34Centrum Equity Research is available on Bloomberg, Thomson Reuters and FactSet Well casted at an inflection point We initiate coverage on Kirloskar Ferrous (KFIL) with a Buy and TP of Rs155 (56% upside). KFIL features i) a well invested asset base with spare capacity of 50%/25% in Castings/Pig Iron, ii) increasing share of high-margin casting business, iii) cost efficiencies from upcoming low-payback projects, iv) an enviable track record of converting cash profits to cash flows (5Y/10Y AOCF/CP ratio of 1x/0.9x) and v) strong earnings growth led by higher volumes and operating leverage, buttressed by a low D/E of 0.3x. Exciting future growth prospects await KFIL’s castings business which boasts of i) a strong product profile and customer relationships, ii) sustainable competitive strengths and iii) satisfactory demand visibility. We expect an impressive EBITDA/PAT CAGR of 28%/29% during FY17-20E driven by castings volume CAGR of 19% coupled with cost efficiencies. Finally, we believe that it merits rerating based on an attractive cash flow yield of 11.4%/15.9% (FY19E/20E). Hard yards covered in castings, strong growth underway: KFIL has already completed the augmentation of the value-added business of castings in the past few years and has invested heavily in i) increasing capacity by 50% to ~133ktpa, ii) adding machining facilities which fetch superior margins, iii) innovation and R&D to reduce new product development cycle time from eight months to two months – a game changer achievement and iv) acquiring several marquee customers across various segments. With its castings business having i) sustainable competitive strengths in a fragmented industry, ii) servicing steadily growing sectors like auto, tractor and diesel engines and iii) having well invested asset base with 50% spare capacity, KFIL is set to achieve a quantum leap in its castings volumes/turnover with CAGR of 19%/21% over FY17-20E and increase castings share in overall turnover to 51% by FY20E (from ~44% in FY18E). Pig iron business being made robust with meaningful cost improvement projects: KFIL has taken several steps to reduce its foundry grade pig iron business’ vulnerability to the vagaries of commodity cycles (which too have become shorter and erratic in the recent past). Cost benefits are likely to accrue from H2FY18 from steps already implemented, such as i) BF-1 upgradation in FY17 and ii) coke sourcing through conversion arrangement at domestic third-party locations vs. imports. Big ticket cost improvement projects like i) installation of PCI system to replace ~80kgs of coke with low cost coal and ii) setting up of 200ktpa coke oven with 15 MW WHR CPP are likely soon and will improve the cost metrics of PI business materially from FY20E. We expect profitability of pig iron business to improve sharply, led by i) cost savings from low-payback projects, ii) higher volumes and iii) better spreads. Splendid combo of consistent cash flows, low D/E and spare capacity: KFIL sports a solid combination of i) consistent cash flows with enviable track record of converting cash profits to cash flows (5Y/10Y AOCF/CP ratio of 1x/0.9x), ii) low D/E of 0.3x and iii) well invested asset base with spare capacity of 50%/25% in Castings/Pig Iron. Additionally, KFIL is part of a pedigreed group run by highly experienced management professionals and scores highly on our corporate governance framework. We expect sustainable improvement in return ratios led by improvement in asset turnover and higher margins (driven by cost efficiency, better spreads and operating leverage) leading to attractive ROE of 25% in FY20E. Valuation and risks – Earnings at an inflection point, re-rating scope strong: We expect EBITDA/PAT CAGR of 28%/29% during FY17-20E, led by volume CAGR of 19% in the castings business coupled with cost efficiencies and operating leverage leading to higher margins and strong improvement in return ratios. We see strong scope for re-rating and value KFIL using our conservative five-year AOCF/EV yield methodology to arrive at a TP of Rs155, upside of ~56%. Key risks are lower volumes and raw material volatility. Currently, the stock has no institutional sell side coverage. Target Price Rs155 Key Data Bloomberg Code KKF IN CMP* Rs99.4 Curr Shares O/S (mn) 137.3 Diluted Shares O/S(mn) 137.3 Upside 55.9% Mkt Cap (Rsbn/USDmn) 13.6/211.7 Price Performance (%)* 52 Wk H / L (Rs) 112/65.5 1M 6M 1Yr 5 Year H / L (Rs) 112/15 KKF IN 24.2 0.3 35.1 Daily Vol. (3M NSE Avg.) 244607 Nifty (3.1) 5.3 23.5 *as on 1 December 2017; Source: Bloomberg, Centrum Research Shareholding pattern (%) * Sep-17 Jun-17 Mar-17 Dec-16 Promoter 59.6 59.6 59.6 59.5 FIIs 0.6 0.6 0.6 0.5 DIIs 2.6 1.8 1.8 1.8 Others 37.2 38.0 38.0 38.2 Source: BSE, * as on 1 December 2017 Well invested asset base with spare capacity Source: Centrum Research Strong volume growth in castings underway Source: Centrum Research Estimates Sharp uptick in per tonne profitability in store Source: Centrum Research Estimates Abhisar Jain, CFA, [email protected], 91 22 42159928 Y/E Mar(Rs mn) Rev YoY (%) EBITDA EBITDA (%) PAT YoY (%) EPS (Rs) RoE (%) RoCE (%) P/E (x) EV/EBITDA (x) FY16 11,139 (18.4) 1,509 13.6 578 17.4 4.2 12.2 11.0 12.5 5.5 FY17 11,337 1.8 1,756 15.5 907 56.9 6.6 16.9 14.0 11.4 6.3 FY18E 15,793 39.3 1,352 8.6 465 (48.7) 3.4 7.8 7.5 29.3 11.1 FY19E 17,086 8.2 2,467 14.4 1,179 153.5 8.6 17.9 14.6 11.6 6.3 FY20E 18,049 5.6 3,730 20.7 1,953 65.7 14.2 25.4 20.2 7.0 4.2 Source: Centrum Research Estimates 133000 390000 65892 291273 67108 98727 50% 25% 0% 50% 100% 0 500000 Castings Pig Iron Tonne Capacity Production Spare Capacity Spare Capacity % - RHS 60396 57257 56661 65892 82000 97000 110000 45% 42% 42% 49% 61% 72% 81% 2.8% -5.2% -1.0% 16.3% 24.4% 18.3% 13.4% -20% 0% 20% 40% 60% 80% 100% 0 20000 40000 60000 80000 100000 120000 FY14 FY15 FY16 FY17 FY18E FY19E FY20E Volumes (Tonne) Utilisation - % YoY % - RHS 14428 15067 17126 14971 17137 19310 3969 4361 5497 3481 5821 8419 34.8 41.4 45.8 44.1 47.7 51.2 0 12 24 36 48 60 0 5000 10000 15000 20000 25000 FY15 FY16 FY17 FY18E FY19E FY20E Rs/t Gross Profit/t Blended EBITDA/t Castings Share - % (RHS) Metals BUY Initiating Coverage 4 December 2017 INDIA Kirloskar Ferrous

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

34Centrum Equity Research is available on Bloomberg, Thomson Reuters and FactSet

Well casted at an inflection point We initiate coverage on Kirloskar Ferrous (KFIL) with a Buy and TP of Rs155 (56% upside). KFIL features i) a well invested asset base with spare capacity of 50%/25% in Castings/Pig Iron, ii) increasing share of high-margin casting business, iii) cost efficiencies from upcoming low-payback projects, iv) an enviable track record of converting cash profits to cash flows (5Y/10Y AOCF/CP ratio of 1x/0.9x) and v) strong earnings growth led by higher volumes and operating leverage, buttressed by a low D/E of 0.3x. Exciting future growth prospects await KFIL’s castings business which boasts of i) a strong product profile and customer relationships, ii) sustainable competitive strengths and iii) satisfactory demand visibility. We expect an impressive EBITDA/PAT CAGR of 28%/29% during FY17-20E driven by castings volume CAGR of 19% coupled with cost efficiencies. Finally, we believe that it merits rerating based on an attractive cash flow yield of 11.4%/15.9% (FY19E/20E).

� Hard yards covered in castings, strong growth underway: KFIL has alreadycompleted the augmentation of the value-added business of castings in the pastfew years and has invested heavily in i) increasing capacity by 50% to ~133ktpa, ii)adding machining facilities which fetch superior margins, iii) innovation and R&Dto reduce new product development cycle time from eight months to two months– a game changer achievement and iv) acquiring several marquee customersacross various segments. With its castings business having i) sustainable competitive strengths in a fragmented industry, ii) servicing steadily growing sectors like auto, tractor and diesel engines and iii) having well invested asset base with 50% spare capacity, KFIL is set to achieve a quantum leap in its castings volumes/turnover with CAGR of 19%/21% over FY17-20E and increase castings share in overall turnover to 51% by FY20E (from ~44% in FY18E).

� Pig iron business being made robust with meaningful cost improvement projects: KFIL has taken several steps to reduce its foundry grade pig iron business’vulnerability to the vagaries of commodity cycles (which too have become shorterand erratic in the recent past). Cost benefits are likely to accrue from H2FY18 from steps already implemented, such as i) BF-1 upgradation in FY17 and ii) coke sourcingthrough conversion arrangement at domestic third-party locations vs. imports. Big ticket cost improvement projects like i) installation of PCI system to replace ~80kgs of coke with low cost coal and ii) setting up of 200ktpa coke oven with 15 MW WHR CPP are likely soon and will improve the cost metrics of PI business materially from FY20E. Weexpect profitability of pig iron business to improve sharply, led by i) cost savings from low-payback projects, ii) higher volumes and iii) better spreads.

� Splendid combo of consistent cash flows, low D/E and spare capacity: KFILsports a solid combination of i) consistent cash flows with enviable track record ofconverting cash profits to cash flows (5Y/10Y AOCF/CP ratio of 1x/0.9x), ii) low D/Eof 0.3x and iii) well invested asset base with spare capacity of 50%/25% inCastings/Pig Iron. Additionally, KFIL is part of a pedigreed group run by highlyexperienced management professionals and scores highly on our corporategovernance framework. We expect sustainable improvement in return ratios led byimprovement in asset turnover and higher margins (driven by cost efficiency, better spreads and operating leverage) leading to attractive ROE of 25% in FY20E.

