Financial and Tax Considerations for Equity Compensation Presented by: Andrew Schwartz, CPA, CEP Vice President Computershare

CFP SOP Presentation Final

Jul 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial and Tax Considerations for Equity Compensation

Presented by:

Andrew Schwartz, CPA, CEP

Vice President

Computershare

Disclaimer

The following presentation and the views expressed by the presenter are not

intended to provide legal, tax, accounting or other professional advice. The

information contained in this presentation is general in nature and based on

authorities that are subject to change. Applicability to specific situations

should be determined through consultation with your legal and/or tax advisor.

DISCLAIMER

2

Agenda

› Types of Equity Compensation

› Taxation differences among award types

› Special situations

› Beginning-to-end tax analysis

› Q&A

Award Types

› Restricted stock

› Right to receive stock in the future

› Will always have some value

› Stock options – Non-qualified and qualified (ISOs)

› Stock appreciation rights

› Rights to benefit from an increase in the stock price

› Employee stock purchase plans (ESPPs)

› Right to purchase stock at a discount

› Can be qualified (§423) or non-qualified

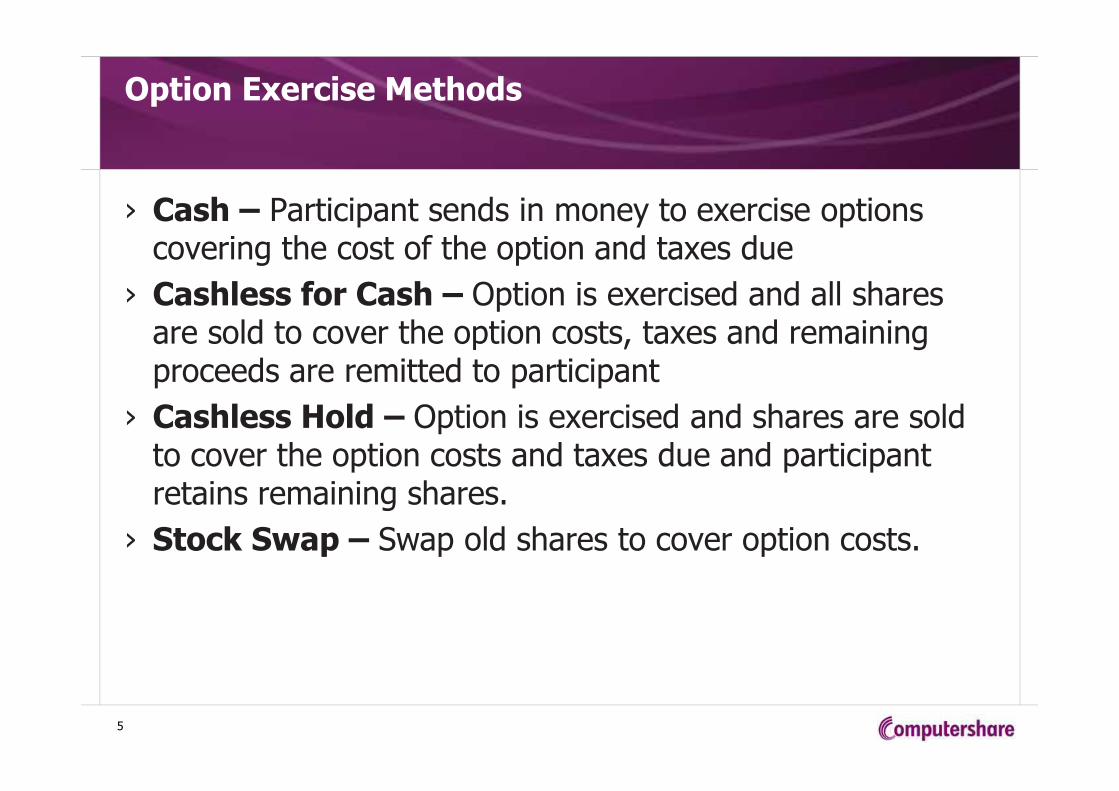

Option Exercise Methods

› Cash – Participant sends in money to exercise options covering the cost of the option and taxes due

› Cashless for Cash – Option is exercised and all shares are sold to cover the option costs, taxes and remaining proceeds are remitted to participant

› Cashless Hold – Option is exercised and shares are sold to cover the option costs and taxes due and participant retains remaining shares.

› Stock Swap – Swap old shares to cover option costs.

5

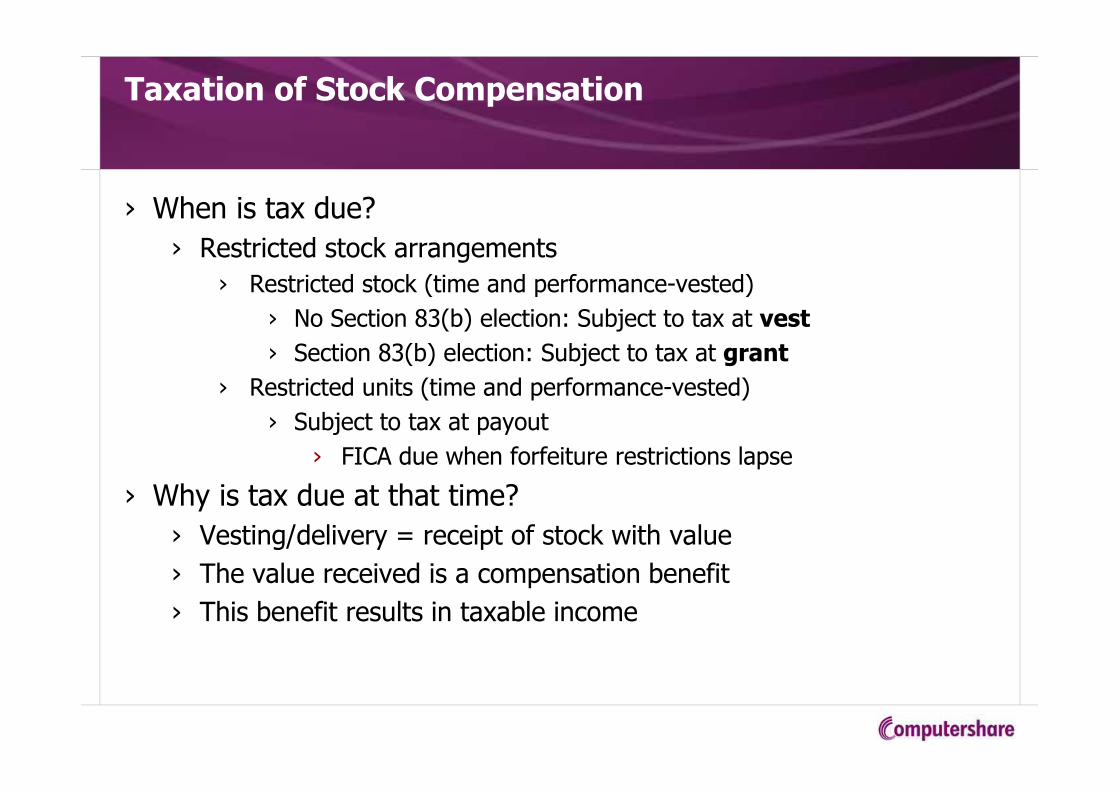

Taxation of Stock Compensation

› When is tax due?

› Restricted stock arrangements

› Restricted stock (time and performance-vested)

› No Section 83(b) election: Subject to tax at vest

› Section 83(b) election: Subject to tax at grant

› Restricted units (time and performance-vested)

› Subject to tax at payout

› FICA due when forfeiture restrictions lapse

› Why is tax due at that time?

