August 5, 2015 Cars 2025: Vol. 2 Solving CO2: Engines, Batteries and Fuel Cells Equity Research Endless powertrain advancement is a boon for suppliers; Aisin Seiki to Buy Regulations drive spending to cut CO2 The automobile industry will require enormous investments over the next decade to meet tighter environmental regulations we expect to take effect in different countries between 2020 and 2025. In this second edition of Cars 2025 we look at technologies that help reduce CO2 and discuss the considerable potential of three: 1) engine thermal efficiency, 2) lithium ion batteries, and 3) fuel cells. Don’t give up on existing engines While electrification is a major theme, we expect 95% of vehicles sold in 2025 will use gasoline or diesel engines for at least part of their power. Increasing thermal efficiency is vital for meeting new standards. This will lift demand for powertrain components that boost efficiency and limit pollutants. We focus on advances in transmissions (Aisin Seiki, up to Buy), the expansion of direct- injection turbochargers (BorgWarner/ Continental), and demand for gasoline particulate filters (NGK Insulators). We see homogeneous charge compression ignition as a powerful solution and we highlight Mazda’s aim to commercialize the world’s first HCCI product. 2017-18 as a turning point for battery We estimate that hybrids (HVs), plug-in hybrid EVs (PHEVs), and EVs will account for 25% of auto sales by 2025 vs. 5% in 2015. The evolution of lithium ion batteries for vehicle electrification is essential and we see 2017-18 as a turning point for cutting battery costs and increasing energy density. Besides Tesla’s Gigafactory (targeting cost reductions of 30-40%) Nissan and LG Chem plan to substantially raise energy density. Fuel cells a nascent, but key presence Furthest out on the horizon are fuel cell vehicles (FCVs) powered by hydrogen rather than carbon. While we forecast FCVs’ share of the overall auto market at just 0.5% (c.400,000 vehicles) in 2025, their role in diversifying energy sources, extending driving distances and meeting California’s zero emission vehicle regulations warrants attention. We focus on the technological innovations in Toyota’s second FCV set for launch around 2020. Kota Yuzawa +81(3)6437-9863 [email protected] Goldman Sachs Japan Co., Ltd. Patrick Archambault, CFA (212) 902-2817 [email protected] Goldman, Sachs & Co. Stefan Burgstaller +44(20)7552-5784 [email protected] Goldman Sachs International Yipeng Yang +86(10)6627-3189 [email protected] Beijing Gao Hua Securities Company Limited Ashik Kurian +44(20)7051-3084 [email protected] Goldman Sachs International Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. The Goldman Sachs Group, Inc. Global Investment Research

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

August 5, 2015

Cars 2025: Vol. 2

Solving CO2: Engines, Batteries and

Fuel Cells Equity Research

Endless powertrain advancement is a boon for suppliers; Aisin Seiki to Buy

Regulations drive spending to cut CO2

The automobile industry will require enormous

investments over the next decade to meet tighter

environmental regulations we expect to take effect

in different countries between 2020 and 2025. In

this second edition of Cars 2025 we look at

technologies that help reduce CO2 and discuss the

considerable potential of three: 1) engine thermal

efficiency, 2) lithium ion batteries, and 3) fuel cells.

Don’t give up on existing engines

While electrification is a major theme, we expect

95% of vehicles sold in 2025 will use gasoline or

diesel engines for at least part of their power.

Increasing thermal efficiency is vital for meeting

new standards. This will lift demand for powertrain

components that boost efficiency and limit

pollutants. We focus on advances in transmissions

(Aisin Seiki, up to Buy), the expansion of direct-

injection turbochargers (BorgWarner/ Continental),

and demand for gasoline particulate filters (NGK

Insulators). We see homogeneous charge

compression ignition as a powerful solution and

we highlight Mazda’s aim to commercialize the

world’s first HCCI product.

2017-18 as a turning point for battery

We estimate that hybrids (HVs), plug-in hybrid EVs

(PHEVs), and EVs will account for 25% of auto

sales by 2025 vs. 5% in 2015. The evolution of

lithium ion batteries for vehicle electrification is

essential and we see 2017-18 as a turning point for

cutting battery costs and increasing energy

density. Besides Tesla’s Gigafactory (targeting

cost reductions of 30-40%) Nissan and LG Chem

plan to substantially raise energy density.

Fuel cells a nascent, but key presence

Furthest out on the horizon are fuel cell vehicles

(FCVs) powered by hydrogen rather than carbon.

While we forecast FCVs’ share of the overall auto

market at just 0.5% (c.400,000 vehicles) in 2025,

their role in diversifying energy sources,

extending driving distances and meeting

California’s zero emission vehicle regulations

warrants attention. We focus on the technological

innovations in Toyota’s second FCV set for launch

around 2020.

Kota Yuzawa

+81(3)6437-9863 [email protected] Goldman Sachs Japan Co., Ltd.

Patrick Archambault, CFA

(212) 902-2817 [email protected] Goldman, Sachs & Co.

Stefan Burgstaller

+44(20)7552-5784 [email protected] Goldman Sachs International

Yipeng Yang

+86(10)6627-3189 [email protected] Beijing Gao Hua Securities Company Limited

Ashik Kurian

+44(20)7051-3084 [email protected] Goldman Sachs International

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

The Goldman Sachs Group, Inc. Global Investment Research

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 2

Contents

Analyst team contributors 2

Executive summary: Fuel efficient technologies for a low-CO2 society 3

Don’t underestimate existing engines; thermal efficiency provides scope for fuel economy 10

Electric Vehicles (EVs): Tesla’s Gigafactory key to EV growth 18

Fuel Cell Vehicles (FCVs): The ultimate eco-car? 25

CO2 regulations: Intermittent tightening of regulations approaching 35

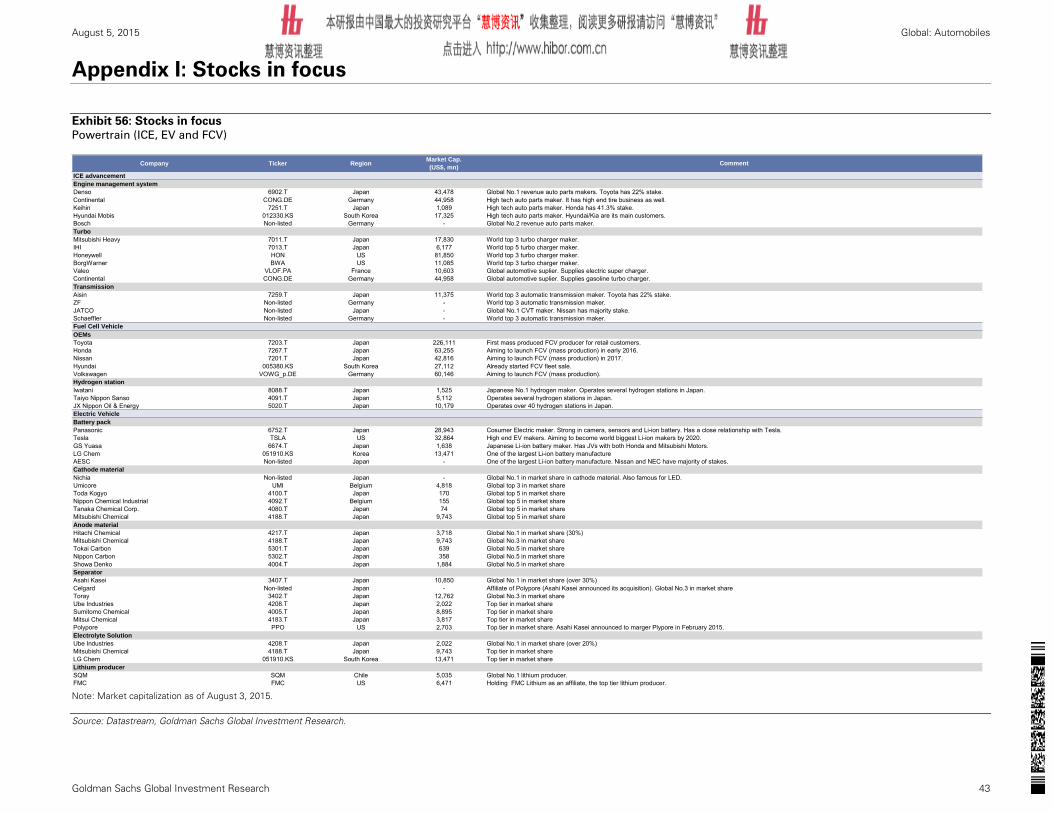

Appendix I: Stocks in focus 43

Appendix II: Tesla valuation methodology 44

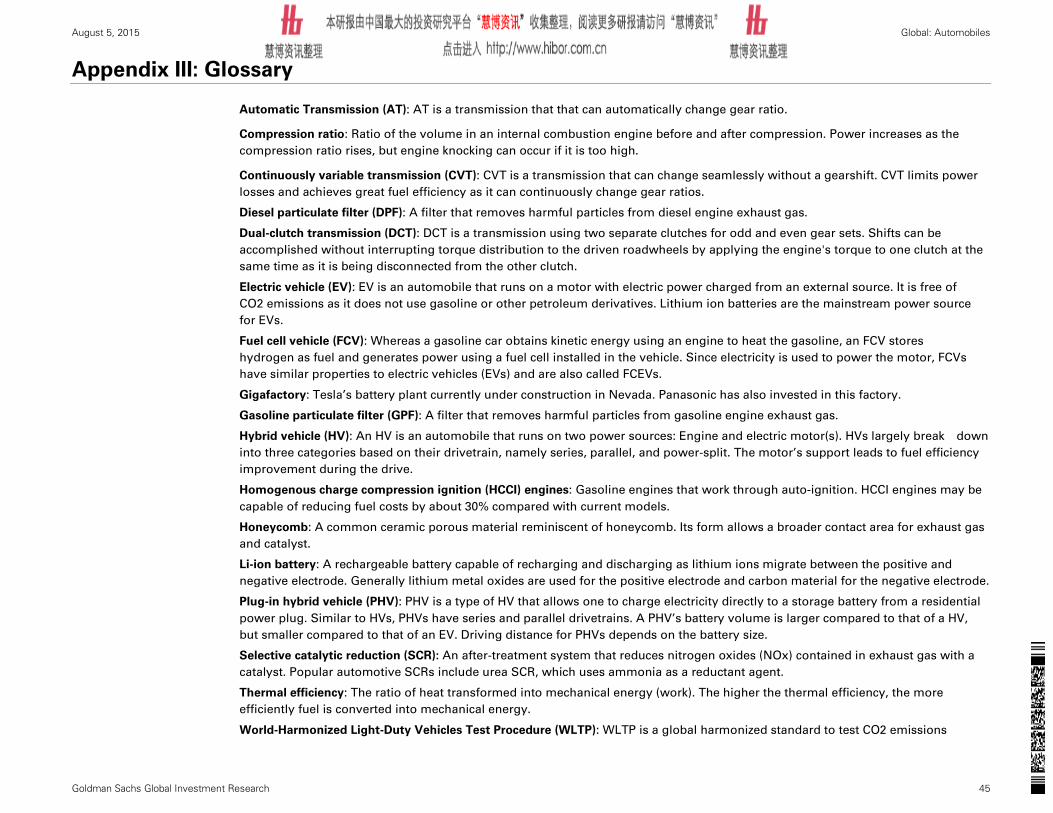

Appendix III: Glossary 45

Disclosure Appendix 47

Prices in this report are based on August 3, 2015 closing prices, unless otherwise stated.

Analyst team contributors

Region Analyst Telephone email Region Analyst Telephone emailAutos/Auto parts Autos/Auto parts (Global)Japan Kota Yuzawa +81 (3) 6437 9863 [email protected] USA Patrick Archambault +1 (212) 902 2817 [email protected]

Toshihide Kinoshita +81 (3) 6437 9934 [email protected] Europe Stefan Burgtaller +44 (20) 7552 5784 [email protected] Matsuzaki +81 (3) 6437 9877 [email protected] Ashik Kurian +44 (20) 7051 3084 [email protected]

Technology (Hardware) Korea Seung Shin +82 (2) 3788 1779 [email protected] Daiki Takayama +81 (3) 6437 9870 [email protected] China Yipeng Yang +86 (10) 6627 3189 [email protected], Trading companies India Pramod Kumar +91 (22) 6616 9043 [email protected] Hiroyuki Sakaida +81 (3) 6437 9896 [email protected]

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 3

Executive summary: Fuel efficient technologies for a low-CO2 society

With the transportation sector accounting for 22% of global CO2 emissions (2013), major developed economies are under

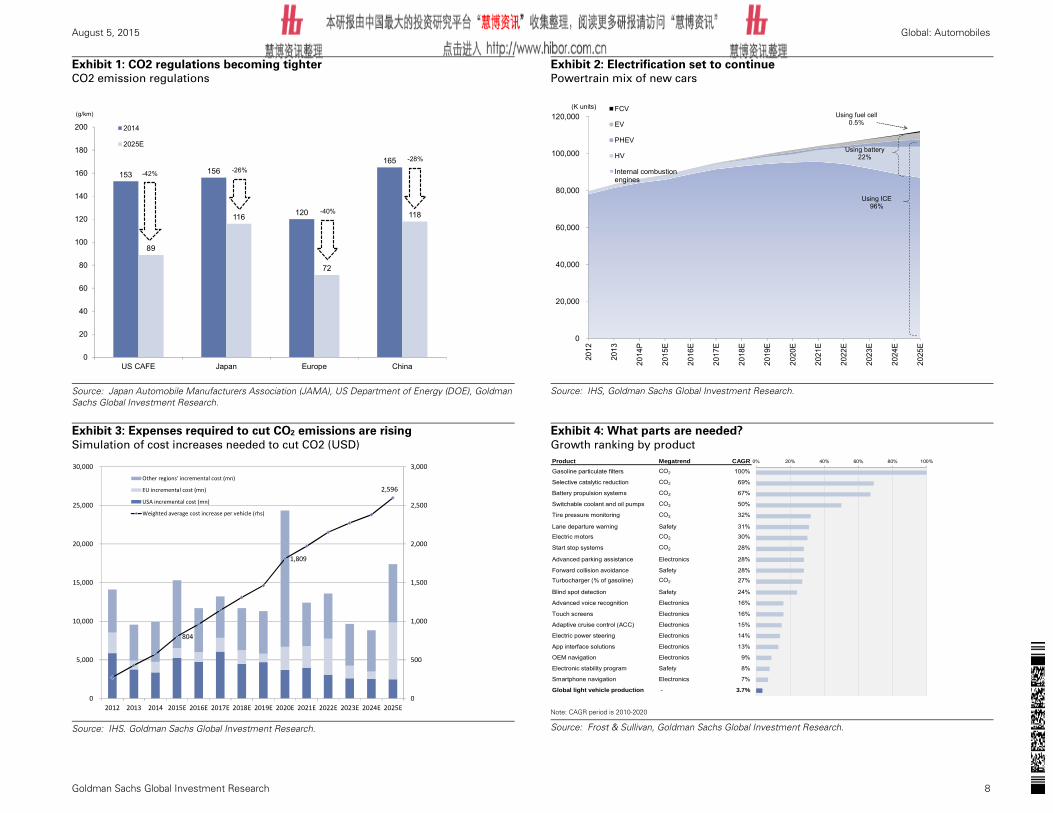

pressure to reduce vehicle CO2 g/km by 30%-40% by 2025. We estimate that cars suited to the low-CO2 society of the next

decade will need to absorb cost increases of at least US$2,500 per vehicle. This implies a US$25 bn additional cost burden

by 2025, equivalent to 20% of global automakers’ US$120 bn profit pool in 2014. Suppliers will benefit as global automakers

compete to incorporate—quickly and at a reasonable cost—powertrain technologies that get the most out of every ounce of

fuel and reduce pollutants.

In this second installment of our Cars 2025 series—where we explore seven mega trends that will transform the global auto

industry—we take an in-depth look at the technologies we expect to play the greatest role in reducing emissions. We begin with

internal combustion engine vehicles and advances that could make them as fuel efficient as today’s hybrids. We turn next to lithium

ion (Li-ion) batteries and significant advances in their cost and energy density that will speed efforts in electrification. And finally we

focus on fuel cell vehicles, which may one day become the ultimate eco-car if the industry can find ways to reduce the CO2 created

in the hydrogen production process.