� Valuation and risks – Earnings at an inflection point, re-rating scope strong:We expect EBITDA/PAT CAGR of 28%/29% during FY17-20E, led by volume CAGRof 19% in the castings business coupled with cost efficiencies and operatingleverage leading to higher margins and strong improvement in return ratios. Wesee strong scope for re-rating and value KFIL using our conservative five-yearAOCF/EV yield methodology to arrive at a TP of Rs155, upside of ~56%. Key risksare lower volumes and raw material volatility. Currently, the stock has noinstitutional sell side coverage.

Target Price Rs155 Key Data

Bloomberg Code KKF IN

CMP* Rs99.4 Curr Shares O/S (mn) 137.3

Diluted Shares O/S(mn) 137.3

Upside 55.9% Mkt Cap (Rsbn/USDmn) 13.6/211.7

Price Performance (%)* 52 Wk H / L (Rs) 112/65.5

1M 6M 1Yr 5 Year H / L (Rs) 112/15

KKF IN 24.2 0.3 35.1 Daily Vol. (3M NSE Avg.) 244607

Nifty (3.1) 5.3 23.5

*as on 1 December 2017; Source: Bloomberg, Centrum Research

Shareholding pattern (%) *

Sep-17 Jun-17 Mar-17 Dec-16

Promoter 59.6 59.6 59.6 59.5

FIIs 0.6 0.6 0.6 0.5

DIIs 2.6 1.8 1.8 1.8

Others 37.2 38.0 38.0 38.2

Source: BSE, * as on 1 December 2017

Well invested asset base with spare capacity

Source: Centrum Research

Strong volume growth in castings underway

Source: Centrum Research Estimates

Sharp uptick in per tonne profitability in store

Source: Centrum Research Estimates

Abhisar Jain, CFA, [email protected], 91 22 42159928

Y/E Mar(Rs mn) Rev YoY (%) EBITDA EBITDA (%) PAT YoY (%) EPS (Rs) RoE (%) RoCE (%) P/E (x) EV/EBITDA (x)

FY16 11,139 (18.4) 1,509 13.6 578 17.4 4.2 12.2 11.0 12.5 5.5

FY17 11,337 1.8 1,756 15.5 907 56.9 6.6 16.9 14.0 11.4 6.3

FY18E 15,793 39.3 1,352 8.6 465 (48.7) 3.4 7.8 7.5 29.3 11.1

FY19E 17,086 8.2 2,467 14.4 1,179 153.5 8.6 17.9 14.6 11.6 6.3

FY20E 18,049 5.6 3,730 20.7 1,953 65.7 14.2 25.4 20.2 7.0 4.2

Source: Centrum Research Estimates

133000

390000

65892

291273

67108 98727

50%

25%

0%

50%

100%

0

500000

Castings Pig Iron

Tonne

Capacity Production

Spare Capacity Spare Capacity % - RHS

60396 57257 5666165892

8200097000

110000

45% 42% 42%49%

61%72%

81%

2.8% -5.2% -1.0%

16.3%24.4%

18.3%13.4%

-20%

0%

20%

40%

60%

80%

100%

0

20000

40000

60000

80000

100000

120000

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Volumes (Tonne) Utilisation - % YoY % - RHS

14428

15067

17126

14971

17137

19310

3969

4361

5497

3481

5821 8419

34.8

41.445.8 44.1

47.7 51.2

0

12

24

36

48

60

0

5000

10000

15000

20000

25000

FY15 FY16 FY17 FY18E FY19E FY20E

Rs/t

Gross Profit/t Blended EBITDA/t

Castings Share - % (RHS)

Metals BUY

Initiating Coverage 4 December 2017

INDIA

Kirloskar Ferrous

2 Kirloskar Ferrous

Table of Contents

Hard yards covered in castings, strong growth underway ................................................. 3

Leading castings producer with strong relationships in a growing industry ................................................ 3

Investment in building capacity and capability of castings division already done ..................................... 6

Strong volume growth in store, better product mix and economies of scale to enhance margins & profitability ........................................................................................................................................................................ 10

Pig iron business being made robust with meaningful cost improvement projects ...... 12

Foundry grade pig iron business with limited competition ............................................................................. 12

Spread contraction in last 12-18m hurt earnings, but recovery underway ................................................. 13

Third party coke manufacturing tie-up to reduce costs .................................................................................... 14

Low-payback backward integration projects being planned, cost metrics likely to improve significantly by FY20E .................................................................................................................................................... 15

Splendid combo of consistent cash flows, low debt/equity and spare capacity ............. 16

Spare capacity of 50%/25% in castings/pig iron businesses ............................................................................ 16

Asset turnover at a multi-year low, set to improve with higher utilisation ................................................. 16

Low leverage gives flexibility to pursue investment projects for cost savings and growth .................. 18

KFIL continues to pursue iron ore mines in Karnataka auctions and looking for attractive bidding price ..................................................................................................................................................................................... 18

Financial Analysis – Earnings at an inflection point .......................................................... 19

Revenue growth to be aided by solid volume growth in castings segment .............................................. 19

EBITDA margins to trend upwards, driven by increasing share of high margin castings and cost saving initiatives .............................................................................................................................................................. 19

Return ratios should inch higher with major uptick in FY20E .......................................................................... 20

Strong dividend payout track record ....................................................................................................................... 20

Key Assumptions and Sensitivity ....................................................................................... 21

Valuation – Strong scope for re-rating, Initiate with Buy and TP of Rs155 ..................... 22

AOCF/EV valuation – 40% premium ascribed to historical AOCF/EV yield .................................................. 22

EV/EBITDA valuation – 25% premium ascribed to historical EV/EBITDA ...................................................... 22

KFIL trading at attractive adjusted cash flow yield, leaving scope for re-rating ........................................ 23

Key risks to our thesis .......................................................................................................... 25

Company Background ......................................................................................................... 26

Corporate governance check – highlighting the finer points .......................................... 27

Independent directors’ representation on the board – KFIL has good balance ........................................ 27

Independent directors’ profile and compensation analysis ............................................................................. 28

Promoter group compensation analysis – as good as it gets .......................................................................... 29

Contingent liability ......................................................................................................................................................... 30

Related party transaction – clean history ................................................................................................................ 31

Auditor pedigree ............................................................................................................................................................. 31

Annexure – Indian Foundry (Castings) Industry ................................................................ 33

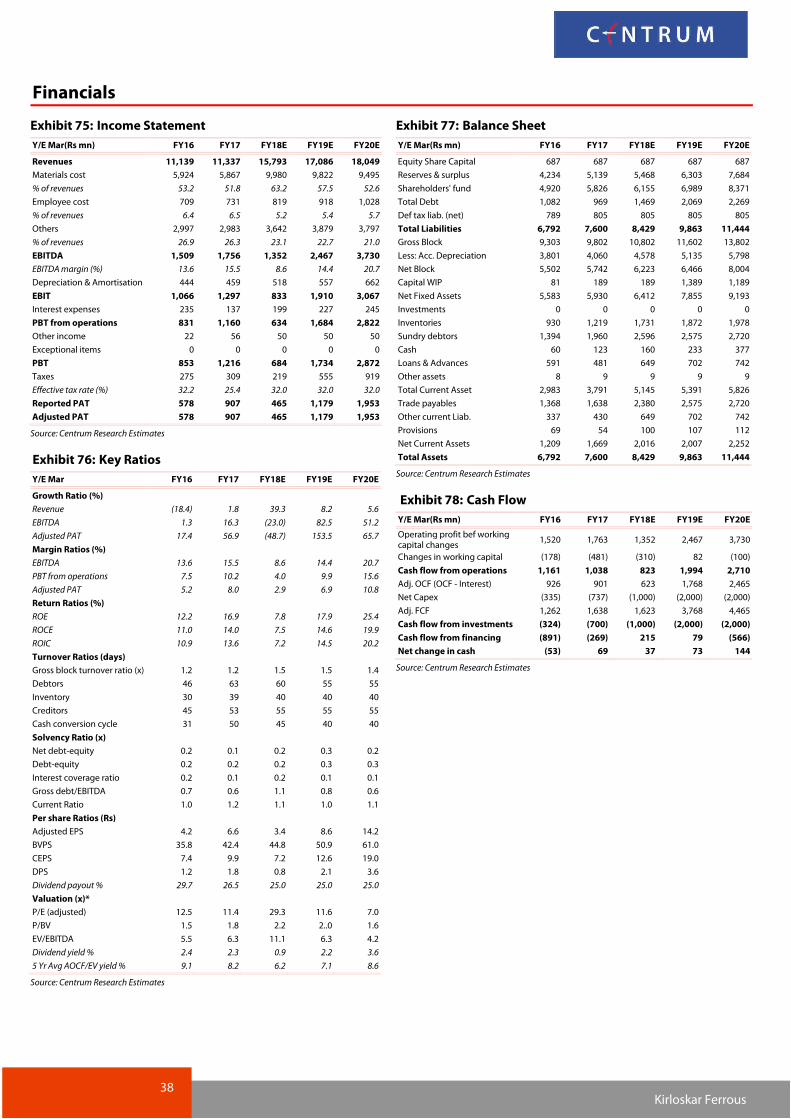

Financials - Historical ........................................................................................................... 37

Financials .............................................................................................................................. 38

3 Kirloskar Ferrous

Hard yards covered in castings, strong growth underway

Leading castings producer with strong relationships in a growing industry

KFIL’s pig iron business is forward-integrated into castings which is expected to account for ~44% of its overall sales in FY18E. Castings is the value added business in KFIL’s basket and the company has invested massively in both asset and capability development which has provided the base for a quantum leap in the castings division’s volumes/turnover with CAGR of 19%/21% expected over FY17-20E through higher utilisation of its existing world class asset base. We expect the share of castings business in overall turnover of KFIL to reach ~51% by FY20E

KFIL is a leading castings producer in India and possesses niche capabilities with production of grey iron and spheroidal graphite iron castings - key components for automobile, tractor and diesel engine OEMs. KFIL has made substantial investments in its castings business in the past two decades and painstakingly developed strong capabilities, giving it a substantial edge over competitors. KFIL also possesses strong customer relationships in a steadily-growing industry and has a well-invested asset base with significant spare capacity that provides a solid platform for strong growth. We discuss KFIL’s castings business in detail below (including industry snapshot) and then discuss the capabilities of KFIL in next section which gives us confidence in the company’s growth potential.

