Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk CHAPTER 9 FOREIGN CURRENCY TRANSACTIONS AND HEDGING FOREIGN EXCHANGE RISK Chapter Outline I. In today’s global economy, a great many companies deal in currencies other than their reporting currencies. A. Merchandise may be imported or exported with prices stated in a foreign currency. B. For reporting purposes, foreign currency balances must be stated in terms of the company’s reporting currency by multiplying it by an exchange rate. C. Accountants face two questions in restating foreign currency balances. 1. What is the appropriate exchange rate for restating foreign currency balances? 2. How are changes in the exchange rate accounted for? D. Companies often engage in foreign currency hedging activities to avoid the adverse impact of exchange rate changes. E. Accountants must determine how to properly account for these hedging activities. II. Foreign exchange rates are determined in the foreign exchange market under a variety of different currency arrangements. A. Exchange rates can be expressed in terms of the number of U.S. dollars to purchase one foreign currency unit (direct quotes) or the number of foreign currency units that can be obtained with one U.S. dollar (indirect quotes). B. Foreign currency trades can be executed on a spot or forward basis. 1. The spot rate is the price at which a foreign currency can be purchased or sold today. 2. The forward rate is the price today at which foreign currency can be purchased or sold sometime in the future. 3. Forward exchange contracts provide companies with the ability to “lock in” a price today for purchasing or selling currency at a specific future date. C. Foreign currency options provide the right but not the obligation to buy or sell foreign currency in the future, and 9-1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

CHAPTER 9FOREIGN CURRENCY TRANSACTIONS AND

HEDGING FOREIGN EXCHANGE RISK

Chapter Outline

I. In today’s global economy, a great many companies deal in currencies other than their reporting currencies.A. Merchandise may be imported or exported with prices stated in a foreign currency.B. For reporting purposes, foreign currency balances must be stated in terms of the

company’s reporting currency by multiplying it by an exchange rate.C. Accountants face two questions in restating foreign currency balances.

1. What is the appropriate exchange rate for restating foreign currency balances?2. How are changes in the exchange rate accounted for?

D. Companies often engage in foreign currency hedging activities to avoid the adverse impact of exchange rate changes.

E. Accountants must determine how to properly account for these hedging activities. II. Foreign exchange rates are determined in the foreign exchange market under a variety of

different currency arrangements.A. Exchange rates can be expressed in terms of the number of U.S. dollars to purchase

one foreign currency unit (direct quotes) or the number of foreign currency units that can be obtained with one U.S. dollar (indirect quotes).

B. Foreign currency trades can be executed on a spot or forward basis.1. The spot rate is the price at which a foreign currency can be purchased or sold

today.2. The forward rate is the price today at which foreign currency can be purchased or

sold sometime in the future. 3. Forward exchange contracts provide companies with the ability to “lock in” a price

today for purchasing or selling currency at a specific future date.C. Foreign currency options provide the right but not the obligation to buy or sell foreign

currency in the future, and therefore are more flexible than forward contracts.

III. Statement 52 of the Financial Accounting Standards Board, issued in December 1981, prescribes accounting rules for foreign currency transactions.Note: SFAS 52 has been incorporated into the FASB Accounting Standards Codification Section 830 Foreign Currency Matters (FASB ASC 830).A. Export sales denominated in foreign currency are reported in U.S. dollars at the spot

exchange rate at the date of the transaction. Subsequent changes in the exchange rate until collection of the receivable are reflected through a restatement of the foreign currency account receivable with an offsetting foreign exchange gain or loss reported in income. This is known as a two-transaction perspective, accrual approach.

B. The two-transaction perspective, accrual approach also is used in accounting for foreign currency payables. Receivables and payables denominated in foreign currency create an exposure to foreign exchange risk; this is the risk that changes in the exchange rate over time will result in a foreign exchange loss.

9-1

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

IV. FASB Statement 133 (as amended by FASB Statement 138) governs the accounting for derivative financial instruments and hedging activities including the use of foreign currency forward contracts and foreign currency options.

9-2

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Note: SFAS 133 and 138 have been incorporated into the FASB Accounting Standards Codification Section 815 Derivatives and Hedging (FASB ASC 815).

A. The fundamental requirement is that all derivatives must be carried on the balance sheet at their fair value. Derivatives are reported on the balance sheet as assets when they have a positive fair value and as liabilities when they have a negative fair value.

B. U.S. GAAP provides guidance for hedges of the following sources of foreign exchange risk:1. foreign currency denominated assets and liabilities.2. foreign currency firm commitments.3. forecasted foreign currency transactions.4. net investments in foreign operations (covered in Chapter 10).

C. Companies prefer to account for hedges in such a way that the gain or loss from the hedge is recognized in net income in the same period as the loss or gain on the risk being hedged. This approach is known as hedge accounting. Hedge accounting for foreign currency derivatives may be applied only if three conditions are satisfied:1. the derivative is used to hedge either a fair value exposure or cash flow exposure

to foreign exchange risk,2. the derivative is highly effective in offsetting changes in the fair value or cash flows

related to the hedged item, and3. the derivative is properly documented as a hedge.

D. Hedge accounting is allowed for hedges of two different types of exposure: cash flow exposure and fair value exposure. Hedges of (1) foreign currency denominated assets and liabilities, (2) foreign currency firm commitments, and (3) forecasted foreign currency transactions can be designated as cash flow hedges. Hedges of (1) and (2) also can be designated as fair value hedges. Accounting procedures differ for the two types of hedges.

E. For cash flow hedges of foreign currency denominated assets and liabilities, at each balance sheet date: 1. The hedged asset or liability is adjusted to fair value based on changes in the spot

exchange rate, and a foreign exchange gain or loss is recognized in net income.2. The derivative hedging instrument is adjusted to fair value (resulting in an asset or

liability reported on the balance sheet), with the counterpart recognized as a change in Accumulated Other Comprehensive Income (AOCI).

3. An amount equal to the foreign exchange gain or loss on the hedged asset or liability is then transferred from AOCI to net income; the net effect is to offset any gain or loss on the hedged asset or liability.

4. An additional amount is removed from AOCI and recognized in net income to reflect (a) the current period’s amortization of the original discount or premium on the forward contract (if a forward contract is the hedging instrument) or (b) the change in the time value of the option (if an option is the hedging instrument).

F. For fair value hedges of foreign currency denominated assets and liabilities, at each balance sheet date:1. The hedged asset or liability is adjusted to fair value based on changes in the spot

exchange rate, and a foreign exchange gain or loss is recognized in net income.2. The derivative hedging instrument is adjusted to fair value (resulting in an asset or

liability reported on the balance sheet), with the counterpart recognized as a gain or loss in net income.

9-3

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

G. Under fair value hedge accounting for hedges of foreign currency firm commitments:1. the gain or loss on the hedging instrument is recognized currently in net income,

and2. the change in fair value of the firm commitment is also recognized currently in net

income. This accounting treatment requires (1) measuring the fair value of the firm commitment, (2) recognizing the change in fair value in net income, and (3) reporting the firm commitment on the balance sheet as an asset or liability. A decision must be made whether to measure

9-4

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

the fair value of the firm commitment through reference to (a) changes in the spot exchange rate or (b) changes in the forward rate.

H. Cash flow hedge accounting is allowed for hedges of forecasted foreign currency transactions. For hedge accounting to apply, the forecasted transaction must be probable (likely to occur). The accounting for a hedge of a forecasted transaction differs from the accounting for a hedge of a foreign currency firm commitment in two ways:1. Unlike the accounting for a firm commitment, there is no recognition of the

forecasted transaction or gains and losses on the forecasted transaction.2. The hedging instrument (forward contract or option) is reported at fair value, but

because there is no gain or loss on the forecasted transaction to offset against, changes in the fair value of the hedging instrument are not reported as gains and losses in net income. Instead they are reported in other comprehensive income. On the projected date of the forecasted transaction, the cumulative change in the fair value of the hedging instrument is transferred from other comprehensive income (balance sheet) to net income (income statement).

V. IFRS is very similar to U.S. GAAP with respect to the accounting for foreign currency

transactions and hedging of foreign exchange risk. A. IAS 21 requires the use of a two-transaction perspective in accounting for foreign

currency transactions with unrealized foreign exchange gains and losses accrued in net income in the period of exchange rate change.

B. IAS 39 allows hedge accounting for foreign currency hedges of recognized assets and liabilities, firm commitments, and forecasted transactions when documentation requirements and effectiveness tests are met. Hedges are designated as cash flow or fair value hedges.

C. One difference between IFRS and U.S. GAAP relates to the type of financial instrument that can be designated as a foreign currency cash flow hedge. Under U.S. GAAP, only derivative financial instruments can be used as a cash flow hedge, whereas IFRS also allows non-derivative financial instruments, such as foreign currency loans, to be designated as hedging instruments in a foreign currency cash flow hedge.

Learning Objectives

Having completed Chapter 9, “Foreign Currency Transactions and Hedging Foreign Exchange Risk,” students should be able to fulfill each of the following learning objectives:

1. Understand concepts related to foreign currency, exchange rates, and foreign exchange risk.

2. Account for foreign currency transactions using the two-transaction perspective, accrual approach.

3. Understand how foreign currency forward contracts and foreign currency options can be used to hedge foreign exchange risk.

4. Account for forward contracts and options used as hedges of foreign currency denominated assets and liabilities.

9-5

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

5. Account for forward contracts and options used as hedges of foreign currency firm commitments.

6. Account for forward contracts and options used as hedges of forecasted foreign currency transactions.

9-6

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

7. Prepare journal entries to account for foreign currency borrowings.

Answer to Discussion Question

Do we have a gain or what?This case demonstrates the differing kinds of information provided through application of current accounting rules for foreign currency transactions and derivative financial instruments.

The Ahnuld Corporation could have received $200,000 from its export sale to Tcheckia if it had required immediate payment. Instead, Ahnuld allows its customer six months to pay. Given the future exchange rate of $1.70, Ahnuld would have received only $170,000 if it had not entered into the forward contract. This would have resulted in a decrease in cash inflow of $30,000. In accordance with current accounting standards, the decrease in the value of the tcheck receivable is recognized as a foreign exchange loss of $30,000. This loss represents the cost of extending credit to the foreign customer if the tcheck receivable is left unhedged.

However, rather than leaving the tcheck receivable unhedged, Ahnuld sells tchecks forward at a price of $180,000. Because the future spot rate turns out to be only $1.70, the forward contract provides a benefit, increasing the amount of cash received from the export sale by $10,000. In accordance with current accounting standards, the change in the fair value of the forward contract (from zero initially to $10,000 at maturity) is recognized as a gain on the forward contract of $10,000. This gain reflects the cash flow benefit from having entered into the forward contract, and is the appropriate basis for evaluating the performance of the foreign exchange risk manager. (Students should be reminded that the forward contract will not always improve cash inflow. For example, if the future spot rate were $1.85, the forward contract would result in $5,000 less cash inflow than if the transaction were left unhedged.)

The net impact on income resulting from the fluctuation in the value of the tcheck is a loss of $20,000. Clearly, Ahnuld forgoes $20,000 in cash inflow by allowing the customer time to pay for the purchase, and the net loss reported in income correctly measures this. The $20,000 loss is useful to management in assessing whether the sale to Tcheckia generated an adequate profit margin, but it is not useful in assessing the performance of the foreign exchange risk manager. The net loss must be decomposed into its component parts to fairly evaluate the risk manager’s performance.