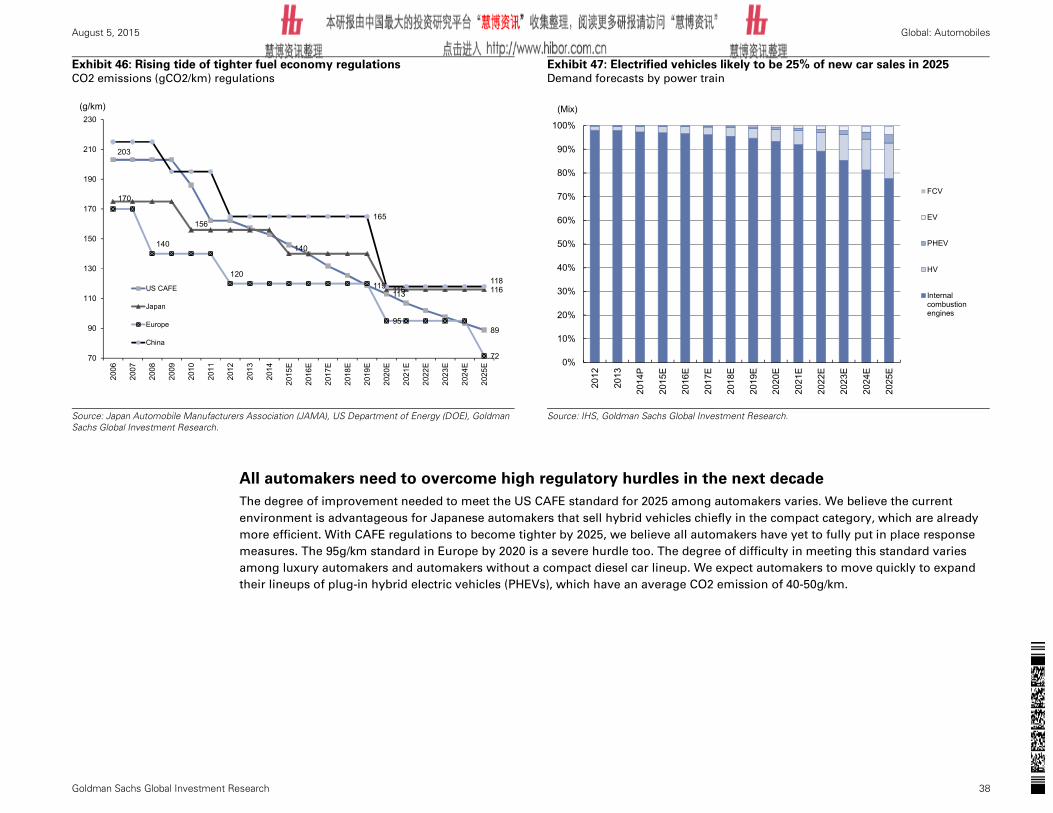

Auto industry faces intermittent tightening of global fuel economy regulations

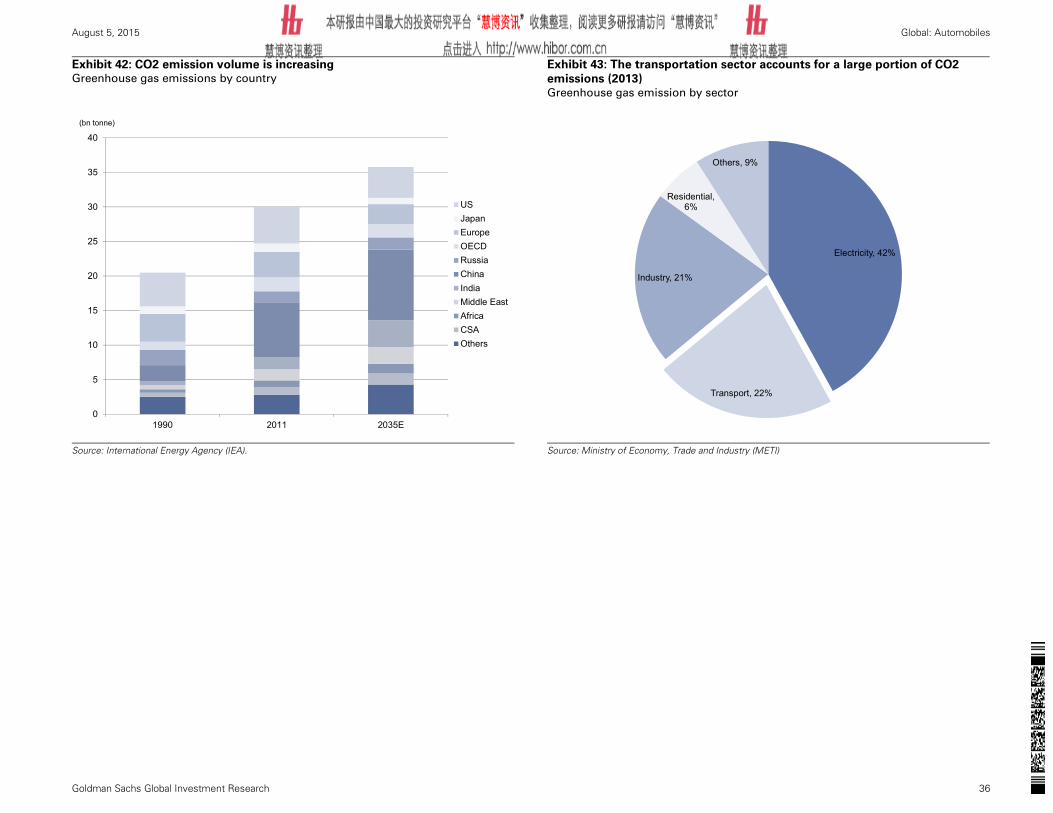

Despite diligent efforts globally, greenhouse gas emission continues to rise. We expect the major markets of Japan, the United

States, Europe, and China to tighten CO2 regulations mainly over 2020-2025. Plans call for the adoption of the World-Harmonized

Light Vehicles Test Procedure (WLTP) for testing CO2 emissions, and intermittent tightening of various regulations, including

emission (NOx, PM) standards and California’s zero emission vehicle (ZEV) regulations. It is no surprise that technologies to curb

CO2 emissions feature at the top of our ranking of products with the most growth potential through to 2020 (see Exhibit 4).

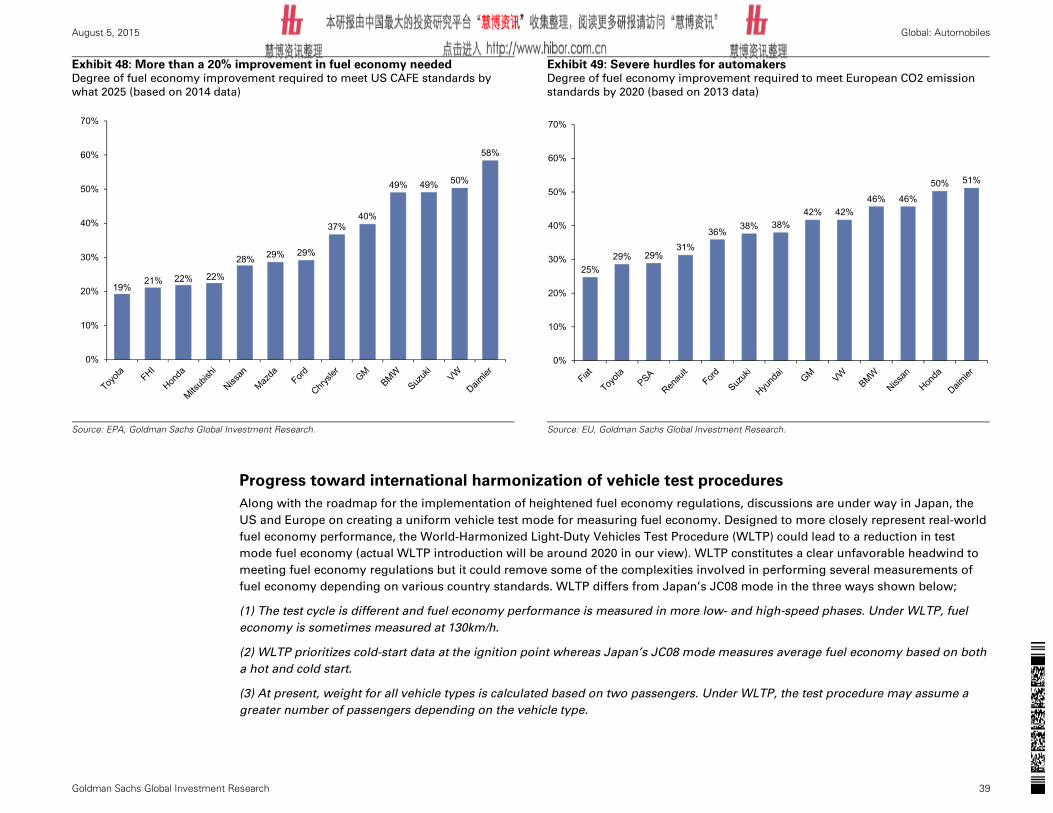

(1) Higher thermal efficiency in engines an opportunity not to be missed

Vehicle electrification is gaining traction, but we expect that in 2025 more than 95% of all new cars will still have gasoline or diesel

engines, either as their sole source of power or in combination with electric motors in hybrid vehicles (HVs) and plug-in HVs.

Automakers are competing to raise the thermal efficiency to 50% from the current 40% (each 1 percentage point improvement in

thermal efficiency boosts fuel economy by 2%-3%). Many automakers are likely to opt for direct injection turbos to wring additional

power from smaller engines and high-speed automatic transmissions to maximize the time engines operate in their optimal gear

range. Mazda and some European makers going further and are aiming to incorporate homogeneous charge compression ignition

(HCCI) technology, which foregoes the spark plug of traditional gasoline engines and instead incorporates characteristics of diesel

engines to improve fuel efficiency with less particulate matter emissions. If these advances raise thermal efficiency to 50%, it would

be possible to achieve a level of fuel efficiency that is on par with current hybrid vehicles with normal gasoline engines.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 4

(2) Li-ion battery innovation in 2017-2018 setting pace of electrification

We estimate that electrified vehicles will account for 25% of auto sales by 2025 versus 5% in 2015. Powertrain electrification is

essential for complying with new regulations and we see hybrid technology becoming mainstream, with our forecast calling for

sales to rise to 17 mn vehicles in 2025 from a little over 2 mn in 2015. We expect languishing sales of PHEVs and EVs to pick up as a

result of lithium ion battery innovation over 2017-2018. Li-ion batteries account for 50% of the cost of an EV; however, costs could be

reduced 30%-40% following the startup in 2017 of Tesla and Panasonic’s Gigafactory (consumer batteries, 50 GWh capacity). A

number of makers are planning to cut auto battery costs 30%-40% by 2020 via energy density increases achieved through cathode

material innovation and scale.

(3) Fuel Cell technology significant potential; FCVs still small market

Toyota released the world’s first mass-market FCV, the Mirai in December 2014, marking a major first step toward the realization of

a hydrogen-based society. Numerous challenges still need to be overcome, including issues related to cost, infrastructure, and

regulatory reform, but this technology has significant mid-term potential from an energy diversification and CO2 emission reduction

standpoint. If production was to reach 50,000 vehicles, the cost of the fuel-cell stack the most expensive component could fall to 20%

of the current price. We expect sales volume to begin rising, chiefly in Japan and California, from 2020 and forecast FCVs’ share of

the overall auto market to rise from 0% in 2015 to 0.5% (roughly 400,000 vehicles) in 2025. However, FCV awareness is still low and

we do not expect FCVs to really gain traction until the second generation of FCVs due for launch in 2020. There has been much

debate about whether FCVs or EVs will emerge as the winning vehicle technology. We do not see the two as being in competition

but as technologies that can coexist given their different vehicle characteristics and both have various global energy policy support.

Stock beneficiaries: Aisin Seiki up to Buy from Neutral; reiterate Mazda Buy

Aisin Seiki (7259.T): Upgrade to Buy: Developing 8- to 10-speed automatic transmission technology

Trend: Automatic Transmission (AT) technology

We raise our rating for Aisin Seiki to Buy, from Neutral, for the following three reasons. (1) We expect the shift to multi-speed

automatic transmissions (AT) to accelerate amid growing demands to cut CO2. We raise our earnings outlook for Aisin AW

(automatic transmission business), which has the world’s top market share for AT, by 10% from FY3/17. (2) The competitive edge of

Aisin’s AT products should become more evident as a new Higashi-Okazaki plant comes online. The company was the first in the

world to commercialize front-engine front-wheel drive (FF) 8-speed AT, and we expect it to accumulate technology as high-speed

advances further. (3) We expect upfront investment to peak in FY3/16 and earnings and cash flow to recover from FY3/17. We expect

growing competitive advantages for AT, which help reduce CO2. Please see Aisin Seiki (7259.T): The need for (multi) speed: AT to

drive growth amid CO2 cuts, to Buy published August 5, 2015.

Aisin Seiki is covered by Japan Autos analyst, Kota Yuzawa.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 5

Mazda (7261.T): Buy: Keen to be the first in the world to commercialize HCCI

Trend: Homogeneous charge compression ignition (HCCI) technology

Mazda has a history of cutting investment in powertrain electrification and downsized direct-injection turbocharger in the process of

prioritizing technologies, and of focusing on improving conventional internal combustion engines. It aims to increase thermal

efficiency in homogeneous charge compression ignition (HCCI) gasoline engines to close to 50% and has expressed confidence in

commercializing the world’s first such engine by 2018-2019. We think the wealth of technologies the company has amassed in

naturally aspirated diesel engines over many years is underpinning HCCI development. HCCI engines do not require high-speed

transmissions given the wider range in which the engine operates with high efficiency (Mazda plans to employ a 6-speed automatic

transmission for the time being). The technological hurdles are high, but we view HCCI as a low-cost technology that can clear CO2

regulations. Current earnings are firm as a result of sales growth for SUVs. Mazda has also announced a technology alliance with

Toyota and is steadily laying the groundwork for the future.

Mazda Motor Corp is covered by Japan Autos analyst, Kota Yuzawa.

NGK Insulators (5333.T): Neutral: Gasoline particulate filters small contribution; large medium-term potential for ceramic products

Trend: Gasoline and diesel particulate filters (GPF/DPF)

Direct-injection gasoline engines that focus on engine thermal efficiency raise concerns about an increase in NOx and PM

(particulate matter). Ahead of stronger exhaust gas regulations (Euro 6c), we think exhaust gas after treatment (GPF) is likely to be

used mainly in Europe for gasoline engines. NGK Insulators has a high market share for exhaust gas treatment DPF for diesel

engines, and we expect it to have a strong presence in GPF as well. In April 2014, the company announced plans to build a new

facility at its first plant in Poland (start production in January 2016). We expect it to commence the first mass production of GPF.

However, the scale of GPF production assumed by NGK Insulators is small and we see larger business opportunities in demand for

medium-sized and large diesel vehicles and from emerging markets (from 2019-2020 onward). NGK Insulators has begun investing

aggressively and is earmarking investment of ¥56 bn in FY3/16 and a total of ¥150 bn by FY3/16-FY3/18, compared with

companywide annual average investment of around ¥30 bn in FY3/13-FY3/15. We think the ceramics business will enter a phase

during which it is difficult to raise profit margins over the next one to two years, due to upfront investments.

NGK Insulators is covered by Japan Electric components analyst, Daiki Takayama.

BorgWarner (BWA): Neutral: Sustained top-line growth out to 2019 driven by powertrain technology advancement

Trend: Turbochargers, Thermal Efficiency

We expect a sustained top-line growth CAGR of 9% from 2015 through 2019 from BWA – well above global car production. This is

driven by leverage to secular growth in fitment rates of products like turbochargers, EGR (Exhaust Gas Recirculation) systems, and

advanced transmissions that will continue to see increased penetration as OEMs work to achieve fuel economy standards globally.

