Winning with Contextual Financial Services Cards and Payments Asia 2015, Singapore Loon Wing Yuen Director, Innovation Enterprise Architecture & Solutioning, Group Information and Operations Division Suntec, Singapore 22-23 April, 2015

Cards and Payments Asia presentation - Apr. 2015

Aug 06, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Winning with Contextual Financial Services

Cards and Payments Asia 2015, Singapore

Loon Wing Yuen Director, Innovation Enterprise Architecture & Solutioning, Group Information and Operations Division

Suntec, Singapore 22-23 April, 2015

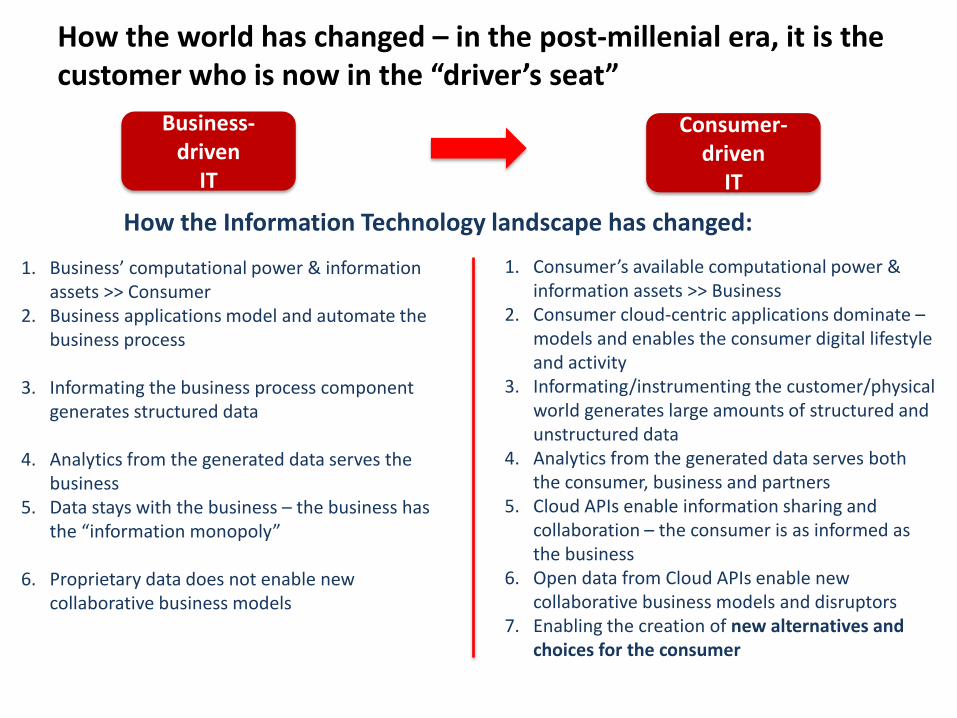

How the world has changed – in the post-millenial era, it is the customer who is now in the “driver’s seat”

Business-driven

IT

Consumer-driven

IT

1. Business’ computational power & information assets >> Consumer

2. Business applications model and automate the business process

3. Informating the business process component generates structured data

4. Analytics from the generated data serves the business

5. Data stays with the business – the business has the “information monopoly”

6. Proprietary data does not enable new collaborative business models

1. Consumer’s available computational power & information assets >> Business

2. Consumer cloud-centric applications dominate – models and enables the consumer digital lifestyle and activity

3. Informating/instrumenting the customer/physical world generates large amounts of structured and unstructured data

4. Analytics from the generated data serves both the consumer, business and partners

5. Cloud APIs enable information sharing and collaboration – the consumer is as informed as the business

6. Open data from Cloud APIs enable new collaborative business models and disruptors

7. Enabling the creation of new alternatives and choices for the consumer

How the Information Technology landscape has changed:

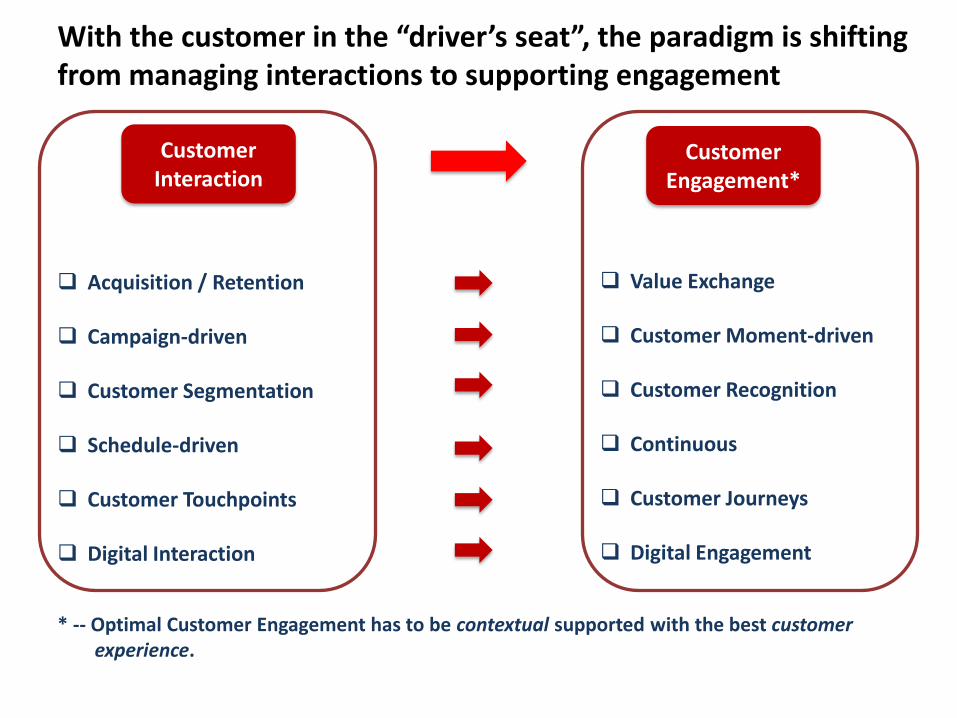

With the customer in the “driver’s seat”, the paradigm is shifting from managing interactions to supporting engagement

Customer Interaction

Customer Engagement*

Acquisition / Retention

Campaign-driven

Customer Segmentation

Schedule-driven

Customer Touchpoints

Digital Interaction

Value Exchange

Customer Moment-driven

Customer Recognition

Continuous

Customer Journeys

Digital Engagement

* -- Optimal Customer Engagement has to be contextual supported with the best customer experience.

