The recent buoyancy in the aluminium market after a prolonged period of depressed prices has done no harm, whatsoever, to Capral Aluminium Ltd’s chances of selling its Kurri Kurri smelter in New South Wales. Capral (formed in 1994 following the decision by Canadian aluminium producer Alcan to sell its 73.3%-owned Australian division) intimated last November that the smelter would be sold when it announced plans to split its smelting and downstream businesses into separate operations (MJ, November 19, 1999, p.417). The sale decision was confirmed in Sydney this Tuesday when the Capral board announced that it was exploring the possibility of a sale as part of a corpo- rate restructuring plan, adding that it had received expressions of interest in Kurri Kurri from a number of potential buyers. The 150,000 t/y capacity smelter located in the Hunter Valley was ear- marked for a A$250 million, 50,000 t/y expansion but the plan was shelved last year, partly because of uncompetitive electricity prices. The facility purchas- es its electricity needs under short-term contracts and the uncertainty about future electricity prices could impact adversely on the sale price. On the posi- tive side, a five-year alumina supply contract has been reached with Kaiser Aluminum & Chemical Corp., effective as from January 1, next year. Analysts estimate the value of Kurri Kurri at about A$350 million. Capral has appointed the investment bank ABN Amro to advise it on its corporate restructuring, and for those parties interested in purchasing the smelter, the company expects to provide a detailed memorandum on the opera- tions later this month. Capral has declined to name suitors but a number of big aluminium produc- ers are believed to be in contention, including Alcoa Inc. of the US and Pechiney of France. Both companies already have significant aluminium interests in Australia, although Pechiney is regarded as a less likely buyer by analysts who suggest it might be more inclined to increase its existing 36% interest in the nearby 380,000 t/y capacity Tomago smelter. The French company has been in talks with CSR Ltd which is intending to divest its alu- minium interests. CSR owns 70% of Gove Aluminium which holds a 36.5% stake in Tomago. Confirmation that Capral intends to sell Kurri Kurri and focus on its down- stream fabricating and distribution activities was well received in the mar- ket place and the company’s share price jumped by seven cents during early trading on Tuesday, to reach a high of A$2.13. ■ JOURNAL London, February 4, 2000 Volume 334 No. 8568 Established 1835 ISSN 0026-5225 Capral courted for Kurri Kurri http://www.mining-journal.com Inside • Gold deposit survey (p.76) • African issues (p.79) • BHP hit by injunction (p.91) • PGM jockeying for position (p.94) • JCI Gold merger off (p.99) No worries for nickel The latest news from Western Australia on the progress of the new generation of lateritic nickel deposits, which employ pressure acid leaching technology to treat the ore, should do little to under- mine the current strength of the nickel market. Technical problems have delayed the various Australian projects from reaching their design capacities and the shortfall in expected output is partly responsible for pushing the cur- rent nickel price to a 4E-year high above US$8,900/ t (this issue, p.94). The biggest of these operations, Anaconda Nickel’s A$1.03 billion Murrin Murrin project, is designed to produce 45,000 t/y of nickel and 3,000 t/y of cobalt at a cash operating cost of US$1.14/lb. Initial output began last May, five months behind schedule, and in the most recent quarter it still managed to produce only minimal amounts of high-grade nickel and cobalt. However, during the month of December output did improve, Africa is certainly ‘elephant country’ for exploration although the targets are not always obvious. To coincide with the Indaba Conference in Cape Town, the ‘focus’ articles in this week’s Mining Journal address African issues. continued on p.76 Personal copy; not for onward transmission Reliability is the point http://www.ensival-moret.com Reliability is the point

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The recent buoyancy in the aluminiummarket after a prolonged period ofdepressed prices has done no harm,whatsoever, to Capral Aluminium Ltd’schances of selling its Kurri Kurrismelter in New South Wales. Capral(formed in 1994 following the decisionby Canadian aluminium producerAlcan to sell its 73.3%-ownedAustralian division) intimated lastNovember that the smelter would besold when it announced plans to split itssmelting and downstream businessesinto separate operations (MJ,November 19, 1999, p.417). The saledecision was confirmed in Sydney thisTuesday when the Capral boardannounced that it was exploring thepossibility of a sale as part of a corpo-rate restructuring plan, adding that ithad received expressions of interest inKurri Kurri from a number of potentialbuyers.

The 150,000 t/y capacity smelterlocated in the Hunter Valley was ear-marked for a A$250 million, 50,000 t/yexpansion but the plan was shelved lastyear, partly because of uncompetitiveelectricity prices. The facility purchas-es its electricity needs under short-termcontracts and the uncertainty aboutfuture electricity prices could impactadversely on the sale price. On the posi-

tive side, a five-year alumina supplycontract has been reached with KaiserAluminum & Chemical Corp., effectiveas from January 1, next year. Analystsestimate the value of Kurri Kurri atabout A$350 million. Capral hasappointed the investment bank ABNAmro to advise it on its corporaterestructuring, and for those partiesinterested in purchasing the smelter,the company expects to provide adetailed memorandum on the opera-tions later this month.

Capral has declined to name suitorsbut a number of big aluminium produc-ers are believed to be in contention,including Alcoa Inc. of the US andPechiney of France. Both companiesalready have significant aluminiuminterests in Australia, althoughPechiney is regarded as a less likelybuyer by analysts who suggest it mightbe more inclined to increase its existing36% interest in the nearby 380,000 t/ycapacity Tomago smelter. The Frenchcompany has been in talks with CSRLtd which is intending to divest its alu-minium interests. CSR owns 70% ofGove Aluminium which holds a 36.5%stake in Tomago.

Confirmation that Capral intends tosell Kurri Kurri and focus on its down-stream fabricating and distribution

activities was well received in the mar-ket place and the company’s share pricejumped by seven cents during earlytrading on Tuesday, to reach a high ofA$2.13. ■■

JOURNALLondon,February 4, 2000Volume 334No. 8568

Established 1835ISSN 0026-5225

Capral courtedfor Kurri Kurri

http://www.mining-journal.com

Inside• Gold deposit survey (p.76)

• African issues (p.79)

• BHP hit by injunction (p.91)

• PGM jockeying forposition (p.94)

• JCI Gold merger off (p.99)

No worriesfor nickel

The latest news from Western Australiaon the progress of the new generation oflateritic nickel deposits, which employpressure acid leaching technology totreat the ore, should do little to under-mine the current strength of the nickelmarket. Technical problems havedelayed the various Australian projectsfrom reaching their design capacitiesand the shortfall in expected output ispartly responsible for pushing the cur-rent nickel price to a 4E-year high aboveUS$8,900/ t (this issue, p.94).

The biggest of these operations,Anaconda Nickel’s A$1.03 billionMurrin Murrin project, is designed toproduce 45,000 t/y of nickel and 3,000t/y of cobalt at a cash operating cost ofUS$1.14/lb. Initial output began lastMay, five months behind schedule, and

in the most recent quarter it stillmanaged to produce only minimalamounts of high-grade nickel andcobalt. However, during the monthof December output did improve,

Africa is certainly ‘elephant country’ forexploration although the targets are not alwaysobvious. To coincide with the Indaba Conferencein Cape Town, the ‘focus’ articles in this week’sMining Journal address African issues.continued on p.76

Personal copy; not for onward transmission

Reliability is the point

h t t p : / / w w w. e n s iva l - m o re t . c o m

Reliability is the point

COMMENT

WORLD GOLDPaul Burton ACSM, M.Sc., MBA

Helen Payne M.Sc., DIC

MINING MAGAZINEJohn Chadwick B.Sc.

Des Clifford B.Sc.

SUPPLEMENTS/REPORTSSean Mulshaw Ph.D., DIC, C.Geol.

Austin Wheeler B.Eng.

MINING ENVIRONMENTAL MANAGEMENTTracey Khanna M.Sc., MCSM

CONSTRUCTION PUBLICATIONSIan Clarke B.Sc.

Alan Kennedy B.Sc.Mike Smith HND (Min.)

RESEARCH SERVICESIris Moncrieff

Editorial Consultant & ChairmanMichael West B.Sc., F.Eng.

Managing Director & PublisherLawrence Williams B.Sc., C.Eng.

THE MINING JOURNAL LTD60 Worship StreetLondon EC2A 2HD

Tel: (+44 207) 216 6060Fax: (+44 207) 216 6050

E-mail: [email protected]

Subscription Dept: PO Box 10Edenbridge, Kent TN8 5NE, UK

Tel: (+44 1732) 864333Fax: (+44 1732) 865747

E-mail: [email protected]

Web Home Page: www.mining-journal.com

Two to tangoEditor

Roger Ellis B.Sc., C.Eng.

Deputy and Finance EditorRichard Morgan M.Sc., DIC, C.Eng.

Assistant Editor: Mineral MarketsAndrew Thomas M.Sc., DIC

Assistant Editor: Industry in ActionDominic Mercer M.Sc., DIC, FGS

ProductionSusan RobertsEileen Smith

AdvertisingMichael Bellenger

Frank GordonShelley Hannan

MarketingGareth Bowers

Carole Hoy

Executive DirectorChris Hinde Ph.D., C.Eng.

