The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. Presenting a live 90-minute webinar with interactive Q&A Buy-Sell Agreements for Corporations and LLCs: Drafting Stock Redemption, Cross-Purchase and Mixed Agreements Navigating Complex Corporate, Tax, Estate Planning and Insurance Law Issues When Planning for a Business Transition Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific WEDNESDAY, JULY 12, 2017 Brian E. Hammell, Esq., Sullivan & Worcester, Boston Martin B. Robins, Partner, FisherBroyles, Chicago

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Buy-Sell Agreements for Corporations and LLCs:

Drafting Stock Redemption, Cross-Purchase

and Mixed Agreements Navigating Complex Corporate, Tax, Estate Planning and Insurance

Law Issues When Planning for a Business Transition

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JULY 12, 2017

Brian E. Hammell, Esq., Sullivan & Worcester, Boston

Martin B. Robins, Partner, FisherBroyles, Chicago

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-888-450-9970 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

6

7

8

9

10

11

12

13

14

15

16

17

• Please don’t hesitate to reach out after this program

• Martin B. Robins of FisherBroyles LLP:

847 277 2580 or [email protected]

www.fisherbroyles.com

18

Buy-Sell Agreements for Corporations and LLCs: Tax Issues Brian E. Hammell [email protected] (617) 338-2462

Redemption vs. Cross-Purchase

Redemption

› Agreement between entity and its owners

› Company agrees to purchase shares/interests upon certain triggering events

Cross-Purchase

› Agreement among owners of the entity

› Other owner(s) agree to purchase shares/interests upon certain triggering events

20 © 2017 Sullivan & Worcester LLP

Redemption vs. Cross-Purchase

Hypothetical

› Corporation with two shareholders

› Value of the Company = $2,000,000

› Shareholder A's Basis = $10,000

› Shareholder B's Basis = $10,000

21 © 2017 Sullivan & Worcester LLP

Redemption vs. Cross-Purchase

Lifetime Transfer – Tax Consequences to the Transferor

› Shareholder A shares purchased for $1,000,000

› Gain on transfer = $990,000

Amount realized ($1,000,000) minus basis ($10,000)

Capital gain (generally)

Federal Income Tax = $198,000 (assuming 20% long-term capital gains rate)

22 © 2017 Sullivan & Worcester LLP

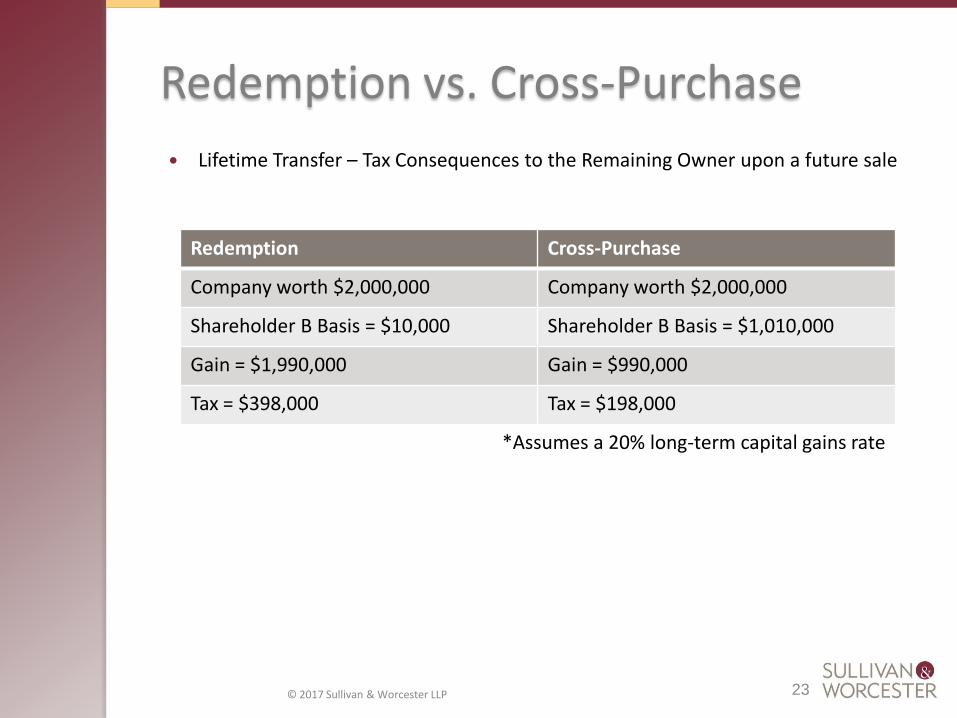

Redemption vs. Cross-Purchase

Lifetime Transfer – Tax Consequences to the Remaining Owner upon a future sale

23 © 2017 Sullivan & Worcester LLP

Redemption Cross-Purchase

Company worth $2,000,000 Company worth $2,000,000

Shareholder B Basis = $10,000 Shareholder B Basis = $1,010,000

Gain = $1,990,000 Gain = $990,000

Tax = $398,000 Tax = $198,000

*Assumes a 20% long-term capital gains rate

Deemed Dividend in Case of Redemption

The above example presumes that the redemption is treated as a sale or exchange under Section 1001 of the Code

