1 Stephen Letwin EVP, Gas Transmission and International Enbridge Inc. Challenges and Opportunities for Natural Gas Delivery Insight Information – Natural Gas Forum April 26, 2010 Calgary, AB

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Stephen LetwinEVP, Gas Transmission and International

Enbridge Inc.

Challenges and Opportunities for

Natural Gas Delivery

Insight Information –

Natural Gas Forum

April 26, 2010

Calgary, AB

2

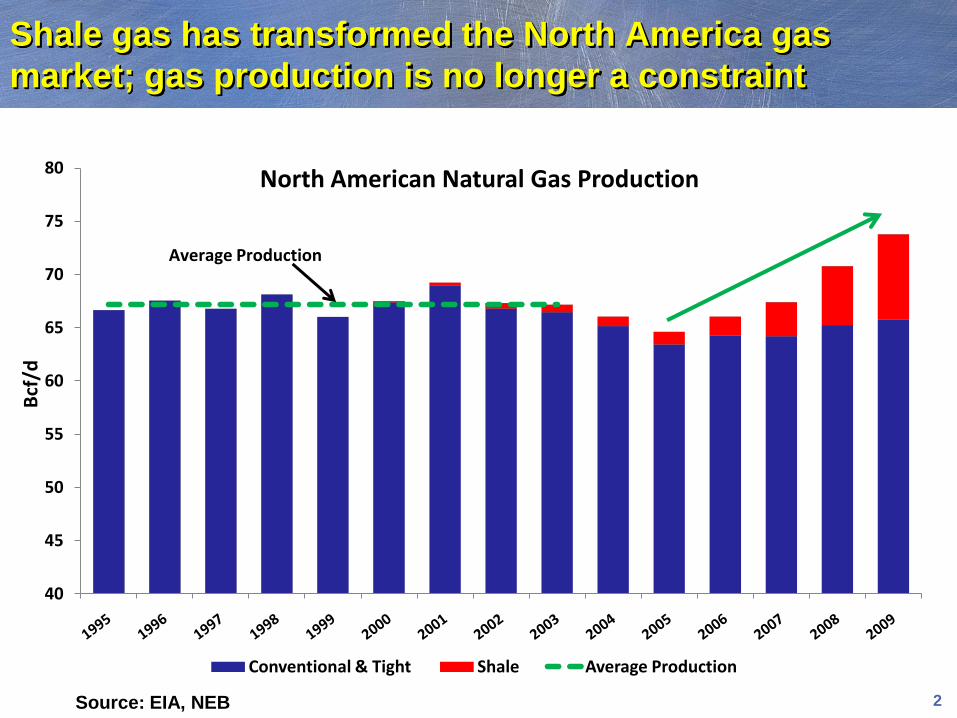

Shale gas has transformed the North America gas

market; gas production is no longer a constraint

40

45

50

55

60

65

70

75

80

Bcf

/d

North American Natural Gas Production

Conventional & Tight Shale Average Production

Average Production

Source: EIA, NEB

3

Unconventional gas provides opportunities to

diversify supply and transportation routes

Supply reductions shown in red

Mackenzie Delta

2015 – 0

2020 – 0

2025 – 0

Alaska

2015 – 0

2020 – 0

2025 – 0

WCSB

2015 – (1.4)

2020 – (0.4)

2025 – 0.6

Appalachia

2015 – 1.5

2020 – 4.1

2025 – 5.8MidCon

2015 – 3.4

2020 – 4.2

2025 – 4.6

West Coast

2015 – (0.2)

2020 – (0.3)

2025 – (0.4)

Rockies

2015 – 1.2

2020 – 2.4

2025 – 2.9

San Juan

2015 – (0.8)

2020 – (1.1)

2025 – (1.5)

North America

2015 – 2.2

2020 – 8.4

2025 – 12.6

LNG

2015 – 0.7

2020 – (0.5)

2025– (0.5)

Cumulative Change from 2008 (Bcf/d)

Eastern Canada

2015 – 0

2020 – (0.1)

2025 – (0.2)

Gulf Coast

2015 – 2.8

2020 – 3.9

2025 – 4.3Offshore

2015 – (2.4)