› Vesting/delivery = receipt of stock with value

› The value received is a compensation benefit

› This benefit results in taxable income

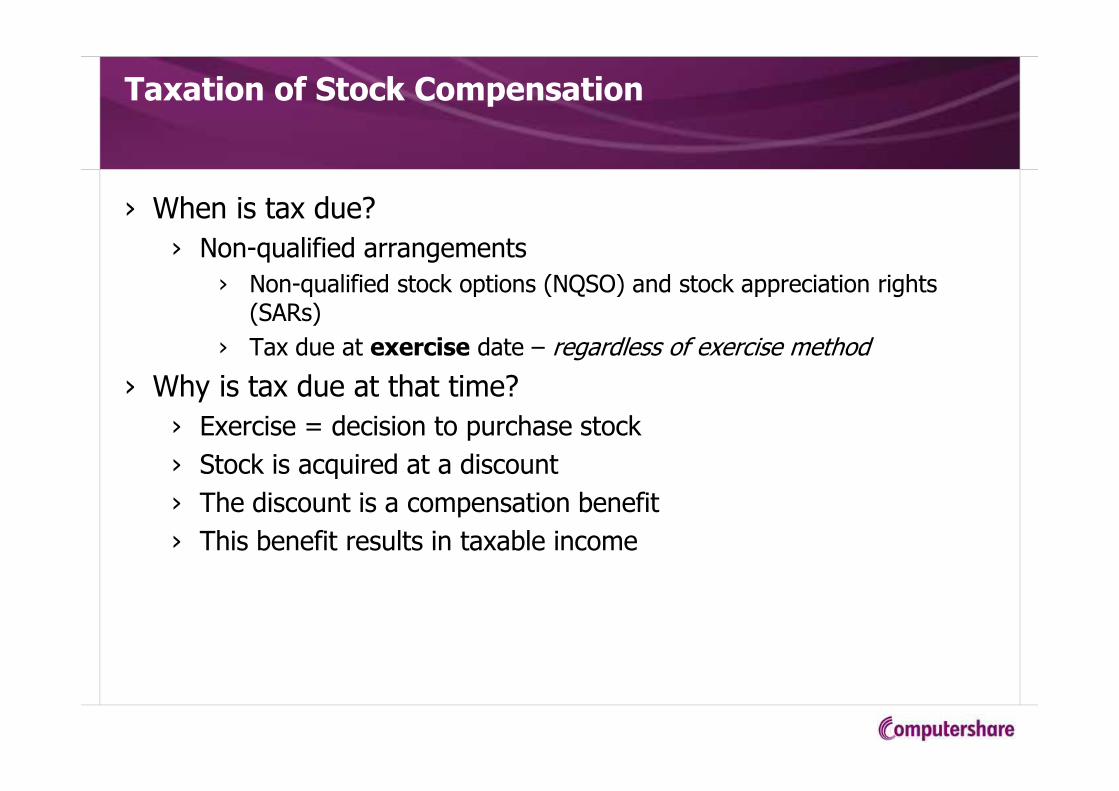

Taxation of Stock Compensation

› When is tax due?

› Non-qualified arrangements

› Non-qualified stock options (NQSO) and stock appreciation rights (SARs)

› Tax due at exercise date – regardless of exercise method

› Why is tax due at that time?

› Exercise = decision to purchase stock

› Stock is acquired at a discount

› The discount is a compensation benefit

› This benefit results in taxable income

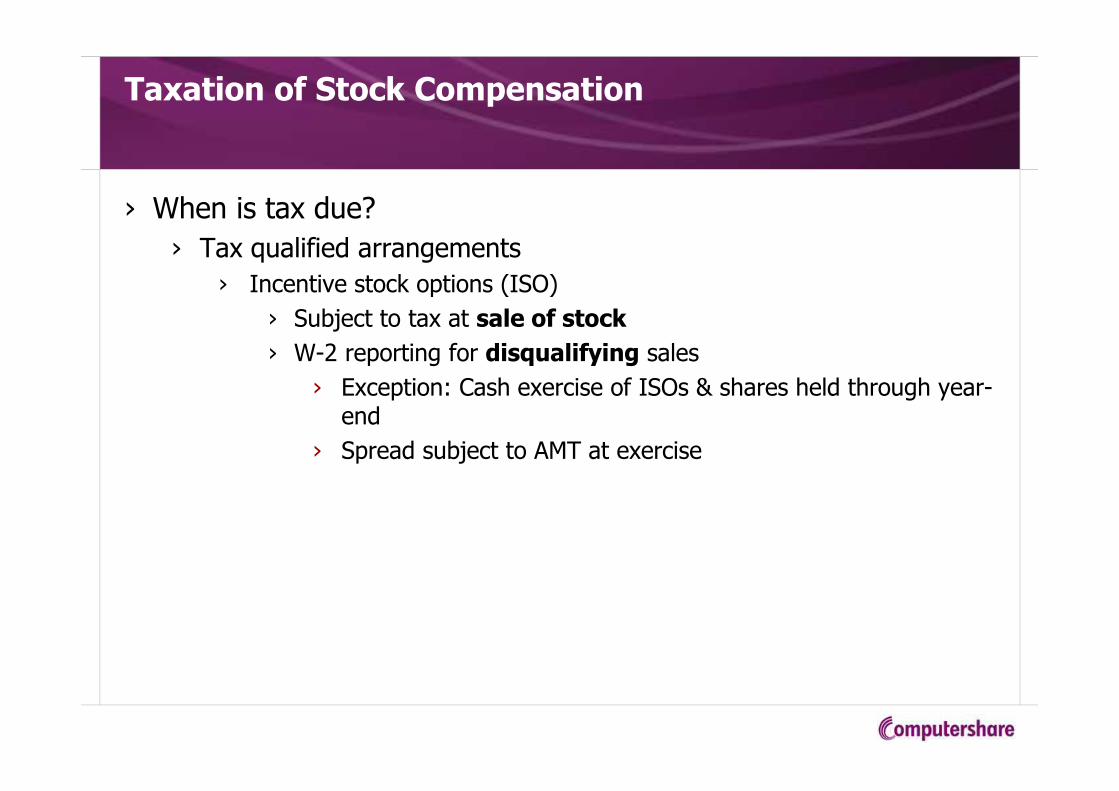

Taxation of Stock Compensation

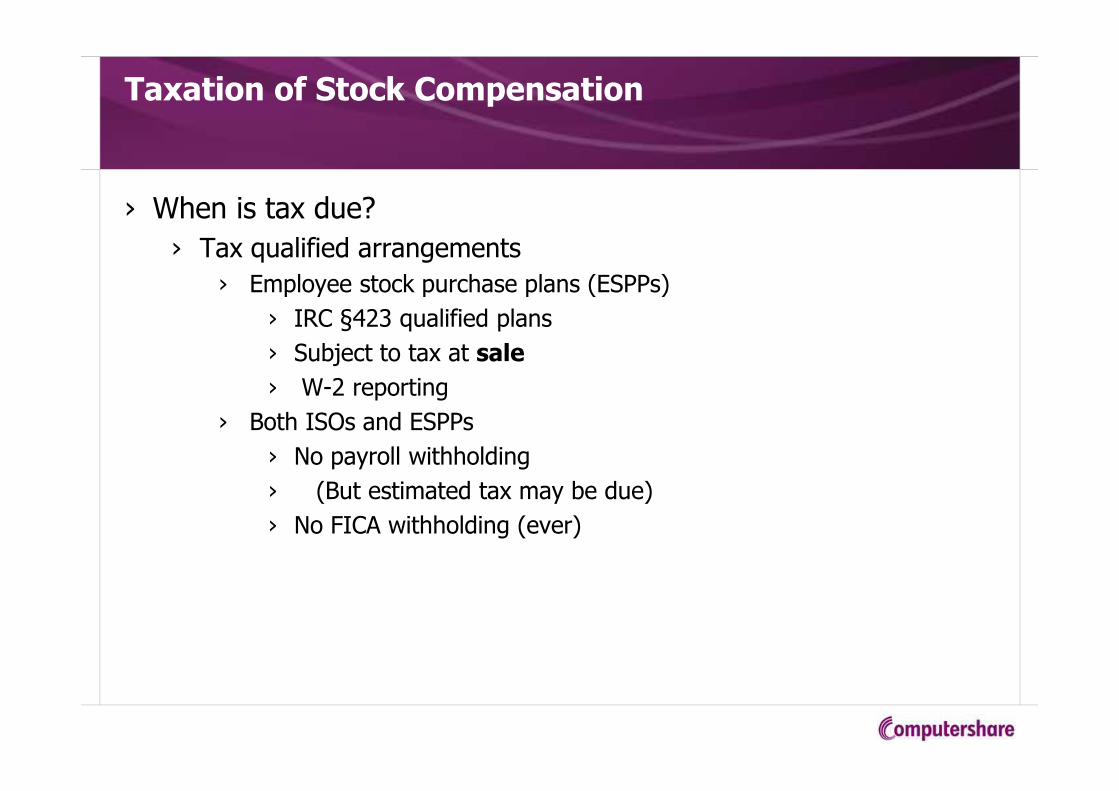

› When is tax due?

› Tax qualified arrangements

› Incentive stock options (ISO)

› Subject to tax at sale of stock

› W-2 reporting for disqualifying sales

› Exception: Cash exercise of ISOs & shares held through year-end

› Spread subject to AMT at exercise

Taxation of Stock Compensation

› When is tax due?

