CFA Institute Research Challenge hosted by CFA Society Vietnam RMIT University Saigon South Campus The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and presentation skills of university students. The following report was prepared in compliance with the Official Rules of the CFA Institute Research Challenge, is submitted by a team of university students as part of this annual educational initiative and should not be considered a professional report. Disclosures: Ownership and material conflicts of interest The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report. Receipt of compensation Compensation of the author(s) of this report is not based on investment banking revenue. Position as an officer or a director The author(s), or a member of their household, does not serve as an officer, director, or advisory board member of the subject company. Market making The author(s) does not act as a market maker in the subject company’s securities. Disclaimer The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by any individual affiliated with CFA Vietnam, CFA Institute, or the CFA Institute Research Challenge with regard to this company’s stock.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CFA Institute Research Challenge hosted by

CFA Society Vietnam RMIT University Saigon South Campus

The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and presentation skills of university students. The following report was prepared in compliance with the Official Rules of the CFA Institute Research Challenge, is submitted by a team of university students as part of this annual educational initiative and should not be considered a professional report.

Disclosures: Ownership and material conflicts of interest The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report. Receipt of compensation Compensation of the author(s) of this report is not based on investment banking revenue. Position as an officer or a director The author(s), or a member of their household, does not serve as an officer, director, or advisory board member of the subject company. Market making The author(s) does not act as a market maker in the subject company’s securities. Disclaimer The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by any individual affiliated with CFA Vietnam, CFA Institute, or the CFA Institute Research Challenge with regard to this company’s stock.

1

Sector: Materials – Industry: Industrial Metals

Ho Chi Minh Stock Exchange (HOSE)

HOA PHAT GROUP (Ticker: HPG.HM)

Closing price: 32,250 VND

USD/VND: 23,145

Target price: 40,610 VND

Recommendation: BUY (+25.92% Upside)

Date: 15th November 2020 EXECUTIVE SUMMARY

HPG: Rise To A New Stature We issue a BUY recommendation on Hoa Phat Group JSC (HPG) with a 12-month target price of 40,610 VND/share, presenting an upside of 25.92% from its closing price of VND 32,250

on 15th November 2020. Although HPG is currently traded at P/E (LTM) of 10.8x, we expect forward P/E

2021F to stand attractively at 6.8x (Figure 2) thanks to the below investment thesis: Dung Quat Super Project To Solidify No.1 Steel Producer Position In Vietnam The company dominates the construction steel and steel pipe market with 26.2% and 31.5% market share, respectively, thanks to large production capacity, competitive pricing strategy, superior product quality. We expect HPG steel revenue will continue to grow strongly (2020F-2024F CAGR of 16.77%) through DQSC Project with 2 key drivers: Expansion to the Central and South of Vietnam & International markets with Construction Steel and High sales from commercialized Hot Rolled Coil (HRC). Double-Digit Growth Fueled By Favorable Industry Outlook HPG is well-poised to capture the construction steel consumption growth that is primarily fueled by (1) fast-tracked government spending on infrastructure of VND 470 trillions (trn), (2) bright outlook of real estate industry and (3) growing export opportunities from accelerated global infrastructure investment and China’s supply-side control. The long-term growth is backed by the (1) abundant room for growth given Vietnam’s low steel consumption per capita and (2) strong macroeconomic fundamentals leading to consistent FDI inflows to the manufacturing sector that sustains the momentum for steel pipe demand. Due to oversupply situation in the market in recent years, the consolidation trend will benefits HPG as a dominant players to seize more market share from small EAF producers. HRC – Strategic Product Portfolio Expansion To Bolster Future Growth With DQSC, HPG has been able to produce HRC for both internal and external use from Q3/2020. Aside from HPG, Formosa can only produce up to 5 mn tons per annum (mpta), while demand was 12 mn tons in 2019. The competitive pricing strategy will allow HPG’s HRC to be entirely absorbed by the heavily undersupplied domestic market. Given the large DQSC’s HRC production capacity of 2.5-3mtpa, this product is envisioned to become the new revenue growth turbine for HPG moving forward. Superior Margins Enabled By Best-in-class Cost Structure While other competitors have to import HRC to produce flat steel products, the ability to produce in-house

HRC allows HPG to become the only Vietnamese steel producer to own a fully integrated production

chain and cut up to 10% total COGS. Moreover, (1) the efficient cost-control from BF-BOF technology,

(2) self-supplied electricity, (3) DQSC’s deep-water seaport to reduce logistic cost, and (4) strong market

power to raise selling prices will allow HPG to enjoy high margins (gross margin: 23.33% in 2019A to

35.69% 2024F) despite the expected increase in raw material prices.

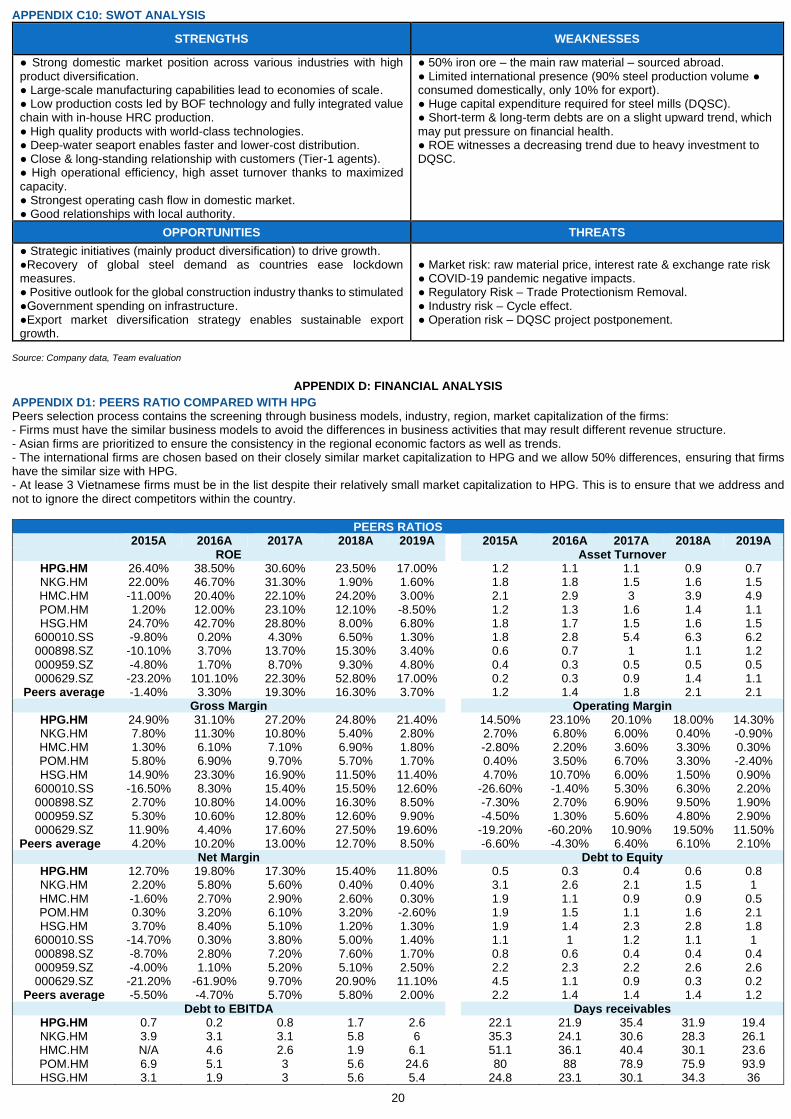

Operational Excellence – Solid Financial Position Stands Strongly Under Grey Sky HPG’s Chairman and Board of Directors have a far-sighted vision for HPG’s growth strategy. As experienced people in the industry, they have developed a great expansion strategy to meet the demand needs regardless of steel industry’s high cyclicality. Moreover, while the leverage ratio of HPG is quite low compared to industry peers, the BOD of HPG has strategically used the leverage efficiently (2019A net D/E of 0.7x) to expand the production scales with DQSC. Thanks to this, HPG will enjoy high revenue growth, excellence profitability and strong cash flow generation which will provide HPG the flexibility to maximize shareholder returns. (ROE: 17.03% in 2019A to 28.00% in 2024F). Noteworthy Environmental, Social, And Governance Despite efforts to mitigate the adverse environmental impact of BOF technology, scandals related to harmful exhaust and environmental degradation still occasionally occur, posing an investment risk for HPG. Although HPG’s executive management team has played an excellent role in securing high growth and earnings, large number of shares owned by internal members (44.22%) can pose the drawbacks in which other shareholders would have no control in the company decisions. Sum-of-the-Parts Valuation To Confirm Attractive Upside Potential As the company’s segments have different business models and risk profiles, we conduct Sum-of-the-Parts Valuation using the Discounted Free Cash Flow to Firm to value the Steel segment, Relative Valuation methodology using Relative P/E for Agriculture and Other Industries, and P/B to value the Real Estate segment. Our target price of VND 40,610 per share for HPG implies a 25.92% upside, reflecting an attractive value for the company’s solid growth profile. Key Risks Factors Well-Hedged By Unrivalled Cost Advantage And Diversification Strategy Raw materials price volatility and global trade protectionisms are identified as the key risks faced by HPG. Hence, we have incorporated the former into scenario and sensitivity analysis to reflect its impact on our target price. With unrivalled cost advantage, HPG’s steel products can withstand the short-term effect of raw material price volatility. The company is also strategically diversifying its export markets to mitigate the negative impact of rising global trade protectionisms.

Key Metrics & Ratios 2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F CAGR

2020-24 Net Revenue (VND bn) 46,161.69 55,836.46 63,658.19 90,994.81 112,281.32 119,316.79 126,641.79 132,516.35 15.79% Gross Profit 12,542.48 13,840.31 13,647.05 22,962.25 32,305.30 37,162.89 40,432.42 43,547.99 26.12% Gross Profit Margin(%) 27.17% 24.79% 21.44% 25.23% 28.77% 31.15% 31.93% 27.17% 9.82% Net Profits 8,014.76 8,600.55 7,578.25 11,189.50 16,939.35 20,678.62 23,015.29 25,359.27 27.32% Net Margin (%) 17.36% 15.40% 11.90% 12.30% 15.09% 17.33% 18.17% 19.14% 9.96% EPS (VND/share) 4,074 3,015 2,726 3,355 5,085 6,212 6,916 7,622 22.83% ROE (%) 30.65% 23.48% 17.03% 21.22% 27.74% 29.42% 27.94% 28.00% 10.46%

Figure 3. Market Snapshot

Stock data, as of 15 November 2020

Price (VND) 32,250

52-week high/low (VND) 32,750 / 13,253

Px. Perf (3/6/12 months) (%) 13.7 / 59.1 /

64.0

Shares outstanding (mn) 3,313

Free float shares (mn) 1,988

Market Cap (VND bn) 106,853

Foreign owned ratio 34%

Foreign ownership limit 49%

EV/EBITDA (LTM) 7.2x

Source: Reuters

Figure 1. HPG’s Historical Share Price

vs VN-Index

Source: Reuters

0

200

400

600

800

1,000

1,200

1,400

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

HPG's Closing Price (LHS) VNIndex (RHS)

Source: Reuters

Figure 2. HPG's Historical P/E (Ltm)

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

Mar2018

Jun2018

Sep2018

Dec2018

Mar2019

Jun2019

Sep2019

Dec2019

Mar2020

Jun2020

Sep2020

Oct2020

HPG's Historical P/E 6Y Average

7.3x

2

BUSINESS DESCRIPTION

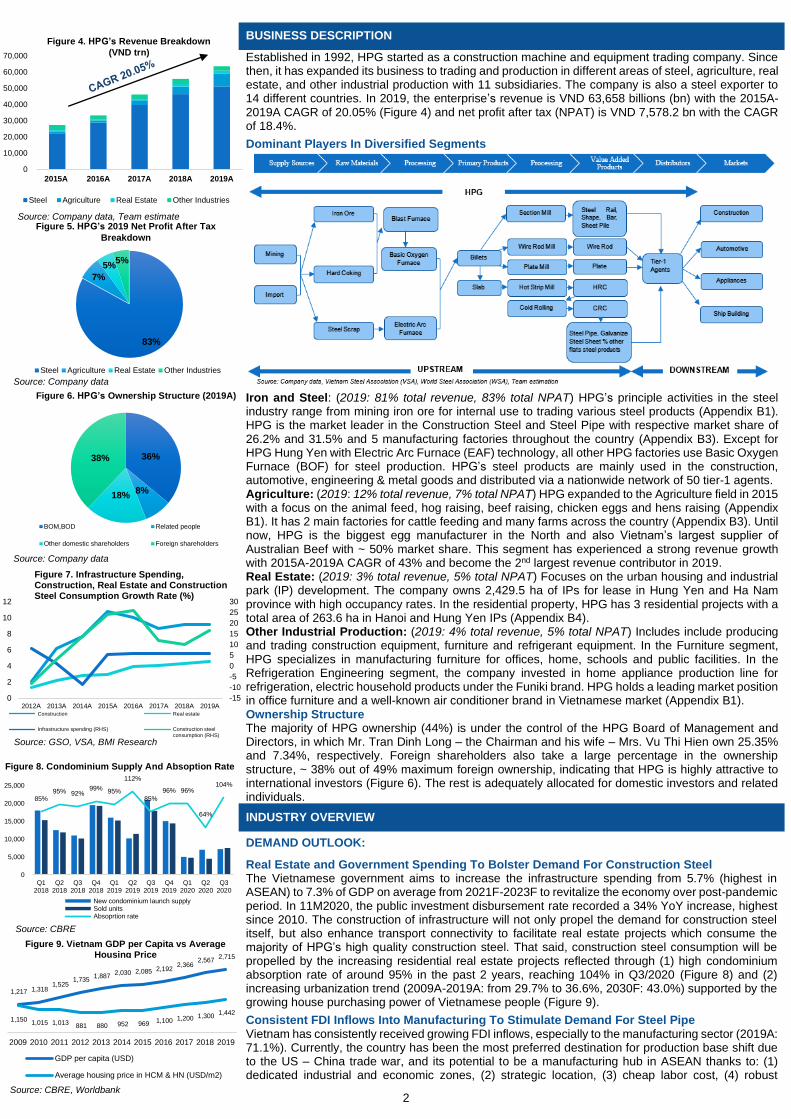

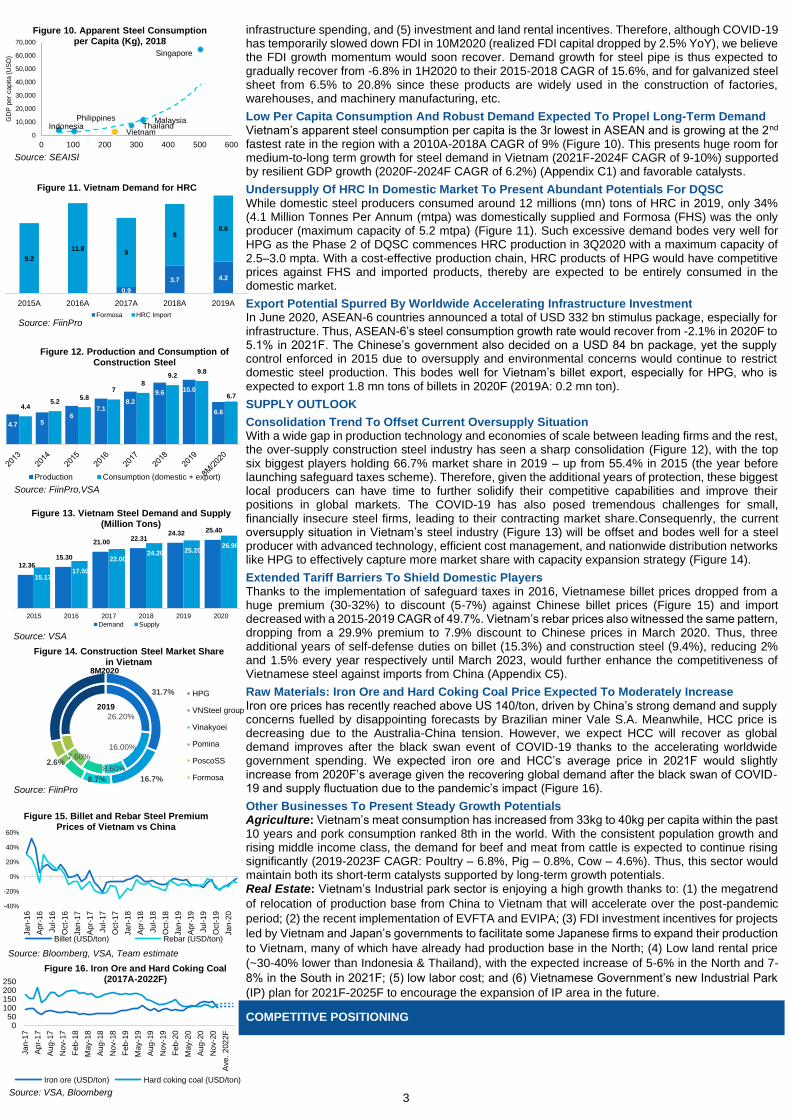

Established in 1992, HPG started as a construction machine and equipment trading company. Since then, it has expanded its business to trading and production in different areas of steel, agriculture, real estate, and other industrial production with 11 subsidiaries. The company is also a steel exporter to 14 different countries. In 2019, the enterprise’s revenue is VND 63,658 billions (bn) with the 2015A-2019A CAGR of 20.05% (Figure 4) and net profit after tax (NPAT) is VND 7,578.2 bn with the CAGR of 18.4%. Dominant Players In Diversified Segments

