www.afterschoool.t k AFTERSCHO OL's MATERIAL ☺ FOR PGPSE PARTICIPANTS CAPITAL STRUCTURE DECISIONS IN FINANCIAL MANAGEMENT Dr. T.K. Jain. AFTERSCHO OL ☺ Centre for social entrepreneurship Bikaner M: 9414430763 [email protected] www.afterschool.tk , www.afterschoool.tk

Capital Structure Decisions in Financial Management

Nov 21, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

CAPITAL STRUCTURE DECISIONS IN FINANCIAL

MANAGEMENTDr. T.K. Jain.

AFTERSCHO☺OLCentre for social entrepreneurship

Bikaner M: [email protected]

www.afterschool.tk, www.afterschoool.tk

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

What is leveraging?

• When a firm uses fixed cost sources of funds, it is called leveraging. Higher the ratio of debt in total funds, higher the leveraging.

• Unleveraged firm is that which has no debt.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

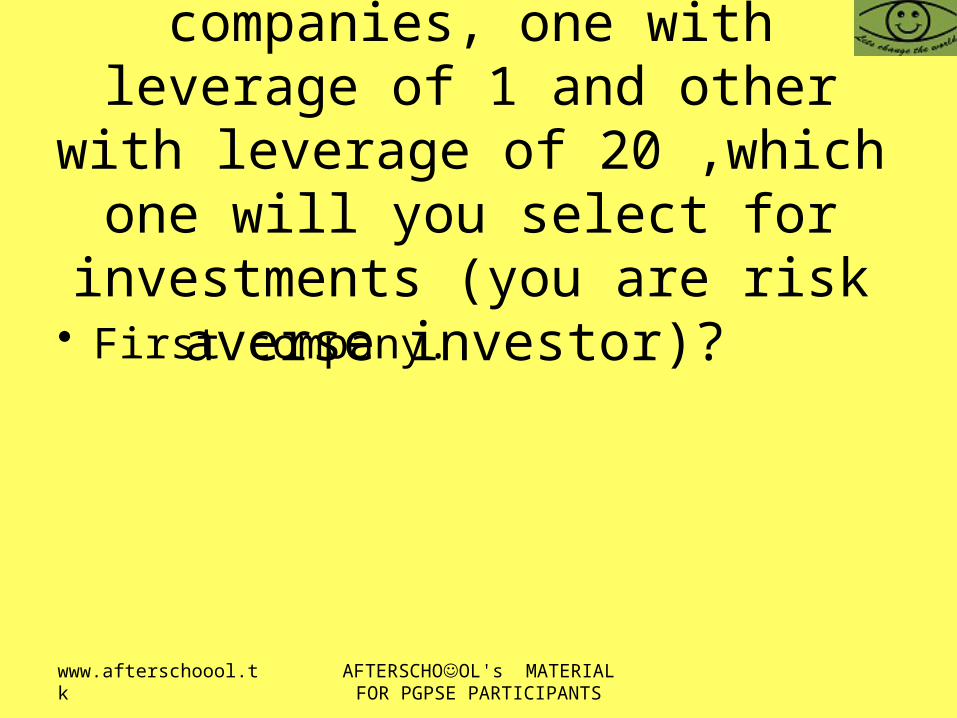

If there are two companies, one with leverage of 1 and other with

leverage of 20 ,which one will you select for investments (you are risk

averse investor)? • First company.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

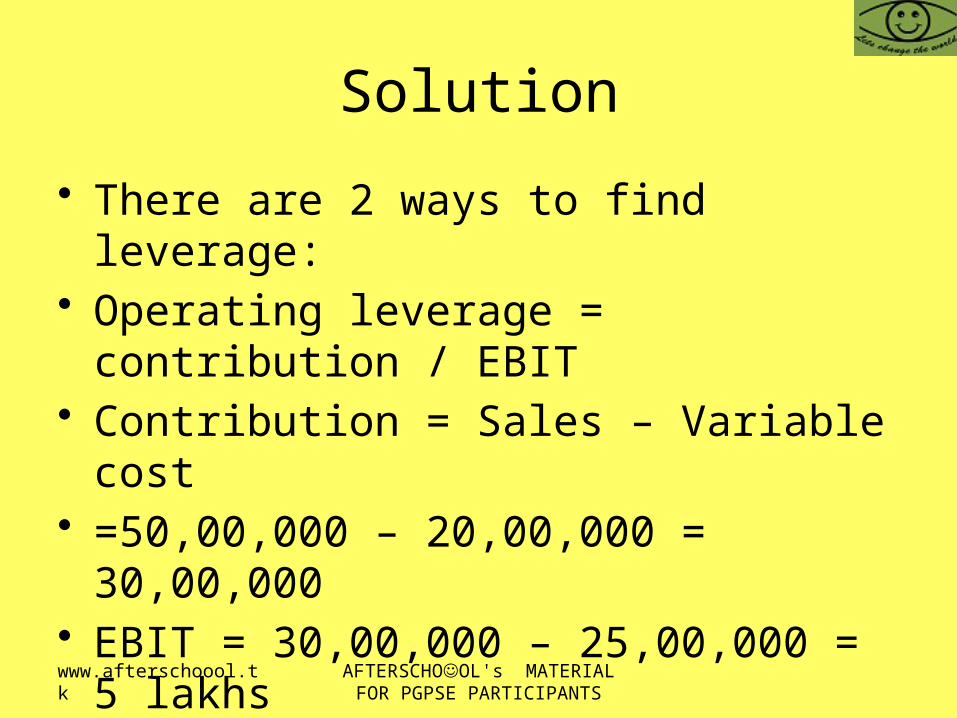

Solution

• There are 2 ways to find leverage: • Operating leverage = contribution / EBIT• Contribution = Sales – Variable cost• =50,00,000 – 20,00,000 = 30,00,000• EBIT = 30,00,000 – 25,00,000 = 5 lakhs• Operating leverage = 30 lakhs/ 5 lakhs• Thus operating leverage is 6 times. Ans.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

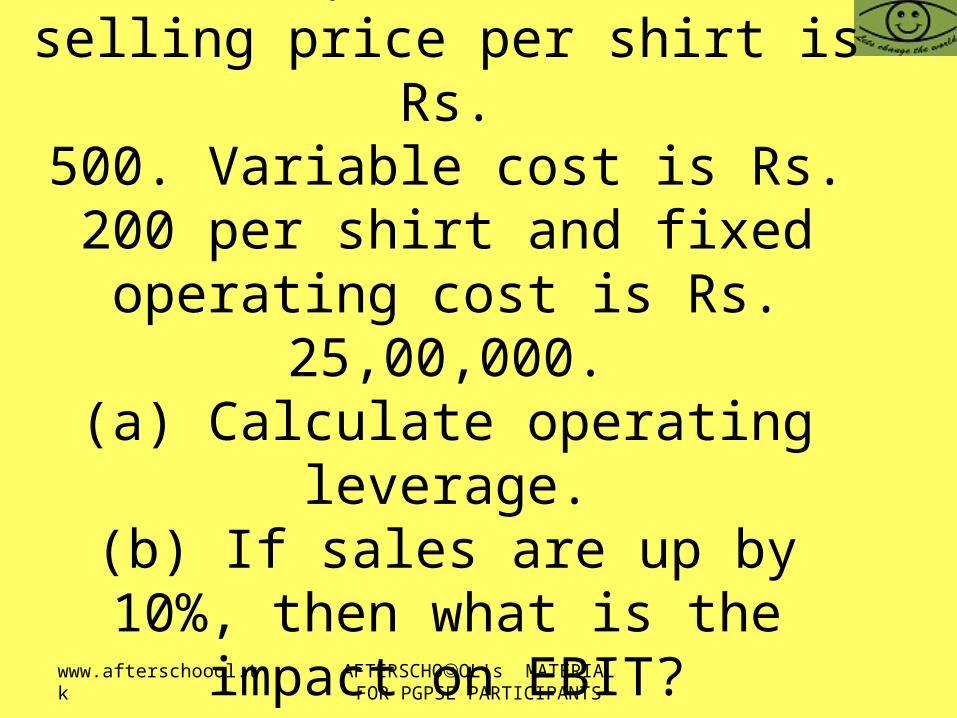

A Company produces and sells 10,000 shirts. The selling price per

shirt is Rs.500. Variable cost is Rs. 200 per

shirt and fixed operating cost is Rs. 25,00,000.

(a) Calculate operating leverage.(b) If sales are up by 10%, then

what is the impact on EBIT?

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

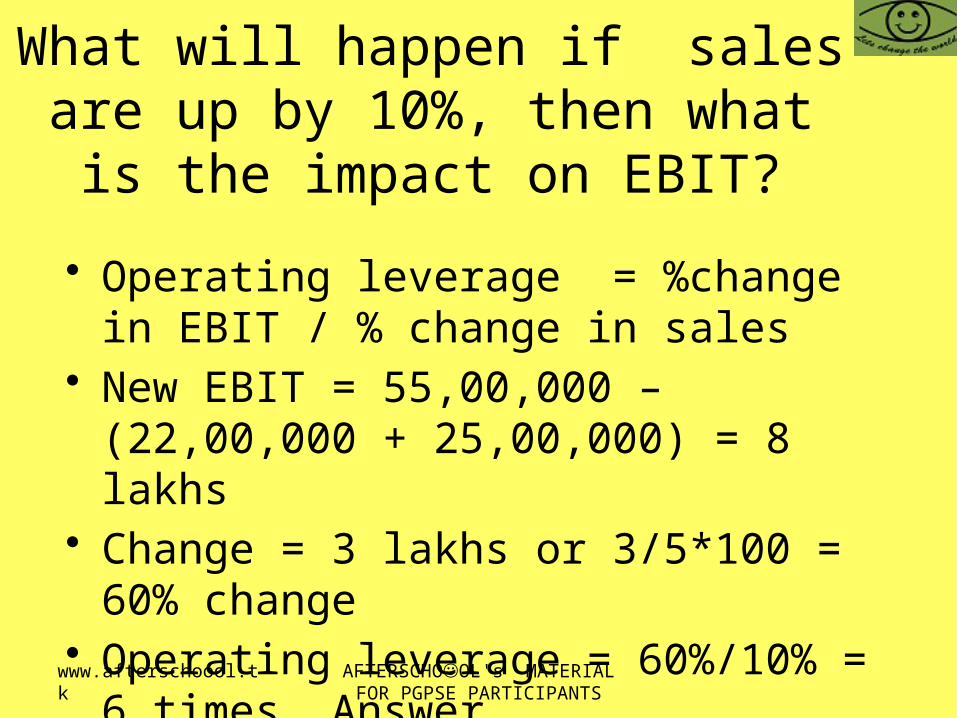

What will happen if sales are up by 10%, then what is the impact on

EBIT?

