Chapter 19 Financial Planning and Forecasting Learning Objectives 1. Explain what a financial plan is and why financial planning is important. 2. Discuss how management uses financial planning models in the planning process, and explain the importance of sales forecasts in the construction of financial planning models. 3. Discuss how the relation between projected sales and balance sheet accounts can be determined, and be able to analyze a strategic investment decision using a percent of sales model. 4. Describe the conditions under which fixed assets vary directly with sales, and discuss the impact of so-called lumpy assets on this relation. 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 19Financial Planning and Forecasting

Learning Objectives

1. Explain what a financial plan is and why financial planning is important.

2. Discuss how management uses financial planning models in the planning process,

and explain the importance of sales forecasts in the construction of financial

planning models.

3. Discuss how the relation between projected sales and balance sheet accounts can be

determined, and be able to analyze a strategic investment decision using a percent of

sales model.

4. Describe the conditions under which fixed assets vary directly with sales, and

discuss the impact of so-called lumpy assets on this relation.

5. Explain what factors determine a firm’s sustainable growth rate, discuss why it is of

interest to management, and be able to compute the sustainable growth rate for a

firm.

I. Chapter Outline

19.1 Financial Planning

A. The Planning Documents

1

Financial planning relates to the identification of the kinds of projects that a

firm needs to undertake and the ways of financing those projects. This results

in a financial plan.

In putting together a financial plan, four main issues are addressed by

management through detailed planning.

Strategic plan—Where is the company headed?

Investment plan—What capital resources does the management need to

get there?

Financing plan—How is the firm going to pay for the resources needed?

Cash budget—How is the firm going to pay its day-to-day bills?

The financial plan integrates the firm’s basic plans into a single planning

document with a detailed budget.

Typically, the plan extends over a three- to five-year period called the

planning horizon.

1. The Strategic Plan

It describes the vision of the firm.

It documents the firm’s long-term goals, the strategies that management will

use to achieve the goals, and the capabilities the firm needs to sustain its

competitive position.

The planning is done by the firm’s top management, with the financial

manager providing key input, and it has to be approved by the board of

directors.

The strategic plan identifies:

2

The line of business that the firm will compete in.

Major areas of investment in real assets.

Capital expenditures

Acquisitions and new lines of business

Mergers, alliances, and divestitures that may happen in the near future.

2. The Investment Plan (Capital Budget)

It is the part of the investment plan that describes the firm’s outlay for plant

and equipment.

A firm’s business strategy determines the capital expenditures it will make.

Capital expenditures can be one-time investments or routine investments that

allow the firm to continue its operations.

Once a capital investment is made, it is almost always impossible to reverse.

Three steps are involved in the capital budgeting process:

Management identifies a list of potential projects that are consistent with

the business strategy.

Senior management ranks the projects according to the value they would

create for the shareholders.

Finally, the proposed capital budget schedule is reviewed by senior

management for funding and sets the capital budget.

3. The Financing Plan

Based on the list prepared in the capital budget, management now needs to

decide how to fund the projects

3

The firm will try and use a blend of internally generated funds and externally

raised funds to finance the capital expenditures.

Depending on the level of internally generated funds available to the firm, the

firm will seek to raise funds in the form of either debt or equity.

There are three elements to a financing plan:

First, a financing plan identifies the dollar amount of funds that has to be

raised externally and the sources of funds available to the firm.

Second, the plan states management’s desired capital structure for the

firm.

Finally, the financing plan states the firm’s dividend policy, which is

relevant because it dictates the amount of funds that have to be raised in

the capital markets.

4. Divisional Business Plans

The business plans prepared by the firm’s various business divisions are also

part of the firm’s financial plans.

They identify how the various divisions will strive to achieve the corporate

goals.

They also identify the resources needed by each of the divisions to implement

their strategies.

5. Cash Budget

An overall cash budget for the firm is generated based on all the divisional

cash budgets and that of the corporate offices.

It focuses on the cash inflows and outflows of the firm.

4

It allows the firm to determine if any borrowing is necessary.

A poorly developed cash budget could lead to serious cash shortages.

B. The Financial Plan—Putting It All Together

The plan focuses on the two major decisions that management will make: (1)

the investment decision and (2) the financing decision.

Next, each of the firm’s business divisions’ plans is integrated.

One important tool used in this process is a financial planning model.

Such models provide management with the ability to prepare projected

financial statements.

These projected statements can be used to analyze the investment

alternatives and estimate the amounts of external funding needed.

C. Benefits of Financial Planning—Alignment and Support

It helps management to establish financial and operating goals for the firm and

to communicate those goals throughout the firm.

The financial plan can help align the actions of managers and their operating

units with the firm’s strategic goals.

19.2 Financial Planning Models

They help management analyze investment and financing alternatives.

Most sophisticated planning models are now created as software and make the

process speedy and accurate.

5

A. The Importance of Sales Forecasts

Sales forecast techniques come in quite an array—from best estimates by the

sales staff to complex multivariate forecast models.

They are usually generated from within the company.

Since sales are often correlated to the regional or national economy,

macroeconomic forecast are incorporated into the model.

B. Building a Financial Planning Model: Inputs and Outputs

Inputs are necessary to build the financial models that are designed to provide

specific outputs.

Financial statements serve as the first major input and become the baseline to

compare the projected financial statements.

Next comes the sales forecast in the form of the projected growth in sales.

Changes in the firm’s balance sheet and income statement items as a result of

the growth in sales are also used in these models.

Macroeconomic forecasts and their impact on the firm’s sales are also

included.

Last, investment and financing decisions are incorporated as inputs.

The outputs of the financial planning model are a series of pro forma financial

statements and financial ratios based on these statements.

These pro forma balance sheets may not be balanced. The difference

between assets and liabilities and owners’ equity, often referred to as the

plug value, often represents the external funding needed.

6

C. A Simple Planning Model

A very basic planning model is called the percent of sales model.

The driving factor of this model is the expected sales growth rate.

All or most of the input variables (i.e., the income statement and balance sheet

elements) vary directly with sales.

19.3 A Better Financial Planning Model

Unlike the previously described model, this model takes a more realistic approach in

its assumptions.

Not all balance sheet and income statement items vary directly with sales.

All variable costs and most current assets and current liabilities vary directly with

sales.

A. The Income Statement

The pro forma income statement is generated by recognizing all variable costs

change directly with sales.

Two key ratios are calculated—dividend payout ratio and retention ratio.

The first measures the percentage of net income paid out as dividends to

shareholders, while the second measures the percentage of net income

reinvested by the firm as retained earnings.

B. The Balance Sheet

7

Some balance sheet items vary directly with sales, while others do not.

To determine which accounts vary directly with sales, a trend analysis may be

conducted on historic balance sheets of the firm.

Typically, working capital accounts like inventory, accounts receivables, and

accounts payables vary directly with sales.

Fixed assets do not always vary directly with sales. It will do so only if the

firm is operating at 100 percent capacity and fixed assets can be incrementally

changed.

The ratio of total assets to net sales is called the capital intensity ratio. This

ratio tells us the amount of assets needed by the firm to generate $1 sales.

The higher the ratio, the more capital the firm needs to generate sales—the

more capital intensive the firm.

Firms that are highly capital intensive are more risky than those that are

not because a downturn can reduce sales sharply, but fixed costs do not

change rapidly.

C. Liabilities and Equity

Only current liabilities are likely to vary directly with sales. The exception

here is notes payables (short-term borrowings) that changes as the firm pays it

down or makes an additional borrowing.

Long-term liabilities and equity accounts change as a direct result of

managerial decisions like debt repayment, stock repurchase, and issuing new

debt or equity.

8

Retained earnings will vary as sales change but not directly. It is affected by

the firm’s dividend payout policy.

D. The Preliminary Pro Forma Balance Sheet

First, calculate the projected values for all the accounts that vary with sales.

Second, calculate the projected value of any other balance sheet account for

which an end-of-period value can be forecast or otherwise determined.

Third, enter the current year’s number for all the accounts for which the next

year’s figure cannot be calculated or forecast.

At this point, the balance sheet will be unbalanced. A plug value is necessary

to get the balance sheet to balance.

First, determine the retained earnings based on the firm’s dividend policy.

Next, the plug figure will represent the external financing necessary to

make the total assets equal total liabilities and equity. This calls for

management to choose a financing option—choosing debt, equity or a

combination—to raise the additional funds needed.

E. Management’s Decision

The first decision relates to the firm’s dividend policy. Should the firm alter

its dividend policy to increase the amount of retained earning?

If external funding is still needed, should the firm issue new debt, or issue

equity? Or should it be a mix of both?

9

It is important to recognize that while financial planning models can identify

the amount of external financing needed, the financing option is a managerial

decision.

19.4 Beyond the Basic Planning Models

A. Improving Financial Planning Models

There are several weaknesses in the previously described models.

First, interest expense was not accounted for. This is difficult to do so until all

the financing options are finalized.

Second, all working capital accounts do not necessarily vary directly with

sales, especially cash and inventory.

Third, how fixed assets are adjusted plays a significant role.

When a firm is not operating at full capacity, sales may be increased

without adding any new fixed assets.

Fixed assets are added in large discrete amounts called lumpy assets. Since

it requires time to get new assets operational, they are added as the firm

nears full capacity.

19.5 Managing and Financing Growth

Managers prefer rapid growth as a goal to capture market share and establish a

competitive position.

Most firms experiencing rapid growth fund the growth with debt, increasing

the firm’s leverage and putting it at risk.

10

A. External Funding Needed

External funding needed (EFN) is defined as the additional debt or equity a

firm needs to issue so it can purchase additional assets to support an increase

in sales.

EFN is tied to new investments the management has deemed necessary to

support the sales growth.

The new investments are the projected capital expenditure plus the increase in

working capital necessary to sustain increases in sales.

Companies first resort to internally generated funds in the form of addition to

retained earnings.

Once internally generated funds are exhausted, the firm looks to raise funds

externally. See Equations 19.5 and 19.6.

In analyzing Equation 19.6 two things are apparent.

First, holding dividend policy constant, the amount of EFN depends on the

firm’s projected growth rate. Higher growth rate implies that the firm

needs more new investments and therefore, more funds to have to be

raised externally.

Second, the firm’s dividend policy also affects EFN. Holding the growth

rate constant, the higher the firm’s payout ratio, the larger the amount of

debt or equity financing needed.

B. Internal Growth Rate

11

The internal growth rate (IGR) is defined as the maximum growth rate that

a firm can achieve without external financing. See Equation 19.7.

The higher the retained earnings generated by a firm and the lower the total

assets a firm has, the higher the growth possible without using external

funding.

Equation 19.8 relates IGR to the plowback ratio, return on equity, and

leverage. Firms that achieve higher growth rates without seeking external

financing have the following characteristics:

They have a high plowback ratio.

They employ less equity and/or are able to generate high net income

leading to a high ROE.

They are not highly leveraged.

C. The Sustainable Growth Rate

The sustainable growth rate (SGR) is the rate of growth that the firm can

sustain without selling additional shares of equity.

This measure is important to management because it helps them determine

whether they can avoid issuing new equity. New equity issues are expensive

and cause dilution of earnings to existing shareholders.

As Equation 19.9 shows, the SGR is a function of the plowback ratio and the

ROE.

12

II. Suggested and Alternative Approaches to the Material

The chapter begins with a discussion of what financial planning is all about. This is followed by

an overview of some simple financial planning models. Then the weaknesses in the simple

models are identified, and some better planning models are discussed. The chapter concepts of

internal growth rates and sustainable growth rates are introduced, and this is followed by

coverage of determination of external funding needed to facilitate growth in sales.

Instructors may choose to cover this chapter in a couple of different ways. Some may

choose to take up this chapter in the order it has been placed in the text. Others may elect to

cover it toward the end of the course. This chapter’s material also lends itself to being placed

anywhere the instructor chooses.

13

III. Summary of Learning Objectives

1. What a financial plan is, and why financial planning is so important.

A financial plan is a set of actionable goals derived from the firm’s strategic plan. The

financial plan focuses on selecting the best investment opportunities and determining

how to finance those investments at the lowest possible cost. The overall goal of the

financial plan is to create as much value for the firm as possible. The major outputs from

a financial plan are the pro forma financial statements. A financial plan provides a

blueprint for the firm’s future, aligns all operating units with the firm’s strategic plan, and

provides a common set of goals. An important benefit from financial planning is that it

forces management to think through a number of alternative scenarios, which provides

insights into dealing with unexpected problems as they arise. Finally, financial planning

helps firms prepare contingency plans for events that are unlikely to occur but that would

cause substantial financial injury if they did occur.

2. Discuss how management uses financial planning models in the planning process,

and explain the importance of sales forecasts in the construction of financial

planning models.

Financial models are the analytical part of the financial planning process. A planning

model is simply a series of equations that model a firm’s financial statements, such as the

income statement and balance sheet. Once the model is constructed, management can

generate projected (pro forma) financial statements to determine the financial impact of

proposed strategic initiatives on the firm.

14

For most financial planning models, a forecast of the firm’s sales is the most

important input variable. The sales forecast is the key driver in financial planning models

because many items on the income statement and balance sheet vary directly with sales.

Thus, once sales are forecast, it is easy to generate projected financial statements using

the historical relationship between a particular account and sales.

3. Discuss how the relation between projected sales and balance sheet accounts can be

determined, and be able to analyze a strategic investment decision using a percent of

sales model

Historical financial data can be examined to determine how a variable changes with sales.

One way to do this is to prepare a table that shows four or five years of historical

financial statement data as a percent of sales. Then, fit trend lines to the data to see what

type of relation exists between that variable and sales. Most income statement and

balance sheet items vary directly with sales, but others may vary in a nonlinear manner.

The analysis in the Blackwell Sales Company example illustrates how to analyze a

strategic investment decision.

4. Describe the conditions under which fixed assets vary with sales, and discuss the

impact of so-called lumpy sales on this relation.

Fixed assets vary directly with sales only when assets can be added in small increments

and production facilities are operating near full capacity. This is typically not the case. In

most situations, fixed assets are added in large, discrete units, and, as a result, much of

the new capacity may go unused for a period of time. These types of assets are often

15

called lumpy assets. After lumpy assets are added, sales can increase for a period of time

with no corresponding change in the level of fixed assets.

