514 ©2013 Pearson Education, Inc. Publishing as Prentice Hall Chapter 15 Raising Capital LEARNING OBJECTIVES (Slide 152) 1. Describe the life cycle of a business. 2. Understand the different sources of capital available to a start-up business and to a growing business. 3. Explain the funding available to a stable or mature business. 4. Explain how companies sell bonds in a capital market. 5. Explain how companies sell stocks in a capital market. 6. Examine some special forms of financing: commercial paper and banker’s acceptance. 7. Describe the options and regulations for closing a business. IN A NUTSHELL… This chapter is about how entrepreneurs and firms go about raising funds for growth and development. As a firm progresses through the various phases of its business cycle, its needs, focus, and conditions change requiring it to use different sources of capital. Firms typically sell bonds and stock to raise capital and so the author explains the process followed by issuing companies. Besides bonds and stock, firms also borrow short-term funds by issuing commercial paper and bankers’ acceptances. The chapter closes with a discussion of the options and regulations that come into play when a firm decides to cease operations and close permanently. LECTURE OUTLINE 15.1 The Business Life Cycle (Slide 153) A firm typically goes through 5 stages in its life cycle: start-up, growth, maturity, decline, and closing. Each stage presents unique problems, opportunities, and funding requirements.

ch_15 financial management: core concepts

Dec 24, 2015

financial management: core concepts by Raymond Brooks. Ch 15 problem solution.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

514

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Chapter 15 Raising Capital LEARNING OBJECTIVES (Slide 15-‐2) 1. Describe the life cycle of a business.

2. Understand the different sources of capital available to a start-up business and to a growing business.

3. Explain the funding available to a stable or mature business. 4. Explain how companies sell bonds in a capital market.

5. Explain how companies sell stocks in a capital market. 6. Examine some special forms of financing: commercial paper and banker’s

acceptance.

7. Describe the options and regulations for closing a business.

IN A NUTSHELL… This chapter is about how entrepreneurs and firms go about raising funds for growth and development. As a firm progresses through the various phases of its business cycle, its needs, focus, and conditions change requiring it to use different sources of capital. Firms typically sell bonds and stock to raise capital and so the author explains the process followed by issuing companies. Besides bonds and stock, firms also borrow short-term funds by issuing commercial paper and bankers’ acceptances. The chapter closes with a discussion of the options and regulations that come into play when a firm decides to cease operations and close permanently.

LECTURE OUTLINE

15.1 The Business Life Cycle (Slide 15-‐3) A firm typically goes through 5 stages in its life cycle: start-up, growth, maturity, decline, and closing.

Each stage presents unique problems, opportunities, and funding requirements.

Chapter 15 n Raising Capital 515

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Business life cycles vary considerably. Some firms go through the early stages fairly rapidly and then settle into maturity for a long time, while others skip to the closing stage in a few years. The US Census Bureau’s Business Information Tracking System estimates that roughly 60% of businesses that employ others besides the owners will close within their first 6 years.

The life cycle approach is a useful way to discuss financing opportunities and sources for businesses.

15.2 Borrowing for a Start-‐up and Growing Business (Slides 15-‐4 to 15-‐12) 5 sources of capital can generally be used to start and grow a business:

1. Personal funds 2. Borrowed funds from family and friends 3. Commercial bank loans 4. Borrowed funds through business start-up programs like the U.S. Small Business

Administration (SBA) 5. Angel financing or venture capital

15.2 (A) Personal Funds and Family Loans: although limited in scope, are often good starting points for most entrepreneurs and sole proprietorships. Professional lenders like commercial banks and venture capitalists view funding by family and friends as a sign that the business has potential. After all, if you can’t convince your family and friends that you have a good business idea, how can you convince a stranger? 15.2 (B) Commercial Bank Loans: constitute the first source that people often seek after they have run out of friends and in-laws to ask. Banks tend to be very conservative lenders often requiring substantial collateral, income history and evidence of stability. Start-ups are rarely directly funded by commercial banks.

15.2 (C) Commercial Bank Loans through the Small Business Association (SBA): are available to qualified small business applicants via a variety of loan programs, the most common of which is the 7(a) Loan Guaranty Program. The 7(a) Loan Guaranty Program administers business loans to individuals or businesses that might not be eligible for a loan through the normal lending agencies. Loan proceeds can be used for working capital and fixed assets, with repayment schedules extending up to 25 years. These loans are delivered through commercial lenders and guaranteed by the SBA.

516 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

The interest rates tend to be quite competitive but the major advantage of this program accrues to the banks since the loans are backed by the SBA.

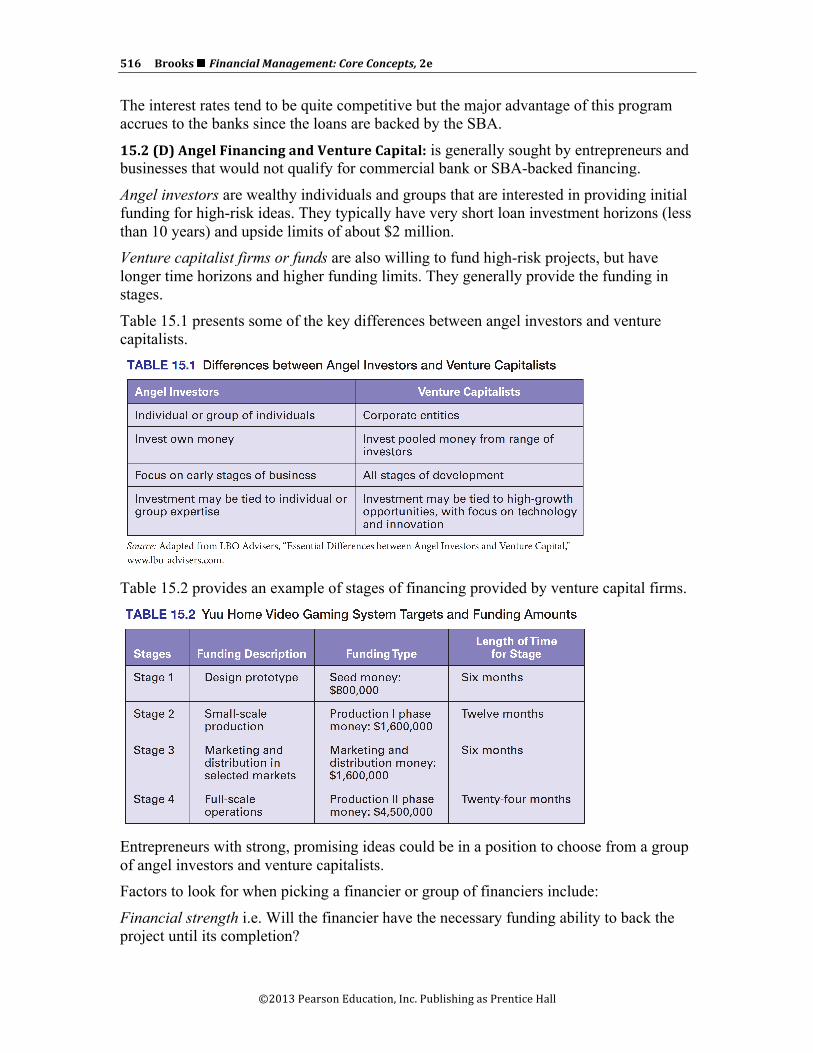

15.2 (D) Angel Financing and Venture Capital: is generally sought by entrepreneurs and businesses that would not qualify for commercial bank or SBA-backed financing.

Angel investors are wealthy individuals and groups that are interested in providing initial funding for high-risk ideas. They typically have very short loan investment horizons (less than 10 years) and upside limits of about $2 million. Venture capitalist firms or funds are also willing to fund high-risk projects, but have longer time horizons and higher funding limits. They generally provide the funding in stages.

Table 15.1 presents some of the key differences between angel investors and venture capitalists.

Table 15.2 provides an example of stages of financing provided by venture capital firms.

Entrepreneurs with strong, promising ideas could be in a position to choose from a group of angel investors and venture capitalists. Factors to look for when picking a financier or group of financiers include:

Financial strength i.e. Will the financier have the necessary funding ability to back the project until its completion?

Chapter 15 n Raising Capital 517

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Contacts: i.e. Can the financier provide valuable contacts to help the entrepreneur reach his or her goal?

Exit strategy: i.e. how much equity is the investor looking to acquire as a condition of providing the funding and how much of control is the entrepreneur willing to give up?

Given that there is a high probability of failure among start-ups, angel investors and financiers commonly look for 60% – 100% potential annual rates of return on their successful ventures in order to provide funding.

Example 1: Expected rate of return for a venture capitalist The Quick Start Funding Group is looking to fund only those projects which have the potential to return $10 million dollars for every $1 million that they have invested within a 5-year period. Calculate the firm’s expected rate of return on its investment. FV = $10 million; PV = 1 million; N=5; CPT I% è58.49%

15.3 Borrowing for a Stable and Mature Business: Bank Loans (Slides 15-‐13 to 15-‐19) Commercial banks provide much of the short-term financing required for the operating needs of a business via straight loans, discount loans, and lines of credit with or without compensating balances. 15.3 (A) Straight loans: represent the simplest of all types of bank loans, and are offered with a quoted APR and pre-set payment amounts and intervals.

Example 2: Calculating payments and EAR of a straight loan The Timken Company wants to borrow $2,000,000 from its local bank. The bank quotes them a rate of 8.25% (APR) on a 5-year loan with payments due monthly. How much will their monthly payment be and what is their EAR? PV = 2,000,000; FV = 0; N=60; i=8.25; P/Y=12;C/Y=12; PMTè40,792.5 EAR = (1 + (.0825/12)12 – 1è8.569%

15.3 (B) Discount Loans: are offered to firms with the interest amount being already subtracted at the start.

The difference between the amount the firm can use and the amount that has to be paid back at the end is the bank’s interest or discount earned.

The loan amount is the amount due at maturity

Example 3: Discount loan Let’s say that a firm needs $500,000 to fund the operations of its new expansion. It approaches a commercial bank, which offers it a discount loan at 9.5% per year which will have to be paid back in full in one payment at the end of twelve months. How much

518 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

will the face value of the loan have to be set at and what rate of interest is the company effectively paying?

Loan amount (face value) = Amount needed/(1-discount rate) è$2m/.9 è$2.209m. Effective rate = discount paid/Amount used è = 209,000/2000000 è10.497%

15.3 (C) Letter of Credit or Line of Credit: is a preapproved borrowing amount that works much like a credit card.

The company can borrow money at a preset rate from bank at any time without seeking additional approval of the loan each time it needs funds.

The bank, however, is compensated based on the outstanding balance of the loan. The compensation can be a fixed interest rate, but often is a floating interest rate tied to a benchmark interest rate. This borrowing style has changing balances and changing interest rates, so it is difficult to state the effective rate on the loan. 15.3 (D) Compensating Balance: loans work like lines of credit except that a portion of the loan is not available to the borrower, even though interest is paid on the full face value of the loan. For example, if a firm takes a loan of $100,000 at a rate of 7.5% per year and a compensating balance requirement of 15%, it will be able to use only $85,000 and be charge $7,500 in interest for the year. The effective rate of interest will therefore be: Effective rate = Interest paid/Amount used è $7,500/$85,000 è8.82%

15.4 Borrowing for a Stable and Mature Business: Selling Bonds (Slides 15-‐20 to 15-‐25) Corporate bonds represent a major source of long-term financing for established companies. Bonds are typically sold in $1,000 units, and publicly auctioned or privately placed.

The public issue of bonds is regulated by the SEC and typically involves the following 5 steps

1. The company selects an investment bank to help design and market the bond. An investment bank is an agent that works with the firm to meet all the listing requirements of the bond issue, the design of the bond terms, the marketing of the bond, and the auction of the bond.

2. The company and investment bank register the bond with the SEC, providing a prospectus and referencing the indenture for the bond

3. The bond is rated by an agency such as Standard & Poor’s or Moody’s to help potential buyers determine an appropriate price for the bond..

4. The investment bank markets the bond to prospective buyers prior to the auction, using the prospectus as the key information on the bond.

Chapter 15 n Raising Capital 519

©2013 Pearson Education, Inc. Publishing as Prentice Hall

5. An auction is conducted to sell the bond. Two key documents that are required during the bond issuance process include the prospectus and the indenture agreement. The prospectus contains much of the information filed in the registration and is used to inform potential buyers about the bond. The indenture agreement is the formal contract for the bond between the issuing company and the eventual buyer. It includes vital information about the bond such as the coupon rate, payment schedule, maturity date, and par value as well as other restrictive covenants i.e. provisions that restrict the activities of the issuing firm to increase the safety of the bond in the eyes of potential buyers.

