CHAPTER 17 GOVERNMENTAL ENTITIES: INTRODUCTION AND GENERAL FUND ACCOUNTING ANSWERS TO QUESTIONS Q17-1 A fund is an independent fiscal and accounting entity with a self- balancing set of accounts recording cash and/or other resources together with all related liabilities, obligations, reserves, and equities which are segregated for the purpose of carrying on specific activities or attaining certain objectives in accordance with special regulations, restrictions, or limitations. A fund may receive resources from a variety of sources, including collection of taxes on property, income, or commercial sales; receipt of grants, fines, or licenses; and collection of service charges. Q17-2 The eleven funds generally used by local and state governments are: Governmental a. General fund b. Special revenue fund c. Capital projects fund d. Debt service fund e. Permanent fund Proprietary f. Internal service fund g. Enterprise fund Fiduciary h. Pension trust fund i. Investment trust fund j. Private-purpose trust fund k. Agency funds The purpose of each fund is individually discussed below: a. General fund: All financial resources except those required to be accounted for in another fund are accounted for in the general fund. b. Special revenue fund: The proceeds of specific revenue sources that are legally restricted for specified purposes are accounted for in the special revenue fund. c. Capital projects fund: Financial resources to be used for the acquisition or construction of major capital projects that will benefit a large population are accounted for in the capital projects fund. McGraw- Hill/Irwin © The McGraw-Hill Companies, Inc., 2002 - 871 -

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER 17

GOVERNMENTAL ENTITIES: INTRODUCTION AND GENERAL FUND ACCOUNTING

ANSWERS TO QUESTIONS

Q17-1 A fund is an independent fiscal and accounting entity with a self-balancing set of accounts recording cash and/or other resources together with all related liabilities, obligations, reserves, and equities which are segregated for the purpose of carrying on specific activities or attaining certain objectives in accordance with special regulations, restrictions, or limitations. A fund may receive resources from a variety of sources, including collection of taxes on property, income, or commercial sales; receipt of grants, fines, or licenses; and collection of service charges.

Q17-2 The eleven funds generally used by local and state governments are:

Governmental a. General fund b. Special revenue fund c. Capital projects fund d. Debt service fund e. Permanent fund

Proprietary f. Internal service fund g. Enterprise fund

Fiduciary h. Pension trust fund i. Investment trust fund j. Private-purpose trust fund k. Agency funds

The purpose of each fund is individually discussed below:

a. General fund: All financial resources except those required to be accounted for in another fund are accounted for in the general fund.

b. Special revenue fund: The proceeds of specific revenue sources that are legally restricted for specified purposes are accounted for in the special revenue fund.

c. Capital projects fund: Financial resources to be used for the acquisition or construction of major capital projects that will benefit a large population are accounted for in the capital projects fund.

d. Debt service fund: The accumulation of resources for, and the payment of, general long-term debt principal and interest are accounted for in the debt service fund.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 871 -

e. Permanent fund: Accounts for resources for which the principal must be maintained, but for which the earnings may be used in support of governmental programs.

f. Internal service fund: The financing of goods or services provided by one department or agency to other departments or agencies of the governmental unit, or to other governmental units, are accounted for in internal service funds.

g. Enterprise fund: Operations of governmental units that charge for services provided to the general public are accounted for in the enterprise funds.

h. Pension trust fund: Resources held by a governmental unit in a trustee capacity for the members and beneficiaries of pension plans, postemployment plans, or other employee benefit plans.

i. Investment trust funds: Accounts for the external portion of investment pools of governing units.

j. Private-purpose trust fund: Accounts for trust arrangements under which both principal and interest may be used to benefit specific individuals, private organizations, or other governmental units. Note that these resources have specific purposes as stated by the donor or grantor, and are not available for general governmental programs.

k. Agency funds: Assets held by a governmental unit in an agency capacity for employees or other individuals are accounted for in agency funds.

Q17-3 The modified accrual basis includes some aspects of accrual accounting and some aspects of cash-basis accounting. Under the modified accrual basis, the emphasis is on reporting how well the government performed by focusing on when the revenue and expenditures are recognized in the accounts and reported in the financial statements. The emphasis is not on how much was earned nor on the amount of expenses.

Q17-4 The modified accrual basis is used for funds for which expendability is the concern because the governing entity is interested in the determination of the resources still remaining to be expended to carry out the objectives of the fund.

Q17-5 Property taxes are recognized as revenue in the general fund when the taxes are levied, provided they apply to and are collectible within the current fiscal period, or within a short period (< 60 days) after the end of the fiscal period.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 872 -

Q17-6 GASB 33 states that taxpayer-assessed income and sales taxes should be accrued in the general fund when they become both measurable and available to finance expenditures of the fiscal period. Sales taxes held by other governmental units should be recognized if the taxes are both measurable and available for expenditure. Measurability in this case is based on an estimate of the sales taxes to be received, and availability is based on the ability of the governing entity that will receive the future distribution to obtain current resources through credit by using future sales tax receipts as collateral for the loan.

Q17-7 Budgetary accounting is the entering of the budgeted revenue, appropriations, and net increase or decrease in fund balance into the formal accounting records as a formal accounting control mechanism. Expected revenue is accounted for as estimated revenue, an anticipatory asset account. The governmental unit anticipates receiving resources from the revenue sources listed in the budget. Anticipated expenditures are accounted for as appropriations, an anticipatory liability account. The governmental unit anticipates incurring liabilities for the budgeted amount. Both the expected revenue and the appropriations accounts are closed at the end of the fiscal period.

Q17-8 All expenditures are not encumbered. Payroll costs and other costs for goods received from within the governmental entity are not encumbered because these are normal and recurring costs.

Q17-9 Some governmental units do not report small amounts of inventories of supplies in their balance sheets because the amount of inventory is not material.

Q17-10 Under the lapsing method the Reserve for Encumbrances account is shown as a reservation of the fund balance on the fiscal year-end balance sheet. The encumbrance account is a nominal account that is closed at the end of the fiscal period. The net effect is to close out the remaining encumbrances against the unreserved fund balance. Alternatively, the GASB does allow for just footnote disclosure of the lapsing open orders at year-end that are expected to be honored in the next fiscal period.

Under the nonlapsing method the expenditure authority from prior periods is carried over as nonlapsing encumbrances. The budget for the next fiscal period does not show these carryovers and is more realistic for situations in which orders placed with outside vendors cannot easily be canceled. The encumbrance account is still closed at the end of the period and the reserve for encumbrances is canceled.

When accounting for the actual expenditure in the subsequent year, the lapsing method requires the new governing board to decide if it will honor the outstanding encumbrances for the previous year by including them in the current budgeted appropriations. If the governing board accepts the obligation to honor their outstanding purchase order by including the expenditure within its budget, the entries made at the end of the previous year are reversed to re-establish the expenditure authority and the normal encumbrance/expenditure entries are made. In the event the new governing board decides not to honor the outstanding encumbrances, the reserve for

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 873 -

outstanding encumbrances is eliminated and the order for the goods is canceled with the external vendor.

When accounting for the actual expenditure in the subsequent year, the nonlapsing method separates expenditures made from spending authority carried over from prior periods. This is done in a reclassification entry made on the first day of the next fiscal period, which dates the reserve for encumbrances. There is no entry to reverse the encumbrance because the encumbrance account was closed in the previous period and no longer exists for this expenditure.

Q17-11 The expenditure for inventories is recognized in the period the supplies are acquired under the purchase method. Under the consumption method, the expenditure for inventories is recognized for only the amount of inventory used in the period.

Q17-12 Interfund services provided and used are interfund activities that would be treated as revenues or expenditures if they were made with parties external to the governmental entity. An example would be if the general fund purchased supplies from the internal service

Interfund transfers out or in are transfers of resources between funds. An example would be a transfer of resources from the general fund (an interfund transfer out) to the capital projects fund (a transfer in) to assist in the construction costs of a new municipal building.

Q17-13 An interfund transfer is reported as "Other Financing Sources or Uses" in the general fund's statement of revenue, expenditures, and changes in fund balance.

Q17-14 The loan of $2,000 from the general fund to the enterprise fund is reported on the financial statements of the general fund on the balance sheet as a receivable. The loan is not shown on the fund's statement of revenue, expenditures, and changes in fund balance.

Q17-15 Governmental accounting places many controls over expenditures, and much of the financial reporting focuses on the various aspects of an expenditure. An expenditure can be made for a function of the governmental entity or an activity within a function. Expenditures for an activity can be classified by object, which is the type of expenditure. The extensive detail required to account for and cross reference an expenditure to ensure it is properly classified at all levels requires a very comprehensive accounting system.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 874 -

SOLUTIONS TO CASES

C17-1 Budget Theory

a. A governmental accounting system must make it possible to:

1. Present fairly and with full disclosure, in conformity with generally accepted accounting principles, the financial position and results of financial operations of the funds and account groups of the governmental unit.

2. Determine and demonstrate compliance with finance-related legal and contractual provisions.

Because the legislative body enacts the budget into law, the budget is recorded in the accounts of a governmental unit. This enables a governmental unit to show legal compliance with the budget by providing an accounting system that measures actual expenditures and obligations against amounts appropriated, and actual revenue against estimated revenue. Appropriations enacted into law constitute maximum expenditure authorizations during the fiscal year, and they cannot legally be exceeded unless subsequently amended by the legislative body.

b. As the new fiscal year begins, the budget, already enacted into law by the legislative body, is recorded. Budgetary accounts are set up to record the estimated revenue and appropriations in the fund accounts by debiting estimated revenue and crediting appropriations. If there is a difference between estimated revenue and appropriations, the excess or deficit is credited or debited, respectively, to fund balance. In addition, subsidiary ledger accounts are maintained for estimated revenue by source and for appropriation/expenditure items.

At the end of the fiscal year, the estimated revenue balance and the appropriations balance are closed out to fund balance.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 875 -

C17-2 Municipal versus Financial Accounting

a. The most significant difference in purpose between municipal accounting and commercial accounting is that commercial enterprises are operated for profit, which places much emphasis on the proper determination of periodic earnings. Governmental units are primarily concerned with providing services to their citizens at minimum cost and reporting on the stewardship of public officials with respect to public funds, which places much emphasis on budgetary controls. However, some municipal units perform commercial services that are generally secondary to their tax-financed primary services.