CIMB’s journey – Embracing the digital frontier

New Enablers

New Digital Offerings

New Channels

Big Data Analytics-enabled Customer

Insights and Applications

STP, Instant Decisioning &

Instant Fulfillment

Regional Converged Clicks Platform

CIMBMessenger

Mobile POS

KWIK

Rekening Ponsel/OctoSend

Instant over the Phone Decisioning Geo-location based Deals

Bank-in-a-Briefcase

Beat Banking’s Collaborative Wallet with AIS telco

CIMB Clicks User Base

‘000

New Core Banking Platform

1Loyalty Regional Loyalty

Platform

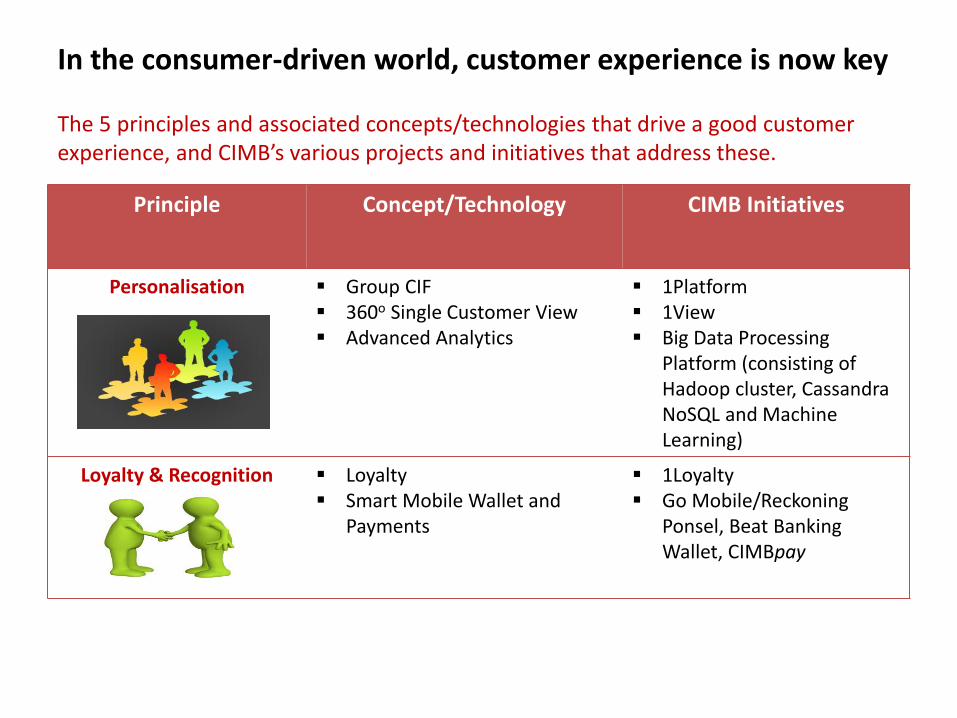

In the consumer-driven world, customer experience is now key

Principle Concept/Technology CIMB Initiatives

Convenience

“Open account where I am” “Pay where I am” “Cash where I need it”

“Motorcycle loan at the shop”

“Merchant Offers Near Me” Enquiries and Complaints via

Bank-in-a-Briefcase Plug n Pay Go Mobile/Reckoning

Ponsel SAMM (Self-Apply Machine

for Motorcycle Loan) CIMB Deals CIMB Assists

Low-friction User Interfaces & Ease-of-Use

Converged Internet-Mobile Platform

Straight-through Processing Messaging and Chat Services Virtual Assistant*

Regional Converged Clicks Platform

1View Instant Decisioning CIMBMessenger Smart MoneyManager

Before considering context, we first need to support the enablement of quality customer engagement via superior customer experience.

* -- In conceptual stage

Principle Concept/Technology CIMB Initiatives

Personalisation Group CIF 360o Single Customer View Advanced Analytics

1Platform 1View Big Data Processing

Platform (consisting of Hadoop cluster, Cassandra NoSQL and Machine Learning)

Loyalty & Recognition

Loyalty Smart Mobile Wallet and

Payments

1Loyalty Go Mobile/Reckoning

Ponsel, Beat Banking Wallet, CIMBpay

In the consumer-driven world, customer experience is now key

The 5 principles and associated concepts/technologies that drive a good customer experience, and CIMB’s various projects and initiatives that address these.

Principle Concept/Technology CIMB Initiatives

Context-based Interactions Location-based Offer Recommendation Engine

Social-awareness Smart Mobile Wallet and

Payments BLE4 Beacons, Smart

Wearables and IoTs* Fraud Detection via Geo-

fencing Advanced Analytics

Offers4Me for CIMBMessenger

OctoPay Facebook Banking CIMBpay, OpenBanking

CIMBpay, OpenBanking

PlugNPay m-POS

Big Data Processing

Platform (consisting of Hadoop cluster, Cassandra NoSQL and Machine Learning)

In the consumer-driven world, customer experience is now key

The 5 principles and associated concepts/technologies that drive a good customer experience, and CIMB’s various projects and initiatives that address these.

* -- In conceptual stage

Context

“Circumstance” – a fact or condition connected with or relevant to an event or action.

Hence all this is about information connected/generated from an event which is related to an action being performed.

In order to gain a full understanding of the underlying customer event or action (customer context), the following information categories are typically needed:

8

“The circumstances that form the setting for an event, statement, or idea, and in terms of which it can be fully understood.” – Dictionary.com

Information Category Contextual Information

Baseline Info CustID, Customer Profile (Demographical, Psychographical, Personas, Preferences & Tastes), Risk Appetite, Loyalty Index, Social Graph

Historical Info Interaction History, Customer Journey

Current/Present Info Channel/Device, Location, Time of Day, Task at Hand, Life-Stage

External Info IoT-generated data, Season, Weather, Stock Market Index, Other Economic Indices

