Chapter 10 Charles P. Jones, Investments: Principles and Concepts, Twelfth Edition, John Wiley & Sons 10 -1

Ch 10 ppt ipm

Dec 23, 2015

Ch 10 ppt ipm

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 10Charles P. Jones, Investments: Principles and Concepts,

Twelfth Edition, John Wiley & Sons

10-1

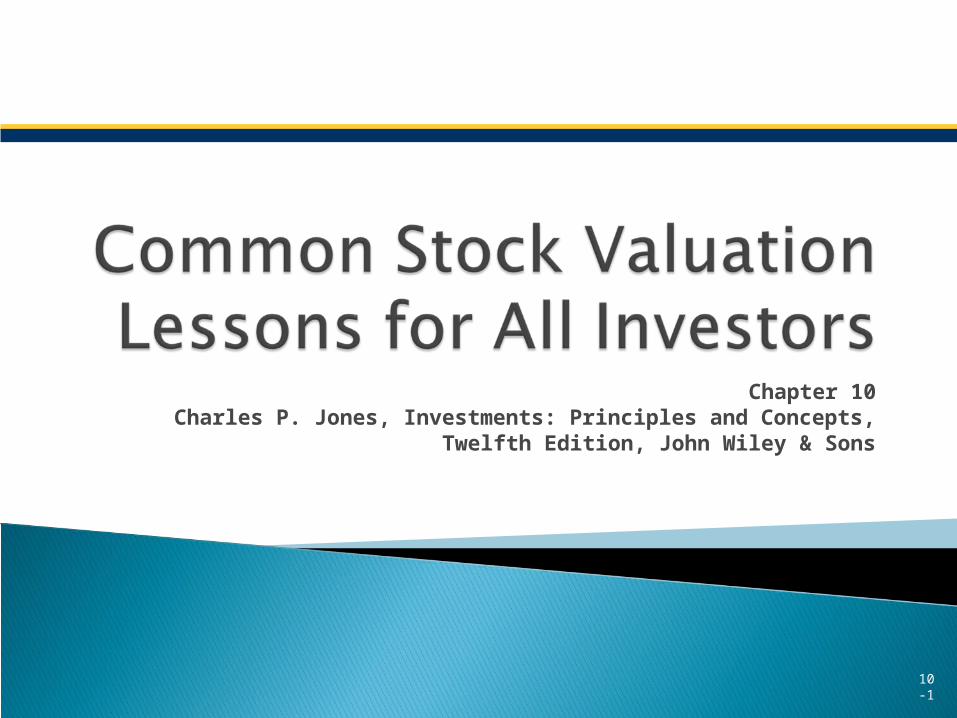

Discounted Cash Flow Techniques◦ Intrinsic value based on the discounted value of