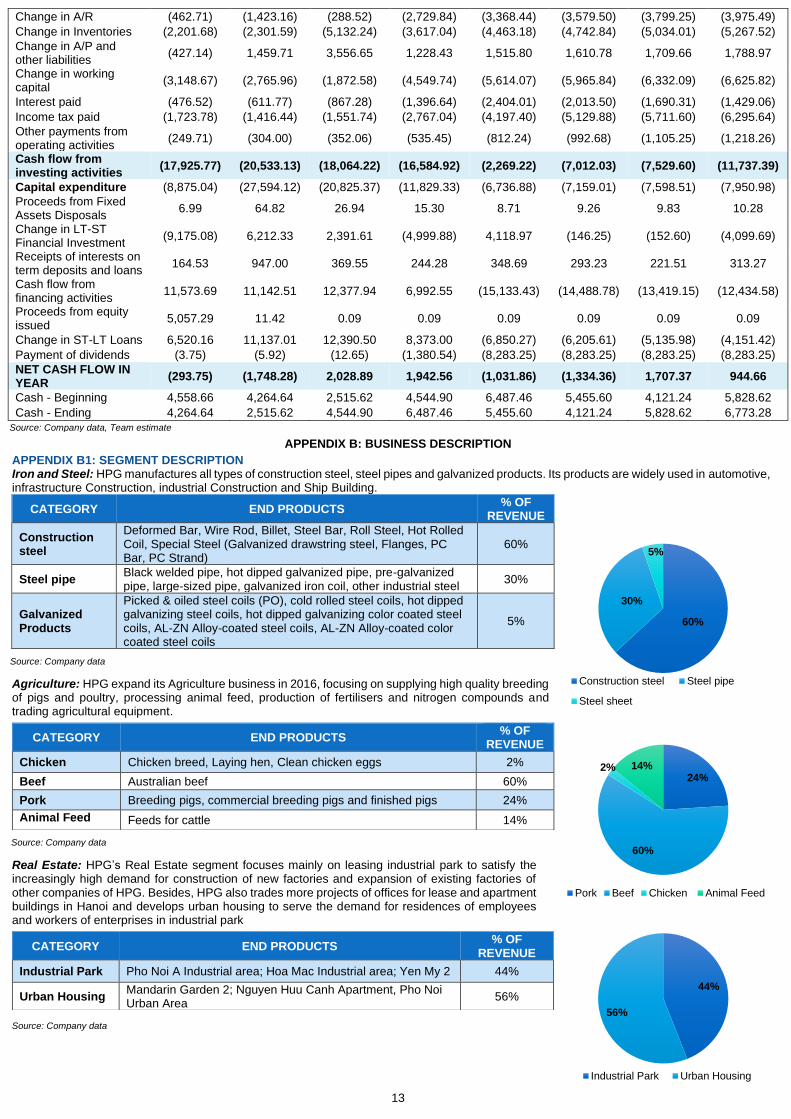

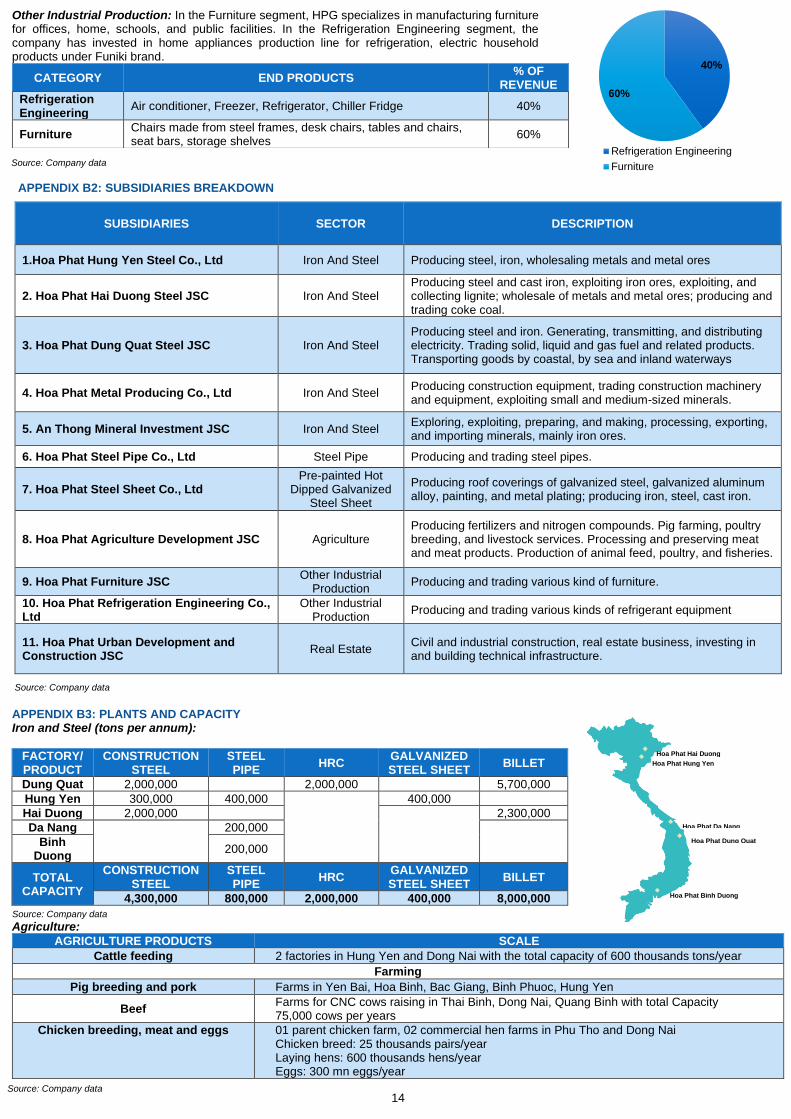

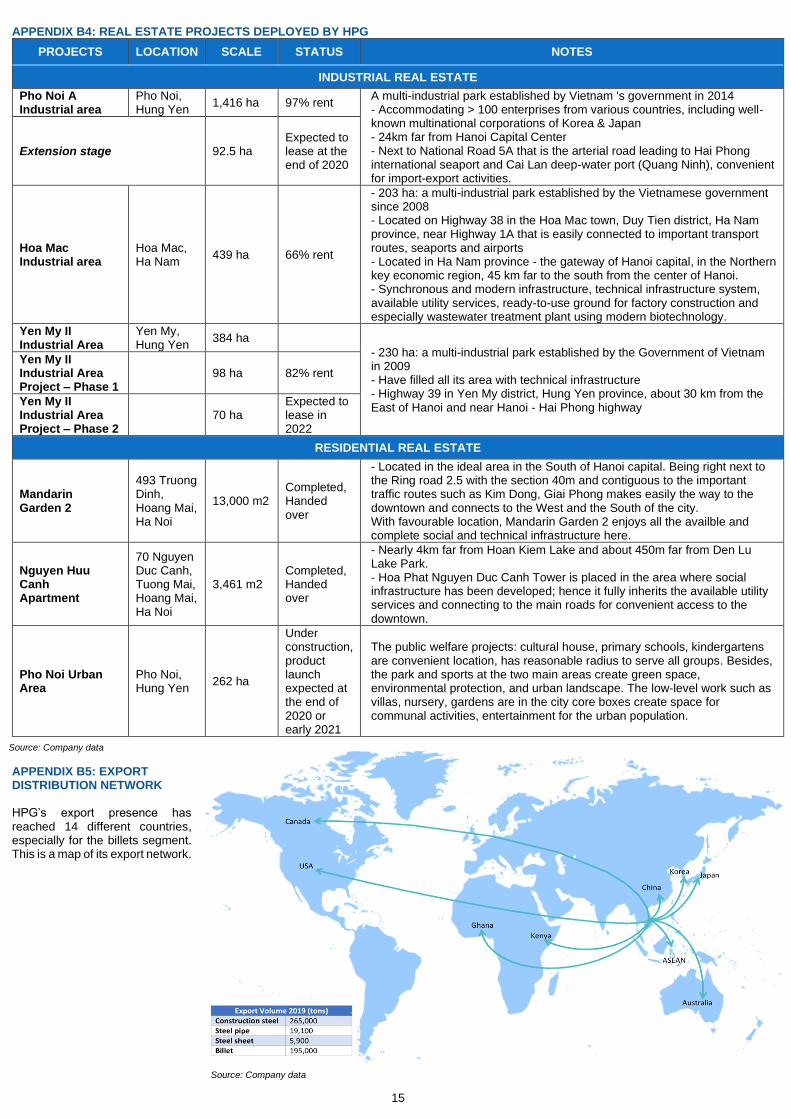

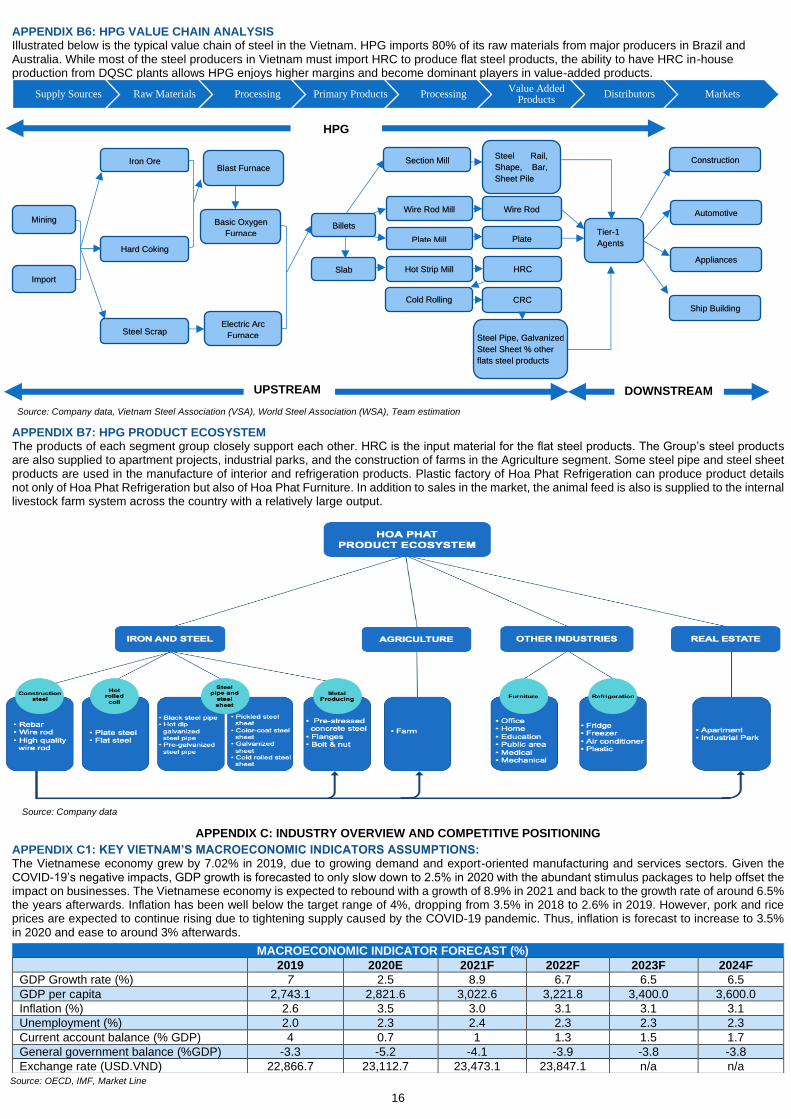

Iron and Steel: (2019: 81% total revenue, 83% total NPAT) HPG’s principle activities in the steel industry range from mining iron ore for internal use to trading various steel products (Appendix B1). HPG is the market leader in the Construction Steel and Steel Pipe with respective market share of 26.2% and 31.5% and 5 manufacturing factories throughout the country (Appendix B3). Except for HPG Hung Yen with Electric Arc Furnace (EAF) technology, all other HPG factories use Basic Oxygen Furnace (BOF) for steel production. HPG’s steel products are mainly used in the construction, automotive, engineering & metal goods and distributed via a nationwide network of 50 tier-1 agents. Agriculture: (2019: 12% total revenue, 7% total NPAT) HPG expanded to the Agriculture field in 2015 with a focus on the animal feed, hog raising, beef raising, chicken eggs and hens raising (Appendix B1). It has 2 main factories for cattle feeding and many farms across the country (Appendix B3). Until now, HPG is the biggest egg manufacturer in the North and also Vietnam’s largest supplier of Australian Beef with ~ 50% market share. This segment has experienced a strong revenue growth with 2015A-2019A CAGR of 43% and become the 2nd largest revenue contributor in 2019. Real Estate: (2019: 3% total revenue, 5% total NPAT) Focuses on the urban housing and industrial park (IP) development. The company owns 2,429.5 ha of IPs for lease in Hung Yen and Ha Nam province with high occupancy rates. In the residential property, HPG has 3 residential projects with a total area of 263.6 ha in Hanoi and Hung Yen IPs (Appendix B4). Other Industrial Production: (2019: 4% total revenue, 5% total NPAT) Includes include producing and trading construction equipment, furniture and refrigerant equipment. In the Furniture segment, HPG specializes in manufacturing furniture for offices, home, schools and public facilities. In the Refrigeration Engineering segment, the company invested in home appliance production line for refrigeration, electric household products under the Funiki brand. HPG holds a leading market position in office furniture and a well-known air conditioner brand in Vietnamese market (Appendix B1). Ownership Structure The majority of HPG ownership (44%) is under the control of the HPG Board of Management and Directors, in which Mr. Tran Dinh Long – the Chairman and his wife – Mrs. Vu Thi Hien own 25.35% and 7.34%, respectively. Foreign shareholders also take a large percentage in the ownership structure, ~ 38% out of 49% maximum foreign ownership, indicating that HPG is highly attractive to international investors (Figure 6). The rest is adequately allocated for domestic investors and related individuals.