Gains and losses on forward contracts designated as fair value hedges of foreign currency assets and liabilities are relevant measures for evaluating the performance of foreign exchange risk managers. (The same is not true for cash flow hedges. For this type of hedge, performance should be evaluated by considering the net gain or loss on the forward contract plus or minus the forward contract premium or discount.) Answers to Questions

1. Under the two-transaction perspective, an export sale (import purchase) and the subsequent collection (payment) of cash are treated as two separate transactions to be accounted for separately. The idea is that management has made two decisions: (1) to make the export sale (import purchase), and (2) to extend credit in foreign currency to the foreign customer (obtain credit from the foreign supplier). The income effect from each of these decisions should be reported separately.

9-7

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

2. Foreign currency receivables resulting from export sales are revalued at the end of accounting periods using the current spot rate. An increase in the value of a receivable will be offset by reporting a foreign exchange gain in net income, and a decrease will be offset by a foreign

9-8

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

exchange loss. Foreign exchange gains and losses are accrued even though they have not yet been realized.

3. Foreign exchange gains and losses are created by two factors: having foreign currency exposures (foreign currency receivables and payables) and changes in exchange rates. Appreciation of the foreign currency will generate foreign exchange gains on receivables and foreign exchange losses on payables. Depreciation of the foreign currency will generate foreign exchange losses on receivables and foreign exchange gains on payables.

4. Hedging is the process of eliminating exposure to foreign exchange risk so as to avoid potential losses from fluctuations in exchange rates. In addition to avoiding possible losses, companies hedge foreign currency transactions and commitments to introduce an element of certainty into the future cash flows resulting from foreign currency activities. Hedging involves establishing a price today at which foreign currency can be sold or purchased at a future date.

5. A party to a foreign currency forward contract is obligated to deliver one currency in exchange for another at a specified future date, whereas the owner of a foreign currency option can choose whether to exercise the option and exchange one currency for another or not.

6. Hedges of foreign currency denominated assets and liabilities are not entered into until a foreign currency transaction (import purchase or export sale) has taken place. Hedges of firm commitments are made when a purchase order is placed or a sales order is received, before a transaction has taken place. Hedges of forecasted transactions are made at the time a future foreign currency purchase or sale can be anticipated, even before an order has been placed or received.

7. Foreign currency options have an advantage over forward contracts in that the holder of the option can choose not to exercise if the future spot rate turns out to be more advantageous. Forward contracts, on the other hand, can lock a company into an unnecessary loss (or a reduced gain). The disadvantage associated with foreign currency options is that a premium must be paid up front even though the option might never be exercised.

8. An enterprise is required to recognize all derivative financial instruments as assets or

liabilities on the balance sheet and measure them at fair value.

9. The fair value of a foreign currency forward contract is determined by reference to changes in the forward rate over the life of the contract, discounted to the present value. Three pieces of

information are needed to determine the fair value of a forward contract at any point in time during its life: (a) the contracted forward rate when the forward contract is entered into, (b) the current forward rate for a contract that matures on the same date as the forward contract entered into, and (c) a discount rate; typically, the company’s incremental borrowing rate.

9-9

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

The manner in which the fair value of a foreign currency option is determined depends on whether the option is traded on an exchange or has been acquired in the over the counter market. The fair value of an exchange-traded foreign currency option is its current market price quoted on the exchange. For over the counter options, fair value can be determined by obtaining a price quote from an option dealer (such as a bank). If dealer price quotes are unavailable, the company can estimate the value of an option using the modified Black-Scholes option pricing model. Regardless of who does the calculation, principles similar to those in the Black-Scholes pricing model will be used in determining the value of the option.

9-10

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

10. Hedge accounting is defined as recognition of gains and losses on the hedging instrument in the same period as the recognition of gains and losses on the underlying hedged asset or liability (or firm commitment).

11. For hedge accounting to apply, the forecasted transaction must be probable (likely to occur), the hedge must be highly effective in offsetting fluctuations in the cash flow associated with the foreign currency risk, and the hedging relationship must be properly documented.

12. In both cases, (1) sales revenue (or the cost of the item purchased) is determined using the spot rate at the date of sale (or purchase), and (2) the hedged asset or liability is adjusted to fair value based on changes in the spot exchange rate with a foreign exchange gain or loss recognized in net income.

For a cash flow hedge, the derivative hedging instrument is adjusted to fair value (resulting in an asset or liability reported on the balance sheet), with the counterpart recognized as a change in Accumulated Other Comprehensive Income (AOCI). An amount equal to the foreign exchange gain or loss on the hedged asset or liability is then transferred from AOCI to net income; the net effect is to offset any gain or loss on the hedged asset or liability. An additional amount is removed from AOCI and recognized in net income to reflect (a) the current period’s amortization of the original discount or premium on the forward contract (if a forward contract is the hedging instrument) or (b) the change in the time value of the option (if an option is the hedging instrument).

For a fair value hedge, the derivative hedging instrument is adjusted to fair value (resulting in an asset or liability reported on the balance sheet), with the counterpart recognized as a gain or loss in net income. The discount or premium on a forward contract is not allocated to net income. The change in the time value of an option is not recognized in net income.

13. For a fair value hedge of a foreign currency asset or liability (1) sales revenue (cost of purchases) is recognized at the spot rate at the date of sale (purchase) and (2) the hedged asset or liability is adjusted to fair value based on changes in the spot exchange rate with a foreign exchange gain or loss recognized in net income. The forward contract is adjusted to fair value based on changes in the forward rate (resulting in an asset or liability reported on the balance sheet), with the counterpart recognized as a gain or loss in net income. The foreign exchange gain (loss) and the forward contract loss (gain) are likely to be of different amounts resulting in a net gain or loss reported in net income.

For a fair value hedge of a firm commitment, there is no hedged asset or liability to account for. The forward contract is adjusted to fair value based on changes in the forward rate (resulting in an asset or liability reported on the balance sheet), with a gain or loss recognized in net income. The firm commitment is also adjusted to fair value based on changes in the forward rate (resulting in a liability or asset reported on the balance sheet), and a gain or loss on firm commitment is recognized in net income. The firm commitment gain (loss) offsets the forward contract loss (gain) resulting in zero impact on net income. Sales revenue (cost of purchases) is recognized at the spot rate at the date of sale (purchase). The firm commitment account is closed as an adjustment to net income in the period in which the hedged item affects net income.

9-11

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

14. For a cash flow hedge of a foreign currency asset or liability (1) sales revenue (cost of purchases) is recognized at the spot rate at the date of sale (purchase) and (2) the hedged asset or liability is adjusted to fair value based on changes in the spot exchange rate with a foreign exchange gain or loss recognized in net income. The forward contract is adjusted to fair

9-12

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

value (resulting in an asset or liability reported on the balance sheet), with the counterpart recognized as a change in Accumulated Other Comprehensive Income (AOCI). An amount equal to the foreign exchange gain or loss on the hedged asset or liability is then transferred from AOCI to net income; the net effect is to offset any gain or loss on the hedged asset or liability. An additional amount is removed from AOCI and recognized in net income to reflect the current period’s allocation of the discount or premium on the forward contract.

For a hedge of a forecasted transaction, the forward contract is adjusted to fair value (resulting in an asset or liability reported on the balance sheet), with the counterpart recognized as a change in Accumulated Other Comprehensive Income (AOCI). Because there is no foreign currency asset or liability, there is no transfer from AOCI to net income to offset any gain or loss on the asset or liability. The current period’s allocation of the forward contract discount or premium is recognized in net income with the counterpart reflected in AOCI. Sales revenue (cost of purchases) is recognized at the spot rate at the date of sale (purchase). The amount accumulated in AOCI related to the hedge is closed as an adjustment to net income in the period in which the forecasted transaction was anticipated to occur.

15. In accounting for a fair value hedge, the change in the fair value of the foreign currency option is reported as a gain or loss in net income. In accounting for a cash flow hedge, the change in the entire fair value of the option is first reported in other comprehensive income, and then the change in the time value of the option is reported as an expense in net income.

16. The accounting for a foreign currency borrowing involves keeping track of two foreign currency payables—the note payable and interest payable. As both the face value of the borrowing and accrued interest represent foreign currency liabilities, both are exposed to foreign exchange risk and can give rise to foreign currency gains and losses.

Answers to Problems

1. C Foreign Currency Transaction; Foreign Exchange Gain/Loss (LO1)An import purchase causes a foreign currency payable to be carried on the books. If the foreign currency depreciates, the dollar value of the foreign currency payable decreases, yielding a foreign exchange gain.

2. D Foreign Currency Transactions; Method of Accounting (LO2) Current accounting standards require a two-transaction perspective, accrual approach.

3. B Foreign Currency Transactions; Foreign Exchange Gain/Loss (LO2)Foreign exchange gains related to foreign currency import purchases are treated as a component of income before income taxes. If there is no foreign exchange gain in operating income, then the purchase must have been denominated in U.S. dollars or there was no change in the value of the foreign currency from October 1 to December 1, 2011.

9-13

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

4. C Foreign Currency Transactions; Calculate Foreign Exchange Gain/Loss (LO2)The dollar value of the LCU receivable has decreased from $110,000 at December 31, 2011 to $95,000 at February 15, 2012. This decrease of $15,000

9-14

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

should be reported as a foreign exchange loss in 2012.

5. D Foreign Currency Borrowing; Calculate Foreign Exchange Gain/Loss (LO2, LO7)The increase in the dollar value of the euro note payable represents a foreign exchange loss. In this case a $25,000 loss would have been accrued in 2011 and a $10,000 loss will be reported in 2012.

6. D Foreign Currency Transactions; Foreign Exchange Gain/Loss (LO1, LO2)A foreign currency receivable will generate a foreign exchange gain when the foreign currency increases in dollar value. A foreign currency payable will generate a foreign exchange gain when the foreign currency decreases in dollar value. Hence, the correct combination is franc (increase) and peso (decrease).

7. D Foreign Currency Transactions; Calculate Foreign Exchange Gain/Loss (LO2)

The merchandise purchase results in a foreign exchange loss of $8,000, the difference between the U.S. dollar equivalent at the date of purchase and at the date of settlement.

The increase in the dollar equivalent of the note’s principal results in a foreign exchange loss of $20,000.

The total foreign exchange loss is $28,000 ($8,000 + $20,000).

8. D Forward Contract Cash Flow Hedge of Foreign Currency Denominated Asset/Liability (LO4)

The Thai baht is selling at a premium (forward rate exceeds spot rate). The exporter will receive more dollars as a result of selling the baht forward than if the baht had been received and converted into dollars on April 1. Thus, the premium results in additional revenue for the exporter.

9. D Forward Contract Fair Value Hedge of Foreign Currency Firm Commitment (LO5)The parts inventory will be recognized at the spot rate at the date of purchase (FC100,000 x $.23 = $23,000).

10. D Determine Fair Value of Forward Contract (LO3)The forward contract must be reported on the December 31, 2011 balance sheet as a liability. Barnum has locked-in to purchase ringgits at $0.042 per ringgit but could have locked-in to purchase ringgits at $0.037 per ringgit if it had waited until December 31 to enter into the forward contract. The forward contract must be reported at its fair value discounted for two months at 12% [($.042 – $.037) x 1,000,000 = $5,000 x .9803 = $4,901.50].

9-15

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

11. C Foreign Currency Transaction; Calculate Foreign Exchange Gain/Loss (LO2)The 10 million won receivable has changed in dollar value from $35,000 at 12/1/11 to $33,000 at 12/31/11. The won receivable will be written down by $2,000 and a foreign exchange loss will be reported in 2011 income.