� Castings products of KFIL: KFIL’s foundries, located at Hospet (Koppal plant, Karnataka) andSolapur (Maharashtra) are equipped to produce Grey Iron & S.G Iron Castings for a variety ofapplications such as cylinder blocks, cylinder heads and different types of housings required byautomobile, tractor, and diesel engine Industries. A large share of production consists ofcomponents developed for the automotive sector, which includes trucks, agriculture and roadconstruction machinery, industrial and marine engines, among others. The parts manufacturedinclude engine blocks, heads, housings and components for brakes, transmission systems andaxles. KFIL has the capacity of 133 ktpa in castings in its two plants.

Exhibit 1: Cylinder blocks Exhibit 2: Cylinder heads

Source: Centrum Research Source: Centrum Research

Exhibit 3: Tractor housings Exhibit 4: SG castings & others

Source: Centrum Research Source: Centrum Research

4 Kirloskar Ferrous

� Marquee client base across auto, tractors, engines and other segments: In automobiles, KFILservices mainly the commercial vehicle (CV) segment and has a well-diversified client base,comprising all leading OEM’s. Within tractors, the company supplies to all large players and hasbeen successful in adding new customers. In the non-auto segment, KFIL services few engineproducers and construction equipment manufacturing companies.

Exhibit 5: KFIL FY17 castings sales by customer segments Exhibit 6: KFIL FY17 casting sales by product segments

Source: Centrum Research Source: Centrum Research

� Domestic castings industry growing at ~5% CAGR: Within this industry whose total productionstood at 11.4 MT in FY17, grey iron castings account for ~70% of the overall market (~8 MT). Theproduction CAGR in the industry for total castings/grey iron castings was at 5%/5.6% over FY14-17. As per various industry sources including snippets offered by the Institute of IndianFoundrymen (IIF), the industry is well poised for much stronger growth in the next five years, driven by higher demand.

Exhibit 7: Castings production in India Exhibit 8: Castings production in India - CAGR trend

Source: IIF, Centrum Research Source: IIF, Centrum Research

47.0%

43.0%

10.0%

Auto

Tractor

Diesel Engines

13.0%

22.0%

32.0%

33.0%

Cylindrical Head

Cylindrical Block

Housings

W/J Block/SG Castings

0

2

4

6

8

10

12

14

FY07 FY10 FY12 FY17

MT

Grey Cast Iron Spheroidal Graphite Iron Malleable Steel Non-Ferrous

7.2 7.4

10.0

11.4

5.6%

3.0%

4.9%5.0%

2.6%

4.7%

0%

1%

2%

3%

4%

5%

6%

3Y (FY14-17) 5Y (FY12-17) 10Y (FY07-17)

Grey Iron Castings Total

5 Kirloskar Ferrous

� Competition largely fragmented; KFIL servicing the Grey cast iron market: KFIL has thecapability of producing several niche products within this segment. As per our industry analysis, KFIL’s addressable market within grey cast iron castings is ~3 MT and the company currently holds a market share of ~3%. The castings industry is considerably fragmented and does not have thepresence of very big players. Foundries generally cater to specific requirements of somecustomers and do not possess scale or the capability to service needs of diverse customers. Keycompetitors of KFIL are Nelcast, DCM Engineering, Menon & Menon, Ghatge Patil, Neosym,Steelcast and Amtek foundry. KFIL has wider and deeper capabilities than its competitors in the greyiron castings segment as per our industry and competition deep dive analysis.

� Castings business has several entry barriers: Some key entry barriers are:-

� Long and complex new product development time – Each casting is unique in nature andneeds to be developed on designs given by clients. The time taken for new product developmentplays a crucial role in procuring an order and successfully executing it within a giventimeframe. The new product development time is between 8 to 18 months for the industry ingeneral.

� Need for technology, innovation and continuous R&D– There is constant need for investing in R&D (as high as ~1% of revenues), innovation in operational efficiencies for getting the desired output and strong technology support for designing and manufacturing customised products.

� Long customer approval time and relationships – New customer acquisition is a longdrawn out process, involving a lengthy procedure for approval of both the productionfacilities and soft skills related to technology, and product development. Customers also tendto have sticky and long-term relationships with their suppliers and don’t change vendorsfrequently.

� High rejection rate, need for high quality, customised products dissuades marginalplayers – The industry suffers from high rejection rate (8-9% on an average) due to thecomplexity of product design and production, as customers look for quality. Moreimportantly, client needs customised products to suit their requirements and hence designand quality are vital. This keeps marginal players out of the game as it is uneconomical forthem.

6 Kirloskar Ferrous

Investment in building capacity and capability of castings division already done

KFIL has made huge strides in not only building up capacity in its castings division but also in developing niche capabilities that give it an edge over competitors and paves way for strong volume growth in the coming years. We discuss these in detail below:-

� Impressive capacity build-up by KFIL in castings division: KFIL has made significant investments in its castings division over the past 10 years and built up a strong production base at Solapur and Hospet (Koppal) plants. The company acquired the Solapur plant in 2008 and subsequently set up a new line of 40 ktpa at the plant while abandoning the old lines completely. At its Koppal plant, KFIL set up the new line in FY13-14 with a capacity of 48 ktpa at a competitive capex. The new lines are highly robotized and efficient. KFIL has also invested in setting up machining facilities at Solapur and more recently at Koppal, providing strong value addition.

Exhibit 9: Capacity build-up in castings

Source: Centrum Research

� Focus on increasing sales of higher margin machined castings: KFIL is also focussed on increasing the sales of machined castings, which adds substantial value and fetches much higher margins. While non-machined castings fetch a realisation of ~Rs80/kgs, machined castings fetch an additional Rs40-50/kg and the company makes EBITDA margins of ~40% on the additional realisations. KFIL is currently doing machining jobs of ~10% of its overall casting volumes but intends to spend further on building more machining facilities for value addition. Machining capabilities also attract more customers who want highly value added machined castings. The payback on the investment done for machining is 4-5 years and currently the company is procuring more orders for machining work.

Exhibit 10: Machining facilities in castings division of KFIL

Source: Centrum Research, *Koppal capacity of machining is on ballpark basis

45,000 45,000

93,000

40000 40000

4000048000

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

FY06 FY08 FY09 FY14 FY17

Tonne/year

Koppal Solapur New Line Solapur Koppal New Line

45000

95000

133000

24000

48000 48000

48000 48000

24000

0

20000

40000

60000

80000

100000

120000

140000

FY08 FY14 FY18

Nos

Solapur - Heads Solapur - Blocks Koppal*

7 Kirloskar Ferrous

� Game-changing achievement of reduction in new product development cycle time from eight to two months: A key determinant of capability in castings production is new product development cycle time and KFIL has in FY17 achieved a big breakthrough in reducing this from as high as eight months earlier to less than two months now. The new product development cycle involves developing the requisite design for castings (after getting the initial design in 2D/3D form from the customer), developing the toolings design for manufacturing of casting (core and moulds making), producing initial samples and procuring customer approval on samples before the product can be sent for production. KFIL earlier took seven to eight months to do the job as the design of toolings, which was outsourced, itself took four to five months. Now this is done in-house within two weeks and other processes have also been streamlined. As a result of reduced new product development cycle time, KFIL can now develop ~15 new products annually versus 4-5 products earlier. This resulted in new customer acquisitions and more orders and was a game changer for the company from FY17 (Refer exhibit 11 for key benefits).

Exhibit 11: Game changing improvement in new product development cycle time

Source: Centrum Research Estimates

� Efforts underway to reduce cycle time further to one month: KFIL is currently working to adopt the new technology of 3D printing which could further reduce new product development cycle time to ~1m. We believe that if successful, this will help the company further in growing volumes strongly and add to its competitive advantage.

� Improved product quality and delivery time: KFIL has also made substantive progress in improving product quality over time by reducing rejection rates and creating better fettling facilities. KFIL’s Solapur facility has rejection rate of only 5% - lowest in the industry - and rejections rates on a whole for the company stands at 7-8%. The company has given the delivery mechanism special importance focussing sharply on customer requirements. This will help retain customers over long periods of time.

� Significant increase in new customer additions & strong geographical presence: KFIL has been able to develop a diversified customer base with several new customer additions over the past two years and also increase its geographical presence in the past five years along with the build-up in volumes from Solapur plants. Customer diversification has been increasing constantly and KFIL has added several new customers in the past few years.

8

2

1

0

1

2

3

4

5

6

7

8

9

Till FY16 From FY17 Likely from FY19-20E

No. of months

Key benefits of cycle time reduction:

� More product developments annually� Flexibility to target and develop products for more customers� Better utilisation of spare capacity in castings� Strong Competitive edge over peers

8 Kirloskar Ferrous

� Strong focus on R&D capability: KFIL has spent ~Rs115mn on R&D in the past two years, which amounts to ~0.5% of sales and ~2% of overall other expenses. The benefits of R&D, as per company’s annual report, has been in the following areas:

� Reduction of new product development cycle time.

� Acquiring of capability of developing critical castings.

� Improved quality and consistency.

� Initiation of prototype casting development through core 3D printing technology.

� Higher productivity through changes in designs of moulds/patterns.

Exhibit 12: R&D spend of KFIL

Source: Centrum Research

� Setting up a 10MW solar power plant at Solapur to reduce power cost: KFIL is currently setting up this plant at a capex of ~Rs500mn at its Solapur castings facility for captive use, which is likely to get commissioned by Q4FY18E. The operational cost of solar power is likely to be less than Rs2/unit and should cater to ~50% of the Solapur plant’s power requirement. The power cost at Solapur plant is currently north of Rs7/unit; our rough estimates suggest cost savings of ~Rs88mn/Rs61mn at EBITDA/PBT level from solar CPP from FY19E and thus translate to a payback of ~5 years from the project.