INDUSTRY OVERVIEW

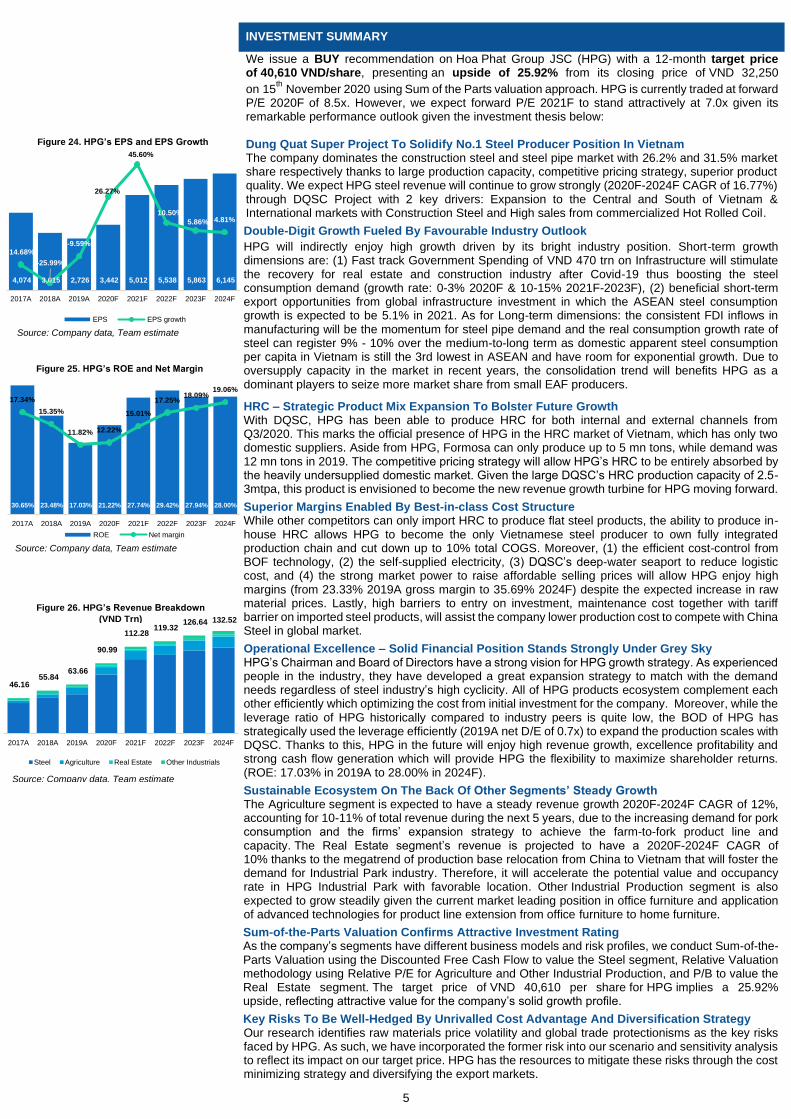

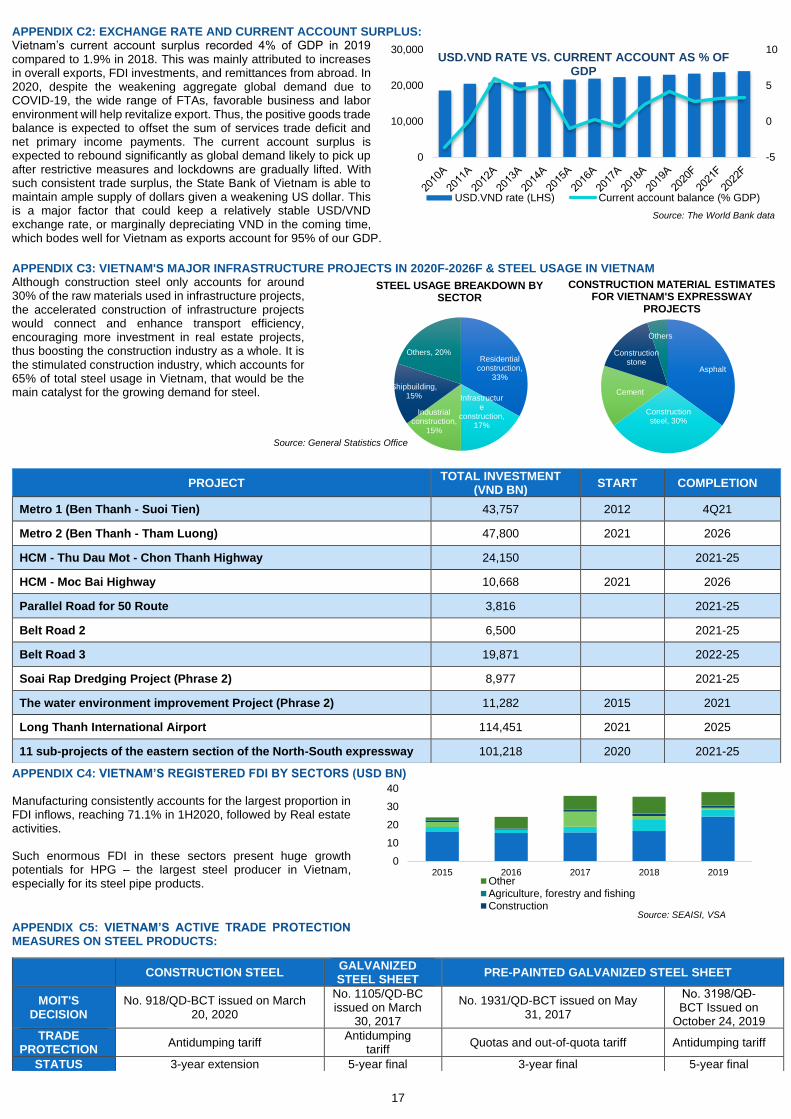

DEMAND OUTLOOK: Real Estate and Government Spending To Bolster Demand For Construction Steel The Vietnamese government aims to increase the infrastructure spending from 5.7% (highest in ASEAN) to 7.3% of GDP on average from 2021F-2023F to revitalize the economy over post-pandemic period. In 11M2020, the public investment disbursement rate recorded a 34% YoY increase, highest since 2010. The construction of infrastructure will not only propel the demand for construction steel itself, but also enhance transport connectivity to facilitate real estate projects which consume the majority of HPG’s high quality construction steel. That said, construction steel consumption will be propelled by the increasing residential real estate projects reflected through (1) high condominium absorption rate of around 95% in the past 2 years, reaching 104% in Q3/2020 (Figure 8) and (2) increasing urbanization trend (2009A-2019A: from 29.7% to 36.6%, 2030F: 43.0%) supported by the growing house purchasing power of Vietnamese people (Figure 9). Consistent FDI Inflows Into Manufacturing To Stimulate Demand For Steel Pipe Vietnam has consistently received growing FDI inflows, especially to the manufacturing sector (2019A: 71.1%). Currently, the country has been the most preferred destination for production base shift due to the US – China trade war, and its potential to be a manufacturing hub in ASEAN thanks to: (1) dedicated industrial and economic zones, (2) strategic location, (3) cheap labor cost, (4) robust

83%

7%

5%5%

Steel Agriculture Real Estate Other Industries

Figure 5. HPG’s 2019 Net Profit After Tax

Breakdown

Source: Company data

36%

8%18%

38%

BOM,BOD Related people

Other domestic shareholders Foreign shareholders

Figure 6. HPG’s Ownership Structure (2019A)

Source: Company data

Source: GSO, VSA, BMI Research

Figure 7. Infrastructure Spending, Construction, Real Estate and Construction Steel Consumption Growth Rate (%)

-15

-10

-5

0

5

10

15

20

25

30

0

2

4

6

8

10

12

2012A 2013A 2014A 2015A 2016A 2017A 2018A 2019AConstruction Real estate

Infrastructure spending (RHS) Construction steelconsumption (RHS)

85%95% 92%

99% 95%

112%

85%

96% 96%

64%

104%

0%

20%

40%

60%

80%

100%

120%

0

5,000

10,000

15,000

20,000

25,000

Q12018

Q22018

Q32018

Q42018

Q12019

Q22019

Q32019

Q42019

Q12020

Q22020

Q32020

New condominium launch supplySold unitsAbsoprtion rate

Figure 8. Condominium Supply And Absoption Rate

Source: CBRE

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2015A 2016A 2017A 2018A 2019A

Steel Agriculture Real Estate Other Industries

Figure 4. HPG’s Revenue Breakdown (VND trn)

Source: Company data, Team estimate

1,217 1,318 1,525

1,735 1,887

2,030 2,085 2,192 2,366

2,567 2,715

1,150 1,015 1,013 881 880 952 969 1,100 1,200 1,300

1,442

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

GDP per capita (USD)

Average housing price in HCM & HN (USD/m2)

Figure 9. Vietnam GDP per Capita vs Average Housing Price

Source: CBRE, Worldbank

3

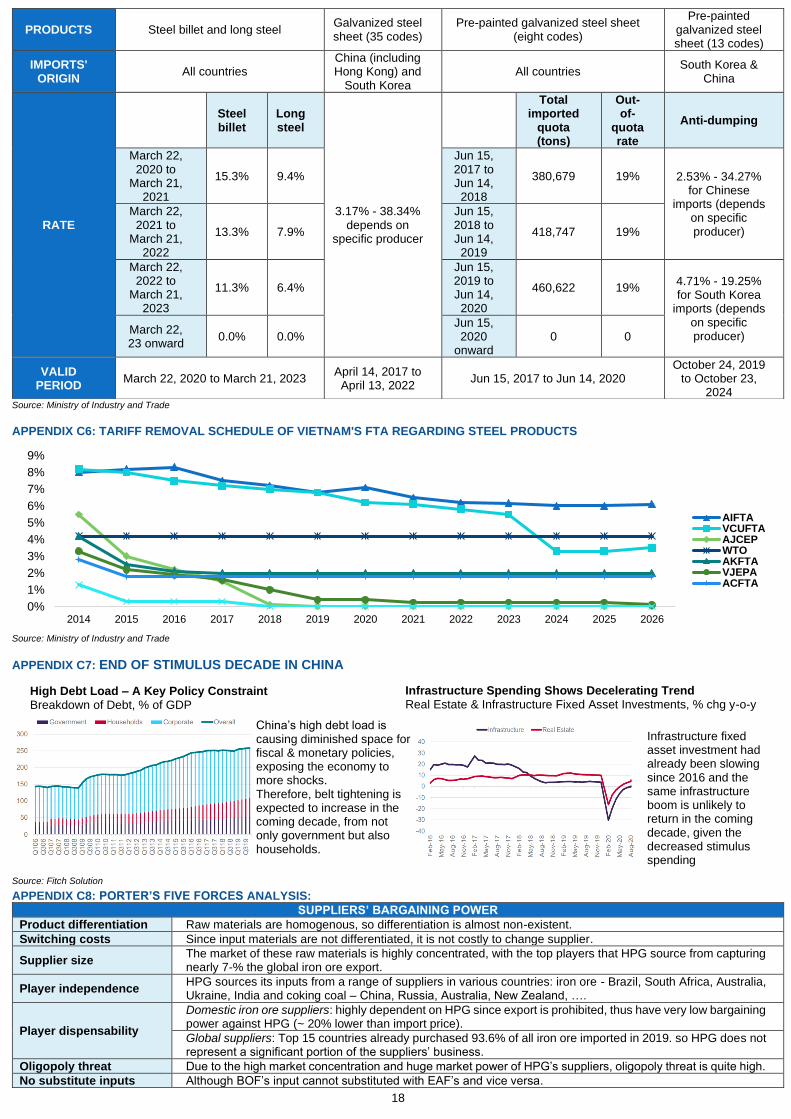

infrastructure spending, and (5) investment and land rental incentives. Therefore, although COVID-19 has temporarily slowed down FDI in 10M2020 (realized FDI capital dropped by 2.5% YoY), we believe the FDI growth momentum would soon recover. Demand growth for steel pipe is thus expected to gradually recover from -6.8% in 1H2020 to their 2015-2018 CAGR of 15.6%, and for galvanized steel sheet from 6.5% to 20.8% since these products are widely used in the construction of factories, warehouses, and machinery manufacturing, etc. Low Per Capita Consumption And Robust Demand Expected To Propel Long-Term Demand Vietnam’s apparent steel consumption per capita is the 3r lowest in ASEAN and is growing at the 2nd fastest rate in the region with a 2010A-2018A CAGR of 9% (Figure 10). This presents huge room for medium-to-long term growth for steel demand in Vietnam (2021F-2024F CAGR of 9-10%) supported by resilient GDP growth (2020F-2024F CAGR of 6.2%) (Appendix C1) and favorable catalysts. Undersupply Of HRC In Domestic Market To Present Abundant Potentials For DQSC While domestic steel producers consumed around 12 millions (mn) tons of HRC in 2019, only 34% (4.1 Million Tonnes Per Annum (mtpa) was domestically supplied and Formosa (FHS) was the only producer (maximum capacity of 5.2 mtpa) (Figure 11). Such excessive demand bodes very well for HPG as the Phase 2 of DQSC commences HRC production in 3Q2020 with a maximum capacity of 2.5–3.0 mpta. With a cost-effective production chain, HRC products of HPG would have competitive prices against FHS and imported products, thereby are expected to be entirely consumed in the domestic market. Export Potential Spurred By Worldwide Accelerating Infrastructure Investment In June 2020, ASEAN-6 countries announced a total of USD 332 bn stimulus package, especially for infrastructure. Thus, ASEAN-6’s steel consumption growth rate would recover from -2.1% in 2020F to 5.1% in 2021F. The Chinese’s government also decided on a USD 84 bn package, yet the supply control enforced in 2015 due to oversupply and environmental concerns would continue to restrict domestic steel production. This bodes well for Vietnam’s billet export, especially for HPG, who is expected to export 1.8 mn tons of billets in 2020F (2019A: 0.2 mn ton). SUPPLY OUTLOOK Consolidation Trend To Offset Current Oversupply Situation With a wide gap in production technology and economies of scale between leading firms and the rest, the over-supply construction steel industry has seen a sharp consolidation (Figure 12), with the top six biggest players holding 66.7% market share in 2019 – up from 55.4% in 2015 (the year before launching safeguard taxes scheme). Therefore, given the additional years of protection, these biggest local producers can have time to further solidify their competitive capabilities and improve their positions in global markets. The COVID-19 has also posed tremendous challenges for small, financially insecure steel firms, leading to their contracting market share.Consequenrly, the current oversupply situation in Vietnam’s steel industry (Figure 13) will be offset and bodes well for a steel producer with advanced technology, efficient cost management, and nationwide distribution networks like HPG to effectively capture more market share with capacity expansion strategy (Figure 14). Extended Tariff Barriers To Shield Domestic Players Thanks to the implementation of safeguard taxes in 2016, Vietnamese billet prices dropped from a huge premium (30-32%) to discount (5-7%) against Chinese billet prices (Figure 15) and import decreased with a 2015-2019 CAGR of 49.7%. Vietnam’s rebar prices also witnessed the same pattern, dropping from a 29.9% premium to 7.9% discount to Chinese prices in March 2020. Thus, three additional years of self-defense duties on billet (15.3%) and construction steel (9.4%), reducing 2% and 1.5% every year respectively until March 2023, would further enhance the competitiveness of Vietnamese steel against imports from China (Appendix C5). Raw Materials: Iron Ore and Hard Coking Coal Price Expected To Moderately Increase Iron ore prices has recently reached above US 140/ton, driven by China’s strong demand and supply concerns fuelled by disappointing forecasts by Brazilian miner Vale S.A. Meanwhile, HCC price is decreasing due to the Australia-China tension. However, we expect HCC will recover as global demand improves after the black swan event of COVID-19 thanks to the accelerating worldwide government spending. We expected iron ore and HCC’s average price in 2021F would slightly increase from 2020F’s average given the recovering global demand after the black swan of COVID-19 and supply fluctuation due to the pandemic’s impact (Figure 16). Other Businesses To Present Steady Growth Potentials Agriculture: Vietnam’s meat consumption has increased from 33kg to 40kg per capita within the past 10 years and pork consumption ranked 8th in the world. With the consistent population growth and rising middle income class, the demand for beef and meat from cattle is expected to continue rising significantly (2019-2023F CAGR: Poultry – 6.8%, Pig – 0.8%, Cow – 4.6%). Thus, this sector would maintain both its short-term catalysts supported by long-term growth potentials. Real Estate: Vietnam’s Industrial park sector is enjoying a high growth thanks to: (1) the megatrend

of relocation of production base from China to Vietnam that will accelerate over the post-pandemic

period; (2) the recent implementation of EVFTA and EVIPA; (3) FDI investment incentives for projects

led by Vietnam and Japan’s governments to facilitate some Japanese firms to expand their production

to Vietnam, many of which have already had production base in the North; (4) Low land rental price

(~30-40% lower than Indonesia & Thailand), with the expected increase of 5-6% in the North and 7-

8% in the South in 2021F; (5) low labor cost; and (6) Vietnamese Government’s new Industrial Park

(IP) plan for 2021F-2025F to encourage the expansion of IP area in the future.

