C11 - 1 Learning Objectives 1. The Nature of Current Liabilities 2. Short-Term Notes Payable 3. Contingent Liabilities 4. Payroll and Payroll Taxes 5. Accounting Systems for Payroll 6. Employees’ Fringe Benefits 7. Financial Analysis and Interpretation Chapter 11 Current liabilities

C11 - 1 Learning Objectives 1.The Nature of Current Liabilities 2.Short-Term Notes Payable 3.Contingent Liabilities 4.Payroll and Payroll Taxes 5.Accounting.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

C11 - 1

Learning Objectives

1. The Nature of Current Liabilities

2. Short-Term Notes Payable

3. Contingent Liabilities

4. Payroll and Payroll Taxes

5. Accounting Systems for Payroll

6. Employees’ Fringe Benefits

7. Financial Analysis and Interpretation

Chapter 11 Current liabilities

C11 - 2

The nature of current liabilities

Liabilities that are to be paid out of current assets and are due within a short time, usually within one year, are called current liabilities.

– Accounts payable– Notes payable– Taxes payable– Interest payable– Wages payable– Unearned revenue– Unearned rent

C11 - 3

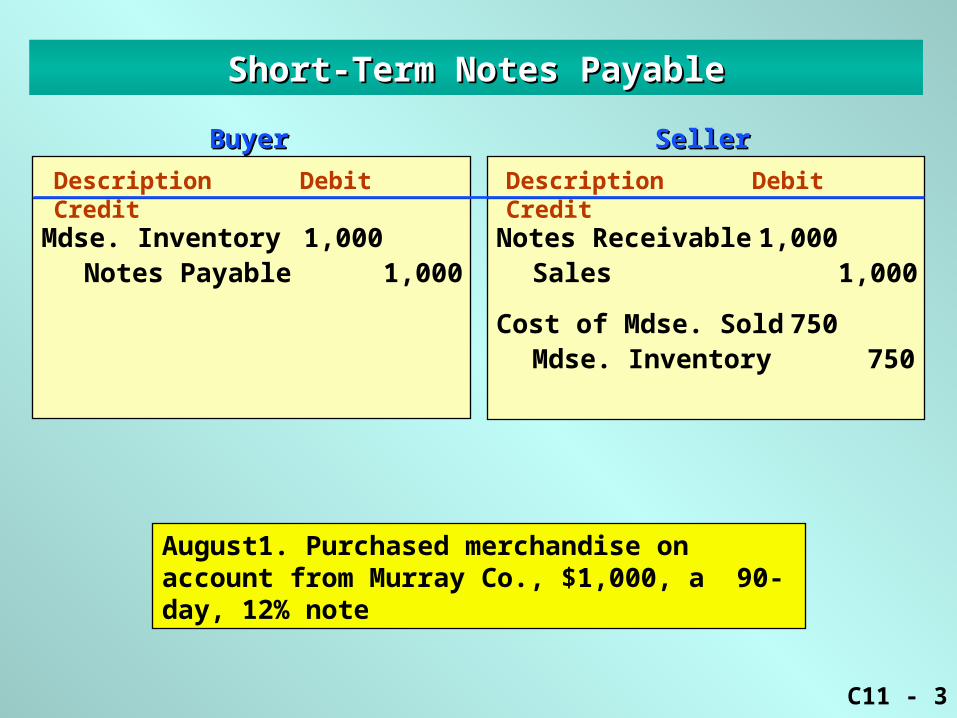

Short-Term Notes PayableShort-Term Notes Payable

Description Debit Credit

Mdse. Inventory 1,000Notes Payable 1,000

Notes Receivable 1,000Sales 1,000

Cost of Mdse. Sold 750Mdse. Inventory 750

BuyerBuyer SellerSeller

Description Debit Credit

August1. Purchased merchandise on account from Murray Co., $1,000, a 90-day, 12% note

C11 - 4

Short-Term Notes PayableShort-Term Notes Payable

Description Debit Credit

Notes payable 1,000Interest expenses 30

Cash 1,000

Cash 1,030 Notes Receivable 1,000 Interest revenue 30

BuyerBuyer SellerSeller

Description Debit Credit

October 30, paid principal and interest due on note.

C11 - 5

Short-Term Notes PayableShort-Term Notes Payable

Description Debit Credit

Mdse. Inventory 10,000Accts. Payable 10,000

Accts. Payable 10,000Notes Payable 10,000

Accts. Receivable 10,000Sales 10,000

Cost of Mdse. Sold 7,500Mdse. Inventory 7,500

Notes Receivable 10,000Accts. Receivable 10,000

Bowden Co. (Buyer/Borrower)Bowden Co. (Buyer/Borrower) Coker Co. (Seller/Creditor)Coker Co. (Seller/Creditor)

Description Debit Credit

May 1. Bowden Co. purchased merchandise from Coker Co.$10,000 on account.

May 31, Bowden Co. issued a 60-day,12% note for $10,000 to Coker Co. on account.

C11 - 6

Short-Term Notes PayableShort-Term Notes Payable

Description Debit Credit

Mdse. Inventory 10,000Accts. Payable 10,000

Accts. Payable 10,000Notes Payable 10,000

Notes Payable 10,000Interest Expense 200

Cash 10,200

Accts. Receivable 10,000Sales 10,000

Cost of Mdse. Sold 7,500Mdse. Inventory 7,500

Notes Receivable 10,000Accts. Receivable 10,000

Cash 10,200Interest Revenue 200Notes Receivable 10,000

Bowden Co. (Buyer/Borrower)Bowden Co. (Buyer/Borrower) Coker Co. (Seller/Creditor)Coker Co. (Seller/Creditor)

Description Debit Credit

July 30. Bowden Co. paid the amount due.

