MICHAEL LIEBREICH SUMMIT KEYNOTE, 5 APRIL 2011 1 / / / / / / / / / / / / / / / / / / / / / / / / / / / / / / / / Michael Liebreich CEO, Bloomberg New Energy Finance Catalysing Investment in Low-Carbon, Climate Resilient Growth OECD Workshop, Paris 7 November 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MICHAEL LIEBREICH SUMMIT KEYNOTE, 5 APRIL 2011 1 / / / / / / / / / / / / / / / / / / / / / / / / / / / / / / / /

Michael Liebreich

CEO, Bloomberg New Energy Finance

Catalysing Investment in Low-Carbon, Climate Resilient Growth

OECD Workshop, Paris

7 November 2011

2 / / / /

AGENDA

2. Clean energy sectoral trends

1. Investment activity

3. Near-term issues

4. Thoughts on solutions

3 / / / /

$52bn

$76bn

$113bn

$151bn

$180bn $186bn

$243bn

48%

48%

34%

19%

4%

30%

2004 2005 2006 2007 2008 2009 2010

GLOBAL TOTAL NEW INVESTMENT IN CLEAN ENERGY

2004–10 ($BN)

Source: Bloomberg New Energy Finance

Note: Includes corporate and government R&D, and small distributed capacity. Adjusted for re-

invested equity. Does not include proceeds from acquisition transactions

4 / / / /

CLEAN VS FOSSIL-BASED GENERATING CAPACITY

INVESTMENT, 2004–10 ($BN)

Source: IEA, EIA, Bloomberg New Energy Finance

Note: Investment for new build – fossil fuel calculated from EIA & IEA numbers, clean energy

taken from Bloomberg New Energy Finance totals. Clean energy capacity includes small

distributed capacity.

Fossil fuel

Clean energy

0

50

100

150

200

250

2004 2005 2006 2007 2008 2009 2010

5 / / / /

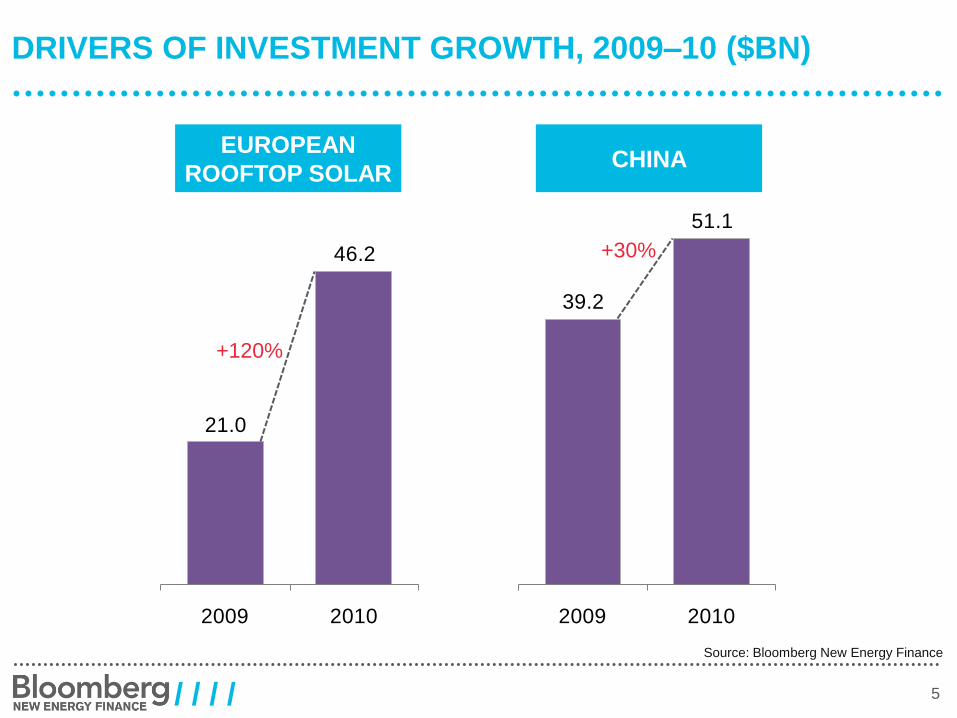

Source: Bloomberg New Energy Finance

DRIVERS OF INVESTMENT GROWTH, 2009–10 ($BN)