Furthermore, we believe BWA is not tied to a single powertrain as it launches products to enhance both existing powertrains –

internal combustion engine through waste heat recovery systems, EGRs, variable valvetrain actuators, eBoosters, eTurbos, amongst

several others and hybrid engines with hybrid clutching technology and a 48V eRDM (Rear Drive Module), as well as fuel cell

vehicles with its fuel cell air supply system planned for launch early next decade. On top of this (and not yet included in our current

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 6

forecast), BWA recently announced an agreement to acquire Remy ($1.2bn in revenue in 2014), further extending the company's

growth profile within powertrain by complementing its existing portfolio with product offerings in electric motors, generators, and

alternators. That said we remain Neutral rated on BWA in the near-term given two consecutive reductions in 2015 guidance

resulting from execution challenges in 1H15 that drive our near-term estimates to the low-end of revised guidance.

BorgWarner is covered by our US Auto and Auto parts analyst, Patrick Archambault.

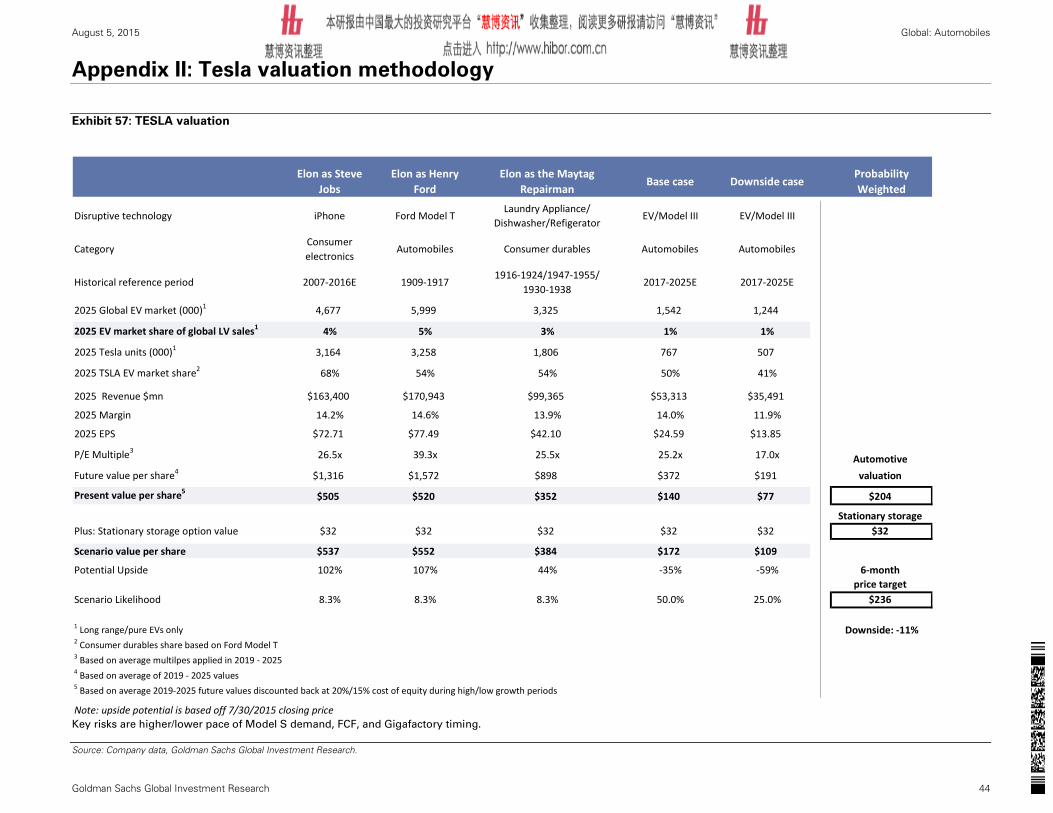

Tesla (TSLA): Neutral: EV manufacturer with a promising product; await a better entry point

Trend: Electric Vehicles

Tesla is a pure EV manufacturer headquartered in Fremont, California. Unlike many other competitive EV offerings, Tesla has

focused on the performance space with its flagship Model S offered at a base price ranging of $70,000-$105,000 (+$10,000 of options

is typical) and with the fastest powertrain accelerating from 0-60 Mph in 3.1 seconds. While there are more than a dozen pure EVs

that are either on the market or planned in the next two years, what sets Tesla apart is its long travel range, with the standard Model

S able to drive 265 miles (430 km)on a single charge. We note the majority of EV offerings reside in the sub 100 mile (160 km) range.

Those that are slated to compete at the high range level, like the Audi Q8 e-tron or R8 e-tron, have planned price tags in the

$130,000-$180,000 range which is higher than the S. As we get into more detail later in this report, a large part of Tesla’s competitive

advantage is its battery cost (about $250/Kwh vs $500/Kwh for large form factors) driven by its use of less expensive 18650 cells,

which are available at scale. While this results in a physically larger battery, it does afford Tesla more flexibility for the price. While

we are believers in the Tesla product, which we think has a real chance of helping transform the auto industry, we believe much is

discounted at this stage and await a better entry point.

Tesla is covered by our US Auto and Auto parts analyst, Patrick Archambault.

Continental (CONG.DE): Neutral: Well positioned to benefit from structural megatrends in the powertrain division

Trend: Turbochargers and selective catalyst reduction (SCR) systems

Continental has a top 3 market position across most of its product offerings in the powertrain division and has also entered fast

growing product segments like SCR (selective catalyst reduction) systems and gasoline turbochargers etc. After a disappointing

level of organic growth in the powertrain division over the last couple of years, we see improvement in the powertrain division

driving growth and margin improvement for Continental. We forecast Continental’s powertrain revenues to increase by c.50% to

€9.6bn by 2019 (Continental’s guidance: €10bn) from €6.5bn in 2014.

In addition to the existing portfolio, we expect a significant part of the growth to come from gasoline turbochargers and SCR

systems. While the Diesel turbocharger penetration is quite high in the mature markets, Gasoline turbochargers are relatively

underpenetrated (currently c.15%). We expect increased penetration to drive strong growth of c.65% CAGR over 2014-2019 and we

believe Continental will be a credible participant in this market along with the current players in the diesel turbocharger market.

Continental has leading (top 3) market share in Gasoline Direct Injection systems which is poised to grow at c.20% CAGR over 2014-

2019 driven by increased penetration from c.20% currently to c.50% by 2019.

Continental is also starting production of SCR systems, the penetration of which is expected to rise significantly post the

introduction of Euro 6 in Europe in 2016. Continental expects of c.€1bn of incremental sales by 2019 from turbochargers and SCR

systems.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 7

Continental is covered by our European Auto parts analysts, Ashik Kurian and Stefan Burgstaller.

Valeo (VLOF.PA): Buy: Increased presence in powertrain solutions driving strong growth

Trend: Engine downsizing and hybrid penetration

We rate Valeo Buy as we believe continued delivery of c.8% organic revenue growth over the next five years will drive further

rerating of the shares. We expect Valeo’s powertrain division to benefit from the ongoing trend of increased efficiency of engines

and transmissions and increased penetration of HEV vehicles. Valeo has a top 2 market position in both its electrical and

transmission business with exposure to fast growing segments like stop-start systems, mild hybrid systems, high speed

transmission systems etc. In addition, Valeo has been the first to market with the electric supercharger system (which uses an

electric motor to give the engine a near instantaneous air flow to boost acceleration) with production expected for the start of 2016.

We expect the superchargers, along with existing turbochargers, to have increased penetration over the coming years as the trend

of engine downsizing continues. While these products currently constitute only a minor part of Valeo’s current powertrain revenues,

the >25% revenue CAGR we forecast over the next 10 years is driving the strong order intake for Valeo.

Valeo is covered by our European Auto parts analysts, Ashik Kurian and Stefan Burgstaller.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 8

Exhibit 1: CO2 regulations becoming tighter CO2 emission regulations

Exhibit 2: Electrification set to continue Powertrain mix of new cars

Source: Japan Automobile Manufacturers Association (JAMA), US Department of Energy (DOE), Goldman Sachs Global Investment Research.

Source: IHS, Goldman Sachs Global Investment Research.

Exhibit 3: Expenses required to cut CO2 emissions are rising

Simulation of cost increases needed to cut CO2 (USD)

Exhibit 4: What parts are needed?

Growth ranking by product

Source: IHS, Goldman Sachs Global Investment Research.

Note: CAGR period is 2010-2020

Source: Frost & Sullivan, Goldman Sachs Global Investment Research.

153 156

120

165

89

116

72

118

0

20

40

60

80

100

120

140

160

180

200

US CAFE Japan Europe China

2014

2025E

(g/km)

-42% -26%

-40%

-28%

0

20,000

40,000

60,000

80,000

100,000

120,000

2012

2013

2014

P

2015

E

2016

E

2017

E

2018

E

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

2025

E

FCV

EV

PHEV

HV

Internal combustionengines

Using ICE96%

Using battery22%

Using fuel cell0.5%

(K units)

804

1,809

2,596

0

500

1,000

1,500

2,000

2,500

3,000

0

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Other regions' incremental cost (mn)

EU incremental cost (mn)

USA incremental cost (mn)

Weighted average cost increase per vehicle (rhs)

Product Megatrend CAGRGasoline particulate filters CO2 100%

Selective catalytic reduction CO2 69%

Battery propulsion systems CO2 67%

Switchable coolant and oil pumps CO2 50%

Tire pressure monitoring CO2 32%

Lane departure warning Safety 31%

Electric motors CO2 30%

Start stop systems CO2 28%

Advanced parking assistance Electronics 28%

Forward collision avoidance Safety 28%

Turbocharger (% of gasoline) CO2 27%

Blind spot detection Safety 24%

Advanced voice recognition Electronics 16%

Touch screens Electronics 16%

Adaptive cruise control (ACC) Electronics 15%

Electric power steering Electronics 14%

App interface solutions Electronics 13%

OEM navigation Electronics 9%

Electronic stability program Safety 8%

Smartphone navigation Electronics 7%

Global light vehicle production - 3.7%

0% 20% 40% 60% 80% 100%

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 9

Exhibit 5: Auto Parts manufacturers that are key to power train evolution Sales weighting of power train-related products (2014)

Note: Sales CAGR period is 2014-2017E. All target price timeframes are 12-month except for BorgWarner (6-month).

Source: Datastream, Goldman Sachs Global Investment Research

(% of total sales) Ticker FX Enginemanagement

o/wTurbo

HV, PHV parts FCV Drive train

(AT/CVT) GPF/DPF Powertrain advancement 3 yr CAGR

BorgWarner BWA $ 60% 60% 0% 0% 30% 0% 90% 5.9%Continental CONG.DE € 9% 1% 1% 0% 5% 5% 19% 9.0%Valeo VLOF.PA € 11% 0% 5% 0% 5% 0% 21% 9.7%Denso 6902.T ¥ 23% 0% 3% 0% 0% 0% 27% 4.8%Aisin 7259.T ¥ 0% 0% 0% 0% 35% 0% 35% 6.8%Ibiden 4062.T ¥ 0% 0% 0% 0% 0% 22% 22% 3.0%NGK 5333.T ¥ 0% 0% 0% 0% 0% 46% 46% 8.3%

(Sales) Ticker FX Enginemanagement

o/wTurbo

HV, PHV parts FCV Drive train

(AT/CVT) GPF/DPF Powertrain advancement Cons. Revenue

BorgWarner BWA $ 4,983 4,983 0 0 2,454 0 7,437 8,305Continental CONG.DE € 3,130 300 200 0 1,565 1,565 6,460 34,506Valeo VLOF.PA € 1,343 0 672 0 672 0 2,686 12,725Denso 6902.T ¥ 995,035 0 150,000 0 0 0 1,145,035 4,308,754Aisin 7259.T ¥ 0 0 0 0 1,026,000 0 1,026,000 2,963,971Ibiden 4062.T ¥ 0 0 0 0 0 70,000 70,000 318,072NGK 5333.T ¥ 0 0 0 0 0 176,000 176,000 378,665

Mkt cap Price TP Return(mn USD) (local) (local) Potential FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

BorgWarner 11,085 Neutral 48.98 55 12% 18.5 17.2 14.6 3.2 3.0 2.8 17.5% 17.7% 19.3%Continental 44,958 Neutral 204.85 231 13% 16.2 14.2 12.9 3.6 3.0 2.6 22.3% 21.4% 20.1%Valeo 10,603 Buy 121.60 152 25% 17.1 14.6 13.0 3.6 3.1 2.6 21.3% 21.2% 20.4%Denso 43,478 Neutral 6,096 6,000 -2% 16.0 14.7 13.5 1.5 1.4 1.3 9.3% 9.3% 9.6%Aisin 11,375 Buy 4,785 5,700 19% 16.0 13.1 12.4 1.4 1.3 1.2 8.6% 10.1% 10.0%Ibiden 2,355 Neutral 1,935 2,100 9% 18.2 17.1 16.0 0.9 0.8 0.8 4.7% 4.9% 5.0%NGK 8,417 Neutral 3,185 3,050 -4% 16.1 14.9 14.0 2.5 2.2 2.0 15.7% 15.1% 14.2%

(Valuation)ROE

RatingP/E P/B

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 10

Don’t underestimate existing engines; thermal efficiency provides scope for fuel economy

While vehicle electrification is clearly gaining traction as a medium-term trend, we forecast that over 95% of all new cars

will still have gasoline or diesel engines by 2025 (HVs and plug-in HVs still have gasoline engines). We believe dramatic

evolution is still possible in engines to increase fuel economy, including the development of:

(1) turbo and direct-injection, and

(2) homogeneous charge compression ignition (HCCI) technology

to make them more efficient.

Further advances in thermal efficiency of existing engines needed

While vehicle electrification often steals the spotlight, we expect 95% of vehicles sold in 2025 will use gasoline or diesel engines for

at least part of their power. Advances in engine technology will still be needed to augment fuel economy in hybrids and PHEVs.

Existing engines are already fast evolving with the shift to direct-injection/downsized turbo/variable displacement models. While the

thermal efficiency of engines is still only around 40% (Exhibit 7), engine manufacturers are conducting R&D with the view to raising

this figure to 45% in five years’ time and 50% in 10 years’ time. Exhibit 6 shows how Toyota plans to meet its 50% thermal efficiency

target not through one decisive technological breakthrough, but by combining and developing different technologies.

Why engine thermal efficiency is attracting attention now

Boosting engine thermal efficiency is not a new concept. However, engines are being used more efficiently now as a result of

transmission evolution (the transition to continuously variable transmissions (CVT) and high-speed automatic transmissions) and

advances in hybrid technology. Based on company feedback across the sector, a 1% improvement in thermal efficiency generally

translates into a 2%-3% improvement in fuel efficiency, so a 10% increase in thermal efficiency would improve fuel efficiency in

existing engines by 20%-30%. Thus, it is theoretically possible to achieve fuel efficiency that is on par with today’s HVs through

engine enhancements alone.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 11

Exhibit 6: There are many options available to improve engines Technologies for improving engine efficiency

Exhibit 7: Toyota targets thermal efficiency of 50% Measures for raising thermal efficiency

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

(1) Turbo and direct-injection technology are the best combination

Technology for developing turbo engines using a variety of components has a long history. Recently, however, it has become

possible to increase engine efficiency through the combination of turbo and direct-injection technology (direct injection of fuel into

engine cylinders). The disadvantage of turbo technology is a temperature increase in the engine, and this can be kept in check

through the use of direct injection. The leading makers of turbo system parts are Honeywell, BorgWarner, Mitsubishi Heavy

Industries, and IHI, and these players dominate the industry. We forecast sales of vehicles with turbo engines will grow from 27% of

all auto sales in 2013, 45% in 2020, and 65% in 2025. We forecast a CAGR of 7.9% for turbo car sales over this 12-year period vs. a

CAGR of 3.1% for global auto sales.

Turbo/DownsizingProvide enough power by

using a smaller engine with supercharger

Conbustion systemOptimize the mix of fuel and air. HCCI performs

by forcibly igniting spontaneous combustion.

Flue gas treatmentAdd flue gas treatmentequipment (ex. DPF) to

reduce NOx and particle pollution

Fuel injectionThe engine operates with ideal combustion in the cylinder via direct fuel

injection

EGRThe engine toperates in the lean zone by using exhaust gas effectively

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 12

Exhibit 8: Turbo parts market is dominated by a few firms Turbocharger parts market share (2013)

Exhibit 9: Turbo market set to grow strongly Turbo market forecast

Source: Company data.

