3 Cairn India Ltd - Company Report VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.) COMPANY REPORT Cairn India Ltd. Operation Desert Storm Equity Research l Oil & gas April 5, 2013 We initiate coverage on Cairn India Ltd. (CIL) with a BUY rating. CIL is one of the best stock plays in India to have direct exposure to global crude prices. With its world-class Rajasthan Block already under production, the company has joined the big league of players in India’s E&P space. Rajasthan Block’s Gross Hydrocarbons Initially In Place (GHIIP) is 7.3bnboe, of which estimated recoverable reserves stand at 1.7bnboe. In two years production from Rajasthan Block is expected to reach 210,000bopd from the current 170,000bopd, which will contribute around 30% of India’s domestic crude production. With world-class oil production assets, exciting E&P prospects and highly competent management, coupled with high crude prices, CIL stock is an attractive investment option. Investment Argument Resource-rich Rajasthan fields CIL’s GHIIP in Rajasthan Block stands at 7.3bnboe, with the expected ultimate recovery of about 1.7bnboe. MBA (Mangala, Bhagyam and Aishwarya,) fields in Rajasthan Block have reserves of around 2.1bnboe, of which 2P reserves are estimated at 1.0bnboe, representing a recovery factor of 48%. Additionally, CIL has estimated recoverable resources of around 165mmboe from the Barmer Hill formation and other discoveries and another 530mmboe from the exploration upside. With the approval from government for resume exploration activities in Rajasthan block (after a gap of four years), Cairn has already embarked upon a 3-year exploration programme to drill over 100 exploratory/appraisal wells. Rajasthan Block production to rise by 22% by end of FY15 CIL is poised to achieve production of 210,000bopd from Rajasthan Block from the current 175,000bopd on the back of sustained production of 150,000bopd from Mangala along-with EOR (Enhanced Oil Recovery) implementation, ramp-up of Bhagyam to 40,000bopd and peak output of 20,000bopd from Aishwarya. A strong output ramp-up, along with high crude prices, will ensure healthy growth in cash-flows for the company. Valuation At the CMP of Rs 288, the stock trades at P/E, EV/EBITDA and P/BV of 5.5x, 2.7x and 0.8x, respectively, on FY14E estimates of EPS, EBITDA and BV. Since the production has begun from MBA fields, the stock has averaged at 7.8x one-year forward earnings. We value MBA fields on a NAV basis and other recoverable reserves on an EV/boe basis to arrive at a target price of Rs 374, which reflects an EV/boe of $9.5/bbl. We initiate coverage on Cairn India with a BUY rating. CIL valuation Block Net 2P/ Recoverable Reserves (mmbbl) Rs/share (USD/boe) MBA + EOR 620 206 12.9 Barmer Hill 116 15 5.2 Exploration Upside Potential 371 49 5.2 Ravva 14 3 9.1 Cambay 4 1 9.1 Total 1,125 275 9.5 Net debt - 99 - Cairn India - 374 - Particulars FY12 FY13E FY14E FY15E Revenue (Rs bn) 118.6 176.0 170.4 164.7 Growth (Y-o-Y) 15.4% 48.4% -3.2% -3.4% EBIDTA (Rs bn) 91.5 131.8 122.1 111.3 EBIDTA margins 77.2% 62.5% 58.9% 55.5% PAT (Rs bn) 79.4 115.1 99.4 85.2 PAT margins 66.9% 54.6% 47.9% 42.5% EPS 41.6 60.4 52.1 44.6 P/E (x) 6.7 4.6 5.4 6.3 EV/EBIDTA (x) 5.2 2.8 2.6 2.4 Source: Company, Violet Arch Research Stock data CMP Rs 288 Reuters Code CAIL.BO Bloomberg Code CAIR IN Equity Shares o/s (mn) 1,908 Market Cap (Rs mn) 534,160 Market Cap (USD mn) 9,891 Stock performance (%) 52-week high / low Rs 366/283 1M 3M 12M Absolute (10.6) (13.9) (20.2) Relative (8.1) (11.4) (28.0) Shareholding pattern (%) Relative stock movement Promoter, 59 Public & others, 16 FII, 15 DII, 10 80 85 90 95 100 105 110 115 120 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Cairn India Ltd Sensex Absolute Rating BUY Target Price Rs 374 Upside 30%

Cairn India 01Apr13 New

Feb 08, 2016

Cairn India IC

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

3

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

COMPANY REPORT

Cairn India Ltd. Operation Desert Storm

Equity Research l Oil & gas

April 5, 2013

We initiate coverage on Cairn India Ltd. (CIL) with a BUY rating. CIL is one of the best stock plays in India to have direct exposure to global crude prices. With its world-class Rajasthan Block already under production, the company has joined the big league of players in India’s E&P space. Rajasthan Block’s Gross Hydrocarbons Initially In Place (GHIIP) is 7.3bnboe, of which estimated recoverable reserves stand at 1.7bnboe. In two years production from Rajasthan Block is expected to reach 210,000bopd from the current 170,000bopd, which will contribute around 30% of India’s domestic crude production. With world-class oil production assets, exciting E&P prospects and highly competent management, coupled with high crude prices, CIL stock is an attractive investment option.

Investment Argument Resource-rich Rajasthan fields CIL’s GHIIP in Rajasthan Block stands at 7.3bnboe, with the expected ultimate recovery of about 1.7bnboe. MBA (Mangala, Bhagyam and Aishwarya,) fields in Rajasthan Block have reserves of around 2.1bnboe, of which 2P reserves are estimated at 1.0bnboe, representing a recovery factor of 48%. Additionally, CIL has estimated recoverable resources of around 165mmboe from the Barmer Hill formation and other discoveries and another 530mmboe from the exploration upside. With the approval from government for resume exploration activities in Rajasthan block (after a gap of four years), Cairn has already embarked upon a 3-year exploration programme to drill over 100 exploratory/appraisal wells.

Rajasthan Block production to rise by 22% by end of FY15 CIL is poised to achieve production of 210,000bopd from Rajasthan Block from the current 175,000bopd on the back of sustained production of 150,000bopd from Mangala along-with EOR (Enhanced Oil Recovery) implementation, ramp-up of Bhagyam to 40,000bopd and peak output of 20,000bopd from Aishwarya. A strong output ramp-up, along with high crude prices, will ensure healthy growth in cash-flows for the company.