Exhibit 13: Significant power cost savings form Solar CPP

EBITDA Level PBT Level

Solar CPP Capacity (MW) 10 10

PLF - % 20 20

Power Production (mn units) 17.5 17.5

Cost/unit (Rs/unit) 2 3.5

Power Purchase Cost (Rs/unit) 7 7

Power cost savings (Rs/unit) 5 3.5

Total Savings (Rs mn) 88 61

Source: Centrum Research Estimates

70.4

43.7

0.6

0.4

2.3

1.5

0.0

0.5

1.0

1.5

2.0

2.5

0

10

20

30

40

50

60

70

80

FY16 FY17

Rs mn

R&D Spend - LHS as % of sales as % of other expenses

9 Kirloskar Ferrous

� Large investments already in place; monetisation of the same in store: As discussed in detail in the current section already, KFIL has made large investments in castings and with crucial capabilities such as quicker new product development time and marquee customer relationships already in place, the stage is set for monetisation of the existing robust asset base through higher capacity utilisation. We expect KFIL to sweat its asset base in castings; note that capacity utilisation at its Koppal/Solapur plant stood at just 44%/62% in FY17, thereby leaving large room for growth. We expect investments in castings business to be focussed incrementally on machining for the next 2-3 years and hence the capex in this business should be limited to ~Rs250-300mn/year.

Exhibit 14: Investments in castings business

Investments done in Castings Business over last 5 years

Set-up of new line (48000 ktpa) at Koppal in FY14

Set-up of new machine shop at Solapur in FY14

Set-up of new machine shop at Koppal in FY18

Set-up of fettling facilities in Solapur in FY17

Investment in R&D to reduce new product development cycle time and improve product quality

Source: Centrum Research

Exhibit 15: Enough room for capacity utilisation improvement going ahead

Source: Centrum Research

93000

40000

133000

41192

24700

6589244%

62%

50%

0%

10%

20%

30%

40%

50%

60%

70%

0

20000

40000

60000

80000

100000

120000

140000

Koppal Solapur Total

Tonne/yr

Capacity Volumes Utilisation - RHS

10 Kirloskar Ferrous

Strong volume growth in store, better product mix and economies of scale to enhance margins & profitability

KFIL has come a long way in the castings business by developing key competencies over time and simultaneously increasing capacities (as explained in detail already in previous sections) and we expect strong volume growth, driven by increased mining of existing customers as well as acquisition of new customers. We also expect better product mix and economies of scale to augment margins, culminating in strong earnings growth from the castings business.

� We expect castings volume CAGR of 18.6% during FY17-20E: We expect KFIL to clock impressive volume CAGR of 18.6% in castings division during FY17-20E with total volumes growing to 110kt by FY20E (versus 66kt in FY17). Revenue growth is likely to increase at a fast clip led by better product mix (increased share of special castings and machined castings) and sales should rise to Rs9.2bn in FY20E (~1.8x of FY17 levels of Rs5.2bn).

Exhibit 16: Castings volumes up-trend Exhibit 17: Revenue growth to remain solid

Source: Centrum Research Estimates Source: Centrum Research Estimates

� Focus on cost optimisation, higher share of machined castings and economies of scale to augment castings margins: The castings business enjoys a high gross profit/t and we expect this to improve as share of castings in the overall mix increases to 51% by FY20E (Refer exhibits 18 & 19). We expect strong margin tailwinds for the castings business for KFIL because of i) a sharp increase in volumes providing economies of scale, ii) higher share of machined castings that fetch substantially higher margins and iii) focus on cost optimisation through set-up of captive power plant at Solapur, and other cost saving exercises.

Exhibit 18: Castings gross profit/t trend Exhibit 19: KFIL gross profit/t to move up led by higher share of castings

Source: Centrum Research Estimates Source: Centrum Research Estimates

60396 57257 5666165892

82000

97000110000

45% 42% 42%49%

61%72%

81%

2.8% -5.2% -1.0%

16.3%24.4%

18.3% 13.4%

-20%

0%

20%

40%

60%

80%

100%

0

20000

40000

60000

80000

100000

120000

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Volumes (Tonne) Utilisation - % YoY % - RHS

4,600 4,745 4,607

5,191 6,970

8,148

9,240

4.1%3.1%

-2.9%

12.7%

34.3%

16.9%13.4%

-5%

5%

15%

25%

35%

1,000

3,000

5,000

7,000

9,000

11,000

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Sales (Rs mn) YoY % - RHS

40,000

45,000

50,000

55,000

60,000

65,000

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Rs/t

12971

14428

15067

17126

14971

17137

19310

37.334.8

41.445.8 44.1

47.751.2

0

10

20

30

40

50

60

10000

12000

14000

16000

18000

20000

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

KFIL - Gross Profit/t (Rs) Castings - % Share - RHS

11 Kirloskar Ferrous

� Growing volumes of industry & key clients => Higher volumes for KFIL castings division: Analysis of sales volume data of CV and tractor industry indicates that i) CV industry is showing steady single digit growth in last few years but market shares of M&M and VECV have been inching up, and ii) tractor industry sales growth is on fast track coupled with increase in market share of Mahindra brand of tractors. KFIL is set to witness strong volume growth with increase in volumes of existing clients with whom the company enjoys a long term relationship coupled with acquisition of new clients.

Exhibit 20: CV industry volume trend Exhibit 21: Market share of KFIL’s clients increasing

Source: SIAM, Centrum Research, *YTD nos annualised Source: SIAM, Centrum Research

Exhibit 22: Tractor industry volume trend Exhibit 23: Market share trend in tractor industry

Source: SIAM, Centrum Research, *YTD nos annualised Source: SIAM, Centrum Research

873258

709776

701014

788828

822495

832232

0

2,00,000

4,00,000

6,00,000

8,00,000

10,00,000

FY13

FY14

FY15

FY16

FY17

YTDFY18A*

Nos

M&HCV LCV Total CV

55.950.8

47.945.4 44.4 43.5

20.525.5 25.1 24.8 25.1 26.6

7.511.4

14.9 17.8 17.6 17.5

5.4 5.5 6.0 6.6 7.1 6.80

10

20

30

40

50

60

FY13 FY14 FY15 FY16 FY17 YTDFY18

%

Tata Motors M&M

Ashok Leyland Volvo Eicher (VECV)

527737

634151

551463

493764

582844

676099

20.2%

-13.0% -10.5%

18.0%16.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

300000

400000

500000

600000

700000

FY13

FY14

FY15

FY16

FY17

YTDFY18A

Nos

Tractor Domestic Sales YoY - %

40.2 40.6 40.1 40.9 42.6

25.0 24.7 24.4 23.020.5

11.7 10.7 10.4 10.3 10.8

9.7 10.3 12.0 11.9 11.9

0

10

20

30

40

50

FY13 FY14 FY15 FY16 FY17

%

M&M TAFE Escorts Sonalika

12 Kirloskar Ferrous

Pig iron business being made robust with meaningful cost improvement projects

Foundry grade pig iron business with limited competition

KFIL produces foundry grade pig iron (FGPI) through its two blast furnaces (MBF1 & 2) and has an installed capacity of 3.9 lakh tpa. KFIL consumes ~15% of pig iron in-house in its castings division and sells the remaining in the merchant market to various foundries through an extensive pan-India dealer network. The FGPI business is characterised by lower competition, higher prices and better margins as compared to steel grade pig iron (SGPI) but remains exposed to cyclical movements in raw material and product prices.

� Pig iron demand-supply remains largely balanced: Pig iron market in India is characterised by supplies from a large number of small producers and demand is generally driven by i) foundries (for making of castings for various end-user industries) and ii) steel producers (as feed into SMS/induction furnaces to form appropriate metallic mix) for making finished steel. Pig iron is usually of two types: steel grade (SGPI) and foundry grade (FGPI) and is manufactured and supplied by various producers having mini blast furnaces in the secondary steel sector. Large producers account for only 10% of the market and include mainly the PSU’s like SAIL & RINL. The pig iron market in India has been passing through a subdued phase with flattish consumption for the last three years, but the market remains largely balanced as supply too has not increased and remains flattish at ~9.5 MT annually.

Exhibit 24: Pig iron demand-supply

FY13 FY14 FY15 FY16 FY17 YTDFY18

Production for Sale 6.9 8.0 9.7 9.2 9.5 5.4

Production growth % 27.9 15.7 21.9 (4.8) 2.4 (2.9)

Import 0.0 0.0 0.0 0.0 0.0 0.0

Exports 0.4 0.9 0.5 0.3 0.4 0.3

Exports as % of production 6.0 11.9 5.6 3.2 4.1 5.7

Net Exports 0.4 0.9 0.5 0.3 0.4 0.3

Consumption 6.5 7.1 9.1 9.0 9.1 5.1

Consumption growth % 30.7 9.4 27.4 (0.4) 0.5 (3.1)

Source: Joint planning commission, Centrum Research

� Foundry grade pig iron less competitive, fetches better prices and margins: While the foundry grade pig iron (FGPI) market is less than 20% of overall pig iron market, the number of producers in foundry grade market is limited, as manufacturing of foundry grade requires keeping sulphur and phosphorous at a lower level and also needs better quality iron ore. While foundry grade pig iron is also a commodity like steel grade pig iron, but limited competition in FGPI enables it to fetch better prices and margins compared to steel grade pig iron.

� Upgradation of MBF1 in FY17 => reduced coke consumption, higher capacity: KFIL has completed a crucial upgrade of its mini blast furnace 1 (MBF1) in FY17 at a capex of ~Rs400mn. The upgradation was aimed at i) increasing the working volume of the furnace to 300m3 resulting in an increase of MBF1 capacity by ~30ktpa, ii) reducing the coke rate through better operational working and iii) paving the way for future installation of pulverised coal injection plant for both MBF1 & 2. The MBF1 has been re-blown at a higher capacity since Jan’17. KFIL’s overall pig iron manufacturing capacity has increased to 1100 tpd (3.9 lakh tpa) and company is also looking to upgrade MBF-2 in due course, post which the capacity would increase to 1250 tpd (4.25 lakh tpa). The company expects the capex for upgradation of MBF2 to be between Rs400 and 500mn.

13 Kirloskar Ferrous

Spread contraction in last 12-18m hurt earnings, but recovery underway

KFIL’s pig iron business has seen substantial spread contraction in the past 12 to 18 months due to a sharp increase in coke/coking coal prices, which was not accompanied by a commensurate increase in pig iron prices. However, raw material prices have recently started stabilising at lower levels, while pig iron prices are showing resilience and hence spread recovery is underway. Additionally, KFIL has already initiated several cost reduction measures for reducing the volatility in spreads of the pig iron business. We expect gross profit/t for KFIL’s pig iron business to improve from H2FY18 from the distress levels of H1FY18.

