CHAPTER 24 Full Disclosure in Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis * 1. The disclosure principle; type of disclosure. 2, 3 1, 2, 3 * 2. Role of notes that accompany financial statements. 1, 4, 5 1, 2 1, 2, 3, 4 * 3. Subsequent events. 6 3 1, 2 1 4, 12 * 4. Segment reporting; diversified firms. 7, 8, 9, 10, 11 4, 5, 6, 7 3 2 5, 6, 7 * 5. Management discussion and analysis. 12, 13 * 6. Interim reporting. 16, 17, 18, 19 8, 9 * 7. Audit opinions and fraudulent reporting. 20, 21 11 * 8. Earnings forecasts. 14, 15 10 *9. Interpretation of ratios. 22, 23, 24 4, 5, 6 5 *10. Impact of transactions on ratios. 8 4, 5, 6 3 13 *11. Liquidity ratios. 8 4, 5, 6 3, 5 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-1

ch24

Oct 27, 2015

ACC326 Solutions Manual and instructors guide Kieso Intermediate Accounting Edition 15

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER 24

Full Disclosure in Financial Reporting

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics Questions BriefExercises Exercises Problems

Concepts for Analysis

* 1. The disclosure principle; type of disclosure.

2, 3 1, 2, 3

* 2. Role of notes that accompany financial statements.

1, 4, 5 1, 2 1, 2, 3, 4

* 3. Subsequent events. 6 3 1, 2 1 4, 12

* 4. Segment reporting; diversified firms.

7, 8, 9, 10, 11

4, 5, 6, 7 3 2 5, 6, 7

* 5. Management discussion and analysis.

12, 13

* 6. Interim reporting. 16, 17, 18, 19

8, 9

* 7. Audit opinions and fraudulent reporting.

20, 21 11

* 8. Earnings forecasts. 14, 15 10

*9. Interpretation of ratios. 22, 23, 24 4, 5, 6 5

*10. Impact of transactions on ratios. 8 4, 5, 6 3 13

*11. Liquidity ratios. 8 4, 5, 6 3, 5

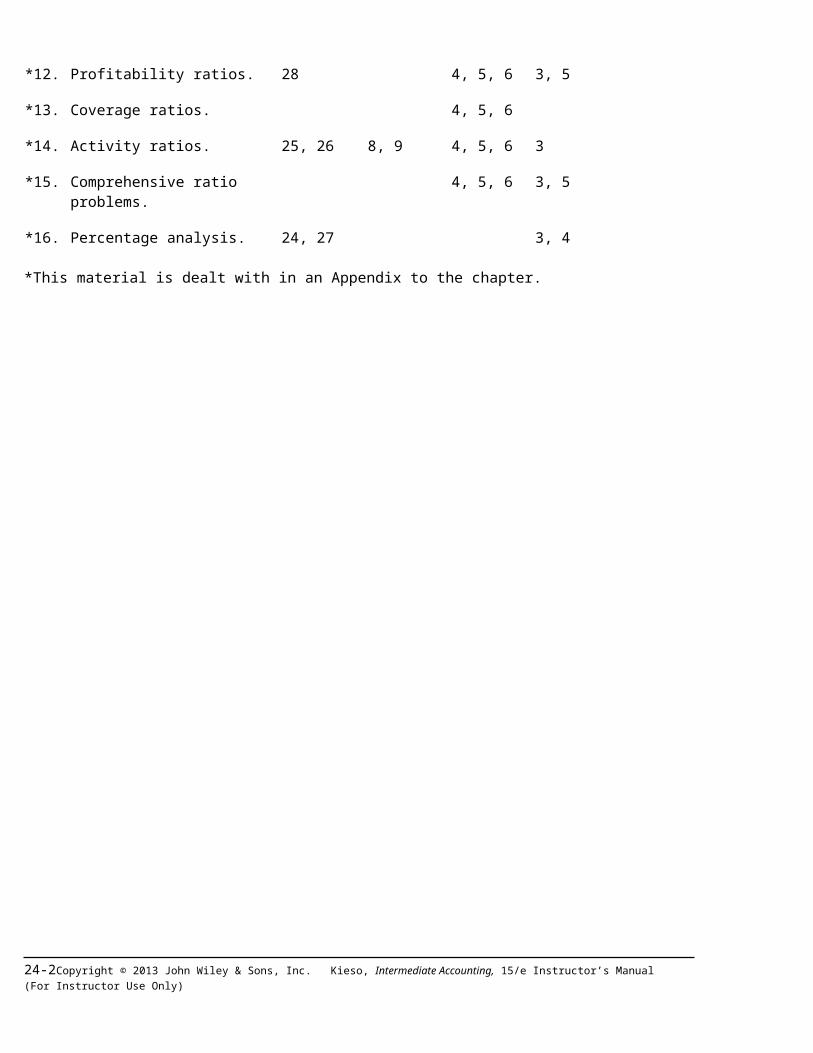

*12. Profitability ratios. 28 4, 5, 6 3, 5

*13. Coverage ratios. 4, 5, 6

*14. Activity ratios. 25, 26 8, 9 4, 5, 6 3

*15. Comprehensive ratio problems. 4, 5, 6 3, 5

*16. Percentage analysis. 24, 27 3, 4

*This material is dealt with in an Appendix to the chapter.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-1