Valuation At the CMP of Rs 288, the stock trades at P/E, EV/EBITDA and P/BV of 5.5x, 2.7x and 0.8x, respectively, on FY14E estimates of EPS, EBITDA and BV. Since the production has begun from MBA fields, the stock has averaged at 7.8x one-year forward earnings. We value MBA fields on a NAV basis and other recoverable reserves on an EV/boe basis to arrive at a target price of Rs 374, which reflects an EV/boe of $9.5/bbl. We initiate coverage on Cairn India with a BUY rating.

CIL valuation

Block Net 2P/ Recoverable

Reserves (mmbbl) Rs/share (USD/boe)

MBA + EOR 620 206 12.9

Barmer Hill 116 15 5.2 Exploration Upside Potential 371 49 5.2

Ravva 14 3 9.1 Cambay 4 1 9.1

Total 1,125 275 9.5 Net debt - 99 -

Cairn India - 374 -

Particulars FY12 FY13E FY14E FY15E

Revenue (Rs bn) 118.6 176.0 170.4 164.7

Growth (Y-o-Y) 15.4% 48.4% -3.2% -3.4%

EBIDTA (Rs bn) 91.5 131.8 122.1 111.3

EBIDTA margins 77.2% 62.5% 58.9% 55.5%

PAT (Rs bn) 79.4 115.1 99.4 85.2

PAT margins 66.9% 54.6% 47.9% 42.5%

EPS 41.6 60.4 52.1 44.6

P/E (x) 6.7 4.6 5.4 6.3

EV/EBIDTA (x) 5.2 2.8 2.6 2.4 Source: Company, Violet Arch Research

Stock data

CMP Rs 288

Reuters Code CAIL.BO

Bloomberg Code CAIR IN

Equity Shares o/s (mn) 1,908

Market Cap (Rs mn) 534,160

Market Cap (USD mn) 9,891

Stock performance (%)

52-week high / low Rs 366/283

1M 3M 12M

Absolute (10.6) (13.9) (20.2)

Relative (8.1) (11.4) (28.0)

Shareholding pattern (%)

Relative stock movement

Promoter, 59Public &

others, 16

FII, 15

DII, 10

80

85

90

95

100

105

110

115

120

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Feb

-13

Mar

-13

Cairn India Ltd Sensex

Absolute Rating BUY

Target Price Rs 374

Upside 30%

4

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Scenario Analysis Particulars Bear Case Base Case Bull Case

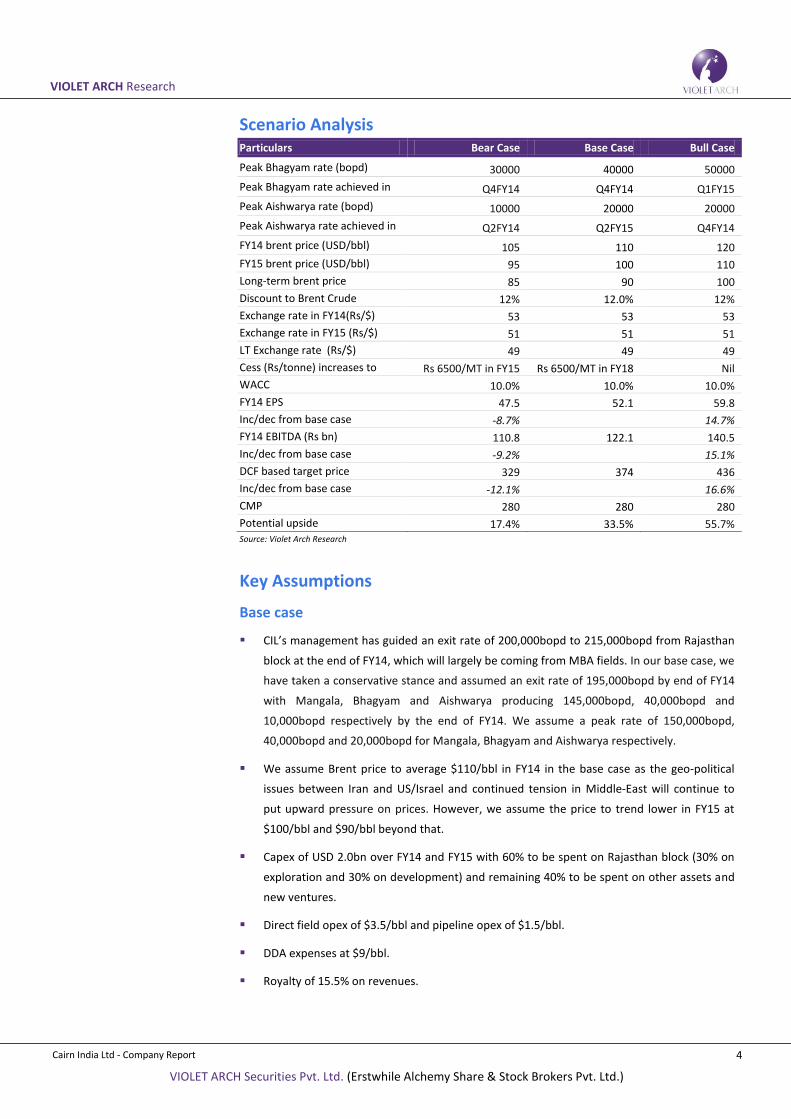

Peak Bhagyam rate (bopd) 30000 40000 50000

Peak Bhagyam rate achieved in Q4FY14 Q4FY14 Q1FY15

Peak Aishwarya rate (bopd) 10000 20000 20000

Peak Aishwarya rate achieved in Q2FY14 Q2FY15 Q4FY14

FY14 brent price (USD/bbl) 105 110 120

FY15 brent price (USD/bbl) 95 100 110

Long-term brent price 85 90 100

Discount to Brent Crude 12% 12.0% 12%

Exchange rate in FY14(Rs/$) 53 53 53

Exchange rate in FY15 (Rs/$) 51 51 51

LT Exchange rate (Rs/$) 49 49 49

Cess (Rs/tonne) increases to Rs 6500/MT in FY15 Rs 6500/MT in FY18 Nil

WACC 10.0% 10.0% 10.0%

FY14 EPS 47.5 52.1 59.8

Inc/dec from base case -8.7% 14.7%

FY14 EBITDA (Rs bn) 110.8 122.1 140.5

Inc/dec from base case -9.2% 15.1%

DCF based target price 329 374 436

Inc/dec from base case -12.1% 16.6%

CMP 280 280 280

Potential upside 17.4% 33.5% 55.7% Source: Violet Arch Research

Key Assumptions

Base case

CIL’s management has guided an exit rate of 200,000bopd to 215,000bopd from Rajasthan

block at the end of FY14, which will largely be coming from MBA fields. In our base case, we

have taken a conservative stance and assumed an exit rate of 195,000bopd by end of FY14

with Mangala, Bhagyam and Aishwarya producing 145,000bopd, 40,000bopd and

10,000bopd respectively by the end of FY14. We assume a peak rate of 150,000bopd,

40,000bopd and 20,000bopd for Mangala, Bhagyam and Aishwarya respectively.