COMPETITIVE POSITIONING

-40%

-20%

0%

20%

40%

60%

Ja

n-1

6

Ap

r-1

6

Ju

l-16

Oct-

16

Ja

n-1

7

Ap

r-1

7

Ju

l-17

Oct-

17

Ja

n-1

8

Ap

r-1

8

Ju

l-18

Oct-

18

Ja

n-1

9

Ap

r-1

9

Ju

l-19

Oct-

19

Ja

n-2

0

Billet (USD/ton) Rebar (USD/ton)

Figure 15. Billet and Rebar Steel Premium Prices of Vietnam vs China

Source: Bloomberg, VSA, Team estimate

Source: SEAISI

IndonesiaPhilippines

ThailandMalaysia

Singapore

Vietnam0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0 100 200 300 400 500 600

GD

P p

er

capita (

US

D)

Figure 10. Apparent Steel Consumption per Capita (Kg), 2018

Source: FiinPro

0.9

3.7 4.2

9.2

11.89

88.6

2015A 2016A 2017A 2018A 2019A

Formosa HRC Import

Figure 11. Vietnam Demand for HRC

4.7 56

7.18.2

9.6 10.0

6.64.4

5.25.8

78

9.29.8

6.7

Figure 12. Production and Consumption of Construction Steel

Production Consumption (domestic + export)

Source: FiinPro,VSA

12.36

15.30

21.00 22.31

24.32 25.40

15.17 17.50

22.00 24.20 25.20

26.96

2015 2016 2017 2018 2019 2020

Figure 13. Vietnam Steel Demand and Supply(Million Tons)

Demand Supply

Source: VSA

26.20%

16.00%

8.60%

7.60%

31.7%

16.7%8.7%

2.6%

Figure 14. Construction Steel Market Share in Vietnam

HPG

VNSteel group

Vinakyoei

Pomina

PoscoSS

Formosa

2019

8M2020

Source: FiinPro

Source: VSA, Bloomberg

050

100150200250

Ja

n-1

7

Ap

r-1

7

Au

g-1

7

Nov-1

7

Feb

-18

May-1

8

Au

g-1

8

Nov-1

8

Feb

-19

May-1

9

Au

g-1

9

Nov-1

9

Feb

-20

May-2

0

Au

g-2

0

Nov-2

0

Ave

. 2

02

2F

Iron ore (USD/ton) Hard coking coal (USD/ton)

Figure 16. Iron Ore and Hard Coking Coal (2017A-2022F)

4

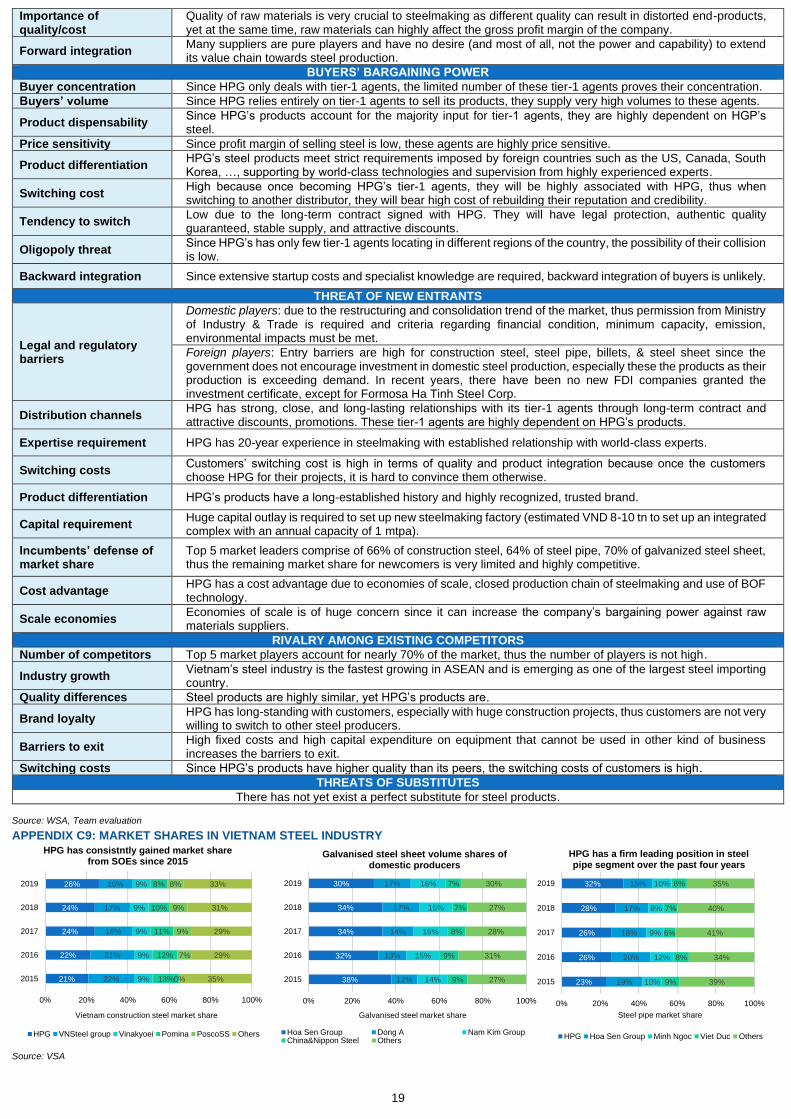

Thanks to the competitive pricing, close relationships with tier-1 agents, huge economies of scale, and superior product quality enhanced by deployment of world-leading technologies, HPG manages to have (1) high bargaining power with buyers, (2) low threat of new entrants; and (3) low threat of substitutes. Yet due to the highly competitive market and huge dependence on overseas suppliers, HPG has (4) relatively low bargaining power with suppliers and (5) moderate rivalry (Figure 17). Fully Integrated Production Chain To Create Huge Gap With Domestic Players HPG is one of the two steelmakers in Vietnam apart from Formosa to have an upstream integrated value chain from raw materials processing to finished products, including HRC production (Appendix B6). This creates a huge competitive advantage for HPG because with control over the production process, HPG can (1) enhance cost control and profit margins thanks to lower logistic cost and self-supplied HRC; (2) secure quality consistency and supply chain continuity; (3) improve demand forecast accuracy; and (4) remain resilient against raw materials and HRC price volatility. Lowest Production Cost Led By BF-BOF Technology And Self-Supplied Electricity HPG is one of the 3 steelmakers (with Formosa & Tisco) to deploy the BF-BOF Technology for making billets (BF-BOF: 95%, EAF: 5% of 2020F’s total capacity).The BF-BOF with cheaper material costs (iron ore, HCC and other) and advanced technology helps save 10-15% production cost per unit compared to all other domestic producers using the EAF technology (steel scrap – 80% of total cost) (Figure 20). Such diversified raw materials of BF-BOF partly shields HPG from commodity price risk. Notably, BF-BOF’s higher initial outlay, operation and maintenance cost as well as low feedstock flexibility compared with EAF act as huge barriers for other domestic producers to adopt BF-BOF technology. The heat generated during HCC processing with BF-BOF technology is also used for thermal power production, which helps self-supply ~80% of Hai Duong plant’s electricity demand and expected 60% of DQSC’s electricity demand. This further cements HPG’s cost advantage compared with domestic players and the primary reason why HPG is able to price its products the lowest among its peers (Figure 18). Unique Advantage Against Southern Peers Thanks To DQSC’s Deep-Water Seaport The deep-water seaport is strategically located in Dung Quat, Quang Ngai province – in the Central of Vietnam, having 11 docks and can accommodate up-to 200,000-ton ships. The port alleviates the HPG’s biggest hindrance to establish its dominance in the Southern market – logistic cost and geographical proximity to customers. Specifically, the port would facilitate importing input materials, exporting finished products from the complex to domestic (both Northern & Southern) and foreign markets. The production cost is also reduced by ~ VND 70,000 – 115,000 per ton, which poses a great cost advantage given that the firm must import millions of tons every year. The cost and geographical advantages of the deep-water seaport will pave the way for HPG to penetrate into this highly attractive market, which accounts for 50% of total domestic steel demand.

CORPORATE STRATEGY

Leverage On HRC Production To Cement Market Leader Position The ability to manufacture HRC allows HPG to fully self-supply the input for steel pipes and galvanized steel, which will significantly enhance the profit margin in the flat steel segments. This feature plays a key role in creating an upstream integrated value chain for steel production (Appendix B6), further improving the already superior gross margin in the domestic market. Moreover, HPG will also sell 60% of its HRC to the heavily under-supplied domestic HRC market, which is expected to be entirely consumed thanks to its competitive pricing against the imported HRC. Expand The Central, Southern Market Share Through DQSC And Competitive Pricing Strategy While HPG is dominating the Northern Market with 32% market share, the company will penetrate further into Central and Southern markets through the DQSC with the enormous, designed capacity of 4 mtpa (Figure 21). Favorably, The HPG’s upstream integrated value chain in the steel production significantly reduces the manufacturing cost, allowing it to implement a competitive pricing strategy to gain an upper hand over the competitors. Moreover, HPG also demonstrates their aggressive sales strategy in these markets through a series of customer conferences for its distributors and the investment in Dong Nai and Can Tho ports to ensure the stability of its distribution stream. Enlarge International Footprint Through Diversified Export Markets Thanks to the high-quality standards products, HPG has imprinted its presence in the export markets of construction steel, steel pipe, steel sheets, and billets (Figure 22). For future plans, HPG aims to gain more international purchases with its competitive price compared to Chinese steel producers in construction steel (Figure 23), which will be fueled by the strong production capacity from DQSC and the low production cost. Moreover, as an attempt to reduce dependency on any specific market, HPG also diversifies its export destinations (Appendix B5). Reap Stable Revenues From Other Segments To Create A Sustainable Ecosystem HPG has expanded to other areas to essentially reduce the dependence on steel and form an ecosystem where steel products will efficiently complement agriculture and real estate segments, which furthers enhance cost optimization, reduces initial investment for HPG’s projects (Appendix B7). Agriculture: HPG plans to supply 450,000 commercial pigs, 75,000 cattle and 300 million eggs per year by 2022. Also, the company will invest in the processing and distribution of safe and high-quality food to the market, completing a farm-to-fork chain. Real Estate: HPG focuses on expanding its industrial parks to capture high occupancy rate fueled by supply chain shift from China to Vietnam. Regarding the residential area, the company aims to sell the Pho Noi-Hung Yen Urban Area by the end of 2020. Other Industrial Production: HPG sets target to continue its leading position in the furniture market with the recent impressive office furniture and plastic-reducing projects. Moreover, the company aims to maintain stable revenues from the white goods segment (freezers, refrigerators, air conditioners).

Source: Team evaluation

Figure 19. Competitive Positioning Map

Figure 21. HPG’s Construction Steel Market Share in Domestic Regions

Source: Company data

31%31% 34%

28%

50%54%

15% 21% 24%

2017A 2018A 2019A Jan2020

Feb2020

Mar2020

Apr2020

May2020

Sep2020

North Central South

012345

SUPPLIERS'BARGANING

POWER

BUYERS'BARGAINING

POWER

THREAT OF NEWENTRANTS

RIVALRYAMONG

EXISTING…

THREAT OFSUBSTITUTES

Source: Team evaluation

Figure 17. Porter’s Five Forces Analysis

Source: Fiinpro

12,350

10,700

12,850

11,145

Jan-1

9

Fe

b-1

9

Mar-

19

Apr-

19

May-1

9

Jun-1

9

Jul-19

Aug-1

9

Sep-1

9

Oct-

19

Nov-1

9

Dec-1

9

Jan-2

0

Fe

b-2

0

Mar-

20

Apr-

20

May-2

0

Jun-2

0

Jul-20

Aug-2

0

Sep-2

0

Oct-

20

HPG Industry Average

Figure 18. HPG’s Competitive Construction Steel Price (VND/kg)

Source: VSA, FiinPro, Team estimate

Figure 20. Average Production Cost from Raw Materials per Ton of Steel (VND)

1,220,967 6,744,814

7,965,781

HPG Others

55%

4%1%

40%

Construction Steel Steel Pipe

Galvanized Steel Sheet Billets

Figure 22. HPG’s 2019A Exports Breakdown

Source: Company data

8

10

12

14

16

18

Jun-1

7

Aug-1

7

Oct-

17

Dec-1

7

Fe

b-1

8

Apr-

18

Jun-1

8

Aug-1

8

Oct-

18

Dec-1

8

Fe

b-1

9

Apr-

19

Jun-1

9

Aug-1

9

Oct-

19

Dec-1

9

Fe

b-2

0

Apr-

20

Jun-2

0

Aug-2

0

VND mn/ton

HPG's steel rebar priceChina domestic steel rebar price

Figure 23. Steel Rebar Price of HPG vs

Chinese Producers

Source: Bloomberg, VSA

5

INVESTMENT SUMMARY

We issue a BUY recommendation on Hoa Phat Group JSC (HPG) with a 12-month target price of 40,610 VND/share, presenting an upside of 25.92% from its closing price of VND 32,250

on 15th November 2020 using Sum of the Parts valuation approach. HPG is currently traded at forward

P/E 2020F of 8.5x. However, we expect forward P/E 2021F to stand attractively at 7.0x given its remarkable performance outlook given the investment thesis below: Dung Quat Super Project To Solidify No.1 Steel Producer Position In Vietnam The company dominates the construction steel and steel pipe market with 26.2% and 31.5% market share respectively thanks to large production capacity, competitive pricing strategy, superior product quality. We expect HPG steel revenue will continue to grow strongly (2020F-2024F CAGR of 16.77%) through DQSC Project with 2 key drivers: Expansion to the Central and South of Vietnam & International markets with Construction Steel and High sales from commercialized Hot Rolled Coil. Double-Digit Growth Fueled By Favourable Industry Outlook