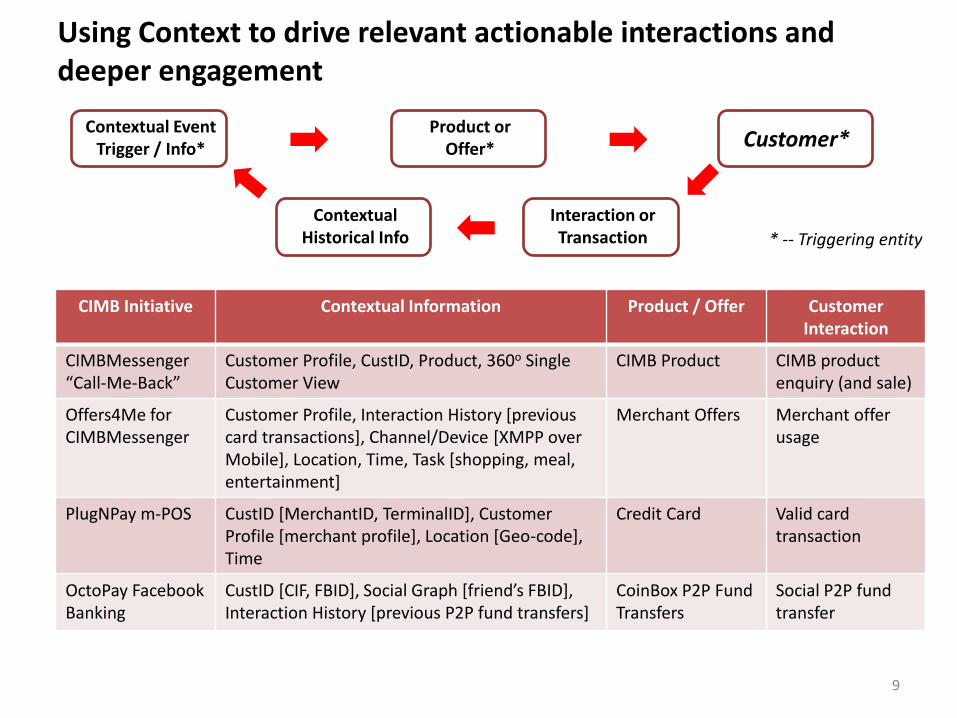

Using Context to drive relevant actionable interactions and deeper engagement

9

Contextual Event Trigger / Info*

CIMB Initiative Contextual Information Product / Offer Customer Interaction

CIMBMessenger “Call-Me-Back”

Customer Profile, CustID, Product, 360o Single Customer View

CIMB Product CIMB product enquiry (and sale)

Offers4Me for CIMBMessenger

Customer Profile, Interaction History [previous card transactions], Channel/Device [XMPP over Mobile], Location, Time, Task [shopping, meal, entertainment]

Merchant Offers Merchant offer usage

PlugNPay m-POS CustID [MerchantID, TerminalID], Customer Profile [merchant profile], Location [Geo-code], Time

Credit Card Valid card transaction

OctoPay Facebook Banking

CustID [CIF, FBID], Social Graph [friend’s FBID], Interaction History [previous P2P fund transfers]

CoinBox P2P Fund Transfers

Social P2P fund transfer

Product or Offer* Customer*

Interaction or Transaction

Contextual Historical Info * -- Triggering entity

Why context matters – CIMBMessenger “Call-Me-Back”

CIMBMessenger is an enhancement module to the CIMB Clicks Mobile App which provides an “always on” communication channel between the bank and the customer. CIMB Product Promotions can optionally have the “Call-Me-Back” function.

10

1. Server automatically checks if the customer will receive notification via Messenger or SMS

/

2. Clicks Mobile customer receives push notification via the Apple or Google Cloud.

3. Clicks Mobile app will display the latest notification upon customer clicking on the push notification.

4. Interested customer responds by pressing the “Call-Me-Back” button.

5. A Lead will be generated in Siebel CRM and routed to the assigned Retail Telemarketing Center agent.

6. RTC agent calls the customer within the same business day with regards to the product enquiry.

Why context matters

► The mobile channel is rapidly becoming the dominant channel of interaction between the bank and the customer

► The mobile has become a very personal device – in particular, customers are very selective about which app to enable notifications – these apps must provide value to them

► Hence, in order for our mobile banking app to “qualify” and being sufficiently “valuable” to the customer to enable push notifications – the interactions between the bank and the customer have to be contextually relevant

With the growing trend of “Out-of-Band” mobile interactions (such as CIMBMessenger), context matters.

11

Targeted Personalised Contextual

Targeted Campaign Offers No choice Push based Segment based

“Send me relevant Offers” Opt In (eg. F&B offers in

KLCC mall) Pull based ‘Segment of One’ based

“Send me relevant Location Offers” Opt In Event trigger based (eg. location

detected at KLCC mall via a BLE4 beacon) during dinner time

‘Segment of One’ based

“In-Band” Post-Login “Out-of-Band” Pre-Login Mobile Banking txns Mobile interactions