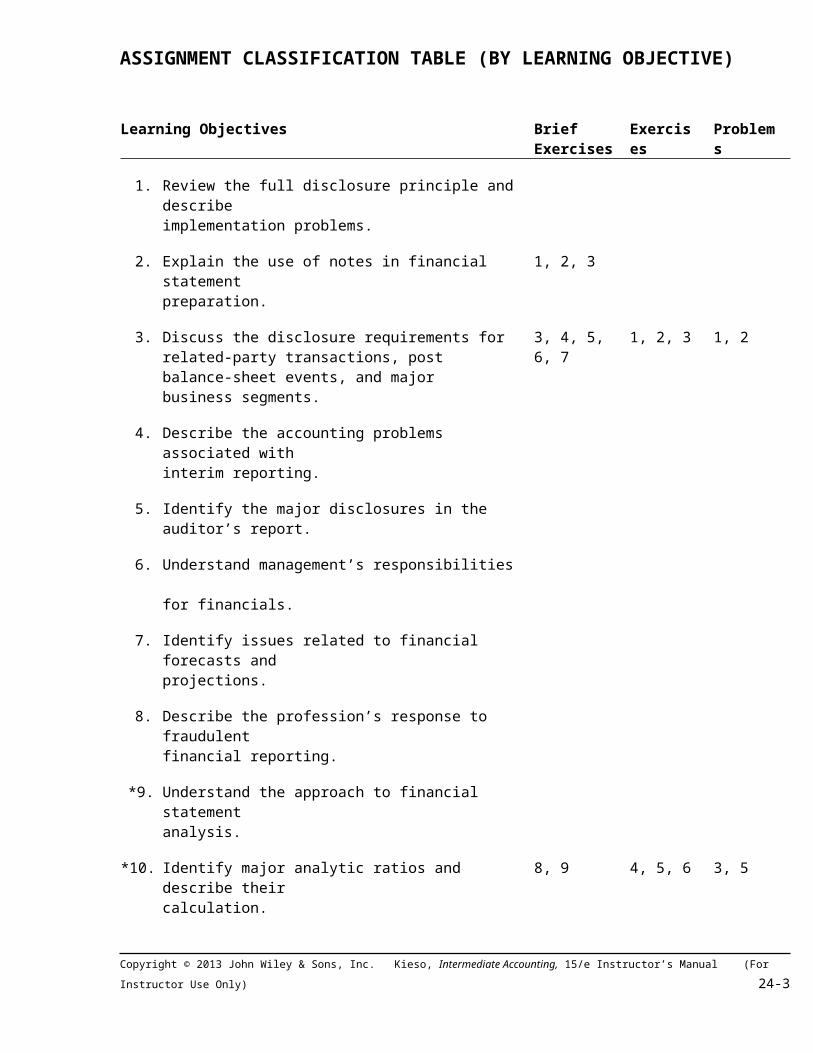

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives Brief Exercises Exercises Problems

1. Review the full disclosure principle and describe implementation problems.

2. Explain the use of notes in financial statement preparation.

1, 2, 3

3. Discuss the disclosure requirements for related-party transactions, post balance-sheet events, and major business segments.

3, 4, 5, 6, 7 1, 2, 3 1, 2

4. Describe the accounting problems associated with interim reporting.

5. Identify the major disclosures in the auditor’s report.

6. Understand management’s responsibilities for financials.

7. Identify issues related to financial forecasts and projections.

8. Describe the profession’s response to fraudulent financial reporting.

*9. Understand the approach to financial statement analysis.

*10. Identify major analytic ratios and describe their calculation.

8, 9 4, 5, 6 3, 5

*11. Explain the limitations of ratio analysis.

*12. Describe techniques of comparative analysis. 3

*13. Describe techniques of percentage analysis. 4

24-2 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

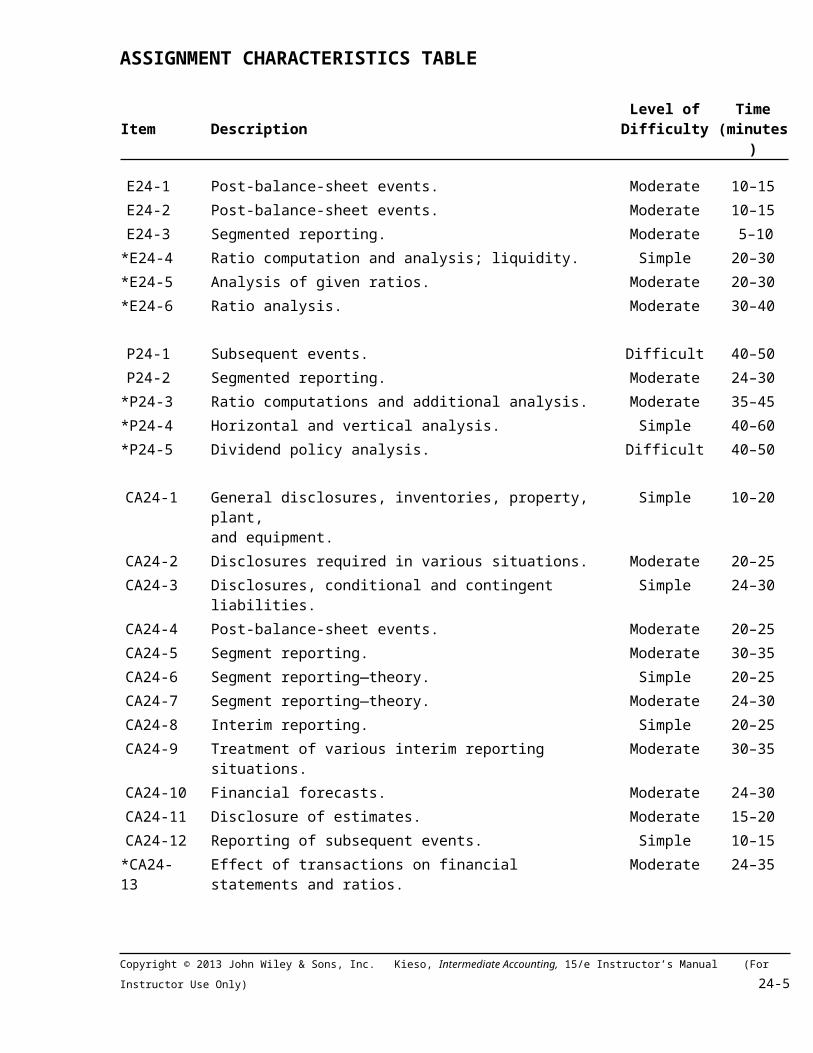

ASSIGNMENT CHARACTERISTICS TABLE

Item DescriptionLevel ofDifficulty

Time(minutes)

E24-1 Post-balance-sheet events. Moderate 10–15

E24-2 Post-balance-sheet events. Moderate 10–15

E24-3 Segmented reporting. Moderate 5–10

*E24-4 Ratio computation and analysis; liquidity. Simple 20–30

*E24-5 Analysis of given ratios. Moderate 20–30

*E24-6 Ratio analysis. Moderate 30–40

P24-1 Subsequent events. Difficult 40–50

P24-2 Segmented reporting. Moderate 24–30

*P24-3 Ratio computations and additional analysis. Moderate 35–45

*P24-4 Horizontal and vertical analysis. Simple 40–60

*P24-5 Dividend policy analysis. Difficult 40–50

CA24-1 General disclosures, inventories, property, plant, and equipment.