the expected stream of cash flows◦ Dividend Discount Model often emphasized in

textbooks Often not used by practitioners

Earnings Multiplier Approach Relative Valuation Metrics

◦ Emphasizes selecting stocks to buy rather than valuation

10-2

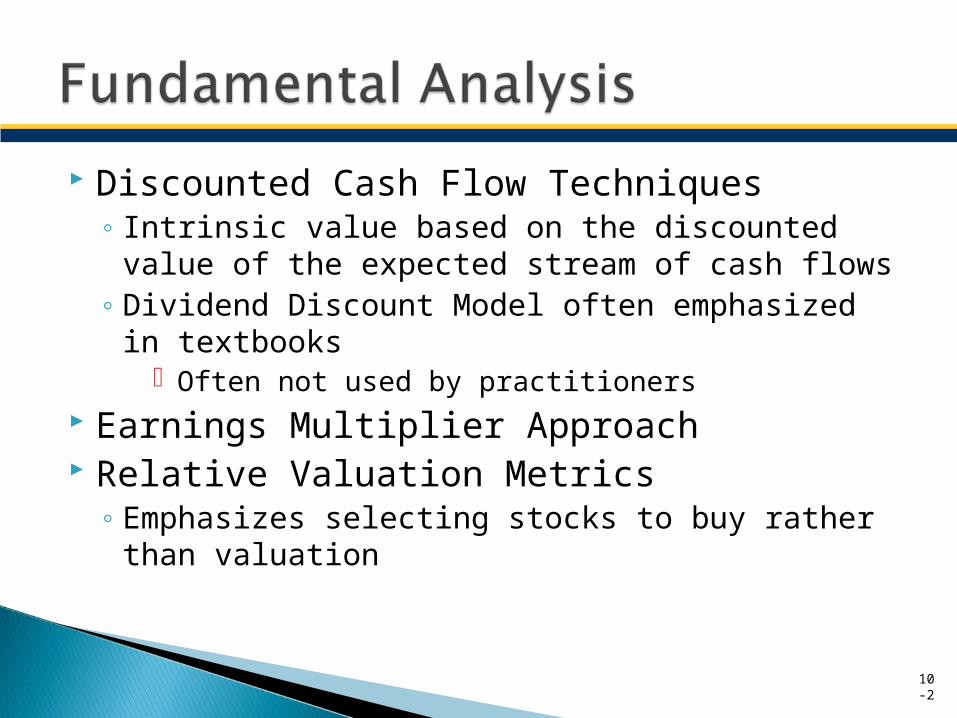

Intrinsic value of a security is

K = appropriate discount rate Estimated intrinsic value compared to the

current market price Can value equity of firm or entire firm

10-3

n

tt k) (

Cash Flows urity secValue of 1 1

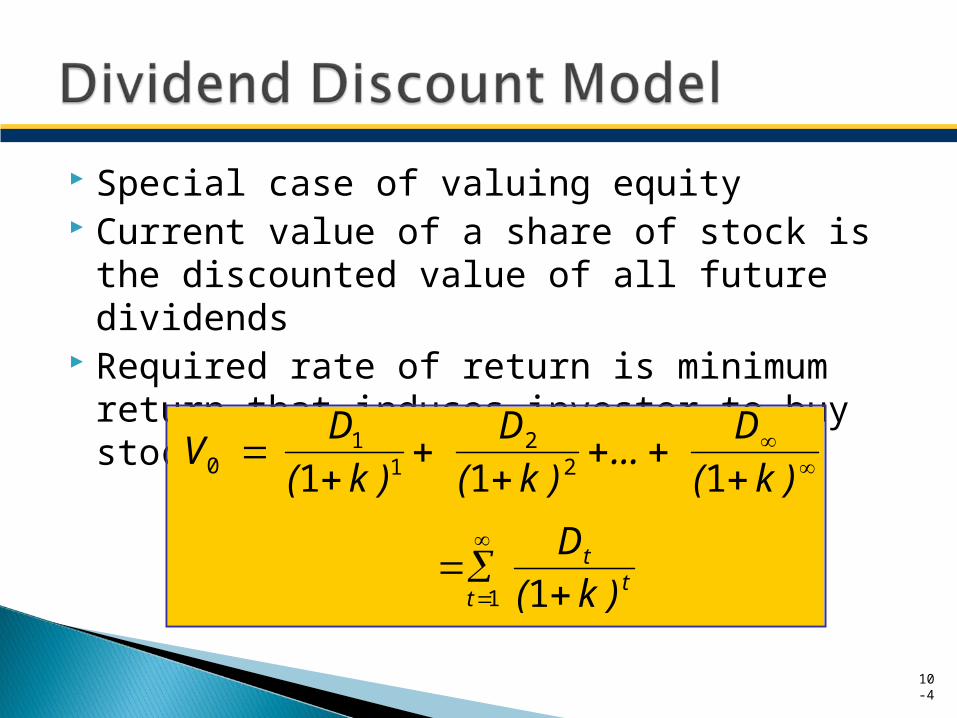

Special case of valuing equity Current value of a share of stock is the

discounted value of all future dividends Required rate of return is minimum return

that induces investor to buy stock

10-4

V0 D1

(1 k )1

D2

(1 k )2...

D

(1 k )

Dt

(1 k )tt1

Dividends must be valued for infinitely long time period◦ Not as large a practical problem as it may seem

