IMO 2020 UPDATE 2,052 scrubbers so far The latest scrubber data from DNV GL show an accelerating increase in planned scrubber installations during 2019. The pre-2020 total of scrubber-fitted vessels now stands at 2,052, quickly closing in on our 2,300 forecast. Dry bulk has the majority of this month’s additions. The accelerating uptake for 2019 installation indicates still-available capacity in our view, and our estimate is looking increasingly conservative. Latest DNV GL numbers show 2,052 installed by end-2019. After increasing its forecasts for 2019 scrubber uptake by 22% last month, this month’s numbers show a further 23% increase, to take scheduled scrubber uptake for end-2019 to 2,052. DNB Markets’ 2,300 forecast starting to look conservative, as 502 scrubbers were added to the pre-2020 orderbooks during the last month. This is up from the 282 increase last month, and we still have 14 months to go before the regulations kick in. Dry bulk uptake growth accelerating 2.0x from last month. Dry bulk was responsible for 51% (255) of the additions in the latest revisions, while 17% (87) was for tankers and 9% (45) for container ships. 2019 installations balloon 52%, to 1,268, with only 105 booked for 2020. The latest data show 1,268 scrubber installations are planned for 2019 (up 52%, or 432 units from 836 reported in October), while only 37 additions leave 2020 installations at 105. We see the accelerating growth in 2019 as a sign of still-available capacity, and are likely to see continued additions ahead, though the minor uptick for 2020 could indicate tighter pre-2020 scrubber availability. Shipping vs OSEBX (12m) Source: Factset EQUITY RESEARCH 2 November 2018 Research report prepared by DNB Markets, a division of DNB Bank ASA This report was completed and disseminated at 7:51 CET on 02 November 2018 70 80 90 100 110 120 Oct Dec Feb Apr Jun Aug Oct Shipping OSEBX (Rebased) Target Share Company Cur Rec Price Price P/E 18e P/E 19e P/E 20e A. P. Møller Mærsk DKK BUY 10400 8364 nm 13.4 10.1 Avance Gas NOK HOLD 22.00 21.10 nm nm 11.2 BW LPG NOK HOLD 37.00 39.89 nm nm 33.0 D/S Norden DKK BUY 139.00 91.10 nm 24.6 8.4 DHT Holdings USD BUY 7.60 5.03 nm 56.7 5.2 Dorian LPG USD HOLD 8.50 7.95 nm nm nm Eagle Bulk Shipping USD BUY 6.30 4.99 37.5 10.6 4.7 Epic Gas NOK BUY 19.40 10.50 6.0 2.0 1.3 Euronav USD BUY 14.80 9.20 nm nm 9.7 Flex LNG NOK BUY 22.30 14.80 nm 24.4 7.0 Frontline NOK BUY 60.00 61.05 nm 18.4 6.4 GasLog USD BUY 19.90 20.46 31.4 20.7 10.3 Genco Shipping & Trading USD BUY 19.20 11.02 13.5 3.9 2.7 Golar LNG USD BUY 43.00 26.78 nm nm nm Golar LNG Partners USD SELL 11.10 14.11 17.6 27.6 16.4 Golden Ocean NOK BUY 95.00 63.25 9.9 5.2 4.0 Hunter Group ASA NOK BUY 5.30 3.92 nm nm 6.2 Höegh LNG Holdings NOK BUY 63.00 39.25 8.1 7.3 6.0 Höegh LNG Partners USD HOLD 19.10 17.81 9.7 11.6 11.9 MPC Container Ships NOK BUY 70.00 40.60 Odfjell NOK BUY 44.00 30.50 nm 12.5 5.3 Safe Bulkers USD BUY 3.80 2.53 9.8 3.7 2.7 Scorpio Tankers USD BUY 3.00 1.79 nm nm nm Stolt-Nielsen NOK BUY 172.0 113.4 7.6 4.7 4.3 Teekay Tankers USD BUY 2.00 1.11 nm 7.8 1.8 Wallenius Wilhelmsen ASA NOK BUY 49.00 28.90 13.2 6.2 5.0 Wilh. Wilhelmsen Holding NOK BUY 273.0 170.0 4.3 6.1 5.2 Source: DNB Markets ANALYSTS Nicolay Dyvik [email protected] +47 24 16 91 87 Jørgen Lian [email protected] +47 24 16 91 88 Mats Bye [email protected] +47 24 16 91 86 Please see the last two pages for important information. This research report was not produced in the US. Analysts employed by non-US affiliates are not registered/ qualified research analysts with FINRA in the United States.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IMO 2020 UPDATE

2,052 scrubbers so far The latest scrubber data from DNV GL show an accelerating increase in planned scrubber installations during 2019. The pre-2020 total of scrubber-fitted vessels now stands at 2,052, quickly closing in on our 2,300 forecast. Dry bulk has the majority of this month’s additions. The accelerating uptake for 2019 installation indicates still-available capacity in our view, and our estimate is looking increasingly conservative.

Latest DNV GL numbers show 2,052 installed by end-2019. After increasing its

forecasts for 2019 scrubber uptake by 22% last month, this month’s numbers show a

further 23% increase, to take scheduled scrubber uptake for end-2019 to 2,052.

DNB Markets’ 2,300 forecast starting to look conservative, as 502 scrubbers were

added to the pre-2020 orderbooks during the last month. This is up from the 282

increase last month, and we still have 14 months to go before the regulations kick in.

Dry bulk uptake growth accelerating 2.0x from last month. Dry bulk was

responsible for 51% (255) of the additions in the latest revisions, while 17% (87) was

for tankers and 9% (45) for container ships.

