CENTRAL BANK AND REAL ESTATE / HOUSING MARKET IN TANZANIA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CENTRAL BANK AND REAL ESTATE / HOUSING MARKET IN

TANZANIA

CENTRAL BANK AND REAL ESTATE / HOUSING MARKET IN

TANZANIA

CASE AT BANK OF TANZANIA [BoT] – HEAD OFFICE, DAR-ES-SALAAM

By

Herbert Maximillian Lyimo

Dissertation Submitted in Partial/Fulfillment of the Requirements for Award of the

Degree of Master of Business Administration in Corporate Management (MBA

CM) of Mzumbe University

2014

i

CERTIFICATION

We, the undersigned, certify that we have read and hereby recommend for acceptance by

the Mzumbe University, the research report titled “Central Bank and Real Estate

Market in Tanzania” in partial/fulfillment of the requirements for award of the degree

of Masters of Business Administration of Mzumbe University.

_______________

Major Supervisor

______________

Internal Examiner

Accepted for the Board of………………….…

____________________________________________________________

DEAN/DIRECTOR, FACULTY/DIRECTORATE/SCHOOL/BOARD

ii

DECLARATION

AND

COPYRIGHT

I, Herbert Maximillian Lyimo, declare that this proposal is my own original work and

that it has not been presented and will not be presented to any other university for a

similar or any other degree award.

Signature ____________________

Date ______________________

© 2014

This dissertation is a copyright material protected under the Berne Convention, the

Copyright Act 1999 and other international and national enactments, in that behalf, on

intellectual property. It may not be reproduced by any means in full or in parts, except

for short extracts in fair dealings, for research or private study, critical scholarly review

or discourse with an acknowledgement, without the written permission of Mzumbe

University, on behalf of the author.

iii

ACKNOWLEDGEMENT

I am grateful to my Lord and Saviour Jesus Christ for the honour of accomplishment of

this study marking the second degree of Business Administration in Corporate

Management, after the first degree of Business Administration which I earned in 2010.

God had much to do in accomplishment of my education than all my strengths put

together. I thank my mother for her support in my study and education; both morally and

financially. I acknowledge the support of friends specifically, Zola H. Komba and

Godfrey Malauri in walking me throughout my study and encouraging me.

I would love to acknowledge the contribution of my supervisor Godbertha Kinyondo

(PhD) for her guidance throughout this work; she is the best I‘ve ever known, so thank

you ‗madam‘. She is an inspiration to me in the economic field and I promised her to

keep up the spirit in my advanced future studies.

My research would not have been accomplished without key figures personnel in Bank

of Tanzania; Mr. Makene, Ms. Prisca, Mr. Milulu, Mr. Misangu and John Mello to

mention the few. It was not easy to penetrate my way into a highly structured and

sensitive organization like Bank of Tanzania, but these few individuals blessed my way

wherever I needed support and guidance.

I would love to appreciate the prayers and spiritual support from my church, Upper

Room Ministry (URM) Tanzania, in nurturing my soul to withheld turbulence in this

study. Specifically I extend my gratitude to Pastor Freddy Okolle and Pastor Casmir

Mabina for their endless encouragement.

It is also kind to appreciate the contribution my office played whenever I needed time-

off to accomplish this study. I appreciate the management of National Health Insurance

Fund (NHIF) in playing a role of making my dream come true.

iv

DEDICATION

I dedicate this work to my loving father, who is now resting in peace, Herbert

Maximillian (Sr) Lyimo. He was and will always be my inspiration to my work and

education. He would be happy to know how far I have reached in contributing this study

to my government.

v

ABBREVIATIONS AND ACRONYMS

BOT - Bank of Tanzania

BRICS - Brazil Russia India China South-Africa

CBD - Central Business District

CRB - Contractors Registration Board

CRDB Bank - Cooperative Rural Development Bank

DSE - Dar-es-salaam Stock Exchange

EU - European Union

EWURA - Energy and Water Utilities Regulatory Authority

GDP - Gross Domestic Product

HPI - House Price Indices

IIF - Institute of International Finance

IPD - Investment Property Databank

KDA - Kigamboni Development Agency

KIA - Kilimanjaro International Airport

NBC Bank - National Bank of Commerce

NHC - National Housing Corporation

NSSF - National Social Security Fund

PPF - Pension Parastatal Fund

SAPOA - South African Property Owners Association

TANESCO - Tanzania Electric Supply Company

TBA - Tanzania Building Agency

TCB - Tanzania Coffee Board

TCF - Trillion Cubic Feet

THB - Tanzania Housing Bank

TMFL - Tanzania Mortgage Finance Limited Company

TZS - Tanzania Shillings

UNESCO - United Nations Educational, Scientific and Cultural Organization

USD - United State Dollar

vi

ABSTRACT

This study evaluates how the Central Bank of Tanzania influences the real

estate/housing market through its policies. The research design employed was case

study. The source of data collection was at Bank of Tanzania (BoT) Head Office, Dar es

salaam. The study used non-probability sampling – ‗judgemental/purposive‘ sampling.

The primary data was gathered through interviews and questionnaires; whereas the

secondary data was gathered from organization brochures, website and empirical/textual

literature. The data collection started on 1st April 2014 and ended in 30

th April 2014.

Only ten (10) out of the intended fifteen (15) respondents could be reached. The data

was categorized and coded to be fed into SPSS (version 16.0) for analysis and

manipulation. The data analysis techniques included frequency analysis, factor analysis,

cross tabulation analysis, correlation analysis and cronbach‘s alpha analysis.

The researcher found that when there is low interest rate, the prices of commodities,

housing and rents also tend to rise up. It was also found that Central Bank exerts certain

penalties to institutions which don‘t adhere to regulations thereby controlling indirectly

housing costs. There is a general appreciation that Bank of Tanzania should be

controlling total volume of credit in the economy and thus principally be controlling real

estate prices and housing rents. It has been rather tricky in analysing the supervisory

discretion in targeting the activities of individual institutions since there are measures of

prudence to be considered; thereby an average consensus. However, there was a widely

accepted fact that Bank of Tanzania doesn‘t control capital flow with prudent purposes.

Thereby existences of weak supervision discretion in combination of slack prudence in

capital flow if not carefully reviewed may sets ground for bubble inflation.

Based on such findings, there is enrichment of monetary policy examination in East

Africa states that have similar economic infrastructures. The most agreed way of asset

bubble prevention is for the government to bail out the businesses; but what is more

important is for the serious and strict policies to take root in guiding businesses and

social lives of citizens.

vii

TABLE OF CONTENTS

CERTIFICATION ............................................................................................................ i

DECLARATION AND COPYRIGHT ......................................................................... ii

Acknowledgement .......................................................................................................... iii

Dedication ........................................................................................................................ iv

ABBREVIATIONS AND ACRONYMS ........................................................................ v

ABSTRACT ..................................................................................................................... vi

TABLE OF CONTENTS .............................................................................................. vii

TABLE OF LIST .......................................................................................................... xii

LIST OF FIGURES ...................................................................................................... xiv

CHAPTER ONE .............................................................................................................. 1

INSIGHT INTO TANZANIA MONETARY POLICY AND ITS LINKAGE TO

REAL ESTATE/HOUSING MARKET ......................................................................... 1 1.1 Background History of the Problem................................................................ 1 1.2 Statement of a Problem ................................................................................... 2 1.3 Objective of the Study ..................................................................................... 3 1.3.1 General Objectives .......................................................................................... 3 1.3.2 Specific Objectives .......................................................................................... 3 1.4 Research Question(s)....................................................................................... 3 1.5 Significance of the Study ................................................................................ 4 1.6 Rationale for Study.......................................................................................... 4 1.7 Scope of the Study........................................................................................... 5 1.8 Limitations of the study................................................................................... 5 1.9 Dissemination of Research Report .................................................................. 5

CHAPTER TWO ............................................................................................................. 6 LITERATURE REVIEW ................................................................................................ 6

2.1 Textual literature and Theoretical Framework ................................................ 6

2.1.1 Definition of Asset Bubble .............................................................................. 6

2.1.2 Current Economic Outlook of Tanzania ......................................................... 6

2.1.3 Inefficacy of Monetary Policies ...................................................................... 7

2.1.4 Household Debt and Monetary Policy ............................................................ 8

2.2 Empirical Literature and Conceptual Framework ......................................... 12

2.2.1 A Central Bank .............................................................................................. 16

2.2.2 Bank Regulation ............................................................................................ 18

2.2.3 Monetary Policy ............................................................................................ 19

2.2.4 Fiscal Policy .................................................................................................. 22

2.2.5 Economic Bubbles......................................................................................... 24

2.2.5.1.2 Housing debt Measures ................................................................................. 28

2.2.5.2 Indicators of bubble (evidence) in Tanzania ................................................. 32

viii

2.2.5.2.1Tanzania Inflation Rate .................................................................................. 35 2.2.5.2.2 Tanzania Shilling........................................................................................... 36