› Tax qualified arrangements

› Employee stock purchase plans (ESPPs)

› IRC §423 qualified plans

› Subject to tax at sale

› W-2 reporting

› Both ISOs and ESPPs

› No payroll withholding

› (But estimated tax may be due)

› No FICA withholding (ever)

Taxation of Stock Compensation

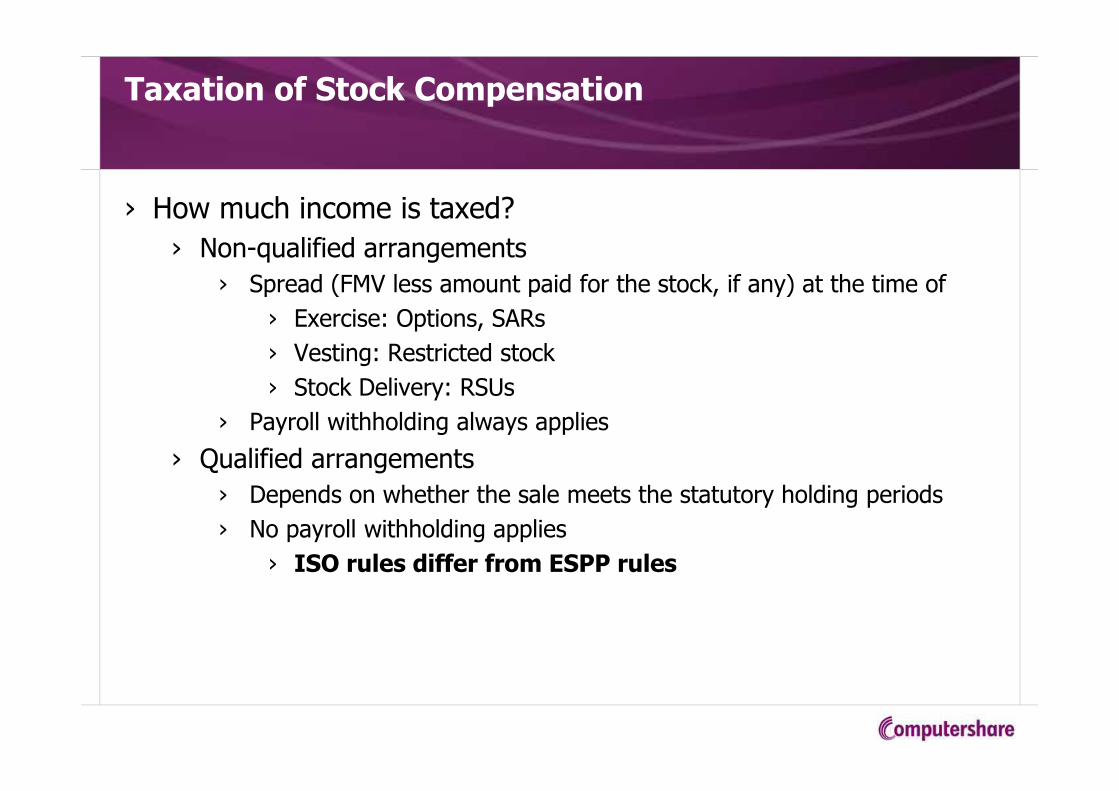

› How much income is taxed?

› Non-qualified arrangements

› Spread (FMV less amount paid for the stock, if any) at the time of

› Exercise: Options, SARs

› Vesting: Restricted stock

› Stock Delivery: RSUs

› Payroll withholding always applies

› Qualified arrangements

› Depends on whether the sale meets the statutory holding periods

› No payroll withholding applies

› ISO rules differ from ESPP rules

Taxation of Stock Compensation

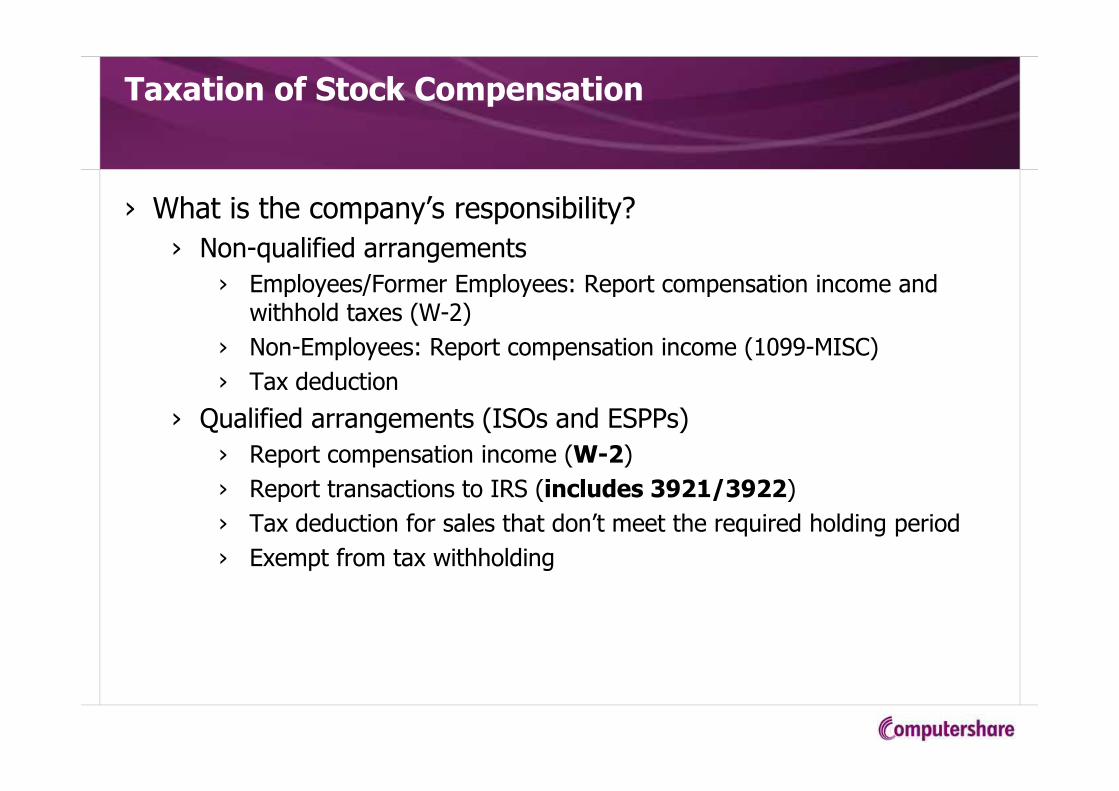

› What is the company’s responsibility?

› Non-qualified arrangements

› Employees/Former Employees: Report compensation income and withhold taxes (W-2)

› Non-Employees: Report compensation income (1099-MISC)

› Tax deduction

› Qualified arrangements (ISOs and ESPPs)

› Report compensation income (W-2)

› Report transactions to IRS (includes 3921/3922)

› Tax deduction for sales that don’t meet the required holding period

› Exempt from tax withholding

Tax Reporting

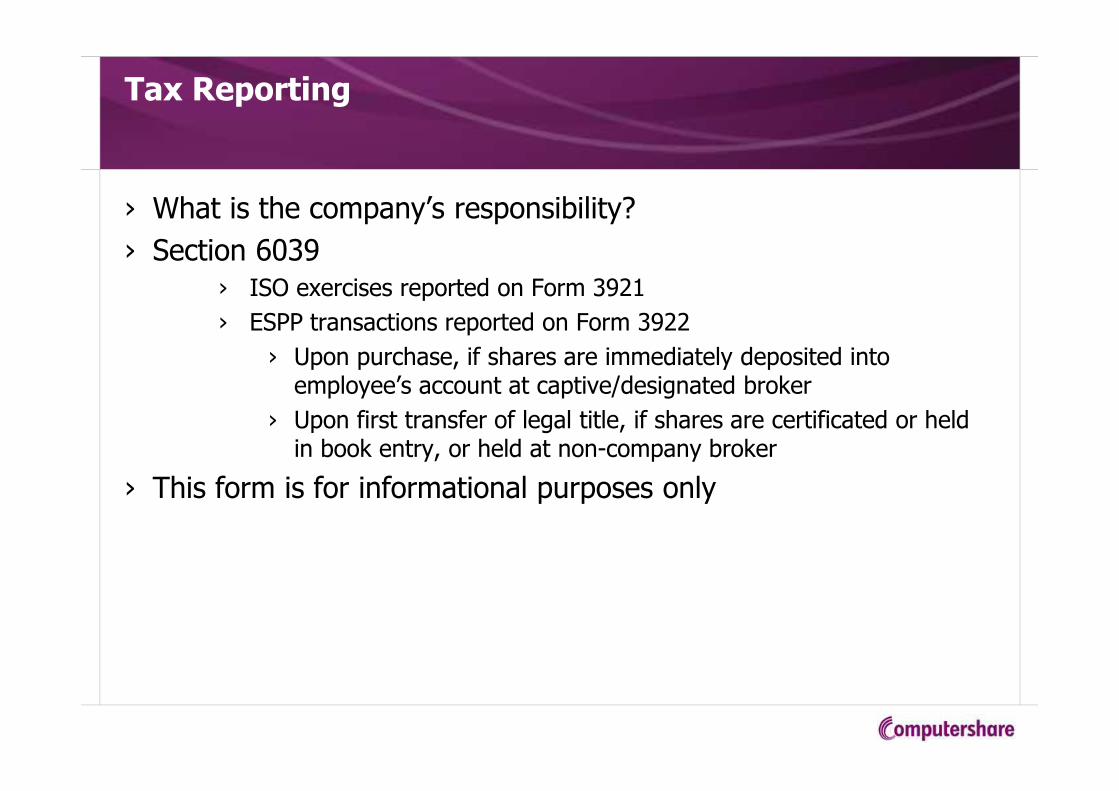

› What is the company’s responsibility?

