Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development Danilo De Rossi March 2015 About the Author I have over twenty years of business experience, of which over ten at senior level working in multinational/multicultural environments. My focus is to achieve growth by developing value chain positioning strategies and improving profitability through process, competitiveness and organisational alignment/development. This paper is part of a set of researches that were initially prepared for my MBA. For my full profile, or to discuss opportunities to contribute to business research, please visit uk.linkedin.com/in/daniloderossi/

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

!!!!!!!!Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development !Danilo De Rossi!March 2015 !!!

About the Author!I have over twenty years of business experience, of which over ten at senior level working in multinational/multicultural environments. My focus is to achieve growth by developing value chain positioning strategies and improving profitability through process, competitiveness and organisational alignment/development. This paper is part of a set of researches that were initially prepared for my MBA. !For my full profile, or to discuss opportunities to contribute to business research, please visit uk.linkedin.com/in/daniloderossi/

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 1

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development!

!Table of contents!

0! Executive Summary1! Introduction to Business Process Outsourcing!2! Major Countries and Regions Involved in Outsourcing and Offshoring!3! Key Drivers and Opportunities of Offshoring!3.1 Cost Reduction 3.2 Focus on Core Operations 3.3 Untapping Global Talent Pools 3.4 Innovation & Learning 3.5 Other Key BPO Drivers 4! Key Risks and Mitigation Strategies!4.1 Cost Saving Mirage 4.2 Lack of Process Maturity 4.3 Heavy Turnover of Key Personnel 4.4 Lack of Understanding or Consensus of Target Business Model 4.5 Competence Gap 4.6 Cultural Misalignment 4.6.1 Client and Vendor Interaction 4.6.2 Vendor’s Direct Interactions with the Client’s end Customers 4.7 Geopolitical Risks 4.8 Performance, Key Performance Indicators, Service Level Agreements!5! Conclusions!6! References!7! Bibliography!8! Websites!9.1! Appendix: SCOR Model overview!9.2! Appendix: Factors in choosing a location!!!0. Executive Summary!This research provides an overview of Business Process Outsourcing (BPO) and Offshoring practices, highlighting opportunities and drivers as well as risks and mitigation strategies. The conclusion is that BPO can contribute to the improvement of Supply Chain performance, reducing costs and providing access to talents and innovation. However, it also presents significant risks that need to be managed proactively, through the selection of the right business models, metrics and an adequate process management framework. !!!

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 2

1. Introduction!According to Gartner: “Business Process Outsourcing (BPO) can be defined as the delegation of one or more IT intensive business processes to an external provider who, in turn, administrates and manages selected processes based upon defined and measurable performance metrics” (Gartner, 2011). When these processes are executed by vendors in a different country, it is known as offshore outsourcing or offshoring. Today the service offering is not just confined to IT activities, but also to processes in Customer Services, Human Resources and Financial functions. One of the key enablers of BPO has been the cost reduction of global communication and the spread of the internet, which is now the backbone of the global economy. !!According to S. Helper and M. Sato (2010): “reduced transportation and communication costs have led to vertical dis-integration and the replacement of dinosaur-like large companies with gazelle-like firms, connected to each other in flexible and modular networks”.

