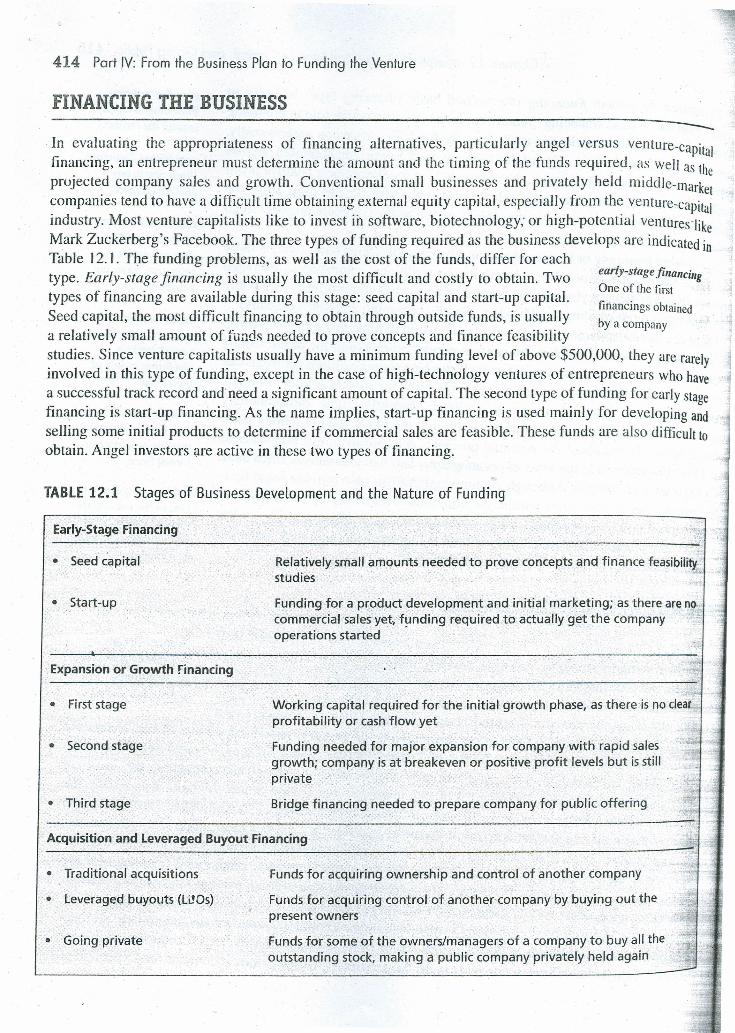

414 Part IV: From the Business Plan to Funding the Venture FINANCING THE BUSINESS --- In evaluating the appropriateness of financing alternatives, particularly angel versus venture-capital financing, an entrepreneur must determine the amount and the timing of the funds required, as well as the projected company sales and growth. Conventional small businesses and privately held middle-market companies tend to hav~ a difficult time obtaining external equity capital, especially from the venture-capital industry. Most venture capitalists like to invest in software, biotechnology; or high-potential ventures'like Mark Zuckerberg's Facebook. The three types of funding required as the business develops are indicatedin Table 12.1. The funding problems, as well as the cost of the funds, differ for each type. Early-stage financing is usually the most difficult and costly to obtain. Two types of financing are available during this stage: seed capital and start-up capital. SeedcapitaI, the most difficult financing to obtain through outside funds, is usually a relatively small amount of funds needed to prove concepts and finance feasibility early-stage financil/g . One of the first financings obtained by a company studies. Since venture capitalists usually have a minimum funding level of above $500,000, they are rarely involved in this type of funding, except in the case of high-technology ventures of entrepreneurs who have a successful track record and need a significant amount of capital. The second type of funding for early stage financing is start-up financing. As the name implies, start-up financing is used mainly for developing and selling some initial products to determine if commercial sales are feasible. These funds are also difficultto obtain. Angel investors are active in these two types of financing. Early-Stage Financing .. ] Relatively small amounts needed to prove concepts and finance feasibility~ studies ~- Funding for a product development and initial marketing; as there are no. commercial sales yet, fundinq required to actually get the company "~- operations started _ TABLE 12.1 Stages of Business Development and the Nature of Funding • Seed capital • Start-up \ • First stage " ." -.r . - .;i Working capital required for the initial growth phase, as there-is no clear ..: profitability or cash flow yet .• • Funding needed for major expansion for company with rapid sales;~ ,,;:, growth; company is at breakeven or positive profit levels but is still '---: private . i~ ;;- .. ~~ Bridge financing needed to prepare company for public offering .~~.~ , Expansion or Growth financing • Second stage • Third stage Acquisition and leveraged Buyout Financing • Traditional acquisitions Funds for acquiring ownership and control of another company Funds for acquiring control of another company by buying out the present owners Funds for some of the owners/managers of a company to buy all the. outstanding stock, making a public company privately held again .< -1 ~ " ,- , ...-. , - "i .~~. .~ 'l:: . ,; :;;:.7,;] ~ • Leveraged buyouts (WOs) • Going private

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

414 Part IV: From the Business Plan to Funding the Venture

FINANCING THE BUSINESS ---In evaluating the appropriateness of financing alternatives, particularly angel versus venture-capitalfinancing, an entrepreneur must determine the amount and the timing of the funds required, as well as theprojected company sales and growth. Conventional small businesses and privately held middle-marketcompanies tend to hav~ a difficult time obtaining external equity capital, especially from the venture-capitalindustry. Most venture capitalists like to invest in software, biotechnology; or high-potential ventures'likeMark Zuckerberg's Facebook. The three types of funding required as the business develops are indicatedinTable 12.1. The funding problems, as well as the cost of the funds, differ for eachtype. Early-stage financing is usually the most difficult and costly to obtain. Twotypes of financing are available during this stage: seed capital and start-up capital.SeedcapitaI, the most difficult financing to obtain through outside funds, is usuallya relatively small amount of funds needed to prove concepts and finance feasibility

early-stage financil/g. One of the first

financings obtainedby a company

studies. Since venture capitalists usually have a minimum funding level of above $500,000, they are rarelyinvolved in this type of funding, except in the case of high-technology ventures of entrepreneurs who havea successful track record and need a significant amount of capital. The second type of funding for early stagefinancing is start-up financing. As the name implies, start-up financing is used mainly for developing andselling some initial products to determine if commercial sales are feasible. These funds are also difficulttoobtain. Angel investors are active in these two types of financing.

Early-Stage Financing ..]

Relatively small amounts needed to prove concepts and finance feasibility~studies ~-

Funding for a product development and initial marketing; as there are no.commercial sales yet, fundinq required to actually get the company "~-operations started _

TABLE 12.1 Stages of Business Development and the Nature of Funding

• Seed capital

• Start-up

\

• First stage

" ."-.r .- .;i

Working capital required for the initial growth phase, as there-is no clear ..:profitability or cash flow yet .• •

Funding needed for major expansion for company with rapid sales;~ ,,;:,growth; company is at breakeven or positive profit levels but is still '---:private . i~

;;-..~ ~Bridge financing needed to prepare company for public offering .~~.~

, Expansion or Growth financing

• Second stage

• Third stage

Acquisition and leveraged Buyout Financing

• Traditional acquisitions Funds for acquiring ownership and control of another company

Funds for acquiring control of another company by buying out thepresent owners

Funds for some of the owners/managers of a company to buy all the.outstanding stock, making a public company privately held again

.< -1

~

",-,...-.,

- "i.~~.