› Section 6039 › ISO exercises reported on Form 3921

› ESPP transactions reported on Form 3922

› Upon purchase, if shares are immediately deposited into employee’s account at captive/designated broker

› Upon first transfer of legal title, if shares are certificated or held in book entry, or held at non-company broker

› This form is for informational purposes only

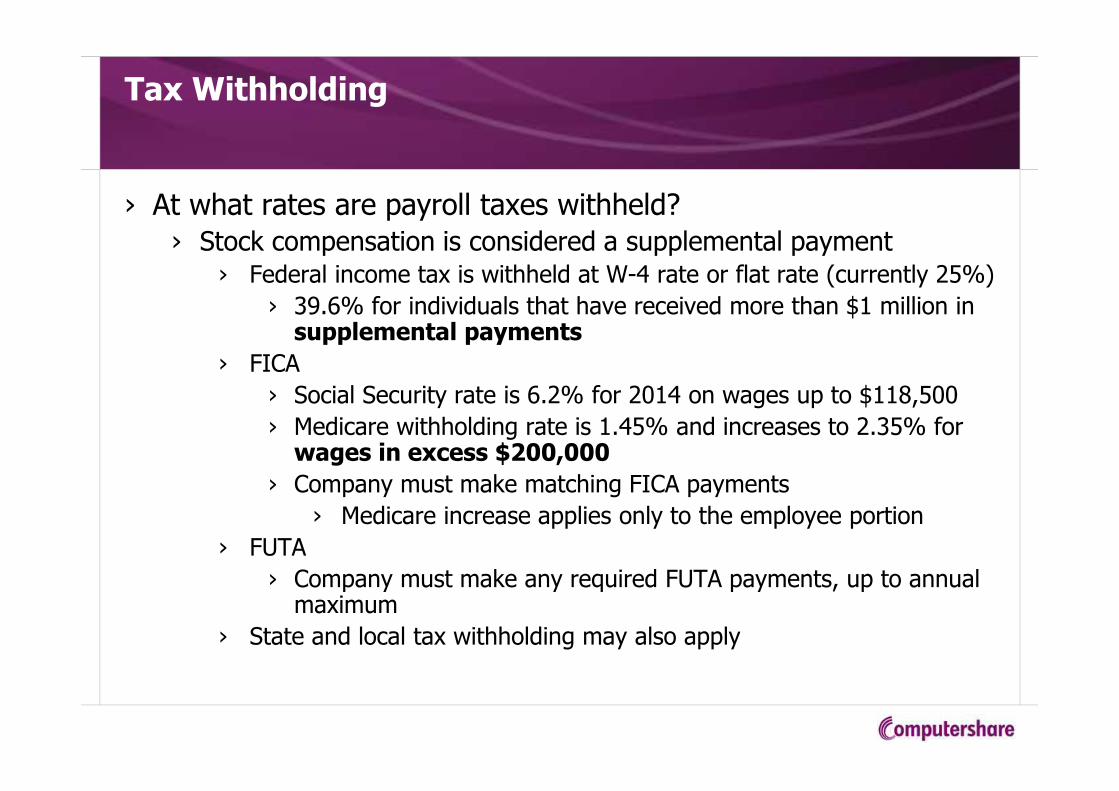

Tax Withholding

› At what rates are payroll taxes withheld?

› Stock compensation is considered a supplemental payment› Federal income tax is withheld at W-4 rate or flat rate (currently 25%)

› 39.6% for individuals that have received more than $1 million in supplemental payments

› FICA

› Social Security rate is 6.2% for 2014 on wages up to $118,500

› Medicare withholding rate is 1.45% and increases to 2.35% for wages in excess $200,000

› Company must make matching FICA payments

› Medicare increase applies only to the employee portion

› FUTA

› Company must make any required FUTA payments, up to annual maximum

› State and local tax withholding may also apply

Tax Withholding

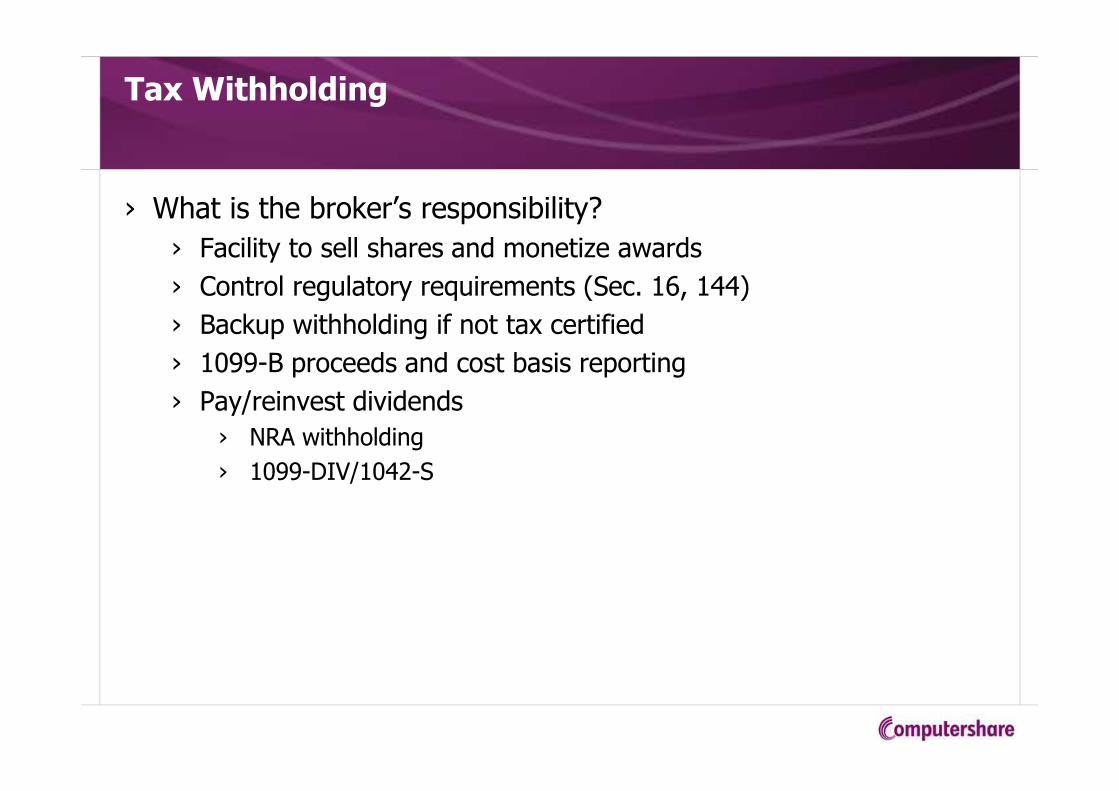

› What is the broker’s responsibility?

› Facility to sell shares and monetize awards

› Control regulatory requirements (Sec. 16, 144)

› Backup withholding if not tax certified

› 1099-B proceeds and cost basis reporting

› Pay/reinvest dividends

› NRA withholding

› 1099-DIV/1042-S

Tax Withholding

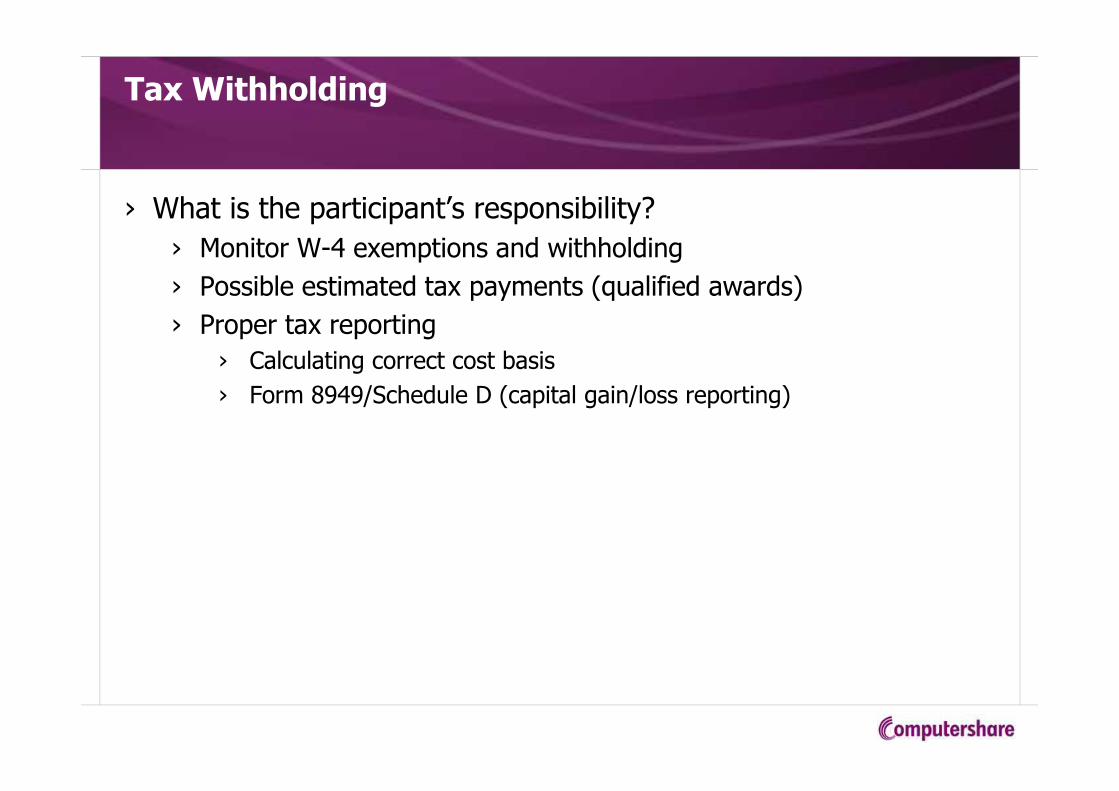

› What is the participant’s responsibility?