› This is the general result for a complete termination of the retiring owner's interest

However, a potential trap exists under Section 302(b) of the Code

› A redemption payment to a retiring shareholder is treated as a distribution to the retiring shareholder with respect to his or her shares (and not in exchange for the shares) if the redemption does not satisfy any of the Section 302(b) tests (e.g., the retiring shareholder continues to own too many shares, actually or by attribution, after the redemption)

› Family attribution rules under Section 318 apply

24 © 2017 Sullivan & Worcester LLP

Deemed Dividend in Case of Redemption

Family Attribution Example

› Father owns 60% of stock in corporation

› Son owns 30%

› Mother owns 10%

› Father's stock is redeemed by the corporation

› Son and Mother's stock is attributed to Father, thus redemption is not a complete redemption and proceeds may be taxed as a dividend

25 © 2017 Sullivan & Worcester LLP

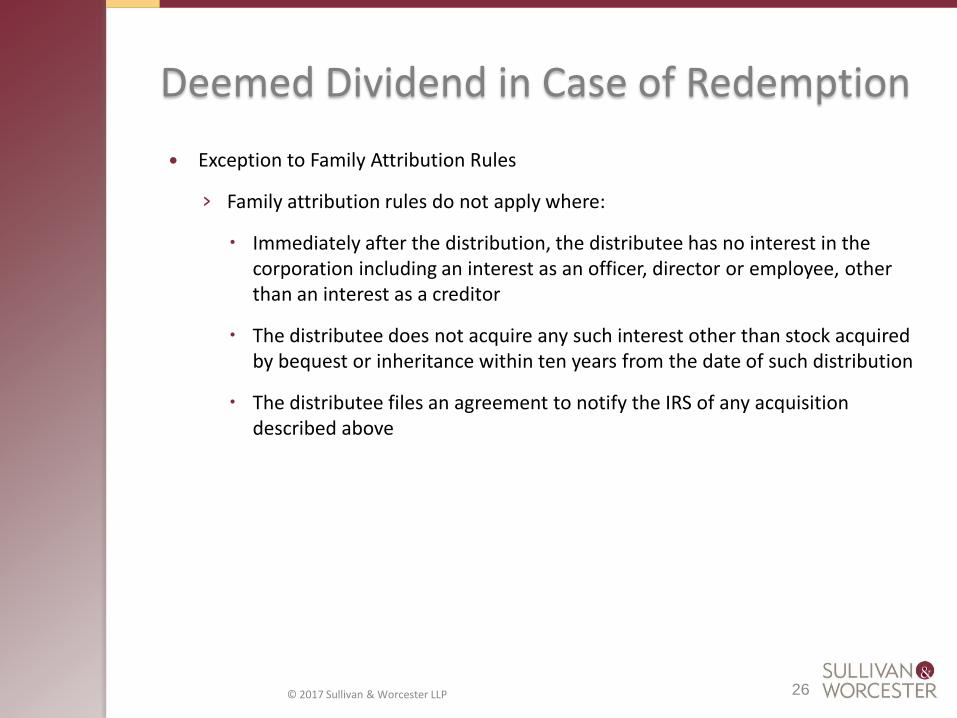

Deemed Dividend in Case of Redemption

Exception to Family Attribution Rules

› Family attribution rules do not apply where:

Immediately after the distribution, the distributee has no interest in the corporation including an interest as an officer, director or employee, other than an interest as a creditor

The distributee does not acquire any such interest other than stock acquired by bequest or inheritance within ten years from the date of such distribution

The distributee files an agreement to notify the IRS of any acquisition described above

26 © 2017 Sullivan & Worcester LLP

Insurance Funded Buy-Sell Agreements

Redemption Agreements

› Entity buys insurance on the lives of its shareholder

Entity is the owner and the beneficiary

› At death, the entity receives life insurance proceeds

› Proceeds are used to purchase shares/interests of the deceased owner

27 © 2017 Sullivan & Worcester LLP

Insurance Funded Buy-Sell Agreements

Issues Related to Insurance Owned by the Entity

› Premiums are non-deductible – Section 264(a)(1)