2020 – (2.9)

2025 – (3.1)

Permian

2015 – (1.9)

2020 – (1.4)

2025 – (0.5)

Source: Enbridge

4

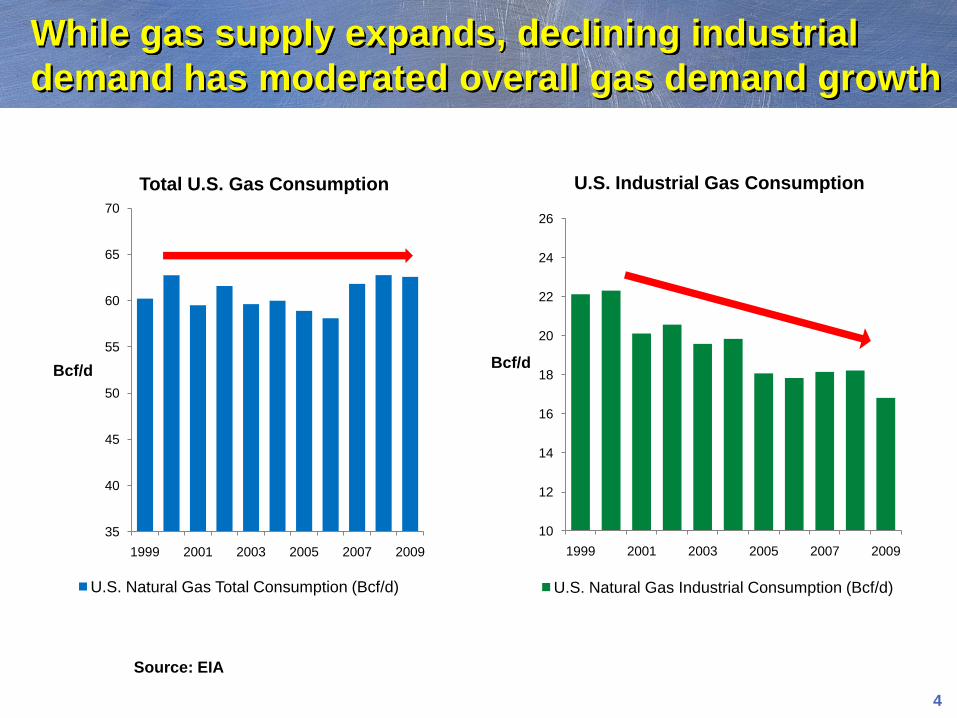

While gas supply expands, declining industrial

demand has moderated overall gas demand growth

35

40

45

50

55

60

65

70

1999 2001 2003 2005 2007 2009

Bcf/d

Total U.S. Gas Consumption

U.S. Natural Gas Total Consumption (Bcf/d)

10

12

14

16

18

20

22

24

26

1999 2001 2003 2005 2007 2009

Bcf/d

U.S. Industrial Gas Consumption

U.S. Natural Gas Industrial Consumption (Bcf/d)

