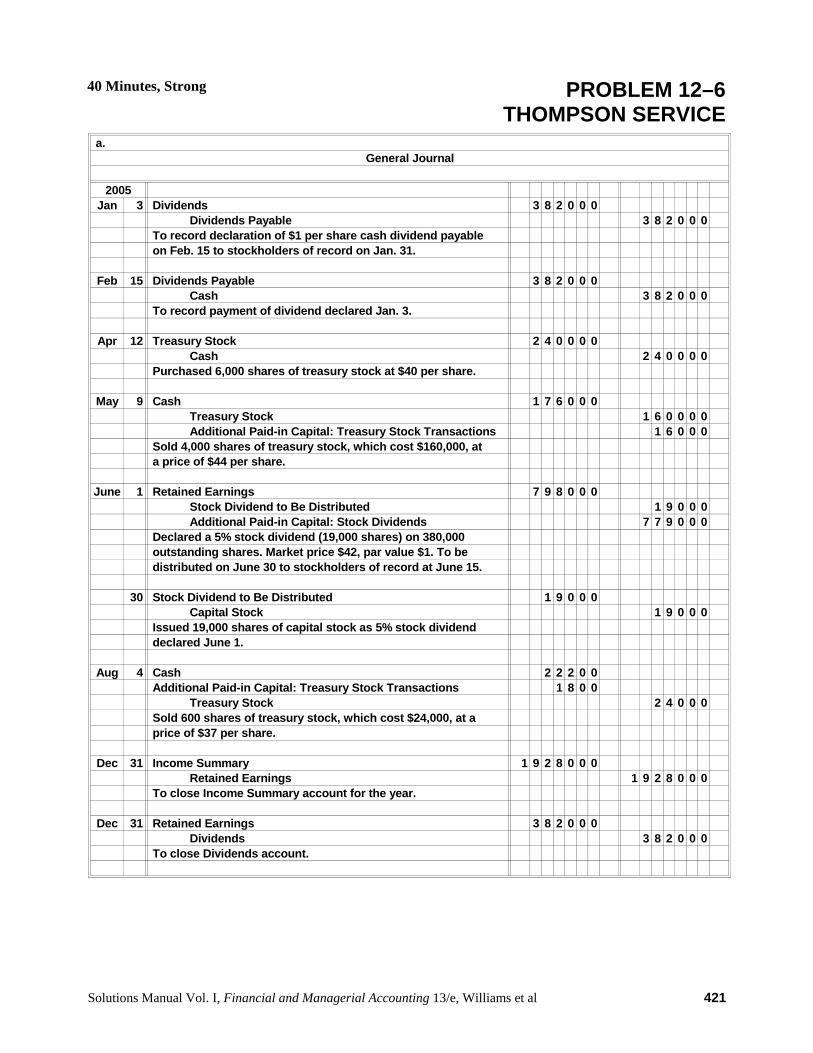

40 Minutes, Strong PROBLEM 12–6THOMPSON SERVICE

a.General Journal

2005Jan 3 Dividends 3 8 2 0 0 0

Dividends Payable 3 8 2 0 0 0 To record declaration of $1 per share cash dividend payable on Feb. 15 to stockholders of record on Jan. 31.

Feb 15 Dividends Payable 3 8 2 0 0 0Cash 3 8 2 0 0 0

To record payment of dividend declared Jan. 3.

Apr 12 Treasury Stock 2 4 0 0 0 0Cash 2 4 0 0 0 0

Purchased 6,000 shares of treasury stock at $40 per share.

May 9 Cash 1 7 6 0 0 0Treasury Stock 1 6 0 0 0 0Additional Paid-in Capital: Treasury Stock Transactions 1 6 0 0 0

Sold 4,000 shares of treasury stock, which cost $160,000, at a price of $44 per share.

June 1 Retained Earnings 7 9 8 0 0 0Stock Dividend to Be Distributed 1 9 0 0 0Additional Paid-in Capital: Stock Dividends 7 7 9 0 0 0

Declared a 5% stock dividend (19,000 shares) on 380,000 outstanding shares. Market price $42, par value $1. To be distributed on June 30 to stockholders of record at June 15.

30 Stock Dividend to Be Distributed 1 9 0 0 0Capital Stock 1 9 0 0 0

Issued 19,000 shares of capital stock as 5% stock dividend declared June 1.

Aug 4 Cash 2 2 2 0 0 Additional Paid-in Capital: Treasury Stock Transactions 1 8 0 0

Treasury Stock 2 4 0 0 0 Sold 600 shares of treasury stock, which cost $24,000, at a price of $37 per share.