CHINA EUROPEAN

ROOFTOP SOLAR

39.2

51.1

2009 2010

21.0

46.2

2009 2010

+120%

+30%

6 / / / /

0.0

0%

20.3

10%

74.5

38% 68

35%

21.4

11%

9.7

5%

2008 2009 2010 2011e 2012e 2013e

GLOBAL CLEAN ENERGY STIMULUS SPENDING BY YEAR,

2011–2013 ($BN)

Source: Bloomberg New Energy Finance Note: 2011–13 according to Bloomberg New Energy Finance expectations

Global total = $193.9bn

7 / / / /

6.5 5.8 5.57.3

8.6

12.510.6

14.916.0

20.619.8

29.1

23.925.9

29.8

44.0

28.6

40.9

37.035.6

21.4

36.935.1

35.732.3

31.7

39.2

51.5

36.9

41.7

45.4

Q1 04

Q2 04

Q3 04

Q4 04

Q1 05

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Four quarter running average

NEW FINANCIAL INVESTMENT IN CLEAN ENERGY Q1 2004–Q3 2011 ($BN)

Source: Bloomberg New Energy Finance

Note: Excludes corporate and government R&D, and small distributed capacity. Not

adjusted for re-invested equity

8 / / / /

1.5 1.6 1.2

2.32.9

3.93.3

5.1

6.67.6

8.8

11.3

10.1 8.8

11.4

14.1

12.3

16.3

12.211.9

4.9

11.1

8.1

10.810.3

10.7 9.7

17.4

9.3

15.6

18.9

Q1 04

Q2 04

Q3 04

Q4 04

Q1 05

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Four quarter running average

NEW FINANCIAL INVESTMENT IN CLEAN ENERGY IN AMER Q1 2004–Q3 2011 ($BN)

Source: Bloomberg New Energy Finance

Note: Excludes corporate and government R&D, and small distributed capacity. Not

adjusted for re-invested equity

9 / / / /

3.0 3.32.3

3.5 3.4

6.2

5.05.6 5.4

9.3

5.8

12.5

8.6

10.3

11.0

23.2

9.3

14.815.8

15.1

6.8

17.2

12.8

10.410.0

8.6

11.5

15.5

9.29.9 9.5

Q1 04

Q2 04

Q3 04

Q4 04

Q1 05

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Four quarter running average

NEW FINANCIAL INVESTMENT IN CLEAN ENERGY IN EMEA Q1 2004–Q3 2011 ($BN)

Source: Bloomberg New Energy Finance

Note: Excludes corporate and government R&D, and small distributed capacity. Not

adjusted for re-invested equity

10 / / / /

2.1

0.9

2.01.5

2.3 2.4 2.3

4.2 4.1 3.7

5.1 5.4 5.2

6.87.4

6.7 7.0

9.89.0

8.5

9.78.6

14.3 14.5

12.012.4

18.018.6

18.4

16.2

16.9

Q1 04

Q2 04

Q3 04

Q4 04

Q1 05

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Four quarter running average

NEW FINANCIAL INVESTMENT IN CLEAN ENERGY IN ASOC Q1 2004–Q3 2011 ($BN)

Source: Bloomberg New Energy Finance

Note: Excludes corporate and government R&D, and small distributed capacity. Not

adjusted for re-invested equity

11 / / / /

ASSET FINANCE FOR NEW BUILD CLEAN ENERGY –

TOP 15 COUNTRIES, 2010 ($BN)

Source: Bloomberg New Energy Finance Note: Total values include estimates for undisclosed deals