• Operating leverage = %change in EBIT / % change in sales

• New EBIT = 55,00,000 – (22,00,000 + 25,00,000) = 8 lakhs

• Change = 3 lakhs or 3/5*100 = 60% change

• Operating leverage = 60%/10% = 6 times. Answer.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

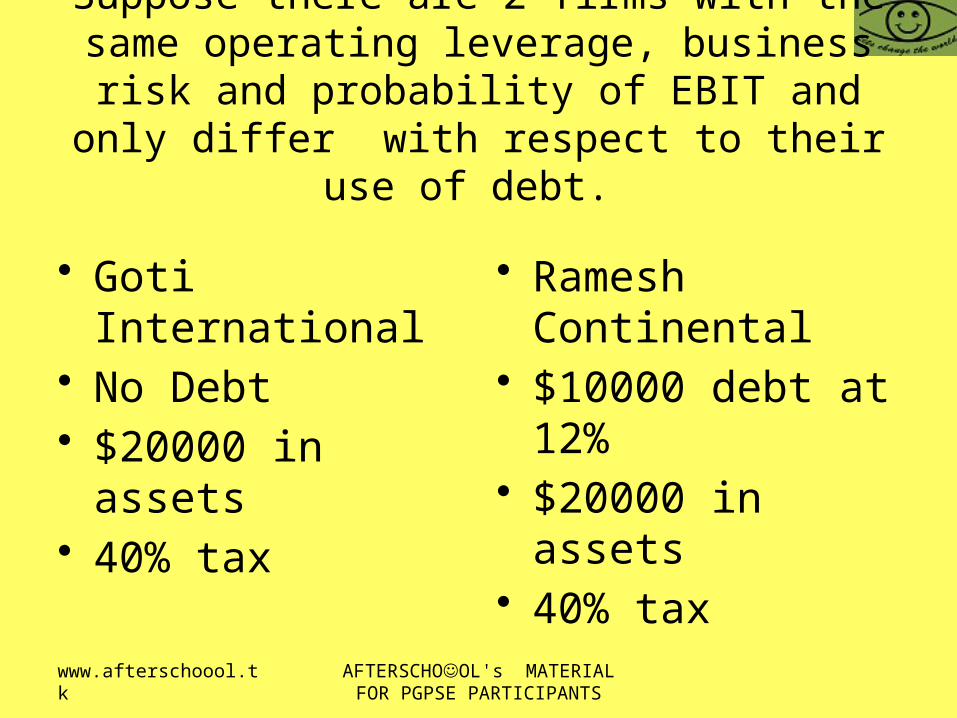

Suppose there are 2 firms with the same operating leverage, business risk and

probability of EBIT and only differ with respect to their use of debt.

• Goti International • No Debt• $20000 in assets• 40% tax

• Ramesh Continental

• $10000 debt at 12%

• $20000 in assets• 40% tax

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

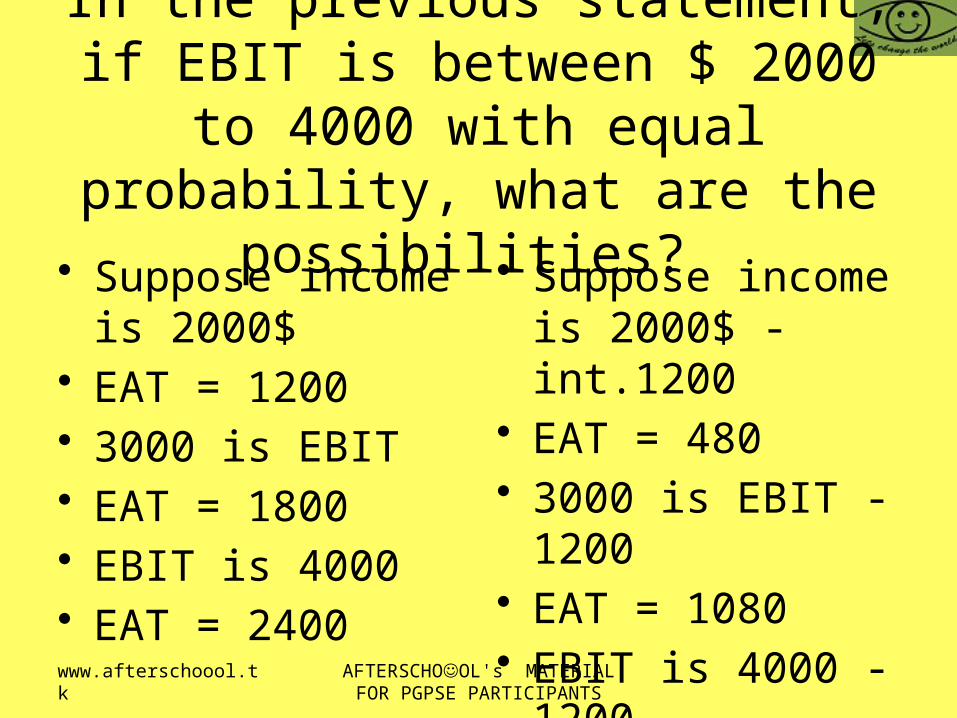

In the previous statement, if EBIT is between $ 2000 to 4000 with equal

probability, what are the possibilities?

• Suppose income is 2000$

• EAT = 1200 • 3000 is EBIT• EAT = 1800• EBIT is 4000• EAT = 2400

• Suppose income is 2000$ - int.1200

• EAT = 480• 3000 is EBIT -

1200• EAT = 1080• EBIT is 4000 -

1200• EAT = 1680

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

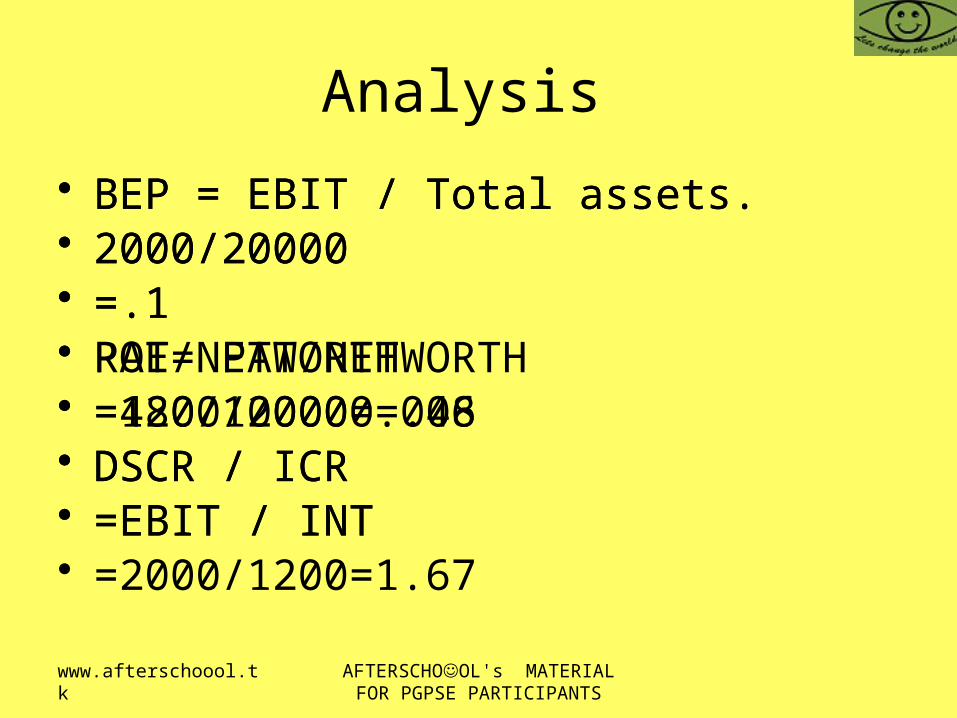

Analysis • BEP = EBIT / Total assets. • 2000/20000• =.1• ROE= PAT/NETWORTH• =1200/20000=.06• DSCR / ICR• =EBIT / INT

• BEP = EBIT / Total assets. • 2000/20000• =.1• PAT/NETWORTH• =480/10000=.048• DSCR / ICR• =EBIT / INT• =2000/1200=1.67

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

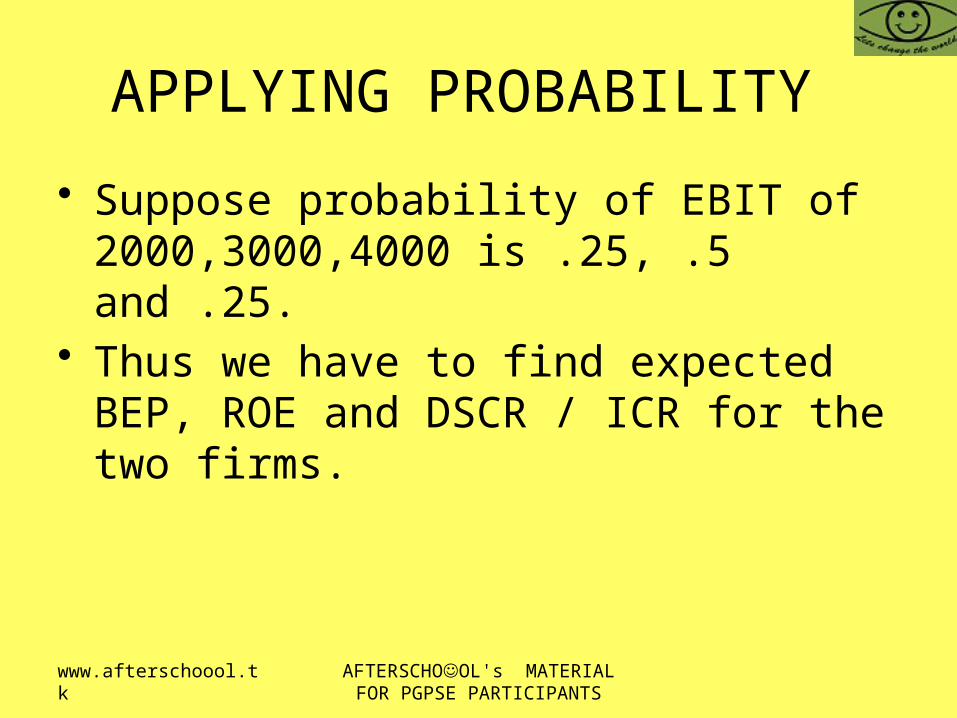

APPLYING PROBABILITY

• Suppose probability of EBIT of 2000,3000,4000 is .25, .5 and .25.

• Thus we have to find expected BEP, ROE and DSCR / ICR for the two firms.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

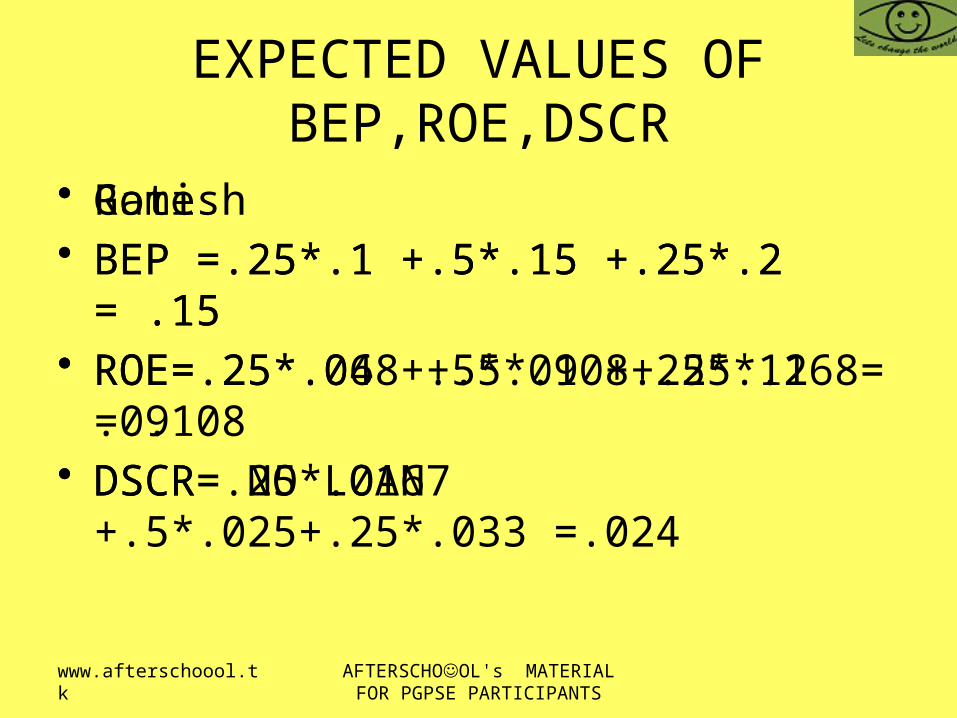

EXPECTED VALUES OF BEP,ROE,DSCR

• Goti • BEP =.25*.1 +.5*.15 +.25*.2 = .15• ROE=.25*.06 +.5*.09 +.25*.12 = .09• DSCR= NO LOAN

• Ramesh• BEP =.25*.1 +.5*.15 +.25*.2 = .15• ROE=.25*.048 +.5*.108+.25*.168 = .108• DSCR=.25*.0167 +.5*.025+.25*.033 =.024