Source: EIA

5

Improved efficiencies and conservation are

also moderating gas demand growth

300

320

340

360

380

400

420

440

460

480

500

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

BCF

Mil

lio

ns o

f C

us

tom

ers

Enbridge Gas Distribution - Comparison of Customer Base with Gas Demand

Average Customer Base Demand Normalized to 2009 DD Bcf

6

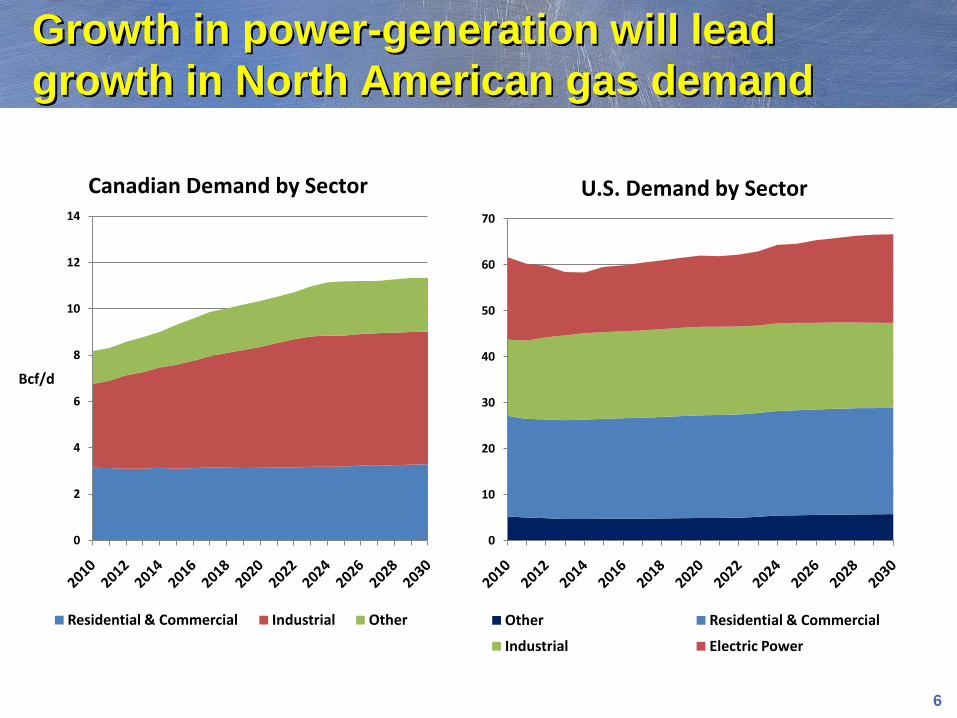

Growth in power-generation will lead

growth in North American gas demand

0

2

4

6

8

10

12

14

Bcf/d

Canadian Demand by Sector

Residential & Commercial Industrial Other

0

10

20

30

40

50

60

70

U.S. Demand by Sector

Other Residential & Commercial

Industrial Electric Power

7

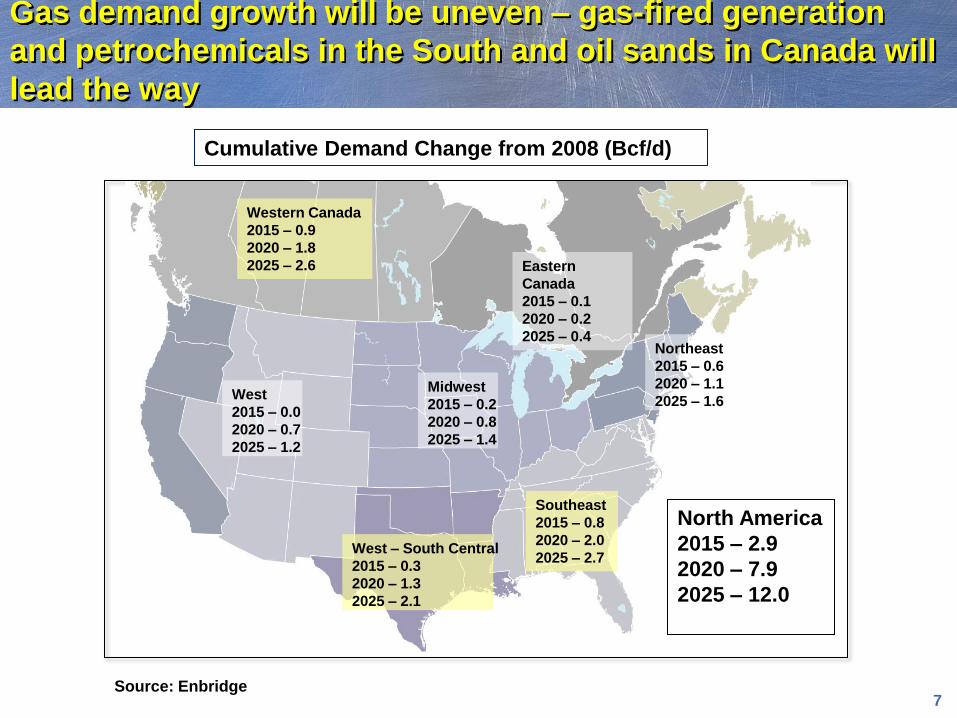

Gas demand growth will be uneven – gas-fired generation

and petrochemicals in the South and oil sands in Canada will

lead the way

Western Canada

2015 – 0.9

2020 – 1.8

2025 – 2.6 Eastern

Canada

2015 – 0.1

2020 – 0.2

2025 – 0.4Northeast

2015 – 0.6

2020 – 1.1

2025 – 1.6West

2015 – 0.0

2020 – 0.7

2025 – 1.2

Midwest

