申請人須知 非專營巴士參與「公共交通費用補貼計劃」(「補貼計劃」) 的基本條件及營運要求 (甲)基本條件 1. 以獨資經營者、合夥人或有限公司/法團名義與運輸署簽訂合約。 • 以表明遵守合約訂明參與計劃所須的營運要求 • 確保所提供的服務及其僱員須遵守特定的營運要求 2. 提供邨巴及員工巴士服務的車輛須安裝八達通收費系統。 3. 營辦商亦須向運輸署登記參與計劃的路線資料。 (乙)營運要求 1. 車輛在提供已參與「補貼計劃」的路線服務時,必須按運輸署要求在車 門旁邊的第一隻左側窗及八達通讀寫器上展示本計劃的標誌。車輛在提 供並未參與「補貼計劃」的服務時(如:合約式出租服務、過境巴士服 務或學生服務等),則須把車門旁邊標誌移除,並把參與「補貼計劃」 的八達通讀寫器遮蓋。 2. 委派授權人士監察八達通卡讀寫器的安裝、儲存及更換安排,並詳細記 錄所有車輛及相關車輛的八達通卡讀寫器的編號。 3. 當有任何八達通卡讀寫器損壞或需作出更換,該授權人士須盡快向運輸 署提交相關記錄及登記。 4. 嚴格遵守獲批准的服務詳情表所載列的各項服務詳情,包括獲批准的路 線、車輛、班次、時間表、以及已向運輸署登記的收費表等。如果營辦 商未能遵守上述規定,政府將會向營辦商發出警告信,甚至暫時或永久 將其服務剔出計劃外。 5. 在完成交易後七天內,將其收費系統收集的交易數據上傳至八達通

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

申請人須知

非專營巴士參與「公共交通費用補貼計劃」(「補貼計劃」)

的基本條件及營運要求

(甲)基本條件

1. 以獨資經營者、合夥人或有限公司/法團名義與運輸署簽訂合約。

• 以表明遵守合約訂明參與計劃所須的營運要求

• 確保所提供的服務及其僱員須遵守特定的營運要求

2. 提供邨巴及員工巴士服務的車輛須安裝八達通收費系統。

3. 營辦商亦須向運輸署登記參與計劃的路線資料。

(乙)營運要求

1. 車輛在提供已參與「補貼計劃」的路線服務時,必須按運輸署要求在車

門旁邊的第一隻左側窗及八達通讀寫器上展示本計劃的標誌。車輛在提

供並未參與「補貼計劃」的服務時(如:合約式出租服務、過境巴士服

務或學生服務等),則須把車門旁邊標誌移除,並把參與「補貼計劃」

的八達通讀寫器遮蓋。

2. 委派授權人士監察八達通卡讀寫器的安裝、儲存及更換安排,並詳細記

錄所有車輛及相關車輛的八達通卡讀寫器的編號。

3. 當有任何八達通卡讀寫器損壞或需作出更換,該授權人士須盡快向運輸

署提交相關記錄及登記。

4. 嚴格遵守獲批准的服務詳情表所載列的各項服務詳情,包括獲批准的路

線、車輛、班次、時間表、以及已向運輸署登記的收費表等。如果營辦

商未能遵守上述規定,政府將會向營辦商發出警告信,甚至暫時或永久

將其服務剔出計劃外。

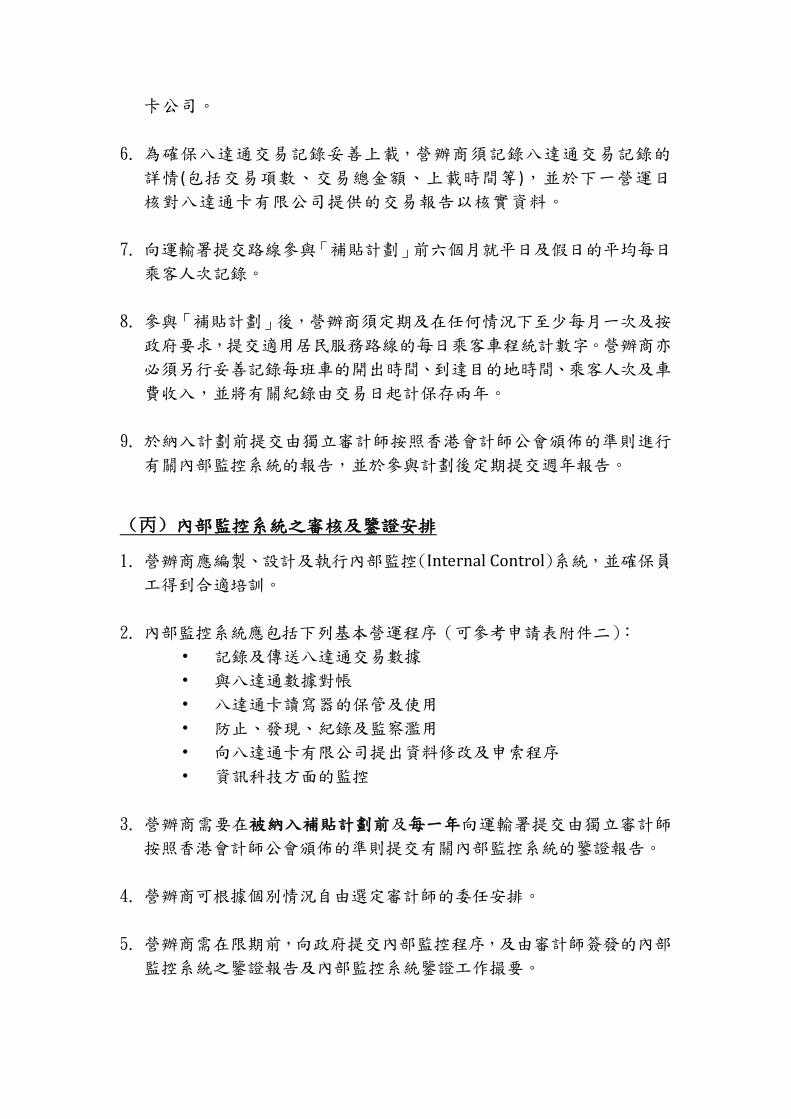

5. 在完成交易後七天內,將其收費系統收集的交易數據上傳至八達通

卡公司。

6. 為確保八達通交易記錄妥善上載,營辦商須記錄八達通交易記錄的

詳情(包括交易項數、交易總金額、上載時間等),並於下一營運日

核對八達通卡有限公司提供的交易報告以核實資料。

7. 向運輸署提交路線參與「補貼計劃」前六個月就平日及假日的平均每日

乘客人次記錄。

8. 參與「補貼計劃」後,營辦商須定期及在任何情況下至少每月一次及按

政府要求,提交適用居民服務路線的每日乘客車程統計數字。營辦商亦

必須另行妥善記錄每班車的開出時間、到達目的地時間、乘客人次及車

費收入,並將有關紀錄由交易日起計保存兩年。

9. 於納入計劃前提交由獨立審計師按照香港會計師公會頒佈的準則進行

有關內部監控系統的報告,並於參與計劃後定期提交週年報告。

(丙)內部監控系統之審核及鑒證安排

1. 營辦商應編製、設計及執行內部監控(Internal Control)系統,並確保員

工得到合適培訓。

2. 內部監控系統應包括下列基本營運程序(可參考申請表附件二):