.~ 'l::

.,;

:;;:.7,;]

~

• Leveraged buyouts (WOs)

• Going private

Chapter 12: Informal Risk Capital, Ventur.e Capital, and Going Public 415

Expansion or growth financing (the .second basic financing type) is easier tobtllinthan early-stage financing. Venture capitalists play an active role in providing

~ndShere. As the firm develops in each stage, the funds for expansion are less costly.Generally, funds in the first stage or this type are used as working capital to support. itial growth. In the second stage, the company is at breakeven or a positive profit::vel and uses the funds for major sales expansion. Funds in the third stage areusuallyused as bridge financing in the interim period as the company prepares to go

public.Acquisitionjinancing or leveraged buyout financing (the/third basic type) is more

specificin nature: It is issued for such activities as traditional acquisitions, leveragedbuyouts(management buying out the present owners), and going private (a publicly

- heldfirm buying out existing stockholders, thereby becoming a private company).- _ There are three risk-capital markets that can be used in tinancing a firm's growth:h,. ,

,·,the informal risk-capital market, the venture-capital market, and the public-equity,lJIarket.Although all three risk-capital markets can be a source of funds for stage-onefinancing, the public-equity market is available only for high-potential ventures,particularly when high technology is involved. Recently, some biotechnology

. companies raised their first-stage financing through the public-equity market since'investors were excited about the potential prospects and returns in this high-interestarea.This also occurred in the areas of oceanography and fuel alternatives when therewasa high level of interest. Although venture-capital firms also provide some first-

. stagefunding, the venture must require the minimum level of capital ($500,000). Aventure-capital company establishes this minimum level of investment due to thehigh costs in evaluating and monitoring a deal. By far the best source of funds forfirst-stage financing is the informal risk-capital market.

INFORMAL RISK-CAPITAL MARKET

growth financingFinancing to rapidlyexpand the business

acquisition financingFinancing to buyanother company

risk-capital marketsMarkets providingdebt and equity tononsecure financingsituations

informal risk-capitalmarket Area of risk-capital marketsconsisting mainly ofindividuals

venture-capital marketOne of the risk-capitalmarkets consisting offormal firms

public-equity marketOne of the risk-capitalmarkets consisting ofpublicly owned stocksof companies

The informal risk-capital market is the most misunderstood type of risk capital. Itconsists of (t virtually invisible group of wealthy investors, often called businessangels, who are looking for equity-type investment opportunities in a wide varietyof entrepreneurial ventures. Typically investing anywhere from $10,000 to$500,000, these angels provide the funds needed in all stages of financing, butparticularly in start-up (first-stage) financing. Firms funded from the informal risk-capital market frequentlyraise second-and third-round financing from professional venture-capital firms or the public-equity market.

Despite being misunderstood by, and virtually inaccessible to, many entrepreneurs, the informaliilVestment market contains the largest pool of risk capital in the United States. In India it is mostly thepersonal funds of the entrepreneur or the funds from friends and relatives. Although there is no verificationof the size of this pool or the total amount of financing provided by the business angels, related statisticsprovide some indication. A 1980 survey in the US of a sample of issuers of private placements by corpora-tions, reported to the Securities and Exchange Commission under Rule 146, found that 87 percent of thosebuying these issues were individual investors or personal trusts, investing an average of $74,000.2 Privateplacements fi led under Rule 145 average over $1 billion per year. Another indication becomes apparent onexamination of the filings under Regulation D-the regulation exempting certain private and limited offeringsfrom the registration requirements of the Securities Act of 1933, discussed in Chapter 11. In its first year, over7,200 filings, worth $15.5 billion, were made under Regulation D. Corporations accounted for 43 percent of

"business angelsA name for individualsin the informalrisk-capital market

AS SEEN IN BUSINESSWEEK

416 Part IV: From the Business Plan to Funding the Venture

OLD BANKS, NEW LENDING TRICKSThat didn't take Ib~g. T.he economy hasn't yet recovered from the impl~sion of risky investments that ledto the worst recession In decades-and already some of the world'~ biggest banks are peddling a negeneration of dicey products to corporations, consumers, and investors. . 'Ii

In recent months such big banks as Bank of America, Citigroup, and JPMorgan Chase have rolled Outnewfangled corporate credit lines tied to complicated and volatile derivatives. Others, including Wells Fargo.-and Fifth Third, are offering payday-loan programs aimed at cash-strapped consumers. Still others aremarketing new, potentially risky "structured notes" to small investors. .

There's no indication that the loans and instruments are doomed to .fail. If the economy keeps movingtoward recovery, as many measures suggest, then the new products might well work out for buyers anctsellers alike.. But it's another scenario that worries regulators, lawmakers, and consumer advocates: that banks onceagain are making dangerous loans to borrowers who can't repay them and selling toxic investments to'investors who don't understand the risks-all of which could cause blowups in the banking sector and~weigh on the economy.

Some of Wall Street's latest innovations give reason for pause. Consider a trend in business loans.Lenders typically tie corporate credit lines to short-term interest rates. But now Citi, JPMorgan Chase, andBofA, among others, are linking credit lines both to short-term rates and credit default swaps (CDSs),thevolatile and complicated derivatives that are supposed to act as "insurance" by paying off the owners ifcompany defaults on its debt. JPMorgan, BofA, and Citi declined to comment.

In these new arrangements, when the price of the CDS rises-generally a sign the market thinks thcompany's health is deteriorating-the cost of the loan increases, too. The result: The weaker the compan~the higher the interest rates it must pay, which hurts the company further.

The lenders stress that the new products give them extra protection against default. But for companithe opposite may be true. Managers now must deal with two layers of volatility-both short-term interestrates and credit default swaps, whose prices can spike for reasons outside their control.. At the other end of the borrower spectrum, big banks are entering another controversial arena: payday.loans, whose interest rates can run as high as 400%. Historically the market has been dominated by small'nonbank lenders, which mainly operate ln poor urban centers and offer customers an advance on their.paychecks. But big lenders Fifth Third and US Bancorp started offering the loans, while Wells Fargo.continues to boost its payday-loan program, which it began in 1994.

More big banks ale getting into the market just as a recent flurry of usury laws has crippled srnalle ~players. In the past two years lawmakers in 15 states have capped interest rates on short-term loans or-'kicked out payday lenders altogether. The state of Ohio, for example, has imposed a 28% interest rate.limit. But thanks to interstate commerce rules, nationally chartered banks don't have to follow local rules. ,After Ohio limited rates, Cincinnati-based Fifth Third, which has 400 branches in the state but also 'operatesin 11 others, introduced its Early Access Loan, with an annual interest rate of 120%. "These banks are skirting_state laws," says Kathleen Day of advocacy group Center for Responsible Lending. Says a spokeswoman for~Fifth Third: "Our Early Access product fully complies with federal regulations and applicable state regulations.'"

Lenders argue they offer a valuable service for those who need emergency cash. Wells Fargo says it warnscustomers using its Direct Deposit Advance that the loan is expensive and tries to offer alternatives. "We·have policies in place to prevent long-term usage of the services," says a spokeswoman. US Bancorp didn'treturn calls. '

National regulators are taking notice; however. The Office of Thrift Supervision says it is "looking into"two institutions that are offering the tiigh-interest loans. "We need to make sure there's no predatorylending and also ensure that there are no risks to the institutions," says an OTS spokesman.

Source: Reprinted from August 17,2009 issue of BusinessWeek by special permission, copyright © 2009 by The McGraw-Hili ':.Companies, Inc., "Old Banks, New Lending Tricks," by Jessica Silver-Greenberg, Thco Francis, and Ben Levisohn, pr. 20-23.

Chapter 12: Informal RiskCapital, Venture Capital, and Going Public 417

'value ($6.7 billion), or 32 percent of the total number of offerings (2,304). Corporations filing limited:;erings (under $500,000) ~ais~d $220 million, an average of $200.,000 per firm. The typical corporate:SSuers tended to be small, with fewer than 10 stockholders, revenues and assets less than $500,000, stock-I Iders' equity of $50,000 or less, and five or fewer employees."/JO Similar results were found in an examination of the funds raised by small technology-based firms prior totheirinitial public offerings. The study revealed that unaffiliated individuals (the informed investment market)accountedfor 15 percent of these funds, while venture capitalists accounted for only 12 to IS percent. Duringthestart-up year, unaffiliated individuals provided 17 percent of the external capital." ,

~,Astudy of business angels in New England again yielded similar results. The 133 individual investorsstudiedreported risk-capital investments totaling over $16 million in 320 ventures between 1976 and 1980.Theseinvestors averaged one deal every two years, with an average size of $50,000. Although 36 perc 'nt oftheseinvestments averaged less than $10,000, 24 percent averaged over $50,000. While 40 percent of theseinvestmentswere start-ups, 80 percent involved ventures less than five years old."