We assume Brent price to average $110/bbl in FY14 in the base case as the geo-political

issues between Iran and US/Israel and continued tension in Middle-East will continue to

put upward pressure on prices. However, we assume the price to trend lower in FY15 at

$100/bbl and $90/bbl beyond that.

Capex of USD 2.0bn over FY14 and FY15 with 60% to be spent on Rajasthan block (30% on

exploration and 30% on development) and remaining 40% to be spent on other assets and

new ventures.

Direct field opex of $3.5/bbl and pipeline opex of $1.5/bbl.

DDA expenses at $9/bbl.

Royalty of 15.5% on revenues.

5

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Cess is assumed at Rs 4500/tonne in the base case for five years through FY13-17 and then

hiked by Rs 2000/tonne every five years.

EOR in Mangala to be implemented in FY15.

Field-life of MBA fields till FY41.

Bear case

In our bear case, we assume an exit rate of 185,000bopd by the end of FY14 with Mangala,

Bhagyam and Aishwarya producing 145,000bopd, 30,000bopd and 10,000bopd respectively

by end of FY14. However, we assume the peak rate of 30,000bopd for Bhagyam and

10,000bopd for Aishwarya.

We assume brent crude to be $105/bbl and $95/bbl in FY14 and FY15 respectively, while

for long-term we assume price to be $85/bbl.

Cess is assumed to increase to Rs 6500/tonne in FY15 and then increase by Rs 2000/MT

every three years.

Bull case

In our bull case, we assume an exit rate of 215,000bopd by end of FY14 with Mangala,

Bhagyam and Aishwarya producing 145,000bopd, 50,000bopd and 20,000bopd respectively

by end of FY14. We assume peak rate of 50,000bopd and 20,000bopd for Bhagyam and

Aishwarya respectively.

We assume brent crude to be $120/bbl and $110/bbl in FY14 and FY15 respectively, while

for long-term we assume price to be $100/bbl.

Cess is assumed to remain constant at Rs 4500/tonne throughout the life of the field.

6

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

CIL’s production from various blocks

Cairn has three producing assets namely, Rajasthan block, Ravva and Cambay. While Rajasthan

block is on a ramp-up phase Ravva and Cambay being mature fields are on decline. Currently

Rajasthan block is producing at the rate of 175,000 bopd and Ravva and Cambay at ~28,000

boepd and ~6,000 boepd.

Crude production (mmboe)* FY10 FY11 FY12 FY13E FY14E FY15E

Rajasthan Block 3.80 25.80 32.82 43.25 47.78 52.93

Growth Y-o-Y

580% 27% 32% 10% 11%

Ravva 3.34 3.03 2.99 2.68 2.41 2.17

Growth Y-o-Y -38% -9% -2% -10% -10% -10%

Cambay 1.97 1.63 1.20 0.96 0.77 0.61

Growth Y-o-Y -21% -17% -26% -20% -20% -20%

Total 9.11 30.47 37.02 46.89 50.96 55.72

Growth Y-o-Y 16% 234% 21% 27% 9% 9% Source: Violet Arch Research;*Cairn’s stake in production

Rajasthan Block

Cairn began production from Mangala block in August 2009 and is currently producing at

150,000 bopd. Bhagyam has started production in Jan 2012 and is currently producing at 20,000

bopd while Aishwarya has commenced production recently.

Production (mnbbls) FY10 FY11 FY12A FY13E FY14E FY15E

Mangala 5.4 36.9 45.6 54.3 53.8 52.0

Growth Y-o-Y

580% 24% 19% -1% -3%

Bhagyam 0.0 0.0 1.2 7.3 11.0 14.6

Growth Y-o-Y

512% 50% 33%

Aishwarya 0.0 0.0 0.0 0.0 3.2 6.8

Growth Y-o-Y - - - - - 114%

Rageshwari and Saraswati 0.0 0.0 0.1 0.2 0.3 0.4

Growth Y-o-Y

143% 50% 33%

Total 5.4 36.9 46.9 61.8 68.3 73.8

Growth Y-o-Y - 580% 27% 32% 10% 8%

Source: Violet Arch Research; Doesn’t include EOR production from MBA

Cairn’s discount to brent moves in tandem with crude heavy-light differential

Source: Violet Arch Research

The crude produced from Rajasthan block is priced according to a certain formula and is linked

to Nigerian bonny Light. However, since the crude produced is heavy in nature it trades at a

discount. The management has given a guidance of 10% to 15% discount to brent. Also

depending on heavy-light differential, the discount varies. If the heavy-light differential widens

the discount to brent may increase resulting in lower realization and if it narrows the discount

may decrease resulting in higher realization.

0%

2%

4%

6%

8%

10%

12%

14%

0

1

2

3

4

5

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Heavy Light differential ($/bbl) Cairns discount to brent (RHS)

7

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Per boe analysis of Rajasthan Block

USD per bbl FY10 FY11 FY12A FY13E FY14E FY15E

Brent Assumption 74.5 86.7 115.0 111.5 110.0 100.0

Gross Realisation 65.6 76.3 103.5 98.1 96.8 88.0

Royalty 0.0 0.0 24.4 14.7 14.5 13.2

Govt share of profit petroleum 0.0 0.0 5.4 12.3 17.7 15.8

Net Realisation 71.0 80.0 73.3 71.1 64.5 59.0

Cess 7.6 7.9 7.5 11.6 11.9 12.4

Direct field opex + Pipeline opex 13.6 3.4 5.0 5.0 5.0 5.1

EBITDA 49.8 68.8 60.8 54.5 47.6 41.5

DDA expense 9.0 9.0 8.0 8.0 9.0 9.0

PBT 40.8 59.8 52.8 46.5 38.6 32.5

Tax expense 8.4 12.2 10.8 9.5 7.9 6.7

PAT 32.5 47.5 42.0 37.0 30.7 25.8

Source: Violet Arch Research

Cairn gross realization for crude produced from Rajasthan block is arrived at a specific

formula approved by the government in the PSC. The crude produced from Rajasthan being

heavy in nature is priced at a discount to brent crude. Depending on the heavy light

differential discount ranges between 10% to 15% to brent crude.

