CHANGING STRUCTURES IN THE NORTH AMERICAN PLASTICS INDUSTRY - FROM LOCAL TO GLOBAL INFLUENCES - Applied Market Information Ltd. 6 Pritchard Street Bristol, BS2 8RH, UK Tel: +44 (0)117 31111511 Fax: +44 (0)117 3111534 Email: [email protected] Applied Market Information LLC 1210 Broadcasting Road, Suite 103 Wyomissing, PA 19610, USA Tel: +1 (610) 478 0800 Fax: +1 (610) 478 0900 Email: [email protected] www.amiplastics.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHANGING STRUCTURES IN THE NORTH

AMERICAN PLASTICS INDUSTRY

- FROM LOCAL TO GLOBAL INFLUENCES -

Applied Market Information Ltd.

6 Pritchard Street

Bristol, BS2 8RH, UK

Tel: +44 (0)117 31111511

Fax: +44 (0)117 3111534

Email: [email protected]

Applied Market Information LLC

1210 Broadcasting Road, Suite 103

Wyomissing, PA 19610, USA

Tel: +1 (610) 478 0800

Fax: +1 (610) 478 0900

Email: [email protected] www.amiplastics.com

©Applied Market Information Ltd 2013

Western Plastics Association

The programme

About Applied Market Information

Where North America fits in the world

The position of North American demand

Downstream industries and changing structures

Global Flexible Packaging markets – the PE example

Consumer trends impacting plastics

Retailer trends impacting plastics

Conclusions

Slide 2 Slide 2

©Applied Market Information Ltd 2013

About AMI Consulting

3 Western Plastics Association

Market Analysis

– In-depth multi-client reports

The NAFTA market for Thermoplastic

Concentrates (March, 2012)

The Global Market for BOPP films

The Global Market for Grass Yarns

Studies by application e.g. Pipes,

membranes, cables

Studies by polymer e.g. PP, PE

– Single client projects and reports

Market & Database products

– Plastics in India

– The Thermoplastic Compounding

Industry Report (NAFTA, Europe,

Asia, Latin America)

– Processor & compounder databases

Conferences

– Compounding World Forum

– AMI Plastics Industry Seminar

– Shrink and Stretch film

– Thermoplastic Concentrates

– Polyethylene Films

– Fire Retardants in Plastics

– Polymers in Cables

Other

Digital magazines

– Compounding World, Injection

World, Film & Sheet, Pipe & Profile

E-publishing contract services

Technical publications

©Applied Market Information Ltd 2013

AMI has over 25 years experience in providing insight and information to the global plastics industry.

AMI has databases on over 30,000 plastic processors globally.

AMI has unrivalled knowledge on down stream plastics markets.

AMI Consulting

4 Western Plastics Association

©Applied Market Information Ltd 2013

AMI Future Events

5 Western Plastics Association

The international marketing, business

and technical conference for the

polyethylene film industry

11-13 February 2014

The Shores Resort & Spa,

Daytona Beach, FL, USA

Organized by Applied Market Information

LLC

©Applied Market Information Ltd 2013

AMI’s Digital magazines

www.filmandsheet.com www.pipeandprofile.com www.injectionworld.com

6 Western Plastics Association

WHERE NORTH AMERICA FITS IN THE

WORLD

Evolving patterns of demand

©Applied Market Information Ltd 2013

Western Plastics Association

The trends that shape the world

Global population growth to 9.2 billion by 2050

– With an increasing share living longer and requiring greater services

Urbanization as more of the population moves to cities

– By 2050 65% of the world population will be city dwellers

Transport needs will mean over 2.5 billion cars are needed by 2050

The fight to access resources:

– Raw materials to drive industrial development

– The basics of life water and food

– Energy and power needs will have grown by 50% from the levels of 2012

Energy efficiency and resource optimisation will be essential drivers in

the globally successful economies

Slide 8 Slide 8

©Applied Market Information Ltd 2013

Western Plastics Association Slide 9

Total polymer demand by type 1983-2017

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1983 1998 2012 2013 2017

mil

lio

n lb

sPolyethylene Polypropylene

PVC Polystyrene

Expanded Polystyrene ABS

PET Engineering polymer

©Applied Market Information Ltd 2013

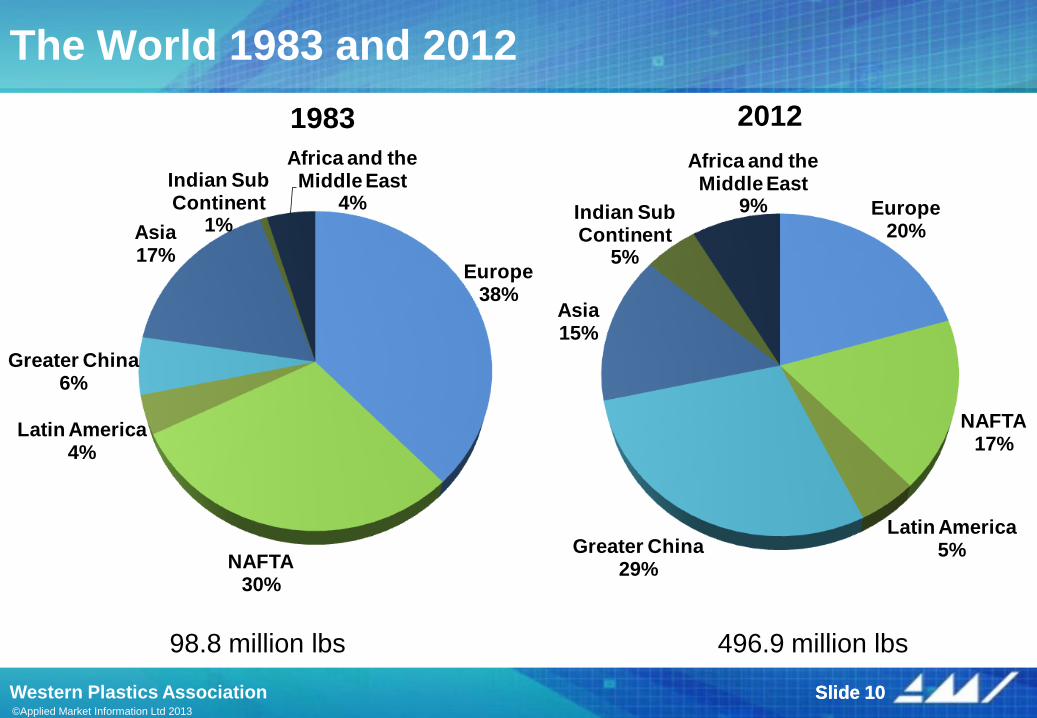

The World 1983 and 2012

98.8 million lbs 496.9 million lbs

Slide 10 Slide 10 Western Plastics Association

1983 2012

Europe20%

NAFTA17%

Latin America5%Greater China

29%

Asia15%

Indian Sub Continent

5%

Africa and the Middle East

9%

Europe38%

NAFTA30%

Latin America4%

Greater China6%

Asia17%

Indian Sub Continent

1%

Africa and the Middle East

4%

©Applied Market Information Ltd 2013

Total world demand 1983-2017

Slide 11 Western Plastics Association

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1983 1998 2012 2013 2017

mil

lio

n lb

s

Europe NAFTA

Latin America Greater China

Asia Indian Sub Continent

Africa and the Middle East

©Applied Market Information Ltd 2013

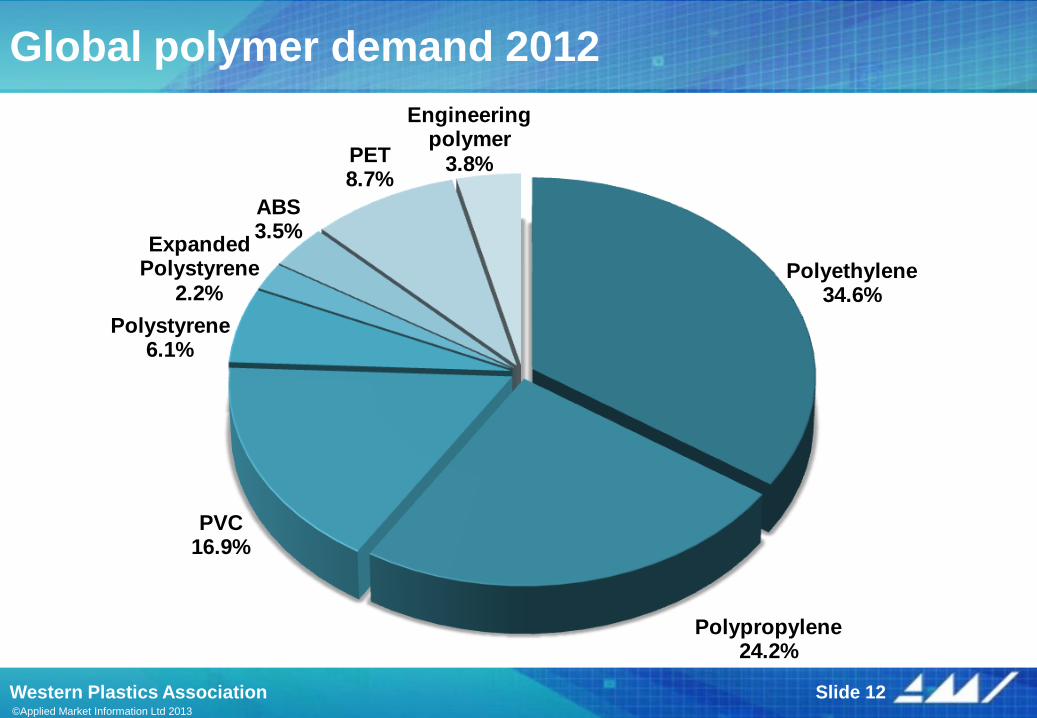