Interest: $10,000 x 12% x 60 / 360 = $200

C11 - 7

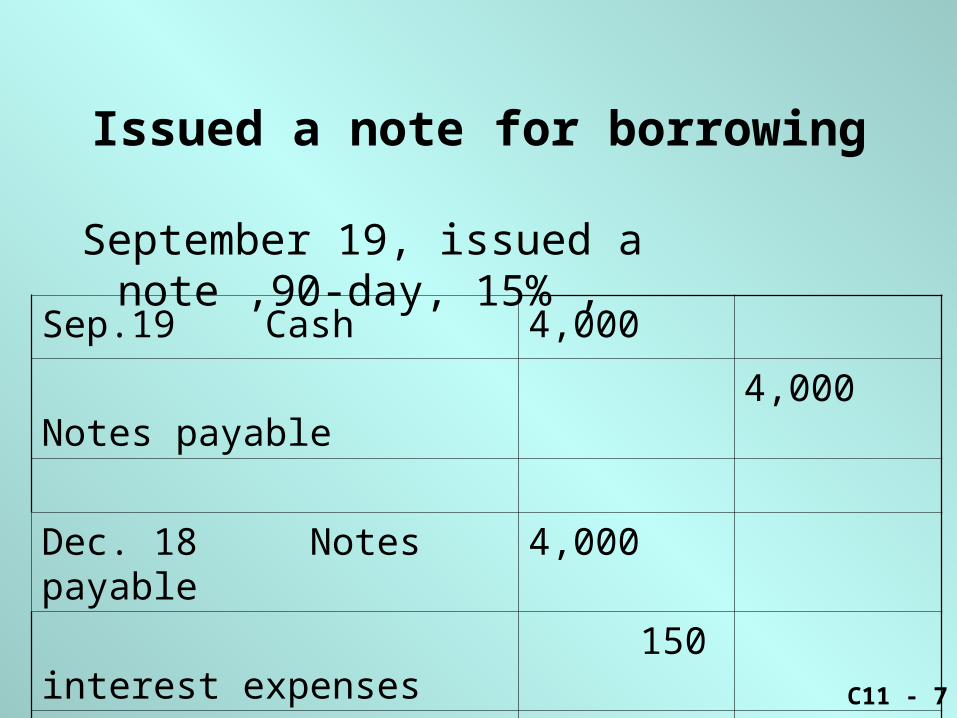

Issued a note for borrowing

September 19, issued a note ,90-day, 15% ,

Sep.19 Cash 4,000

Notes payable 4,000

Dec. 18 Notes payable 4,000

interest expenses 150

Cash 4,150

C11 - 8

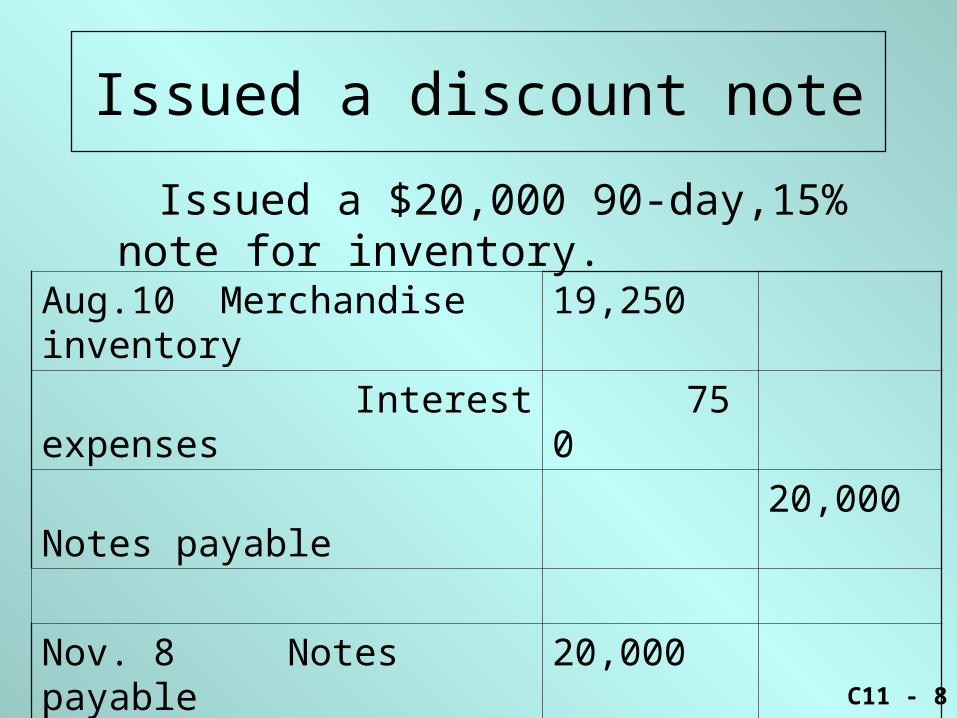

Issued a discount note

Issued a $20,000 90-day,15% note for inventory.

Aug.10 Merchandise inventory 19,250

Interest expenses 750

Notes payable 20,000

Nov. 8 Notes payable 20,000

Cash 20,000

C11 - 9

DateDate DescriptionDescription DebitDebit CreditCredit

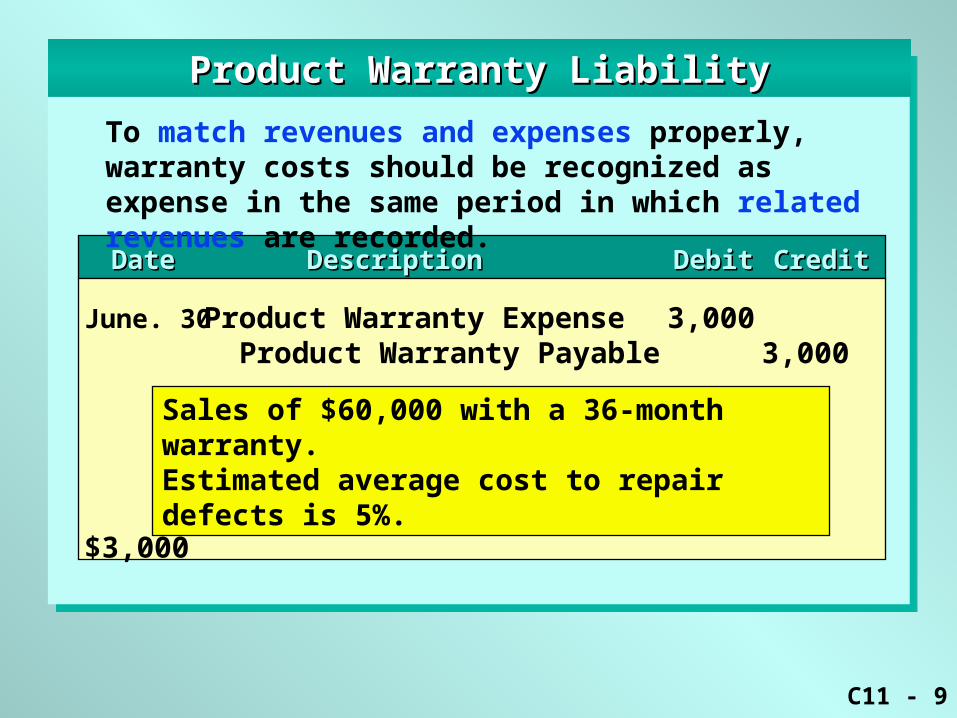

Product Warranty LiabilityProduct Warranty Liability

Product Warranty Expense 3,000Product Warranty Payable 3,000

Estimated warranty: $60,000 x 5% = $3,000

June. 30

Sales of $60,000 with a 36-month warranty.Estimated average cost to repair defects is 5%.