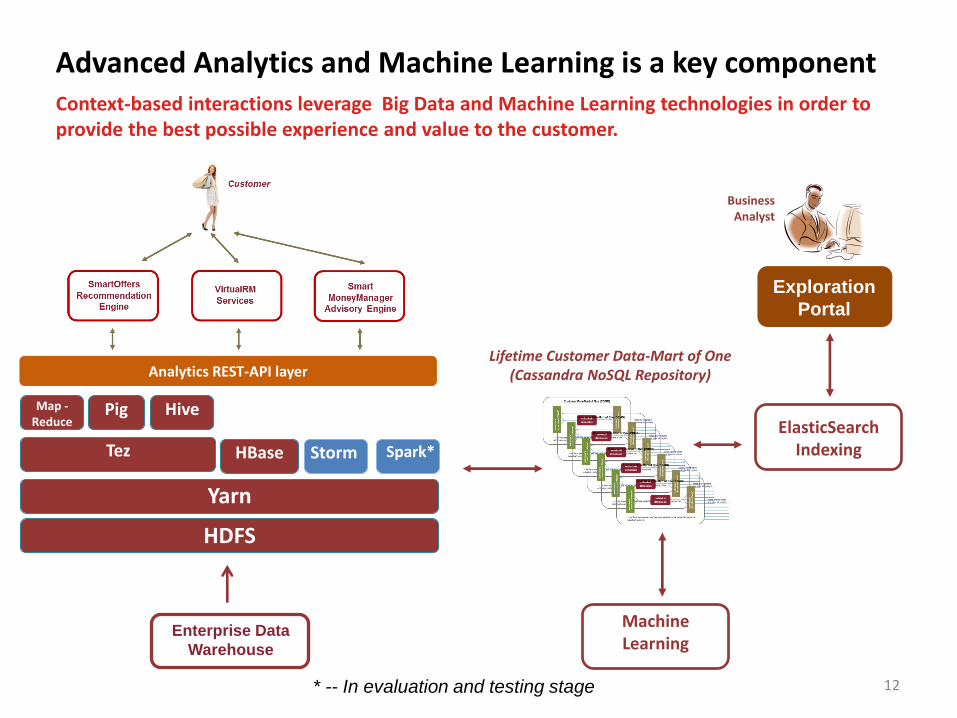

Advanced Analytics and Machine Learning is a key component Context-based interactions leverage Big Data and Machine Learning technologies in order to provide the best possible experience and value to the customer.

12

ElasticSearch Indexing

Map - Reduce

Pig Hive

Tez HBase Storm Spark*

Yarn

HDFS

Exploration

Portal

Enterprise Data

Warehouse

Lifetime Customer Data-Mart of One (Cassandra NoSQL Repository) Analytics REST-API layer

Business Analyst

Machine Learning

* -- In evaluation and testing stage

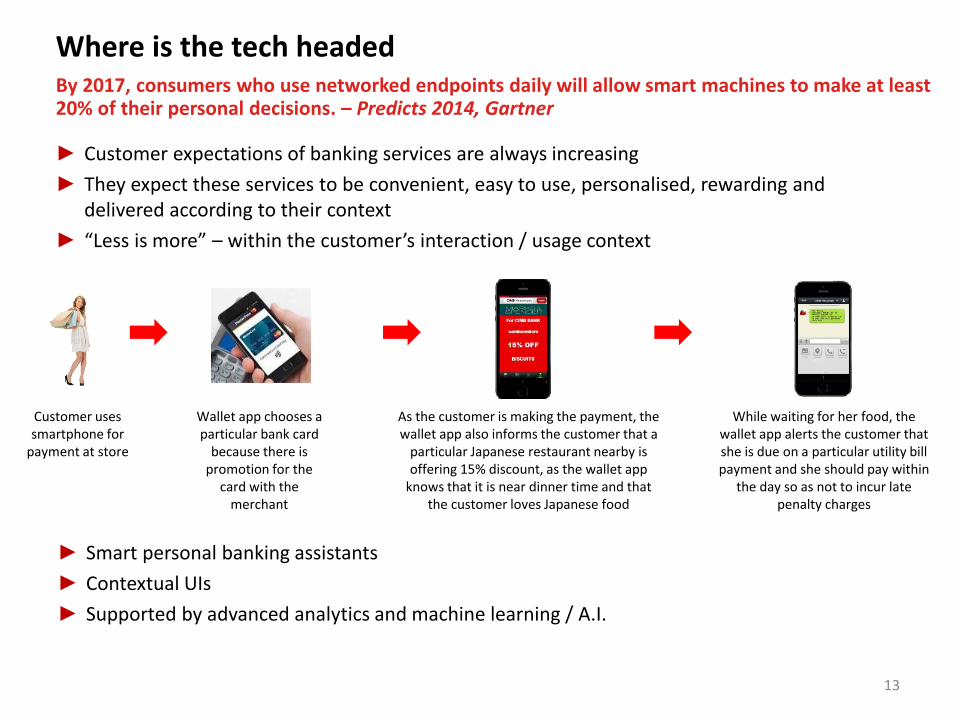

Where is the tech headed

► Customer expectations of banking services are always increasing

► They expect these services to be convenient, easy to use, personalised, rewarding and delivered according to their context