Another difference in accounting purpose is that municipal accounting operations are controlled by legal provisions in constitutions, charters, and regulations having the force and effect of law. Because of these legal provisions and the diversity of its governmental operations, a municipality cannot use a single, unified set of accounts for recording and summarizing all financial transactions. If there is a conflict between legal provisions and generally accepted accounting principles applicable to governmental units, legal provisions should take precedence to the extent that the accounting system must enable the ready disclosure of compliance. However, for financial reporting purposes, generally accepted accounting principles must take precedence. Commercial enterprises usually are not controlled by charters that are restrictive; therefore, their accounting systems are designed differently.

Legislative action may limit the use of certain tax revenue for expenditure on particular programs, the methods of tax collection, or the rates of tax assessment. Such provisions must be reflected in the accounting system and be appropriately disclosed in the municipality's financial statements as a report on the stewardship of public officials with respect to public funds.

In governmental accounting all required accounts are organized on the basis of funds, each of which is independent of the other. Each fund must be so accounted for that the identity of its resources, obligations, revenue, expenditures, and fund balance is continually maintained. These purposes are accomplished by providing a complete self-balancing set of accounts for each fund.

The basis of accounting for the reporting on governmental units is often different from that used by commercial enterprises. For example, the accrual basis of accounting is recommended for all funds except the general, special revenue, debt service, capital projects, agency, and expendable trust funds. These funds should be accounted for by the modified accrual basis. The modified accrual basis is recommended for these funds because some of their revenue sources are difficult to measure in advance and frequently become available only a short time before cash receipt.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 876 -

C17-2 (continued)

Generally, fair presentation of financial position and results of operations in conformity with generally accepted accounting principles requires that the financial statements of expendable funds (those that use the modified accrual basis) include a balance sheet and a statement of revenue, expenditures, and changes in fund balance. In contrast, however, a commercial enterprise would usually prepare a statement of financial position, an earnings statement, a statement of retained earnings, and a statement of cash flows. The statement of revenue and expenditures of the general fund and certain special revenue funds should include a comparison with a formal budget in order to conform with generally accepted accounting principles; there is no such requirement for a commercial enterprise.

b. Inventories are often ignored in governmental accounting because of an emphasis on budgeting revenue against outlays without looking behind the outlays to determine the extent to which they represent actual usage or consumption. Put another way, there is an emphasis on the cash or fiscal aspects rather than the operational aspects. This is easy to understand when one considers that general-fund expenditures for firemen's salaries and for the purchase of a new fire truck are accounted for in the same way.

However, inventories are not wholly ignored in governmental accounting. In those funds in which accounting parallels commercial accounting practice, such as enterprise funds, inventories are taken into consideration. Similarly, in an internal service fund concerned with rendering service involving the consumption of supplies or the delivery of stores to other funds and activities, the inventories of supplies or stores are taken into consideration in computing billings to departments serviced.

Inventories can and should be taken into consideration when preparing budgets. A fund, such as a general fund, having departments that possess large inventories at year-end obviously has need for smaller appropriations for the coming year than it would if those departments had zero inventories.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 877 -

SOLUTIONS TO EXERCISES

E17-1 Multiple-Choice Questions on the General Fund [AICPA Adapted]

1. b

2. a

3. b

4. b

5. c

6. b

E17-2 Matching for General Fund Transactions [AICPA Adapted]

1. K

2. C

3. B

4. B

5. K

6. A

7. H

8. I

9. M 10. F 11. B

12. B

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 878 -

E17-3 Multiple-Choice Questions on Budgets, Expenditures, and Revenue [AICPA Adapted] 1. c

2. d

3. c

4. a

5. b

6. c

7. d

8. b

9. c

10. d

E17-4 Multiple-Choice Questions on the General Fund

1. b

2. d

3. c The balance in the ENCUMBRANCES CONTROL and the FUND BALANCE RESERVED FOR ENCUMBRANCES accounts is the same. Therefore, an excess of one account over the other indicates a recording error.

4. c The following entry is made when a purchase order is approved:

ENCUMBRANCES CONTROL BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES

5. b The 60-day rule for property tax revenues requires that property taxes collected within 60 days after the end of the year are revenues of the preceding fiscal year. The entry to record the tax levy would be:

Property Taxes Receivable - Current 700,000 Allowance for Uncollectible Taxes 10,000 Revenue - Property Taxes 600,000 Deferred Revenue (reported as a liability on the general fund balance sheet) 90,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 879 -

E17-4 (continued)

6. a Upon receipt of the order, Oak would record the following entries:

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 5,000 ENCUMBRANCES CONTROL 5,000

Expenditures Control 4,950 Vouchers Payable 4,950

7. a Johnson would record the following entry:

ESTIMATED REVENUES CONTROL 9,000,000 ESTIMATED OTHER FINANCING SOURCE - TRANSFER IN (Internal Service) 1,000,000 ESTIMATED OTHER FINANCING SOURCE - TRANSFER IN (Debt Service) 500,000 APPROPRIATIONS CONTROL XXXXXX BUDGETARY FUND BALANCE UNRESERVED XXX

8. c

9. a

10. b

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 880 -

E17-5 Encumbrances at Year-End

a. Outstanding encumbrances lapse at year-end.

(1) Year-end entries:

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 12,500 ENCUMBRANCES 12,500 Close remaining budgeted encumbrances.

Unreserved Fund Balance 12,500 Fund Balance Reserved for Encumbrances 12,500 Reserve actual fund balance for outstanding encumbrances at year-end.

(2) City Council accepts outstanding encumbrances:

Fund Balance Reserved for Encumbrances 12,500 Unreserved Fund Balance 12,500 Reverse prior-year encumbrance reserve.

ENCUMBRANCES 12,500 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 12,500 Establish budgetary control over encumbrances renewed from prior year.

(3) Equipment received:

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 12,500 ENCUMBRANCES 12,500 Remove budgetary reserve for goods received.

Expenditures 12,750 Vouchers Payable 12,750 Record expenditure for goods received at actual cost of $12,750.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 881 -

E17-5 (continued)

b. Outstanding encumbrances are nonlapsing.

(1) Year-end entries:

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 12,500 ENCUMBRANCES 12,500 Close remaining budgetary encumbrances.

Unreserved Fund Balance 12,500 Fund Balance Reserved for Encumbrances 12,500 Reserve fund balance for outstanding encumbrances.

(2) Date the encumbrances:

Fund Balance Reserved for Encumbrances 12,500 Fund Balance Reserved for Encumbrances - 20X1 12,500 Reclassify reserve from prior year.

(3) Equipment received:

Expenditures - 20X1 12,500 Expenditures - 20X2 250 Vouchers Payable 12,750 Record actual expenditure for goods received.

(4) Closing entry:

Fund Balance Reserved for Encumbrances - 20X1 12,500 Expenditures - 20X1 12,500 Close expenditures account for prior year encumbrances.

Unreserved Fund Balance 250 Expenditures 250 Close expenditures for current year.

(Note: In entry (3), the excess of actual cost over the encumbered amount must be approved as part of 20X2's expenditures. Entry (3) records a debit to Expenditures - 20X2 which increases 20X2's expenditures. The expenditures for 20X2 are closed in a separate entry. If the actual cost was less than the encumbered amount, then the difference should be closed to Unreserved Fund Balance, although some governmental units have a policy of closing any difference between actual and encumbered amounts for prior year encumbrances to the current year's expenditures.)

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 882 -

E17-6 Accounting for Inventories of Office Supplies

a. Consumption method of accounting for inventories:

(1) Purchase of supplies:

August 8, 20X2 Expenditures 3,600 Vouchers Payable 3,600 Acquire inventory of supplies.

(2) Entries at end of 20X2 fiscal year:

September 30, 20X2 Inventory of Supplies 2,800 Expenditures 2,800 Recognize ending inventory of supplies.

Unreserved Fund Balance 2,800 Fund Balance Reserved for Inventories 2,800 Establish fund reserve for ending inventory.

Unreserved Fund Balance 800 Expenditures 800 Close expenditures account. (3) Entries at end of 20X3 fiscal year:

September 30, 20X3 Expenditures 2,800 Inventory of Supplies 2,800 Record expenditures for inventories consumed.

Fund Balance Reserved for Inventories 2,800 Unreserved Fund Balance 2,800 Remove fund balance reserve for inventories consumed.

Unreserved Fund Balance 2,800 Expenditures 2,800 Close expenditures account.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 883 -

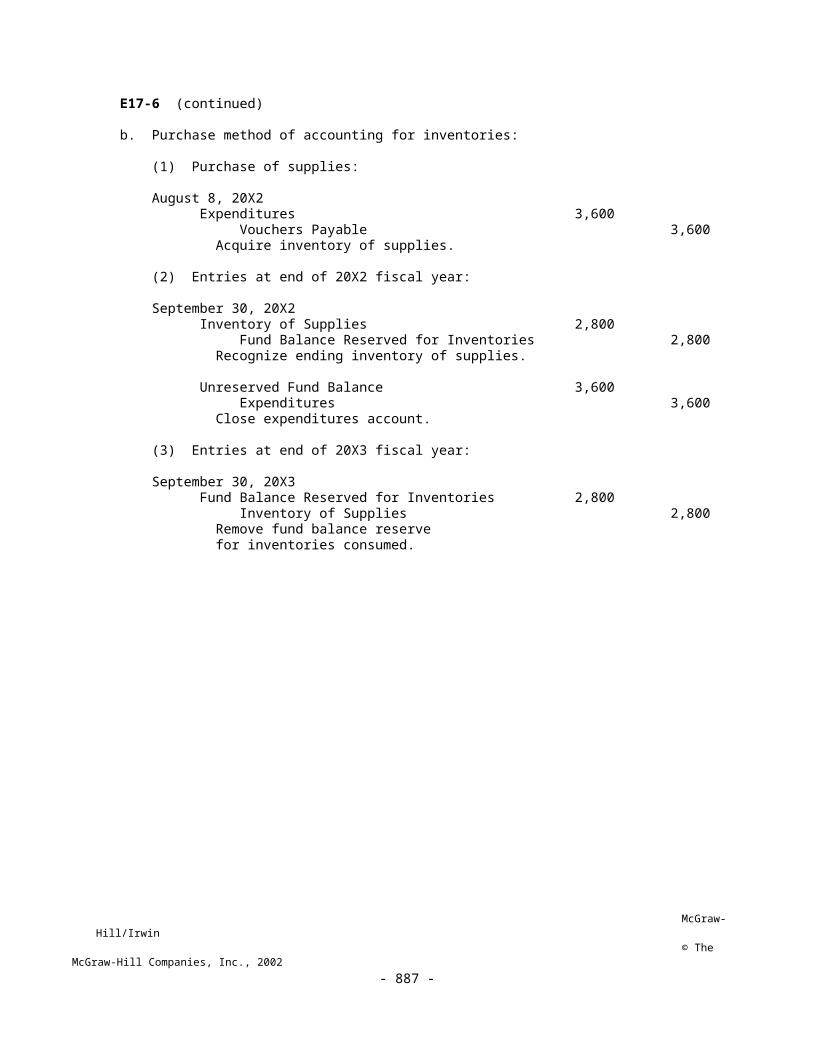

E17-6 (continued)

b. Purchase method of accounting for inventories:

(1) Purchase of supplies:

August 8, 20X2 Expenditures 3,600 Vouchers Payable 3,600 Acquire inventory of supplies.