Cairn pays royalty at 20% of well-head value, which works out to 15%-16% of realized

value. Till Q1FY12, ONGC was paying the entire royalty burden on its behalf and on behalf

of Cairn as well. However, Government imposed the condition to make royalty cost

recoverable to approve the Cairn – Vedanta deal, which Cairn had to accept and also make

provisions for royalty paid by ONGC till Q1FY12.

PSC allows 100% cost recovery for Cairn before arriving at profit petroleum. Cairn is

allowed to recover entire exploration and development capex, royalty cess & operating

expenditure incurred before any profit petroleum is shared with the government.

Government’s share of profit petroleum is calculated based on investment multiple (IM =

(Net Cumulative Income)/( Net Cumulative Investment)). The IM in a particular year

determines government’s share of profit petroleum in subsequent year.

IM (applied on fiscal year basis) Govt share JV share

<1.5 20% 80% 1.5-2 30% 70% 2-2.5 40% 60% >2.5 50% 50%

Cairn pays cess at the rate of Rs 4500/MT which was increased from Rs 2500/MT in Budget

FY13. Earlier Cairn had contested that ONGC has to bear the burden of cess for both of

them. However, to approve the Cairn-Vedanta deal, government imposed the condition to

make cess cost recoverable.

Cairn has given a guidance of $3.5/bbl for direct field opex of and $1.5/bbl for pipeline opex

which makes it one of the low cost operators in the E&P sector.

Cairn’s DDA (Depreciation, depletion and amortization) expense has moved in the range of

$8-$10/bbl and Cairn has given a long-term guidance of $9.0/bbl for the same.

Cairn enjoys a seven year tax holiday from the day of start of production from Rajasthan

Block. However, it has to pay a MAT at approximately 20.5% which will be eligible for set

off against the applicable tax liability beyond the tax holiday period. However, for next two

years it will continue to pay tax at effective tax rate of 5% to 9% as it avails the MAT credit

entitlements.

8

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Sensitivity Analysis

Impact of 5% change in various parameters on EPS and EBITDA in FY14

Particulars EBITDA impact EPS impact

Crude price 6.2% 6.3%

Exchange rate 6.0% 5.2%

Production volume 5.0% 4.3%

Source: Company, Violet Arch Research

Cairn is a pure play on crude and as such it has a very high co-relation with how the crude prices

move. The correction in crude prices during June’12 from $125/bbl to $100/bbl also saw 15-20%

correction in Cairn. We expect crude prices to remain stable at $110/bbl for next one year and

$90/bbl in the long-term and USD-INR to average Rs 53/$ in FY14 and Rs 49/$ in long-term.

Valuation

Long-term crude price assumption (USD/bbl)

80 90 100 110 120

Long-term USD-INR rate assumption

45 320 348 380 412 444

47 328 357 391 424 457

49 337 367 401 435 470

51 340 376 411 447 482

53 349 385 422 458 495

EPS FY14

FY14 crude price assumption (USD/bbl)

100 105 110 115 120

FY14 USD-INR rate assumption

49 42.5 45.3 48.0 50.8 53.5

51 44.3 47.2 50.1 52.9 55.8

53 46.1 49.1 52.1 55.1 58.1

55 47.9 51.0 54.1 57.2 60.3

57 49.7 52.9 56.2 59.4 62.6

EBITDA FY14

FY14 crude price assumption (USD/bbl)

1 100 105 110 115 120

FY14 USD-INR rate assumption

49 98.2 104.6 111.0 117.4 123.7

51 103.2 109.9 116.5 123.2 129.8

53 108.2 115.1 122.1 129.0 135.9

55 113.3 120.4 127.6 134.8 141.9

57 118.3 125.7 133.1 140.6 148.0

Source: Violet Arch Research

9

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

SWOT Analysis

Source: Violet Arch Research

SWOT Analysis

Strengths

1) World class asset 'Rajasthan Block' with GHIIP at around 7.3bnboe and recoverable reserves at about 1.7bnboe.

2) Low cost of production with direct field opex and pipeline opex at $3.5/bbl and $1.5/bbl.

3) Strong balance sheet with cash in hand at Rs 140bn as of 31st Dec'12.

4) Superior execution capabilities as seen in the case of Rajasthan block, Ravva and Cambay.

Weaknesses

1) As of now, Cairn is considered a single asset player, as majority of its production is expected from Rajasthan Block in the near term.

2) Being mature fileds, Cambay and Ravva production on decline.

Opportunities

1)The Barmer Hill formation reserves recovery factor at around 8%. Reserves of similar nature has had recovery factors of up to 20%.

2) Further exploratory efforts could lead to upgradation of 2P reserves in Rajasthan Block.

3) 10 exploratory assets in three strategically focused areas: one in Rajasthan; three on the west coast of India; six on the east coast of India, including one in Sri Lanka.

Threats

1) Delay in approvals from the government could lead to delays in achieveing the production guidance in Rajasthan Block.

2) The government raising statutory levies impacting profitability of Cairn.

3) Falling crude prices leading to a fall in profits.

10

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Geo-politics and crude Country Its role in geo-politics

US

US has recently established powerful sanctions that prevent Iran from receiving earnings to which it is entitled from its shrinking oil export trade. Under the new set of sanctions the Islamic regime has no choice but to continue with barter trades and local currencies, with limited access to the foreign exchange it desperately needs to continue its nuclear program and its customary support of international terrorism in the four corners of the world. Has been consistently mounting pressure on Iran and garnering support from EU for the same so that Iran comes to negotiation table. Though the shale oil production in US is increasing rapidly, it may not become completely import independent in the near future, which will mandate it to keep its influence over middle-east oil politics.

Israel Israel is strongly opposed to Iran going ahead with its nuclear ambitions. It has not ruled out military strike to bring Iran’s nuclear program to halt. Israel has full support of US when it comes to any conflict in Iran or Middle-East as well.

Iran

Declining oil exports has caused the Iranian rial to shed more than 60 percent of its value against the U.S. dollar, leading to spiraling inflation and mounting unemployment. Uncontrolled inflation has raised food and commodity prices to such a degree that the majority of Iranian citizens presently cannot afford even basic necessities. Super inflation and unemployment in Iran are now presenting a serious danger to the regime. the opportunity costs of the nuclear program has been at well over $100bn in terms of lost foreign investment and oil revenues. However, Iran is still not ready to give up on its nuclear ambitions.