2019 installations balloon 52%, to 1,268, with only 105 booked for 2020. The

latest data show 1,268 scrubber installations are planned for 2019 (up 52%, or 432

units from 836 reported in October), while only 37 additions leave 2020 installations at

105. We see the accelerating growth in 2019 as a sign of still-available capacity, and

are likely to see continued additions ahead, though the minor uptick for 2020 could

indicate tighter pre-2020 scrubber availability.

Shipping vs OSEBX (12m)

Source: Factset

EQUITY RESEARCH 2 November 2018

Research report prepared by DNB Markets, a division of DNB Bank ASA

This report was completed and disseminated at 7:51 CET on 02 November 2018

70

80

90

100

110

120

Oct Dec Feb Apr Jun Aug Oct

Shipping OSEBX (Rebased)

Target Share

Company Cur Rec Price Price P/E 18e P/E 19e P/E 20e

A. P. Møller Mærsk DKK BUY 10400 8364 nm 13.4 10.1

Avance Gas NOK HOLD 22.00 21.10 nm nm 11.2

BW LPG NOK HOLD 37.00 39.89 nm nm 33.0

D/S Norden DKK BUY 139.00 91.10 nm 24.6 8.4

DHT Holdings USD BUY 7.60 5.03 nm 56.7 5.2

Dorian LPG USD HOLD 8.50 7.95 nm nm nm

Eagle Bulk Shipping USD BUY 6.30 4.99 37.5 10.6 4.7

Epic Gas NOK BUY 19.40 10.50 6.0 2.0 1.3

Euronav USD BUY 14.80 9.20 nm nm 9.7

Flex LNG NOK BUY 22.30 14.80 nm 24.4 7.0

Frontline NOK BUY 60.00 61.05 nm 18.4 6.4

GasLog USD BUY 19.90 20.46 31.4 20.7 10.3

Genco Shipping & Trading USD BUY 19.20 11.02 13.5 3.9 2.7

Golar LNG USD BUY 43.00 26.78 nm nm nm

Golar LNG Partners USD SELL 11.10 14.11 17.6 27.6 16.4

Golden Ocean NOK BUY 95.00 63.25 9.9 5.2 4.0

Hunter Group ASA NOK BUY 5.30 3.92 nm nm 6.2

Höegh LNG Holdings NOK BUY 63.00 39.25 8.1 7.3 6.0

Höegh LNG Partners USD HOLD 19.10 17.81 9.7 11.6 11.9

MPC Container Ships NOK BUY 70.00 40.60

Odfjell NOK BUY 44.00 30.50 nm 12.5 5.3

Safe Bulkers USD BUY 3.80 2.53 9.8 3.7 2.7

Scorpio Tankers USD BUY 3.00 1.79 nm nm nm

Stolt-Nielsen NOK BUY 172.0 113.4 7.6 4.7 4.3

Teekay Tankers USD BUY 2.00 1.11 nm 7.8 1.8

Wallenius Wilhelmsen ASA NOK BUY 49.00 28.90 13.2 6.2 5.0

Wilh. Wilhelmsen Holding NOK BUY 273.0 170.0 4.3 6.1 5.2

Source: DNB Markets

ANALYSTS

Nicolay Dyvik

+47 24 16 91 87

Jørgen Lian

+47 24 16 91 88

Mats Bye

+47 24 16 91 86

Please see the last two pages for important information. This research report was not produced in the US.Analysts employed by non-USaffiliates are not registered/qualified research analysts with FINRA in the United States.

DNB Markets

02 November 2018

2

502 scrubbers added to DNV GL’s end-2019 forecast DNV GL’s updated scrubber uptake data shows a 502 (23%) increase MOM (which is up from

the 282, or 22%, revision for October) in the number of scrubbers scheduled to be fitted by end-

2019. This lifts the total to 2,052 from 1,268 in our initial report on scrubber uptake from 13

September and the 1,550 reported a month ago. This compares to DNB Market’s 2,300

estimate, which now seems rather conservative given that more than 500 scrubbers were added

in a month and we still have 14 months to go, despite reports that the main scrubber producers

are nearing full order books for pre-2020 delivery.

DNV GL’s current number of vessels with scrubbers at year-end and by segment

(including newbuilds)

Source: DNV GL (underlying data), DNB Markets (calculations)

Of all confirmed scrubber orders by end-2019, 76% (up from 71% in our 13 September report)

are scheduled to be installed in the three major shipping segments: dry bulk, tankers, and

container. A still-growing portion of all scrubber orders are confirmed retrofits (now 72%, up

from 62%).

DNV GL’s current number of newbuilds and retrofits (year-end, including newbuilds)

Source: DNV GL (underlying data), DNB Markets (calculations)

DNV GL’s latest forecasts show an accelerating increase in scrubber uptake, but still leave

some upside to our estimate of 2,300 scrubbers installed by early 2020. While 98% of

October revisions were additional scrubbers in the three main segments (dry bulk, tankers,

and container), the November revisions were down to 77% within these segments (12%, or

59 scrubbers were added in the Cruise & Ferry segment).

786 808 811

161

513 537 537

120

270 288 288

103 149 165

200

248289 304

96

118118 118

97234

306378

784

20522157 2175

0

500

1000

1500

2000

2500

2014 2015 2016 2017 2018 2019 2020 2021

Vessels

with s

cru

bber

(num

ber)

Bulk Tankers Container Gas Cruise&Ferry RoRo&PCC General cargo Other

18 49 73

123

283 5

92

614

618

79 185

233

255

501

1460

1543

1557

97234

306378

784

20522157 2175

19% 18% 17%

24%

54%

76% 76% 75%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

500

1000

1500

2000

2500

2014 2015 2016 2017 2018 2019 2020 2021

Share

of

majo

r segm

ents

(dry

bulk

, ta

nkers

and c

onta

iner)

Vessels

with s

cru

bber

(num

ber)

Newbuildings Retrofits Dry bulk, tankers and container's share of scrubber uptake

DNB Markets

02 November 2018

3

DNV GL scrubber uptake and remaining upside to DNB

Markets’ early 2020 scrubber estimate by segment

Revisions to DNV GL’s scrubber uptake by end-2019 per

segment since our 13 September report

Source: DNV GL (historical data), DNB Markets (forecasts) Source: DNV GL (underlying data), DNB Markets (calculations)

Since our September report, increases to DNV GL’s data have been disproportionately high

for tankers compared to our forecasts while for dry bulk and container, aggregate growth has

been in line with expectations after the latest revisions.