The size and number of these investors have increased dramatically, due in part to the rapid accumulationQfwealthin various sectors of the economy. One study of consumer finances found that the net worth of 1.3millionUS families was over $1 million." These families, representing about 2 percent of the population,accumulated mOSIof their weaith from earnings, not inheritance, and invested over $151 billion in nonpublicbusinessesin which they have no management interest. Each year, over 100,000 individual.investors financebetween30,000 and 50,000 firms, with a total dollar investment of between $7 billion and $10 billion. Giventheirinvestment capability, it is important to know the characteristics of these angels.

One article determined that the angel money available for investment each year was about $20 billion."Thisamount was confirmed by another study indicating that there are about 250,000 angel investors whoinvestan amount of $10 biliion to $20 billion annually in about 30,000 firms. R A recent study found that onlyabout20 percent of the angel investors surveyed tended to specialize in a particular industry, with the typicalinvestmentin the first round bei ng between $29,000 to over $100,000.9

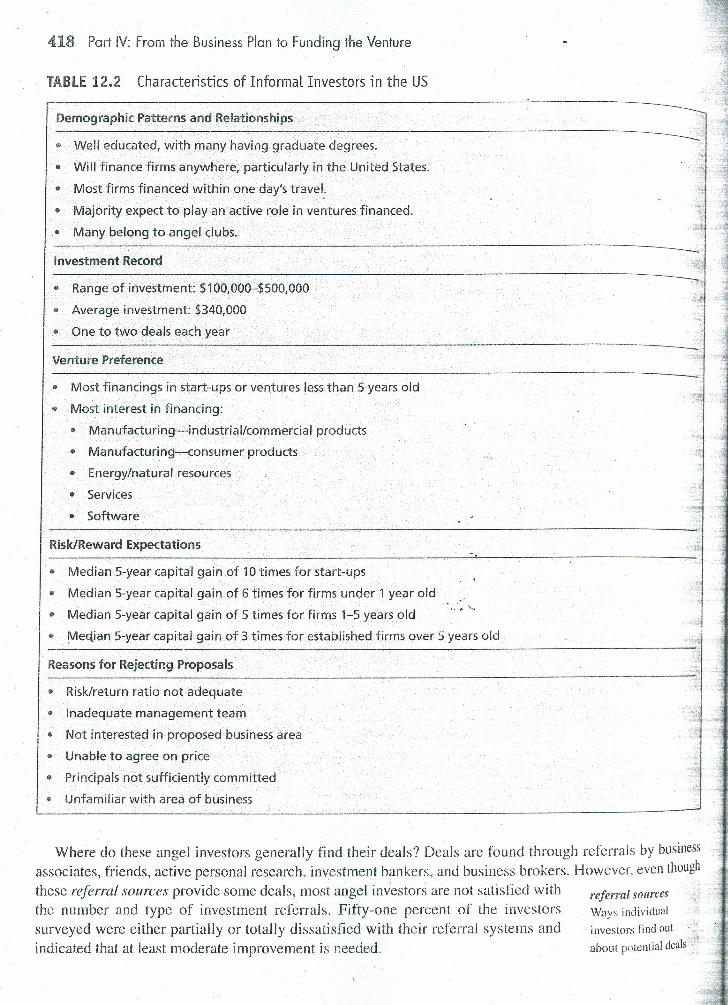

The characteristics of these informal investors, or angels, are indicated in Table 12.2. They tend to be welleducated;many have graduate degrees. Although they will finance firms anywhere in the United States (andafewin other parts of the world), most of the firms that receive funding are within one day's travel. Businessangelswill make one to two deals each year, with individual firm investments ranging from $100,000 to$500,000ami the average being $340,000. If the opportunity is right, angels might invest from $500,000 to$1million. In some cases, angels will join with other angels, usually from a common circle of friends, tofinancelarger deals.

Is there a preference for the type of ventures in which they invest? Whileangels invest in every type ofinvestment opportunity, from small retail stores to large oil exploration operations, some prefer manufac-turing of both industria! and consumer products, energy, service, and the retail/wholesale trade. Thereturns expected decrease as the number of years the firm has been in business increases, from a medianfive-year capital gain of j 0 times for start-ups to 3 times for established firms over five years old. Theseinvesting angels are more patient in their investment horizons and do not have a problem waiting for aperiod of 7 to 10 years before cashing out. This is in contrast to' the more predominant five-year timehorizon in the formal venture-capital industry. Investment opportunities are rejected when there is aninadequate risk/return ratio, a subpar management team, a lack of interest in the business area, or insuffi-cientcommitment to the venture from the principals. ,, The angel investor market averages about $20 billion each year; which is about the same level of yearlyInvestment of the venture-capital industry. The angel investment is in about eight times the number ofcompanies. In normal economic conditions, the number of active investors is around 2S0,000 individuals intheUnited States, with five or six investors typically being involved in an. investment.

418 Part IV: From the Business Plan to Funding the Venture

TABLE 12.2 Characteristics of Informal Investors in the US

Demographic Patterns and Relationships .

II Well educated, with many having graduate degrees.

• Will finance firms anywhere, particularly in the United States.

• Most firms financed within one day's travel;

• Majority expect to play an active role in ventures financed.

• Many belong to angel clubs.

Where do these angel investors generally find their deals? Deals are found through referrals by businessassociates, friends, active personal research, investment bankers, and business brokers. However,even thoughthese referral sources provide some deals, most angel investors are not satisfied with referral sourcesthe number and type of investment referrals. Fifty-one percent of the investors Ways individualsurveyed were either partially or totally dissatisfied with their referral systems and investors find out

"l~indicated that at least moderate improvement is needed. about potential deals !.' .,

Investment Record

• Range of investment: $100,000-$500,000

•• Average investment: $340,000

• One to two deals each year

Venture Preference

•• Most financings in start-ups or ventures lessthan 5 years old

•• Most interest in financing:

• Manufacturing-industrial/commercial products

• Manufacturing--consumer products

• Energy/natural resources

• Services

• Software

Risk/Reward Expectations

• Median 5-year capital gain of 10 times for start-ups

•• Median S-year capital gain of 6 times for firms under 1 year old

•• Median 5-year capital gain of 5 times for firms 1-5 years old

• Median 5-year capital gain of 3 times for established firms over 5 years old

...."",

. Reasons for Rejecting Proposals

• Risk/return ratio not adequate

• Inadequate management team

•• Not interested in proposed business area

• Unable to agree on price

•• Principals not sufficiently committed

• Unfamiliar with area of business

Chapter 12: Informal Risk Capital, Venture Capital, and Goin.9 Public 419

A phenomenon that is spreading throughout the United States is "brands" of angels or organized angel. vestof groups. Each angel group or club usually has a meeting for about two to three hours about 8 to 101~ es each year. Some groups are now starting to co-invest with other groups. The group as a whole does not:e any ~oney but serves as .a convening. and. sCI:e~ning devic~ for the ~resentati~ns. TI~e individu~1membersof the group make the investment either individually or with others interested If any mvestment IS

made. . .'The typical club process is that you send the required form to the designated club member. Following

iiUtialscreening, if the entrepreneur is chosen, then follow-up meetings with several club members occur. If~lhe entrepreneur is selected to present at a future meeting, then the entrepreneur is provided guidance in terms

of business plan refinement and the presentation. Usually 30 minutes is allocated for a presentation andquestions, and then any interested club members meet with the entrepreneur to discuss further steps in theinvestment decision process. Approximately 200 organized angel investor groups are identified by theKauffman Foundation (www.kauffman.org).

In several cases, these organized clubs have spawned an angel fund, which is a pool of money dedicated-toa specific region and several industries. The fund size is between $5 and $lO million. The few angel fundsin existence operate very much like university-sponsored venture-capital funds, which will be discussed laterinthis chapter.

Business angels in India are not as well organized as in the West. However, with the arrival of the Internet,ihere are many web-based enterprises that offer 'match-making' services for entrepreneurs and angelinvestors. Some examples of such service providers are: Indian Angel Network (IAN) (www.indianangel-network.com); Angel Investment Network (www.investmentnetwork.in); Venture Giant lndia (www.venturegiant.co.in); and Angel Investment India (www.angelinvestrnent.co). While these companies. arecreatedfor providing investment support to Indian entrepreneurs, the angel investors in their network are fromother countries as well. Please refer to the homepage of Indian Angel Network (www.indianangelnetwork.com/index.aspx) in order to have an idea of the types of enterprises that are likely to receive angelinvestment, its services, and stipulations.

