Capability Building in Global Markets Barcelona 8 th October 2008

Capability Building in Global Markets Barcelona 8 th October 2008.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Capability Building in Global Markets

Barcelona

8th October 2008

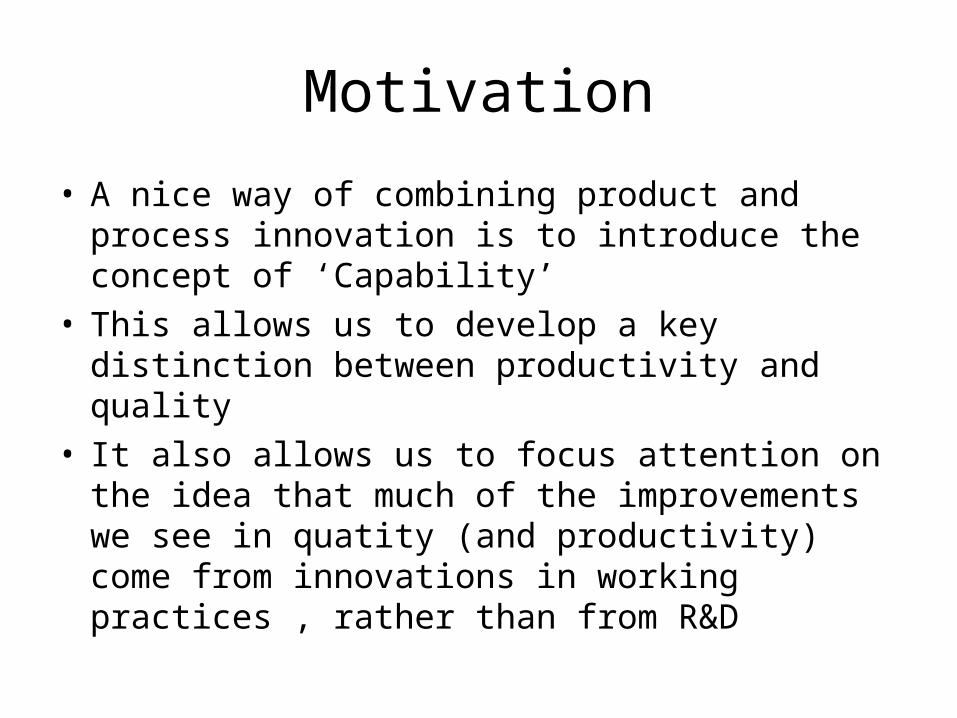

Motivation

• A nice way of combining product and process innovation is to introduce the concept of ‘Capability’

• This allows us to develop a key distinction between productivity and quality

• It also allows us to focus attention on the idea that much of the improvements we see in quatity (and productivity) come from innovations in working practices , rather than from R&D

Sources

• Sutton, Quality,Trade and the ‘Moving Window’, Economic Journal , Nov 2007

• Brandt, Rawski, Sutton, China’s Great Economic Transformation, Cambridge University Press 2008

• Sutton, The auto-component industry in China and India: A Benchmarking Study

Capabilitiesd

dc

u c = ‘productivity’

u = ‘quality’

Capability is a pair (c, u) for each technical trajectory (submarket)

1)( zuxU

Key feature:

The consumers choose products offering the best u/p

Implication: if u>v, the market share of a firm offering u cannot be eroded to zero by any number of firms offering v