Saudi Arabia

Saudi has a majority Sunni population while Iran has majority Shi’a population. Theocracy in Iran has openly challenged the legitimacy of the Royal House of Saud. Both harbor ambitions to become economic and political power in Middle-East. Saudi has made up for production losses due to sanctions on Iran. Saudi Arabia is the largest member of the OPEC and the only one with significant unused capacity to produce more. It reduced output in Dec’12 by 4.9 percent to 9.025mbpd, the lowest level in 19 months primarily to stabilize oil prices.

China

When it comes down to its foreign policies China follows its own interests without buckling down to any international pressure. Latest examples were the conflict between China and Japan for islands in South China sea. It has not also opposed North Korea’s war rhetoric. And with the change in leadership it is claiming Taiwan as part of China. Even in the case of Iran it has not opposed any sanctions on it and will not support any military actions against Iran. It has been getting oil from Iran at discount to international rates. However it is reducing its oil imports from Iran just to comply with international sanctions.

Russia

Russia wants to curtail western powers especially US hegemony in Middle-East. It never supported any sanctions or any military actions against Iran. Russia had also helped Iran in building a nuclear reactor. However, business interests are not the main drivers of its relationship with Iran. Russia is extremely dependent on energy exports, particularly on the export of crude oil. Russia robust state finances (Russia has by far the lowest debt/GDP ratio of any major country) are almost entirely due to its sizable exports of oil and natural gas. Thus any conflict in Middle-East which supports elevated crude prices will be beneficial to Russia.

Venezuela

Venezuela has the largest known oil reserves in the world, but oil output has slumped by almost a third because of Mr Chavez’s nationalization of the industry. The country holds 17.9% of the world’s known oil reserves, compared with 16.1% in Saudi Arabia and 10.6% in Canada. However, it only represented 3.5% of global production compared with 13.2% in Saudi Arabia. It is likely that oil output could rise, should there be an easing of the country’s antagonism to foreign investors. Some believe this could lead to a fall in the oil price and a consequent boost to the global economy. However, the state oil company PDVSA has increasingly been handing over its income to fund various government programmes, leaving it with negative cash flows for the past five years. The result of this has been a lack of investments as old fields matured and new ones were not explored, hence the drop in output. Consequently, for the output to rise from Venezuela will take much more time.

Sudan-South Sudan

South Sudan seceded from Sudan in July 2011. Along with this South Sudanese independence came 75% of Sudan’s oil resources—minus the infrastructure (pipelines and ports) which remains in Sudan. So South Sudan became now rich in oil which is land-locked. However recently, Sudan and South Sudan reached an agreement for the resumption of South Sudanese oil exports through Sudanese infrastructure. The deal calls for a withdrawal of troops from both Sudan and South Sudan and the creation of a demilitarized zone to facilitate the flow of oil. Oil hasn’t flowed for about a year after South Sudan blocked exports via Sudan over a tariff dispute.

Nigeria Oil production in Nigeria, Africa’s biggest producer, is down by about 1.0mbpd because of violence and theft in the Niger River delta. Currently, producing at 2.5mbpd, well below it’s capacity of 3.7mbpd.

North Korea - South Korea – US

North Korea has said that it had entered "a state of war" with South Korea in its latest threat aimed at the United States and its ally after two American B-2 bombers flew a training mission in the region. The situation on the peninsula is now more volatile, with the North controlled by a relatively new leader, Kim Jong Un, and the South Korea promising an immediate military counterstrike if provoked. North Korea’s army has said it had received approval for a nuclear strike on the United States, adding that the situation on the peninsula had reached an explosive stage. Analysts say a full-scale conflict is extremely unlikely and North Korea's threats are instead aimed at drawing Washington into talks that could result in aid and boosting leader Kim Jong Un's image at home.

Source: Violet Arch Research; Various news-paper articles

11

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Policy-Regulatory Risks / Uncertainties for Cairn

Particulars Comments

- Crude price Arrived at a specific formula approved by the government in the PSC. Discount to brent crude ranges in between 10% to 15%.

Since Aug’09 Royalty It is 20% of well-head value. However, it works out to 15-16% of realizaed value and may vary slightly depending on government calculation of post well-head value. A further 5% increase in royalty could impact FY14 EPS by ~7% and valuation by ~6%.

Last increased in Feb’12

Cess

Cess increased by government in budget FY13 from Rs 2500/MT to Rs 4500/MT. There is a chance of hike in cess going forward. However, too high a hike or too frequent a hike in cess may also impact ONGC and Oil India to a large extent with their crude realization being determined by government. An increase in cess by Rs 2000/MT further could impact FY14 EPS by ~7% and repeatedly similarly thereafter every three years could affect valuation by ~10%.

- Cost Petroleum

Cairn is allowed to recover its capex and production costs (upto 100% of revenues) before sharing any profit petroleum. However, government may disapprove some capex or costs upon its own assessment. Government has earlier rejected USD 238mn of capex by Cairn during its previous exploration phase in Rajasthan block.

Since Q1FY12 Profit Petroleum

Post all the cost recovery, Profit Petroleum sharing with the government as is calculated as per the investment multiple. If government disapproves some costs, the share of profit petroleum of Cairn may decrease. In FY14 government share of profit petroleum will be 30% compared to 20% in FY13 and it will impact FY14 EPS by ~12%.

Since Aug’09 Tax Holiday Seven year tax holiday form the start of production. However Cairn continues to pay Minimum Alternate Tax (MAT). Also, any gas commercialization may not come under tax holiday as natural gas is not considered as mineral oil.

Signed in May’94 Contract period The contract is valid upto May 2020 and can be extended on mutual agreement but terms may be changed by DGH while giving approval for extension.

Government may take decision this year or next.

Gas price hike

As per recommendations of Rangarajan panel, the government may look into hiking the price of gas by linking it to a price arrived upon by taking into consideration gas prices across various sources. Cairn is looking forward to monetize its gas discoveries in Rajasthan block. However, Rajasthan being a pre-NELP block gas price will be determined by government. For any discovery from NELP blocks awarded to Cairn, gas price hike would be a positive step. Recently, Cairn has started commercial sales of its gas produced from Rajasthan block. At present it ~0.14mmscmd and adds about Rs 500mn to revenues. Every $1/mmbtu increase in gas price could increase its revenues by ~100mn.

