9 - 1 ©2003 Prentice Hall Business Publishing, Advanced A ccounting 8/e, Beams/Anthony/Clement/Lowensohn Indirect and Mutual Holdings Chapter 9

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 1/50

9 - 1©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Indirect and Mutual Holdings

Chapter 9

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 2/50

9 - 2©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Learning Objective 1

Prepare consolidated statements

when the parent company

controls through indirect holdings.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 3/50

9 - 3©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Affiliation Structures

The potential complexity of corporate

affiliation structure is limited only by one’s imagination .

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 4/50

9 - 4©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

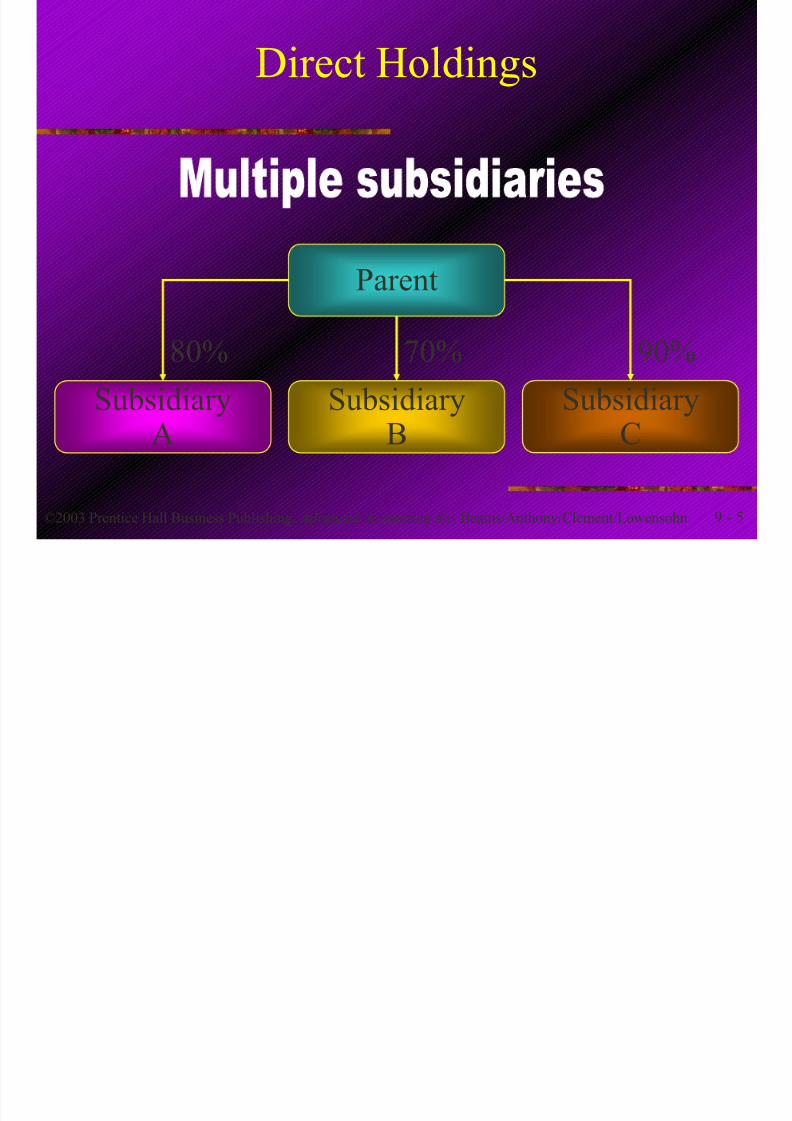

Direct Holdings

Parent

SubsidiaryA

80%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 5/50

9 - 5©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Direct Holdings

Parent

SubsidiaryB

70%

SubsidiaryA

80%

SubsidiaryC

90%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 6/50

9 - 6©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Indirect Holdings

Parent

Subsidiary

A

80%

SubsidiaryB

70%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 7/50

9 - 7©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Indirect Holdings

Parent

SubsidiaryA

SubsidiaryB

80% 20%

40%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 8/50

9 - 8©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Mutual Holdings

Parent

SubsidiaryA

80% 10%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 9/50

9 - 9©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Mutual Holdings

Parent

SubsidiaryA

SubsidiaryB

80% 20%

40%

20%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 10/50

9 - 10©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

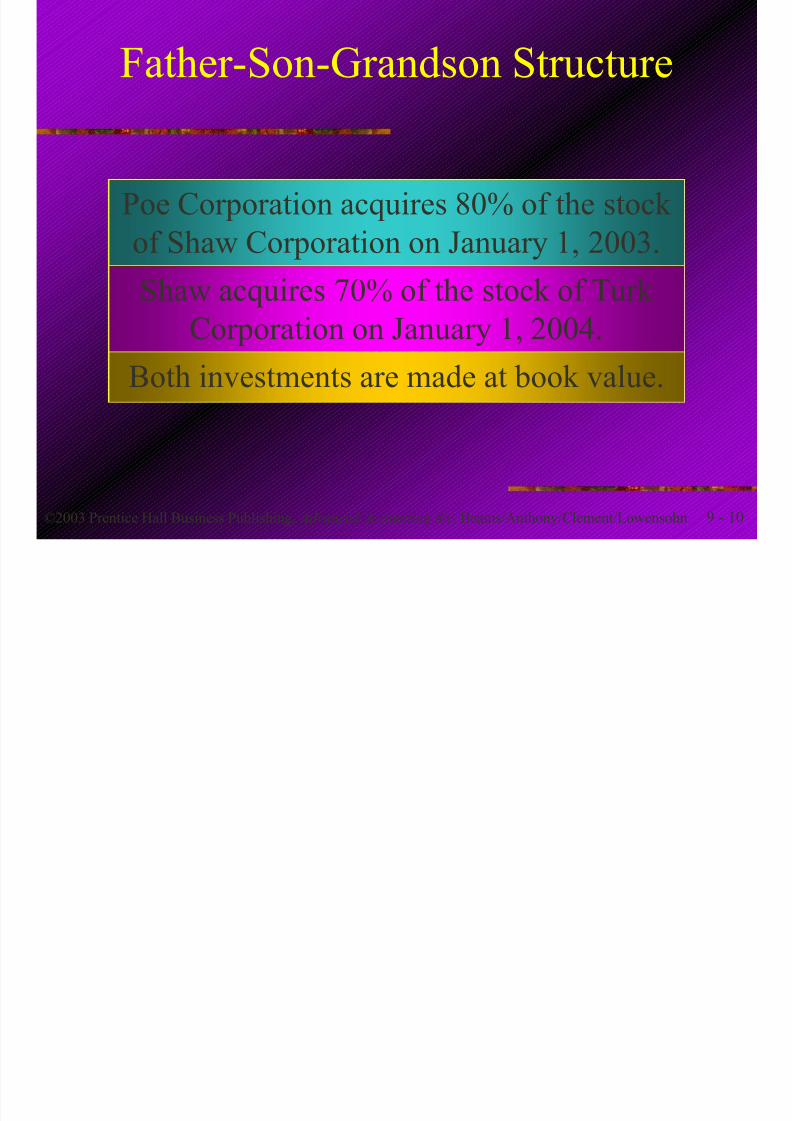

Father-Son-Grandson Structure

Poe Corporation acquires 80% of the stock

of Shaw Corporation on January 1, 2003.Shaw acquires 70% of the stock of Turk

Corporation on January 1, 2004.

Both investments are made at book value.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 11/50