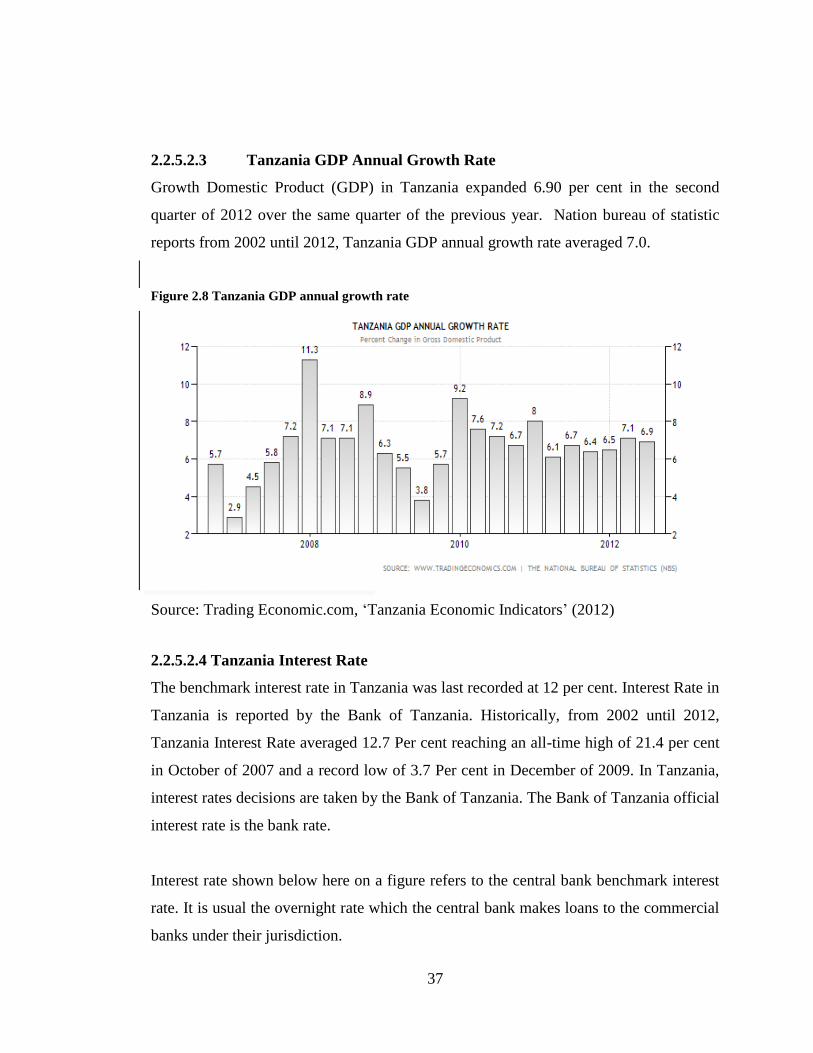

2.2.5.2.3 Tanzania GDP Annual Growth Rate ............................................................. 37

2.2.5.2.4 Tanzania Interest Rate ................................................................................... 37

2.2.5.3 Basic Coverage of a Bubble .......................................................................... 40

2.2.5.3.1 Stock Market Bubble ..................................................................................... 40

2.2.5.3.2 Real Estate Bubble ........................................................................................ 40

2.2.6 Construction Industry and Real Estate in Africa and Tanzania .................... 40

2.2.7 Relationship between monetary policy, economic bubble and real

Estate/Housing Market .................................................................................. 48

2.2.8 Monetary and Fiscal Policies of Tanzania in Assessment of Housing

Market/Real Estate ........................................................................................ 53

2.2.9 Extent of Monetary Policy in Precipitating Asset Bubble in Real

Estate/Housing Prices and what can Tanzania learn. .................................... 56

2.2.10 Economic Bubble Prevention ........................................................................ 61

2.3 Knowledge Gap ............................................................................................. 65

2.4 Conceptual Framework ................................................................................. 66

2.5 Hypotheses .................................................................................................... 67

CHAPTER THREE ....................................................................................................... 68

STATISTICS, COMPUTATION AND DESIGN OF A RESEARCH PROBLEM 69 3.1 Introduction: Research Methodology ............................................................ 69

3.2 Conceptual Definition ................................................................................... 69

3.2.1 Asset Bubble ................................................................................................. 69

3.2.2 Austrian Economic(s):................................................................................... 69

3.2.3 Bail (bail out): ............................................................................................... 69

3.2.4 Bond (Government Bond) ............................................................................. 70

3.2.5 Boom (Economic): ........................................................................................ 70

3.2.6 Borrowing...................................................................................................... 70

3.2.7 Budget ........................................................................................................... 70

3.2.8 Construction Industry .................................................................................... 70

3.2.9 Contractors .................................................................................................... 70

3.2.10 Credit Market ................................................................................................ 71

3.2.11 Crush (bubble, Economy) ............................................................................. 71

3.2.12 Currency Board ............................................................................................. 71

3.2.13 Debt ............................................................................................................... 71

3.2.14 Deregulation ................................................................................................. 71

3.2.15 Dollarization .................................................................................................. 71

3.2.16 Economic Bubble .......................................................................................... 71

3.2.17 Economic Crisis ............................................................................................ 72

3.2.18 Expenditure ................................................................................................... 72

3.2.19 Financial Crisis .............................................................................................. 72

3.2.20 Financial Institution(s) .................................................................................. 72

3.2.21 Financial Market .......................................................................................... 72

ix

3.2.22 Financial Year ............................................................................................... 72 3.2.23 Fiscal Policy .................................................................................................. 73

3.2.24 Government ................................................................................................... 73

3.2.25 Greater Fool (Theory) ................................................................................... 73

3.2.26 Heterodox Economic(s)................................................................................. 73

3.2.27 Housing Bubble ............................................................................................. 73

3.2.28 Housing Market ............................................................................................. 73

3.2.30 Inflation ......................................................................................................... 74

3.2.31 Infrastructure ................................................................................................. 74

3.2.32 Intrinsic Value (Finance) ............................................................................... 74

3.2.33 Investment (finance) ...................................................................................... 74

3.2.34 Jackson Hole Consensus ............................................................................... 75

3.2.35 Keynesian Economic(s)................................................................................. 75

3.2.36 Lending.......................................................................................................... 75

3.2.37 Liquidity Trap ............................................................................................... 75

3.2.38 Liquidity ........................................................................................................ 76

3.2.39 Macroeconomic ............................................................................................. 76

3.2.40 Macroprudential Regulation .......................................................................... 76

3.2.41 Mainstream economic(s) .............................................................................. 76

3.2.42 Monetary Policy ............................................................................................ 76

3.2.43 Mortgage Market ........................................................................................... 76

3.2.44 Mortgage (loan) ............................................................................................. 77

3.2.45 Open market operations (OMO) ................................................................... 77

3.2.46 Peak (Business, Economic) ........................................................................... 77

3.2.47 Pricking (punching) the bubble ..................................................................... 77

3.2.48 Purchase ........................................................................................................ 77

3.2.49 Real estate ..................................................................................................... 78

3.2.50 Recession (business, economic) .................................................................... 78

3.2.51 Rent .............................................................................................................. 78

3.2.52 Repo Market .................................................................................................. 78

3.2.53 Security (Banking, Economics)..................................................................... 78

3.2.54 Sell ................................................................................................................. 79

3.2.55 Speculation ................................................................................................... 79

3.2.56 Spending ........................................................................................................ 79

3.2.57 Stock Market Margin .................................................................................... 79

3.2.59 Taxation ......................................................................................................... 80

3.2.60 Taylor Rule .................................................................................................... 80

3.2.61 Time Varying Bank Capital Ratio ................................................................. 80

3.2.62 Too Big to Fail (Theory) ............................................................................... 81

3.3 Research Procedure ....................................................................................... 81

3.3.1 Research Design ............................................................................................ 81

3.3.2 Research Strategy .......................................................................................... 82

3.3.3 Area of the Research ..................................................................................... 83

3.3.4 Location of case study - Bank of Tanzania ................................................... 83

x

3.3.5 Unit of study .................................................................................................. 85

3.3.6 Types of Study .............................................................................................. 85

3.3.7 Types of Data ................................................................................................ 86

3.3.8 Unit of Analysis ............................................................................................ 86

3.3.9 Study Population ........................................................................................... 86

3.3.10 Sampling methods ......................................................................................... 87

3.3.10.2 Sample Frame/Size ........................................................................................ 88

3.3.10.3 Sample Size Determination ........................................................................... 89

3.3.11 Methods of Data Collection .......................................................................... 89

3.3.12 Tools of Data Collection ............................................................................... 90

3.3.13 Data Organization ......................................................................................... 90

3.3.13.1 Response Rate ............................................................................................... 90

3.3.13.2 Data organization .......................................................................................... 90

3.3.13.2 Data editing ................................................................................................... 90

3.3.13.3 Data processing and analysis........................................................................ 91

3.3.13.4 Data presentation ........................................................................................... 91

3.3.14 Variables and their measurements................................................................. 91

3.3.15 Reliability and validity issues ....................................................................... 92

3.3.16 Ethical Issues ................................................................................................. 93

CHAPTER FOUR .......................................................................................................... 93