To match revenues and expenses properly, warranty costs should be recognized as expense in the same period in which related revenues are recorded.

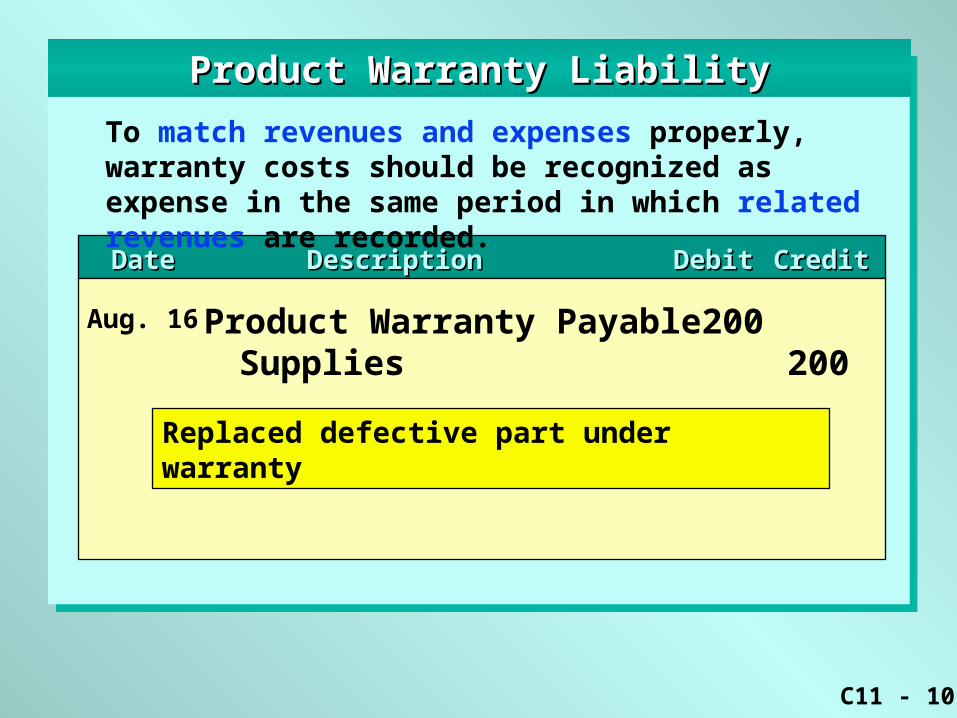

C11 - 10

DateDate DescriptionDescription DebitDebit CreditCredit

Product Warranty LiabilityProduct Warranty Liability

Product Warranty Payable 200Supplies 200

Aug. 16

Replaced defective part under warranty

To match revenues and expenses properly, warranty costs should be recognized as expense in the same period in which related revenues are recorded.

C11 - 11

1. Good employee relations demand that payrolls be

calculated accurately and paid as scheduled.

2. Payroll expenditures are subject to a variety of

federal, state, and local taxes.

3. Total payroll expense (gross payroll plus payroll

taxes) has a major impact on net income.

Payroll and Payroll TaxesPayroll and Payroll Taxes

Payroll is the amount paid to employees for services provided. Payrolls are important because:

C11 - 12

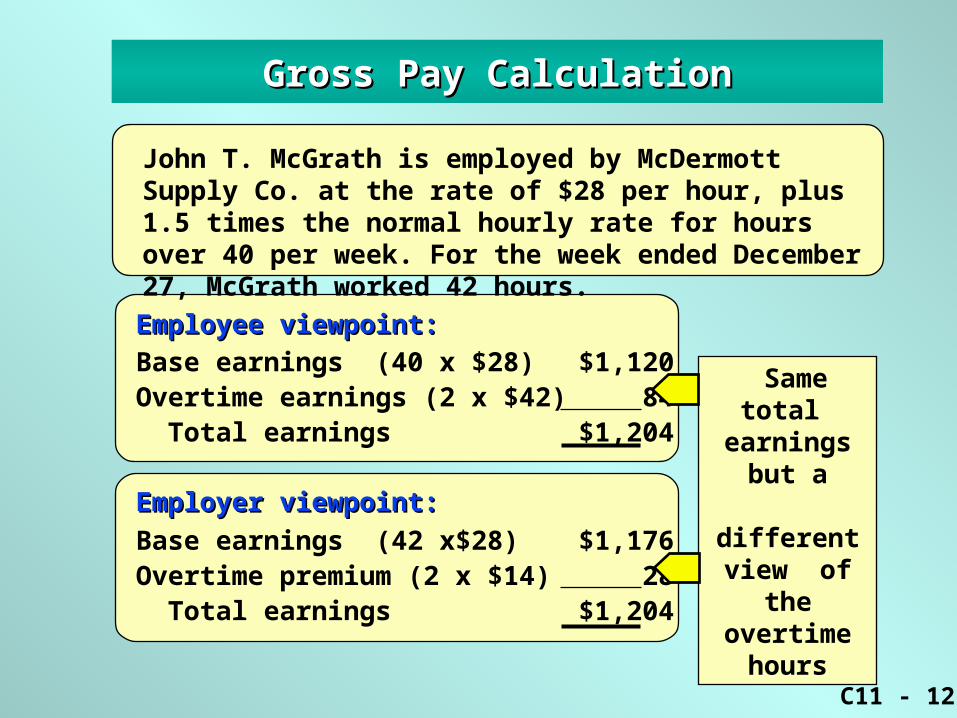

Base earnings (40 x $28) $1,120Overtime earnings (2 x $42) 84 Total earnings $1,204

Base earnings (42 x$28) $1,176Overtime premium (2 x $14) 28 Total earnings $1,204

Gross Pay CalculationGross Pay Calculation

John T. McGrath is employed by McDermott Supply Co. at the rate of $28 per hour, plus 1.5 times the normal hourly rate for hours over 40 per week. For the week ended December 27, McGrath worked 42 hours.