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

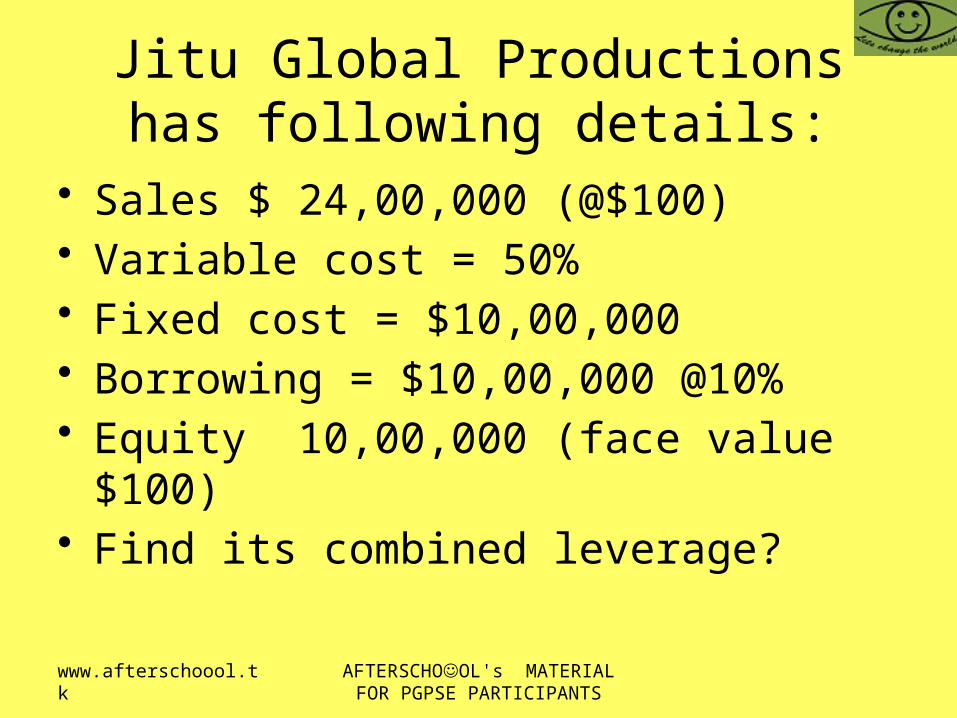

Jitu Global Productions has following details:

• Sales $ 24,00,000 (@$100)• Variable cost = 50%• Fixed cost = $10,00,000• Borrowing = $10,00,000 @10%• Equity 10,00,000 (face value $100)• Find its combined leverage?

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

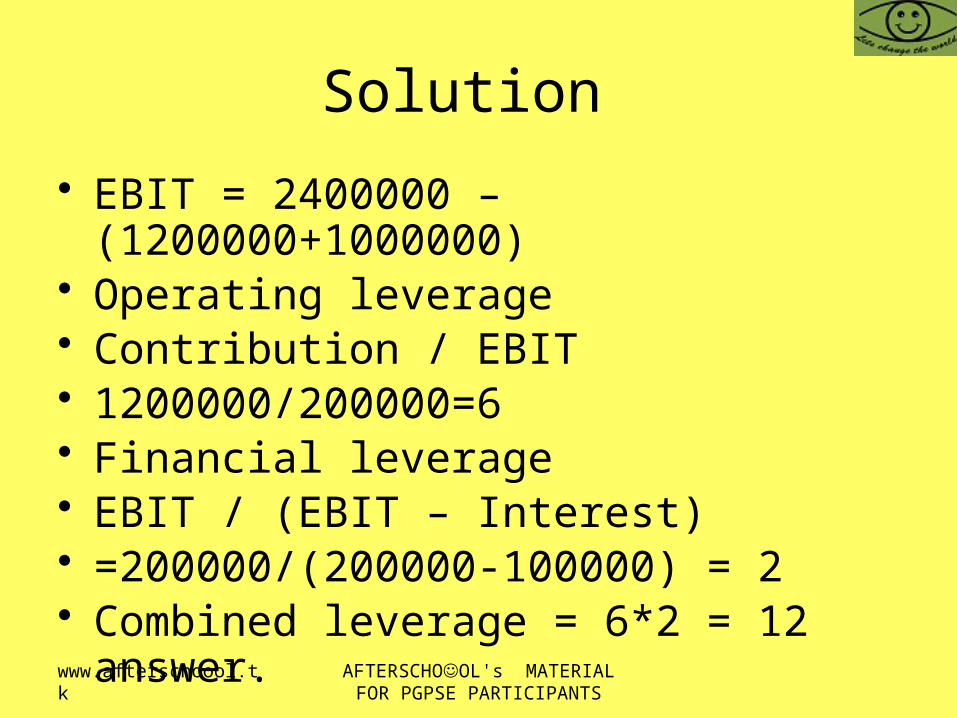

Solution • EBIT = 2400000 – (1200000+1000000)• Operating leverage • Contribution / EBIT• 1200000/200000=6• Financial leverage• EBIT / (EBIT – Interest)• =200000/(200000-100000) = 2• Combined leverage = 6*2 = 12 answer.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

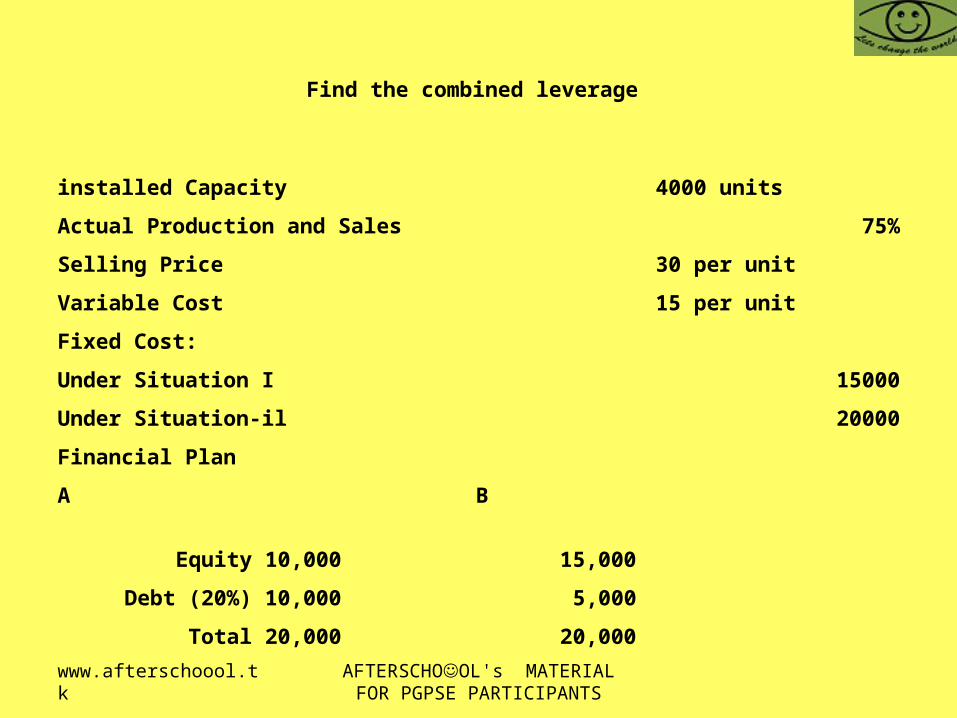

Find the combined leverage

installed Capacity 4000 unitsActual Production and Sales 75%Selling Price 30 per unitVariable Cost 15 per unitFixed Cost:Under Situation I 15000Under Situation-il 20000Financial PlanA B

Equity 10,000 15,000Debt (20%) 10,000 5,000

Total 20,000 20,000

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

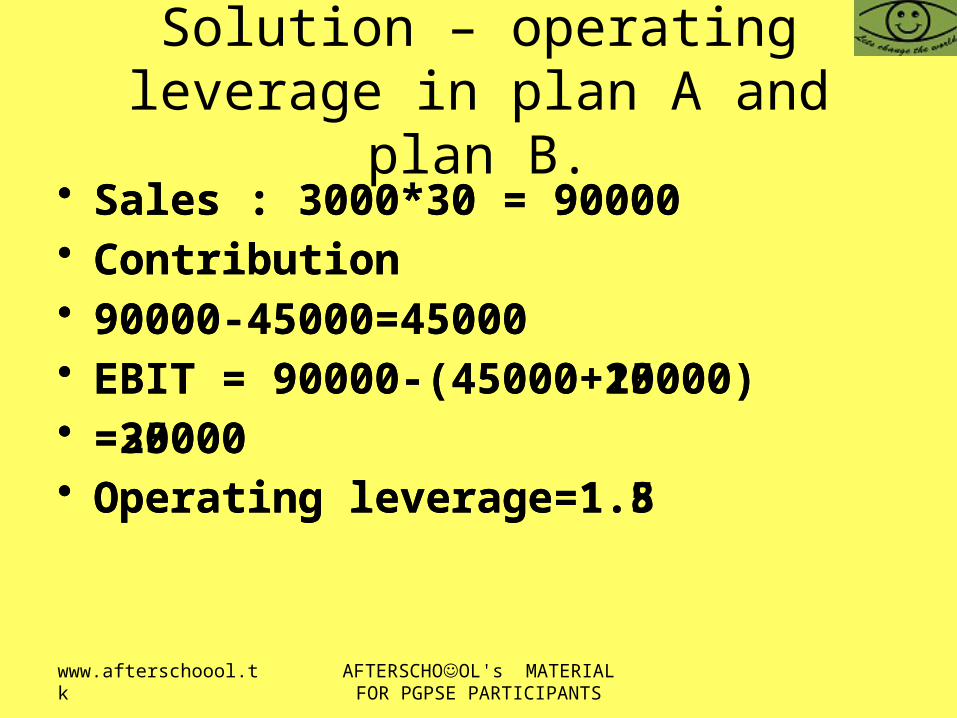

Solution – operating leverage in plan A and plan B.