› Monitor W-4 exemptions and withholding

› Possible estimated tax payments (qualified awards)

› Proper tax reporting

› Calculating correct cost basis

› Form 8949/Schedule D (capital gain/loss reporting)

Dividends

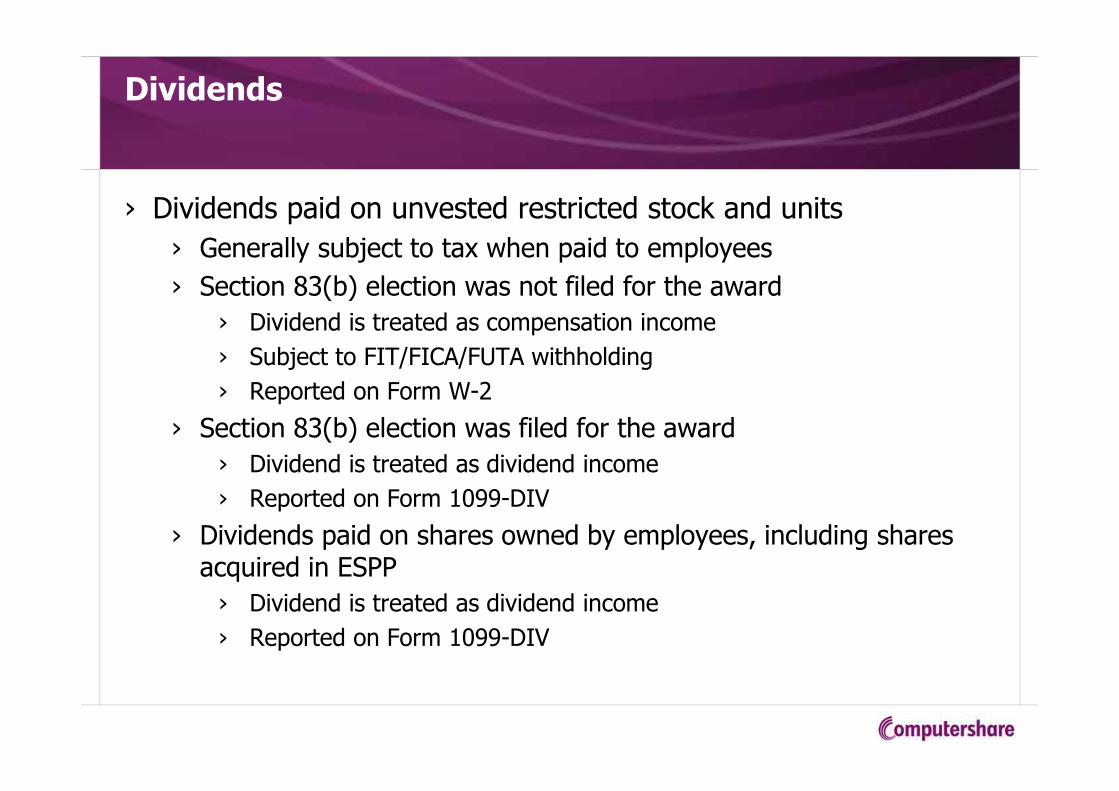

› Dividends paid on unvested restricted stock and units

› Generally subject to tax when paid to employees

› Section 83(b) election was not filed for the award

› Dividend is treated as compensation income

› Subject to FIT/FICA/FUTA withholding

› Reported on Form W-2

› Section 83(b) election was filed for the award

› Dividend is treated as dividend income

› Reported on Form 1099-DIV

› Dividends paid on shares owned by employees, including shares acquired in ESPP

› Dividend is treated as dividend income

› Reported on Form 1099-DIV

Retirement

Best practices

› Understand plan terms

› FICA taxes upon retirement-eligibility event

› Keep track of expiration dates on options once terminated

›Even those currently out-of-the-money

› Provide HR with address changes after retirement

17

Death

›Best practices

›Set up beneficiaries in advance

›Inform Plan administrator ASAP

›May change vesting terms

›ESPPs & ISOs – special tax rules

›Planning Tip: NQ options – waiting until after calendar year of death saves Social Security and Medicare tax

18

Diversification

Diversification/Optimization

• Avoid wealth concentration

• Cashless exercises vs. buy-and-hold

• Risk of stock decline and job loss

• Options/SARs – Tax event deferral, but eventually expire

• ESPPs – Tax event deferral, but may not be optimal

• RSAs – No deferral – taxed at vesting

• RSUs – Deferral possible if plan allows

19

Diversification

Diversification/Optimization

• 10b5-1 sales plans

• Allow for monetization in controlled fashion over time

• Allows for sales during blackout periods

• Ultimate questions:

• Do you need the money?

• Do you think the stock price will increase or not?

• Are you planning to leave the company?

20

Why Tax Issues are Important

Assume an individual in the highest tax bracket starts with the $800,000 in option value and lives in a state like CA. He exercises the options and pays off the payroll taxes by selling shares and keeping the balance. The $800,000 will be taxed at 54.94% ($439,547). Leaving $360,543.

Unfortunately, this individual dies the next day. His assets could get taxed at 40% on his assets at death ($144,181). This leaves $216,362 for his heirs. Which they spend and are taxed again at the sales tax rate of 7.5% so $16,227 more is deducted. In total this one transaction resulted in taxes of 75%.

21

Taxation – Example

› For all employee awards:

› Total Cost Basis = Purchase Price + Compensatory Income

› For covered employee awards:

› Covered – paid cash to receive award

› As of 2014, agents required to report only the purchase price

› Will create shareholder confusion, likely overpayment of taxes

› Share transfers from administration system will sever links to data required for cost basis calculations.

22

TAX UPDATE – Cost Basis

› No cost basis will be reported on noncovered securities:

› Vesting restricted stock

› Vesting restricted stock units

› Exercises of stock settled appreciation rights

› Stock swap exercises of stock options

› Net-settled exercises of stock options

› Part of the cost basis will be reported for:

› ESPP purchases = Purchase price only

› Cashless stock option exercises = exercise price only

› Will require participant to know and add compensatory portion to cost basis on Form 8949

23

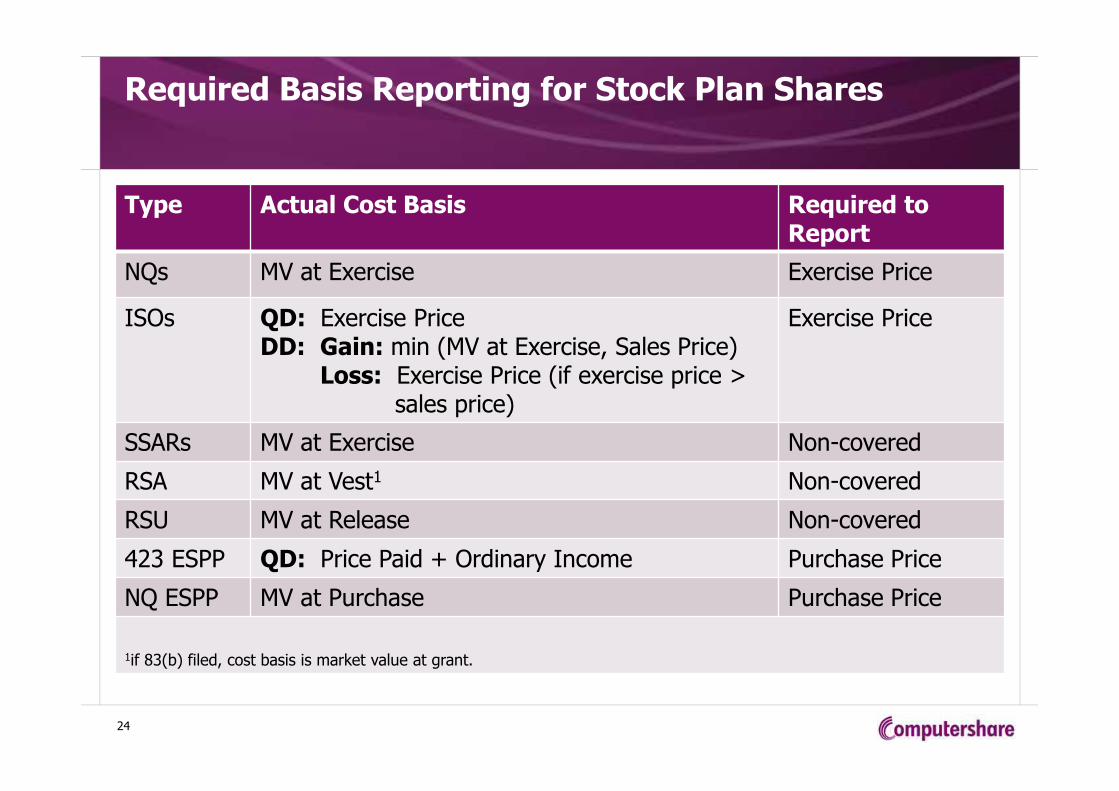

Required Basis Reporting for Stock Plan Shares

Type Actual Cost Basis Required to Report

NQs MV at Exercise Exercise Price

ISOs QD: Exercise PriceDD: Gain: min (MV at Exercise, Sales Price)

Loss: Exercise Price (if exercise price >sales price)

Exercise Price

SSARs MV at Exercise Non-covered

RSA MV at Vest1 Non-covered

RSU MV at Release Non-covered

423 ESPP QD: Price Paid + Ordinary Income Purchase Price

NQ ESPP MV at Purchase Purchase Price

1if 83(b) filed, cost basis is market value at grant.