5. Explain what factors determine a firm’s sustainable growth rate, discuss why it is of

interest to management, and be able to compute the sustainable growth rate for a

firm.

A firm’s sustainable growth rate (SGR) is the maximum rate at which a firm can grow

without external equity financing and with leverage held constant. The determinants of

SGR are (1) profit margins (the greater a firm’s profit margins, the greater the firm’s

SGR); (2) asset utilization (the more efficiently a firm uses its assets, the higher its SGR);

(3) leverage (as a firm increases its use of leverage, its SGR increases); (4) dividend

policy (as a firm decreases its payout ratio, its SGR increases); and (5) economic

conditions (the more favorable the economic environment, the higher the firm’s SGR).

Management may be interested in knowing the SGR for two reasons. First, the SGR is

the rate of growth at which a firm’s capital structure (debt to equity) will remain constant

without the firm selling or repurchasing stock. Second, if a firm’s actual growth rate

exceeds its SGR, the firm could face cash shortage problems in the future unless it can

sell new equity. Learning by Doing Application 19.3 uses the SGR formula.

16

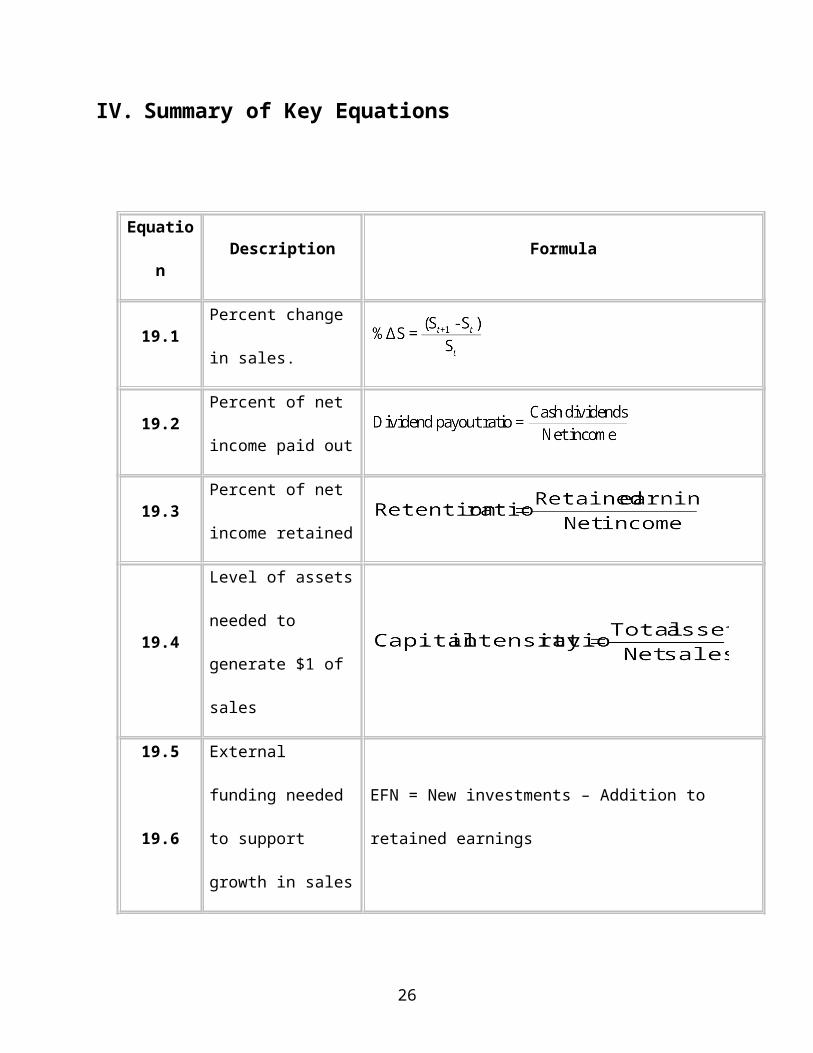

IV. Summary of Key Equations

Equation Description Formula

19.1Percent change in

sales.

19.2Percent of net income

paid out

19.3Percent of net income

retained

19.4Level of assets needed

to generate $1 of sales

19.5

19.6

External funding

needed to support

growth in sales

EFN = New investments – Addition to retained earnings

= (Growth rate × Initial assets) – Addition to retained

earnings

19.7

19.8

Internal growth rate

(level of growth that

can be supported

without raising

external funds) = Plowback ratio × Return on equity × Measure of

17

leverage

19.9

Sustainable growth

rate (level of growth

that can be supported

without raising

external equity or

increasing current

leverage)

SGR = Plowback ratio × ROE

18

V. Before You Go On Questions and Answers

Section 19.1

1. What are the four planning documents on which the financial plan is based?

The four important planning documents are: (1) the strategic plan, which describes where

the firm is headed and articulates the strategies that will be used to get it there; (2) the

investment plan, which identifies the capital assets needed to execute the strategies; (3)

the financing plan, which explains how the firm will raise the money to buy the assets;

and (4) the cash budget, which determines whether the firm will have sufficient cash to

pay its bills. These four planning documents provide the foundation for the firm’s

financial plan, which consolidates the documents into a single scheme.

2. What is the strategic plan?

The strategic plan is developed to communicate the firm’s long term goals from a very

high conceptual level. It is extremely important as the strategy of the firm ultimately

drives all other decisions at the firm.

3. How are the investment decision and financing decision related?

19

When a firm makes a decision to invest in some asset, it must also identify a source of

funding to pay for it. Thus, these two decisions are intertwined and must be made

together.

Section 19.2

1. Why is the sales forecast the key component of a financial model?

Sales forecast is the key component in a financial model as the majority of data used are

calculated as a percentage of sales. Hence, it is important to get as accurate a sales

forecast as possible in order to build a meaningful model.

2. What are pro forma financial statements, and why are they an important part of the

financial planning process?

Pro forma financial statements are hypothetical statements that are projected into the

future. They are then evaluated to determine which investment and under what conditions

will be the most beneficial for the firm.

3. What is the plug factor in a financial model?

The plug factor in a financial model is the source of external financing needed to bring

the balance sheet into balance.

20

Section 19.3

1. How are historical financial data used to determine the forecasted values of balance sheet

accounts?

To forecast balance sheet values, the financial manager prepares a table that shows

several years of historical accounting data as a percentage of sales. Then some simple

trend lines are fitted to the data to see if there are any trends. This allows the forecaster to

decide which financial accounts can safely be estimated as a percent of sales and which

must be forecasted using other information.

2. Explain why you might expect accounts receivable to vary with sales.

Accounts receivable can be expected to vary with sales since higher sales mean more

money coming in, and hence increased level of receivables.

Section 19.4

1. Why is it that some working capital accounts may not vary proportionately with sales?

Working capital takes into account current assets and current liabilities, and in many

instances inventories and cash balances do not proportionately change with sales. The

working capital ratio often increases at a decreasing rate as sales increase.

2. What are lumpy assets, and how do these assets vary with sales?

21

In most instances, fixed assets do not vary directly with sales, but are rather periodically

added in large increments or lumps, hence the name “lumpy assets”.

Section 19.5

1. What two factors determine the amount of EFN?

The amount of EFN is determined by the difference between the total amount of new

assets the firm needs to finance less the amount of internal financing available.

2. What is IGR, and why is it of interest to management?

IGR stands for internal growth rate and is defined as the maximum growth rate a firm can

achieve without external financing. IGR is of management interest, as firms that can

generate a high volume of retained earnings and/or use fewer assets can sustain a higher

growth rate without raising more capital

3. If a firm continually exceeds its SGR, what problems may it face in the future?

If the firm’s actual growth rate consistently exceeds its sustainable growth, the firm will

have a cash shortage problem if it is unwilling to change its targeted capital structure or

22

sell equity. If the firm has a high credit rating and its use of leverage is not excessive, the

firm may have no problem going to the market and securing additional funds.