� Large increase in coke prices has hurt spreads in last 12-18 months: Coke prices have more than doubled in the last 18 months on account of supply disruptions in coking coal; this led to a sharp squeeze in the difference between pig iron and coke prices, as pig iron prices in the domestic market couldn’t mirror similar gains (refer Exhibit 25 & 26). In the last few months, coke prices have softened 25% from the peak while pig iron has remained steady to marginally positive, thereby brightening the spread situation.

Exhibit 25: Coke & coking coal prices have more than doubled in last 18m

Exhibit 26: Difference between pig iron and coke prices reduced, squeezed spreads

Source: Steelmint, Centrum Research Source: Steelmint, Centrum Research

� Spreads have bottomed out, improvements underway aided by cost improvement initiatives: Pig iron spreads have been under pressure in the past one year and have been trending well below their long-term average. We see improvements in spreads already underway and expect the same to further improve. However, we remain conservative in our assumptions for improvement in gross profit/t of pig iron business and have factored in gross profit/t of Rs3984/5657 in FY19E/20E as compared to the last five-year average of ~Rs6200/t. Moreover, a major portion of our recovery assumptions is based on several cost improvement initiatives that KFIL is taking (explained in detail in the next section) and not purely on market related improvement in spreads. Improvement in gross profit/t from current distressed levels would help KFIL see its profitability in pig iron business stabilising by Q4FY18E, in our view.

Exhibit 27: KFIL’s pig iron gross profit/t trend – we expect recovery but remain conservative

Source: Centrum Research Estimates

0

100

200

300

400

May-15

Jul-15

Sep-15

Nov-15

Jan-16

Mar-16

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-17

Sep-17

Nov-17

US$/t

Coke (Met Coke 64% China - CNF India)

Coking Coal (HCC 8% Ash - CNF India)

Sharp increase seen in last 12-18 months 4000

8000

12000

16000

20000

5000

10000

15000

20000

25000

30000

May-15

Jul-15

Sep-15

Nov-15

Jan-16

Mar-16

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-17

Sep-17

Nov-17

Rs/t

Rs/t

Pig Iron (Foundry Grade - Ex Kharagpur)Met Coke import landed (from China)Spread (PI - 0.7x Coke)

6223

5023

6846

63696713

2809

3984

5657

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Rs/t

14 Kirloskar Ferrous

Third party coke manufacturing tie-up to reduce costs

KFIL has been procuring coke mainly through imports till now and was thus getting adversely impacted by the increase in international coke prices. But the company is likely to have tied up with two domestic coke manufacturers for a third party conversion of coking coal into coke exclusively for KFIL, at a fixed conversion cost. This arrangement is likely to yield substantial cost savings of ~Rs1570/t of coke and ~Rs300mn annually at the current coking coal and coke prices as per our estimates.

� Coke manufacturing being done at third party coke plants: KFIL is likely to have tied up with two third party plants in Karnataka and Tamil Nadu for exclusive third-party conversion of coking coal into coke. The volume tie-up is for a quantity of ~10,000 tonne/month with each supplier and the agreed conversion cost is approx. Rs2000/t. KFIL is targeting savings on coke procurement through this arrangement while the producers are looking for fixed return on their capacities without taking on commodity price movement risk.

� Coke cost reduction of ~Rs1570/t vs. imports at current prices: Our calculations on potential cost savings and workings on comparison of landed cost of coke from third party arrangement vs. imports indicates a saving of ~Rs1570/t on coke landed cost for KFIL (Exhibit 28, 29 & 30 below). We note that savings on coke are dynamic in nature and dependent on the prevailing prices of coking coal and imported coke. This translates to ~Rs1100/t in savings on pig iron manufacturing, implying annual savings of ~Rs300mn at current prices. We believe KFIL can realise a significant portion of this despite volatility in both coking coal and coke prices and this would help the company to manage its spreads in the pig iron business better. The coke supply arrangements with suppliers can be terminated at short notice if it becomes non-remunerative for KFIL.

Exhibit 28: 3rd party coke landed cost for KFIL Exhibit 29: Imported coke landed cost for KFIL

Hard Coking Coal Aus - CNF India – US$/t 195

Import Duty (2.5%) – US$/t 4.9

Port Charges – US$/t 5

Ex-Port Coking Coal Price US$/t 205

USD/INR 65

Ex-Port Coking Coal Price Rs/t 13,317

Internal Freight (Port to 3rd Party Coke Plants) – Rs/t 1,000

Coking Coal Landed Cost at 3rd Party – Rs/t 14,317

Coking coal reqd. for conversion to coke 1.42

Total Coking Coal Cost for making 1 tonne of Coke – Rs/t 20,330

Conversion Charges paid to 3rd party – Rs/t 2,000

Freight from 3rd party plant to KFIL plant – Rs/t 550

Landed cost of Coke at KFIL plant – Rs/t (A) 22,880

Met Coke 64% China - CNF India – US$/t 315

Import Duty (5%) – US$/t 15.8

Anti-dumping duty – US$/t 25

Port Charges – US$/t 5

Ex-Port Coking Coal Price US$/t 361

USD/INR 65

Ex-Port Coking Coal Price Rs/t 23,449

Freight from port to KFIL plant – Rs/t 1,000

Landed cost of Coke at KFIL plant – (B) 24,449

Source: Centrum Research Estimates Source: Centrum Research Estimates

Exhibit 30: Coke savings snapshot

Price differential of imported coke vs 3rd party converted coke (B-A) - (Rs/t) 1,569

Coke reqd/t of Pig Iron 0.72

Savings per tonne of Pig Iron (Rs/t) 1,130

Coke quantity tied up on annual basis 2,40,000

Likely quantity received (80%) 1,92,000

Annual Savings (Rs mn) 301

Source: Centrum Research Estimates

15 Kirloskar Ferrous

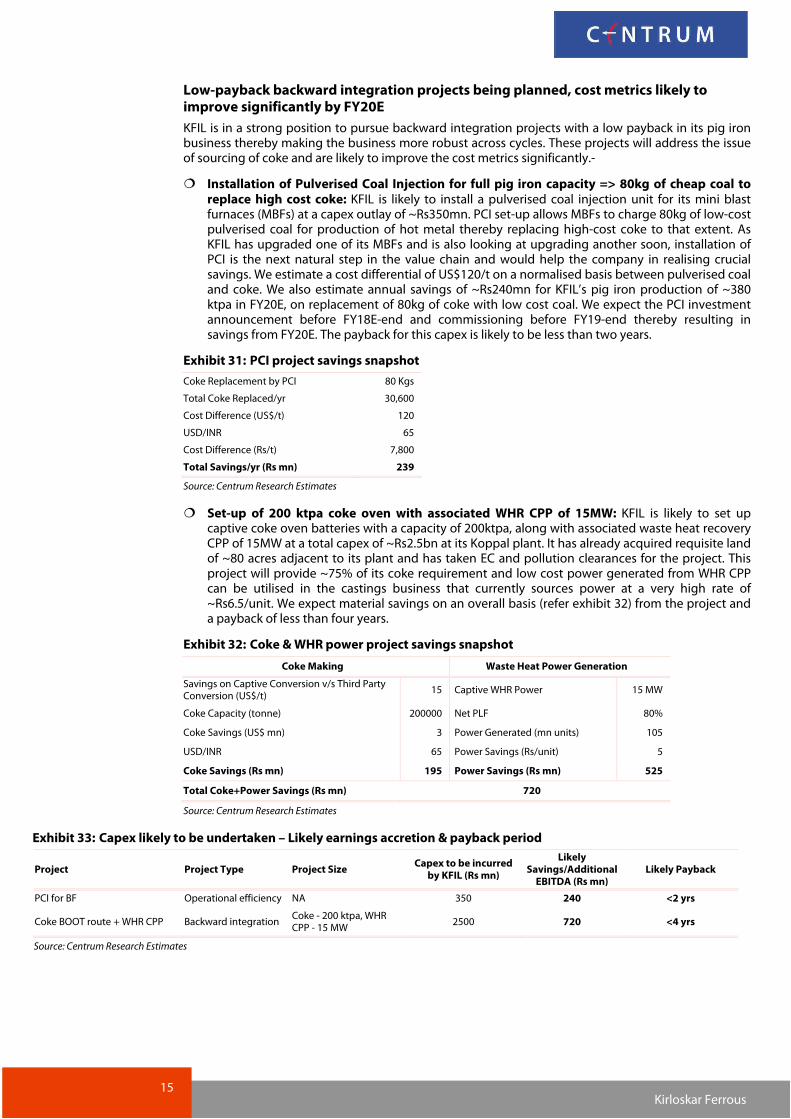

Low-payback backward integration projects being planned, cost metrics likely to improve significantly by FY20E

KFIL is in a strong position to pursue backward integration projects with a low payback in its pig iron business thereby making the business more robust across cycles. These projects will address the issue of sourcing of coke and are likely to improve the cost metrics significantly.-

� Installation of Pulverised Coal Injection for full pig iron capacity => 80kg of cheap coal to replace high cost coke: KFIL is likely to install a pulverised coal injection unit for its mini blast furnaces (MBFs) at a capex outlay of ~Rs350mn. PCI set-up allows MBFs to charge 80kg of low-cost pulverised coal for production of hot metal thereby replacing high-cost coke to that extent. As KFIL has upgraded one of its MBFs and is also looking at upgrading another soon, installation of PCI is the next natural step in the value chain and would help the company in realising crucial savings. We estimate a cost differential of US$120/t on a normalised basis between pulverised coal and coke. We also estimate annual savings of ~Rs240mn for KFIL’s pig iron production of ~380 ktpa in FY20E, on replacement of 80kg of coke with low cost coal. We expect the PCI investment announcement before FY18E-end and commissioning before FY19-end thereby resulting in savings from FY20E. The payback for this capex is likely to be less than two years.