1.4

1.5

1.8

2.2

2.2

2.3

2.4

3.2

4.4

4.6

4.8

6.2

6.9

20.7

47.3

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0 50.0

Poland

Pakistan

Portugal

Australia

United Kingdom

Mexico

Belgium

India

Canada

Spain

Italy

Germany

Brazil

United States

China

ASOC

AMER

EMEA

12 / / / /

AGENDA

2. Clean energy sectoral trends

1. Investment activity

3. Near-term issues

4. Thoughts on solutions

13 / / / /

LEVELISED COST OF ENERGY Q3 2011 ($/MWH)

Source: Bloomberg New Energy Finance

Carbon forecasts from the BNEF European Carbon Model with a 2020 horizon $74/tCO2. Coal and nat gas prices

from the US Department of Energy EIA Annual Energy Outlook 2011. % change represents change in mid from

Q2 2011.

0 50 100 150 200 250 300 350 400 450 500

Natural Gas CCGT

Landfill Gas

Coal Fired

Wind - Onshore

Municipal Solid Waste

Geothermal - Flash Plant

Biomass - Incineration

Biomass - Anaerobic Digestion

PV - c-Si Tracking

Biomass - Gasification

Geothermal - Binary Plant

PV - Thin Film

STEG - Tower & Heliostat w/storage

PV - c-Si

STEG - LFR

STEG - Tower & Heliostat

Wind - Offshore

STEG - Parabolic Trough + Storage

STEG - Parabolic Trough

Marine - Wave

Marine - Tidal

LCOE BNEF 2011 EU-ETS EUA Forecast Q3 2011 Central Scenario Q2 2011 Central Scenario

+5%

+1%

+5%

+1%

-2%

+1%

-1%

+6%

+1%

-4%

-2%

-3%

-9%

+6%

+1%

-9%

-1%

-1%

-3%

799 +23%

740 +8%

14 / / / /

THE PV MODULE EXPERIENCE CURVE, 1976–2011 ($/W)

Source: Paul Maycock,

Bloomberg New Energy Finance, FSLR filings

Notes: Inflation adjustment using US PPI, R2 of c-Si regression = 0.94, R2 of FSLR regression =

0.98

MW (log)

0.1

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

historic prices experience curve Chinese c-Si module prices

Thin-film experience curve First Solar thin-film module cost

1976

1985

2003

2011

2006

2011

2010

15 / / / /

Source: Bloomberg New Energy Finance

UK

$/kWh average residential power price

RESIDENTIAL PV PRICE PARITY

Note: LCOE based on 6% weighted average cost of capital, 0.7%/year module degradation, 1%

capex as O&M annually. $3.5/W capex assumed for 2011, $2/W for 2015.

More sun

CA CA

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

800 1,000 1,200 1,400 1,600

kWh/kW/year

2011

LCOE

Germany

Italy

Denmark

PortugalTurkey

Hawai

Spain

France

Netherlands

United Kingdom Czech Republic

Japan

CaliforniaSwitzerland

China South Africa

South Korea

United States

2015

LCOE

50GW

16 / / / /

'CHINA' AND 'INTERNATIONAL' SPOT PRICE OF SOLAR-

GRADE SILICON, MAY 2009 – 24 OCTOBER 2011 ($/KG)

Source: Bloomberg New Energy Finance Solar Spot Price

Index

Note: For longer-term spot prices, see Appendix. Starting 11 July 2011 the Index is

conducted weekly and the dates in chart represent first day of the week

0

10

20

30

40

50

60

70

80

90M

ay

Ju

nJu

lA

ug

Se

pO

ct

No

vD

ec

Ja

nF

eb

Ma

rA

pr

Ma

yJu

nJu

lA

ug

Se

pO

ct

No

vD

ec

Ja

nF

eb

Ma

rA

pr

Ma

yJu

n0

4 J

ul

11

Ju

l 1

8 J

ul

25

Ju

l 0

1 A

ug

0

8 A

ug

1

5 A

ug

2

2 A

ug

2

9 A

ug

0

5 S

ep

1

2 S

ep

1

9 S

ep

2

6 S

ep

0

3 O

ct

10

Oct

17

Oct

24

Oct

2009 2010 2011

"China price" "International price"