Source: Company data, Goldman Sachs Global Investment Research

Dealing with emissions the stumbling block for direct-injection engines

Direct-injection engines are helping greatly to boost fuel efficiency, but their emissions contain higher amounts of particulate matter.

Results of a study conducted by Japan’s National Institute for Environmental Studies in December 2013 show that direct-injection

engines emit over 10 times more particles than port injection engines. With tighter emission standards (Euro 6c standards) looming,

as we discuss later, we believe gasoline particulate filters (GPFs) will be adopted for use in gasoline engines, mainly in Europe.

Makers with a high market share in diesel particulate filters (DPFs) substrates for diesel engines will likely gain a strong presence in

GPFs also (given similar technical know-how). We think this holds true for the makers of DPF modules (or “canners” as some refer

to them). Leading companies like Tenneco and Faurecia have deep customer relationships, significant scale, and the capability to

design and manufacture emission solutions from the manifold to the tailpipe, leaving them in a good position to also benefit from

additional GPF content.

In fact, NGK Insulators (covered by Japan Electronic Components analyst, Daiki Takayama) announced in April 2014 that it will build

a new facility at its first plant in Poland (start production in January 2016). Our team expects it to commence the first mass

production of GPF. GPF accounts for a small weighting of new facility investment (€95 mn) and capacity expansion (honeycomb

equivalent of about 1.9X based on the total for cordierite products at the facility), and the main objective is to augment large

honeycomb and Cd-DPF. However, the company is also preparing for future GPF demand. NGK Insulators announced in January

29.3%

24.4%

16.8%

17.6%

8.6%

2.6%0.4% 0.3%

HoneywellBorgWarnerMitsubishi HeavyIHICumminsBoschContinentalOthers

0%

10%

20%

30%

40%

50%

60%

0

10

20

30

40

50

60

70

2013 2020E 2025E

Units (LHS)

Turbo ratio (RHS)

(mn units)

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 13

2015 that it will build a second plant in Poland (¥17 bn) and expand capacity for SiC-DPF (mainly for diesel passenger cars in Europe).

It has also announced that it will expand NOx sensor capacity in Japan and build a new facility in Thailand for Southeast Asia

(various products including honeycomb, large honeycomb, and DPF; cultivate demand in Southeast Asia and India toward 2020). It

is pursuing aggressive investment, targeting ¥56 bn in FY3/16 and a total of ¥150 bn in FY3/16-FY3/18, compared with companywide

annual average investment of around ¥30 bn in FY3/13-FY3/15. Our team expects a worldwide strengthening of fuel economy

regulations to help propel growth in the company’s ceramics business through 2020.

Exhibit 10: Emissions are a drawback of direct-injection engines

Direct-injection engine emission study

Exhibit 11: Three makers dominate the DPF substrate market

DPF substrates and module global share by volume (2014)

Source: National Institute for Environmental Studies (NIES)

Source: Company data, Goldman Sachs Global Investment Research

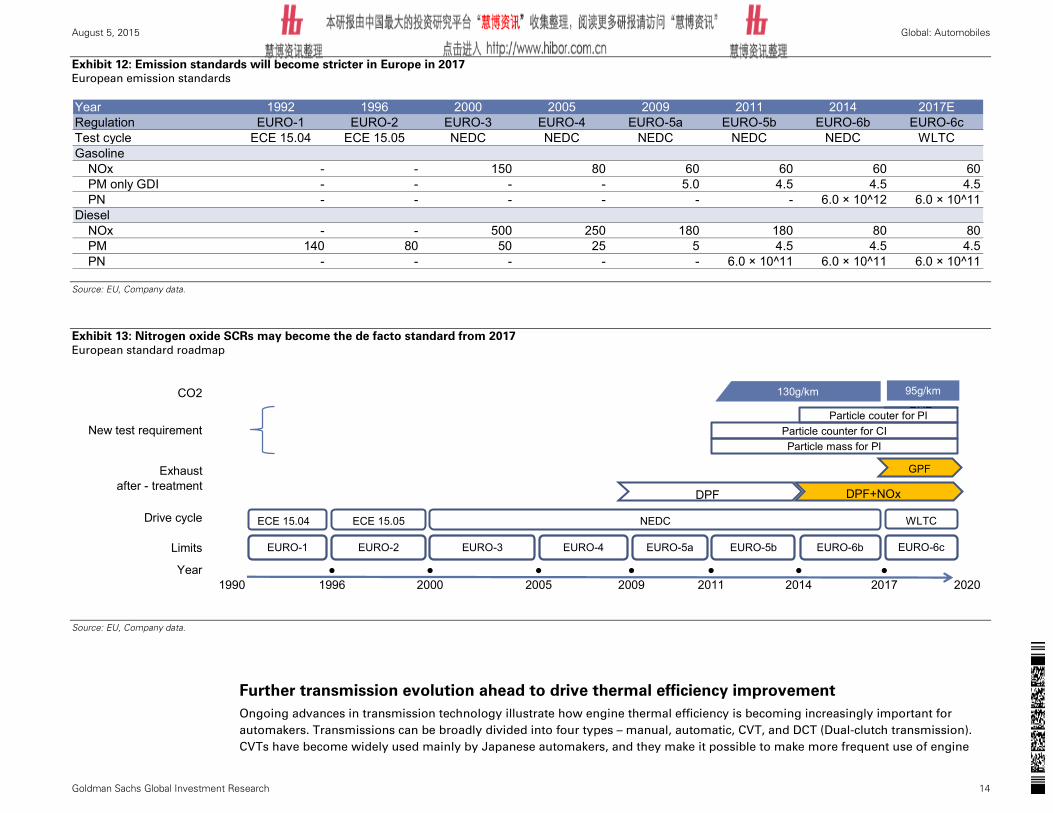

Costs to rise on adoption of Euro 6c emission standards in 2017

The Euro 6c emission standards scheduled to be adopted by Europe in 2017 call for the move to WLTP and strengthening of exhaust

gas particle standards (to one-tenth the level of the Euro 6b standards). Previously, particulate matter in emissions was regulated by

weight, but with this method it is hard to detect numerically ultra-fine particles that can easily enter the body. Strengthening of

particulate matter standards will make it necessary to measure and eliminate ultra-fine particles. To meet Euro 6c standards, new

gasoline engine cars will need to have gasoline particulate filters (GPF). Diesel engine cars will need urea selective catalyst reduction

(SCR) systems to eliminate particulate matter and nitrogen oxides, in addition to the diesel particulate filters (DPF) they are already

required to have. We expect this to increase cost by several hundred dollars per vehicle, which we believe could cause a decline in

demand of compact diesel engine cars as a proportion of overall new car sales.

Nor

mal

Gas

olin

e

Dire

ct fu

el(J

apan

)

Dire

ct fu

el(E

urop

e)1 x 1012

2 x 1012

3 x 1012

4 x 1012

5 x 1012

6 x 1012

7 x 1012

EURO regulation from 2014

EURO regulation from 2017

PM/N

Ox(

unit/

km)

NGK, 40%

Corning, 30%

Ibiden, 20%

Others, 10%

Faurecia, 26%

Tenneco, 15%

Eberspacher, 7%

Futaba, 7%

Yutaka Giken, 7%

Calsonic Kansei, 5%

Benteler, 4%Boysen, 4%

Magneti Marelli, 4%Sejong, 3%Module, 3%

Others, 15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Substrate Module

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 14

Exhibit 12: Emission standards will become stricter in Europe in 2017 European emission standards

Source: EU, Company data.

Exhibit 13: Nitrogen oxide SCRs may become the de facto standard from 2017

European standard roadmap

Source: EU, Company data.

Further transmission evolution ahead to drive thermal efficiency improvement

Ongoing advances in transmission technology illustrate how engine thermal efficiency is becoming increasingly important for

automakers. Transmissions can be broadly divided into four types – manual, automatic, CVT, and DCT (Dual-clutch transmission).

CVTs have become widely used mainly by Japanese automakers, and they make it possible to make more frequent use of engine

Year 1992 1996 2000 2005 2009 2011 2014 2017ERegulation EURO-1 EURO-2 EURO-3 EURO-4 EURO-5a EURO-5b EURO-6b EURO-6cTest cycle ECE 15.04 ECE 15.05 NEDC NEDC NEDC NEDC NEDC WLTCGasoline

NOx - - 150 80 60 60 60 60PM only GDI - - - - 5.0 4.5 4.5 4.5PN - - - - - - 6.0 × 10^12 6.0 × 10^11

DieselNOx - - 500 250 180 180 80 80PM 140 80 50 25 5 4.5 4.5 4.5PN - - - - - 6.0 × 10^11 6.0 × 10^11 6.0 × 10^11

CO2

New test requirement

DPF + NOx

Drive cycle

Limits

Year ● ● ● ● ● ● ●1990 1996 2000 2005 2009 2011 2014 2017 2020

Exhaustafter - treatment

EURO-1

GPF

EURO-2 EURO-3 EURO-4 EURO-5a EURO-5b EURO-6b EURO-6c

ECE 15.04 ECE 15.05 NEDC WLTC

Particle mass for PIParticle counter for CI

Particle couter for PIRDE

130g/km 95g/km

DPF+NOxDPF

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 15

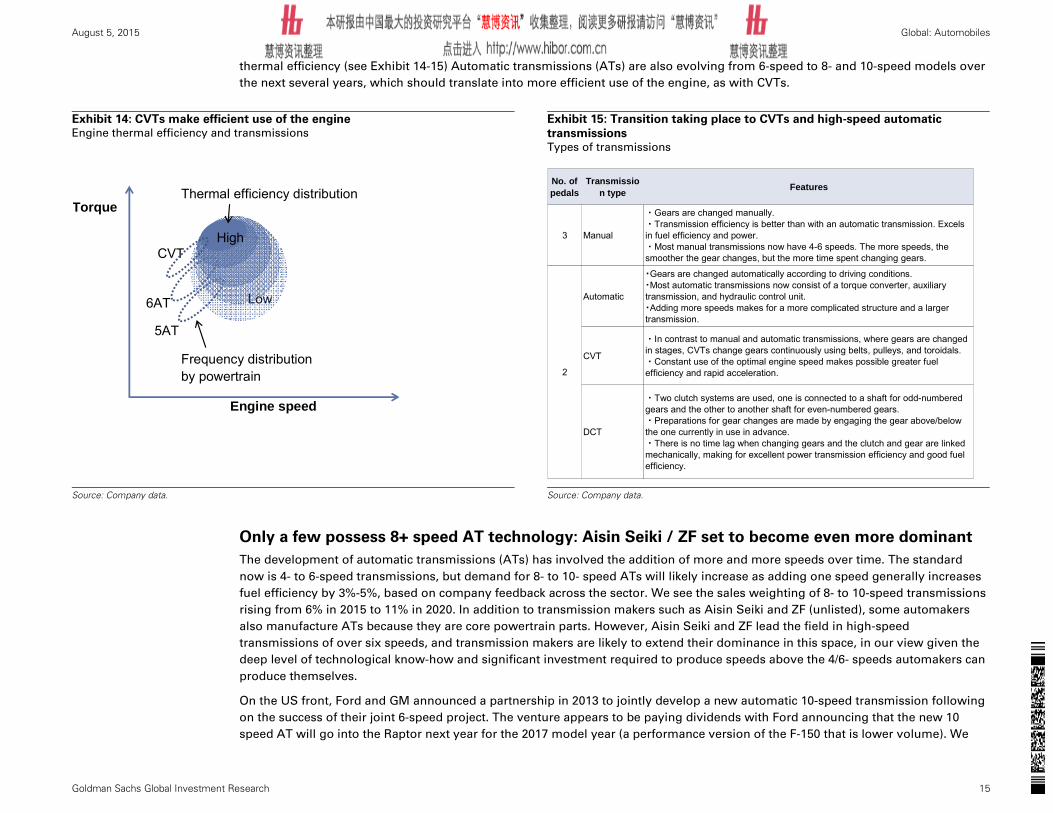

thermal efficiency (see Exhibit 14-15) Automatic transmissions (ATs) are also evolving from 6-speed to 8- and 10-speed models over

the next several years, which should translate into more efficient use of the engine, as with CVTs.

Exhibit 14: CVTs make efficient use of the engine Engine thermal efficiency and transmissions

Exhibit 15: Transition taking place to CVTs and high-speed automatic

transmissions Types of transmissions

Source: Company data.

Source: Company data.

Only a few possess 8+ speed AT technology: Aisin Seiki / ZF set to become even more dominant

The development of automatic transmissions (ATs) has involved the addition of more and more speeds over time. The standard

now is 4- to 6-speed transmissions, but demand for 8- to 10- speed ATs will likely increase as adding one speed generally increases

fuel efficiency by 3%-5%, based on company feedback across the sector. We see the sales weighting of 8- to 10-speed transmissions

rising from 6% in 2015 to 11% in 2020. In addition to transmission makers such as Aisin Seiki and ZF (unlisted), some automakers

also manufacture ATs because they are core powertrain parts. However, Aisin Seiki and ZF lead the field in high-speed

transmissions of over six speeds, and transmission makers are likely to extend their dominance in this space, in our view given the

deep level of technological know-how and significant investment required to produce speeds above the 4/6- speeds automakers can

produce themselves.

On the US front, Ford and GM announced a partnership in 2013 to jointly develop a new automatic 10-speed transmission following

on the success of their joint 6-speed project. The venture appears to be paying dividends with Ford announcing that the new 10

speed AT will go into the Raptor next year for the 2017 model year (a performance version of the F-150 that is lower volume). We

Thermal efficiency distribution

Frequency distributionby powertrain

Engine speed

Torque

Low

CVT

6AT

5AT

High

No. of pedals

Transmission type Features

3 Manual

・Gears are changed manually.・Transmission efficiency is better than with an automatic transmission. Excels in fuel efficiency and power.・Most manual transmissions now have 4-6 speeds. The more speeds, the smoother the gear changes, but the more time spent changing gears.

Automatic

・Gears are changed automatically according to driving conditions.・Most automatic transmissions now consist of a torque converter, auxiliary transmission, and hydraulic control unit.・Adding more speeds makes for a more complicated structure and a larger transmission.

CVT

・In contrast to manual and automatic transmissions, where gears are changed in stages, CVTs change gears continuously using belts, pulleys, and toroidals.・Constant use of the optimal engine speed makes possible greater fuel efficiency and rapid acceleration.

DCT

・Two clutch systems are used, one is connected to a shaft for odd-numbered gears and the other to another shaft for even-numbered gears.・Preparations for gear changes are made by engaging the gear above/below the one currently in use in advance.・There is no time lag when changing gears and the clutch and gear are linked mechanically, making for excellent power transmission efficiency and good fuel efficiency.

2

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 16

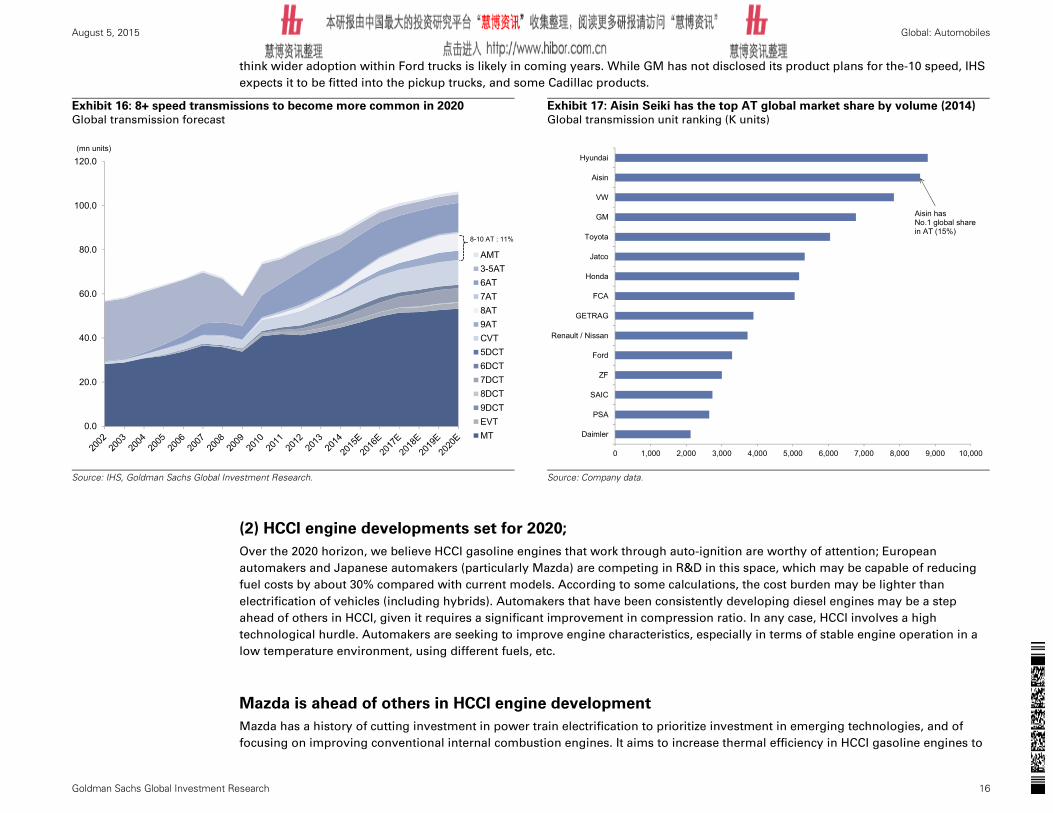

think wider adoption within Ford trucks is likely in coming years. While GM has not disclosed its product plans for the-10 speed, IHS

expects it to be fitted into the pickup trucks, and some Cadillac products.