PRESENTATION OF FINDINGS ............................................................................... 94

4.1 Introduction ................................................................................................... 94

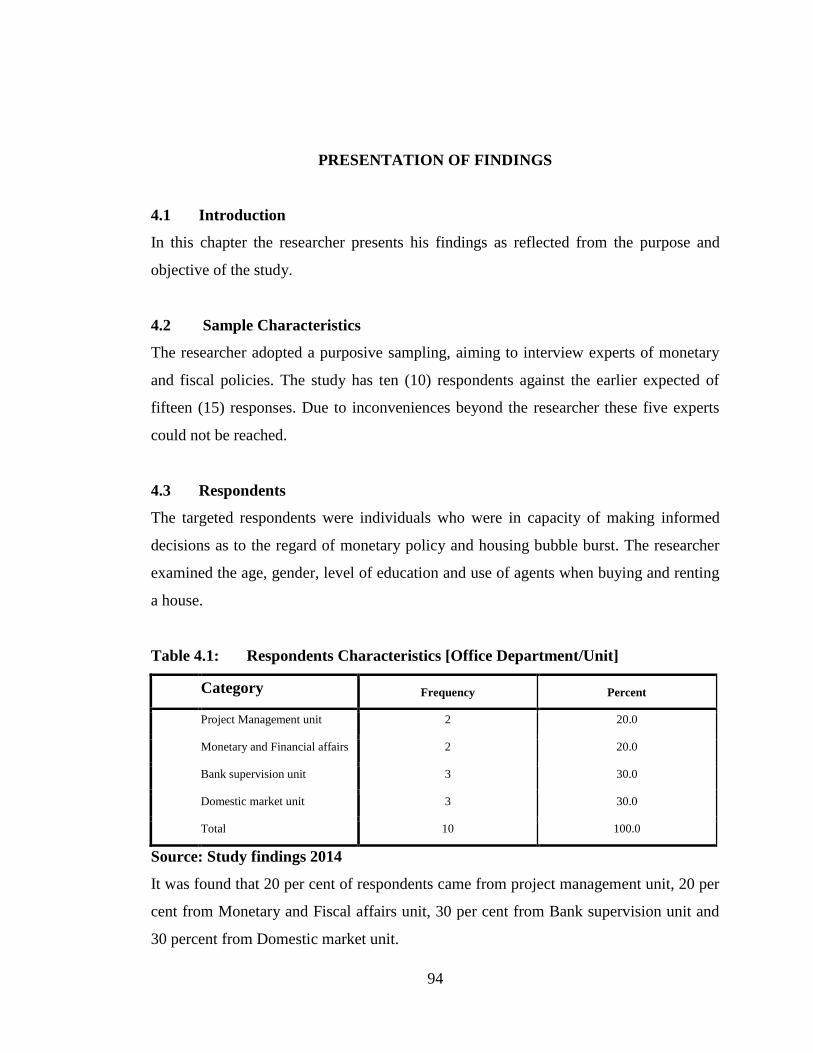

4.2 Sample Characteristics ................................................................................. 94

4.3 Respondents .................................................................................................. 94

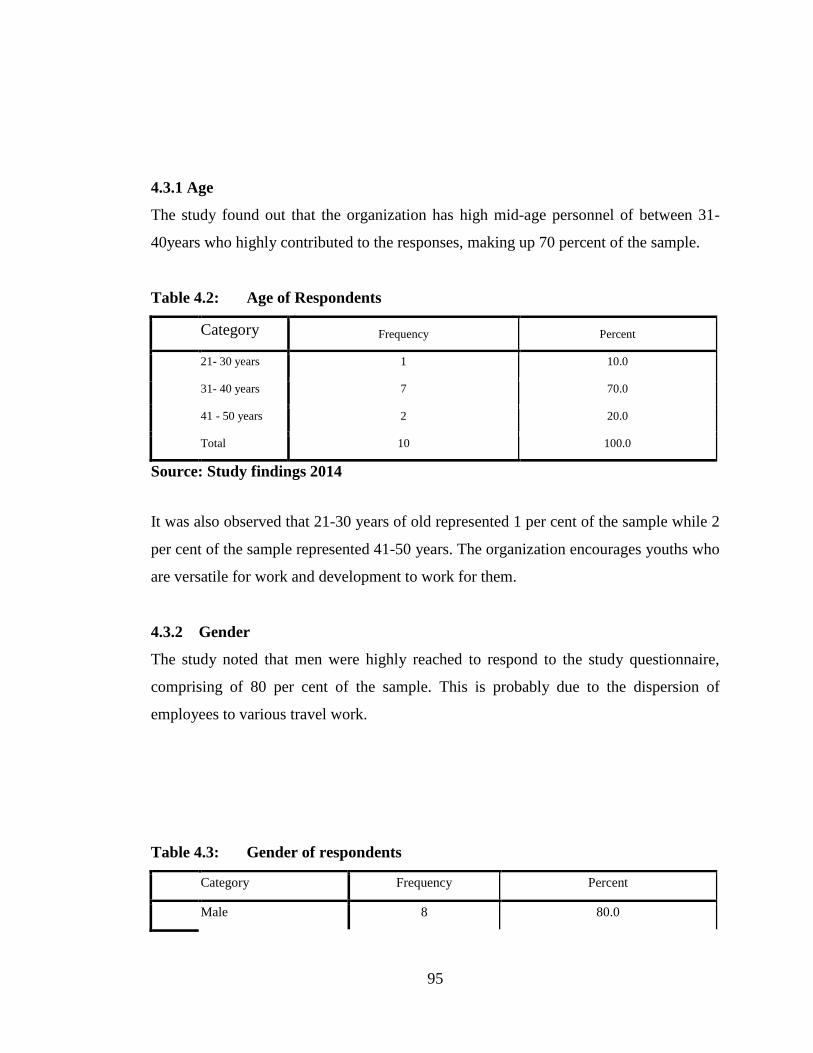

4.2.1 Age ................................................................................................................ 95

4.2.2 Gender ........................................................................................................... 95

4.2.3 Level of Education ........................................................................................ 96

4.2.4 Use of agents when buying and renting a house ........................................... 96

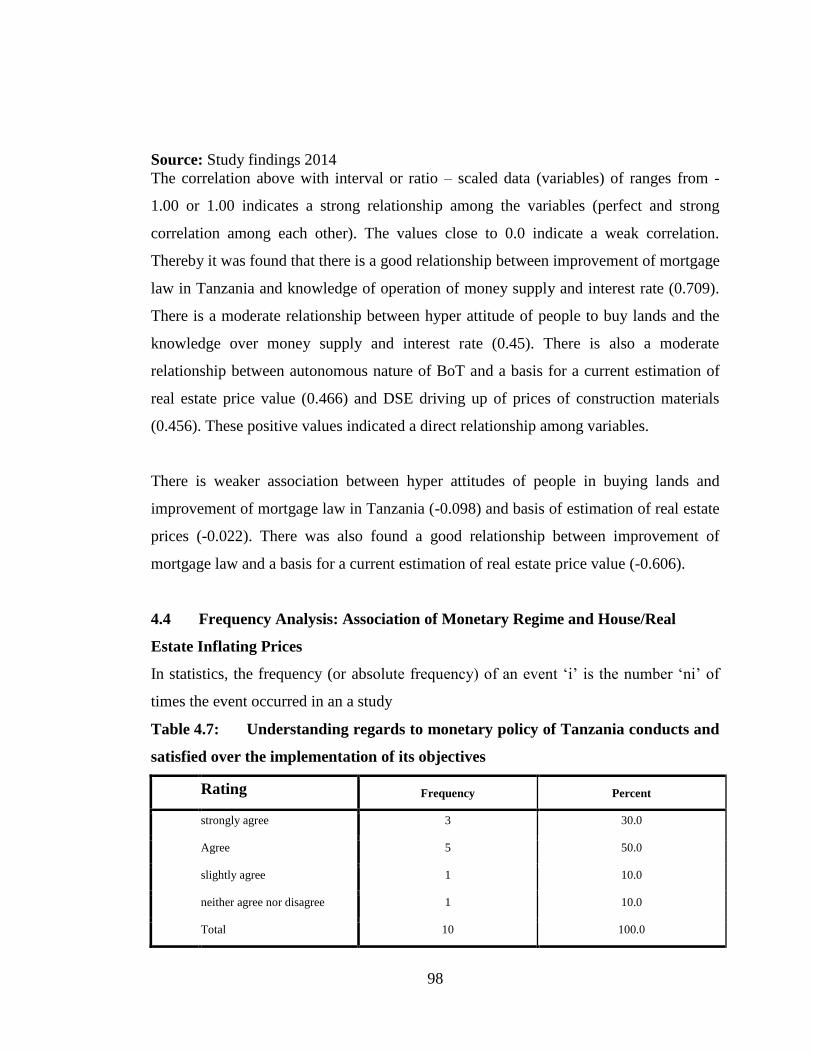

4.4 Frequency Analysis: Association of Monetary Regime and House/Real

Estate Inflating Prices.................................................................................... 98

4.5 Cross Tabulation: Association of Monetary Regime and House/Real Estate

Inflating Prices ............................................................................................ 103