• Sales : 3000*30 = 90000• Contribution • 90000-45000=45000• EBIT = 90000-(45000+15000)• =30000• Operating leverage=1.5

• Sales : 3000*30 = 90000• Contribution • 90000-45000=45000• EBIT = 90000-(45000+20000)• =25000• Operating leverage=1.8

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

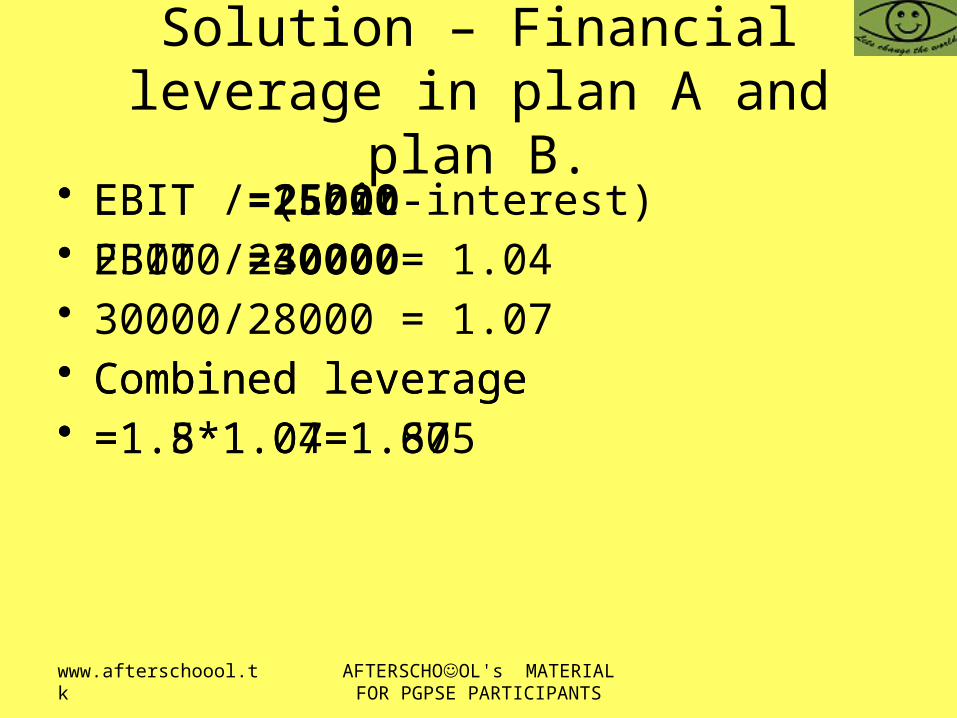

Solution – Financial leverage in plan A and plan B.

• EBIT / (Ebit-interest)• EBIT =30000• 30000/28000 = 1.07• Combined leverage • =1.5*1.07=1.605

• EBIT =25000• 25000/24000 = 1.04

• Combined leverage • =1.8*1.04=1.87

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

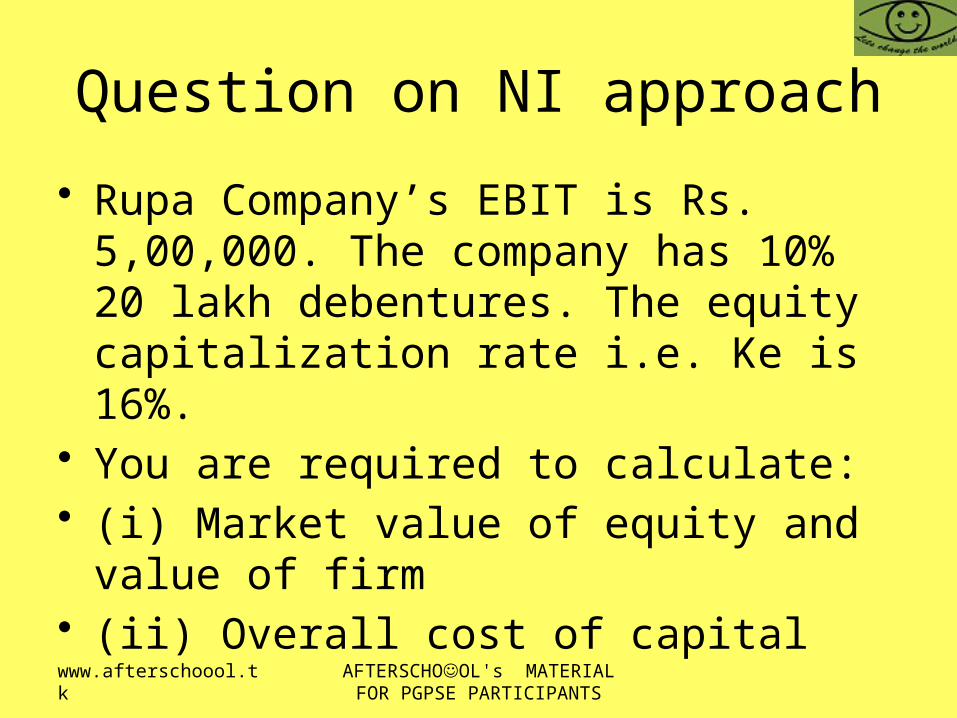

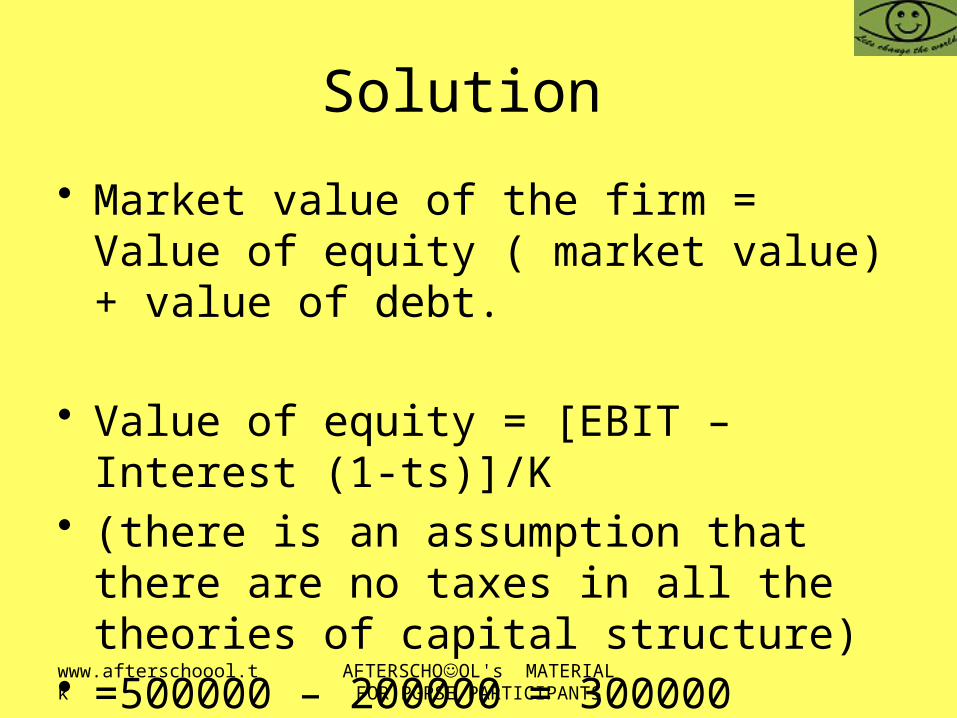

Question on NI approach

• Rupa Company’s EBIT is Rs. 5,00,000. The company has 10% 20 lakh debentures. The equity capitalization rate i.e. Ke is 16%.

• You are required to calculate:• (i) Market value of equity and value of firm• (ii) Overall cost of capital

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Solution

• Market value of the firm = Value of equity ( market value) + value of debt.

• Value of equity = [EBIT – Interest (1-ts)]/K• (there is an assumption that there are no

taxes in all the theories of capital structure)

• =500000 – 200000 = 300000

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

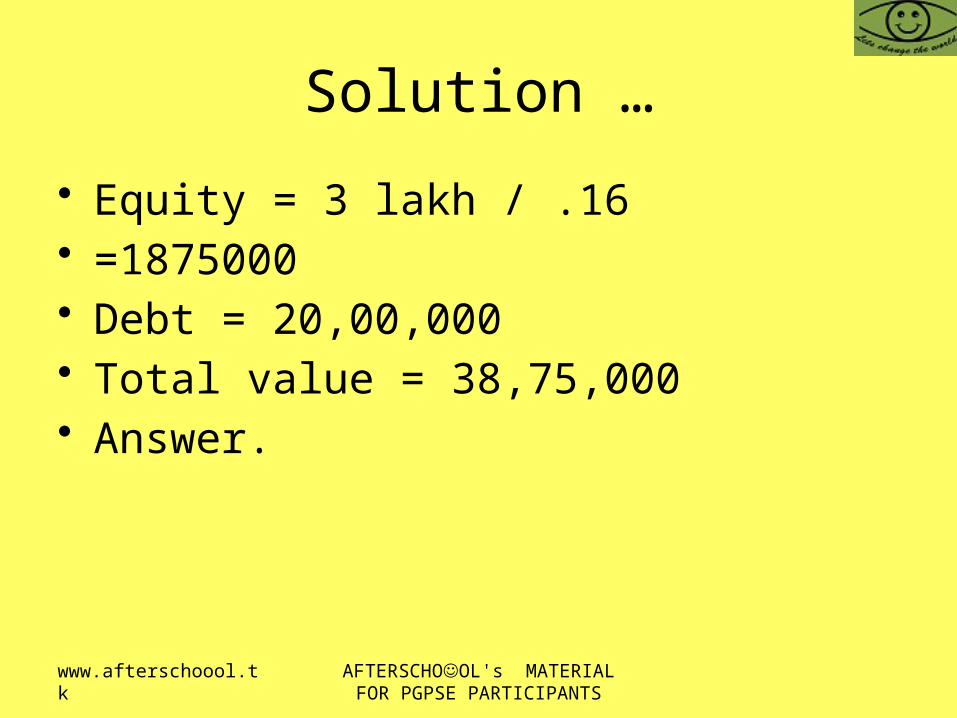

Solution …

• Equity = 3 lakh / .16• =1875000• Debt = 20,00,000• Total value = 38,75,000 • Answer.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

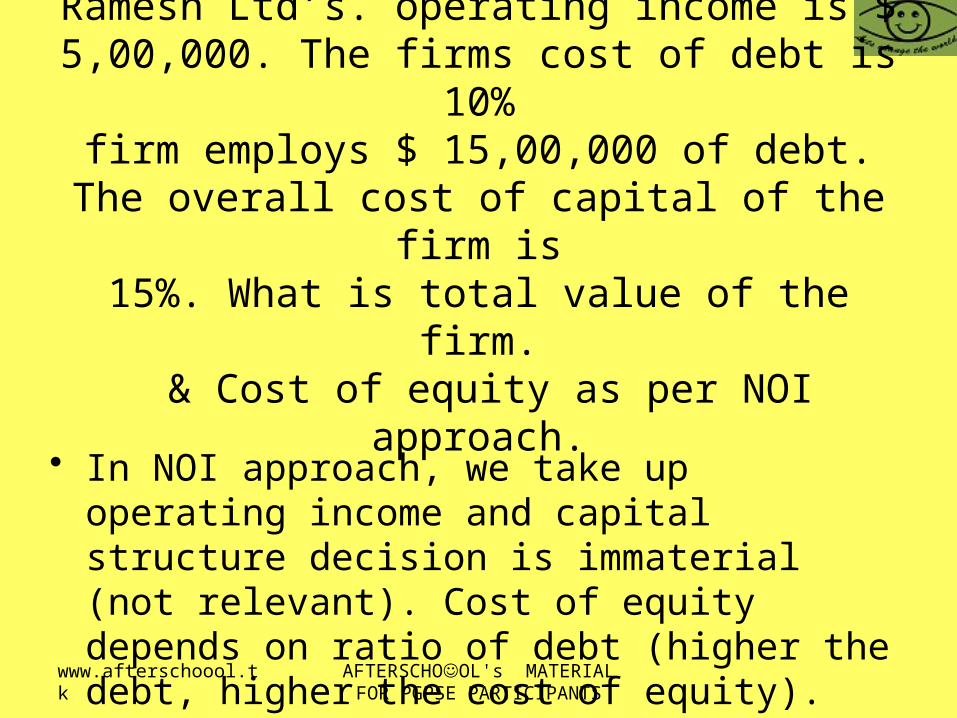

Ramesh Ltd’s. operating income is $ 5,00,000. The firms cost of debt is 10%

firm employs $ 15,00,000 of debt. The overall cost of capital of the firm is

15%. What is total value of the firm. & Cost of equity as per NOI approach.