Dec 31 Income Summary 1 9 2 8 0 0 0Retained Earnings 1 9 2 8 0 0 0

To close Income Summary account for the year.

Dec 31 Retained Earnings 3 8 2 0 0 0Dividends 3 8 2 0 0 0

To close Dividends account.

422 © The McGraw-Hill Companies, Inc., 2005

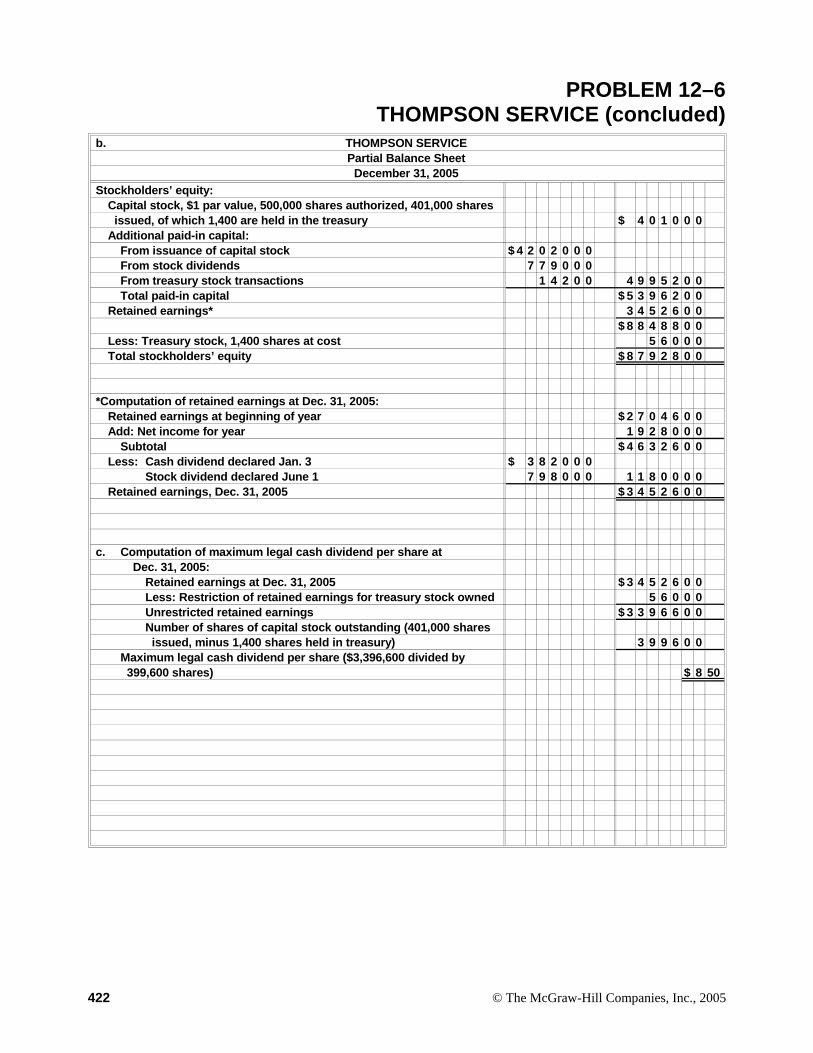

PROBLEM 12–6THOMPSON SERVICE (concluded)

b. THOMPSON SERVICEPartial Balance Sheet

December 31, 2005 Stockholders’ equity:

Capital stock, $1 par value, 500,000 shares authorized, 401,000 shares issued, of which 1,400 are held in the treasury $ 4 0 1 0 0 0Additional paid-in capital:

From issuance of capital stock $ 4 2 0 2 0 0 0From stock dividends 7 7 9 0 0 0From treasury stock transactions 1 4 2 0 0 4 9 9 5 2 0 0Total paid-in capital $ 5 3 9 6 2 0 0

Retained earnings* 3 4 5 2 6 0 0$ 8 8 4 8 8 0 0

Less: Treasury stock, 1,400 shares at cost 5 6 0 0 0Total stockholders’ equity $ 8 7 9 2 8 0 0

*Computation of retained earnings at Dec. 31, 2005:Retained earnings at beginning of year $ 2 7 0 4 6 0 0Add: Net income for year 1 9 2 8 0 0 0

Subtotal $ 4 6 3 2 6 0 0Less: Cash dividend declared Jan. 3 $ 3 8 2 0 0 0

Stock dividend declared June 1 7 9 8 0 0 0 1 1 8 0 0 0 0Retained earnings, Dec. 31, 2005 $ 3 4 5 2 6 0 0

c. Computation of maximum legal cash dividend per share atDec. 31, 2005:

Retained earnings at Dec. 31, 2005 $ 3 4 5 2 6 0 0Less: Restriction of retained earnings for treasury stock owned 5 6 0 0 0Unrestricted retained earnings $ 3 3 9 6 6 0 0Number of shares of capital stock outstanding (401,000 shares issued, minus 1,400 shares held in treasury) 3 9 9 6 0 0

Maximum legal cash dividend per share ($3,396,600 divided by 399,600 shares) $ 8 50

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 423

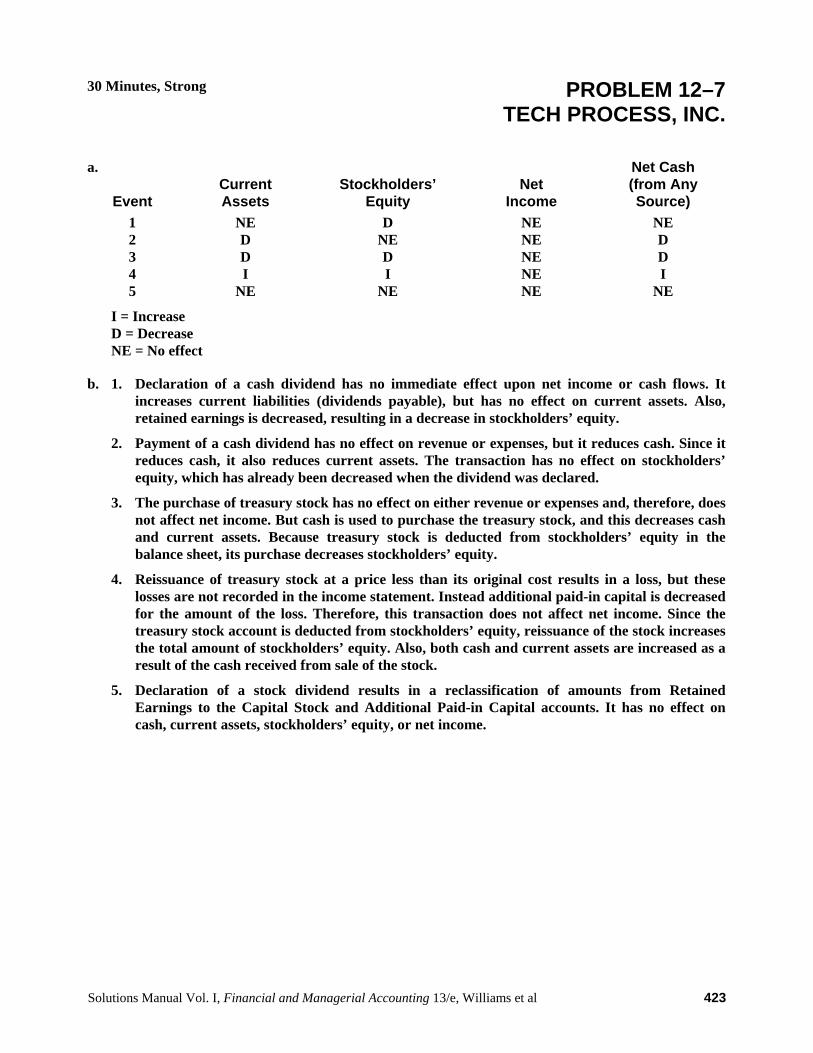

30 Minutes, Strong PROBLEM 12–7TECH PROCESS, INC.

a.

Event

Current Assets

Stockholders’

Equity

Net

Income

Net Cash(from AnySource)

1 2 3 4 5

NE D D I

NE

D NE D I

NE

NE NE NE NE NE

NE D D I

NE I = Increase

D = Decrease NE = No effect

b. 1. Declaration of a cash dividend has no immediate effect upon net income or cash flows. Itincreases current liabilities (dividends payable), but has no effect on current assets. Also, retained earnings is decreased, resulting in a decrease in stockholders’ equity.

2. Payment of a cash dividend has no effect on revenue or expenses, but it reduces cash. Since itreduces cash, it also reduces current assets. The transaction has no effect on stockholders’ equity, which has already been decreased when the dividend was declared.

3. The purchase of treasury stock has no effect on either revenue or expenses and, therefore, doesnot affect net income. But cash is used to purchase the treasury stock, and this decreases cash and current assets. Because treasury stock is deducted from stockholders’ equity in thebalance sheet, its purchase decreases stockholders’ equity.

4. Reissuance of treasury stock at a price less than its original cost results in a loss, but these losses are not recorded in the income statement. Instead additional paid-in capital is decreased for the amount of the loss. Therefore, this transaction does not affect net income. Since thetreasury stock account is deducted from stockholders’ equity, reissuance of the stock increasesthe total amount of stockholders’ equity. Also, both cash and current assets are increased as aresult of the cash received from sale of the stock.