Tanker additions were roughly flat MOM (0.94x) at 87 additions, dry bulk accelerated rapidly

and nearly doubled the monthly additions to 255 (1.96x), and container growth slowed to 45

additions (0.79x). To reach our forecasts we need just 16 more scrubbers in tankers, 186

more in dry bulk, and 85 more in container.

In scrubber installation capacity, the order book currently indicates 1,268 scrubbers will be

installed during 2019. This is a large increase (52%) from last month’s outlook for 836 after an

addition of 432 for 2019, and contrary to the previous revision showing slowing growth for

2019. However, we are starting to see a marginal increase in uptake for 2020 as well, which

could be an indication that MOM increases for pre-2020 could be slowing in future revisions,

probably due to capacity constraints starting to take effect.

DNV GL’s annual scrubber installations DNV GL’s revision to annual scrubber installations

Source: DNV GL (underlying data), DNB Markets (calculations) Source: DNV GL (underlying data), DNB Markets (calculations)

513

786

270 248118 58 59

16

186

85

8

529

972

355

221126

54 45

0

200

400

600

800

1,000

1,200

Tan

kers

Dry

bu

lk

Co

nta

ine

r

Cru

ise

&F

err

y

RO

RO

&P

CC

Ga

s

Ge

ne

ral carg

o&

Oth

er

Nu

mber

of

scru

bbers

Latest DNV GL data Remaining to meet DNB's 2020 forecast

184

364

85

52

17

14

14

200

550

170

25

25

10

0

0

100

200

300

400

500

600

Ta

nke

rs

Dry

bu

lk

Co

nta

ine

r

Cru

ise

&F

err

y

RO

RO

&P

CC

Ga

s

Ge

ne

ral carg

o&

Oth

er

Re

vis

ions f

rom

our

13 S

epte

mber

report

Additions since 13 September DNB Market's forecast for early-2020

65

249

388

46

4

69

286

616

48

4

70

348

836

68

4

72

406

1,2

68

105

18

0

200

400

600

800

1,000

1,200

1,400

2017 2018 2019 2020 2021

Nu

mb

er

of

scru

bb

ers

in

sta

lled

pe

r ye

ar

August '18 September '18 October '18 November '18

4

37

228

2 01

62

220

20

02

58

432

37

14

0

50

100

150

200

250

300

350

400

450

500

2017 2018 2019 2020 2021

Re

vis

inos t

o s

cru

bberin

sta

llatio

ns p

er

year

September '18 October '18 November '18

DNB Markets

02 November 2018

4

Monthly revisions to DNV GL’s scrubber uptake data

DNV GL total scrubber uptake revisions DNV GL total scrubber installations per year

Source: DNV GL (underlying data), DNB Markets (calculations) Source: DNV GL (underlying data), DNB Markets (calculations)

Revisions to total scrubber uptake by end-2019 Revisions to total scrubber uptake by end-2020

Source: DNV GL (underlying data), DNB Markets (calculations) Source: DNV GL (underlying data), DNB Markets (calculations)

End-2019 uptake revisions by segment Share of end-2019 revisions by segment

Source: DNV GL (underlying data), DNB Markets (calculations) Source: DNV GL (underlying data), DNB Markets (calculations)

291

356

605

993

1,0

39

294

363

649

1,2

65

1,3

13

296

366

714

1,5

50

1,6

18

306

378

784

2,0

52

2,1

57

0

500

1,000

1,500

2,000

2,500

2016 2017 2018 2019 2020

Scru

bbers

in

sta

lled b

y end o

f ye

ar

August '18 September '18 October '18 November '18

76

65

249

388

4664

69

286

616

4865

70

348

836

68

72

72

406

1,2

68

105

0

200

400

600

800

1,000

1,200

1,400

2016 2017 2018 2019 2020

Nu

mber

of

scru

bbers

in

sta

lled p

er

year

August '18 September '18 October '18 November '18

993

1,2

65

1,5

50 2,0

52272

285

502

0

500

1,000

1,500

2,000

2,500

Nu

mber

of

scru

bbers

by

end 2

019

1,0

39

1,3

13

1,6

18 2

,157274

305

539

0

500

1,000

1,500

2,000

2,500

Nu

mber

of

scru

bbers

by

end 2

020

130

255

93

87

57

45

59

285

502

0

100

200

300

400

500

600

Oct'18 Nov'18

End-2

019 r

evis

ions

Bulk Tankers Container Gas

Cruise&Ferry RoRo&PCC General cargo Other

46%51%

33% 17%

20%

9%

12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Oct'18 Nov'18

Share

of

end

-2019 r

evis

ions

Bulk Tankers Container Gas

Cruise&Ferry RoRo&PCC General cargo Other

DNB Markets

02 November 2018

5

DNV GL dry bulk scrubber uptake revisions DNV GL dry bulk scrubber installations per year

Source: DNV GL (underlying data), DNB Markets (calculations) Source: DNV GL (underlying data), DNB Markets (calculations)

DNV GL tankers scrubber uptake revisions DNV GL tankers scrubber installations per year