► “Less is more” – within the customer’s interaction / usage context

By 2017, consumers who use networked endpoints daily will allow smart machines to make at least 20% of their personal decisions. – Predicts 2014, Gartner

13

Customer uses smartphone for

payment at store

Wallet app chooses a particular bank card

because there is promotion for the

card with the merchant

As the customer is making the payment, the wallet app also informs the customer that a

particular Japanese restaurant nearby is offering 15% discount, as the wallet app

knows that it is near dinner time and that the customer loves Japanese food

► Smart personal banking assistants

► Contextual UIs

► Supported by advanced analytics and machine learning / A.I.

While waiting for her food, the wallet app alerts the customer that she is due on a particular utility bill payment and she should pay within

the day so as not to incur late penalty charges

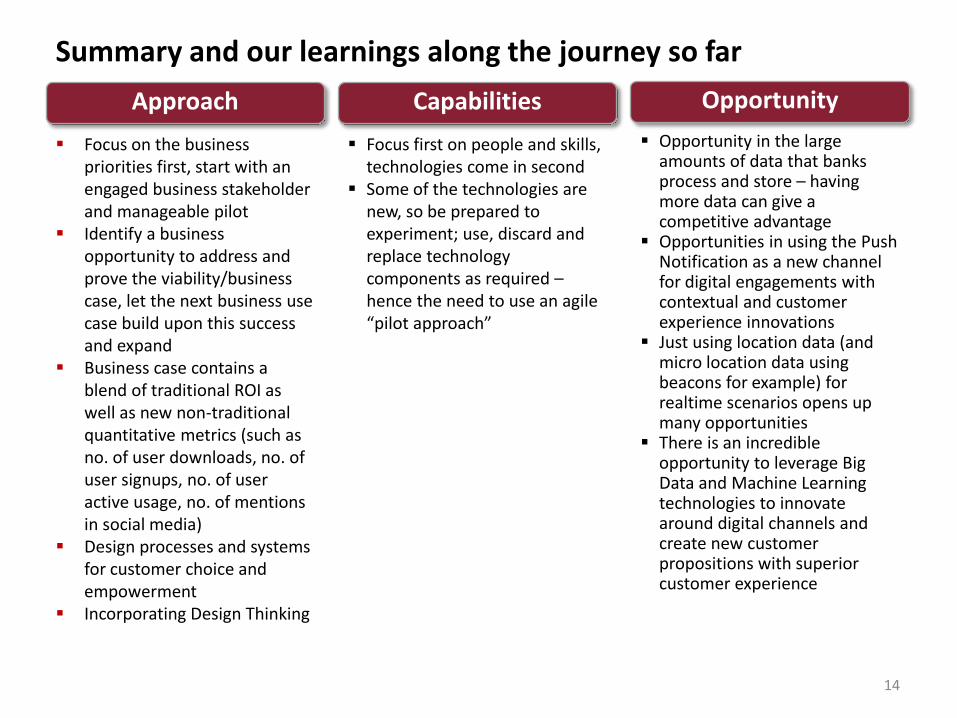

Focus on the business priorities first, start with an engaged business stakeholder and manageable pilot

Identify a business opportunity to address and prove the viability/business case, let the next business use case build upon this success and expand

Business case contains a blend of traditional ROI as well as new non-traditional quantitative metrics (such as no. of user downloads, no. of user signups, no. of user active usage, no. of mentions in social media)

Design processes and systems for customer choice and empowerment

Incorporating Design Thinking

Focus first on people and skills, technologies come in second

Some of the technologies are new, so be prepared to experiment; use, discard and replace technology components as required – hence the need to use an agile “pilot approach”

Approach Capabilities

Opportunity in the large amounts of data that banks process and store – having more data can give a competitive advantage

Opportunities in using the Push Notification as a new channel for digital engagements with contextual and customer experience innovations

Just using location data (and micro location data using beacons for example) for realtime scenarios opens up many opportunities

There is an incredible opportunity to leverage Big Data and Machine Learning technologies to innovate around digital channels and create new customer propositions with superior customer experience

Opportunity

14

Summary and our learnings along the journey so far

Thank You

Related Documents