24

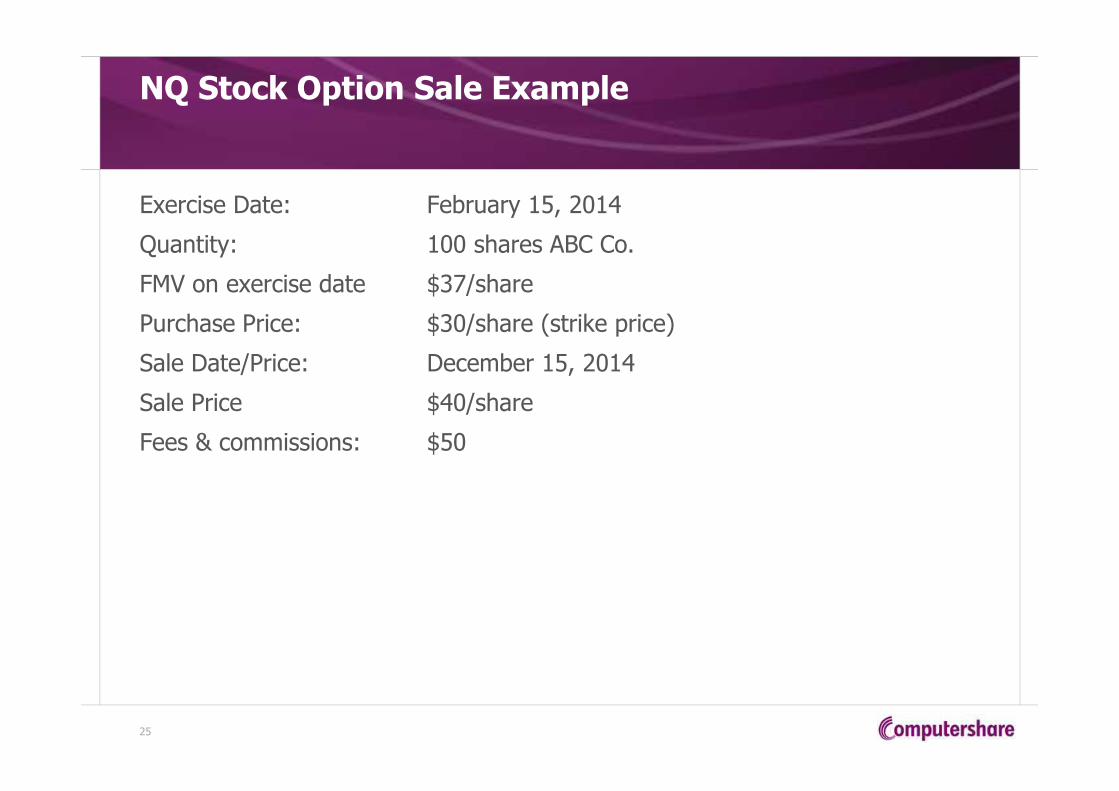

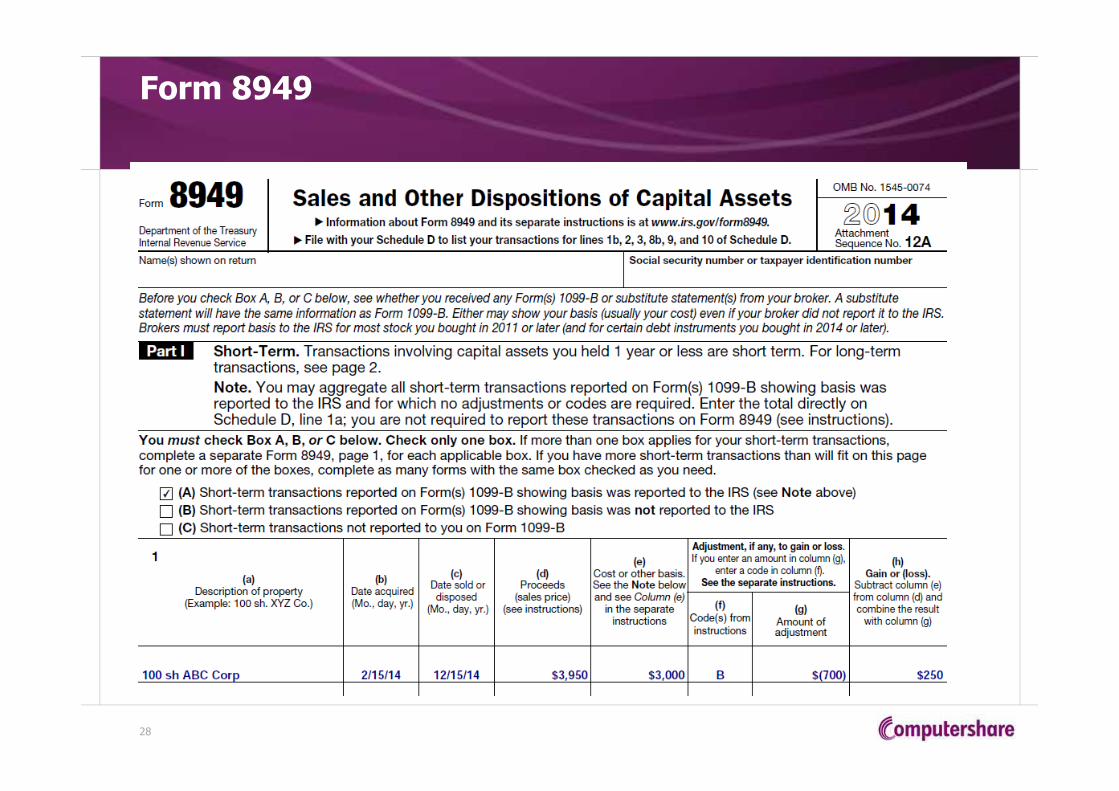

NQ Stock Option Sale Example

Exercise Date: February 15, 2014

Quantity: 100 shares ABC Co.

FMV on exercise date $37/share

Purchase Price: $30/share (strike price)