12. B Forward Contract Fair Hedge of Foreign Currency Denominated Asset/Liability (LO4)The nominal value of the forward contract on December 31, 2011 is a positive $2,000, the difference between the amount to be received from the forward contract actually entered into, $34,000 ($.0034 x 10 million), and the amount that could be received by entering into a forward contract on December 31, 2011 that matures on March 31, 2012, $32,000 ($.0032 x 10 million). The fair value of the forward contract is the present value of $2,000 discounted for two months ($2,000 x .9706 = $1,941.20). On December 31, 2011, MNC Corp. will recognize a $1,941.20 gain on the forward contract and a foreign exchange loss of $2,000 on the won receivable. The net impact on 2011 income is –$58.80.

13. A Forward Contract Cash Flow Hedge of Forecasted Foreign Currency Transaction (LO6)The krona is selling at a premium in the forward market, causing Pimlico to pay more dollars to acquire kroner than if the kroner were purchased at the spot rate on March 1. Therefore, the premium results in an expense of $10,000 [($.12 – $.10) x 500,000].The Adjustment to Net Income is the amount accumulated in Accumulated Other Comprehensive Income (AOCI) as a result of recognizing the premium expense and the fair value of the forward contract. The journal entries would be as follows:

3/1 no journal entries

6/1 Premium Expense $10,000AOCI $10,000

AOCI $2,500Forward Contract $2,500

Foreign Currency $57,500Forward Contract 2,500

Cash $60,000

AOCI $7,500Adjustment to Net Income $7,500

9-16

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

14. C Option Cash Flow Hedge of Forecasted Foreign Currency Transaction (LO6)This is a cash flow hedge of a forecasted transaction. The original cost of the option is recognized as an Option Expense over the life of the option.

15-17. Option Fair Value Hedge of a Foreign Currency Firm Commitment (LO5)

15. B

16. DThe easiest way to solve problems 15 and 16 is to prepare journal entries for the option fair value hedge and the firm commitment. The journal entries are as follows:

9/1/11Foreign Currency Option $2,000

Cash $2,000

12/31/11Foreign Currency Option $300

Gain on Foreign Currency Option $300

Loss on Firm Commitment $980.30Firm Commitment $980.30

[($.79 – $.80) x 100,000 = $1,000 x .9803 = $980.30]

Net impact on 2011 net income:Gain on Foreign Currency Option $300.00Loss on Firm Commitment (980 .30 )

$(680 .30 )3/1/12

Foreign Currency Option $700Gain on Foreign Currency Option $700

Loss on Firm Commitment $2,019.70Firm Commitment $2,019.70

[($.77 – $.80) x 100,000 = $3,000 – $980.30 = $2,019.70]

Foreign Currency (C$) $77,000Sales $77,000

Cash $80,000Foreign Currency (C$) $77,000Foreign Currency Option 3,000

Firm Commitment $3,000

9-17

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Adjustment to Net Income $3,000

9-18

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

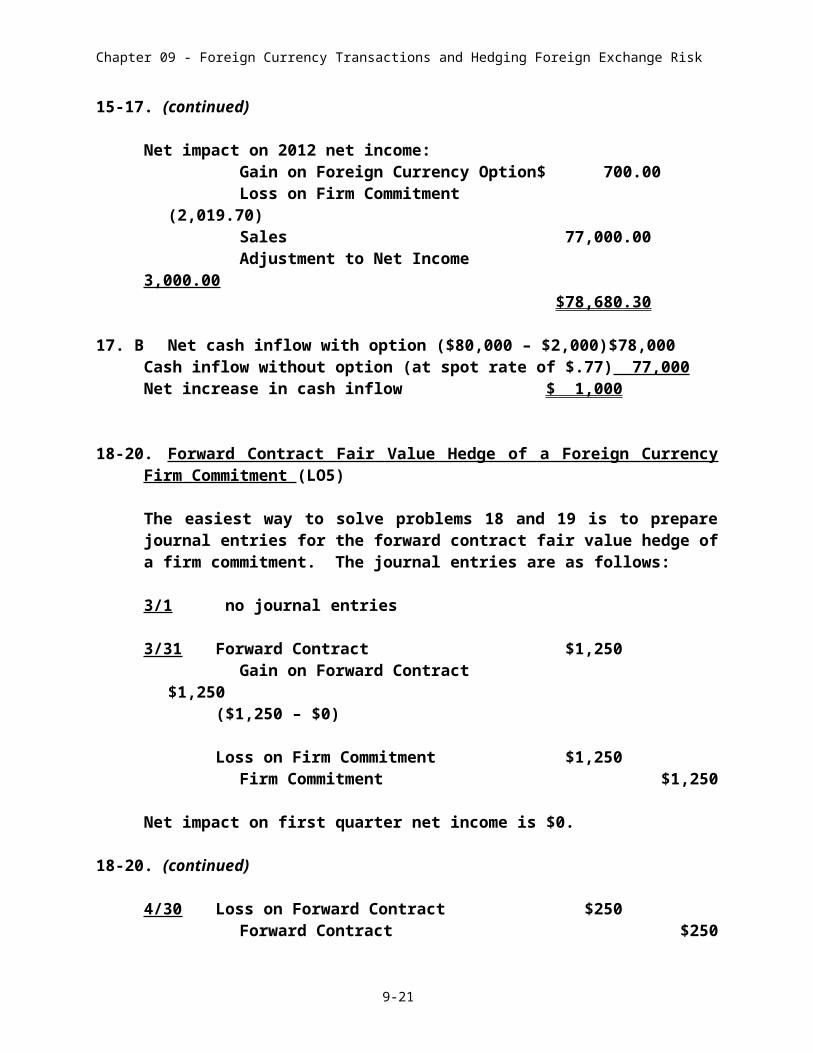

15-17. (continued)

Net impact on 2012 net income:Gain on Foreign Currency Option $ 700.00Loss on Firm Commitment (2,019.70)Sales 77,000.00Adjustment to Net Income 3,000 .00

$78,680 .30

17. B Net cash inflow with option ($80,000 – $2,000) $78,000Cash inflow without option (at spot rate of $.77) 77,000Net increase in cash inflow $ 1,000

18-20. Forward Contract Fair Value Hedge of a Foreign Currency Firm Commitment (LO5)

The easiest way to solve problems 18 and 19 is to prepare journal entries for the forward contract fair value hedge of a firm commitment. The journal entries are as follows:

3/1 no journal entries

3/31 Forward Contract $1,250Gain on Forward Contract $1,250

($1,250 – $0)

Loss on Firm Commitment $1,250Firm Commitment $1,250

Net impact on first quarter net income is $0.

18-20. (continued)

4/30 Loss on Forward Contract $250Forward Contract $250[Fair value of forward contract is ($.120 – $.118) x 500,000 = $1,000; $1,000 – $1,250 = $250]

Firm Commitment $250Gain on Firm Commitment $250

Foreign Currency (pesos) $59,000Sales [500,000 pesos x $.118] $59,000

9-19

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Cash [500,000 x $.120] $60,000Foreign Currency (pesos) $59,000Forward Contract 1,000

Firm Commitment $1,000Adjustment to Net Income $1,000

Net impact on second quarter net income is: Sales $59,000 – Loss on Forward Contract $250 + Gain on Firm Commitment $250 + Adjustment to Net Income $1,000 = $60,000.

18. A

19. C

20. B Cash inflow with forward contract [500,000 pesos x $.12] $60,000Cash inflow without forward contract [500,000 pesos x $.118] 59,000Net increase in cash flow from forward contract $ 1,000

21-22.Option Cash Flow Hedge of a Forecasted Foreign Currency Transaction (LO6)

The easiest way to solve problems 21 and 22 is to prepare journal entries for the option cash flow hedge of a forecasted transaction. The journal entries are as follows:

11/1/11Foreign Currency Option $1,500

Cash $1,500

12/31/11Option Expense $400

Foreign Currency Option $400(The option has no intrinsic value at 12/31/11 so the entire change in fair value is due to a change in time value; $1,500 – $1,100 = $400 decrease in time value. The decrease in time value of the option is recognized as an expense in net income.)

Option Expense decreases net income by $400.

2/1/12Option Expense $1,100Foreign Currency Option 900

Accumulated Other Comprehensive Income (AOCI) $2,000

9-20

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

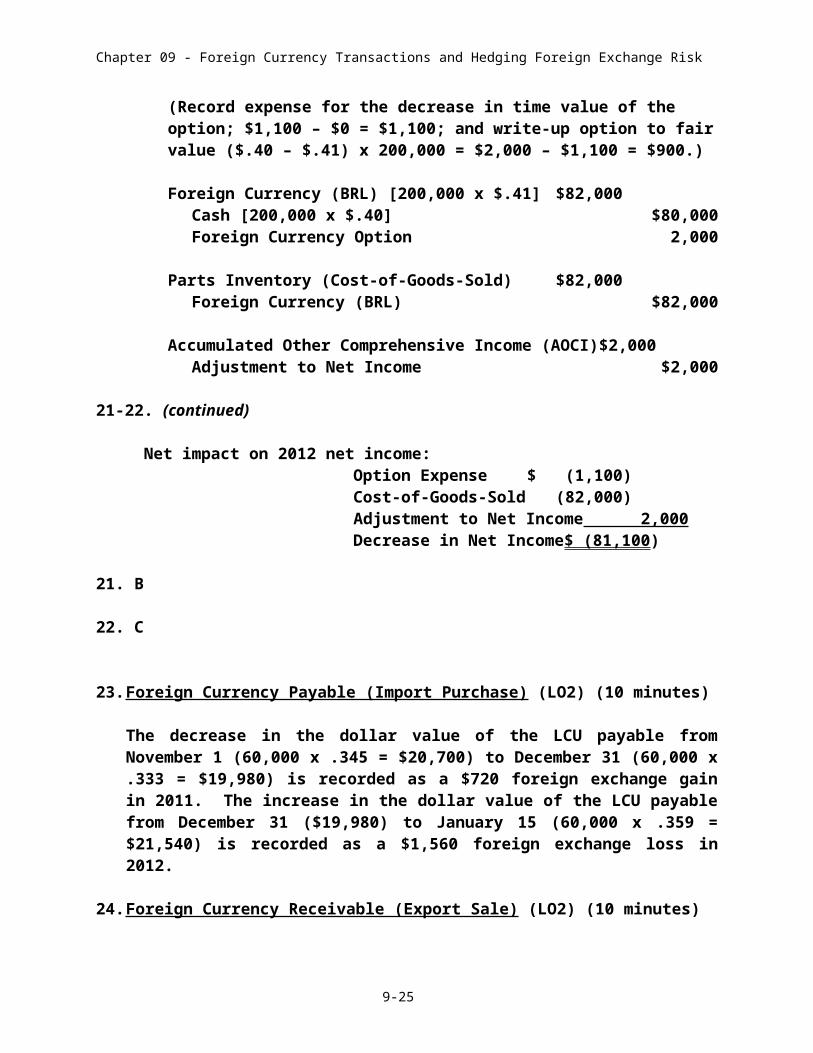

(Record expense for the decrease in time value of the option; $1,100 – $0 = $1,100; and write-up option to fair value ($.40 – $.41) x 200,000 = $2,000 – $1,100 = $900.)