Global polymer demand 2012

Slide 12 Western Plastics Association

Polyethylene34.6%

Polypropylene24.2%

PVC16.9%

Polystyrene6.1%

Expanded Polystyrene

2.2%

ABS3.5%

PET8.7%

Engineering polymer

3.8%

©Applied Market Information Ltd 2013

Western Plastics Association

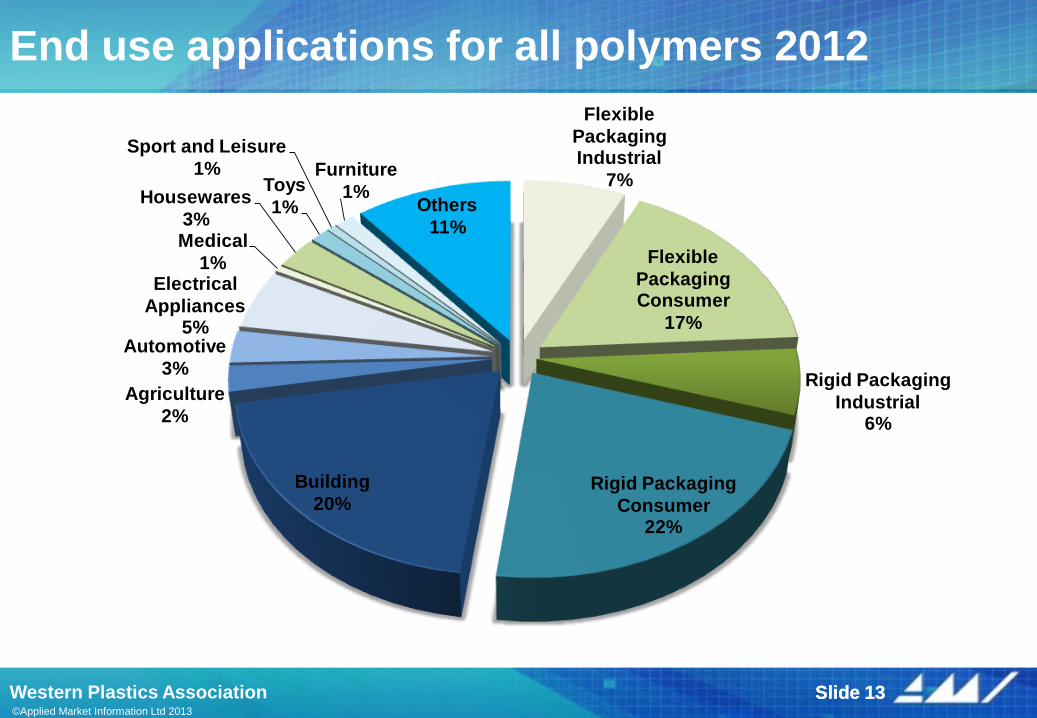

End use applications for all polymers 2012

Slide 13 Slide 13

Flexible

Packaging Industrial

7%

Flexible

Packaging Consumer

17%

Rigid Packaging

Industrial6%

Rigid Packaging

Consumer22%

Building

20%

Agriculture

2%

Automotive

3%

Electrical

Appliances5%

Medical

1%

Housewares

3%

Toys

1%

Sport and Leisure

1% Furniture

1%Others

11%

©Applied Market Information Ltd 2013

Total NAFTA demand 1983-2017

Slide 14 Western Plastics Association

0

20,000

40,000

60,000

80,000

100,000

120,000

1983 1998 2012 2013 2017

Mil

lio

n lb

s

PolyethylenePolypropylenePVCPolystyreneExpanded PolystyreneABSPETEngineering Polymer

©Applied Market Information Ltd 2013

Total NAFTA demand 1983-2017

Slide 15 Western Plastics Association Slide 15

Units: million lbs 1983 1998 2012 2013 2017

Polyethylene 13,272 30,640 34,673 35,467 40,075

Polypropylene 3,526 13,444 15,626 16,067 18,232

PVC 6,094 13,962 13,427 13,619 14,399

Polystyrene 3,758 6,083 4,728 4,761 4,904

Expanded Polystyrene 496 937 1,358 1,395 1,492

ABS 904 1,631 1,713 1,770 1,940

PET 551 4,188 10,238 10,612 12,100

Engineering Polymer 886 2,513 4,033 4,232 4,963

Total 29,487 73,398 85,795 87,922 98,105

©Applied Market Information Ltd 2013

Western Plastics Association

Dynamics of the NAFTA market

Highly evolved market dominated by USA economy

– Mexico the faster growing area

2012 characterised by:

– Acceleration of domestic demand

– Profitability maintained

Evidence of renewed acquisition activity in processing industry

Renewed confidence in domestic manufacturing of both resin and

plastics processing; shale gas driven

Global investments continuing, driven by the desire to serve brands on a

global basis

– Importance of retailers in encouraging low cost goods from around the world

– Continued global investments by US companies

North American resin and additive companies continue to be at the

forefront of global development

Slide 16 Slide 16

Downstream industries and their changing

structures

©Applied Market Information Ltd 2013

Western Plastics Association Slide 18

The plastics industry in 2013

Plastics processing is successfully established in every region and

country of the world

The impact of plastics products and goods is felt in every economy

and society on the planet

The average consumer relies on and uses numerous distinct plastics

products every day

Plastics drive the global economy

– Building and infrastructure

– Communications

– Transport

– Packaging of all consumer goods (rigid and flexible)