• 記錄及傳送八達通交易數據

• 與八達通數據對帳

• 八達通卡讀寫器的保管及使用

• 防止、發現、紀錄及監察濫用

• 向八達通卡有限公司提出資料修改及申索程序

• 資訊科技方面的監控

3. 營辦商需要在被納入補貼計劃前及每一年向運輸署提交由獨立審計師

按照香港會計師公會頒佈的準則提交有關內部監控系統的鑒證報告。

4. 營辦商可根據個別情況自由選定審計師的委任安排。

5. 營辦商需在限期前,向政府提交內部監控程序,及由審計師簽發的內部

監控系統之鑒證報告及內部監控系統鑒證工作撮要。

(丁)注意事項

1. 參與「補貼計劃」後,如營辦商獲批准更改服務詳情表所載列的項目(如

車輛、時間表等),請填寫預先設定的表格,並遞交給運輸署及八達通

公司,以便更新記錄。

2. 參與「補貼計劃」後,如營辦商獲批准更改收費表,請填寫更改收費表

表格,並遞交運輸署,經運輸署批核後,再交與八達通卡有限公司進行

收費表更新。八達通卡有限公司需時最少 5個工作天作收費表修改,而

營辦商須預留足夠時間下載及更新相關資料。

3. 收取已參與「補貼計劃」路線的車費時,必須使用一個獨立的八達

通商户編號及一部獨立的八達通卡讀寫器。在提供並未參與「補貼

計劃」的服務時(如﹕合約式出租服務、過境巴士服務或學生服務) ,

必須使用不同的八達通商户編號及八達通卡讀寫器,或以其他途徑

收取車費(如現金)。

4. 營辦商亦需要預留足夠時間申請八達通卡讀寫器,並盡快與八達通卡有

限公司安排進行安裝,以完成審核及鑒證程序。

表格

(第 頁,共 頁)

郵寄或傳真(傳真號碼:3525 0040)

致: 九龍油麻地海庭道 11 號西九龍政府合署南座 11 樓

運輸署渡輪及輔助客運部

公共交通費用補貼計劃組

「公共交通費用補貼計劃」

(下稱「補貼計劃」)

加入補貼計劃申請表

本*公司/人

(公司名稱/申請人姓名: ___________________________

將參與「補貼計劃」並提交申請表及所列資料。本*公司 /人同意八

達通卡有限公司 (下稱「八達通」 )向運輸署提供本營辦商及聯營伙

伴在「八達通」登記之提供居民服務的非專營巴士路線的相關資

料,以便政府作進一步處理有關路線加入補貼計劃之用。本*公司 /

人明白運輸署保留批准各路線參與補貼計劃的權利,遞交此申請表

並不代表申請成功。若申請成功,本*公司 /人同意運輸署根據申請

表及附件所填寫的資料準備「補貼計劃」的協議文件及作該協議的

簽訂安排。

承諾遵守運輸署所批准及規定的營運細節

本*公司/人承諾遵守運輸署批准的客運營業證及其夾附的服務詳情表及

經營有關服務條件的規定。本*公司/人明白,如果本*公司/人未能遵守

上述規定,運輸署可對本*公司/人發出警告信,甚至可以暫時或永久禁

止本*公司/人名下路線參與補貼計劃。

*請刪去不適用者

PTFSS: RS (2019/07)

機密

(第 頁,共 頁)

第一部分-基本資料

英文 中文

營辦商名稱

[註:必須為公司註冊證書

(適用於有限公司)/商業登記

證(適用於合夥經營 /個人名

義經營) 上的名稱]

註冊辦事處地址

[註:必須為周年申報表(適

用於有限公司)/商業登記證

(適用於合夥經營 /個人名義

經營) 上的地址]

客運營業證號碼

客運營業證名稱

八達通商戶編號(SPID)

(若未有八達通商戶編號

SPID,請填寫向八達通公

司申請的日期)

八達通商戶名稱(如有)

通訊地址

經辦人 Attent ion:

*Mr./Miss./Ms.

*先生 /小姐 /女士

聯絡電話

電郵地址

傳真號碼

*請刪去不適用者

(第 頁,共 頁)

第二部分 : (授權)簽署人 (Authorised Signatory)資料

如營辦商以有限公司或合夥形式經營,請填寫(A)部份。

如營辦商以個人名義作商業登記,請填寫(B)部份。

(A)只適用於有限公司或合夥經營

本公司現委任下列*經理 /董事 /職員代表本公司與政府簽訂「補貼計

劃」的協議。營辦商須同時隨本申請表夾附相關董事會會議記錄證

明下列*經理 /董事 /職員已於董事會獲授權代表本公司簽訂協議,其

個人資料如下:

英文 中文

姓名:

Name:

*Mr./Miss./Ms.

*先生 /小姐 /女士

職銜:

Post:

聯絡電話:

Tel. No.:

*請刪去不適用者

(B)只適用於以個人名義作商業登記

本人將與政府簽訂「補貼計劃」的協議,本人個人資料如下:

英文 中文

姓名:

Name:

*Mr./Miss./Ms.

*先生 /小姐 /女士

職銜:

Post:

聯絡電話:

Tel. No.:

*請刪去不適用者

請蓋上公司印章

(第 頁,共 頁)

第三部分 :見證人 (Witness)資料

此部分將於運輸署接納其申請後,用以處理協議之用。

本*公司 /人現委任下列人士作為本 *公司 /人與政府簽訂「補貼計

劃」協議的見證人,其個人資料如下:

英文 中文

姓名:

Name:

*Mr./Miss./Ms.

*先生 /小姐 /女士

職銜:

Post:

聯絡電話:

Tel. No.:

*請刪去不適用者

第四部分-證明文件

本*公司/人現提交以下證明文件副本:

1 客運營業證-提供居民服務的非專營巴士服務

2

- 公司註冊證書

- 商業登記證

- 最近年度之周年申報表

(如以個人名義營運,只需提供有效的商業登記證)

3 由「八達通」發出的「八達通商戶資料確認書」 (如有),提供本

*公司/人在「八達通」的開戶資料

4 客運營業證下的所有路線的服務詳情表

*請刪去不適用者

(如見證人為公司,請蓋上公司印章)

(第 頁,共 頁)