Firms that issue coupon bonds have to make periodic coupon payments and a large lump sum payment at maturity.

Sinking funds or reserve accounts are often set up by bond issuers to put away funds every year so as to have the necessary funds available to retire the bond when it matures.

Example 4: Bond proceeds The Golden Corral Corporation is in the process of issuing a 30-year, 8% coupon (paid semi-annually) AA1-rated corporate bond with $1000 par value. If by the time the bonds receive SEC clearance, the market yield on this bond goes to 8.35%, and the company sells 3000 of these bonds with the help of an investment banker who charges them a commission rate of 3% on the proceeds, what will the total proceeds be for the issuing company, and what is the cost of these bonds to the firm in terms of the cost of capital? What are the firm’s future cash obligations? P/Y=2;C/Y=2;N=60;PMT=40;FV=1000;I=8.35; PVè$962

Gross proceeds from sale of bonds = 3000*$962=$2,885,058.18 Investment banker’s commission = .03*$2,885,058.18= $86,551.75

Total proceeds received by the issuing company = $2,798, 506.43 Net proceeds per bond = $962*(1-.03) = $932.84 Cost of debt to Golden Corral based on net price:

P/Y=2; C/Y=2; PV=-932.84; N=60;PMT=40;FV=1000;I è9.01% Future cash obligations:

Annual Coupon payments = $40*2*3000 = $240,000 Principal payment at maturity= $1000*3000 = $3,000,000

520 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

15.5 Borrowing for a Stable and Mature Business: Selling Stock (Slides 15-‐26 to 15-‐37) The other major source of capital for a firm to avail of is common stock or equity.

Equity holders get voting rights as part owners and share in the residual profits of the firm. Stocks are sold as initial public offerings (IPOs) when the firm first goes public and seasoned offerings for subsequent issues. 15.5 (A) Initial Public Offerings and Underwriting: Firms sell stock to the public with the help of investment banking firms, who perform due diligence and are experts in marketing the issue.

Investment banks partner with issuing firms in exchange for compensation that can be set up on a best-efforts basis or on a fixed-commitment basis.

Under a best-efforts arrangement the investment bank pledges to use its best efforts to sell all the authorized shares and takes a cut on each individual share sold, but provides no guarantee as to how many shares will be sold. The more shares sold, the higher the payoff to the investment bank.

Under a fixed-commitment arrangement, also known as an underwriting arrangement, the investment banker guarantees a fixed amount of proceeds to the issuer. The investment banker makes up/keeps the difference between the actual selling price and the guaranteed price.

Example 5: Best efforts versus fixed commitment underwriting The Wed Link Inc. wants to raise capital by issuing common stock. They contact a few investment bankers and the one with the best offer has presented them with 2 options: 1) A fixed commitment offer of $8,500,000 2) A best efforts arrangement in which the investment banker will receive $1.50 per

share for every share of stock sold up to $$1,500,000 for the 1,000.000 shares to be offered to the public at $11 per share.

a) If 100% of the shares are sold, what are Wed Link’s proceeds? What is the payment to the investment banking firm under each method of issuing securities?

b) What if 85% of the shares are sold? At what percentage of shares sold are the proceeds to you the same under the two compensation arrangements?

c) At what percentage is the payment to the investment banking firm the same?

a) If 100% of the shares are sold i.e. 1,000,000 shares at $11 per share, to the public, the proceeds are as follows:

1) With the firm commitment arrangement, the issuer gets $8,500,000

The investment banker gets $11,000,000 – $8,500,000 = $2,500,000 2) With the best efforts arrangement, the issuer gets ($11-

$1.50)*1,000,000è$9,500,000

Chapter 15 n Raising Capital 521

©2013 Pearson Education, Inc. Publishing as Prentice Hall

The investment banker gets $1.50*1,000,000è$1,500,000 So, if the issue is 100% sold, the issuer is better off with the best efforts arrangement, while the investment banker would be better off with the fixed commitment arrangement.

b) If 85% of the shares are sold, i.e. 850,000 shares at $11 per share, the proceeds are as follows:

1) With the firm commitment arrangement, the issuer gets $8,500,000

The investment banker gets $9,350,000 – $8,500,000 = $$850,000 2) With the best efforts arrangement, the issuer gets ($11-

$1.50)*850,000è$8,075,000 The investment banker gets $$1.5*850,000è$1,275,000

èSo if the issue is only 85% sold, the issuer is better off with a firm commitment offer while the investment banker would be better off with the best efforts arrangement.

c) Firm commitment offer = best effort $ per share sold $8,500,000 = $9.50*1,000,000 * X% è X% = $8,500,000/$9,500,000 è89.47% So, if 89.47% of the shares are sold, the payment to the investment banking firm will be the same under either arrangement.

15.5 (B) Registration, Prospectus, and Tombstone: All new issues of shares have to be registered with the SEC prior to being sold in the capital markets. Once an application is filed, the approval process could take anywhere from 20 to 40 days (cool-off period.) During the waiting period, the issuer can circulate a preliminary prospectus (red herring) informing potential investors of the issue. No commitments can be obtained from buyers until after SEC approval.

If information is missing, the SEC issues a comment letter, requiring corrections and a new application to be filed.

Once re-filed, the cool-off period starts again. During the waiting period the issuer and investment bank place large advertisements (tombstone ads.) in newspapers and magazines, containing the name of the issuer, some details about the issue, and a list of participating investment banks.

There are 2 exceptions to the usual SEC registration process requirement: 1. If the issue has a maturity of less than 270 days e.g. commercial paper issues.

2. If the issue is worth less than $5 million (Regulation A)

15.5 (C) The Marketing Process: Road Show: involves taking the issue on the road to attract interest among potential investors.

522 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

This process usually last about 2 weeks and enables the investment banker to get a feel for what the price should be set at.

After a successful road show and marketing campaign, a price is set and the issue proceeds forward to be auctioned off in the primary capital market.

15.5 (D) The Auction: takes place on a single trading day, during which time buyers submit their bids at pre-set prices. If over-subscribed, the bids are filled on a pro-rata basis until all the shares are sold. 15.5 (E) The Aftermarket: Dealer in the Shares: After completion of the auction the outstanding shares trade in the secondary market and the investment banker typically functions as a dealer in the stock for a minimum of 18 months, for which the bank is given a “green-shoe provision.” The green shoe provision allows the investment banker the right to purchase up to 15% of additional shares over a thirty-day period beyond that offered to the public during the auction so as to maintain inventory and fill any pent-up demand.

Another standard agreement is a lock-up agreement, which requires the original owners of the firm to maintain their shares of stock for 180 days, so as to prevent dumping of stock and free-fall in its price due to profit-taking on part of the original owners.

15.6 Other Borrowing Options for a Mature Business (Slides 15-‐38 to 15-‐41) Commercial paper and bankers’ acceptances are two other popular financing options used by mature businesses. 15.6 (A) Commercial paper is a discounted note sold by a company directly to an investor with both principal and interest repaid within 270 days just like a treasury bill. These issues typically have a face value of $100,000, putting them out of the reach of most small investors. It is generally assumed institutions and sophisticated investors purchase commercial paper.

The reason firms issue commercial paper over other forms of borrowing is that they can get lower rates than through commercial banks and since they mature within 270 days, they qualify for short-form registration with the SEC.

Example 6: The Large-Scale Industrial Corporation, a large well established company, is about to issue $6,000,000 worth of commercial paper. The paper has a maturity of 9 months (270 days), and commands a price worth 97.5% of par value in the market. The paper will be sold with a face or par value of $100,000. How many commercial papers will be sold? What is the cost of this borrowing to the firm? Proceeds from the issue = Face Value *Discounted Value = $6m*.975=$5.85m

Cost of this borrowing over 270 days = ($6m-$5.85m)/$5.85mè.02564 APR = .02564*365/270 = 0.03466è3.47% EAR = (1.02564)365/270 – 1è3.48%

Chapter 15 n Raising Capital 523

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Number of commercial papers issued = Total Face Value/Par Value of 1 = $6,000,000/$100,000 = 60 papers

15.6 (B) A Bankers’ acceptance is a short-term credit arrangement created by a firm and guaranteed by a bank, and it is ordinarily used to finance inventories or other assets that will be self-liquidated over a relatively short period of time. Its specific purpose is to promote trade. It typically involves an importing firm having its invoice guaranteed (accepted) by a bank and sent over to the exporter as assurance of payment in the next few months (typically 60-90 days). The exporter turns in the banker’s acceptance to his bank in exchange for a reduced payment and in return the bank in the exporting country takes title to the exported goods until payment is received. The importing firm is able to finance its purchases and releases funds as inventory is liquidated.

15.7 The Final Phase: Closing the Business (Slides 15-‐42 to 15-‐46) Sometimes, successful solvent firms decide to cease operations, in which case they sell off their assets, pay off all outstanding debts and expenses, and distribute the residual value to the stockholders. When firms are unsuccessful, they may decide to cease operations, declare bankruptcy, and liquidate their assets; or they may decide to re-organize, attempt to re-establish themselves, and try to re-emerge as stronger firms.

15.7 (A) Straight Liquidation: Chapter 7 of the Federal Bankruptcy Reform Act (1978) deals with the process that has to be followed when a firm decides to close its business and liquidate its assets. Once a firm files for Chapter 7, the bankruptcy court judge appoints a trustee to oversee the process of liquidation, the order of which is as follows:

524 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Note that common stockholders are last on the list and typically get little to nothing of the proceeds from the sale of the remaining assets.

15.7 (B) Reorganization: Chapter 11 is what some firms file for if their managers feel that there is a chance that they could re-structure the firm and be worth more alive than dead. Ina typical re-organization the process is as follows: First, a petition for Chapter 11 is filed by either the company or by a creditor, and a bankruptcy court judge either accepts or denies the petition. If accepted, a date is set by the judge for all claimants to show proof of their claims and for the firm to establish who exactly the claimants are. A reorganization plan is presented to the court and must be approved by a majority of the members of a claimant class. If the claimants cannot agree on the reorganization plan, the judge may issue a ruling on all or parts of a plan and thus “decree” the reorganization plan. If a minority of classes does not agree to the plan, the judge may listen to their objections and alter the reorganization plan. Often, the current managers continue to run the business while it operates under the reorganization plan, but the court may also appoint a trustee to oversee the operations and protect the rights of the claimants during this period of time.

The reorganization plan may allow the issuance of new securities and thus add another set of claimants to the firm.

Old debt may be restructured in terms of both maturity and rates. The plan itself holds off claimants while the company tries to reorganize and come out of bankruptcy as a new operating firm. If a firm fails to make the reorganization plan work, it will probably fall into Chapter 7 bankruptcy.

Questions 1. What are the five stages of a business life cycle? Do all companies go through all

five stages? There are a number of classifications of the business life cycle; here we will use the five active phases of startup, growth, maturity, decline, and closing. Not all companies move through all five phases, some never get past the start-up phase.

2. According to the U.S. Census Bureau’s Business Information Tracking System, what is the failure rate of companies over the first six years? According to the U.S. Census Bureau’s Business Information Tracking System (BITS), three out of every five employer businesses (businesses that employ others besides the owners) will close within their first six years.

3. What is the function of the Small Business Administration in regard to business loans? Who receives the guaranty on the loans?

Chapter 15 n Raising Capital 525

©2013 Pearson Education, Inc. Publishing as Prentice Hall

The 7(a) Loan Guaranty Program administers business loans to individuals or businesses that might not be eligible for a loan through the normal lending agencies. Loan proceeds can be used for working capital and fixed assets, with repayment schedules extending up to 25 years. These loans are delivered through commercial lenders and guaranteed by the SBA. The lending institution gets the guarantee not the borrower.

4. What is the difference between an angel investor and a venture capitalist? What event do these investors want to see happen? Why? Angel investors are lenders who provide funding for new, high-risk ideas. The term does not refer to a well-defined set of lenders but rather is a generic term applied to individuals or groups that seek to support new start-up business ventures. As such, an angel financier is usually a wealthy individual. Like angel investors, venture capitalists are not a well defined group of lenders, but rather a general term applied to groups or institutions that provide funding at a level higher (larger loans) than that of most angel investors. Both these lenders want to see a liquidity event where they are repaid their initial investment plus a large profit.