Simple 10–20

CA24-2 Disclosures required in various situations. Moderate 20–25

CA24-3 Disclosures, conditional and contingent liabilities. Simple 24–30

CA24-4 Post-balance-sheet events. Moderate 20–25

CA24-5 Segment reporting. Moderate 30–35

CA24-6 Segment reporting—theory. Simple 20–25

CA24-7 Segment reporting—theory. Moderate 24–30

CA24-8 Interim reporting. Simple 20–25

CA24-9 Treatment of various interim reporting situations. Moderate 30–35

CA24-10 Financial forecasts. Moderate 24–30

CA24-11 Disclosure of estimates. Moderate 15–20

CA24-12 Reporting of subsequent events. Simple 10–15

*CA24-13 Effect of transactions on financial statements and ratios. Moderate 24–35

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-3

LEARNING OBJECTIVES

1. Review the full disclosure principle and describe implementation problems.2. Explain the use of notes in financial statement preparation.3. Discuss the disclosure requirements for related-party transactions, post balance-sheet events,

and major business segments.4. Describe the accounting problems associated with interim reporting.5. Identify the major disclosures in the auditor’s report.6. Understand management’s responsibilities for financials.7. Identify issues related to financial forecasts and projections.8. Describe the profession’s response to fraudulent financial reporting.

*9. Understand the approach to financial statement analysis.*10. Identify major analytic ratios and describe their calculation.*11. Explain the limitations of ratio analysis.*12. Describe techniques of comparative analysis.*13. Describe techniques of percentage analysis.

*This material is covered in an Appendix to the chapter.

24-4 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

CHAPTER REVIEW

1. Chapter 24 addresses the topic of financial statement disclosure. Accountants and business executives are fully aware of the importance of full disclosure when presenting financial statements. However, determining what constitutes full disclosure in financial reporting is not an easy task. The purpose of this chapter is to review present disclosure requirements and gain insight into future trends in this area. Appendix 24A presents basic financial statement analysis.

2. (L.O. 1) Recent trends in financial reporting reflect an increase in the amount of disclosure found in financial statements. This increased disclosure is a result of the efforts of the SEC and the FASB. The pronouncements issued by these organizations include many disclosure requirements that are designed to improve the financial reporting process. Numerous reasons can be cited for this increased emphasis on disclosure requirements. Some of the more significant reasons include (a) the complexity of the business environment, (b) the necessity for timely information, and (c) the use of accounting as a control and monitoring device.

3. A trend toward differential disclosure is also occurring. For example, the SEC requires that companies report to it certain substantive information that is not found in annual reports to stockholders. Likewise, the FASB, recognizing that certain disclosure requirements are costly and unnecessary for certain companies, has eliminated reporting requirements for nonpublic enterprises in such areas as fair value of financial instruments and segment reporting. The FASB is working with an advisory committee to explore ways that its standards can be more cost-effective for all companies, regardless of size.

Notes to Financial Statements

4. (L.O. 2) Notes are an integral part of the financial statements of a business enterprise. Although they are normally drafted in somewhat technical language, notes are the accountant’s means of amplifying or explaining the items presented in the main body of the statements. Many of the note disclosures which are common in financial accounting are discussed and presented throughout the text. The more common note disclosures are as follows:

a. Accounting Policies. This information is designed to inform the statement reader of the accounting methods used in preparing the information included in the financial statements. Accounting policies of a given entity are the specific accounting principles and methods currently employed and considered most appropriate in the circumstances to present fairly the financial statements of the enterprise.

b. Inventory. The basis upon which inventory amounts are stated (lower of cost or market) and the method used in determining cost (LIFO, FIFO, average cost, etc.) must also be reported.

c. Property, Plant and Equipment. The basis of valuation for property, plant, and equip-ment should be stated (usually historical cost). Pledges, liens, and other commitments related to these assets should be disclosed. In the presentation of depreciation,

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-5

companies should disclose the following in the financial statements or in the notes: (1) depreciation expense for the period; (2) balances of major classes of depreciable assets, by nature and function at the balance sheet date; (3) accumulated depreciation, either by major classes of depreciable assets or in total at the balance sheet date; and (4) a general description of the method or methods used in computing depreciation with respect to major classes of depreciable assets. Finally, companies should explain any major impairments.

d. Creditor Claims. Note schedules regarding such obligations provide additional information about how a company is financing its operations, the costs it will bear in future periods, and the timing of future cash outflows. Financial statements must disclose for each of the next five years following the date of the statements the aggregate amount of maturities and sinking fund requirements for all long-term borrowings.

e. Equityholders’ Claims. The rights of various equity security issues along with certain unique features that may apply to certain issues are commonly disclosed in notes to the financial statements. In addition, it is necessary to disclose certain types of restrictions currently in force.

f. Contingencies and Commitments. Because many contingent gains or losses are not included in the accounts, their disclosure in the notes provides relevant information to financial statement users. These contingencies may take a variety of forms such as litigation, debt, and other guarantees, possible tax assessments, renegotiation of government contracts, sales of receivables with recourse, and more.

g. Fair Values. Companies that have assets or liabilities measured at fair value must disclose both the cost and the fair value of the financial instruments in the notes. Information that enables users to determine the extent of usage of fair value and the inputs used to implement fair value measurement is also disclosed.

h. Deferred Taxes, Pensions, and Leases. Extensive disclosures are required in these three areas. A careful reading of the notes to the financial statements provides information as to off-balance sheet commitments, future financing needs, and the quality of a company’s earnings.

i. Changes in Accounting Principles. Either in the summary of significant accounting policies or in the other notes, changes in accounting principles (as well as material changes in estimates and corrections of errors) should be discussed.

Special Transactions

5. In some instances, a corporation is faced with a sensitive issue that requires disclosure in the financial statements. Examples of items that can be characterized as sensitive include: related party transactions, errors and irregularities, and illegal acts. It is important for the accountant/auditor, who must determine the adequacy of the disclosure, to exercise care in balancing the rights of the company and the needs of the financial statement users.