9 - 11©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

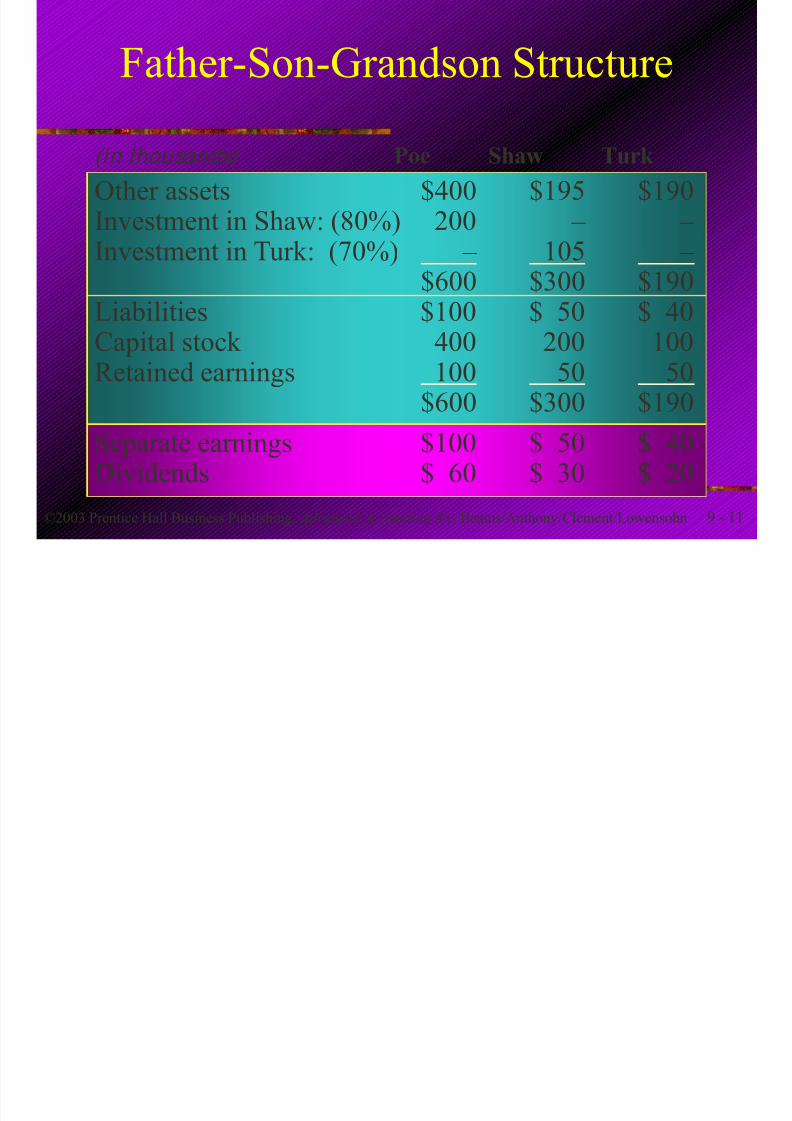

Father-Son-Grandson Structure

Other assets $400 $195 $190Investment in Shaw: (80%) 200 – –

Investment in Turk: (70%) – 105 – $600 $300 $190

Liabilities $100 $ 50 $ 40Capital stock 400 200 100

Retained earnings 100 50 50$600 $300 $190

(in thousands) Poe Shaw Turk

Separate earnings $100 $ 50 $ 40Dividends $ 60 $ 30 $ 20

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 12/50

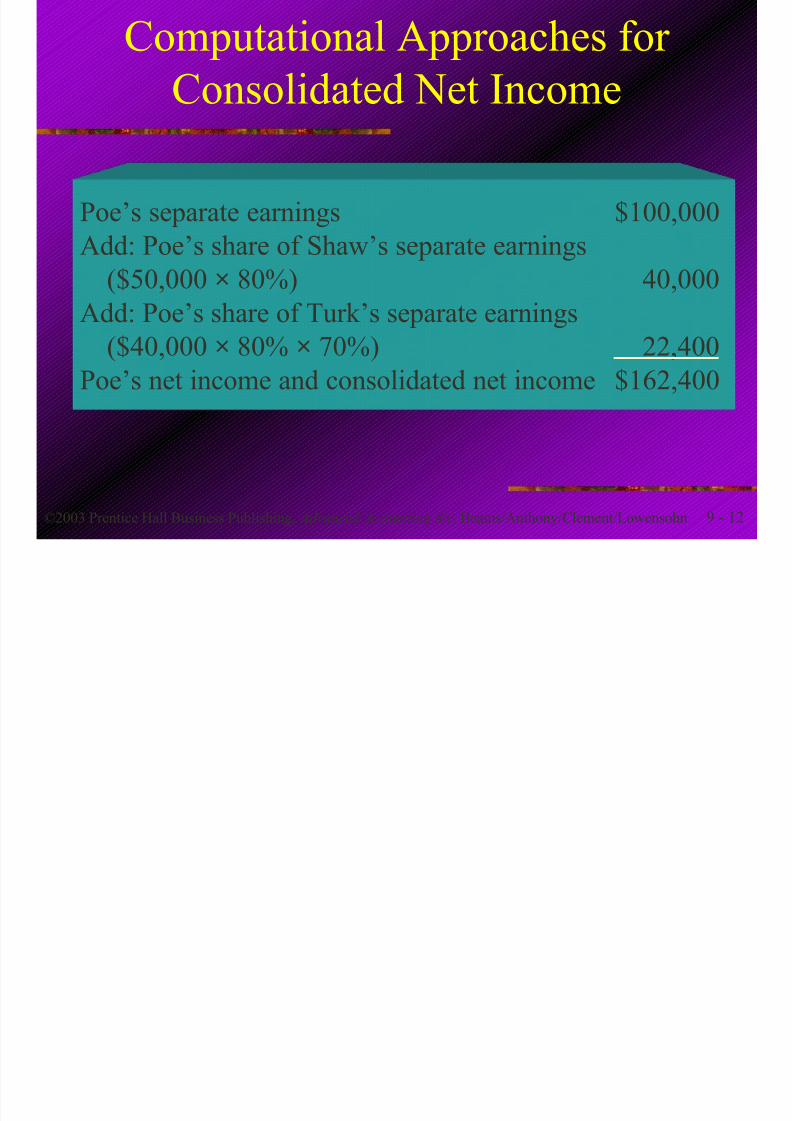

9 - 12©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Computational Approaches for

Consolidated Net Income

Poe’s separate earnings $100,000

Add: Poe’s share of Shaw’s separate earnings ($50,000 × 80%) 40,000

Add: Poe’s share of Turk’s separate earnings

($40,000 × 80% × 70%) 22,400

Poe’s net income and consolidated net income $162,400

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 13/50

9 - 13©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

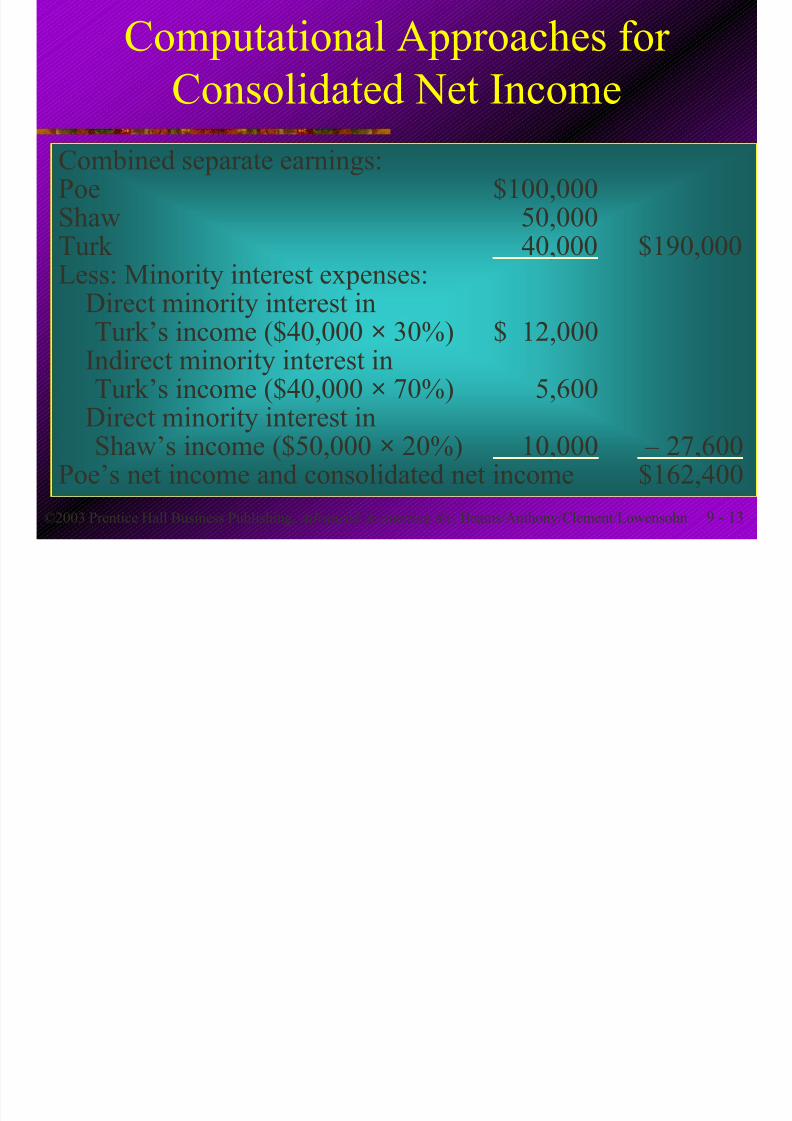

Computational Approaches for

Consolidated Net Income

Combined separate earnings:Poe $100,000Shaw 50,000

Turk 40,000 $190,000Less: Minority interest expenses:Direct minority interest inTurk’s income ($40,000 × 30%) $ 12,000