HPG will indirectly enjoy high growth driven by its bright industry position. Short-term growth dimensions are: (1) Fast track Government Spending of VND 470 trn on Infrastructure will stimulate the recovery for real estate and construction industry after Covid-19 thus boosting the steel consumption demand (growth rate: 0-3% 2020F & 10-15% 2021F-2023F), (2) beneficial short-term export opportunities from global infrastructure investment in which the ASEAN steel consumption growth is expected to be 5.1% in 2021. As for Long-term dimensions: the consistent FDI inflows in manufacturing will be the momentum for steel pipe demand and the real consumption growth rate of steel can register 9% - 10% over the medium-to-long term as domestic apparent steel consumption per capita in Vietnam is still the 3rd lowest in ASEAN and have room for exponential growth. Due to oversupply capacity in the market in recent years, the consolidation trend will benefits HPG as a dominant players to seize more market share from small EAF producers. HRC – Strategic Product Mix Expansion To Bolster Future Growth With DQSC, HPG has been able to produce HRC for both internal and external channels from Q3/2020. This marks the official presence of HPG in the HRC market of Vietnam, which has only two domestic suppliers. Aside from HPG, Formosa can only produce up to 5 mn tons, while demand was 12 mn tons in 2019. The competitive pricing strategy will allow HPG’s HRC to be entirely absorbed by the heavily undersupplied domestic market. Given the large DQSC’s HRC production capacity of 2.5-3mtpa, this product is envisioned to become the new revenue growth turbine for HPG moving forward. Superior Margins Enabled By Best-in-class Cost Structure While other competitors can only import HRC to produce flat steel products, the ability to produce in-house HRC allows HPG to become the only Vietnamese steel producer to own fully integrated production chain and cut down up to 10% total COGS. Moreover, (1) the efficient cost-control from BOF technology, (2) the self-supplied electricity, (3) DQSC’s deep-water seaport to reduce logistic cost, and (4) the strong market power to raise affordable selling prices will allow HPG enjoy high margins (from 23.33% 2019A gross margin to 35.69% 2024F) despite the expected increase in raw material prices. Lastly, high barriers to entry on investment, maintenance cost together with tariff barrier on imported steel products, will assist the company lower production cost to compete with China Steel in global market. Operational Excellence – Solid Financial Position Stands Strongly Under Grey Sky HPG’s Chairman and Board of Directors have a strong vision for HPG growth strategy. As experienced people in the industry, they have developed a great expansion strategy to match with the demand needs regardless of steel industry’s high cyclicity. All of HPG products ecosystem complement each other efficiently which optimizing the cost from initial investment for the company. Moreover, while the leverage ratio of HPG historically compared to industry peers is quite low, the BOD of HPG has strategically used the leverage efficiently (2019A net D/E of 0.7x) to expand the production scales with DQSC. Thanks to this, HPG in the future will enjoy high revenue growth, excellence profitability and strong cash flow generation which will provide HPG the flexibility to maximize shareholder returns. (ROE: 17.03% in 2019A to 28.00% in 2024F). Sustainable Ecosystem On The Back Of Other Segments’ Steady Growth The Agriculture segment is expected to have a steady revenue growth 2020F-2024F CAGR of 12%, accounting for 10-11% of total revenue during the next 5 years, due to the increasing demand for pork consumption and the firms’ expansion strategy to achieve the farm-to-fork product line and capacity. The Real Estate segment’s revenue is projected to have a 2020F-2024F CAGR of 10% thanks to the megatrend of production base relocation from China to Vietnam that will foster the demand for Industrial Park industry. Therefore, it will accelerate the potential value and occupancy rate in HPG Industrial Park with favorable location. Other Industrial Production segment is also expected to grow steadily given the current market leading position in office furniture and application of advanced technologies for product line extension from office furniture to home furniture. Sum-of-the-Parts Valuation Confirms Attractive Investment Rating As the company’s segments have different business models and risk profiles, we conduct Sum-of-the-Parts Valuation using the Discounted Free Cash Flow to value the Steel segment, Relative Valuation methodology using Relative P/E for Agriculture and Other Industrial Production, and P/B to value the Real Estate segment. The target price of VND 40,610 per share for HPG implies a 25.92% upside, reflecting attractive value for the company’s solid growth profile. Key Risks To Be Well-Hedged By Unrivalled Cost Advantage And Diversification Strategy Our research identifies raw materials price volatility and global trade protectionisms as the key risks faced by HPG. As such, we have incorporated the former risk into our scenario and sensitivity analysis to reflect its impact on our target price. HPG has the resources to mitigate these risks through the cost minimizing strategy and diversifying the export markets.

Figure 24. HPG’s EPS and EPS Growth

Source: Company data, Team estimate

4,074 3,015 2,726 3,442 5,012 5,538 5,863 6,145

-14.68%

-25.99%

-9.59%

26.27%

45.60%

10.50%

5.86% 4.81%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

EPS EPS growth

Source: Company data, Team estimate

Figure 26. HPG’s Revenue Breakdown

(VND Trn)

46.16 55.84

63.66

90.99

112.28 119.32

126.64 132.52

-

20,000.00

40,000.00

60,000.00

80,000.00

100 ,000.00

120 ,000.00

140 ,000.00

2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

Steel Agriculture Real Estate Other Industrials

Figure 25. HPG’s ROE and Net Margin

Source: Company data, Team estimate

30.65% 23.48% 17.03% 21.22% 27.74% 29.42% 27.94% 28.00%

17.34%

15.35%

11.82% 12.22%

15.01%

17.25%18.09%

19.06%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

ROE Net margin

6

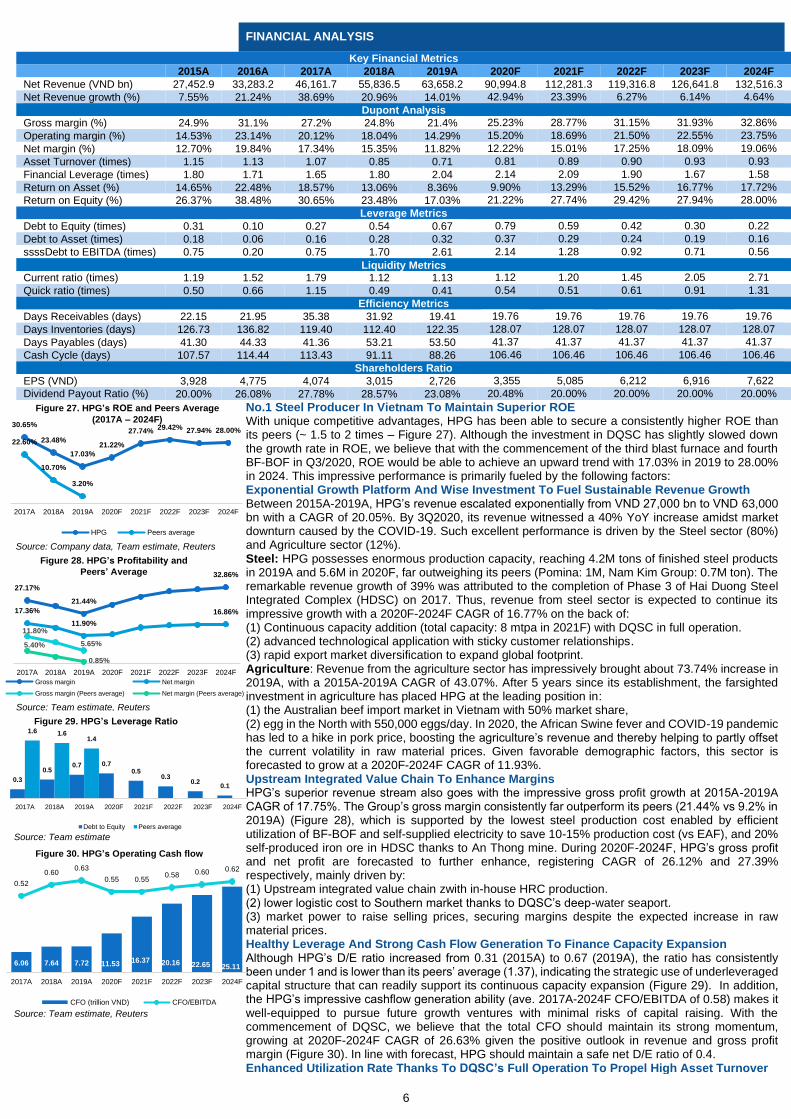

FINANCIAL ANALYSIS

Key Financial Metrics

2015A 2016A 2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

Net Revenue (VND bn) 27,452.9 33,283.2 46,161.7 55,836.5 63,658.2 90,994.8 112,281.3 119,316.8 126,641.8 132,516.3

Net Revenue growth (%) 7.55% 21.24% 38.69% 20.96% 14.01% 42.94% 23.39% 6.27% 6.14% 4.64%

Dupont Analysis

Gross margin (%) 24.9% 31.1% 27.2% 24.8% 21.4% 25.23% 28.77% 31.15% 31.93% 32.86%

Operating margin (%) 14.53% 23.14% 20.12% 18.04% 14.29% 15.20% 18.69% 21.50% 22.55% 23.75%

Net margin (%) 12.70% 19.84% 17.34% 15.35% 11.82% 12.22% 15.01% 17.25% 18.09% 19.06%

Asset Turnover (times) 1.15 1.13 1.07 0.85 0.71 0.81 0.89 0.90 0.93 0.93

Financial Leverage (times) 1.80 1.71 1.65 1.80 2.04 2.14 2.09 1.90 1.67 1.58

Return on Asset (%) 14.65% 22.48% 18.57% 13.06% 8.36% 9.90% 13.29% 15.52% 16.77% 17.72%

Return on Equity (%) 26.37% 38.48% 30.65% 23.48% 17.03% 21.22% 27.74% 29.42% 27.94% 28.00%

Leverage Metrics

Debt to Equity (times) 0.31 0.10 0.27 0.54 0.67 0.79 0.59 0.42 0.30 0.22

Debt to Asset (times) 0.18 0.06 0.16 0.28 0.32 0.37 0.29 0.24 0.19 0.16

ssssDebt to EBITDA (times) 0.75 0.20 0.75 1.70 2.61 2.14 1.28 0.92 0.71 0.56

Liquidity Metrics Current ratio (times) 1.19 1.52 1.79 1.12 1.13 1.12 1.20 1.45 2.05 2.71

Quick ratio (times) 0.50 0.66 1.15 0.49 0.41 0.54 0.51 0.61 0.91 1.31

Efficiency Metrics

Days Receivables (days) 22.15 21.95 35.38 31.92 19.41 19.76 19.76 19.76 19.76 19.76

Days Inventories (days) 126.73 136.82 119.40 112.40 122.35 128.07 128.07 128.07 128.07 128.07

Days Payables (days) 41.30 44.33 41.36 53.21 53.50 41.37 41.37 41.37 41.37 41.37

Cash Cycle (days) 107.57 114.44 113.43 91.11 88.26 106.46 106.46 106.46 106.46 106.46

Shareholders Ratio

EPS (VND) 3,928 4,775 4,074 3,015 2,726 3,355 5,085 6,212 6,916 7,622

Dividend Payout Ratio (%) 20.00% 26.08% 27.78% 28.57% 23.08% 20.48% 20.00% 20.00% 20.00% 20.00%

0

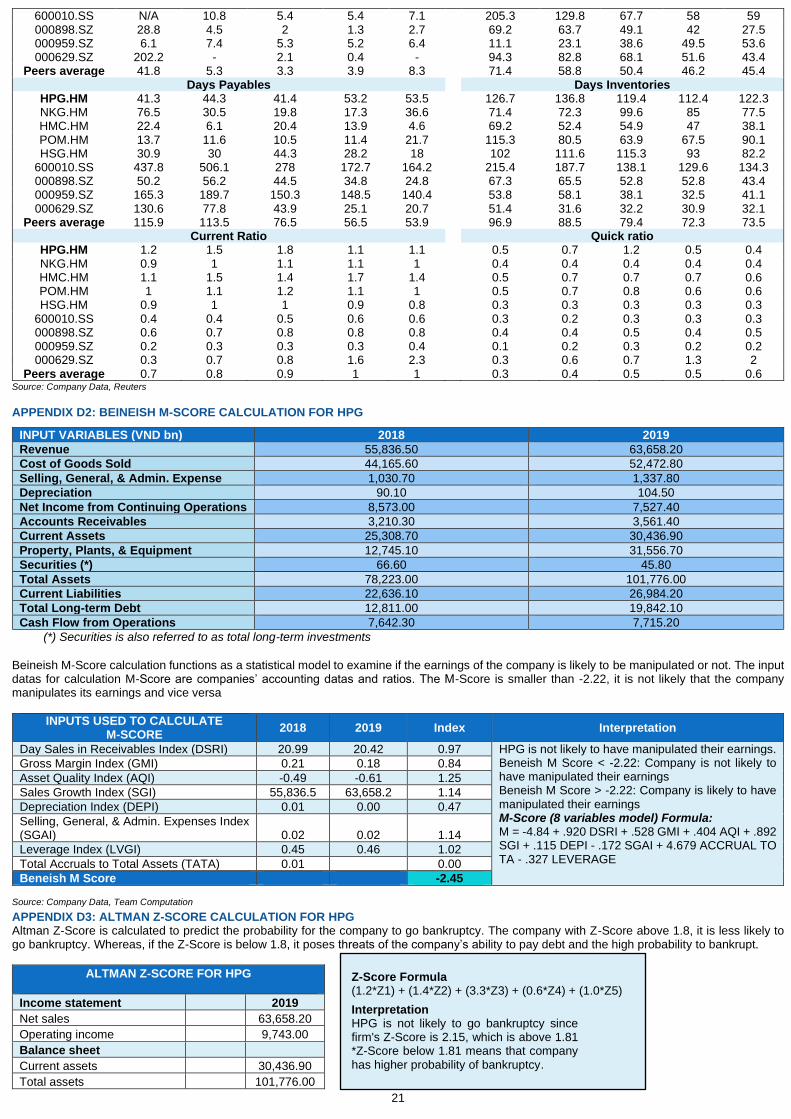

No.1 Steel Producer In Vietnam To Maintain Superior ROE With unique competitive advantages, HPG has been able to secure a consistently higher ROE than its peers (~ 1.5 to 2 times – Figure 27). Although the investment in DQSC has slightly slowed down the growth rate in ROE, we believe that with the commencement of the third blast furnace and fourth BF-BOF in Q3/2020, ROE would be able to achieve an upward trend with 17.03% in 2019 to 28.00% in 2024. This impressive performance is primarily fueled by the following factors: Exponential Growth Platform And Wise Investment To Fuel Sustainable Revenue Growth Between 2015A-2019A, HPG’s revenue escalated exponentially from VND 27,000 bn to VND 63,000 bn with a CAGR of 20.05%. By 3Q2020, its revenue witnessed a 40% YoY increase amidst market downturn caused by the COVID-19. Such excellent performance is driven by the Steel sector (80%) and Agriculture sector (12%). Steel: HPG possesses enormous production capacity, reaching 4.2M tons of finished steel products in 2019A and 5.6M in 2020F, far outweighing its peers (Pomina: 1M, Nam Kim Group: 0.7M ton). The remarkable revenue growth of 39% was attributed to the completion of Phase 3 of Hai Duong Steel Integrated Complex (HDSC) on 2017. Thus, revenue from steel sector is expected to continue its impressive growth with a 2020F-2024F CAGR of 16.77% on the back of: (1) Continuous capacity addition (total capacity: 8 mtpa in 2021F) with DQSC in full operation. (2) advanced technological application with sticky customer relationships. (3) rapid export market diversification to expand global footprint. Agriculture: Revenue from the agriculture sector has impressively brought about 73.74% increase in 2019A, with a 2015A-2019A CAGR of 43.07%. After 5 years since its establishment, the farsighted investment in agriculture has placed HPG at the leading position in: (1) the Australian beef import market in Vietnam with 50% market share, (2) egg in the North with 550,000 eggs/day. In 2020, the African Swine fever and COVID-19 pandemic has led to a hike in pork price, boosting the agriculture’s revenue and thereby helping to partly offset the current volatility in raw material prices. Given favorable demographic factors, this sector is forecasted to grow at a 2020F-2024F CAGR of 11.93%. Upstream Integrated Value Chain To Enhance Margins HPG’s superior revenue stream also goes with the impressive gross profit growth at 2015A-2019A CAGR of 17.75%. The Group’s gross margin consistently far outperform its peers (21.44% vs 9.2% in 2019A) (Figure 28), which is supported by the lowest steel production cost enabled by efficient utilization of BF-BOF and self-supplied electricity to save 10-15% production cost (vs EAF), and 20% self-produced iron ore in HDSC thanks to An Thong mine. During 2020F-2024F, HPG’s gross profit and net profit are forecasted to further enhance, registering CAGR of 26.12% and 27.39% respectively, mainly driven by: (1) Upstream integrated value chain zwith in-house HRC production. (2) lower logistic cost to Southern market thanks to DQSC’s deep-water seaport. (3) market power to raise selling prices, securing margins despite the expected increase in raw material prices. Healthy Leverage And Strong Cash Flow Generation To Finance Capacity Expansion Although HPG’s D/E ratio increased from 0.31 (2015A) to 0.67 (2019A), the ratio has consistently been under 1 and is lower than its peers’ average (1.37), indicating the strategic use of underleveraged capital structure that can readily support its continuous capacity expansion (Figure 29). In addition, the HPG’s impressive cashflow generation ability (ave. 2017A-2024F CFO/EBITDA of 0.58) makes it well-equipped to pursue future growth ventures with minimal risks of capital raising. With the commencement of DQSC, we believe that the total CFO should maintain its strong momentum, growing at 2020F-2024F CAGR of 26.63% given the positive outlook in revenue and gross profit margin (Figure 30). In line with forecast, HPG should maintain a safe net D/E ratio of 0.4. Enhanced Utilization Rate Thanks To DQSC’s Full Operation To Propel High Asset Turnover