Mining Journal, published weekly, is available only as part of asubscription with Mining Magazine and Mining Annual Review.

Annual Subscription:£247 (US$440)

© Mining Journal Ltd 2000

Member of the Audit Bureau of Circulations

MJ

Corruption in the international miningindustry is a bit like adultery: we allknow it happens but it is seldom dis-

cussed in public. Those that campaignagainst corruption argue that it is preciselythis lack of willingness to air the issue,albeit perhaps from a misguided desire toprotect an industry’s collective reputation,that allows the practice to flourish. In themining sector, the consequences for thehost country could include the awarding oflicences, contracts etc., on less than opti-mal terms, and the circumvention of the nor-mal conditions designed to serve the inter-ests of the population, such as environmen-tal safeguards, labour practices and propertaxes. The main consequence for the law-abiding majority in the mining industry is ashort-term competitive disadvantage fromrefusing to participate.

Although cases of corruption are exposedin the media, it seems a fair assumption thatthe majority go unnoticed. One way for theanti-corruption campaigners to bring theissue more generally into the open, withoutmaking allegations that could end in thecourts, has been to publish league tables ofcorruption. These have in the past tended tofocus on countries where taking or demand-ing bribes is rife, partly to shame govern-ments there into acting.

Recognising, that every bribe taker needsa payer, Transparency International (TI)*, anon-governmental organisation based inBerlin, has this year added a bribe-payers’survey to its five-year-old corruption percep-tions index (bribe-takers’ survey). TI derivesthe bulk of its funding from governmentalinstitutions and foundations, but alsoreceives donations from the private sectorand includes several mining and relatedcompanies, such as Rio Tinto, Placer Dome,BHP, Bechtel and IAMGOLD, among itsmany supporters.

The bribe-payers’ index was compiledfrom research conducted by GallupInternational with 779 business executivesand other professionals in 14 selectedemerging-market countries. The survey con-cerned only serious corruption (ie not pettycorruption at airports etc.), and concentrat-

ed on the interviewees’ perceptions of bribepaying by companies from 19 leadingexporting countries in their dealings in the14 countries surveyed. The intervieweeswere also asked the sources from whichtheir perceptions were formed; 79% citedpress and media reports, 67% conversationswith colleagues and friends, and 56% per-sonal experience.

The ‘cleanest’ foreign investors (of the 19countries about which the intervieweeswere asked) are to be found in Sweden, fol-lowed by Australia and Canada. At the footof the table are Taiwan, South Korea andChina. The most corrupt industry sector ispublic works and other construction; fol-lowed by arms; power (including energy);and general industry (including mining). Theleast corrupt sector is agriculture.

The author of the bribe-payers’ survey,Fredrik Galtung, reports a high degree ofstatistical correlation between the inter-viewees with regard to the averages onwhich these rankings are based. However,Mr Galtung does concede that the industryrankings are partly a function of the 14countries in which the survey was conduct-ed. The industry rankings are also affectedby the structure of the industries and thepattern of foreign investment: sectors inwhich high-value deals with large up-frontpayments are common, and in which offi-cials have high discretionary powers aregenerally more prone to bribery.

The survey also includes a section onunfair, as opposed to illegal, business prac-tices, such as using diplomatic pressure insupport of an exporter, or tying deals to aid.Unfair is defined as anything that mightinfluence a contract to be awarded otherthan the contract’s merits (even if the recip-ient country gains in other ways). Here, theUS scored decisively worst, followed byFrance and Japan. The least prone to unfairpractice is Switzerland. TI ascribes theseresults mainly to the political clout of theworst-scoring countries and, in the case ofthe US, to firm legislation against bribe-pay-ing causing resort to other means.

*TI International Secretariat. Tel: (+49 30) 34 38 20 0.Fax: 34 70 39 12. E-mail: [email protected]

Change High- Year’son week Low Max/Min

Share Indices Feb 2 (%) (%)FT 30 3,711 –1.1 33 4,148-3,491US Dow Jones 11,003 –0.3 77 11,551-9,177FTSE Gold Mines 831 –0.2 24 1,232-702Australian All Mining 704 n/a 69 771-558South African Gold 1,102 0.4 53 1,358-807Toronto Met/Min 4,141 1.1 68 4,749-2,862Nikkei Dow 19,579 2.4 100 19,579-13,404Hang Seng 15,790 2.3 94 16,249-9,076

Commodity Prices Feb 2Gold (London) $285.25 –0.1 45 $324-254Copper (LME) $1,784.50 –1.9 82 $1,877.50-1,361Aluminium (U.S. prod.) 64.50c 0.0 59 69-58Brent Blend (dated) $27.06 –0.6 99 $27.25-9.83

LEADING INDICATORSChange High- Year’son week Low Max/Min

HSBC Indices Feb 2 (%) (%)(100 on 31/12/88 except*†)

Global Mining 132 –2.3 76 146-88Global Diversified Mining 172 –4.9 73 198-102Smaller Mining Companies 53 –1.4 67 59-42Global Base Metal 184 1.1 80 204-104North American Base Metal† 425 3.0 82 489-136Global Gold 55 –1.4 4 78-54Global Gold Ex S Africa 58 –1.4 0 85-58North American Gold 65 –1.2 0 97-65Global Coal Mining† 152 –4.2 26 195-137Other Metals/Minerals† 265 –1.3 97 271-96Latin American Mining* 272 –5.1 91 286-120Latin American (Ex CVRD)* 176 –2.2 92 184-90*100 on 31.12.89 †100 on 31/12/85

74 Mining Journal, London, February 4, 2000

75Mining Journal, London, February 4, 2000

The success of any system depends

on the right partnership between the

user and supplier. We take pride in

providing you with professional ser-

vice - during the project as well as

afterwards. Service protects your

investment by ensuring continued

high availability and profitable return.

Outokumpu’s services are close to

you wherever you are in the world,

speaking the same language and

offering an intensive level of care

that safeguards the future of your

operation.

Take Care

Outokumpu’s mineral processing

equipment and services are built on years

of experience. We offer you increased

profitability through top performance

technologies. Flexibility, a high degree of

automation, energy efficiency and

environmental responsibility are all

integral to each delivery.

CARPCO, recently acquired by

Outokumpu, incorporates service in all

its physical separation solutions. On-site

service visits and personnel training help

customers gain more from their process,

from electrostatic separation to magnetic

and gravity separation.

The new compact COURIER® 3 SLand high-performance COURIER ®30 XPelemental analyzers, PSI-200 particle size

measurement instruments and

PROSCON® 2100 automation system

increase plant performance and pro-

ductivity. Outokumpu’s customer support

agreements ensure high availability

through preventative maintenance, cali-

bration service and continuous training.

TankCell® and SkimAir ® Flotation

cells have been designed for easy and

uninterupted operation. In addition we

add value through process audits and

tailor made training programs as well as

preventive maintenance recommenda-

tions.

SUPAFLO® High Rate and High

Compression Thickeners provide

comprehensive testing and advisory

service for customers looking at

new installations and up-

grading existing thickener

operations.

CERAMEC ® capillary action filters

are built on solid expertise and compe-

tence to give trouble free operation.

Customer support is available in all cor-

ners of the world for rapid response to

customer’s process needs.

Outokumpu is committed to serve you

in every sense of the word. We dedicate

ourselves to be your long-term partner to

help you take care of your investment.

We concentrateon your concentrate

outokumpuOutokumpu Technology (Pty) Ltd, South Africa

Tel. +27 11 799 2410, Fax +27 11 799 2449

e-mail [email protected]

www.outokumpu.com

B A S E M E T A L S • S T A I N L E S S S T E E L • C O P P E R P R O D U C T S • T E C H N O L O G Y

Gold prospects – aglobal survey

Arizona-based Mining Investment Service(MIS) has recently published a 112-pagereport* on worldwide gold exploration inwhich it considers 970 greenfield golddeposits distributed in 88 countries. Theprospects are in various stages of explo-ration but in most cases there are sufficientdata to establish a resource estimate. Foreach prospect, MIS has examined location,tonnage, grade, contained gold and owner-ship.

North America ranks first among regionsin terms of the number of identifiedprospects, with 301 deposits dividedbetween the US (126) and Canada (175).Australasia ranks second with 282 deposits,followed by Latin America with 195.Compared with a survey conducted by MISone year previously, Australasia has postedthe biggest rise in the number of prospects,with an increase of 17. Australia is the mostimportant country in this region, with 168deposits. Other significant countries in theregion include the Philippines with 25deposits, Indonesia, with 24, China (15)and Papua New Guinea (12).

Elsewhere, the European region boasts100 prospects whilst Africa has 92. WesternAfrica has shown the most robust growth inrecent years within the African region, withGhana contributing 19 prospects, BurkinaFaso 10, Mali eight and Ivory Coast four.