Employee viewpoint:Employee viewpoint:

Employer viewpoint:Employer viewpoint:

Same total earnings

but a different

view of the overtime

hours

C11 - 13

($80,000 - $79,296) $704Social security tax rate x 6% Social security tax $42.24

Current earnings $1,204Medicare tax rate x 1.5% Medicare tax 18.06Total FICA tax $60.30

FICA Tax CalculationFICA Tax Calculation

Assume that John T. McGrath’s annual earnings prior to the current period total $79,296. The current period earnings are $1,204.

FICA tax calculation:FICA tax calculation:

Earnings subject to 6.0% social security tax

Earnings subject to 1.5% Medicare tax

C11 - 14

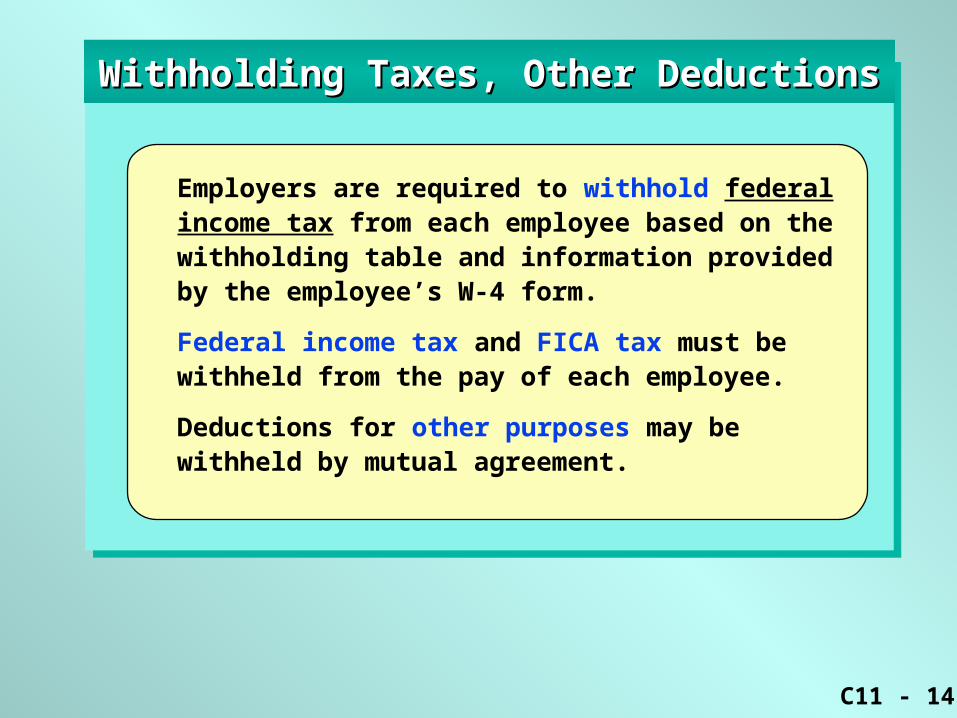

Withholding Taxes, Other DeductionsWithholding Taxes, Other Deductions

Employers are required to withhold federal income tax from each employee based on the withholding table and information provided by the employee’s W-4 form.

Federal income tax and FICA tax must be withheld from the pay of each employee.

Deductions for other purposes may be withheld by mutual agreement.

C11 - 15

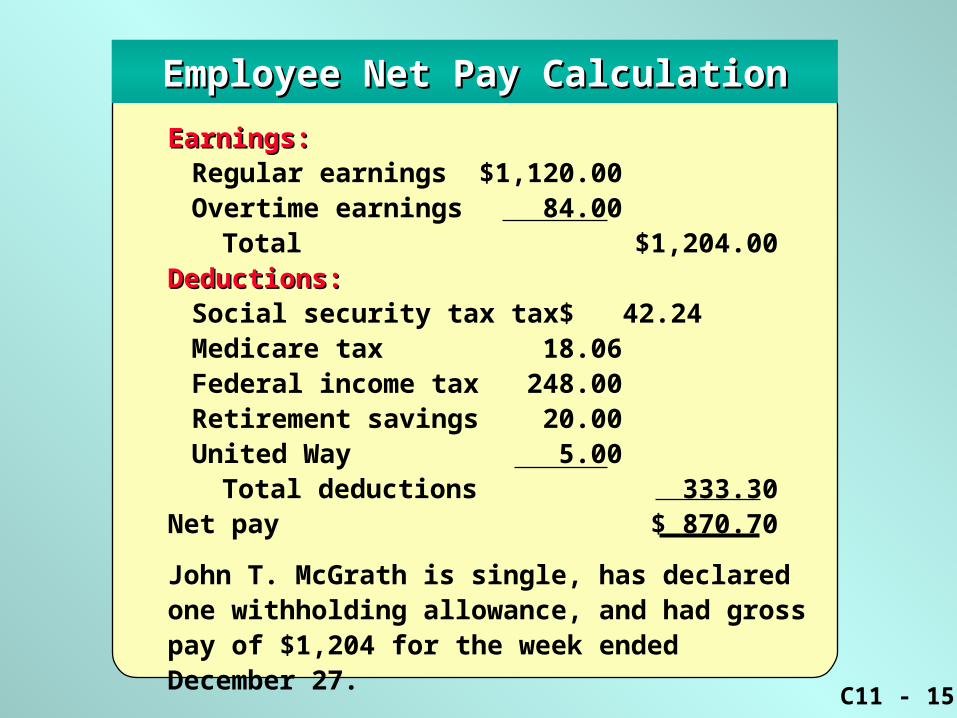

Earnings:Earnings:Regular earnings $1,120.00Overtime earnings 84.00

Total $1,204.00Deductions:Deductions:

Social security tax tax $ 42.24Medicare tax 18.06Federal income tax 248.00Retirement savings 20.00United Way 5.00

Total deductions 333.30Net pay $ 870.70

John T. McGrath is single, has declared one withholding allowance, and had gross pay of $1,204 for the week ended December 27.