VENTURE CAPITAL

The important and little understood area of venture capital will be discussed in terms of its nature, theventure-capital industry in the United States, and the venture-capital process. '

Nature of Venture CapitalVenturecapital is one of the least understood areas in entrepreneurship. Some thinkthat venture capitalists do the early-stage financing of relatively small, rapidlygrowing technology companies. It is more accurate to view venture capital broadlyas a professionally managed pool of equity capital. Frequently, the equity pool isformed from the resources of wealthy limited partners. Other principal investors in venture-capital limitedpartnerships are pension funds, endowment funds, and other institutions, including foreign investors. Thepool is managed by a general partner-that is, the venture-capital firm-in exchange for a percentage of thegain realized on the investment and a fee. The investments are in early-stage deals as well as second- and~hird-stage deals and leveraged buyouts. In fact, venture capital can best be characterized as a long-termIOVestmentdiscipline, usually occurring over a five-year period, that is found in the creation of early-stagecompanies, the expansion and revitalization of existing businesses, and the financing of leveraged buyouts ofeXisting divisions of major corporations or privately owned businesses. In each investment, the venture

equity pool Money :

raised by venturecapitalists to invest

420 .Part IV: From the Business Plan to Funding the Venture

AS SEEN IN BUSINESSWEEK --SHE'S AN ANGELBarbara Boxer, a practicing attorney in Milwaukee, knows just how difficult it can be for women entrepre.neurs to raise money. She ran her own rnail-order.medical supply company for 20 years before selling it in1990, and now many of her clients are women who own businesses. After participating in a conference for

. women trying to raise funding, the 56-year-old decided to take matte~s into her own hands. Last summer,Boxer started Women Angels, a group of women investors that focuses on women-owned businesses in theMidwest. Now the group's 22 members are getting ready to make their first investments. They will put ~$150,000 to $500,000 in each of two companies, one in biotech and one in transportation.

Boxer is part of a small but growing legion of women angel investors, who are using their own moneyto back young companies. Often, those are companies led by women. "We're seeing more women entre.preneurs who are cashing out of their businesses," says Jeffrey Sohl, a professor of entrepreneurship at theUniversity of New Hampshire. "The more women who are successful in business, particularly in entrepre.neurship, the more women angels we're likely to see." That's because the prime candidates to be angelinvestors are former entrepreneurs, There are at least six women-focused angel groups in the U.S., with anadditional dozen or so just getting started, according to a recent report from the Kauffman Foundation.

Angels are a rich source of capital for entrepreneurs. Last year, 225,000 angels invested $23.1 billion inroughly 49,500 deals, according to the Center for Venture Research. Women represented 9% of thatgroup,up from 5% in 2004. Part of that increase is coming from new women-led investment groups, but there'sstill plenty of room for growth. Women not only control 50% of the country's wealth, but they alsorepresent an increasing percentage of entrepreneurs. About half of private companies are majority-ownedby women, according to the Center for Women's Business Research.

Why aren't there more women angel groups? There are plenty of reasons. For one, only about15%-20% of angels are organized into groups at all, with the rest investing on their own. Angel investorstend to be serial entrepreneurs, and serial entrepreneurs tend to be men. Social networks also playa role,since angel groups usually form around investors' social circles. "Men tend to socialize and affiliate withpeople they do business with," says Maggie Kenefake, manager of growth entrepreneurship for theKauffman Foundation. "If you look at women, their networks are more social, philanthropic, or family-based."

Just because many women are new to the investment game, it doesn't mean they're any less discerning. than men. Although women angels actively seek out, and tend to attract, more women entrepreneurs, thegroups conduct the same amount of due diligence and ultimately fund companies at the same (ate as mendo, roughly 10% of the proposals they see. And while many of these new groups have every intention ofhelping other women entrepreneurs, being an angel is, in the end, still an investment decision. SaysBoxer:"This isn't about altruism. It's about making money."

Source: Reprinted from Summer 2006 Small Biz Supplement issue of BusinessWeek by special permission. copyright © 2006 byThe McGraw-Hill Companies, Inc., "She's an Angel," by Adrienne Carter, p. 34.

capitalist takes an equity participation through stock, warrants, and/or convertiblesecurities and has an active involvement in the monitoring of each portfolio company,bringing investment, financing planning, and business skills to the firm.

equity participationTaking an ownership

position

Overview of the Venture-Capital IndustryAlthough venture capitalists were a major source of financing throughout the industrialization of the UnitedStates, the system did not become institutionalized until after World War II. Before World War II, venture-

Chapter 12: Informal RiskCapital, Venture Capital, and Going Public 421

'tal investment activity was a monopoly led by wealthy individuals, investment banking syndicates, and aCapl family organizations with a professional manager. The first step toward institutionalizing the venture-feWitalindustry took place in 1946 with the formation of the American Research and Development CorporationC~D) in Boston. The ARD had a small pool of capital from individuals and institutions put together by~neral Georges Doriot to make active investments in selected emerging businesses.

- The next major development, the Small Business Investment Act of 1958, marriedovate capitai with government funds to be used by professionally managed small-

~siness investment companies (SBIC firms) to infuse capital into start-ups andgrowingsmall businesses. With their tax advantages, govern~ent funds for leverage,and status as a private-capital company, SBICs were the start of the now formal

enture-capital industry. The 1961):; saw a significant expansion of SBICs with thev .approvalof approxim~t~ly 585 SB~C licen.ses that inv~l~ed more than $205 million in priva~e capit~1. Manyofthese early SBICs failed due to inexperienced portfolio managers, unreasonable expectations, a focus onshort-term profitability, and an excess of government regulations. These early failures caused the SBICprogram to be restructured,. which. in turn eli)~inated some of t.he unnecessary governm~nt reglilatil~ns ~ndIncreased the amount of capitalization needed. There are approximately 360 SBICs operaung today, of which130 are minority enterprise small-business investment companies (MESBICs) funding minority enterprises.

During the late 1960s. small private venture-capita! firms emerged. 10 These wereusuallyformed as limited partnerships, with the venture-capita! company acting asthegeneral partner that received a management fee and a percentage of the profits

. earned on a deal. The limited partners, who supplied the funding, were frequently. institutional investors such as insurance companies, endowment funds, bank trustdepartments, pension funds, and wealthy individuals and families. There are over 900ofthis type of venture-capital establishment in the United States.

Another type of venture-capital firm was also developed during this time: the venture-capital division ofmajorcorporations. These firms, of which there are approximately 100, are usually associated with banks andinsurance companies, although companies such as 3M, Monsanto, Xerox, Intel, and Unilever house suchfirmsas well. Corporate venture-capital firms are more prone to invest in windows on technology or newmarketacquisitions than are private venture-capital firms or SBICs. Some of these corporate venture-capitalfirmshave not had strong results.

In response to the need for economic development, a fourth type of venture-capital firm has emerged in the form of the state-sponsored venture-capitalfund,Thesestate-sponsored funds have a variety of formats. While the size and investmentfocusand industry orientation vary from state to state, each fund typically is requiredto invest a certain percentage of its capital in the particular state. Generally, thefunds that are professionally managed by the private sector, outside the state'sbureaucracy and political processes, have performed better.