The MIS report examines the tonnage foreach prospect and considers this against aworld average size of deposit, calculated tobe 26.6 Mt. On this basis, Latin Americaeasily outstrips all other regions with anaverage of 50.6 Mt. The average tonnage forEurope is 27.7 Mt, whilst the Australasianaverage is 23.4 Mt. North America has anaverage of 19.4 Mt and Africa just 8.8 Mt.Amongst individual deposits, NewmontMining’s Batu Hijau deposit in Indonesiapossesses the largest tonnage identified inthe study, at 1,495 Mt followed by theAldebaran deposit in Chile, with 1,000 Mt.The smallest tonnage identified in the sur-vey is the Santa Rosa deposit in Cost Rica,with a little over 4,000 t.

A more important criterion is the amountof contained gold. On this measure, which isa simple combination of tonnage and grade,MIS finds the European region in first placewith a deposit average of 3.2 Moz. The aver-age for Latin America is nearer 1.2 Moz,almost twice the average for North America(0.72 Moz). MIS estimates the world aver-age at 1.05 Moz.

The MIS analysis of ownership throws upsome interesting pointers. Examining

North America-based companies it findsthat, compared with its previous surveys,US-based Homestake has become a partici-pant in far more gold prospects (13), largelyas a result of its acquisition of PlutonicResources in Australia, and Argentina Goldin Latin America. Barrick Gold Corp. ofCanada is also well represented, especiallyin Latin America, and is mentioned 13 timesin the survey’s project listings. MIS alsopoints out that Barrick is one of the fewinternational mining companies currentlyexploring in China. Placer Dome ranks inthird place with 11 deposits currently beingexplored and MIS believes that recentmoves suggest that Placer is strengtheningits position in Southeast Asia. NewmontMining Corp., with 11 explorationprospects, is also in the top tier, and thesefour companies have been joined by TVXGold, with nine direct prospects and twoindirect interests.

Outside North America, the AngloAmerican group, the world’s biggest goldproducer, is directly exploring 13 goldprospects and Rio Tinto ranks near the topwith 12 prospects. Normandy Mining ofAustralia is identified as a significant new-comer, with 10 prospects. In Africa, AshantiGoldfields of Ghana has been identified asthe front-runner with 11 prospects althoughRandgold Resources has become a “worthycompetitor” in the region.

The MIS report profiles 38 significantgold companies accounting for output ofsome 39 .1 Moz (in 1998), almost 50% oftotal world gold production in that year.MIS says it is noteworthy that many of thecompanies identified are increasinglyadopting a global perspective when it comesto gold exploration. ■■

No worries for nickel

reaching 600 t of LME-grade nickel and 53 tof high-grade cobalt, and Anaconda says itexpects the project to “commence cash posi-tive operations during the current quarter”.The company also says that the ‘robustness’of the process has been demonstrated andthat plans for a rolling expansion to 100,000t/y continue.

There is better news from Centaur con-cerning its Cawse project, where output thisyear is scheduled to reach full capacity of10,000 t/y of nickel and 2,500 t/y of cobalt.In the December quarter, processing was11% above forecast, with production of1,237 t of nickel and 272 t of containedcobalt representing gains of 43% and 39%respectively compared with the Septemberquarter. Centaur reports that cash operat-ing costs fell 17% to US$1.64/lb after cobaltcredits of US$13.12/lb.

At the third project, Preston Resources’Bulong operation, December quarter nickelproduction reached 1,329 t, more than 100 t

ahead of target, with output in Decemberreaching 537 t. At design capacity, Bulongshould produce 9,000 t/y of nickel, and theprojected output for 2000 is around 8,000 t,plus 700 t of cobalt.

Meanwhile, Heron Resources, one of sev-eral second-generation lateritic nickel pro-ducers, says it intends to produce up to 500 tof nickel this year from ore mined from itsGoongarrie lode, which will be run throughthe nearby Cawse processing plant on atolling basis. Heron envisages annual pro-duction of 12,000 t beginning in about threeyears’ time.

The prevailing strong nickel prices aregiving all producers a strong incentive toraise output and to re-examine operationspreviously closed because of poor marketconditions. This week, Australia’s biggestnickel producer, WMC, said that it hasraised annual production above 100,000 t,and that it will make a decision within thenext month or so on whether or not toreopen mothballed operations which havebeen idled over the past two years at thecompany’s Kambalda operations. Thesecould add a further 10,000 t/y and raiseKambalda’s combined annual output to20,000 t. The five small, but high-grade,mines under review are Wanaway, Blair,Otter-Juan, Long/Victor and Mariners.

Last year, as a result of a major failure atits Kalgoorlie smelter, WMC’s nickel out-put fell back to an annualised 78,000 t/y. Amajor rebuild at the smelter was necessaryand, according to Peter Johnson, WMC’sgeneral manager for nickel and gold, theopportunity was taken to install a newhearth and to complete a new hooding pro-ject on the converters – in the past, air pol-lution from the smelter has periodically ledto its temporary closure. Commenting onnickel prices, he said that “everywhere inthe world is profitable at the moment, eventhe socialist producers are making money”,but Mr Johnson cautioned against over-whelming the market by rushing in withmarginal production. ■■

Western Australia’sindustrial minerals

Best known as Australia’s most importantproducer of iron ore, nickel, gold and dia-monds, Western Australia is also a very sig-nificant producer of industrial minerals.The state includes 29 commodities in thiscategory and has relaxed the strict defini-tion of industrial minerals (all non-metallic,non-fuel minerals extracted and processedfor industrial end-uses) to include gallium,tantalum, titanium minerals, vanadiumand zirconium.

As a contributor to world production, thestate supplies 34% of diamonds (byweight), 29% of zircon, 27% of rutile and15% of ilmenite. At the end of 1998, themerger of RGC and Westralian Sands to

MINING WEEK

76 Mining Journal, London, February 4, 2000

Continued from p.73

*Further details of the study can be obtained from MiningInvestment Service, 6336 Oracle Road, Apartment 326-386,Tucson, Arizona 85704, US. Tel: (+1 520) 575 8467. Fax: 2196430.

Mining Journal, London, February 4, 2000 77

form Iluka Resources Ltd established thelatter as the world’s second biggest producerof titanium minerals, accounting for rough-ly one third of the global market.

According to Western Australia’sDepartment of Resources Development(DRD) in its recently published 1999review of industrial minerals, in 1998 thesector contributed A$2.1 billion, or morethan 10% of WA’s total revenues from min-erals and petroleum, far in excess of SouthAustralia (A$245 million), Queensland(A$221 million in 1997/98) and New SouthWales (A$196 million in 1997/98).

Despite the onset of lower prices for anumber of mineral commodities during1998, record values were achieved forexports of industrial minerals such as salt,tantalite and mineral sands, whilst ArgyleDiamonds posted a 48% jump in sales toA$622 million. Gypsum is reported asanother success story, with a fivefoldincrease in sales to A$18.3 million.

The DRD regards the prospects forindustrial minerals as remaining “extreme-ly positive”, and it highlights the potentialof WA’s first vanadium project, atWindimurra, near Mt Magnet, where con-struction of the processing plant was com-pleted last October. There are other vanadi-um projects under consideration, byTanganyika Gold and Dominion Mining atBalla Balla in the Pilbara region, byGreater Pacific Gold at Gabinatha, and byAustralian Gold Resources at its Youanmideposit near Windimurra.

In July last year, the world’s leading tan-talite producer, Sons of Gwalia, commis-sioned its Wodgina plant upgrade at a costof A$1.5 million. This will boost annualcapacity to 300,000 lb (136 t) of containedtantalum pentoxide. The company is alsoconsidering expanding its Kemerton silicasand mine from 400,000 t to 700,000 t/y.

Feasibility studies into the Mt Weld rareearths and tantalum projects have beencontinued by Ashton Mining and LynasGold, and Lynas is funding the next stage ofthe studies, spending A$3.2 million to earn a35% stake. The A$75 million project couldbe operational by 2001, and could supply10% of the world’s rare earths requirement.

WMC Resources, meanwhile, is con-structing an A$11 million, 45,000 t/y capac-ity talc mill at its Three Springs operationin the southwest of the state, with initialproduction due in March. In the far north,near Port Hedland, Sovereign Resources isconsidering a A$78 million manganese pro-ject which would produce both electrolyticmanganese dioxide and manganese sul-phate.

On a disappointing note, the beginning of1999 saw the closure of a major mineralsands operation, BHP’s Beenup mine,where commissioning had only begun in1997. The mine had been expected to pro-duce 600,000 t/y of ilmenite plus 20,000 t/yof zircon, but was closed because of poor

production levels and tailings managementproblems. There was a more positive devel-opment, however, with news early last yearthat a Japanese titanium minerals compa-ny, ISK, had finalised a joint venture withItochu Australia to develop a mineral sandsmine at Dardanup, with a planned produc-tion of 100,000 t/y of ilmenite plus minorrutile and zircon.