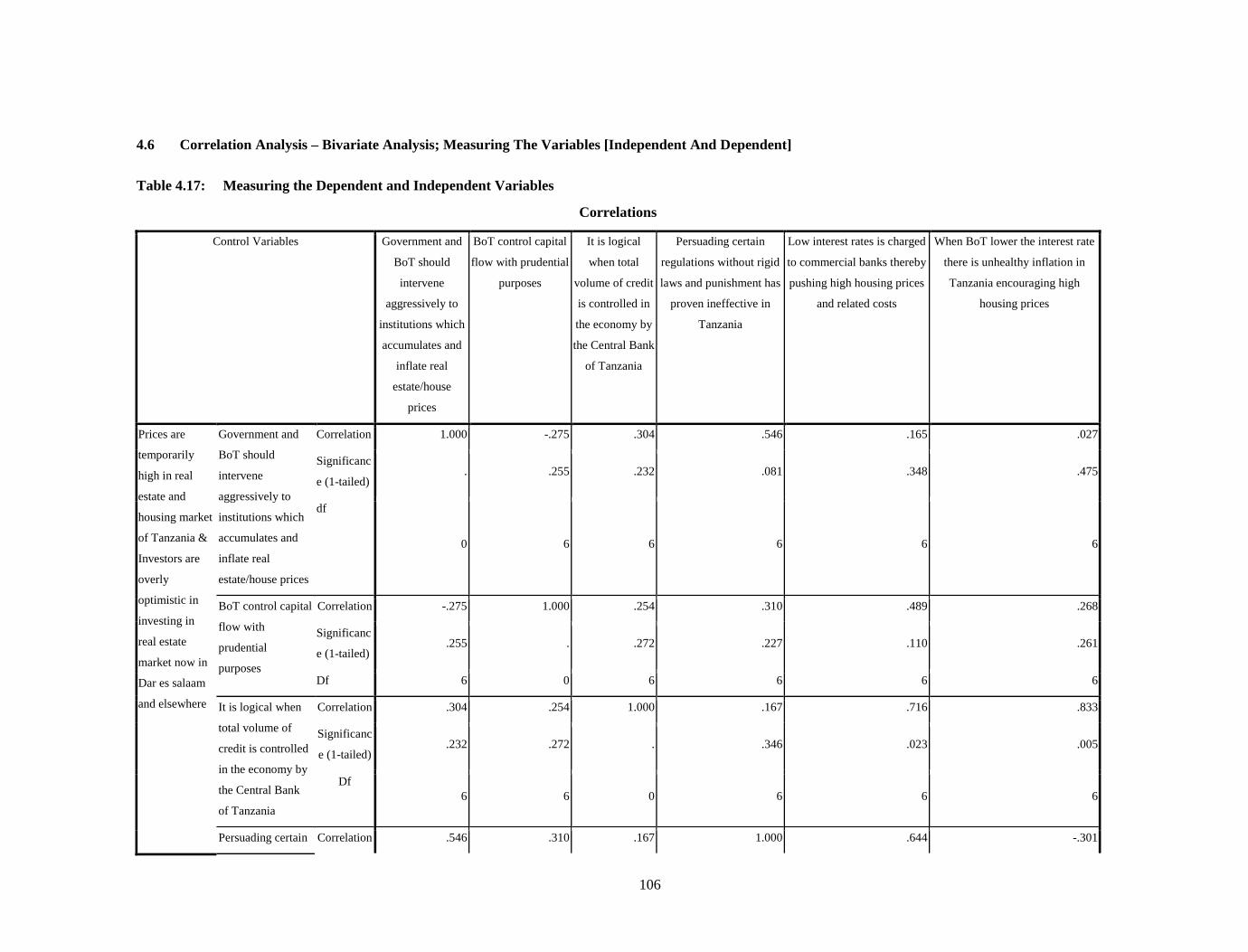

4.6 Correlation Analysis – Bivariate Analysis; Measuring The Variables

[Independent And Dependent] .................................................................... 106

4.7 Cronbach‘s Alpha Analysis - Testing Consistency/Validity of Data .......... 108

4.8 Analyzing The Hypothesis of The Study .................................................... 108

4.8.1 When BoT lower the interest rate there is unhealthy inflation in Tanzania

encouraging high housing prices. ................................................................ 109

4.8.2 The low interest rate charged to commercial banks and other depository

institutions on loans they receive from BoT encourage high money supply

resulting into inflationary tendencies giving negative effect in housing

market prices. .............................................................................................. 110

xi

4.8.3 Due to high cut throat competition in the banking and financial sector in

general, persuading a certain regulation without rigid laws and punishment

has proven ineffective in Tanzania. ............................................................. 110

4.8.4 It is logical when total volume of credit is controlled in the economy by the

Central Bank of Tanzania. ........................................................................... 111

4.8.5 BoT control capital flow with prudential purposes ..................................... 111

4.8.6 The Central Bank and where possible government should intervene

aggressively to the institution(s) which possess a threat in a forerunner in

accumulating and inflating real estate/house prices. ................................... 112

CHAPTER FIVE .......................................................................................................... 113

DISCUSSION OF THE FINDING ............................................................................. 113

5.0 Introduction ................................................................................................. 113

5.1 Discussion of General Findings and Data Analysis .................................... 114

5.2 Discussion of Specific Objectives ............................................................... 117

5.2.1 Traditional monetary policy tools effectiveness in addressing economic

bubble .......................................................................................................... 117

5.2.2 Supervisory discretion in targeting the activities of individual institutions ...... 119

5.2.3 Credit market controls evaluation ............................................................... 120

5.2.4 Establishment of a time varying bank capital ratio ..................................... 121

CHAPTER SIX ............................................................................................................ 123

CONCLUSION, IMPLICATIONS, LIMITATIONS, RECOMMENDATIONS

AND FUTURE RESEARCH ................................................................................ 123

6.0 Introduction ................................................................................................. 123

6.1 Conclusion ................................................................................................... 123

6.2 Implications of the Study ............................................................................ 123

6.3 Limitations of the Study .............................................................................. 124

6.4 Recommendations ....................................................................................... 124

6.5 Future Research Suggestion ........................................................................ 126

REFERENCE ............................................................................................................... 127

APPENDICES .............................................................................................................. 138

Appendix One: Questionnaire .................................................................................... 138

Appendix Two: Macroprudential regulation .............................................................. 151

Appendix 3: Budget for the Research ..................................................................... 153

Appendix 5: Concept Note ..................................................................................... 155

xii

TABLE OF LIST

Pages

2.2.5.1 Housing Market Indicators ..................................................................... 26

2.2.5.1.1 Housing Affordability Measures ............................................................ 27

2.2.5.1.3 Housing Ownership and Rent Measures ................................................ 29

2.2.5.1.4 Housing Price Indices ........................................................................... 32

3.3.10.1 Sampling technique ................................................................................ 87

Table 3.1: Distribution of Respondents ................................................................... 88

Table 4.1: Respondents Characteristics [Office Department/Unit]......................... 94

Table 4.2: Age of Respondents ............................................................................... 95

Table 4.3: Gender of respondents............................................................................ 95

Table 4.5: Use of agents When Buying and Renting A House ............................... 96

Table 4.6 Correlation matrix vs correlation of Monetary regime and House/Real

Estate inflating prices ............................................................................. 97

Table 4.7: Understanding regards to monetary policy of Tanzania conducts and

satisfied over the implementation of its objectives ................................ 98

Table 4.8: BoT is autonomous and independent from the government interventions

................................................................................................................ 99

Table 4.9: BoT should follow the lead of financial markets ................................... 99

Table 4.10 : It is logical for BoT to adopt gradualism attitude (steady and regular

techniques) in the housing market asset bubble circumstance at a

moment ................................................................................................. 100

Table 4.11: There is a tremendous pressure of rising rents in Dar es salaam (and

other regions) ....................................................................................... 101

Table 4.12: People have a hyper attitude to buy lands in Tanzania even though not

necessarily developing them ................................................................ 101

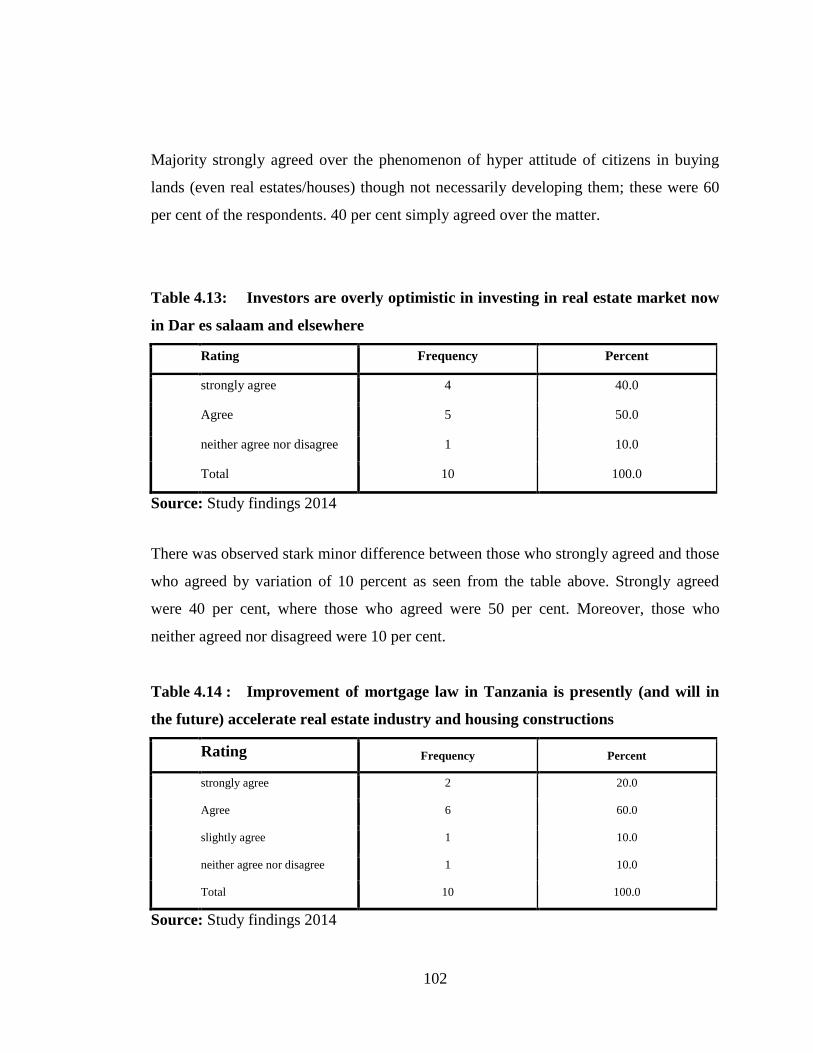

Table 4.13: Investors are overly optimistic in investing in real estate market now in

Dar es salaam and elsewhere................................................................ 102

xiii

Table 4.14 : Improvement of mortgage law in Tanzania is presently (and will in the

future) accelerate real estate industry and housing constructions ........ 102

Table 4.15: DSE stock brokers negatively drives up prices of major construction

industry particularly cement ................................................................. 103

Table 4.16: Crosstab*Count; Pressure of rising rents against monetary policy and

implementation of monetary objectives ............................................... 104

Table 4.17: Measuring the Dependent and Independent Variables......................... 106

Table 4.18 : Cranbach‘s alpha Analysis of the study variables – Reliability statistics

.............................................................................................................. 108

xiv

LIST OF FIGURES

Pages

Figure 2.1: Expansion vs Contraction Monetary Policy ............................................... 14

Figure 2.2: Bank of Tanzania view............................................................................... 17