5. What is a letter of credit or line of credit? How does it work? A letter of credit or line of credit is a preapproved borrowing amount that works much like a credit card. The company can borrow money at a preset rate from the bank at any time without seeking additional approval of the loan each time it needs funds.

6. What is the role of an investment bank in selling bonds? An investment bank is an agent that works with the firm to meet all the listing requirements of the bond issue, the design of the bond terms, the marketing of the bond, and the auction of the bond.

7. What is the role of an investment bank in selling stock? The investment bank becomes a partner of the company as it guides the company through the selling process. As part of their role as a partner in the process, investment banks are required to perform due diligence in making sure that all information released during the process is accurate and that all material information has been released. Failing to perform this due diligence task puts the investment bank and the company at risk for litigation after the sale of the stock.

8. What is commercial paper? Why does it not need SEC approval? As its name implies, commercial paper is issued for commercial purposes; it is a discounted note sold by a company directly to an investor with both principal and interest repaid within 270 days. Because the standard face value of commercial paper is typically $100,000, it is out of the reach of most small investors. One of the exceptions to the requirement of registering with the SEC is if the maturity of the issue is less than nine months, or 270 days.

9. Banker’s acceptance supports lending for what type of activities? Explain how collateral works in a banker’s acceptance arrangement. A banker’s acceptance is a short-term credit investment created by a firm and guaranteed by a bank, and is ordinarily used to finance inventories or other assets that will be self-liquidated over a relatively short period of time. Its specific purpose is to promote trade. As inventories are sold, the banker’s acceptance is repaid.

526 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

10. What is the difference between Chapter 7 and Chapter 11 bankruptcies? Why might Chapter 11 be better for claimants than Chapter 7? Chapter 7 of the Federal Bankruptcy Reform Act of 1978 deals with straight liquidation – the selling off of the assets of the firm. In Chapter 7 filings, the company is ceasing all business operations, and the final act of selling off all remaining assets and distributing these proceeds to the legal claimants is governed by a bankruptcy court. A Chapter 11 filing entails reorganization of a company’s business affairs and restructuring of its debt. The company in effect asks the court to step between it and its legal claimants in order to provide the company with an opportunity to work out its financial difficulties without the claimants taking action. Chapter 11 is for a specific time period only and is not a permanent solution to the financial difficulties of a company.

Prepping for Exams 1. c

2. d

3. c 4. c

5. d 6. c

7. a 8. b

9. c 10. b

Problems 1. Venture capital required rate of return. Blue Angel Investors has a success ratio of

10% with its venture funding. Blue Angel requires a rate of return of 20% for its portfolio of lending, and the average length on its loan is five years. If you were to apply to Blue Angel for a $100,000 loan, what is the annual percentage rate you would be required to pay for this loan?

ANSWER Your loan rate means that if one out of ten succeed you need to cover the nine failures after five years, so if Blue Angel makes 10 loans of $100,000 each, i.e. $1,000,000 and requires a return of 20% on its lending portfolio, it will have to accumulate the following amount after 5 years: $1,000,000 × (1.20)5 = $2,488,320. So given a success rate of 1 out of 10 loans, it will charge you the following rate è ($2,488,320 / $100,000)1/5 – 1 = 0.901872 or 90.1872%

Chapter 15 n Raising Capital 527

©2013 Pearson Education, Inc. Publishing as Prentice Hall

2. Venture capital required rate of return. Red Devil Investors has a success rate of one project for every four funded. Red Devil has an average loan period of two years and requires a portfolio return of 25%. If you borrow from Red Devil, what is your annual cost of capital?

ANSWER Hint, do this on a per dollar borrowed basis per project funded.

Your loan rate means that if one out of four succeed you need to cover the three failures after two years: $4 × (1.25)2 = $6.25 Your rate is ($6.25 / $1)1/2 – 1 = 1.50 or 150%

3. Straight bank loan. Left Bank has a standing rate of 8% (APR) for all bank loans, and requires monthly payments. What is a monthly payment if a loan is for (a) $100,000 for five years, (b) $250,000 for ten years, or (c) $1,000,000 for 25 years? What is the effective annual rate of each of these loans?

ANSWER For $100,000 over five years

Mode: P/Y = 12, C/Y =12 Input 60 8.0 -100,000 0 Keys N I/Y PV PMT FV CPT $2,027.64

For $250,000 over ten years Mode: P/Y = 12, C/Y =12 Input 120 8.0 -250,000 0 Keys N I/Y PV PMT FV CPT $3,033.19

For $1,000,000 over twenty five years

Mode: P/Y = 12, C/Y =12 Input 300 8.0 -1,000,000 0 Keys N I/Y PV PMT FV CPT $7,718.16

The EAR for all three loans is: EAR = (1 + 0.08/12)12 – 1 = 8.299%

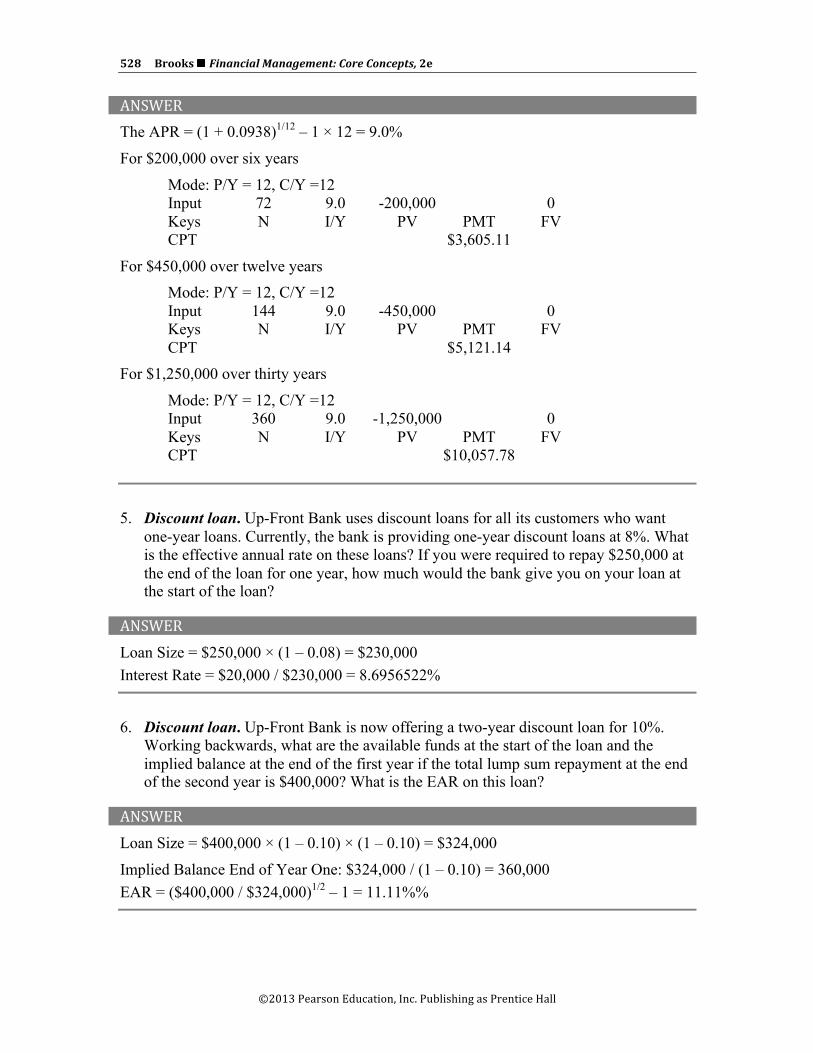

4. Straight bank loan. Right Bank offers EAR loans of 9.38% and requires a monthly payment on all loans. What is the APR for these monthly loans? What is the monthly payment for (a) a loan of $200,000 for six years, (b) a loan of $450,000 for twelve years, or (c) a loan of $1,250,000 for thirty years?

528 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

ANSWER The APR = (1 + 0.0938)1/12 – 1 × 12 = 9.0%

For $200,000 over six years

Mode: P/Y = 12, C/Y =12 Input 72 9.0 -200,000 0 Keys N I/Y PV PMT FV CPT $3,605.11

For $450,000 over twelve years Mode: P/Y = 12, C/Y =12 Input 144 9.0 -450,000 0 Keys N I/Y PV PMT FV CPT $5,121.14

For $1,250,000 over thirty years

Mode: P/Y = 12, C/Y =12 Input 360 9.0 -1,250,000 0 Keys N I/Y PV PMT FV CPT $10,057.78

5. Discount loan. Up-Front Bank uses discount loans for all its customers who want one-year loans. Currently, the bank is providing one-year discount loans at 8%. What is the effective annual rate on these loans? If you were required to repay $250,000 at the end of the loan for one year, how much would the bank give you on your loan at the start of the loan?

ANSWER Loan Size = $250,000 × (1 – 0.08) = $230,000 Interest Rate = $20,000 / $230,000 = 8.6956522%

6. Discount loan. Up-Front Bank is now offering a two-year discount loan for 10%. Working backwards, what are the available funds at the start of the loan and the implied balance at the end of the first year if the total lump sum repayment at the end of the second year is $400,000? What is the EAR on this loan?

ANSWER Loan Size = $400,000 × (1 – 0.10) × (1 – 0.10) = $324,000

Implied Balance End of Year One: $324,000 / (1 – 0.10) = 360,000 EAR = ($400,000 / $324,000)1/2 – 1 = 11.11%%

Chapter 15 n Raising Capital 529

©2013 Pearson Education, Inc. Publishing as Prentice Hall

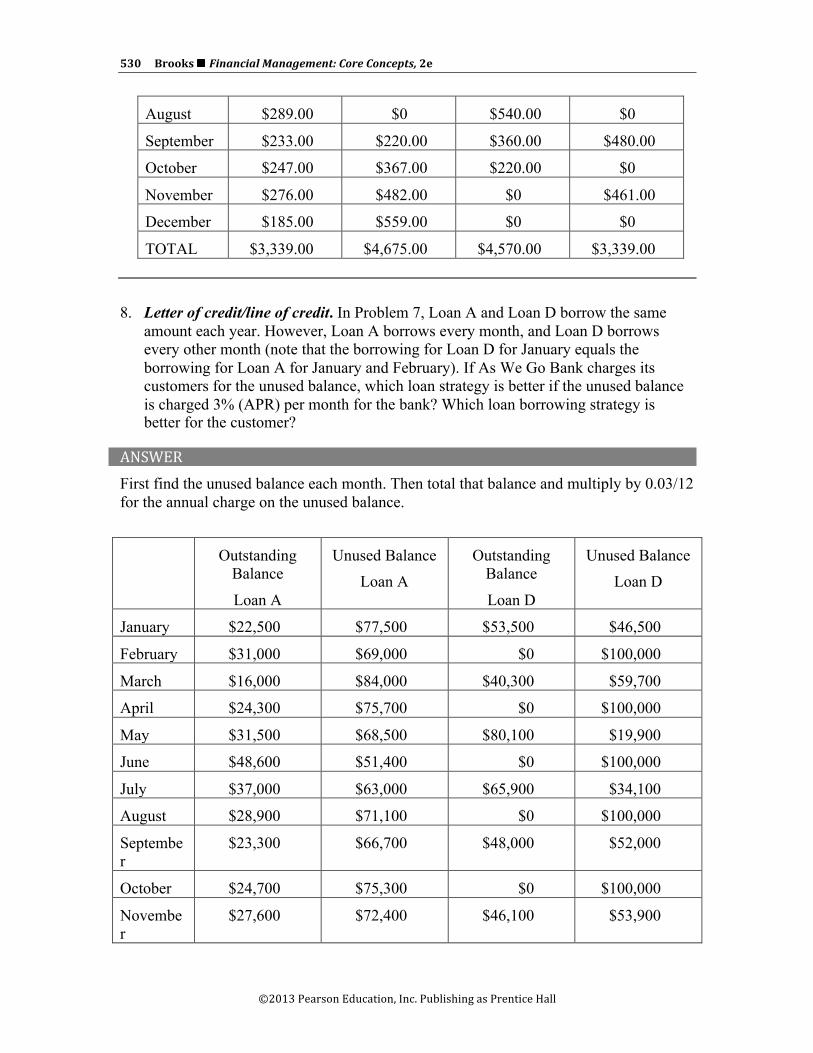

7. Letter of credit/line of credit. As We Go Bank offers its customers a line of credit loan in which each month’s outstanding balance requires a 12% (APR). What are the monthly interest payments required on the following loans and total interest paid for the year on these loans with a $100,000 credit line?