– Leisure and social activities

©Applied Market Information Ltd 2013

Western Plastics Association Slide 19

Development of the processing industry

Local production

National and regional processors

Interregional processors

Global dimension

Pre 1970’s

1970’s-1980’s

1980’s- 1990’s

2000’s-2010

In same

time resin

producers exit

processing and

financial

groups

take larger

holdings

©Applied Market Information Ltd 2013

Western Plastics Association Slide 20

Global distribution of processors 2013

Total number 196,255

Europe13.2%

NAFTA7.1%

Latin America5.9%

Greater China34.2%

Asia18.6%

Indian Sub Continent

15.4%

Africa and Middle East

5.6%

©Applied Market Information Ltd 2013

Western Plastics Association Slide 21

Global processors by activity 2013

Total Number 196,255

Injection Moulding

61.5%Blow Moulding7.9%

Rotational Moulding

0.9%

Film14.6%

Pipe 2.6%

Profile4.7%

Cable0.9%

Sheet2.3%

Compounders2.5%

Other2.1%

©Applied Market Information Ltd 2013

Western Plastics Association Slide 22

Processor industry structure 2013

% of polymer demand % of processor numbers

Europe13.2%

NAFTA7.1%

Latin America5.9%

Greater China34.2%

Asia18.6%

Indian Sub Continent

15.4%

Africa and Middle East

5.6%Europe20.5%

NAFTA17.3%

Latin America5.0%

Greater China28.8%

Asia14.8%

Indian Sub Continent

5.2%

Africa and the Middle

East8.5%

©Applied Market Information Ltd 2013

Industry dispersed in all countries

– Strong structure in United States

– Developed industry in Canada

– Rapidly evolving industry in Mexico

Many companies but limited resources

– The average company have limited management skills and resources

Consolidation in the last ten years

– Takeovers and mergers driven by specialisation

– Consolidation of the customer base

– Movement of business to Asia and developing world

– Future of equity owned assets uncertain

Specialization increasing

Number of truly National players

– Few with truly global ties

Western Plastics Association Slide 23

The plastics industry in NAFTA

©Applied Market Information Ltd 2013

The structure of the North American industry

Slide 24 Western Plastics Association

Injection Molding

66%Blow Molding

6%

Polyolefin Film

6%

Rotational

Moulding2%

Pipe and Profile

8%

Cable

1%

Sheet

4%Compounders

5%

Others

2%

Global flexible packaging markets

-the Polyethylene example-

©Applied Market Information Ltd 2013

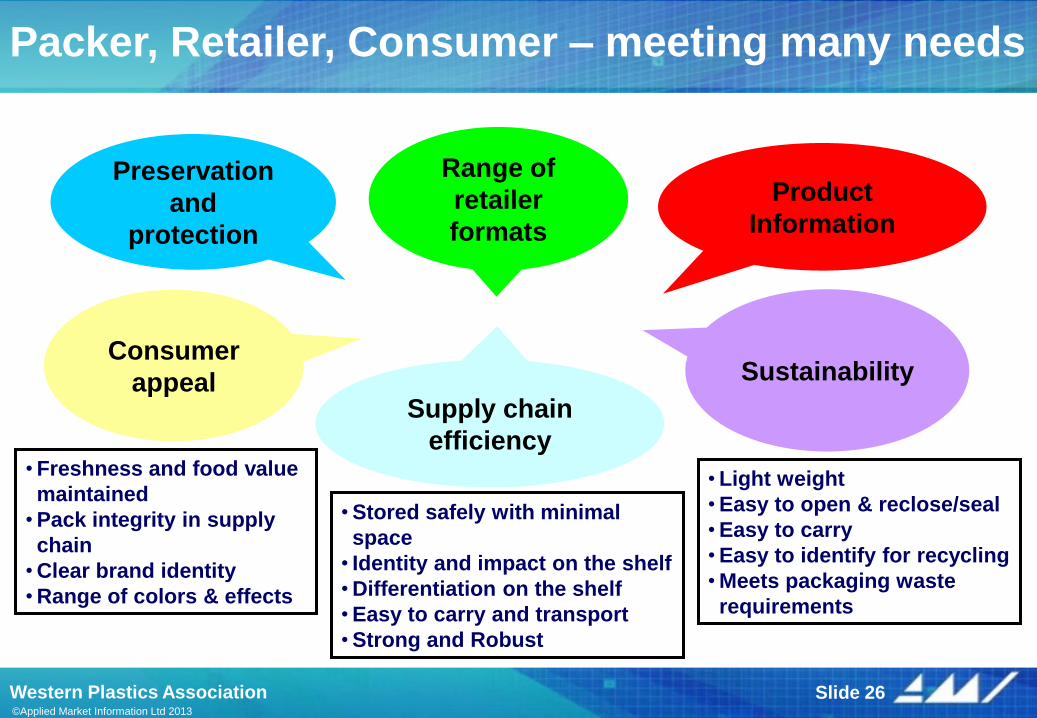

Western Plastics Association Slide 26

Preservation

and

protection

Product

Information

Consumer

appeal Supply chain

efficiency

Sustainability

• Freshness and food value

maintained

• Pack integrity in supply

chain

• Clear brand identity

• Range of colors & effects

• Stored safely with minimal

space

• Identity and impact on the shelf