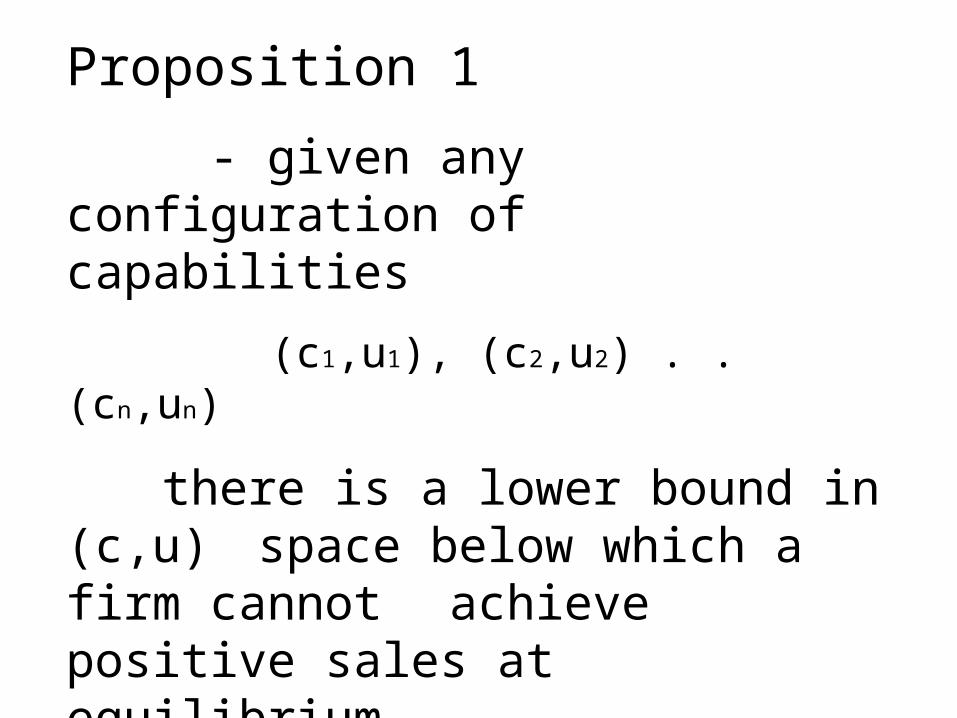

Proposition 1

- given any configuration of capabilities

(c1,u1), (c2,u2) . . (cn,un)

there is a lower bound in (c,u) space below which a firm cannot achieve positive sales at equilibrium

(ex. Cournot equilibrium)

xu

(Quality)

1/c (Productivity)

x

u/c = bu/c = ax

Competing in Capabilities

Fixed /Sunk costs

• Iso-elastic response of quality(beta)

• Isoelastic response of labour productivity (gamma)

• Unit variable cost = labour cost + materials cost

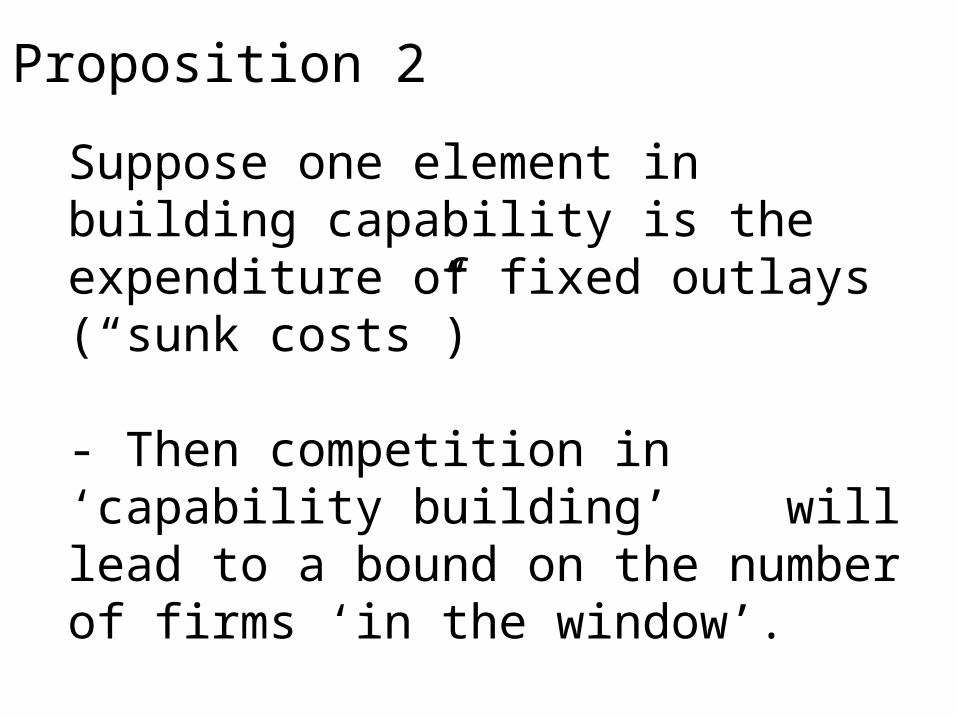

Proposition 2

Suppose one element in building capability is the expenditure of fixed outlays (“sunk costs”)

- Then competition in ‘capability building’ will lead to a bound on the number of firms ‘in the window’.