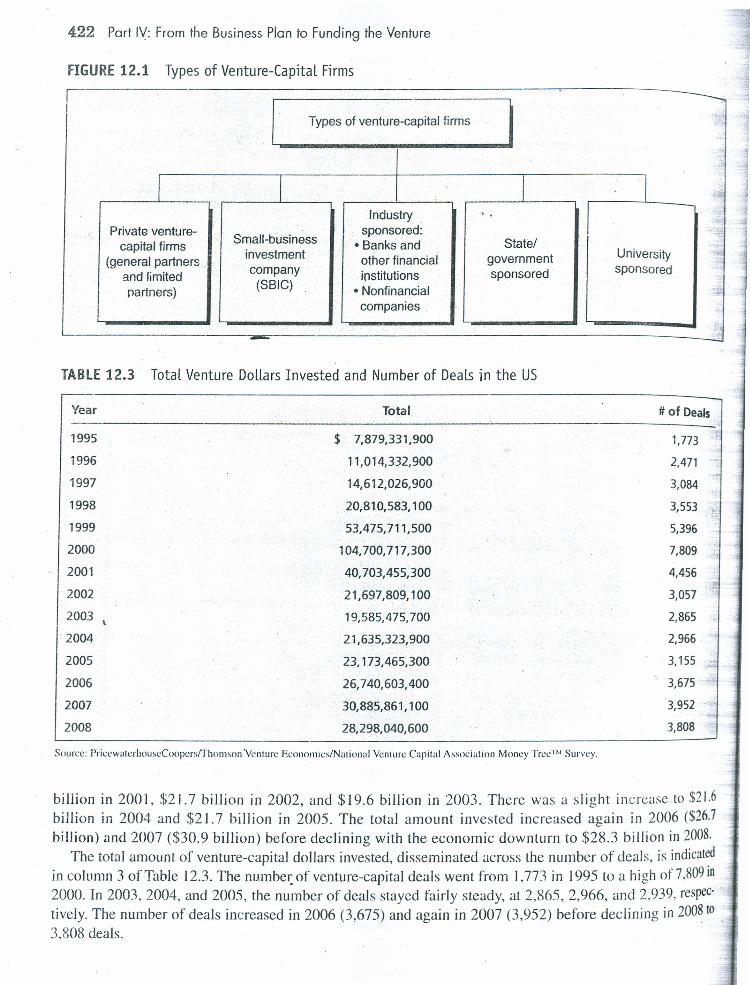

An overview of the types of venture-capital firms is indicated in Figure 12. I. Besides the four types previ-ously discussed, there are now emerging university-sponsored venture-capital funds. These funds, usuallymanaged as separate entities, invest in the technology of the particular university. At such schools as Stanford,Columbia, and MIT, students assist professors and other students in creating business plans for funding as wellas assisting the fund manager in his or her due diligence, thereby learning more about the venture-fundingprocess.

The venture-capital industry has not returned to the highest level or dollars invested in 1999,2000, and2001. While the total amount of venture-capital dollars invested increased steadily from $7.8 billion in1995 to a high of $104.7 billion in 2000 (see Table 12.3), "the total dollars invested declined to $40.7

SRlCfirms Small

companies with some

govcmmeut money

that invest in other

companies

private venture-capitalfirms A type ofventure-capital linn

having general andlimited partners

state-sponsoredventure-capita/fundA fund containingstate government

money that invests

primarily ill

companies in the state

422 Part I'{ From the Business Plan to Funding the Venture

FIGURE 12.1 Types of Venture-Capital Firms----------------------------------------------------------~-----------------

Types of venture-capital firms

I I I IIndustry . .'

Private venture-Small-business

sponsored:capital firms • Banks and State/

(general partners ,investment other financial government University

and limited company institutions sponsored sponsored

partners) (SBIC) • Nonfinancialcompanies .

•••••••

TABLE12.3 Total Venture DoLLarsInvested and Number of Deals in the US

Year Total # of Deals

$ 7,879,331,900 1,773

11,014,332,900 2,471

14,612,026,900 3,084

20,810,583,100 3,553« r:

53,475,711,500 5,396

104,700,717,300 7,809

40,703,455,300 4,456

21,697,809,100 3,057

19,585,475,700 2,865

2.1,635,323,900 2,966

23,173,465,300 3,155

26,740,603,400 3,675

30,885,861,100 3,952

28,298,040,600 3,808

1995

1996

1997

1998

1999

2000

2001

2002

2003

, 2004

2005

2006

2007

2008

Source: Priccwaterhousef.oopcrs/Thomson Venture Economics/Nauonal Venture Capital Association Money Tree"''' Survey,

billion in 200L $21.7 billion in 2002, and $19.6 billion in 2003. There was a slight increase to $21.6billion in 2004 and $21.7 billion in 2005. The total amount invested increased again in 2006 ($26.7billion) and 2007 ($30.9 billion) before declining with the economic downturn to $28.3 billion in 2008.

The total amount of venture-capital dollars invested, disseminated across the number of deals, is indicatedin column 3 of Table 12.3. The number of venture-capital deals went from 1,773 in 1995 to a high of7 ,809in2000. In 2003, 2004, and 2005, the number of deals stayed fairly steady, at 2,865,2,966, and 2,939. respec-tively. The number of deals increased in 2006 (3,675) and again in 2007 (3,952) before declining in 2008to ,3,808 deals.

Chapter 12: Informal Risk Capital, Venture Capital, and Going Public 423

These deals concentrated in three primary areas in 2008: software-$4,919 million (17 percent), indus-. Venergy-$4,65I million (16 percent), and biotechnology-$4,500 million (16 percent). This investment

Ifl:significantly impacted the growth and development of these three industry sectors. As indicated in Figure~~.2,other industry are.as. receiving venture-capit.al investment 1~1cJudethe followin~: .medical devices andequipment-$3,460 .~I1llOn (12 percent), media ~nd. entertamment-. $~,039 million (7 percent?, IT

, rvices-$1,832 million (6 percent), telecommunications=-S'l.oxx million (6 percent), and sermcon-:Uctors-$ 1,651 million (6. percent).

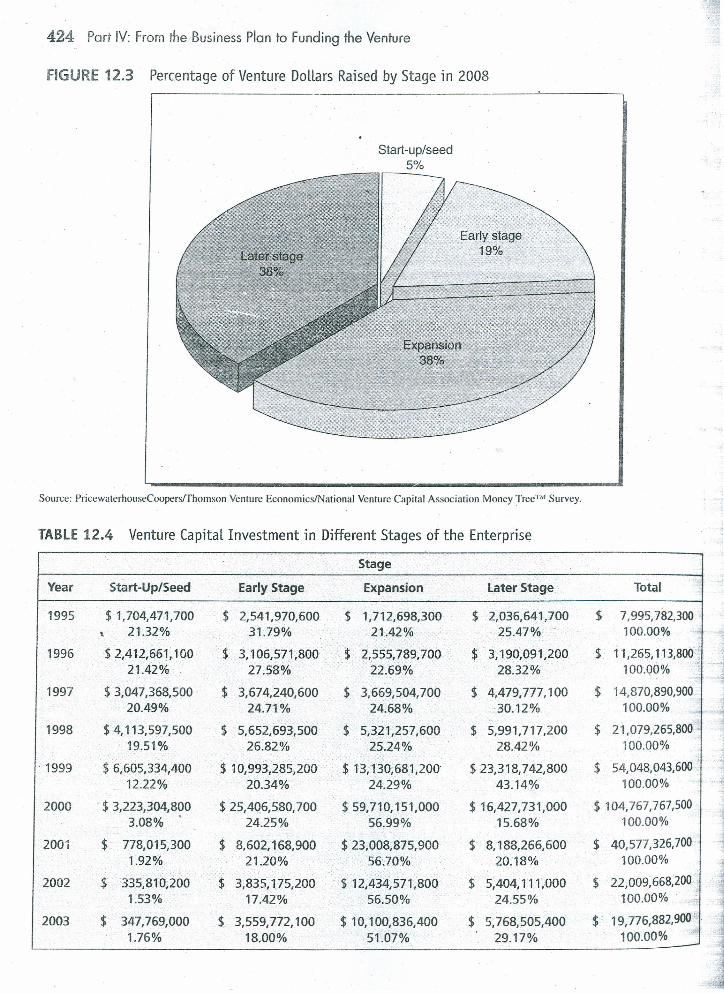

At what stage of the business development is this money invested? The percentage of venture-capital. oneyraised by stage of the venture in 2008 is indicated in Figure 12.3. The largest amount of money raised

1 :as for later-stage and expansion-stage investments (38 percent), followed by early-stage (19 percent), andstart-up/seed stage (5 percent). Traditionally the largest amount of money raised is for expansion-stageinvestment. In 2002, for example, 57 percent of the venture money raised was for expansion, followed byearlystage (23 percent), later stage (18 percent), and start-up (2 percent) .