Dividend stream is uncertain Dividends expected to grow over time

◦ Estimated growth in dividends can be included in DDM

◦ Three growth cases: zero, constant, multiple

10-5

Implementing the DDM

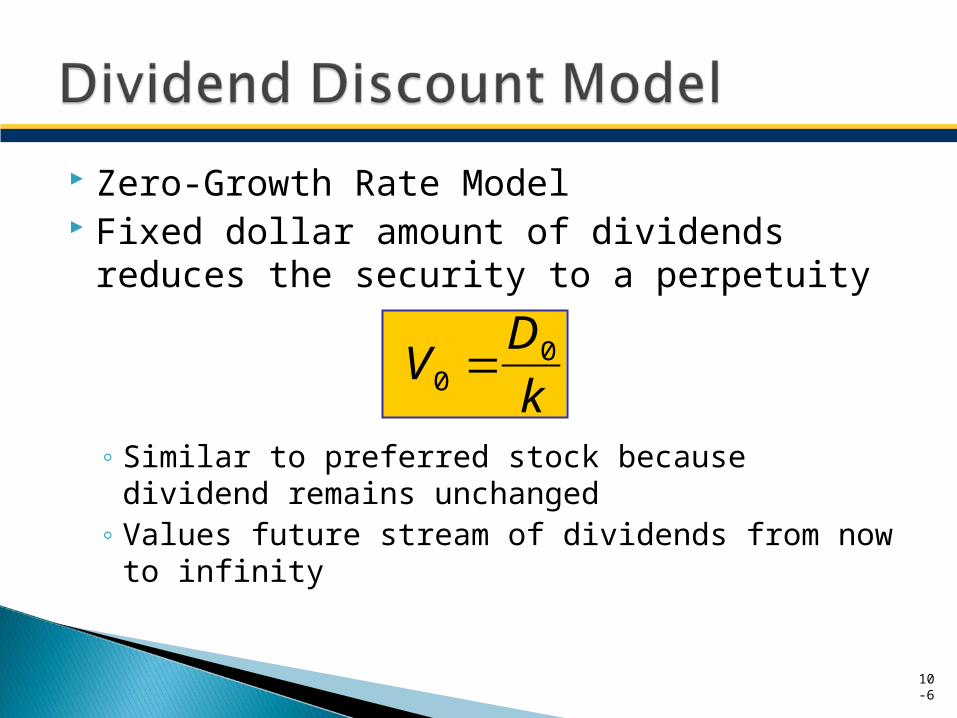

Zero-Growth Rate Model Fixed dollar amount of dividends reduces

the security to a perpetuity

◦ Similar to preferred stock because dividend remains unchanged

◦ Values future stream of dividends from now to infinity

10-6

V0 D0

k

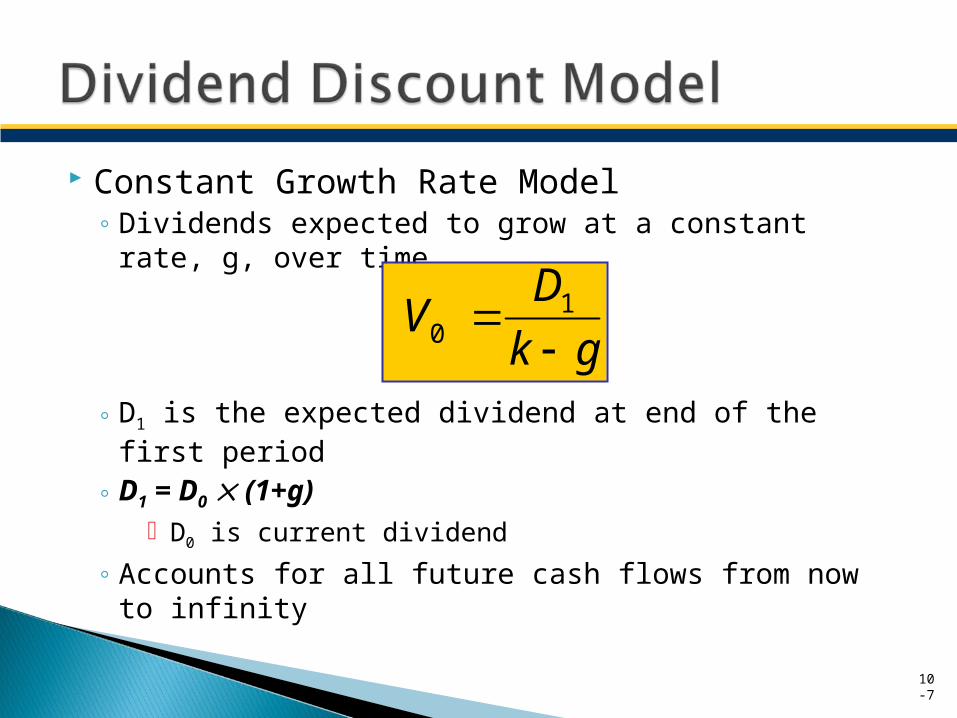