Employee Net Pay CalculationEmployee Net Pay Calculation

C11 - 16

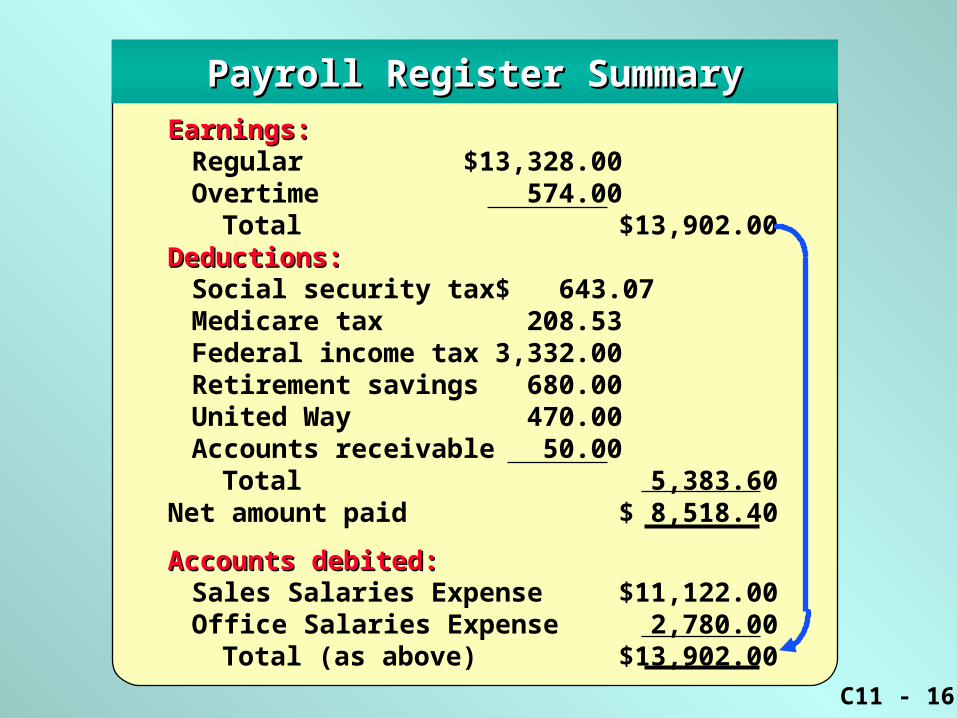

Earnings:Earnings:Regular $13,328.00Overtime 574.00

Total $13,902.00Deductions:Deductions:

Social security tax $ 643.07Medicare tax 208.53Federal income tax 3,332.00Retirement savings 680.00United Way 470.00Accounts receivable 50.00

Total 5,383.60Net amount paid $ 8,518.40

Accounts debited:Accounts debited:Sales Salaries Expense $11,122.00Office Salaries Expense 2,780.00

Total (as above) $13,902.00

Payroll Register SummaryPayroll Register Summary

C11 - 17

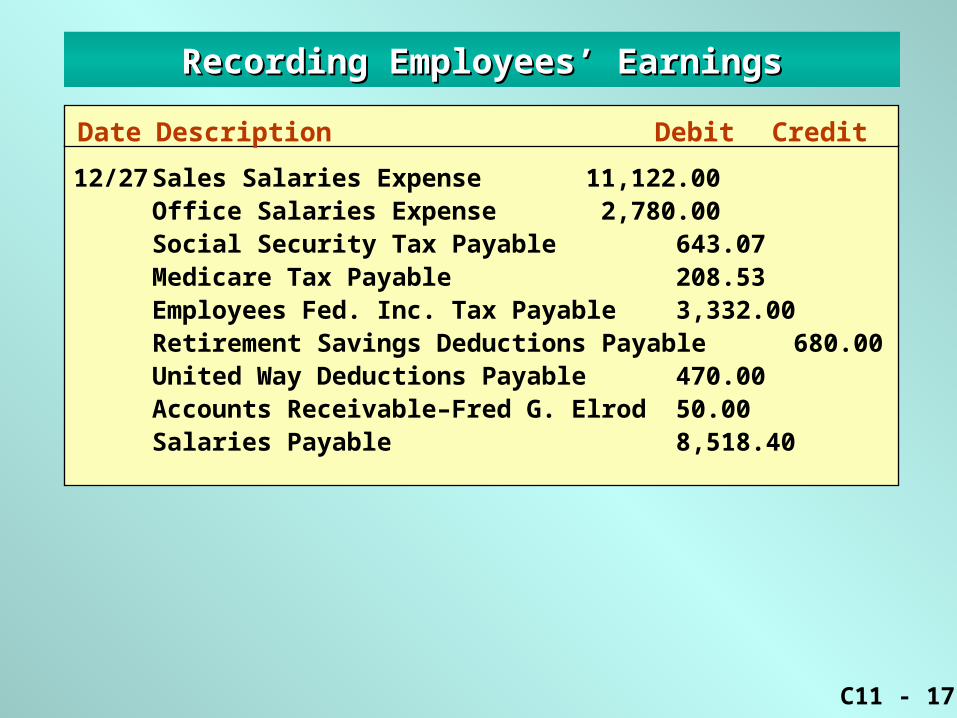

Recording Employees’ EarningsRecording Employees’ Earnings

Date Description Debit Credit

12/27 Sales Salaries Expense 11,122.00Office Salaries Expense 2,780.00

Social Security Tax Payable 643.07Medicare Tax Payable 208.53Employees Fed. Inc. Tax Payable 3,332.00Retirement Savings Deductions Payable 680.00United Way Deductions Payable 470.00Accounts Receivable–Fred G. Elrod 50.00Salaries Payable 8,518.40

C11 - 18

1. FICA tax must be paid by the employer on the earnings of each employee.

2. Employers must pay federal unemployment compensation tax at the rate of .8% (.008) on the first $7,000 of annual earnings of each employee.

3. Employers in most states also pay state unemployment compensation tax based on claims experience at a rate not to exceed 5.4% (.054) of the first $7,000 of annual earnings.