Figure 27. HPG’s ROE and Peers Average

(2017A – 2024F)

Source: Company data, Team estimate, Reuters

30.65%

23.48%

17.03%

21.22%

27.74%29.42% 27.94% 28.00%

22.60%

10.70%

3.20%

2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

HPG Peers average

Source: Team estimate, Reuters

27.17%

21.44%

32.86%

17.36%

11.90%

16.86%

11.80%

5.65%5.40%

0.85%

2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

Gross margin Net margin

Gross margin (Peers average) Net margin (Peers average)

Figure 28. HPG’s Profitability and

Peers’ Average

Source: Team estimate, Reuters

Figure 30. HPG’s Operating Cash flow

6.06 7.64 7.72 11.5316.37 20.16 22.65 25.11

0.52

0.600.63

0.55 0.550.58 0.60 0.62

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.00

5.00

10.00

15.00

20.00

25.00

30.00

2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

CFO (trillion VND) CFO/EBITDA

Source: Team estimate

Figure 29. HPG’s Leverage Ratio

0.3

0.50.7 0.7

0.50.3

0.20.1

1.6 1.61.4

2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

Debt to Equity Peers average

7

The long-term assets in-progress have increased exponentially from VND 4,342 bn to VND 37,435 bn between 2015 and 2019. The ongoing construction of DQSC during this period has hindered HPG from fully utilizing these assets to generate revenue, leading to a decreasing asset turnover rate from 1.15 (2015A) to 0.71 (2019A), lower than its rivals (Appendix D1). However, the historical data during HDSC’s Phase 1 & 2 prove that once fully operate, utilization rate can reach up to 120%. Therefore, we confidently propose that HPG’s Return on Asset (ROA) would increase from 8.36% (2019A) to 17.72% (2024F) with the full operation of all four blast furnaces in DQSC. Profitable Investment Pool Reflected Through Brightening Shareholders’ Return EPS has shown a gradual downward trend after DQSC’s kick-start due to the increasing share issuance followed the increasing number of subsidiaries. Therefore, the roadmap to increase its share capital by VND 10,000 –15,000 bn (from 2017 onwards) and issuance of additional shares would not pose a dilution threat. Furthermore, from 6/2020 to 8/2020, HPG has distributed dividends through 20% bonus share and 5% in cash. The company has issued 552 mn shares to pay dividend and been back to the traditional dividend payment by cash since 2017(Figure 31). Such dividend payment signals HPG’s confidence in its future cashflow generation after the completion of DQSC.