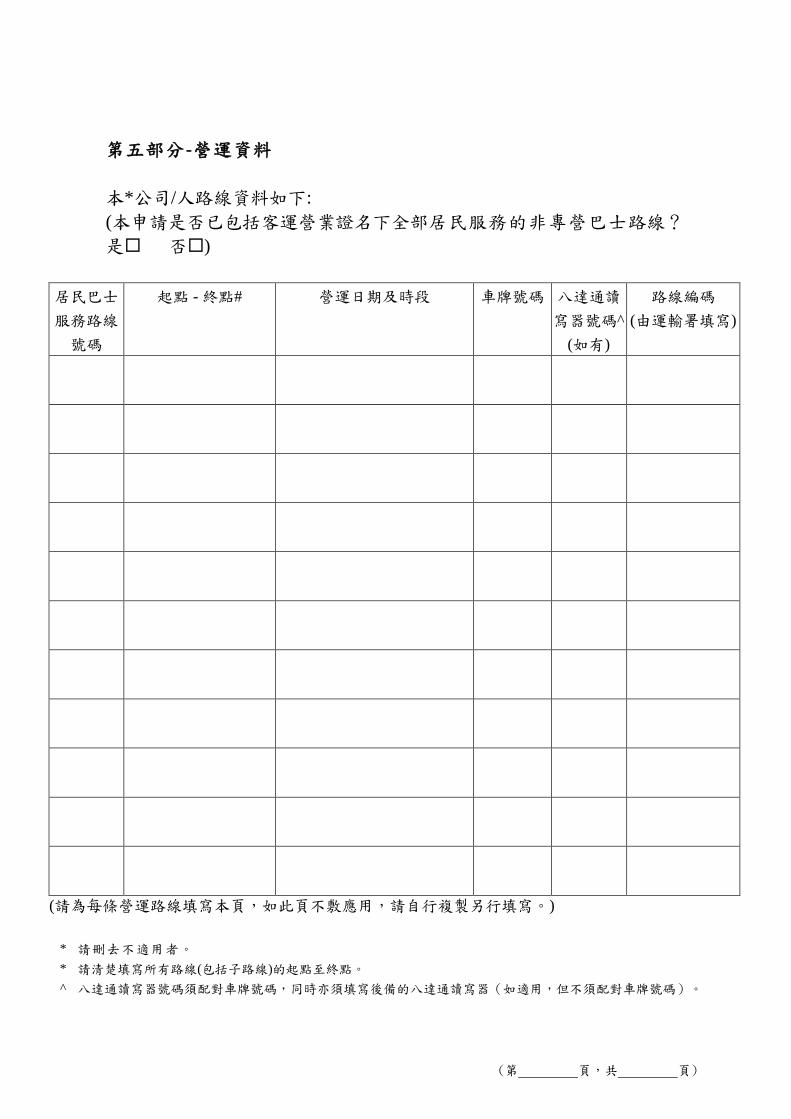

第五部分-營運資料

本*公司/人路線資料如下:

(本申請是否已包括客運營業證名下全部居民服務的非專營巴士路線?

是 否)

居民巴士

服務路線

號碼

起點 - 終點# 營運日期及時段 車牌號碼 八達通讀

寫器號碼^

(如有)

路線編碼

(由運輸署填寫)

(請為每條營運路線填寫本頁,如此頁不敷應用,請自行複製另行填寫。)

* 請刪去不適用者。

* 請清楚填寫所有路線(包括子路線)的起點至終點。

^ 八達通讀寫器號碼須配對車牌號碼,同時亦須填寫後備的八達通讀寫器(如適用,但不須配對車牌號碼)。

(第 頁,共 頁)

第五部分-營運資料(收費表)

本*公司/人營辦的每條路線收費表資料如下 :

營辦商名稱:

八達通商戶編號(SPID)

居民巴士服務路線號碼:

起點 - 終點:

包括的所有路線編碼:

(由運輸署填寫)

收費詳情 成人 長者 學生 小童 殘疾人士

全費

(雙向分段收費)#

分段收費

(雙向分段收費)#

分段收費

(雙向分段收費)#

分段收費

(雙向分段收費)#

分段收費

(雙向分段收費)#

分段收費

(雙向分段收費)#

分段收費

(雙向分段收費)#

#:請以括號填寫雙向分段收費

(如此頁不敷應用,請自行複製及另行填寫。)

營辦商簽署及蓋印

(第 頁,共 頁)

第六部分- 每日平均人次(每條路線填寫一份)

本*公司/人現提交各路線過去六個月就平日及假日的每日平均人次的記

錄:

居民巴士服務

路線號碼: 路線(起點 - 終點):

月份 平日的每日平均人次

(星期一至五)

假日的每日平均人次

(星期六、日及公眾假期)

(如此頁不敷應用,請自行複製另行填寫。)

*請刪去不適用者

(第 頁,共 頁)

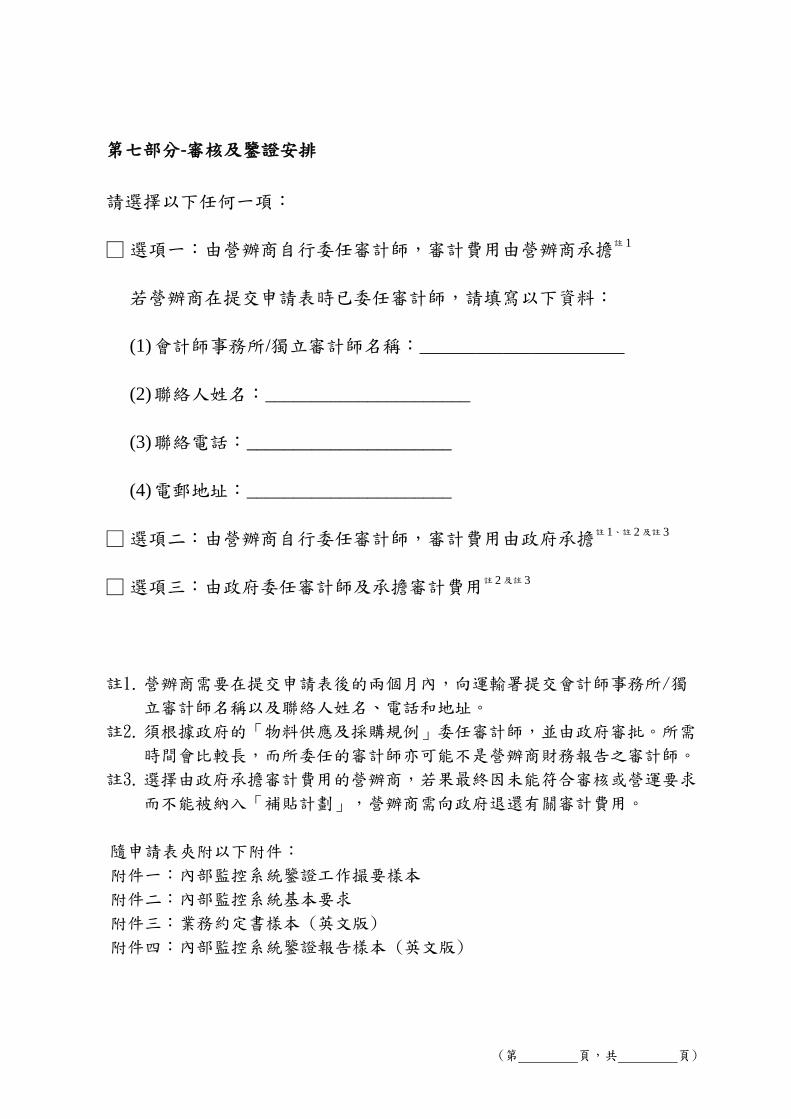

第七部分-審核及鑒證安排

請選擇以下任何一項:

□ 選項一:由營辦商自行委任審計師,審計費用由營辦商承擔註 1

若營辦商在提交申請表時已委任審計師,請填寫以下資料:

(1) 會計師事務所/獨立審計師名稱:______________________

(2) 聯絡人姓名:______________________

(3) 聯絡電話:______________________

(4) 電郵地址:______________________

□ 選項二:由營辦商自行委任審計師,審計費用由政府承擔註 1、註 2 及註 3

□ 選項三:由政府委任審計師及承擔審計費用註 2 及註 3

註1. 營辦商需要在提交申請表後的兩個月內,向運輸署提交會計師事務所/獨

立審計師名稱以及聯絡人姓名、電話和地址。

註2. 須根據政府的「物料供應及採購規例」委任審計師,並由政府審批。所需

時間會比較長,而所委任的審計師亦可能不是營辦商財務報告之審計師。

註3. 選擇由政府承擔審計費用的營辦商,若果最終因未能符合審核或營運要求

而不能被納入「補貼計劃」,營辦商需向政府退還有關審計費用。

隨申請表夾附以下附件:

附件一:內部監控系統鑒證工作撮要樣本

附件二:內部監控系統基本要求

附件三:業務約定書樣本 (英文版)

附件四:內部監控系統鑒證報告樣本 (英文版)

(第 頁,共 頁)

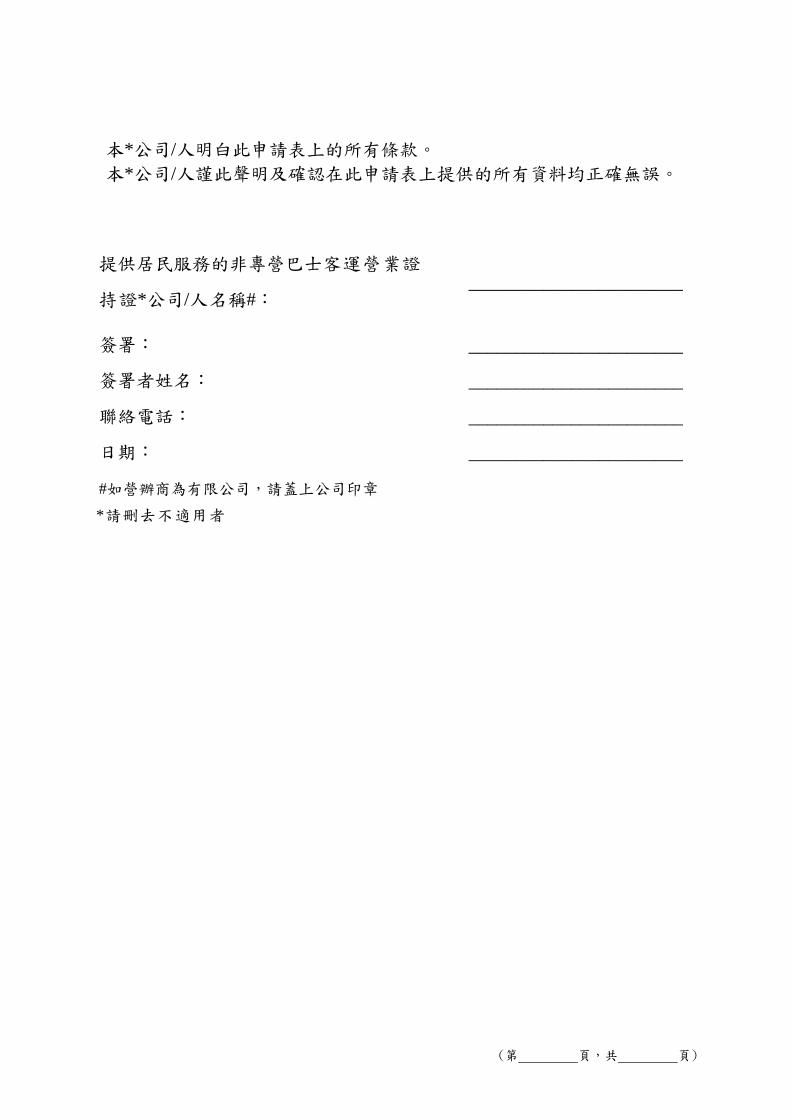

本*公司/人明白此申請表上的所有條款。

本*公司/人謹此聲明及確認在此申請表上提供的所有資料均正確無誤。

提供居民服務的非專營巴士客運營業證

持證*公司/人名稱#:

_______________________

簽署: _______________________

簽署者姓名: _______________________

聯絡電話: _______________________

日期: _______________________

#如營辦商為有限公司,請蓋上公司印章

*請刪去不適用者

(第 頁,共 頁)

認 收 申 請 表

我們收到 *貴公司/你申請加入「公共交通費用補貼計劃」的申請

表,現正詳加審閱。若我們需要進一步資料,則會另行發信與 *貴公司/

你聯絡。

營辦商名稱:

經辦人:

傳真號碼:

申請編號:

(由運輸署填寫)

------------------------------------------------------------------------------------------------

申 請 書 覆 函

我們收到 *貴公司/你申請加入「公共交通費用補貼計劃」的申請

表,現確認*貴公司/你填妥及提交相關資料及證明文件予運輸署。另

外,請 *貴公司/你 於三個月內提交內部監控程序及內部監控系統之鑒證

報告的初稿供本署審閱。

營辦商名稱:

經辦人:

傳真號碼:

申請編號:

(由運輸署填寫)

____________________

(運輸署蓋印及日期)

____________________

(運輸署蓋印及日期)

回郵地址(必須填寫地址)

營辦商名稱:

地 址:

營辦商名稱:

地 址:

附件一

For assurance of the system of internal controls of [Name of Public Transport Operator] under the

Public Transport Fare Subsidy Scheme as of [Date]

有關 [營辦商名稱 ]就公共交通費用補貼計劃的內部監控系統鑒證(截至 [日期 ])

[Name of Public Transport Operator]

[營辦商名稱 ]

[Auditor]

[核數師 ]

Control Process

監控過程

Control Objectives

監控目的

Control Description

內部監控說明

Assurance Work Procedures

鑒證工作

附件二

內部監控程序的基本要求

邨巴/員工巴士營辦商提交的內部監控程序,需包括以下基本要求,並就相關要

求製定監控目的及內部監控說明:

1. 記錄及傳送八達通交易數據

a) 營辦商定時(不多於 7天)收集及上傳有關八達通交易數據。

b) 如使用八達通進行涉及「補貼計劃」的測試,營辦商須於有關測試進行不少於

7天前通知運輸署並在完成測試後儘快向運輸署遞交有關記錄。另於每年年結

後一個月內,負責職員須向運輸署遞交有關測試的全年記錄。

2. 八達通數據對帳

a) 營辦商確保上傳八達通數據後,與八達通卡有限公司提供的報表與上數記錄作

對帳。

b) 營辦商核對八達通報表後,並與銀行的入帳記錄作比對,確保所有款項收取無

誤。

3. 八達通讀寫器的保管及使用

a) 所使用的八達通讀寫器會妥善地存放於上鎖的邨巴/員工巴士或房間内,避免

遺失,只有授權人仕才能提取。

b) 如該行車路線/時段不受「補貼計劃」覆蓋,司機應以機套遮蓋「補貼計劃」

的八達通讀寫器。

c) 每部邨巴/員工巴士所安裝的八達通讀寫器機身編號及所有備用八達通讀寫器

機身編號會完整地按車牌編號或存放地點記錄在「八達通讀寫器記錄冊」中。

如有新增、減少或更換,必須事先向運輸署登記才交付八達通卡有限公司跟進,

並於完成後相應地更新「八達通讀寫器記錄冊」。

d) 當有需要更換八達通讀寫器的情況時,營辦商應確保新更換之八達通讀寫器(例

如後備八達通讀寫器)適當地完成軟件更新後及確保有關八達通讀寫器所載入

的路線收費表正確無誤後才安裝到邨巴/員工巴士上使用。

e) 有關的更換應得到營辦商適當授權職員的批准及清楚記錄。

4. 防止、發現、監察、記錄及報告濫用的程序

a) 營辦商給予邨巴司機及相關員工有關培訓和指引,包括要求司機記錄每班車的

乘客人次。有關數據需要每月提交及運輸署審閱。

b) 每月就八達通卡有限公司提供的按月報表資料,與之前/同期月份作出比對,

避免有濫用計劃的情況發生。如發現有任何不尋常的變動,需立刻通知運輸署。

c) 每月按司機記錄的載客量記錄表、班次、車輛數目跟八達通卡有限公司提供的

報表資料作出比對,避免有濫用計劃的情況發生。如發現有任何不尋常的變動,

必須立刻通知運輸署。

5. 向八達通卡有限公司提出資料修改及申索的程序

a) 如有有關路線收費表、客運營業證及路線或營辦商於八達通登記的商戶資料更

附件二

改,在得到運輸署批核或向運輸署登記後,按時填妥有關表格向八達通卡有限

公司提出更改申請。

b) 如發現有遲報交易、數據遺失或數據差異等情況時,按程序填妥有關表格連同

有關證明文件向八達通卡有限公司提出申索,並確保有關申索得到妥善處理及

收回有關款項。

c) 專責的職員應記錄向八達通卡有限公司提出涉及計劃的申索,並查明原因,在

有需要時檢討相關程序以減少申索處理之情況及風險。

6. 資訊科技方面的監控

a) 每輛邨巴/員工巴士都會定時回車房給專業維修人士檢查八達通讀寫器是否運

作正常,有關負責職員亦需不時聯絡八達通卡有限公司查詢是否所有軟件已被

妥善更新。

b) 當職員在每次使用掌上電腦完成收集交易數據後都會將該掌上電腦放回上鎖的

房間内。該房間只有授權人仕能夠進入。

c) 有關補貼計劃的資料應被妥善保存及根據運輸署及有關法例要求備份。

d) 所有相關文件及資料都應保密存取,只有特定的職員才有權限存取相關資料。

1

附件三

(Note: This document is for illustrative purpose only and shall be refined to suit auditor’s engagement. No responsibility shall be borne by the HKSAR Government for your reference to this document.)

System of Internal Controls – Engagement Letter

Pro-forma

Private and confidential

[Company Name] (“the Company”)

Public Transport Fare Subsidy Scheme – System of Internal Controls of the Company

relating to the Recording of Public Transport Expense

Engagement Letter

1. Introduction

The purpose of this letter is to confirm our mutual understanding of the terms of your

engagement with us in connection with the Public Transport Fare Subsidy Scheme (“Fare

Subsidy Scheme”) to offer a non-means tested subsidy that Octopus users whose monthly

public transport expenses exceed HK$400 will be entitled to a subsidy amounting to 25

per cent of the actual public transport expenses in excess of HK$400, subject to a cap of

HK$300 a month. We understand that the purpose of our engagement is to report on

assurance of the system of internal controls of the Company relating to the recording of

Public Transport Expense under the Fare Subsidy Scheme and report accordingly to the

Government of the Hong Kong Special Administrative Region as represented by the

Commissioner for Transport (“the HKSAR Government”). We confirm that we would be

pleased to act for you in this matter on the terms set out below.

2. Scope of Our Work

(a) Our scope of work is to conduct our engagement in accordance with Hong Kong Standard

on Assurance Engagements 3000 (Revised) “Assurance Engagements Other Than Audits

or Reviews of Historical Financial Information” (“HKSAE 3000 (Revised)”) issued by

the Hong Kong Institute of Certified Public Accountants (“HKICPA”). This standard

requires that we comply with the requirements of the Code of Ethics for Professional

Accountants, including independence and other ethical requirements, issued by the

HKICPA, and implement quality control procedures that are applicable to the individual

engagement in accordance with the requirements of Hong Kong Standard on Quality

Control 1 “Quality Control for Firms that Perform Audits and Reviews of Financial

Statements, and Other Assurance and Related Services Engagements” and plan and

perform our engagement to obtain reasonable assurance about whether the system of

internal controls as described by the Company relating to the recording of Public

Transport Expense under the Fare Subsidy Scheme (“Controls Description”) (the relevant

independent assurance report is referred to hereinafter as the “Internal Control Report”),

is effective, in all material respects, to achieve the related control objectives (“the Control

Objectives”) as set out in the Controls Description of the Company as of the date of the

Internal Control Report based on the work to be performed as summarised in Annex A to

the Internal Control Report.

2

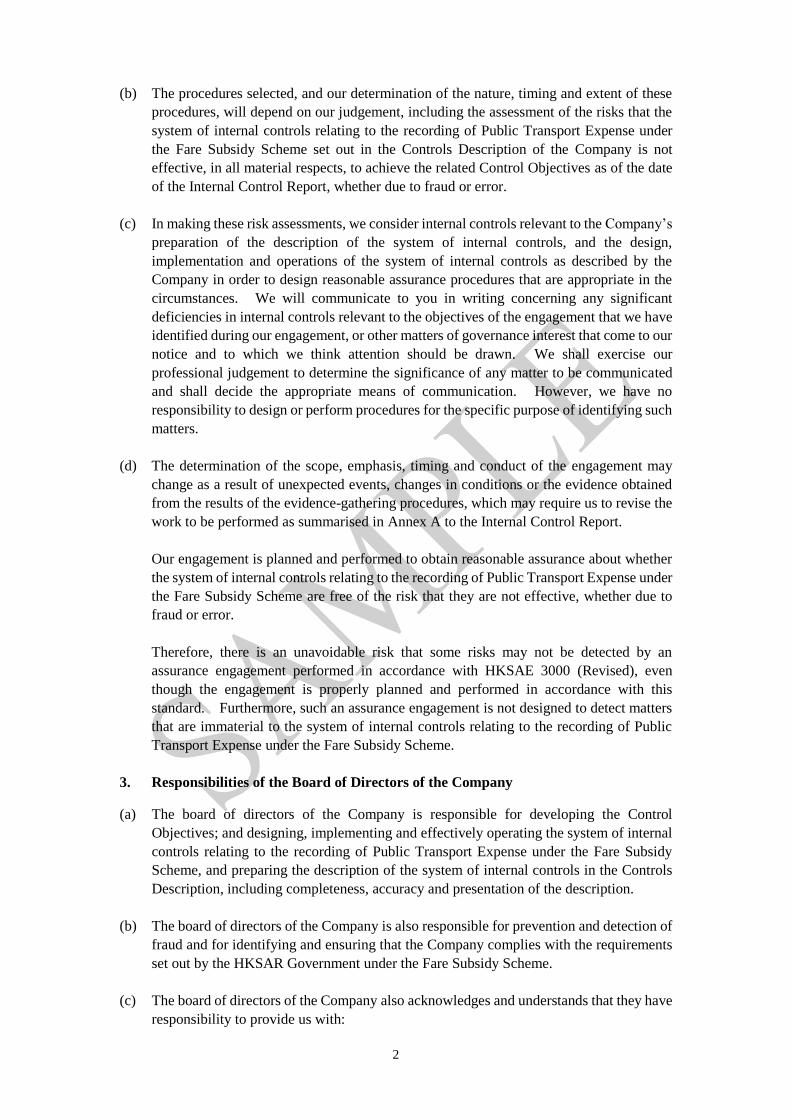

(b) The procedures selected, and our determination of the nature, timing and extent of these