5. Declaration of a stock dividend results in a reclassification of amounts from Retained Earnings to the Capital Stock and Additional Paid-in Capital accounts. It has no effect on cash, current assets, stockholders’ equity, or net income.

424 © The McGraw-Hill Companies, Inc., 2005

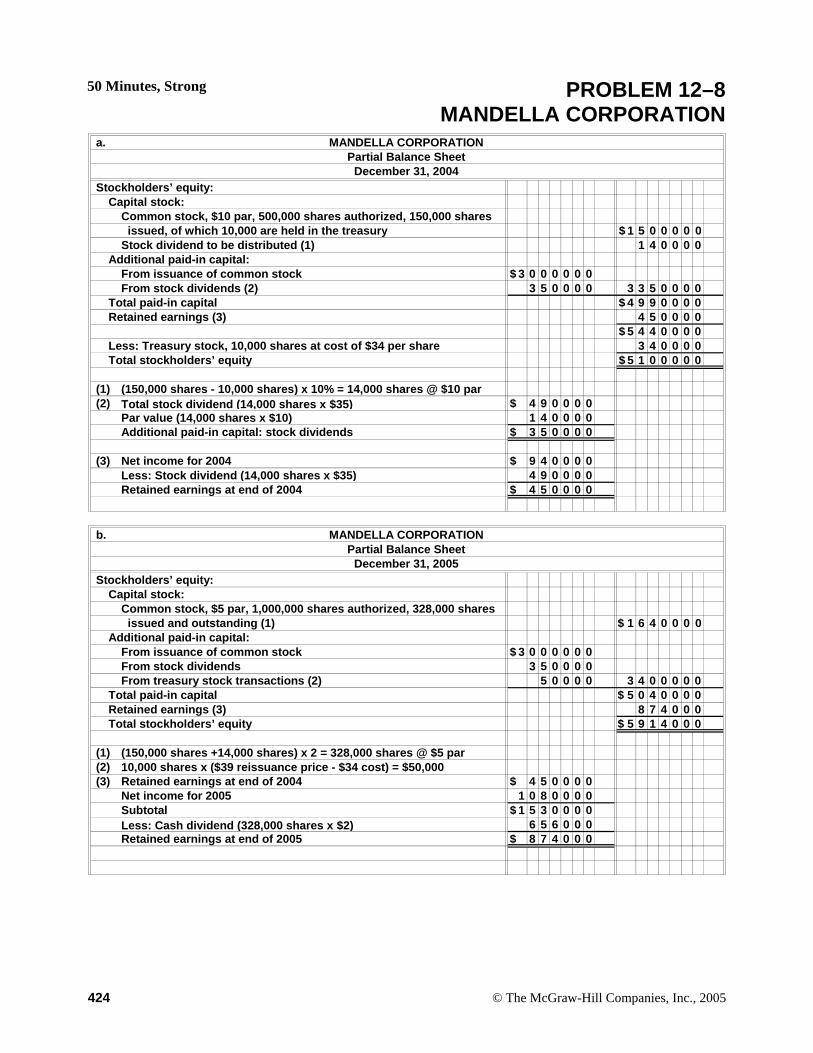

50 Minutes, Strong PROBLEM 12–8MANDELLA CORPORATION

a. MANDELLA CORPORATIONPartial Balance Sheet

December 31, 2004 Stockholders’ equity:

Capital stock:Common stock, $10 par, 500,000 shares authorized, 150,000 shares issued, of which 10,000 are held in the treasury $ 1 5 0 0 0 0 0Stock dividend to be distributed (1) 1 4 0 0 0 0

Additional paid-in capital:From issuance of common stock $ 3 0 0 0 0 0 0From stock dividends (2) 3 5 0 0 0 0 3 3 5 0 0 0 0

Total paid-in capital $ 4 9 9 0 0 0 0Retained earnings (3) 4 5 0 0 0 0

$ 5 4 4 0 0 0 0Less: Treasury stock, 10,000 shares at cost of $34 per share 3 4 0 0 0 0Total stockholders’ equity $ 5 1 0 0 0 0 0

(1) (150,000 shares - 10,000 shares) x 10% = 14,000 shares @ $10 par (2) Total stock dividend (14,000 shares x $35) $ 4 9 0 0 0 0

Par value (14,000 shares x $10) 1 4 0 0 0 0Additional paid-in capital: stock dividends $ 3 5 0 0 0 0