Government may take decision this year before NELP X auction.

Profit sharing model to revenue sharing model

Under the existing production sharing contract (PSC), the contractor first recovers his expenditure before sharing profit. What is under consideration is production-linked payment, which is said to be more transparent and will have less intervention in routine exploration and development activities. Under this proposal, oil companies would have to pay the Government an agreed amount, depending on the level of output, and not on the investment in the exploration block. The existing production from Rajasthan block comes under profit sharing model. However, with Cairn embarking once again on exploration programme in Rajasthan block, any new commercial discovery may come under revenue sharing model.

Allowed since Feb’13 Allowing exploration in producing blocks

The petroleum ministry has allowed exploration in mining lease (producing fields) areas but exploration costs will be allowed for cost recovery only if a discovery is technically and commercially viable. The contractor will therefore carry out further exploration activities at its risk in the Mining Lease area, after the expiry of the exploration period. Positive for the whole sector. Cairn has already embarked on a 3 year exploration programme in Rajasthan block to tap 3.2bnboe of reserves of exploration upside. However, the costs will be recoverable only on the establishment of commerciality of discovery.

-

Defense ministry declaring certain exploration areas as No-Go areas.

Force majeure had been declared in Cairn's KG-OSN-2009/3, MB-DWN-2009/1, PR-OSN-2004/1 blocks due to the denial of permission to carry out exploration activity in the restricted area by the Ministry of Defence. CCI in its meeting held in Mar’13 has given clearance for exploration activity in small portion of the KG-OSN-2009/3 block. However, further clarity is awaited on the rest of the blocks.

Jun’11 to Sept’11 Cairn-Vedanta deal

The government gave its approval for the Cairn-Vedanta deal only after Cairn agreed to make royalty cost recoverable in the Rajasthan block. Prior to this, as per a previous agreement, the entire royalty burden was being borne by ONGC which owns a 30% stake in the block. The government also forced Cairn to withdraw a court case against cess levied in the Rajasthan block which it was paying under protest.

Source: VioletArch Research

12

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Investment Arguments

Resource-rich Rajasthan fields

Recently, CIL raised its Rajasthan potential resource to around 7.3 billion barrels of oil

equivalent (boe) from earlier estimates of about 6.5boe, with discovered resources in Mangala,

Bhagyam, Aishwarya, Rageshwari, Saraswati and other fields at around 4.2bnboe. The

Fatehgarh formation in MBARS fields hold 2.1bnboe, of which the proved and probable (2P)

recoverable reserves are estimated at over 1 billion barrels, including enhanced oil recovery

(EOR) reserves of 308mmboe (recently, 70mmboe has been moved from 2C reserves to 2P

reserves ). Twenty other fields, including the Barmer Hill formation, are estimated to hold about

2.0bnboe, of which the gross 2P recoverable resource is estimated to be 165mmboe (compared

to earlier estimates of 140mmboe). The further exploration upside potential in Rajasthan is

currently estimated at around 3.1bnboe. A detailed basin re-evaluation, through re-analysis of

well data, re-processing of seismic data and updated understanding of petroleum systems, has

shown significant growth in the exploration portfolio, with gross risked prospective recoverable

resources of 530mmboe (compared to earlier estimates of 250mmboe). The expected ultimate

recovery (EUR) for Rajasthan Block currently stands at 1.7bnboe from the earlier estimate of

1.4bnboe.

Rajasthan resource potential

The stock tank oil initially in-place (STOIIP) of 2.1bnbbl of MBA fields has an implied recovery

factor of around 30% from primary oil recovery techniques. After implementing EOR

techniques, the same would increase to 48%. The Barmer Hill formation, along with 19

discoveries, with an STOIIP of 2.0bnbbl has an expected ultimate recovery (EUR) of 8%. Fields in

other parts of the world with characteristics similar to Barmer Hill are being developed and have

demonstrated recovery factors in the range of 7-20%. However, we prefer to maintain a

conservative stance and assume a recovery factor of 8% in our valuation as per CIL. Prospective

resources (35-plus prospects) in Rajasthan Block have a EUR of 17%. Recently, Government of

India (GoI) has decided to permit exploration in the development area of Rajasthan block.

R & S STOIIP & S STOIIP

Gas

Gross InitialGross

In Place

Volumes

~2.5 Billion boe in

35+ prospects

Reserves, Resources

and Potential

20 additional

discovered

fields including

Contingent

In Place

GIIP

Oil

STOIIP

Barmer Hill

78

MBA Fields,

Raageshwari MBA

1 293

468

293

and Saraswati

FDP approved

STOIIP

M B A R & SContingent

Resource

MBA

308

R & S 12

A 66

707

EOR

M

477

B

151

2P+2C MBA EOR

250

140

Risked

Prospective

Resource

BH

+ Others

Barmer Hill

+Other Fields

Risked

Prospects,

Leads &

Concepts

The independent estimates of ReservesAnd Contingent Resourcesrecentlycarried out by D&M arein line with the CIL estimates

Top 35 prospects audited by D&Mrisked resource 178 mmbbls

2

1

13

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Pursuant to policy clarity on exploration, Management Committee (MC) has requested the JV to

submit an exploration work programme for the Rajasthan block. The company has drilled its

first exploratory well in Feb’13 (first such well after a hiatus of almost 4 years) in the Rajasthan

block. Rajasthan exploration and appraisal well drilling is planned over a three year period.

Approximately 30 exploration and appraisal wells are to be drilled per year (divided into 20

exploration, 10 appraisal approximately). The company plans to drill over 100 prospects in total

over the next three year period. Capex of approximpately USD 1.0bn is planned for these

activities and depending on the technical and commercial viability of discoveries, the

exploration capex will be cost recoverable. Given the proven prospectivity of the block and track

record of the company, we expect further addition to its reserve potential.