X

X

X

X

X

X

XX

X

X

XX

X

X

XX

So what’s new?

• The model has been chosen so that prices and qualities, and therefore productivity and quality enter in a completely symmetric fashion

• The key point is that unit materials cost sets a floor to price, thus limiting the degree to which changes in wages and productivity can offset changes in quality

Quality vs. productivity

• Once raw materials at international prices are an input….

• Wage adjustment can rescue poor productivity…

• But not poor quality

Capability Threshold

Quality

uB

1/cBProductivity

uB

WB 0

WB >>0

A Digression ….

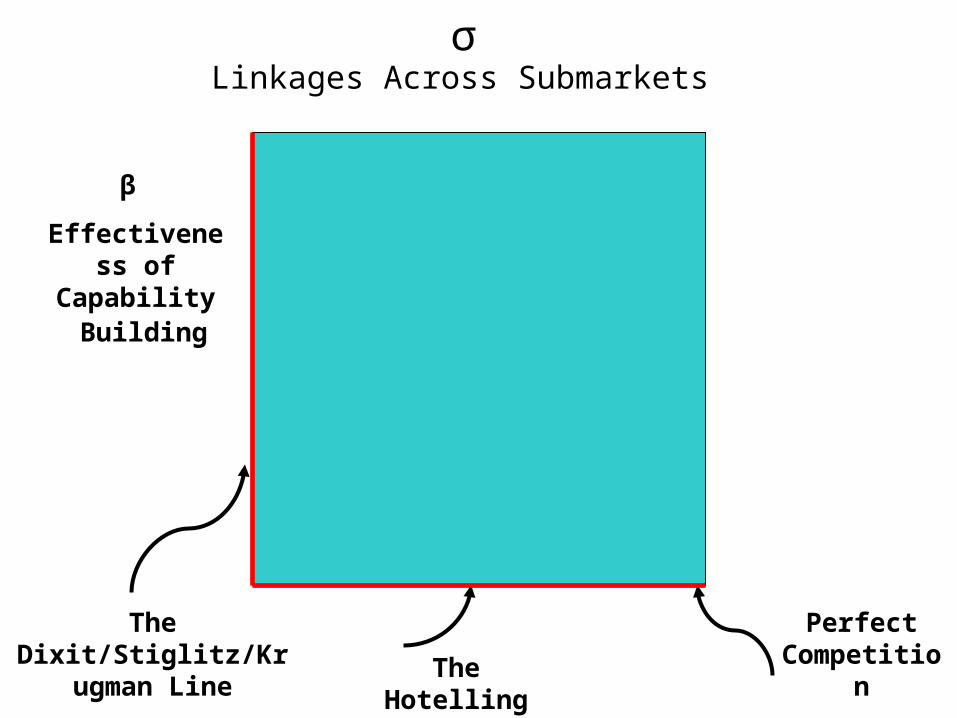

• An extension of the model adds a second parameter (horizontal differentiation)

• This can be further generalized to “linkages between sub-markets”

• This extension is important in providing an explanation for cross-industry differences in market structure