procedures, will depend on our judgement, including the assessment of the risks that the

system of internal controls relating to the recording of Public Transport Expense under

the Fare Subsidy Scheme set out in the Controls Description of the Company is not

effective, in all material respects, to achieve the related Control Objectives as of the date

of the Internal Control Report, whether due to fraud or error.

(c) In making these risk assessments, we consider internal controls relevant to the Company’s

preparation of the description of the system of internal controls, and the design,

implementation and operations of the system of internal controls as described by the

Company in order to design reasonable assurance procedures that are appropriate in the

circumstances. We will communicate to you in writing concerning any significant

deficiencies in internal controls relevant to the objectives of the engagement that we have

identified during our engagement, or other matters of governance interest that come to our

notice and to which we think attention should be drawn. We shall exercise our

professional judgement to determine the significance of any matter to be communicated

and shall decide the appropriate means of communication. However, we have no

responsibility to design or perform procedures for the specific purpose of identifying such

matters.

(d) The determination of the scope, emphasis, timing and conduct of the engagement may

change as a result of unexpected events, changes in conditions or the evidence obtained

from the results of the evidence-gathering procedures, which may require us to revise the

work to be performed as summarised in Annex A to the Internal Control Report.

Our engagement is planned and performed to obtain reasonable assurance about whether

the system of internal controls relating to the recording of Public Transport Expense under

the Fare Subsidy Scheme are free of the risk that they are not effective, whether due to

fraud or error.

Therefore, there is an unavoidable risk that some risks may not be detected by an

assurance engagement performed in accordance with HKSAE 3000 (Revised), even

though the engagement is properly planned and performed in accordance with this

standard. Furthermore, such an assurance engagement is not designed to detect matters

that are immaterial to the system of internal controls relating to the recording of Public

Transport Expense under the Fare Subsidy Scheme.

3. Responsibilities of the Board of Directors of the Company

(a) The board of directors of the Company is responsible for developing the Control

Objectives; and designing, implementing and effectively operating the system of internal

controls relating to the recording of Public Transport Expense under the Fare Subsidy

Scheme, and preparing the description of the system of internal controls in the Controls

Description, including completeness, accuracy and presentation of the description.

(b) The board of directors of the Company is also responsible for prevention and detection of

fraud and for identifying and ensuring that the Company complies with the requirements

set out by the HKSAR Government under the Fare Subsidy Scheme.

(c) The board of directors of the Company also acknowledges and understands that they have

responsibility to provide us with:

3

i. a description of the system of internal controls relating to the recording of Public

Transport Expense under the Fare Subsidy Scheme;

ii. access to all information of which the Company is aware that is relevant to the

preparation of the description of the system of internal controls relating to the

recording of Public Transport Expense under the Fare Subsidy Scheme such as

records, source documentation and other matters;

iii. additional information that we may request from the Company for the purpose of the

engagement; and

iv. unrestricted access to persons within the Company from whom we determine it

necessary to obtain evidence.

4. Reporting

(a) Our report will be addressed to the HKSAR Government. We do not assume

responsibility towards or accept liability to any other person for the contents of our

Internal Control Report. The pro-forma of the Internal Control Report and the Summary

of Assurance Work Procedures on the System of Internal Controls are attached as

Attachment 1 and Attachment 2 to this letter respectively. The form and content of our

report may be amended in light of our findings.

(b) The Company shall inform us any material event occurring between the date of our report

and that of submission of the report to the HKSAR Government which may affect the

system of internal controls.

(c) We understand that the report is intended solely for the purpose of assisting the Company

in respect of its reporting obligations to the HKSAR Government with respect to the Fare

Subsidy Scheme. Our report is not intended to be, and should not be, relied upon or used

for any other purpose and we expressly disclaim any liability or duty to any other party in

this respect.

(d) Our report should not be disclosed, referred to or quoted in whole or in part, or distributed

to any other parties without our prior written consent, save that we agree that, in addition

to the HKSAR Government, a copy of our report will be provided to you without further

comment from us.

5. Applicable Criteria

(a) The system of internal controls is effective, suitably designed and operating effectively,

if: (i) the Company has identified the risks that threaten achievement of the Control

Objectives stated in the Controls Description; (ii) the system of internal controls set out

in the Controls Description would, if operated as described, provide reasonable assurance

that those risks do not prevent the stated Control Objectives from being achieved; and (iii)

the controls are to be consistently applied as designed. This includes whether manual

controls are applied by individuals who have the appropriate competence and authority.

The Control Objectives have been internally developed by the Company.

(b) The assurance report we provide will note these characteristics, as they are of particular

relevance to the intended users.