2015 – 0.2

2020 – 0.8

2025 – 1.4

Southeast

2015 – 0.8

2020 – 2.0

2025 – 2.7West – South Central

2015 – 0.3

2020 – 1.3

2025 – 2.1

North America

2015 – 2.9

2020 – 7.9

2025 – 12.0

Cumulative Demand Change from 2008 (Bcf/d)

Source: Enbridge

8

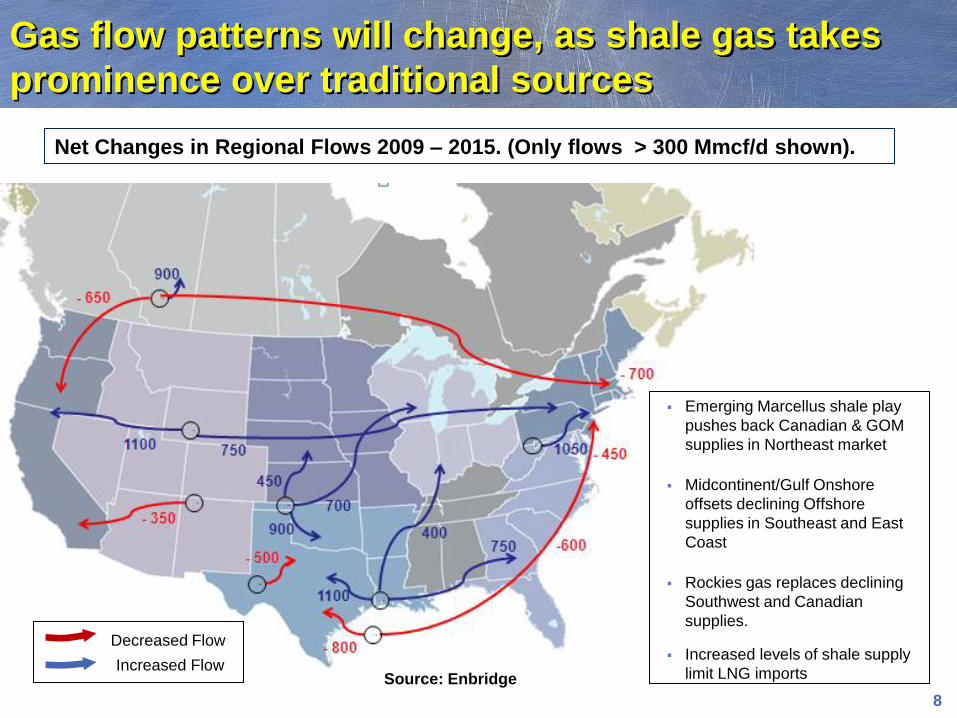

Gas flow patterns will change, as shale gas takes

prominence over traditional sources

Net Changes in Regional Flows 2009 – 2015. (Only flows > 300 Mmcf/d shown).

Source: Enbridge

Emerging Marcellus shale play

pushes back Canadian & GOM

supplies in Northeast market

Midcontinent/Gulf Onshore

offsets declining Offshore

supplies in Southeast and East

Coast

Rockies gas replaces declining

Southwest and Canadian

supplies.

Increased levels of shale supply

limit LNG importsIncreased Flow

Decreased Flow

9

The U.S. and Canada will need 29,000 to 62,000 miles of additional

pipeline and 370 to 600 Bcf of additional storage capacity.

From 2009 to 2030, US $133 to $210 billion (or US $6 to 10 billion per

year) will be needed for pipelines and related infrastructure.