(2) Entries at end of 20X2 fiscal year:

September 30, 20X2 Inventory of Supplies 2,800 Fund Balance Reserved for Inventories 2,800 Recognize ending inventory of supplies.

Unreserved Fund Balance 3,600 Expenditures 3,600 Close expenditures account.

(3) Entries at end of 20X3 fiscal year:

September 30, 20X3 Fund Balance Reserved for Inventories 2,800 Inventory of Supplies 2,800 Remove fund balance reserve for inventories consumed.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 884 -

E17-7 Accounting for Prepayments and Capital Assets

1. Acquired three-year insurance policy:

September 1, 20X1 Expenditures 5,400 Vouchers Payable 5,400 Record acquisition of three-year insurance policy.

2. New furniture for the city council meeting room:

September 17, 20X1 ENCUMBRANCES 15,600 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 15,600 Encumber for purchase orders for new furniture.

October 1, 20X1 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 15,600 ENCUMBRANCES 15,600 Reverse reserve for furniture received.

Expenditures 15,200 Vouchers Payable 15,200 Receive furniture at actual cost.

3. Acquired supplies - consumption method used:

November 4, 20X1 Expenditures 1,800 Vouchers Payable 1,800 Acquire supplies.

Closing entries:

December 31, 20X1 Inventory of Supplies 1,120 Expenditures 1,120 Recognize ending inventory of supplies.

Unreserved Fund Balance 1,120 Fund Balance Reserved for Inventories 1,120 Establish fund reserve for ending inventory.

Unreserved Fund Balance 21,280 Expenditures 21,280 Close expenditures account: $ 5,400 Insurance Policy 15,200 Furniture 680 Supplies $21,280 Total

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 885 -

E17-8 Computation of Revenues Reported on the Statement of Revenues,Expenditures, and Changes in Fund Balance for the General Fund

Gilbert CityRevenue Reported by the General FundFor the Year Ended June 30, 20X8

Property tax revenue $1,860,000Interest revenue on advance 1,500Grant revenue used to acquire computer equipment 235,000Sales tax revenue 125,000Liquor license revenue 66,000Total revenue reported $2,287,500

Notes:(1) The amount reported for property tax revenue, $1,860,000 is computed in the following way: Levy $2,000,000 Less: The allowance for uncollectible taxes($2,000,000 X .02) (40,000) Property taxes expected to be collected after August 31, 20X8 - the 60 day rule for property tax collections - report as deferred revenue at June 30, 20X8 (100,000) Property tax revenue for year ended June 30, 20X8 $1,860,000

(2) The receipt of $50,000 for the repayment of the advance is recorded in the following manner by the general fund: Cash 51,500 Advance to Internal Service Fund 50,000 Interest revenue 1,500

(3) Collection of property taxes during the year ended June 30, 20X8, does not affect the recognition of revenue. The revenue was recognized at the levy date, not the collection date.

(4) Revenue recognition related to the State grant is based upon spending the grant to acquire computer equipment. Therefore, revenue from the State grant is $235,000, the amount of the grant expended.

(5) Revenue from the sales tax is the amount collected during the year ended June 30, 20X8, or $125,000. The additional sales taxes of $25,000 will be revenue of the next fiscal year when the taxes are received from the State and are available to pay for expenditures incurred in the next fiscal year.

(6) The borrowing of the $800,000 using the property tax levy as collateral represents a liability in the general fund. This amount is not revenue.

(7) The $30,000 received from a terminated debt service fund is reported as an other financing source - transfer in, not revenue.

(8) The revenue from liquor licenses is the amount collected, not the amount expected to be collected. Therefore, revenue of $66,000 is recognized from the sale of liquor licenses for the year ended June 30, 20X8.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 886 -

E17-8 (continued)

(9) The $15,000 reimbursement is not reported as revenue in the general fund. Reimbursements are recorded as reductions in expenditures.

(10) The collection of the delinquent property taxes is not reported as revenue by the general fund for the year ended June 30, 20X8. The revenue associated with the delinquent property taxes was reported in the preceding fiscal year, because the property taxes were expected to be collected within 60 days of the end of the fiscal year.

E17-9 Computation of Expenditures Reported on the Statement of Revenues, Expenditures, and Changes in Fund Balance for the General Fund

Benson CityAmount Reported for Expenditures by the General Fund

For the Year Ended June 30, 20X8

Computer equipment acquisitions in September, 20X7 $ 202,000Reimbursement to special revenue fund in May, 20X8 15,000Use of city water during the fiscal year 12,000Supplies acquisitions 35,000Salaries and wages of general fund employees 900,000Interest paid on loan from local bank 15,000Employer’s pension contribution to pension trust 95,000Lease payments 10,000 Total amount reported for expenditures $1,284,000

Notes:(1) The $150,000 transfer to the capital projects fund in March, 20X8, is reported as an other financing use - transfer out. Therefore, it should not be included in the amount reported for expenditures for the year ended June 30, 20X8.

(2) The amount paid for the computer equipment is the amount reported for expenditures. Therefore, $202,000 is included in expenditures for equipment, not the estimated amount of $200,000 that was recorded for the order(encumbrances).

(3) None of the $500,000 transferred to the internal service fund should be reported as expenditures. The $200,000 that must be repaid by the internal service fund should be accounted for as an advance (a receivable in the general fund), while the $300,000 that represented a permanent contribution should be accounted for as an other financing use - transfer out.

(4) The $15,000 reimbursement to the special revenue fund should be included in the expenditures of the general fund for the year ended June 30, 20X8.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 887 -

E17-9 (continued)

(5) The $12,000 of billings from the water department should be accounted for as expenditures by the general fund. Billings for water usage constitute an interfund services provided and used transaction. Note that the amount paid by the general fund, $11,500, is not the correct amount of the expenditures. The correct amount is $12,000.

(6) The acquisition of supplies and the payment of salaries and wages by the general fund should be accounted for as expenditures. The entire cost of the supplies purchased should be reported as expenditures because the general fund uses the purchase method of accounting for supplies.

(7) The outstanding encumbrances at June 30, 20X8, are not included in expenditures. The outstanding encumbrances will be reported on the general fund balance sheet as a reservation of fund equity.

(8) The repayment of the principal of the bank loan is not an expenditure. However, the amount paid for interest, $15,000, should be included in expenditures for the year ended June 30, 20X8.

(9) The general fund’s $95,000 contribution to the city’s pension trust should be included in expenditures of the general fund for the year ended June 30, 20X8. The employer’s contribution to a pension trust is an example of an interfund services provided or used transaction.

(10) The general fund’s lease payments should be included in the amount reported for expenditures for the year ended June 30, 20X8.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 888 -

E17-10 Closing Entries and Balance Sheet

a. Closing entries for the general fund:

(1) APPROPRIATIONS CONTROL 1,145,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT 25,000 BUDGETARY FUND BALANCE UNRESERVED 30,000 ESTIMATED REVENUES CONTROL 1,200,000 Close budgetary accounts.

(2) BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 32,000 ENCUMBRANCES 32,000 Close remaining encumbrances by reversing remaining budgetary balance.

(3) Unreserved Fund Balance 32,000 Fund Balance Reserved for Encumbrances 32,000 Reserve fund balance for encumbrances that lapse, but are expected to be honored in 20X2.

(4) Property Tax Revenue 1,130,000 Miscellaneous Revenue 40,000 Expenditures 1,140,000 Unreserved Fund Balance 30,000 Close operating statement accounts.

(5) Unreserved Fund Balance 25,000 Other Financing Use - Transfer Out 25,000 Close transfer out.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 889 -

E17-10 (continued)

b. General fund balance sheet:

Lone Wolf General Fund Balance Sheet December 31, 20X1

Assets

Cash $ 90,000Property Taxes Receivable - Delinquent $100,000Less: Allowance for Uncollectibles - Delinquent (7,200) 92,800Due from Other Funds 14,600Total Assets $ 197,400

Liabilities and Fund Balance

Vouchers Payable $ 65,000Due to Other Funds 8,400Fund Balance: Reserved for Encumbrances $32,000 Unreserved 92,000 124,000Total Liabilities and Fund Balance $ 197,400

E17-11 Statement of Revenues, Expenditures, and Changes in Fund Balance

Lone Wolf General Fund Statement of Revenues, Expenditures, and Changes in Fund Balance For the Fiscal Year Ended December 31, 20X1

Revenue: Property Taxes $1,130,000 Miscellaneous 40,000 $1,170,000 Expenditures 1,140,000 Excess of Revenue over Expenditures $ 30,000 Other Financing Sources (Uses): Transfer Out (25,000) Net Change in Fund Balance $ 5,000 Fund Balance, January 1, 20X1 119,000 Fund Balance, December 31, 20X1 $ 124,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 890 -

E17-12 Matching Questions Involving Interfund Activities in the General Fund

1. B

2. C

3. C

4. C

5. C

6. B

7. A

8. D

9. A

10. B

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 891 -

SOLUTIONS TO PROBLEMS

P17-13 General Fund Entries [AICPA Adapted]

(1) ESTIMATED REVENUES CONTROL 2,000,000 APPROPRIATIONS CONTROL 1,940,000 BUDGETARY FUND BALANCE UNRESERVED 60,000 Record the budget.