23

VI. Self-Study Problems

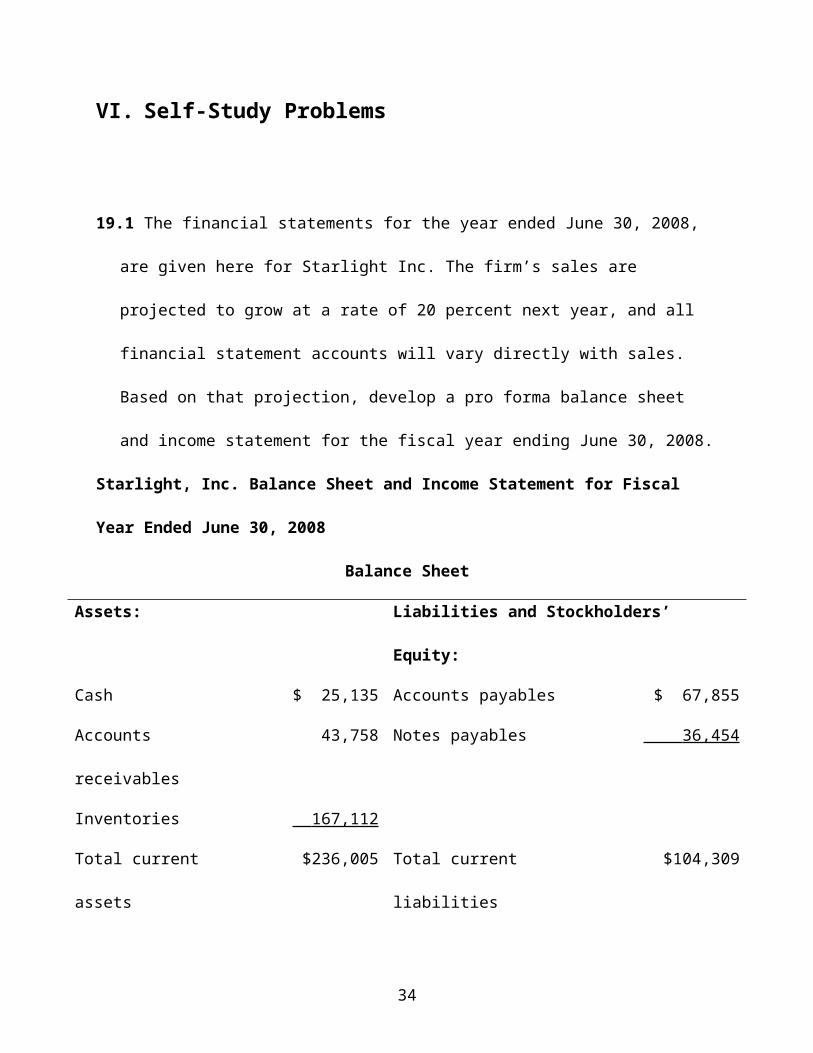

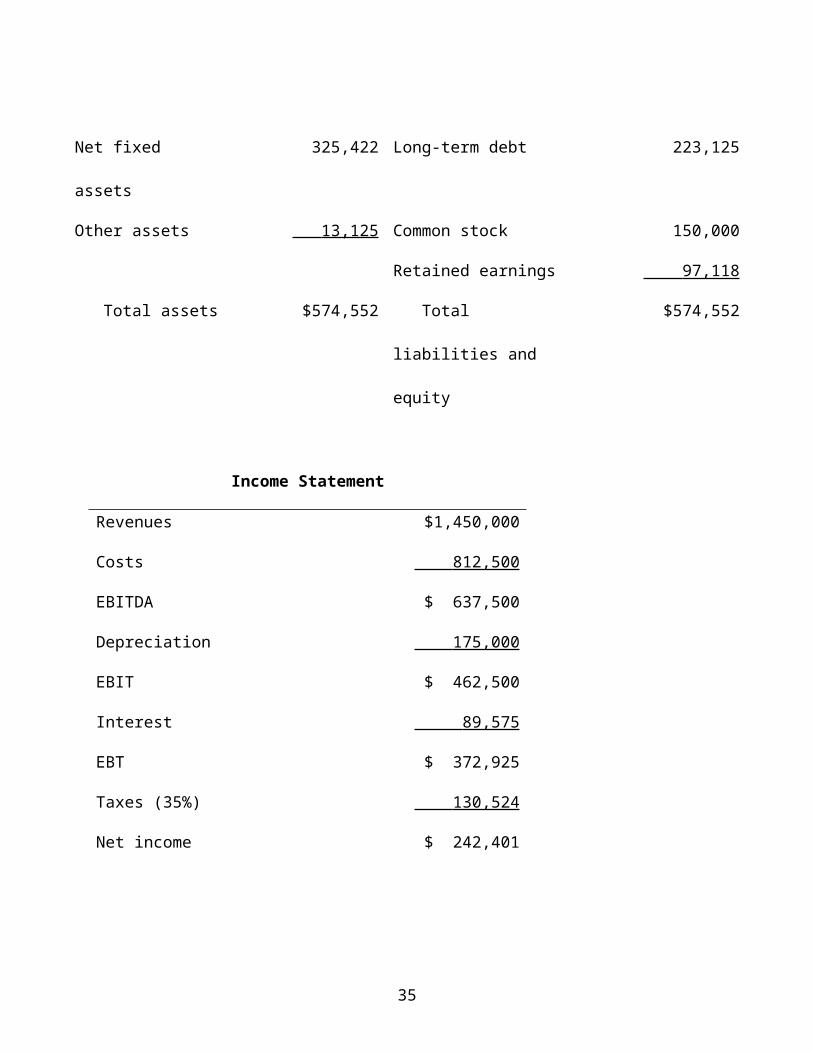

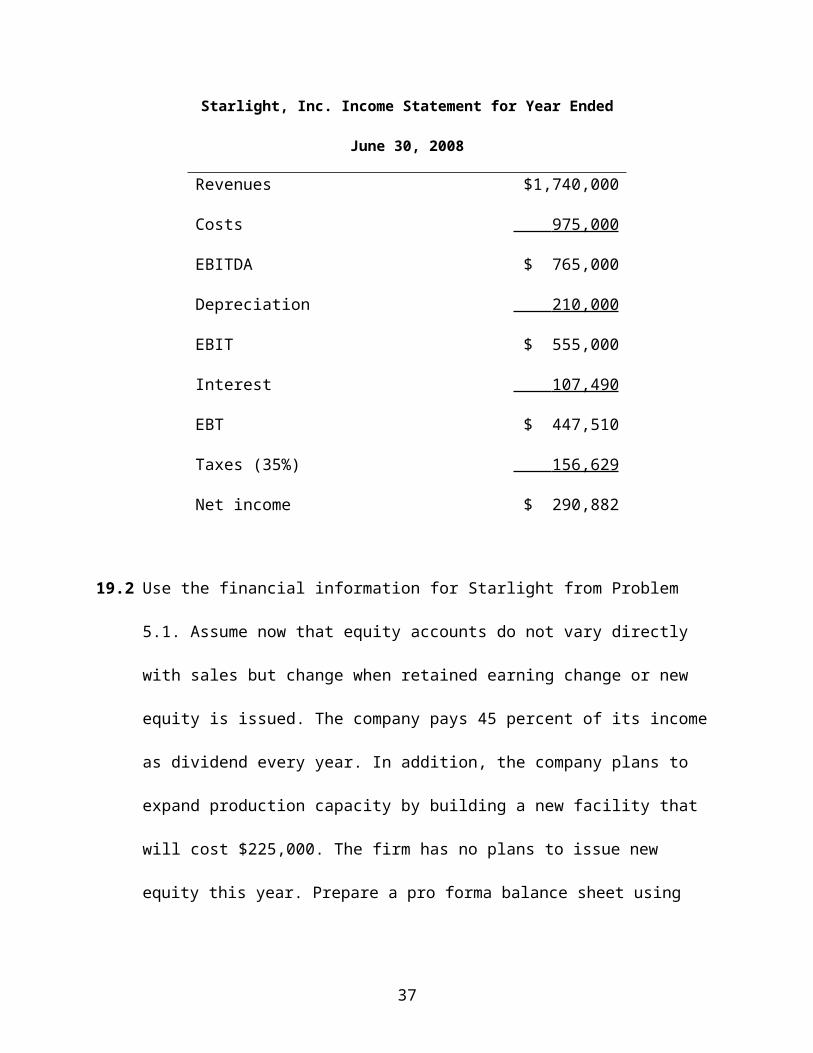

19.1 The financial statements for the year ended June 30, 2008, are given here for Starlight

Inc. The firm’s sales are projected to grow at a rate of 20 percent next year, and all financial

statement accounts will vary directly with sales. Based on that projection, develop a pro

forma balance sheet and income statement for the fiscal year ending June 30, 2008.

Starlight, Inc. Balance Sheet and Income Statement for Fiscal Year Ended June 30, 2008

Balance Sheet

Assets: Liabilities and Stockholders’ Equity:

Cash $ 25,135 Accounts payables $ 67,855

Accounts receivables 43,758 Notes payables 36,454

Inventories 167,112

Total current assets $236,005 Total current liabilities $104,309

Net fixed assets 325,422 Long-term debt 223,125

Other assets 13,125 Common stock 150,000

Retained earnings 97,118

Total assets $574,552 Total liabilities and equity $574,552

Income Statement

Revenues $1,450,000

Costs 812,500

EBITDA $ 637,500

24

Depreciation 175,000

EBIT $ 462,500

Interest 89,575

EBT $ 372,925

Taxes (35%) 130,524

Net income $ 242,401

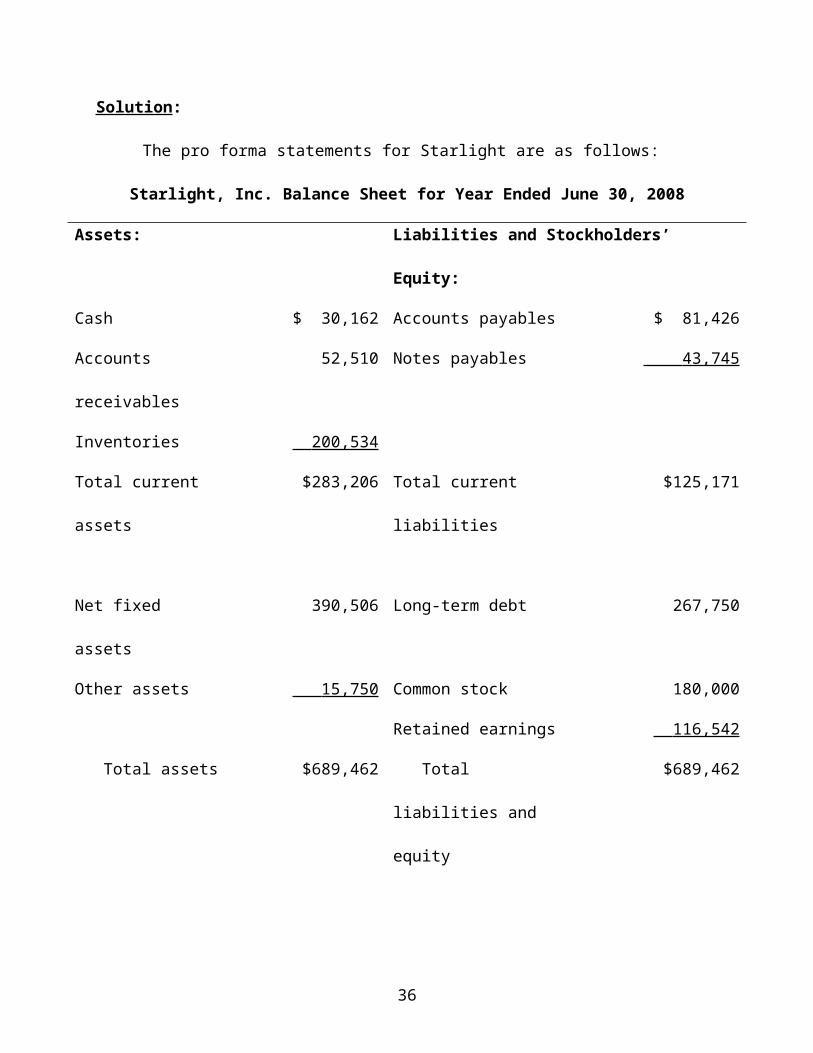

Solution:

The pro forma statements for Starlight are as follows:

Starlight, Inc. Balance Sheet for Year Ended June 30, 2008

Assets: Liabilities and Stockholders’ Equity:

Cash $ 30,162 Accounts payables $ 81,426

Accounts receivables 52,510 Notes payables 43,745

Inventories 200,534

Total current assets $283,206 Total current liabilities $125,171

Net fixed assets 390,506 Long-term debt 267,750

Other assets 15,750 Common stock 180,000

Retained earnings 116,542

Total assets $689,462 Total liabilities and equity $689,462

25

Starlight, Inc. Income Statement for Year Ended June 30, 2008

Revenues $1,740,000

Costs 975,000

EBITDA $ 765,000

Depreciation 210,000

EBIT $ 555,000

Interest 107,490

EBT $ 447,510

Taxes (35%) 156,629

Net income $ 290,882

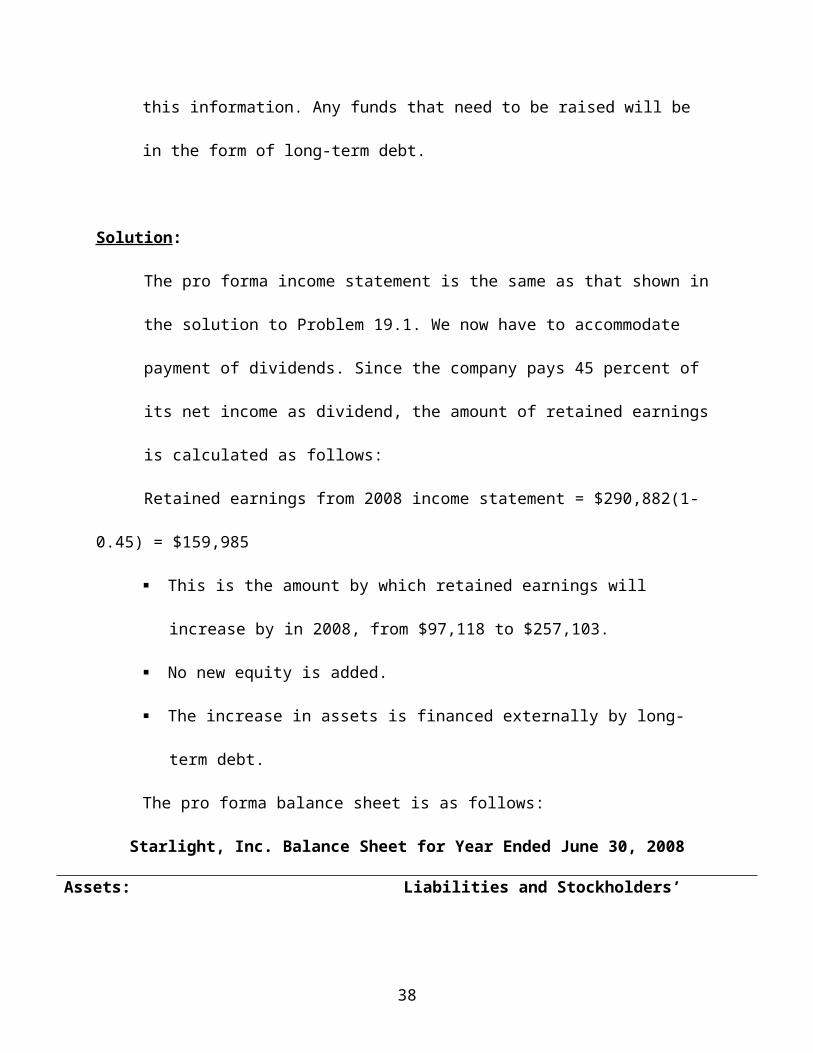

19.2 Use the financial information for Starlight from Problem 5.1. Assume now that equity

accounts do not vary directly with sales but change when retained earning change or new

equity is issued. The company pays 45 percent of its income as dividend every year. In

addition, the company plans to expand production capacity by building a new facility that

will cost $225,000. The firm has no plans to issue new equity this year. Prepare a pro

forma balance sheet using this information. Any funds that need to be raised will be in the

form of long-term debt.

Solution:

The pro forma income statement is the same as that shown in the solution to Problem

19.1. We now have to accommodate payment of dividends. Since the company pays 45

26

percent of its net income as dividend, the amount of retained earnings is calculated as

follows:

Retained earnings from 2008 income statement = $290,882(1-0.45) = $159,985

This is the amount by which retained earnings will increase by in 2008, from $97,118

to $257,103.

No new equity is added.

The increase in assets is financed externally by long-term debt.

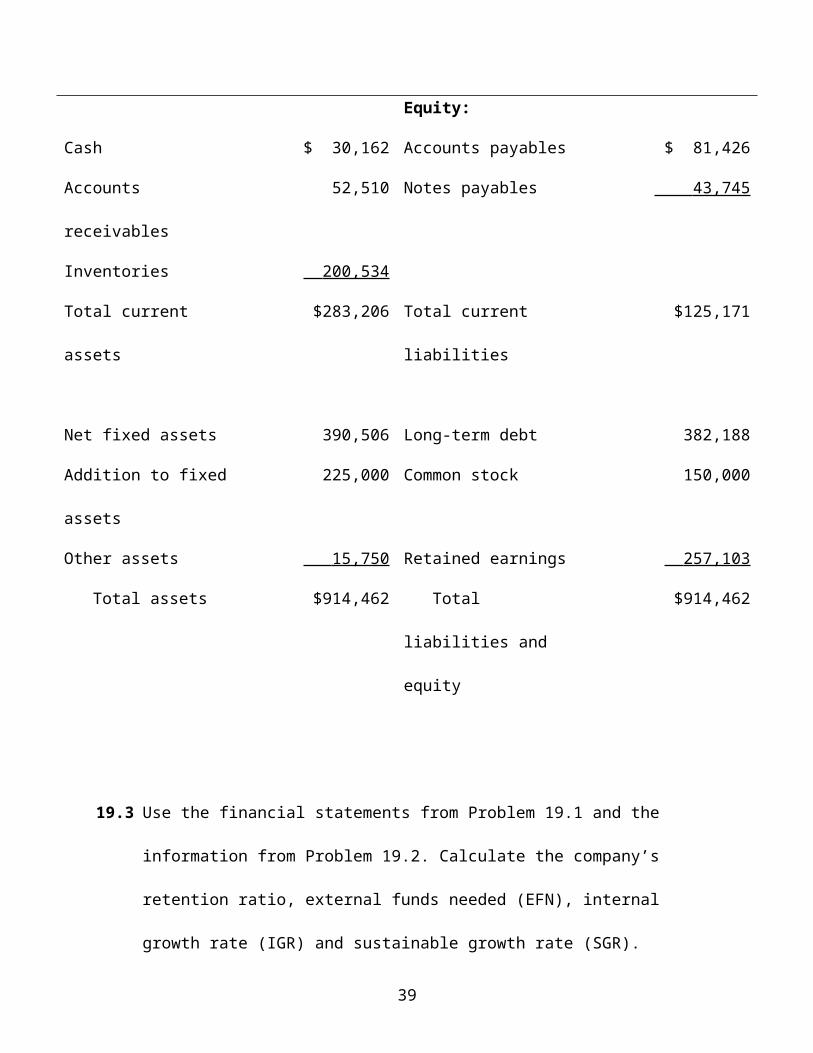

The pro forma balance sheet is as follows:

Starlight, Inc. Balance Sheet for Year Ended June 30, 2008

Assets: Liabilities and Stockholders’ Equity:

Cash $ 30,162 Accounts payables $ 81,426

Accounts receivables 52,510 Notes payables 43,745

Inventories 200,534

Total current assets $283,206 Total current liabilities $125,171

Net fixed assets 390,506 Long-term debt 382,188

Addition to fixed assets 225,000 Common stock 150,000

Other assets 15,750 Retained earnings 257,103

Total assets $914,462 Total liabilities and equity $914,462

27

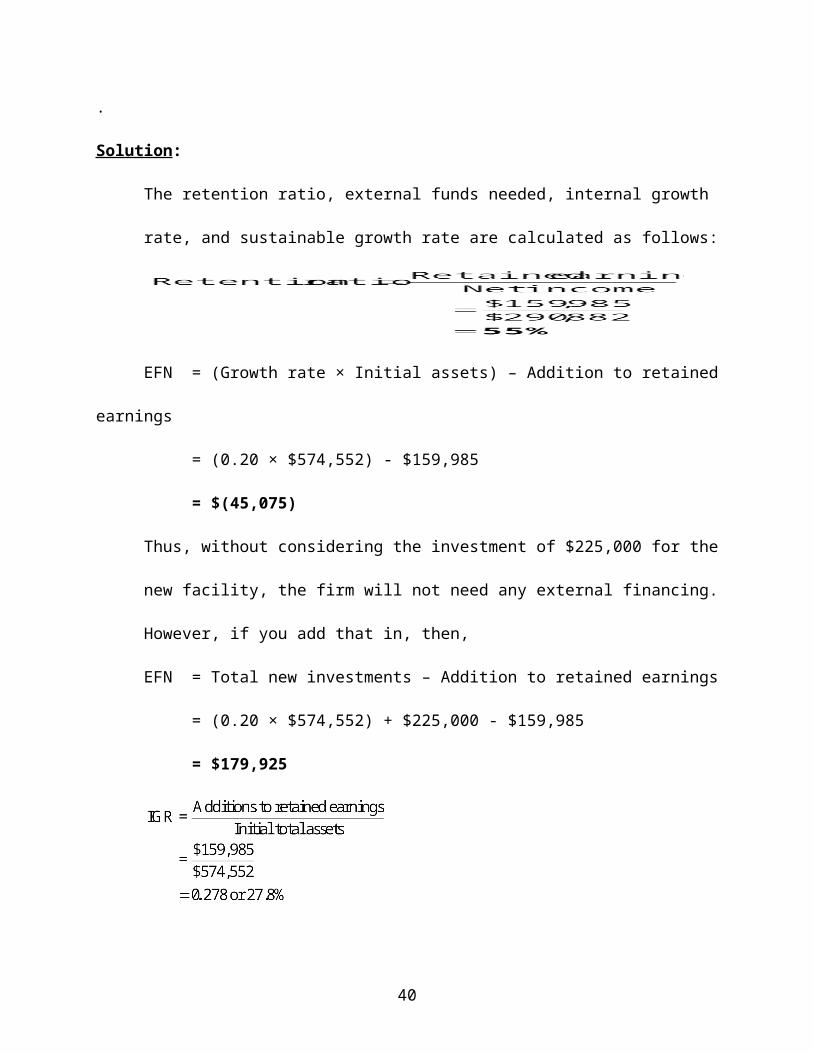

19.3 Use the financial statements from Problem 19.1 and the information from Problem 19.2.

Calculate the company’s retention ratio, external funds needed (EFN), internal growth

rate (IGR) and sustainable growth rate (SGR).

.

Solution:

The retention ratio, external funds needed, internal growth rate, and sustainable growth

rate are calculated as follows:

EFN = (Growth rate × Initial assets) – Addition to retained earnings

= (0.20 × $574,552) - $159,985

= $(45,075)

Thus, without considering the investment of $225,000 for the new facility, the firm will

not need any external financing. However, if you add that in, then,

EFN = Total new investments – Addition to retained earnings

= (0.20 × $574,552) + $225,000 - $159,985

= $179,925

28

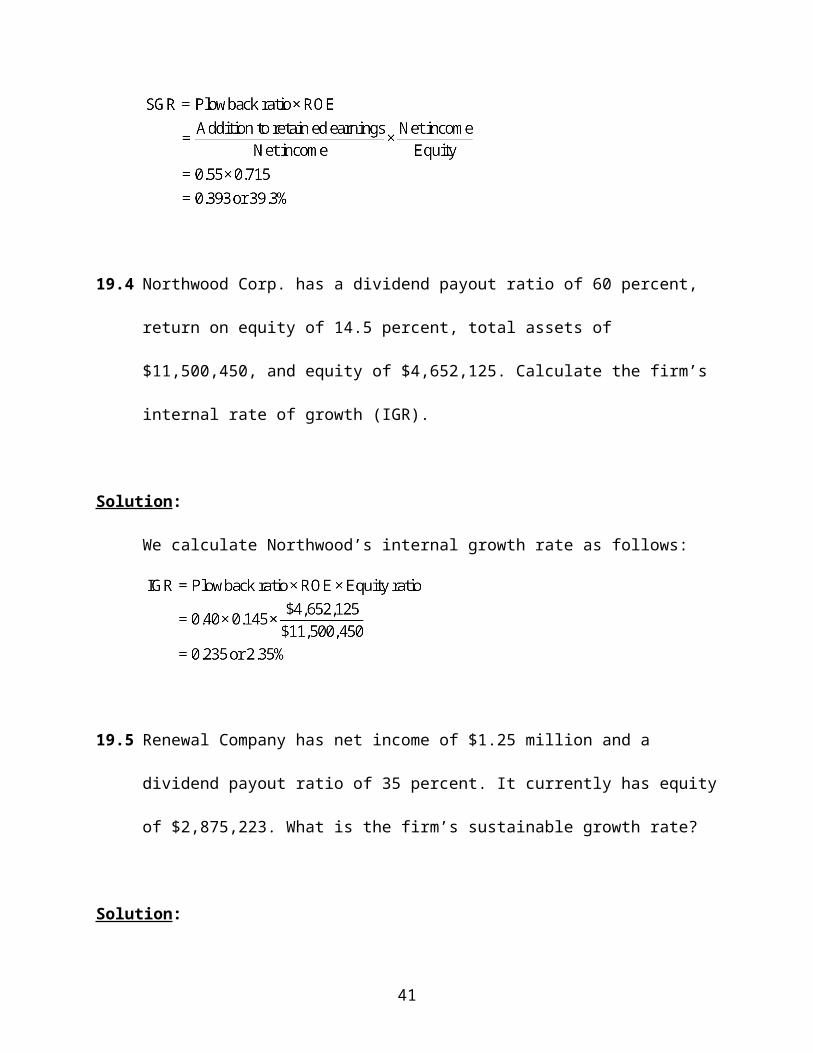

19.4 Northwood Corp. has a dividend payout ratio of 60 percent, return on equity of 14.5

percent, total assets of $11,500,450, and equity of $4,652,125. Calculate the firm’s

internal rate of growth (IGR).

Solution:

We calculate Northwood’s internal growth rate as follows:

19.5 Renewal Company has net income of $1.25 million and a dividend payout ratio of 35

percent. It currently has equity of $2,875,223. What is the firm’s sustainable growth rate?

Solution:

Renewal’s sustainable growth rate is:

29

VII. Critical Thinking Questions

19.1 What is financial planning? What are the four types of plans in financial planning?

Financial planning is the process by which a company’s management identifies the best

investment opportunities from a strategic perspective and determines how to finance

these investments. The end result is referred to as a financial plan. The four plans in

financial planning are the strategic plan, the investment plan or capital budget, the

financing plan, and the cash budget.

19.2 Why is the capital budget an important part of a firm’s financial planning?

The strategic plan of a firm determines the investments the company will make, and the

capital budget describes in detail all the firm’s planned spending on productive assets like

plant and equipment.

19.3 Why do financing and investment decisions have to be made concurrently?

Any investment decision has to be linked to a source of funds to pay for the assets, and

hence the investment decision and the financing decision have to be made concurrently.

19.4 Explain how sales can be used to develop pro forma financial statements.

30

The forecasted sales can be the basis for a financial planning model and is called the

percent of sales method. In such a framework, all financial statement accounts vary

directly with the level of sales.

19.5 Why are sales not always a good measure to forecast fixed assets?

When a percent of sales method is used to prepare pro forma financial statements, the

issue of whether or not a firm is operating at full capacity is ignored. Only if the firm is

operating at full capacity does fixed assets vary directly with sales. If a firm has excess

capacity, then sales can increase without a need to invest in additional fixed assets.

Two industries that may be considered to be capital intensive are the electric utilities

industry and the aluminum processing industry.

19.6 List all the accounts affected by the “plug” value. How does this value help managers?

The plug value relates to the amount of external funds needed given a level of sales.

Thus, all the various sources of funds for a firm like short-term and long-term debt,

common equity, and retained earnings are affected by the plug value.

19.7 Explain why the fixed asset account may or may not vary with sales.

Generally, companies invest in fixed assets in large discrete amounts rather than in small,

continuous amounts. Thus, each investment in fixed assets can accommodate a further

31

growth in sales without calling for additional investment in plant and equipment. Only

after each level of sales is accomplished at full production capacity would management

have to consider another increase in fixed assets.

19.8 How does the dividend payout ratio affect the amount of funds needed to fund growth?

Any change in the dividend payout ratio directly affects the amount of funds retained by

the company. The higher the firm’s ratio for a given level of net income, the lower the

amount of retained earnings, and hence the larger will be the amount of external debt

financing.

19.9 Define internal growth rate (IGR). Identify the characteristics of a high-growth firm with

no external funds needed.

Internal growth rate (IGR) is the maximum growth rate a firm can sustain without

needing any external financing. Such firms have a high enough retention ratio to fund

growth, generate a high level of net income for every dollar of equity, and use low

amounts of leverage or debt financing.

19.10 What is sustainable growth rate? Why is it important?

Sustainable growth rate (SGR) is the maximum growth rate a firm can sustain without

needing any external equity financing, holding leverage constant. Holding the firm to a

32

sustainable growth rate allows the firm to avoid costly equity issues, thus reducing the

dilution of earnings. Whenever firms grow faster than the SGR, the firm is going to need

external financing and may have to resort to debt financing, which increases the

company’s risk.

33

VIII. Questions and Problems

BASIC

19.1 Strategic plan: Explain the importance of the strategic plan.

Solution:

The strategic plan is the blueprint for a company’s management that determines the

firm’s long-term goals, identifies the strategies to achieve these goals, and determines the

company’s ability to be competitive. It drives all decision making within the firm and

covers all areas of a firm’s operations.

19.2 Capital budget: What are the various steps in preparing a capital budget?

Solution:

First, management identifies all strategically acceptable investment opportunities and

ranks them based on their contribution to shareholder wealth. Next, the senior

management reviews the capital budget plan and may revise it, if necessary, based on

need and the amount they can finance.

19.3 Financing plan: What are the elements of a financing plan?

Solution:

34

First, the financing plan identifies the amount of external financing needed and where the

funds could be obtained from. Second the plan identifies the firm’s target capital

structure. Last, the plan identifies the firm’s dividend policy, which determines the

amount of funds that need to be raised by the company.

19.4 Financial planning: Identify the steps in the financial planning process.

Solution:

o Establish a set of financial goals.

o Identify the investment opportunities and financing alternatives.

o Employ a financial planning model.

o Evaluate the investment and financing choices and decide on the ones that are the

best fit for the firm.

o Prepare contingency plans for future use.

19.5 Financial modeling: List the various elements of financial modeling.

Solution:

The important elements of financial modeling are the sales forecast, economic

assumptions, pro forma statements, investment decisions, financing requirements, and the

“plug factor” that determines the source of the external funds needed.

19.6 Payout ratio: Define the retention ratio and the dividend payout ratio.

35

Solution:

The dividend payout ratio tells us how much of a firm’s earnings are paid to the

shareholders as dividends. The retention ratio is complementary to the payout ratio and

tells us how much of the firm’s earnings are retained in the firm.

Thus, the retention ratio equals:

19.7 Addition to retained earnings: Northwood, Inc., has revenue of $455,316 and costs of

$316,487, and pays a tax rate of 31 percent. If the firm pays out 45 percent of its earnings

as dividends every year, what is the amount of retained earnings and what is the firm’s

retention ratio?

Solution:

Revenue = $455,316 Costs = $316,487

Tax rate = 31% Payout ratio = 45%

Retained earnings = 95,792 (1-0.45)

= $52,686

Retention ratio =

36

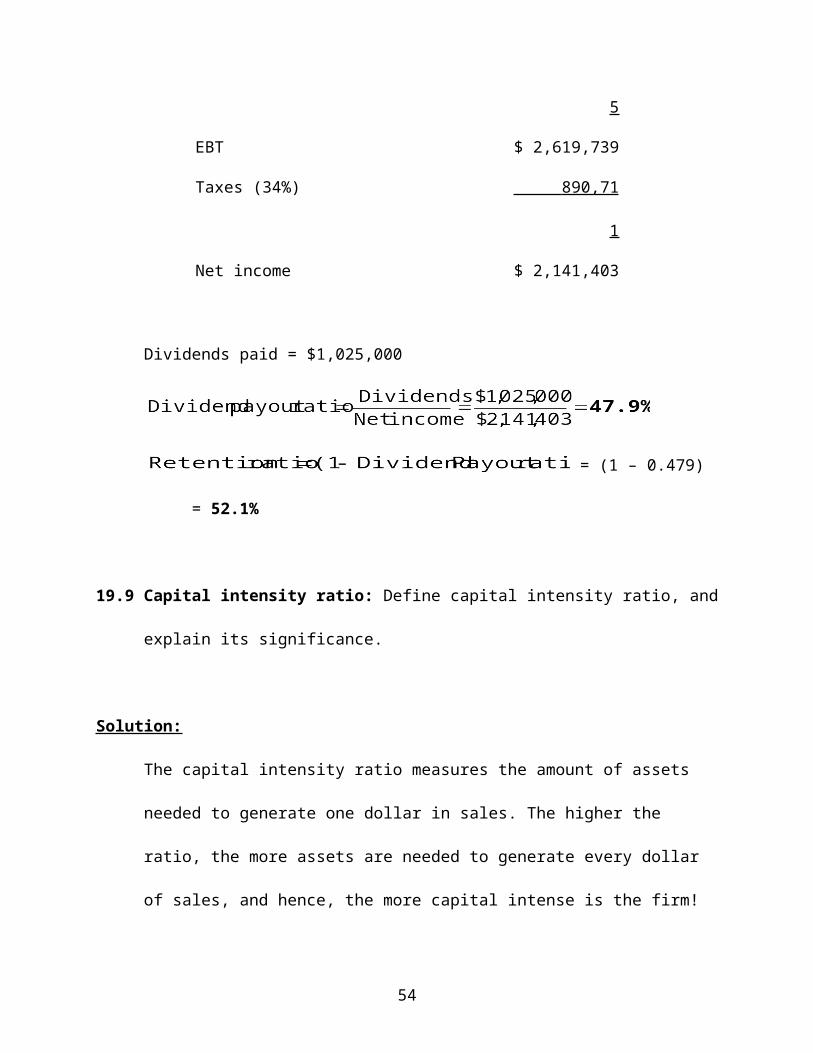

19.8 Payout and retention ratio: Goodwin Corp. has revenues of $12,112,659, costs of

$9,080,545, interest payments of $412,375, and a tax rate of 34 percent. It paid dividends

of $1,025,000 to its shareholders. Find the firm’s dividend payout ratio and retention

ratio.