Outstanding Balance

Loan A

Outstanding Balance

Loan B

Outstanding Balance

Loan C

Outstanding Balance

Loan D

January $22,500 $68,000 $0 $53,500

February $31,000 $82,500 $0 $0

March $16,000 $96,000 $0 $40,300

April $24,300 $45,000 $98,000 $0

May $31,500 $13,200 $92,000 $80,100

June $48,600 $0 $95,000 $0

July $37,000 $0 $60,000 $65,900

August $28,900 $0 $54,000 $0

September $23,300 $22,000 $36,000 $48,000

October $24,700 $36,700 $22,000 $0

November $27,600 $48,200 $0 $46,100

December $18,500 $55,900 $0 $0

ANSWER Multiply each balance at the end of each month by 12% / 12 or 1% for that month’s interest:

Example: Loan A for January is $22,500 × 0.01 = $225.00

Interest Loan A

Interest Loan B

Interest Loan C

Interest Loan D

January $225.00 $680.00 $0 $535.00

February $310.00 $825.00 $0 $0

March $160.00 $960.00 $0 $403.00

April $243.00 $450.00 $980.00 $0

May $315.00 $132.00 $920.00 $801.00

June $486.00 $0 $950.00 $0

July $370.00 $0 $600.00 $659.00

530 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

August $289.00 $0 $540.00 $0

September $233.00 $220.00 $360.00 $480.00

October $247.00 $367.00 $220.00 $0

November $276.00 $482.00 $0 $461.00

December $185.00 $559.00 $0 $0

TOTAL $3,339.00 $4,675.00 $4,570.00 $3,339.00

8. Letter of credit/line of credit. In Problem 7, Loan A and Loan D borrow the same amount each year. However, Loan A borrows every month, and Loan D borrows every other month (note that the borrowing for Loan D for January equals the borrowing for Loan A for January and February). If As We Go Bank charges its customers for the unused balance, which loan strategy is better if the unused balance is charged 3% (APR) per month for the bank? Which loan borrowing strategy is better for the customer?

ANSWER First find the unused balance each month. Then total that balance and multiply by 0.03/12 for the annual charge on the unused balance.

Outstanding Balance

Loan A

Unused Balance Loan A

Outstanding Balance

Loan D

Unused Balance Loan D

January $22,500 $77,500 $53,500 $46,500

February $31,000 $69,000 $0 $100,000

March $16,000 $84,000 $40,300 $59,700

April $24,300 $75,700 $0 $100,000

May $31,500 $68,500 $80,100 $19,900

June $48,600 $51,400 $0 $100,000

July $37,000 $63,000 $65,900 $34,100

August $28,900 $71,100 $0 $100,000

September

$23,300 $66,700 $48,000 $52,000

October $24,700 $75,300 $0 $100,000

November

$27,600 $72,400 $46,100 $53,900

Chapter 15 n Raising Capital 531

©2013 Pearson Education, Inc. Publishing as Prentice Hall

December $18,500 $81,500 $0 $100,000

TOTAL $333,900 $856,100 $333,900 $866,100

Interest charge

$3,339.00 $2,140.25 $3,339.00 $2,165.25

Monthly borrowing under Option A is charged slightly less interest due to its lower overall unused balance of $10,000.

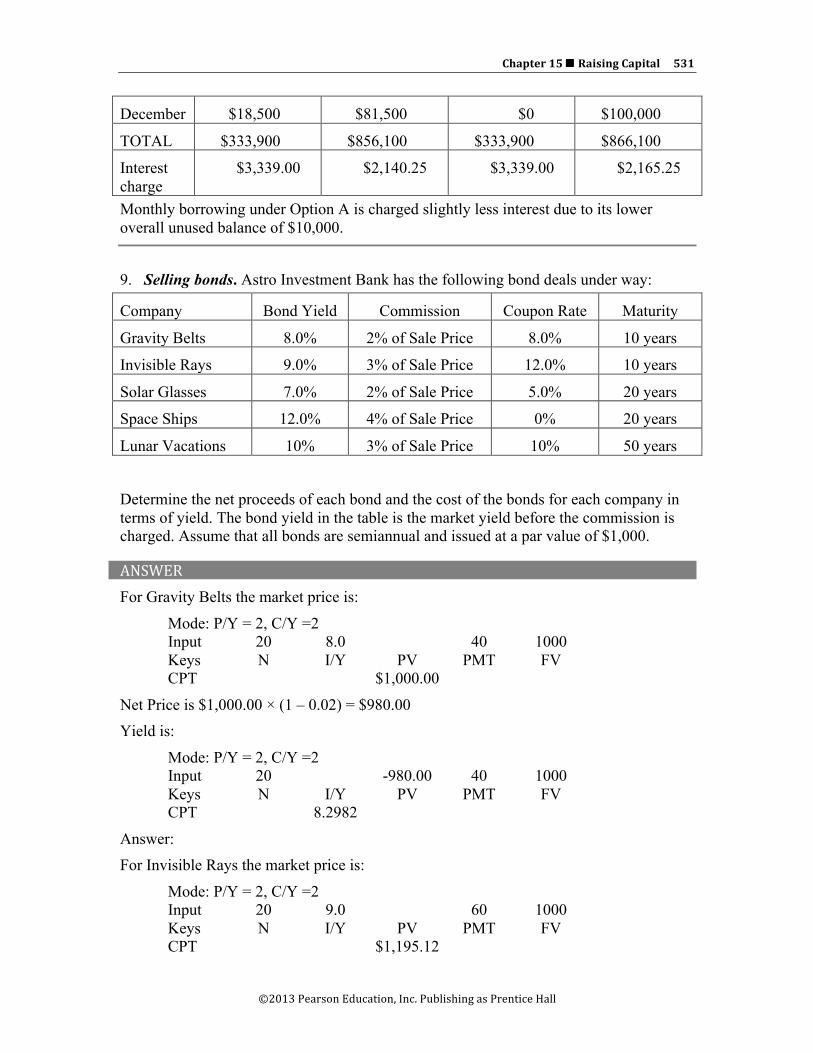

9. Selling bonds. Astro Investment Bank has the following bond deals under way:

Company Bond Yield Commission Coupon Rate Maturity

Gravity Belts 8.0% 2% of Sale Price 8.0% 10 years

Invisible Rays 9.0% 3% of Sale Price 12.0% 10 years

Solar Glasses 7.0% 2% of Sale Price 5.0% 20 years

Space Ships 12.0% 4% of Sale Price 0% 20 years

Lunar Vacations 10% 3% of Sale Price 10% 50 years

Determine the net proceeds of each bond and the cost of the bonds for each company in terms of yield. The bond yield in the table is the market yield before the commission is charged. Assume that all bonds are semiannual and issued at a par value of $1,000.

ANSWER For Gravity Belts the market price is:

Mode: P/Y = 2, C/Y =2 Input 20 8.0 40 1000 Keys N I/Y PV PMT FV CPT $1,000.00

Net Price is $1,000.00 × (1 – 0.02) = $980.00 Yield is:

Mode: P/Y = 2, C/Y =2 Input 20 -980.00 40 1000 Keys N I/Y PV PMT FV CPT 8.2982

Answer: For Invisible Rays the market price is:

Mode: P/Y = 2, C/Y =2 Input 20 9.0 60 1000 Keys N I/Y PV PMT FV CPT $1,195.12

532 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

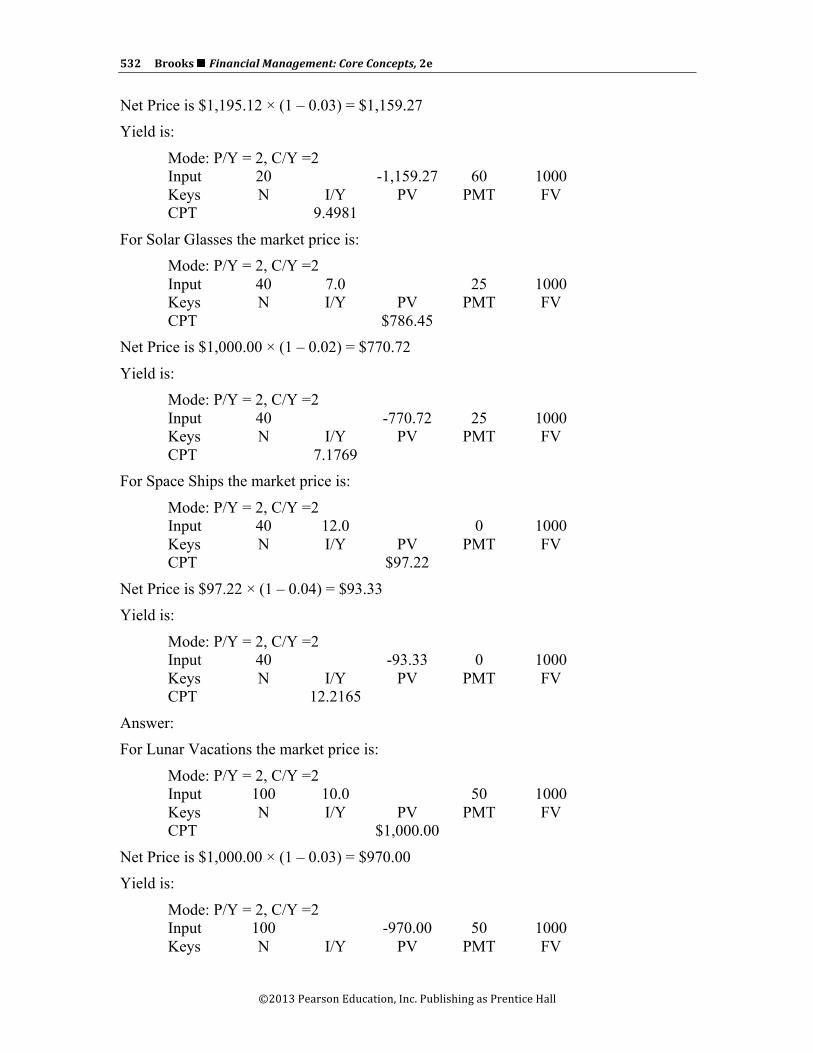

Net Price is $1,195.12 × (1 – 0.03) = $1,159.27 Yield is:

Mode: P/Y = 2, C/Y =2 Input 20 -1,159.27 60 1000 Keys N I/Y PV PMT FV CPT 9.4981

For Solar Glasses the market price is: Mode: P/Y = 2, C/Y =2 Input 40 7.0 25 1000 Keys N I/Y PV PMT FV CPT $786.45

Net Price is $1,000.00 × (1 – 0.02) = $770.72

Yield is: Mode: P/Y = 2, C/Y =2 Input 40 -770.72 25 1000 Keys N I/Y PV PMT FV CPT 7.1769

For Space Ships the market price is:

Mode: P/Y = 2, C/Y =2 Input 40 12.0 0 1000 Keys N I/Y PV PMT FV CPT $97.22

Net Price is $97.22 × (1 – 0.04) = $93.33 Yield is:

Mode: P/Y = 2, C/Y =2 Input 40 -93.33 0 1000 Keys N I/Y PV PMT FV CPT 12.2165

Answer: For Lunar Vacations the market price is:

Mode: P/Y = 2, C/Y =2 Input 100 10.0 50 1000 Keys N I/Y PV PMT FV CPT $1,000.00

Net Price is $1,000.00 × (1 – 0.03) = $970.00 Yield is:

Mode: P/Y = 2, C/Y =2 Input 100 -970.00 50 1000 Keys N I/Y PV PMT FV

Chapter 15 n Raising Capital 533

©2013 Pearson Education, Inc. Publishing as Prentice Hall

CPT 10.3114

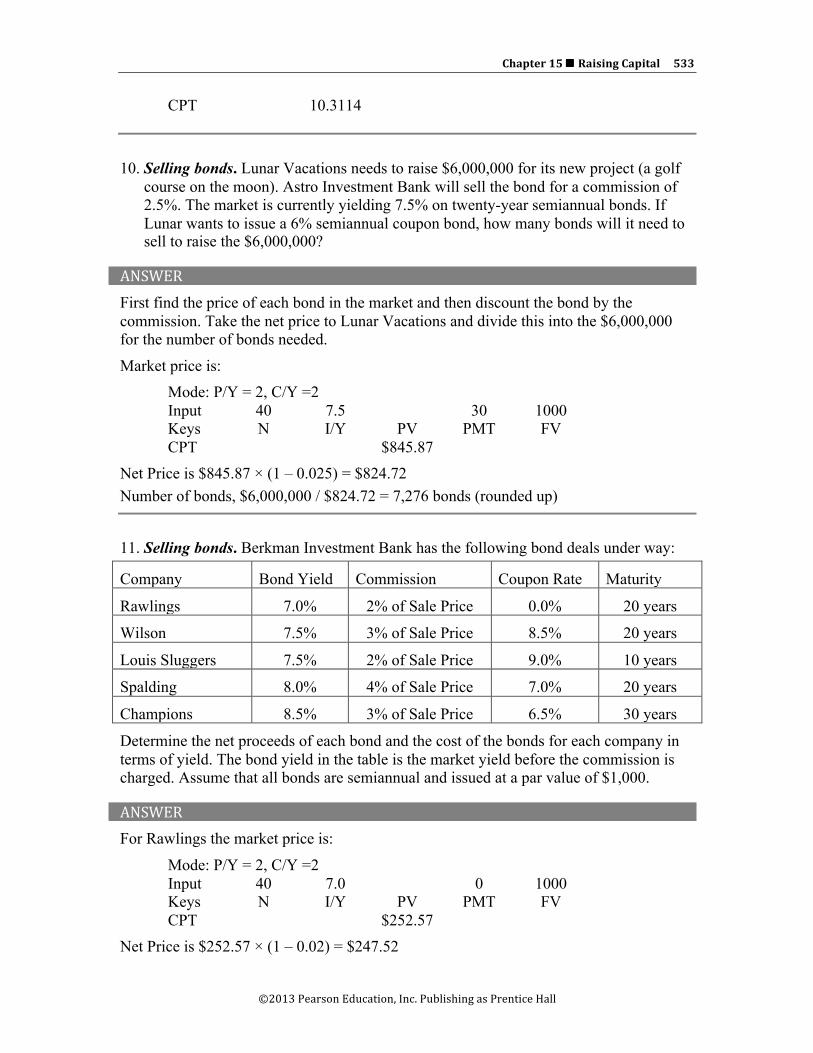

10. Selling bonds. Lunar Vacations needs to raise $6,000,000 for its new project (a golf course on the moon). Astro Investment Bank will sell the bond for a commission of 2.5%. The market is currently yielding 7.5% on twenty-year semiannual bonds. If Lunar wants to issue a 6% semiannual coupon bond, how many bonds will it need to sell to raise the $6,000,000?

ANSWER First find the price of each bond in the market and then discount the bond by the commission. Take the net price to Lunar Vacations and divide this into the $6,000,000 for the number of bonds needed.

Market price is: Mode: P/Y = 2, C/Y =2 Input 40 7.5 30 1000 Keys N I/Y PV PMT FV CPT $845.87

Net Price is $845.87 × (1 – 0.025) = $824.72 Number of bonds, $6,000,000 / $824.72 = 7,276 bonds (rounded up)

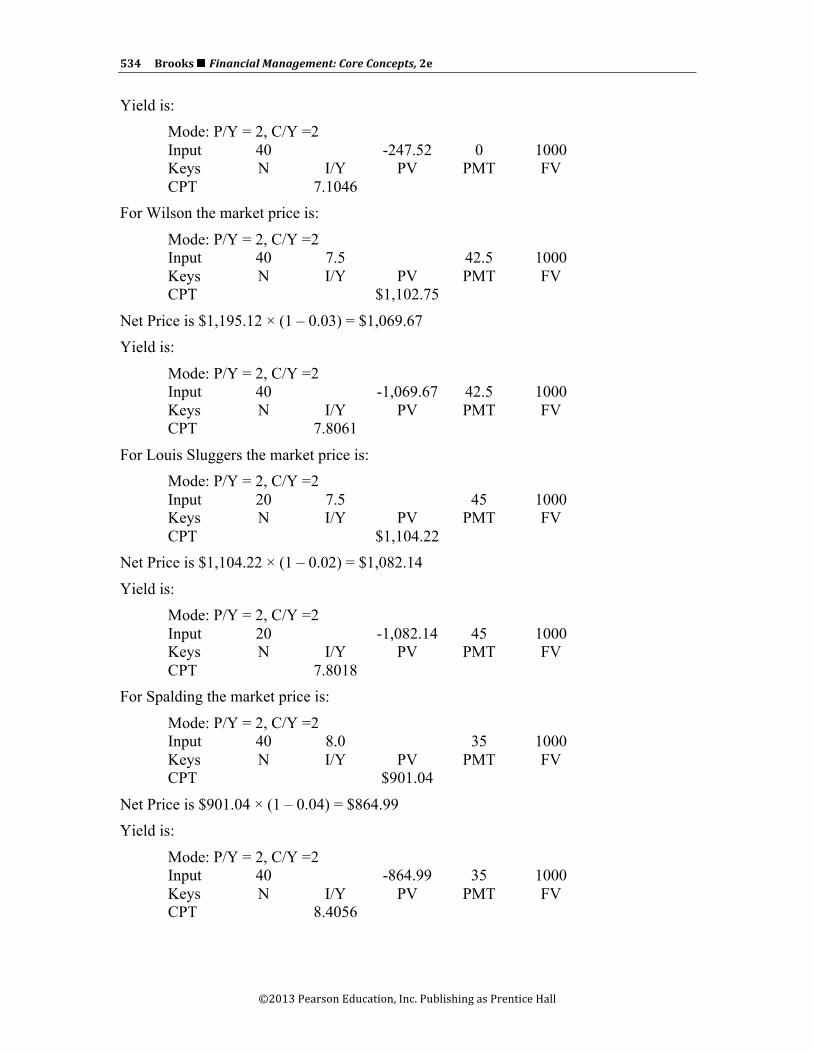

11. Selling bonds. Berkman Investment Bank has the following bond deals under way:

Company Bond Yield Commission Coupon Rate Maturity

Rawlings 7.0% 2% of Sale Price 0.0% 20 years

Wilson 7.5% 3% of Sale Price 8.5% 20 years

Louis Sluggers 7.5% 2% of Sale Price 9.0% 10 years

Spalding 8.0% 4% of Sale Price 7.0% 20 years

Champions 8.5% 3% of Sale Price 6.5% 30 years

Determine the net proceeds of each bond and the cost of the bonds for each company in terms of yield. The bond yield in the table is the market yield before the commission is charged. Assume that all bonds are semiannual and issued at a par value of $1,000.

ANSWER For Rawlings the market price is:

Mode: P/Y = 2, C/Y =2 Input 40 7.0 0 1000 Keys N I/Y PV PMT FV CPT $252.57

Net Price is $252.57 × (1 – 0.02) = $247.52

534 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Yield is: Mode: P/Y = 2, C/Y =2 Input 40 -247.52 0 1000 Keys N I/Y PV PMT FV CPT 7.1046

For Wilson the market price is:

Mode: P/Y = 2, C/Y =2 Input 40 7.5 42.5 1000 Keys N I/Y PV PMT FV CPT $1,102.75

Net Price is $1,195.12 × (1 – 0.03) = $1,069.67 Yield is:

Mode: P/Y = 2, C/Y =2 Input 40 -1,069.67 42.5 1000 Keys N I/Y PV PMT FV CPT 7.8061

For Louis Sluggers the market price is: Mode: P/Y = 2, C/Y =2 Input 20 7.5 45 1000 Keys N I/Y PV PMT FV CPT $1,104.22

Net Price is $1,104.22 × (1 – 0.02) = $1,082.14

Yield is: Mode: P/Y = 2, C/Y =2 Input 20 -1,082.14 45 1000 Keys N I/Y PV PMT FV CPT 7.8018

For Spalding the market price is:

Mode: P/Y = 2, C/Y =2 Input 40 8.0 35 1000 Keys N I/Y PV PMT FV CPT $901.04

Net Price is $901.04 × (1 – 0.04) = $864.99 Yield is:

Mode: P/Y = 2, C/Y =2 Input 40 -864.99 35 1000 Keys N I/Y PV PMT FV CPT 8.4056

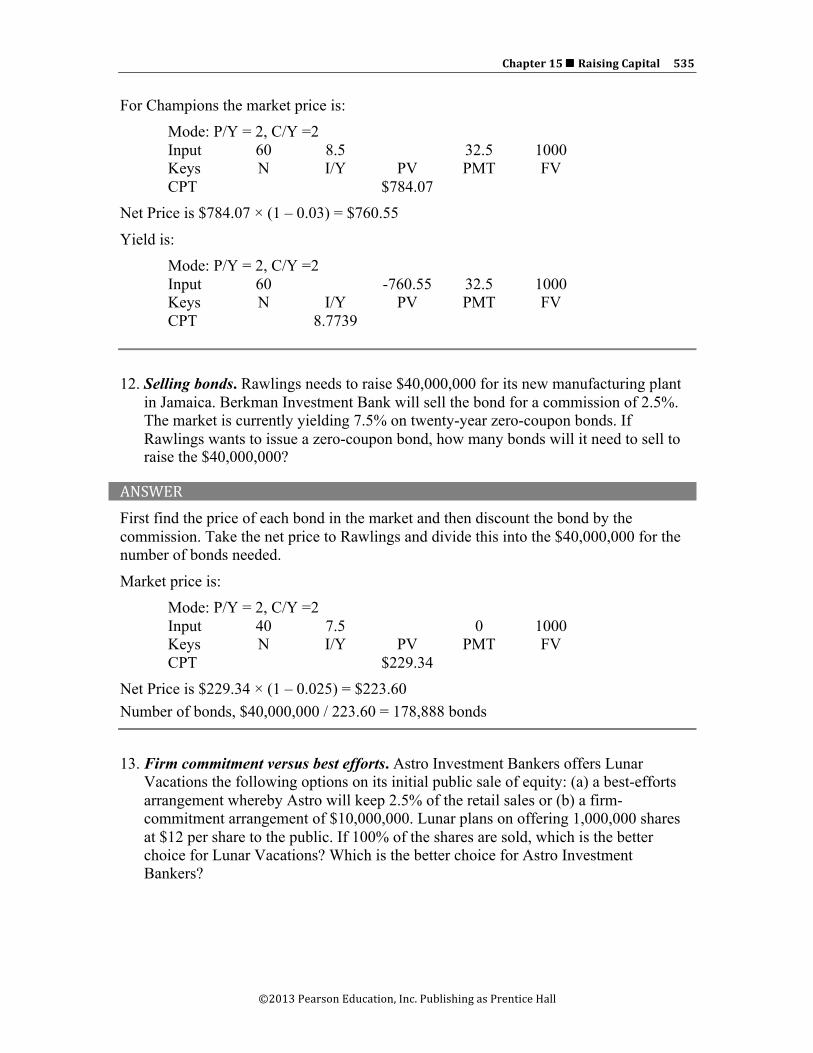

Chapter 15 n Raising Capital 535

©2013 Pearson Education, Inc. Publishing as Prentice Hall

For Champions the market price is: Mode: P/Y = 2, C/Y =2 Input 60 8.5 32.5 1000 Keys N I/Y PV PMT FV CPT $784.07

Net Price is $784.07 × (1 – 0.03) = $760.55

Yield is: Mode: P/Y = 2, C/Y =2 Input 60 -760.55 32.5 1000 Keys N I/Y PV PMT FV CPT 8.7739

12. Selling bonds. Rawlings needs to raise $40,000,000 for its new manufacturing plant in Jamaica. Berkman Investment Bank will sell the bond for a commission of 2.5%. The market is currently yielding 7.5% on twenty-year zero-coupon bonds. If Rawlings wants to issue a zero-coupon bond, how many bonds will it need to sell to raise the $40,000,000?

ANSWER First find the price of each bond in the market and then discount the bond by the commission. Take the net price to Rawlings and divide this into the $40,000,000 for the number of bonds needed.

Market price is: Mode: P/Y = 2, C/Y =2 Input 40 7.5 0 1000 Keys N I/Y PV PMT FV CPT $229.34

Net Price is $229.34 × (1 – 0.025) = $223.60 Number of bonds, $40,000,000 / 223.60 = 178,888 bonds

13. Firm commitment versus best efforts. Astro Investment Bankers offers Lunar Vacations the following options on its initial public sale of equity: (a) a best-efforts arrangement whereby Astro will keep 2.5% of the retail sales or (b) a firm-commitment arrangement of $10,000,000. Lunar plans on offering 1,000,000 shares at $12 per share to the public. If 100% of the shares are sold, which is the better choice for Lunar Vacations? Which is the better choice for Astro Investment Bankers?