Source: DNV GL (underlying data), DNB Markets (calculations) Source: DNV GL (underlying data), DNB Markets (calculations)

DNV GL container scrubber uptake revisions DNV GL container scrubber uptake revisions

Source: DNV GL (underlying data), DNB Markets (calculations) Source: DNV GL (underlying data), DNB Markets (calculations)

16 27 7

6

278

289

12 23

84

401

419

16 27

128

531

549

17 26

140

786

808

0

100

200

300

400

500

600

700

800

900

2016 2017 2018 2019 2020

Scru

bbers

in

sta

lled b

y end o

f ye

ar

August '18 September '18 October '18 November '18

3 11 4

9

202

11

3 11

61

317

18

3 11

101

403

18

3 9

114

646

22

0

100

200

300

400

500

600

700

2016 2017 2018 2019 2020

Nu

mber

of

scru

bbers

in

sta

lled p

er

year

August '18 September '18 October '18 November '18

17 29

113

220

225

18 35

140

333

338

18 35

152

426

439

15 33

161

513 537

0

100

200

300

400

500

600

2016 2017 2018 2019 2020

Scru

bbers

in

sta

lled b

y end o

f ye

ar

August '18 September '18 October '18 November '18

9 12

84

107

55

17

105

193

55

17

117

274

13

5

18

128

352

24

0

50

100

150

200

250

300

350

400

2016 2017 2018 2019 2020

Nu

mber

of

scru

bbers

in

sta

lled p

er

year

August '18 September '18 October '18 November '18

18 3

1

111

148 1

70

13 2

4

108

168 186

15 2

6

116

225 243

19 3

0

120

270 288

0

50

100

150

200

250

300

350

2016 2017 2018 2019 2020

Scru

bbers

in

sta

lled b

y end o

f ye

ar

August '18 September '18 October '18 November '18

5

13

80

37

22

2

11

84

60

18

2

11

90

109

18

2

11

90

150

18

0

20

40

60

80

100

120

140

160

2016 2017 2018 2019 2020

Nu

mber

of

scru

bbers

in

sta

lled p

er

year

August '18 September '18 October '18 November '18

DNB Markets

02 November 2018

6

Important Information This report has been prepared by DNB Markets, a division of DNB Bank ASA. DNB Bank ASA is a part of the DNB

Group. This report is based on information obtained from public sources that DNB Markets believes to be reliable but

which DNB Markets has not independently verified, and DNB Markets makes no guarantee, representation or warranty

as to its accuracy or completeness. This report does not, and does not attempt to, contain everything material which

there is to be said about the Company. Any opinions expressed herein reflect DNB Markets’ judgement at the time the

report was prepared and are subject to change without notice.

Any use of non-DNB logos in this report is solely for the purpose of assisting in identifying the relevant issuer. DNB is not

affiliated with any such issuer.

This report is for clients only, and not for publication, and has been prepared for information purposes only by DNB Markets, a division of DNB Bank ASA. This report is the property of DNB Markets. DNB Markets retains all intellectual property rights (including, but not limited to, copyright) relating to the report. Sell-side investment firms are not allowed any commercial use (including, but not limited to, reproduction and redistribution) of the report contents, either partially or in full, without DNB Markets’ explicit and prior written consent. However, buy-side investment firms may use the report when making investment decisions, and may also base investment advice given to clients on the report. Such use is dependent on the buy-side investment firm citing DNB Markets as the source.

Price targets are based on a combination of several valuation methods such as discounted cash flow, pricing based on earnings multiples, multiple on book value, net asset value and peer comparison. Substantial material sources for coverage of this company include historical financial figures and communication with the company, and relevant third party information. If you would like further information on the valuation, methodology or underlying assumptions used in this note, please contact the analyst (contact details on front page).

Recommendation structure and risk classification

DNB Markets recommendations are based on absolute performance:

Buy - indicates an expected return greater than 10% within 12 months

Hold - indicates an expected return between 0 and 10% within 12 months

Sell - indicates an expected negative return within 12 months

The return-requirement bands above may be applied with some degree of flexibility depending on the liquidity and volatility characteristics of the individual share.

High risk - Volatility over 40 percent.

Medium risk - Volatility from 25 percent to 40 percent.

Low risk - Volatility under 25 percent.

Investing in any security is subject to substantial risk. Return on investment may vary greatly.

Careful consideration for possible financial distress should be accounted for before investing in any security.

Recommendation distribution and corporate clients for the last 12 months

Buy Hold Sell No_rec Total

Number 136 70 21 8 235

% of total 58% 30% 9% 3%

DNB Markets client 23% 10% 2% 1% 86

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

30

35

40

45

50

55

60

65

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Frontline (FRO NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

19-2-18H : 33.0

6-3-18 B : 42.0

29-5-18 B : 60.0

Current 6 months volatility rates this security as HIGH risk.

DNB Markets

02 November 2018

7

DNB Markets is market maker/liquidity provider for Odfjell. DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

28

30

32

34

36

38

40

42

44

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Odfjell (ODF NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

25-8-17B : 37.0

7-5-18 B : 44.0

14-5-18 B : 43.0

27-8-18 B : 44.0

Current 6 months volatility rates this security as MEDIUM risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 2000 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

90

100

110

120

130

140

150

160

170

180

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Stolt-Nielsen (SNI NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

5-2-18B : 143

10-4-18 B : 138

6-7-18 B : 172

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 77 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

8

160

180

200

220

240

260

280

300

320

340

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Wilh. Wilhelmsen Holding (WWI NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

13-11-17B : 323

14-5-18 B : 273

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

20

25

30

35

40

45

50

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Golar LNG (GLNG US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

13-9-17B : 33.0

23-4-18 B : 49.0

31-5-18 B : 39.0

5-9-18 B : 43.0

Current 6 months volatility rates this security as HIGH risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