.The money invested by stage and year from 1995 to 2008 is broken down in Table 12.4. Venture-capital_ m~neyinvested at the start-up/seed stage (for seed capital) went from $1,704 million in 1995 to a high of

$6,605 million in 1999, before declining to a low of $335 million in 2002. The amount invested in this early-stagearea increased to $1,268 million in 2007 and again to $1.510 million in 2008. Venture capitalists in 2008showeda significant interest in funding start-up/seed capital deals. despitethe economic downturn .

•1fIGURE 12.2 Percentage of Venture Dollars Invested in 2008 by Industry Sector

IT services, 6.47% .

II Numbersrounded to the nearest whole percent. ,

Source: PricewaterhouseCoopers/Tholllson Venture Economics/National Venture Capital 'Association Money Tree! Survey.

Biotechnology, 15.90% '

Industrial/energy,16.44%

Media and entertainment,7.21%

Sbftware,17.38%

Other, 0.5%

Health care services, 0.69%. Retailing/distribution, 0.95%

Computers andperipherals, 1.45%

Consumer products andservices. 1.54%Business products andJ

services, 1.70% JFinancial services, 1.89%

Telecommunications, 5.97%

Semiconductors, 5.83%Networking and equipment,

2.28%

Electronics/instrumentation,2.02%

424 Port IV: From the Business Plan to Funding the Venture

FIGURE 12.3 Percentage of Venture Dollars Raised by Stage in 2008

Start-up/seed5%

Source: Pricewaterhousef'oopers/Thornson Venture Economics/National Venture Capital Association Money Treenl Survey.

TABLE 12.4 Venture Capital Investment in Different Stages of the Enterprise" Stage

Year Start-Up/Seed Early Stage Expansion later Stage Total

1995 $ 1,704,471,700 $ 2,541,970,600 $ 1,712,698,300 $ 2,036,641,700 $ 7,995,782,30021.32% 31.79% 21.42% 25.47% '. 100.00%\-

1996 $ 2,412,661; 100 $ 3,106,571;800 $ 2,555,789,700 $ 3,190,091,200 $ 11,265,113,80021.42% 27.58% 22.69% 28.32% 100.QO%

1997 $ 3,047,368,500 . $ 3,674,240,600 $ 3,669,504,700 $ 4,479,777,100 $ 14,870,890,90020.49% 24.71 % 24.68% -30.12% 100.00%

1998 $ 4,113,597,500 $ 5,652,693,500 $ 5,321,257,600 $ 5,991,717,200 $ 21,079,265,80019.51% 26.82% 25.24% 28.42% 100.00%

. 1999 $ 6,605,334,400 $ 10,993,285,200 $ 13,130,681,200' $ 23,318,742,800 $ 54,048,043,600 ..12.22% 20.34% 24.29% 43.14% 100.00%

2000 -$ 3,223,304,800 $ 25,406,580,700 $ 59,710,151,000 $ 16,427,731,000 $ 104,767,767,5003.08% 24.25% 56.99% 15.68% 100,00%

2001 $ 778,015,300 $ 8,602,168,900 $ 23,008,875,900 $ 8,188,266,600 $ 40,577,326,700 ,1.92% 21.20% 56.70% 20.18% 100.00%

2002 $ 335,810,200 $ 3,835,175,200 $ 12,434,571,800 $ 5,404,111,000 $ 22,009,668,2001.53% 17.42% 56.50% 24.55% 100.00% !

2003 $ 347,769,000 $ 3,559,772,100 $ 10,100,836,400 $ 5,768,505,400 $ 19,776,882,900" .1.76% 18.00% 51.07% 29.17% 100.00% - i'

1~

Chapter 12: Informal RiskCcpitol, Venture Capital, and Going Public 425

$ 470,124,200 $ 4,011,236,300 $ 9,165,044,300 $ 8,821,753,200 $ 22,468,158,0002.09% 17.85% 40.79% 39.26% . 100.00%

$ 897,707,300 $ 3,819,745,600 $ 8,663,870,300 $ 9,792,142,100 $ 23,173,465,3003.87% 16.48% 37.39% 42.26% 100.00%

$ 1,177,319,200 $ 4,172,001,400 $ 11,521,031,400 $ 9,870,251,400 $ 26,740,603,4004.40% 15.60% 43.08% 36.91 % 100.00%

. $ 1,267,968,200 $ 5,486,760,800 $ 11,677,215,200 $ 12,453,916,900 $ 30,885,~61,1004.11% 17.76% 37.81% 40.32% 100.00%

$ 1,509,963,800 $ 5,339,272,800 $ 10,604,468,700 $ 10,844,335,300 $ 28,298,040,600·5.34% 18.87% 37.47% 38.32% 100.00%

Source:PncewaterhouseCoopersrrhomson Venture Economics/National Venture Capital Association Money Treen! Survey.

Venture-Capital Investments by Region (2008)

# of Companies· % $ Invested (in millions) %r_SiliconValley' 1,170 ·30.72% $10,980 38.80%

!:New England 460 12.08 $ 3,260 11.52

. WOrange County 237 6.22 $ 1,994 7.05

NY Metro 308 8.09 ; $ 1,879 6.64

267 7.01 $ 1,348 4.76

146 3.83 $ 1,283 4.53

207 5-44 $ 1,240 4.38

126. 3.31 $ 1,217 4.30

208 5.46 $ 1,160 4.10

190 4.99 $ 1,015 3.59

100 2.63 $ 813 2.87

hilade1phiaMetro 140 3.68 $ 750 2.65

NorthCentral 77 2.02 $ 623 2.20

78 2.05 $ 484 1.71,

29 0.76 $ 88 0.31

19 0.50 $ 73 0.26

38 1.00 $ 71 0.25

8 0.21 $ 21 0.07

GrandTotal 3,808. 100.0 % $28,299 100.0%,

Source:PricewaterhouseCoopersrrhomson Venture EconomicslNational Venture Capital Association Money Tree" Survey.

Wheredo these deals take place? Table 12.5 shows the amount of money invested in 2008 ($28.2 billion)by the regions of the United States. It should come as no surprise that the areas receiving the largest amountof venture capital were the Silicon VaIIey-$lll. 7 billion in 1,170 companies (31 percent), and NewEngland-$3.3 billion in 460 companies (12 percent). Other areas receiving funding were metro New York-

\ $1.9billion in 308 companies (8 percent), Los Angeles/Orange County-$1.9 billion in 237 companies (6percent),and the Midwest-$1.3 billion in 2('J7companies (7 percent). .

426 Part IV: From the Business Plan to Funding the Venture

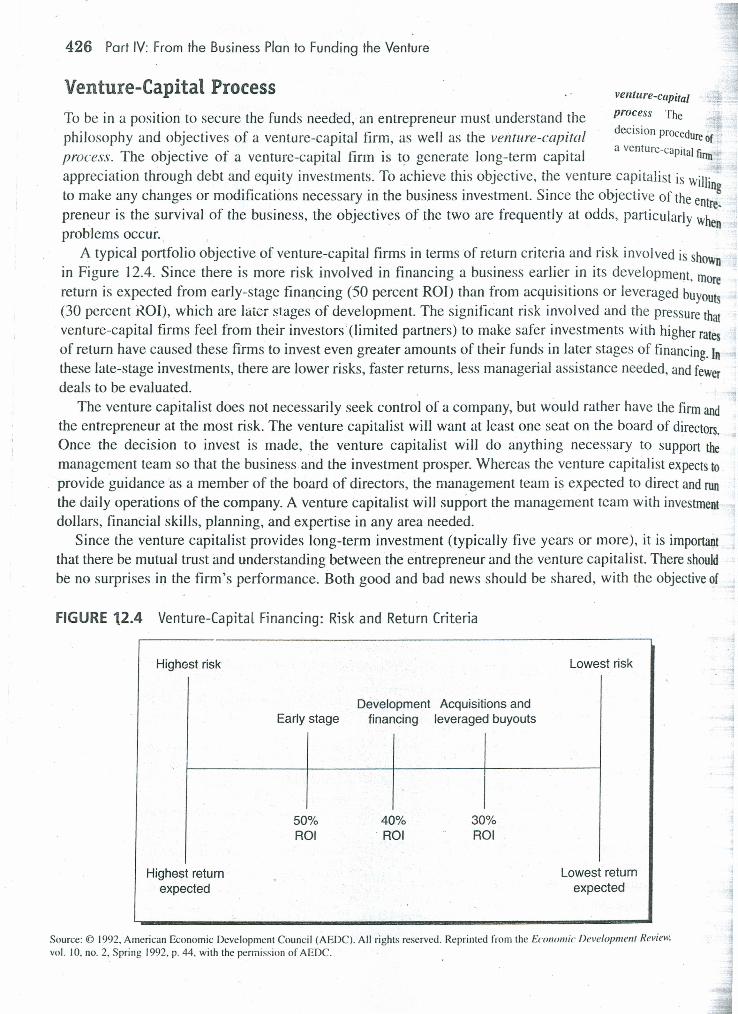

Venture-Capital Process venture-capitalprocess Thedecision procedure ofa venture-capitalfinn