536 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

ANSWER Proceeds for Lunar Vacations under each type of sales agreement:

Best Efforts 1,000,000 × $12 × (1 – 0.025) = $11,700,000

Firm Commitment $10,000,000 Best choice for Lunar Vacations is Best Efforts

Proceeds for Astro Investments under each type of sales agreement: Best Efforts 1,000,000 × $12 × (0.025) = $300,000

Firm Commitment 1,000,000 × $12 – $10,000,000 = $2,000,000 Best choice for Astro Investments is Firm Commitment

14. Firm commitment versus best efforts. Using the information in Problem 13, what is the break-even sales percentage for Lunar Vacations? What are the proceeds to Lunar Vacations and Astro Investment Bankers at the break-even sales percentage?

ANSWER Sales Units × $12 (1 – 0.025) = $10,000,000

Sales Units = $10,000,000 / $11.70 = 854,700 shares Best Efforts at 854,700 shares

To Lunar Vacations: 854,700 × $12 × (1 – 0.025) = $10,000,000 To Astro Investment: 854,700 × ($12 – $11.70) = $256,410

Firm Commitment at 854,000 sales: To Lunar Vacations: $10,000,000 To Astro Investments: 854,700 × $12 – $10,000,000 = $256,410

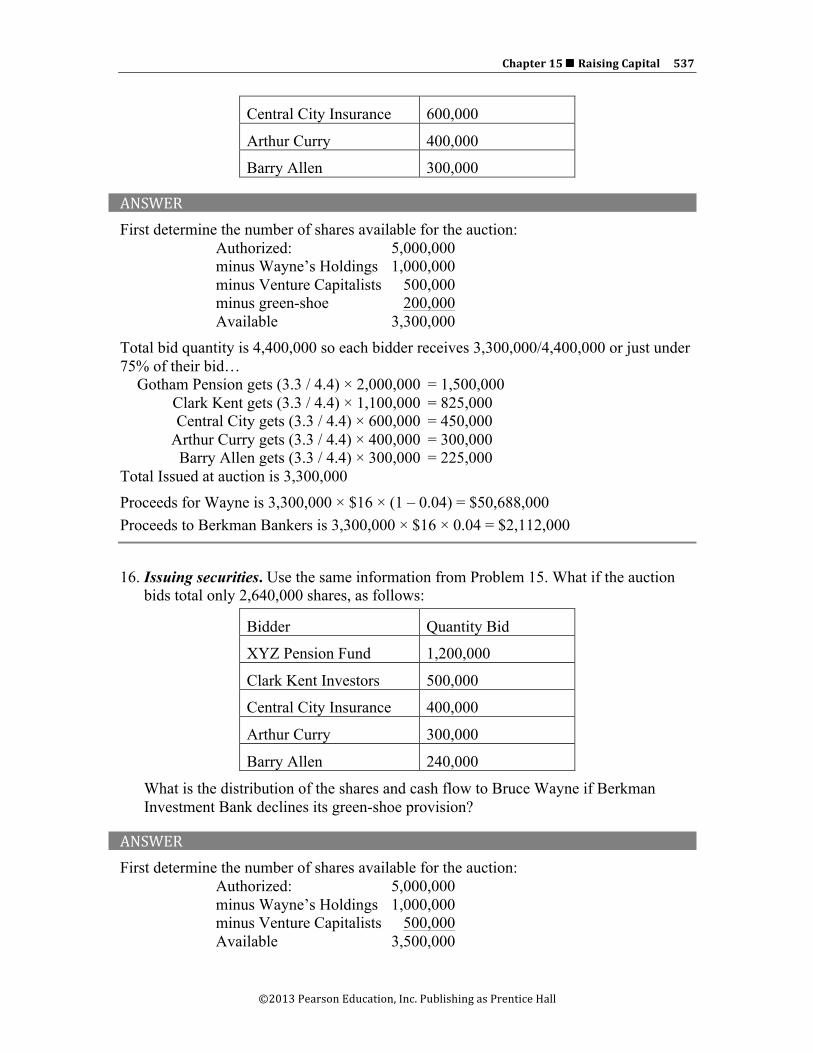

15. Issuing securities. Bruce Wayne is going public with his new business. Berkman Investment Bank will be his banker and is doing a best-efforts sale with a 4% commission fee. Wayne has been authorized 5,000,000 shares for this issue. He plans on keeping 1,000,000 shares for himself, holding back an additional 200,000 shares for a green-shoe provision for Berkman Bank, paying off Venture Capitalists with 500,000 shares, and selling the remaining shares at $16 a share. Given the following bids at the auction, distribute the shares to all bidders using a pro-rata share procedure and assume Berkman Bankers takes its green-shoe provision. What is the total cash flow to Wayne after the sale? To Berkman Bankers?

Bidder Quantity Bid

Gotham Pension Fund 2,000,000

Clark Kent Investors 1,100,000

Chapter 15 n Raising Capital 537

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Central City Insurance 600,000

Arthur Curry 400,000

Barry Allen 300,000

ANSWER First determine the number of shares available for the auction: Authorized: 5,000,000 minus Wayne’s Holdings 1,000,000 minus Venture Capitalists 500,000 minus green-shoe 200,000 Available 3,300,000 Total bid quantity is 4,400,000 so each bidder receives 3,300,000/4,400,000 or just under 75% of their bid… Gotham Pension gets (3.3 / 4.4) × 2,000,000 = 1,500,000 Clark Kent gets (3.3 / 4.4) × 1,100,000 = 825,000 Central City gets (3.3 / 4.4) × 600,000 = 450,000 Arthur Curry gets (3.3 / 4.4) × 400,000 = 300,000 Barry Allen gets (3.3 / 4.4) × 300,000 = 225,000 Total Issued at auction is 3,300,000 Proceeds for Wayne is 3,300,000 × $16 × (1 – 0.04) = $50,688,000 Proceeds to Berkman Bankers is 3,300,000 × $16 × 0.04 = $2,112,000

16. Issuing securities. Use the same information from Problem 15. What if the auction bids total only 2,640,000 shares, as follows:

Bidder Quantity Bid

XYZ Pension Fund 1,200,000

Clark Kent Investors 500,000

Central City Insurance 400,000

Arthur Curry 300,000

Barry Allen 240,000

What is the distribution of the shares and cash flow to Bruce Wayne if Berkman Investment Bank declines its green-shoe provision?

ANSWER First determine the number of shares available for the auction: Authorized: 5,000,000 minus Wayne’s Holdings 1,000,000 minus Venture Capitalists 500,000 Available 3,500,000

538 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Total bid quantity is only 2,640,000 so each bidder receives their entire bid. XYZ Pension gets 1,200,000 Clark Kent gets 500,000 Central City gets 400,000 Arthur Curry gets 300,000 Barry Allen gets 240,000

Total Issued at auction is 2,640,000 and Bruce Wayne (the company) keeps the remaining shares (3,500,000 – 2,640,000 = 860,000) as authorized but unissued stock.

Proceeds for Wayne is 2,640,000 × $16 × (1 – 0.04) = $40,550,400 Proceeds to Berkman Bankers is 2,640,000 × $16 × 0.04 = $1,689,600

17. Commercial paper. Criss-Cross Manufacturers will issue commercial paper for a short-term cash inflow. The paper is for 91 days, has a face value of $50,000, and is anticipated to sell at 96% of par value. Criss-Cross wants to raise $3,000,000, so what is the cost of this borrowing (annual terms) and how many “papers” will be sold?

ANSWER Selling price is 0.96 × $50,000 = $48,000 The cost of this borrowing is: Three-Month Interest Rate = ($50,000 – $48,000) / $48,000 = 0.041667 Stated annually we have: Annual Percentage Rate = 0.041667 × 4 = 16.67% Effective Annual Rate = (1 + 0.04167)4 – 1 = 17.738%. The total number of “papers” sold will be: Number issued = $3,000,000 / $48,000 = 63(must sell in whole units)

18. Commercial paper. Criss-Cross has decided that it will need to raise more than $3,000,000 in commercial paper (see Problem 17). Criss-Cross must now raise $5,000,000, and the paper will have a maturity of 182 days. If this paper has a maturity value of $50,000 and is selling at an annual interest rate of 9%, what are the proceeds from each paper, that is, what is the discount rate on the commercial paper?

ANSWER Discount rate is the stated annual 9% APR but to determine the 182 rate (six month rate) you need to divide 9% by 2 for the 4.5% or 95.5% of par selling price.

Selling price is $50,000 × (1 – 0.045) = $47,750 Total number of sold is $5,000,000 / $47,750 = 105 (must sell in whole units)

19. Bankruptcy, Chapter 7. Gigantic Furniture is having its annual “Going Out of Business Sale.” If Gigantic Furniture is filing under Chapter 7, will it be back next year for another going out of business sale?

Chapter 15 n Raising Capital 539

©2013 Pearson Education, Inc. Publishing as Prentice Hall

ANSWER: In a word, NO. Chapter 7 bankruptcy is for the selling off of the assets of the firm and ceasing all business operations.

20. Bankruptcy, Chapter 7. A customer and an employee are waiting for payment from Gigantic Furniture after the company has filed for bankruptcy under Chapter 7 of the IRS bankruptcy laws. The employee’s claim against Gigantic Furniture is for $500 for health care benefits that were not paid to the health care carrier during the last month of company operations, plus $300 for the pension plan. The customer’s claim is for $400 for a deposit on a specialty sofa that was never shipped. In what order will the bankruptcy courts pay these claims?

ANSWER The claims will be paid in this order, 1. The $500 health care claim not paid to the health care carrier for used benefits.

2. The sofa deposit of $400. 3. The unfunded pension plan of $300.

540 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

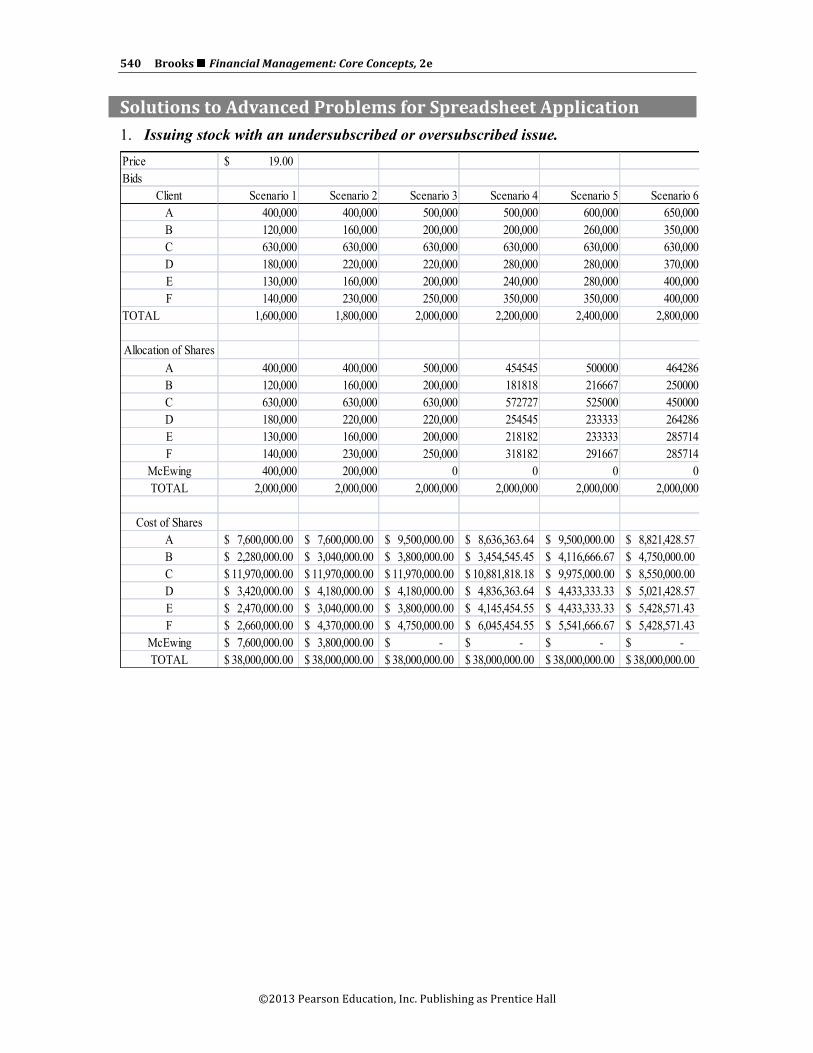

Solutions to Advanced Problems for Spreadsheet Application 1. Issuing stock with an undersubscribed or oversubscribed issue. Price 19.00$ Bids