Employer’s Payroll TaxesEmployer’s Payroll Taxes

In addition to the amounts due employees, the employer must calculate and pay the following:

C11 - 19

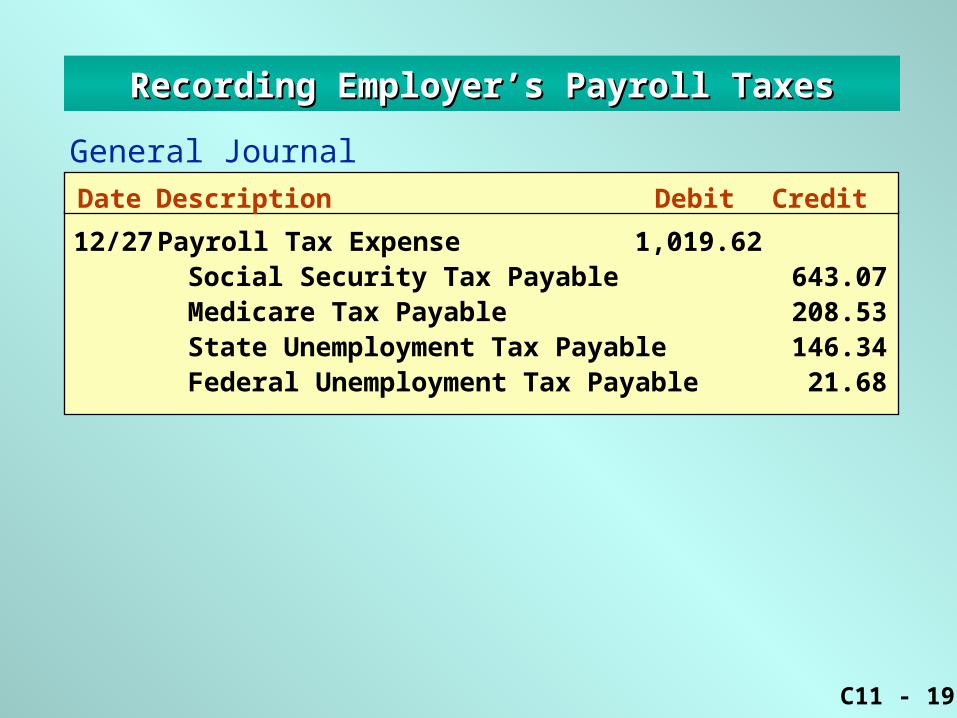

Recording Employer’s Payroll TaxesRecording Employer’s Payroll Taxes

General Journal

Date Description Debit Credit

12/27 Payroll Tax Expense 1,019.62Social Security Tax Payable 643.07Medicare Tax Payable 208.53State Unemployment Tax Payable 146.34Federal Unemployment Tax Payable 21.68

C11 - 20

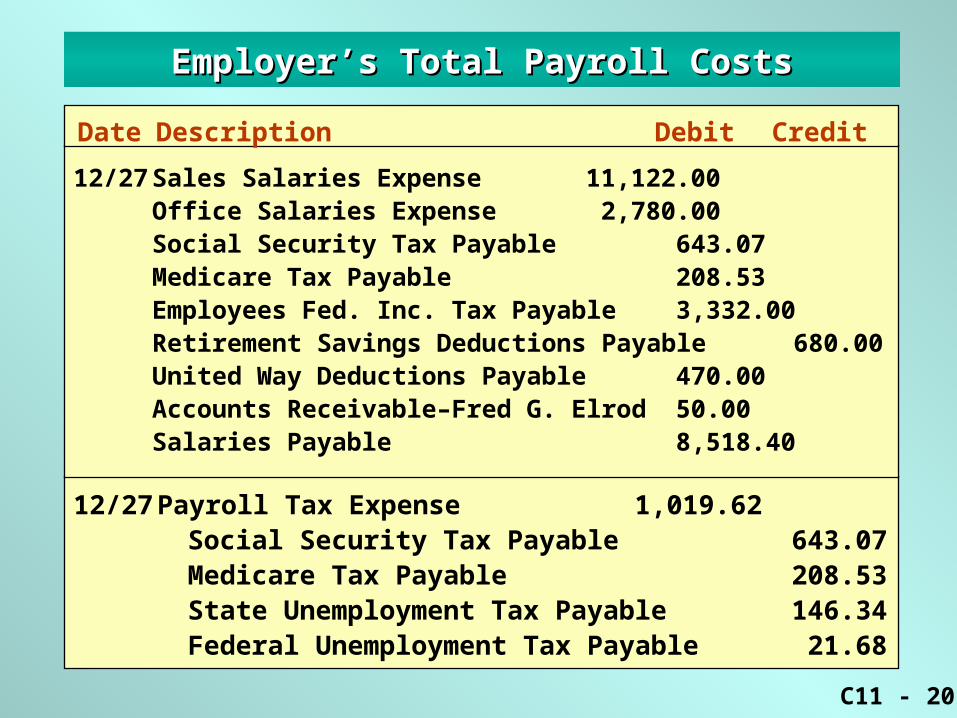

Employer’s Total Payroll CostsEmployer’s Total Payroll Costs

Date Description Debit Credit

12/27 Sales Salaries Expense 11,122.00Office Salaries Expense 2,780.00

Social Security Tax Payable 643.07Medicare Tax Payable 208.53Employees Fed. Inc. Tax Payable 3,332.00Retirement Savings Deductions Payable 680.00United Way Deductions Payable 470.00Accounts Receivable–Fred G. Elrod 50.00Salaries Payable 8,518.40

12/27 Payroll Tax Expense 1,019.62Social Security Tax Payable 643.07Medicare Tax Payable 208.53State Unemployment Tax Payable 146.34Federal Unemployment Tax Payable 21.68