Colin Barnett, WA’s Minister forResource Development, says that industrialminerals are important, both for the invest-ment opportunities that they provide andfor the jobs that the sector generates –about 4,800 people are employed directly,often in remote areas, and many more areemployed in support services across a widerange of business areas. ■■

South African reviewThe latest ‘South African Minerals Review’(1998-99) has been published by theMinerals and Energy Policy Centre*. Theauthor, Magnus Ericsson from Stockholm-based Raw Materials Group, notes thatmore than five years after the ANC came topower, the final uncertainties about theSouth African mineral policy seem to havedisappeared and a new mineral legislationcould soon be promulgated. However, heconcludes that the changes will probablynot be as dramatic as initially expected.

The most important part of the new min-erals policy is the announced change to asystem of state-held mineral rights. TheANC government is clearly in the interna-tional political mainstream in setting as itslong-term objective to have “all mineralrights vested in the state for the benefit andon behalf of all the people of South Africa”.The proposal has naturally met with manyangry and nervous protests from the currentmineral rights holders. It is clear, accordingto Mr Ericsson, that government will treatthis contentious issue with great care. Themost recent policy document and signalsfrom the government discussions certainlysuggest a more cautious approach than wasexpected, one that is more pro-industry thanthe political statements made prior to thefirst democratic elections in 1994.

The review notes that a second phase ofrestructuring of the South African miningindustry has started, with new participants,both local and foreign, entering the stage.The first phase of structural change in theSouth African mining industry came to anend in early 1999 when Anglo Americanmoved its headquarters to London. Mostcorporate restructuring had been completedby then and the internal structures over-hauled. Mr Ericsson says that it is surpris-ing how little discussion the loss of themajor companies has provoked in South

Africa, particularly in the case of Anglo,which has long been the symbol of SouthAfrican economic power.

New companies have profited from thosedeposits which were too small to interest themining houses. Kalahari Goldridge (nowmerged with Harmony) and the AfrikanderLease operation are prime examples.Among the more senior companies isMetorex, with a base metals, coal andindustrial minerals portfolio which hasattracted Canadian capital and grownrapidly.

South African investment abroad hasaccelerated and AngloGold, having com-pleted its major internal restructuring,made an offer for Australian gold producerAcacia. Mr Ericsson concludes that moreaggressive bids can be expected from Anglo.Some of the smaller South African compa-nies are also making their debut on the inter-national scene. Examples are Harmony buy-ing into the Canadian gold mine Bisset,Metorex taking a share in Chibuluma inZambia, and Durban Roodepoort Deep’slong fight for Australian gold producer,Hargraves Resources.

The shifting focus of the South Africanmining companies will not leave a vacuumat home. The empty space is being filledboth by emerging local juniors (particularlywith black entrepreneurial participation)and by gradually more and more estab-lished and senior international mining com-panies. A second phase of restructuring,after the first major entrants Placer Domeand Xstrata (active in ferroalloys), willprobably be new players coming in andforming alliances with the emerging localcompanies, whether owned by the new blackelite or by white entrepreneurs.

The review concludes that, provided theannounced policy changes are carriedthrough with caution, it is probable thatforeign investors will more than make up forthe spread of South African mining inter-ests around the world. Paradoxically one ofthe most important safeguards of stabilitywill be the quickly growing new class ofblack mining entrepreneurs. They will notwant to see their emerging empires lost. Butall new investors will be highly sensitive toeconomic and political changes, and the roleof South Africa’s ‘new foreigners’, Angloand Billiton, will remain crucial.• The South African Code for Reporting ofMineral Resources and Mineral Reserves(SAMREC Code) has now been producedafter more than two years of deliberation bythe SAMREC Committee under the aus-pices of the South African Institute ofMining and Metallury (SAIMM), chairedby Ferdi Camissani. Essentially the same asthe highly regarded revised AustralianJORC Code, the SAMREC Code has beenformally recognised by the JohannesburgStock Exchange which is enforcing it withinthe JSE reporting rules. The code will be onsale from the SAIMM by mid-March. ■■

MINING WEEK

*Available for US$250 from: Minerals and Energy PolicyCentre, Johannesburg, South Africa. Tel: (+27 11) 403 8013.Fax: 403 8023. E-mail: [email protected]

78 Mining Journal, London, February 4, 2000

SRK Consulting employs the world’s leadinggeological, engineering and environmentalconsultants to the exploration and mining industr y.

With offices on 5 continents, SRK Consulting isthe first one stop consultancy of specialists toprovide a full in house service to their clients.

Should you consider using the world ’s best andonly comprehensive independent service?

For more information visit our websitehttp://www.srk.com/.

Alternatively, call one of our head offices now foryour local office contact details.

World’s leading specialists in:• Aeromagnetic/radiometric/gravity/Landsat/2D and 3D seismic interpretation• Mineral and petroleum system evaluation• Ore deposit structural controls, alteration and

geochemical zonation• Advanced resource and reserve modelling• Geostatistics• Open pit and underground mine planning• Geotechnical engineering• Tailings disposal and landll investigations• Hydrology and geohydrology• Environmental impact and management• Feasibility studies and risk management• Independent reports and due diligence.

Africa+27 11 4411111

Australasia+61 7 3832 9999

Canada+16046814196

Europe+44 1222 235566

South America+56 2 2690353

USA+1 303 9851333

Photo reproduced with kind permission from the USGS

You don’t have to bealone out there…

Our worldwide experience is your worldwide experience

SRK

AFRICA FOCUS

In addition to its normal circulation,this week’s Mining Journal is being dis-tributed to delegates at the Investing in

African Mining (Indaba) conference beingheld at the Cape Sun IntercontinentalHotel, Cape Town, South Africa onFebruary 8-10, 2000. The following com-ments are drawn from some of the papersbeing presented at this annual event.

Setting the scene for delegates, as usual,will be David Williamson*, with a paperentitled ‘An Optimistic Start to the NewMillennium’. In his presentation, MrWilliamson will note that, until recently,most metal markets have been experiencinga period of prolonged price weakness which,at the low point of the cycle, reduced realprices to their lowest levels in decades. Thisprice weakness followed a period where met-al production growth coincided with theeconomic crisis in Asia. Inventories rose sig-nificantly, thereby allowing consumersto perceive, correctly, that there would beno immediate metal supply shortages.However, Mr Williamson believes that met-al prices, including gold, might now be setfor an extended period of price strength.

The reasons for Mr Williamson’s predic-tion go back ten years to the collapse of theFormer Soviet Union (FSU). He notes that,although now a distant memory, there was atime when the Soviet Union was a super-

power producing and consuming significanttonnages of all the major metals requiredfor the sustenance of such a large, albeitinefficient, economy. However, between1989 and 1998, the FSU’s demand for cop-per and aluminium fell by 83%, and fornickel and zinc by 73% and 75%.

Yet, in its desire to earn foreign exchange,almost at whatever cost, production fromthe FSU has declined only modestly in thecase of copper and aluminium, whilst it hasrisen in the case of nickel. As a result, theFSU turned from being just a moderateexporter of these metals to becoming a sub-stantial exporter immediately after theSoviet Union collapsed. In the case of cop-per, exports from the FSU increased by700,000 t/y, for aluminium by 2 Mt/y andfor nickel by about 115,000 t/y.

Compared with the decade prior to itscollapse, Mr Williamson calculates thatduring the past decade the additional metalexported by the FSU to the West amounted

to over 7 Mt of copper, 20 Mt of aluminium,0.9 Mt of nickel and 2.5 Mt of zinc. All thisadditional metal has had to be absorbed byWestern markets. Also, in its desperatesearch for foreign exchange, the countryexported significant quantities of scrap andstockpiled metal, which simply added to themetallic surge swamping the markets atthat time. The FSU also sold some 2,000 t ofgold in the early part of the decade.

Unfortunately, immediately after thedemise of the Soviet Union, the world econ-omy went into recession, further adding tothe glut of metals on world markets.Industrial production in the US remainedvirtually unchanged from 1989 to 1992, anddid not really advance strongly until 1994.The same is true of Germany, whilst Japanis still experiencing industrial productionlevels little changed from a decade earlier.Hence, because of the fundamental changesin the FSU, combined with the recession inthe early part of the decade, industrial con-sumers were allowed the luxury of knowingthat there were no real metal shortages.This was reflected in the metal markets,where prices declined in the early 1990s andremained subdued to 1994. At that time, inanticipation of a global recovery, metalprices recovered dramatically.

Investingin Africa

*Managing director, David Williamson Associates Ltd.

79Mining Journal, London, February 4, 2000

What better place in the world to purify goldthan to bring it home.

TO AFRICA.For over 75 years, the Rand Refinery Limitedhas strengthened its reputation of being the world’s finest, most dedicated andexperienced gold refiner.

Little wonder that itsannual productioncapacity exceeds 1200 tonnes. And itsseal - or chop - isregarded interna-tionally as the globalbenchmark for goldrefining excellence.