› Proceeds are income tax free – Section 101(a)(1)

Exception for a C Corporation which is subject to the Alternative Minimum Tax

› Proceeds are not includable in the Estate of the Decedent – Treas. Reg. 20.2042-1(c)(6)

28 © 2017 Sullivan & Worcester LLP

Insurance Funded Buy-Sell Agreements

Issues Related to Insurance Owned by the Entity

› COLI Best Practices Act

› Section 101(j)

› Applies to employer-owned polices issued after August 17, 2006 and previously issued policies in the event of material change

› IRS Form 8925: Provides notice of (a) number of policies held and (b) the total face amount of said policies

› Death benefits of employer-owned policies will generally not be taxable if:

29 © 2017 Sullivan & Worcester LLP

Employer gives employee written NOTICE and gets written CONSENT from

employee before policy is issued

AND

Insured employee fits SPECIFIED EXCEPTIONS

OR

Death benefits fit SPECIFIED

EXCEPTIONS

Insurance Funded Buy-Sell Agreements

Cross-Purchase Agreement

› Each owner purchases life insurance on the lives of each other owner

› Shareholders/members are owners and beneficiaries of the policy

› At death, surviving owner(s) receive life insurance proceeds from policy insuring life of deceased owner

› Surviving owners buy shares/interests from estate of deceased shareholder

30 © 2017 Sullivan & Worcester LLP

Insurance Funded Buy-Sell Agreements

Cross-Purchase Agreement

› Premiums must be paid by the owners and not the entity

Potential equity problem due to cost differences in underwriting

Payments from company are regarded as taxable compensation or distribution of S corporation profits

Split dollar still an option to consider

› Premiums are non-deductible – Section 264

› Proceeds are income tax free

› Purchase of interests increases cost basis of surviving owners, reducing capital gains at time of future sale