C11 - 21

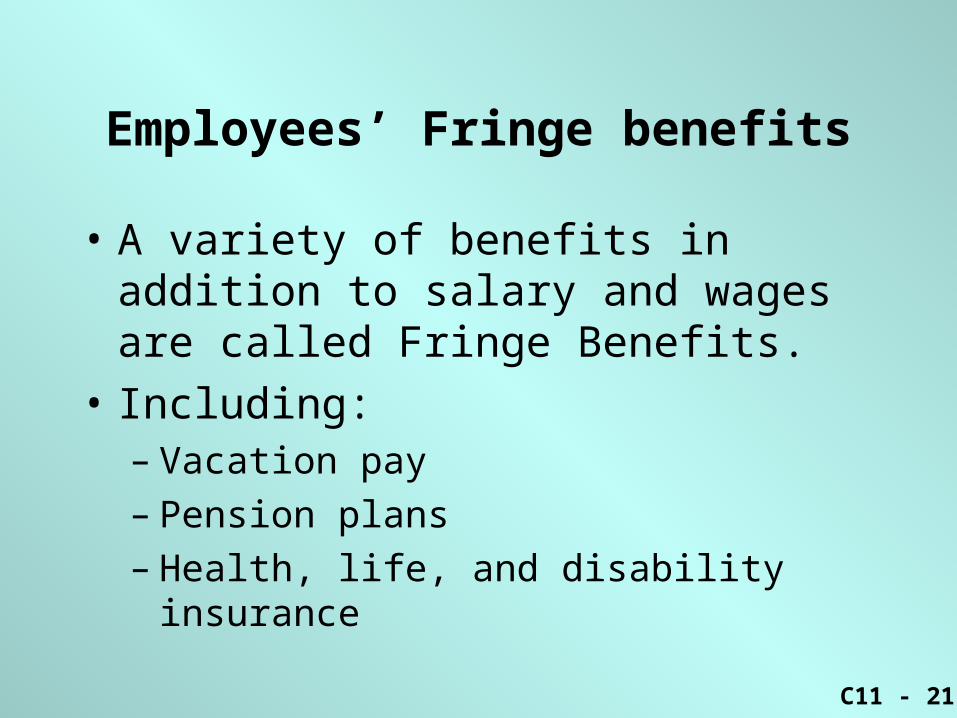

Employees’ Fringe benefits

• A variety of benefits in addition to salary and wages are called Fringe Benefits.

• Including:– Vacation pay– Pension plans– Health, life, and disability insurance

C11 - 22

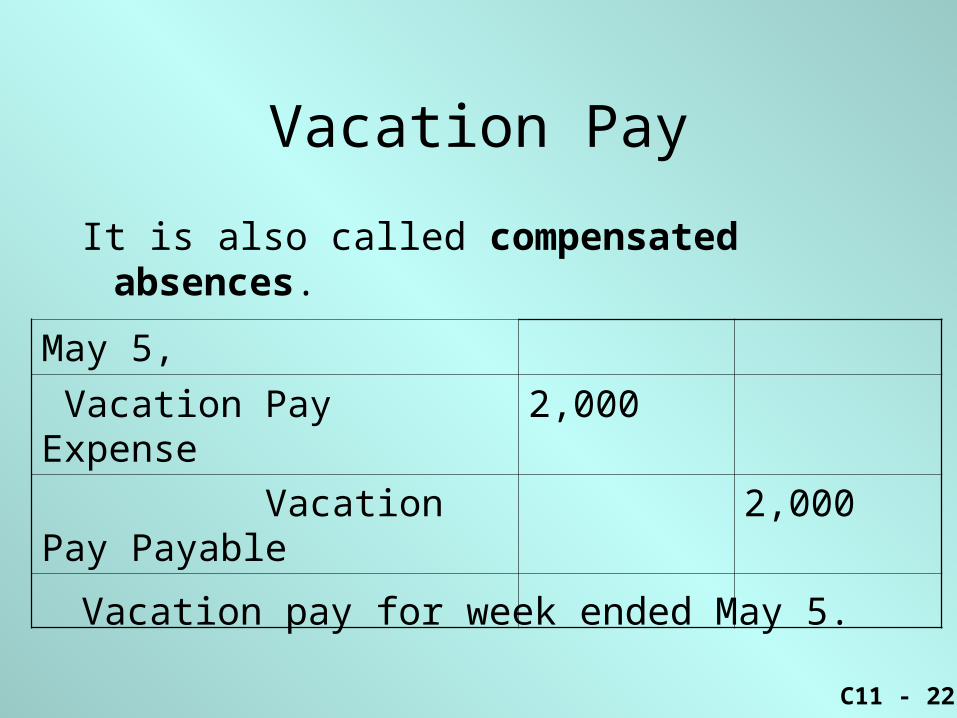

Vacation Pay

It is also called compensated absences.

Vacation pay for week ended May 5.

May 5,

Vacation Pay Expense 2,000

Vacation Pay Payable 2,000

C11 - 23

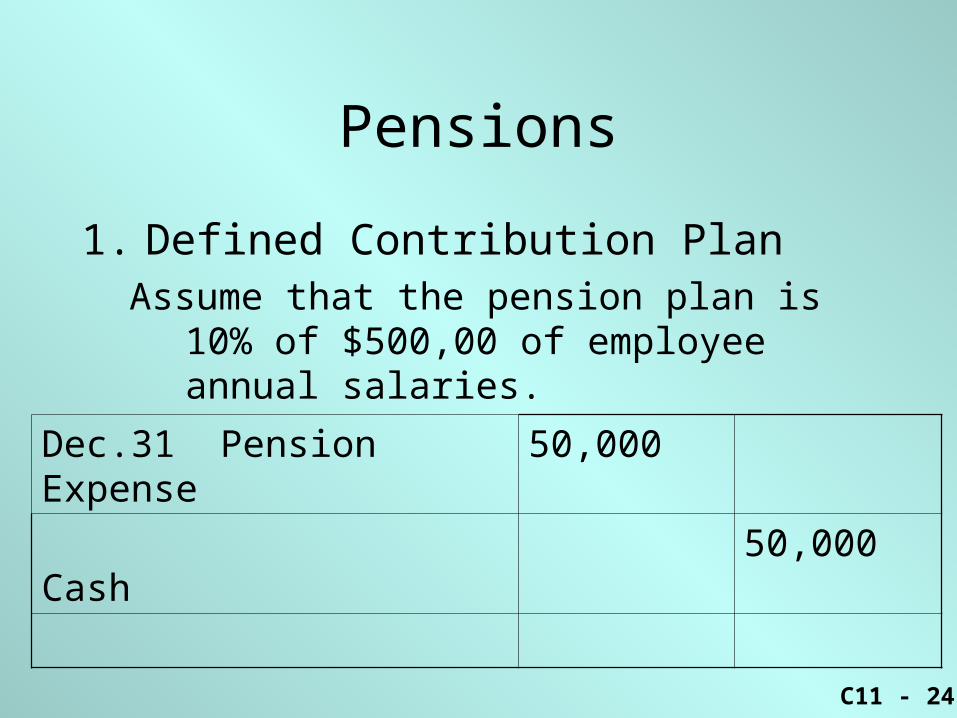

Pensions

1. Defined Contribution Plan• A defined contribution plan requires that a fixed

amount of money be invested for the employee’s behalf during the employee’s working years. The employer is required to make annual pension contributions.