(2) Taxes Receivable 1,870,000 Allowance for Uncollectible Taxes 10,000 Property Tax Revenue 1,860,000 Record the property tax levy.

(3) Allowance for Uncollectible Taxes 8,000 Taxes Receivable 8,000 Write off uncollectible taxes receivable.

(4) Cash 1,820,000 Taxes Receivable 1,820,000 Record property tax collections.

(5) ENCUMBRANCES 1,070,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 1,070,000 Record purchase commitments.

(6) BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 1,000,000 ENCUMBRANCES 1,000,000 Reverse for purchase orders received.

(7) Expenditures 1,840,000 Vouchers Payable 1,840,000 Record actual expenditures.

(8) Vouchers Payable 1,852,000 Cash 1,852,000 Record payment of vouchers during period.

(9) APPROPRIATIONS CONTROL 1,940,000 BUDGETARY FUND BALANCE UNRESERVED 60,000 ESTIMATED REVENUES CONTROL 2,000,000 Close budgetary accounts.

(10) BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 70,000 ENCUMBRANCES 70,000 Close remaining encumbrances by reversing remaining budgetary balance.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 892 -

P17-13 (continued)

(11) Unreserved Fund Balance 70,000 Fund Balance Reserved for Encumbrances 70,000 Reserve fund balance for outstanding purchase commitments.

(12) Property Tax Revenue 1,860,000 Expenditures 1,840,000 Unreserved Fund Balance 20,000 Close operating statement accounts.

P17-14 General Fund Entries

1. Entry to record operating budget for general fund: ESTIMATED REVENUES CONTROL 925,000 ESTIMATED OTHER FINANCING SOURCE - TRANSFER IN 75,000 APPROPRIATIONS CONTROL 960,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT 25,000 BUDGETARY FUND BALANCE UNRESERVED 15,000

2. Entries to record lapsed encumbrances from the preceding year which were included in current appropriations: Fund Balance Reserved for Encumbrances 18,000 Unreserved Fund Balance 18,000

ENCUMBRANCES CONTROL 18,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 18,000

3. Entry to record property tax levy: Property Taxes Receivable - Current 816,000 Allowance for Uncollectible Taxes - Current 16,000 Revenue - Property Tax 800,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 893 -

P17-14 (Continued)

4. Entry to record receipt of cash from property tax collections: Cash 805,000 Property Taxes Receivable - Current 805,000

Entry to record adjustment to the allowance account: Allowance for Uncollectible Taxes - Current 10,000 Revenue - Property Tax 10,000

Entry to record reclassification of property taxes receivable: Property Taxes Receivable - Delinquent 11,000 Allowance for Uncollectible Taxes – Current 6,000 Allowance for Uncollectible Taxes - Delinquent 6,000 Property Taxes Receivable - Current 11,000

5. Entry to record receipt of sales taxes and other revenue: Cash 126,000 Revenue - Sales Tax 102,000 Revenue - Licenses and Permits 24,000

6. Entry to record interfund receivable for transfer in: Due from Special Revenue Fund 70,000 Other Financing Source - Transfer In from Special Revenue Fund 70,000

Entry to record cash transferred: Cash 70,000 Due from Special Revenue Fund 70,000

Entry to record interfund payable for transfer out: Other Financing Use - Transfer Out to Internal Service Fund 25,000 Due to Internal Service Fund 25,000

Entry to record cash transferred: Due to Internal Service Fund 25,000 Cash 25,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 894 -

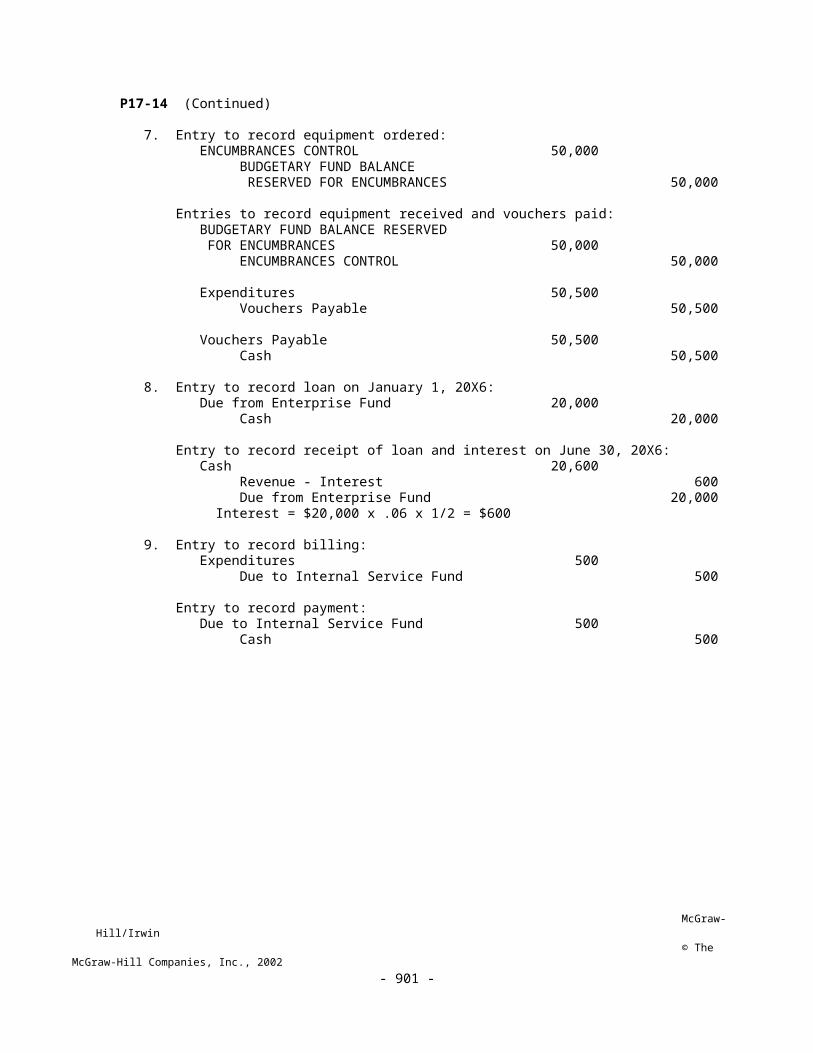

P17-14 (Continued)

7. Entry to record equipment ordered: ENCUMBRANCES CONTROL 50,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 50,000

Entries to record equipment received and vouchers paid: BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 50,000 ENCUMBRANCES CONTROL 50,000

Expenditures 50,500 Vouchers Payable 50,500

Vouchers Payable 50,500 Cash 50,500

8. Entry to record loan on January 1, 20X6: Due from Enterprise Fund 20,000 Cash 20,000

Entry to record receipt of loan and interest on June 30, 20X6: Cash 20,600 Revenue - Interest 600 Due from Enterprise Fund 20,000 Interest = $20,000 x .06 x 1/2 = $600

9. Entry to record billing: Expenditures 500 Due to Internal Service Fund 500

Entry to record payment: Due to Internal Service Fund 500 Cash 500

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 895 -

P17-15 General Fund Entries [AICPA Adapted]

1. ESTIMATED REVENUES CONTROL 3,000,000 APPROPRIATIONS CONTROL 2,980,000 BUDGETARY FUND BALANCE UNRESERVED 20,000 Record the budget.

Taxes Receivable 2,870,000 Allowance for Uncollectible Taxes 70,000 Revenue from Taxes 2,800,000 Record tax levy.

Cash 2,810,000 Taxes Receivable 2,810,000 Record tax collection.

Allowance for Uncollectible Taxes 40,000 Taxes Receivable 40,000 Record write-off of uncollectible taxes: July 1, 20X1, taxes receivable balance $ 150,000 20X2 tax levy 2,870,000 Less: Taxes collected (2,810,000) Taxes receivable final balance (170,000) Taxes written off as uncollectible $ 40,000

Cash 130,000 Miscellaneous Revenue 130,000 Collect miscellaneous revenue.

2. Fund Balance Reserved for Encumbrances 60,000 Unreserved Fund Balance 60,000 Reverse prior reserve which has been renewed.

ENCUMBRANCES 60,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 60,000 Renew encumbrances from prior period.

ENCUMBRANCES 2,700,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 2,700,000 Record encumbrances.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 896 -

P17-15 (Continued)

3. Expenditures 142,000 Due to Other Funds 142,000 Record liability to other funds for services received.

4. BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 2,700,000 ENCUMBRANCES 2,700,000 Reverse encumbrances for items received.

Expenditures 2,700,000 Vouchers Payable 2,700,000 Record expenditures.

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 60,000 ENCUMBRANCES 60,000 Reverse reserve for encumbrances.

Expenditures (Prior Period) 58,000 Vouchers Payable 58,000 Actual expenditure for goods received.

Due to Other Funds 210,000 Vouchers Payable 210,000 Record approval for payment to other funds.

Vouchers Payable 2,640,000 Cash 2,640,000 Record voucher payments.