Infrastructure needs are driven by:

the shift to unconventional gas areas from traditional sources, and

market growth from power generation

Insufficient natural gas infrastructures can lead to price volatility,

reduced economic growth, and reduced delivery of natural gas supply.

Significant and continuous investment in additional

infrastructure will be required as supply dynamics shift

Source: INGAA

10

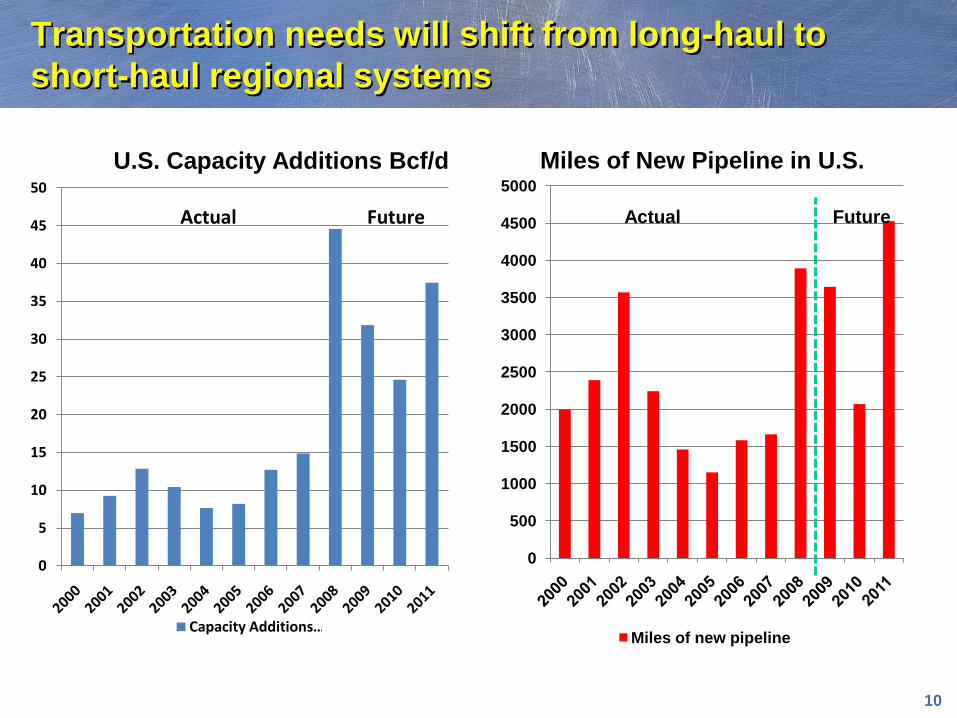

Transportation needs will shift from long-haul to

short-haul regional systems

0

5

10

15

20

25

30

35

40

45

50

Capacity Additions …

Actual Future

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Miles of New Pipeline in U.S.