As the world’s largest, most modern goldrefiners, Rand Refinery offers:

• an extremely high processing speed - including the processing of value-added products (investment bars, granules, gold salts, alloys and coin blanks)

• a comprehensive range of financial packages, pre-payment options, aggressive pricing

• assay standards which are the world-wide industry benchmark

• strong relationships with all market participants

For further details please contact Marketing Department:Tel: +27 11 873-2222, Fax: +27 11 873-4940,

http//:www.randref.co.za, e-mail: [email protected]

AFRICA FOCUS

However, just as the mining industrygathered strength on the back of declininginventories, the global economy was againshaken by the Asian crisis, not to mentionthe continuing economic stagnation inJapan. The shock that this caused to theworld economy, and in particular to percep-tions regarding the knock-on effect of thecrisis, caused metal prices to plummet onceagain as demand faltered and productioncontinued to climb. As it happens, the actu-al effect of the Asian crisis was not as greatas originally feared and was mitigated bythe driving strength of the US economy,where growth in demand countered thereduced demand from the former SouthEast Asian ‘Tiger’ economies.

In his paper, Mr Williamson notes that,as if this was not enough, the mining sectorsuffered in early 1997 the psychologicalshock resulting from the Bre-X scandal inIndonesia. This gigantic fraud decimatedthe junior mining sector and virtually elimi-nated that market for exploration funding.

However, as the industry enters a newmillennium, the outlook for metal marketsappears exceptional. Mr Williamson notesthat, for the first time in years, all the majoreconomies are enjoying strong growth, andthis rare coincidence of positive economicfactors should stimulate metal demand forthe foreseeable future.

Implication for AfricaAs noted in the Mining Journal Emerging

Markets supplement of October 22, 1999,the Asian financial crisis of 1997 had a dra-matic effect on the economies of most devel-oping countries. It played havoc in south-east Asia and Russia throughout 1998, setback the progress achieved in LatinAmerica and, in the most seriously affectedcountries, wiped out the fruits of decades ofeconomic growth. In its wake, growth in thedeveloping world slowed from almost 6% in1996 to less than 2% in 1998, and for thefirst time in ten years growth in the develop-ing countries was less than in the developedcountries.

With this depressing scenario for theeconomies of developing countries, thefinancial pump-priming role of mining com-panies is enhanced. Because their choice ofinvestment location is limited by the distri-bution of mineral deposits, mining execu-tives are perhaps less likely to be influencedby current market trends than companyexecutives in other industries.

This relatively robust outlook was evi-dent from the fourth Mining Journal surveyof emerging countries, published in theEmerging Markets supplement threemonths ago (see box below). Despite the

economic malaise in the region, LatinAmerica again emerged as the recipient ofmost mining interest, with five countries inthe top six. Moreover, Africa managed acreditable four countries in the top ten. Themining executives did register concern overAsia, however, with Indonesia being the solerepresentative from the continent in the topten rated emerging mining countries.

The South American bloc found itselfcompeting with an African bloc consistingof South Africa (ranked 5th), Ghana (7th),Tanzania (8th) and Namibia (10th posi-tion). South Africa has moved up in theexecutive ranking from 7th position in 1998,9th in 1997 and a lowly 15th in 1996. Ghanahas remained in a remarkably stable 7thposition for the past four years. The rankingof Burkina Faso (13th), Cote d’Ivoire(14th) and Botswana (15th) emphasises thestrengthening interest in Africa. Angolawas ranked 17th overall but the opinions ofthe executives polled were sharply dividedover the country’s mining potential.

Mining Journal canvassed the chief executives of the majormining corporations, asking them to rank the top tenemerging countries (out of a list of 50) which they, personal-ly, believed offered the best opportunities within the nextfive years for the development of profitable mines. In theirevaluation they were asked to consider geological potential,current property values, ease of doing business, the operat-ing environment and individual countries’ political stabili-ty.

80 Mining Journal, London, February 4, 2000

CCOOPPPPEERRBBEELLTT MMIINNIINNGG,,

AAGGRRIICCUULLTTUURRAALL &&

CCOOMMMMEERRCCIIAALL SSHHOOWW(incorporating separate tradedays for ZAMINEX exhibitors)

May 31st - June 4th

Contact: PO Box 20944, Kitwe, ZambiaTel: +260 2 225008/230611

Fax: +260 2 227033E-Mail: [email protected]

The copperbelt Mining, Agricultural and Commercial Show is situated at thecentre of Zambia’s fastest growing business area. Take advantage of theprivatization of the Mines to promote your products and services to the

people that count in the Zambian Mining Industry.

CACSS ZAMINEX

AFRICA FOCUS

Risk managementOne of the reasons for differences of opin-

ion over a country’s mining potential is thatof the perception of political and businessrisk in the region. This increasingly impor-tant element of mining companies’ opera-tions will be addressed at the Indaba confer-ence in a paper by Tara O’Connor#. Shenotes that a hundred years ago minerswould happily take enormous personal risksto explore in hostile environments – some-times with spectacular rewards – but this ismore or less impossible in the increasinglyregulated and accountable world of the 21stCentury. Only the most foolhardy will enterinto a new enterprise without first properlyweighing up the consequences.

Yet risk is a notoriously difficult conceptto define properly. Ten individuals will allhave different perceptions of what riskmeans to them, and how risk should beapproached. In the business sense, risk isperhaps a threat that a company will notachieve its corporate objectives – though, ofcourse, not all risks are equal in their impactand importance to a particular company.

Traditionally, businesses have focusedtoo much on market, financial and credit

risk; too few companies have adopted aholistic approach, considering the entirerange of risks, from the market to economic,political, operational and, increasingly, rep-utational.

Of course, the other side of the risk ‘coin’is reward, or opportunity, and companiesthat successfully link the two are often suc-cessful in their enterprises. All enterprisesmust take risks to stand any chance ofmaking money, and an entirely risk-aversefirm is very unlikely to be profitable.Appreciation of risk will help understandthe returns, while an awareness of risk willassist board members and senior manage-ment to plan and allocate resources effec-tively.

Ms O’Connor notes that many firms areoperating in environments where nationalauthorities are at least beginning to recom-mend clear standards on risk assessmentand management and, in some cases, torequire them. In the UK, for example, areport produced in 1999 by the TurnbullCommittee on corporate governancerequires all companies listed on the LondonStock Exchange to report annually on pro-cedures for risk identification, evaluationand risk control from 2000. The reportspecifically sets out that such reviewsshould cover all relevant risks – not just nar-rowly defined financial ones.

The implications of the Turnbull Reportare potentially far-reaching. Many non-UKbased companies will be forced to complyowing to their London listing. Already, theEuropean Union has shown interest inproposing similar guidelines elsewhere inEurope. Australia and New Zealand haveco-operated to produce what is probably themost comprehensive code for risk identifica-tion, evaluation and management.

An effective methodology to identify,evaluate and manage risk is crucial to min-ing companies if they are to ensure properrisk control. There are literally hundreds ofmethodologies to choose from: quantitative,qualitative, subjective, objective, academic,software-based and instinct-driven. There isnot one that will fit all corporate cultures,however. Each company has its very ownspecific tolerances, capabilities and atti-tudes towards risk. The most effectivemethodologies are those that are easy tounderstand, straightforward to use, widelyapplicable, and with clearly useful outputs.Hard-pressed country managers are muchmore likely to use a more straightforwardprocess that allows for a relatively highdegree of experience and subjectivity, than ahighly complex, ‘scientific’ approach.

To meet this need, Control Risks has pro-duced its own methodology. This has beendeveloped from its own 25 years experience#Regional manager, Africa, Control Risks Group Ltd.

81Mining Journal, London, February 4, 2000

Continuing the 30-Year Traditionof Technology and Integrity

■ Geology and Resource Estimation

■ Permitting and Closure Planning

■ Financial Evaluation and Analysis

■ Metallurgy and Process Engineering

■ Feasibility Studies and Due Diligence

■ Capital and Operating Cost Estimation

■ Mine Engineering and Reserve Estimation

■ Geotechnical and Environmental Engineering

Denver:274 Union Blvd., Suite 200

Lakewood, CO 80228

(303) 986-6950

Fax (303) 987-8907

New York SeattleGillette

LimaSantiago

Vancouver:14th Floor, 400 Burrard St.

Vancouver, B.C. V6C 3G2

(604) 643-1730

Fax (604) 643-1731

Fax (206) 328-5581

e-mail: [email protected] www.pincock.com

PINCOCK ALLEN & HOLTDelivering smarter solutions

founded 1911 MINERALS INDUSTRY CONSULTANTSDenver: 303-620-0020 ● London 44-20-7589-9903Santiago: 562-243-0022 ● Toronto 416-369-9011

Guadalajara: 523-121-1073 ● New York: 212-684-4150Sydney: 612-9954-4988 ● Vancouver: 604-646-4666

w w w . d o l b e a r . c o m

BEHRE DOLBEAR

A F R I C A

V A L U EFocus On

in

AFRICA FOCUS

as well as benchmarking best practice fromrisk management around the world. It isdesigned to be used when focusing on a spe-cific project, but can be applied to a widerbusiness, or even a country. A summary ofthese risks in Africa is contained in theadjoining article (this issue, p.84).