Client Scenario 1 Scenario 2 Scenario 3 Scenario 4 Scenario 5 Scenario 6A 400,000 400,000 500,000 500,000 600,000 650,000B 120,000 160,000 200,000 200,000 260,000 350,000C 630,000 630,000 630,000 630,000 630,000 630,000D 180,000 220,000 220,000 280,000 280,000 370,000E 130,000 160,000 200,000 240,000 280,000 400,000F 140,000 230,000 250,000 350,000 350,000 400,000

TOTAL 1,600,000 1,800,000 2,000,000 2,200,000 2,400,000 2,800,000

Allocation of SharesA 400,000 400,000 500,000 454545 500000 464286B 120,000 160,000 200,000 181818 216667 250000C 630,000 630,000 630,000 572727 525000 450000D 180,000 220,000 220,000 254545 233333 264286E 130,000 160,000 200,000 218182 233333 285714F 140,000 230,000 250,000 318182 291667 285714

McEwing 400,000 200,000 0 0 0 0TOTAL 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000

Cost of SharesA 7,600,000.00$ 7,600,000.00$ 9,500,000.00$ 8,636,363.64$ 9,500,000.00$ 8,821,428.57$ B 2,280,000.00$ 3,040,000.00$ 3,800,000.00$ 3,454,545.45$ 4,116,666.67$ 4,750,000.00$ C 11,970,000.00$ 11,970,000.00$ 11,970,000.00$ 10,881,818.18$ 9,975,000.00$ 8,550,000.00$ D 3,420,000.00$ 4,180,000.00$ 4,180,000.00$ 4,836,363.64$ 4,433,333.33$ 5,021,428.57$ E 2,470,000.00$ 3,040,000.00$ 3,800,000.00$ 4,145,454.55$ 4,433,333.33$ 5,428,571.43$ F 2,660,000.00$ 4,370,000.00$ 4,750,000.00$ 6,045,454.55$ 5,541,666.67$ 5,428,571.43$

McEwing 7,600,000.00$ 3,800,000.00$ -$ -$ -$ -$ TOTAL 38,000,000.00$ 38,000,000.00$ 38,000,000.00$ 38,000,000.00$ 38,000,000.00$ 38,000,000.00$

Chapter 15 n Raising Capital 541

©2013 Pearson Education, Inc. Publishing as Prentice Hall

2. Firm commitment versus best efforts.

Shares Available4,000,000

Price Per Share

5.50$

Volume3,000,000

3,300,000

3,600,000

3,700,000

3,768,252

3,800,000

Firm CommitmentProceeds To Client

20,000,000$

20,000,000$

20,000,000$

20,000,000$

20,000,000$

20,000,000$

Proceeds from Sale16,500,000

$ 18,150,000

$ 19,800,000

$ 20,350,000

$ 20,725,389

$ 20,900,000

$ Compensation to M

cEwing: Shares Purchased

1,000,000

700,000

400,000

--

- Cost per Share

3.50

2.64

0.50

-

-

-

NET Compensation(3,500,000)

$ (1,850,000)

$ (200,000)

$ 350,000

$ 725,389

$ 900,000

$

Best EffortsVolume

3,000,000

3,300,000

3,600,000

3,700,000

3,768,252

3,800,000

Proceeds To Client15,922,500

$ 17,514,750

$ 19,107,000

$ 19,637,750

$ 20,000,000

$ 20,168,500

$ Compensation to M

cEwing:577,500

$ 635,250

$ 693,000

$ 712,250

$ 725,389

$ 731,500

$ Total Proceeds from Auction

16,500,000$

18,150,000$

19,800,000$

20,350,000$

20,725,389$

20,900,000$

DifferenceBest Efforts vs. Firm CommitmentClient Company

(4,077,500)$

(2,485,250)$

(893,000)$

(362,250)$

-$

168,500$

McEwing Investments Bankers

4,077,500$

2,485,250$

893,000$

362,250$

-$

(168,500)$

Break Even Quantity for McEwing/Client

Volume3768252.5

542 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

$(4,000,000)

$(3,500,000)

$(3,000,000)

$(2,500,000)

$(2,000,000)

$(1,500,000)

$(1,000,000)

$(500,000)

$-‐

$500,000

$1,000,000

$1,500,000

McEwing Firm Commitment

McEwing Best Efforts

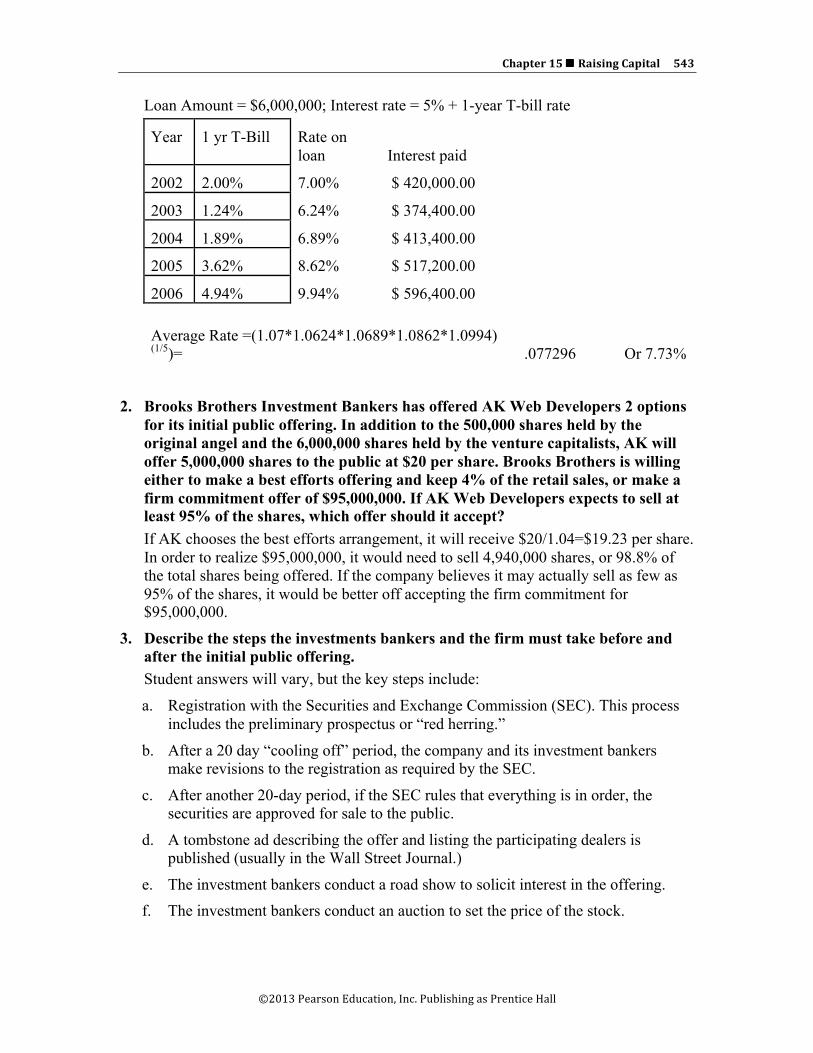

Solutions to Mini-‐Case AK Web Developers.com This case reviews the life cycle of a successful business from angel financing, through the venture capital stage, and IPO liquidity event. It also covers shorter-term borrowing decisions and requires computations to determine the lowest cost of borrowing. 1. The 1-year Treasury bill rates for 2002 through 2006 are given below:

Year

2002 2.00%

2003 1.24%

2004 1.89%

2005 3.62%

2006 4.94%

How much interest did MR Venture Capital receive each year? What was the average interest rate paid by AK Web Developers over the 5-year period?

Chapter 15 n Raising Capital 543

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Loan Amount = $6,000,000; Interest rate = 5% + 1-year T-bill rate

Year 1 yr T-Bill Rate on loan Interest paid

2002 2.00% 7.00% $ 420,000.00

2003 1.24% 6.24% $ 374,400.00

2004 1.89% 6.89% $ 413,400.00

2005 3.62% 8.62% $ 517,200.00

2006 4.94% 9.94% $ 596,400.00

Average Rate =(1.07*1.0624*1.0689*1.0862*1.0994)

(1/5)= .077296 Or 7.73%

2. Brooks Brothers Investment Bankers has offered AK Web Developers 2 options

for its initial public offering. In addition to the 500,000 shares held by the original angel and the 6,000,000 shares held by the venture capitalists, AK will offer 5,000,000 shares to the public at $20 per share. Brooks Brothers is willing either to make a best efforts offering and keep 4% of the retail sales, or make a firm commitment offer of $95,000,000. If AK Web Developers expects to sell at least 95% of the shares, which offer should it accept? If AK chooses the best efforts arrangement, it will receive $20/1.04=$19.23 per share. In order to realize $95,000,000, it would need to sell 4,940,000 shares, or 98.8% of the total shares being offered. If the company believes it may actually sell as few as 95% of the shares, it would be better off accepting the firm commitment for $95,000,000.

3. Describe the steps the investments bankers and the firm must take before and after the initial public offering. Student answers will vary, but the key steps include:

a. Registration with the Securities and Exchange Commission (SEC). This process includes the preliminary prospectus or “red herring.”

b. After a 20 day “cooling off” period, the company and its investment bankers make revisions to the registration as required by the SEC.

c. After another 20-day period, if the SEC rules that everything is in order, the securities are approved for sale to the public.

d. A tombstone ad describing the offer and listing the participating dealers is published (usually in the Wall Street Journal.)

e. The investment bankers conduct a road show to solicit interest in the offering. f. The investment bankers conduct an auction to set the price of the stock.

544 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

g. Trading begins on NASDAQ. The investment bankers serve as dealers. A “green shoe” provision is often included to allow the dealer to meet demand for the shares.

h. After a “lock-up” period of 180 days, insiders -- including the angel, venture capitalists, and company officers -- may begin to trade their shares.

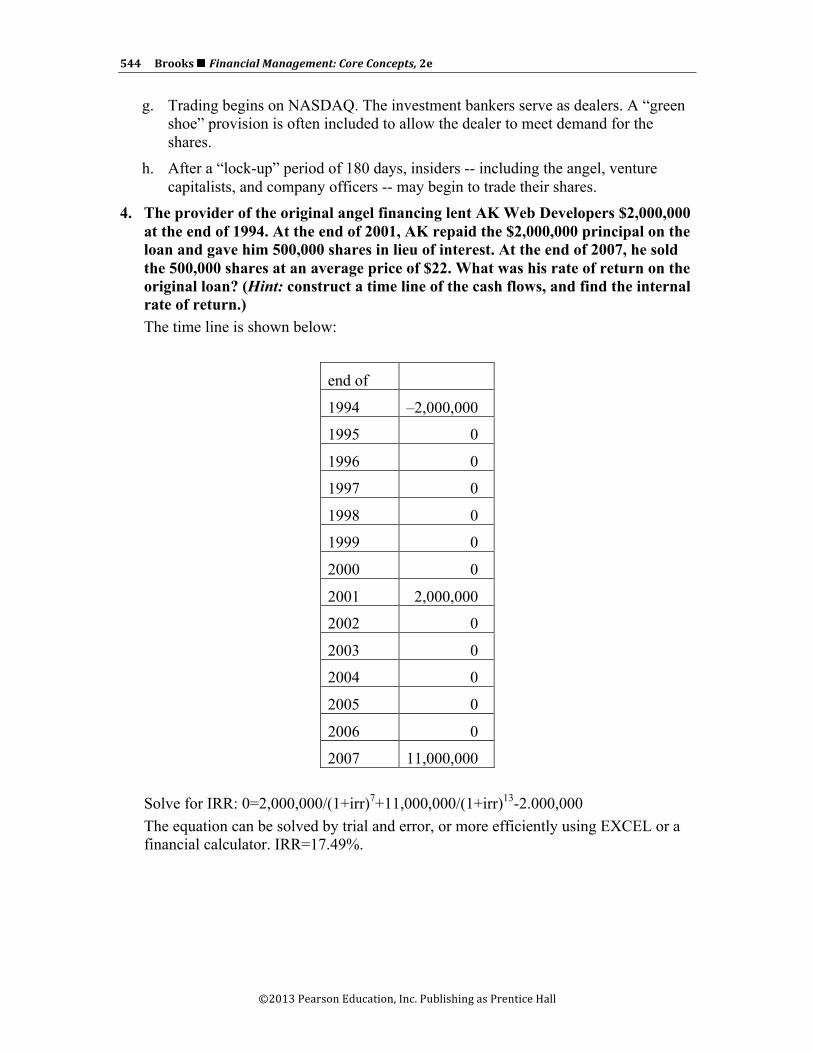

4. The provider of the original angel financing lent AK Web Developers $2,000,000 at the end of 1994. At the end of 2001, AK repaid the $2,000,000 principal on the loan and gave him 500,000 shares in lieu of interest. At the end of 2007, he sold the 500,000 shares at an average price of $22. What was his rate of return on the original loan? (Hint: construct a time line of the cash flows, and find the internal rate of return.) The time line is shown below:

end of

1994 –2,000,000

1995 0

1996 0

1997 0

1998 0

1999 0

2000 0

2001 2,000,000

2002 0

2003 0

2004 0

2005 0

2006 0

2007 11,000,000

Solve for IRR: 0=2,000,000/(1+irr)7+11,000,000/(1+irr)13-2.000,000 The equation can be solved by trial and error, or more efficiently using EXCEL or a financial calculator. IRR=17.49%.