Exhibit 31: PCI project savings snapshot

Coke Replacement by PCI 80 Kgs

Total Coke Replaced/yr 30,600

Cost Difference (US$/t) 120

USD/INR 65

Cost Difference (Rs/t) 7,800

Total Savings/yr (Rs mn) 239

Source: Centrum Research Estimates

� Set-up of 200 ktpa coke oven with associated WHR CPP of 15MW: KFIL is likely to set up captive coke oven batteries with a capacity of 200ktpa, along with associated waste heat recovery CPP of 15MW at a total capex of ~Rs2.5bn at its Koppal plant. It has already acquired requisite land of ~80 acres adjacent to its plant and has taken EC and pollution clearances for the project. This project will provide ~75% of its coke requirement and low cost power generated from WHR CPP can be utilised in the castings business that currently sources power at a very high rate of ~Rs6.5/unit. We expect material savings on an overall basis (refer exhibit 32) from the project and a payback of less than four years.

Exhibit 32: Coke & WHR power project savings snapshot

Coke Making Waste Heat Power Generation

Savings on Captive Conversion v/s Third Party Conversion (US$/t)

15 Captive WHR Power 15 MW

Coke Capacity (tonne) 200000 Net PLF 80%

Coke Savings (US$ mn) 3 Power Generated (mn units) 105

USD/INR 65 Power Savings (Rs/unit) 5

Coke Savings (Rs mn) 195 Power Savings (Rs mn) 525

Total Coke+Power Savings (Rs mn) 720

Source: Centrum Research Estimates

Exhibit 33: Capex likely to be undertaken – Likely earnings accretion & payback period

Project Project Type Project Size Capex to be incurred

by KFIL (Rs mn)

Likely Savings/Additional EBITDA (Rs mn)

Likely Payback

PCI for BF Operational efficiency NA 350 240 <2 yrs

Coke BOOT route + WHR CPP Backward integration Coke - 200 ktpa, WHR CPP - 15 MW

2500 720 <4 yrs

Source: Centrum Research Estimates

16 Kirloskar Ferrous

Splendid combo of consistent cash flows, low debt/equity and spare capacity

Spare capacity of 50%/25% in castings/pig iron businesses

KFIL has spare capacity of 50%/25% in castings/pig iron as both businesses are well endowed with substantial investments made in the past few years. Castings has spare capacity at both Solapur and Koppal plants and with reduction in new product development cycle time already achieved, both plants are likely to see better utilisation. KFIL has focussed on building its capabilities in the past few years and has set itself up strongly for volume growth from FY18E onwards. We believe that volume growth will be strong in the years ahead as existing assets get better utilised. This will be driven by i) long-standing, vital customer relationships and quicker product development in castings, and ii) higher operational efficiency of blast furnaces for pig iron.

Exhibit 34: Snapshot of capacity and utilisations in KFIL’s castings/pig iron businesses

Source: Centrum Research

Asset turnover at a multi-year low, set to improve with higher utilisation

KFIL has been allocating capital in the past five years to projects on forward integration (increase in castings capacity for value addition and higher profitability) and operational efficiency (upgradation of blast furnace for cost savings and expansion). While the gross block has expanded by ~70% (over FY13-17), volumes and turnover have remained largely flat. Asset turnover in FY17 was at a multi-year low of 1.2x (versus 1.9x in FY13) and we see improvement in asset turnover led by higher utilisation of the existing solid asset base.

Exhibit 35: Revenue/Gross block trend

Source: Centrum Research Estimates

133000

390000

65892

291273

6710898727

50%

25%

0%

10%

20%

30%

40%

50%

60%

0

100000

200000

300000

400000

500000

Castings Pig Iron

Tonne

Capacity Production Spare Capacity - RHS Spare Capacity - RHS

1.9

1.5

1.6

1.21.2

1.5 1.5

1.3

1.0

1.2

1.4

1.6

1.8

2.0

0

4000

8000

12000

16000

20000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Rs mn

Revenues Gross Block Rev/GB (x) - RHS

17 Kirloskar Ferrous

Strong conversion of cash profit into adjusted operating cash flows (excl. interest) => hallmark of a well-run business

We believe that one of the key signals of prudent capital management is conversion of cash profits (CP) into adjusted operating cash flows (AOCF=OCF-Interest). KFIL boasts of an enviable track record of conversion of cash profits to cash flows (5Y/10Y AOCF/CP ratio of 1x/0.9x). This in turn has resulted in greater flexibility to undertake capex and reduce debt. We expect KFIL to continue to convert majority of its cash profits into cash flows going forward.

Exhibit 36: AOCF/CP trend

Source: Centrum Research Estimates

Working capital management remains sound

KFIL’s integrated business is not working capital-intensive and the management has done a good job in controlling inventories to below 40 days. Debtor days for the pig iron business have remained low as KFIL sells specialised foundry grade on favourable terms to various markets through a strong dealer network. As per industry standards, debtors for the castings business is between 60-70 days and supplies are to long-standing customers. Creditors are between 40-60 days for sourcing of coke depending on negotiations while iron ore is procured from e-auctions in Karnataka on bidding and cash payment. On an overall basis, KFIL’s working capital management remains sound with cash conversion cycle maintained at ~30 days on an average in the past (FY11-17 average); we expect the same to remain at 40 days in FY19E/20E.

Exhibit 37: Cash conversion cycle trend

Source: Centrum Research Estimates

0.8

1.1

1.3

0.9

0.7 0.6

1.00.9

0.5

0.7

0.9

1.1

1.3

1.5

0

500

1000

1500

2000

2500

3000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Rs mn

Cash Profit AOCF AOCF/CP (x) - RHS

33 32

24

31

50

45

40 40

0

10

20

30

40

50

60

-80

-60

-40

-20

0

20

40

60

80

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Days

Days

Inventory Debtors Creditors Cash Conversion Cycle - RHS

18 Kirloskar Ferrous

Low leverage gives flexibility to pursue investment projects for cost savings and growth

KFIL boasts of a strong balance sheet with low Net Debt (incl. acceptances)/Equity ratio of 0.3x. Despite investing for growth in the past few years, the company has continuously repaid its debt and reduced leverage. KFIL currently does not have any long-term debt and existing debt is only for working capital. Strong balance sheet with low leverage coupled with strong cash flow generation gives KFIL enormous flexibility to pursue growth as well as backward integration projects which will help make its operations more rewarding across cycles.

Exhibit 38: Consistent debt reduction has led to low leverage

Source: Centrum Research Estimates

KFIL continues to pursue iron ore mines in Karnataka auctions and looking for attractive bidding price

Apart from pursuing backward integration projects for coke sourcing, KFIL is also actively looking to acquire iron ore mines in the ongoing auctions in Karnataka. KFIL currently buys iron ore from e-auctions in Karnataka but aspires to have their own captive mine for long term, dedicated sourcing. While the bidding so far in mine auctions has been too aggressive and well above the threshold levels from an economic point of view, KFIL would remain a key participant in upcoming mine auctions and looks to procure the iron ore mines at much better bidding prices which provides both savings on a per tonne basis and captive feed for long term.

17021896

1327

1082969

2946 2947 2487 1721 1762

0.70.7

0.5

0.30.3

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0

500

1000

1500

2000

2500

3000

3500

FY13 FY14 FY15 FY16 FY17

Rs mn

Net Debt Net Debt (Incl. acceptances) Net Debt/Equity (x) - RHS

19 Kirloskar Ferrous

Financial Analysis – Earnings at an inflection point

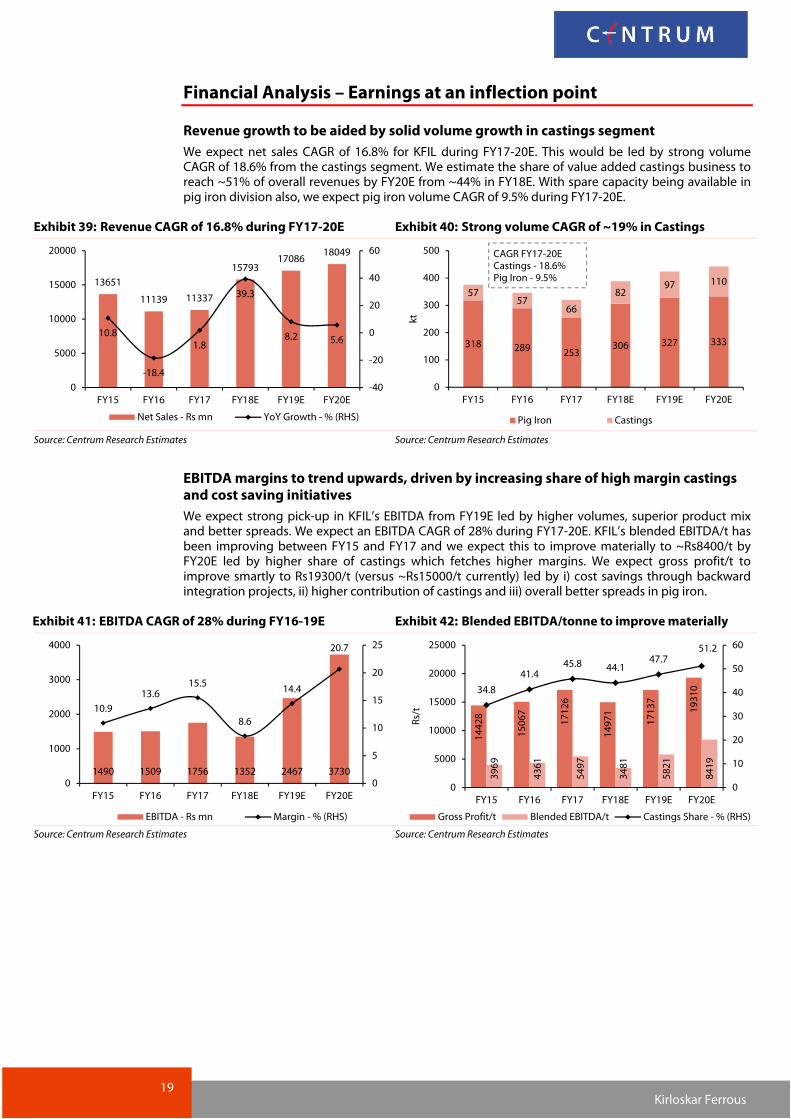

Revenue growth to be aided by solid volume growth in castings segment

We expect net sales CAGR of 16.8% for KFIL during FY17-20E. This would be led by strong volume CAGR of 18.6% from the castings segment. We estimate the share of value added castings business to reach ~51% of overall revenues by FY20E from ~44% in FY18E. With spare capacity being available in pig iron division also, we expect pig iron volume CAGR of 9.5% during FY17-20E.