To be in a position to secure the funds needed, an entrepreneur must understand thephilosophy and objectives of a venture-capital firm, as well as the venture-capitalprocess. The objective of a venture-capital firm is to generate long-term capitalappreciation through debt and equity investments. To achieve this objective, the venture capitalist is willito make any changes or modifications necessary in the business investment. Since the objective of the ent~~preneur is the survival of the business, the objectives of the two are frequently at odds, particularly whenproblems occur.. .

A typical portfolio objective of venture-capital firms in terms of return criteria and risk involved is shownin Figure 12.4. Since there is more risk involved in financing a business earlier in its development, morereturn is expected from early-stage financing (50 percent ROO than from acquisitions or leveraged buyouts(30 percent KOI), which are later stages of development. The significant risk involved and the pressure thatventure-capital firms feel from their investors (limited partners) to make safer investments with higher ratesof return have caused these firms to invest even greater amounts of their funds in later stages of financing. Inthese late-stage investments, there are lower risks, faster returns, less managerial assistance needed, and fewerdeals to be evaluated.

The venture capitalist does not necessarily seek control of a company, but would rather have the firm andthe entrepreneur at the most risk. The venture capitalist will want at least one seat on the board of directors.Once the decision to invest is made, the venture capitalist will do anything necessary to support themanagement team so that the business and the investment prosper. Whereas the venture capitalist expects toprovide guidance as a member of the board of directors, the management team is expected to direct and runthe daily operations of the company. A venture capitalist will support the management team with investmentdollars, financial skills, planning, and expertise in any area needed.

Since the venture capitalist provides long-term investment (typically five years or more), it is importantthat there be mutual trust and understanding between the entrepreneur and the venture capitalist. There shouldbe no surprises in the firm's performance. Both good and bad news should be shared, with the objective of

FIGURE 12.4 Venture-Capital Financing: Risk and Return Criteria

Highest risk Lowest risk

Development Acquisitions andEarly stage financing leveraged buyouts

Lowest returnexpected

40%. ROI

30%ROI

50%ROI

Source: © 1992. American Economic Development Council (AEDC). All rights reserved. Reprinted from the Economic Development Review.vol. 10. no. 2. Spring 1992. p. 44. with the permission of AEDC.

Highest returnexpected

Chapter 12: lnformel Risk Capital, Venture Capital, and Going Public 427

.takingthe necessary action to allow the company to grow and develop in the long run. The venture capitalist

hould be available to the entrepreneur to discuss problems and develop strategic plans.s .The venture capitalist expects a company to satisfy three general criteria before he or she will commit to

theventure. First, the company must have a strong management team that consists of individuals with solidexperience and backgrounds, a strong commitment to the company, capabilities in their specific areas ofexpertise, the ability to meet challenges, and the flexibility te scramble wherever necessary. A venturecapitalist would rather invest in a first-rate management team and a second-rate product than the reverse.

~1be management team's commitment should be reflected in dollars invested in the company. Although theaJI\ountof the investment is important, more telling is the size of this investment relative to the managementteam's ability to invest. The commitment of the management team should be backed by the support of thefamily,particularly the spouse, of each key team player. A positive family environment and spousal supportalloWteam members to spend the 60 to 70 hours per week necessary to start and grow the company. Onesuccessfu'i venture capitalist makes it a point to have dinner with the entrepreneur and spouse, and even tovisitthe entrepreneur's home, before making an investment decision. According to the venture capitalist, "I

- find it difficult to believe an entrepreneur can successfully run and manage a business and put in thenecessary time when the home environment is out of control."

The second criterion is that the product and/or market opportunity must be unique, having a differentialadvantage in a growing market. Securing a unique market niche is essential since the product or service mustbe able to compete and grow during the investment period. This uniqueness needs to be carefully spelled outin the marketing portion of the business plan and is even better when it is protected by a patent or a tradesecret.

The final criterion for investment is that the business opportunity must have signif-icant capitaL appreciation. The exact amount of capital appreciation varies,depending on such factors as the size of the deal, the stage of development of thecompany, the upside potential, the downside risks, and the available exits. Theventure capitalist typically expects a 40 to 60 percent return on investment in most

. investment situations.The venture-capital process that implements these criteria is both an art and a

science.12 The element of art is illustrated in the venture capitalist's intuition, gutfeeling, and creative thinking that guide the process. The process is scientific due tothesystematic approach and data-gathering techniques involved in the assessment.

The process starts with the venture-capital firm establishing its philosophy and investment objectives. Thefirmmust decide on the following: the composition of its portfolio mix, including the number of start-ups,expansion companies, and management buyouts; the types of industries; the geographic region for

t investment; and any product or industry specializations.J The venture-capital process can be broken down into four primary stages: prelim-1 inaryscreening, agreement on principal terms, due diligence, and final approval. The

~

preliminary screening begins with the receipt of the business plan. A good business.: planis essential in the venture-capital process. Most venture capitalists will not even

talkto an entrepreneur who doesn't have one. ASJhe starting point, the business plan niust have a clear-cutmissionand clearly stated objectives that are supported by an in-depth industry and market analysis and proforma income statements. The executive summary is an important part of this businessplan,as it is usedfor initial screening in this preliminary. evaluation. Many business plans are never evaluated beyond theexecutive summary. When evaluating the business, the venture capitalist first determines if the deal or similardealshave been seen previously. The investor then determines if the proposal fits his or her long-term policyandshort-term needs in developing a portfolio balance. In this preliminary screening, the venture capitalist

significant capitalappreciationSignificant capitalappreciation is theincrease in value ofthe organizationduring a specificperiod of time

preliminary screeningInitial evaluation of adeal

428 Part IV: From the Business Plan to Funding the Venture

investigates the nature of the industry and evaluates whether he or she has the appropriate knowledoability to invest in that industry. The investor reviews the numbers presented to determine whethOe

eand

business can reasonably deliver the ROI required. In addition, the credentials and capability 0; themanagement team are evaluated to determine if they can carry out the plan presented. the

The second st~ge. is the agreeme~t on principa~ terms betwe~n ~he entrepreneur and the vel:ture capitali to'The venture caplta!lst wants .a basic u.nd~rstand~ng of the'pfII~clpal ter~ns of the deal at ~11lSstage of theprocess before making the major comnutment of time and effort involved in the formal due ddigence prOCe

The third stage, detailed review and due diligence, is the longest stage, involving anywhere from onethree months. There is a detailed review of the company's history, the business plan, tothe resumes of the individuals, their financial history, and target market customers. due diligence The"·

process of deal :.The upside potential and downside risks are assessed, and there is a thorough evalu-evaluation

ation of the markets, industry, finances, suppliers, customers, and management.In the last stage, final approval, a comprehensive, internal investment

memorandum isprepared. This document reviews the venture capitalist's findingsand details the investment terms and condidons of the investment transaction. Thisinformation is used to prepare the forma! legal documents that both the entrepreneurand venture capitalist will sign to finalize the deal. 13

final approval A . .

document showingthe fi nal terms of thedeal

Locating Venture CapitalistsOne of the most important decisions for the entrepreneur lies in selecting which venture-capital firm toapproach. Since venture capitalists tend to specialize either geographically by industry (manufacturing·industrial products or consumer products, high technology, or service) or by size and type of investmen~the entrepreneur should approach only those that may have an interest in the investment opportunity.Where do you find this venture capitalist?