24-6 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

6. Related-party transactions arise when a company engages in transactions in which one of the parties has the ability to significantly influence the policies of the other. In order to make adequate disclosure, companies should report the economic substance, rather than the legal form, of these transactions.

7. Errors and Irregularities. Companies should correct the financial statements when they discover errors. The same treatment should be given fraud.

8. Illegal acts encompass such items as illegal political contributions, bribes, kickbacks, and other violations of laws and regulations. In these situations, the accountant/auditor must evaluate the adequacy of disclosure in the financial statements.

Subsequent Events

9. Events or transactions which occur subsequent to the balance sheet date, but prior to the issuance of the financial statements should be disclosed in the financial statements. Events that provide additional evidence about conditions that existed at the balance sheet date are referred to as recognized subsequent events and require adjustments to the financial statements. Events that arise subsequent to the balance sheet date are referred to as nonrecognized subsequent events and do not require adjustment of the financial statements.

Reporting for Diversified (Conglomerate) Companies

10. (L.O. 3) With the increase in diversification within business entities, investors are seeking more information concerning the details of diversified (conglomerate) companies. Particularly, they have requested revenue and income information on the individual segments that comprise the total business income figure. Various arguments have been presented both for and against increased disclosure of disaggregated financial information. The FASB has issued extensive reporting guidelines in this area.

11. The basic reporting requirements of segmented information are:

a. Objective of Reporting Segmented Information.

(1) Better understand the enterprise’s performance.

(2) Better assess its prospects for future net cash flows.

(3) Make more informed judgments about the enterprise as a whole.

b. Basic Principles.

General purpose financial statements are required to include selected information on a single basis of disaggregation. The method chosen is referred to as the management approach—which is based on the way management segments the company for making operating decisions.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-7

c. Identifying Operating Segments.

An operating segment is a component of an enterprise:

(1) That engages in business activities from which it earns revenues and incurs expenses.

(2) Whose operating results are regularly reviewed by the company’s chief operating decision-maker to assess segment performance and allocate resources to the segment.

(3) For which discrete financial information is available that is generated by or based on the internal financial reporting system.

Information about two or more operating segments may be aggregated only if the segments have the same basic characteristics in each of the following areas:

(1) The nature of the products or services provided.

(2) The nature of the production process.

(3) The type of class of customer.

(4) The methods of product or service distribution.

(5) If applicable, the nature of the regulatory environment.

12. Whether a segment is significant enough to disclose depends upon whether it satisfies one of the following tests: (a) its revenue is 10% or more of the combined revenue of all the company’s industry segments, (b) the absolute amount of its profit or loss is 10% or more of the greater of the combined operating profit of all operating segments that did not incur a loss, or the combined loss of all operating segments that did incur a loss, or (c) its identifiable assets are 10% or more of the combined assets of all operating segments. In addition, the segmented results must equal or exceed 75% of the combined sales to unaffiliated customers for the entire company, and a company should probably not report more than 10 segments.

13. The accounting principles to be used for segment disclosure need not be the same as the principles used to prepare the consolidated statements. Allocations of joint, common, or company-wide costs solely for external reporting purposes are not required.

14. The FASB, however, does require that a company report (a) general information about its operating segments, (b) segment profit and loss and related information, (c) segment assets, (d) reconciliations, (e) information about products and services and geographic areas, and (f) major customers.

Interim Reports

15. (L.O. 4) Interim reports are financial reports issued by a business enterprise for a period of less than one year. The SEC requires certain companies coming under its control to file quarterly financial statements that are similar in form and content to their annual reports.

24-8 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

16. The same accounting principles used for annual reports should be applied in preparing interim reports. However, the general approach used in preparing these reports is the subject of some debate. Two different approaches have been advocated in practice. One approach is referred to as the discrete approach and the other is the integral approach. Those advocating the discrete approach believe that each interim period should be treated as a separate accounting period. Those who favor the integral approach consider the interim report to be an integral part of the annual report. At present, many companies follow the discrete approach for certain types of expenses and the integral approach for others, because the standards employed in practice are vague and lead to differing interpretations.

17. GAAP reflects a preference for the integral approach in preparing interim reports. However, certain items do not lend themselves to strict application of the guideline. As a result, unique reporting problems are encountered for such items as (a) advertising and similar costs, (b) expenses subject to year-end adjustments, (c) income taxes, (d) extraordinary items, (e) earnings per share, and (f) seasonality.

18. The fact that many business entities encounter seasonal variations in their operations poses a problem in the analysis of interim reports. The greater the degree of seasonality experienced by a company, the greater the possibility for distortion. For example, a seasonal business that earns 50% of its net income in one quarter may lead the analyst to spurious conclusions. In such a situation, the analyst would be misled if the results of any one of the quarters were interpreted as representing one-fourth of the year’s operating results. Thus, caution should be exercised when attempting to draw generalizations from a single interim report.

19. Although some standards exist for interim reporting, the subject is in need of a thorough review and analysis. It is unclear as to whether the discrete, integral, or some combination of these two methods will be proposed. In addition to the problems noted, the profession continues to debate the extent of involvement an independent auditor should have with interim reports.

Auditor’s Report

20. (L.O. 5) An auditor’s report is issued each time an independent auditor performs an audit of a company’s financial statements. An auditor’s report is essentially the expression of an opinion, by the auditor, on the fairness with which the financial statements present the company’s financial position and results of operations. In the auditor’s report, the auditor must state whether the financial statements were presented in accordance with generally accepted accounting principles. Also, if such principles were not consistently applied, the auditor should make the reader aware of this fact in the auditor’s report.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-9

21. If an auditor arrives at the opinion that the financial statements are fairly presented, the report that is issued is known as an unqualified opinion. When an auditor is unable to express an unqualified opinion (normally as a result of scope limitation, financial statement inadequacies, or material uncertainties), he will issue either (a) a qualified opinion, (b) an adverse opinion, or (c) disclaim an opinion. Departures from an unqualified opinion put the financial statement reader on guard as to possible deficiencies in the presentation of the financial statements. When the auditor departs from the standard unqualified audit report, the reason for the departure must be clearly indicated in the audit report.