• Differentiation on the shelf

• Easy to carry and transport

• Strong and Robust

• Light weight

• Easy to open & reclose/seal

• Easy to carry

• Easy to identify for recycling

• Meets packaging waste

requirements

Range of

retailer

formats

Packer, Retailer, Consumer – meeting many needs

©Applied Market Information Ltd 2013

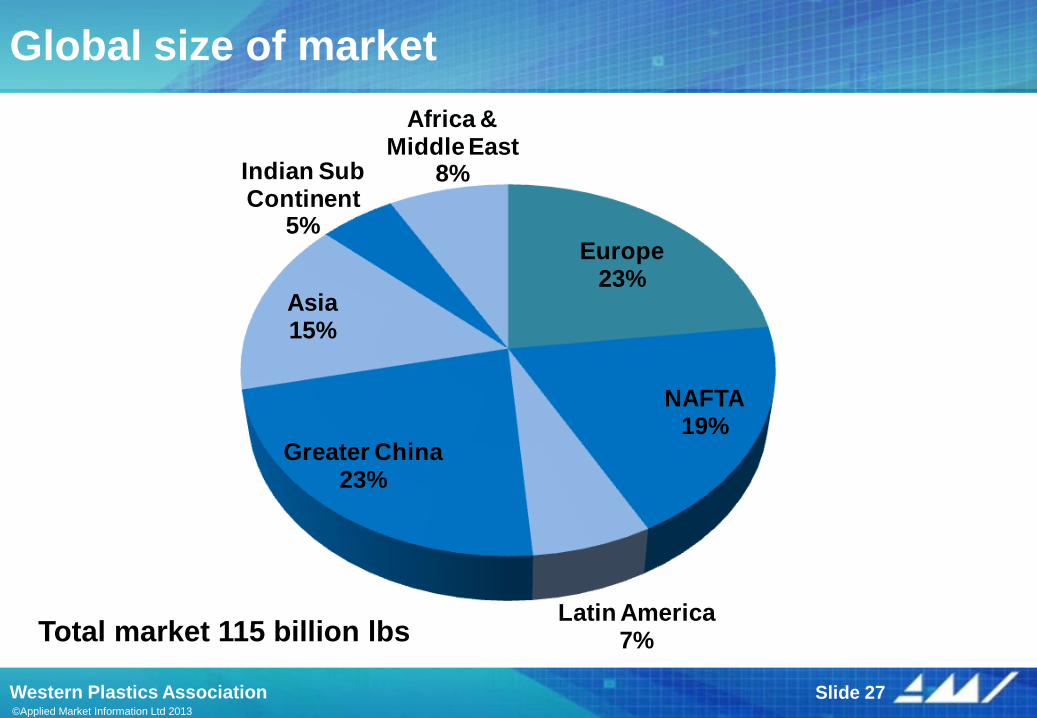

Global size of market

Europe23%

NAFTA19%

Latin America7%

Greater China23%

Asia15%

Indian Sub Continent

5%

Africa & Middle East

8%

Western Plastics Association Slide 27

Total market 115 billion lbs

©Applied Market Information Ltd 2013

Western Plastics Association Slide 28

Global distribution of PE extruders 2013

Total number of

companies 28,620

Europe7% NAFTA

4%Latin America

9%

Greater China38%

Asia23%

Indian Sub Continent

14%

Africa and Middle East

5%

©Applied Market Information Ltd 2013

Average film producer throughput 2012

Slide 29 Western Plastics Association

0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 18.00

Indian Sub Continent

Asia

Greater China

Latin America

Africa & The Middle

East

Europe

NAFTA

Million lbs

©Applied Market Information Ltd 2013

Base substrate demand – trends and comments

Western Plastics Association

PE Film market is a 84 billion lbs.

market globally accounting for over

half of world PE demand, future

growth globally 4.5% per annum

PP Film market is a 19 billion lbs.

market global market growing at

over 6% per annum

Other films and plastic substrates

account for over 11 billion lbs. and

are growing at over 7% per annum

Strong regional focus to most

markets, but with trade increasingly

influencing markets

Polyethylene73%

BOPP14%

PP film3%

PET6%

Others4%

Slide 30

©Applied Market Information Ltd 2013

Increased specialisation and focus

Materials - wide range of polymers and copolymers

Innovation in additives and modification

Extrusion - more sophisticated processing (co-extrusion)

Conversion

– Improved printing (more colors greater print definition)

– Pack making (specialized shapes and structures)

– Lamination

Need to understand new materials

- training and investment

Investments in co-extrusion often

necessary to fully exploit palette of

materials

Co-extrusion often the route to

achieve downgauging and superior

performance

Development of new products

essential to justify investment

Western Plastics Association Slide 31

Technology Advances Impact on Extruders

©Applied Market Information Ltd 2013

Western Plastics Association Slide 32

Key drivers of packaging growth

Environmental

– Recycling

– Minimisation

Cost savings

– line speed/filling speed improvement often related to sealing time

– Greater pack integrity

– Down gauging

Others

– Reclosability

– Tamper evidence

– Excitement!