• In NOI approach, we take up operating income and capital structure decision is immaterial (not relevant). Cost of equity depends on ratio of debt (higher the debt, higher the cost of equity).

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

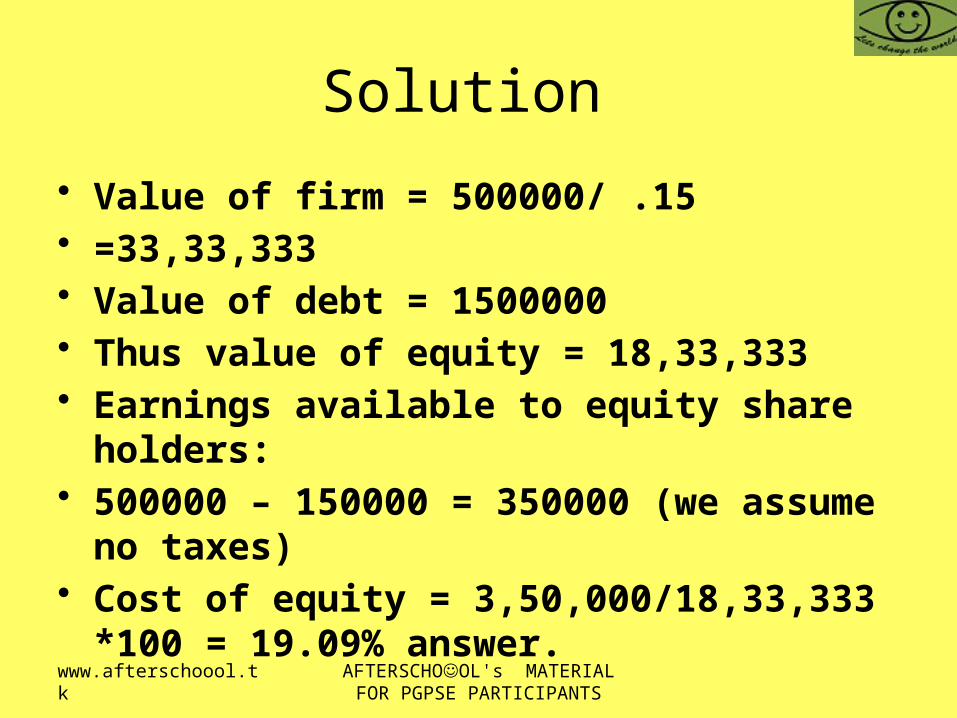

Solution • Value of firm = 500000/ .15• =33,33,333• Value of debt = 1500000• Thus value of equity = 18,33,333• Earnings available to equity share holders: • 500000 – 150000 = 350000 (we assume no

taxes)• Cost of equity = 3,50,000/18,33,333 *100 =

19.09% answer.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

There are two firms – Goti International & Ramesh Global. Goti International is leveraged

company having debt of $ 100,000 @ 7%. Cost of equity of both the

companies is 11.5% and 10% respectively.analyse using MM

approach. EBIT = $20000 • As you can see that the overall value of

the firm is same – so no impact of debt.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Analysis • Goti• Debt = 100000• EAI = 20000-7000• =13000 (we assume no taxes)• Equity • =13000/.115• =113043• Total value • =2,13,043

• Ramesh• EBIT = 20000• Equity = 20000/.1• =200000

• Thus we can see that the value of Goti International is little bit higher

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Arbitrage process • you may invest in Goti International • Suppose we invest 10000, we get = 1150• You may borrow (take personal leverage) and invest in

Ramesh – because it it unleveraged firm • Here we can borrow 10000 and invest our own 10000.

We get 2000 as return, and we have to pay interest of 700, so finally we have 1300 left out.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Vinod Bhugari Continental has EBIT of $ 100000. Company has 10% debentures of $ 5 Lakhs and equity capitalisation rate is 15%.

What is the value of the firm as per traditional approach ?

• Earnings after interest = 100000-50000• =50000 (we ignore taxes)• Value of equity = 50000/.15 = 333333 • Value of the firm=$ 833333 answer.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

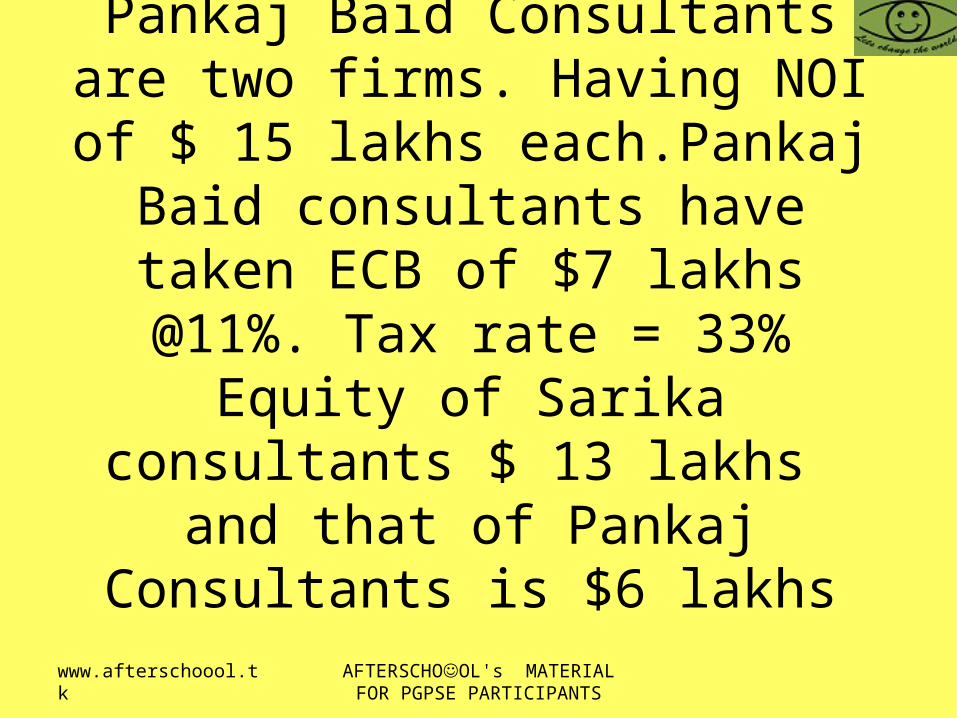

Sarika Consultants & Pankaj Baid Consultants are two firms. Having

NOI of $ 15 lakhs each.Pankaj Baid consultants have taken ECB of $7

lakhs @11%. Tax rate = 33% Equity of Sarika consultants $ 13

lakhs and that of Pankaj Consultants is $6 lakhs

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

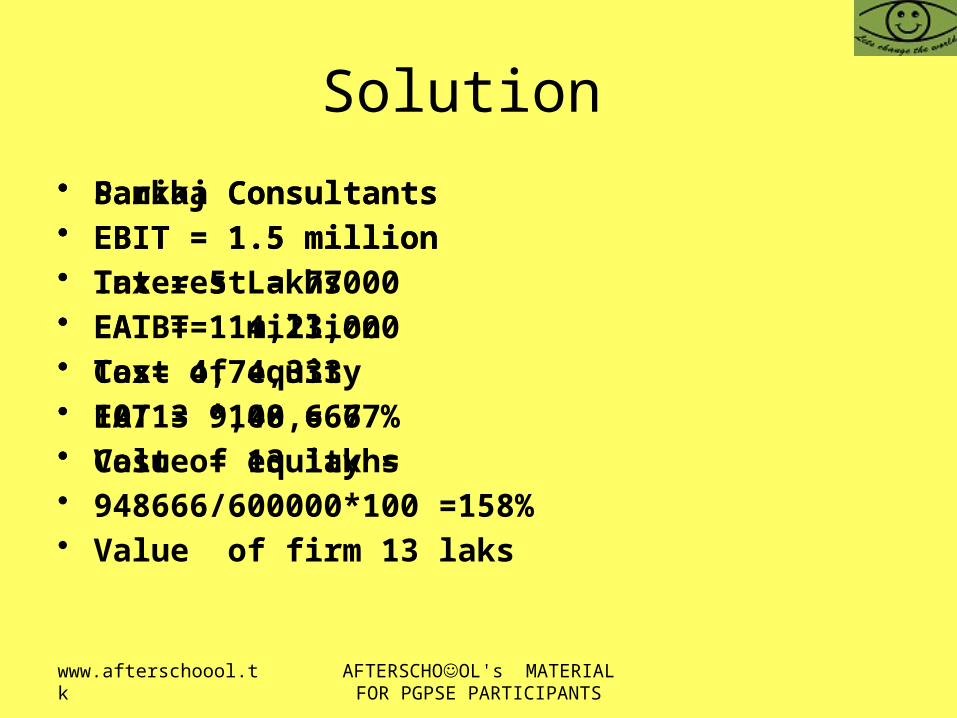

Solution • Sarika Consultants• EBIT = 1.5 million• Tax = 5 Lakhs• EAT = 1 million• Cost of equity • 10/13 *100 = 77%• Value = 13 lakhs

• Pankaj Consultants• EBIT = 1.5 million• Interest = 77000• EAIBT= 14,23,000• Tax= 4,74,333• EAT = 9,48,666• Cost of equity = • 948666/600000*100 =158%• Value of firm 13 laks

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

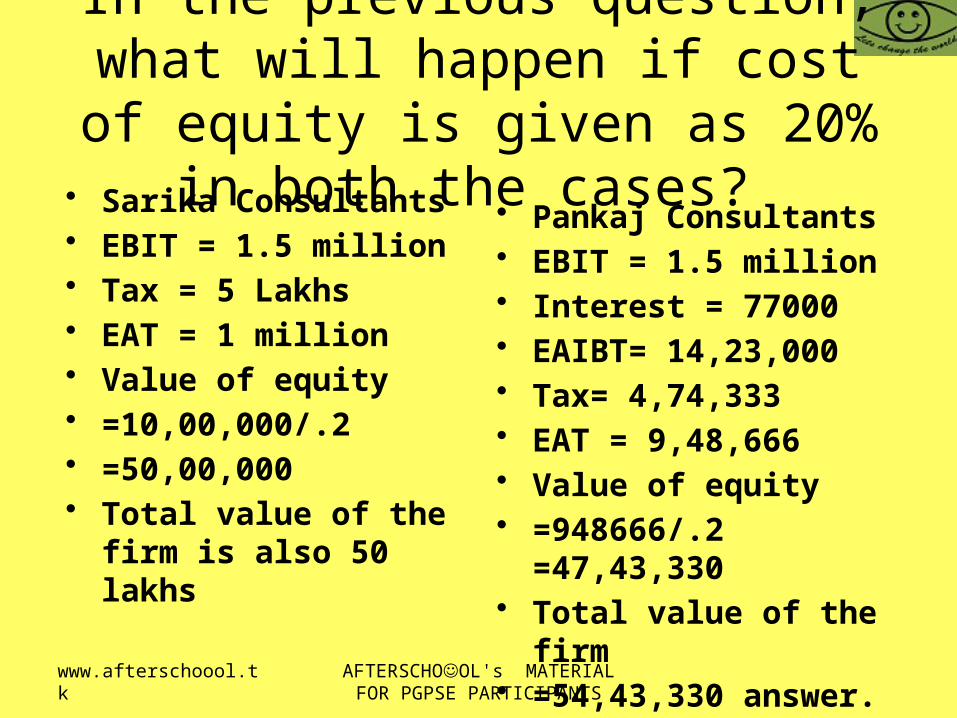

In the previous question, what will happen if cost of equity is given as

20% in both the cases? • Sarika Consultants• EBIT = 1.5 million• Tax = 5 Lakhs• EAT = 1 million• Value of equity• =10,00,000/.2• =50,00,000• Total value of the firm is

also 50 lakhs

• Pankaj Consultants• EBIT = 1.5 million• Interest = 77000• EAIBT= 14,23,000• Tax= 4,74,333• EAT = 9,48,666• Value of equity • =948666/.2 =47,43,330• Total value of the firm • =54,43,330 answer.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