17 / / / /

SPOT PRICES OF WAFERS AND CELLS, MAY 2009-17

OCTOBER 2011 ($/W)

Source: Bloomberg New Energy Finance Solar Spot Price

Index

Note: See methodology about conversion. Starting 11 July 2011 the Index is conducted

weekly. The dates in chart represent first day of the week for which the price applies.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6M

ay

Ju

nJu

lA

ug

Se

pO

ct

No

vD

ec

Ja

nF

eb

Ma

rA

pr

Ma

yJu

nJu

lA

ug

Se

pO

ct

No

vD

ec

Ja

nF

eb

Ma

rA

pr

Ma

yJu

n0

4 J

ul

11

Ju

l 1

8 J

ul

25

Ju

l 0

1 A

ug

0

8 A

ug

1

5 A

ug

2

2 A

ug

2

9 A

ug

0

5 S

ep

1

2 S

ep

1

9 S

ep

2

6 S

ep

0

3 O

ct

10

Oct

17

Oct

24

Oct

2009 2010 2011

5" mono wafers 6" multi wafers 6" mono wafers Mono cells Multi cells

18 / / / /

UTILITY-SCALE PV SYSTEM PRICE FORECAST, 2010-2020

(2010 $/W)

Source: Bloomberg New Energy Finance

1.72

1.35

1.060.95 0.90

0.810.73 0.66 0.59 0.53 0.48

0.30

0.30

0.270.24 0.22

0.210.19

0.17 0.16 0.15 0.14

0.50

0.50

0.470.45

0.440.42

0.400.39

0.370.36

0.34

0.41

0.41

0.390.37

0.360.34

0.330.32

0.310.29

0.28

0.18

0.18

0.170.17

0.160.16

0.150.15

0.150.14

0.14

$3.12/W

$2.74/W

$2.36/W$2.19/W

$2.08/W$2.00/W

$1.81/W$1.68/W

$1.57/W$1.47/W

$1.38/W

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Module Inverter Balance of plant Engineering, procurement & construction Other

19 / / / /

ASSET FINANCE FOR LARGE-SCALE SOLAR PROJECTS,

2007-Q3 2011

Source: Bloomberg New Energy Finance

Note: Based on individual deals tracked, with a „buffer‟; subject to change, usually

upwards, as more deals are discovered

$1.6bn$1.9bn

$3.6bn

$4.6bn$3.8bn

$5.2bn

$6.6bn$6.4bn

$2.2bn

$5.8bn

$4bn

$4.2bn

$4.3bn

$4.8bn

$6.6bn

$10.3bn

$4.9bn

$14.1bn

$19.5bn

Q1

'07

Q2

'07

Q3

'07

Q4

'07

Q1

'08

Q2

'08

Q3

'08

Q4

'08

Q1

'09

Q2

'09

Q3

'09

Q4

'09

Q1

'10

Q2

'10

Q3

'10

Q4

'10

Q1

'11

Q2

'11

Q3

'11

PV >1MW Solar Thermal Electricity Generation

20 / / / /

ONSHORE WIND TURBINE PRICE DATA, 1984–2011

(EUR M/MW)

Source: Bloomberg New Energy Finance, ExTool

Note: Plotted against cumulative global installed capacity. All prices are real EUR. Each marker represents one year

for the corresponding series. ExTool data is for Denmark and Germany. BNEF Rest of World (RoW) is BNEF Wind

Turbine Price Index, excluding Asian turbine contracts. BNEF China is domestic turbine contracts.