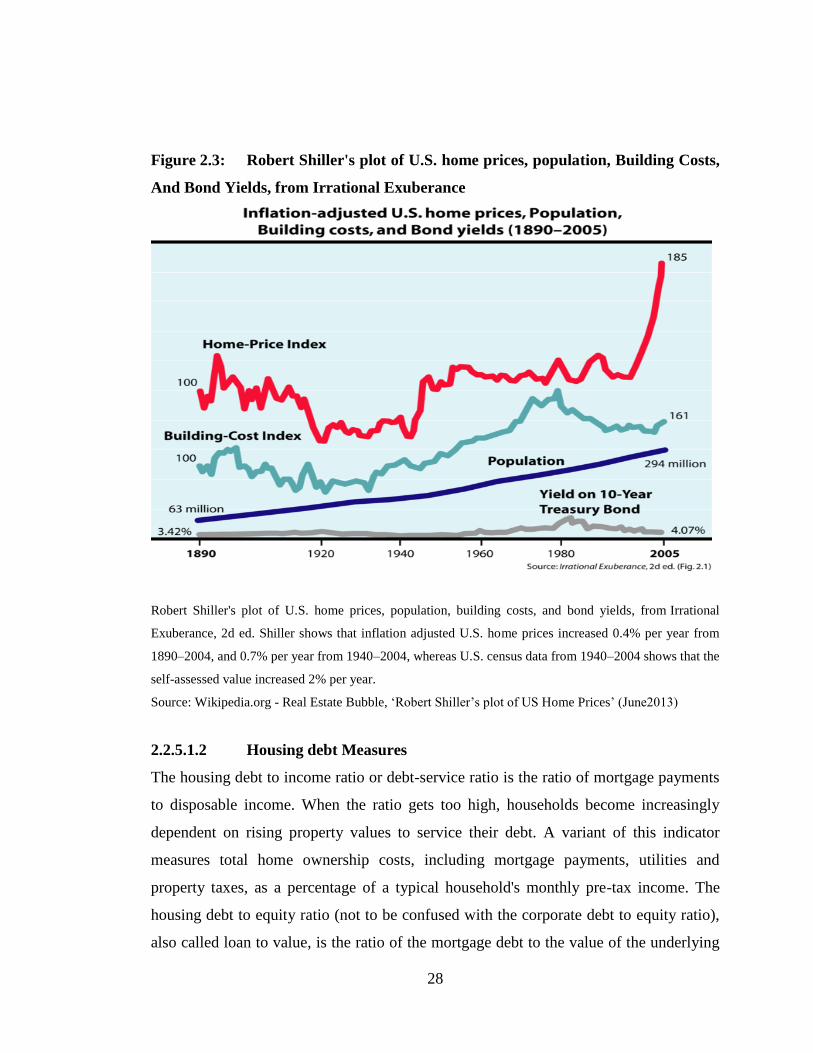

Figure 2.3: Robert Shiller's plot of U.S. home prices, population, Building Costs, And

Bond Yields, from Irrational Exuberance ................................................ 28

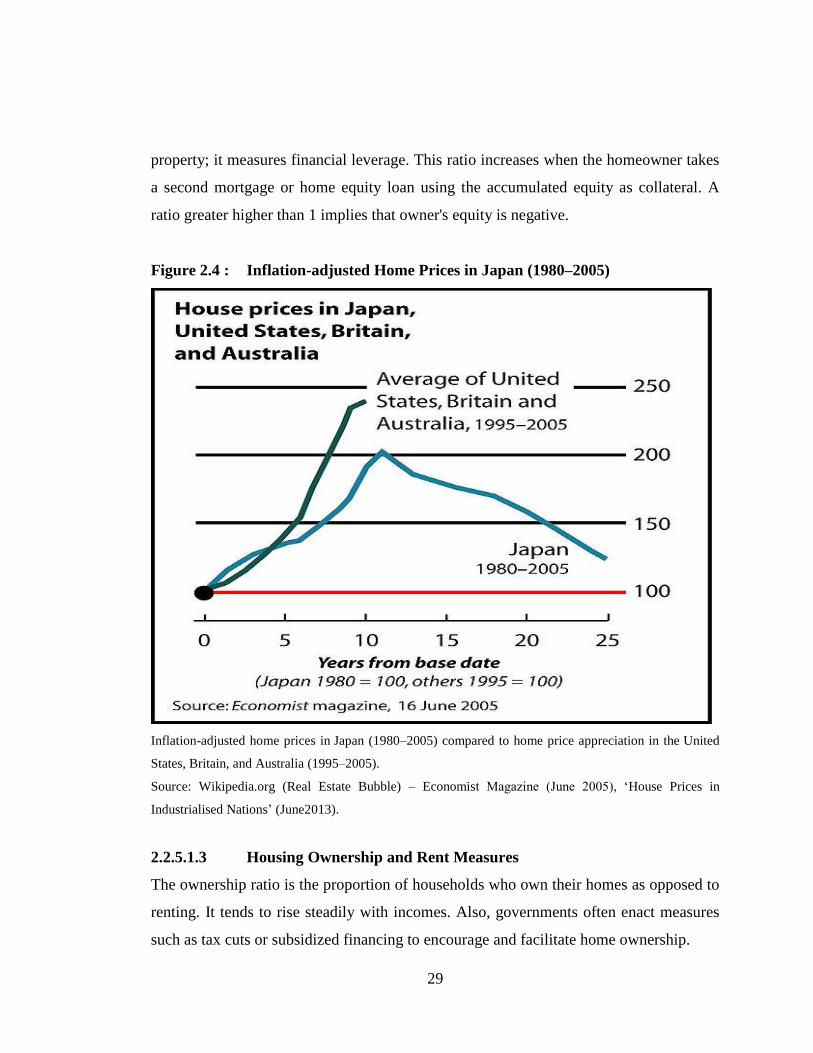

Figure 2.4 : Inflation-adjusted Home Prices in Japan (1980–2005) ............................ 29

Figure 2.5 : The Case–Shiller index (national, quarterly) 1987–2008 ......................... 32

Figure 2.6 : Tanzania inflation Rate............................................................................. 35

Figure 2.7 : Tanzania Shilling ...................................................................................... 36

Figure 2.9: Tanzania Interest Rate .............................................................................. 38

Figure 2.10 : Conceptual Framework ............................................................................ 66

Figure 3.1: Research Process ...................................................................................... 83

Figure 3.2: Overview map of Dar es salaam ............................................................... 84

Figure 3.3 : Detail map of Dar es salaam City Centre (locating BoT) ........................ 85

Figure 4.1: Bar graph; Pressure of rising rents against monetary policy and

implementation of monetary objectives ................................................. 105

1

CHAPTER ONE

INSIGHT INTO TANZANIA MONETARY POLICY AND ITS LINKAGE TO

REAL ESTATE/HOUSING MARKET

1.1 Background History of the Problem

Monetary policy that increases the supply of money (expansionary policy) leads to

reduction in interest rates, stimulate the consumption and investment in the economy.

Increased consumption and investment mean higher aggregate demand as well as

increased personal income and employment. This all translates into ability to rent,

purchase and sell houses/apartment. Tanzania is in the heights of high inflation, meaning

there is plenty of money in circulation which clearly explains the use of Bank of

Tanzania (BOT) contractionary policy at a moment. Inflation is not always a bad thing

especially if it is on a short-run; it may suggest there is injection of some money

‗quantities‘ in the economy due to supposedly discovery of new sources of raw

materials, energy and minerals. This is what has undoubtedly taken place in Tanzania

giving citizens and private sector‘s power to drive real estate/housing market to high

new unimaginable levels. In financial year 2010/11, government allocated 13 per cent of

expenditure budget into infrastructure. Construction industry by 2009 accounted to 7.9

per cent of GDP, growing at a rate of 7.5 per cent and by 2010 it employed about 9 per

cent of Tanzania workforce (UNESCO, August 2010). There were 2,621 projects worth

nearly TZS 2.4 Trillion during 2009. Contractors Registration Board (CRB) of Tanzania

in 2009 registered 930 applicants compared to 656, 662 and 608 in 2008, 2007 and 2006

respectively. Some 33 of the newly registered contractors were foreigners, leading to a

total of 236 foreign contractors in the country which was 4.1 per cent of the total

contractors in the Contractors Registration Board (CRB) register compared to 3.6 per

cent in 2009, UNESCO report added. No hesitation that Tanzania is booming; the fiscal

policy is relaxed which encouraged spending and monetary policy though is tightened, is

not ‗tightened‘ enough and the central message of this research is that there is excessive

availability of credit in the economy.

2

According to National Housing Corporation (NHC), Tanzania runs a housing deficit

estimated at 3 million units valued at $180 billion by the end of 2007, while the current

annual demand for houses in urban areas is 200,000 units estimated to cost $12 billion.

1.2 Statement of a Problem

Though Tanzania housing/real estate market seems young, there are ongoing

developments which will soon in near future put the country at the edge. Tanzania

government has committed itself in Kigamboni City Project with expected cash injection

of about Tzs 11.6 trillion upon completion in 2012 (The East African, 12th

July 2012).

Monetary policy set up coincides with the rate of housing development, that is a relaxed

policy with evidence of 8.2 per cent of inflation (Bank of Tanzania, June 2012). In other

words, for the pace of construction to be encouraged, money supply needs to be

encouraged (in constricting supply of money, by raising interest rates or raising bank

rates is to discourage such developments). This is in alignment of a global annual value

of construction industry at about USD 1.5 trillion (Nguguna, H.B, 2008). Thereby rent

and housing market is expanding in Tanzania; with a current deficit of estimated 3

million units valued at USD 180 billion by the end of 2007, while current annual

demand of houses in urban areas is 200,000 units estimated to cost USD 12 billion

(Business Times, 2013).