Foreign Currency (BRL) [200,000 x $.41] $82,000Cash [200,000 x $.40] $80,000Foreign Currency Option 2,000

Parts Inventory (Cost-of-Goods-Sold) $82,000Foreign Currency (BRL) $82,000

Accumulated Other Comprehensive Income (AOCI) $2,000Adjustment to Net Income $2,000

21-22. (continued)

Net impact on 2012 net income:Option Expense $ (1,100)Cost-of-Goods-Sold (82,000)Adjustment to Net Income 2,000Decrease in Net Income $ (81,100)

21. B

22. C

23. Foreign Currency Payable (Import Purchase) (LO2) (10 minutes)

The decrease in the dollar value of the LCU payable from November 1 (60,000 x .345 = $20,700) to December 31 (60,000 x .333 = $19,980) is recorded as a $720 foreign exchange gain in 2011. The increase in the dollar value of the LCU payable from December 31 ($19,980) to January 15 (60,000 x .359 = $21,540) is recorded as a $1,560 foreign exchange loss in 2012.

24. Foreign Currency Receivable (Export Sale) (LO2) (10 minutes)

The ostra receivable decreases in dollar value from (50,000 x $1.05) $52,500 at December 20 to $51,000 (50,000 x $1.02) at December 31, resulting in a foreign exchange loss of $1,500 in 2011. The further decrease in dollar value of the ostra receivable from $51,000 at December 31 to $49,000 (50,000 x $.98) at January 10 results in an additional $2,000 foreign exchange loss in 2012.

25. Foreign Currency Receivable (Export Sale) (LO2) (10 minutes)

9-21

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

9/15 Accounts Receivable (FCU) [100,000 x $.40] $40,000 Sales $40,000

9/30 Accounts Receivable (FCU) $2,000Foreign exchange Gain $2,000

[100,000 x ($.42 – $.40)]

10/15 Foreign Exchange Loss $5,000Accounts Receivable (FCU)

[100,000 x ($.37 – $.42)] $5,000

Cash $37,000Accounts Receivable (FCU) $37,000

26. Foreign Currency Payable (Import Purchase) (LO2) (10 minutes)

12/1/11 Inventory $52,800Accounts Payable (LCU) [60,000 x $.88] $52,800

12/31/11 Accounts Payable (LCU) [60,000 x ($.82 – $.88)] $3,600Foreign Exchange Gain $3,600

1/28/12 Foreign Exchange Loss $4,800 Accounts Payable (LCU) [60,000 x ($.90 – $.82)] $4,800

Accounts payable (LCU) $54,000Cash $54,000

27. Determine U.S. Dollar Balance for Foreign Currency Transactions (LO2) (15 minutes)

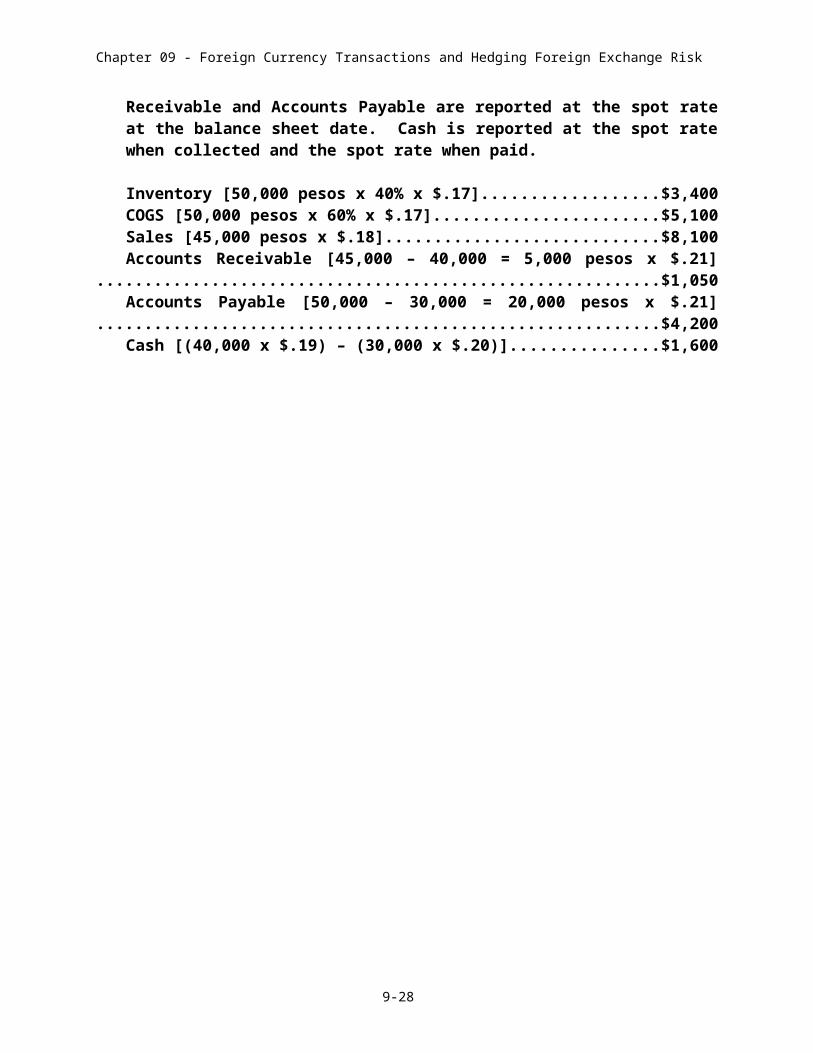

Inventory and Cost of Goods Sold are reported at the spot rate at the date the inventory was purchased. Sales are reported at the spot rate at the date of sale. Accounts Receivable and Accounts Payable are reported at the spot rate at the balance sheet date. Cash is reported at the spot rate when collected and the spot rate when paid.

Inventory [50,000 pesos x 40% x $.17].........................................................$3,400COGS [50,000 pesos x 60% x $.17]...............................................................$5,100Sales [45,000 pesos x $.18]...........................................................................$8,100Accounts Receivable [45,000 – 40,000 = 5,000 pesos x $.21]....................$1,050Accounts Payable [50,000 – 30,000 = 20,000 pesos x $.21].......................$4,200Cash [(40,000 x $.19) – (30,000 x $.20)]........................................................$1,600

9-22

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

28. Prepare Journal Entries for Foreign Currency Transactions (LO2) (25 minutes)

2/1/11 Equipment $17,600Accounts Payable (L) [40,000 x $.44] $17,600

4/1/11 Accounts Payable (L) $17,600Foreign Exchange Loss 400

Cash [40,000 x $.45] $18,000

6/1/11 Inventory $14,100Accounts Payable (L) [30,000 x $.47] $14,100

8/1/11 Accounts Receivable (L) [40,000 x $.48] $19,200Sales $19,200

Cost of Goods Sold $9,870Inventory [$14,100 x 70%] $9,870

10/1/11 Cash [30,000 x $.49] $14,700Accounts Receivable (L) [$19,200 x 3/4] $14,400

Foreign Exchange Gain 300

11/1/11 Accounts Payable (L) [$14,100 x 2/3] $9,400Foreign Exchange Loss [20,000 x ($.50 – $.47)] 600

Cash [20,000 x $.50] $10,000

12/31/11 Foreign Exchange Loss $500Accounts Payable (L) [10,000 x ($.52 – $.47)] $500

Accounts receivable (L) [10,000 x ($.52 – $.48)] $400Foreign Exchange Gain $400

2/1/12 Cash [10,000 x $.54] $5,400Accounts Receivable (L) [10,000 x $.52] $5,200Foreign Exchange Gain 200

3/1/12 Accounts Payable (L) [10,000 x $.52] $5,200Foreign Exchange Loss 300Cash [10,000 x $.55] $5,500

29. Determine Income Effect of Foreign Currency Payable (Import Purchase) (LO2)

(20 minutes)

9-23

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

a. Benjamin, Inc. has a liability of AL 160,000. On the date that this liability

9-24

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

was created (December 1, 2011), the liability had a dollar value of $70,400 (AL 160,000 x $.44). On December 31, 2011, the dollar value has risen to $76,800 (AL 160,000 x $.48). The increase in the dollar value of the liability creates a foreign exchange loss of $6,400 ($76,800 – $70,400) in 2011.

By March 1, 2012, when the liability is paid, the dollar value has dropped to $72,000 (AL 160,000 x $.45) creating a foreign exchange gain of $4,800 ($72,000 – $76,800) to be reported in 2012.

b. Benjamin, Inc. has a liability of AL 160,000. On the date that this liability was created (September 1, 2011), the liability had a dollar value of $73,600 (AL 160,000 x $.46). On December 1, 2011, when the liability is paid, the dollar value has decreased to $70,400 (AL 160,000 x $.44). The drop in the dollar value of the liability creates a foreign exchange gain of $3,200 ($70,400 – $73,600) in 2011.

c. Benjamin, Inc. has a liability of AL 160,000. On the date that this liability was created (September 1, 2011), the liability had a dollar value of $73,600 (AL 160,000 x $.46). On December 31, 2011, the dollar value has risen to $76,800 (AL 160,000 x $.48). The increase in the dollar value of the liability creates a foreign exchange loss of $3,200 ($76,800 – $73,600) in 2011.By March 1, 2012, when the liability is paid, the dollar value has dropped to $72,000 (AL 160,000 x $.45) creating a foreign exchange gain of $4,800 ($72,000 – $76,800) to be reported in 2012.

30. Foreign Currency Borrowing (LO7) (30 minutes)

a. 9/30/11 Cash $100,000Note Payable (dudek) [1,000,000 x $.10] $100,000

(To record the note and conversion of 1 million dudeks into $ at the spot rate.)

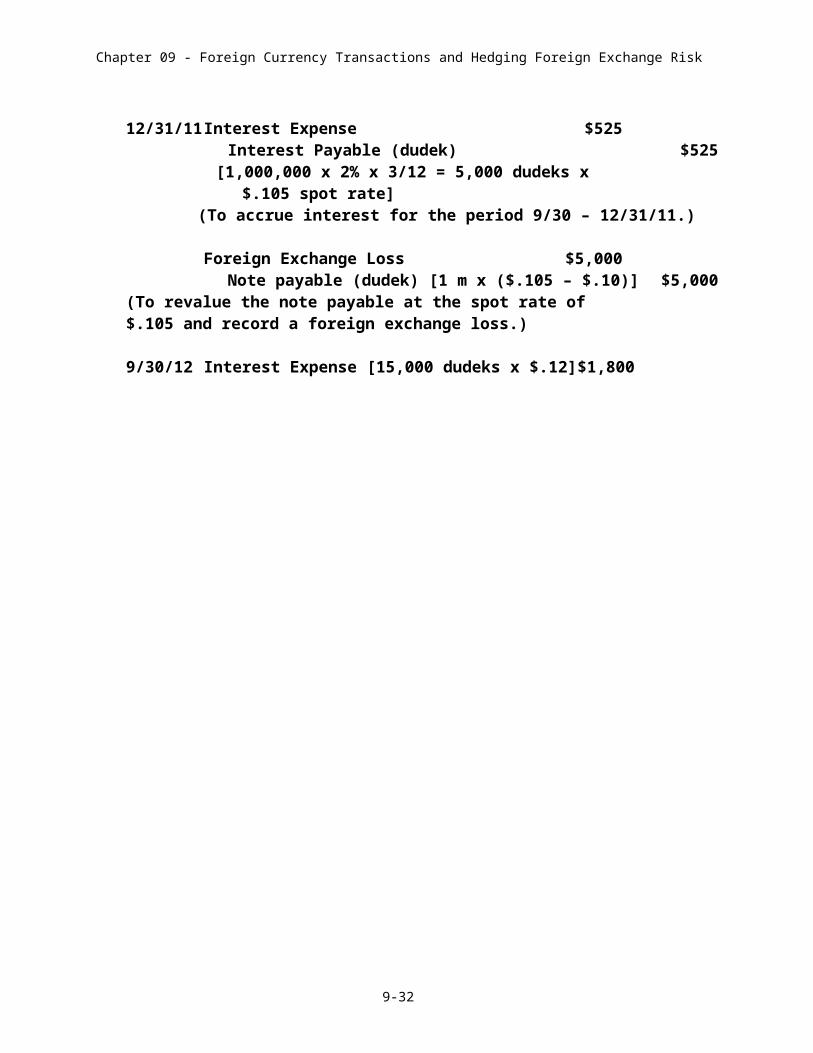

12/31/11 Interest Expense $525 Interest Payable (dudek) $525

[1,000,000 x 2% x 3/12 = 5,000 dudeks x $.105 spot rate]

(To accrue interest for the period 9/30 – 12/31/11.)