Chapter 15 n Raising Capital 545

©2013 Pearson Education, Inc. Publishing as Prentice Hall

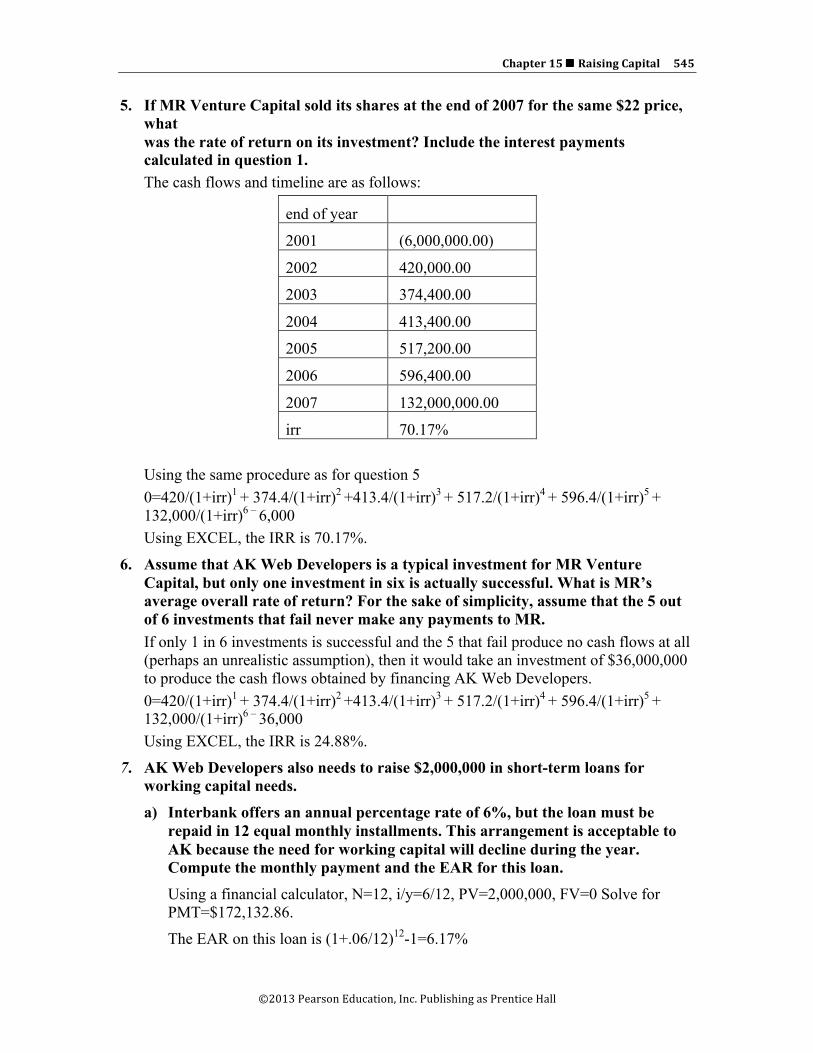

5. If MR Venture Capital sold its shares at the end of 2007 for the same $22 price, what was the rate of return on its investment? Include the interest payments calculated in question 1. The cash flows and timeline are as follows:

end of year

2001 (6,000,000.00)

2002 420,000.00

2003 374,400.00

2004 413,400.00

2005 517,200.00

2006 596,400.00

2007 132,000,000.00

irr 70.17%

Using the same procedure as for question 5 0=420/(1+irr)1 + 374.4/(1+irr)2 +413.4/(1+irr)3 + 517.2/(1+irr)4 + 596.4/(1+irr)5 + 132,000/(1+irr)6 – 6,000 Using EXCEL, the IRR is 70.17%.

6. Assume that AK Web Developers is a typical investment for MR Venture Capital, but only one investment in six is actually successful. What is MR’s average overall rate of return? For the sake of simplicity, assume that the 5 out of 6 investments that fail never make any payments to MR. If only 1 in 6 investments is successful and the 5 that fail produce no cash flows at all (perhaps an unrealistic assumption), then it would take an investment of $36,000,000 to produce the cash flows obtained by financing AK Web Developers. 0=420/(1+irr)1 + 374.4/(1+irr)2 +413.4/(1+irr)3 + 517.2/(1+irr)4 + 596.4/(1+irr)5 + 132,000/(1+irr)6 – 36,000 Using EXCEL, the IRR is 24.88%.

7. AK Web Developers also needs to raise $2,000,000 in short-term loans for working capital needs.

a) Interbank offers an annual percentage rate of 6%, but the loan must be repaid in 12 equal monthly installments. This arrangement is acceptable to AK because the need for working capital will decline during the year. Compute the monthly payment and the EAR for this loan.

Using a financial calculator, N=12, i/y=6/12, PV=2,000,000, FV=0 Solve for PMT=$172,132.86.

The EAR on this loan is (1+.06/12)12-1=6.17%

546 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

b) Bancnet offers a one year loan discounted at 6%. How much would AK need to borrow in order to meet its initial need for $2,000,000? What is the EAR for this loan?

AK would need to borrow $2,000,000/(1 – .06) = $2,127,659.57. The EAR is .06/(1 – .06) = 6.38%

c) Webster Bank offers a one year loan at 6% add-on interest with a compensating balance of 10%. How much would AK need to borrow in order to meet its initial need for $2,000,000? What is the EAR for this loan?

AK would need to borrow $2,000,000/(1 – .10) = $2,222,222.22. The EAR is .06/(1 – .10) = 6.67%

Additional Problems with Solutions 1. Venture capital required rate of return. Risk R Us Investors has a success ratio of

15% with its venture funding. Their owners require a rate of return of 25% for their portfolio of lending, and the average length on each loan is 4 years. If you were to apply to Risk R Us for a $200,000 loan, what is the annual percentage rate you would be required to pay for this loan?

ANSWER (Slides 15-‐47 to 15-‐48) First calculate how much $200,000 is 15% of? i. e. $200,000/.15è$1,333,333

So, in essence for every $200,000 they are lending you they effectively would be looking to earn 25% on an investment of $1.33m to achieve their objective.

i.e. The venture capitalist will expect to earn a rate of 25% per year for 4 years on An investment if $1,333,333.

Calculate the FV of $1,333,333 at the rate of 25% per year for 4 years. N=4; I=25; PV=1333333; PMT = 0; CPT FV è$3,255,208.33

So they expect the $200,000 investment in your venture to return $3,255,208.33. Calculate the expected rate of return as follows: N=4; PV = -200,000, FV = 3,255,208,33; PMT =0; CPT I = 100.86% èAPR

2. Discount loan versus straight loan. You want to borrow $250,000 for 1 year from your bank and are given the following 2 options:

1) Pay $35,000 per month for 12 months starting at the end of the 1st month.

2) Take a discount loan at the rate of 8% per year and pay the entire face value of the loan at the end of 12 months.

ANSWER (Slides 15-‐49 to 15-‐50) Calculate the EAR under each option and indicate your choice with an explanation.

Chapter 15 n Raising Capital 547

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Option 1 is a straight loan with PV = $250,000; N=12; PMT = -35,000; FV=0; iè9.05% èAPR; EARè(1 + (.0905/12))12 – 1 = 9.43%

Option 2 is an 8% discounted loan, so to have $250,000 we would have to take on a loan with a face value of $250,000/0.92 = $271, 739.13 which is what we would owe at the end of 12 months. So our APR = Interest paid/Amount usedè$21,739.13/$250,000 è8.695% è which is also our EAR Option 2 is better!

3. Bond proceeds. The Fire-Keepers Casino is in the process of issuing a 25-year, 9% coupon (paid semi-annually) AA2-rated corporate bond with $1000 par value. If by the time the bonds receive SEC clearance, the market yield on this bond goes to 9.35%, and the company sells 25000 of these bonds with the help of an investment banker who charges them a commission rate of 2.5% on the proceeds, what will the total proceeds be for the issuing company, and what is the cost of these bonds to the firm in terms of the cost of capital? What are the firm’s future cash obligations?

ANSWER (Slides 15-‐51 to 15-‐52) P/Y=2;C/Y=2;N=50;PMT=45;FV=1000;I=9.35; PVè$966.38

Gross proceeds from sale of bonds = 2500*$966.38=$2,415,9468.13 Investment banker’s commission = .025*$2,415,943.13= $60,398.65

Total proceeds received by the issuing company = $2,355,547.47 Net proceeds per bond = $966.38*(1-.025) = $942.22

Cost of debt to Golden Corral based on net price: P/Y=2; C/Y=2; PV=-942.22; N=50; PMT=45; FV=1000; I è9.61%

Future cash obligations: Annual Coupon payments = $45*2*25=00 = $225,000 Principal payment at maturity = $1000*2500 = $2,500,000

4. Firm commitment versus best efforts. Big Apple Investment Bankers offers Northern Diagnostics the following options on its initial public sale of equity: (1) a best-efforts arrangement whereby Big Apple will keep 2 % of the retail sales or (2) a firm-commitment arrangement of $6,000,000. Lunar plans on offering 1,000,000 shares at $7.50 per share to the public. If 100% of the shares are sold, which is the better choice for Northern Diagnostics? Which is the better choice for Big Apple Investment Bankers? What is the break-even sales percentage for Northern Diagnostics (point of indifference) and what will each party receive at the break-even sales percentage?

ANSWER (Slides 15-‐53 to 15-‐55) Proceeds for Northern Diagnostics under each type of sales agreement:

548 Brooks n Financial Management: Core Concepts, 2e

©2013 Pearson Education, Inc. Publishing as Prentice Hall

Best Efforts 1,000,000 × $7.5 × (1 – 0.02) = $7,350,000 Firm Commitment $6,000,000

Best choice for Northern Diagnostics is Best Efforts Proceeds for Big Apple Investments under each type of sales agreement:

Best Efforts 1,000,000 × $7.50 × (0.02) = $150,000 Firm Commitment 1,000,000 × $7.50 – $6,000,000 = $1,500,000

Best choice for Big Apple Investments is Firm Commitment To calculate break-even sales:

Sales Units × $7.50 (1 – 0.02) = $6,000,000 Sales Units = $6,000,000 / $7.35 = 816,327 shares

Best Efforts at 816,327 shares To Northern Diagnostics: 816,327 × $7.50 × (1 – 0.02) = $6,000,000

To Big Apple Investment: 816,327 × ($7.5-$7.35) = $122,450 Firm Commitment at 816,327 sales:

To Northern Diagnostics: $6,000,000 To Big Apple Investments: 816,327 × $7.5 – $6,000,000 = $122,450

5. Commercial paper. Cereal City Instruments will issue commercial paper for a short-term cash inflow. The paper is for 182 days, has a face value of $50,000, and is anticipated to sell at 94% of par value. Cereal City wants to raise $5,000,000, so what is the cost of this borrowing (annual terms) and how many “papers” will be sold?

ANSWER: (Slides 15-‐56 to 15-‐57) Selling price is 0.94 × $50,000 = $47,000

The cost of this borrowing is: 182-day interest rate = ($50,000 – $47,000) / $47,000 = 0.06383

Stated annually we have: Annual Percentage Rate = 0.06383 × 365/182 = 12.801%

Effective Annual Rate = (1 + 0.06383)365/182 – 1 = 13.21% The total number of “papers” sold will be: Number issued = $5,000,000 / $47,000 = 107 (must sell in whole units)

Related Documents