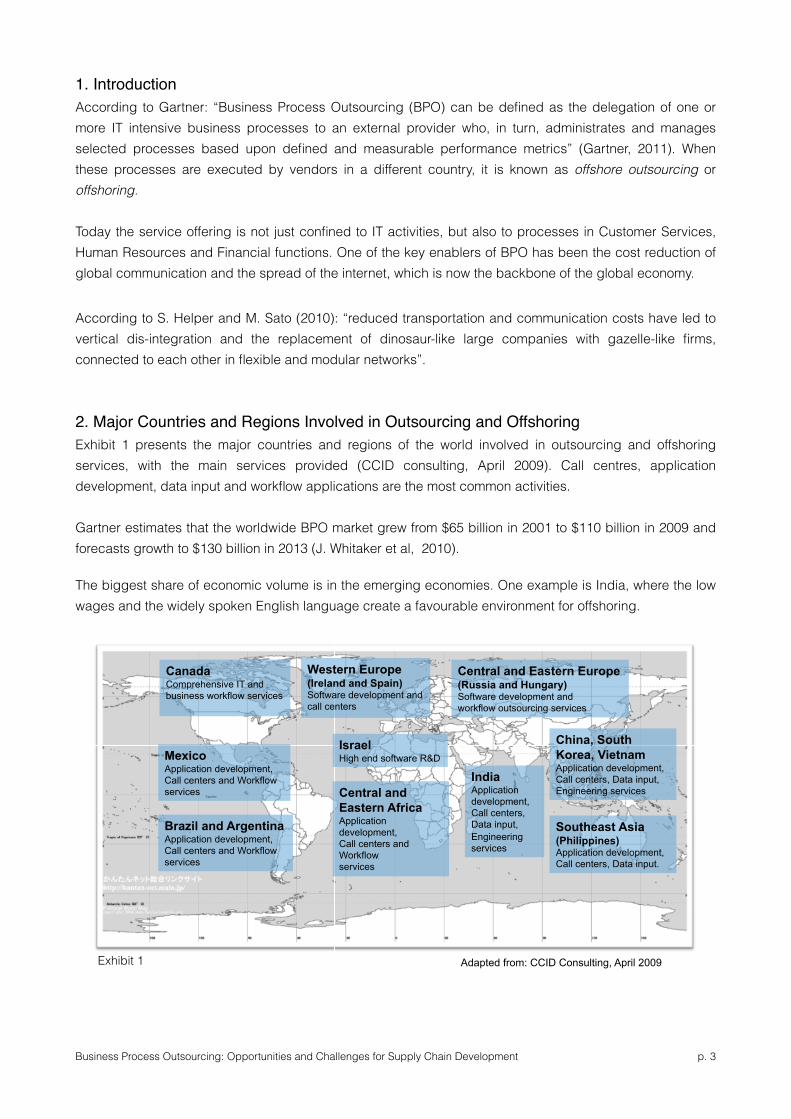

!2. Major Countries and Regions Involved in Outsourcing and Offshoring!Exhibit 1 presents the major countries and regions of the world involved in outsourcing and offshoring services, with the main services provided (CCID consulting, April 2009). Call centres, application development, data input and workflow applications are the most common activities. !Gartner estimates that the worldwide BPO market grew from $65 billion in 2001 to $110 billion in 2009 and forecasts growth to $130 billion in 2013 (J. Whitaker et al, 2010).

The biggest share of economic volume is in the emerging economies. One example is India, where the low wages and the widely spoken English language create a favourable environment for offshoring.

!Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 3

Canada Comprehensive IT and business workflow services

Mexico Application development, Call centers and Workflow services

Brazil and Argentina Application development, Call centers and Workflow services

Western Europe (Ireland and Spain) Software development and call centers

Central and Eastern Africa Application development, Call centers and Workflow services

Israel High end software R&D

Central and Eastern Europe (Russia and Hungary) Software development and workflow outsourcing services

China, South Korea, Vietnam Application development, Call centers, Data input, Engineering services

India Application development, Call centers, Data input, Engineering services

Southeast Asia (Philippines) Application development, Call centers, Data input.