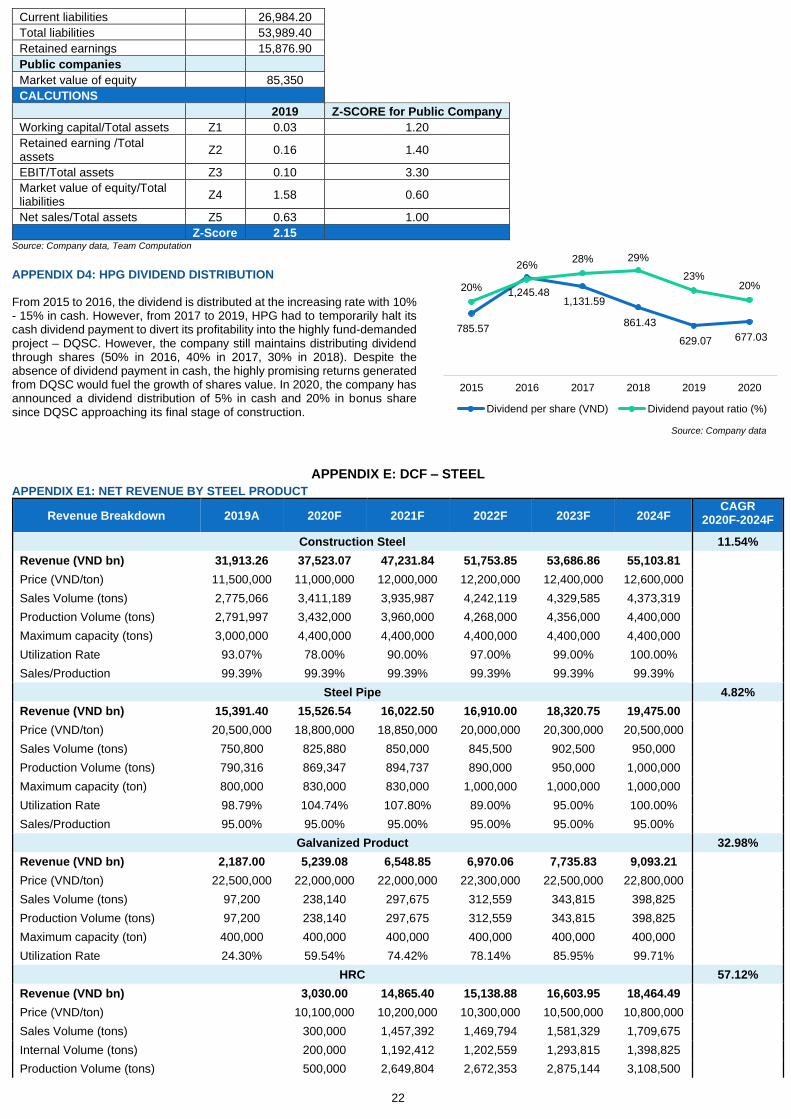

VALUATION

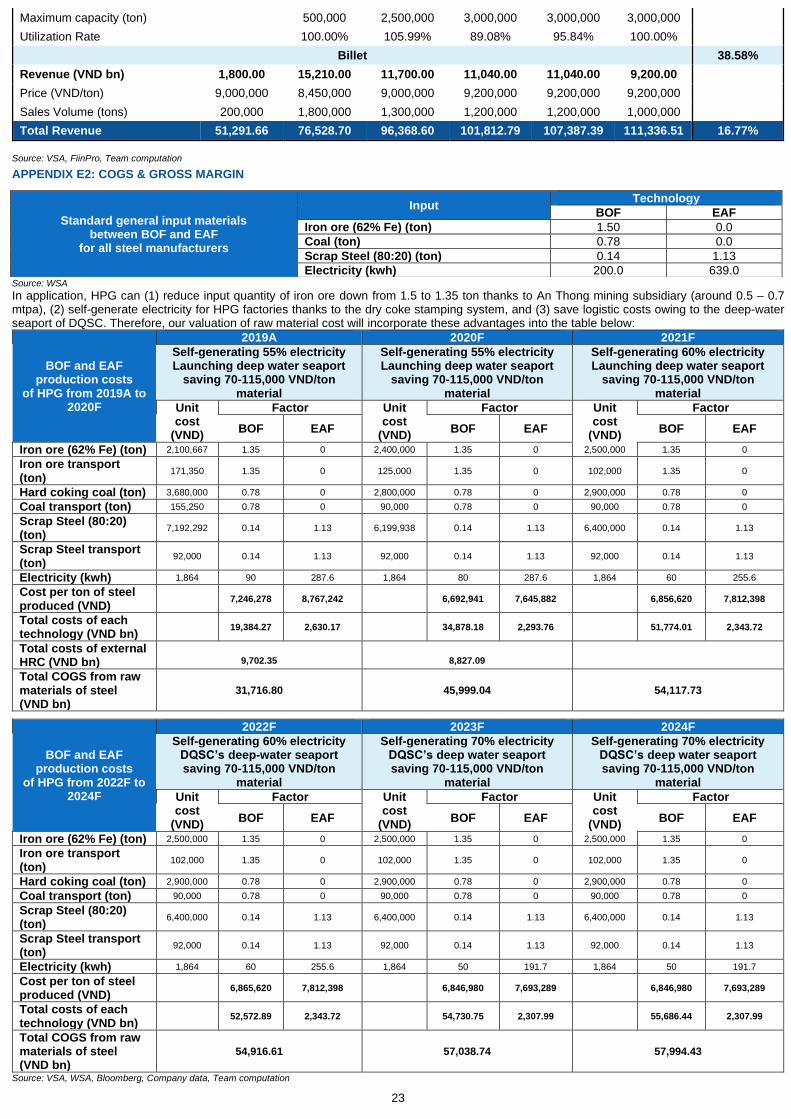

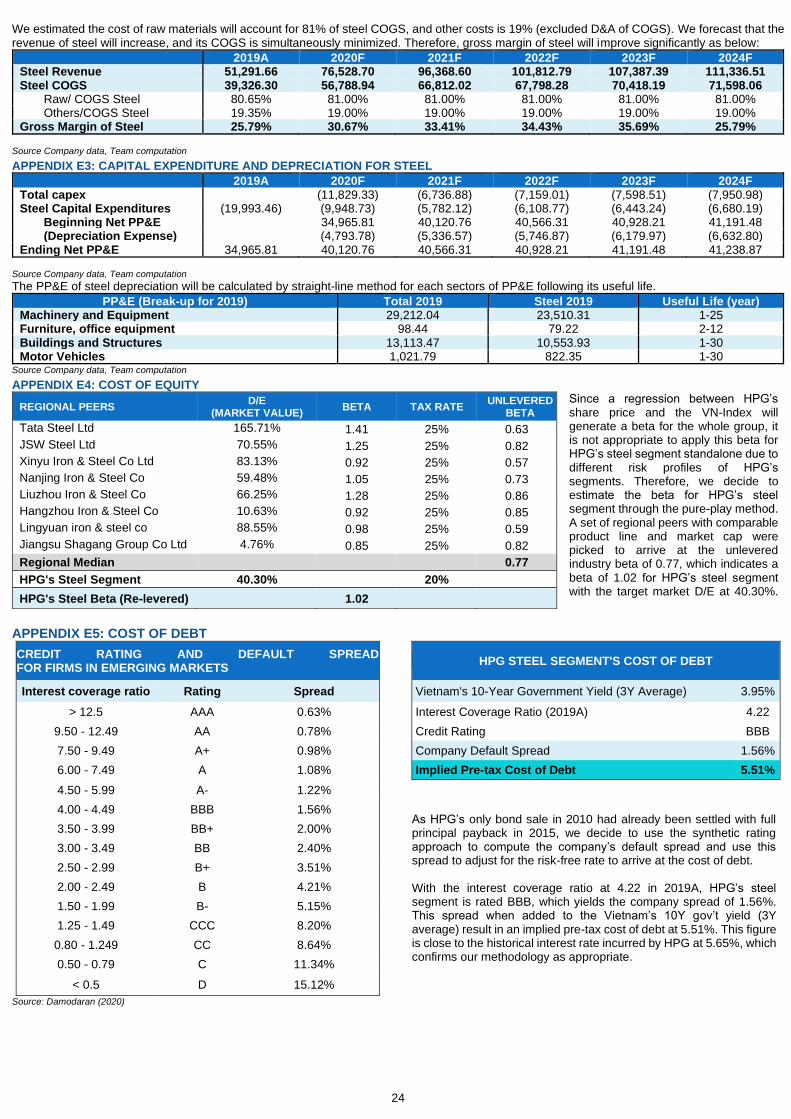

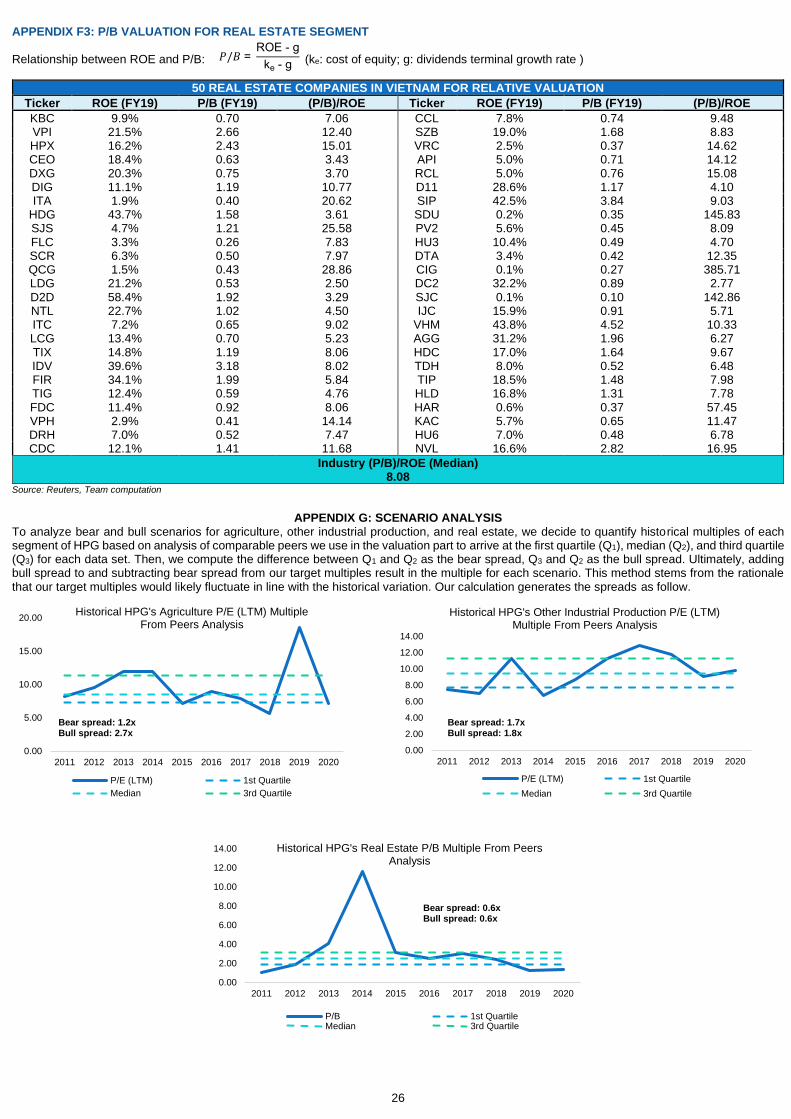

Our methodology stems from the rationale that since each segment carries different risk profile and growth drivers, valuing HPG as a whole will lead to a skewed result. Specifically, we value the Steel segment by the Discounted Cash Flow (DCF) model, the Agriculture and Other industrial production segments by the relative P/E (LTM) multiple, and the Real estate segment by the P/B (FY19) multiple. Ultimately, we arrive at the 12-month target price of 40,610 VND per share, presenting 25.92% upside from its closing price of VND 32,250 on 15th November 2020. 1. DCF Steel We apply the Discounted Free Cash Flow to Firm (FCFF) method to value the Steel sector. This method estimates the equity value of steel from the steel enterprise value and the net debt of steel. Particularly, the DCF analysis concentrates on the steel-related operation such as key drivers of revenue and gross margin (Appendix E). In the 2020’s Annual general shareholder meeting, the Board of HPG has disclosed the information about DQSC phase 3, and most shareholders have accepted to increase the investment capital of DQSC (adding VND 60,000 bn of PP&E). However, we stand conservative regarding this expansion phase of DQSC owing to the pending approval from the government. Therefore, our valuation does not incorporate this project in the forecasted timeline. a. Revenue Projection To forecast steel revenue, we focus on all five steel product lines and their historical performance. The projected revenue breakdown (2019A – 2024F) is indicated in Figure 34. Construction steel: Accumulated 8M2020, sales volume has reached 2.1mn tons (20.3% YoY), especially 101.7% YoY sales growth from the South and 87.5% from export (Figure 35). Therefore, we believe that DQSC’s large capacity and high utilization rate will continue to drive construction steel revenue at 2020F- 2024F CAGR of 11.54% given the historical 99% consumption rate (Figure 36). Steel pipe: The segment revenue was continuously recorded at 2% growth YoY in sales, nearly 500,000 tons steel pipe within 8M2020. We expect HPG to extend designed capacity of steel pipe from 0.8 mn tons (2019A) to 1.0 mn tons (2022F) due to an internal supplying of HRC (Figure 37). Thus, the revenue of steel pipe is forecasted to slightly increase at 2020F-2024F CAGR of 4.82%. HRC: The production of HRC has been commercially launched since Q3/2020, in which HPG can self-supply 40% to manufacture steel pipe and galvanized products. Another 60% of HRC will be sold to the under-supplied market which means more rooms for HPG to increase the capacity to 3mn tons. Therefore, we predict revenue of HRC to grow at 2020F- 2024F CAGR of 57.12%. Galvanized product: Since 2018, HPG has extended its product line for galvanized sheet to pre-painted hot dipped galvanized sheet coil products, fueling the revenue growth by 5 times YoY in 2019 for this specific product. Moreover, HPG has also recorded the impressive 150% YoY growth of the total sales of galvanized product in 9M/2020. Thanks to the production of in-house HRC as inputs, HPG can set a competitive price to gain more market share of galvanized products. Thus, the revenue of galvanized product is expected to grow at 2020F - 2024F CAGR of 32.98%. Billet: With the large production capacity from DQSC, 1.25 mn tons of billet has been sold in 9M2020 to domestic and export markets, so we expect sales volume to reach 1.8mn tons by the end of 2020F. However, the production of billet is forecasted to decrease significantly from 2021F–2024F because HPG will prioritize to produce other value-added steel products. Therefore, we forecast revenue of billets to reach VND 15,210 bn in 2020, but it then decreases to VND 8,900 bn in 2024. Despite the impact of the COVID-19, steel revenue of HPG in 9M/2020 robustly grew 27.50% YoY. Therefore, we strongly believe that steel sector can be continuously considered as the main driver of HPG steel revenue in the next 5 years with 2020F – 2024F CAGR 16.77 %. b. Gross Margin Improvement Gross profit margin of steel is forecasted to improve significantly based on the following factors: (1) Significant lower cost structure of BF-BOF technology than EAF technology (Figure 38, 39 & 40). (2) The operation of DQSC creates the upstream integrated value chain which cuts imported HRC costs for HPG since Q3/2020. Furthermore, the deep-water seaport which can reduce logistic cost is also reflected detailly to the valuation in Appendix E2. (3) After having acquired superior market share in Vietnam, HPG has started to increase the selling price of construction steel from November 2020. Thereby, we forecast HPG to gradually bring the average price of its products back to the historical level by 2024F with such strong market power. (4) From 2021F to 2024F, HPG will prioritize the production of high value-added products to earn higher profits. That said, we expect HPG to minimize 5% average cost per one ton of steel (excluded D&A expense of COGS) in the next 5 years (Figure 41) and the gross profit margin of steel is poised to increase from 23.33% (2019A) to 35.69% (2024F) (Figure 42).

Figure 32. Sum-of-the-Parts Valuation Results (Attributable Equity Value in VND bn)

Source: Team estimate

120,476.62

134,552.498,597.44 3,045.30 2,433.13

3.00

20,003.00

40,003.00

60,003.00

80,003.00

100,003.00

120,003.00

140,003.00

Steel Agriculture Other Industrial Product

Real Estate Total

Figure 34. Steel Revenue Breakdown (VND trn)

Source: Team estimate

2019A 2020F 2021F 2022F 2023F 2024F

Construction steel Steel pipe Galvanized products HRC Billet

51.29 76.53

96.37 101.81 107.39 111.34

62%

30% 4%

4%

49%

20% 4%

20% 7%

49%

17%

15% 12%

7%

51%

17%

11% 15% 7%

50%

17%

10% 15% 7%

49%

17%

9% 17% 8%

Figure 37. Utilization Rate of HPG’s Steel Pipe (2016A-2024F)

Source: Company data, Team estimate

0.6 0.6

0.8 0.8 0.8 0.8 1.0 1.0 1.0

91%

109%

89%

99%105%

108%

90%95%

100%

0%

20%

40%

60%

80%

100%

120%

(0.3)

0.2

0.7

1.2

1.7

2.2

2016A 2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

Designed Capacity (mn tons) Utilization rate

Figure 36. Utilization Rate of Construction Steel

Source: Company data, Team estimate

1.3 1.3 2.0

2.0 2.4 3.0

4.4

4.4 4.4 4.4 4.4

78%

107%

91%

110%

100%93%

78%

90%97%

99%100%

0%

20%

40%

60%

80%

100%

120%

(0.6)

0.4

1.4

2.4

3.4

4.4

5.4

6.4

7.4

2014A 2015A 2016A 2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

Designed Capacity (mn tons) Utilization rate

Source: Team estimate, Reuters

785.57

1,245.48

1,131.59

861.43

629.07 699.97

946.74 1,057.41

1,146.94 1,230.85

20.00

26.08 27.7828.57

23.0820.48

20.00

20.00

2015A 2016A 2017A 2018A 2019A 2020F 2021F 2022F 2023F 2024F

Dividend per share (VND) Dividend payout ratio (%)

Figure 31. HPG Dividend Payment

Figure 33. Valuation Summary

Source: Team estimate

HPG'S VALUATION SUMMARY (VND BN)

Total Attributable Equity Value 134,552.49

Number of outstanding shares (VND mn)

3,313

Target Price (VND) 40,610

Current Price (VND) 32,250

Upside 25.92%

Figure 35. Steel Consumption in 8M2020

HPG Industry

Construction

steel

YoY YoY

20.3% -4.3%

The North -6.4% -4.5%

The South 101.7% -6.2%

Central 10.2% -7.8%

Export 87.5% -5.4%

Source: Fiinpro, VSA

8

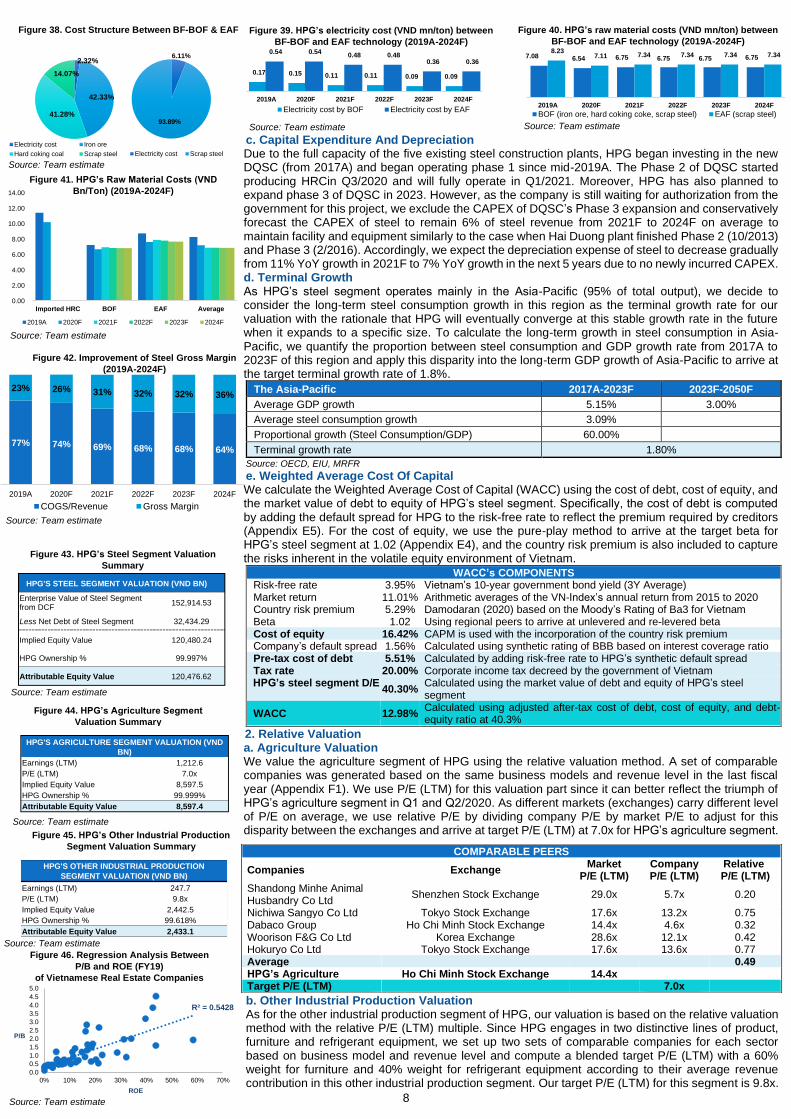

c. Capital Expenditure And Depreciation Due to the full capacity of the five existing steel construction plants, HPG began investing in the new DQSC (from 2017A) and began operating phase 1 since mid-2019A. The Phase 2 of DQSC started producing HRCin Q3/2020 and will fully operate in Q1/2021. Moreover, HPG has also planned to expand phase 3 of DQSC in 2023. However, as the company is still waiting for authorization from the government for this project, we exclude the CAPEX of DQSC’s Phase 3 expansion and conservatively forecast the CAPEX of steel to remain 6% of steel revenue from 2021F to 2024F on average to maintain facility and equipment similarly to the case when Hai Duong plant finished Phase 2 (10/2013) and Phase 3 (2/2016). Accordingly, we expect the depreciation expense of steel to decrease gradually from 11% YoY growth in 2021F to 7% YoY growth in the next 5 years due to no newly incurred CAPEX. d. Terminal Growth As HPG’s steel segment operates mainly in the Asia-Pacific (95% of total output), we decide to consider the long-term steel consumption growth in this region as the terminal growth rate for our valuation with the rationale that HPG will eventually converge at this stable growth rate in the future when it expands to a specific size. To calculate the long-term growth in steel consumption in Asia-Pacific, we quantify the proportion between steel consumption and GDP growth rate from 2017A to 2023F of this region and apply this disparity into the long-term GDP growth of Asia-Pacific to arrive at the target terminal growth rate of 1.8%.

The Asia-Pacific 2017A-2023F 2023F-2050F

Average GDP growth 5.15% 3.00%

Average steel consumption growth 3.09%

Proportional growth (Steel Consumption/GDP) 60.00%

Terminal growth rate 1.80%

Source: OECD, EIU, MRFR

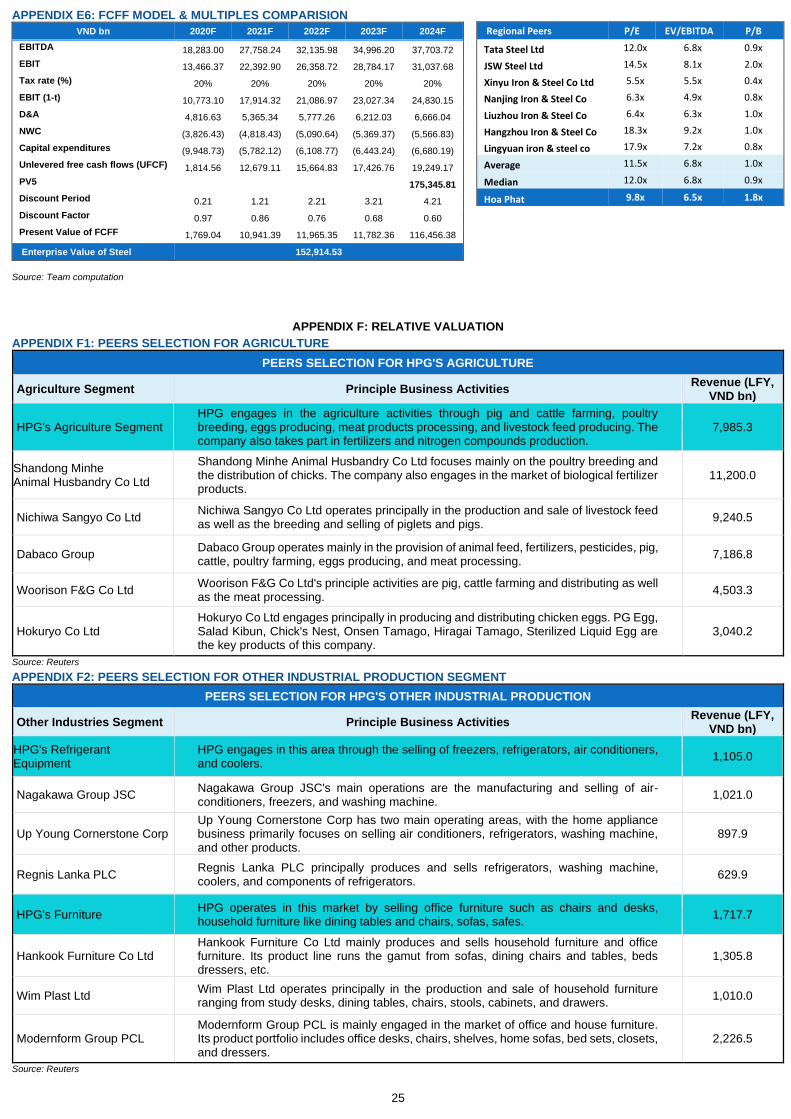

e. Weighted Average Cost Of Capital We calculate the Weighted Average Cost of Capital (WACC) using the cost of debt, cost of equity, and the market value of debt to equity of HPG’s steel segment. Specifically, the cost of debt is computed by adding the default spread for HPG to the risk-free rate to reflect the premium required by creditors (Appendix E5). For the cost of equity, we use the pure-play method to arrive at the target beta for HPG’s steel segment at 1.02 (Appendix E4), and the country risk premium is also included to capture the risks inherent in the volatile equity environment of Vietnam.

WACC’s COMPONENTS Risk-free rate 3.95% Vietnam’s 10-year government bond yield (3Y Average) Market return 11.01% Arithmetic averages of the VN-Index’s annual return from 2015 to 2020 Country risk premium 5.29% Damodaran (2020) based on the Moody’s Rating of Ba3 for Vietnam Beta 1.02 Using regional peers to arrive at unlevered and re-levered beta Cost of equity 16.42% CAPM is used with the incorporation of the country risk premium Company’s default spread 1.56% Calculated using synthetic rating of BBB based on interest coverage ratio Pre-tax cost of debt 5.51% Calculated by adding risk-free rate to HPG’s synthetic default spread Tax rate 20.00% Corporate income tax decreed by the government of Vietnam

HPG’s steel segment D/E 40.30%

Calculated using the market value of debt and equity of HPG’s steel segment

WACC 12.98% Calculated using adjusted after-tax cost of debt, cost of equity, and debt-equity ratio at 40.3%

2. Relative Valuation a. Agriculture Valuation We value the agriculture segment of HPG using the relative valuation method. A set of comparable companies was generated based on the same business models and revenue level in the last fiscal year (Appendix F1). We use P/E (LTM) for this valuation part since it can better reflect the triumph of HPG’s agriculture segment in Q1 and Q2/2020. As different markets (exchanges) carry different level of P/E on average, we use relative P/E by dividing company P/E by market P/E to adjust for this disparity between the exchanges and arrive at target P/E (LTM) at 7.0x for HPG’s agriculture segment.

b. Other Industrial Production Valuation As for the other industrial production segment of HPG, our valuation is based on the relative valuation method with the relative P/E (LTM) multiple. Since HPG engages in two distinctive lines of product, furniture and refrigerant equipment, we set up two sets of comparable companies for each sector based on business model and revenue level and compute a blended target P/E (LTM) with a 60% weight for furniture and 40% weight for refrigerant equipment according to their average revenue contribution in this other industrial production segment. Our target P/E (LTM) for this segment is 9.8x.