Constant Growth Rate Model◦ Dividends expected to grow at a constant rate, g,

over time

◦ D1 is the expected dividend at end of the first period

◦ D1 = D0 (1+g) D0 is current dividend

◦ Accounts for all future cash flows from now to infinity

10-7

V0 D1

k g

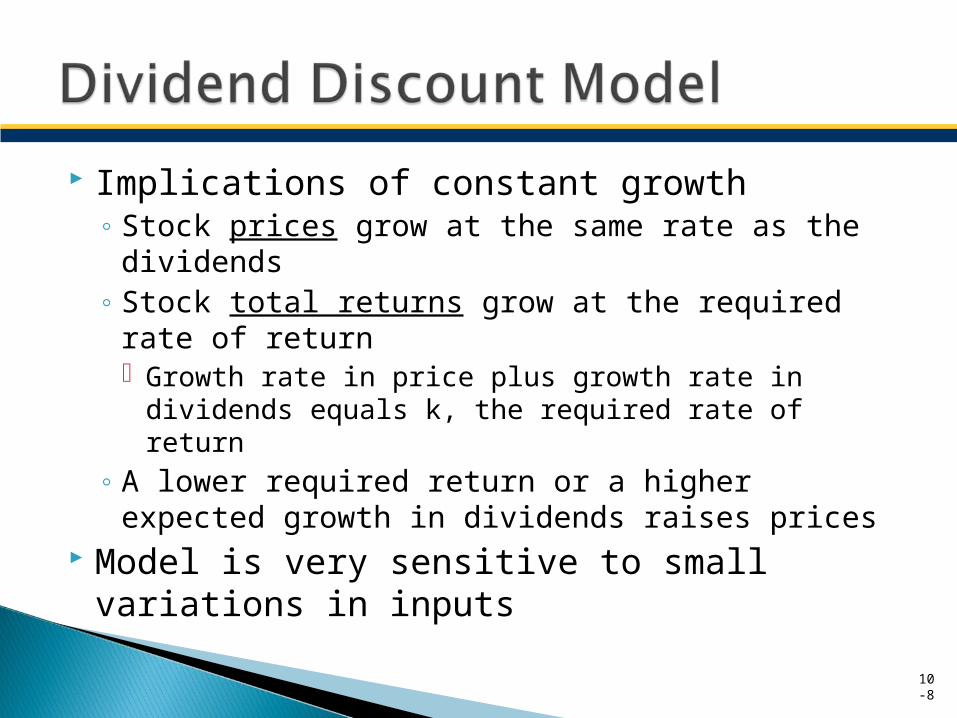

Implications of constant growth◦ Stock prices grow at the same rate as the

dividends◦ Stock total returns grow at the required rate of

return Growth rate in price plus growth rate in dividends

equals k, the required rate of return◦ A lower required return or a higher expected

