Did Enron fail because of illegal activities, falsified accounting, governance failure, or something else? Governance Failure at Enron

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Did Enron fail because of illegal activities,

falsified accounting, governancefailure, or something else?

Governance Failure at Enron

2-2

Governance Failure at Enron: Case Questions1. Which parts of the corporate governance system, internal

and external, do you believe failed Enron the most?

2. Describe how you think each of the individual stakeholders and components of the corporate governance system should have either prevented the problems at Enron or acted to resolve the problems before they reached crisis proportions.

3. If all publicly-traded firms in the United States are operating within the same basic corporate governance system as Enron, why would some people believe this was an isolated incident, and not an example of many failures to come?

2-3

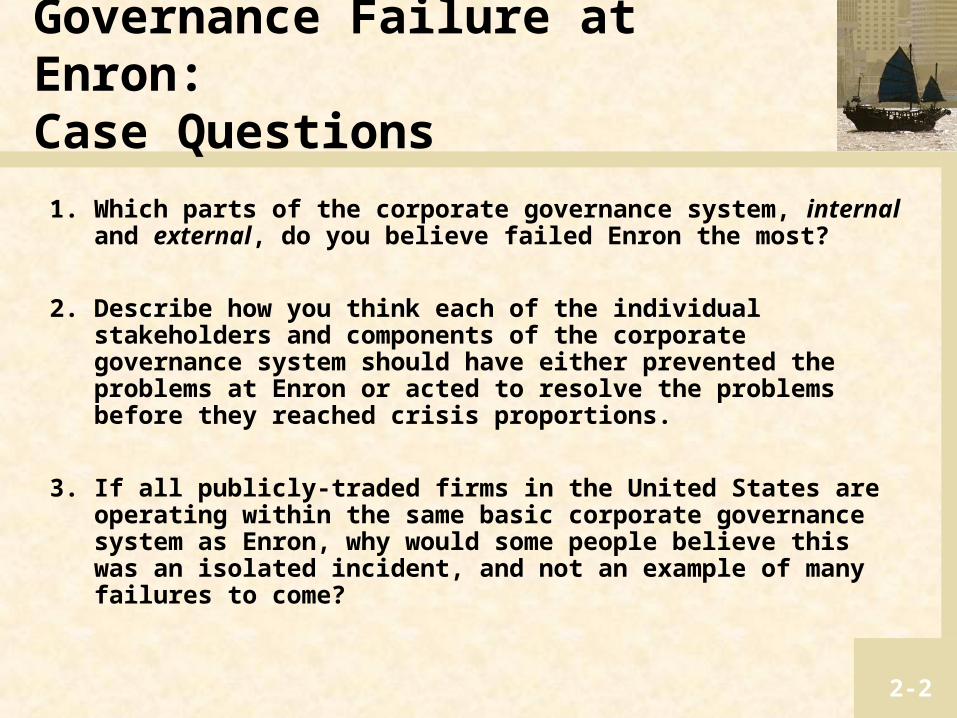

Exhibit 1 Enron’s Actual Operating Income

2-4

Report of Investigation

“The tragic consequences of the related-party transactions and accounting errors were the result of failures at many levels and by many people: a flawed idea, self-enrichment by employees,inadequately-designed controls, poor implementation,inattentive oversight, simple (and not-so-simple) accounting mistakes, and overreaching in a culture that appears to have encouraged pushing the limits. Our review indicates that many of these consequences could and should have been avoided.”

Special Investigative Committee of the Board of Directors of Enron CorporationFebruary 1, 2002