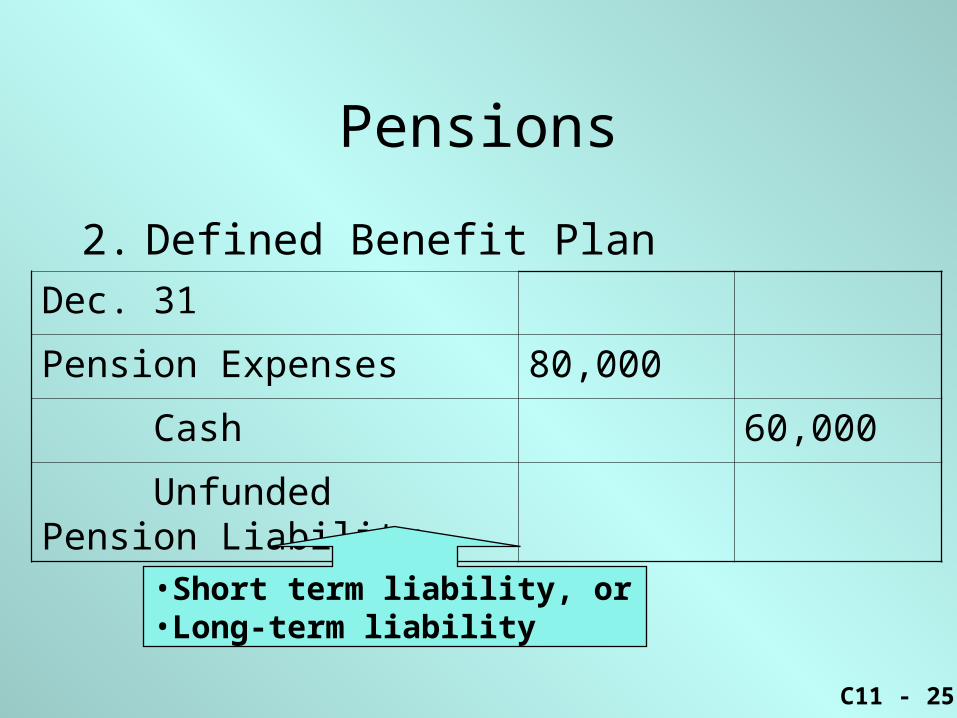

2. Defined Benefit Plan• Employers may choose to promise employees a

fixed annual pension benefit at retirement, based on years of service and compensation levels.

C11 - 24

Pensions

1. Defined Contribution PlanAssume that the pension plan is 10% of $500,00

of employee annual salaries.

Dec.31 Pension Expense 50,000

Cash 50,000

C11 - 25

Pensions

2. Defined Benefit PlanDec. 31

Pension Expenses 80,000

Cash 60,000

Unfunded Pension Liability

•Short term liability, or•Long-term liability

C11 - 26

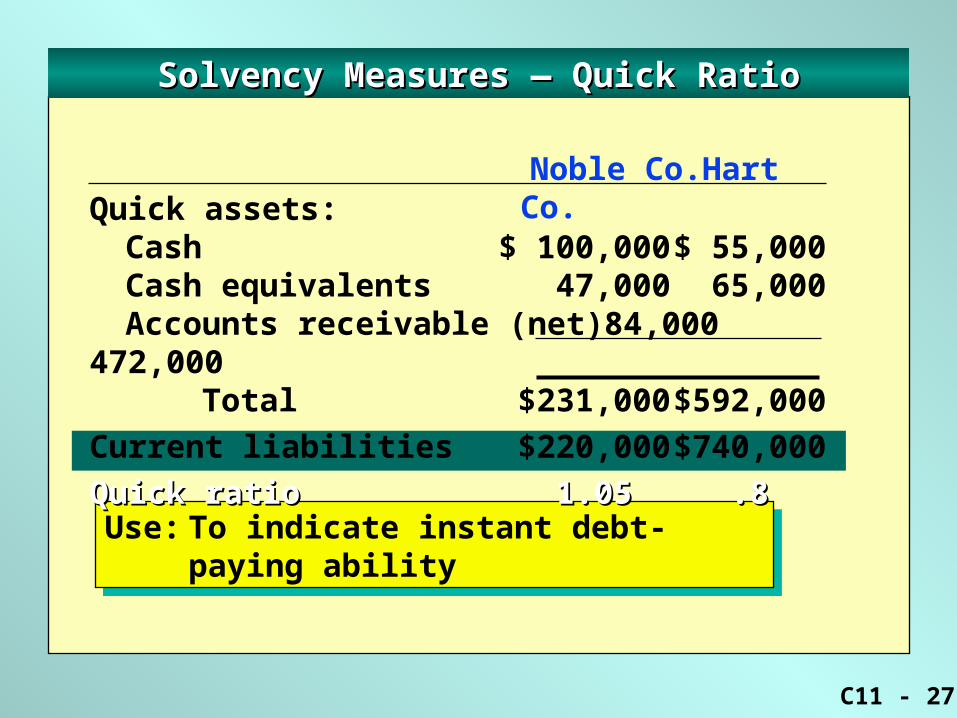

Solvency Measures — Quick RatioSolvency Measures — Quick Ratio

Noble Co. Hart Co.Quick assets:

Cash $ 100,000 $ 55,000Cash equivalents 47,000 65,000Accounts receivable (net) 84,000 472,000 Total $231,000 $592,000

Current liabilities $220,000 $740,000

Quick Ratio = Quick assets / Current liabilities

C11 - 27

Solvency Measures — Quick RatioSolvency Measures — Quick Ratio

Use: To indicate instant debt-paying abilityUse: To indicate instant debt-paying ability

Noble Co. Hart Co.Quick assets:

Cash $ 100,000 $ 55,000Cash equivalents 47,000 65,000Accounts receivable (net) 84,000 472,000 Total $231,000 $592,000

Current liabilities $220,000 $740,000

Quick ratioQuick ratio 1.05 1.05 .8 .8

C11 - 28

HOME WORK

READING:1. Illustrative problem

2. Self- examination questions

3. Multiple choice

Writing:1. Exercise

2. Problem 11-1A

Discussion:1. Activity 11-2;11-3

C11 - 29

This is the end of Chapter 11

Related Documents