Indirect minority interest inTurk’s income ($40,000 × 70%) 5,600

Direct minority interest inShaw’s income ($50,000 × 20%) 10,000 – 27,600

Poe’s net income and consolidated net income $162,400

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 14/50

9 - 14©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

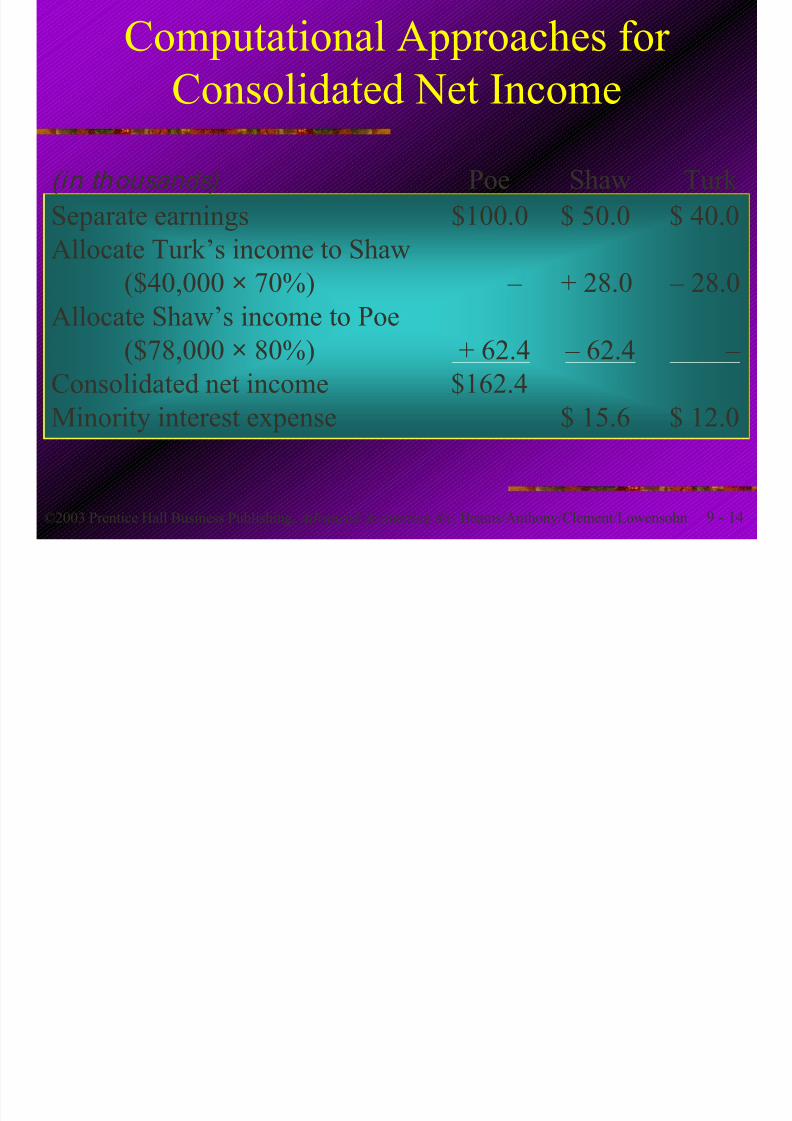

Computational Approaches for

Consolidated Net Income

(in thousands) Poe Shaw Turk

Separate earnings $100.0 $ 50.0 $ 40.0

Allocate Turk’s income to Shaw ($40,000 × 70%) – + 28.0 – 28.0

Allocate Shaw’s income to Poe

($78,000 × 80%) + 62.4 – 62.4 –

Consolidated net income $162.4Minority interest expense $ 15.6 $ 12.0

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 15/50

9 - 15©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Indirect Holdings –

Connecting Affiliates Structure

Pet

20%Sal

70%

Ty

60%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 16/50

9 - 16©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

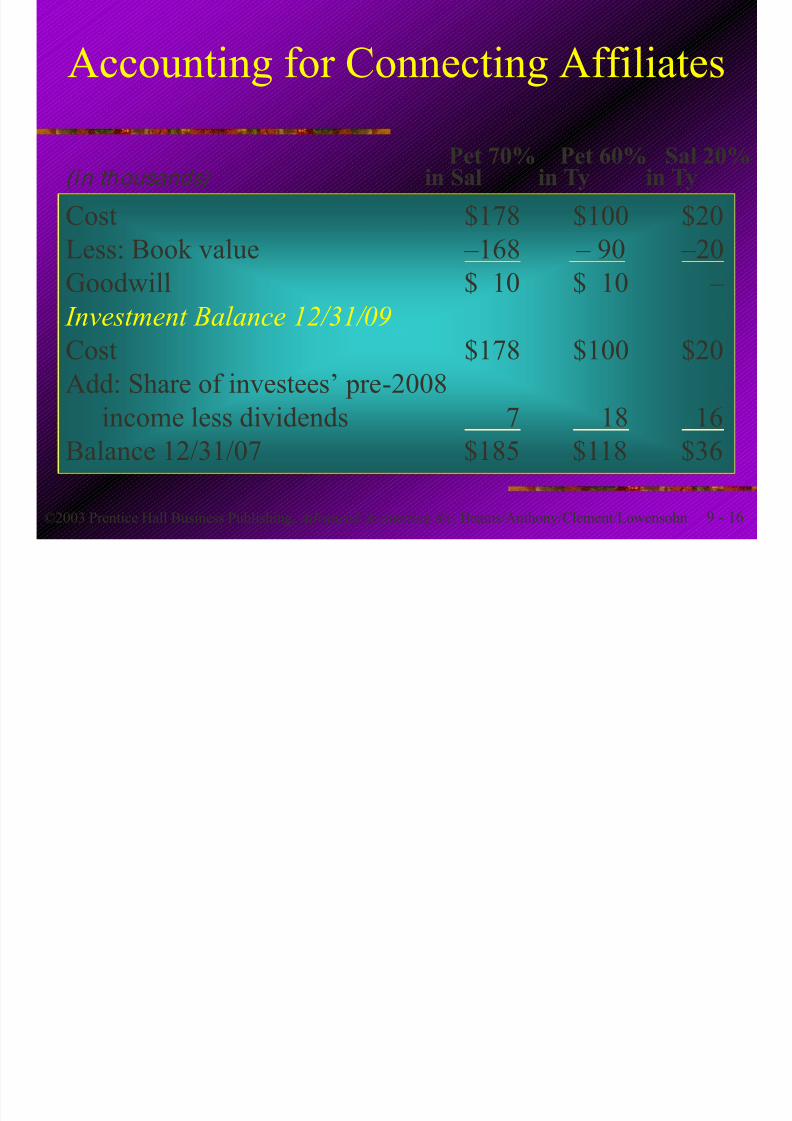

Accounting for Connecting Affiliates

Pet 70% Pet 60% Sal 20%(in thousands) in Sal in Ty in Ty

Cost $178 $100 $20

Less: Book value – 168 – 90 – 20Goodwill $ 10 $ 10 –

Investment Balance 12/31/09

Cost $178 $100 $20

Add: Share of investees’ pre-2008income less dividends 7 18 16

Balance 12/31/07 $185 $118 $36

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 17/50

9 - 17©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Accounting for Connecting Affiliates

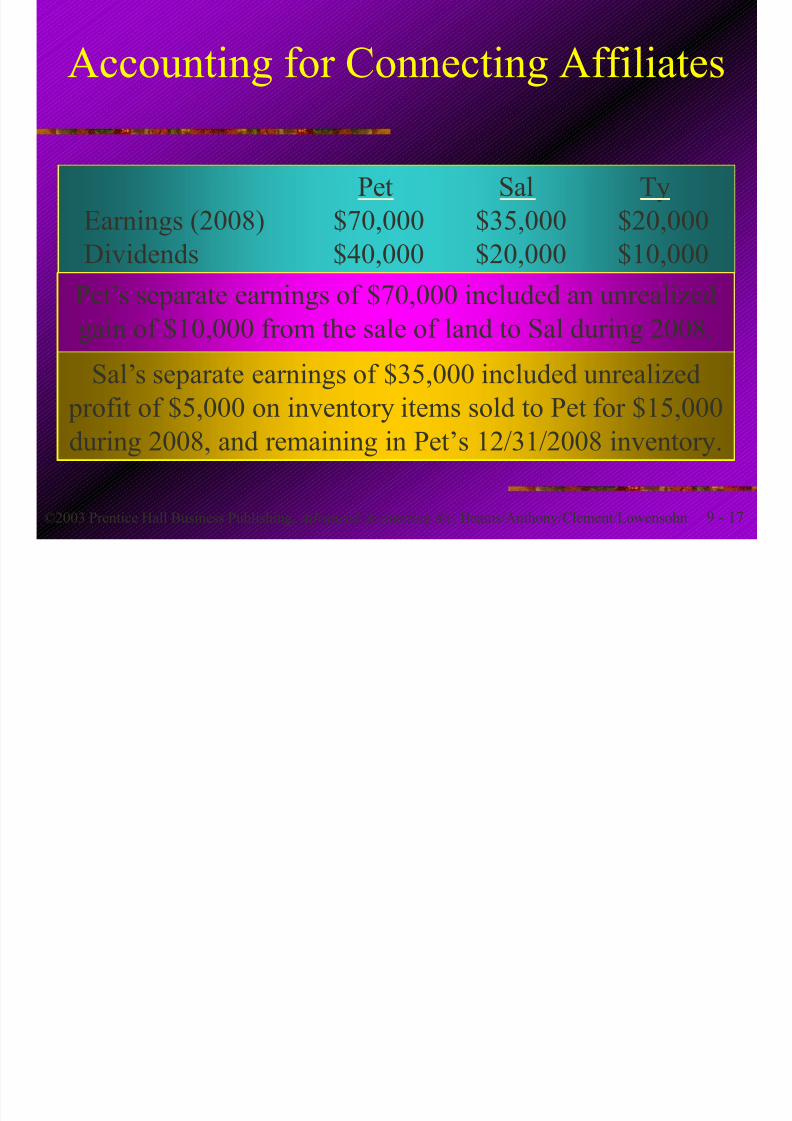

Pet Sal Ty

Earnings (2008) $70,000 $35,000 $20,000

Dividends $40,000 $20,000 $10,000Pet’s separate earnings of $70,000 included an unrealized

gain of $10,000 from the sale of land to Sal during 2008.