Exhibit 16: 8+ speed transmissions to become more common in 2020 Global transmission forecast

Exhibit 17: Aisin Seiki has the top AT global market share by volume (2014) Global transmission unit ranking (K units)

Source: IHS, Goldman Sachs Global Investment Research.

Source: Company data.

(2) HCCI engine developments set for 2020;

Over the 2020 horizon, we believe HCCI gasoline engines that work through auto-ignition are worthy of attention; European

automakers and Japanese automakers (particularly Mazda) are competing in R&D in this space, which may be capable of reducing

fuel costs by about 30% compared with current models. According to some calculations, the cost burden may be lighter than

electrification of vehicles (including hybrids). Automakers that have been consistently developing diesel engines may be a step

ahead of others in HCCI, given it requires a significant improvement in compression ratio. In any case, HCCI involves a high

technological hurdle. Automakers are seeking to improve engine characteristics, especially in terms of stable engine operation in a

low temperature environment, using different fuels, etc.

Mazda is ahead of others in HCCI engine development

Mazda has a history of cutting investment in power train electrification to prioritize investment in emerging technologies, and of

focusing on improving conventional internal combustion engines. It aims to increase thermal efficiency in HCCI gasoline engines to

0.0

20.0

40.0

60.0

80.0

100.0

120.0

AMT3-5AT6AT7AT8AT9ATCVT5DCT6DCT7DCT8DCT9DCTEVTMT

8-10 AT : 11%

(mn units)

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

Daimler

PSA

SAIC

ZF

Ford

Renault / Nissan

GETRAG

FCA

Honda

Jatco

Toyota

GM

VW

Aisin

Hyundai

Aisin has No.1 global share in AT (15%)

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 17

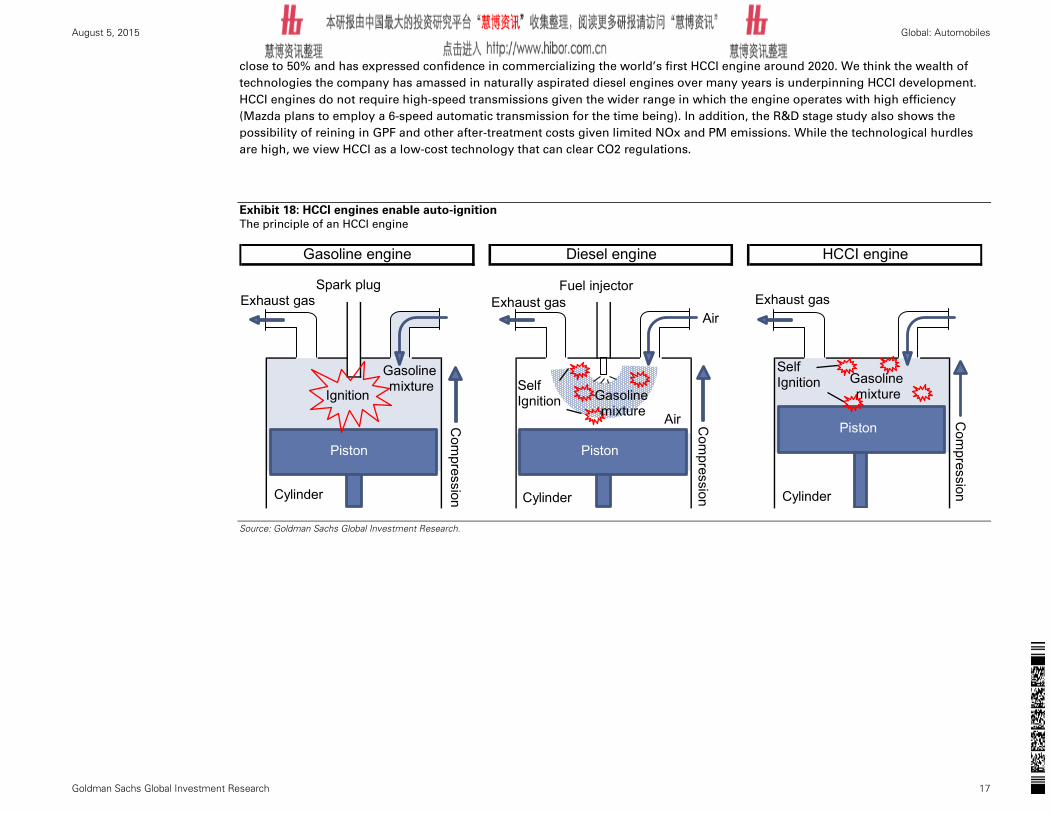

close to 50% and has expressed confidence in commercializing the world’s first HCCI engine around 2020. We think the wealth of

technologies the company has amassed in naturally aspirated diesel engines over many years is underpinning HCCI development.

HCCI engines do not require high-speed transmissions given the wider range in which the engine operates with high efficiency

(Mazda plans to employ a 6-speed automatic transmission for the time being). In addition, the R&D stage study also shows the

possibility of reining in GPF and other after-treatment costs given limited NOx and PM emissions. While the technological hurdles

are high, we view HCCI as a low-cost technology that can clear CO2 regulations.

Exhibit 18: HCCI engines enable auto-ignition

The principle of an HCCI engine

Source: Goldman Sachs Global Investment Research.

Gasoline engine Diesel engine HCCI engine

Ignition

Piston

Cylinder

Spark plug

Piston

Fuel injector

Air Piston

Exhaust gas Exhaust gas Exhaust gas

Gasolinemixture

Gasolinemixture

Cylinder Cylinder

Air

SelfIgnition

SelfIgnition Gasoline

mixture

Com

pression

Com

pression

Com

pression

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 18

Electric Vehicles (EVs): Tesla’s Gigafactory key to EV growth

We think the major hurdle to greater market penetration by EVs/PHEVs has been the high cost of Li-ion batteries, but Tesla

and its partner Panasonic see the potential for their Gigafactory, which they expect to be operational by late 2016 and

ultimately ramping up to 50 GWh of capacity, to cut battery costs by 30%-40%. EV sales have been fairly moderate for the

last several years, but we think sales could reaccelerate if the industry can develop an affordable EV with a long travel

distance per charge. FCVs are often discussed in contrast to EVs and the debate often focuses on which technology will win

out over the other. Given each technology has its own idiosyncrasies and varying energy policies adopted around the world,

we see FCV and EV as technologies that can co-exist rather than compete. Our EV sales volume projection for 2025 is 3 mn

units (this would still make the EV market small – we project sales of 17 mn HVs by 2025).

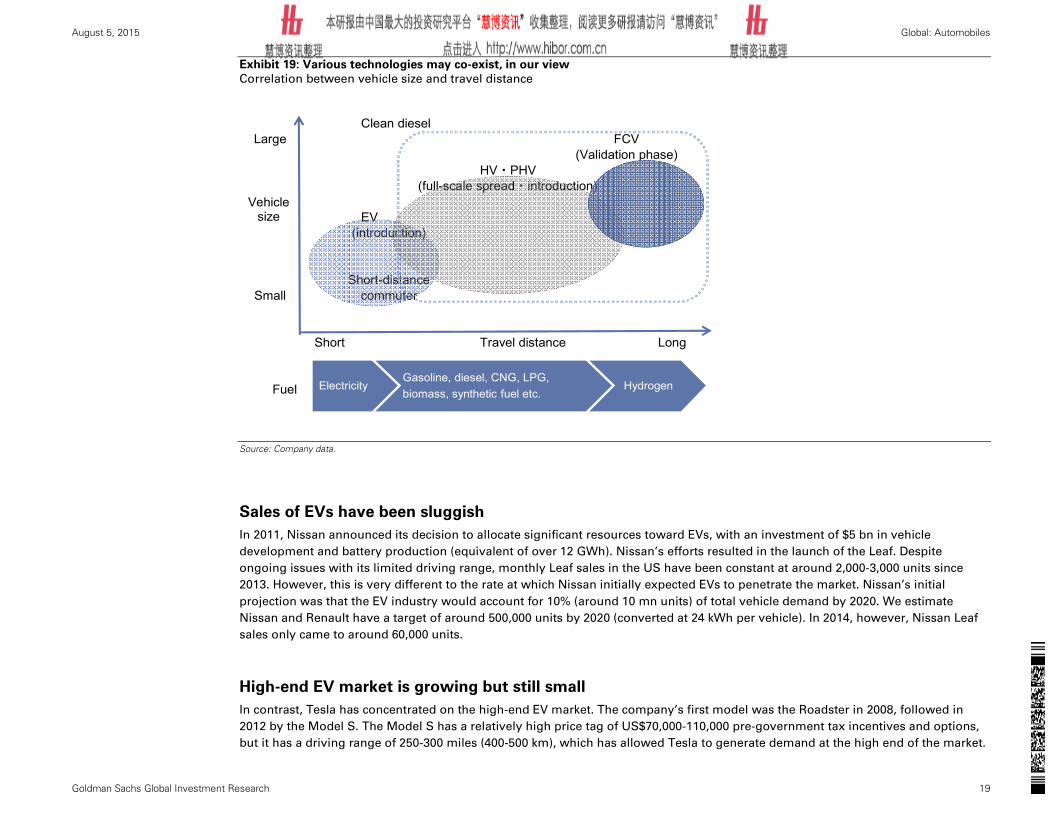

EV vs. FCV view is mistaken; coexisting technologies

The arrival of FCVs is often discussed in contrast to EVs. However, the two technologies can coexist, and they should not be viewed

as an either/or choice. FCVs have the advantages of longer driving ranges and shorter fill-up times (three minutes), but also the

disadvantages of vehicle size restrictions and hydrogen infrastructure development. EVs have the advantage of simple construction

of charging stations, but the disadvantages of low driving ranges and battery degradation. In fact, most EV driving ranges are

limited to around 100 miles (160 kms), although we note Tesla is an important exception with a median range of 265 miles (425 kms)

per charge. We think the use and appeal of FCVs and EVs could differ depending on the driving distance needs of consumers.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 19

Exhibit 19: Various technologies may co-exist, in our view

Correlation between vehicle size and travel distance

Source: Company data.

Sales of EVs have been sluggish

In 2011, Nissan announced its decision to allocate significant resources toward EVs, with an investment of $5 bn in vehicle

development and battery production (equivalent of over 12 GWh). Nissan’s efforts resulted in the launch of the Leaf. Despite

ongoing issues with its limited driving range, monthly Leaf sales in the US have been constant at around 2,000-3,000 units since

2013. However, this is very different to the rate at which Nissan initially expected EVs to penetrate the market. Nissan’s initial

projection was that the EV industry would account for 10% (around 10 mn units) of total vehicle demand by 2020. We estimate

Nissan and Renault have a target of around 500,000 units by 2020 (converted at 24 kWh per vehicle). In 2014, however, Nissan Leaf

sales only came to around 60,000 units.

High-end EV market is growing but still small

In contrast, Tesla has concentrated on the high-end EV market. The company’s first model was the Roadster in 2008, followed in

2012 by the Model S. The Model S has a relatively high price tag of US$70,000-110,000 pre-government tax incentives and options,

but it has a driving range of 250-300 miles (400-500 km), which has allowed Tesla to generate demand at the high end of the market.

Clean dieselLarge FCV

(Validation phase)HV・PHV

(full-scale spread・introduction)

EV(introduction)

Short-distanceSmall commuter

Short Travel distance Long

Fuel Electricity Gasoline, diesel, CNG, LPG, biomass, synthetic fuel etc.

Hydrogen

Vehiclesize

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 20

Model S sales were just over 30,000 units last year, which is low volume, but growth is fast; the company is set to hit 55,000

deliveries this year and is expecting over 100,000 next year, following the addition of the Model X to the lineup.

Exhibit 20: Constant demand in low-price EVs Nissan Leaf sales in US

Exhibit 21: Travel distance of EVS is relatively short Travel distance of EVs in market

Source: Autodata.

Source: Company data, Nikkei Automotive.

Initial market penetration slow, but new entrant technologies could revive sales momentum

EV sales over the past several years did not necessarily meet initial expectations. However, structural advantages of EVs have

allowed companies from other industries to enter the market which could signal the first step toward renewed growth. EVs have

only about one-third of the number of components of on board vehicles powered by a gasoline engine. As a result; (1) the ability to

coordinate and integrate production across several fronts, which is a key strength of conventional automakers, as well as (2) their

supplier management practices, are not necessarily a competitive advantage. Hence, a breakthrough in battery technology could

dramatically change the EV competitive landscape, given Li-ion batteries account for around 50% of the cost of an EV.

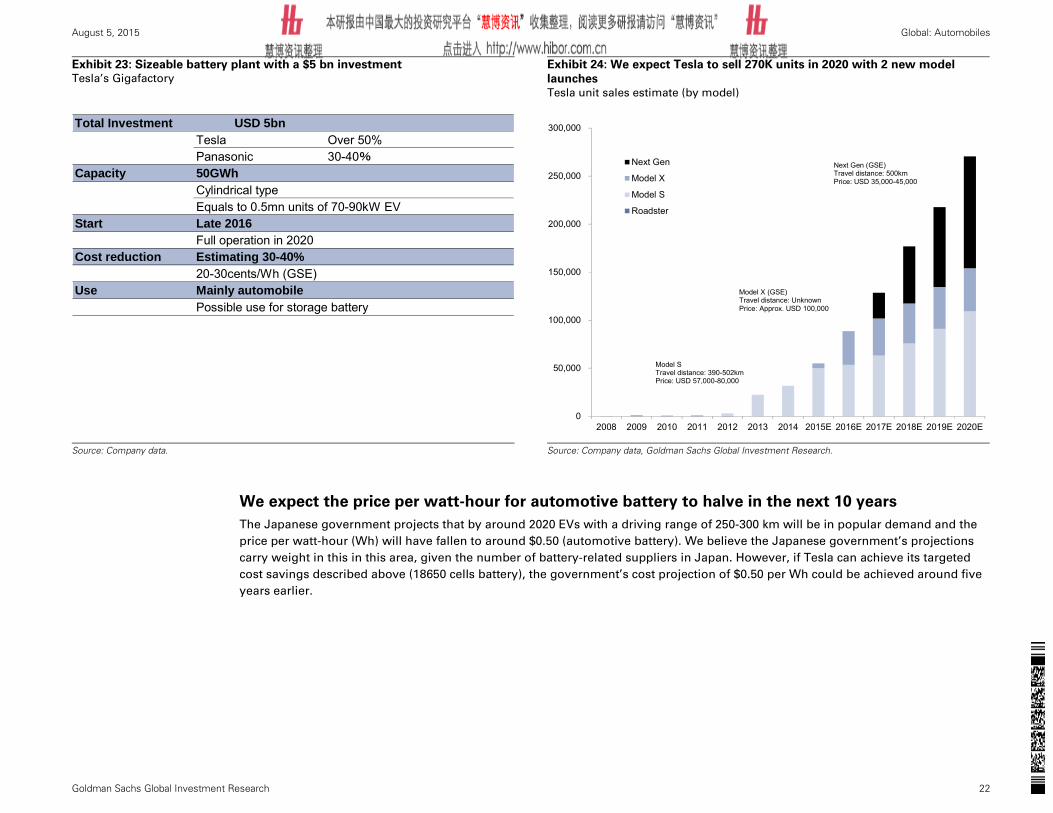

Tesla slated to start operation of its Gigafactory from 2017

While the battery technology required to realize vehicle electrification continues to develop rapidly, we expect the outcome of