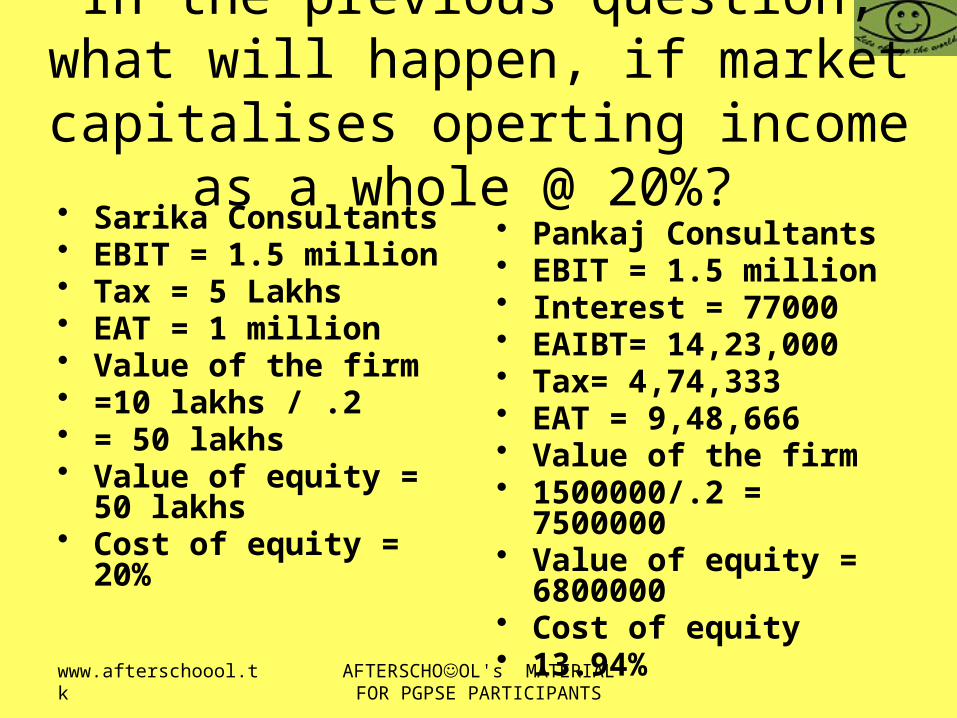

In the previous question, what will happen, if market capitalises operting

income as a whole @ 20%? • Sarika Consultants• EBIT = 1.5 million• Tax = 5 Lakhs• EAT = 1 million• Value of the firm• =10 lakhs / .2• = 50 lakhs • Value of equity = 50

lakhs• Cost of equity = 20%

• Pankaj Consultants• EBIT = 1.5 million• Interest = 77000• EAIBT= 14,23,000• Tax= 4,74,333• EAT = 9,48,666• Value of the firm• 1500000/.2 = 7500000• Value of equity =

6800000• Cost of equity • 13.94%

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Operating leverage…

• = % change in EBIT / % change in sales• Actually it measures the impact of fixed

cost (as aginst variable cost).

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Financial leverage…

• % change in EPS / % change in EBIT• Actually it measures the impact of interest

and other such fixed charge securities on EPS.

• EPS = earning per share.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Alternate formulaes

• Operating leverage • = Contribution / EBIT• Financial leverage • = EBIT / (EBIT – interest)

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

What is capital structure?

• Combination of capital is called capital structure. The firm may use only equity, or only debt, or a combination of equity + debt, or a combination of equity+debt+preference shares or may use other similar combinations.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

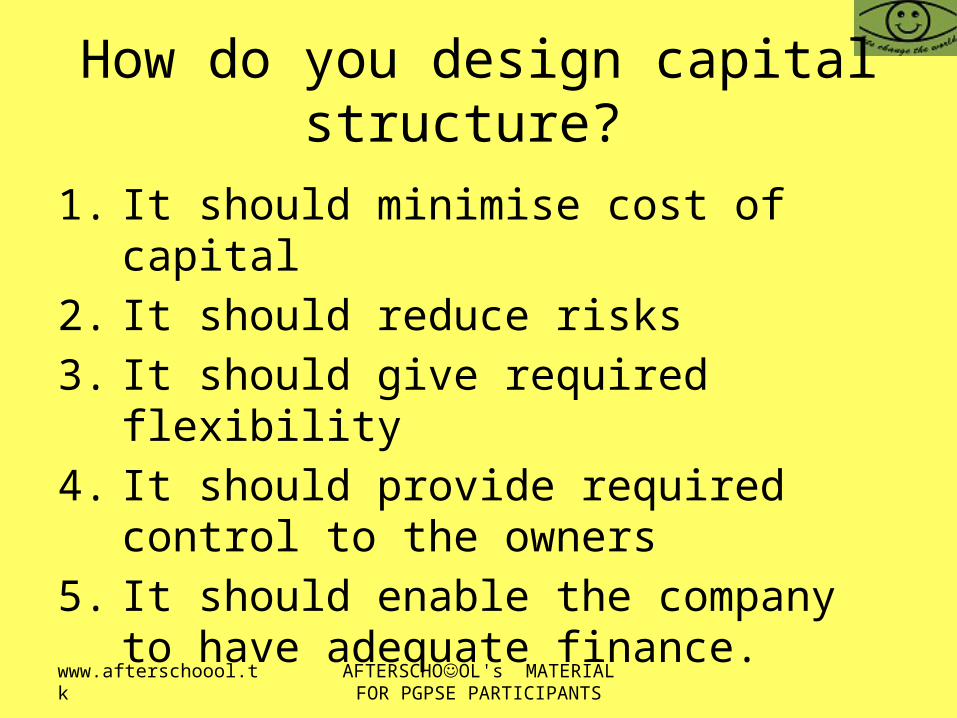

How do you design capital structure?

1. It should minimise cost of capital2. It should reduce risks3. It should give required flexibility4. It should provide required control to the

owners 5. It should enable the company to have

adequate finance.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

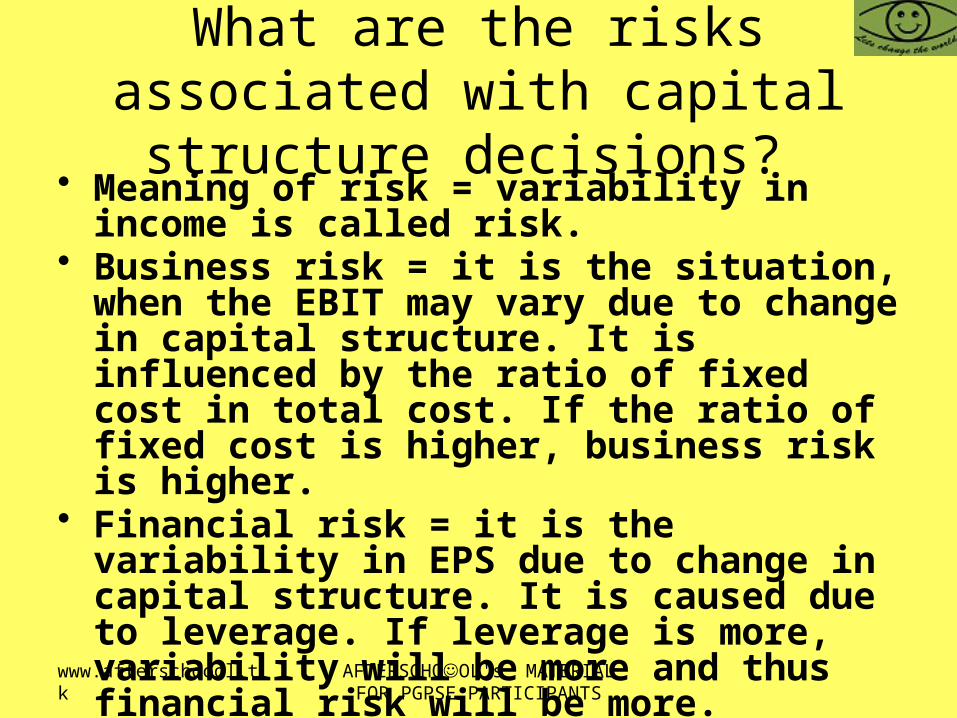

What are the risks associated with capital structure decisions?

• Meaning of risk = variability in income is called risk.

• Business risk = it is the situation, when the EBIT may vary due to change in capital structure. It is influenced by the ratio of fixed cost in total cost. If the ratio of fixed cost is higher, business risk is higher.

• Financial risk = it is the variability in EPS due to change in capital structure. It is caused due to leverage. If leverage is more, variability will be more and thus financial risk will be more.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

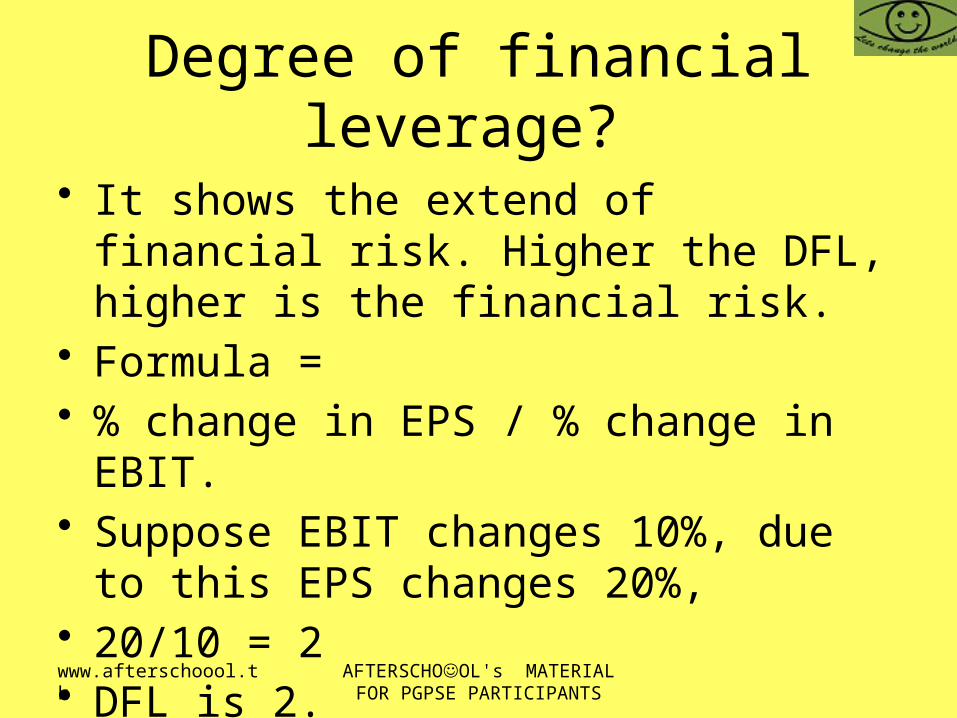

Degree of financial leverage?