ExTool BNEF RoW

BNEF China

0.25

0.50

1.00

2.00

100 1,000 10,000 100,000 1,000,000MW

1984 1990 2000 2011

6%

14%

21 / / / /

LEVELIZED COSTS: BEST NEW WIND VS NEW COAL

($/MWh)

• New coal must cover cost of capital

• New coal requires advanced

pollution control

• Wind turbines back to 2005 prices,

but now perform much better

• Wind bankability has driven down

cost of capital

• Coal suffers from carbon price risk

Perception:

Reality:

Source: Bloomberg New Energy Finance

30

120

Coal

Wind

68

65

Coal

Wind

22 / / / /

Electric vehicles - past

23 / / / /

ELECTRIC VEHICLES - PRESENT

24 / / / /

LITHIUM-ION BATTERY PACK COST, TRACTION BATTERY

PRODUCTION, 2010–30

Source: Bloomberg New Energy Finance Note: Total pack cost includes the battery management system

Total pack cost ($/kWh) Annual production (GWh)

0

200

400

600

800

1,000

1,200

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

0

50

100

150

200

250

300

350

Total capacity of batteries manufactured per year (GWh) Total cost of pack ($/kWh)

25 / / / /

73,714 508 124 45

GLOBAL EV CAPACITY, 2011 (‘000 VEHICLES)

Source: OICA, L‟Argus, Bloomberg New Energy Finance * Figures from 2010

Global auto & light commercial

vehicle production*

2011 EV battery

production

capacity

2011 EV

production

capacity

2011 EV

sales

forecast

26 / / / /

500+ SMART GRID PROJECTS WORLDWIDE

CANADA

Smart meters and

automation in

Ontario and BC

USA

Over 200 projects;

$4.5bn stimulus for

smart grids

EU

80% smart

metering by 2020;

Over 100 projects

BRAZIL

Proposed smart

metering mandate;

large-scale pilots

CHINA

High voltage “Strong Smart Grid”;

48m smart meters by 2010.

SOUTH KOREA

Jeju Island pilot;

Nationwide smart grid by

2030 SINGAPORE

Smart metering

pilot 2011–12

AUSTRALIA

Smart metering in

Victoria; Newcastle

Smart Grid, Smart City

project

UK

100% smart metering

by 2019; GBP 500m

for Low Carbon

Networks

JAPAN

Multiple pilots

27 / / / /

Worldwide computer and storage power, 1980 - 2010

Source: Seagate; PhysOrg.com; Computer Industry Almanac; Bloomberg New Energy Finance

0.0001

0.001

0.01

0.1

1

10

100

1000

10000

100000

1000000

1980 1985 1990 1995 2000 2005 2010

Worwide total computing power

Worldwide computer storage volume

96%

CAGR

81%

CAGR

28 / / / /

Case study: mobile telephony

US telecoms revenue split ($bn) US fixed line vs mobile prices ($/min)

Source: Federal Communications Commission; Bloomberg New Energy Finance

Source: Federal Communications Commission; Bloomberg New Energy Finance

0

50

100

150

200

250

300

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Mobile Fixed line

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Mobile Fixed line

29 / / / /

AGENDA

2. Clean energy sectoral trends

1. Investment activity

3. Near-term issues

4. Thoughts on solutions

30 / / / /

EUROPE – FINANCIAL CRISIS

Source: AP

31 / / / /

GREECE SENIOR 5-YEAR USD DENOMINATED CDS

Bloomberg Terminal

32 / / / /

CDS SPREADS - PORTUGAL

33 / / / /

SPAIN SENIOR 5-YEAR USD DENOMINATED CDS

Bloomberg Terminal

34 / / / /

ITALY SENIOR 5-YEAR USD DENOMINATED CDS

Bloomberg Terminal

35 / / / /

FRANCE SENIOR 5-YEAR USD DENOMINATED CDS

Bloomberg Terminal Bloomberg Terminal

36 / / / /

US – CLIMATE SCEPTICISM

37 / / / /

0.0

0%

20.3

10%

74.5

38% 68

35%

21.4

11%

9.7

5%

2008 2009 2010 2011e 2012e 2013e

GLOBAL CLEAN ENERGY STIMULUS SPENDING BY YEAR,

2011–2013 ($BN)

Source: Bloomberg New Energy Finance Note: 2011–13 according to Bloomberg New Energy Finance expectations

Spent = $94.8bn, 49% Unspent = $31.1bn, 16%

Global total = $193.9bn

38 / / / /

MARGINAL COST OF GAS-LEVERED PRODUCERS AND

HENRY HUB PRICE FORECAST ($/MMBTU)

Source: Bloomberg New Energy Finance Note: Basket comprises 17 E&P companies with an

average 85% gas/liquids production ratio and combined 2010 output of 4,250Bcf. „DD&A‟ is

depletion, depreciation and amortisation; „G&A‟ is general and administrative expenses.