Exhibit 39: Revenue CAGR of 16.8% during FY17-20E Exhibit 40: Strong volume CAGR of ~19% in Castings

Source: Centrum Research Estimates Source: Centrum Research Estimates

EBITDA margins to trend upwards, driven by increasing share of high margin castings and cost saving initiatives

We expect strong pick-up in KFIL’s EBITDA from FY19E led by higher volumes, superior product mix and better spreads. We expect an EBITDA CAGR of 28% during FY17-20E. KFIL’s blended EBITDA/t has been improving between FY15 and FY17 and we expect this to improve materially to ~Rs8400/t by FY20E led by higher share of castings which fetches higher margins. We expect gross profit/t to improve smartly to Rs19300/t (versus ~Rs15000/t currently) led by i) cost savings through backward integration projects, ii) higher contribution of castings and iii) overall better spreads in pig iron.

Exhibit 41: EBITDA CAGR of 28% during FY16-19E Exhibit 42: Blended EBITDA/tonne to improve materially

Source: Centrum Research Estimates Source: Centrum Research Estimates

13651

11139 11337

1579317086

18049

10.8

-18.4

1.8

39.3

8.2 5.6

-40

-20

0

20

40

60

0

5000

10000

15000

20000

FY15 FY16 FY17 FY18E FY19E FY20E

Net Sales - Rs mn YoY Growth - % (RHS)

318 289 253306 327 333

5757

66

8297 110

0

100

200

300

400

500

FY15 FY16 FY17 FY18E FY19E FY20Ekt

Pig Iron Castings

CAGR FY17-20ECastings - 18.6%Pig Iron - 9.5%

1490 1509 1756 1352 2467 3730

10.9

13.615.5

8.6

14.4

20.7

0

5

10

15

20

25

0

1000

2000

3000

4000

FY15 FY16 FY17 FY18E FY19E FY20E

EBITDA - Rs mn Margin - % (RHS)

14428

15067

17126

14971

17137

19310

3969

4361

5497

3481

5821

8419

34.8

41.445.8 44.1

47.751.2

0

10

20

30

40

50

60

0

5000

10000

15000

20000

25000

FY15 FY16 FY17 FY18E FY19E FY20E

Rs/t

Gross Profit/t Blended EBITDA/t Castings Share - % (RHS)

20 Kirloskar Ferrous

Return ratios should inch higher with major uptick in FY20E

KFIL’s return ratios have remained subdued on account of front loaded investments and low asset turnover due to low utilisation. However, this is set to change sustainably and with meaningful contribution from spare capacity in value-added business of castings coming in progressively by FY20E, we expect material jump in ROE/ROCE by FY20E. We forecast ROE/ROCE (post tax) to be at ~25%/20% in FY20E.

The DuPont analysis of ROE shows that the improvement is well distributed between key metrics:-

� Profit margins – This is expected to improve materially (to double digits) by FY20E led by i) higher share of high margin value-added castings, ii) cost improvement projects in pig iron business coupled with captive power facilities for castings and iii) operating leverage from higher volumes.

� Asset Turnover – We expect substantial sweating of assets despite incremental capital getting invested in backward integration projects (like coke oven and CPP which don’t fetch additional sales), and hence an increase in return ratios.

� Leverage – The leverage for KFIL remain low with no long-term debt and we expect the company to largely maintain this situation through internal accruals. Hence, leverage is expected to play a bare minimum role in improvement of ROE’s and hence ROE improvement is not borrowed from increased leverage which is again a positive sign.

Exhibit 43: Return ratios to inch up Exhibit 44: DuPont analysis

FY15 FY16 FY17 FY18E FY19E FY20E

Profit Margin - % 3.6 5.2 8.0 2.9 6.9 10.8

Asset Turnover (Net Sales/Assets) - x

1.4 1.2 1.2 1.5 1.4 1.3

Financial Leverage (Assets/Equity) - x

2.2 1.9 1.7 1.8 1.9 1.8

ROE - % 11.2 12.2 16.9 7.8 17.9 25.4

Source: Centrum Research Estimates Source: Centrum Research Estimates

Strong dividend payout track record

KFIL has maintained a good record of dividend payout of ~30% of PAT. We note that the company has carefully calibrated its cash flows and allocated them appropriately over time to i) dividends, ii) debt repayments and iii) new project investments as part of capex. We expect strong dividend payout to be maintained. We also note that promoters of KFIL do not draw any salary from the company (except board sitting fees) and instead realise money as general shareholders by way of dividends. This is positive for all shareholders (refer to details in Corporate governance section on page 27).

Exhibit 45: Dividend payout

Source: Centrum Research Estimates

11.212.2

16.9

7.8

17.9

25.4

10.4 11.0

14.0

7.5

14.6

19.9

5

10

15

20

25

30

FY15 FY16 FY17 FY18E FY19E FY20E

%

ROE ROCE (post tax)

1.2 1.2

1.8

0.8

2.1

3.635%

30%

26%25% 25% 25%

3% 2% 2%1%

2%4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY15 FY16 FY17 FY18E FY19E FY20E

Dividend (Rs/Sh) - LHS Payout - % Div Yield - % (RHS)

21 Kirloskar Ferrous

Key Assumptions and Sensitivity

Exhibit 46: Key Assumptions

FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Revenue (Rs mn)

Pig Iron 7,174 8,437 6,231 5,889 8,423 8,498 8,325

Castings 4,600 4,745 4,607 5,191 6,970 8,148 9,240

Sales Volumes (kt)

Pig Iron 2,75,692 3,18,023 2,89,485 2,53,495 3,06,300 3,26,850 3,33,000

Castings 60,396 57,257 56,661 65,892 82,000 97,000 1,10,000

Net Sales Realisations (Rs/t)

Pig Iron 26,021 26,528 21,525 23,231 27,500 26,000 25,000

Castings 76,170 82,864 81,303 78,786 85,000 84,000 84,000

Gross Profit (Rs/t)

Pig Iron 5,023 6,846 6,369 6,713 2,809 3,984 5,657

Castings 49,251 56,543 59,502 57,186 60,399 61,460 60,640

KFIL - Total 12,971 14,428 15,067 17,126 14,971 17,137 19,310

Source: Centrum Research Estimates

Exhibit 47: Earnings sensitivity to castings volumes & realisations (+1% change)

1% Chg EBITDA PAT

Castings FY19E FY20E FY19E FY20E

Volume 2.0 1.5 2.9 2.0

Realisations 3.1 2.4 4.5 3.1

Source: Centrum Research Estimates

Exhibit 48: Earnings sensitivity to RM costs (+1% change)

1% Chg EBITDA PAT

RM Costs FY19E FY20E FY19E FY20E

Iron Ore (1.1) (0.7) (1.6) (0.9)

Coke (2.2) (1.3) (3.2) (1.7)

Source: Centrum Research Estimates

22 Kirloskar Ferrous

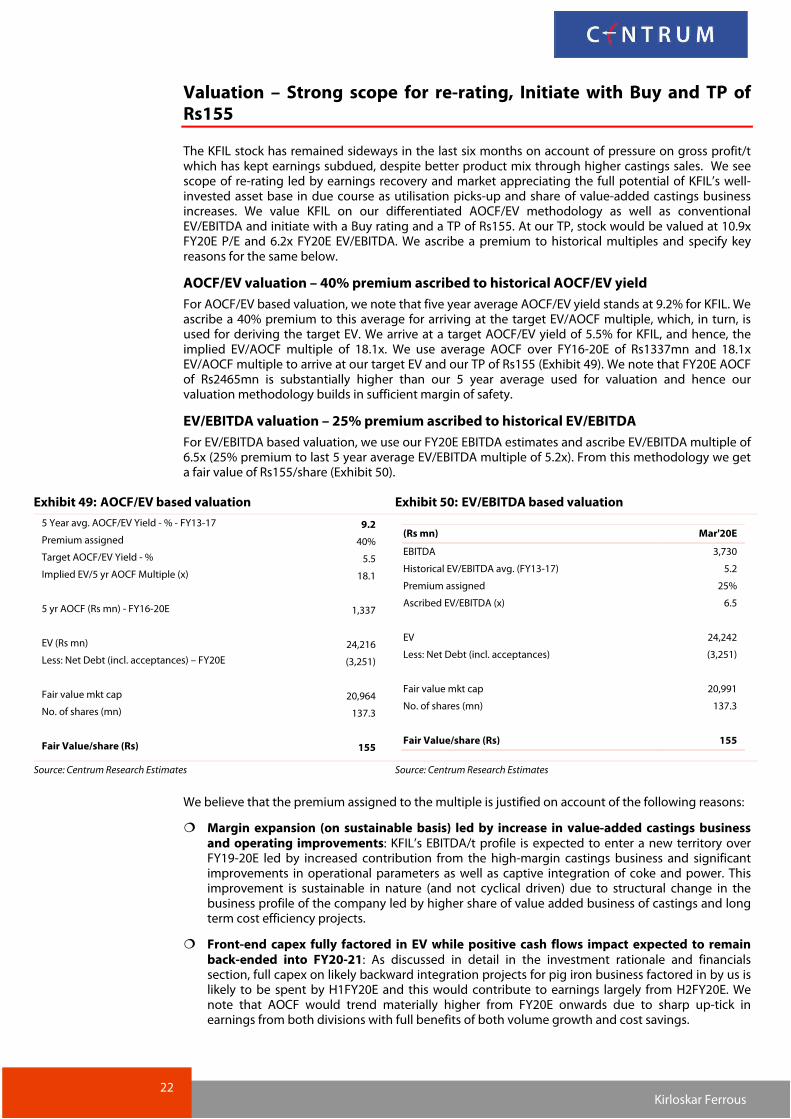

Valuation – Strong scope for re-rating, Initiate with Buy and TP of Rs155

The KFIL stock has remained sideways in the last six months on account of pressure on gross profit/t which has kept earnings subdued, despite better product mix through higher castings sales. We see scope of re-rating led by earnings recovery and market appreciating the full potential of KFIL’s well-invested asset base in due course as utilisation picks-up and share of value-added castings business increases. We value KFIL on our differentiated AOCF/EV methodology as well as conventional EV/EBITDA and initiate with a Buy rating and a TP of Rs155. At our TP, stock would be valued at 10.9x FY20E P/E and 6.2x FY20E EV/EBITDA. We ascribe a premium to historical multiples and specify key reasons for the same below.