5. ENCUMBRANCES 91,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 91,000 Record May 10 encumbrance.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 897 -

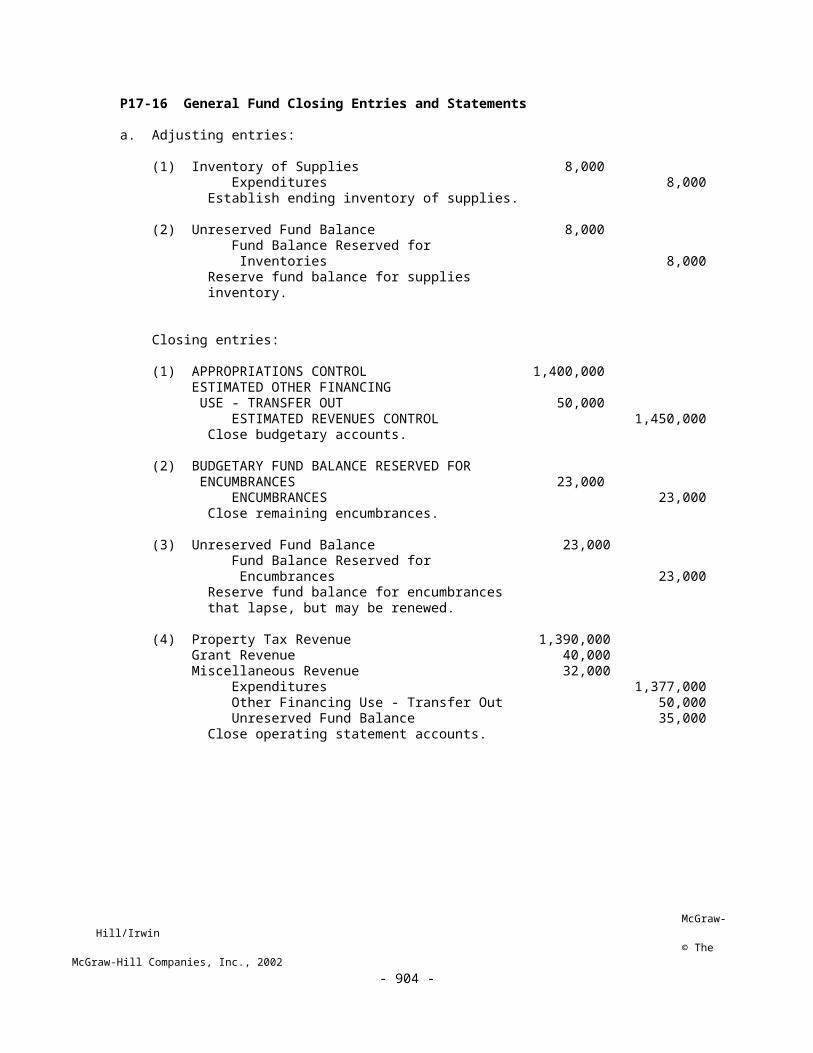

P17-16 General Fund Closing Entries and Statements

a. Adjusting entries:

(1) Inventory of Supplies 8,000 Expenditures 8,000 Establish ending inventory of supplies.

(2) Unreserved Fund Balance 8,000 Fund Balance Reserved for Inventories 8,000 Reserve fund balance for supplies inventory.

Closing entries:

(1) APPROPRIATIONS CONTROL 1,400,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT 50,000 ESTIMATED REVENUES CONTROL 1,450,000 Close budgetary accounts.

(2) BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 23,000 ENCUMBRANCES 23,000 Close remaining encumbrances.

(3) Unreserved Fund Balance 23,000 Fund Balance Reserved for Encumbrances 23,000 Reserve fund balance for encumbrances that lapse, but may be renewed.

(4) Property Tax Revenue 1,390,000 Grant Revenue 40,000 Miscellaneous Revenue 32,000 Expenditures 1,377,000 Other Financing Use - Transfer Out 50,000 Unreserved Fund Balance 35,000 Close operating statement accounts.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 898 -

P17-16 (continued)

b. Quincy General Fund Balance Sheet June 30, 20X2

Assets

Cash $ 100,000Property Taxes Receivable - Delinquent $ 108,000Less: Allowance for Uncollectibles - Delinquent (8,400) 99,600Due from Data Processing Fund 10,000Inventory of Supplies 8,000Total Assets $ 217,600

Liabilities and Fund Balance

Vouchers Payable $ 44,000Due to Printing Service Fund 2,600Fund Balance: Reserved for Inventories $ 8,000 Reserved for Encumbrances 23,000 Unreserved Fund Balance 140,000 171,000Total Liabilities and Fund Balance $ 217,600

c. Quincy General Fund Statement of Revenues, Expenditures, and Changes in Fund Balance For Fiscal Year Ended June 30, 20X2

Revenue: Property Taxes $1,390,000 Grants 40,000 Miscellaneous 32,000 $1,462,000Expenditures 1,377,000Excess of Revenue over Expenditures $ 85,000Other Financing Sources (Uses): Transfer Out (50,000)Net Change in Fund Balance $ 35,000Fund Balance, July 1, 20X1 136,000Fund Balance, June 30, 20X2 $ 171,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 899 -

P17-17 General Fund Entries and Statements

a. Budget and transaction entries for 20X2:

1. & 2.

ESTIMATED REVENUES CONTROL 1,420,500 APPROPRIATIONS CONTROL 1,356,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT TO INTERNAL SERVICE FUND 25,000 BUDGETARY FUND BALANCE UNRESERVED 39,500 Record budget.

Property Taxes Receivable - Current 1,300,000 Allowance for Uncollectibles - Current 19,500 Property Tax Revenue 1,280,500 Record levy.

Fund Balance Reserved for Encumbrances 18,000 Fund Balance Reserved for Encumbrances - 20X1 18,000 Reclassify reserve for prior year.

3. Cash 1,314,000 Property Taxes Receivable - Current 1,245,000 Property Taxes Receivable - Delinquent 69,000 Record tax collections.

Cash 166,000 Grants Revenue 90,000 Miscellaneous Revenue 46,000 Other Financing Source - Transfer In from Capital Projects Fund 30,000 Other cash receipts.

Allowance for Uncollectibles - Delinquent 8,000 Property Tax Revenue 3,000 Property Taxes Receivable - Delinquent 11,000 Write off remaining delinquent taxes from 20X1.

Allowance for Uncollectibles - Current 12,000 Property Tax Revenue 12,000 Reduce current allowance to $7,500.

Property Taxes Receivable - Delinquent 55,000 Allowance for Uncollectibles - Current 7,500 Property Taxes Receivable - Current 55,000 Allowance for Uncollectibles - Delinquent 7,500 Remainder of unpaid 20X2 property taxes reclassified as delinquent.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 900 -

P17-17 (continued)

4. ENCUMBRANCES 1,336,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 1,336,000 Issue purchase orders.

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 1,216,000 ENCUMBRANCES 1,216,000 Receive ordered items: $1,216,000 = $1,336,000 - $120,000 outstanding

Expenditures - 20X1 18,000 Expenditures - (20X2) 2,000 Vouchers payable 20,000 Actual cost for prior year's encumbrance is $20,000. The approved excess of $2,000 is charged to current year's expenditures.

Expenditures - (20X2) 1,220,000 Vouchers Payable 1,209,000 Inventory of Supplies 11,000 Actual expenditures, including beginning inventory of supplies: $1,220,000 = $1,240,000 - $20,000 prior year’s

Fund Balance Reserved for Inventories 11,000 Unreserved Fund Balance 11,000 Eliminate present reserve for inventories. (Will properly re-establish in adjusting entry process.)

Vouchers payable 1,227,000 Cash 1,227,000 Pay vouchers.

5. Other Financing Use – Transfer Out to Internal Service Fund 25,000Due from Computer Center Fund 20,000 Cash 45,000 Other cash payments.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 901 -

P17-17 (continued)

b. Ruby Valley General Fund Preadjusting Trial Balance June 30, 20X2

Debit Credit

Cash $ 311,000Property Tax Receivable - Delinquent 55,000Allowance for Uncollectibles - Delinquent $ 7,500Due from Computer Center Fund 20,000Inventory of Supplies -0-Vouchers Payable 44,000Fund Balance Reserved for Inventories -0-Fund Balance Reserved for Encumbrances - 20X1 18,000Unreserved Fund Balance 126,000Property Tax Revenue 1,289,500Grants Revenue 90,000Miscellaneous Revenue 46,000Other Financing Source - Transfer In from Capital Projects Fund 30,000Expenditures - 20X1 18,000Expenditures 1,222,000Other Financing Use - Transfer Out to Internal Service Fund 25,000ESTIMATED REVENUES CONTROL 1,420,500APPROPRIATIONS CONTROL 1,356,000ESTIMATED OTHER FINANCING USES - TRANSFER OUT TO INTERNAL SERVICE FUND 25,000ENCUMBRANCES 120,000BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 120,000BUDGETARY FUND BALANCE UNRESERVED 39,500 $3,191,500 $3,191,500

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 902 -

P17-17 (continued)

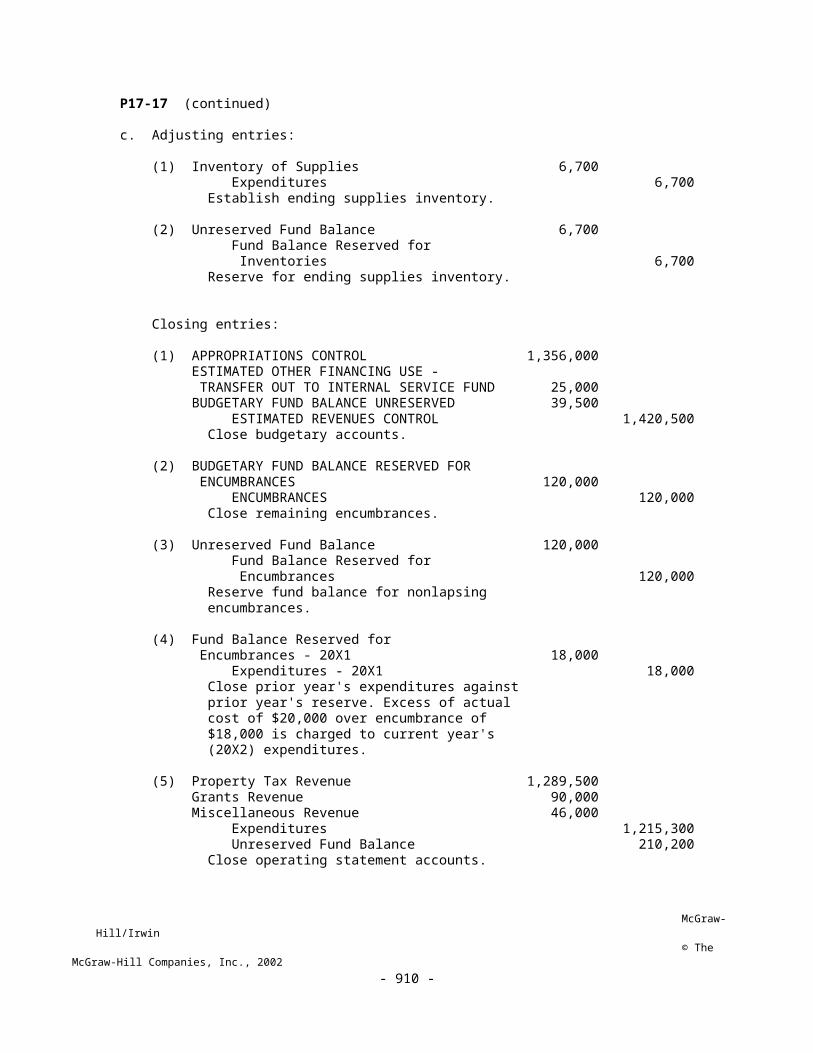

c. Adjusting entries:

(1) Inventory of Supplies 6,700 Expenditures 6,700 Establish ending supplies inventory.