Most companies’ ultimate objective intheir risk management processes is to knowand understand all the risks that are facedby a particular business. While this is clear-ly well beyond the remit of most analysis,this process can be replicated on a smallerscale. Many companies organise large-scaleworkshops and brainstorming sessions tocollate a wide range of internal views aboutthe risks that a business faces, and question-naires and checklists of risks are usuallypart of this process.

However, a detailed checklist called the‘Basic Menu of Risks’ is the foundation ofthis process in Control Risks’ methodology.The main benefit of using a checklist is topromote the spread of a common under-standing about business risk, as anyattempt to generate a consolidated pictureof risk will be frustrated if agreed terminol-ogy is not recognised by all.

The menu document comprises eight fun-damental categories of risks that could real-istically impact upon a project. Each riskcategory includes around 10-20 risk eventsor processes; some appear under more thanone category. The categories also include acolumn of ‘Actors’ (such as criminals, ter-rorists, business partners, vested interests,corrupt officials, regulatory bodies, and soon). A third column comprises the Channelsor Causes of a risk taking place (eg, socialproblems, political crisis, mismanagement,fraud and nepotism in the legal system).

The main elements are:1. Identification. A workshop team compris-ing country risk analysts and other consul-tants uses Control Risks’ eight-sectionBasic Menu of Risks to identify the risksthat could realistically impact upon a pro-ject. Ideally, additional risk areas such asmarket risk and credit risk are added, givinga comprehensive overall picture. 2. Evaluation. The team then measures theimpact of a risk on a project (in terms offinancial and operational impact), againstits likelihood of occurring, using anImpact:Likelihood Matrix. This stage willhighlight the risks that need detailed assess-ment and management.3. Assessment. Next, a detailed writtenreport or briefing, focusing on significantrisks identified and evaluated in the firsttwo stages, is produced. This typicallyincludes a section on the essential political,security and operational contexts, anddetailed discussion of how and why the vari-ous risks could impact on a project. 4. Recommendations. Lastly, recommenda-tions on priorities for immediate manage-ment and longer-term strategy are given.

Project financeAnother paper being presented at the

Indaba conference is by Alex Panko+, enti-tled ‘Back to basics – the re-emergence ofmining project finance’. Mr Panko notesthat mining project finance has sufferedalong with the industry itself in the pastthree years, which has witnessed the Bre-Xscandal; the Asian and Russian financialcrises; a slump in basic commodity prices;a marked decrease in global explorationspending; a wave of industry consolida-tions, mergers and acquisitions; and contin-uing political crises in a number of emergingmining regions.

Some banks have concluded that miningis all together too risky, and that the onlymining projects that would get financed inthe future would be those undertaken by thevery largest mining companies, with termsand conditions reflecting their balancesheets and credit ratings. All of this putspressure on banks worldwide to focus onreturn on equity, rather than market shareand, as a result, the mining project financemarket has indeed contracted. Mr Pankobelieves that there are probably fewer thanten ‘serious’ mining banks left.

Mr Panko argues that, because mining isa capital intensive business, and the sectoritself is highly cyclical and anything butstable, it makes sense to deal with bankswhich thoroughly appreciate the miningindustry, and have the size, experience, andsufficiently flexible approach to share theburden – and not just be good to you whencommodity prices enable everyone to makea decent living.

Whilst those companies with sufficientresources and critical mass will continue togrow and finance new projects through acombination of cash-flow and cheap creditlines, there will always be circumstances forcompanies such as these to seek projectfinance for the development of a new mine,and, of course, project finance is likely toremain the main vehicle for smaller andmedium-sized mining companies to expandand develop.

The true definition of project, or non-recourse, finance is that the borrowing is onlyrepaid from project cash-flows, and the pro-ject assets represent the only security avail-able. Thus it is important to emphasise that:

First, lenders will be effectively sharingproject and political risks with the sponsorfor, once the project has been fully con-structed and has passed a number of perfor-mance (or completion) tests, the bank willno longer have any financial recourse to theproject sponsor.

Second, as project finance is tailored tothe characteristics and lifespan of a particu-lar project, it can be available for longerrepayment terms than simple corporateloans. For the right project and sponsor,transactions involving a commitment (from

the date of signing until the end of thescheduled repayment period) of ten years orsometimes more are available, even forthose in certain emerging markets.

Third, by going non-recourse, the debtobligation on a sponsor’s balance sheet canbe removed, thereby helping to free-up cred-it lines and borrowing capacity for otherthings, such as the truly huge mining deals;for acquisitions, when acting quickly canmean the difference between success andfailure; for reserving balance sheet capacityfor unforeseen opportunities; when needingto consider the financing position of fellowsponsors; or when the financing involves amining project as part of a much larger deal.

Fourth, project finance (by definition)has to involve a flexible approach fromlenders. This is because each individualfinancing is usually tailor-made for the indi-vidual project. Loan repayments have to beflexible, and are usually structured toreflect anticipated project cash-flows. Inaddition, ‘borrowing base’ mechanisms canlink the provision of additional funding tothe proving up of additional reserves.

Fifth, the workload involved in obtainingthe requisite finance can be shared with thearranger of a project finance facility. Forexample, a suitably qualified arranger orarrangers can save a sponsor the expense ofappointing a separate financial adviser,through balancing the desires of lenderswith the commercial realities of a project.

Sixth, a syndicated project financing,which is required for the larger project loans,can often open doors to new banks. In addi-tion, a strong syndicate of quality bankshelps give a project and its sponsor(s) a cer-tain degree of commercial acceptability.

Seventh, project finance can help savecosts, as construction will invariablyinvolve one or a number of fixed-price con-tracts with associated penalty and bonusclauses attached. This in turn helps ensurethat costs are realistically forecast andclosely adhered to.

Finally, in certain situations, projectfinancing can be structured to enable asmall sponsor to maximise ownership andminimise dilution. There will always be acertain price to pay for this, not least beingthe premium attached to a fixed-price con-struction contract with third party contrac-tors, and usually some form of additionalequity-based remuneration for the arranger.However, Mr Panko notes that small spon-sored projects will only get financed in thecurrent climate if the project economics areexceptional, political risk is fully covered,and the sponsor can clearly demonstrate ahighly visible means of coping with capitalcost overruns or construction delays.

In his paper to the Indaba conference, MrPanko observes that many potential inter-national investors are not so much hostile as

+Global sector co-ordinator (metals & mining), DresdnerKleinwort Benson.

82 Mining Journal, London, February 4, 2000

AFRICA FOCUS

indifferent to Africa, and many mean SouthAfrica when they talk about the continent.Africa suffers generally from a shortage ofskilled workers, and an infrastructure whichis almost non-existent.

Moreover, after a gap of a few years, polit-ical instability in the region has once againignited, with chaos in the DemocraticRepublic of Congo pulling in many neigh-bouring countries. Angola’s civil war hasflared up, as have those in Ethiopia, andSierra Leone, Lesotho and Namibia havealso had their conflicts, and the relationshipbetween South Africa and Zimbabweremains frosty. All this has convinced inter-national investors that Africa is a dangerousplace in which to operate. Throw in theAIDS epidemic and the culture of corrup-tion, and potential investment looks evenmore unstable.

African low pointsMr Panko notes the failure of the Hartley

platinum project in Zimbabwe andAshanti’s hedging problems as being partic-ular low points during the past year for theAfrican mining industry. Hartley was thelargest single private sector investment inZimbabwe since independence in 1980, andthe withdrawal of BHP has shaken the

country and its mining industry. AlthoughHartley was a very difficult mine to run,analysts believe the political and economicclimate in Zimbabwe and the increasing ill-will and political interference by the govern-ment towards the company was the decid-ing factor in the withdrawal. Hartley’ssophisticated trackless mining technologyrequired skilled and experienced staff, anddelays in granting visas to experiencedexpatriate staff contributed to the failure.

Ghana had been the role model for emerg-ing African countries, and AshantiGoldfields was an indigenous company ofwhich black Africa could be proud. Thecountry’s enlightened economic climateattracted other mining companies, andcountries such as Tanzania looked to Ghanawhen drawing up legislation to encourageforeign investors to help them exploit theirown mineral wealth. Ashanti’s reported dif-ficulties are a sad development for Africanmining as a whole, especially as the prob-lems were not due to political risks attachedto doing business in Africa.

African high pointsMr Panko notes that, despite the contin-

uing bad press about Africa, mining projectfinancings are still being done, and coun-

tries are continuing to make foreign invest-ment more attractive. It is very encourag-ing to see numerous mining companiesusing project finance to develop a range ofmining and metals operations, with recentexamples being Barrick’s Bulyanhulu goldmine in Tanzania; Billiton’s Mozal alumini-um smelter in Mozambique; RandgoldResources’ Morila gold project in Mali;Goldfield’s Tarkwa gold mine in Ghana;and Avmin’s Chambishi copper-cobalt pro-ject in Zambia.