Management’s Reports

22. (L.O. 6) The Securities and Exchange Commission (SEC) requires corporate management to include a disclosure in the corporate annual report referred to as management’s discussion and analysis (MD&A). This section of the annual report includes management’s beliefs about favorable and unfavorable trends in liquidity, capital resources, and results of operations. Also, management is to identify significant events and uncertainties that affect these three factors. The MD&A section also must provide information concerning the effects of inflation and changing prices, if material, to the financial statements.

23. Companies also report on management’s responsibilities for financial statements which includes explanation of its responsibilities for, and assessment of, the internal control system. The purposes of this report are (1) to increase the investor’s understanding of the roles of management and the auditor in preparing financial statements, and (2) to heighten the awareness of senior management of its responsibilities for the company’s financial and internal control system.

Reporting on Financial Forecasts and Projections

24. (L.O. 7) Prospective financial statements are financial statements based upon the entity’s expectations about future operation. There are two types of prospective financial statements: (a) financial forecasts, and (b) financial projections. A financial forecast is composed of prospective financial statements that present, to the best of the company’s knowledge and belief, its expected financial position, results of operations, and cash flows. A financial projection is composed of prospective financial statements that present, to the best of the company’s knowledge and belief—given one or more hypothetical assumptions—its expected financial position, results of operations, and cash flows.

Internet Financial Reporting

25. Organizations are developing new technologies and standards to further enable Internet financial reporting. XBRL (eXtensible Business Reporting Language) is used to “tag” accounting data to correspond to financial reporting items in the balance sheet, income statement, and cash flow statement. Once tagged, the data can be easily processed using spreadsheets and other computer programs. The SEC is planning to require all companies and mutual funds to prepare their financial reports using XBRL.

24-10 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

Fraudulent Financial Reporting

26. (L.O. 8) Fraudulent financial reporting is defined as intentional or reckless conduct, whether act or omission, that results in materially misleading financial statements. Situational pressures on the company as well as individual pressures on management personnel can result in fraudulent activities which lead to fraudulent financial reporting. A weak corporate climate contributes to these situations. The Sarbanes-Oxley Act, in response to corporate fraud, raised the penalty substantially for executives who are involved in fraudulent financial reporting.

Appendix 24A: Basic Financial Statement Analysis

*27. (L.O. 9) Appendix 24A focuses on the methodology used in the interpretation and evaluation of the information presented in financial statements. The appendix discusses the computational aspects of the various techniques used in the analysis of financial statements as well as their meaning and significance. A variety of groups are interested in the financial progress of a business organization. These groups include creditors, stockholders, potential investors, management, governmental agencies, and labor leaders to name a few. The interests of these groups and the kind of financial information and analysis that can satisfy those interests are discussed in this appendix.

Ratio Analysis

*28. (L.O. 10) Thus far, the discussion presented in the text has been concerned with the measurement and reporting functions of accounting. Appendix 24A discusses the communication function of accounting that involves analyzing and interpreting the economic information presented in financial statements. The techniques used in the analysis of financial statement data include: (a) ratio analysis, (b) comparative analysis, and (c) percentage analysis.

*29. Effective financial statement analysis is a skill that requires knowledge of the available techniques and extensive experience. The techniques can be learned by studying a textbook presentation on the subject. However, effective financial statement analysis requires the ability to (a) select the appropriate technique, and (b) interpret the significance of the results obtained.

*30. Ratios can be classified as follows:

a. Liquidity Ratios. Measures of the company’s short-run ability to pay its maturing obligations.

b. Activity Ratios. Measures of how effectively the company is using the assets employed.

c. Profitability Ratios. Measures of the degree of success or failure of a given company or division for a given period of time.

d. Coverage Ratios. Measures of the degree of protection for long-term creditors and investors.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-11

*31. In the following paragraphs, the individual ratios included in the four classifications will be presented. The method of presentation will include: (a) identification of the ratio, (b) the manner in which the ratio is computed, and (c) the significance of the ratio. It is important to note that the significance of ratio analysis is dependent on a complete understanding of the circumstances surrounding the computation. Thus, the interpretation of any one ratio cannot be accomplished in a vacuum. The proper interpretation of ratios involves trend analysis, comparisons with other ratios or industry averages, and a thorough understanding of the environment within which the entity operates.

LIQUIDITY RATIOS

*32. The current ratio (Ch. 13) is the ratio of total current assets to total current liabilities. It is computed by dividing current assets by current liabilities, and is sometimes referred to as the working capital ratio. The significance of the current ratio concerns the company’s ability to meet its maturing short-term obligations.

*33. The acid-test ratio (Ch. 13) relates total current liabilities to the most liquid current assets (cash, short-term investments, and net receivables). To compute the acid-test ratio, these current assets are divided by total current liabilities. This ratio is significant in that it focuses on the ability of a company to meet its short-term debt immediately.

*34. The current cash debt coverage ratio (Ch. 5) is computed by dividing net cash provided by operating activities by average current liabilities. This ratio measures a company’s ability to pay off its current liabilities in a given year out of its operations.

ACTIVITY RATIOS

*35. The receivables turnover ratio (Ch. 7) is computed by dividing net sales by net average receivables (beginning plus ending divided by 2) outstanding during the year. This ratio provides an indication of how successful a firm is in collecting its outstanding receivables. As a general rule, the receivables turnover is acceptable if it does not exceed the time allowed for payment under the selling terms by more than 10 to 15 days.

*36. The inventory turnover ratio (Ch. 9) is a function of average inventory (beginning plus ending divided by 2) and cost of goods sold. This ratio is computed by dividing cost of goods sold by average inventory. Normally, a high inventory turnover is sought by a company along with a minimum of “stock-out costs.”

*37. The asset turnover ratio (Ch. 11) is determined by dividing net sales for the period by average total assets. This ratio indicates how efficiently the company utilizes its assets. If the turnover ratio is high, the implication is that the company is using its assets effectively to generate sales. If the asset turnover ratio is low, the company either has to use its assets more efficiently or dispose of them.

PROFITABILITY RATIOS

*38. The profit margin on sales (Ch. 11) is computed by dividing net income by net sales for the period. The significance of this ratio is that it indicates that amount of profit, on a percentage basis, that results from each sales dollar earned by the company.