Sal’s separate earnings of $35,000 included unrealized profit of $5,000 on inventory items sold to Pet for $15,000

during 2008, and remaining in Pet’s 12/31/2008 inventory.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 18/50

9 - 18©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Accounting for Connecting Affiliates

(in thousands) Pet Sal Ty

Separate earnings $70.0 $35.0 $20.0Deduct unrealized profit – 10.0 – 5.0 –

Separate realized earnings $60.0 $30.0 $20.0Allocate Ty’s income:

20% to Sal – + 4.0 – 4.060% to Pet +12.0 – – 12.0

Allocate Sal’s income: 70% to Pet +23.8 – 23.8 –

Consolidated net income $95.8Minority interest expense $10.2 $ 4.0

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 19/50

9 - 19©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Accounting for Connecting Affiliates

Cash 6,000Investment in Ty 6,000

To record dividends received from Ty

Investment in Ty 12,000

Income from Ty 12,000

To record income from Ty

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 20/50

9 - 20©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Accounting for Connecting Affiliates

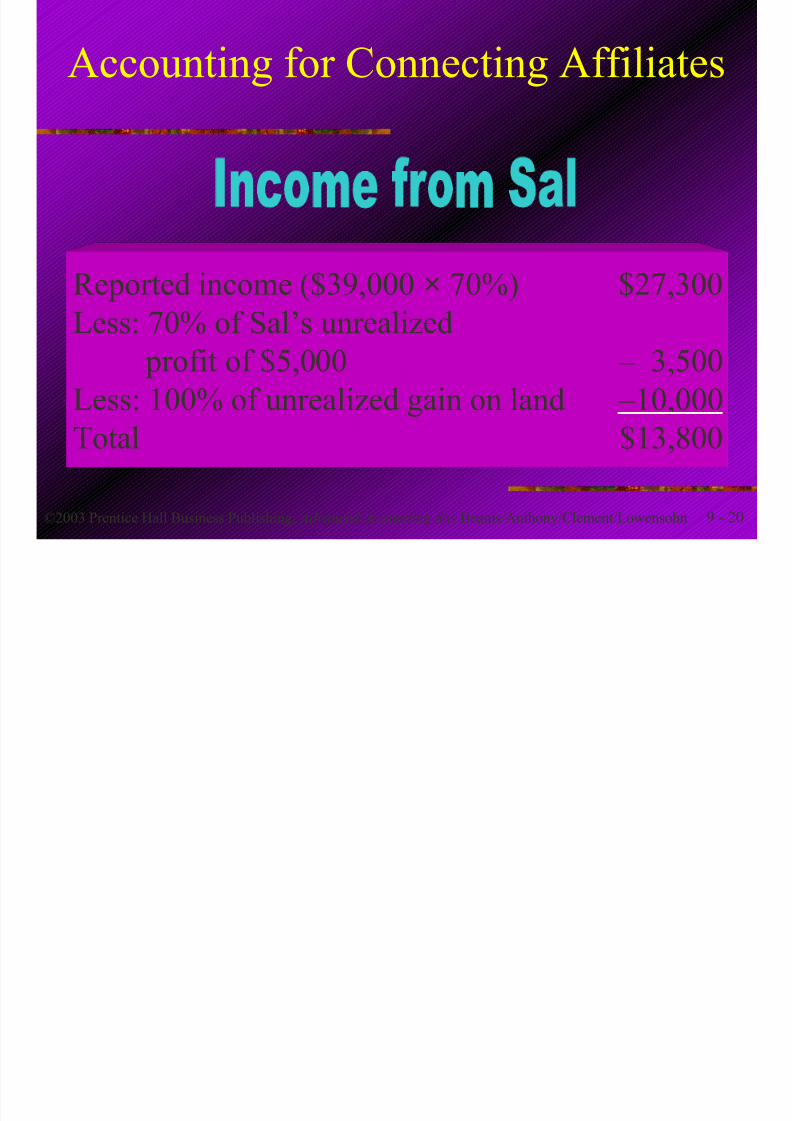

Reported income ($39,000 × 70%) $27,300

Less: 70% of Sal’s unrealized

profit of $5,000 – 3,500

Less: 100% of unrealized gain on land – 10,000

Total $13,800

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 21/50

9 - 21©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

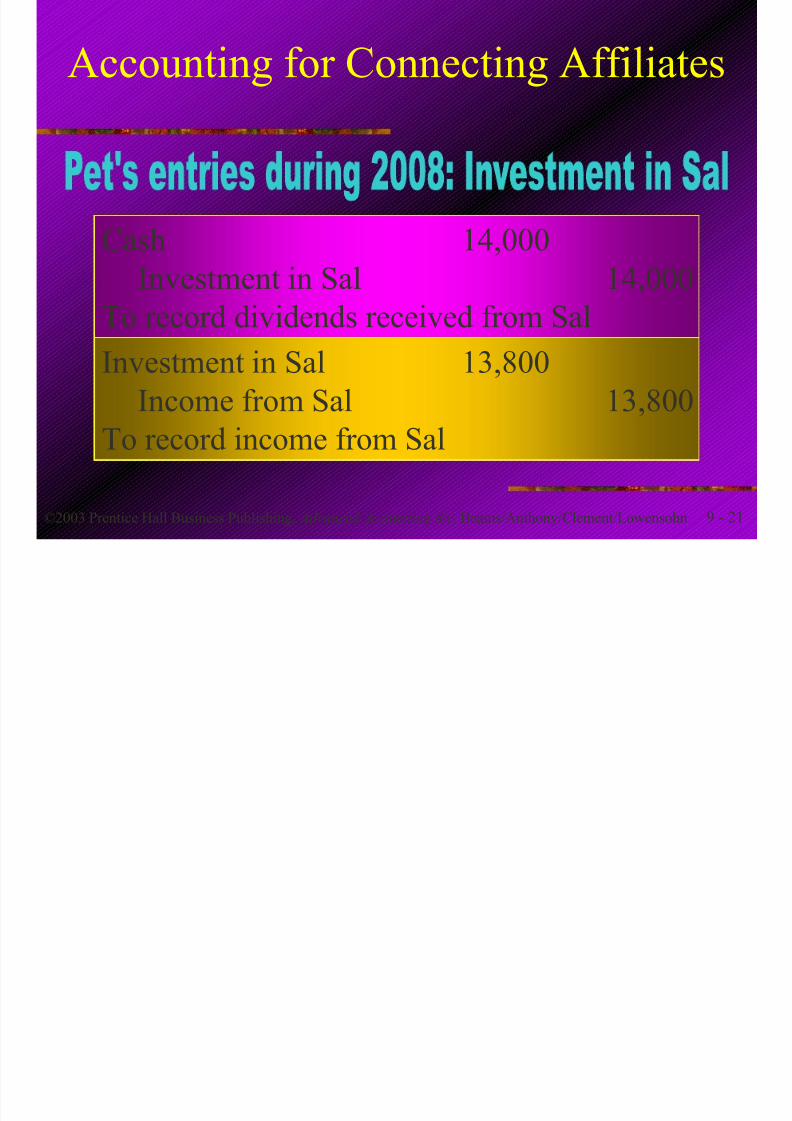

Accounting for Connecting Affiliates

Cash 14,000Investment in Sal 14,000

To record dividends received from Sal

Investment in Sal 13,800

Income from Sal 13,800

To record income from Sal

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 22/50

9 - 22©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Accounting for Connecting Affiliates

Pet’s investment Investment Investmentaccounts at 12/31/08 in Sal (70%) in Ty (60%)

Balance 12/31/2007 $185,000 $118,000

Add: Investment income 13,800 12,000

Deduct: Dividends – 14,000 – 6,000

Balance 12/31/2008 $183,800 $124,000

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 23/50

9 - 23©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Learning Objective 2

Apply consolidated procedures of

indirect holdings to the special

case of mutual holdings.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 24/50

9 - 24©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

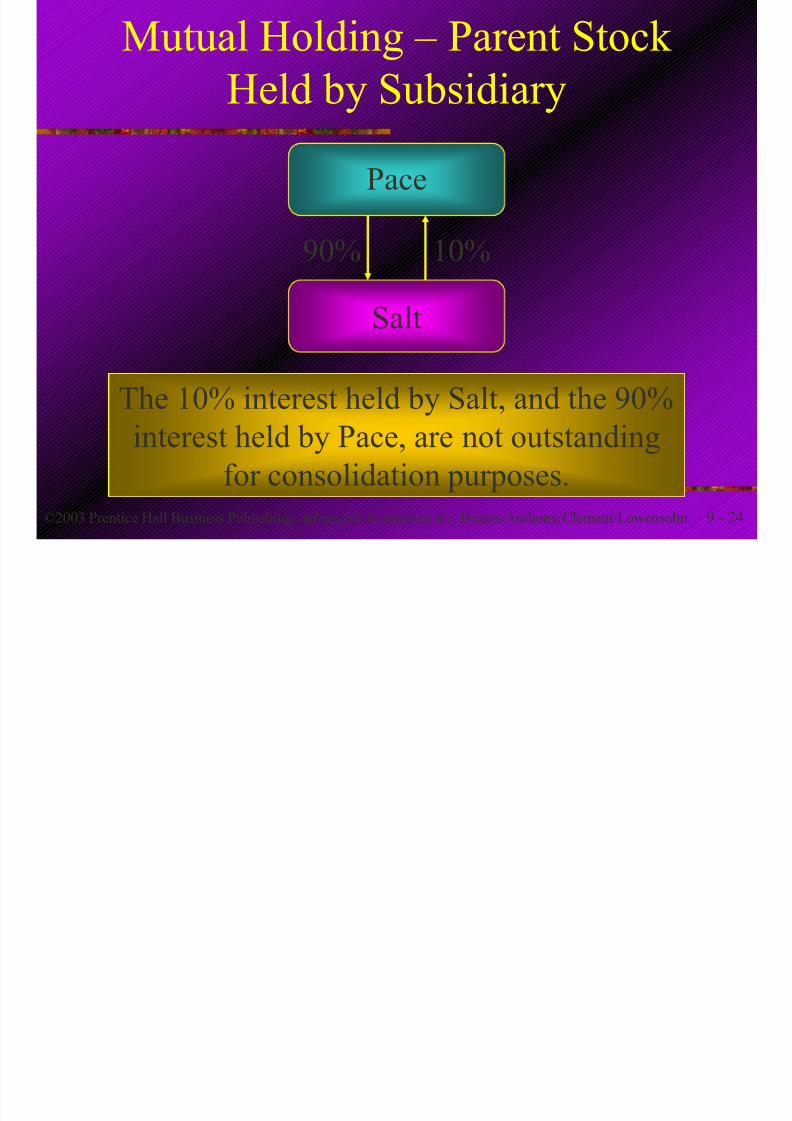

Mutual Holding – Parent Stock

Held by Subsidiary

Pace

Salt

90% 10%

The 10% interest held by Salt, and the 90%

interest held by Pace, are not outstanding

for consolidation purposes.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 25/50

9 - 25©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Mutual Holding – Parent Stock