Solution:

Goodwin Corp.

Revenues $12,112,659

Costs 9,080,545

EBIT $ 3,032,114

Interest 412,375

EBT $ 2,619,739

Taxes (34%) 890,711

Net income $ 2,141,403

Dividends paid = $1,025,000

= (1 – 0.479) = 52.1%

19.9 Capital intensity ratio: Define capital intensity ratio, and explain its significance.

Solution:

37

The capital intensity ratio measures the amount of assets needed to generate one dollar in

sales. The higher the ratio, the more assets are needed to generate every dollar of sales,

and hence, the more capital intense is the firm!

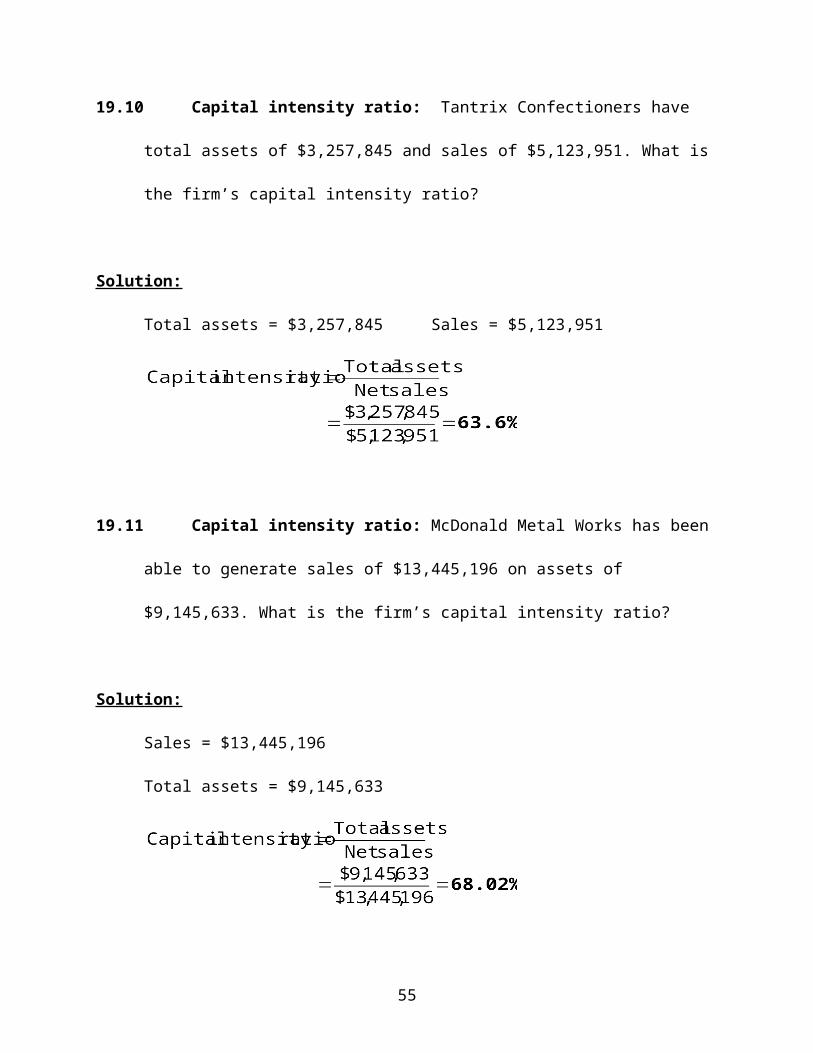

19.10 Capital intensity ratio: Tantrix Confectioners have total assets of $3,257,845 and sales

of $5,123,951. What is the firm’s capital intensity ratio?

Solution:

Total assets = $3,257,845 Sales = $5,123,951

19.11 Capital intensity ratio: McDonald Metal Works has been able to generate sales of

$13,445,196 on assets of $9,145,633. What is the firm’s capital intensity ratio?

Solution:

Sales = $13,445,196

Total assets = $9,145,633

38

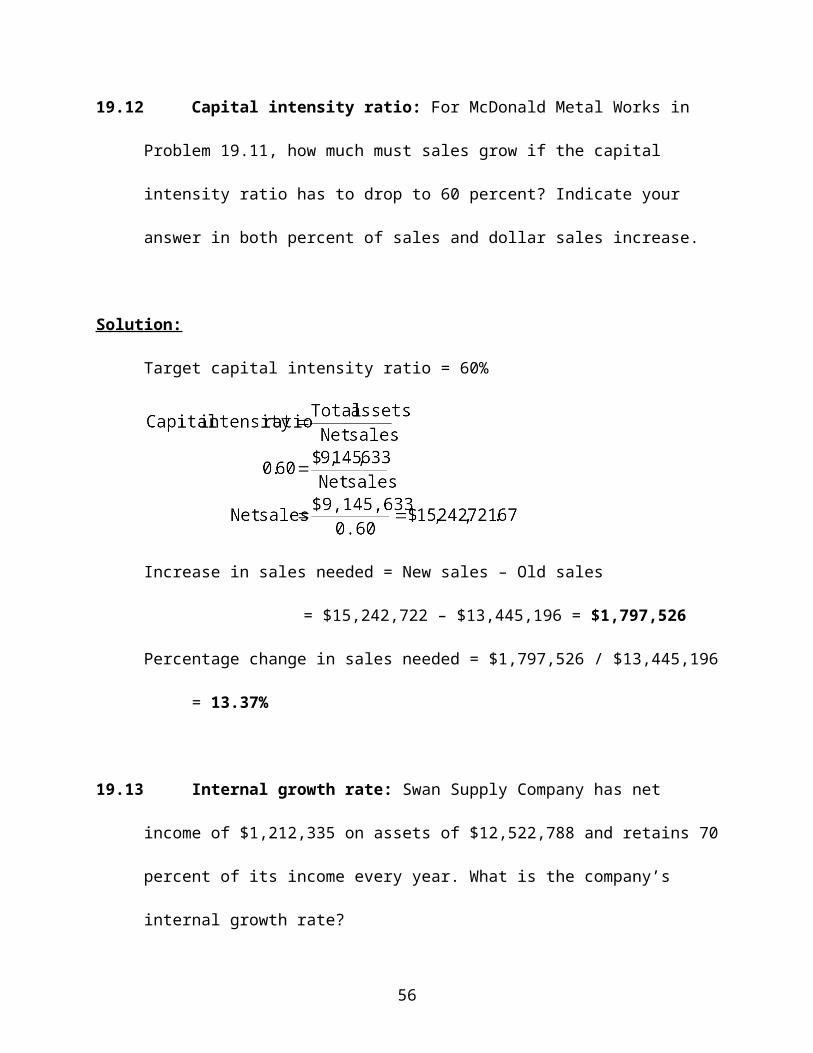

19.12 Capital intensity ratio: For McDonald Metal Works in Problem 19.11, how much must

sales grow if the capital intensity ratio has to drop to 60 percent? Indicate your answer in

both percent of sales and dollar sales increase.

Solution:

Target capital intensity ratio = 60%

Increase in sales needed = New sales – Old sales

= $15,242,722 – $13,445,196 = $1,797,526

Percentage change in sales needed = $1,797,526 / $13,445,196 = 13.37%

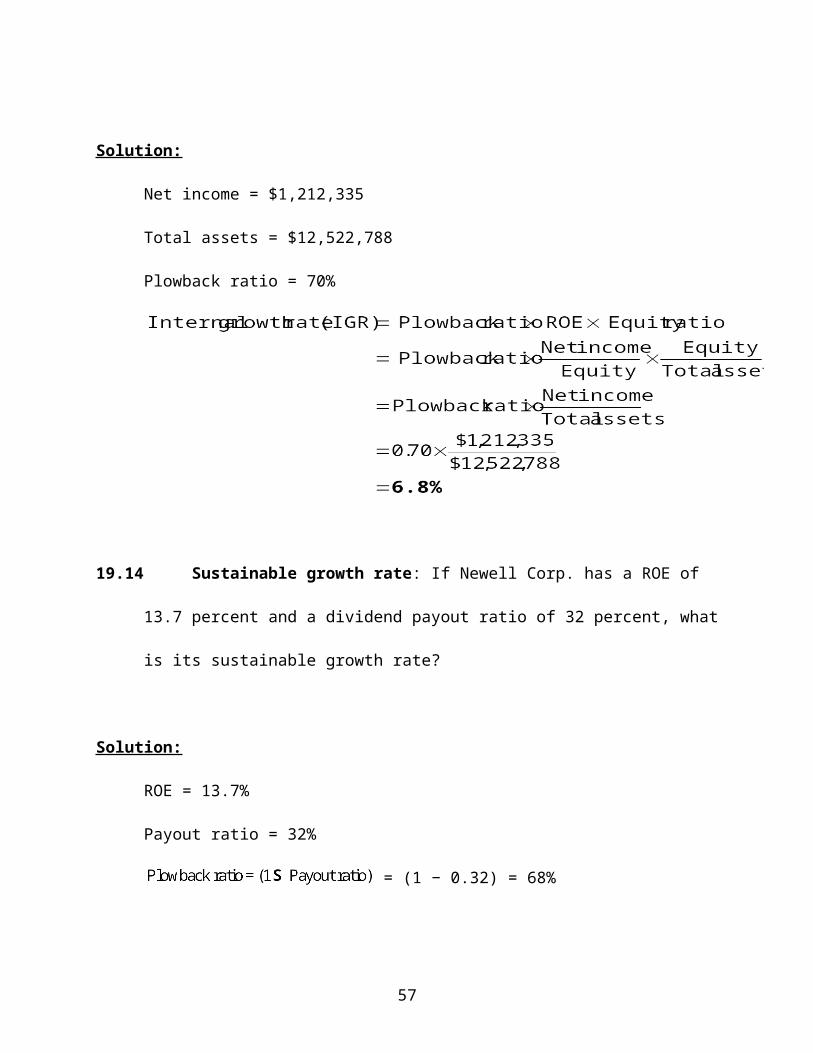

19.13 Internal growth rate: Swan Supply Company has net income of $1,212,335 on assets of

$12,522,788 and retains 70 percent of its income every year. What is the company’s

internal growth rate?

Solution:

Net income = $1,212,335

Total assets = $12,522,788

Plowback ratio = 70%

39

19.14 Sustainable growth rate: If Newell Corp. has a ROE of 13.7 percent and a dividend

payout ratio of 32 percent, what is its sustainable growth rate?

Solution:

ROE = 13.7%

Payout ratio = 32%

= (1 − 0.32) = 68%

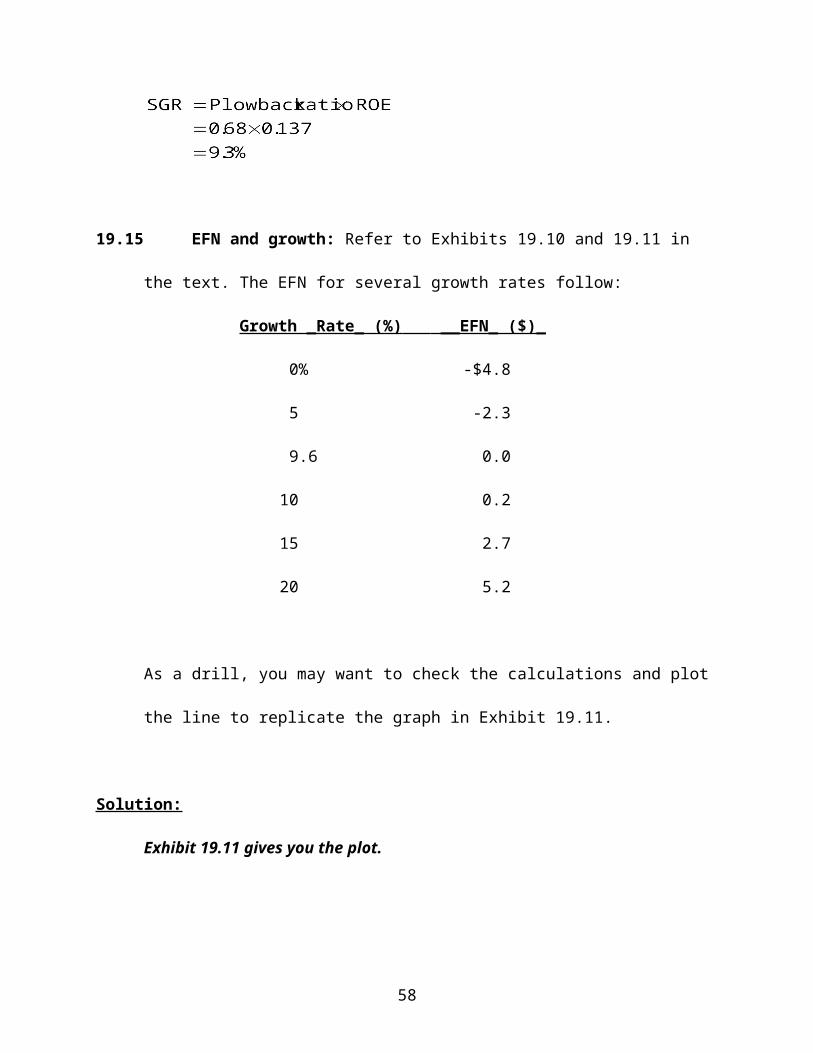

19.15 EFN and growth: Refer to Exhibits 19.10 and 19.11 in the text. The EFN for several

growth rates follow:

Growth _Rate_ (%) __EFN_ ($)_

0% -$4.8

5 -2.3

9.6 0.0

10 0.2

15 2.7

40

20 5.2

As a drill, you may want to check the calculations and plot the line to replicate the graph

in Exhibit 19.11.