Adapted from: CCID Consulting, April 2009 Exhibit 1

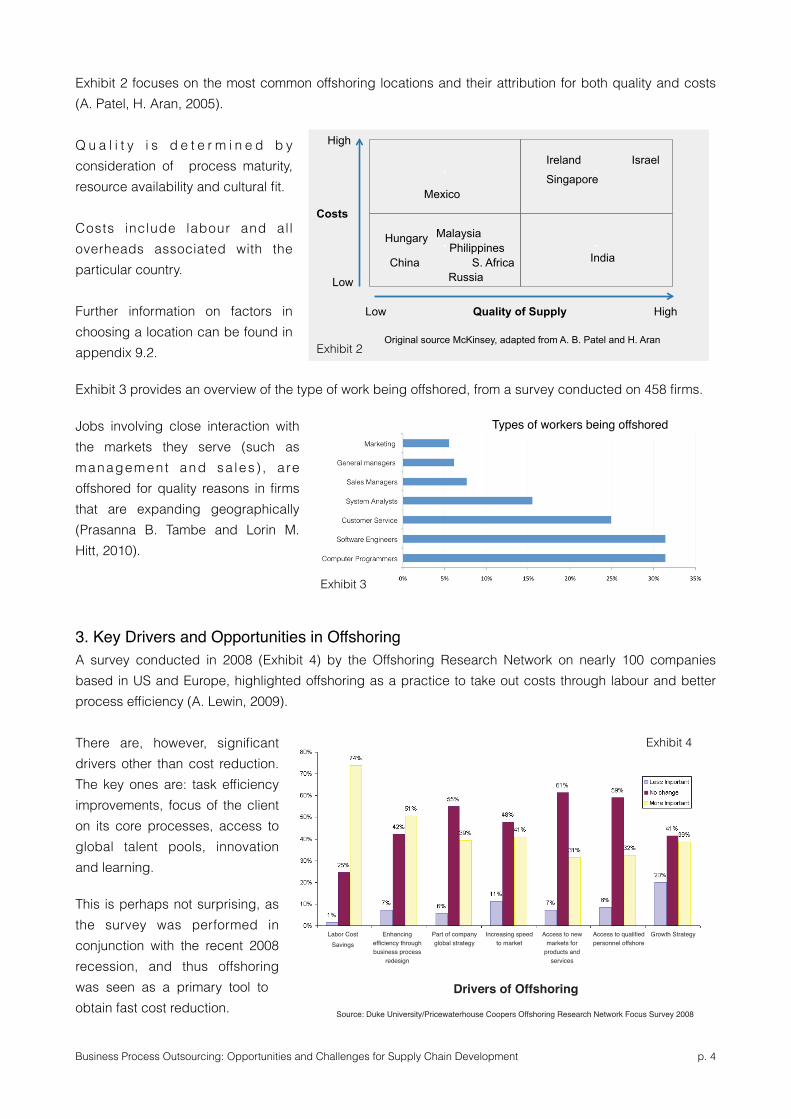

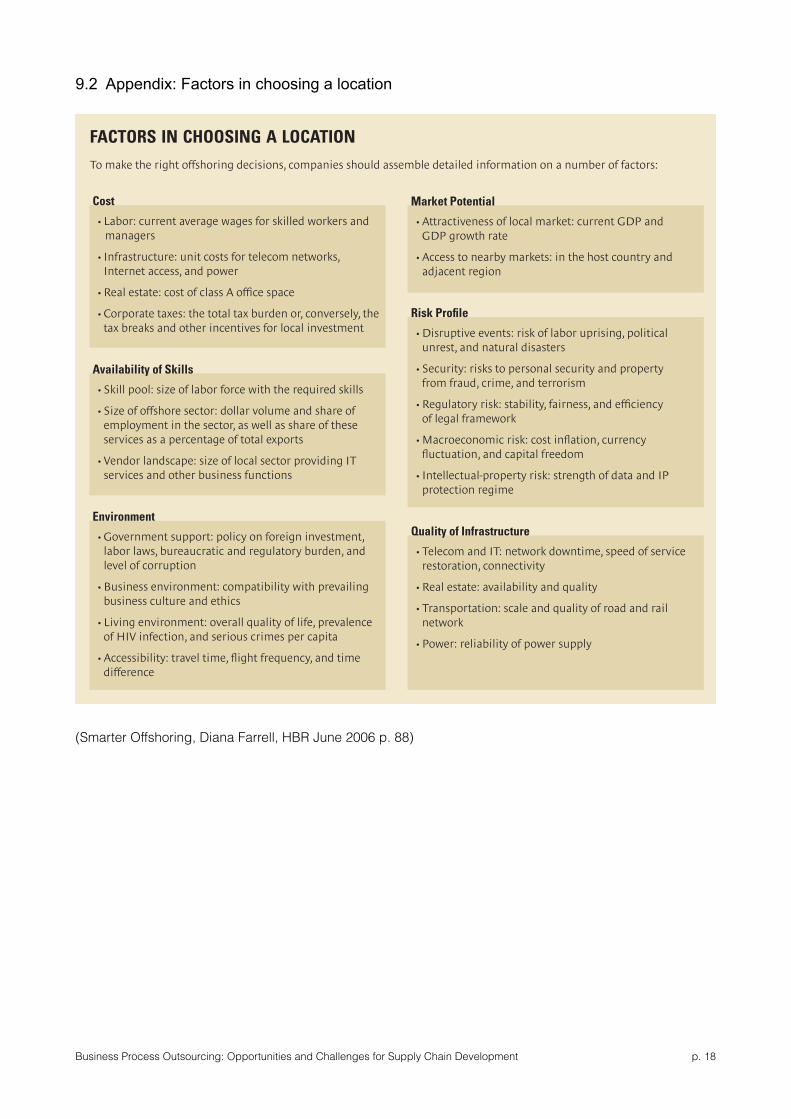

Exhibit 2 focuses on the most common offshoring locations and their attribution for both quality and costs (A. Patel, H. Aran, 2005). !Q u a l i t y i s d e t e r m i n e d b y consideration of process maturity, resource availability and cultural fit. !Costs include labour and al l overheads associated with the particular country. !Further information on factors in choosing a location can be found in appendix 9.2.!

Exhibit 3 provides an overview of the type of work being offshored, from a survey conducted on 458 firms.

Jobs involving close interaction with the markets they serve (such as management and sa les ) , a re offshored for quality reasons in firms that are expanding geographically (Prasanna B. Tambe and Lorin M. Hitt, 2010).

!!3. Key Drivers and Opportunities in Offshoring!A survey conducted in 2008 (Exhibit 4) by the Offshoring Research Network on nearly 100 companies based in US and Europe, highlighted offshoring as a practice to take out costs through labour and better process efficiency (A. Lewin, 2009). There are, however, significant drivers other than cost reduction. The key ones are: task efficiency improvements, focus of the client on its core processes, access to global talent pools, innovation and learning.

This is perhaps not surprising, as the survey was performed in conjunction with the recent 2008 recession, and thus offshoring was seen as a primary tool to obtain fast cost reduction.

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 4

Shared Services News/February 2009 19

column / off shoring in a struggling economy

Getting Serious About Offshoring in a Struggling EconomyThe fi nancial crisis introduces new dynamics with possible direct consequences for companies that are outsourcing services off shore or are considering such strategies. Business press suggests that companies exercise more caution and favor a defensive strategy rather than taking an aggressive approach when planning their moves. But how does this mark signifi cant change in off shoring implementations? The answer, we have concluded, is that businesses plan to continue to implement their strategies for sourcing some functions off shore, and may even accelerate such plans.