Foreign Exchange Loss $5,000Note payable (dudek) [1 m x ($.105 – $.10)] $5,000

(To revalue the note payable at the spot rate of $.105 and record a foreign exchange loss.) 9/30/12 Interest Expense [15,000 dudeks x $.12] $1,800

9-25

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Interest Payable (dudek) 525Foreign Exchange Loss [5,000 dudeks x ($.12 – $.105)] 75

Cash [20,000 dudeks x $.12] $2,400(To record the first annual interest payment, record interest expense for the period 1/1 – 9/30/12, and record a foreign exchange loss on the interest payable accrued at 12/31/11.)

12/31/12 Interest Expense $625Interest Payable (dudek) [5,000 dudeks x $.125] $625

(To accrue interest for the period 9/30 – 12/31/12.)

Foreign Exchange Loss $20,000Note Payable (dudek) [1 m x ($.125 – $.105)] $20,000

(To revalue the note payable at the spot rate of $.125 and record a foreign exchange loss.)

30. (continued)

9/30/13 Interest Expense [15,000 dudeks x $.15] $2,250Interest Payable (dudek) 625Foreign Exchange Loss [5,000 dudeks x ($.15 – $.125)] 125

Cash [20,000 dudeks x $.15] $3,000(To record the second annual interest payment,record interest expense for the period 1/1 – 9/30/13,and record a foreign exchange loss on the interestpayable accrued at 12/31/12.)

Note Payable (dudek) $125,000Foreign Exchange Loss 25,000

Cash [1 m dudeks x $.15] $150,000(To record payment of the 1 million dudek note.)

b. The effective cost of borrowing can be determined by considering the total interest expense and foreign exchange losses related to the loan and comparing this with the amount borrowed:

2011Interest expense $525Foreign exchange loss 5,000Total $5,525 / $100,000 = 5.525% for 3 months =

= 22.1% for 12 months

9-26

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

2012Interest expense $2,425Foreign exchange losses 20,075Total $22,500 / $100,000 = 22.5% for 12 months

2013Interest expense $2,250Foreign exchange losses 25,125Total $27,375 / $100,000 = 27.38% for 9 months

= 36.5% for 12 months

= 36.5% for 12 monthsBecause of appreciation in the value of the dudek, the effective annual borrowing costs range from 22.1% – 36.5%.

30. (continued)

The net cash flow from this borrowing is:

Cash outflows:Interest ($2,400 + $3,000) $5,400 Principal 150,000

$155,400

Cash inflow:Borrowing (100,000)Net cash outflow $ 55,400

Ignoring compounding, this results in an effective borrowing cost of approximately 27.7% per year [$55,400 / $100,000 = 55.4% over two years / 2 years = 27.7% per year].

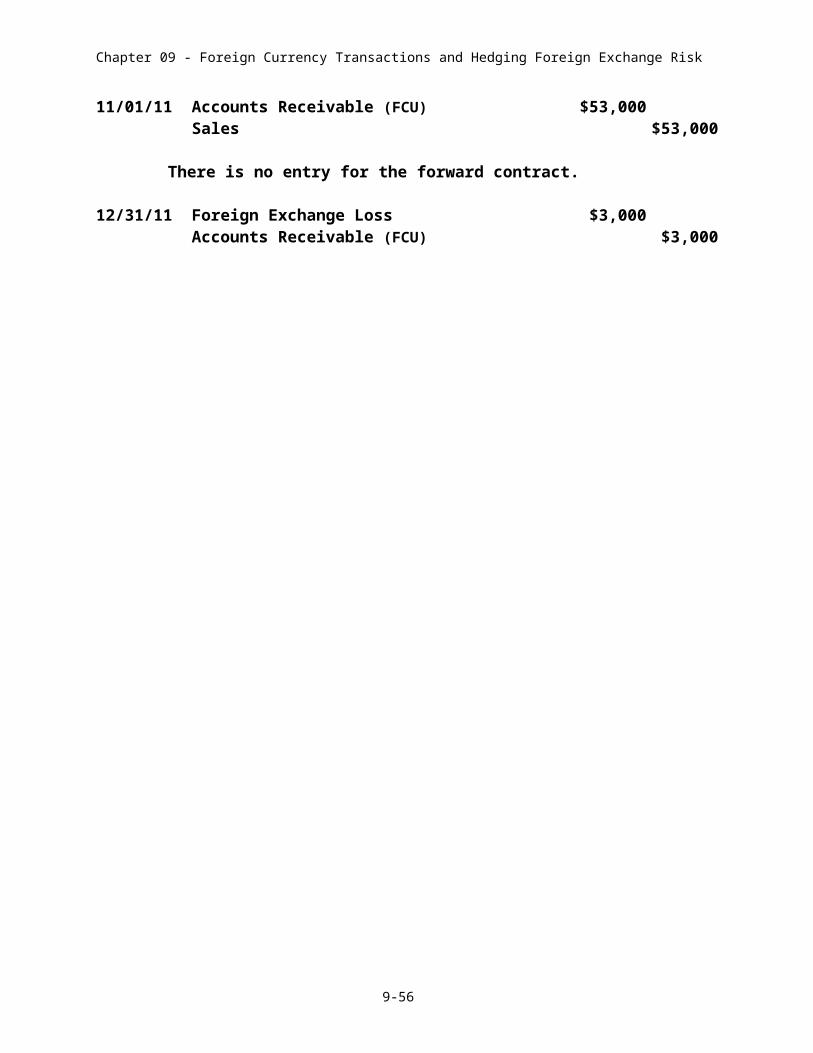

31. Forward Contract Hedge of Foreign Currency Receivable (LO4) (40 minutes)

a. Cash Flow Hedge

12/1/11 Accounts Receivable (K) [20,000 x $2.00] $40,000Sales $40,000

No entry for the forward contract.

12/31/11 Accounts Receivable (K) $2,000Foreign Exchange Gain $2,000

[20,000 x ($2.10-$2.00)]

9-27

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

AOCI $2,450.75Forward Contract $2,450.75

[20,000 x ($2.075 – $2.20) = $2,500 x .9803 = $2,450.75]

Loss on Forward Contract $2,000AOCI $2,000

AOCI $500Premium Revenue $500

[20,000 x ($2.075 – $2.00) = $1,500 x 1/3 = $500]

31. (continued)

Impact on 2011 income:Sales $40,000Foreign Exchange Gain 2,000Loss on Forward Contract (2,000)Premium Revenue 500Total $40,500

3/1/12 Accounts Receivable (K) $3,000Foreign Exchange Gain $3,000

[20,000 x ($2.25 – $2.10)]

AOCI $1,049.25Forward Contract

$1,049.25 [20,000 x ($2.25 – $2.075) = $3,500 – 2,450.75] = $1,049.25

Loss on Forward Contract $3,000AOCI $3,000

AOCI $1,000Premium Revenue $1,000

[$1,500 x 2/3 = $1,000]

Foreign Currency (K) [20,000 x $2.25] $45,000Accounts Receivable (K) $45,000

Cash [20,000 x $2.075] $41,500Forward Contract 3,500

Foreign Currency (K) $45,000

Impact on 2012 income:Foreign Exchange Gain $3,000

9-28

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Loss on Forward Contract (3,000)Premium Revenue 1,000Total $1,000

Impact on net income over both periods: $40,500 + $1,000 = $(41,500); equal to cash inflow.

31. (continued)

b. Fair Value Hedge 12/1/11 Accounts Receivable (K) [20,000 x $2.00] $40,000

Sales $40,000

No entry for the forward contract.

12/31/11 Accounts Receivable (K) $2,000Foreign Exchange Gain $2,000

[20,000 x ($2.10 – $2.00)]

Loss on Forward Contract $2,450.75Forward contract $2,450.75

[20,000 x ($2.075 – $2.20) = $2,500 x .9803 = $2,450.75]

Impact on 2011 income:Sales $40,000.00Foreign exchange gain 2,000.00Loss on forward contract (2,450 .75 )Total $39,549 .25

3/1/12 Accounts Receivable (K) $3,000Foreign Exchange Gain $3,000

[20,000 x ($2.25 – $2.10)]

Loss on Forward Contract $1,049.25Forward Contract $1,049.25

[20,000 x (2.25 – $2.075) = $3,500 – 2,450.75 = $1,049.25]

Foreign Currency (K) [20,000 x $2.25] $45,000Accounts Receivable (K) $45,000

Cash [20,000 x $2.075] $41,500Forward Contract 3,500

Foreign Currency (K) $45,000

9-29

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Impact on 2012 income:Foreign Exchange Gain $3,000.00Loss on Forward Contract (1,049 .25 )Total $1,950 .75

Impact on net income over both periods: $39,549.25 + $1,950.75 = $41,500; equal to cash inflow.

32. Forward Contract Hedge of Foreign Currency Payable (LO4) (40 minutes)

a. Cash Flow Hedge

12/1/11Parts Inventory (COGS) $40,000Accounts Payable (K) $40,000

[20,000 x $2.00]

No entry for the Forward Contract.

12/31/11 Foreign Exchange Loss $2,000Accounts Payable (K) $2,000

[20,000 x ($2.10 – $2.00)]

Forward Contract $2,450.75AOCI $2,450.75

[20,000 x ($2.075 – $2.20) = $2,500 x .9803 = $2,450.75]

AOCI $2,000Gain on Forward Contract $2,000

Premium Expense $500AOCI $500

[20,000 x ($2.075 – $2.00) = $1,500 x 1/3 = $500]

Impact on 2011 income:Parts Inventory (COGS) $(40,000)Foreign Exchange Loss (2,000)Gain on forward contract 2,000Premium Expense (500)Total $(40,500)

32. (continued)

3/1/12 Foreign Exchange Loss $3,000Accounts Payable (K) $3,000

9-30

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

[20,000 x ($2.25 – $2.10)]

Forward Contract $1,049.25AOCI $1,049.25

[20,000 x ($2.25 – $2.075) = $3,500 – 2,450.75 = $1,049.25]

AOCI $3,000Gain on Forward Contract $3,000

Premium Expense $1,000AOCI $1,000

[$1,500 x 2/3 = $1,000]

Foreign Currency (K) [20,000 x $2.25] $45,000Cash $41,500Forward Contract 3,500

Accounts Payable (K) $45,000Foreign currency (K) $45,000

Impact on 2012 income:Foreign Exchange Loss $(3,000)Loss on Forward Contract 3,000Premium revenue (1,000)Total $(1,000)

Impact on net income over both periods: $(40,500) + $(1,000) = $(41,500); equal to cash outflow.

32. (continued)

b. Fair Value Hedge

12/1/11Parts Inventory (COGS) $40,000Accounts Payable (K) $40,000

[20,000 x $2.00]

No entry for the forward contract.