Solution:

Exhibit 19.11 gives you the plot.

INTERMEDIATE

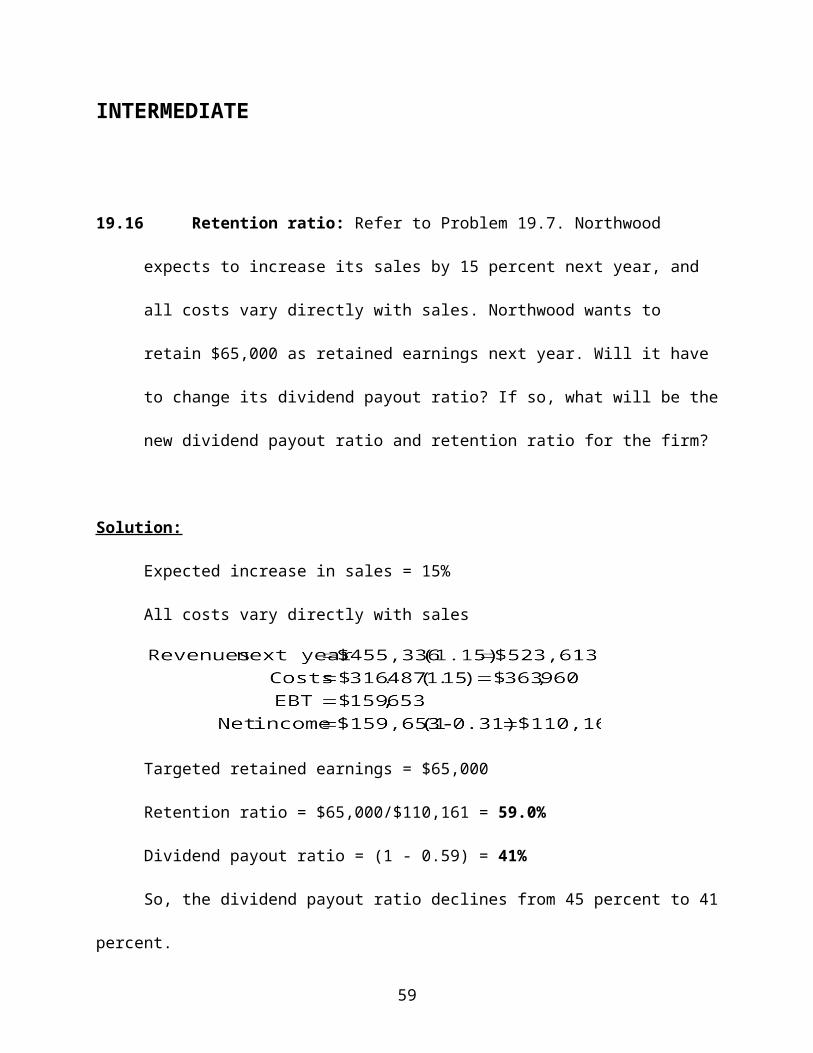

19.16 Retention ratio: Refer to Problem 19.7. Northwood expects to increase its sales by 15

percent next year, and all costs vary directly with sales. Northwood wants to retain

$65,000 as retained earnings next year. Will it have to change its dividend payout ratio?

If so, what will be the new dividend payout ratio and retention ratio for the firm?

Solution:

Expected increase in sales = 15%

All costs vary directly with sales

Targeted retained earnings = $65,000

Retention ratio = $65,000/$110,161 = 59.0%

41

Dividend payout ratio = (1 - 0.59) = 41%

So, the dividend payout ratio declines from 45 percent to 41 percent.

19.17 Capital intensity: Identify two industries (other than airlines) that are capital intensive.

Using online or other data sources, compute the capital-intensive ratio for the largest firm

in each of the chosen industries.

Solution:

Two industries that may be considered to be capital intensive are the electric utilities

industry and the aluminum processing industry.

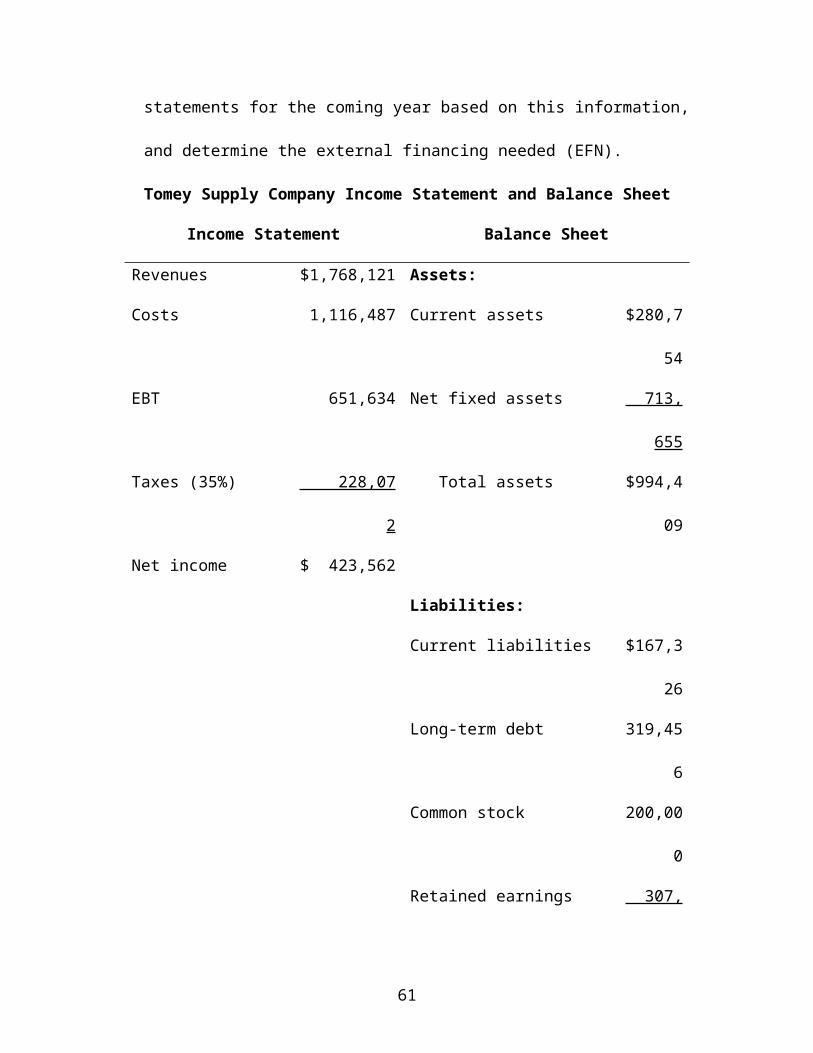

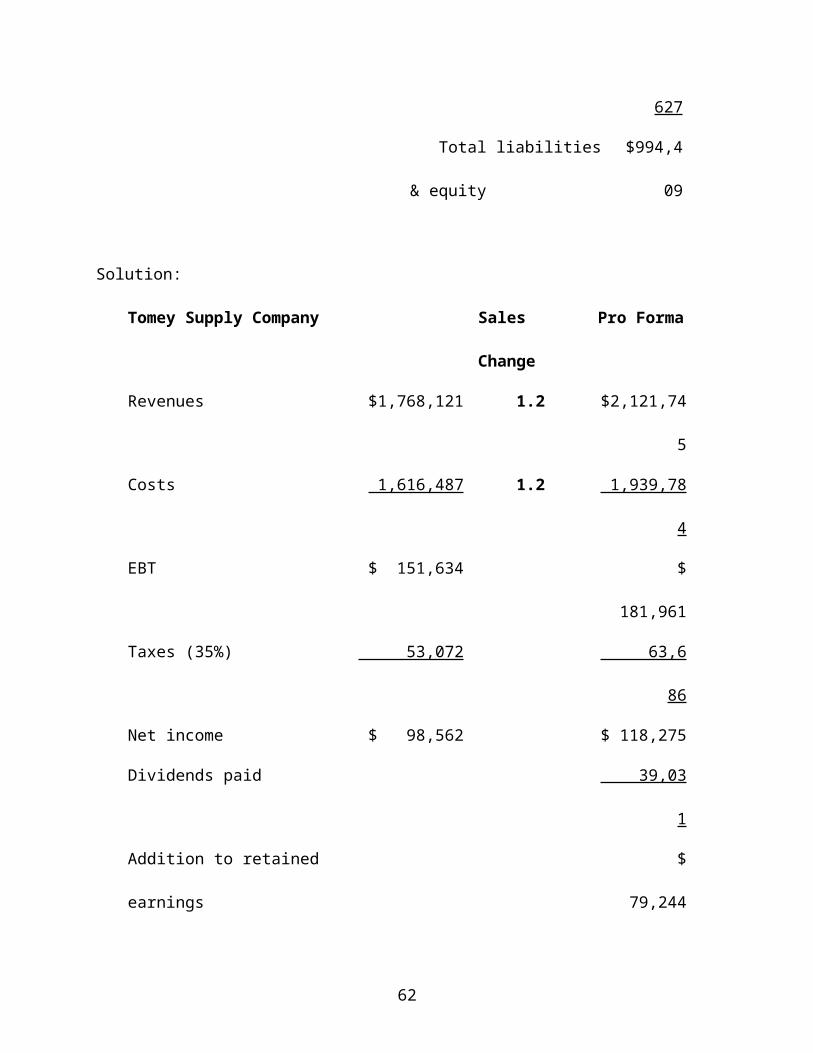

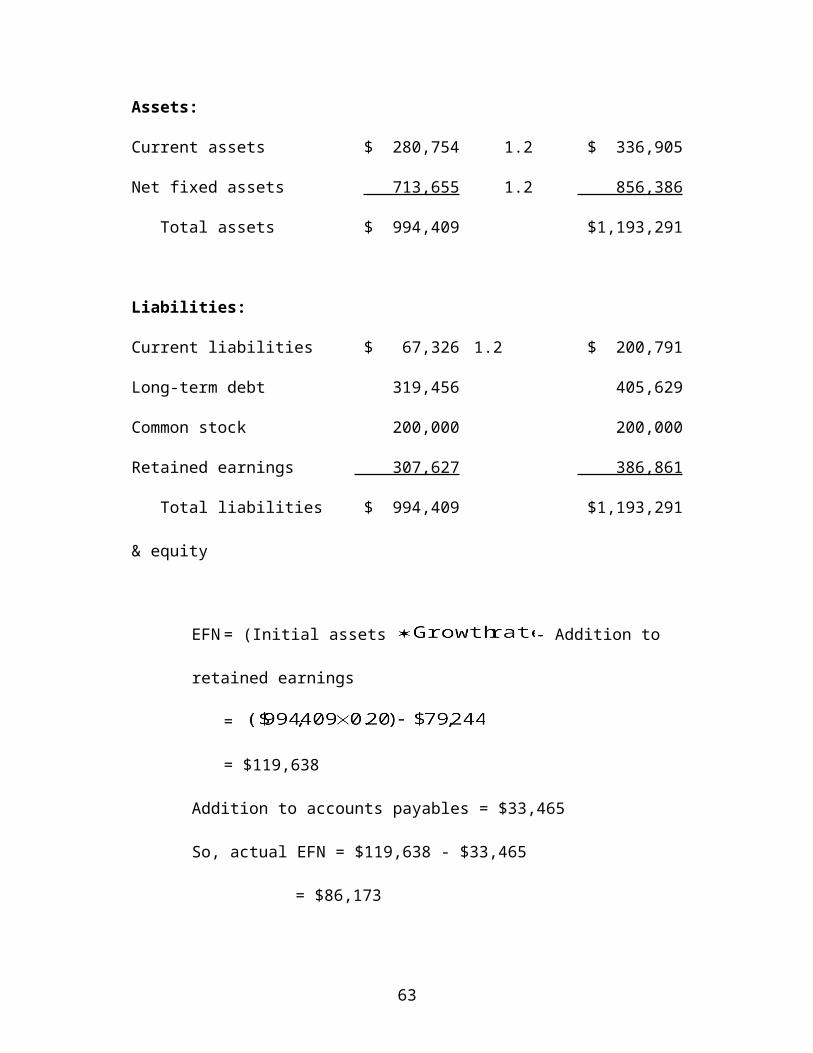

19.18 Percent of sales: Tomey Supply Company’s financial statement for the most recent fiscal

year is shown in the following table. The company projects that sales will increase by 20

percent next year. Assume that all costs and assets increase directly with sales. The

company has a constant 33 percent dividend payout ratio and has no plans to issue new

equity. Any financing needed will be in the form of long-term debt. Prepare pro forma

financial statements for the coming year based on this information, and determine the

external financing needed (EFN).

Tomey Supply Company Income Statement and Balance Sheet

Income Statement Balance Sheet

Revenues $1,768,121 Assets:

Costs 1,116,487 Current assets $280,754

EBT 651,634 Net fixed assets 713,655

42

Taxes (35%) 228,072 Total assets $994,409

Net income $ 423,562

Liabilities:

Current liabilities $167,326

Long-term debt 319,456

Common stock 200,000

Retained earnings 307,627

Total liabilities & equity $994,409

Solution:

Tomey Supply Company Sales Change Pro Forma

Revenues $1,768,121 1.2 $2,121,745

Costs 1,616,487 1.2 1,939,784

EBT $ 151,634 $ 181,961

Taxes (35%) 53,072 63,686

Net income $ 98,562 $ 118,275

Dividends paid 39,031

Addition to retained earnings $ 79,244

Assets:

Current assets $ 280,754 1.2 $ 336,905

Net fixed assets 713,655 1.2 856,386

Total assets $ 994,409 $1,193,291

43

Liabilities:

Current liabilities $ 67,326 1.2 $ 200,791

Long-term debt 319,456 405,629

Common stock 200,000 200,000

Retained earnings 307,627 386,861

Total liabilities & equity $ 994,409 $1,193,291

EFN= (Initial assets - Addition to retained earnings

=

= $119,638

Addition to accounts payables = $33,465

So, actual EFN = $119,638 - $33,465

= $86,173

19.19 Internal growth rate: Using the pro forma financial statements for Tomey Supply

Company developed in Problem 19.18, find the internal growth rate for the firm.