(3) Net income for 2004 $ 9 4 0 0 0 0Less: Stock dividend (14,000 shares x $35) 4 9 0 0 0 0Retained earnings at end of 2004 $ 4 5 0 0 0 0

b. MANDELLA CORPORATIONPartial Balance Sheet

December 31, 2005 Stockholders’ equity:

Capital stock:Common stock, $5 par, 1,000,000 shares authorized, 328,000 shares issued and outstanding (1) $ 1 6 4 0 0 0 0

Additional paid-in capital:From issuance of common stock $ 3 0 0 0 0 0 0From stock dividends 3 5 0 0 0 0From treasury stock transactions (2) 5 0 0 0 0 3 4 0 0 0 0 0

Total paid-in capital $ 5 0 4 0 0 0 0Retained earnings (3) 8 7 4 0 0 0Total stockholders’ equity $ 5 9 1 4 0 0 0

(1) (150,000 shares +14,000 shares) x 2 = 328,000 shares @ $5 par (2) 10,000 shares x ($39 reissuance price - $34 cost) = $50,000 (3) Retained earnings at end of 2004 $ 4 5 0 0 0 0

Net income for 2005 1 0 8 0 0 0 0Subtotal $ 1 5 3 0 0 0 0Less: Cash dividend (328,000 shares x $2) 6 5 6 0 0 0Retained earnings at end of 2005 $ 8 7 4 0 0 0

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 425

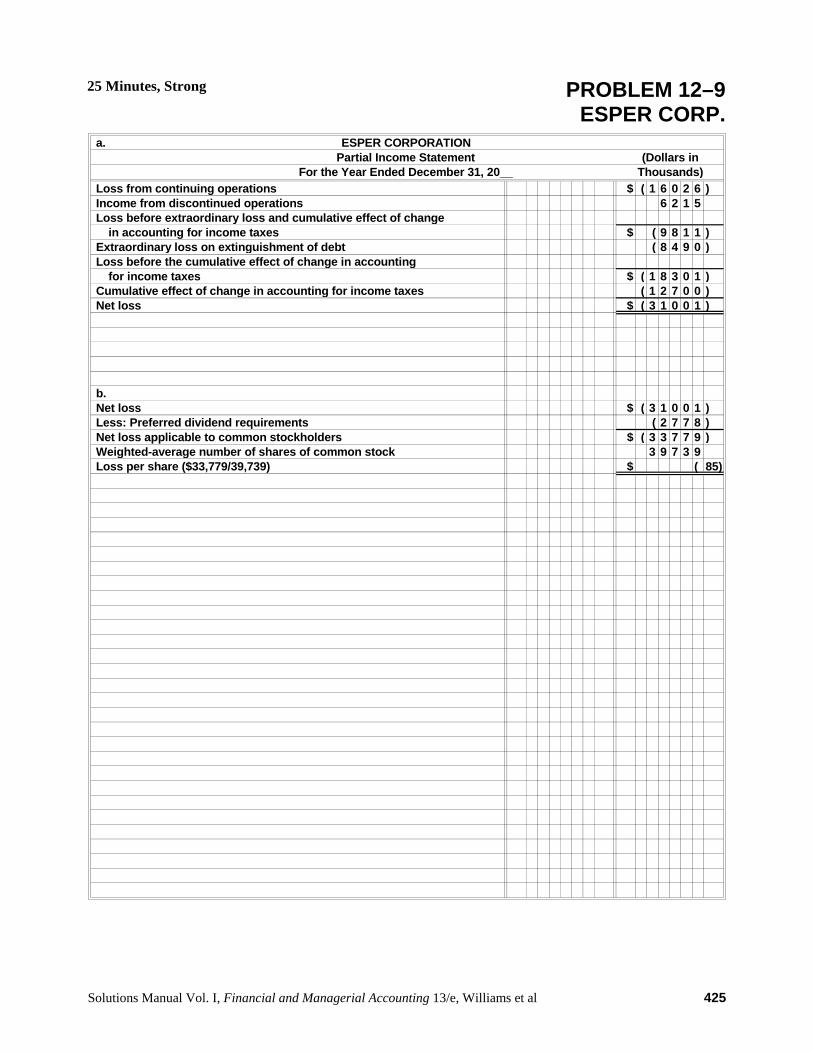

25 Minutes, Strong PROBLEM 12–9ESPER CORP.

a. ESPER CORPORATION Partial Income Statement (Dollars in

For the Year Ended December 31, 20__ Thousands) Loss from continuing operations $ ( 1 6 0 2 6 ) Income from discontinued operations 6 2 1 5 Loss before extraordinary loss and cumulative effect of change

in accounting for income taxes $ ( 9 8 1 1 ) Extraordinary loss on extinguishment of debt ( 8 4 9 0 ) Loss before the cumulative effect of change in accounting

for income taxes $ ( 1 8 3 0 1 ) Cumulative effect of change in accounting for income taxes ( 1 2 7 0 0 ) Net loss $ ( 3 1 0 0 1 )

b. Net loss $ ( 3 1 0 0 1 ) Less: Preferred dividend requirements ( 2 7 7 8 ) Net loss applicable to common stockholders $ ( 3 3 7 7 9 ) Weighted-average number of shares of common stock 3 9 7 3 9 Loss per share ($33,779/39,739) $ ( 85)