(2) Unreserved Fund Balance 6,700 Fund Balance Reserved for Inventories 6,700 Reserve for ending supplies inventory.

Closing entries:

(1) APPROPRIATIONS CONTROL 1,356,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT TO INTERNAL SERVICE FUND 25,000 BUDGETARY FUND BALANCE UNRESERVED 39,500 ESTIMATED REVENUES CONTROL 1,420,500 Close budgetary accounts.

(2) BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 120,000 ENCUMBRANCES 120,000 Close remaining encumbrances.

(3) Unreserved Fund Balance 120,000 Fund Balance Reserved for Encumbrances 120,000 Reserve fund balance for nonlapsing encumbrances.

(4) Fund Balance Reserved for Encumbrances - 20X1 18,000 Expenditures - 20X1 18,000 Close prior year's expenditures against prior year's reserve. Excess of actual cost of $20,000 over encumbrance of $18,000 is charged to current year's (20X2) expenditures.

(5) Property Tax Revenue 1,289,500 Grants Revenue 90,000 Miscellaneous Revenue 46,000 Expenditures 1,215,300 Unreserved Fund Balance 210,200 Close operating statement accounts.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 903 -

P17-17 (continued)

(6) Other Financing Source - Transfer In from Capital Projects Fund 30,000 Other Financing Use - Transfer Out to Internal Service Fund 25,000 Unreserved Fund Balance 5,000 Close interfund transfers.

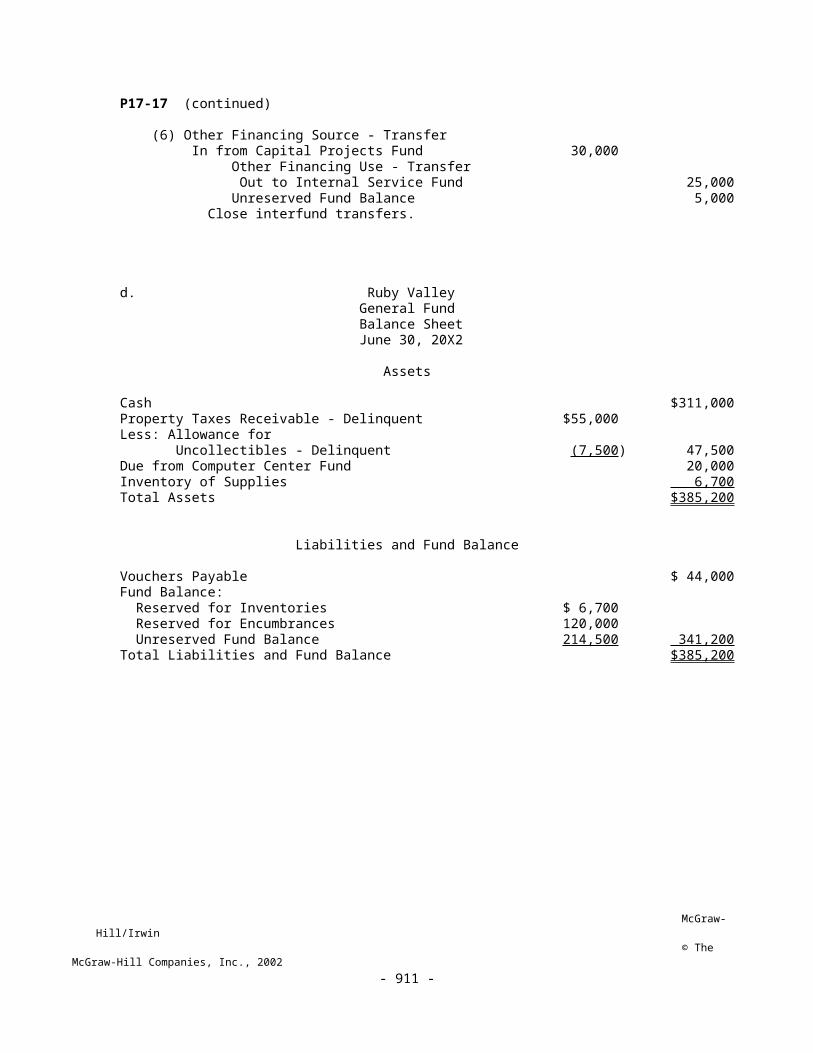

d. Ruby Valley General Fund Balance Sheet June 30, 20X2

Assets

Cash $311,000Property Taxes Receivable - Delinquent $55,000Less: Allowance for Uncollectibles - Delinquent (7,500) 47,500Due from Computer Center Fund 20,000Inventory of Supplies 6,700Total Assets $385,200

Liabilities and Fund Balance

Vouchers Payable $ 44,000Fund Balance: Reserved for Inventories $ 6,700 Reserved for Encumbrances 120,000 Unreserved Fund Balance 214,500 341,200Total Liabilities and Fund Balance $385,200

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 904 -

P17-17 (continued)

e. Ruby Valley General Fund Statement of Revenues, Expenditures, and Changes in Fund Balance For Fiscal Year Ended June 30, 20X2

Actual Revenue: Property Taxes $1,289,500 Grants 90,000

Miscellaneous 46,000

Total Revenues $1,425,500Expenditures: Chargeable to 20X2 Appropriations: Current (Schedule A) $1,170,300 Capital Outlay 45,000 Total Expenditures of 20X2 Appropriations $1,215,300 Chargeable to 20X1 Appropriations:

Current (20X1 encumbrance) 18,000

Total Expenditures $1,233,300Excess of Revenue over Expenditures $ 192,200Other Financing Sources (Uses): Transfer Out $ (25,000) Transfer In 30,000 5,000Change in Fund Balance $ 197,200Fund Balance, July 1, 20X1 144,000Fund Balance, June 30, 20X2 $ 341,200

Schedule A: Actual expenditures: Preadjusting trial balance, expenditures $1,222,000 Inventory adjustment (6,700) Capital expenditure outlay for elevator (45,000) Actual current operating expenditures $1,170,300

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 905 -

P17-18 General Fund Entries and Statements

a. Entries for 20X2 budget and transactions:

1. ESTIMATED REVENUES CONTROL 1,877,000 APPROPRIATIONS CONTROL 1,840,000 ESTIMATED OTHER FINANCIAL USE - TRANSFER OUT 37,000 Record budget.

ENCUMBRANCES 21,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 21,000 Renew encumbrances from prior period.

Fund Balance Reserved for Encumbrances 21,000 Unreserved Fund Balance 21,000 Reverse reserve for renewed encumbrances.

Property Tax Receivable - Current 1,600,000 Allowance for Uncollectibles - Current 16,000 Property Tax Revenue 1,584,000 Record property tax levy.

2. Cash 1,590,000 Property Taxes Receivable - Current 1,507,000 Property Taxes Receivable - Delinquent 83,000 Collect property taxes.

Allowance for Uncollectibles - Delinquent 9,000 Property Taxes Receivable - Delinquent 7,000 Property Tax Revenue 2,000 Write off remaining delinquent property taxes.

Property Taxes Receivable - Delinquent 93,000 Allowance for Uncollectibles - Current 16,000 Property Taxes Receivable - Current 93,000 Allowance for Uncollectibles - Delinquent 16,000 Reclassify remainder of uncollected 20X2 property taxes.

Cash 333,000 Sales Tax Revenue 284,000 Miscellaneous Revenue 39,000 Due to Motor Pool Fund 10,000 Other cash receipts.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 906 -

P17-18 (continued)

3. ENCUMBRANCES 1,800,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 1,800,000 Record purchase orders.

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 1,773,000 ENCUMBRANCES 1,773,000 Reverse reserve for items received.

Expenditures 1,788,000 Vouchers Payable 1,788,000 Actual expenditures for items received.

Vouchers Payable 1,793,000 Cash 1,793,000 Vouchers paid.

4. Due from Central Stores Fund 13,000 Other Financing Use - Transfer Out 37,000 Cash 50,000 Other cash payments and transfer.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 907 -

P17-18 (continued)

b. Pine Ridge General Fund Preclosing Trial Balance December 31, 20X2

Debit Credit

Cash $ 191,000Property Tax Receivable - Delinquent 93,000Allowance for Uncollectibles - Delinquent $ 16,000Due from Central Stores Fund 13,000Vouchers Payable 26,000Due to Motor Pool Fund 10,000Unreserved Fund Balance 161,000Property Tax Revenue 1,586,000Sales Tax Revenue 284,000Miscellaneous Revenue 39,000Expenditures 1,788,000Other Financing Use - Transfer Out 37,000ESTIMATED REVENUES CONTROL 1,877,000APPROPRIATIONS CONTROL 1,840,000ESTIMATED OTHER FINANCING USE - TRANSFER OUT 37,000ENCUMBRANCES 48,000BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 48,000 $4,047,000 $4,047,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 908 -

P17-18 (continued)

c. Closing entries:

APPROPRIATIONS CONTROL 1,840,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT 37,000 ESTIMATED REVENUES CONTROL 1,877,000 Close budgetary accounts.

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 48,000 ENCUMBRANCES 48,000 Close remaining encumbrances.

Unreserved Fund Balance 48,000 Fund Balance Reserved for Encumbrances 48,000 Reserve fund balance for outstanding purchase orders.