24-12 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

*39. Dividing net income by average total assets yields the rate of return on assets (Ch. 11) earned by a company. In computing this ratio, companies sometimes use net income before the subtraction of interest charges because, they contend, interest represents a cost of securing additional assets and, therefore, should not be considered as a deduction in arriving at the amount of return on assets.

*40. The rate of return on common stock equity (Ch. 15) is computed by dividing net income minus preferred dividends by average common stockholders equity. When the rate of return on total assets is lower than the rate of return on common stock equity, the company is said to be trading on the equity at a gain. The term “trading on the equity” describes the practice of using borrowed money at fixed interest rates or issuing preferred stock with constant dividend rates in hopes of earning a higher rate of return on the money used than the interest or preferred dividends paid.

*41. As mentioned earlier in the text, many investors consider earnings per share (Ch. 16) to be the most significant statistic presented by a business entity. A discussion of the significance of earnings per share and the manner in which it is computed is presented in Chapter 16. Basically, earnings per share is computed by dividing net income minus preferred dividends by the weighted-average number of shares of common stock outstanding. However, a complex capital structure alters this computation significantly.

*42. The payout ratio (Ch. 15) is the ratio of cash dividends paid to common shareholders to net income. This ratio gives investors an indication of the portion of net income a company distributes to its common stockholders. If investors desire cash yield from an investment in stock, they should seek out entities with high payout ratios.

COVERAGE RATIOS

*43. The extent to which creditors are protected in the event of an entity’s insolvency may be determined by the debt to total assets ratio (Ch. 14). This information may also be gained from the ratio of long-term debt to stockholders’ equity or the ratio of stockholders’ equity to long-term debt.

*44. The times interest earned ratio (Ch. 14) is computed by dividing net income before interest charges and taxes by the interest charge. This ratio focuses on the ability of a company to cover all its interest charges. In general, difficulty in meeting interest obligations is indicative of serious financial problems.

*45. The cash debt coverage ratio (Ch. 5) is computed by dividing net cash provided by operating activities by average total liabilities. This ratio indicates a company’s ability to repay its liabilities from net cash provided by operating activities, without having to liquidate the assets employed in its operations.

*46. The book value per share of stock (Ch. 15) is the amount each share would receive if a company were liquidated and the amounts reported on the balance sheet were realized. Book value per share is computed by allocating the stockholders’ equity items among the various classes of stock and then dividing the total so allocated to each class of stock by the number of shares outstanding. This calculation loses its significance when the amounts reported on the balance sheet do not reflect the fair value of the items.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-13

Limitations of Ratio Analysis

*47. (L.O. 11) Ratio analysis is not without its limitations. Before placing a great deal of reliance on ratios alone, an investor must be aware of the fact that any ratio is only as sound as the financial data upon which it is built. The great variety of accounting policies relating to the computation of net income provides a good example of the reasons for exercising caution when interpreting financial ratios.

*48 One important limitation of ratios is that they generally are based on historical cost, which can lead to distortions in measuring performance. Investors must remember that where estimated items (such as depreciation and amortization) are significant, income ratios lose some of their credibility. Probably the greatest limitation of ratio analysis is the difficult problem of achieving comparability among firms in a given industry.

Comparative and Percentage Analysis

*49. (L.O. 12) The presentation of comparative financial statements affords an analyst the opportunity to determine trends and analyze the progress an entity has made over a specified period of time. The annual financial statement presentation in a corporate annual report normally includes detailed comparative financial statements for the current and preceding year along with a 5- or 10-year summary of pertinent financial data.

*50. (L.O. 13) Percentage or common-size analysis is a method frequently used to evaluate a company. This type of analysis involves reducing all the dollar amounts to a percentage of a base amount in the financial statement. All items in an income statement are frequently expressed as a percentage of sales or sometimes as a percentage of cost of sales. The items in a balance sheet are often analyzed as a percentage of total assets. Horizontal analysis is a form of percentage analysis that is useful in evaluating trend situations. Another approach, called vertical analysis, involves expressing each number on a financial statement in a given period as a percentage of some base amount.

*Note: All asterisked (*) items relate to material contained in the Appendices to the chapter.

24-14 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

LECTURE OUTLINE

The material in this chapter can be covered in two or three class periods.

A. (L.O. 1) Full Disclosure Principle: Report any financial facts significant enough to influence the judgment of an informed reader. However, issues to be considered are:

1. Costs of disclosure.

2. Information overload.

3. The increase in disclosure requirements is linked to:

a. Complexity of the business enterprise.

b. Necessity for timely information.

c. Accounting as a control and monitoring device.

4. Differential disclosure,

a. Big GAAP versus little GAAP.

Illustration 24-1 provides an overview of the types of information that are useful in financial decisions.

B. (L.O. 2) Notes to the Financial Statements: A means of full disclosure and providing qualitative and supplementary data:

1. Summary of Significant Accounting Policies. Should be the first note.

2. Inventory (Chapter 9). The basis upon which inventory amounts are stated and the method used in determining cost.

3. Property, Plant, and Equipment (Chapter 11). The basis of valuation, pledges, loans, or other commitments related to these assets. For depreciation: period expense, balances of major classes of depreciation assets, and balance of accumulated depreciation by major class or in total.

4. Creditor Claims (Chapter 14). How financing operations, costs to be borne in future periods, and timing of future cost outflows. Disclose for each of 5 years after the financial statement date, the aggregate amount of maturities and sinking fund requirements for all long-term borrowings.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-15

5. Equityholders’ Claims (Chapters 15 and 16). In addition to number of shares authorized, issued and outstanding, disclose such items as stock options, convertible securities, and types of restrictions on the amount of earnings available for dividend distribution.

6. Contingencies and Commitments (Chapters 7, 9, and 13). Contingencies related to litigation, debt, tax assessments, etc. Commitments related to dividend restrictions, purchase agreements, hedge contracts, and employment contracts must be disclosed.

7. Fair Values (Chapter 17). Companies that have assets or liabilities measured at fair value must disclose both cost and the fair value of all financial instruments in the notes. Information that enables users to determine the extent of usage of fair value and the inputs used to implement fair value measurement is also disclosed.

8. Deferred Taxes, Pensions, and Leases (Chapters 19, 20, and 21). Extensive disclosures are required. Should provide information about off-balance-sheet commitments, future financing needs, and the quality of a company’s earnings.