426 © The McGraw-Hill Companies, Inc., 2005

SOLUTIONS TO CASES

20 Minutes, Easy CASE 12–1UNUSUAL EVENTS IN PUBLISHED

FINANCIAL STATEMENTS

a. Both the operating loss from the noncoal minerals activities and the loss on disposal should be classified in ARCO’s income statement as discontinued operations and should be shown separatelyfrom the results of ARCO’s ongoing business operations. These losses qualify for this separatetreatment because the discontinued activities represented an entire identifiable segment ofARCO’s business operations.

b. A change in the estimated useful life of depreciable assets is a change in estimate, not a change inaccounting principle. Changes in estimate affect only the current year and future years; the cumulative effect of such changes upon prior years is not computed. On the other hand, hadAmerican Airlines changed the method used in computing depreciation expense, the cumulativeeffect of such a change in accounting principle would be shown in the income statement in the yearof the change.

c. The explosion of a chemical plant appears to meet the criteria for classification as anextraordinary loss. These criteria are (1) material in amount, (2) unusual in nature, and (3) not expected to recur in the foreseeable future.

d. A change in the method used to depreciate assets is a change in accounting principle. Therefore,the cumulative effect of this change upon the net income of prior periods (a $175 millionreduction) would appear as a separate item in AT&T’s income statement in the year of thechange.

e. The criteria for classification as an extraordinary item are (1) material in amount, (2) unusual innature and (3) not expected to recur in the foreseeable future. Condemnations of assets by governmental authorities generally are viewed as meeting these criteria. Therefore, the $10 milliongain would be classified as an extraordinary item in Georgia Pacific’s income statement.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 427

20 Minutes, Medium CASE 12–2LIFE WITHOUT BASEBALL

a. If JPI had not sold the baseball team at the end of 2005, it still would have incurred the team’s$1,300,000 operating loss for the year. However, the company would not have realized the$4,700,000 gain on the sale. Other items in the income statement would not have been affected. Thus, JPI’s income for 2005 would have been $4,700,000 less than was actually reported, or$2,600,000 ($7,300,000 − $4,700,000 = $2,600,000).

b. In 2005, JPI’s newspaper business earned $4,500,000, as shown by the subtotal, Income from Continuing Operations. If the profitability of these operations increased by 7% in 2006, theywould earn approximately $4,815,000 ($4,500,000 × 1.07 = $4,815,000). If the baseball team were still owned and lost $2,000,000 in 2006, JPI could be expected to earn a net income of about $2,815,000 in that year.

c. Given that the baseball team was sold in 2005, JPI should earn a net income of approximately$4,815,000 in 2006, assuming that the profitability of the continuing newspaper operationsincreases by 7% ($4,500,000 × 1.07 = $4,815,000).

d. The operating loss incurred by the baseball team in 2005 indicates that the team’s expenses (net oftax effects) exceeded its net revenue by $1,300,000. If the expenses were $32,200,000, the netrevenue must have amounted to $1,300,000 less, or $30,900,000.

428 © The McGraw-Hill Companies, Inc., 2005

30 Minutes, Strong CASE 12–3PICK A NUMBER

a. The company reports earnings per share computed on both a basic and a diluted basis because ithas outstanding convertible preferred stock. The conversion of these securities into common stock would increase the number of common shares outstanding and thereby dilute (reduce) earningsper share of common stock. The primary purpose of a company’s disclosing diluted earnings pershare is to warn investors of the dilution in earnings that could occur if the convertible securitiesactually were converted.

It is important to recognize that diluted earnings represent a hypothetical case. The convertiblesecurities have not actually been converted into common shares as of the close of the current year.

b. The total dollar amount of the company’s extraordinary loss can be computed from the earningsper share information as follows:

Extraordinary loss per share ($6.90 − $3.60) ..................................................................... $3.30 Total extraordinary loss ($3.30 per share × 3 million shares) .......................................... $9,900,000

c. The approximate market price of the company’s common stock is $69 per share. When acompany’s income statement includes an extraordinary item, the price-earnings ratio shown in newspapers is based upon basic earnings before extraordinary items ($6.90 × 10 = $69).

d. (1) $9.02 ($8.20 × 110%) Only the continuing operations will be earning revenue and incurring expenses next year, and

the extraordinary item is not expected to recur. Therefore, the starting point for projecting future net earnings should be earnings from continuing operations. Since both revenue andexpenses are expected to increase by 10%, earnings per share also should increase 10%.