Held by Subsidiary

Treasury Stock Approach

Conventional Approach

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 26/50

9 - 26©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

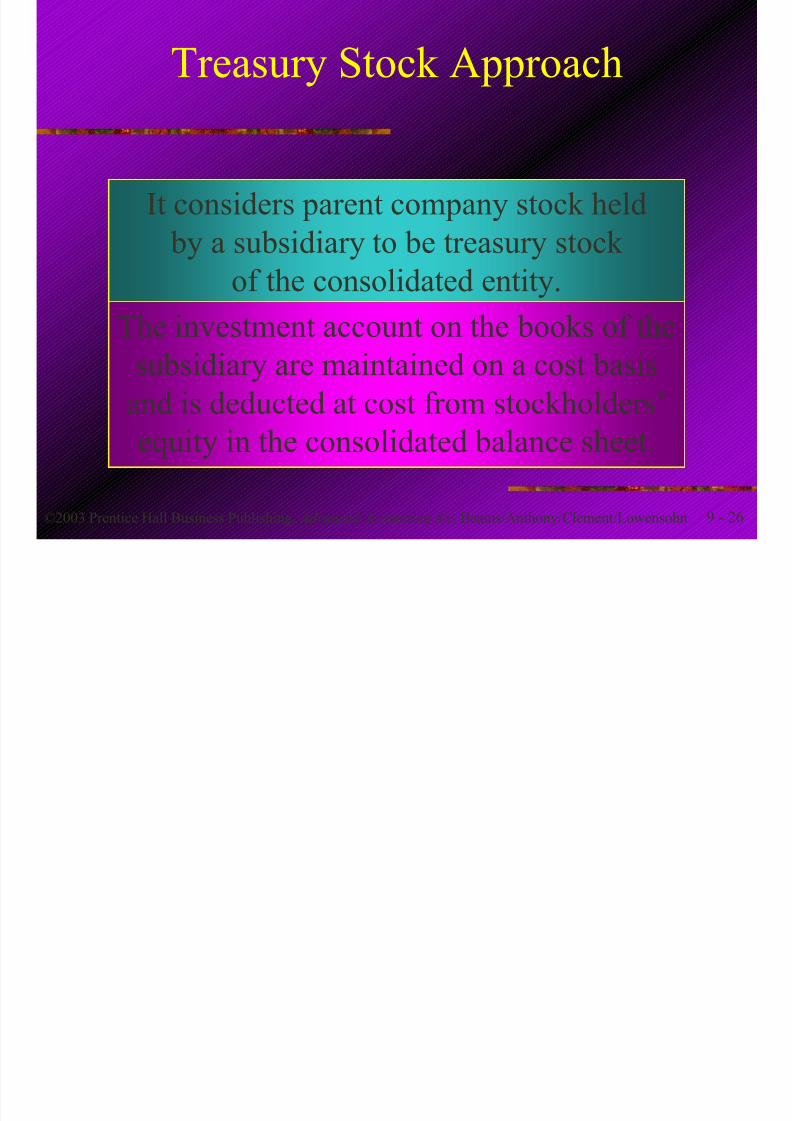

Treasury Stock Approach

It considers parent company stock held

by a subsidiary to be treasury stock of the consolidated entity.

The investment account on the books of the

subsidiary are maintained on a cost basis

and is deducted at cost from stockholders’

equity in the consolidated balance sheet.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 27/50

9 - 27©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

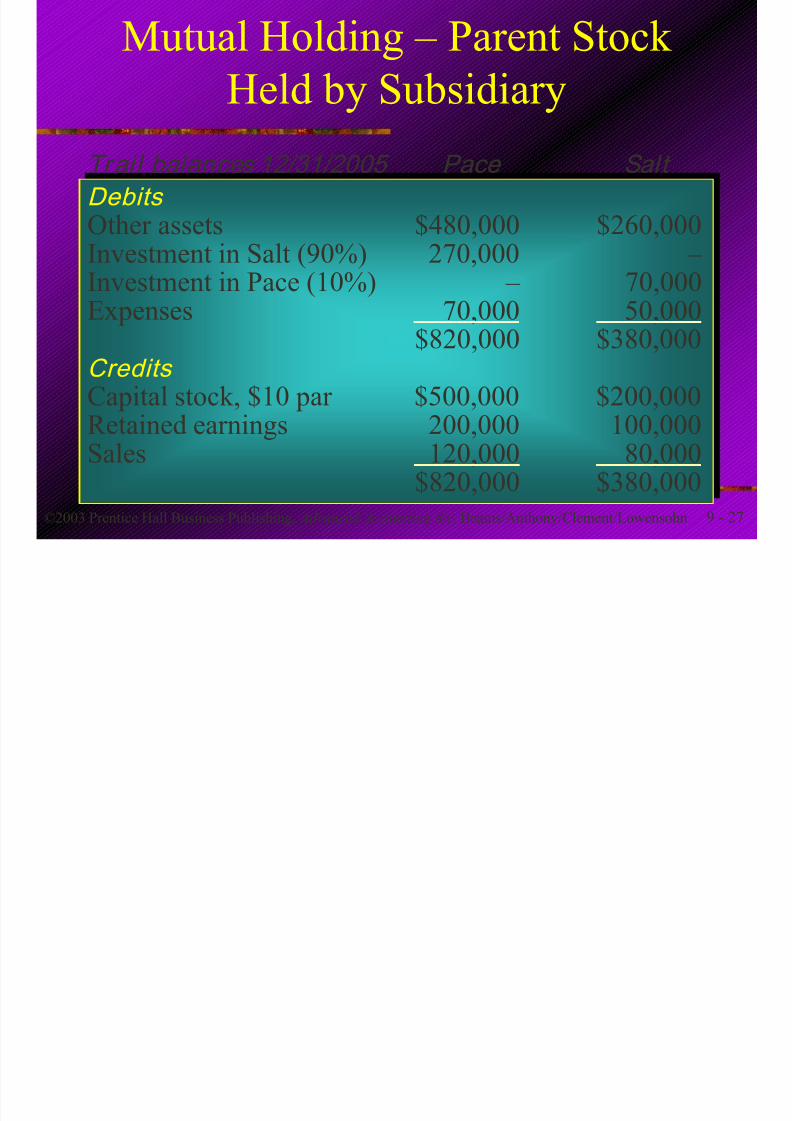

Mutual Holding – Parent Stock

Held by Subsidiary

Trail balances 12/31/2005 Pace Salt

Debits Other assets $480,000 $260,000

Investment in Salt (90%) 270,000 – Investment in Pace (10%) – 70,000Expenses 70,000 50,000

$820,000 $380,000Credits Capital stock, $10 par $500,000 $200,000Retained earnings 200,000 100,000Sales 120,000 80,000

$820,000 $380,000

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 28/50

9 - 28©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

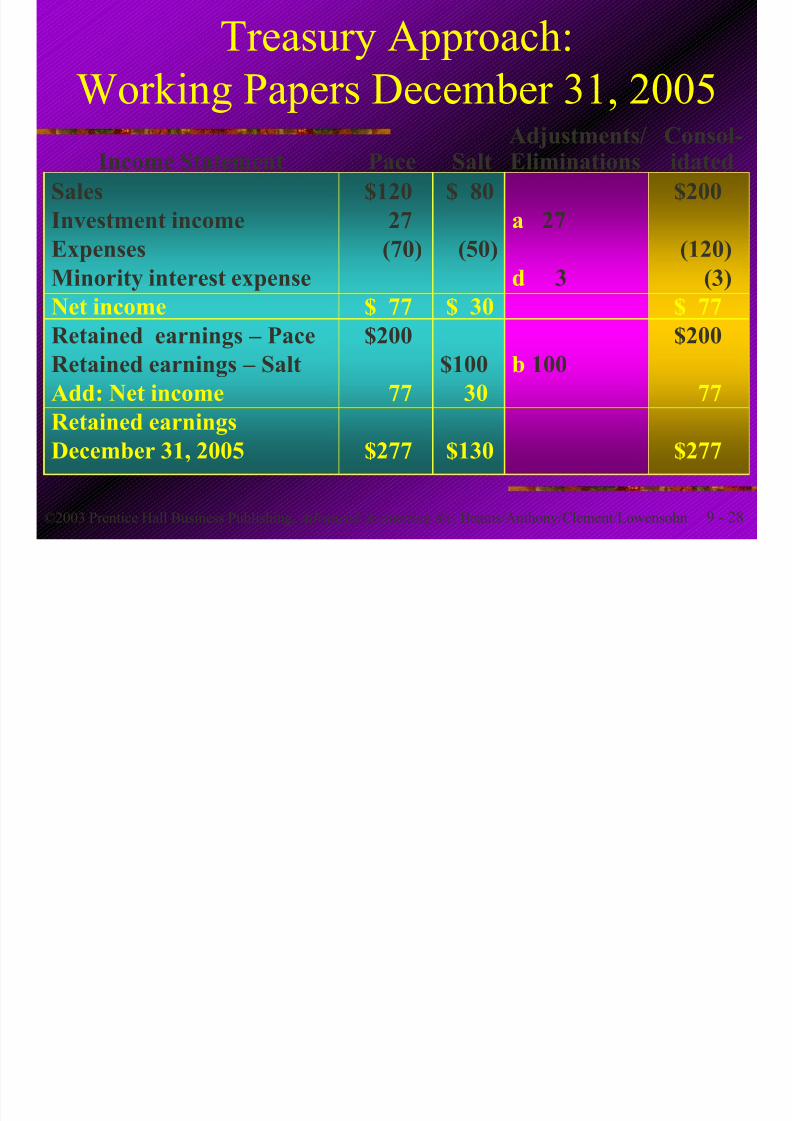

Treasury Approach:

Working Papers December 31, 2005Adjustments/ Consol-

Pace Salt Eliminations idated

Sales

Investment income

ExpensesMinority interest expense

Net income

Retained earnings – Pace

Retained earnings – Salt

Add: Net income

Retained earnings

December 31, 2005

$120

27

(70)

$ 77

$200

77

$277

$ 80

(50)

$ 30

$100

30

$130

a 27

d 3

b 100

$200

(120)(3)

$ 77

$200

77

$277

Income Statement

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 29/50

9 - 29©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

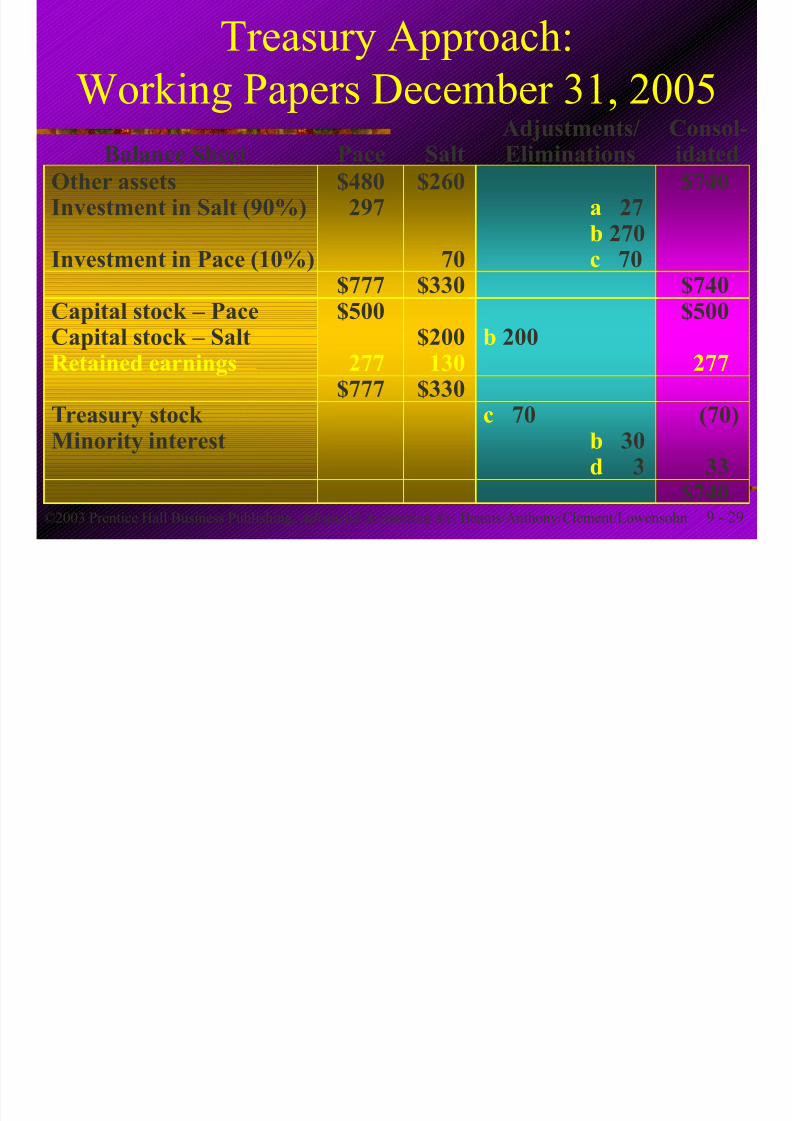

Treasury Approach:

Working Papers December 31, 2005

Other assetsInvestment in Salt (90%)

Investment in Pace (10%)

Capital stock – PaceCapital stock – SaltRetained earnings

Treasury stock Minority interest

$480297

$777$500

277

$777

$260

70$330

$200130

$330

a 27b 270

c 70

b 200

c 70b 30d 3

$740

$740$500

277

(70)

33$740

Balance SheetAdjustments/ Consol-

Pace Salt Eliminations idated

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 30/50

9 - 30©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

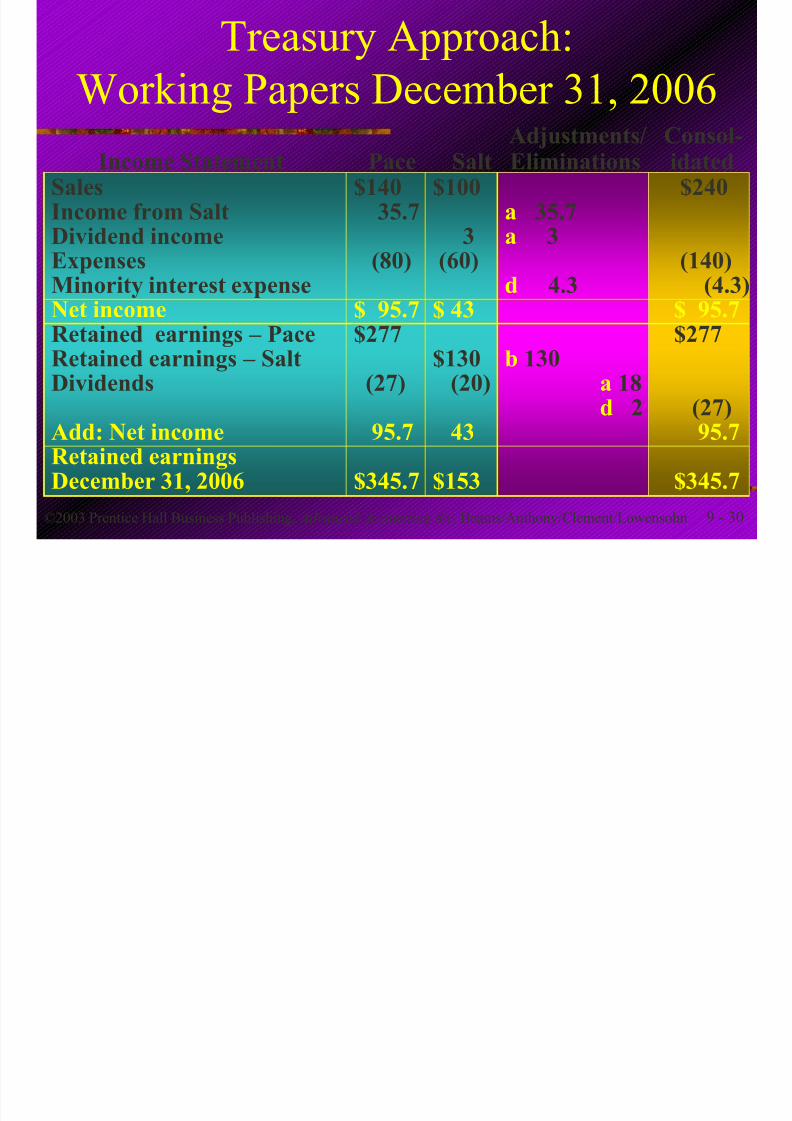

Treasury Approach:

Working Papers December 31, 2006Adjustments/ Consol-

Pace Salt Eliminations idatedSalesIncome from SaltDividend income

ExpensesMinority interest expenseNet incomeRetained earnings – PaceRetained earnings – Salt

Dividends

Add: Net incomeRetained earningsDecember 31, 2006

$14035.7

(80)

$ 95.7$277

(27)

95.7

$345.7

$100

3

(60)

$ 43

$130

(20)

43

$153

a 35.7a 3

d 4.3

b 130

a 18d 2

$240

(140)(4.3)

$ 95.7$277

(27)95.7

$345.7

Income Statement

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 31/50

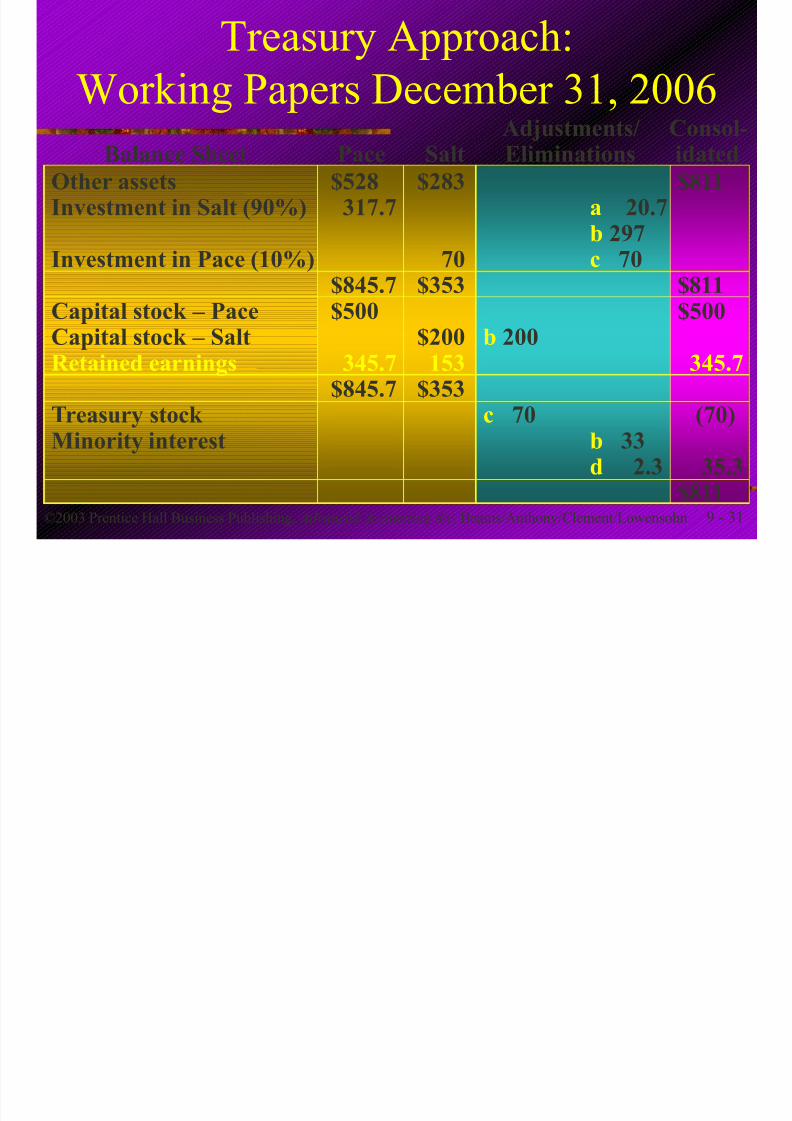

9 - 31©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Treasury Approach:

Working Papers December 31, 2006

Other assetsInvestment in Salt (90%)

Investment in Pace (10%)

Capital stock – PaceCapital stock – SaltRetained earnings

Treasury stock Minority interest

$528317.7

$845.7$500

345.7

$845.7

$283

70$353

$200153

$353

a 20.7b 297

c 70

b 200

c 70b 33d 2.3

$811

$811$500

345.7

(70)

35.3$811

Balance SheetAdjustments/ Consol-

Pace Salt Eliminations idated

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 32/50

9 - 32©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Conventional Approach

It accounts for the subsidiary investment in

parent company stock on an equity basis.