4

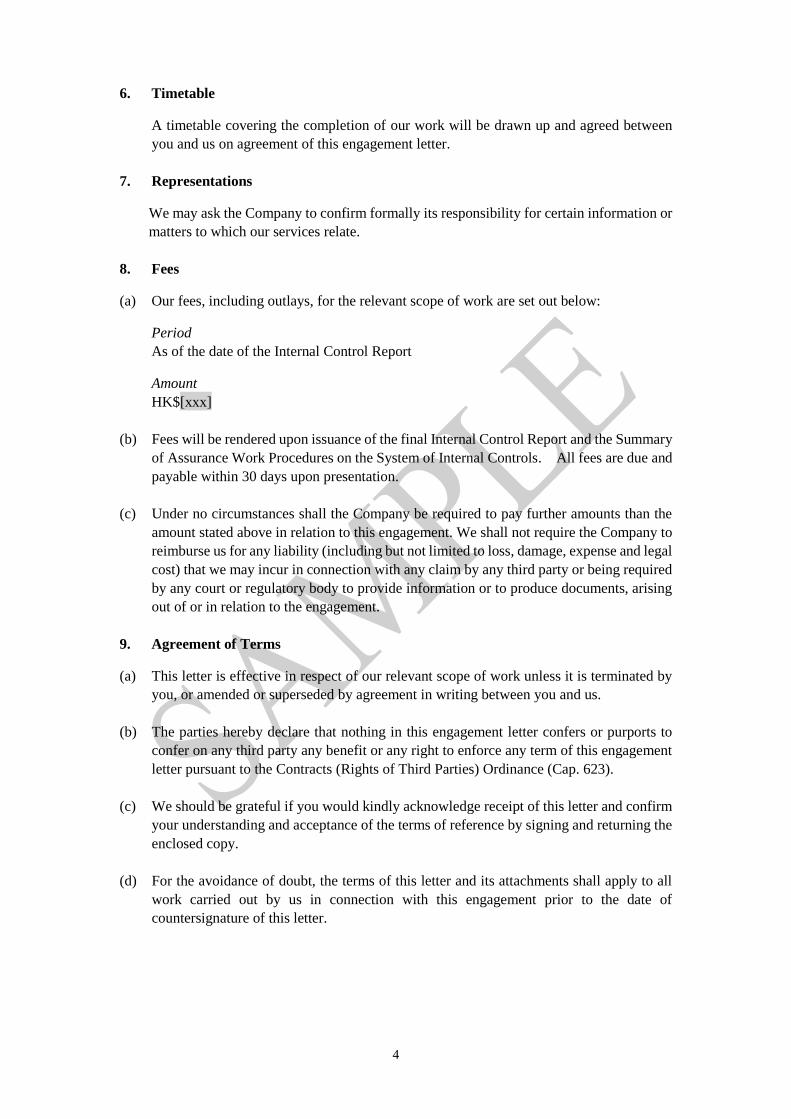

6. Timetable

A timetable covering the completion of our work will be drawn up and agreed between

you and us on agreement of this engagement letter.

7. Representations

We may ask the Company to confirm formally its responsibility for certain information or

matters to which our services relate.

8. Fees

(a) Our fees, including outlays, for the relevant scope of work are set out below:

Period

As of the date of the Internal Control Report

Amount

HK$[xxx]

(b) Fees will be rendered upon issuance of the final Internal Control Report and the Summary

of Assurance Work Procedures on the System of Internal Controls. All fees are due and

payable within 30 days upon presentation.

(c) Under no circumstances shall the Company be required to pay further amounts than the

amount stated above in relation to this engagement. We shall not require the Company to

reimburse us for any liability (including but not limited to loss, damage, expense and legal

cost) that we may incur in connection with any claim by any third party or being required

by any court or regulatory body to provide information or to produce documents, arising

out of or in relation to the engagement.

9. Agreement of Terms

(a) This letter is effective in respect of our relevant scope of work unless it is terminated by

you, or amended or superseded by agreement in writing between you and us.

(b) The parties hereby declare that nothing in this engagement letter confers or purports to

confer on any third party any benefit or any right to enforce any term of this engagement

letter pursuant to the Contracts (Rights of Third Parties) Ordinance (Cap. 623).

(c) We should be grateful if you would kindly acknowledge receipt of this letter and confirm

your understanding and acceptance of the terms of reference by signing and returning the

enclosed copy.

(d) For the avoidance of doubt, the terms of this letter and its attachments shall apply to all

work carried out by us in connection with this engagement prior to the date of

countersignature of this letter.

5

Enclosures:

Attachment 1 – Pro-forma Internal Control Report and Annexes

Attachment 2 – Pro-forma Summary of Assurance Work Procedures on the System of Internal

Controls

I have read and understood the terms and conditions of this letter and attachment and I agree to

and accept them.

For and on behalf of

[Auditor]

For and on behalf of

[Company Name]

Name : [xxx] Name : [xxx]

Position : [xxx] Position : [xxx]

Date : [xxx] Date : [xxx]

Note to Operators 備註

Operators shall submit the pre-implementation assurance report according to the timeline as

requested by the Government before joining the Scheme. The post-implementation assurance

report shall be submitted according to the reporting period as agreed between the Company and

the HKSAR Government

在加入「優惠計劃」前,營辦商須在政府要求之限期前提交首份內部監控系統之鑒證報

告。在加入「優惠計劃」後,營辦商須根據與政府約定之報告期於每年提交周年報告。

1

附件四

(Note: This document is for illustrative purpose only and shall be refined to suit auditor’s engagement. No responsibility shall be borne by the HKSAR Government for your reference to this document.)

Attachment 1

System of Internal Controls – Auditor’s Report

Pro-forma

Independent Assurance Report to the Government of the Hong Kong Special

Administrative Region as represented by the Commissioner for Transport (“the HKSAR

Government”) regarding the System of Internal Controls of [Company Name] (“the

Company”) relating to the Recording of Public Transport Expense under the Public

Transport Fare Subsidy Scheme (“the Fare Subsidy Scheme”) as of [Date]

We have been engaged by the Company to provide a reasonable assurance conclusion on

whether the system of internal controls as described by the Company set out in Annex B relating

to the recording of Public Transport Expense under the Fare Subsidy Scheme (“the Controls

Description”) was effective, in all material respects, to achieve the related control objectives

(“the Control Objectives”) set out in the Controls Description as of [Date], based on the work

performed as summarised in Annex A.

Responsibilities of the Board of Directors of the Company

The board of directors of the Company is responsible for developing the Control Objectives of

the system of internal controls relating to the recording of Public Transport Expense under the

Fare Subsidy Scheme in accordance with the requirements set out by the HKSAR Government

under the Fare Subsidy Scheme; designing, implementing and effectively operating controls to

achieve the related Control Objectives; and preparing the description of the system of internal

controls in the Controls Description, including the completeness, accuracy and presentation of

the description.

The board of directors of the Company is responsible for preventing and detecting fraud and for

identifying and ensuring that the Company complies with the requirements set out by the

HKSAR Government under the Fare Subsidy Scheme.

The board of directors of the Company is also responsible for ensuring that staff involved in the

system of internal controls relating to the recording of Public Transport Expense is properly

trained and the related information systems are properly updated.

Our Independence and Quality Control

We have complied with the independence and other ethical requirements of the Code of Ethics

for Professional Accountants issued by the Hong Kong Institute of Certified Public Accountants

(the “HKICPA”), which is founded on fundamental principles of integrity, objectivity,

professional competence and due care, confidentiality and professional behavior.

2

Our firm applies Hong Kong Standard on Quality Control 1 and, accordingly, maintains a

comprehensive system of quality control including documented policies and procedures

regarding compliance with ethical requirements, professional standards and applicable legal

and regulatory requirements.

Our Responsibilities

Our responsibility is to carry out a reasonable assurance engagement and to express an opinion

on the system of internal controls as stated in the Controls Description, based on our work

performed. We conducted our reasonable assurance engagement in accordance with Hong Kong

Standard on Assurance Engagements 3000 (Revised) “Assurance Engagements Other Than

Audits or Reviews of Historical Financial Information” issued by the HKICPA. That standard

requires that we plan and perform our work to form the opinion.

A reasonable assurance engagement involves performing procedures to obtain sufficient

appropriate evidence whether the system of internal controls relating to the recording of Public

Transport Expense as set out in the Controls Description, was effective, in all material respects,

to achieve the related Control Objectives as of [Date] based on the work performed as

summarised in Annex A.

Procedures Performed

The procedures selected depend on our judgement, including the assessment of the risks that the

system of internal controls relating to the recording of Public Transport Expense under the Fare

Subsidy Scheme set out in the Controls Description is not effective, in all material respects, to

achieve the related Control Objectives as of [Date], whether due to fraud or error.