growth in dividends raises prices Model is very sensitive to small variations in

inputs

10-8

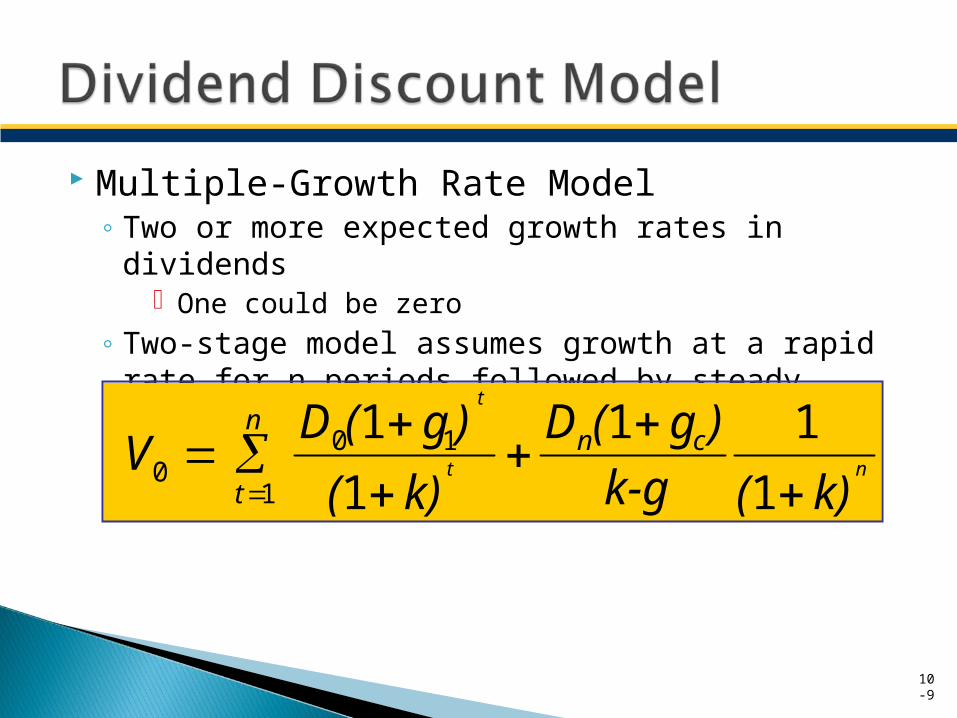

Multiple-Growth Rate Model◦ Two or more expected growth rates in dividends

One could be zero◦ Two-stage model assumes growth at a rapid rate

for n periods followed by steady growth

10-9

V0 D0(1 g1)

t

(1 k)t

t1

n

Dn(1 gc)