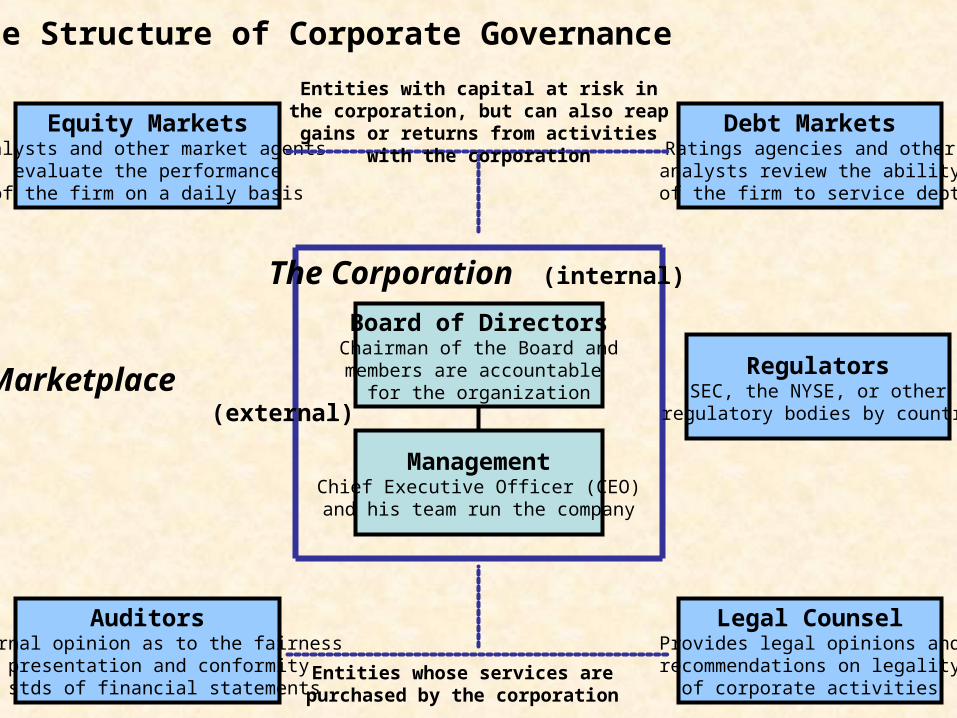

Board of DirectorsChairman of the Board andmembers are accountable

for the organization

ManagementChief Executive Officer (CEO)and his team run the company

The Corporation (internal)

The Marketplace (external)

Equity MarketsAnalysts and other market agents

evaluate the performanceof the firm on a daily basis

Debt MarketsRatings agencies and otheranalysts review the abilityof the firm to service debt

AuditorsExternal opinion as to the fairness

of presentation and conformity to stds of financial statements

RegulatorsSEC, the NYSE, or other

regulatory bodies by country

Legal CounselProvides legal opinions andrecommendations on legalityof corporate activities

Entities with capital at risk in the corporation, but can also reap gains or returns from activities

with the corporation

Entities whose services arepurchased by the corporation

The Structure of Corporate Governance

2-6

•Enron’s original business model consumed capital•The asset-heavy side of the business, power plants and pipelines, required massive amounts of capital up-front for their construction, yet would not generate cash in-flows for many years to cover (if ever)•As the asset-heavy businesses aged, they did not really produce the net operating cash in-flows which had been promised; as a result, Enron needed more and more capital to “feed the beast”•The asset-light side of the business, primarily power trading, required substantially less capital; trading is a service-oriented activity which does not require substantial capital infrastructure

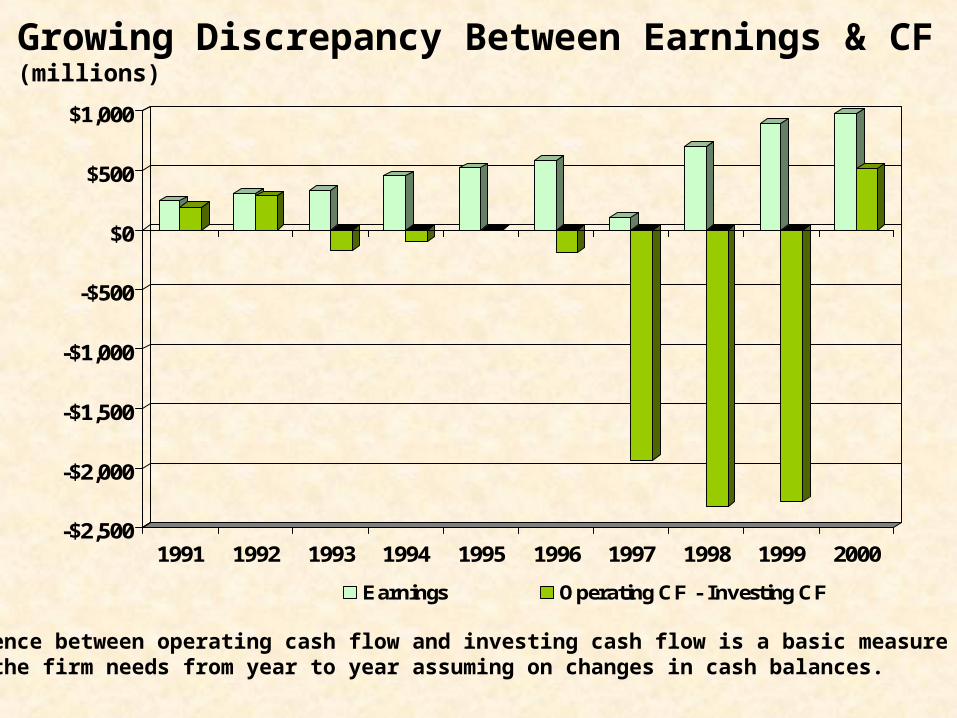

•Enron needed more and more capital to grow the business•But it had existed for most of its short corporate life as BBB-, on the edge of being considered “speculative grade” by the rating agencies given the industries it was operating in and its relatively high levels of debt•It therefore saw the Special Purpose Entities (SPE) as a way for the company to acquire more and more debt and yet not have that debt show up on its balance sheet – raising debt and hiding it in-short•The following exhibit illustrates the growing financing needs of the firm by simply illustrating how its statement of cash flows evolved over time

Discrepancy Between Earnings & Cash Flow

Growing Discrepancy Between Earnings & CF (millions)

-$2,500

-$2,000

-$1,500

-$1,000

-$500

$0

$500

$1,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000Earnings Operating CF - Investing CF

The difference between operating cash flow and investing cash flow is a basic measure of the addedFinancing the firm needs from year to year assuming on changes in cash balances.