– Barrier properties

©Applied Market Information Ltd 2013

Case study of the opportunity: Labels

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pressure Sensative Glue Applied IML Sleeves and Others

Plastic Paper

Western Plastics Association Slide 33

©Applied Market Information Ltd 2013

Case study of the opportunity: Sacks

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Europe NAFTA Asia Latin America Japan Rest of the

World

Polyethylene Polypropylene Paper

Western Plastics Association Slide 34

Consumer trends impacting

the plastics industry

©Applied Market Information Ltd 2013

Western Plastics Association Slide 36

Profits from forecasting and understanding

Future behaviour and attitudes

Future needs

©Applied Market Information Ltd 2013

Western Plastics Association Slide 37

How are our lives changing?

Time is money

“instant

convenience”

Individual as a

market

Communications

age

Appealing to

the young at

heart

The natural

world

Healthy lifestyle

choices

How are our lives

changing?

©Applied Market Information Ltd 2013

Western Plastics Association Slide 38

True value propositions

Can I offer elements of uniqueness?

Do my products contribute to the

uniqueness of the brand?

Retailers and brands and their

influence on market development

©Applied Market Information Ltd 2013

Retailer brand issues/challenges

Slide 40 Western Plastics Association

Shorter product life cycles

– More product variants

Environmental challenge

Rise of private label

– Walmart private label $135 billion

– Nestle is a $98 billion company

Need for brand protection

How to sell in an interactive world

©Applied Market Information Ltd 2013

Retailers & Consumers

Slide 41 Western Plastics Association

What is a brand?