COMPARABLE PEERS

Companies Exchange Market

P/E (LTM) Company P/E (LTM)

Relative P/E (LTM)

Shandong Minhe Animal Husbandry Co Ltd

Shenzhen Stock Exchange 29.0x 5.7x 0.20

Nichiwa Sangyo Co Ltd Tokyo Stock Exchange 17.6x 13.2x 0.75 Dabaco Group Ho Chi Minh Stock Exchange 14.4x 4.6x 0.32 Woorison F&G Co Ltd Korea Exchange 28.6x 12.1x 0.42 Hokuryo Co Ltd Tokyo Stock Exchange 17.6x 13.6x 0.77 Average 0.49 HPG’s Agriculture Ho Chi Minh Stock Exchange 14.4x

Target P/E (LTM) 7.0x

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Imported HRC BOF EAF Average

2019A 2020F 2021F 2022F 2023F 2024F

Source: Team estimate

Figure 41. HPG’s Raw Material Costs (VND

Bn/Ton) (2019A-2024F)

Figure 42. Improvement of Steel Gross Margin

(2019A-2024F)

Source: Team estimate

77% 74% 69% 68% 68% 64%

23% 26% 31% 32% 32% 36%

0%

20%

40%

60%

80%

2019A 2020F 2021F 2022F 2023F 2024F

COGS/Revenue Gross Margin

R² = 0.5428

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0% 10% 20% 30% 40% 50% 60% 70%

P/B

ROE

Figure 46. Regression Analysis Between

P/B and ROE (FY19) of Vietnamese Real Estate Companies

Source: Team estimate

Source: Team estimate

6.11%

93.89%

Electricity cost Scrap steel

2.32%

42.33%

41.28%

14.07%

Electricity cost Iron ore

Hard coking coal Scrap steel

Figure 38. Cost Structure Between BF-BOF & EAF

7.08 6.54 6.75 6.75 6.75 6.75 8.23

7.11 7.34 7.34 7.34 7.34

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

2019A 2020F 2021F 2022F 2023F 2024F

BOF (iron ore, hard coking coke, scrap steel) EAF (scrap steel)

Figure 40. HPG’s raw material costs (VND mn/ton) between

BF-BOF and EAF technology (2019A-2024F)

Source: Team estimate

0.17 0.15 0.11 0.11 0.09 0.09

0.54 0.54 0.48 0.48

0.36 0.36

2019A 2020F 2021F 2022F 2023F 2024F

Electricity cost by BOF Electricity cost by EAF

Figure 39. HPG’s electricity cost (VND mn/ton) between

BF-BOF and EAF technology (2019A-2024F)

Source: Team estimate

HPG'S STEEL SEGMENT VALUATION (VND BN) Enterprise Value of Steel Segment from DCF 152,914.53 Less Net Debt of Steel Segment 32,434.29 Implied Equity Value 120,480.24 HPG Ownership % 99.997% Attributable Equity Value 120,476.62

Figure 43. HPG’s Steel Segment Valuation

Summary

Source: Team estimate Figure 44. HPG’s Agriculture Segment

Valuation Summary

HPG'S AGRICULTURE SEGMENT VALUATION (VND

BN)

Earnings (LTM) 1,212.6

P/E (LTM) 7.0x

Implied Equity Value 8,597.5

HPG Ownership % 99.999%

Attributable Equity Value 8,597.4

Source: Team estimate

HPG'S OTHER INDUSTRIAL PRODUCTION

SEGMENT VALUATION (VND BN) Earnings (LTM) 247.7 P/E (LTM) 9.8x Implied Equity Value 2,442.5 HPG Ownership % 99.618% Attributable Equity Value 2,433.1 Source: Team estimate

Figure 45. HPG’s Other Industrial Production

Segment Valuation Summary

9

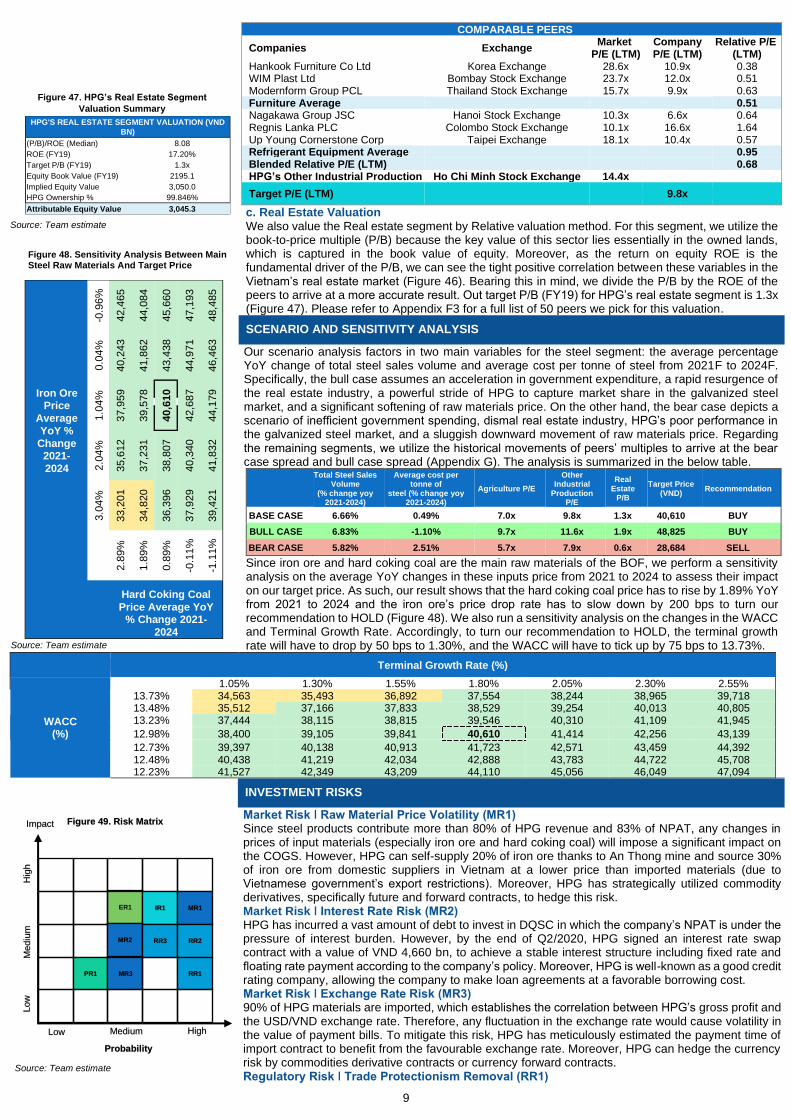

COMPARABLE PEERS

Companies Exchange Market

P/E (LTM) Company P/E (LTM)

Relative P/E (LTM)

Hankook Furniture Co Ltd Korea Exchange 28.6x 10.9x 0.38 WIM Plast Ltd Bombay Stock Exchange 23.7x 12.0x 0.51 Modernform Group PCL Thailand Stock Exchange 15.7x 9.9x 0.63 Furniture Average 0.51 Nagakawa Group JSC Hanoi Stock Exchange 10.3x 6.6x 0.64 Regnis Lanka PLC Colombo Stock Exchange 10.1x 16.6x 1.64 Up Young Cornerstone Corp Taipei Exchange 18.1x 10.4x 0.57 Refrigerant Equipment Average 0.95 Blended Relative P/E (LTM) 0.68 HPG’s Other Industrial Production Ho Chi Minh Stock Exchange 14.4x

Target P/E (LTM) 9.8x

c. Real Estate Valuation We also value the Real estate segment by Relative valuation method. For this segment, we utilize the book-to-price multiple (P/B) because the key value of this sector lies essentially in the owned lands, which is captured in the book value of equity. Moreover, as the return on equity ROE is the fundamental driver of the P/B, we can see the tight positive correlation between these variables in the Vietnam’s real estate market (Figure 46). Bearing this in mind, we divide the P/B by the ROE of the peers to arrive at a more accurate result. Out target P/B (FY19) for HPG’s real estate segment is 1.3x (Figure 47). Please refer to Appendix F3 for a full list of 50 peers we pick for this valuation.

SCENARIO AND SENSITIVITY ANALYSIS

Our scenario analysis factors in two main variables for the steel segment: the average percentage YoY change of total steel sales volume and average cost per tonne of steel from 2021F to 2024F. Specifically, the bull case assumes an acceleration in government expenditure, a rapid resurgence of the real estate industry, a powerful stride of HPG to capture market share in the galvanized steel market, and a significant softening of raw materials price. On the other hand, the bear case depicts a scenario of inefficient government spending, dismal real estate industry, HPG’s poor performance in the galvanized steel market, and a sluggish downward movement of raw materials price. Regarding the remaining segments, we utilize the historical movements of peers’ multiples to arrive at the bear case spread and bull case spread (Appendix G). The analysis is summarized in the below table.

Total Steel Sales Volume

(% change yoy 2021-2024)

Average cost per tonne of

steel (% change yoy 2021-2024)

Agriculture P/E

Other Industrial

Production P/E

Real Estate

P/B

Target Price (VND)

Recommendation

BASE CASE 6.66% 0.49% 7.0x 9.8x 1.3x 40,610 BUY

BULL CASE 6.83% -1.10% 9.7x 11.6x 1.9x 48,825 BUY

BEAR CASE 5.82% 2.51% 5.7x 7.9x 0.6x 28,684 SELL

Since iron ore and hard coking coal are the main raw materials of the BOF, we perform a sensitivity analysis on the average YoY changes in these inputs price from 2021 to 2024 to assess their impact on our target price. As such, our result shows that the hard coking coal price has to rise by 1.89% YoY from 2021 to 2024 and the iron ore’s price drop rate has to slow down by 200 bps to turn our recommendation to HOLD (Figure 48). We also run a sensitivity analysis on the changes in the WACC and Terminal Growth Rate. Accordingly, to turn our recommendation to HOLD, the terminal growth rate will have to drop by 50 bps to 1.30%, and the WACC will have to tick up by 75 bps to 13.73%.

Terminal Growth Rate (%)

WACC (%)

1.05% 1.30% 1.55% 1.80% 2.05% 2.30% 2.55% 13.73% 34,563 35,493 36,892 37,554 38,244 38,965 39,718 13.48% 35,512 37,166 37,833 38,529 39,254 40,013 40,805 13.23% 37,444 38,115 38,815 39,546 40,310 41,109 41,945

12.98% 38,400 39,105 39,841 40,610 41,414 42,256 43,139

12.73% 39,397 40,138 40,913 41,723 42,571 43,459 44,392 12.48% 40,438 41,219 42,034 42,888 43,783 44,722 45,708 12.23% 41,527 42,349 43,209 44,110 45,056 46,049 47,094

INVESTMENT RISKS

Market Risk ǀ Raw Material Price Volatility (MR1) Since steel products contribute more than 80% of HPG revenue and 83% of NPAT, any changes in prices of input materials (especially iron ore and hard coking coal) will impose a significant impact on the COGS. However, HPG can self-supply 20% of iron ore thanks to An Thong mine and source 30% of iron ore from domestic suppliers in Vietnam at a lower price than imported materials (due to Vietnamese government’s export restrictions). Moreover, HPG has strategically utilized commodity derivatives, specifically future and forward contracts, to hedge this risk. Market Risk ǀ Interest Rate Risk (MR2) HPG has incurred a vast amount of debt to invest in DQSC in which the company’s NPAT is under the pressure of interest burden. However, by the end of Q2/2020, HPG signed an interest rate swap contract with a value of VND 4,660 bn, to achieve a stable interest structure including fixed rate and floating rate payment according to the company’s policy. Moreover, HPG is well-known as a good credit rating company, allowing the company to make loan agreements at a favorable borrowing cost. Market Risk ǀ Exchange Rate Risk (MR3) 90% of HPG materials are imported, which establishes the correlation between HPG’s gross profit and the USD/VND exchange rate. Therefore, any fluctuation in the exchange rate would cause volatility in the value of payment bills. To mitigate this risk, HPG has meticulously estimated the payment time of import contract to benefit from the favourable exchange rate. Moreover, HPG can hedge the currency risk by commodities derivative contracts or currency forward contracts. Regulatory Risk ǀ Trade Protectionism Removal (RR1)

ER1

High Medium

Mediu

m

Hig

h

Low

HPG'S REAL ESTATE SEGMENT VALUATION (VND

BN) (P/B)/ROE (Median) 8.08 ROE (FY19) 17.20% Target P/B (FY19) 1.3x Equity Book Value (FY19) 2195.1 Implied Equity Value 3,050.0 HPG Ownership % 99.846% Attributable Equity Value 3,045.3

Figure 47. HPG’s Real Estate Segment

Valuation Summary

Source: Team estimate

Iron Ore Price

Average

YoY %

Change 2021-

2024

3.0

4%

2.0

4%

1.0

4%

0.0

4%

-0

.96%

Hard Coking Coal

Price Average YoY % Change 2021-

2024

2.8

9%

33,2

01

35,6

12

37,9

59

40,2

43

42,4

65

1.8

9%

34,8

20

37,2

31

39,5

78

41,8

62

44,0

84

0.8

9%

36,3

96

38,8

07

40,6

10

43,4

38

45,6

60

-0.1

1%

37,9

29

40,3

40

42,6

87

44,9

71

47,1

93

-1.1

1%

39,4

21

41,8

32

44,1

79

46,4

63

48,4

85

Figure 48. Sensitivity Analysis Between Main Steel Raw Materials And Target Price

Source: Team estimate

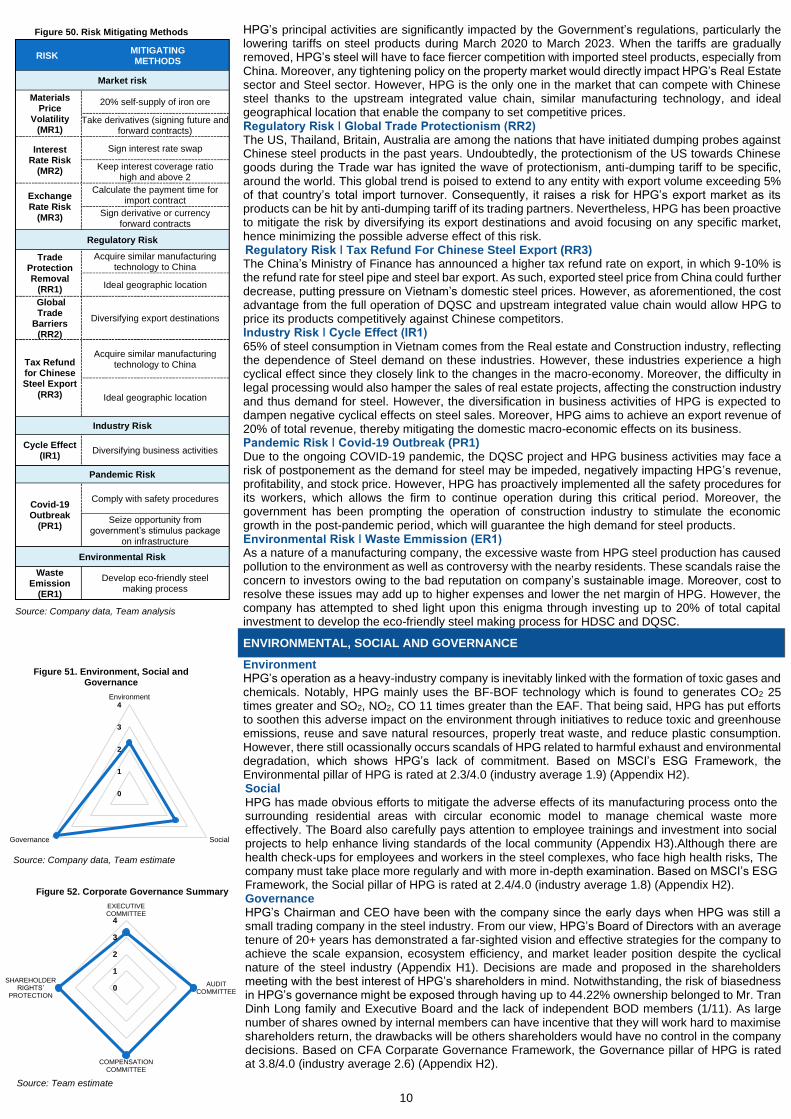

Probability

Impact

Low

IR1 MR1

MR2 RR3 RR2

PR1 MR3 RR1

Figure 49. Risk Matrix

Source: Team estimate

10