12/31/11 Foreign Exchange Loss $2,000Accounts Payable (K) $2,000

[20,000 x ($2.10 – $2.00)]

9-31

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Forward Contract $2,450.75Gain on Forward Contract $2,450.75

[20,000 x ($2.075 – $2.20) = $2,500 x .9803 = $2,450.75]

Impact on 2011 income:Parts Inventory (COGS) $(40,000.00)Foreign Exchange Loss (2,000.00)Gain on forward contract 2,450 .75 Total $(39,549 .25 )

3/1/12 Foreign Exchange Loss $3,000Accounts Payable (K) $3,000

[20,000 x ($2.25 – $2.10)]

Forward Contract $1,049.25Gain on Forward Contract $1,049.25

[20,000 x ($2.25 – $2.075) = $3,500 – 2,450.75 = $1,049.25]

Foreign Currency (K) [20,000 x $2.25] $45,000Cash $41,500Forward Contract 3,500

Accounts Payable (K) $45,000Foreign currency (K) $45,000

32. (continued)

Impact on 2012 income:Foreign Exchange Loss $(3,000.00)Gain on Forward Contract 1,049 .25 Total $(1,950 .75 )

Impact on net income over both periods: $(39,549.25) + $(1,950.75) = $(41,500.00); equal to cash outflow.

33. Option Hedge of Foreign Currency Receivable (LO4) (30 minutes)

a. Cash Flow Hedge

6/1 Accounts Receivable (P) $45,000Sales [$.045 x 1,000,000 pesos] $45,000

9-32

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Foreign Currency Option $2,000Cash

$2,000

6/30 Accounts Receivable (P) $3,000Foreign Exchange Gain

[($.048 – $.045) x 1,000,000] $3,000

Accumulated Other Comprehensive Income (AOCI) $200

Foreign Currency Option $200 [($.0018 – $.0020) x 1,000,000]

Loss on Foreign Currency Option $3,000Accumulated Other Comprehensive Income (AOCI) $3,000

Option Expense $200Accumulated Other Comprehensive

Income (AOCI) $200

Date Fair Value Intrinsic Value Time Value Change in Time Value6/1 $2,000 $0 $2,000 – 6/30 $1,800 $0 $1,800 –$ 2009/1 $1,000 $1,000 $0 –$1,800

33. (continued)

9/1 Foreign Exchange Loss $4,000Accounts Receivable (P) $4,000

[($.044 – $.048) x 1,000,000]

Accumulated Other Comprehensive Income (AOCI) $800

Foreign Currency Option $800 [$1,800 – $1,000]

Accumulated Other Comprehensive Income (AOCI) $4,000

Gain on Foreign Currency Option $4,000

Option Expense $1,800Accumulated Other Comprehensive

Income (AOCI) $1,800 (Change in time value of option recognized as expense)

9-33

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

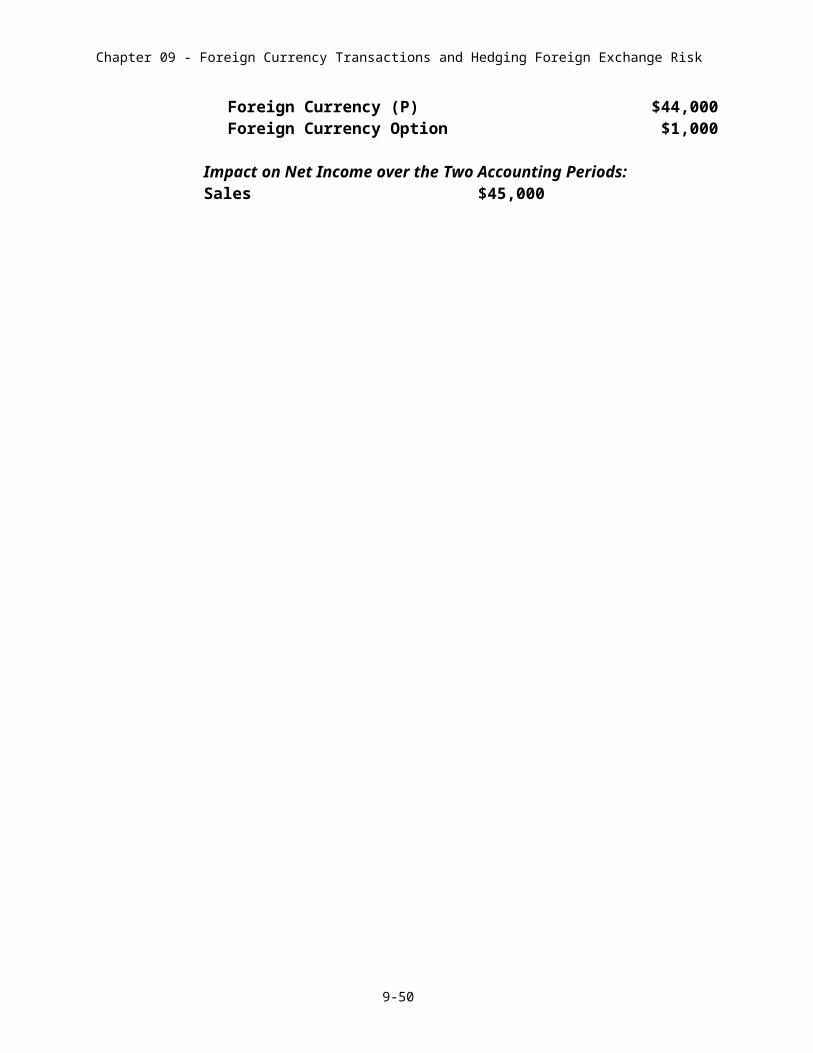

Foreign Currency (P) $44,000Accounts Receivable (P) $44,000

Cash $45,000Foreign Currency (P) $44,000Foreign Currency Option $1,000

Over the two accounting periods, Sales are $45,000 and Option Expense is $2,000. Net increase in cash is $43,000.

b. Fair Value Hedge

6/1 Accounts Receivable (P) $45,000Sales [$.045 x 1,000,000] $45,000

Foreign Currency Option $2,000Cash $2,000

6/30 Accounts Receivable (P) $3,000Foreign Exchange Gain $3,000

[($.048 – $.045) x 1,000,000]

Loss on Foreign Currency Option $200Foreign Currency Option $200

33. (continued)

9/1 Foreign Exchange Loss $4,000Accounts Receivable (P) $4,000

[($.044 – $.048) x 1,000,000]

Loss on Foreign Currency Option $800Foreign Currency Option $800

Foreign Currency (P) $44,000Accounts Receivable (P) $44,000

Cash $45,000Foreign Currency (P) $44,000Foreign Currency Option $1,000

Impact on Net Income over the Two Accounting Periods:Sales $45,000

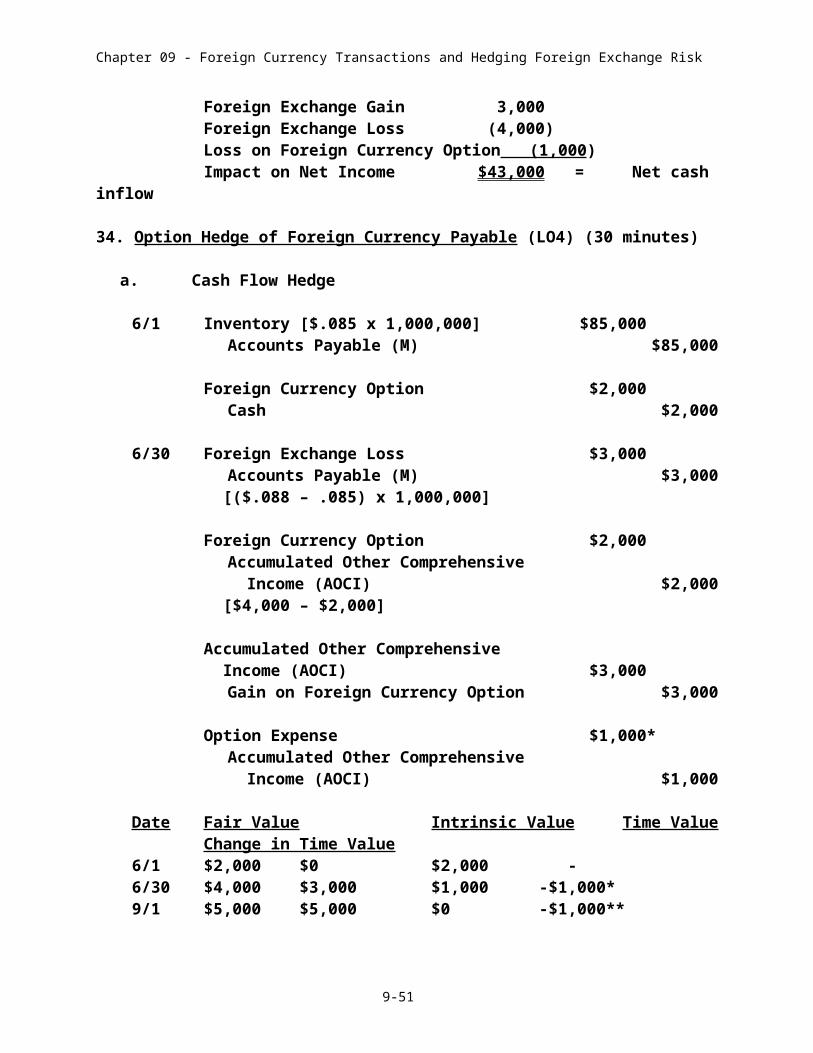

9-34

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Foreign Exchange Gain 3,000Foreign Exchange Loss (4,000)Loss on Foreign Currency Option (1,000)Impact on Net Income $43,000 = Net cash inflow

34. Option Hedge of Foreign Currency Payable (LO4) (30 minutes)

a. Cash Flow Hedge

6/1 Inventory [$.085 x 1,000,000] $85,000Accounts Payable (M) $85,000

Foreign Currency Option $2,000Cash $2,000

6/30 Foreign Exchange Loss $3,000Accounts Payable (M) $3,000

[($.088 – .085) x 1,000,000]

Foreign Currency Option $2,000Accumulated Other Comprehensive

Income (AOCI) $2,000 [$4,000 – $2,000]

Accumulated Other Comprehensive Income (AOCI) $3,000

Gain on Foreign Currency Option $3,000

Option Expense $1,000*Accumulated Other Comprehensive Income (AOCI) $1,000

Date Fair Value Intrinsic Value Time Value Change in Time Value6/1 $2,000 $0 $2,000 - 6/30 $4,000 $3,000 $1,000 -$1,000*9/1 $5,000 $5,000 $0 -$1,000**

34. (continued)

9/1 Foreign Exchange Loss $2,000Accounts Payable (M) $2,000

[($.09 – $.088) x 1,000,000]

Foreign Currency Option $1,000

9-35

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Accumulated Other Comprehensive Income (AOCI) $1,000

[$5,000 – $4,000]

Accumulated Other Comprehensive Income (AOCI) $2,000

Gain on Foreign Currency Option $2,000

Option Expense $1,000**Accumulated Other Comprehensive Income (AOCI) $1,000

Foreign Currency (M) $90,000Cash $85,000Foreign Currency Option $5,000

Accounts Payable (M) $90,000Foreign Currency (M) $90,000

Impact on net income:Option Expense $ 2,000Inventory (Cost of Goods Sold) 85,000Cash outflow $87,000

34. (continued)

b. Fair Value Hedge

6/1 Inventory $85,000Accounts Payable (M) $85,000

[$.085 x 1,000,000]

Foreign Currency Option $2,000Cash $2,000

6/30 Foreign Exchange Loss $3,000Accounts Payable (M) $3,000

[($.088 – $.085) x 1,000,000]

Foreign Currency Option $2,000Gain on Foreign Currency Option $2,000

[$4,000 – $2,000]

9/1 Foreign Exchange Loss $2,000

9-36

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Accounts Payable (M) $2,000 [($.09 – $.088) x 1,000,000]

Foreign Currency Option $1,000Gain on Foreign Currency Option $1,000

[$5,000 – $4,000]

Foreign Currency (M) $90,000Cash $85,000Foreign Currency Option $5,000

Accounts Payable (M) $90,000Foreign currency (M) $90,000

Impact on net income:Foreign Exchange Loss ($5,000)Gain on Foreign Currency Option 3,000 Impact on net income ($2,000)Inventory 85,000Cash Outflow $87,000

35. Forward Contract Cash Flow Hedge of Foreign Currency Denominated Asset (LO4) (30 minutes)

Account Receivable (FCU) Forward Forward Contract Spot U.S. Dollar Change in U.S. Rate to Change in

Date Rate Value Dollar Value 4/30/10 Fair Value Fair Value11/01/11 $.53 $53,000 - $.52 $0 -12/31/11 $.50 $50,000 -$3,000 $.48 $3,8441 +$3,8444/30/12 $.49 $49,000 -$1,000 $.49 $3,0002 - $ 844

1 $52,000 – $48,000 = $(4,000) x .961 = $3,844; where .961 is the present value factor for four months at an annual interest rate of 12% (1% per month) calculated as 1/1.014.2 $52,000 – $49,000 = $3,000.