Parent company stock held by a subsidiary

is constructively retired.

Capital stock and retained earnings applicable to

the interest held by the subsidiary do not appear

in the consolidated financial statements.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 33/50

9 - 33©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Conventional Approach

Capital stock $500,000 $450,000

Retained earnings 200,000 180,000

Stockholders’ equity $700,000 $630,000

January 1, 2005 Pace Consolidated

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 34/50

9 - 34©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

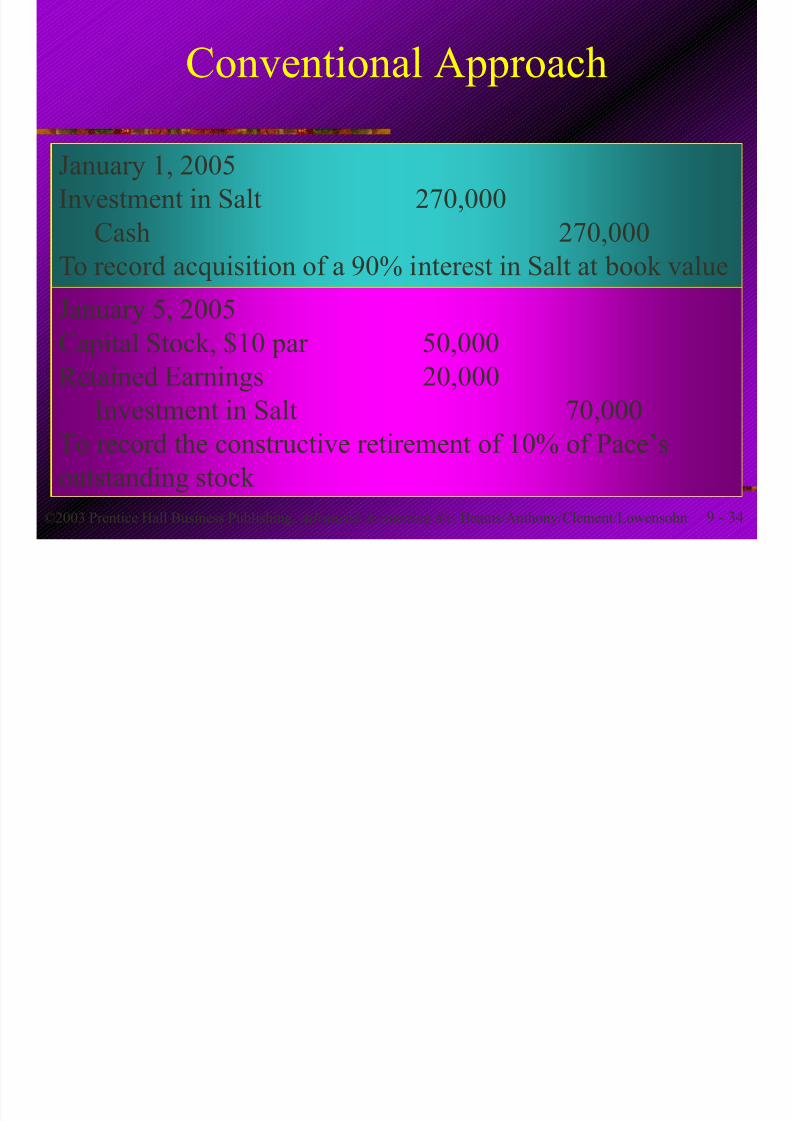

Conventional Approach

January 1, 2005

Investment in Salt 270,000

Cash 270,000

To record acquisition of a 90% interest in Salt at book value

January 5, 2005

Capital Stock, $10 par 50,000

Retained Earnings 20,000Investment in Salt 70,000

To record the constructive retirement of 10% of Pace’s

outstanding stock

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 35/50

9 - 35©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Allocation of Mutual Income

Determine income on a consolidated basis.

P = Pace’s separate earnings of $50,000 + 90%S

S = Salt’s separate earnings of $30,000 + 10% P

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 36/50

9 - 36©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Allocation of Mutual Income

P = $50,000 + 0.9($30,000 + 0.1 P )

P = $50,000 + $27,000 + 0.09 P 0.91 P = $77,000 P = $84,615

S = $30,000 + 0.1($84,615)

S = $30,000 + $8,462 = $38,462

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 37/50

9 - 37©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Allocation of Mutual Income

P S Total

Before allocation: $50,000 $30,000 $ 80,000

After allocation: $84,615 $38,462 $123,077

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 38/50

9 - 38©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Allocation of Mutual Income

Determine Pace’s net income on an equity basis and minority interest.

P = 84,615 × 90% = $76,154

MI = 38,462 × 10% = $3,846

$76,154 + $3,846 = $80,000

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 39/50

9 - 39©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Accounting for Mutual Income

($38,462 × 90%) – ($84,615 × 10%) = $26,154

How does Pace record its investment income?Investment in Salt 26,154

Income from Salt 26,154

To record income from Salt

C ti l A h

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 40/50

9 - 40©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Conventional Approach:

Working Papers December 31, 2005Adjustments/ Consol-

Pace Salt Eliminations idated

Sales

Investment income

ExpensesMinority interest

expense

Net income

Retained earnings – P

Retained earnings – S

Add: Net income

Retained earnings

December 31, 2005

$120,000

26,154

(70,000)

$ 76,154

$180,000

76,154

$256,154

$ 80,000

(50,000)

$ 30,000

$100,000

30,000

$130,000

b 26,154

d 3,846

c 100,000

$200,000

(120,000)(3,846)

$ 76,154

$180,000

76,154

$256,154

Income Statement

C ti l A h

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 41/50

9 - 41©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Conventional Approach:

Working Papers December 31, 2005

Other assetsInvestment in S

Investment in P

Capital stock – PCapital stock – SRetained earnings

Minority interest

$480,000226,154

$756,154$450,000

256,154

$706,154

$260,000

70,000$330,000

$200,000130,000

$330,000

a 70,000 b 26,154c 270,000

a 70,000

c 200,000

b 30,000d 3,846

$740,000

$740,000$450,000

256,154

33,846$740,000

Balance SheetAdjustments/ Consol-

Pace Salt Eliminations idated

C i t E it M th d

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 42/50

9 - 42©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

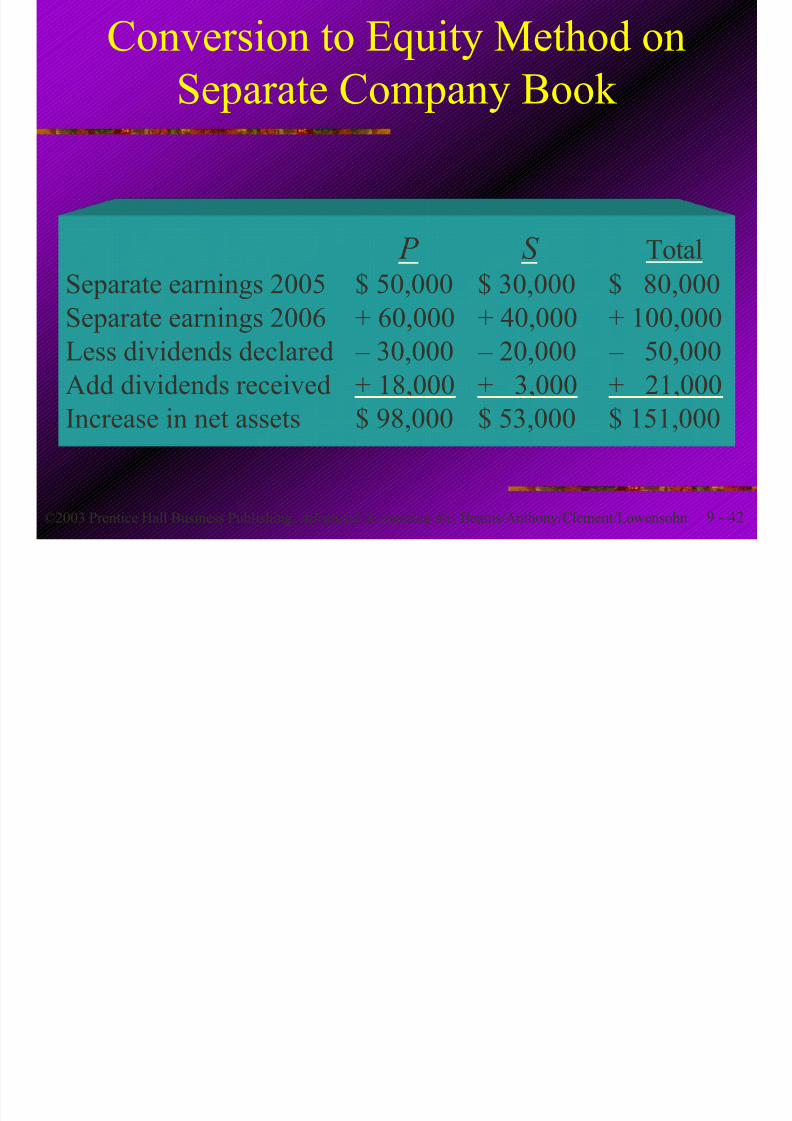

Conversion to Equity Method on

Separate Company Book

P S TotalSeparate earnings 2005 $ 50,000 $ 30,000 $ 80,000

Separate earnings 2006 + 60,000 + 40,000 + 100,000

Less dividends declared – 30,000 – 20,000 – 50,000

Add dividends received + 18,000 + 3,000 + 21,000Increase in net assets $ 98,000 $ 53,000 $ 151,000