k-g

1

(1 k)n

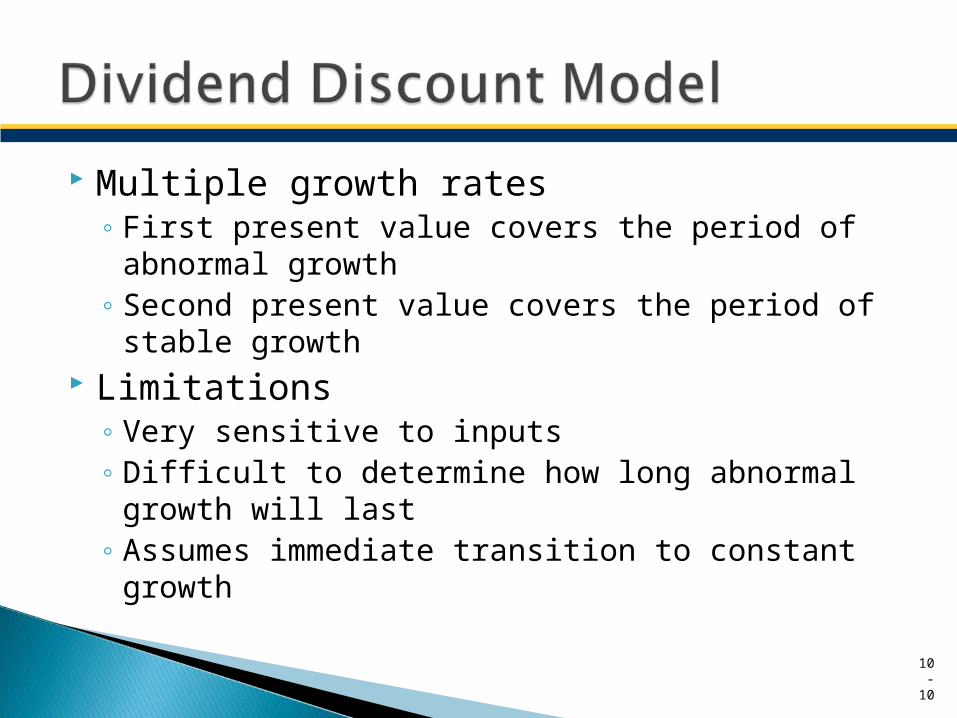

Multiple growth rates◦ First present value covers the period of abnormal

growth◦ Second present value covers the period of stable

growth Limitations

◦ Very sensitive to inputs◦ Difficult to determine how long abnormal growth

will last◦ Assumes immediate transition to constant growth

10-

10

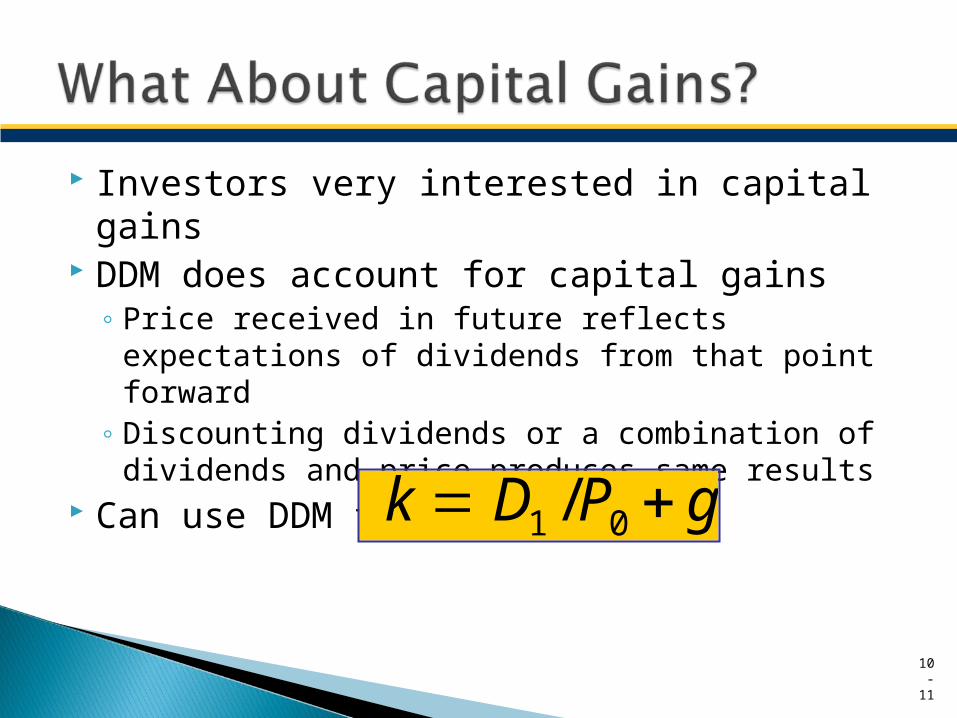

Investors very interested in capital gains DDM does account for capital gains

◦ Price received in future reflects expectations of dividends from that point forward

◦ Discounting dividends or a combination of dividends and price produces same results

Can use DDM to select stocks

10-

11

k D1 /P0 g

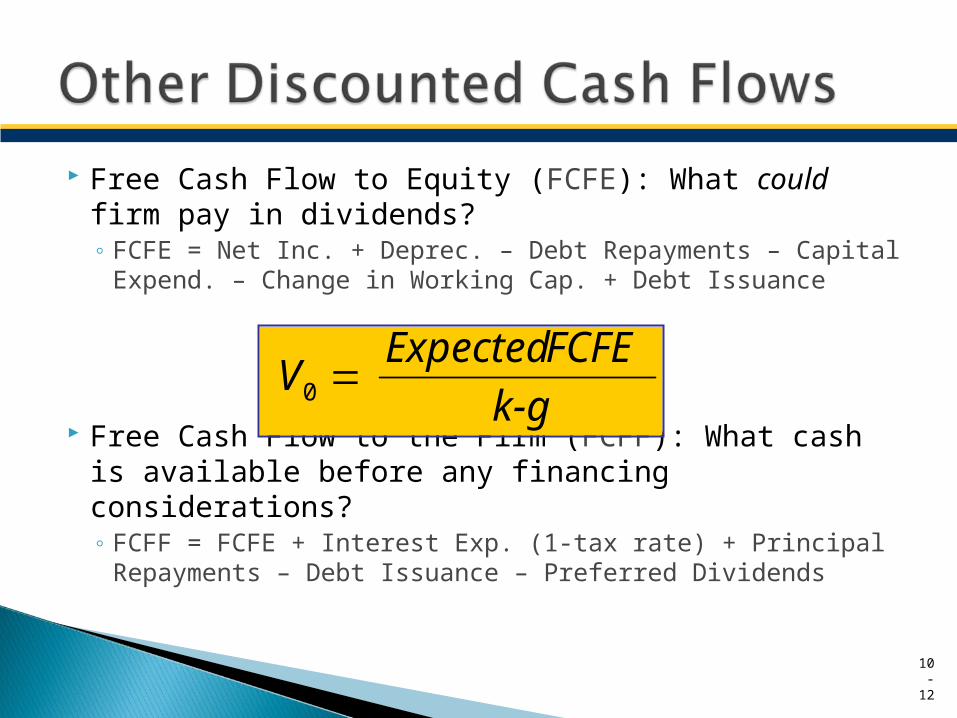

Free Cash Flow to Equity (FCFE): What could firm pay in dividends?◦ FCFE = Net Inc. + Deprec. – Debt Repayments –

Capital Expend. – Change in Working Cap. + Debt Issuance

Free Cash Flow to the Firm (FCFF): What cash is available before any financing considerations?◦ FCFF = FCFE + Interest Exp. (1-tax rate) + Principal