Miles of new pipeline

Actual Future

U.S. Capacity Additions Bcf/d

11

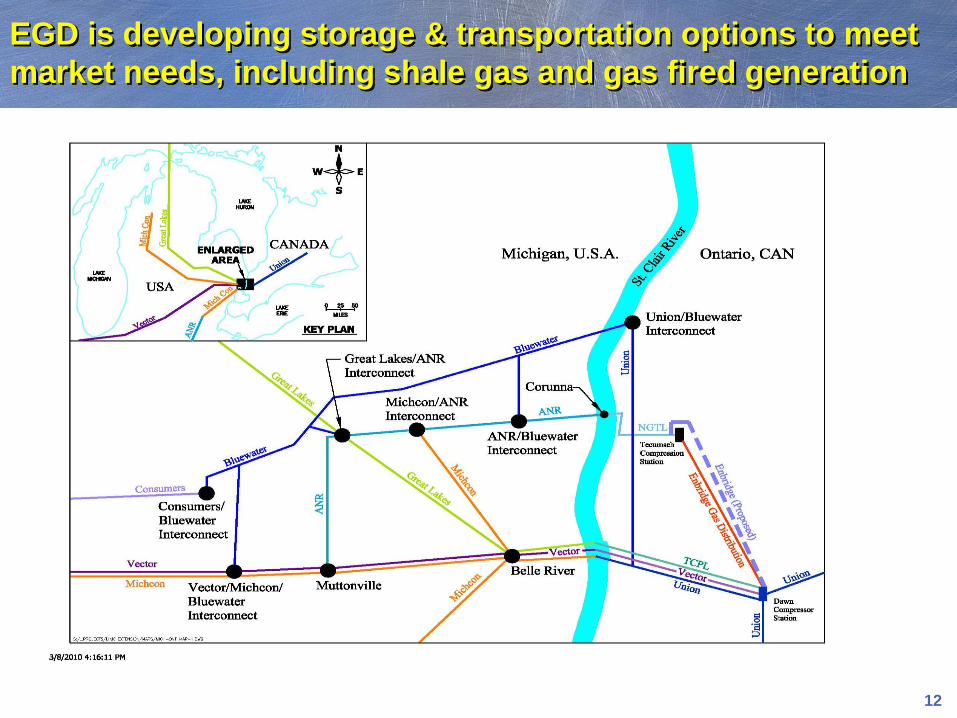

Enbridge Gas Distribution Operates Storage Facilities

with links to the Ontario and eastern U.S. markets

~100 Bcf of capacity

10 storage pools

Pipeline Interconnects

• Union (Dawn)

• TCPL

• Link

• Vector

12

EGD is developing storage & transportation options to meet

market needs, including shale gas and gas fired generation

13

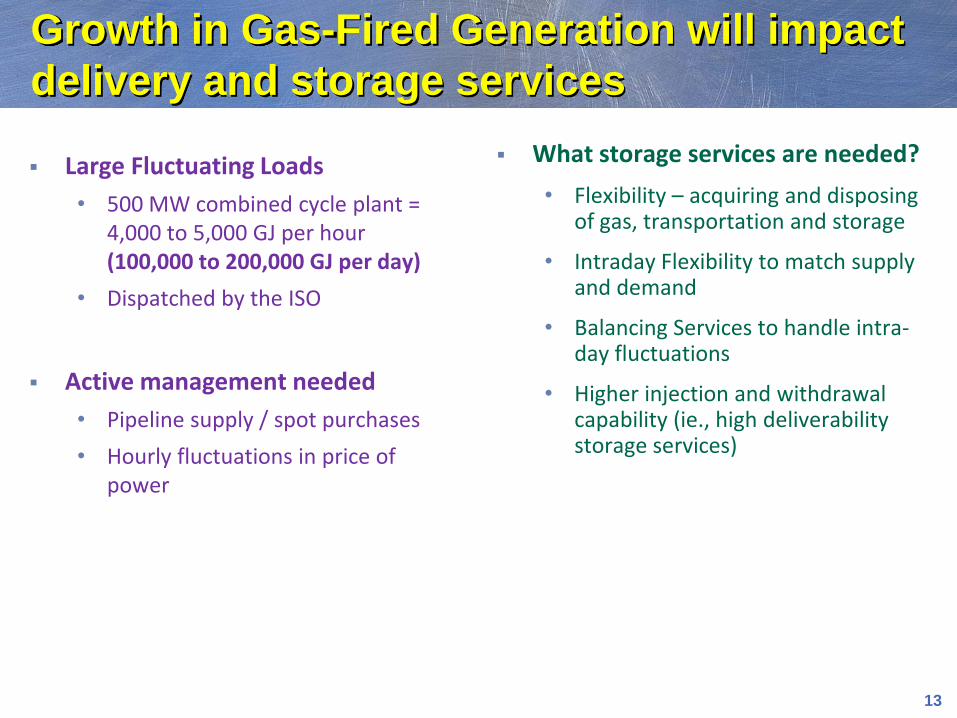

Growth in Gas-Fired Generation will impact

delivery and storage services

Large Fluctuating Loads

• 500 MW combined cycle plant = 4,000 to 5,000 GJ per hour (100,000 to 200,000 GJ per day)

• Dispatched by the ISO

Active management needed

• Pipeline supply / spot purchases

• Hourly fluctuations in price of power

What storage services are needed?