9. Changes in Accounting Principles (Chapter 22). Accounting principle changes, including material changes in estimates and corrections of errors, should be disclosed in the summary of significant accounting policies or in other notes.

C. Disclosure of Special Transactions or Events.

1. Related Party Transactions: Transactions which have not been carried out on an “arms-length” or free market basis. The nature of the relationship, a description of the transaction, and the dollar amounts involved must be disclosed.

2. Errors (unintentional mistakes) and irregularities (intentional distortions of financial statements).

3. Illegal Acts. Include bribes, kickbacks, and other violations of laws and regulations.

D. Subsequent Events. Events that occur subsequent to date of the financial statements, but before issuance.

1. Events that provide additional evidence about conditions that existed at the balance sheet date, and that require adjustments to the financial statements.

2. Events that provide evidence about conditions that did not exist at the balance sheet date, but arise subsequent to that date, and that do not require adjustment of the financial statements.

E. (L.O. 3) Reporting for Diversified (Conglomerate) Companies.

1. Segment data allow users to see how different product lines contribute to the firm’s profitability, risk, and growth potential.

2. Pros and Cons of Disclosing Segment Information.

24-16 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

Reasons against disclosing segment information:

a. Data which is meaningless for, or misleading, to investors.

b. Competitive harm.

c. Adverse impact on internal decisions.

d. Limited usefulness.

e. Investor should be concerned with overall, not segment, performance.

f. Difficulty in allocating common costs.

Reasons for segmented data disclosure:

a. Needed for intelligent decision making by investors.

b. Complete disclosure by all firms (both diversified companies and single product-line companies) creates a better competitive environment.

3. Objective of reporting segmented information: To provide information about the different types of business activities a company engages in, and the different economic conditions in which it operates, to allow users:

a. A better understanding of the enterprise’s performance.

b. The ability to better assess its prospects for future net cash flows.

c. The ability to make more informed judgments about the enterprise as a whole.

4. Management approach. Segments are those components of the business that manage-ment uses to make decisions about operating matters. Evident from organization structure.

5. Identifying operating segments. An operating segment is a component of an enterprise:

a. That engages in business activities from which it earns revenues and incurs expenses.

b. Whose operating results are regularly reviewed by the chief operating decision-maker to assess segment performance and allocate resources to the segment.

c. For which discrete financial information is available that is generated by or based on the internal financial reporting system.

6. Aggregation of Segments is allowed if the combined segments have the same basic characteristics in each of the following areas:

a. The nature of the products or services provided.

b. The nature of the production process.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-17

c. The type or class of customer.

d. The methods of product or service distribution.

e. If applicable, the nature of the regulatory environment.

7. Tests for significance. Made to determine if a segment is significant enough to warrant disclosure. Must satisfy at least one of the following:

a. Its revenue is 10% or more of the combined revenue of all segments.

b. The absolute amount of its profit or loss is 10% or more of the greater, in absolute amount, of:

(1) The combined operating profit of all operating segments that did not incur a loss, or

(2) The combined loss of all operating segments that did incur a loss.

c. Its identifiable assets are 10% or more of the combined assets of all operating segments.

8. Additional factors.

a. Segmented results to be disclosed, based on the tests for significance, must equal or exceed 75% of the combined sales to unaffiliated customers, and

b. The maximum number of segments disclosed should not exceed 10.

9. Measurement principles.

a. Accounting principles used for segment disclosure need not be the same as those used to prepare the consolidated statements.

b. Allocations to segments are assumed to be directly attributable or reasonably allocable.

10. Segmented information reported. The FASB requires that an enterprise report:

a. General information about its operating segments.

b. Segment profit and loss and related information.

(1) Revenues from transactions with external customers.

(2) Revenues from transactions with other operating segments.

(3) Interest revenue and expense.

(4) Depreciation, depletion, and amortization expense.

24-18 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

(5) Unusual items.

(6) Equity in the net income of investees accounted for by the equity method.

(7) Income tax expense or benefit.

(8) Extraordinary items.

(9) Significant noncash items other than depreciation, depletion, and amortization expense.

c. Segment assets.

d. Reconciliations.

(1) Total operating segments’ profits and losses to the company’s income before taxes.

(2) Total operating segments’ assets to total assets of the company.

e. Information about products and services and geographic areas. For each operating segment not based on geography, the company must report, if practicable.

(1) Revenues from external customers.

(2) Long-lived assets.

(3) Expenditures during the period for long-lived assets.

This information, if material, must be reported in the company’s country of domicile and each other country.

f. Major customers. Disclose the total amount of revenues from each customer that accounts for 10% or more of the segment’s revenues.

F. (L.O. 4) Interim Reports.

Illustration 24-2 can be used to discuss the reporting requirements associated with interim reports.

1. Discrete versus Integral Views. Many companies use both approaches.

a. Discrete view. Each interim period is treated as a separate accounting period.

b. Integral view. Interim reports are an integral part of the annual report.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-19

2. GAAP requirements.

a. Exceptions allowed for inventory pricing.

(1) The use of the gross profit method.

(2) LIFO liquidation.

(3) Temporary inventory market declines.

(4) Planned variances expected to be absorbed should be deferred.

b. Period costs. May be expensed as incurred or allocated among interim periods on the basis of an estimate of time expired, benefit received, or activity associated with the periods.

c. Minimum disclosures.

(1) Sales or gross revenues, provision for income taxes, extraordinary items, and net income.

(2) Basic and diluted EPS where appropriate.

(3) Seasonal revenue, cost, or expenses.

(4) Significant changes in estimates or provisions for income taxes.

(5) Disposal of a component of a business extraordinary, unusual, or infrequently occurring items.

(6) Contingent items.

(7) Changes in accounting principles or estimates.

(8) Significant changes in financial position.

3. Unique Problems of Interim Reporting.

a. Advertising and Similar Costs: Should such costs be deferred in an interim period if the benefits extend beyond that period?

b. Expenses Subject to Year-End Adjustment: Examples such as bad debts and executive bonuses. These costs should be estimated and allocated to interim periods.

c. Income Taxes: The estimated annual effective tax rate should be used.

d. Extraordinary Items: Charge or credit the gain or loss in the quarter that it occurs instead of allocating.