Sale Date/Price: December 15, 2014

Sale Price $40/share

Fees & commissions: $50

25

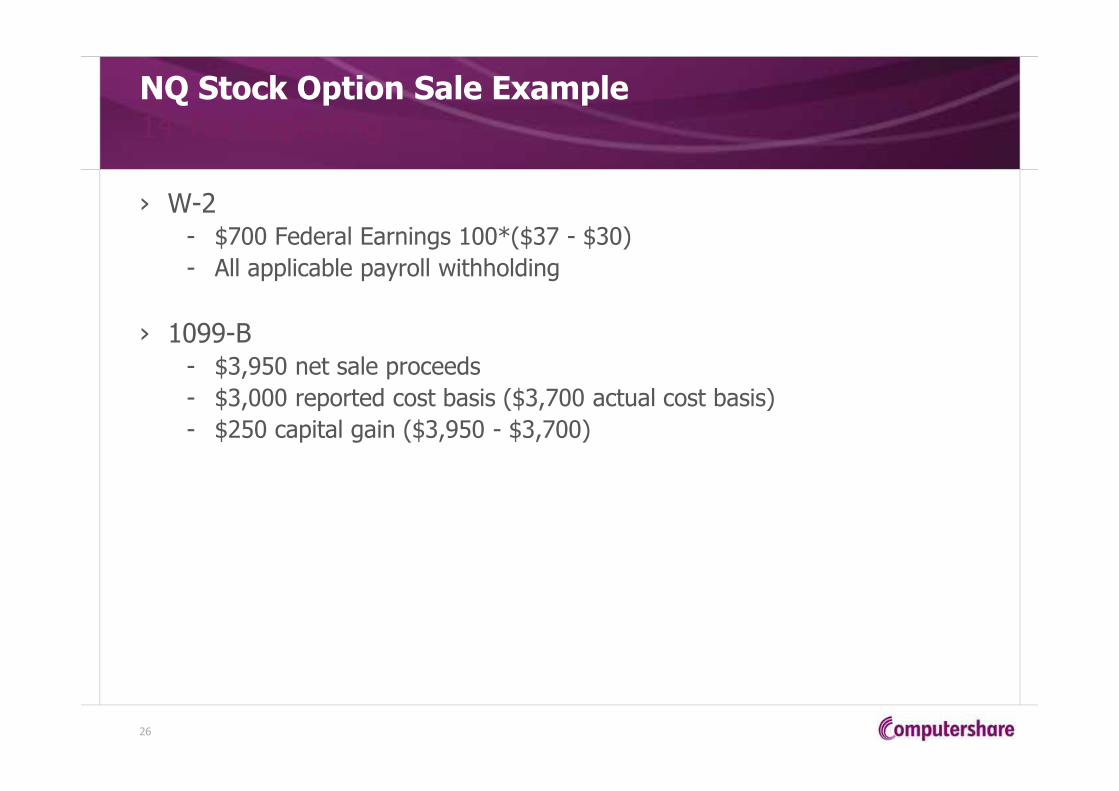

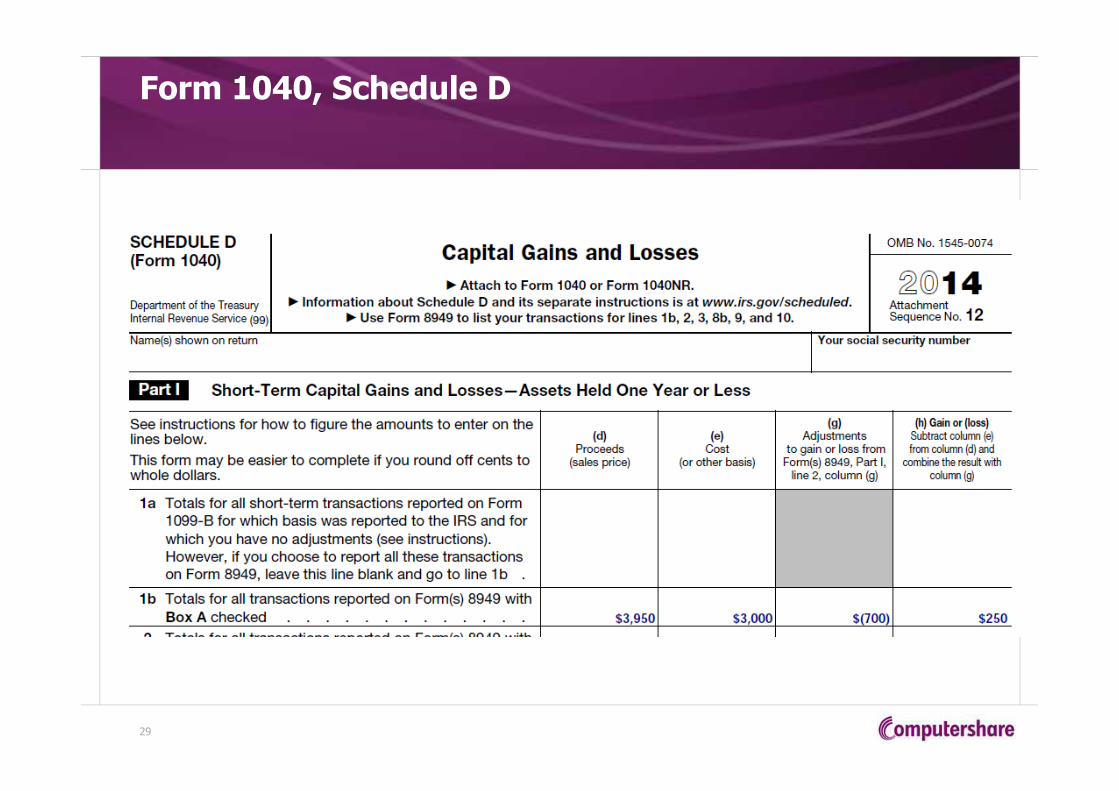

NQ Stock Option Sale Example14 Tax Reporting

› W-2- $700 Federal Earnings 100*($37 - $30)

- All applicable payroll withholding

› 1099-B- $3,950 net sale proceeds

- $3,000 reported cost basis ($3,700 actual cost basis)

- $250 capital gain ($3,950 - $3,700)

26

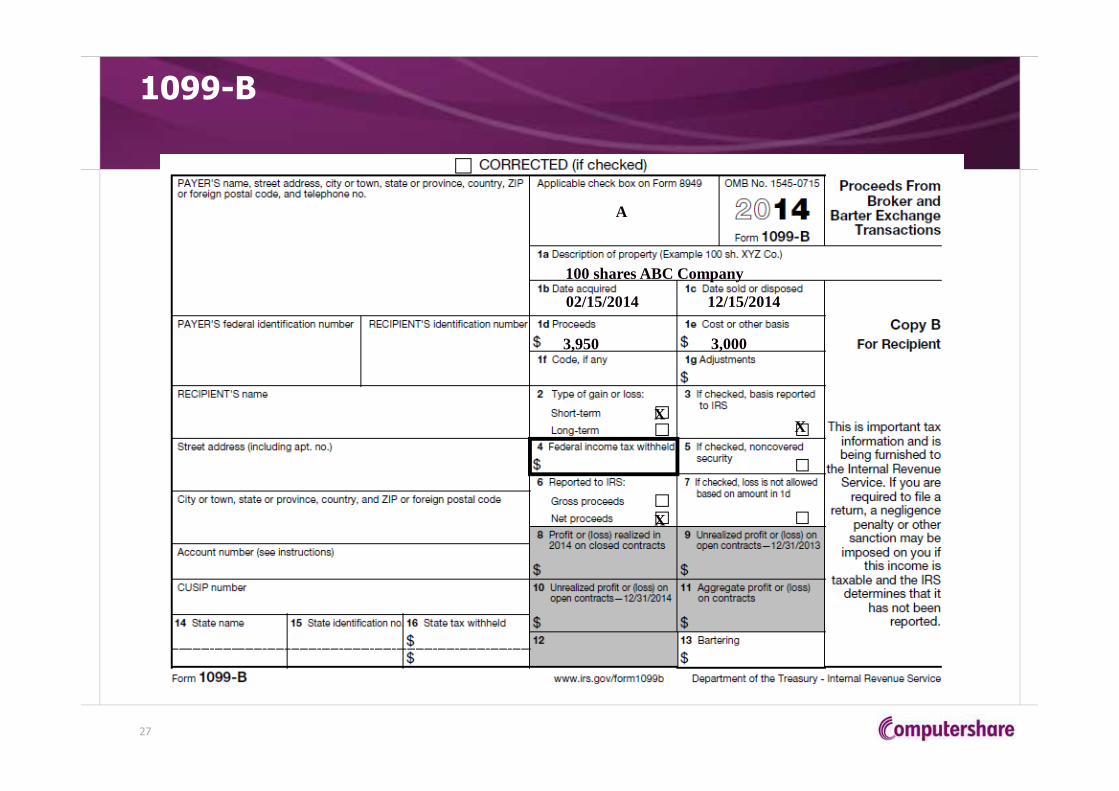

1099-B

27

A

100 shares ABC Company

02/15/2014 12/15/2014

3,950 3,000

XX

X

Form 8949

28

Form 1040, Schedule D

29

› Equity Compensation Resources

› Certified Equity Professional program (cepi.scu.edu)

› Reference books

› The Stock Options Book (NCEO)

› Selected Issues in Equity Compensation (NCEO)

› Equity Alternatives (NCEO)

› Consider Your Options (fairmark.com)