2011 Journal Entries

11/01/11 Accounts Receivable (FCU) $53,000Sales $53,000

There is no entry for the forward contract.

12/31/11 Foreign Exchange Loss $3,000Accounts Receivable (FCU) $3,000

9-37

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Accumulated Other Comprehensive Income (AOCI) $3,000Gain on Forward Contract $3,000

Forward Contract $3,844Accumulated Other Comprehensive Income (AOCI) $3,844

Discount Expense $333.33Accumulated Other Comprehensive Income (AOCI) $333.33

[100,000 x ($.53 – $.52) = $1,000 x 2/6 = $333.33]

The impact on net income for the year 2011 is:

Sales $53,000.00Foreign Exchange Loss (3,000.00)Gain on Forward Contract 3,000 .00 Net gain (loss) 0.00Discount Expense (333 .33 )Impact on net income $52,666 .67

35. (continued)

2012 Journal Entries

4/30/12 Foreign Exchange Loss $1,000Accounts Receivable (FCU) $1,000

Accumulated Other Comprehensive Income (AOCI) $1,000Gain on Forward Contract $1,000

Accumulated Other Comprehensive Income (AOCI) $844Forward Contract $844

Discount Expense $666.67Accumulated Other Comprehensive Income (AOCI) $666.67

Foreign Currency (FCU) $49,000Accounts Receivable (FCU) $49,000

Cash $52,000Foreign Currency (FCU) $49,000Forward Contract $3,000

The impact on net income for the year 2012 is:

Foreign Exchange Loss $(1,000.00)

9-38

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Gain on Forward Contract 1,000 .00 Net gain (loss) 0.00Discount Expense (666 .67 )Impact on net income $(666 .67)

36. Forward Contract Fair Value Hedge of Net Foreign Currency Denominated Asset (LO4) (30 minutes)

Account Receivable (Payable) (mongs)Forward Forward Contract Change in U.S. Rate to Change in

Date U.S. Dollar Value Dollar Value 1/31/12 Fair Value Fair Value11/30/11 $265,000 ($159,000) - $.52 $0 -12/31/11 $250,000 ($150,000) -$15,000 (-$9,000) $.48 $7,9211 +$7,9211/31/12 $245,000 ($147,000) -$ 5,000 (-$3,000) $.49 $6,0002 - $1,921

1 $104,000 – $96,000 = $(8,000) x .9901 = $7,921; where .9901 is the present value factor for one month at an annual interest rate of 12% (1% per month) calculated as 1/1.01.2 $104,000 – $98,000 = $6,000.

2011 Journal Entries

11/30 Accounts Receivable (mongs) $265,000Sales $265,000

[$.53 x 500,000 mongs]

Inventory $159,000Accounts Payable $159,000

[$.53 x 300,000 mongs]

There is no formal entry for the Forward Contract.

12/31 Foreign Exchange Loss $15,000Accounts Receivable (mongs) $15,000

Accounts Payable (mongs) $9,000Foreign Exchange Gain $9,000

Forward Contract $7,921Gain on Forward Contract $7,921

The impact on net income for the year 2011 is:

Sales $265,000Net Foreign Exchange Loss $ (6,000)Gain on Forward Contract 7,921

9-39

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Net gain (loss) 1,921Impact on net income $266,921

36. (continued)

2012 Journal Entries

1/31 Foreign Exchange Loss $5,000Accounts Receivable (mongs) $5,000

Accounts Payable (mongs) $3,000Foreign Exchange Gain $3,000

Loss on Forward Contract $1,921Forward Contract $1,921

Foreign Currency (mongs) $245,000Accounts Receivable (mongs) $245,000

Accounts Payable (mongs) $147,000Foreign Currency (mongs) $147,000

Cash $104,000Foreign Currency (mongs) $98,000Forward Contract $6,000

The impact on net income for the year 2012 is:

Net Foreign Exchange Loss $(2,000)Loss on Forward Contract (1,921)Impact on net income $(3,921)

The net effect on the balance sheet is an increase in cash of $104,000 and an increase in inventory of $159,000 with a corresponding increase in retained earnings of $263,000 ($266,921 – $3,921).

37. Forward Contract Fair Value Hedge (LO4, LO5) (40 minutes)

a. Foreign Currency Receivable

10/01 Accounts Receivable (LCU) $69,000Sales (100,000 LCUs x $.69) $69,000

There is no formal entry for the forward contract.

9-40

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

12/31 Accounts Receivable (LCU) $2,000Foreign Exchange Gain $2,000

[($.71 – $.69) x 100,000]

Loss on Forward Contract $8,910.90Forward Contract $8,910.90

[($.74 – $.65) x 100,000 = $ 9,000 x .9901 = $ 8,910.90]

1/31 Accounts Receivable (LCU) $1,000Foreign Exchange Gain $1,000

[($.72 – $.71) x 100,000]

Forward Contract $ 1,910.90Gain on Forward Contract $ 1,910.90

[($.72 – $.65) x 100,000 = $ 7,000 loss – 8,910.90 = $ 1,910.90 gain]

Foreign Currency (LCU) $72,000Accounts Receivable (LCU) $72,000

Cash $65,000Forward Contract $7,000

Foreign Currency (LCU) $72,000

The impact on net income:

Sale $69,000.00Foreign Exchange Gain 3,000.00Loss on Forward Contract (8,910.90)Gain on Forward Contract 1,910 .90 Impact on net income $65,000 .00 = Cash Inflow

37. (continued)

b. Foreign Currency Firm Commitment (Sale)

10/01 There is no entry to record either the sales agreement or the forward contract as both are executory contracts.

12/31 Loss on Forward Contract $8,910.90Forward Contract $8,910.90

Firm Commitment $8,910.90Gain on Firm Commitment $8,910.90

9-41

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

1/31 Forward Contract $1,910.90Gain on Forward Contract $1,910.90

Loss on Firm Commitment $1,910.90Firm Commitment $1,910.90

Foreign Currency (LCU) $72,000Sales $72,000

Cash $65,000Forward Contract $7,000

Foreign Currency (LCU) $72,000

Adjustment to Net Income $7,000Firm Commitment $7,000

Impact on Net Income:

Sales $72,000Net loss on Forward Contract (7,000)Net gain on Firm Commitment 7,000Adjustment to Net Income (7,000)

$65,000 = Cash Inflow

38. Forward Contract Fair Value Hedge of a Foreign Currency Firm Commitment (Purchase) (LO5) (30 minutes)

Forward Forward Contract Firm CommitmentRate to Change in Change in

Date 10/31 Fair Value Fair Value Fair Value Fair Value8/1 $.30 $0 - $0 $0 -9/30 $.325 $4,950.501 + $4,950.50 $(4,950.50)1 – $4,950.5010/31 $.320 (spot) $4,0002 – $ 950.50 $(4,000)2 + $ 950.50

1 ($65,000 – $60,000) = $5,000 x .9901 = $4,950.5; where .9901 is the present value factor for one month at an annual interest rate of 12% (1% per month) calculated as 1/1.01.2 ($64,000 – $60,000) = $4,000.

8/1 There is no entry to record either the purchase agreement or the forward contract as both are executory contracts.

9/30 Forward Contract $4,950.50Gain on Forward Contract $4,950.50

Loss on Firm Commitment $4,950.50

9-42

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Firm Commitment $4,950.50

10/31 Loss on Forward Contract $950.50Forward Contract $950.50

Firm Commitment $950.50Gain on Firm Commitment $950.50

Foreign Currency (rupees) $64,000Cash $60,000Forward Contract 4,000

Inventories (Cost-of-goods-sold) $64,000Foreign Currency (rupees) $64,000

Firm Commitment $4,000Adjustment to Net Income $4,000

The net cash outflow is $60,000. Assuming the inventory is sold in the fourth quarter, the net impact on net income is negative $60,000:

Cost of goods sold $(64,000)Adjustment to net income 4,000Net impact on net income $(60,000)

39. Option Fair Value Hedge of a Foreign Currency Firm Commitment (Sale)(LO5) (30 minutes)

Firm Commitment Option OptionSpot Change in Premium Change in

Date Rate Fair Value Fair Value for 9/1 Fair Value Fair Value6/1 $1.00 - - $0.010 $5,000 -6/30 $0.99 $(4,901.50)1 – $ 4,901.50 $0.016 $8,000 + $3,0009/1 $0.97 $(15,000)2 – $10,098.50 $0.030 $15,000 + $7,000

1 $495,000 – $500,000 = $(5,000) x .9803 = $(4,901.5), where .9803 is the present value factor for two months at an annual interest rate of 12% (1% per month) calculated as 1/1.012. 2 $485,000 – $500,000 = $(15,000).

6/1 Foreign Currency Option $5,000Cash $5,000

There is no entry to record the sales agreement because it is an executory contract.

9-43

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

6/30 Loss on Firm Commitment $4,901.50Firm Commitment $4,901.50

Foreign Currency Option $3,000Gain on Foreign Currency Option $3,000

The impact on net income for the second quarter is:

Loss on Firm Commitment $(4,901.50)Gain on Foreign Currency Option 3,000 .00 Impact on net income $(1,901 .50 )

39. (continued)

9/1 Loss on Firm Commitment $10,098.50Firm Commitment $10,098.50

Foreign Currency Option $7,000Gain on Foreign Currency Option $7,000

Foreign Currency (lek) $485,000Sales $485,000

Cash $500,000Foreign Currency (lek) $485,000Foreign Currency Option 15,000

Firm Commitment $15,000Adjustment to Net Income $15,000

The impact on net income for the third quarter is:

Sales $485,000.00Loss on Firm Commitment (10,098.50)Gain on Foreign Currency Option 7,000.00Adjustment to Net Income 15,000 .00 Impact on net income $496,901 .50

The impact on net income over the second and third quarters is:$495,000 ($496,901.50 – $1,901.50)

The net cash inflow resulting from the sale is: $500,000 – $5,000 = $495,000

9-44

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

40. Option Fair Value Hedge of a Foreign Currency Firm Commitment (Purchase)(LO5) (20 minutes)

Firm Commitment Option OptionSpot Change in Premium Change in

Date Rate Fair Value Fair Value for 12/20 Fair Value Fair Value11/20 $.20 - - $.008 $400 -a) 12/20 $.21 $(500)1 – $500 $.0103 $500 + $100b) 12/20 $.18 $1,0002 + $1,000 $.0004 $0 – $400

1 $10,000 – $10,500 = $(500). 2 $10,000 – $9,000 = $1,000.3 The premium on 12/20 for an option that expires on that date is equal to the option’s

intrinsic value. Given the spot rate on 12/20 of $.21, a call option with a strike price of $.20 has an intrinsic value of $.01 per mark.