(2) $7.48 ($6.80 × 110%) The diluted earnings per share figures show the effect that conversion of all of the convertible

preferred stock into common shares would have had upon this year’s earnings. Earnings pershare from continuing operations would have been only $6.80, rather than $8.20. Thus, $6.80per share becomes the logical starting point for forecasting next year’s net earnings. As inpart (1), next year’s earnings are expected to rise by 10% over those of the current year.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 429

35 Minutes, Strong CASE 12–4. . . BUT WHAT DOES IT ALL MEAN?

a. Beginning of year: 79,395,732 shares outstanding (83,989,396 issued − 4,593,664 held in treasury) End of year: 78,767,415 shares outstanding (83,989,396 issued − 5,221,981 treasury shares)

b. $95,200,000 total dividend declared on common stock 79,333,333 approximate number of shares entitled to $1.20 per share dividend ($95,200,000 ÷

$1.20 per share)

This answer appears reasonable, since the number of common shares outstanding ranged from79,395,732 at the beginning of the year to 78,767,415 at year-end. We cannot determine precisely the number of shares receiving each quarterly dividend of 30 cents per share, but the 79,333,333approximate figure for the overall $1.20 annual dividend appears compatible with the beginningand ending actual figures because it falls between these numbers.

c. The stock issued during the year for the stock option plans consisted of treasury shares, not newlyissued shares. The Treasury Stock account is used to account for repurchases of a corporation’sstock, as well as the reissuance of treasury shares. When stock is repurchased and subsequentlyreissued, the Common Stock account is not affected; these transactions do, however, affect theTreasury Stock account, a contra-stockholders’ equity account.

d. $28.93 average cost per share of treasury stock at the beginning of the year ($132,900,000 total cost ÷ 4,593,664 treasury shares)

e. The aggregate reissue price for the treasury shares must have been lower than the cost to acquirethose treasury shares, because the Additional Paid-in Capital account was reduced by the reissuance of the treasury stock. The cost of the treasury shares reissued was $16,700,000; thereissue price for the treasury shares must have been $15,300,000 to cause a $1,400,000 reductionin Additional Paid-in Capital.

f. $55.79 average cost per share for treasury stock acquired during the current year ($68,600,000 aggregate cost ÷ 1,229,700 shares repurchased)

g. Earnings per share: Divide by the weighted-average number of shares outstanding throughout the year

Book value per share: Divide by the actual number of shares outstanding as of the specific date(usually a balance sheet date)

430 © The McGraw-Hill Companies, Inc., 2005

60 Minutes, Strong CASE 12–5EXTRAORDINARY?

a. An asset represents something with future economic benefit. But if the amount at which the asset is presented in the balance sheet (i.e., its book value) cannot be recovered through future use or sale,any future economic benefit appears to be less than the asset’s current book value. In such cases,the asset should be written down to the recoverable amount.

b. Although materiality in terms of size is important, size alone does not qualify a loss as anextraordinary item. Nor does the fact that the item is not routine.

To qualify as extraordinary, an event should be unusual in nature, and not be expected to recur in the foreseeable future. Given that Elliot-Cole has operations in more than 90 countries, losses ofthis nature could recur. The fact that in a single year, such losses were incurred in severaldifferent countries suggests that this may be more than a one-time event. Thus, in light of Elliot-Cole’s business environment, it appears that we would not classify these losses as extraordinary.

Note to instructor: We do not consider this answer cut and dried. If these assets had been expropriated, the losses would be classified as extraordinary. These assets have not been expropriated—nor is there any indication that they will be. Nonetheless, there are some parallelsbetween this situation and an expropriation of assets by a foreign government. These similarities may be set forth as an argument for classifying the losses as extraordinary.

c. 1. Net income will be reduced by the same amount regardless of whether these losses are classified as ordinary or extraordinary. In either case, they are deducted in the computation ofnet income.

2. Income before extraordinary items will be reduced only if the losses are classified as ordinary.If they are classified as extraordinary, they will be deducted after the computation of the subtotal, Income before Extraordinary Items.

3. Extraordinary items are deducted after the determination of Income from Continuing Operations. Therefore, this subtotal will be reduced only if the losses are classified as ordinary.