C i t E it M th d

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 43/50

9 - 43©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Conversion to Equity Method on

Separate Company Book

P = $98,000 + 0.9S S = $53,000 + 0.1 P

P = $98,000 + 0.9($53,000 + 0.1 P ) = $160,110

Pace’s RE increase: $160,110 × 90% = $144,099

MI RE increase: 69,011 × 10% = $6,901 Net asset increase: $144,099 + $6,901= $151,000

S = $53,000 + (0.1 × $160,110) = $69,011

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 44/50

9 - 44©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Subsidiary Stock Mutually Held

The mutually held stock involves subsidiaries

holding the stock of each other, and the

treasury stock approach is not applicable.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 45/50

9 - 45©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Subsidiary Stock Mutually Held

Poly

Seth

Uno

70% 10%

80%

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 46/50

9 - 46©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

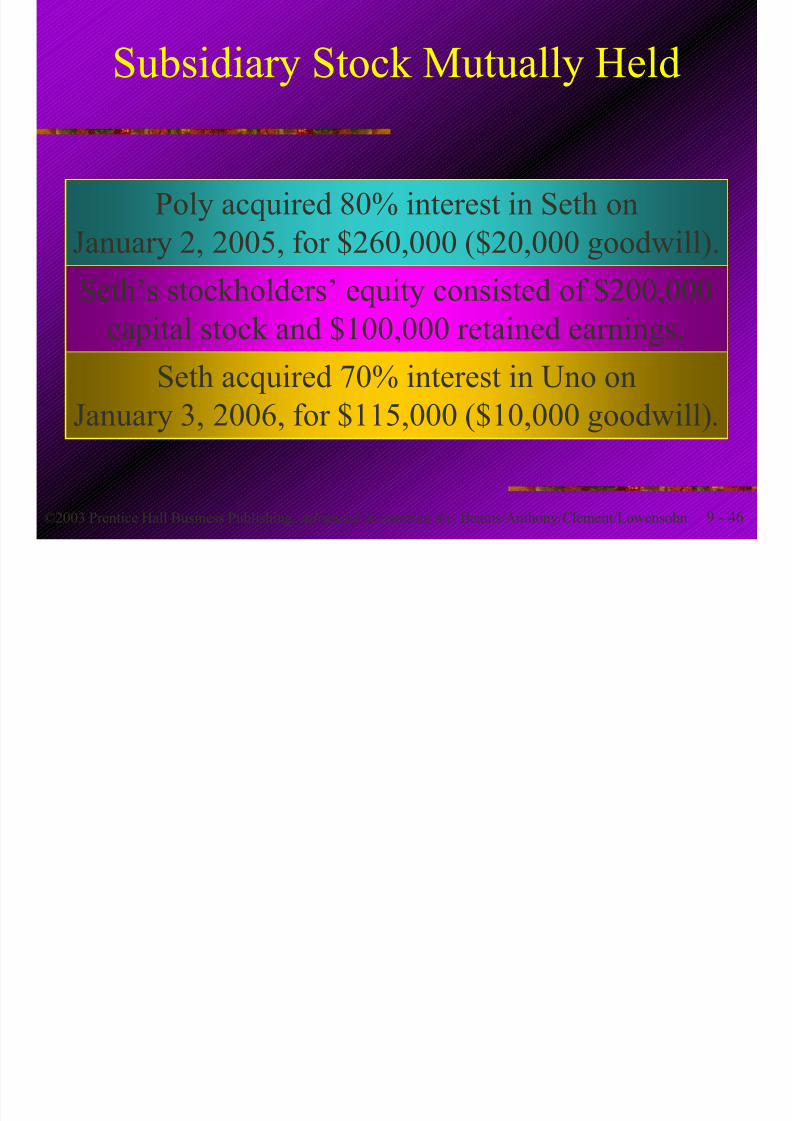

Subsidiary Stock Mutually Held

Poly acquired 80% interest in Seth on

January 2, 2005, for $260,000 ($20,000 goodwill).Seth’s stockholders’ equity consisted of $200,000

capital stock and $100,000 retained earnings.

Seth acquired 70% interest in Uno onJanuary 3, 2006, for $115,000 ($10,000 goodwill).

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 47/50

9 - 47©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Subsidiary Stock Mutually Held

Uno’s stockholders’ equity consisted of $100,000

capital stock and $50,000 retained earnings.

Uno acquired 10% interest in Seth on

December 31, 2006, for $40,000.

Seth’s stockholders’ equity consisted of $200,000 capital stock and $200,000 retained earnings.

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 48/50

9 - 48©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

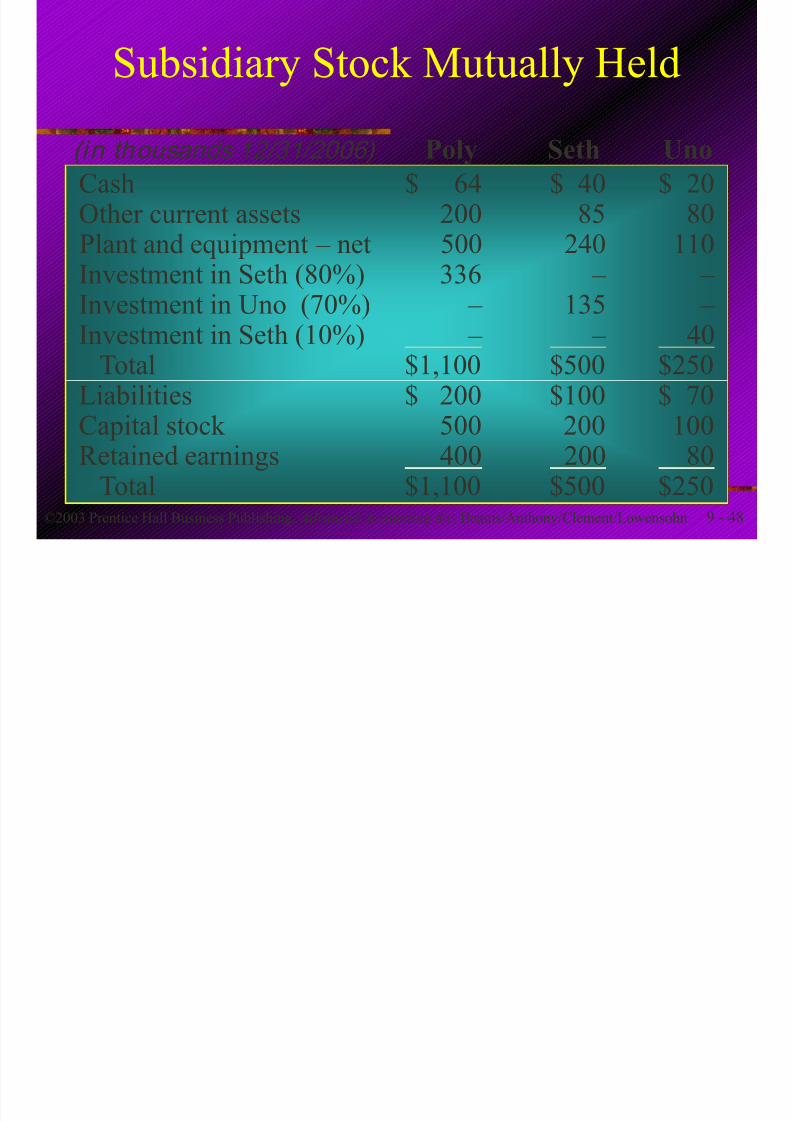

Subsidiary Stock Mutually Held

Cash $ 64 $ 40 $ 20Other current assets 200 85 80Plant and equipment – net 500 240 110Investment in Seth (80%) 336 – – Investment in Uno (70%) – 135 – Investment in Seth (10%) – – 40

Total $1,100 $500 $250Liabilities $ 200 $100 $ 70Capital stock 500 200 100Retained earnings 400 200 80

Total $1,100 $500 $250

(in thousands 12/31/2006) Poly Seth Uno

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 49/50

9 - 49©2003 Prentice Hall Business Publishing, Advanced Accounting 8/e, Beams/Anthony/Clement/Lowensohn

Subsidiary Stock Mutually Held

Poly 80% Seth 70% Uno 10%in Seth in Uno in Seth

Cost $260,000 $115,000 $40,000

Add: Income less

dividends (2005) 32,000 – –

Add: Income less

dividends (2006) 48,000 21,000 – Balance 12/31/2006 $340,000 $136,000 $40,000

7/16/2019 ch09-Advance Accounting-Mutual Holding

http://slidepdf.com/reader/full/ch09-advance-accounting-mutual-holding 50/50

End of Chapter 9

Related Documents