9

7,000

8,000

9,000

10,000

11,000

12,000

13,000

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History A. P. Møller Mærsk (MAERSKB DC) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

20-2-18B : 12900

22-5-18 B : 11800

4-7-18 B : 10400

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

55

60

65

70

75

80

85

90

95

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Golden Ocean (GOGL NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

20-2-18B : 83.0

25-5-18 B : 84.0

31-5-18 B : 85.0

7-8-18 B : 88.0

20-8-18 B : 90.0

13-9-18 B : 95.0

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

10

7

8

9

10

11

12

13

14

15

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Euronav (EURN US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

26-1-18H : 9.00

6-3-18 B : 10.7

6-7-18 B : 12.5

10-8-18 B : 12.8

31-10-18 B : 14.8

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Eagle Bulk Shipping (EGLE US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

#N/A18-6-18 B : 7.10

14-8-18 B : 7.50

13-9-18 B : 6.30

Current 6 months volatility rates this security as HIGH risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

11

10

12

14

16

18

20

22

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Genco Shipping & Trading (GNK US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

13-2-18B : 16.8

4-5-18 B : 19.8

11-5-18 B : 20.6

7-8-18 B : 19.4

14-8-18 B : 19.6

13-9-18 B : 19.7

26-10-18 B : 19.2

Current 6 months volatility rates this security as HIGH risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

80

90

100

110

120

130

140

150

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History D/S Norden (DNORD DC) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

3-9-17B : 145

4-5-18 B : 135

7-8-18 B : 141

17-8-18 B : 137

13-9-18 B : 139

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

12

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

4.2

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Safe Bulkers (SB US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

16-2-18B : 4.10

7-8-18 B : 3.90

13-9-18 B : 3.80

Current 6 months volatility rates this security as HIGH risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months. DNB Markets has been lead or co-lead manager related to an Investment Banking assignment for the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 1600 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

25

30

35

40

45

50

55

60

65

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Wallenius Wilhelmsen ASA (WALWIL NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

19-2-18H : 65.0

9-5-18 H : 46.0

14-6-18 B : 51.0

10-8-18 B : 49.0

Current 6 months volatility rates this security as HIGH risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

13

35

40

45

50

55

60

65

70

75

80

85

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Höegh LNG Holdings (HLNG NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

15-2-18B : 84.0

1-3-18 B : 76.0 1-3-18 B : 76.0

25-5-18 B : 78.0

31-5-18 B : 67.0

3-8-18 B : 65.0

24-8-18 B : 63.0

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

11

12

13

14

15

16

17

18

19

20

21

22

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Golar LNG Partners (GMLP US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

13-9-17H : 21.0

5-9-18 S : 11.1

Current 6 months volatility rates this security as HIGH risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

14

1.5

2.0

2.5

3.0

3.5

4.0

4.5

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Scorpio Tankers (STNG US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

21-11-17H : 3.40

6-3-18 H : 2.40

25-4-18 B : 3.70

30-4-18 B : 4.00

29-10-18 B : 3.00

Current 6 months volatility rates this security as HIGH risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Teekay Tankers (TNK US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

24-11-17H : 1.50

6-3-18 B : 1.80

6-7-18 B : 2.00

Current 6 months volatility rates this security as HIGH risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

15

15

16

17

18

19

20

21

22

23

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

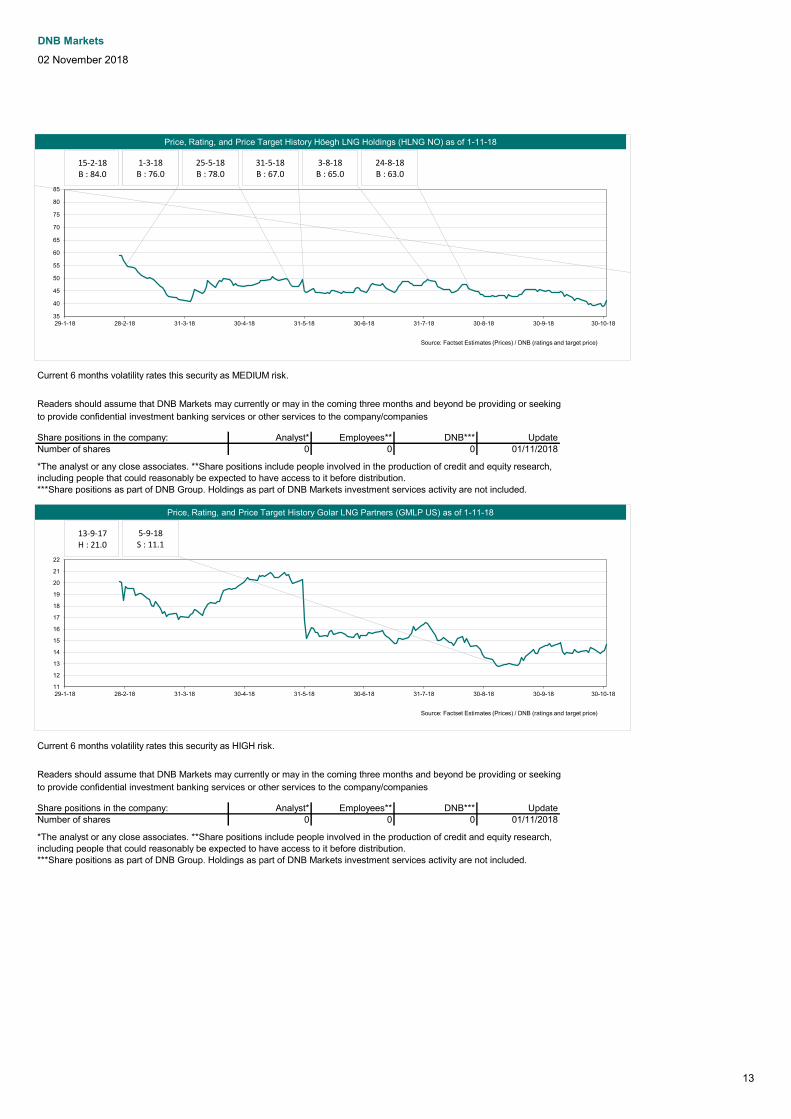

Price, Rating, and Price Target History GasLog (GLOG US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