σ Linkages Across Submarkets

The Dixit/Stiglitz/Krugman

LineThe Hotelling

Line

Perfect Competition

β

Effectiveness of Capability

Building

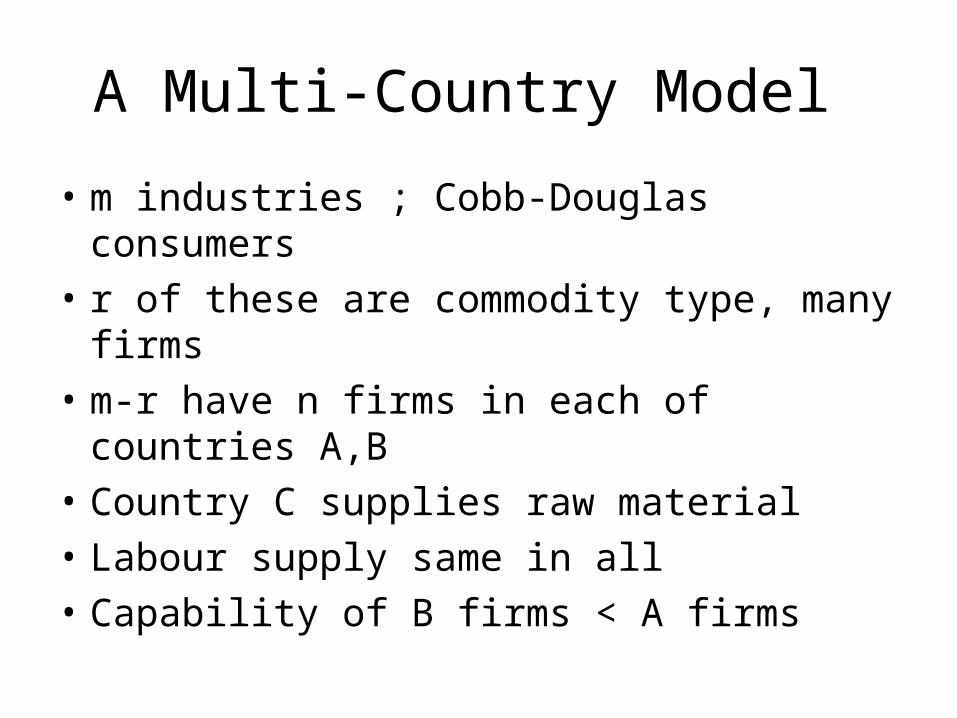

A Multi-Country Model

• m industries ; Cobb-Douglas consumers

• r of these are commodity type, many firms

• m-r have n firms in each of countries A,B

• Country C supplies raw material

• Labour supply same in all

• Capability of B firms < A firms

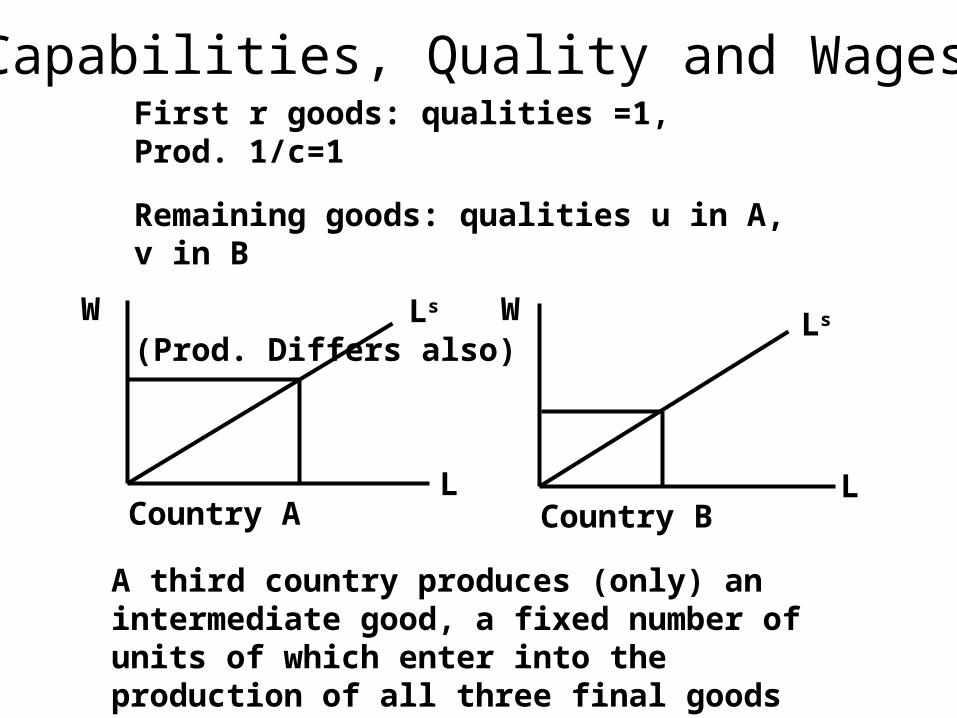

Capabilities, Quality and WagesFirst r goods: qualities =1, Prod. 1/c=1

Remaining goods: qualities u in A, v in B

(Prod. Differs also)

W

L

Ls

Country A

W

L

Ls

Country B

A third country produces (only) an intermediate good, a fixed number of units of which enter into the production of all three final goods

Modelling Pre-Globalisation

• The aim is to exclude competition in “quality” goods, while allowing A and B to source materials from C.