Tanzania is therefore booming with housing industry, but there might be signs of unclear

regulation which could threaten the very economy; such as lack of real estate/housing

regulatory authority and the unclear policy set up of monetary policy. The future of the

economy is shrouded with doubts of how devastating might the housing prices and rents

rises to uncontrollable levels.

3

1.3 Objective of the Study

1.3.1 General Objectives

Evaluating how the Central Bank of Tanzania influences the real estate/housing market

through its policies.

1.3.2 Specific Objectives

(i.) To analyse if traditional monetary policy tools can effectively address

housing/real estate market. They include; bank rate, reserve requirements and

discount rate as well as moral suasion.

(ii.) To find out if supervisory discretion could be used to target the activities of

individual institutions that are systematically important firm so as to achieve a

level of controlling prices of housing market.

(iii.) To evaluate if employment of ‗credit market controls‘ aimed at specific market

such as mortgage market and commercial real estate can result into established

and stable housing market prices.

(iv.) To assess if establishing a time varying bank capital ratio-one in which the

capital ratio requirement varies over business cycle can address housing bubble

phenomenon.

1.4 Research Question(s)

How should the Central Bank of Tanzania influence the real estate/housing market

through its policies?

(i.) How can traditional monetary policy tools be effectively administered to address

housing market prices issue?

(ii.) Is supervisory discretion beneficial if it is targeted towards the activities of

individual institutions that are systematically important so as to achieve a level of

controlling prices of housing market?

4

(iii.) Does the employment of ‗credit market controls‘ at specific market such as

mortgage market and commercial real estate market result into established and

stable housing market prices?

(iv.) Can establishing a time varying bank capital ratio-one in which the capital ratio

requirement varies over business cycle address housing asset bubble

phenomenon?

1.5 Significance of the Study

By understanding the link between Central Bank and real estate/housing market,

pertinent measures can be taken to protect the policy set up in this fragile sector which is

given considerable amount of attention at a moment.

In addition, the following are important to this study:

(i.) Findings will bring new insights on how to effectively design the monetary

policies.

(ii.) Findings will add new information to the economic and business field as far as

Tanzania is concerned.

(iii.) The study aims at contributing in a small way towards a deeper understanding of

economic bubbles in the developing countries context.

(iv.) The beneficiaries of this information may include policy makers, ministries,

economists and academicians.

1.6 Rationale for Study

The economy at present times is unstable with inflation prices almost in every

commodity and other sectors. Construction industry being prime to Tanzanians, and thus

by understanding the right policy injection, we can save an important sector‘s

unnecessary rising of prices. Addressing of this current phenomenon will be a turning

point for the nation and most companies‘ achievements.

5

1.7 Scope of the Study

Evaluating how the Central Bank of Tanzania influences the real estate/housing market

through its policies.

1.8 Limitations of the study

The researcher encountered scarcity of literature contents relating to Tanzania and even

relating to East Africa. This study being an ongoing debate among world greatest

scholars, the researcher had to study and update himself with literatures in every

successive period of the research.

1.9 Dissemination of Research Report

This report will be distributed to the learning institutions, Bank of Tanzania, World

Bank and International Monetary Fund, government ministries, libraries and online

contents sites.

6

CHAPTER TWO

LITERATURE REVIEW

2.1 Textual literature and Theoretical Framework

2.1.1 Definition of Asset Bubble

This is an economic development in which the price of class of physical or financial

assets rises to a level that appears to be unsustainable and well above the asset‘s value as

determined by economic fundamentals (Lahart. J, 2008)

2.1.2 Current Economic Outlook of Tanzania

Giugale and Canuto (2010) noted that the global financial crises changed the way we

think about the global economic order leading to doubting the principles and practices

that were once accepted. For the developing world, that conceptual uncertainty is

particularly uncomfortable, and we have witnessed the various policies in Tanzania

bringing confusion and debates. Some people may relate the economic bubble in

Tanzania from the explicit cost side, on the basis of unaffordability of instrument like

treasuries, bonds and share of Tanzania financial market. This is not always the case, as

it could be a purely purchasing power issue with nothing to do with price increase or

inflation. The current times where the bubble is growing (has not burst yet) it is prudent

for the Central Bank of Tanzania to avoid any rush decisions. This is because as the

bubble build-up it takes years until a visual pattern is noticed, making it hard to identify

and predict the magnitude of the bubble. For such observance a precise monetary policy

can hardly be adopted in this period of uncertainty. Furthermore, there is no need to

directly target the bubble; as an asset bubble steadily increases so do the wealth build up,

that stimulates consumption. The more increase of asset bubble like for the case of real

estate/housing market should surely result in a dangerous limit of inflation, thus the

Central Bank of Tanzania should act to curb it. In other words we can agree that bank

rate cannot always be adjusted to housing market/real estate sector (until a certain right

time). It should be highly concerned that in this regard of inactiveness of monetary

7

policy the bubble keeps on inflating and ultimately burst. This burst leads to a decline of

a real economy which now forces the Central Bank to quickly reduce the bank rate to

offset the negative impacts of the bubble burst.

African Economic Outlook (2014) observed that inflation in Tanzania has declined to

single digits and gross domestic product (GDP) growth projected at about 7% in the

medium term where among the main drivers of growth being construction and such

growth is significantly being boosted by natural gas discoveries. But we ought to be

careful that it is not a mere rise or drop of inflation but at what rate and how much

supply of money is there in the economy; this is a gist of a story.

2.1.3 Inefficacy of Monetary Policies

During the 2008 Global Financial and Economic crisis there was shortage of money in

most Western economies thus no enough money to be lent to the businesses. According

to Ngowi (2013) one of the causes of the 2008‘s Economic Crisis is the situation where

banks and other financial institutions extended and made credit accessible and available

even to people and institutions who could not honour the loan covenant – that is

repaying the monies plus accrued interest when maturity was due. This occurred due to

inadequate supervision of banks and financial institutions by monetary authorities by

way of Central Banks in general and the Fed in the US in particular. Remember when

the recent crisis took place the most hit sectors were real estate and stock exchange, and

then ripple effects were felt in other sectors. It is unquestionably the affected people in

the West were concentrated into the housing market (so did the effect), this is another

way of saying most money borrowed from financial institutions large chunk of it was in

mortgage spending loans.

Supervision of banks and monetary matters in a country is the responsibility of central

bank, and for our case is Bank of Tanzania. In United States, regulation of financial

sector was left minimal - left too independent in a hope that the free forces of market

8

would sort out the demand and supply; but in the end it was a shameful devastation. In

2009 the government of Tanzania injected TZS 1.7 Trillion as a rescue package against

the global financial crisis; was this package sustainable and was it efficiently utilized? If

not, then it is another unhealthy ‗quantities‘ of money injected to weaken the TZS

strength (that is inflation).

Global economic crisis brought about careless policies of Federal Reserve in United

States led into the jobs loss, decline of GDP, increase in poverty levels, protest and civil

unrest, collapse of governments, and billions of business losses globally. Perhaps if we

can re-visit how the crisis crippled Tanzanian economy we might be careful to design

our local monetary policies and maybe shelter our little economy. Tanzania experienced

approximate downturn of economic growth from nearly 7 per cent in 2009 to 4.5 per

cent in 2010 (Ngowi, 2013). In 2008, proceeds from cotton dropped by 54.4 per cent,

losing TZS 40 billion due to export failure; by 2008 exports were expected to drop to 44

per cent. Arabica coffee price dropped to 34 per cent and Robusta coffee dropped to 30

per cent by December 2008, leading to an average decline of coffee export by 32 per

cent. Nile perch (fish) normally exported to European Union (EU), accounting to 80 per

cent of export dropped to average of between 50 to 60 per cent (normally Nile perch

brings over USD 200 million revenue). Now as it can be seen, the economic meltdown

due to ineffective monetary policy is not an easy forgiving circumstance as it tears apart

people‘s lives. This can happen to our economy too.

2.1.4 Household Debt and Monetary Policy

In the five years to 2003, US household debt rose by 52 per cent and the ratio to income

reached a record132 per cent. In the UK debt jumped 63 per cent over the same period,

while in Australia it rose even faster, by a whopping 90 per cent (Calverley, 2004). In

relation to household incomes, debts soared to over 150 per cent in both countries. By

way of contrast, Japan and Germany, where house prices are weak saw much smaller

increases in debt and their ratios to incomes have remained stable. Part of the rise in debt

9

was attributed to a greater proportion of the population owning their own homes; and

part is due to individuals taking out mortgages on investment properties. However, the

bulk of the increase in debt can only be explained in relation to higher home prices. New

buyers and people trading up are forced to take on large mortgages to be able to afford

today’s high prices. Meanwhile, many others are taking advantage of higher prices to

increase their existing mortgages, either to pay down debt or to finance major

purchases. In a rising market it is quiet rational for individuals to increase their

borrowing to finance buying a larger house for themselves or an investment property.

It should be noted that the amount of lending in the economy is determined by financial

institutions, based on their assessment of the risk and profitability of the lending

opportunities open to them. Overall lending is not controlled by the government; once it

was, and in some countries in the developing world it still is (Calverley, 2004). In

advanced economies the banking system can lend as much as it wants to, subject only to

having sufficient capital from shareholders and meeting the capital and regulatory

requirements of the authorities. But some people argue that the system encourages too

much lending; in principle if banks are to make profits and avoid bankruptcy they have a

strong incentive not to over lend. Still if banks relax their risk criteria even a little,

lending will increase. Suppose that banks raise the proportion of their mortgage book

provided at a risky 100 per cent loan-to-value ratio from 1 per cent to 2 per cent. If the

risk of loss on such loans is seen as 5 per cent (relatively high for mortgages), this may

still be an acceptable risk/reward for the bank and be prudent enough for the regulators.