• Flexibility – acquiring and disposing of gas, transportation and storage

• Intraday Flexibility to match supply and demand

• Balancing Services to handle intra-day fluctuations

• Higher injection and withdrawal capability (ie., high deliverability storage services)

14

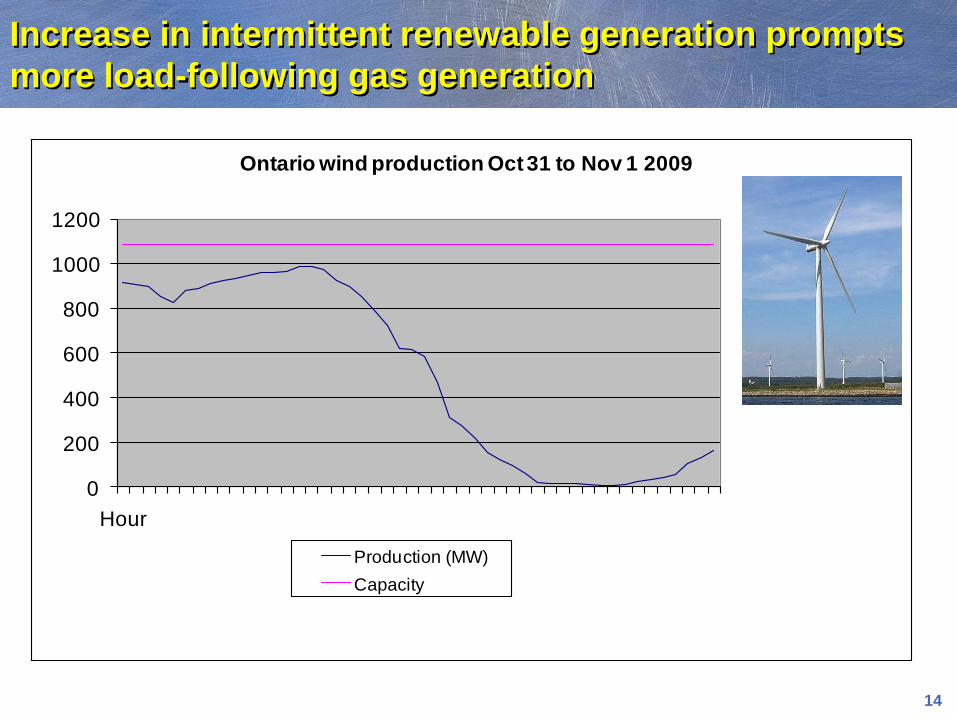

Increase in intermittent renewable generation prompts

more load-following gas generation

0

200

400

600

800

1000

1200

Hour

Ontario wind production Oct 31 to Nov 1 2009

Production (MW)

Capacity

15

Enbridge Gas Distribution (EGD) has been building and supporting the natural gas vehicle (NGV) market in Ontario for over 20 years.

NGV’s account for 75% of EGD’s 825-vehicle fleet – the largest such fleet in Canada.

Enbridge benefited in 2007 from $916,000 in cost savings across the whole fleet ($1,447 per NGV per year) and reduced carbon dioxide emissions by an estimated 680 tonnes.

Natural Gas Vehicles may be an opportunity to

expand gas markets in the future

16

Replacing heavy diesel fleet with LNG trucks offers

environmental benefits, if barriers can be overcome

Long-haul trucks are one of the fastest growing sources of GHGs, accounting for 24%

Barriers face the trucking industry’s entry to LNG:

Need for liquefaction facilities

LNG refueling locations

Capital/conversion cost premiums

Pilot projects proposed to confirm the viability of “blue corridors”

Role for government in policy and fiscal measures

17

In conclusion, the industry simply needs

demand!

Unconventional gas is a “game-changer”Resource base is vastly expanded

Diversity in supply sources and transportation options is increased

Gas prices will be moderate

Investment in infrastructure is critical

More pipelines are required to deliver gas from unconventional sources to markets

Expansions to storage capacity

North American market is demand-constrainedPower generation will lead growth, but resource endowment can support more

Is this the time for NGVs?

Related Documents