› NASPP Resources

› NASPP University online programs

› NASPP website

Resources

Q&A

31

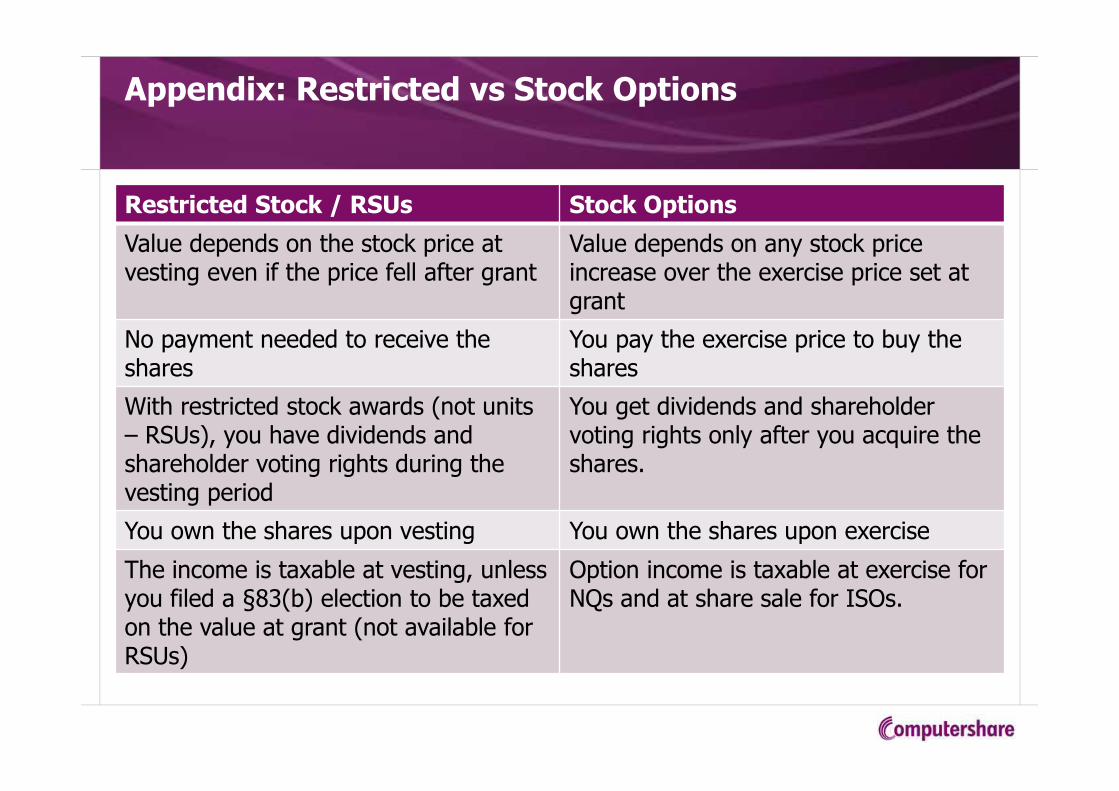

Appendix: Restricted vs Stock Options

Restricted Stock / RSUs Stock Options

Value depends on the stock price at vesting even if the price fell after grant

Value depends on any stock price increase over the exercise price set at grant

No payment needed to receive theshares

You pay the exercise price to buy the shares

With restricted stock awards (not units – RSUs), you have dividends and shareholder voting rights during the vesting period

You get dividends and shareholder voting rights only after you acquire the shares.

You own the shares upon vesting You own the shares upon exercise

The income is taxable at vesting, unless you filed a §83(b) election to be taxed on the value at grant (not available for RSUs)

Option income is taxable at exercise for NQs and at share sale for ISOs.

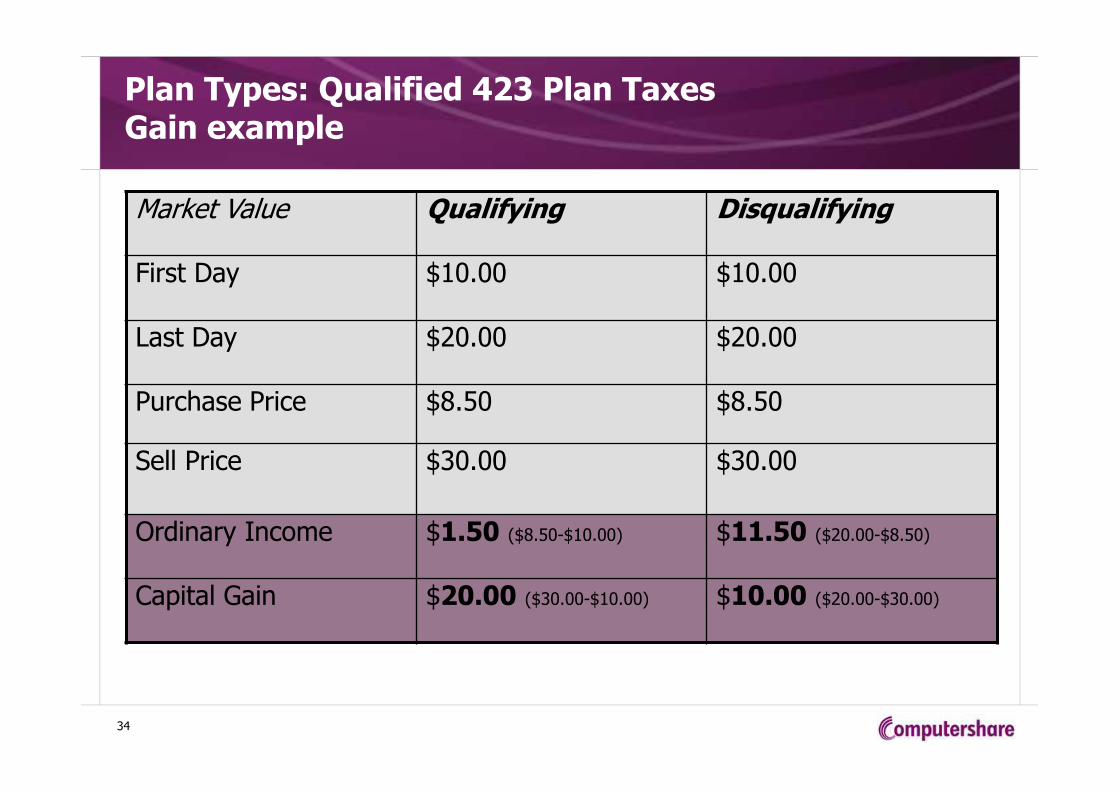

Plan Types: Qualified 423 Plan TaxesGain example

Market Value Qualifying Disqualifying

First Day $10.00 $10.00

Last Day $20.00 $20.00

Purchase Price $8.50 $8.50

Sell Price $30.00 $30.00

Ordinary Income $1.50 ($8.50-$10.00) $11.50 ($20.00-$8.50)

Capital Gain $20.00 ($30.00-$10.00) $10.00 ($20.00-$30.00)

34

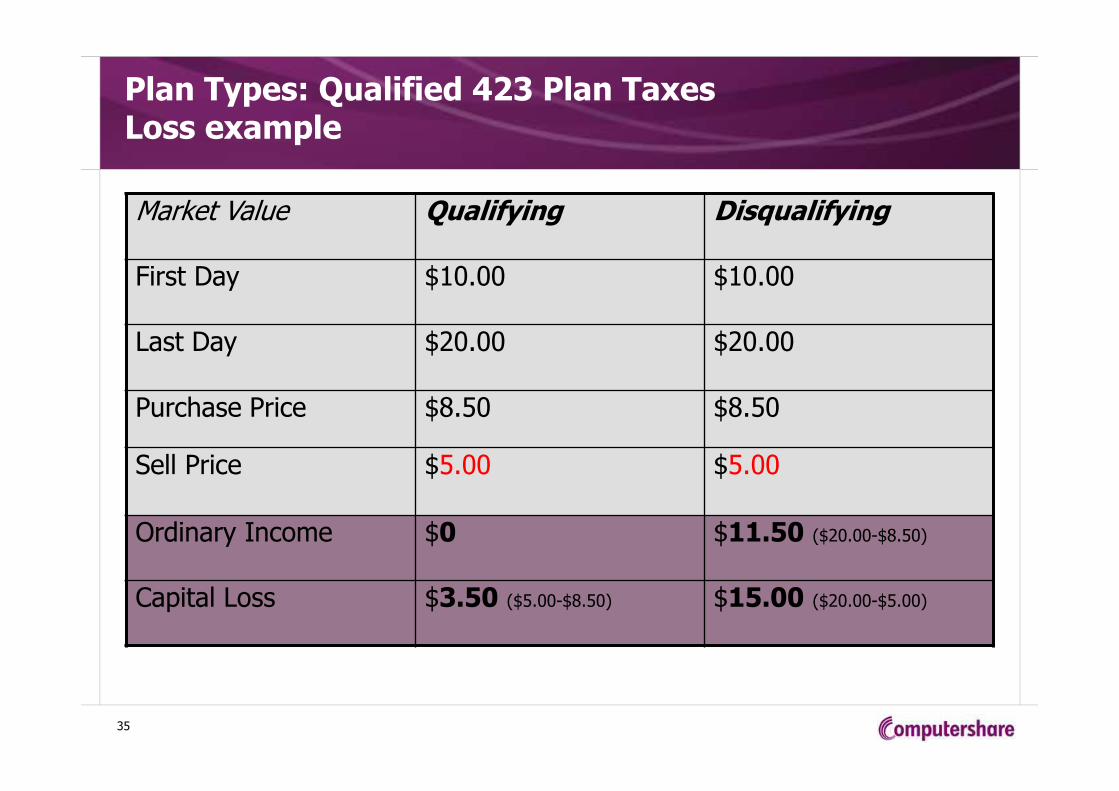

Plan Types: Qualified 423 Plan TaxesLoss example

Market Value Qualifying Disqualifying

First Day $10.00 $10.00

Last Day $20.00 $20.00

Purchase Price $8.50 $8.50

Sell Price $5.00 $5.00

Ordinary Income $0 $11.50 ($20.00-$8.50)

Capital Loss $3.50 ($5.00-$8.50) $15.00 ($20.00-$5.00)

35

Related Documents

![[PPT]PowerPoint Presentation - Login - Community Hubapps.naspa.org/cfp/uploads/NASPA17_InvisibleMinority.pptx · Web viewUnderstanding Intersecting Identities: The Invisible Minority](https://static.cupdf.com/doc/110x72/5b060d6c7f8b9a93418c3b3f/pptpowerpoint-presentation-login-community-viewunderstanding-intersecting.jpg)