2-8

Governance Failure at Enron: Case Questions1.Which parts of the corporate governance system, internal and

external, do you believe failed Enron the most?• The failures at Enron were so wide and deep, it is difficult to say which failed most. Clearly Enron’s leadership – its Board and senior executives, failed to protect all stakeholders in the company.

• Internally, although there were a few cases proven of malfeasance and illegal activities and fraudulent reporting, much of the internal failure appears to have been a combination of corporate culture failure and what many authors have characterized as “massive incompetence.”

• Externally, it appears that nearly every institution which is part of the U.S. governance system failed as a result of self-interest and greed.

• If pushed, it might be argued that the massive failures and internal culture of accounting earnings and self-enrichment at all costs led to a contagion of the external governance.

• Because many of Enron’s businesses such as power trading fell between the cracks of many regulatory systems, some failures were inevitable. In other cases, however, such as with its auditors and the debt and equity markets, the failures were in many cases related to the self-enrichment and profits at all costs culture which permeated many of these businesses inside and out.

2-9

Governance Failure at Enron: Case Questions

2.Describe how you think each of the individual stakeholders and components of the corporate governance system should have either prevented the problems at Enron or acted to resolve the problems before they reached crisis proportions.

•As it turns out, much of what Enron reported as earnings were not. Much of the debt raised by the company via a number of partnerships which was not disclosed in corporate financial statements should have been. •massive compensation packages and bonuses earned by corporate officers were inappropriate. •It appears that the executive officers of the firm were successful in managing the Board of Directors towards their own goals. Management had moved the company into a number of new markets in which the firm suffered substantial losses, resulting in redoubled attempts on their part to somehow generate the earnings needed to meet Wall Street’s unquenchable thirst for profitable growth. •The Board failed in its duties to protect shareholder interests due to lack of due diligence and most likely a faith in the officers which proved unfounded. It is also notable that Enron’s legal advisors, some of whom report to the Board, also failed to provide leadership on a number of instances of malfeasance.

2-10

Governance Failure at Enron: Case Questions

2. Describe how you think each of the individual stakeholders and components of the corporate governance system should have either prevented the problems at Enron or acted to resolve the problems before they reached crisis proportions (continued).

• Enron’s auditors, Arthur Andersen, committed serious errors in judgment regarding accounting treatment for many Enron activities including the above partnerships. Andersen was reported to have had serious conflicts of interest, earning roughly $5 million in auditing fees from Enron in 2001, but more than $50 million in consulting fees in the same year.

• Enron’s analysts were, in a few cases, blinded by the sheer euphoria over Enron’s latent successes in the mid to late 1990s, or working within investment banks which were earning substantial investment banking fees related to the complex partnerships. Although a few analysts continued to note that the company’s earnings seemed strangely large relative to the falling cash flows reported, Enron’s management was generally successful in arguing their point.

2-11

Governance Failure at Enron: Case Questions3. If all publicly-traded firms in the United States

are operating within the same basic corporate governance system as Enron, why would some people believe this was an isolated incident, and not an example of many failures to come?

• This may, in the end, be the most critical question related to Enron. Why did it happen? Was it indeed the “perfect storm,” in which the wrong combination of leadership, business evolution, market behaviors, and the ‘times’ all combined to create a monster, or was it something else?

• This is commonly the most hotly debated question in any classroom, and often is the concluding thought for further debate. Many argue that although many of the corporate governance and regulatory systems failed in the case of Enron, the core cause was human failure – the failure of leadership in many organizations to do the numbers, know the law, and do the right thing.

2-12

What Happened at Enron?

“What I can tell you straight up-front is that life hasn't been the same ever since the collapse. Working at Enron was like dope. You couldn't get enough of it. You're surrounded by talent, money is good, lavish expense accounts, and you're all on a race against a snowball called MTM - aka, the accounting magic called market-to-market! Pretty exciting, huh? Well, not if you were one of the thousands who ‘doubled or nothing’ their 401k’s on Enron... how's that for starters? I see the corporate world and life under a whole different light now. Unfortunately, I see Enrons everywhere. They are just not as good, and are probably still around because they are not as greedy as Skilling, Fastow and Lay.” --- A former Enron employee

Related Documents

![[Enron] New hire welcome binder (policies, org chart, tips, etc.)mattmg83.github.io/cynicalcapitalist/documents/[Enron... · 2019-09-27 · Enron Operator (71)853·6161 Enron Voice](https://static.cupdf.com/doc/110x72/5f1e01293cf2d927c4643421/enron-new-hire-welcome-binder-policies-org-chart-tips-etc-enron-2019-09-27.jpg)