21-2-18H : 18.9

30-4-18 H : 17.7

14-5-18 H : 18.2

5-9-18 B : 19.9

Current 6 months volatility rates this security as MEDIUM risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

16

18

20

22

24

26

28

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

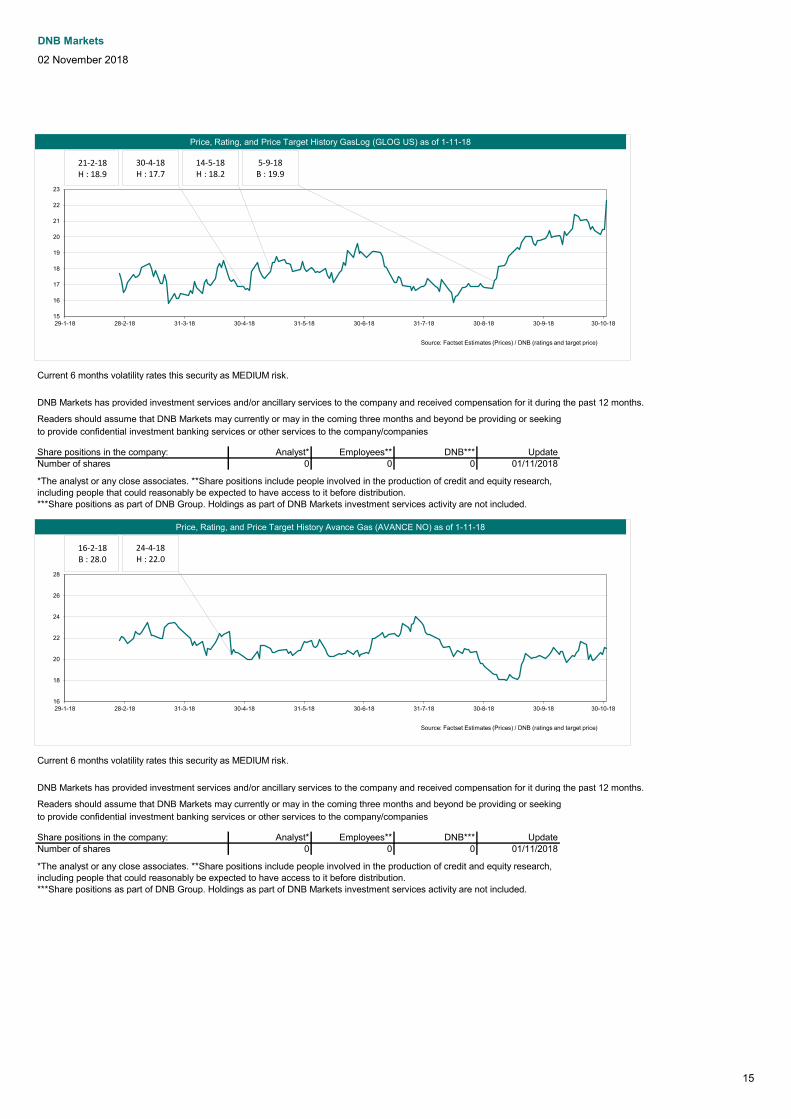

Price, Rating, and Price Target History Avance Gas (AVANCE NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

16-2-18B : 28.0

24-4-18 H : 22.0

Current 6 months volatility rates this security as MEDIUM risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

16

6.8

7.0

7.2

7.4

7.6

7.8

8.0

8.2

8.4

8.6

8.8

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Dorian LPG (LPG US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

23-2-18H : 8.20

29-10-18 H : 8.50

Current 6 months volatility rates this security as HIGH risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

28

30

32

34

36

38

40

42

44

46

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History BW LPG (BWLPG NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

13-2-18B : 44.0

2-3-18 B : 45.0 2-3-18 B : 45.0

24-4-18 H : 31.0

31-5-18 H : 34.0

9-8-18 H : 36.0

30-10-18 H : 37.0

Current 6 months volatility rates this security as HIGH risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

17

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History DHT Holdings (DHT US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

5-2-18H : 4.00

6-3-18 B : 5.20

11-5-18 B : 5.10

6-7-18 B : 6.30

1-11-18 B : 7.60

Current 6 months volatility rates this security as MEDIUM risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

6

8

10

12

14

16

18

20

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Epic Gas (EPICME NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

15-2-18B : 19.4

Current 6 months volatility rates this security as HIGH risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months. DNB Markets has been lead or co-lead manager related to an Investment Banking assignment for the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

18

10

12

14

16

18

20

22

24

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Flex LNG (FLNG NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

16-2-18B : 16.2

23-5-18 B : 16.6

5-9-18 B : 18.8

15-10-18 B : 22.3

Current 6 months volatility rates this security as MEDIUM risk.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 0 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

15

16

17

18

19

20

21

22

23

24

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Höegh LNG Partners (HMLP US) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

13-9-17B : 23.1

3-8-18 H : 19.1

Current 6 months volatility rates this security as LOW risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months. DNB Markets has been lead or co-lead manager related to an Investment Banking assignment for the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 500 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