4 The premium on 12/20 for an option that expires on that date is equal to the option’s intrinsic value. Given the spot rate on 12/20 of $.18, a call option with a strike price of $.20 has no intrinsic value – the premium on 12/20 is $.000.

a. The option strike price ($.20) is less than the spot rate ($.21) on December 20,

the date the parts are to be paid for. Therefore, Big Arber will exercise its option. The journal entries are as follows:

11/20 Foreign Currency Option $400Cash $400

There is no entry to record the purchase agreement because it is an executory contract.

12/20 Loss on Firm Commitment $500Firm Commitment $500

Foreign Currency Option $100Gain on Foreign Currency Option $100

Foreign Currency (pijio) $10,500Cash $10,000Foreign Currency Option 500

Parts Inventory $10,500Foreign Currency (pijio) $10,500

Firm Commitment $500Adjustment to Net Income $500

(Note that this last entry is not made until the period when the parts inventory affects net income through cost of goods sold.)

9-45

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

40. (continued)

b. The option strike price ($.20) is greater than the spot rate ($.18) on December 20, the date the parts are to be paid for. Therefore, Big Arber will allow the option to expire unexercised. Foreign currency will be acquired at the spot rate on December 20. The journal entries are as follows:

11/20 Foreign Currency Option $400Cash $400

There is no entry to record the purchase agreement because it is an executory contract.

12/20 Firm Commitment $1,000Gain on Firm Commitment $1,000

Loss on Foreign Currency Option $400Foreign Currency Option $400

Foreign Currency (pijio) $9,000Cash $9,000

Parts Inventory $9,000Foreign Currency (pijio) $9,000

Adjustment to Net Income $1,000Firm Commitment $1,000

(Note that this last entry is not made until the period when the parts inventory affects net income through cost of goods sold.)

41. Option Cash Flow Hedge of Forecasted Transaction (LO6) (20 minutes)

12/15/11 Foreign Currency Option $5,000Cash [1 million marks x $.005] $5,000

No journal entry related to the forecasted transaction.

12/31/11 Foreign Currency Option $3,000AOCI $3,000

To recognize the increase in the value of the foreign currency option with the counterpart recorded in AOCI.

9-46

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Option Expense $1,000AOCI $1,000

To recognize the decrease in the time value of the option as expense.[($.584 – $.58) x 1,000,000 = $4,000 – $3,000 = $1,000]

3/15/12 Foreign Currency Option $2,000AOCI $2,000

To recognize the increase in the value of the foreign currency option with the counterpart recorded in AOCI.

Option Expense $4,000AOCI $4,000

To recognize the decrease in the time value of the option as expense.

Foreign Currency (marks) $590,000Cash $580,000Foreign Currency Options 10,000

To record exercise of the foreign currency option at the strike price of $.58 and close out the foreign currency option account.

Parts Inventory $590,000Foreign Currency (marks) $590,000

To record the purchase of parts and payment of 1 million marks to the supplier.

41. (continued)

AOCI $10,000Adjustment to Net Income $10,000

To transfer the amount accumulated in AOCI as an adjustment to net income in the period in which the forecasted transaction occurs. Impact on net income: 2011 – Option expense $(1,000)

2012 – Cost of Goods Sold $(590,000)Option Expense (4,000)Adjustment to Net Income 10,000

$(584,000)

9-47

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Net cash outflow for parts: $585,000 = ($5,000 + $580,000)

42. Foreign Currency Transaction, Forward Contract and Option Hedge of Foreign Currency Liability, Forward Contract and Option Hedge of Foreign Currency Firm Commitment (LO2, LO4, LO5) (60 minutes)

Part a. Foreign Currency Liability (Unhedged)

9/15 Inventory $200,000Accounts Payable (euro) $200,000

9/30 Foreign Exchange Loss $10,000Accounts Payable (euro) $10,000

10/31 Foreign Exchange Loss $10,000Accounts Payable (euro) $10,000

Foreign Currency (euro) $220,000Cash $220,000

Accounts Payable (euro) $220,000Foreign Currency (euro) $220,000

42. (continued)

Part b. Forward Contract Fair Value Hedge of a Foreign Currency Liability

Accounts Payable (C) Forward Forward Contract Spot U.S. Dollar Change in U.S. Rate to Change in

Date Rate Value Dollar Value 10/31 Fair Value Fair Value9/15 $1.00 $200,000 - $1.06 $0 -9/30 $1.05 $210,000 +$10,000 $1.09 $5,940.601 +$5,940.6010/31 $1.10 $220,000 +$10,000 $1.10 $8,000.002 +$2,059.40

1 $218,000 – $212,000 = $6,000 x .9901 = $5,940.60; where .9901 is the present value factor for one month at an annual interest rate of 12% (1% per month) calculated as 1/1.01.2 $220,000 – $212,000 = $8,000.

9/15 Inventory $200,000Accounts Payable (euro) $200,000

There is no formal entry for the forward contract.

9/30 Foreign Exchange Loss $10,000Accounts Payable (euro) $10,000

9-48

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Forward Contract $5,940.60Gain on Forward Contract $5,940.60

10/31 Foreign Exchange Loss $10,000Accounts Payable (euro) $10,000

Forward Contract $2,059.40Gain on Forward Contract $2,059.40

Foreign Currency (euro) $220,000Cash $212,000Forward Contract $8,000

Accounts Payable (euro) $220,000Foreign Currency (euro) $220,000

42. (continued)

Part c. Forward Contract Fair Value Hedge of a Foreign Currency Firm Commitment

9/15 There is no formal entry for the forward contract or the purchase order.

9/30 Forward Contract $5,940.60Gain on Forward Contract $5,940.60

Loss on Firm Commitment $5,940.60Firm Commitment $5,940.60

10/31 Forward Contract $2,059.40Gain on Forward Contract $2,059.40

Loss on Firm Commitment $2,059.40Firm Commitment $2,059.40

Foreign Currency (euro) $220,000Cash $212,000Forward Contract $8,000

Inventory $220,000Foreign Currency (euro) $220,000

Firm Commitment $8,000

9-49

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Adjustment to Net Income $8,000(Note that this last entry is not made until the period when the inventory affects net income through cost of goods sold.)

42. (continued)

Part d. Option Cash Flow Hedge of a Foreign Currency Liability

The following schedule summarizes the changes in the components of the fair value of the euro call option with a strike price of $1.00 for October 31.

Change ChangeSpot Option Fair in Fair Intrinsic Time in Time

Date Rate Premium Value Value Value Value Value 09/15 $1.00 $.035 $7,000 - $0 $7,0001 -09/30 $1.05 $.070 $14,000 + $7,000 $10,0002 $4,0002 - $3,00010/31 $1.10 $.100 $20,000 + $6,000 $20,000 $03 - $4,000

1 Because the strike price and spot rate are the same, the option has no intrinsic value. Fair value is attributable solely to the time value of the option.

2 With a spot rate of $1.05 and a strike price of $1.00, the option has an intrinsic value of $10,000. The remaining $4,000 of fair value is attributable to time value.

3 The time value of the option at maturity is zero.

9/15 Inventory $200,000Accounts Payable (euro) $200,000

Foreign Currency Option $7,000Cash $7,000

9/30 Foreign Exchange Loss $10,000Accounts Payable (euro) $10,000

Foreign Currency Option $7,000Accumulated Other Comprehensive Income (AOCI) $7,000

Accumulated Other Comprehensive Income (AOCI) $10,000Gain on Foreign Currency Option $10,000

Option Expense $3,000Accumulated Other Comprehensive Income (AOCI) $3,000

42. (continued)

9-50

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

10/31 Foreign Exchange Loss $10,000Accounts Payable (euro) $10,000

Foreign Currency Option $6,000Accumulated Other Comprehensive Income (AOCI) $6,000

Accumulated Other Comprehensive Income (AOCI) $10,000Gain on Foreign Currency Option $10,000

Option Expense $4,000Accumulated Other Comprehensive Income (AOCI) $4,000

Foreign Currency (euro) $220,000Cash $200,000Foreign Currency Option $20,000

Accounts Payable (euro) $220,000Foreign Currency (euro) $220,000

42. (continued)

Part e. Option Fair Value Hedge of a Foreign Currency Firm Commitment

Firm Commitment Option Foreign Currency OptionSpot Change in Premium Change in

Date Rate Fair Value Fair Value for 10/31 Fair Value Fair Value9/15 $1.00 $0 - $.035 $ 7,000 -9/30 $1.05 $ (9,901) –$ 9,9011 $.070 $14,000 +$7,00010/31 $1.10 $(20,000) –$10,099 $.100 $20,000 +$6,000

1 $210,000 – $200,000 = $(10,000) x .9901 = $(9,901), where .9901 is the present value factor for one month at an annual interest rate of 12% (1% per month) calculated as 1/1.01.

9/15 Foreign Currency Option $7,000Cash $7,000

9/30 Foreign Currency Option $7,000Gain on Foreign Currency Option $7,000

Loss on Firm Commitment $9,901Firm Commitment $9,901

10/31 Foreign Currency Option $6,000Gain on Foreign Currency Option $6,000

9-51

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk

Loss on Firm Commitment $10,099Firm Commitment $10,099

Foreign Currency (euro) $220,000Cash $200,000Foreign Currency Option 20,000

Inventory $220,000Foreign Currency (euro) $220,000

Firm Commitment $20,000Adjustment to Net Income $20,000

(Note that this last entry is not made until the period when the inventory affects net income through cost of goods sold.)

Answers to Develop Your Skills Cases

Research Case—International Flavors and Fragrances

The responses to this assignment might change over time as the company changes its use of foreign currency derivatives or changes the manner in which it discloses its foreign currency hedging activities in the annual report. The following responses are based on IFF’s 2008 annual report.

1. In 2008, IFF provided information in the annual report related to its management of foreign exchange risk in the following locations:a. Item 1A. Risk Factors.b. Item 7A. Quantitative and Qualitative Disclosures about Market Risk.c. Note 14. Financial Instruments.

2. IFF uses foreign currency forward contracts to reduce exposure to cash flow volatility arising from foreign currency fluctuations associated with certain foreign currency receivables and payables (hedges of foreign currency denominated assets and liabilities) and anticipated purchases of raw materials used in operations (hedges of forecasted transactions).The company also uses a Japanese Yen- U.S. Dollar swap to hedge monthly sale and purchase transactions between the U.S. and Japan.

3. In Note 14, IFF indicates that the notional amount and maturity dates of its forward contracts match those of the underlying transactions.

Accounting Standards Case—Forecasted Transactions

Source of guidance: FASB Accounting Standards Codification (paragraph 815-20-55-24): Derivatives and Hedging; Hedging-General; Implementation

9-52

Chapter 09 - Foreign Currency Transactions and Hedging Foreign Exchange Risk