Tesla’s Gigafactory initiative to be a significant turning point over the next five to ten years. Part of what drives this less crowded

field is Tesla’s advantage in battery cost. As we have highlighted in the past, Tesla has been very successful in taking cost out of its

battery packs over time, taking the cost down from $550/kWh for the original Roadster to about $250/kWh for the Model S based on

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jan-

13Fe

b-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug-

13Se

p-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug-

14Se

p-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15

Leaf

Model S (Tesla)Model X (Tesla)

Model 3 (Tesla)

Q8 e-tron (Audi)

R8 e-tron (Audi)

i3 (BMW)B-class (ML)

Bolt (Chevrolet)

Spark (Chevrolet)

E-Gold (VW)

Focus (Ford)

i-MiEV (MMC)

Soul EV (kia)

500e (Fiat)Leaf (Nissan)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

0 50 100 150 200 250 300 350 400Travel distance(mile)

Price($)

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 21

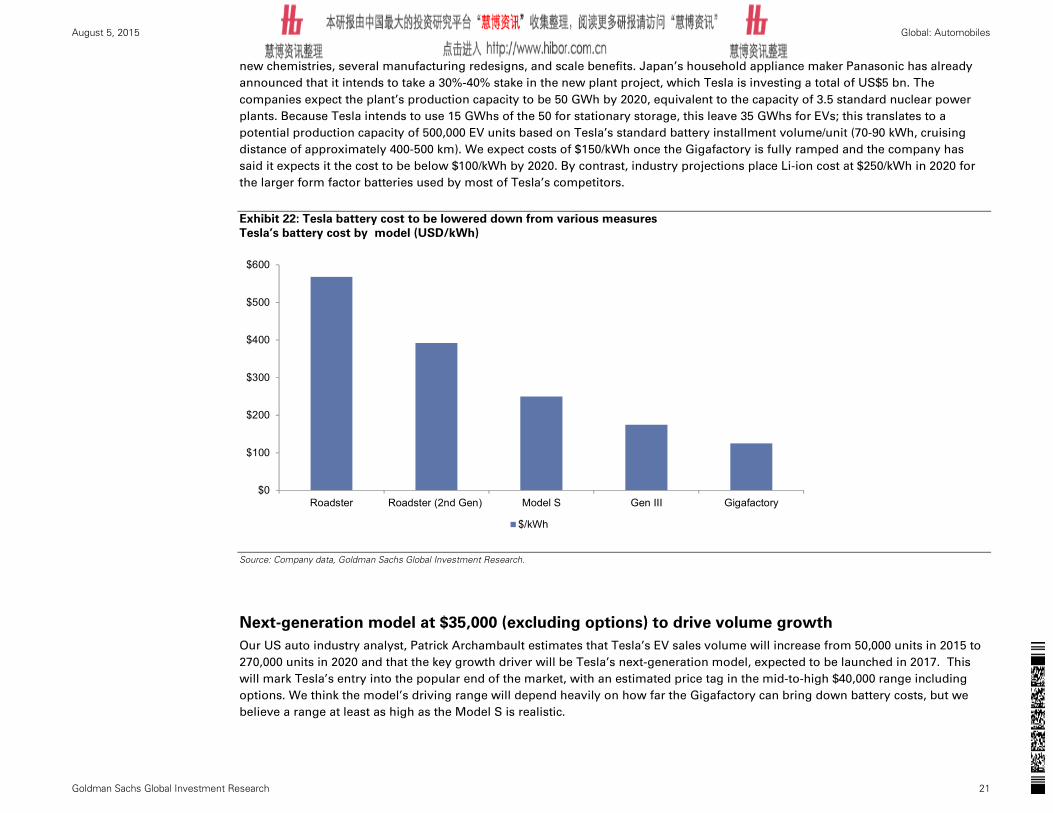

new chemistries, several manufacturing redesigns, and scale benefits. Japan’s household appliance maker Panasonic has already

announced that it intends to take a 30%-40% stake in the new plant project, which Tesla is investing a total of US$5 bn. The

companies expect the plant’s production capacity to be 50 GWh by 2020, equivalent to the capacity of 3.5 standard nuclear power

plants. Because Tesla intends to use 15 GWhs of the 50 for stationary storage, this leave 35 GWhs for EVs; this translates to a

potential production capacity of 500,000 EV units based on Tesla’s standard battery installment volume/unit (70-90 kWh, cruising

distance of approximately 400-500 km). We expect costs of $150/kWh once the Gigafactory is fully ramped and the company has

said it expects it the cost to be below $100/kWh by 2020. By contrast, industry projections place Li-ion cost at $250/kWh in 2020 for

the larger form factor batteries used by most of Tesla’s competitors.

Exhibit 22: Tesla battery cost to be lowered down from various measures

Tesla’s battery cost by model (USD/kWh)

Source: Company data, Goldman Sachs Global Investment Research.

Next-generation model at $35,000 (excluding options) to drive volume growth

Our US auto industry analyst, Patrick Archambault estimates that Tesla’s EV sales volume will increase from 50,000 units in 2015 to

270,000 units in 2020 and that the key growth driver will be Tesla’s next-generation model, expected to be launched in 2017. This

will mark Tesla’s entry into the popular end of the market, with an estimated price tag in the mid-to-high $40,000 range including

options. We think the model’s driving range will depend heavily on how far the Gigafactory can bring down battery costs, but we

believe a range at least as high as the Model S is realistic.

$0

$100

$200

$300

$400

$500

$600

Roadster Roadster (2nd Gen) Model S Gen III Gigafactory

$/kWh

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 22

Exhibit 23: Sizeable battery plant with a $5 bn investment Tesla’s Gigafactory

Exhibit 24: We expect Tesla to sell 270K units in 2020 with 2 new model

launches

Tesla unit sales estimate (by model)

Source: Company data.

Source: Company data, Goldman Sachs Global Investment Research.

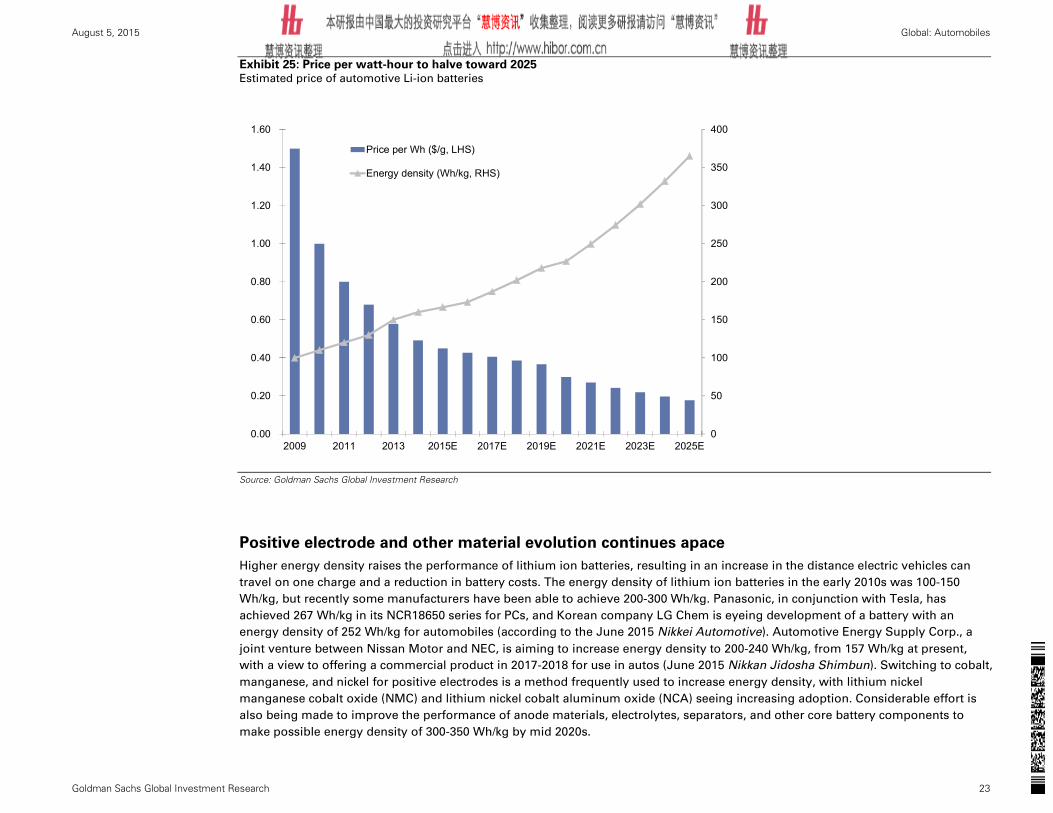

We expect the price per watt-hour for automotive battery to halve in the next 10 years

The Japanese government projects that by around 2020 EVs with a driving range of 250-300 km will be in popular demand and the

price per watt-hour (Wh) will have fallen to around $0.50 (automotive battery). We believe the Japanese government’s projections

carry weight in this in this area, given the number of battery-related suppliers in Japan. However, if Tesla can achieve its targeted

cost savings described above (18650 cells battery), the government’s cost projection of $0.50 per Wh could be achieved around five

years earlier.

Total Investment USD 5bnTesla Over 50%Panasonic 30-40%

Capacity 50GWhCylindrical typeEquals to 0.5mn units of 70-90kW EV

Start Late 2016Full operation in 2020

Cost reduction Estimating 30-40%20-30cents/Wh (GSE)

Use Mainly automobilePossible use for storage battery

0

50,000

100,000

150,000

200,000

250,000

300,000

2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

Next Gen

Model X

Model S

Roadster

Next Gen (GSE)Travel distance: 500kmPrice: USD 35,000-45,000

Model X (GSE)Travel distance: UnknownPrice: Approx. USD 100,000

Model STravel distance: 390-502kmPrice: USD 57,000-80,000

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 23

Exhibit 25: Price per watt-hour to halve toward 2025 Estimated price of automotive Li-ion batteries

Source: Goldman Sachs Global Investment Research

Positive electrode and other material evolution continues apace

Higher energy density raises the performance of lithium ion batteries, resulting in an increase in the distance electric vehicles can

travel on one charge and a reduction in battery costs. The energy density of lithium ion batteries in the early 2010s was 100-150

Wh/kg, but recently some manufacturers have been able to achieve 200-300 Wh/kg. Panasonic, in conjunction with Tesla, has

achieved 267 Wh/kg in its NCR18650 series for PCs, and Korean company LG Chem is eyeing development of a battery with an

energy density of 252 Wh/kg for automobiles (according to the June 2015 Nikkei Automotive). Automotive Energy Supply Corp., a

joint venture between Nissan Motor and NEC, is aiming to increase energy density to 200-240 Wh/kg, from 157 Wh/kg at present,

with a view to offering a commercial product in 2017-2018 for use in autos (June 2015 Nikkan Jidosha Shimbun). Switching to cobalt,

manganese, and nickel for positive electrodes is a method frequently used to increase energy density, with lithium nickel

manganese cobalt oxide (NMC) and lithium nickel cobalt aluminum oxide (NCA) seeing increasing adoption. Considerable effort is

also being made to improve the performance of anode materials, electrolytes, separators, and other core battery components to

make possible energy density of 300-350 Wh/kg by mid 2020s.

0

50

100

150

200

250

300

350

400

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2009 2011 2013 2015E 2017E 2019E 2021E 2023E 2025E

Price per Wh ($/g, LHS)

Energy density (Wh/kg, RHS)

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 24

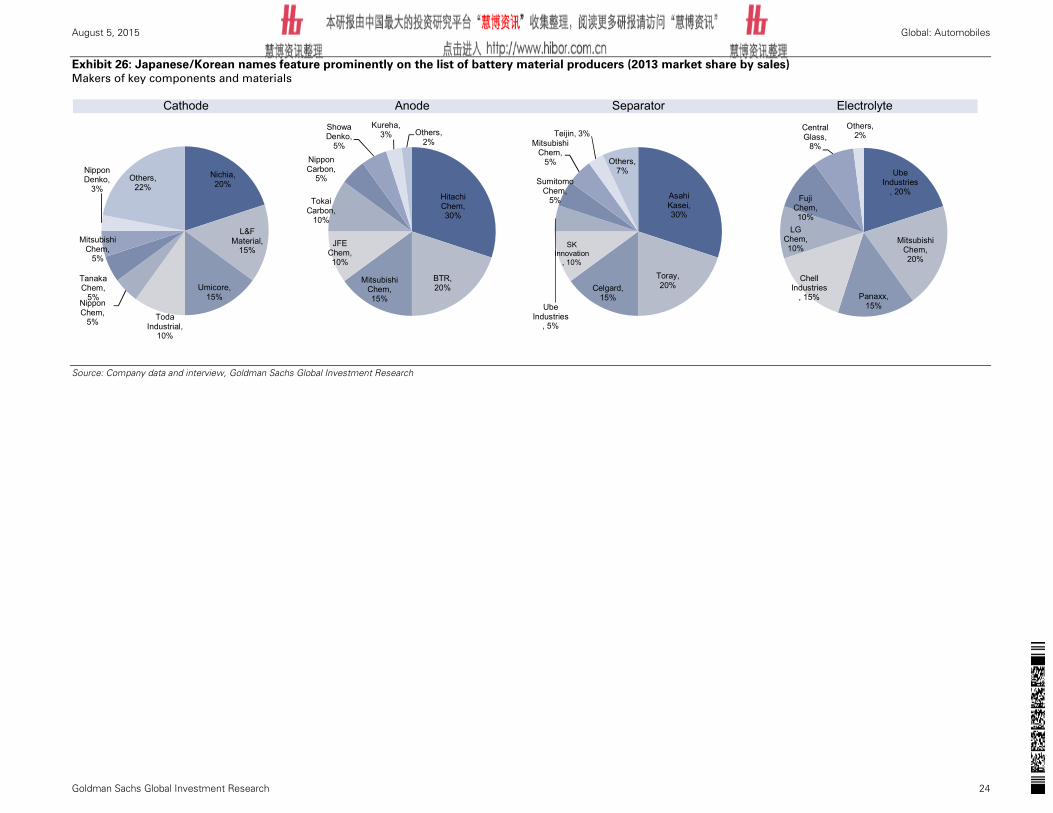

Exhibit 26: Japanese/Korean names feature prominently on the list of battery material producers (2013 market share by sales) Makers of key components and materials

Source: Company data and interview, Goldman Sachs Global Investment Research

Cathode Anode Separator Electrolyte

Nichia, 20%

L&F Material,

15%

Umicore, 15%

Toda Industrial,

10%

Nippon Chem,

5%

Tanaka Chem,

5%

Mitsubishi Chem,

5%

Nippon Denko,

3%Others,

22%Hitachi Chem, 30%

BTR, 20%

Mitsubishi Chem, 15%

JFE Chem, 10%

Tokai Carbon,

10%

Nippon Carbon,

5%

Showa Denko,

5%

Kureha, 3% Others,

2%

Asahi Kasei, 30%

Toray, 20%Celgard,

15%

SK Innovation

, 10%

Ube Industries

, 5%

Sumitomo Chem,

5%

Mitsubishi Chem,

5%

Teijin, 3%

Others, 7% Ube

Industries, 20%

Mitsubishi Chem, 20%

Panaxx, 15%

Chell Industries

, 15%

LG Chem, 10%

Fuji Chem, 10%

Central Glass,

8%

Others, 2%

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 25

Fuel Cell Vehicles (FCVs): The ultimate eco-car?

Toyota released the world’s first commercially available FCV, the Mirai, in December 2014. This represented a major step

toward the achievement of a hydrogen-based society. FCVs face many obstacles –cost, infrastructure, and regulatory

reform– that are yet to be overcome but the technology has significant medium-term potential from an energy

diversification and CO2 emission reduction standpoint. We expect FCV sales volumes to start increasing mainly in Japan

and California from 2020 given strong regulatory focus on emissions reduction.