• Two routes:

• (i) Partition country C

• (ii) Unify C but inhabitants are insensitive to quality differences

Three Phases

• Phase I: Impact phase…Capabilities given

• Phase II: Transfer phase

• Phase III: Re-investment (escalation) phase

Phase I : Impact

• There are three regimes, depending on the size of the gap in capability

• Regime I….gap ~ 0

• Regime II…..moderate gap

• Regime III….wide gap

Relative Wages

1Relative Quality

wB

v

u

I

II

III

wA

Main substantive argument

• The case for globalisation should rest primarily on the transfer and growth of capabilities it induces

• A fundamental set of mechanisms are driven by the coexistence of high capabilities and low wages

• These mechanisms include, inter alia, • ---self help driven by new incentives• ---Transfers via FDI/ Supply chains, etc.

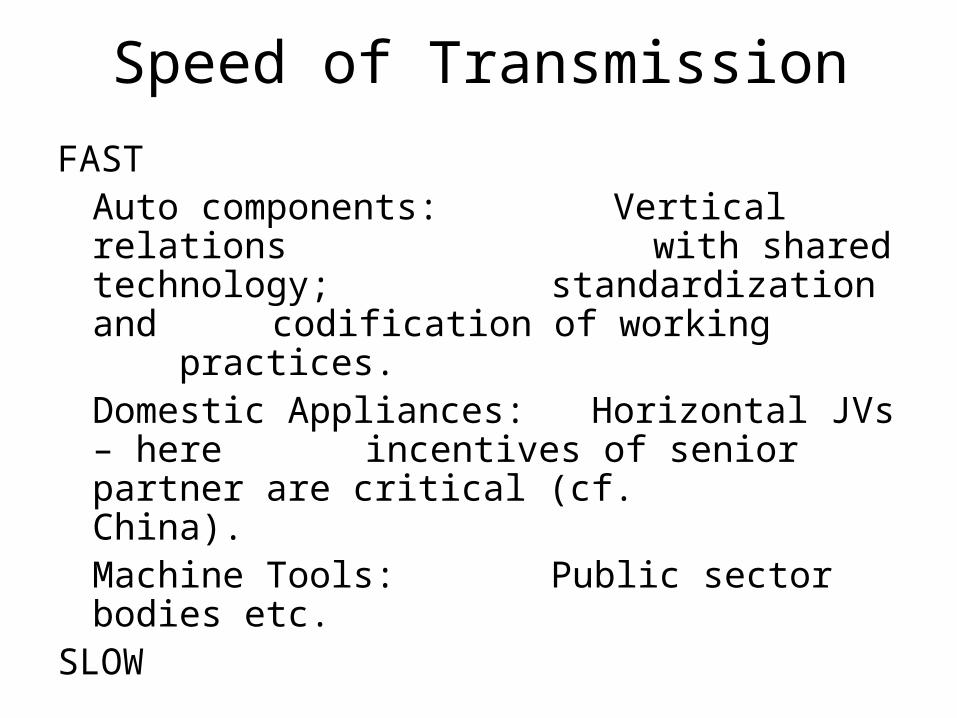

Speed of Transmission

FASTAuto components: Vertical relations

with shared technology; standardization and

codification of working practices.Domestic Appliances: Horizontal JVs – here

incentives of senior partner are critical (cf.

China).Machine Tools: Public sector bodies etc.

SLOW

Component Suppliers to Multi-National Car Makers

0

0.1

0.2

0.3

0.4

0.5

0.6

India

China

The Mahindra Story

CNC Machine Tools

The Machine Tool Industry

How trajectories develop/divide

Conventional Machines CNC Machines

Controls

Ball-screws

The ‘machine’

Pre 1970 Post 1970

The Invidious Trade-Off

controls

ball-screws

15% wages

Bought-in Components

Materials, Energy costs,

etc.

15%

15%

55%

A typical cost breakdown

Gross Labour Productivity

3-axis, 15 kW

7.5 kW,165mm

11 kW,350mm

0.25 1 4

size

& c

om

ple

xity

Japan

India Taiwan

Phase III

• Escalation and shakeout

• Outcome depends on initial post-transfer gap

• Under a full transfer regime, shakeout occurs only for low-beta industries

• But…only a sub-set of firms re-invest

Related Documents