31 © 2017 Sullivan & Worcester LLP

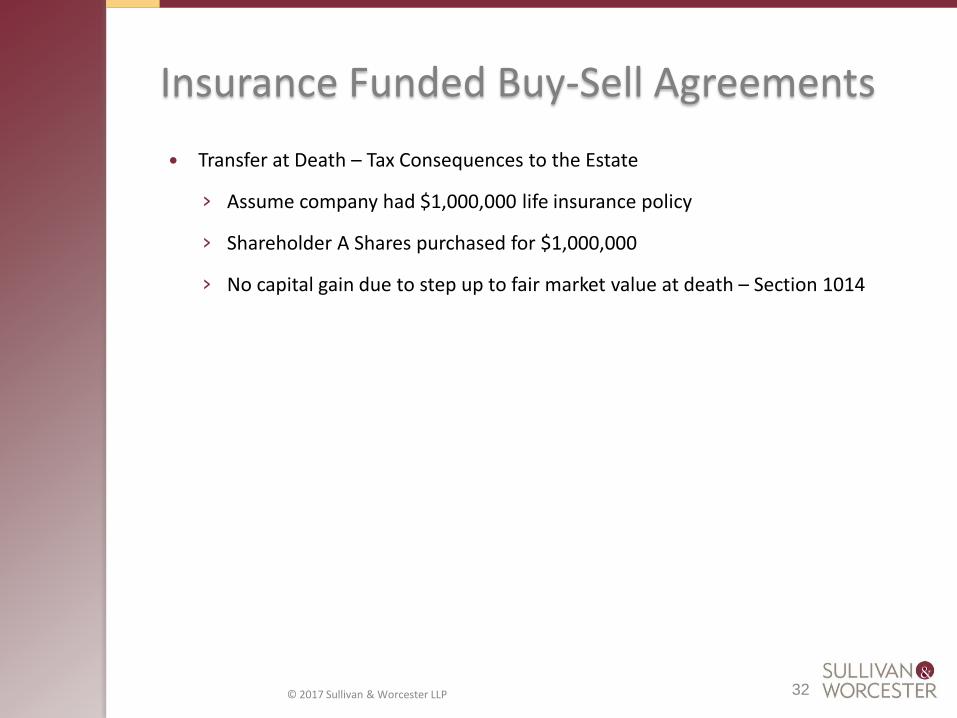

Insurance Funded Buy-Sell Agreements

Transfer at Death – Tax Consequences to the Estate

› Assume company had $1,000,000 life insurance policy

› Shareholder A Shares purchased for $1,000,000

› No capital gain due to step up to fair market value at death – Section 1014

32 © 2017 Sullivan & Worcester LLP

Insurance Funded Buy-Sell Agreements

Lifetime Transfer – Tax Consequences to the Remaining Owner upon a future sale

33 © 2017 Sullivan & Worcester LLP

Redemption Cross-Purchase

Company worth $2,000,000 Company worth $2,000,000

Shareholder B Basis = $10,000 Shareholder B Basis = $1,010,000

Gain = $1,990,000 Gain = $990,000

Tax = $398,000 Tax = $198,000

*Assumes a 20% long-term capital gains rate

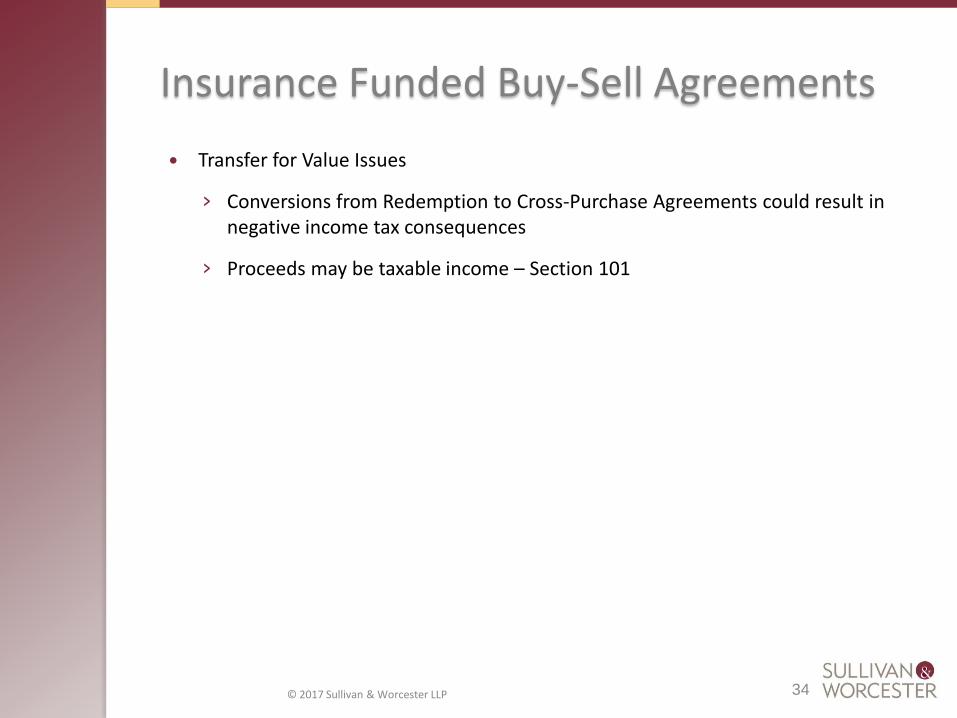

Insurance Funded Buy-Sell Agreements

Transfer for Value Issues

› Conversions from Redemption to Cross-Purchase Agreements could result in negative income tax consequences

› Proceeds may be taxable income – Section 101

34 © 2017 Sullivan & Worcester LLP

Fixing the Value of the Estate

Special Valuation Rules – Section 2703

Buy-Sell Agreement must satisfy the following rules:

› Be a bona fide business arrangement – Section 2703(b)(1)

› Not be a device to transfer business interest to family members for less than full and adequate consideration – Section 2703(b)(2)

› Be comparable to similar arrangements entered into by unrelated parties bargaining at arm's length – Section 2703(b)(3)

35 © 2017 Sullivan & Worcester LLP

Fixing the Value of the Estate

Cannot fix price between family members

Bottom Line: Purchase price needs to be Fair Market Value or based upon a formula which approximates Fair Market Value

Whipsaw Potential

› State law will likely declare a sale for less than Fair Market Value to be binding on the parties

36 © 2017 Sullivan & Worcester LLP

Other Drafting Points

Transfer restrictions to avoid adverse tax consequences

› e.g., prohibit transfers of S corporation stock to ineligible S corporation shareholders

Purchase price allocation for S corporations and partnerships

Tax indemnification obligations

› Impact of new partnership audit procedures

Deferred compensation arrangements

37 © 2017 Sullivan & Worcester LLP

Buy-Sell Agreements for Corporations and LLCs: Tax Issues Brian E. Hammell [email protected] (617) 338-2462

Related Documents