Repayments – Debt Issuance – Preferred Dividends10

-12

V0 Expected FCFE

k-g

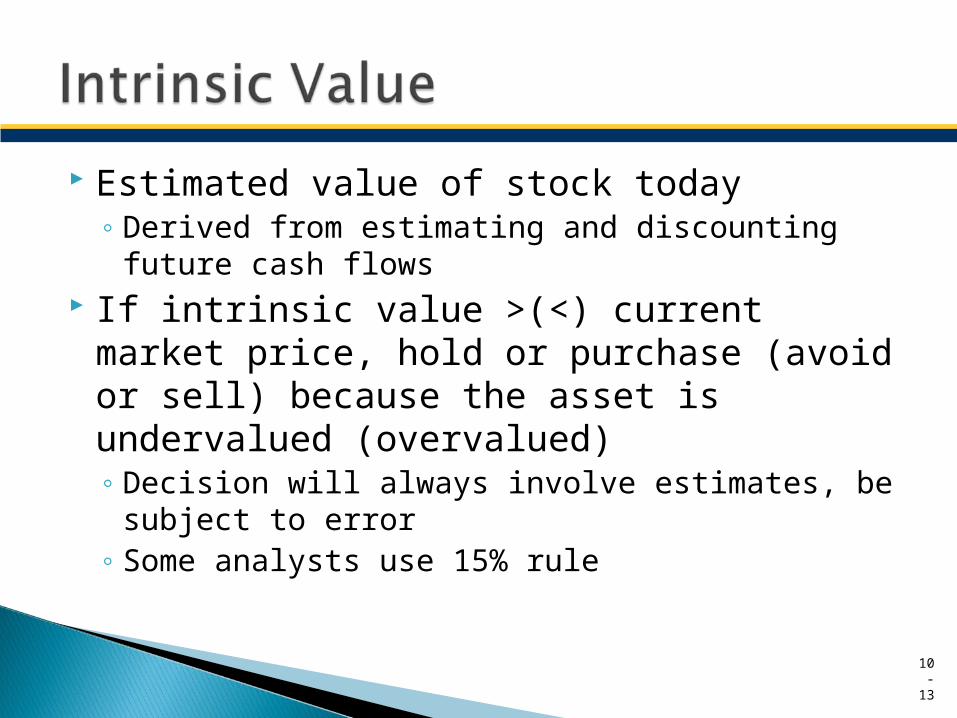

Estimated value of stock today◦ Derived from estimating and discounting future

cash flows If intrinsic value >(<) current market price,

hold or purchase (avoid or sell) because the asset is undervalued (overvalued)◦ Decision will always involve estimates, be subject

to error◦ Some analysts use 15% rule

10-

13

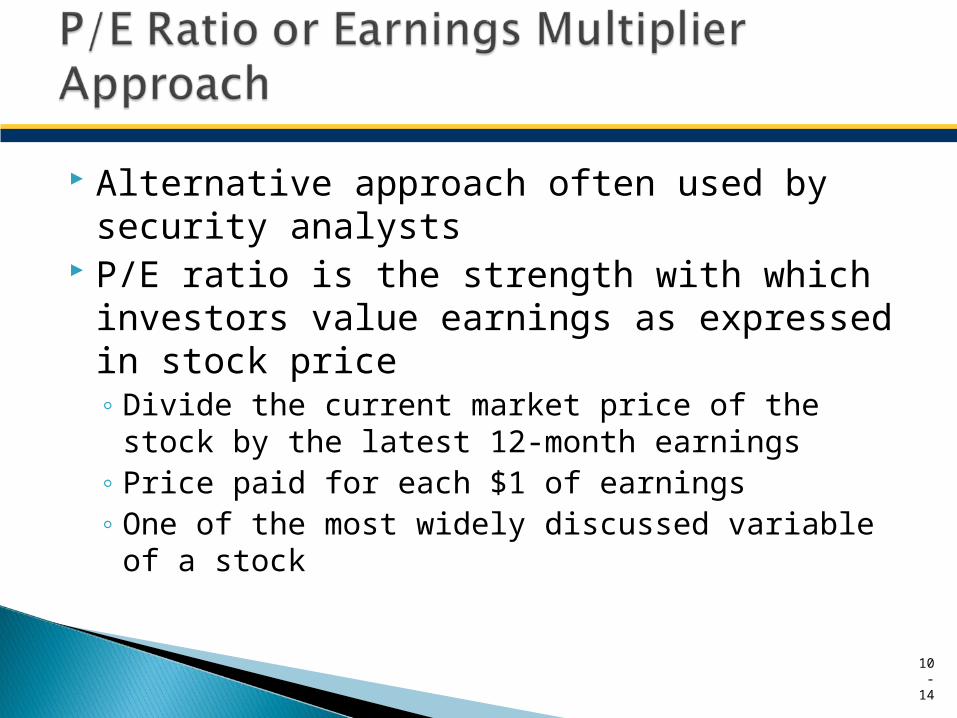

Alternative approach often used by security analysts

P/E ratio is the strength with which investors value earnings as expressed in stock price◦ Divide the current market price of the stock by