Property Tax Revenue 1,586,000 Sales Tax Revenue 284,000 Miscellaneous Revenue 39,000 Expenditures 1,788,000 Other Financing Use - Transfer Out 37,000 Unreserved Fund Balance 84,000 Close operating statement accounts.

d. Pine Ridge General Fund Balance Sheet December 31, 20X2

AssetsCash $ 191,000Property Tax Receivables - Delinquent $ 93,000Less: Allowance for Uncollectibles - Delinquent (16,000) 77,000Due from Central Stores Fund 13,000Total Assets $281,000

Liabilities and Fund BalanceVouchers Payable $ 26,000Due to Motor Pool Fund 10,000Fund Balance: Reserved for Encumbrances $ 48,000 Unreserved Fund Balance 197,000 245,000Total Liabilities and Fund Balance $281,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 909 -

P17-18 (continued)

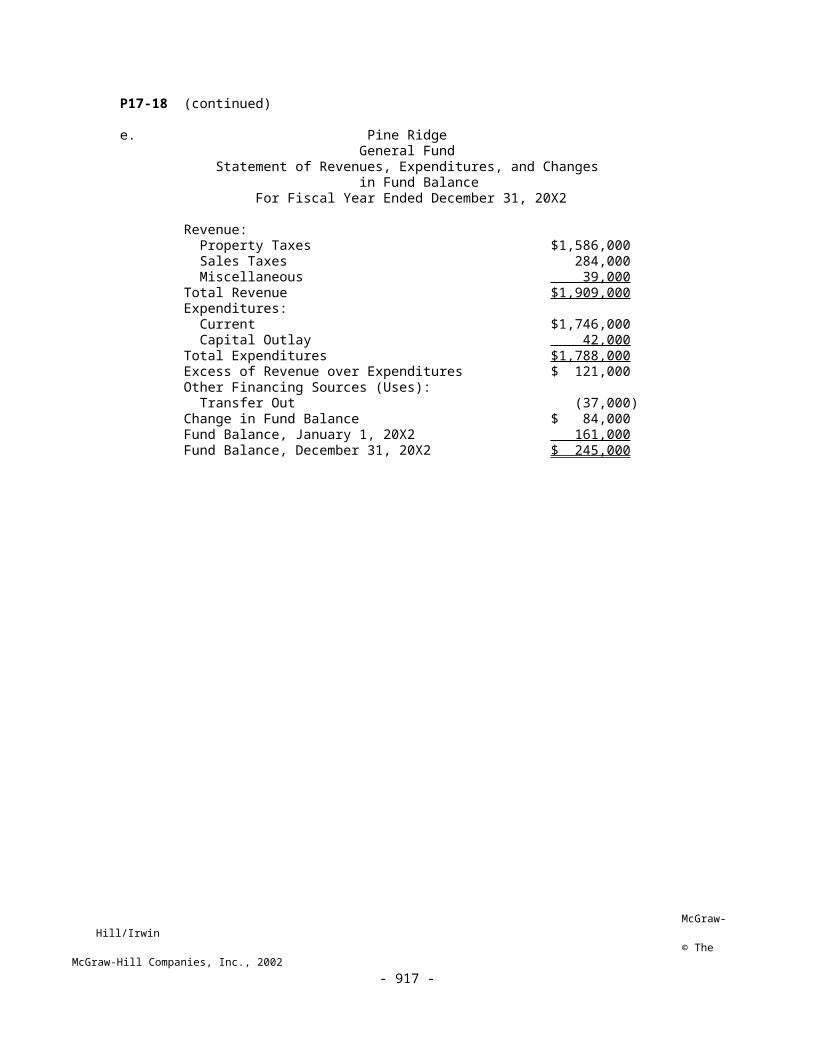

e. Pine Ridge General Fund Statement of Revenues, Expenditures, and Changes in Fund Balance For Fiscal Year Ended December 31, 20X2

Revenue: Property Taxes $1,586,000 Sales Taxes 284,000 Miscellaneous 39,000 Total Revenue $1,909,000 Expenditures: Current $1,746,000 Capital Outlay 42,000 Total Expenditures $1,788,000 Excess of Revenue over Expenditures $ 121,000 Other Financing Sources (Uses): Transfer Out (37,000) Change in Fund Balance $ 84,000 Fund Balance, January 1, 20X2 161,000 Fund Balance, December 31, 20X2 $ 245,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 910 -

P17-19 General Fund Entries

ESTIMATED REVENUE - PROPERTY TAXES 4,500,000 ESTIMATED REVENUE - LICENSES AND PERMITS 300,000 ESTIMATED REVENUE - FINES 200,000 APPROPRIATIONS - GENERAL GOVERNMENT 1,500,000 APPROPRIATIONS - POLICE SERVICES 1,200,000 APPROPRIATIONS - FIRE DEPARTMENT SERVICES 900,000 APPROPRIATIONS - PUBLIC WORKS SERVICES 800,000 APPROPRIATIONS - FIRE ENGINES 400,000 BUDGETARY FUND BALANCE UNRESERVED 200,000 Record the budget.

1. Property Taxes Receivable - Current 4,650,000 Allowance for Uncollectibles - Current 150,000 Property Tax Revenue 4,500,000 Record property tax levy.

2. Cash 3,900,000 Property Taxes Receivable 3,900,000 Record collection of taxes.

Property Taxes Receivable - Delinquent 750,000 Allowance for Uncollectibles - Current 150,000 Property Taxes Receivable - Current 750,000 Allowance for Uncollectibles - Delinquent 150,000 Record reclassification of taxes.

3. Cash 300,000 Notes Payable 300,000 Record issue of tax anticipation notes.

4. Cash 485,000 Revenue - Licenses and Permits 270,000 Revenue - Fines 200,000 Revenue - Sale of Fixed Assets 15,000 Record other cash collections.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 911 -

P17-19 (continued)

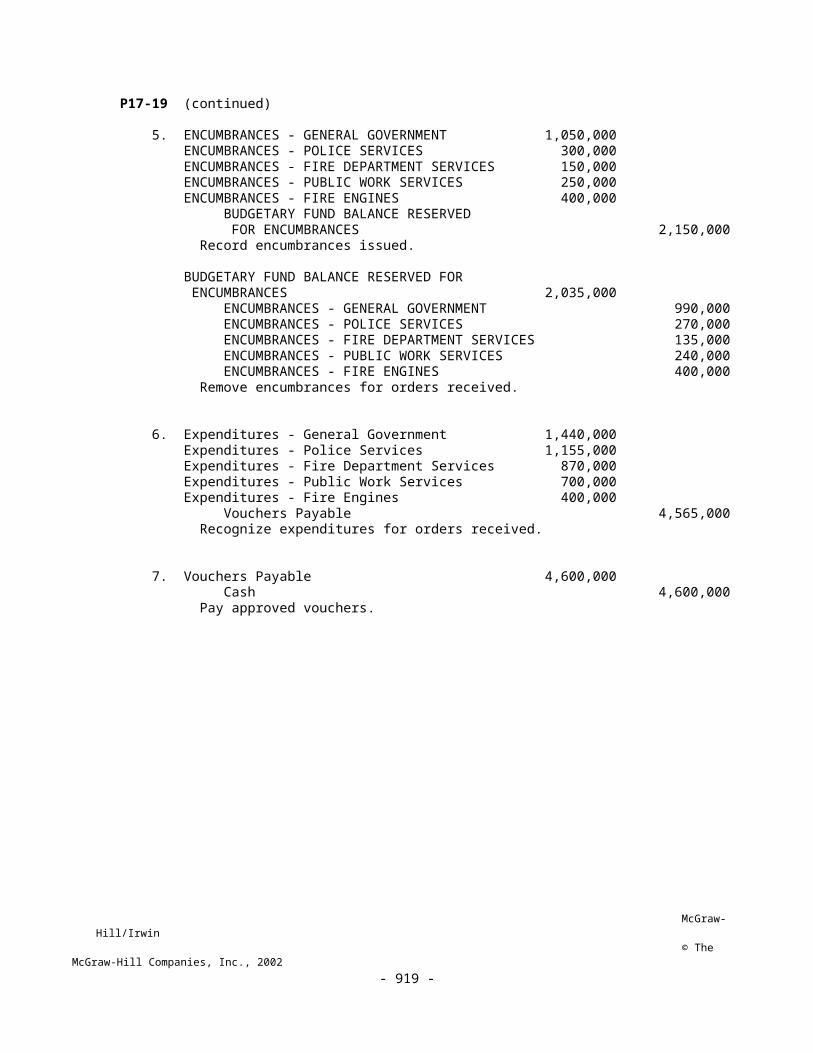

5. ENCUMBRANCES - GENERAL GOVERNMENT 1,050,000 ENCUMBRANCES - POLICE SERVICES 300,000 ENCUMBRANCES - FIRE DEPARTMENT SERVICES 150,000 ENCUMBRANCES - PUBLIC WORK SERVICES 250,000 ENCUMBRANCES - FIRE ENGINES 400,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 2,150,000 Record encumbrances issued.

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 2,035,000 ENCUMBRANCES - GENERAL GOVERNMENT 990,000 ENCUMBRANCES - POLICE SERVICES 270,000 ENCUMBRANCES - FIRE DEPARTMENT SERVICES 135,000 ENCUMBRANCES - PUBLIC WORK SERVICES 240,000 ENCUMBRANCES - FIRE ENGINES 400,000 Remove encumbrances for orders received.

6. Expenditures - General Government 1,440,000 Expenditures - Police Services 1,155,000 Expenditures - Fire Department Services 870,000 Expenditures - Public Work Services 700,000 Expenditures - Fire Engines 400,000 Vouchers Payable 4,565,000 Recognize expenditures for orders received.

7. Vouchers Payable 4,600,000 Cash 4,600,000 Pay approved vouchers.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 912 -

P17-20 General Fund Entries [AICPA Adapted]

1. Budget adopted:

ESTIMATED REVENUE - TAXES 220,000 ESTIMATED REVENUE - FINES, FORFEITS, AND PENALTIES 80,000 ESTIMATED REVENUE - MISCELLANEOUS 100,000 ESTIMATED OTHER FINANCING SOURCES - PROCEEDS OF BOND ISSUE 200,000 APPROPRIATIONS - PROGRAM OPERATIONS 360,000 APPROPRIATIONS - GENERAL ADMINISTRATION 120,000 APPROPRIATIONS - CAPITAL OUTLAYS 80,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT TO CAPITAL PROJECTS FUND 20,000 BUDGETARY FUND BALANCE UNRESERVED 20,000 Record budget.