AOCF/EV valuation – 40% premium ascribed to historical AOCF/EV yield

For AOCF/EV based valuation, we note that five year average AOCF/EV yield stands at 9.2% for KFIL. We ascribe a 40% premium to this average for arriving at the target EV/AOCF multiple, which, in turn, is used for deriving the target EV. We arrive at a target AOCF/EV yield of 5.5% for KFIL, and hence, the implied EV/AOCF multiple of 18.1x. We use average AOCF over FY16-20E of Rs1337mn and 18.1x EV/AOCF multiple to arrive at our target EV and our TP of Rs155 (Exhibit 49). We note that FY20E AOCF of Rs2465mn is substantially higher than our 5 year average used for valuation and hence our valuation methodology builds in sufficient margin of safety.

EV/EBITDA valuation – 25% premium ascribed to historical EV/EBITDA

For EV/EBITDA based valuation, we use our FY20E EBITDA estimates and ascribe EV/EBITDA multiple of 6.5x (25% premium to last 5 year average EV/EBITDA multiple of 5.2x). From this methodology we get a fair value of Rs155/share (Exhibit 50).

Exhibit 49: AOCF/EV based valuation Exhibit 50: EV/EBITDA based valuation

9.2

40%

5.5

5 Year avg. AOCF/EV Yield - % - FY13-17

Premium assigned

Target AOCF/EV Yield - %

Implied EV/5 yr AOCF Multiple (x) 18.1

5 yr AOCF (Rs mn) - FY16-20E 1,337

EV (Rs mn) 24,216

Less: Net Debt (incl. acceptances) – FY20E (3,251)

Fair value mkt cap 20,964

No. of shares (mn) 137.3

Fair Value/share (Rs) 155

(Rs mn) Mar'20E

3,730

5.2

25%

EBITDA

Historical EV/EBITDA avg. (FY13-17)

Premium assigned

Ascribed EV/EBITDA (x) 6.5

EV 24,242

Less: Net Debt (incl. acceptances) (3,251)

Fair value mkt cap 20,991

No. of shares (mn) 137.3

Fair Value/share (Rs) 155

Source: Centrum Research Estimates Source: Centrum Research Estimates

We believe that the premium assigned to the multiple is justified on account of the following reasons:

� Margin expansion (on sustainable basis) led by increase in value-added castings business and operating improvements: KFIL’s EBITDA/t profile is expected to enter a new territory overFY19-20E led by increased contribution from the high-margin castings business and significantimprovements in operational parameters as well as captive integration of coke and power. Thisimprovement is sustainable in nature (and not cyclical driven) due to structural change in thebusiness profile of the company led by higher share of value added business of castings and longterm cost efficiency projects.

� Front-end capex fully factored in EV while positive cash flows impact expected to remain back-ended into FY20-21: As discussed in detail in the investment rationale and financialssection, full capex on likely backward integration projects for pig iron business factored in by us islikely to be spent by H1FY20E and this would contribute to earnings largely from H2FY20E. Wenote that AOCF would trend materially higher from FY20E onwards due to sharp up-tick inearnings from both divisions with full benefits of both volume growth and cost savings.

23 Kirloskar Ferrous

� Increase in return ratios with efficient capital management: KFIL’s return ratios are expected to see sharp improvement by FY20E led by efficient capital management coupled with sustainable increase in share of high-margin castings business. Return ratio profile is expected to improve sustainably for KFIL and merits a multiple re-rating.

� Undiscovered and under-owned at Institutional level: We believe that the stock has largely remained undiscovered and out of the radar of institutional investors and its capability in the castings segment has not been recognised; this could be one of the reasons for its lower valuations in the past. We see scope for re-rating once profitability improves and KFIL’s capabilities get recognised. We thus believe that premium to historical valuations is justified on account of superior fundamentals, future growth opportunity, and strong management capabilities.

KFIL trading at attractive adjusted cash flow yield, leaving scope for re-rating

We have plotted KFIL’s AOCF yield on corresponding year’s enterprise value. KFIL’s cash flow yield stands at attractive levels of 11.4%/15.9% on FY19E/20E basis, leaving strong scope for re-rating.

Exhibit 51: KFIL trades at attractive adjusted cash flow yield

Source: Centrum Research Estimates

11.4

18.4

16.3

11.2

8.1

4.2

11.4

15.9

0

4

8

12

16

20

0

500

1000

1500

2000

2500

3000

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

AOCF - Rs mn AOCF-EV Yield - % (RHS)

24 Kirloskar Ferrous

Exhibit 52: 1 year forward EV/EBITDA chart Exhibit 53: 1 year forward P/E chart

Source: Bloomberg, Centrum Research Estimates Source: Bloomberg, Centrum Research Estimates

Exhibit 54: Peer comparison – Historical Financials

Company Net Sales (Rs mn) EBITDA (Rs mn) PAT (Rs mn) EBITDA Margin % PAT Margin %

FY15 FY16 FY17 FY15 FY16 FY17 FY15 FY16 FY17 FY15 FY16 FY17 FY15 FY16 FY17

Kirloskar Ferrous 13,651 11,139 11,337 1,490 1,509 1,756 493 578 907 10.9 13.6 15.5 3.6 5.2 8.0

Nelcast 5,449 5,607 5,746 460 643 640 219 319 340 8.4 11.5 11.1 4.0 5.7 5.9

Jayaswal Neco Industries 30,243 26,326 25,162 3,593 2,628 2,800 3 (936) (4,593) 11.9 10.0 11.1 0.0 (3.6) (18.3)

Steelcast 791 1,370 1,343 0 263 154 (185) 1 24 (0.1) 19.2 11.5 (23.4) 0.1 1.8

Alicon Castalloy 7,136 7,489 7,728 709 769 868 198 222 262 9.9 10.3 11.2 2.8 3.0 3.4

Precision Camshafts 5,144 4,381 4,430 1,374 1,192 1,006 476 549 609 26.7 27.2 22.7 9.3 12.5 13.7

Company CAGR 15-17 (%) ROE % Div Yield % P/E (x) EV/EBITDA (x)

Revenue EBITDA PAT FY15 FY16 FY17 FY15 FY16 FY17 FY15 FY16 FY17 FY15 FY16 FY17

Kirloskar Ferrous (8.9) 8.6 35.7 11.2 12.2 16.9 2.5 2.4 2.3 13.9 12.5 11.4 5.5 5.5 6.4

Nelcast 2.7 18.0 24.4 8.0 10.9 10.7 2.1 1.4 1.5 12.7 14.4 14.9 7.1 7.8 8.2

Jayaswal Neco Industries (8.8) (11.7) NM 0.0 (4.3) (24.4) 0.0 0.0 0.0 NM (5.5) (1.1) 13.4 16.8 15.5

Steelcast 30.3 NM NM NM NM 3.2 - - - (3.7) 670.2 59.9 NM 3.3 8.2

Alicon Castalloy 4.1 10.6 14.9 16.9 16.3 16.4 1.1 1.3 0.9 11.4 16.1 16.6 5.5 6.8 7.6

Precision Camshafts (7.2) (14.5) 13.0 23.1 14.7 11.5 - 0.7 1.1 - 23.6 22.9 - 10.7 11.2

Source: Bloomberg, Centrum Research

0

3

6

9

12

Nov-11

May-12

Nov-12

May-13

Nov-13

May-14

Nov-14

May-15

Nov-15

May-16

Nov-16

May-17

Nov-17

EV/EBITDA Mean

Mean + Std Dev Mean - Std Dev

0

5

10

15

20

25

30

35

Nov-11

May-12

Nov-12

May-13

Nov-13

May-14

Nov-14

May-15

Nov-15

May-16

Nov-16

May-17

Nov-17

P/E Mean

Mean + Std Dev Mean - Std Dev

25 Kirloskar Ferrous

Key risks to our thesis

� Margin pressure due to higher competition from peers: The domestic castings (foundry) industry is fragmented and has unutilised capacity. Though demand outlook is good and the business is characterised by product positioning and client relationships, thus limiting competition-related margin pressures, a sudden increase in activity from some players with low utilisation could pose a potential risk to margins.

� Client concentration: KFIL has large exposures to some of its big clients and is exposed to risks associated with any issues in the volume trajectories of its large clients. However, the company has been able to increase its client base significantly in last few years and has been reducing this risk over time.

� High volatility in raw material prices: KFIL’s key raw materials are iron ore, scrap, coke and coking coal which have witnessed sharp fluctuations in the past. The raw material price fluctuations are not easily passed on to customers and any major volatility in raw material prices would impact gross margins and profitability.

� Foreign exchange fluctuations: KFIL imports its key raw materials like coking coal/coke and has to prudently manage its foreign exchange risk on the same. The company has been entering into forward covers for hedging and has incurred forex related costs both on account of losses as well as premium on contracts. The forex related costs have been brought under control through prudent management over the last few years but risk to earnings could potentially arise again.

Exhibit 55: KFIL forex gain/loss trend

(Rs mn) FY12 FY13 FY14 FY15 FY16 FY17

Forex gains (in other inc.) 0 0 0 2 0 2

Forex loss (in other exp) 178 137 1 0 0 0

PBT 557 624 580 718 853 1,216

PBT (excl. forex gain/loss) 735 761 580 716 853 1,214

Source: Centrum Research

� Transition of auto industry to electric vehicles over long term: Over the longer term, it is expected that a major portion of automobile industry might move towards electric vehicles that will not need internal combustion engines. Some of KFIL’s products find applications in engines of the CV industry and could see the impact of transition to EV in long term. However, we believe that EV transition would first be felt in passenger vehicles rather than CVs and KFIL doesn’t have any exposure to passenger vehicles segment currently. Also, we believe that EV transition could be a very long process stretching to 15-20 years and threat of the same in next ten years in KFIL’s segments remains low.

26 Kirloskar Ferrous

Exhibit 56: Shareholding pattern (%)

Sep-17 Jun-17 Mar-17 Dec-16

Promoter 59.6 59.6 59.6 59.5

FIIs 0.6 0.6 0.6 0.5

DIIs 2.6 1.8 1.8 1.8

Others 37.2 38.0 38.0 38.2

Source: BSE

Company Background