Solution:

IGR = Addition to retained earnings/Initial costs

= $79,244/$994,409

= 8%

44

19.20 Sustainable growth rate: Use the pro forma information for Tomey Supply Company

for next year: net income = $508,275; addition to retained earnings = $340,544; common

equity = $848,171; net sales = $2,121,745. Assume the company does not want its ratio

of long-term debt to equity to exceed its current long-term debt to equity ratio of 63

percent and it does not want to issue new equity. What level of sales growth can it

sustain? Calculate the new sales level.

Solution:

Current debt to equity ratio = 63%

Sustainable growth rate (SGR) = Plowback ratio

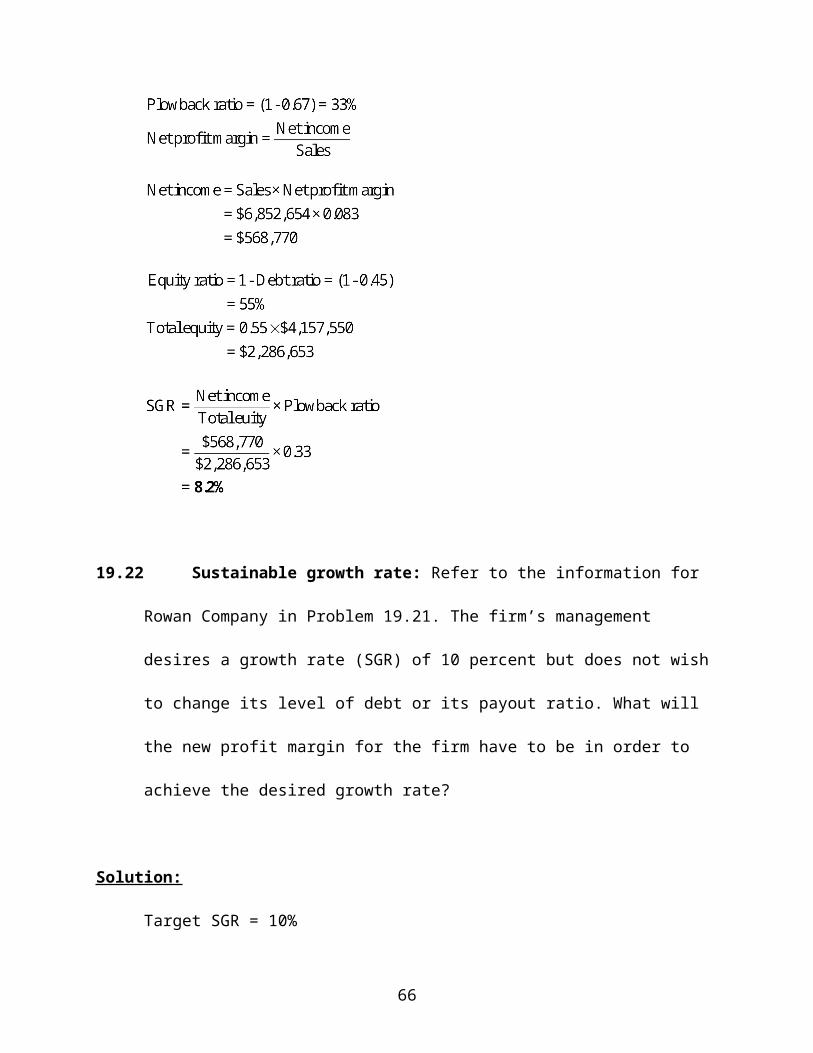

19.21 Sustainable growth rate: Rowan Company has a net profit margin of 8.3 percent, a debt

ratio of 45 percent, total assets of $4,157,550, and sales of $6,852,654. If the company

has a dividend payout ratio of 67 percent, what is the company’s sustainable growth rate?

Solution:

Net profit margin = 8.3%

Debt ratio = 45%

45

Total assets = $4,157,550

Sales = $6,852,654

Dividend payout ratio = 67%

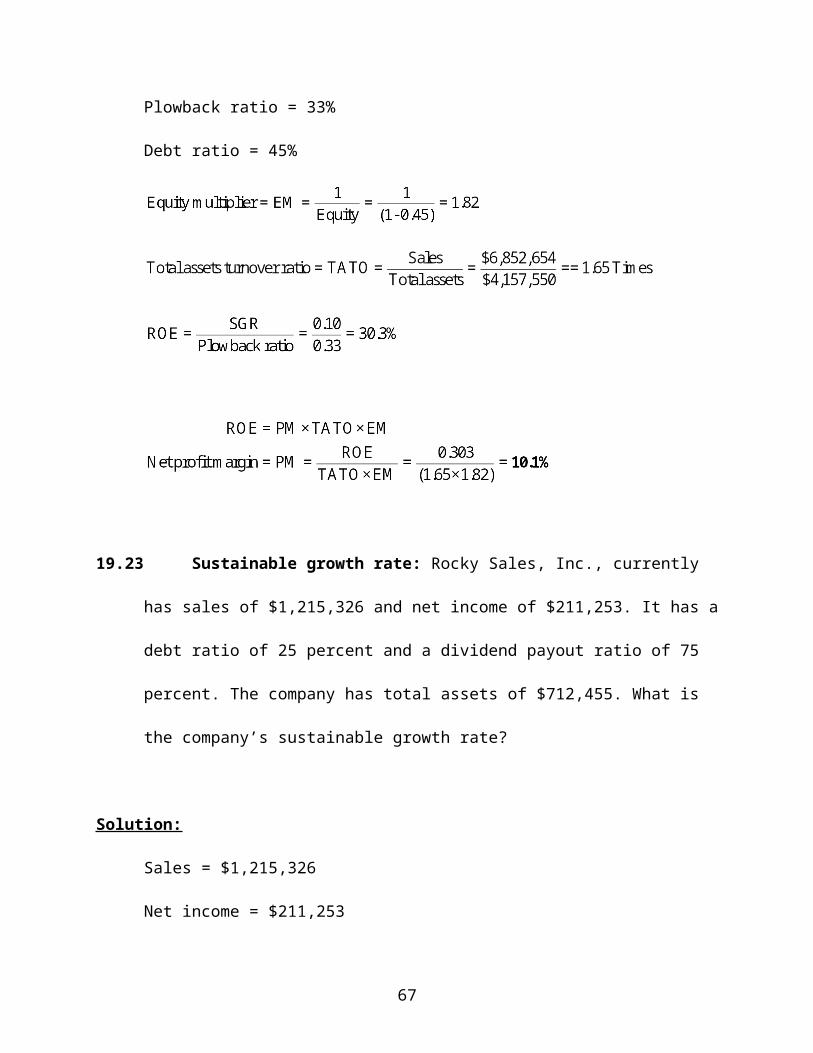

19.22 Sustainable growth rate: Refer to the information for Rowan Company in Problem

19.21. The firm’s management desires a growth rate (SGR) of 10 percent but does not

wish to change its level of debt or its payout ratio. What will the new profit margin for

the firm have to be in order to achieve the desired growth rate?

Solution:

Target SGR = 10%

Plowback ratio = 33%

46

Debt ratio = 45%

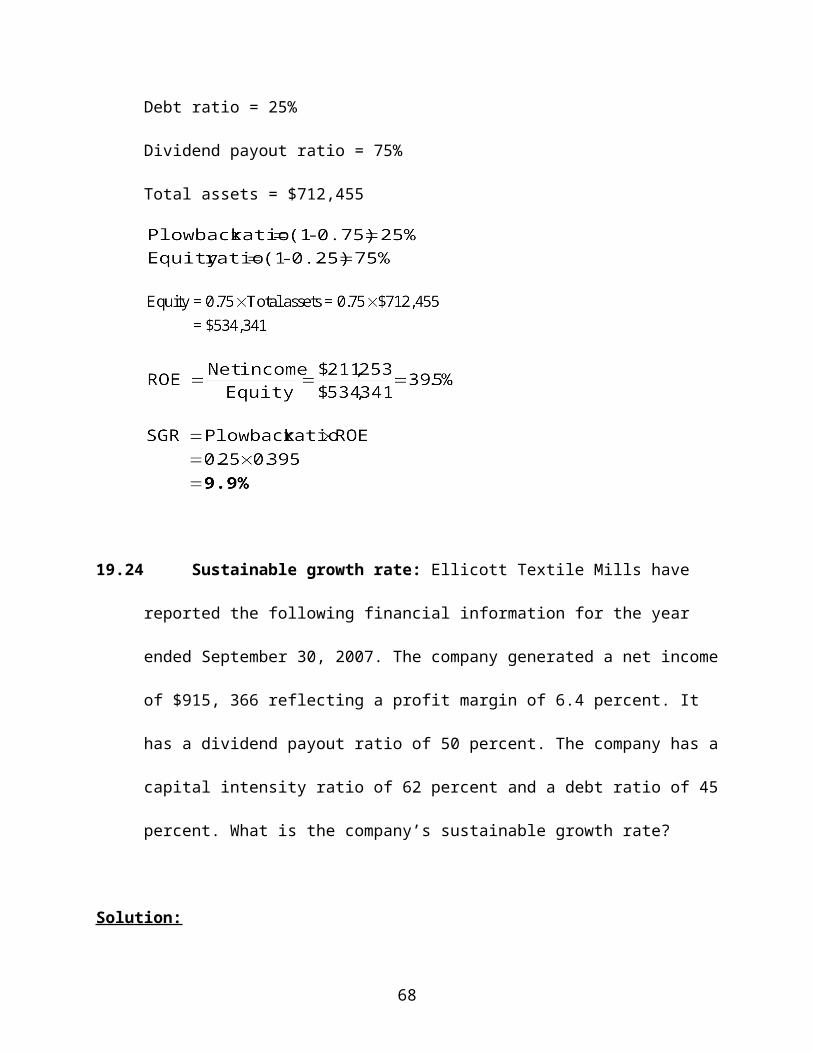

19.23 Sustainable growth rate: Rocky Sales, Inc., currently has sales of $1,215,326 and net

income of $211,253. It has a debt ratio of 25 percent and a dividend payout ratio of 75

percent. The company has total assets of $712,455. What is the company’s sustainable

growth rate?

Solution:

Sales = $1,215,326

Net income = $211,253

Debt ratio = 25%

Dividend payout ratio = 75%

Total assets = $712,455

47

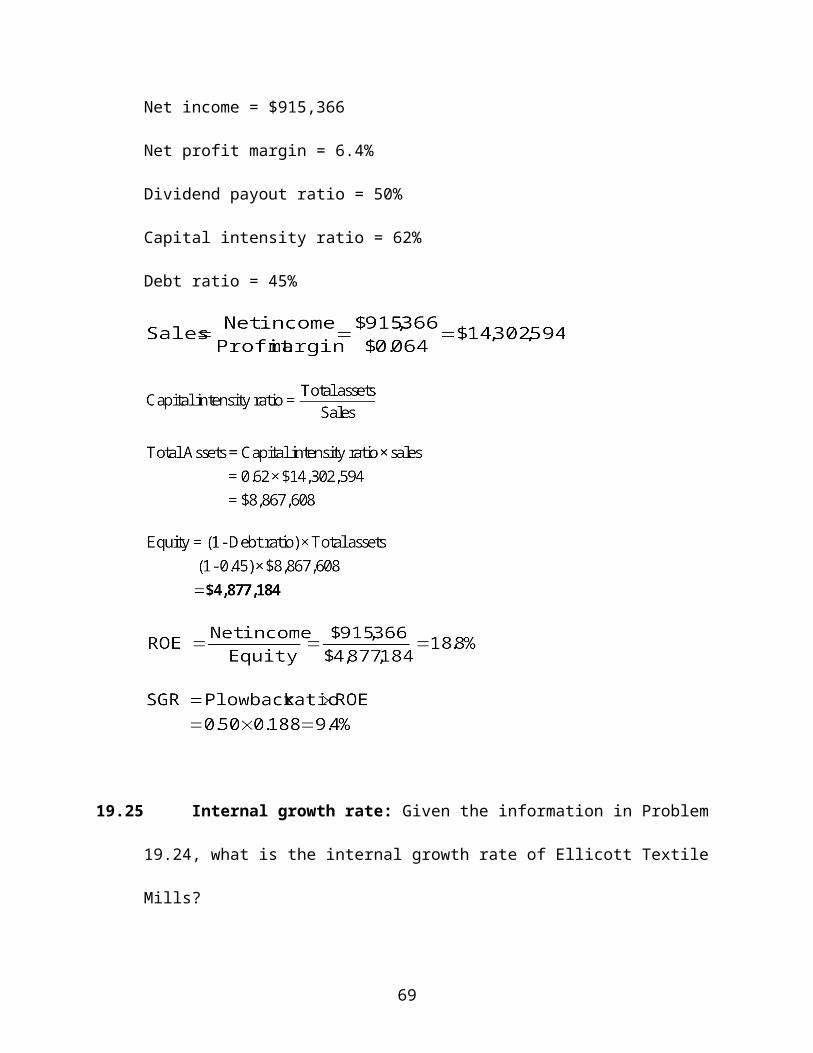

19.24 Sustainable growth rate: Ellicott Textile Mills have reported the following financial

information for the year ended September 30, 2007. The company generated a net income

of $915, 366 reflecting a profit margin of 6.4 percent. It has a dividend payout ratio of 50

percent. The company has a capital intensity ratio of 62 percent and a debt ratio of 45

percent. What is the company’s sustainable growth rate?

Solution:

Net income = $915,366

Net profit margin = 6.4%

Dividend payout ratio = 50%

Capital intensity ratio = 62%

Debt ratio = 45%

48

19.25 Internal growth rate: Given the information in Problem 19.24, what is the internal

growth rate of Ellicott Textile Mills?

Solution:

19.26 Internal growth rate: Fantasy Travel Company has a return on equity of 17.5 percent,

an equity ratio of 65 percent, and a dividend payout ratio of 75 percent. What is the

company’s internal growth rate?