the latest 12-month earnings◦ Price paid for each $1 of earnings◦ One of the most widely discussed variable of a

stock

10-

14

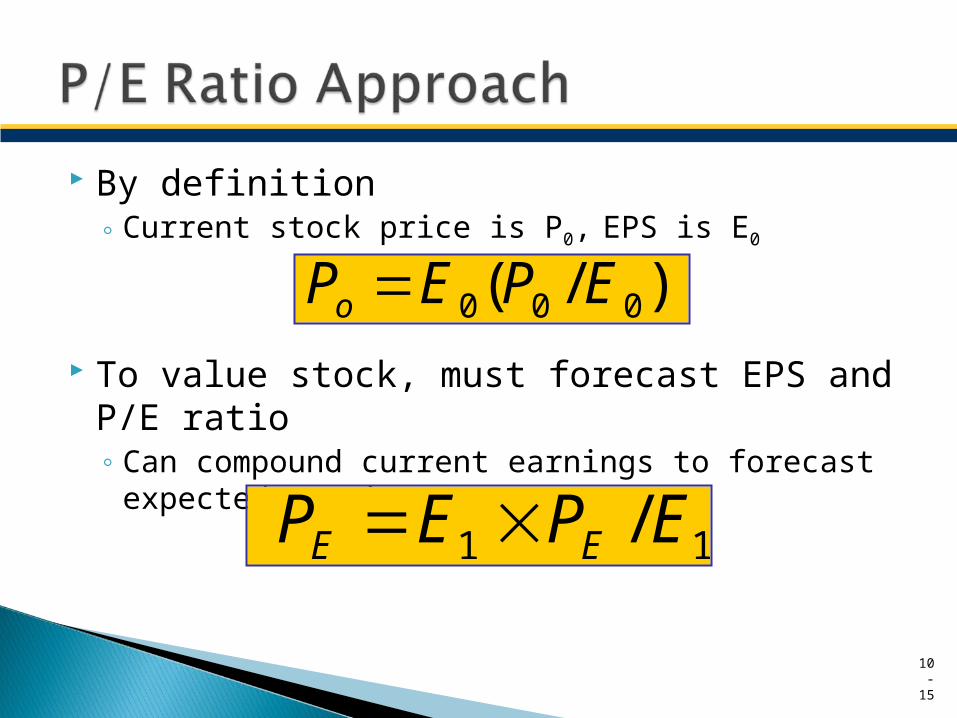

By definition◦ Current stock price is P0, EPS is E0

To value stock, must forecast EPS and P/E ratio◦ Can compound current earnings to forecast

expected earnings

10-

15

Po E0(P0 /E0)

PE E1 PE /E1

Compare company relative to peers, the market

P/E ratios◦ High P/E ratios can result from several factors, not

all equally desirable for investor◦ Best used to make specific comparisons

Price/Book value◦ Price/Stockholders’ Equity◦ Best suited for companies with hard assets

10-

16

Relative Valuation

Price/Sales Ratio (PSR)◦ Can be used to value companies without earnings◦ Price/Revenues per share over four most recent

quarters◦ Important to interpret within industry norms

Economic Value Added (EVA)◦ Difference between operating profits and

company’s capital cost◦ Emphasizes return on capital

10-

17

Relative Valuation

Discounted cash flow theoretically best◦ May be unrealistic because accurate estimates

difficult P/E multiplier serves dual role

◦ Estimating intrinsic value of stock◦ Relative valuation

All methods subject to estimation error Traditional methods do apply to “new

economy” stocks: revenues and profits matter

10-

18

Copyright 2013 John Wiley & Sons, Inc.All rights reserved. Reproduction or translation of this

work beyond that permitted in section 117 of the 1976 United States Copyright Act without express permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages caused by the use of these programs or from the use of the information herein.

10-

19

Related Documents