24-20 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

e. Earnings per Share: In computing EPS each interim period stands alone.

f. Seasonality: The seasonal nature of the business should be disclosed.

G. (L.O. 5) Auditor’s report.

1. Reporting standards.

a. The report must state whether the financial statements are presented in accordance with GAAP.

b. The report must state those circumstances where consistency does not exist.

c. Disclosures are to be regarded as reasonably adequate, unless otherwise stated in the report.

d. The report must contain an expression of opinion regarding the financial statements taken as a whole or an assertion to the effect that an opinion cannot be expressed.

2. Opinions which the auditor may express: unqualified, qualified, adverse, or disclaimer of opinion.

3. Certain circumstances, although they do not affect the auditor’s unqualified opinion, may require the auditor to add an explanatory paragraph to the audit report.

a. Going concern.

b. Lack of consistency.

c. Emphasis of a matter.

4. Reasons for departure from unqualified opinion.

a. Scope of examination is limited or effected by conditions or restrictions.

b. Statements do not fairly present financial position or results of operations because of lack of conformity with GAAP and/or inadequate disclosure.

H. (L.O. 6) Management’s reports.

1. Management’s discussion and analysis (MD&A). Requires management to high-light favorable or unfavorable trends and to identify significant events and uncertainties that affect:

a. Liquidity.

b. Capital resources.

c. Results of operations. Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-21

2. MD&A must also provide information concerning the effects of inflation and changing prices, if material to financial statement trends.

3. Management’s responsibilities for financial statements.

a. The Sarbanes-Oxley act requires the SEC to develop guidelines for all publicly traded companies to report on management’s responsibilities for, and assessment of, the internal control system.

I. (L.O. 7) Reporting on Financial Forecasts and Projections.

1. Forecasts and projections take one of two forms:

a. Financial forecasts provide information on what is expected to happen.

b. Financial projections provide information on what might take place given one or more hypothetical assumptions.

2. Arguments for requiring published forecasts:

a. Better decision-making information.

b. Already circulated informally.

c. Historical cost information may not be adequate.

3. Reasons against requiring published forecasts:

a. Problems with accuracy.

b. Impact on internal decisions.

c. Legal liability.

d. Competitive harm.

4. AICPA standards.

5. SEC safe harbor rule.

6. Questions of liability.

7. Internet financial reporting and XBRL.

J. (L.O. 8) Fraudulent Financial Reporting.

1. Causes.

2. Response of the profession, including Sarbanes-Oxley Act.

24-22 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

K. (L.O. 9) Appendix 24A. Basic Financial Statement Analysis.

1. Uses of Financial Analysis. The type of analysis employed depends on who the analyst is, and what his or her interest is:

a. Short-term creditors. Ability to pay currently maturing obligations.

b. Bondholders. Long-term prospects.

c. Stockholders. Long-term prospects, particularly stability of future earnings.

d. Managers. Composition of capital structure and changes and trends in earnings.

2. (L.O. 10) Basic Measures of Financial Analysis.

a. Liquidity Ratios. Measure short-run ability of the firm to pay its maturing obligations.

b. Activity Ratios. Measure effectiveness in using assets.

c. Profitability Ratios. Measure the overall success of the firm.

d. Coverage Ratios. Measure the degree of protection for long-term creditors and investors.

Illustration 24-3 summarizes the financial ratios presented throughout the text.

3. (L.O. 11) Limitations of Ratio Analysis.

a. Fair value information is generally not considered.

b. Data for different firms in an industry may not be comparable.

c. The role of estimates in the accounting process should be considered.

d. Important information appears in sources other than just the financial statements.

4. (L.O. 12) Comparative Analysis: Analyzing data from the same firm at two or more different dates or periods.

5. (L.O. 13) Percentage (Common-Size) Analysis: Reducing a series of related amounts to a series of percentages of a given base.

a. Horizontal analysis. Indicates the proportionate change of an item between periods.

b. Vertical analysis. Indicates the proportion of each item on a statement to a base figure.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-23

*L. (L.O. 14) IFRS Insights

1. IFRS and GAAP disclosure requirements are similar in many regards. The IFRS addressing various disclosure issues are IAS 24 (“Related Party Disclosures”), disclosure and recognition of post-statement of financial position events in IAS 10 (“Events after the Balance Sheet Date”), segment reporting IFRS provisions in IFRS 8 (“Operating Segments”), and interim reporting requirements in IAS 34 (“Interim Financial Reporting”).

2. Similarities

a. GAAP and IFRS have similar standards on post-statement of financial position (subsequent) events. That is, under both sets of standards, events that occurred after the statement of financial position date, and which provide additional evidence of conditions that existed at the statement of financial position date, are recognized in the financial statements.

b. Like GAAP, IFRS requires that for transactions with related parties, companies disclose the amounts involved in a transaction; the amount, terms, and nature of the outstanding balances; and any doubtful amounts related to those outstanding balances for each major category of related parties.

c. Following the recent issuance of IFRS 8, “Operating Segments,” the requirements under IFRS and GAAP are very similar. That is, both standards use the management approach to identify reportable segments, and similar segment disclosures are required.

d. Neither GAAP nor IFRS require interim reports. Rather, the SEC and securities exchanges outside the United States establish the rules. In the United States, interim reports generally are provided on a quarterly basis; outside the United States, six-month interim reports are common.

3. Differences

a. Due to the broader range of judgments allowed in more principles-based IFRS, note disclosures generally are more expansive under IFRS compared to GAAP.

b. Subsequent (or post-statement of financial position) events under IFRS are evaluated through the date that financial instruments are “authorized for issue.” GAAP uses the date when financial statements are “issued.” Also, for share dividends and splits in the subsequent period, IFRS does not adjust but GAAP does.

c. Under IFRS, there is no specific requirement to disclose the name of the related party, which is this case under GAAP.

d. Under IFRS, interim reports are prepared on a discrete basis; GAAP generally follows the integral approach.

24-24 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

ILLUSTRATION 24-1TYPES OF FINANCIAL INFORMATION

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-25

ILLUSTRATION 24-2INTERIM REPORTS

24-26 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only)

ILLUSTRATION 24-3RATIOS

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e Instructor’s Manual (For Instructor Use Only) 24-27

Related Documents