Toyota releases long-awaited mass-production FCV

We think FCVs stand alongside EVs as a technology that could transform automobile internal combustion engines in 10 years.

Gasoline-powered vehicles generate power by burning gasoline, whereas FCVs generate power using hydrogen as fuel and onboard

fuel cells. These vehicles are also known as fuel cell electric vehicles (FCEVs) because they combine elements of EVs to use

generated electricity to drive the motor. Toyota released the Mirai as the world’s first mass-production FCV in December 2014. The

vehicle is priced at ¥7.24 mn (US$60,000), or ¥5.22 mn (US$43,000) after subsidies, which is high compared with ¥4.22 mn

(US$35,000) for the similar class Crown HV. Toyota developed the Mirai using parts from existing models, including the motor and

inverters from the Harrier HV and rechargeable batteries from the Camry, but we think the fuel cells and tank likely increased costs

significantly. FCV consumer awareness is still not high, but governments in Japan, California, Germany, UK, and elsewhere have

taken aggressive stances on their penetration through various regulations and subsidies.

Competitors prepare to follow Toyota’s foray into FCVs

Honda plans to release a mass-production FCV sedan in FY3/16, roughly one year after the Toyota Mirai. Nissan plans to release an

FCV developed jointly with Daimler and Ford in 2017. Volkswagen is also developing an FCV, although the release timing is unclear.

Hyundai released an FCV in 2013, but we estimate that most of these were sold for fleet use rather than to general consumers.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 26

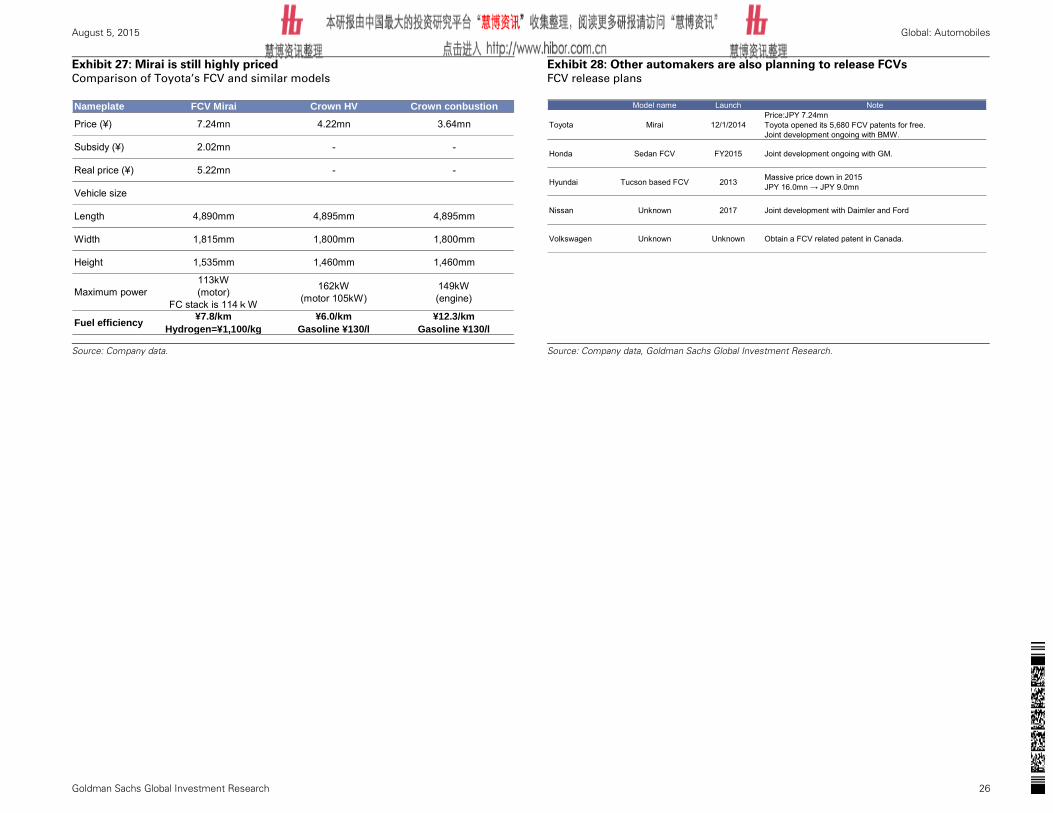

Exhibit 27: Mirai is still highly priced Comparison of Toyota’s FCV and similar models

Exhibit 28: Other automakers are also planning to release FCVs FCV release plans

Source: Company data.

Source: Company data, Goldman Sachs Global Investment Research.

Nameplate FCV Mirai Crown HV Crown conbustion

Price (¥) 7.24mn 4.22mn 3.64mn

Subsidy (¥) 2.02mn - -

Real price (¥) 5.22mn - -

Vehicle size

Length 4,890mm 4,895mm 4,895mm

Width 1,815mm 1,800mm 1,800mm

Height 1,535mm 1,460mm 1,460mm

Maximum power113kW(motor)

FC stack is 114kW

162kW(motor 105kW)

149kW(engine)

Fuel efficiency ¥7.8/kmHydrogen=¥1,100/kg

¥6.0/kmGasoline ¥130/l

¥12.3/kmGasoline ¥130/l

Model name Launch Note

Toyota Mirai 12/1/2014Price:JPY 7.24mnToyota opened its 5,680 FCV patents for free. Joint development ongoing with BMW.

Honda Sedan FCV FY2015 Joint development ongoing with GM.

Hyundai Tucson based FCV 2013 Massive price down in 2015JPY 16.0mn → JPY 9.0mn

Nissan Unknown 2017 Joint development with Daimler and Ford

Volkswagen Unknown Unknown Obtain a FCV related patent in Canada.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 27

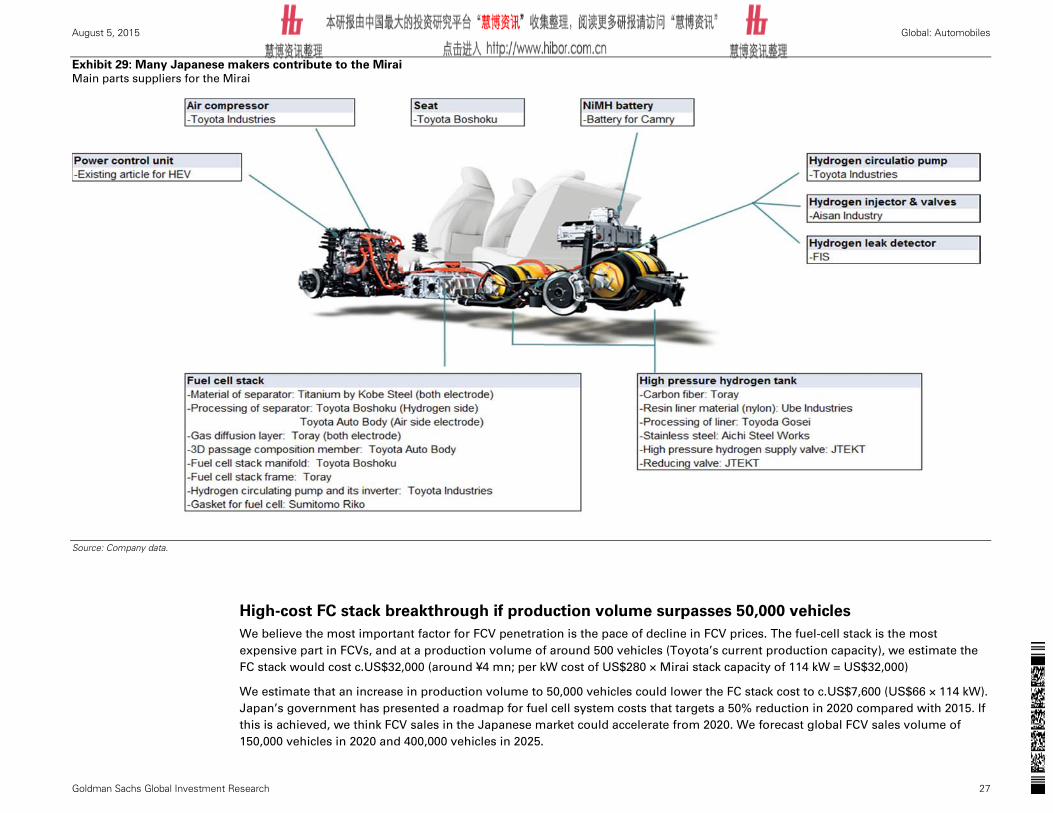

Exhibit 29: Many Japanese makers contribute to the Mirai Main parts suppliers for the Mirai

Source: Company data.

High-cost FC stack breakthrough if production volume surpasses 50,000 vehicles

We believe the most important factor for FCV penetration is the pace of decline in FCV prices. The fuel-cell stack is the most

expensive part in FCVs, and at a production volume of around 500 vehicles (Toyota’s current production capacity), we estimate the

FC stack would cost c.US$32,000 (around ¥4 mn; per kW cost of US$280 × Mirai stack capacity of 114 kW = US$32,000)

We estimate that an increase in production volume to 50,000 vehicles could lower the FC stack cost to c.US$7,600 (US$66 × 114 kW).

Japan’s government has presented a roadmap for fuel cell system costs that targets a 50% reduction in 2020 compared with 2015. If

this is achieved, we think FCV sales in the Japanese market could accelerate from 2020. We forecast global FCV sales volume of

150,000 vehicles in 2020 and 400,000 vehicles in 2025.

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 28

Exhibit 30: Global FCV penetration in 2020/2025 FCV penetration plans

Exhibit 31: FC costs fall sharply at a production volume of 50,000 vehicles Production volume and cost per kW

Source: New Energy and Industrial Technology Development Organization (NEDO)

Source: New Energy and Industrial Technology Development Organization (NEDO)

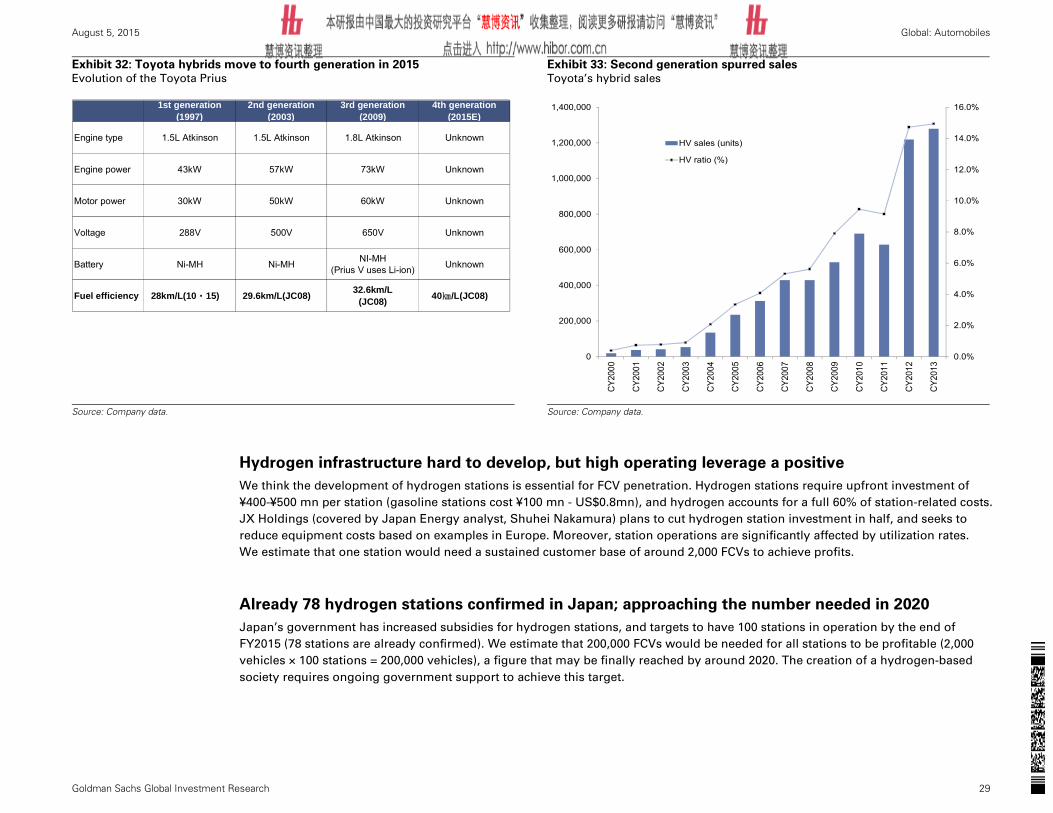

Major advances in Toyota’s second generation Prius HV

We wonder if anyone could have accurately forecasted the current sales volume of hybrid vehicles (HVs) 18 years ago, when Toyota

presented the Prius to the world as the first HV in 1997. The model had a strong tailwind from high energy prices, but HVs are now

viewed as a mainstream rather than stopgap technology by the world’s automakers. In particular, we find it interesting that Prius

sales volumes accelerated following the release of the second-generation model in 2003. This suggests that perhaps we should not

focus too much on volumes for the first generation of FCVs, given quality and emphasis on production technology maturity is their

key focus. We think the second generation of FCVs planned for release around 2020 will mark the full start of hydrogen vehicles.

Region Plan/estimate Plan

Japan CY2025E:Total 2mn units 1,000 H2 station. 2,000 cars/station.

US CA CY2017E:53thous units Conducting interviews on ZEV regulation to auto makers3.3mn ZEVs until 2025 in CA+7states

Germany CY2023E:0.5mn units Next National Implementation Plan (Jun. 2013)

England CY2030E:1.6mn units UK H2Mobility project (Apr. 2013)

South Korea CY2020E:0.1mn units Green Growth National Committee (Dec. 2010)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2015E 2020E 2025E

South KoreaEnglandGermanyUS CAJapan

280.33

103.58

66.6854.83

0

50

100

150

200

250

300

0 100,000 200,000 300,000 400,000 500,000 600,000

(USD/kW)

(Production)

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 29

Exhibit 32: Toyota hybrids move to fourth generation in 2015 Evolution of the Toyota Prius

Exhibit 33: Second generation spurred sales Toyota’s hybrid sales

Source: Company data.

Source: Company data.

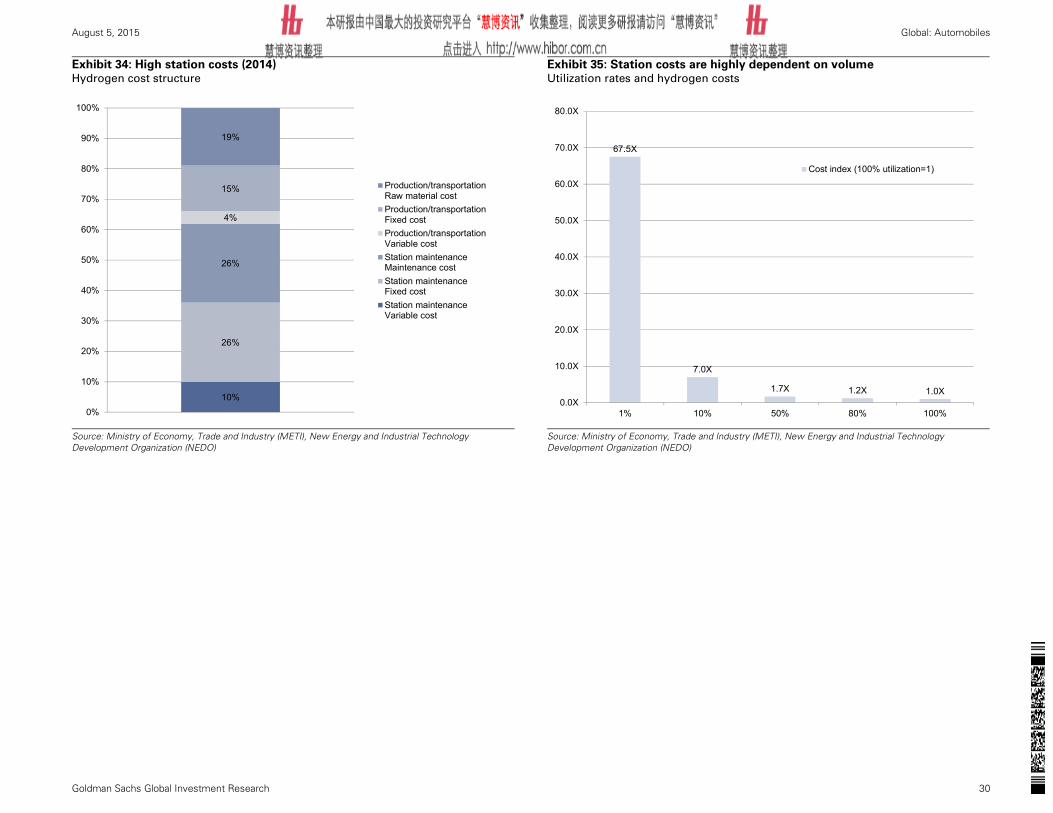

Hydrogen infrastructure hard to develop, but high operating leverage a positive

We think the development of hydrogen stations is essential for FCV penetration. Hydrogen stations require upfront investment of

¥400-¥500 mn per station (gasoline stations cost ¥100 mn - US$0.8mn), and hydrogen accounts for a full 60% of station-related costs.