• It shows the extend of financial risk. Higher the DFL, higher is the financial risk.

• Formula = • % change in EPS / % change in EBIT. • Suppose EBIT changes 10%, due to this

EPS changes 20%, • 20/10 = 2 • DFL is 2.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

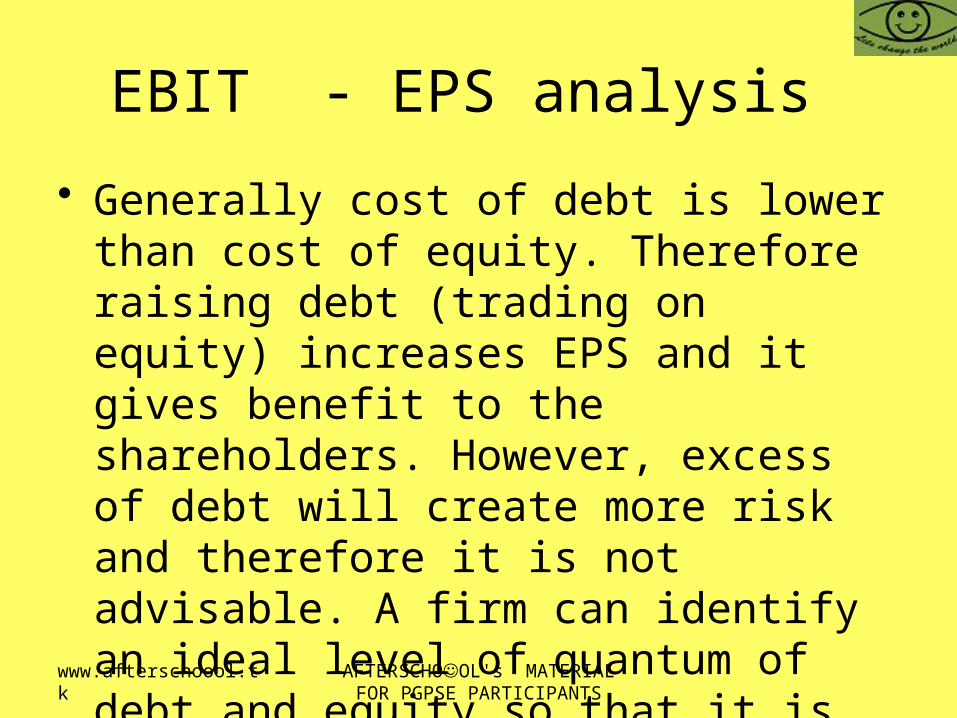

EBIT - EPS analysis

• Generally cost of debt is lower than cost of equity. Therefore raising debt (trading on equity) increases EPS and it gives benefit to the shareholders. However, excess of debt will create more risk and therefore it is not advisable. A firm can identify an ideal level of quantum of debt and equity so that it is within proportion.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

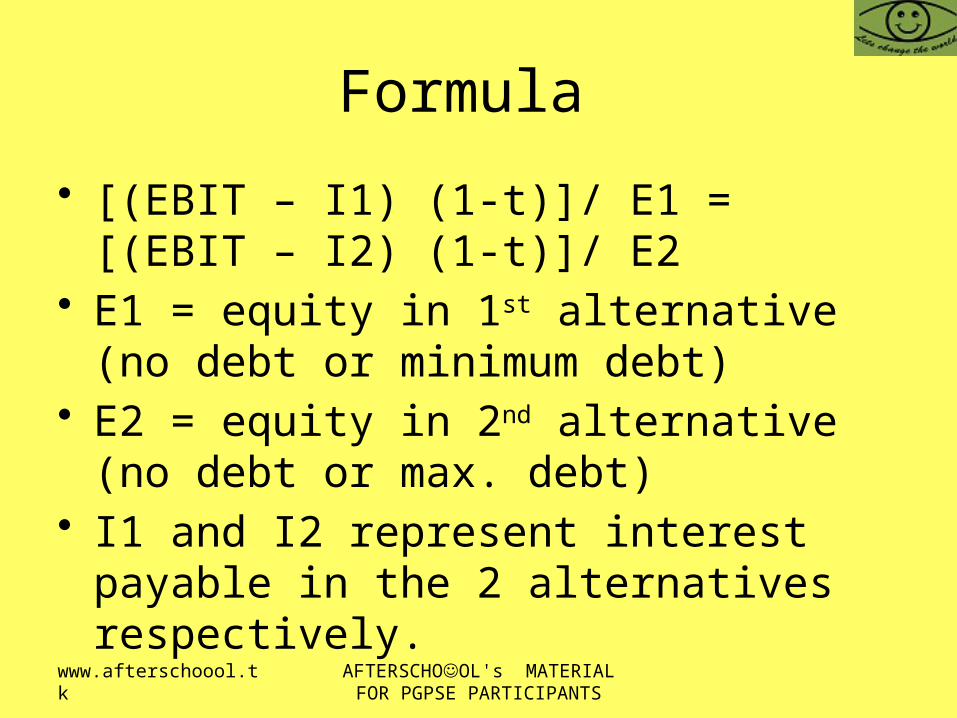

Formula

• [(EBIT – I1) (1-t)]/ E1 = [(EBIT – I2) (1-t)]/ E2

• E1 = equity in 1st alternative (no debt or minimum debt)

• E2 = equity in 2nd alternative (no debt or max. debt)

• I1 and I2 represent interest payable in the 2 alternatives respectively.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

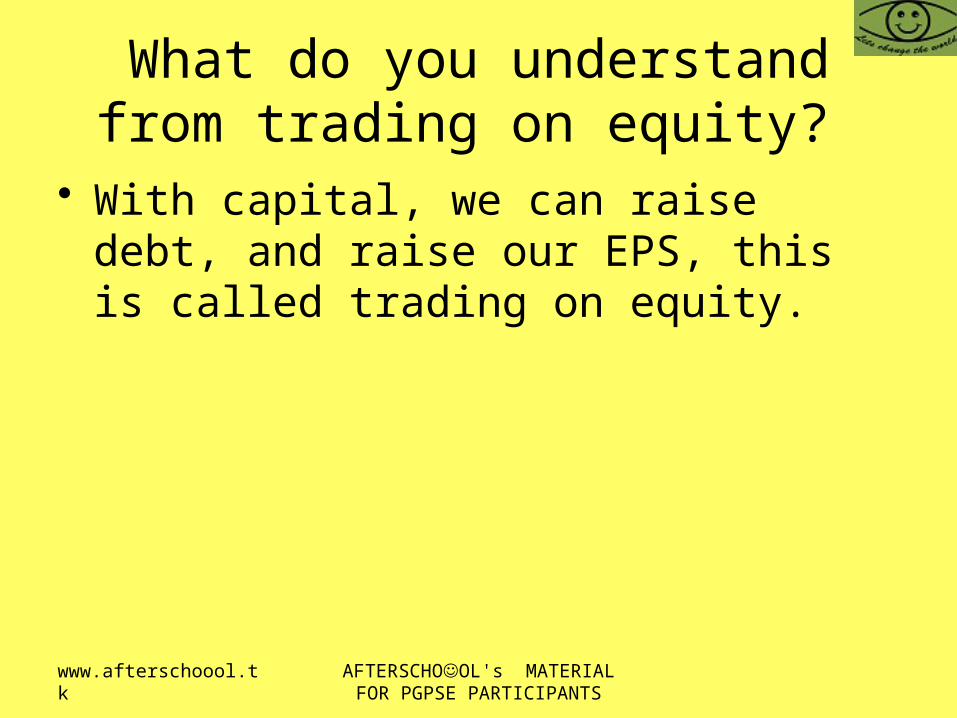

What do you understand from trading on equity?

• With capital, we can raise debt, and raise our EPS, this is called trading on equity.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

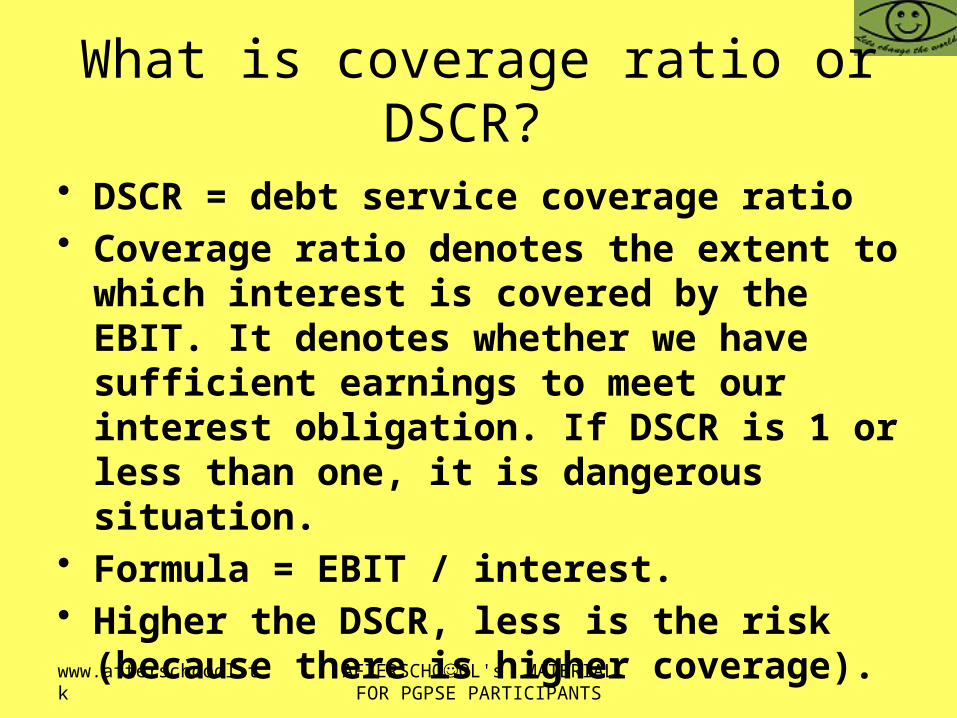

What is coverage ratio or DSCR?

• DSCR = debt service coverage ratio• Coverage ratio denotes the extent to which

interest is covered by the EBIT. It denotes whether we have sufficient earnings to meet our interest obligation. If DSCR is 1 or less than one, it is dangerous situation.

• Formula = EBIT / interest. • Higher the DSCR, less is the risk (because

there is higher coverage).

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

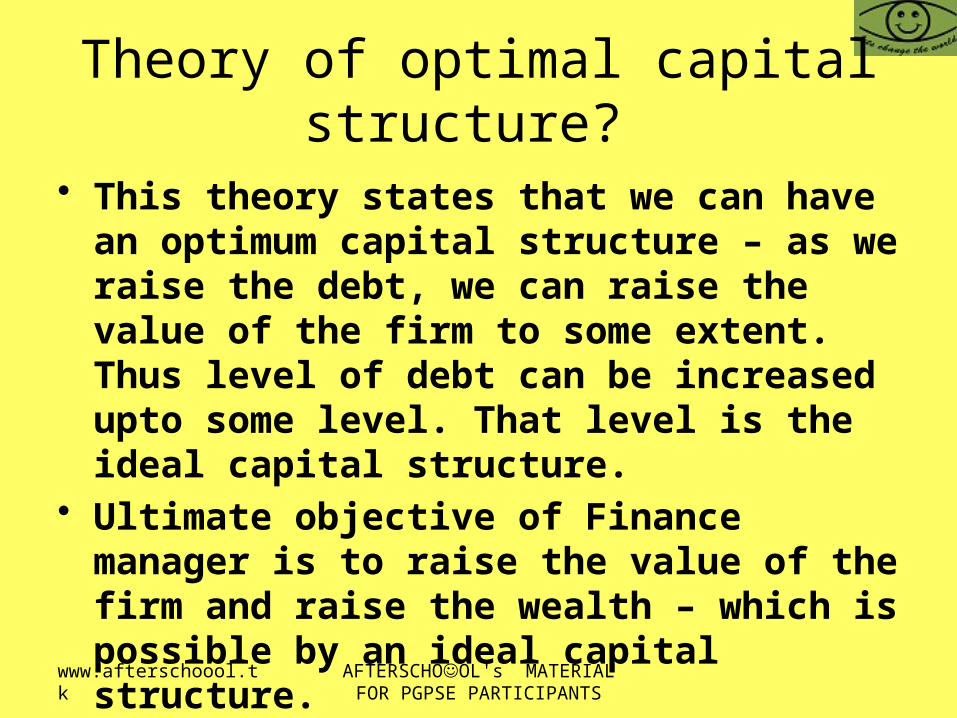

Theory of optimal capital structure?