DNB Markets

02 November 2018

19

Legal statement These materials constitute research as defined in section 9-27 (1) of the Norwegian Securities Trading Regulations (Norwegian: verdipapirforskriften), and are not investment advice as defined in section 2-4(1) of the Norwegian securities trading act (Norwegian verdipapirhandelloven). The analyst hereby certifies that (i) the views expressed in this report accurately reflect that research analyst’s personal views about the company and the securities that are the subject of this report, and (ii) no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in this report. DNB Markets employees, including research analysts, may receive compensation that is generated by overall firm profitability. Confidentiality rules and internal rules restricting the exchange of information between different parts of DNB Markets/DNB Bank ASA or the DNB Group are in place to prevent employees of DNB Markets who are preparing this report from utilizing or being aware of information available in the DNB Group that may be relevant to the recipients’ decisions. DNB Markets and the DNB Group have incorporated internal rules and regulations in order to avoid any potential conflicts of interest.

The Report has been prepared by DNB Markets, a division of DNB Bank ASA, a Norwegian bank organized under the laws of the Kingdom of Norway and under supervision by the Norwegian Financial Supervisory Authority, The Monetary Authority of Singapore, and on a limited basis by the Financial Conduct Authority and the Prudential Regulation Authority of the UK, and the Financial Supervisory Authority of Sweden. Details about the extent of our regulation by local authorities outside Norway are available from us on request. It is issued subject to the General Business Terms for DNB Markets and information about the terms is available at www.dnb.no. For requests regarding the General Business Terms of the Singapore Branch of DNB Bank ASA, please contact +65 6212 6144. Information about the DNB Group can be found at www.dnb.com. DNB Markets is a member of The Norwegian Securities Dealers Association, which has issued recommendations and market standards for securities companies. The Association's Internet address where the recommendations and market standards can be found is: www.vpff.no. This report is not an offer to buy or sell any security or other financial instrument or to participate in any investment strategy. No liability whatsoever is accepted for any direct or indirect (including consequential) loss or expense arising from the use of this report. Distribution of research reports is in certain jurisdictions restricted by law. Persons in possession of this report should seek further guidance regarding such restrictions before distributing this report. Please contact DNB Markets at 08940 (+47 915 08940) for further information and inquiries regarding this report, including an overview on all recommendations from DNB Markets over the last 12 Months according to Market Abuse Regulations.

Additional information for clients in Singapore

40

45

50

55

60

65

70

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History MPC Container Ships (MPCC NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

12-2-18B : 68.0

10-4-18 B : 66.0

1-6-18 B : 70.0

Current 6 months volatility rates this security as MEDIUM risk.

DNB Markets has provided investment services and/or ancillary services to the company and received compensation for it during the past 12 months. DNB Markets has been lead or co-lead manager related to an Investment Banking assignment for the company and received compensation for it during the past 12 months.

Readers should assume that DNB Markets may currently or may in the coming three months and beyond be providing or seeking

to provide confidential investment banking services or other services to the company/companies

Share positions in the company: Analyst* Employees** DNB*** Update

Number of shares 0 60000 0 01/11/2018

*The analyst or any close associates. **Share positions include people involved in the production of credit and equity research,

including people that could reasonably be expected to have access to it before distribution.

***Share positions as part of DNB Group. Holdings as part of DNB Markets investment services activity are not included.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

29-1-18 28-2-18 31-3-18 30-4-18 31-5-18 30-6-18 31-7-18 30-8-18 30-9-18 30-10-18

Price, Rating, and Price Target History Hunter Group ASA (HUNT NO) as of 1-11-18

Source: Factset Estimates (Prices) / DNB (ratings and target price)

#N/A3-10-18 B : 5.30

Current 6 months volatility rates this security as HIGH risk.

DNB Markets

02 November 2018

20

The report has been distributed by the Singapore Branch of DNB Bank ASA. It is intended for general circulation and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of any product referred to in the report, taking into account your specific financial objectives, financial situation or particular needs before making a commitment to purchase any such product. You have received a copy of the report because you have been classified either as an accredited investor, an expert investor or as an institutional investor, as these terms have been defined under Singapore's Financial Advisers Act (Cap. 110) ("FAA") and/or the Financial Advisers Regulations ("FAR"). The Singapore Branch of DNB Bank ASA is a financial adviser exempt from licensing under the FAA but is otherwise subject to the legal requirements of the FAA and of the FAR. By virtue of your status as an accredited investor or as an expert investor, the Singapore Branch of DNB Bank ASA is, in respect of certain of its dealings with you or services rendered to you, exempt from having to comply with certain regulatory requirements of the FAA and FAR, including without limitation, sections 25, 27 and 36 of the FAA. Section 25 of the FAA requires a financial adviser to disclose material information concerning designated investment products which are recommended by the financial adviser to you as the client. Section 27 of the FAA requires a financial adviser to have a reasonable basis for making investment recommendations to you as the client. Section 36 of the FAA requires a financial adviser to include, within any circular or written communications in which he makes recommendations concerning securities, a statement of the nature of any interest which the financial adviser (and any person connected or associated with the financial adviser) might have in the securities. Please contact the Singapore branch of DNB Bank ASA at +65 6212 6144 in respect of any matters arising from, or in connection with, the report. The report is intended for and is to be circulated only to persons who are classified as an accredited investor, an expert investor or an institutional investor. If you are not an accredited investor, an expert investor or an institutional investor, please contact the Singapore Branch of DNB Bank ASA at +65 6212 6144. We, the DNB group, our associates, officers and/or employees may have interests in any products referred to in the report by acting in various roles including as distributor, holder of principal positions, adviser or lender. We, the DNB group, our associates, officers and/or employees may receive fees, brokerage or commissions for acting in those capacities. In addition, we, the DNB group, our associates, officers and/or employees may buy or sell products as principal or agent and may effect transactions which are not consistent with the information set out in the report.