Cairn reserve upgrades over the years

Source: Company; VioletArch Securities

0%

20%

40%

60%

80%

100%

0.0

2.0

4.0

6.0

8.0

Pre-IPO Post-IPO FY08 FY10 FY12

GHIIP EUR Growth in GHIIP Growth in EUR

CAIRN INDIA ANNUAL REPORT 2010-1114

Rajasthan resource base and vision for growth

Target Potential

Production

240,0

00 b

opd

Bhagyam

40,000 bopd

Aishwariya

10,000 bopd

Mangala

125,000 bopd

FDP Approved

Production

175,000 bopd

Further

investment and

Government of

India approval

Raageshwari

+

Others

in m

mbb

lsin

mm

bo

e

Aishwariya

Mangala

Bhagyam

Risked

Prospective

Resource

2P+2C 2P+2C+EOR

Barmer Hill +

other f elds

Risked

Prospects,

Leads and

Cocepts

1 The independent estimates of Reserves and Contingent Resources

carried out by D&M are in line with the CIL estimates

2 Top 35 prospects audited by D&M risked resource 178 mmbbls

12

66

151

477

707

308

140

250

Barmer Hill

and Saraswati

308 EOR

14

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Rajasthan resource base potential

mmboe Stock Tank Oil

Initially in Place Recoverable

(EUR) Recovery Factor

MBA + EOR 2168 1044 48%

Barmer Hill + 19 discoveries 2010 165 8%

Prospective 3100 530 17%

Total 7278 1739 24%

Source: Violet Arch Research

Rajasthan Block production to increase by 22% by end of FY15

In August 2009, CIL began production at Mangala Field. Initially, it was expected to produce at

the plateau rate of 125,000bopd. However, later it was observed that the excellent reservoir

performance could support a higher plateau rate of 150,000bopd. Subsequently, the company

ramped up production at Mangala Field from 125,000bopd to 150,000bopd in April within a day

of securing government’s approval, since all development wells were ready. Incidentally,

Bhagyam has approval to produce at 40,000bopd, but its current production is stuck between

20,000bopd to 25,000bopd as shallow nature of the field combined with higher viscosity of oil

resulted in lower well productivity than anticipated. As per management, approximately 70

additional wells (according to Bhagyam FDP, to reach 40,000bopd 81 development wells were

required out of which 64 has been drilled) would be required to be drilled in the Bhagyam field

to achieve the production rate of 40,000bopd. The company has already received approval for

15 such wells from the management committee and expects production to reach 40,000bopd in

H2FY14. Bhagyam is also expected to produce at higher levels, but a revised FDP is yet to be

submitted. However, taking a conservative stance we assume Bhagyam to achieve a peak rate

of 40,000bopd instead of 50,000bopd (see the graph below). In Aishwarya field, oil-in-place is

substantially higher than originally estimated. According to our calculations, the field can

produce oil at the rate of 20,000bopd. However, at present, CIL has approval only for

production of 10,000bopd and it has to submit revised FDP for raising the production. We

expect company to be more aggressive on this front and submit FDPs in 2HFY14. The company

management has guided exit rate of 200,000bopd to 215,000bopd by end of FY14, of which a

major portion of production is expected from MBA fields. In our model, we have assumed exit

rates for MBA fields of 195,000bopd and 210,000bopd for FY14 and FY15, respectively.

MBA production (bopd)

Source: Violet Arch Research

0

50000

100000

150000

200000

Q1

FY1

0

Q2

FY1

0

Q3

FY1

0

Q4

FY1

0

Q1

FY1

1

Q2

FY1

1

Q3

FY1

1

Q4

FY1

1

Q1

FY1

2

Q2

FY1

2

Q3

FY1

2

Q4

FY1

2

Q1

FY1

3

Q2

FY1

3

Q3

FY1

3

Q4

FY1

3

FY1

4E

FY1

5E

Mangala Bhagyam Aishwarya Rageshwari & Saraswati

15

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Additionally, CIL estimates about 165mmboe of recoverable resources from Barmer Hill and 19

other fields, besides another 530mmboe, compared to 250mmboe earlier, from the exploration

upside. CIL expects incremental production from these resources, which will help the company

to achieve its long-term target of peak production of 300,000bopd from Rajasthan Block.

MBA field production rates

CIL has the requisite approval for production in Mangala, Bhagyam and Aishwarya for

150,000bopd, 40,000bopd and 10,000bopd, respectively. It has secure approvals for further

scale-up of production from Bhagyam and Aishwarya.

Current production

rate (bopd) Approved production

rate (bopd) Peak production rate

(bopd) Comments

Mangala 150000 150000 150000 All approvals in place

Bhagyam 25000 40000 Not yet disclosed Revised FDP for higher rate yet to be submitted

Aishwarya N.A.* 10000 20000 Revised FDP for 20,000bopd yet to be submitted

Source: Violet Arch Research; *CIL has commenced production in Aishwarya field on 25th

Mar’13. However, the data is not available

Peak rate calculation

Although the management has not given any guidance on the peak potential of Bhagyam Field,

we expect the same to be about 50,000bopd as per calculations shown below.

2P Reserves (mmboe)

Peak production rate as of now as per company (bopd)

2P/Peak rate Peak production

rate as per our estimate (bopd)

2P/Peak rate

Mangala 477 150000 3.18 150000 3.18

Bhagyam 151 40000 3.78 50000 3.02

Aishwarya 66 10000 6.60 20000 3.30

Rageshwari & Saraswati 12

3500 3.43

Total 706 200000 3.53 223500 3.02

Source: Violet Arch Research; This is our own assumption and is not based on any scientific theory. Peak rates could vary depending on reservoir characteristics.

MBA production schedule over FY14-15

Rajasthan Block has the requisite approval for achieving a production rate of 190,000bopd.

However, due to delay in ramp-up of Bhagyam and commencement of production from

Aishwarya, it is unable to clock a production rate currently beyond 175,000bopd. Also the

pipeline capacity (175,000bopd) constraint has to be taken care before ramp-up at Bhagyam

happens. The management has indicated that the pipeline can support 10% additional flow-rate

with debottlenecking. Further, the company plans to use DRA (Drag Reducing Agents) to reduce

the viscosity of oil so that flow rate could be increased further to support the upper-end of

management guidance of 215,000bopd. We estimate an exit rate from MBA of 195,000bopd

210,000bopd in FY14 and FY15, respectively.

Q1FY14E Q2FY14E Q3FY14E Q4FY14E Q1FY15E Q2FY15E Q3FY15E Q4FY15E

Mangala 150,000 150,000 145,000 145,000 145,000 145,000 140,000 140,000

Bhagyam 20,000 20,000 30,000 40,000 40,000 40,000 40,000 40,000

Aishwarya 5,000 10,000 10,000 10,000 15,000 20,000 20,000 20,000

Mangala EOR

10,000 10,000 10,000 10,000

Total 175,000 180,000 185,000 195,000 210,000 215,000 210,000 210,000

Source: Violet Arch Research

16

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Key Risks and Concerns

Delay in approvals from ONGC and DGH

The CIL management expects to hit exit rate of 215,000bopd in FY14 post-commencement of

production in Aishwarya and ramp-up in Bhagyam. Revised FDPs for Bhagyam and Aishwarya

are yet to be submitted, which would help the company reach beyond 215,000bopd production

target in the near term. In our model, we have assumed production from Aishwarya to touch

10,000bopd in Q2FY14 and 20,000bopd in Q2FY15 and production from Bhagyam to touch

40,000bopd in Q4FY14. Any further delay could result in delayed cash-flows for the company.