5.85

6.50 7.00

0

1

2

3

4

5

6

7

8

9

10

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

E

20

15

E

20

20

E

20

30

E

DD&A Lease operating expense

Production taxes G&A

Interest expense Price

39 / / / /

NET COSTS OF FEED-IN TARIFFS (EUR BN)

Source: Bloomberg New Energy Finance

-

2

4

6

8

10

12

14

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029Germany Czech Republic Italy Spain France Greece Ontario

40 / / / /

0

50

100

150

200

250

300

350

400

450

500

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

NEX CLEAN ENERGY INDEX 2003 – 30 SEPTEMBER 2011

Note: Values as of 30 Sep 2011; AMEX Oil, NASDAQ and S&P 500 rebased to 100 on 01 Jan 2003 Source: Bloomberg New Energy Finance

NEX AMEX Oil

S&P 500

NASDAQ

41 / / / /

CHINA POWER CAPACITY ADDITIONS BY TECHNOLOGY, 2001-11E (GW)

Source: China Electricity Council, Bloomberg New Energy Finance

0

20

40

60

80

100

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011e

Solar

Biomass &

WtE

Wind

Hydro

Nuclear

Natural Gas

Coal

42 / / / /

WORLD’S LARGEST BANKS BY TOTAL BALANCE SHEET

($ BN)

Note: as at 16 September 2011

13,459

10,810

10,460

10,337

2,455

2,265

2,118

1,998

1,914

1,906

1,594

1,490

1,454

1,317

1,258

1,218

1,132

1,032

992

930

206

173

161

Ind and Comm Bank of ChinaChina Construction Bank

Bank of ChinaAgricultural Bank of China

HSBC

Bank of AmericaJP Morgan Chase

BNP ParibasCitigroup

Deutsche BankCrédit Agricole

BarclaysRBSUBS

Wells FargoSantander

Société GénéraleCredit Suisse

Lloyds Banking groupUniCredit

Mitsubishi UFJ

SunTrust BanksMizuho Financial Group

Source: Bloomberg

43 / / / /

AGENDA

2. Clean energy sectoral trends

1. Investment activity

3. Near-term issues

4. Thoughts on solutions

44 / / / /

Accelerating the shift to clean energy

1. Level playing field

• Remove subsidies

• Neutralise externalities

• Improve risk transparency

• Remove barriers to innovation

• Accelerated retirement

• Utility regulation

• Trade barriers

• Standards

• Financial regulation (risk, solvency

vs liquidity)

2. Smart support

• Importance of price discovery

• TLC = transparent, limited, carefully applied

• Focus on R&D or cost reduction

• Avoid “green jobs” fallacy

• Education & Skills

• Public procurement

• Climate finance

• APPROPRIATE use of PPP

• Communications / Leadership

/ / / / / / / / / / / / / / / / / / / / / / / / / / / /

Subscription-based news, data

and analysis to support your

decisions in clean energy, power

and water and the carbon markets

MARKETS Renewable Energy

Carbon Markets

Energy Smart Technologies

Renewable Energy Certificates

Carbon Capture & Storage

Power

Water

Nuclear

SERVICES Insight: research, analysis & forecasting

Industry Intelligence: data & analytics

News & Briefing: daily, weekly & monthly

Applied Research: custom research & data mining

Knowledge Services: Summit, Leadership Forums, Executive Briefings &

workshops

MICHAEL LIEBREICH TWITTER: @MLIEBREICH

Related Documents