4. Given that these losses do not affect income taxes, they have no cash effects. Therefore, netcash flow from operating activities will be unaffected.

d. The p/e ratio is based upon income before extraordinary items (stated on a per-share basis). As stated in c (2), above, income before extraordinary items will be unaffected if the losses are classified as extraordinary. Therefore, the p/e ratio will be unaffected. But if the losses are classified as ordinary,income before extraordinary items will be reduced, and the p/e ratio, therefore, will be higher.

e. Yes. Members of management have a self-interest in seeing stock prices increase, which wouldfavorably affect the value of their stock options as well as stock they already own. In addition, arising stock price makes it easier for the company to raise capital, benefits stockholders, andmakes management look good.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 431

CASE 12–5EXTRAORDINARY? (concluded)

The classification of these losses may well affect Elliot-Cole’s stock price. Investors consider income from continuing operations a predictive subtotal. If the losses are classified as ordinary, this key subtotal will decline, probably below last year’s level. (The losses amount to 18% of pre-loss earnings, which exceeds the company’s normal earnings growth of 15%. Thus, these losses may be sufficient to cause a decline in earnings relative to the preceding year.) This could have an adverseeffect on stock price.

On the other hand, if the losses are considered extraordinary, this subtotal will be unaffected and, presumably, continue to reflect the company’s 15% annual growth rate.

Similarly, classifying the losses as ordinary will reduce income before extraordinary items, whichis the income figure used in computing p/e ratios. Thus, the p/e ratio reported in the financial press will rise significantly above its normal level. This, too, may have a depressing effect uponstock price. But if the losses are classified as extraordinary, the per-share earnings used in the computation of the company’s p/e ratio will not be affected.

In summary, the adverse effects of these losses on the company’s stock price are likely to begreater if the losses are classified as ordinary, rather than extraordinary. Therefore, managementhas a self-interest in seeing these losses classified as an extraordinary item.

f. These write-offs are likely to increase the earnings reported in future periods, especially if thecompany continues to do business in any of the related countries. With the assets having no bookvalue, future earnings from these operations will not be reduced by charges for depreciation (or,in some cases, for a cost of goods sold).

g. The ethical dilemma is the classification of these losses. Because of the probable effects upon stockprice, classifying them as extraordinary may be to management’s advantage. The case isarguable—though we think it’s a bit of a reach. Bear in mind that a higher stock price alsobenefits the company’s current stockholders. So who, if anybody, stands to lose?

In management’s shoes, how would you classify these losses? (We find this question easier to askthan to answer.)

Note to instructor: This case is adapted from an incident involving an international pharmaceuticalcompany. The details of the situation have been altered for the purpose of creating an introductory level textbook assignment, and the so-called quotations from corporate officers are entirely fictitious.Nonetheless, we believe that the outcome of the actual event provides insight into the financialreporting process and also to the importance that investors attach to the various computations ofearnings per share.

Management originally classified the losses as extraordinary, and the auditors concurred. The SEC, however, did not agree. It insisted that the corporation revise and reissue its financial statement—with the controversial items classified as ordinary operating losses. When the company announced the reclassification of these losses, its stock price fell substantially—despite the fact that the reported amount of net income remained unchanged.

Who were the losers? Anyone who bought the stock between the release of the original earningsfigures and the announcement that substantial losses would be reclassified.

432 © The McGraw-Hill Companies, Inc., 2005

15 Minutes, Medium CASE 12–6BUSINESS WEEK ASSIGNMENT

Several reasons may be cited for why there is an increase in “special items” in U.S. corporations’income statements. Perhaps the most persuasive is that companies are constantly looking for ways tomake their performance look better to investors and creditors. If a special item is a loss, separating that item out from normal, recurring operations, and presenting an income subtotal before and afterthat loss may encourage investors and creditors to discount that item in terms of it recurring in thefuture.

For all companies to report by the same rules is critical to being able to compare the performance ofone company against others. For that reason, the FASB has spent a great deal of time, effort, andmoney to try to develop financial reporting standards to increasingly move companies toward more comparable financial reporting. Special items, however, have been a particularly difficult area, andachieving a balance between prescriptive standards that border on absolute rules and allowingjudgment in the application of standards is a difficult task.

Solutions Manual Vol. I, Financial and Managerial Accounting 13/e, Williams et al 433

SOLUTION TO INTERNET ASSIGNMENT

30 Minutes, Easy INTERNET 12–1PRICE-EARNINGS RATIOS

Note: We cannot supply quantitative answers to this assignment as they will vary depending uponwhich companies the student selects. In general, it would be expected that the NASDAQ company willhave a higher price-earnings ratio than the Fortune 500 company.

Related Documents