Promise How does it look

Aesthetic appeal

Environmental impact

Experience How does it work

Functionality

Memory What brings you back

©Applied Market Information Ltd 2013

Western Plastics Association Slide 42

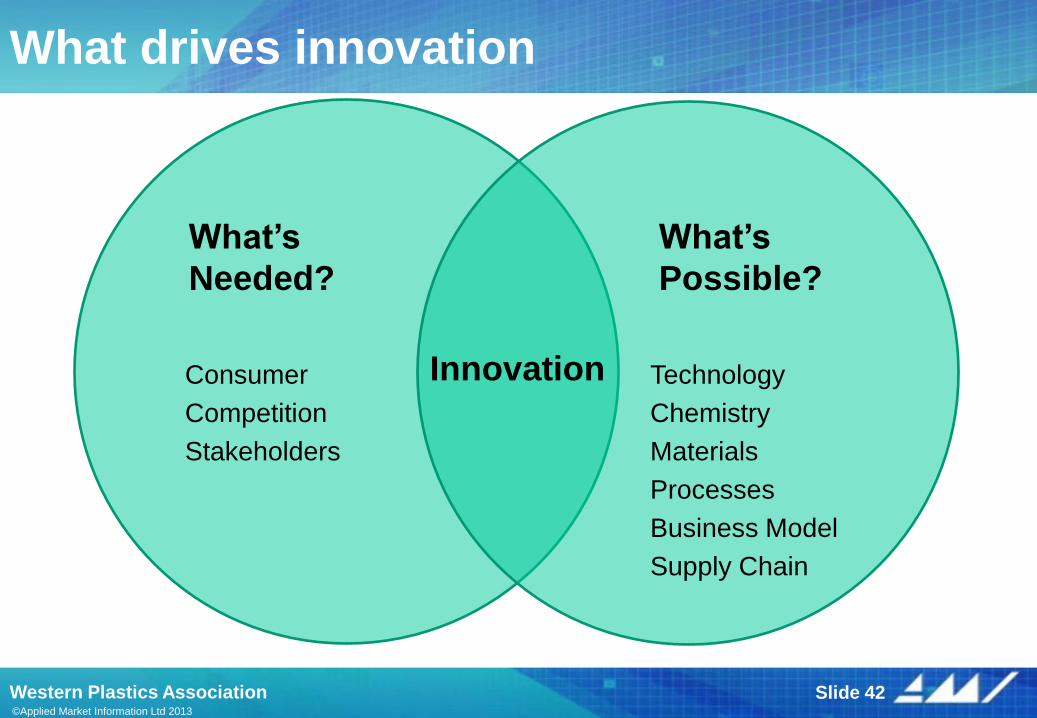

What drives innovation

Innovation

What’s

Needed?

Consumer

Competition

Stakeholders

What’s

Possible?

Technology

Chemistry

Materials

Processes

Business Model

Supply Chain

Summary and

conclusions

©Applied Market Information Ltd 2013

Western Plastics Association Slide 44

Observations – Market overview

The footprint and influence of plastics products are now global in scope and contribute to all areas of industry and the economy

Although we are slowly seeing a global industry emerge in many markets the extent of globalisation is limited:

– Few global standards exist

– Resin availability and its pricing remains regional

The activities of global brands, combined with modern technology, are the major factors reshaping the structure of the upper levels of the processing industry. A limited number of players are adapting to this circumstance

The demand for plastics are also developing under the influence of economic, environmental and an increasingly political/legal frameworks.

Stronger growth is occurring in the more populous developing economies of India and China. Other countries joining this group are Russia, Brazil and Indonesia.

All around the world the opportunity to replace traditional material is strong

©Applied Market Information Ltd 2013

Western Plastics Association Slide 45

Observations – industry structure

The processing industry continues to be extremely fragmented with the faster growing regions of the world seeing the number of processors advance while the more developed world is seeing a decrease in processor numbers.

Within each major region and also on a global scale the larger processors are gaining an increasing share of the overall market. This process is most advanced in the NAFTA region where a single market has existed for many years, but similar trends are observable in the other regions.

Thus in the future the industry shape will be characterised by:

– The big will get bigger, the small entrepreneurial and focused supplier will remain

– The medium size processor will be challenged

“Disruption” will be the characteristic of markets to an increasing extent

As larger groups improve their profitability, access to capital and strong balance sheets, this will drive a further process of company acquisition and restructuring

Energy costs are emerging as a longer term driver of processing location

THANK YOU

www.amiplastics.com

Applied Market Information Ltd.

6 Pritchard Street

Bristol, BS2 8RH, UK

Tel: +44 (0)117 3111511

Fax: +44 (0)117 3111534

Email: [email protected]

Applied Market Information LLC

1210 Broadcasting Road, Suite 103

Wyomissing, PA 19610, USA

Tel: +1 (610) 478 0800

Fax: +1 (610) 478 0900

Email: [email protected]

Attendees to this seminar are reminded that the contents are copyrighted and that the

copyright belongs to Applied Market Information Ltd. and/or its subsidiaries. Unless

otherwise agreed and confirmed by Applied Market Information Ltd. in writing, it is

forbidden to distribute the contents to any third parties or transmit it via any electronic

medium forum.

Andrew Reynolds: [email protected]

Applied Market Information Ltd. 6 Pritchard Street

Bristol BS2 8RH, UK Tel: +44(117) 3111511 Fax: +44(117) 3111534

E: [email protected] www.amiplastics.com

Applied Market Information LLC 1210 Broadcasting Road, Suite 103

Wyomissing, PA 19610 USA Tel: +1(610) 478 0800 Fax: +1(610) 478 0900

E: [email protected] www.amiplastics.com

Related Documents

![What happen to Ch’I’ibalil [family]? Changing Family Structures in Ucí, Yucatán By: Anita María Moo.](https://static.cupdf.com/doc/110x72/56649ddf5503460f94ad8f36/what-happen-to-chiibalil-family-changing-family-structures-in-uci.jpg)

![What happen to Ch’I’ibalil [family]? Changing Family Structures in Ucí, Yucatán](https://static.cupdf.com/doc/110x72/56813fa3550346895daa90de/what-happen-to-chiibalil-family-changing-family-structures-in-uci-568fd2913ccbd.jpg)