• This theory states that we can have an optimum capital structure – as we raise the debt, we can raise the value of the firm to some extent. Thus level of debt can be increased upto some level. That level is the ideal capital structure.

• Ultimate objective of Finance manager is to raise the value of the firm and raise the wealth – which is possible by an ideal capital structure.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

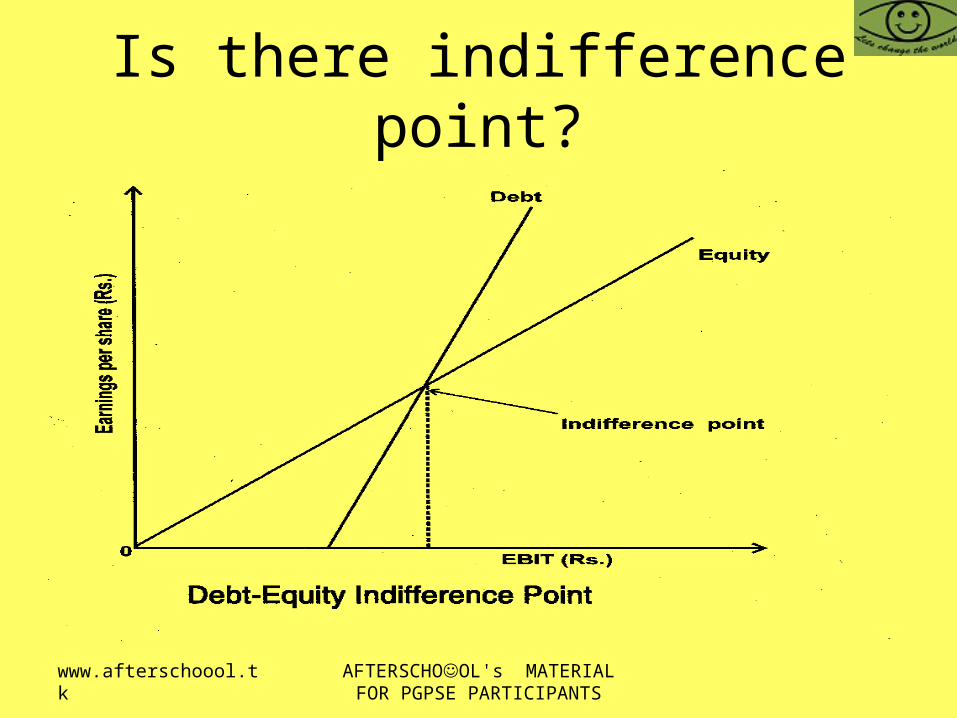

Is there indifference point?

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Solve the following • Goti continental Inc. a profit makipg company, has a paid-

up capital of Rs. 100 lakhs consisting of 10 lakhs ordinary shares of Rs. 10 each. Currently, it is earning an annual pre-tax profit of Rs. 60 lakhs. The company’s shares are listed and are quoted in the range of Rs. 50 to Rs. 80. The management wants to diversify production and has approved a project which will cost Rs. 50 lakhs and which is expected to yield a pre-tax income of Rs. 40 lakhs per annum. To raise this additional capital, the following options are under consideration of the management:

• (a) To issue equity capital for the entire additional amount. It is expected that the new shares (face value of Rs. 10) can be sold at a premium of Rs. 15.

• (b) To issue 16% non-convertible debentures of Rs. 100 each for the entire amount. Tax rate = 30%

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Solution

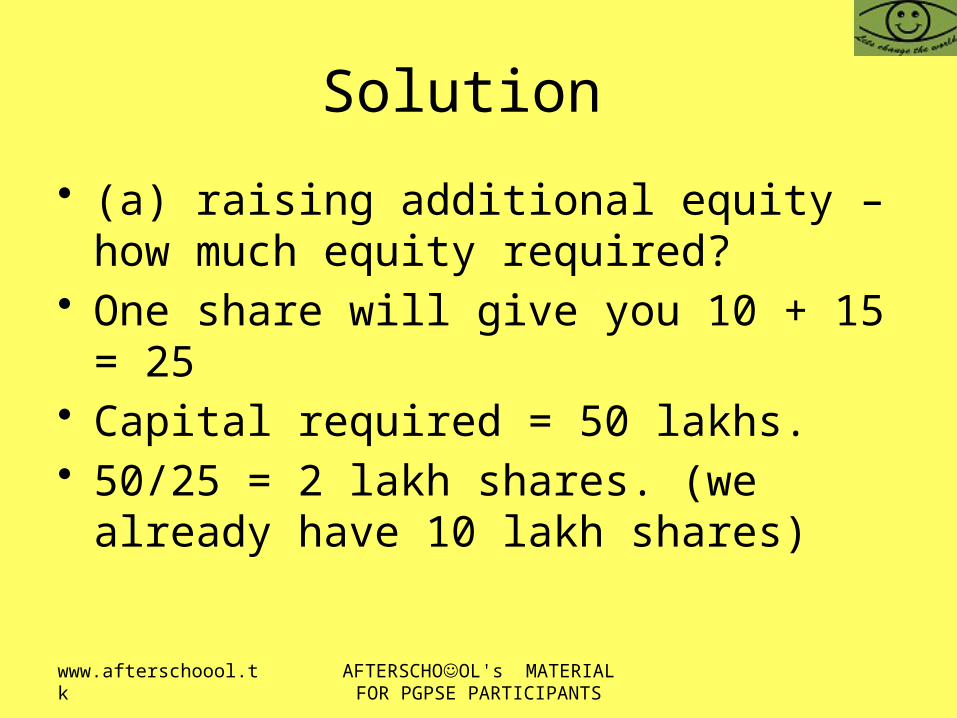

• (a) raising additional equity – how much equity required?

• One share will give you 10 + 15 = 25• Capital required = 50 lakhs.• 50/25 = 2 lakh shares. (we already have

10 lakh shares)

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

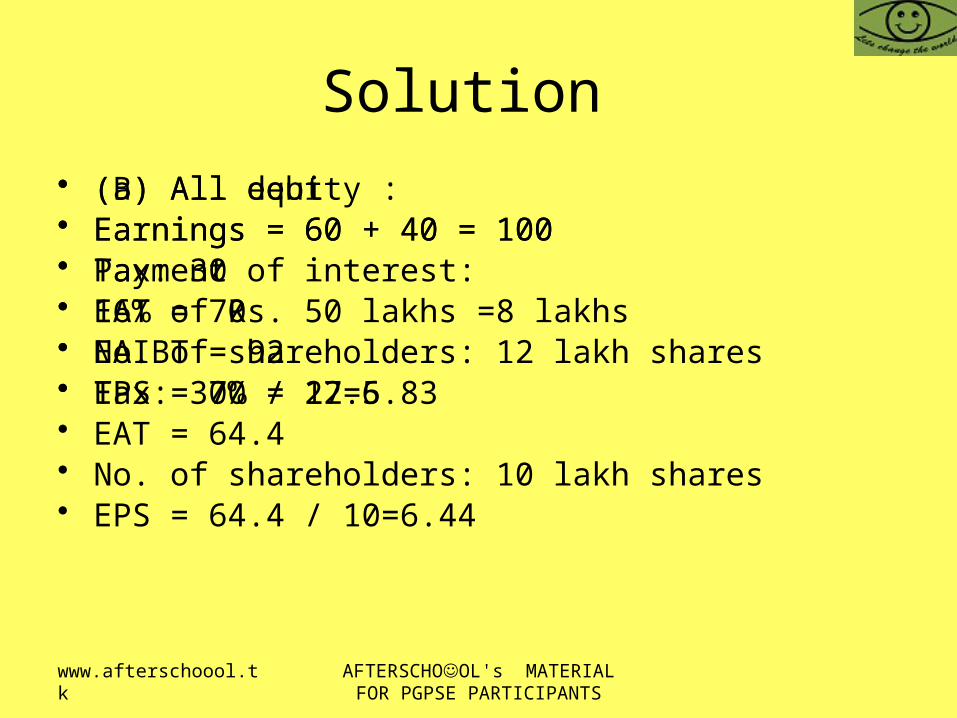

Solution • (a) All equity : • Earnings = 60 + 40 = 100• Tax: 30• EAT = 70• No. of shareholders: 12 lakh shares• EPS = 70 / 12=5.83

• (B) All debt• Earnings = 60 + 40 = 100• Payment of interest: • 16% of Rs. 50 lakhs =8 lakhs• EAIBT = 92• Tax: 30% = 27.6• EAT = 64.4• No. of shareholders: 10 lakh shares• EPS = 64.4 / 10=6.44

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Analysis

• From the above analysis, it is clear that EPS is higher in the case when we are raising debt. (therefore this option is better and the firm should go for raising debt).

• We also have to look at the overall market capitalisation and overall value of the firm.

• Suppose, PE ratio of the industry is 20, the value of the firm is as under:

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Solution • (a) all equity • 5.83 *20 = 116.6• Multiply it with 12 lakhs,• The value of the firm is 1399.2 lakhs. Thus from this

analysis, this option is better.

• Debt • Use of debt will reduce the PE ratio to some extent as

Beta will increase. However, let us calculate using 20 as PE ratio:

• 20*6.44 = 128.8 *10 lakhs + 16 lakhs • =1304 lakhs

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Theories of capital structures . .

• There are 4 theories: 1. NI approach (net income approach)2. NOI approach (net operating income

approach)3. MM approach (Modigliani Millar

Approach)4. Traditional approach

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

Assumptions in capital structure theories …..

1. There are only 2 sources of finance – debt and equity

2. Taxes are ignored3. Dividend payout ratio is 100%4. Business risk is constant5. Firm’s total financing remains constant.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

NI approach (net income approach) • When you raise debt, leverage will increase. The

overall value of the firm will incrase. Debt will have lower cost, so overall cost of capital will reduce (it is better if the cost of capital reduces).

• V = S+ D• V = value of the firm, S = equity, D = debt• An increase in leverage will increase the value

of the firm, it will raise EPS, it will raise the market price of the shares and it will reduce weighted average cost of capital, thus leverage is always beneficial.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

NOI approach (Net operating income approach)

• Capital structure decision is irrelevant. If you raise debt, the cost of equity will increase. The overall cost of capital will remain constant in spite of leverage. Thus there is no advantage of raising debt. As we raise the debt, the cost of equity increases in the same proportion. The market discounts the firm, which is leveraged. Thus capital structure decision has no relevance.

AFTERSCHO☺OL's MATERIAL FOR PGPSE PARTICIPANTS

www.afterschoool.tk

MM approach

• It is similar to NOI approch

Related Documents