Further, CIL has expects to monetize the other smaller discoveries in Rajasthan block to meet its

guidance rate of 215,000bopd in FY14. Any delay in seeking the regulator and JV partner’s

approval will push back the company’s cash-flows, thereby eroding investor confidence.

Falling crude prices

Being a direct play on crude oil prices, CIL is exposed to crude price volatility. In our valuation,

we have assumed a long-term brent crude price of $90/bbl. Any correction in crude prices

beyond that level will affect the company’s profitability and share price.

CIL valuation sensitivity analysis

Long-term crude price assumption (USD/bbl)

80 90 100 110 120

Long-term USD-INR rate assumption

45 318 345 377 409 441

47 326 355 387 420 453

49 334 364 398 432 466

51 338 373 408 443 478

53 346 382 418 454 491

FY14 EPS sensitivity analysis

FY14 crude price assumption (USD/bbl)

100 105 110 115 120

FY14 USD-INR rate assumption

49 42.5 45.3 48.0 50.8 53.5

51 44.3 47.2 50.1 52.9 55.8

53 46.1 49.1 52.1 55.1 58.1

55 47.9 51.0 54.1 57.2 60.3

57 49.7 52.9 56.2 59.4 62.6

Source: Company, Violet Arch Research

Increase in statutory levies by government

In the Budget FY13, the government increased the cess from Rs 2500 per tonne to Rs 4500 per

tonne, which impacted CIL’s profitability by USD6/bbl. The move impacted FY13 EPS by around

Rs4.2 and valuation by about 8%. To be on conservative side we have assumed cess to increase

by Rs 2000/tonne after every five years which resulted in CIL valuation of Rs 364/share as

compared to Rs 380/share if these is no increase in cess further.

17

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Failure to convert exploration assets into unrisked potential reserves

Currently, CIL is considered a single-asset player (Rajasthan Block), and any failure to convert its

current exploration portfolio into unrisked potential resource base could lead to erosion of

investor confidence in the company.

Also Cairn has embarked upon a 3-year exploration programme in Rajasthan block to tap the

~3.1bnboe of prospective reserves from exploration upside. Any failure to convert these

exploration upsides into production would be a negative trigger for the stock as the exploration

costs for these are cost recoverable only upon commercial and technical success of the

discovery.

Mis-use of strong cash-flow of CIL by Vedanta

Over the years Cairn India has done well in exploration and production space through a

tremendous performance in Rajasthan, Cambay and Ravva. But the change in ownership has

created doubts in the investors’ minds considering the inexperience of Vedanta in oil and gas

sector as well as chance of mis-use of strong cash-flow of CIL to repay debt of its other group

companies in a way that it may not be beneficial to minority shareholder. However, Vedanta has

sought to allay these fears by stating to fulfill Cairn India’s commitments towards exploration

and production activities in India, Sri Lanka.

18

VIOLET ARCH Research

Cairn India Ltd - Company Report

VIOLET ARCH Securities Pvt. Ltd. (Erstwhile Alchemy Share & Stock Brokers Pvt. Ltd.)

Valuation

On the back of a further ramp-up of Bhagyam and Aishwarya, CIL’s production is expected to

reach 195,000bopd by end-FY14 from the current rate of 175,000bopd. Rajasthan Block’s near-

term potential is estimated at 215,000bopd, which is expected to come largely from MBA fields.

The long-term potential, as per the management guidance, is 300,000bopd, which is expected

from monetization of Barmer Hill and 19 discoveries as well as exploration upsides. We value

MBA fields on a NAV basis and other reserves on an EV/boe basis in order to arrive at a target

price of Rs 374 per share, which reflects an EV/boe of $9.5/bbl.

Assumptions for MBA

MBA production Production to be 187,000 bopd in FY14; 207,250 bopd in FY15 and ~210,000 bopd through FY16-FY20

MBA - EOR To start in mid-FY15 in Mangala, in FY16 in Bhagyam and in FY17 in Aishwarya

Brent crude price USD 110/bbl in FY14 and USD 100/bbl in FY15 and USD 90/bbl for long-term

Discount to Brent crude 12%

Exchange rate Rs 53/USD in FY14; Rs 51/USD in FY15 and Rs 49/USD for long-term

Capex USD 2.0 bn over FY14 and FY15

Direct field opex USD 3.5/bbl

Pipeline opex USD 1.5/bbl

Royalty 15.0% of Revenues

Cess Rs 4500/tonne for through FY13-17 and hiked by Rs 2000/tonne thereafter every five years

WACC 10%

Source: Violet Arch Research

CIL's cash-flows from MBA (Rs bn)

FY14E FY15E FY16E FY17E FY18E FY19E FY20E

Revenues 200.2 194.9 159.3 147.6 155.7 156.2 156.6

Production costs 12.7 13.9 15.3 16.8 18.4 19.3 20.3

Cess + Royalty 66.9 69.0 65.4 65.4 80.1 80.1 80.0

Capex 15.7 12.4 3.9 3.9 3.9 3.9 3.9

Pre-tax cash-flows 104.9 99.6 74.8 61.5 53.4 52.9 52.4

Tax 20.0 18.0 11.2 8.5 6.9 6.8 10.8

Post-tax cash-flow 84.8 81.6 63.6 53.0 46.5 46.1 41.6

NAV 393.4

No of o/s shares (mn) 1908

NAV per share (Rs/share) 206

Source: Violet Arch Research

CIL valuation

Block Net 2P/ Recoverable

Reserves (mmbbl) Rs/share (USD/boe)

MBA + EOR 620 206 12.9

Barmer Hill 116 15 5.2

Exploration Upside Potential 371 49 5.2

Ravva 14 3 9.1

Cambay 4 1 9.1

Total 1,125 275 9.5

Debt - 0 -

Cash & Cash Eq - 99 -

Cairn India - 374 -

Source: Violet Arch Research

Related Documents