Fund Balance Reserved for Encumbrances 12,000 Fund Balance Reserved for Encumbrances - 20X2 12,000 Reclassify reserve from prior year.

2. Taxes Receivable - Current 230,000 Allowance for Uncollectible Taxes - Current 9,200 Revenue - Taxes 220,800 Record tax levy: $230,000 = ($220,800/.96)

3. ENCUMBRANCES 316,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 316,000 Record encumbrance for ordered goods.

4. Unreserved Fund Balance 20,000 Fund Balance Designated for Capital Outlays 20,000 Designation of fund balance.

5. Cash 664,000 Taxes Receivable - Delinquent 38,000 Taxes Receivable - Current 226,000 Expenditures - Capital Outlay 4,000 Revenue - Fines, Forfeits, and Penalties 88,000 Revenue - Miscellaneous 90,000 Other Financing Source - Proceeds of Bond Issue 200,000 Other Financing Source - Transfer In from Discontinued Fund 18,000 Record cash collections and transfers.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 913 -

P17-20 (continued)

6. Allowance for Uncollectible Accounts – Current 6,200 Revenue - Taxes 6,200 Adjust current allowance account.

Allowance for Uncollectible Accounts - Delinquent 8,000 Taxes Receivable - Delinquent 8,000 Write off remaining delinquent taxes receivable

7. BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 290,000 ENCUMBRANCES 290,000 Reverse budgetary encumbrance for orders received: ($302,000 - $12,000) Expenditures - 20X2 - Program Operations 12,000 Expenditures - Program Operations 154,000 Expenditures - General Administration 80,000 Expenditures - Capital Outlay 62,000 Vouchers Payable 308,000 Record expenditures for orders received.

8. Expenditures - Program Operations 188,000 Expenditures - General Administration 38,000 Expenditures - Capital Outlay 18,000 Other Financing Use - Transfer Out to Capital Projects Fund 20,000 Vouchers Payable 244,000 Due to Capital Projects Fund 20,000 Record additional vouchers.

9. Taxes Receivable - Current 2,000 Deferred Revenue - Taxes 2,000 Record credit for overpayment.

10. Vouchers Payable 580,000 Cash 580,000 Pay approved vouchers.

11. Fund Balance Reserved for Stores Inventory 6,000 Stores Inventory - Program Operations 6,000 Record reduction in stores inventory.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 914 -

P17-21 General Fund Entries and Balance Sheet

a.

1. ESTIMATED REVENUES CONTROL 290,000 ESTIMATED OTHER FINANCING SOURCE - TRANSFER IN 20,000 APPROPRIATIONS CONTROL 285,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT 15,000 BUDGETARY FUND BALANCE UNRESERVED 10,000 Record the operating budget for fiscal 20X6.

2. Fund Balance Reserved for Encumbrances 16,000 Unreserved Fund Balance 16,000

ENCUMBRANCES CONTROL 16,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 16,000 Record the encumbrances that lapsed at June 30, 20X5, which were included in 20X6 appropriations.

3. Property Taxes Receivable - Current 220,000 Allowance for Uncollectible Taxes - Current 8,800 Revenue - Property Taxes 211,200 Record property tax levy for fiscal 20X6.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 915 -

P17-21 (continued)

4. Cash 320,000 Property Taxes Receivable - Delinquent 15,000 Property Taxes Receivable - Current 198,000 Revenue - State Grants 50,000 Revenue - Sales Taxes 17,500 Revenue - Fines, Licenses, and Permits 11,000 Other Financing Source - Transfer In from Capital Projects Fund 18,000 Due from Enterprise Fund 10,000 Revenue - Interest 500 Record cash collections in the general fund for fiscal 20X6.

Allowance for Uncollectible Property Taxes - Delinquent 7,000 Property Taxes Receivable - Delinquent 7,000 Write-off uncollectible property taxes from fiscal 20X5.

Property Taxes Receivable - Delinquent 22,000 Allowance for Uncollectible Taxes - Current 8,800 Property Taxes Receivable - Current 22,000 Allowance for Uncollectible Taxes - Delinquent 6,000 Revenue - Property Taxes 2,800 Reclassify property taxes receivable to delinquent and to reduce the allowance for uncollectible taxes from $8,800 to $6,000.

5. ENCUMBRANCES CONTROL 49,000 BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 49,000 Record goods ordered during fiscal 20X6, exclusive of the goods ordered in entry (2): $49,000 = $65,000 - $16,000

BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 57,000 ENCUMBRANCES CONTROL 57,000 Reverse encumbrances for invoices received: $57,000 = $65,000 - $8,000 Expenditures 58,000 Vouchers Payable 58,000 Record actual cost of goods received.

Vouchers Payable 49,500 Cash 49,500 Record vouchers paid: $49,500 = $58,000 - $8,500

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 916 -

P17-21 (continued)

6. Expenditures 215,000 Vouchers Payable 215,000 Record expenditures for fiscal 20X6 which were not encumbered.

Vouchers Payable 203,000 Cash 203,000 Record vouchers paid: $203,000 = $215,000 - $12,000

7. Due to Internal Service Fund 8,000 Cash 8,000 Record payment of billing from fiscal 20X5.

Vouchers Payable 27,000 Cash 27,000 Record payment of vouchers from fiscal 20X5.

8. Other Financing Use - Transfer Out to Debt Service Fund 15,000 Due to Debt Service Fund 15,000 Record transfer out to debt service fund.

Due to Debt Service Fund 15,000 Cash 15,000 Record cash transferred to debt service fund.

9. Inventory of Supplies 2,500 Fund Balance Reserved for Inventories 2,500 Adjust inventory of supplies to $7,500 balance at June 30, 20X6.

10. BUDGETARY FUND BALANCE UNRESERVED 10,000 APPROPRIATIONS CONTROL 285,000 ESTIMATED OTHER FINANCING USE - TRANSFER OUT 15,000 ESTIMATED REVENUES CONTROL 290,000 ESTIMATED OTHER FINANCING SOURCE - TRANSFER IN 20,000 Close the budgetary accounts at June 30, 20X6.

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 917 -

P17-21 (continued)

11. Revenue - Property Taxes 214,000 Revenue - State Grants 50,000 Revenue - Sales Taxes 17,500 Revenue - Fines, Licenses, and Permits 11,000 Revenue - Interest 500 Other Financing Source - Transfer In from Capital Projects Fund 18,000 Expenditures 273,000 Other Financing Use - Transfer Out to Debt Service Fund 15,000 Unreserved Fund Balance 23,000 Close the accounts containing actual resource flows.

12. BUDGETARY FUND BALANCE RESERVED FOR ENCUMBRANCES 8,000 ENCUMBRANCES CONTROL 8,000 Close the encumbrances which lapsed on June 30, 20X6.

Unreserved Fund Balance 8,000 Fund Balance Reserved for Encumbrances 8,000 Reserve fund balance for encumbrances that lapsed.

b.Village of MargaretBalance Sheet - General Fund

June 30, 20X6

Assets

Cash $52,500 Property Taxes Receivable - Delinquent $22,000 Less: Allowance for Uncollectible Taxes - Delinquent (6,000) 16,000 Inventory of Supplies 7,500 Total Assets $76,000

Liabilities and Fund Balance

Vouchers Payable $20,500 Fund Balance: Reserve for Encumbrances $ 8,000 Reserve for Inventories 7,500 Unreserved 40,000 55,500 Total Liabilities and Fund Balance $76,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 918 -

P17-22 Matching Governmental Terms with Descriptions

1. J

2. I

3. H

4. G

5. M

6. Q

7. R

8. E

9. N

10. D

11. F

12. P

13. A

14. B

15. L

16. C

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 919 -

P17-23 Identification of Governmental Accounting Terms

1. Government-wide financial statements

2. The Governmental Accounting Standards Board, or GASB

3. A fund

4. Interfund services provided or used

5. Internal service and enterprise funds

6. Infrastructure assets

7. Agency and trust funds

8. Modified accrual basis

9. Accrual basis

10. The property tax levy

11. The general, special revenue, capital projects, debt service funds and permanent funds

12. The allowance for uncollectible property taxes

13. Budgetary fund balance unreserved

14. Encumbrances

15. The consumption method

16. Other financing use - transfer out

17. Expenditures

18. Unreserved fund balance

19. Expenditures

20. Appropriations

21. Nonlapsing method

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 920 -

P17-24 Questions on General Fund Entries [AICPA Adapted]

1. D 2. C 3. C 4. C 5. N 6. D 7. N 8. C 9. C 10. N

11. D 12. C 13. N 14. N 15. N

16. C 17. D 18. D 19. C 20. N

21. N 22. N 23. C 24. D 25. N

26. C 27. D 28. D 29. D 30. C

31. D 32. C 33. D 34. N 35. N

36. C 37. D 38. D 39. C

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 921 -

17-25 Questions on General Fund Items [AICPA Adapted]

1. P $700,000 = $630,000 of current year’s taxes collected plus $70,000 of 20X1 taxes expected to be collected within 60 days after the end of the year

2. H $170,000 = $80,000 of the restricted grant that has been expended, plus $50,000 in fines plus $40,000 in fees

3. C $50,000 = the fair and present value of the lease agreement

4. F $140,000 = the capital outlay for the new police vehicles

5. B $30,000 = the amount of the transfer in received by the debt service fund and then expended for interest for the year

6. R $760,000 = $260,000 for governmental services and $500,000 for police services. Note the capital outlay for the new police vehicle is not a functional expenditure.

7. G $150,000 = the amount of the state grant. The bond proceeds would be reported as an other financing source.

8. M $500,000 = the amount of the expenditures in the capital projects fund

9. K $345,000 = Unreserved fund balance on 1/1/X1 $110,000 Add: Grant revenues $150,000 Other financing sources 610,000 760,000 Less: Expenditures $500,000 Fund balance reserved for encumbrances 25,000 (525,000) Unreserved fund balance

on 12/31/X1 $345,000

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2002

- 922 -