But it is extra fuel for the market, allowing some people to buy who otherwise might not

have been able to afford to do so.

Banks also make mistakes; during a bubble the management can be caught up in the

general euphoria. There is a danger as the bank management take more risks than would

be ideal for their shareholders; earning high salaries and large bonuses. This keep on

crippling the free market system, but perhaps it is because the management and

10

shareholders know that there is a potential guarantor for the system, namely the

government.

At present banks regard consumer lending in general and mortgage lending in particular

as one of the most profitable areas of business. Lower interest rates have made it

possible for people to fund larger loans. But when mortgages are agreed based on the

appraised value of a house, while the value of housing is pushed higher by the easy

availability of mortgages, there is a serious risk that house prices can reach extreme

levels. If house prices should fall significantly, people who buy near the peak with high

loan-to-value ratios will face significant losses. High debt burdens can then exacerbate

the impact of falling house prices on the economy as a whole. It is at this period you

witness debt deflation, where people are forced to sell their homes to pay off debts,

leading to further falls in house prices.

In Tanzania, we have seen discovery of new oil fields, new minerals and influx of

foreign capital which obviously motivates the growth of construction industry. Indeed

housing and real estate is an engine of growth from low income citizen to a large

company. Thus it brings us to a very important area of observing interaction of housing

with the economy. Rising house prices and growing borrowing has supported low

savings rate and high consumer spending growth. We can clearly attribute the high

spending goes into the real estate/housing sectors. If we want to prevent a bigger asset

bubble in housing market in Tanzania it is wise to try to reverse the high spending habit

into housing (or at least control it). But it is not so simple to design this move and avoid

strong economic repercussions; that is increasing the saving rate imply reducing the

consumer spending and thus economy would grow much more slowly. It is thus

important if a government could increase spending so as to expand growth; but time and

time again the Tanzanian budget is ever in deficit (like the rest of developing nations). In

these turbulent global crises even the industrial nations are in steep deficit. The new

resources discovered in Tanzania cannot fast track high economic paces in a short-run,

11

much of the benefits will be realized in a long-run; this is due to Return on Invested

Capital – too much capital invested which takes many years to be recovered. The most

crucial sector to save the economy will always be export sector. This will also be saviour

area even in times of bubble burst in Tanzania; but it will all depend how prepared we

would be by then (or rather now).

Tanzania can learn much over application of monetary policy towards housing market

from the experiences of Britain as well. During 2001-2003, with the world economy

weak and the pound strong, hurting exports and depressing Britain‘s manufacturing

sector, the overall economy grew slower than its trend rate (around 2.5 per cent) and

inflation was below target (Calverley, 2004). As a result, interest rates were cut from 6

per cent to 3.5 per cent, well below ‗neutral‘ levels. But with unemployment stable and

consumers less pessimistic than manufacturers, house prices boomed.

The housing bubble threatens a weak economy in future if house prices fall abruptly,

which could pull inflation below the Bank of England‘s 2 per cent target. But trying to

prick the bubble to avoid this risk might simply precipitate the crisis later. In 2003-4,

with the economy strengthening, rates began to move up, but this was no more than the

conventional monetary policy response, aimed at returning interest rates gradually

towards the neutral level, believed to be around 5 per cent in the UK. The main reason

for gradualism is that the Bank of England wanted growth to exceed trend for a while, to

help push inflation back up to 2 per cent target. But, perhaps inevitably, house prices and

debt responded to this very gradual approach by accelerating in the first half of 2004. A

good lesson we can get during bubble inflation is that monetary policy cannot only alone

solve much to keep the economy afloat (but one of the means to try approach the crisis).

US household debt payments as a per cent of income reached their highest level in 2000

at over 13 per cent. But despite the fall in interest rates, the ratio has remained about the

same level since then, due to increased borrowing. In contrast, during the early 1990s in

the last recession, the ratio came down sharply, with lower interest rates and slower

12

borrowing. From the low point of 1 per cent in 2003 the Federal Funds moved back to

neutral levels and then rose higher (for Fed to slow the economy at some stage). Bond

yield was above 2002-3 levels of around 4 per cent, increasing mortgage rates on new

loans.

2.2 Empirical Literature and Conceptual Framework

The economic effects from the recent global financial crisis has undoubtedly triggered a

renewal discussion about the impact of bubbles and the role of public policy in

addressing them (Evanoff, D., Kaufman, D. and Malliaris, A.G1. It is enough to say that

the financial crisis can be looked into; (a) Conceptual issues concerning the existence of

asset price bubbles; (b) The consequences of bursting such bubbles; (c) Monetary policy

‗management‘ of bubbles and (d) The role of macro prudential regulation in addressing

bubbles.

Conceptual issues concerning the existence of asset price bubbles: A bubble is

generally said to exist if an asset price exceeds its price as determined by

―fundamentals‖ – i.e., the present value of its discounted expected future cash flows – by

a significant amount and this premium persists for some time. If the price of an asset

exceeds its fundamentals only by a very small amount, the differential may only

represent noise instead of bubble. If the deviation from fundamentals lasts for only a

very short trading interval, this may represent temporary mispricing. A bubble forms

because the purchase of an asset is made not necessarily based on the rate of return on

the investment, but in anticipation that the asset can be sold to a ―greater fool‖ at an ever

higher price. A price increase for an asset leads to investor enthusiasm, which further

causes increased demand and additional price increases, and so on. The high demand is

supported by the public‘s memory of high past returns or by optimism that this new asset

will generate high future earnings. This positive trend of increase in prices will finally

1 Evanoff, D.,Kaufman,G.,Mallians A.G. Asset Price Bubbles: Lessons from recent financial crisis.

Retrieved 11th

February 2014 from the World Wide Web: http://www.worldfinancialreview.com/?p=2200

13

change pace and sceptics will rise and turn-around the direction; now a bubble burst out

of this confusion due to sudden drop in price. The significant price decline reflect the

bursting of bubbles in stock markets and real estate markets since the macro economy

analysis on these sectors shows equity and homeownership account for most of

household wealth.

Asset Price Bubbles and Monetary Policy: Any Central Bank such (as Tanzania) has a

mandate to promote price stability and maximum sustainable employment, as well as

maintain financial stability. In United States, Federal Reserve Chairman Greenspan,

tried to formulate the monetary policy in a risk management framework. This framework

assessed the various sources of risks and uncertainty facing the economy, quantified the

risks, and calculated an expected cost associated with the risk. Now, whenever no

significant financial risks or bubble risks existed, the Fed would review inflation,

economic growth, and employment conditions and implement monetary policy by

adjusting the Fed funds rate along the lines of Taylor rule. At one point it was generally

concluded that during bubble‘s expansion stage, the Fed should not increase the Fed

fund rates to deflate the asset bubble. However, if the bubble burst, the Fed should act

immediately and reduce the Fed funds rate to reduce the adverse economic impact of the

bursting. This asymmetric approach to asset bubble became known as the ‘Jackson Hole

Consensus’.

14

Figure 2.1: Expansion vs Contraction Monetary Policy

Monetary policy division

Source: Researcher

Macroprudential Regulation: This relate to a specific policy tool that can be more

accurately directed at the bubble related sector (housing market) as well as bringing

price stability. Adjustment (changes) in bank rate is a blunt policy tool affecting the

market as a whole instead of specific sectors. In addressing asset bubbles, the goal is

typically to target a price build-up in a particular sector – housing market in such as our

concern. Financial regulation can broadly be separated into ‘microprudential’

regulation, which considers the condition of individual financial institutions, and

‘macroprudential’ regulation, which focuses across financial institutions and markets,

and on the efficient functioning of the financial system as a whole. Until recently,

regulatory and supervisory policies operated on the presumption that the financial

system as a whole could be made safe by ensuring that individual financial institutions

were made safe. This ignored market interconnections and externalities, whereby the

actions of one financial institution can lead to a spill-over effects that adversely affect

other financial institutions, general market conditions, and ultimately the economy as a

whole. Instead it may be necessary to use both microprudential and macroprudential

policies to manage financial system risks and achieve financial stability.General

15

monetary policy tools are used to influence the overall macroeconomic situation without

concern about the particular sector of the economy to be affected; such as bank rate,

reserve requirements and discount rate, and the use of moral suasion. Specific tools may

be a bit trickier however there are suggestions. These are; credit market control,

changes in stock market margin requirements, a time varying bank capital ratio,

monitoring of a credit to GDP ratio and supervisory discretion against activities of

important firms in the economy. Soft Central Bank policy may be the precursor of major

asset price exaggerations down the road Hofrichter (2014). Hofrichter says, according to

Charles Kindleberger, an economic historian from his seminal book, ―Maniacs, Panics,

and Crashes‖; asset bubbles usually do not come as single events, but rather as multiple

asset bubbles or as a series of bubbles in quick succession. Emerging markets, as far as

they have linked their currencies to hard currencies, are importing easy monetary policy

from the West. This also applies to developing countries like Tanzania. In a case of a

financial market deregulation2as it may seem practical tools can largely contribute to a

strong private sector credit growth and so precipitate the bubble.

It is undeniable truth that every citizen in the world if it were possible would love to own

a house someday, and this has proven true from the angle of Western nations judging

from the recent real estate bubble which devastated millions of household owners and

citizens. A house is a basic security and most potential part of any moral human.

Americans' love of their homes is widely known and acknowledged (Time, 2005)

however, many believe that enthusiasm for home ownership is currently high even by

American standards, calling the real estate market "frothy" (Greenspan, A. 2005). Only

if the ‗world‘ citizens knew that it has been observed historically; equity price busts

occur on average every 13 years, lasts for 2.5 years, and result in about 4 per cent loss in

GDP then we‘ll be keen on our drive in this sector. Housing price busts are less frequent,

2financial market deregulation include among others the liberalization of the credit market, introduction of

new financial instruments (such as wealth management products) as well as the opening up of the capital

account, which facilitate the capital inflows.