Although venture capitalists are located throughout the United States, the traditional areas of concentrationare found in Los Angeles, New York, Chicago, Boston, and San Francisco. Most venture capital firms belongto the National Venture Capital Association and are listed on its Web site (www.nvca.org). An entrepreneurshould carefully research the names and addresses of prospective venture-capital firms that might have aninterest i~ the particular investment opportunity. There are also regional and state-level venture-capital associ-ations. For a nominal fee or none at all, these associations will frequently send the entrepreneur a directorythat lists their members, the types of businesses their members invest in, and any investment restrictions, Theresponse of the VC is likely to be more positive if the entrepreneur is introduced to the venture capitalist.Bankers, accountants, lawyers, and professors are good.sources for introductions.

Approaching a Venture CapitalistThe entrepreneur should approach a venture capitalist in a professional business manner. Since venturecapitalists receive hundreds of inquiries and are frequently out of the office working with portfolio companiesor investigating potential investment opportunities, it is important to begin the relationship positively. Theentrepreneur should call any potential venture capitalist to ensure that the business is in an area of theirinvestment interest. Then the business plan should be sent, accompanied by a short professional letter.

Since venture capitalists receive many more plans than they are capable of funding, many plans arescreened out as soon as possible. Venture capitalists tend to focus and put more time and effort on those plansthat are referred to them by reliable persons. In fact, one venture-capital group said that 80 percent of itsinvestments over the last five years were in referred companies. Consequently, it is well worth the entre-

Chapter 12: Informal Risk Capital, Venture Copitol, and Going Public 429

·reneur's time to seek out an introduction to the venture capitalist. Typically this can be obtained from anP utive of a portfolio company, an accountant, a lawyer, a banker, or a business school professor.eX~heentrepreneur should be aware of some basic rilles of thumb before implementing the actual approach

d should follow the detailed guidelines presented in Table 12.6. First, great care should be taken in selecting: right venture capitalist to approach. Venture capitalists tend to specialize in certain industries and willrarelyinvest in a business outside those areas, regardless of the merits of rt.e business proposal and plan.second, recognize that venture capitalists know each other, particularly in a specific region of the country.Whena large amount of money is involved, they will invest in the deal together, with one venture-capital firmtakingthe lead. Since such high degree of familiarity is present, a venture-capital firm will probably find outif others have seen your business plan. Do not shop among venture capitalists, as even a good business plancanquickly become "shopworn." Third, when meeting the venture capitalist, particularly for the first time,bring only one or two key members of the management team: A venture capitalist is investing in you and your~agement team and its track record. not in outside consultants and experts. Any experts can be called in as

.•~ed. "

Guidelines for Dealing with Venture Capitalists

• Carefullydetermine the venture capitalist to approach for funding the particular type of deal. Screen and-target the approach. Venture capitalists do not like deals that have been excessively "shopped."

~-,_It.• Oncea discussion is started with a venture capitalist, do not discuss the deal with other venture capitalists., Working several deals in parallel can create problems unless the venture capitalists are working together.

lime and resource limitations may require a cautious simultaneous approach to several funding sources.• It isbetter to approach a venture capitalist through an intermediary who is respected and has a preexisting

relationship with the venture capitalist. Limit and carefully define the role and compensation of the. intermediary.

• Theentrepreneur or manager, not an intermediary, should lead the discusslonswith the venture capitalist.~ 0.0 not bring a lawyer, accountant, or other advisors to the first meeting. Since there are no negotiations

during this first meeting, it is a chance for the venture capitalist to get to know the entrepreneur withoutInterference from others. '

'1 Bevery careful about what is projected or promised. The entrepreneur will probably be held accountable forthese projections in the pricing, deal structure, or compensation.

• Discloseany significant problems or negative situations, in this initial meeting. Trust is a fundamental part ofthe long-term relationship with the venture capitalist; subsequent discovery by the venture capitalist of anundisclosed problem will cause a loss of confidence and probably prevent' a.dsal, '

• Reacha flexible, reasonable understanding with the venture capitalist regarding the timing of a response tothe proposal and the accomplishment of the various steps in the financing transaction. Patience is needed, asthe process is complex and time consuming. Too much pressure for a rapid decision can cause problems with

·~the venture capitalist. '!~Donot sell the project on the basis that other venture capitalists have committed themselves, Most venture

. ,capitalists are independent and take pride in their own decision making.• Becareful about glib statements such as, "There is no competition for this prod net" or "There is nothing like• !his technology available today." These statements can reveal a failure to do one's homework or can indicate· that a perfect product has been designed for a nonexistent market. ,' ..t Donot show an inordinate concern for salary, benefits, or other forms of current compensation. Money is

preclous in a new venture. The venture capitalist wants the entrepreneur committed to an equity· appreciation similar to that of the venture capitalist.

,- Eliminateto the extent possible any use of new investments to take care of past problems, such as payment• of past debts or deferred salaries of the management. New investments from the venture capitalist are for

growth, to move the business forward.

430 Part IV: From the Business Plan to Funding t,he Venture

Finally, be sure to develop a succinct, well-thought-out oral presentation. This should cover the campa .business, the uniqueness of the product or service,' the prospects for growth, the major factors be~Ysachieving the sales and profits indicated, the backgrounds and track records 'of the key managers, the amound

of financing required, and the returns anticipated. This first presentation is critical, as is indicated in thecomment of one venture capitalist: "I need to sense a competency, a capability, a chemistry within the firehalf hour of our initial meeting. The entrepreneur needs to look me in the eye and present his story clearly an~logically. If a chemistry does not start to develop, I start looking for reasons not to do the deal." -

.Following a favorable initial meeting, the venture capitalist will do some preliminary investigation of theplan. If favorable, another meeting between the management team and the venture capitalist will be scheduledso that both parties can assess the other and determine if a good working relationship can be established andif a feeling of trust and confidence is evolving. During this mutual evaluation, the entrepreneur should becareful not to be too inflexible about the amount of company equity he or she is willing to share. If the entre.preneur is too inflexible, the venture capitalist might end negotiations. During this meeting, initial agreementof terms is established. If you are turned down by one venture capitalist, do not become discouraged. Insteadselect several other nonrelated venture-capitalist candidates and repeat the procedure. A significant num~of companies denied funding by one venture capitalist are able to obtain funds from other outside Sourcesincluding other venture capitalists. '

Venture capital funds are quite active in India too. There are about 180 such -funds registered with theSecurities and Exchange Board of India (SEBI). There is therefore, enough diversity in their areas of special-ization, which makes it fairly easy for new ventures to get VC funds, if they are willing to explore a fewoptions. Many of these funds are members of the Indian Private Equity and Venture Capital Association(lVCA). The IVCA website gives detailed explanations and instructions on how to go about sourcing andsecuring VC funds, a compilation of which are reproduced in the next section.

A problem confronting the entrepreneur in obtaining outside equity funds, whetherfrom the informal investor market (the angels) or from the formal venture-capitalindustry, is determining the value of the company. This valuation is at the core ofdetermining how much ownership an investor is entitled to for funding the venture.This is determined by considering the factors in valuation. This, as well as otheraspects of securing funding, has a potential for ethical conflict that must be carefullyhandled.

factors in I'aiuatiolf"Nonmonetary aspeeathat affect the fundvaluation of a

VALUING YOUR COMPANY

company

Factors in ValuationThere are eight factors that, although they vary by situation, the entrepreneur should consider when valuingthe venture. The first factor, and the starting point in any valuation, is the nature and history of the businThe characteristics of the venture and the industry in which it operates are fundamental to every evaluationprocess. The history of the company from its inception provides information on the strength and diversityofthe company's operations, the risks involved, and the company's ability to withstand any adverse conditions.

The valuation process must also consider the outlook of the economy in general as well as the outlookf(1the particular industry. This, the second factor, involves an examination of the financial data of the venru:ecompared with those of other companies in the industry. Management's capability now and in the future -assessed, as well as the future market for the company's products. Will these markets grow, decline.QC

stabilize, and in what economic conditions?

Related Documents