In the United States Each research analyst named on the front page of this research report, or at the beginning of any subsection hereof, hereby certifies that (i) the views expressed in this report accurately reflect that research analyst’s personal views about the company and the securities that are the subject of this report; and (ii) no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in this report.

The research analyst(s) named on this report are foreign research analysts as defined by FINRA Rule 1050. The only affiliate contributing to this research report is DNB Bank through its DNB Markets division (“DNB Markets/DNB Bank”); the foreign research analysts employed by DNB Markets/DNB Bank are named on the first page; the foreign research analysts are not registered/qualified as research analysts with FINRA; foreign research analysts are not associated persons of DNB Markets, Inc. and therefore are not subject to the restrictions set forth in FINRA Rules 2241 and 2242 regarding restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

This is a Third Party Research Report as defined by FINRA Rules 2241 and 2242. Any material conflict of interest that can reasonably be expected to have influenced the choice of DNB Markets/DNB Bank as a research provider or the subject company of a DNB Markets/DNB Bank research report, including the disclosures required by FINRA Rules 2241 and 2242 can be found above.

This report is being furnished solely to Major U.S. Institutional Investors within the meaning of Rule 15a-6 under the U.S. Securities Exchange Act of 1934 and to such other U.S. Institutional Investors as DNB Markets, Inc. may determine. Distribution to non-Major U.S. Institutional Investors will be made only by DNB Markets, Inc., a separately incorporated subsidiary of DNB Bank that is a U.S. broker-dealer and a member of the Financial Industry Regulatory Authority (“FINRA”) and the Securities Investor Protection Corporation (“SIPC”).

Any U.S. recipient of this report seeking to obtain additional information or to effect any transaction in any security discussed herein or any related instrument or investment should contact DNB Markets, Inc., 200 Park Avenue, New York,NY 10166-0396, telephone number +1 212-551-9800.

In Canada The Report has been distributed in reliance on the International Dealer Exemption pursuant to NI 31-103 subsection 8.18(2) and subsection 8.18(4)(b). Please be advised that: 1. DNB Bank ASA (DNB Markets) and DNB Markets, Inc. are not registered as a dealer in the local jurisdiction to make the trade. We provide our services in Canada as an exempt international dealer. 2. The jurisdiction of DNB Bank ASA (DNB Markets) and DNB Markets, Inc.'s head office is Norway. 3. There may be difficulty enforcing legal rights against DNB Bank ASA (DNB Markets) and DNB Markets, Inc. because all or substantially all of their assets may be situated outside of Canada. 4. The name and address of the agent for service of process for DNB Bank ASA (DNB Markets) and DNB Markets, Inc. in the local jurisdiction is: Alberta: Blake, Cassels & Graydon LLP, 855 - 2nd Street S.W., Suite 3500, Bankers Hall East Tower, Calgary, AB T2P 4J8. British Columbia: Blakes Vancouver Services Inc., 595 Burrard Street, P.O. Box 49314, Suite 2600, Three Bentall Centre, Vancouver, BC V7X 1L3. Manitoba: Aikins, MacAulay & Thorvaldson LLP, 30th Floor, Commodity Exchange Tower, 360 Main Street, Winnipeg, MB R3C 4G1. New Brunswick: Stewart McKelvey, Suite 1000, Brunswick House, 44 Chipman Hill, PO Box 7289, Station A, Saint John, NB E2L 2A9. Newfoundland and Labrador: Stewart McKelvey, Suite 1100, Cabot Place, 100 New Gower Street, P.O. Box 5038, St. John's, NL A1C 5V3. Nova Scotia: Stewart McKelvey, Purdy's Wharf Tower One, 1959 Upper Water Street, Suite 900, P.O. Box 997, Halifax, NS B3J 2X2. Northwest Territories: Gerald Stang, Suite 201, 5120-49 Street, Yellowknife, NT X1A 1P8. Nunavut: Field LLP, P.O. Box 1779, Building 1088C, Iqaluit, NU X0A 0H0. Ontario: Blakes Extra-Provincial Services Inc., Suite 4000, 199 Bay Street, Toronto, ON M5L 1A9. Prince Edward Island: Stewart McKelvey, 65 Grafton Street, Charlottetown, PE C1A 1K8. Québec: Services Blakes Québec Inc., 600 de Maisonneuve Boulevard Ouest, Suite 2200, Tour KPMG, Montréal, QC H3A 3J2. Saskatchewan: MacPherson, Leslie & Tyerman LLP, 1500 Continental Bank Building, 1874 Scarth Street, Regina, SK S4P 4E9. Yukon: Grant Macdonald, Macdonald & Company, Suite 200, Financial Plaza, 204 Lambert Street, Whitehorse, YK Y1A 3T2.

In Brazil The analyst or any close associates do not hold nor do they have any direct/indirect involvement in the acquisition, sale, or intermediation of the securities discussed herein. Any financial interests, not disclosed above, that the analyst or any close associates holds in the issuer discussed in the report is limited to investment funds that do not mainly invest in the issuer or industry discussed in the report and the management of which these persons cannot influence.

Related Documents

![#CiveItUp LPG (LPG a) IOCL Cl / BPCL D / HPCL C] LPG àà àa … · · 2018-02-28iocl cl / bpcl d / hpcl c] lpg àà àa-r/àkft lpg àž lpg t:- lpg dgcc (poi) lpg 17 lpg id"](https://static.cupdf.com/doc/110x72/5ae5ebd07f8b9acc268cac07/civeitup-lpg-lpg-a-iocl-cl-bpcl-d-hpcl-c-lpg-a-cl-bpcl-d-hpcl-c.jpg)