16

but last nearly twice as long and lead to output losses that are twice as large (IMF World

Economic Outlook, 2003). It has been noticed that whenever the Tanzania Electricity

Supply Company (TANESCO) rises the cost of their utility, owners of houses also finds

a way (or call it excuse) to raise the cost/price of their houses. TANESCO raises their

prices because of their struggle with debt and systemlosses. As at January 2014, Energy

and Water Utilities Regulatory Authority (EWURA) announced new power tariffs,

which are 40 per cent increase.3In this circle cyclical price war we can notice how the

monetary and fiscal policy affects the Tanzanians. We can refer to a letter of intent to

IMF in June 2013, when the state said it ‗would limit subsidies to TANESCO to 105

million USD (this is about TZS 200 billion) in the 2013/14 financial year against the

company‘s projected financial needs of 352 million USD (over TZS 560 billion).4It is

this that has pushed TANESCO to raise tariff, but we also see the hand of government

interplay in all this to influence the power costs. According to World Bank estimates,

TANESCO‘s arrears have jumped from 270 million USD as at the end of 2012 to about

500 million USD, with the figure said to be growing at 30 million USD monthly. It is

clearly, monetary policy is crawling beneath and influencing the value and figures

indirectly and we breathe the effects directly.

2.2.1 A Central Bank

A Central Bank, reserve bank or monetary authority is an institution that manages a

state‘s currency, money supply and interest rates. This is an organ which supervises

commercial banking system of their respective countries. Central Bank of Tanzania is a

typical example of one described here. The primary function of Bank of Tanzania (BoT)

3 Ihucha, A (1

st February 2014). Consumers to dig deeper into their pockets as TANESCO raises tariffs.

The East African. Retrieved 5th

March 2014 from World Wide Web:

http://www.theeastafrican.co.ke/business/Costly-power-as-Tanesco-raises-tariffs-/-/2560/2169138/-

/wdb61kz/-/index.html

4 Daily News (5

th July 2013). Power consumers to pay more as TANESCO seeks tariff hike. Daily News

retrieved 5th

March 2014 from World Wide Web: http://dailynews.co.tz/index.php/biz/19480-power-

consumers-to-pay-more-as-tanesco-seeks-tariff-hike?device=desktop

17

is to manage the national‘s money supply through ‗monetary policy‘. Bank of Tanzania

is responsible to monitor commercial banks do not run out of money, restrict discipline

in business conduct and act as lender of last resort.

Tanzania Central Bank and others worldwide possess the following functions;

(i.) Implementing monetary policies

(ii.) Determining interest rates

(iii.) Controlling the nation‘s entire money supply

(iv.) The government‘s banker and the bankers‘ bank (lender of last resort)

(v.) Managing the country‘s foreign exchange and gold reserves and the

government‘s stock register

(vi.) Regulating and supervising the banking industry

(vii.) Setting the official interest rate – used to manage both inflation and the country‘s

exchange rate – and ensuring that this rate take effect via a variety of policy

mechanisms

Figure 2.2: Bank of Tanzania view

Overview of Bank of Tanzania Twin Towers, Conference Centre and Parking Arcade

Source: Bank of Tanzania Org, ‗Overview of BOT‘ (2014)

18

2.2.2 Bank Regulation

Bank regulations are a form of government regulation which subject banks to certain

requirements, restrictions and guidelines. This regulatory structure creates transparency

between banking institutions and the individuals and corporations with whom they

conduct business, among other things. Given the interconnectedness of the banking

industry and the reliance that the national (and global) economy hold on banks, it is

important for regulatory agencies to maintain control over the standardized practices of

these institutions. Supporters of such regulation often hinge their arguments on the "too

big to fail" notion. This holds that many financial institutions (particularly investment

banks with a commercial arm) hold too much control over the economy to fail without

enormous consequences. This is the premise for government bailouts, in which

government financial assistance is provided to banks or other financial institutions that

appear to be on the brink of collapse. The belief is that without this aid, the crippled

banks would not only become bankrupt, but would create rippling effects throughout the

economy leading to systemic failure. General principles of bank regulation throughout

the world include; Minimum requirements, Supervisory review and Market discipline.

The recent asset bubble in housing market in the western nations is a result of market

irregularity and poor regulations of Central Banks, typically at a core of disaster –

United States of America [Federal Reserve]

Among the reasons for maintaining close regulation of banking institutions is the

concern over the global repercussions that could result from a bank's failure; the idea

that these bulge bracket banks are "too big to fail". The objective of Bank of Tanzania is

to avoid situations in which the government must decide whether to support a struggling

bank or to let it fail (this has been faced by Federal Reserve in United States in the

recent economic crisis, but luckily not in Tanzania). The issue, as many argue, is that

providing aid to crippled banks creates a situation of moral hazard. The general

premise is that while the government may have prevented a financial catastrophe for the

time being, they have reinforced confidence for high risk taking and provided an

19

invisible safety net. This can lead to a vicious cycle, wherein banks take risks, fail,

receive a bailout and then continue to take risks once again. Most economics have

further debated importance of bailout as ‗perhaps‘ it is interfering with principles of free

economy and thus seems with government money to these private firms comes strings

which gives a view of government in control of the economy. In fact the recent asset

bubble and global recession has led to economists to question over the efficiency of

‗capitalist market economy‘, is free-economy insufficient? As much as democracy is

now questioned in various governments and so is the whole trunk of capitalist economy

being doubted now when the government inject money to its agencies and private firms.

2.2.3 Monetary Policy

Is the process by which the monetary authority of a country controls the supply of

money, often targeting a rate of interest for the purpose of promoting economic growth

and stability (Elsevier, 2010). The official goals usually include relatively stable prices

and low unemployment. Monetary policy is referred to as either being expansionary or

contractionary, where an expansionary policy increases the total supply of money in the

economy more rapidly than usual, and contractionary policy expands the money supply

more slowly than usual or even shrinks it. Expansionary policy is traditionally used to

try to combat unemployment in a recession by lowering interest rates in the hope that

easy credit will entice businesses into expanding. This too often leads to bubble build up

as there is too much money in the economy that citizens (as Tanzanians) tempts to rise

prices to curb the endless lust and desire to grab everyshilling in the economy.For some

reasons, in most developing nations, Tanzania included there is relaxed monetary

policies (expansionary) during major political presidential campaigns and elections. This

awkward decision reinforced by politicians to Central Banks, in a brief time money

circulation brings happy faces and confidence to the government from its citizen (which

is a primary objective). The dark-side of this choice to the entire nation is that,it raises

the inflation levels, introducing a grim future of clean-up ofthe self-imposed economic

mess which deteriorate national development.Contractionary policy is intended to slow

20

inflation in order to avoid the resulting distortions and deterioration of asset values.

Contractionary monetary policy is also without neither weaknesses nor pinch no matter

how convincing it looks in solving inflationary tendencies.Bank of Tanzania (BoT) has

in the past constricted the money supply so as to control the supply of currency. This has

never gone smooth and enthusiastically accepted as it touches potential businesses and

slows economic growth as in the incidence of 2011.5Economy by itself is self-regulated,

prices being regulated by the demand and supply forces, though it is inevitable for

government not to interfere once in a while. Monetary policy actions prompt rise or fall

of prices, with that, gives the birth of the bubble. Speculation of bubble is a mere sight

of rising of the prices of assets from their intrinsic stage (value). It should be noted that,

speculation powerfully touches the high capital sectors – housing and stocks mostly. In

Tanzania, housing industry and stocks are not strongly reflected in bubble as compared

to the western nations, however all developing nations feels (or rather, have felt) is the

economic pressure (burst of bubbles) - as waves travels from industrial to developing

nations. In other words, we can use a term ‘ripple effects’. Tanzania economy is

surrounded by much tale-tale indicators to show not only economic bubbles are in

speculations, but indeed bubbles are inflating, and there is unforeseen danger if they are

not controlled.

Developing countries may have problems establishing an effective operating monetary

policy. The primary difficulty is that few developing countries have deep markets in

government debt. The matter is further complicated by the difficulties in forecasting

money demand and fiscal pressure to levy the inflation tax by expanding the monetary

base rapidly. In general, the central banks in many developing countries have poor

records in managing monetary policy. This is often because the monetary authorities are

5 Business Times. Tanzania: tighter monetary policy could slow down economic growth (23

rd December

2011). Retrieved 15th

February 2014 from World Wide Web:

http://www.businesstimes.co.tz/index.php?option=com_content&view=article&id=1614:-tanzania-tighter-

monetary-policy-could-slow-down-economic-growth&catid=1:latest-news&Itemid=57

21

not independent of government interference. Thereby, good monetary policy takes a

backseat to the political desires of the government or is used to pursue other non-

monetary goals. For this and other reasons, developing countries that want to establish

credible monetary policy may institute a currency board or adopt dollarization. Such

forms of monetary institutions thus essentially tie the hands of the government from

interference and, it is hoped, that such policies will import the monetary policy of the

anchor nation.

Monetary policy uses three main tactical approaches to maintain monetary stability:

The first tactic manages the money supply; involves buying government bonds

(expanding the money supply) or selling them (contracting the money supply). In the

Central Bank of Tanzania, these are known as open market operations, because the

central bank buys and sells government bonds in public markets. Most of the

government bonds bought and sold through open market operations are short-term

government bonds bought and sold from BoT member banks (like CRDB and NBC

Banks) and from large financial institutions. When the Central Bank disburses or

collects payment for these bonds, it alters the amount of money in the economy while

simultaneously affecting the price (and thereby the yield) of short-term government

bonds. The change in the amount of money in the economy in turn affects interbank