Solution:

ROE = 17.5%

Equity ratio = 65%

Dividend payout ratio = 75%

Plowback ratio = 25%

49

19.27 EFN: Maryland Micro Brewers have for the year ended September 30, 2008, generated

revenues of $12,125,800 with a 72 percent capital intensity ratio. Its net income was

$873,058. With the introduction of half a dozen new specialty beers, the brewery expects

to grow its sales by 15 percent next year. Assume that all costs vary directly with sales

and the firm maintains its dividend payout ratio of 70 percent. What will be the external

financing (EFN) needed by this firm? If the company wanted to raise no more than

$750,000 externally and was not averse to adjusting its payout policy, what will be the

new dividend payout ratio?

Solution:

Total sales = $12,125,800

Capital intensity ratio = 72%

Net income = $873,058

Dividend payout ratio = 70%

50

Target EFN = $750,000

19.28 EFN: Ritchie Marble Company has total assets of $12,899,450, sales of $18,174,652, and

net income of $4,589,774. The company expects its sales to grow by 25 percent next

year. All assets and costs (including taxes) vary directly with sales, and the firm expects

to maintain its payout ratio of 65 percent. Calculate the external financing needed (EFN).

Solution:

Total assets = $12,899,450

Sales = $18,174,652

Net income = $4,589,774

Expected growth rate = 25%

Expected net income = $4,589,774 (1.25) = $5,737,217.50

Payout ratio = 65%

51

19.29 EFN: Norton Group, Inc., expects to add $1,213,777 to retained earnings and currently

has total assets of $23,159,852. If the company has the ability to borrow up to $1 million,

how much growth can the firm support if it is willing to borrow to its maximum capacity?

Solution:

Addition to retained earnings = $1,213,777

Total Assets = $23,159,852

EFN = $1,000,000

(AU: Initial cap needed, e.g., Addition to retained earnings)

19.30 Maximum sales growth: Rockville Consulting Group expects to add $271,898 to

retained earnings this year. The company has total assets of $3,425,693 and wishes to add

no new external funds for the coming year. If assets and costs vary directly with sales,

how much sales growth can the company support while retaining an EFN of zero? What

is the firm’s internal growth rate?

52

Solution:

Addition to retained earnings = $271,898

Total assets = $3,425,693

EFN = 0

With no external financing, the maximum possible growth equals the internal growth

rate.

ADVANCED

19.31 The financial statements for the year ended June 30, 2008, are given for Morgan

Construction Company. The firm’s revenues are projected to grow at a rate of 25 percent

next year, and all financial statement accounts will vary directly with sales. Based on that

projection, develop a pro forma balance sheet and an income statement for the 2007–2008

fiscal year.

Morgan Construction Company Balance Sheet and Income Statement

for Fiscal Year Ended June 30,2008

Balance Sheet

53

Assets: Liabilities and Stockholders’ Equity:

Cash $ 3,349,239 Accounts payables $ 9,041,679

Accounts receivables 5,830,754 Notes payables 4,857,496

Inventories 22,267,674

Total current assets $31,447,667 Total current liabilities $13,899,175

Net fixed assets 43,362,482 Long-term debt 29,731,406

Other assets 1,748,906 Common stock 19,987,500

Retained earnings 12,940,974

Total assets $76,559,055 Total liabilities and equity $76,559,055

Income Statement

Revenues $193,212,500

Costs 145,265,625

EBITDA $ 47,946,875

Depreciation 23,318,750

EBIT $ 24,628,125

Interest 11,935,869

EBT $ 12,692,256

Taxes (35%) 4,442,290

Net income $ 8,249,966

54

Solution:

Morgan Construction Company—Pro Forma Balance Sheet for Year Ended June 20, 2009

2008 2009 2008 2009

Cash $ 3,349,239 1.25 $ 4,186,548 Accounts payable $ 9,041,679 1.25 $11,302,098

Accounts receivables 5,830,754 1.25 7,288,442 Notes payable 4,857,496 1.25 6,071,869

Inventories 22,267,674 1.25 27,834,593

Total current assets $31,447,666 $39,309,583 Total current liabilities $13,899,174 $17,373,968

Net fixed assets 43,362,482 1.25 54,203,102 Long-term debt 29,371,406 1.25 37,164,258

Other assets 1,748,482 1.25 2,186,133 Common stock 19,987,500 1.25 24,984,375

Retained earnings 12,940,974 1.25 16,176,217

Total assets $76,559,054 $95,698,818 Total liabilities & equity $76,559,054 $95,698,818

Pro Forma Income Statement for Year Ended June 30, 2009

2008 2009

Revenues $193,212,500 1.25 $241,515,625

Costs 145,265,625 1.25 181,582,031

EBITDA $ 47,946,875 $ 59,933,594

55

Depreciation 23,318,750 1.25 29,148,438

EBIT $ 24,628,125 $ 30,785,156

Interest 11,935,869 1.25 14,919,836

EBT $ 12,692,256 $ 15,865,320

Taxes (35%) 4,442,290 1.25 5,552,862

Net income $ 8,249,967 $ 10,312,458

56

19.32 Use the financial information for Morgan Construction Company from Problem 19.31.

Assume now that equity accounts do not vary directly with sales but change when

retained earning change or new equity is issued. The company pays 75 percent of its

income as dividend every year. In addition, the company plans to increase production

capacity by expanding the current facility and acquiring additional equipment. This will

cost the firm $10 million. The firm has no plans to issue new equity this year. Prepare a

pro forma balance sheet using this information. Any funds that need to be raised (in

addition to changes in current liabilities) will be in the form of long-term debt. What is

the external financing needed in this case?

57

Solution:

Retention ratio = 25% Net income in 2007 = $10,312,458

Addition to retained earnings = $2,578,114.50 or $2,578,115

Morgan Construction Company—Pro Forma Balance Sheet for Year Ended June 20, 2009

2008 2009 2008 2009

Cash $ 3,349,239 1.25 $ 4,186,548 Accounts payable $ 9,041,679 1.25 $11,302,098

Accounts receivables 5,830,754 1.25 7,288,442 Notes payable 4,857,496 1.25 6,071,869

Inventories 22,267,674 1.25 27,834,593

Total current assets $31,447,666 $ 39,309,583 Total current liabilities $13,899,174 $ 17,373,968

Net fixed assets 43,362,482 1.25 54,203,102 Long-term debt 29,371,406 1.25 52,818,262

Addition to fixed assets 10,000,000 Common stock 19,987,500 1.25 19,987,500

Other assets 1,748,482 1.25 2,186,133 Retained earnings 12,940,974 1.25 12,940,974

Total assets $76,559,054 $105,698,818 Total liabilities & equity $76,559,054 $105,698,818

58

19.33 Using the information for Morgan Construction Company in the preceding problem, calculate the firm’s internal growth rate

and sustainable growth rate.

Solution:

19.34 Use the information for Morgan Construction Company from Problems 19.31 and 19.32. Assume that equity accounts do not

vary directly with sales but change when retained earnings change or new equity is issued. The company’s long-term-debt-to-

equity ratio is approximately 90 percent, and its equity-to-total-assets ratio is about 43 percent. The company wishes to

increase its equity-to-total-assets ratio to at least 50 percent. It is willing to reduce its payout ratio but will retain no more than

40 percent of its retained earnings. The company will raise any additional funds needed, including for expansion in new equity.

No new long-term debt will be issued. Prepare pro forma statements to reflect the new scenario.

a. What is the external financing needed (EFN) to accommodate the expected growth?

59

b. What is the firm’s internal growth rate (IGR)?

c. What is the firm’s sustainable growth rate (SGR)?

d. How much new equity will the firm have to issue?

e. What is the firm’s new equity ratio and debt to equity ratio?

Solution:

a. Retention ratio = 40%

b.

c.

d. Retained earnings in 2009 = $12,940,974 + $4,124,983 = $17,069,957

Total liabilities and equity = $105,698,818

Current liabilities = $17,373,968

Common equity = $105,698,818 – ($17,373,968+$29,731,406+$17,069,957)

= $41,523,486

60

Common equity in 2008 = $19,987,500

New common equity issued = $41,523,486 - $19,987,500 = $21,535,986

e.

EFN including expansion = $25,839,777

Morgan Construction Company—Pro Forma Balance Sheet for Year Ended June 20, 2009

2008 2009 2008 2009

Cash $ 3,349,239 1.25 $ 4,186,548 Accounts payable $ 9,041,679 1.25 $11,302,098

Accounts receivables 5,830,754 1.25 7,288,442 Notes payable 4,857,496 1.25 6,071,869

Inventories 22,267,674 1.25 27,834,593

Total current assets $31,447,666 $ 39,309,583 Total current liabilities $13,899,174 $ 17,373,968

Net fixed assets 43,362,482 1.25 54,203,102 Long-term debt 29,371,406 1.25 52,818,262

Addition to fixed assets 10,000,000 Common stock 19,987,500 1.25 19,987,500

Other assets 1,748,482 1.25 2,186,133 Retained earnings 12,940,974 1.25 12,940,974

Total assets $76,559,054 $105,698,818 Total liabilities & equity $76,559,054 $105,698,818

61

19.35 Munson Communications Company has just reported earnings for the year ended June 30, 2008. Given here are the firm’s

Income Statement and Balance Sheet. The company has a 55 percent dividend payout ratio for the last 10 years and does not

plan to make any changes in its policy. Based on internal forecasts, the company expects the demand for its products to grow at

a rate of 20 percent for the next year, and it has projected the sales growth for 2009 to be right at 20 percent. Assume that

equity accounts and long-term debt do not vary directly with sales but change when retained earning change or additional

capital is issued.

Munson Communications Company Balance Sheet and Income Statement

for Fiscal Year Ended June 30,2008

Balance Sheet

Assets: Liabilities and Stockholders’ Equity:

Cash $ 1,728,639 Accounts payables $ 4,666,673

Accounts receivables 3,009,421 Notes payables 2,507,094

Inventories 11,492,993

Total current assets $16,231,054 Total current liabilities $ 7,173,767

Net fixed assets 22,380,636 Long-term debt 13,345,242

Other assets 1,748,906 Common stock 10,165,235

62

Retained earnings 9,676,351

Total assets $40,360,595 Total liabilities and equity $40,360,595

Income Statement

Revenues $79,722,581

Costs 59,358,499

EBITDA $20,364,082

Depreciation 7,318,750

EBIT $13,045,332

Interest 3,658,477

EBT $ 9,386,855

Taxes (35%) 3,285,399

Net income $ 6,101,456

a. What is the firm’s internal growth rate (IGR)?

b. What is the firm’s sustainable growth rate (SGR)?

63

c. What is the external financing needed (EFN) to accommodate the expected growth?

d. Construct the firm’s 2008 pro forma financial statements under the assumption that all external financing will be done

with long-term debt.

Solution:

a. Retention ratio = 45.0%

Net income in 2008 = $ 6,101,456

Expected net income in 2008 = $6,101,456 (1.20) = $7,321,747

Addition to retained earnings = $ 3,294,786

ROE = 30.8%

Growth rate = 20%

b.

c.

d.

64

Munson Communications Company—Pro Forma Balance Sheet for Year Ended June 20, 2009

2008 2009 2008 2009

Cash $ 1,728,639 1.20 $ 2,074,367 Accounts payable 4,666,673 1.20 $ 5,600,007

Accounts receivables 3,009,421 1.20 3,611,305 Notes payable 2,507,094 1.20 3,008,513

Inventories 11,492,993 1.20 13,791,592

Total current assets $16,231,054 $19,477,264 Total current liabilities $ 7,173,767 $ 8,608,521

Net fixed assets 22,380,635 1.20 26,856,763 Long-term debt 13,345,242 1.20 17,236,953

Other assets 1,748,906 1.20 2,098,688 Common stock 10,165,235 1.20 10,165,235

Retained earnings 9,676,351 1.0 12,422,006

Total assets $40,360,595 $48,432,714 Total liabilities & equity $40,360,595 $48,432,714

Pro Forma Income Statement for Year Ended June 30, 2009

2008 2009

Revenues $79,722,581 1.20 $95,667,097

Costs 59,358,499 1.20 71,230,199

EBITDA $20,364,082 $24,436,898

Depreciation 7,318,750 1.20 8,782,500

65

EBIT $13,045,332 $15,654,398

Interest 3,658,477 1.20 4,390,172

EBT $ 9,386,855 $11,264,226

Taxes (35%) 3,285,399 1.20 3,942,479

Net income $ 6,101,456 $ 7,321,747

66

Sample Test Problems

19.1 Mercury Corp. has produced revenues of $2,512,654, costs of $1,080,227, interest

payments of $132,375 and a tax rate of 34 percent. It paid dividends of $525,000 to its

shareholders. Find the firm’s dividend payout ratio and retention ratio.

Solution:

Net income = ($2,512,654 – $1,080,227 – $132,375)(1 – 0.34) = $858,034.32

Retention ratio= 1 – Dividend payout ratio = (1 – 0.6119) = 0.3881

= 38.81%

19.2 Assume that Rex Corp. was operating at a capital intensity ratio of 63.5 percent and is

able to generate net sales of $3,123,443. What is the firm’s level of assets?

Solution:

Net sales = $3,123,443

67

19.3 Centennial Beverages currently has sales of $1,415,326 and net income of $411,253. It

has a debt ratio of 25 percent and a dividend payout ratio of 70 percent. The company has

total assets of $1,850,325. What is the company’s sustainable growth rate?

Solution:

Payout ratio = 70%

= (1 - 0.70) = 30%

19.4 Given the information in Problem 19.3, what is the internal growth rate of Centennial

Beverages?

Solution:

19.5 Mirabelle Company has total assets of $3,267,450, sales of $5,174,652, and net income

of $1,789,774. The company expects its sales to grow by 20 percent next year. All assets

68

and costs (including taxes) vary directly with sales, and the firm expects to maintain its

payout ratio of 75 percent. Calculate the external financing needed (EFN).

Solution:

Total assets = $3,267,450

Sales = $5,174,652

Net income = $1,789,774

Expected growth rate = 20%

Expected net income = $1,789,774 (1.20) = $2,147,729

Payout ratio = 75%

69

Related Documents