A golden opportunity for Africa has to bethe privatisation of state assets, withZambia’s ZCCM being the most obviousexample. It is also pleasing to seeMozambique, one of the poorest countriesin the world, inviting international energyand mining companies into the countrywith a regime that is highly business friend-ly (and a supplement on Mozambique is dueto be published with the Mining Journalshortly). Tanzania is also hoping to use itsgold-mining industry to prime the localeconomy. Although opinions on SouthAfrica remain divided, it will continue to bea beacon for the continent.

Investor opinion in the ‘West’ still tendsto view all of Africa as being too insecureand politically unstable for mining invest-ment, which experienced explorationists inAfrica know is generally not the case.

83Mining Journal, London, February 4, 2000

CONTACT: DENNIS TUCKER

Switchboard (27 11) 286 3600

Mobile (27) 82 492 4957

Fax (27 11) 286 3666i

SOUTH AFRICA’S

INDEPENDENT RESOURCES

ADVISORY GROUP

FOR MORE DETAILS ON ITS

SPECIALISED ADVISORY, FINANCING

AND INVESTMENT SERVICES

TH

EC

O R N E R H

OU

SE

The Corner House (Pty) Ltd(Registration number 97/08185/07)

THE ECONOMIC DEFINITION OF

OREThis radical and scholarlybook by Ken Lane,mathematician andmining consultant,presents the theoreticalbasis for the definition ofore and a series of CaseStudies for its practicalapplication. The work isbased on his longexperience of minedesign for large scaleinternational operations-particularly forRio Tinto. It isessential reading formining geologists andmining engineers - bothat the mine and in theconsulting office. It willalso be very important toeveryone concerned withconservation studies.Available from: Mining Journal Books Ltd., P.O. Box 10,Edenbridge, Kent TN8 5NE England. Price: GBP25 (USD46)by airmail. Cash with order please.ISBN 0 900 117 45 1

Africa remains a difficult investmentenvironment for foreign companies.Across the region, levels of armed

crime continue to rise, while governmentefforts to control corruption are provingineffective. Few countries are makingmajor strides forward to improve theirinfrastructure and, although IMF andWorld Bank pressure is reducing the size ofpublic sector bureaucracy, this has yet totranslate to an improvement in policy-mak-ing and implementation. Many of theseissues were addressed by Charlie Weeks inthe December 1999 issue of Control RisksGroup’s Regional Risk Forecast. The follow-ing is an edited version of that article.

Governments may exercise formal con-trol, but in too many countries, companiesoperate in a shadowy zone between the for-mal state and the influence of ‘big men’, andlocal regional and ethnic tensions thatdetermine the stability of the operatingenvironment.

Investors will continue to look at hydro-carbons, minerals and agriculture as themain recipients of foreign direct invest-ment, though investment in power, waterand telecommunications facilities will alsoincrease.

Africa’s renaissance will depend on thesuccess of the region’s major economies.There have been a few positive develop-ments that could have a major impact onthe region over the next few years. The firstis the re-entry of Nigeria into the interna-tional community. Nigeria has its bestchance in many years of fulfilling its posi-tion as one of Africa’s two World Bank-designated strategic markets. The otherstrategic market – South Africa – has suc-cessfully managed the transition of poweraway from Nelson Mandela, and is embark-ing on the reform and consolidation of itseconomy. Economic harmonisation andgrowth in the franc zone also provides rea-son for optimism. If the conflicts inEthiopia and Eritrea and central Africa canbe resolved, this hope could fuel Afro-optimism.

Regional risksOver the next year the principal risks to

companies operating in Africa will be:

1. Security of contractsWhether investing in the private or publicsector in sub-Saharan Africa, breach of con-tract is a major threat to business activity.Investors may not be able to rely on localpartners to honour their commitments andmay face unsolicited demands for addition-al payments. In the worst cases, companiesmay find that contracts are arbitrarilyrevoked after they have invested significantcapital. Companies are often left with littlerecourse to arbitration. Contract delaysand disputes can be costly, as well as compli-

cated and time-consuming to resolve. Onlyin large-scale productions, where the projectis crucial to the economy (oil and miningsectors), are companies able to exercisesome influence over contractual issues.However, even in these sectors, some gov-ernment intervention in business activity isinevitable.

Companies will be at increased risk ofbreach of contract in countries where amajor change in government is likely. Keypartners in the venture may lose influenceor the new government may decide toreform policy in a sector and consequentlyrevise existing contracts and agreements.A number of companies which agreedcontracts with General AbdulsalamiAbubakar’s transitional government inNigeria, and paid up front, lost this moneywhen President Olusegun Obasanjo tookpower. Changes in government over the next12 months that could impact on contractsecurity are likely in Congo (DRC) andSierra Leone.

Another factor that threatens security ofcontract is inconsistency of policy decisions.This is most likely where the formal institu-tions are weak and political power is highlypersonalised, and therefore strongly depen-dent on a leadership’s whims. The countrieswhere these risks are greatest are Gabonand Liberia. In other countries, for exampleZimbabwe or Kenya, where the judiciary ismore independent and effective, the risks tocontracts are reduced. However, if contractdisputes emerge in these countries, govern-ment rulings on disputes can prove difficultto reverse.

In an environment where Africaneconomies are slowly deregulating butwhere ‘big men’ (such as Uganda’s formermilitary head and President YoweriMuseveni’s brother Salim Salek, and, inNigeria, former President IbrahimBabangida) dominate the political environ-ment, hostile local vested interests canblock contracts. This is a risk across theregion, but particularly for investors enter-ing sectors traditionally controlled bydomestic ‘big men’.

In the rapidly deregulating telecommuni-cations sector, control of GSM mobile tele-phone network licences and the local mobilephone market has often been given to thoseclose to the local ‘big men’. Existinginvestors may also face continued bureau-cratic problems and security issues as localplayers use underhand tactics to gaingreater influence in the domestic market.

Nationality can also have an impact.Non-French based companies entering

Francophone countries such as Gabon,Cameroon or Congo (Brazzaville) may facesignificant obstacles as French and regionalcompanies use their close contacts withexisting governments to make entry diffi-cult for others.

2. Security of personnel/assetsThe security environment is a major con-cern for investors and businesses operatingin sub-Saharan Africa. The nature of thethreat varies from direct attacks on compa-ny assets and personnel while operating in awar zone to kidnap and crime. A difficultsecurity environment disrupts businessactivity and makes it difficult to recruitskilled staff.

Crime (ranging from petty theft to armedrobbery) remains high across the region.Austere economic policies, rapid populationgrowth and slow economic developmentmarginalise large sections of urban popula-tions. Continued conflict increases the sup-ply of weapons, while governments fail toinvest in law and order. As such, crime posesa risk to most business activity in sub-Saharan Africa, and particular areas of riskto expatriates are major cities across theregion – Johannesburg, Nairobi, Lagos andAbidjan. Crime also pervades ports and air-ports, and is a primary concern on mine andfactory sites. It can seriously hamper busi-ness activity. However, on balance, even inextreme situations such as unloadingexports at Dar es Salaam or operating incentral Johannesburg, adequate precau-tions can reduce the risk from crime to a rea-sonable level.

Conflict undermines business operationsacross a vast swathe of Africa from easternUganda to Angola on the Atlantic coast.The impact of conflict on business activitydepends on the nature of the conflict and onthe specific project being undertaken.Although the oil and mining industries willcontinue to operate in Angola, they mayface increasing stress on their operationsfrom continued conflict. Oil companies inthe country have been little affected by theresumption of civil war but, during 2000,will remain wary of the threat of a UNITArebel attack on oil assets, either onshoreat Soyo or Cabinda, or against offshoreassets that are within range of artillery ormissiles.

In Congo (DRC) instability as a result ofregional Hutu/Tutsi tensions, the de factopartition of the east into Rwandan andUgandan spheres of interest and tensionsbetween Rwanda and Uganda as they com-pete for assets, such as diamonds and gold,mean that it is unlikely that major foreigninterests in the mining sector will be con-verted into realisable projects. Although theconflict has reached a stalemate, the with-drawal of Zimbabwean troops could funda-mentally alter the balance of power in thewar, enabling rebels to capture Mbuji-Mayiand Lubumbashi rapidly. Although they are

AFRICA FOCUS

Renaissancepostponed

84 Mining Journal, London, February 4, 2000

unlikely to target foreign companies, per-sonnel and assets in the frontline would beat incidental risk.

The conflict between Ethiopia andEritrea will cause instability in Somalia,Kenya and Djibouti in 2000. Although themain conflict will end, hostility betweenEthiopia and Eritrea will lead them to sup-port opposition groups in the other country.Eritrea is likely to offer support, in particu-lar for the Oromo Liberation Front (OLF).Both countries are also likely to continue tosupport rival warring factions in Somalia’sanarchic struggle. Somalia is expected toremain off-limits to foreign business in2000. Foreign investors will have to takeincreasing note of zones of instability in theHorn of Africa that could threaten the secu-rity of assets and personnel.