JX Holdings (covered by Japan Energy analyst, Shuhei Nakamura) plans to cut hydrogen station investment in half, and seeks to

reduce equipment costs based on examples in Europe. Moreover, station operations are significantly affected by utilization rates.

We estimate that one station would need a sustained customer base of around 2,000 FCVs to achieve profits.

Already 78 hydrogen stations confirmed in Japan; approaching the number needed in 2020

Japan’s government has increased subsidies for hydrogen stations, and targets to have 100 stations in operation by the end of

FY2015 (78 stations are already confirmed). We estimate that 200,000 FCVs would be needed for all stations to be profitable (2,000

vehicles × 100 stations = 200,000 vehicles), a figure that may be finally reached by around 2020. The creation of a hydrogen-based

society requires ongoing government support to achieve this target.

1st generation(1997)

2nd generation(2003)

3rd generation(2009)

4th generation(2015E)

Engine type 1.5L Atkinson 1.5L Atkinson 1.8L Atkinson Unknown

Engine power 43kW 57kW 73kW Unknown

Motor power 30kW 50kW 60kW Unknown

Voltage 288V 500V 650V Unknown

Battery Ni-MH Ni-MH NI-MH(Prius V uses Li-ion) Unknown

Fuel efficiency 28km/L(10・15) 29.6km/L(JC08) 32.6km/L(JC08) 40㎞ /L(JC08)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

CY2

000

CY2

001

CY2

002

CY2

003

CY2

004

CY2

005

CY2

006

CY2

007

CY2

008

CY2

009

CY2

010

CY2

011

CY2

012

CY2

013

HV sales (units)

HV ratio (%)

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 30

Exhibit 34: High station costs (2014) Hydrogen cost structure

Exhibit 35: Station costs are highly dependent on volume Utilization rates and hydrogen costs

Source: Ministry of Economy, Trade and Industry (METI), New Energy and Industrial Technology Development Organization (NEDO)

Source: Ministry of Economy, Trade and Industry (METI), New Energy and Industrial Technology Development Organization (NEDO)

10%

26%

26%

4%

15%

19%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Production/transportationRaw material costProduction/transportationFixed costProduction/transportationVariable costStation maintenanceMaintenance costStation maintenanceFixed costStation maintenanceVariable cost

67.5X

7.0X

1.7X 1.2X 1.0X0.0X

10.0X

20.0X

30.0X

40.0X

50.0X

60.0X

70.0X

80.0X

1% 10% 50% 80% 100%

Cost index (100% utilization=1)

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 31

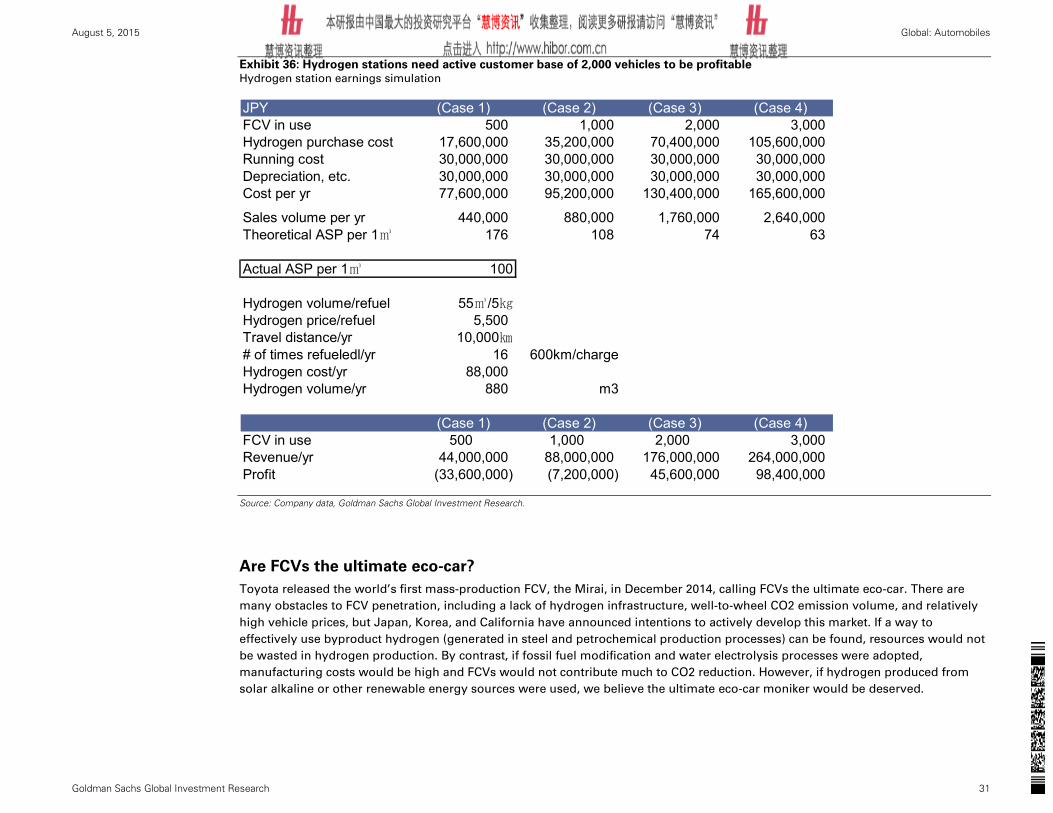

Exhibit 36: Hydrogen stations need active customer base of 2,000 vehicles to be profitable Hydrogen station earnings simulation

Source: Company data, Goldman Sachs Global Investment Research.

Are FCVs the ultimate eco-car?

Toyota released the world’s first mass-production FCV, the Mirai, in December 2014, calling FCVs the ultimate eco-car. There are

many obstacles to FCV penetration, including a lack of hydrogen infrastructure, well-to-wheel CO2 emission volume, and relatively

high vehicle prices, but Japan, Korea, and California have announced intentions to actively develop this market. If a way to

effectively use byproduct hydrogen (generated in steel and petrochemical production processes) can be found, resources would not

be wasted in hydrogen production. By contrast, if fossil fuel modification and water electrolysis processes were adopted,

manufacturing costs would be high and FCVs would not contribute much to CO2 reduction. However, if hydrogen produced from

solar alkaline or other renewable energy sources were used, we believe the ultimate eco-car moniker would be deserved.

JPY (Case 1) (Case 2) (Case 3) (Case 4)FCV in use 500 1,000 2,000 3,000Hydrogen purchase cost 17,600,000 35,200,000 70,400,000 105,600,000Running cost 30,000,000 30,000,000 30,000,000 30,000,000Depreciation, etc. 30,000,000 30,000,000 30,000,000 30,000,000Cost per yr 77,600,000 95,200,000 130,400,000 165,600,000

Sales volume per yr 440,000 880,000 1,760,000 2,640,000Theoretical ASP per 1㎥ 176 108 74 63

Actual ASP per 1㎥ 100

Hydrogen volume/refuel 55㎥/5㎏Hydrogen price/refuel 5,500Travel distance/yr 10,000㎞# of times refueledl/yr 16 600km/chargeHydrogen cost/yr 88,000Hydrogen volume/yr 880 m3

(Case 1) (Case 2) (Case 3) (Case 4)FCV in use 500 1,000 2,000 3,000Revenue/yr 44,000,000 88,000,000 176,000,000 264,000,000Profit (33,600,000) (7,200,000) 45,600,000 98,400,000

August 5, 2015 Global: Automobiles

Goldman Sachs Global Investment Research 32

Exhibit 37: CO2 is sometimes produced in the hydrogen production process Well to Wheel CO2 g/km emission comparison

Exhibit 38: Hydrogen production methods and costs vary Hydrogen production methods

Source: Japan Automobile Research Institute (JARI), Ministry of Economy, Trade and Industry (METI), New Energy and Industrial Technology Development Organization (NEDO)

Source: Motor Fan

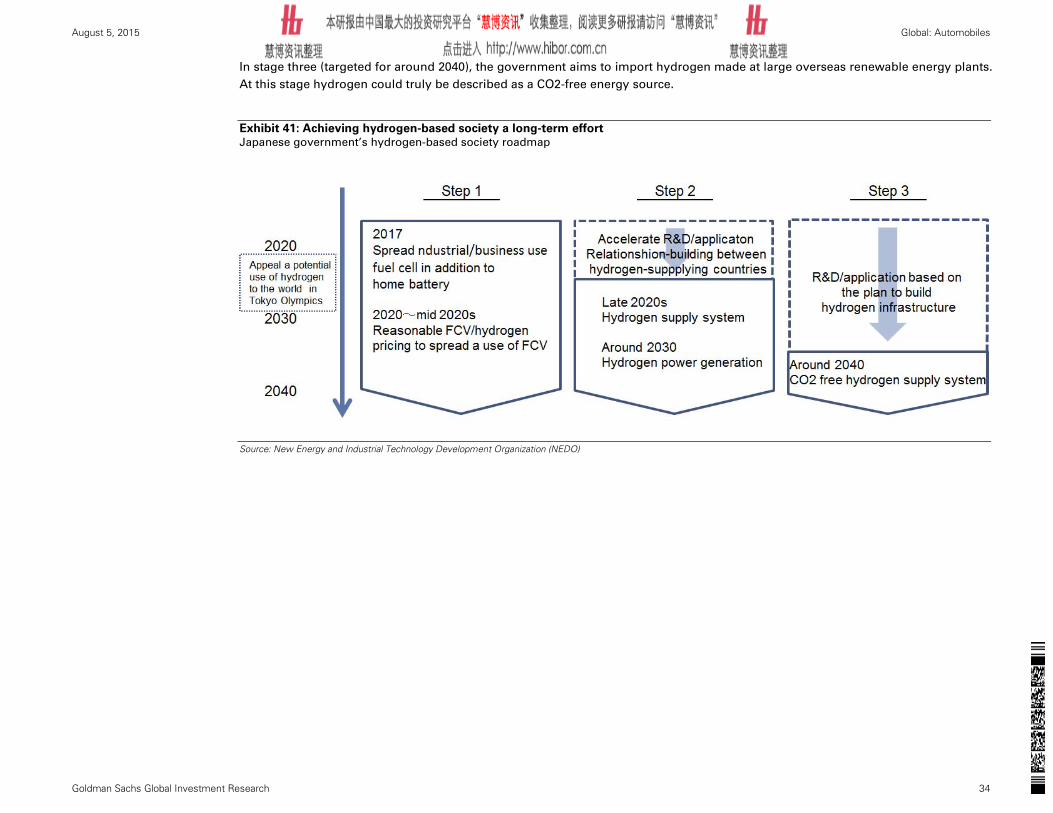

FCVs only one of the building blocks required to achieve a hydrogen-based society

The release of the Mirai created the impression among some that the transition to FCVs constitutes a shift to a hydrogen-based

society; in fact, FCVs are merely one step towards achieving a hydrogen-based society. Due to its lack of national energy resources,

Japan, in particular, plans to diversify its energy sources and take steps to achieve energy security. Amid poor visibility on the

nuclear power outlook, high expectations for hydrogen power generation as a means of addressing greenhouse gas regulations are

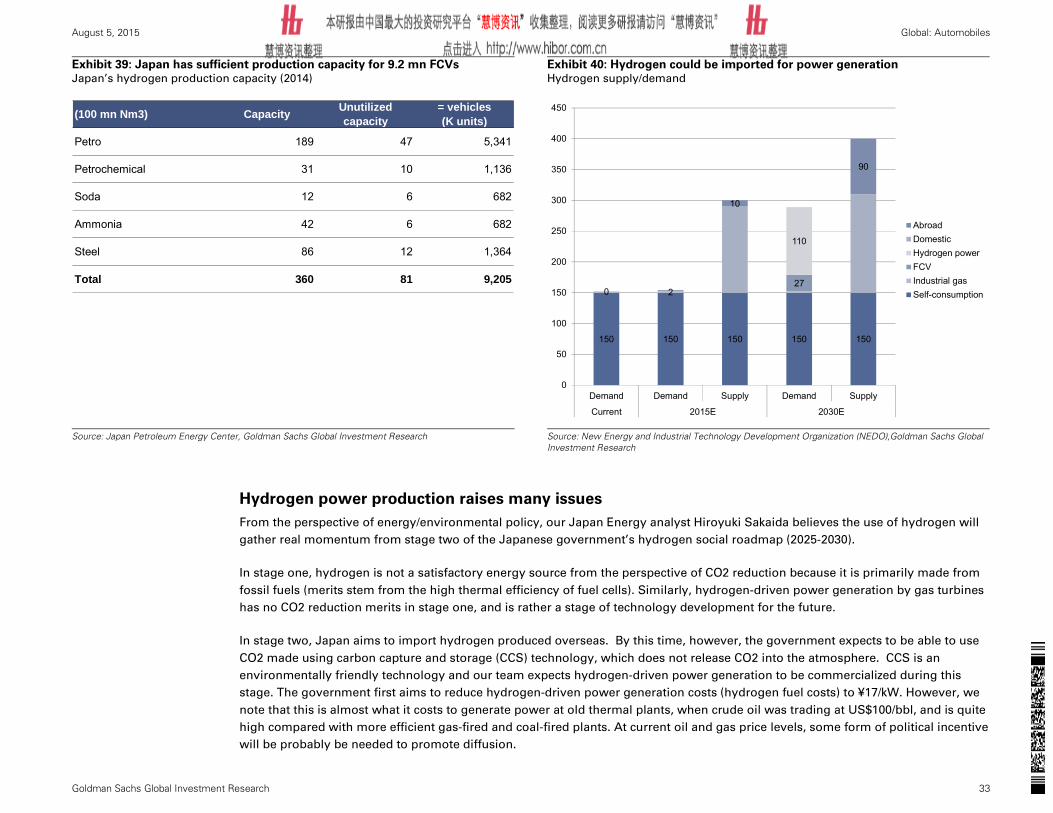

understandable. Japan Petroleum Energy Center estimates surplus hydrogen capacity in Japan to be 8.1 bn normal cubic meters

(Nm3) in 2014, which is enough to fuel 9.2 mn FCVs on our calculations. This suggests that making effective use of surplus energy

in Japan is by itself a sufficiently worthwhile project from an FCV standpoint alone.

Ultimate eco-car requires CO2-free hydrogen development

From a medium-term standpoint, taking into account issues such as further hydrogen cost cuts and CO2-free hydrogen production;

FCVs do not mark the end of the discussion. If the field is broadened to include hydrogen power generation also, attention must be

given to hydrogen production from lignite, transporting hydrogen from overseas, and hydrogen production methods using

hydraulic and solar power.

79

78

14

147

132

95

79

55

0 20 40 60 80 100 120 140 160

FCV(Onsight reforming town gas)

FCV(Insight reforming natural gas)

FCV(alkaline water electrolysis by solar)

Gasoline

Diesel

HV

PHEV

EV

Productionprocess

Prospect of practical use

Production cost(JPY/㎥) Characteristic

By-product hydrogen Steel ✓ 24-32 Production volume is dependent on purpose-grown proudct

Petrochemical ✓ 20 18bn ㎥/yr surplus production in steel and petrochemical industry

Purpose-grown Oil refining ✓ 23-32 Produced in unused spare capacity.

(Existing facility) 4bn ㎥/yr produced by oil refining