In making the above risk assessments, we have considered the internal controls relevant to the

preparation of the Controls Description, and the design, implementation and operations of the

system of internal controls relating to the recording of Public Transport Expense in accordance

with the Company’s description in order to design reasonable assurance procedures that are

appropriate in the circumstances. Our procedures included testing the operating effectiveness of those controls that we consider

necessary to provide reasonable assurance that the Control Objectives stated in the Controls

Description were achieved; and evaluating the suitability of the Control Objectives stated

therein.

We believe that the evidence we have obtained is sufficient and appropriate to provide a basis

for our opinion.

Historic evaluation of the operation of an internal control system may not be relevant to future

periods if there is a change in conditions or that the degree of compliance with the Company’s

policies and procedures may deteriorate. Also, because of their nature, controls at the

Company may not prevent or detect all errors or omissions in processing or reporting

transactions.

3

Criteria

The system of internal controls is effective, suitably designed and operating effectively, if: (a)

the Company has identified the risks that threaten achievement of the Control Objectives stated

in the Controls Description; (b) the system of internal controls set out in the Controls Description

would, if operated as described, provide reasonable assurance that those risks do not prevent the

stated Control Objectives from being achieved; and (c) the controls are to be applied as designed.

This includes whether manual controls are applied by individuals who have the appropriate

competence and authority. The Control Objectives have been internally developed by the

Company.

Conclusion

In our opinion, the system of internal controls relating to the recording of Public Transport

Expense set out in the Controls Description was effective, in all material respects, to achieve the

related Control Objectives as of [Date], based on the work performed as summarised in Annex

A.

Use of This Report

This report is intended solely for the purpose of expressing a reasonable assurance conclusion

on whether the system of internal controls relating to the recording of Public Transport Expense

was effective, in all material respects, based on the work performed as set out in Annex A, as of

[Date]. This report is not intended to be, and should not be, relied upon or used for any other

purpose and we expressly disclaim any liability or duty to any party.

Other than as set out in the agreed terms of engagement between the Company and us, this report

should not be disclosed, referred to or quoted in whole or in part, or distributed to any other

parties without our prior written consent.

[Auditor]

Certified Public Accountants

Hong Kong

[Date]

Annex A : Summary of the Scope of Work Performed on the System of Internal Controls of

[Company Name] (“the Company”) relating to the Recording of Public Transport Expense

under the Public Transport Fare Subsidy Scheme (“the Fare Subsidy Scheme”) as of [Date]

Annex B : System of Internal Controls of [Company Name] (“the Company”) relating to the

Recording of Public Transport Expense under the Public Transport Fare Subsidy Scheme (“the

Fare Subsidy Scheme”) as of [Date]

4

Annex A to Attachment 1

Summary of the Scope of Work Performed on the System of Internal Controls of

[Company Name] (the Company”) relating to the Recording of Public Transport Expense

under the Public Transport Fare Subsidy Scheme (“the Fare Subsidy Scheme”) as of

[Date]

1. Inquire of management on the control objectives relevant to the recording of Public

Transport Expense under the Fare Subsidy Scheme.

2. Assess whether the risks that threaten the achievement of the control objectives are

identified by the Company.

3. Assess whether control procedures with respect to the Fare Subsidy Scheme are properly

established and implemented to achieve the control objectives, taking into consideration

the risks that threaten the achievement of the control objectives.

4. Test the system of internal controls for the recording of Public Transport Expense on a

sampling basis to assess whether the controls were applied as designed to achieve the

control objectives as of [Date].

5

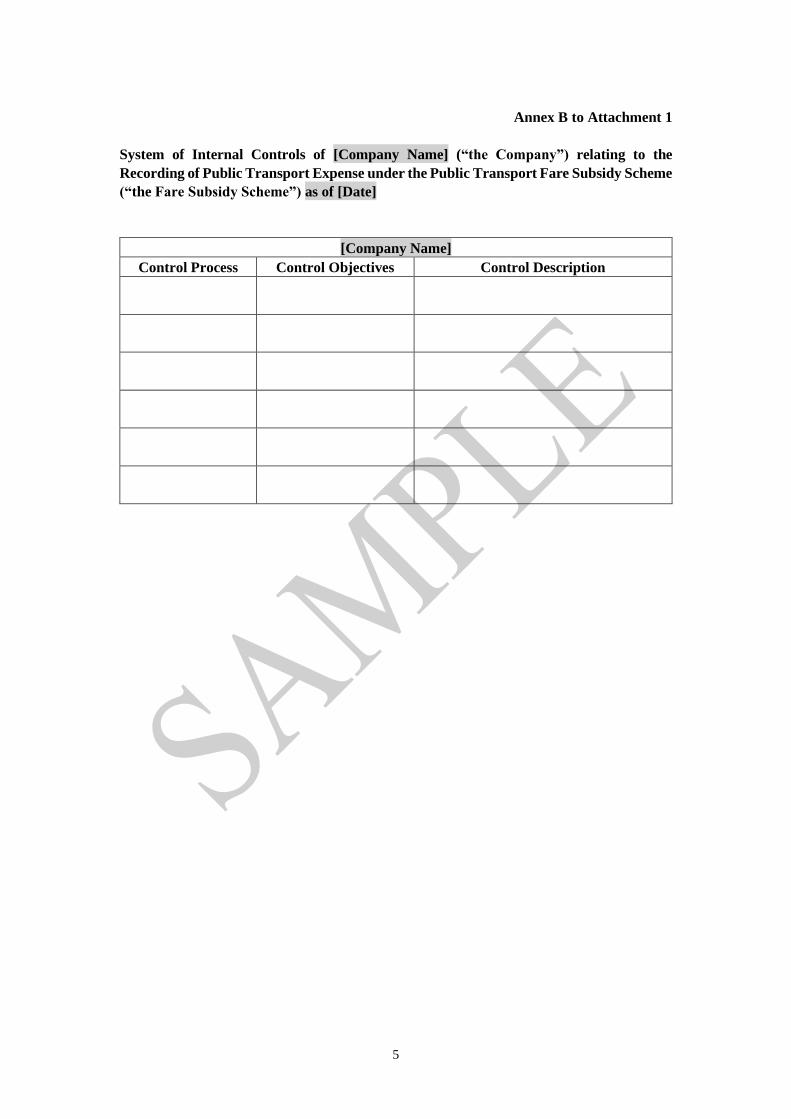

Annex B to Attachment 1

System of Internal Controls of [Company Name] (“the Company”) relating to the

Recording of Public Transport Expense under the Public Transport Fare Subsidy Scheme

(“the Fare Subsidy Scheme”) as of [Date]

[Company Name]

Control Process Control Objectives Control Description

6

Attachment 2

Summary of Assurance Work Procedures on the System of Internal Controls of

[Company Name] (“the Company”) relating to the Recording of Public Transport

Expense under the Public Transport Fare Subsidy Scheme (“the Fare Subsidy Scheme”)

as of [Date]

[Company Name] [Auditor]

Control

Process

Control

Objectives

Control Description Assurance Work Procedures

Related Documents