The risk of kidnap is spreading acrossAfrica, but varies in terms of intensity,motive and security of personnel. There is agrowing awareness of the potential valueof taking hostages. In mid to late 1999 therewere high-profile kidnaps in Sierra Leone,Liberia, Nigeria, Uganda and SouthAfrica.

In war-torn areas, kidnaps are generallycarried out by rebel groups who want to putacross their particular message and to gainprovisions and supplies. In some areas, suchas Uganda, where groups such as the ethnic

Hutu Interahamwe operate, their limitedunderstanding of the potential value ofhostages can lead to hostages being killed.Four tourists were killed in the Rwenzorimountains (western Uganda) in August1998 and eight tourists were killed inBwindi National Park (south-westernUganda) in March 1999.

By contrast, in the troubled Niger delta,local communities have learnt how to usehostages to gain practical rewards and makepolitical points. Local communities regular-ly take local and foreign workers hostage forperiods of up to three weeks and hostagesare seldom harmed. In the past 18 monthsthe intensity and frequency of kidnaps haverisen to the extent that hostage-takingoccurs on an almost weekly basis.

In South Africa, a new phenomenon ofpurely criminal abductions derived fromthe Nigerian Advance Fee Fraud or ‘419’scam is emerging. Abduction will remain arisk to companies in all the current war, low-intensity conflict and high crime zones ofAfrica in 2000. Countries where rebels arelikely to kidnap foreigners in 2000 includeAngola, Liberia, Sierra Leone, Somalia,eastern Ethiopia and Congo (DRC).

3. Operational and economic obstaclesAside from contract difficulties and securi-ty of personnel and assets, the main risks to

companies operating in Africa are opera-tional. The principal problem is corruption,which increases production costs (by upto 50%) and delays production, while alsocontravening international legislation andputting company reputations at risk.

Incidents of corruption range from dailypayments to police at roadblocks, to facili-tatory payments to bureaucrats in returnfor speedy hassle-free completion of admin-istration procedures, to payment of highlyinfluential key players to arrange contractsand provide high level protection to pro-jects. Corruption also means that relianceon legal redress for commercial disputescan be problematic – companies will contin-ue to avoid African courts wherever possi-ble.

There is certainly a greater global aware-ness of the need to clamp down on corrup-tion. A number of countries are makinghigh-profile efforts to clean up their con-tract tendering procedures. In Kenya, CivilService Minister Richard Leakey is leadinganti-corruption efforts, in Nigeria PresidentOlusegun Obasanjo is undertaking a similarcampaign, and in Côte d’Ivoire revelationsof ministerial corruption involving EU aidare fuelling international pressure forreform.

These efforts should result in a marginalimprovement for companies operating in

AFRICA FOCUS

85Mining Journal, London, February 4, 2000

When it comes to resources...we thrive between a rock and a hard place

SYDNEY +61 2 9250 0000 PERTH +61 8 9322 1822

This announcement appears as a mattter of record onlyAugust 1999

This announcement appears as a mattter of record onlySeptember 1999

has sold its interest in the

Moura Coal Mineheld by BHP Mitsui Coal Pty Ltd

toPEABODY RESOURCES LIMITED

and

MITSUI COAL HOLDINGS PTY LIMITED

The consideration obtained byBHP Mitsui Coal Pty Ltd was

A$89,000,000The undersigned acted on behalf of BHP

A member of the Resource Finance Corporation Group

has acquiredthe NSW Coal Assets of

Rio Tinto Limited

together with the remining interestin the Howick Coal Mine from

Mitsubishi Development Pty Ltd

The consideration was comprisedmostly of Coal & Allied shares

and had a market value of

A$361,500,000

The undersigned acted on behalf of Coal & Allied

A member of the Resource Finance Corporation Group

COAL & ALLIED INDUSTRIES LIMITEDTHE BROKEN HILL PROPRIETARY

COMPANY LIMITED

BHP&C A

AFRICA FOCUS

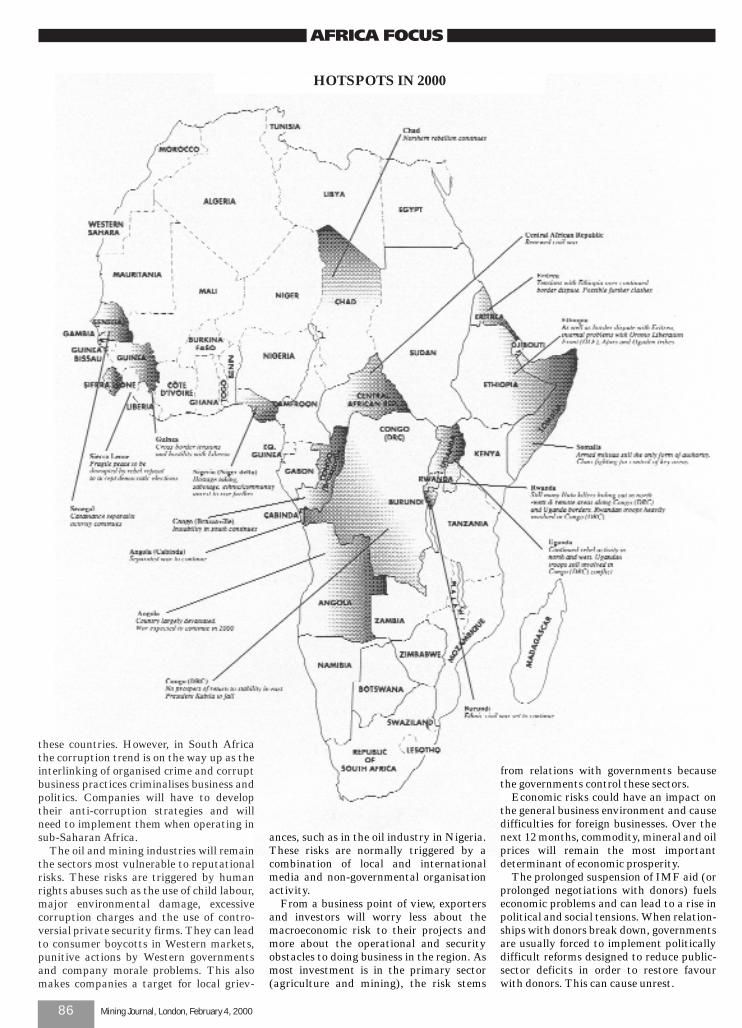

HOTSPOTS IN 2000

these countries. However, in South Africathe corruption trend is on the way up as theinterlinking of organised crime and corruptbusiness practices criminalises business andpolitics. Companies will have to developtheir anti-corruption strategies and willneed to implement them when operating insub-Saharan Africa.

The oil and mining industries will remainthe sectors most vulnerable to reputationalrisks. These risks are triggered by humanrights abuses such as the use of child labour,major environmental damage, excessivecorruption charges and the use of contro-versial private security firms. They can leadto consumer boycotts in Western markets,punitive actions by Western governmentsand company morale problems. This alsomakes companies a target for local griev-

ances, such as in the oil industry in Nigeria.These risks are normally triggered by acombination of local and internationalmedia and non-governmental organisationactivity.

From a business point of view, exportersand investors will worry less about themacroeconomic risk to their projects andmore about the operational and securityobstacles to doing business in the region. Asmost investment is in the primary sector(agriculture and mining), the risk stems

from relations with governments becausethe governments control these sectors.

Economic risks could have an impact onthe general business environment and causedifficulties for foreign businesses. Over thenext 12 months, commodity, mineral and oilprices will remain the most importantdeterminant of economic prosperity.

The prolonged suspension of IMF aid (orprolonged negotiations with donors) fuelseconomic problems and can lead to a rise inpolitical and social tensions. When relation-ships with donors break down, governmentsare usually forced to implement politicallydifficult reforms designed to reduce public-sector deficits in order to restore favourwith donors. This can cause unrest.

86 Mining Journal, London, February 4, 2000

AFRICA FOCUS

87Mining Journal, London, February 4, 2000

Investing in the mining sector in French-speaking Africa has been a rather chal-lenging endeavour in recent years. The

paradox of investors with a legal traditionso radically different from that of the hostcountries is difficult to tackle. Indeed, mostmining companies are established in coun-tries with a common law tradition. Theseissues were addressed in a recent report byStephane Brabant* and Natalie Stevens#,of which this is a heavily-edited extract.

These differences are true not only forAustralian, Canadian and American com-panies but also for South African andEnglish mining companies. While the latterhave a long tradition of mining in English-speaking Africa, they are often unfamiliarwith the conditions applicable to mininginvestments in French-speaking Africa.This has to do not only with a language bar-rier but, more fundamentally, with a differ-ence in legal tradition – a common law tradi-tion in the English-speaking countries and acivil law tradition in the French-speakingcountries. The fact that the same wordingcan be used with different meaning in thetwo legal regimes illustrates this difference.Another essential difference is the role of theState and the rules governing its relationswith the private investor. The nature of theState’s jurisdiction also affects the issue ofmineral ownership.