n this article, we discuss the recent findings drawn from an Offshoring Research

Network (ORN) 1. focused survey conducted on nearly 100 companies based in the United States and Europe about their plans to source some job functions and business processes offshore. The survey aims to detect early signals that companies are adapting their aggressive plans to expand existing outsourcing projects and to initiate new ones.

The focused survey explored the following three key issues:

• To what extent have the financial crisis and the unfolding economic conditions changed the strategic drivers for offshoring at the responding company? • What are specific measures that existing or future offshoring companies are taking or considering in the next six to 12 months in response to the economic situation?• To what extent are companies rethinking or modifying their financial strategies for expanding or initiating new offshoring projects?

The near-term impact and corporate responses to the global economic downturn have been multifaceted. Organizations are

By Arie Y. Lewin, Professor of Strategy and International Business Director, Center for International Business Education and Research, Lead Principal Investigator, International ORN Project, Duke University CIBER, The Fuqua School of Business; Silvia Massini, Senior Lecturer in Economics and Technology Management, Manchester Institute of Innovation Research, Manchester Business School, University of Manchester;Nidthida Perm-Ajchariyawong, ORN Research Associate, Duke University CIBER, The Fuqua School of Business; Derek Sappenfi eld, Director, Shared Services and Outsourcing Advisory, PricewaterhouseCoopers; Jeff Walker, Director, Shared Services and Outsourcing Advisory, PricewaterhouseCoopers

more focused on reducing costs, developing greater visibility to their markets, and improving transparency into their operations. As revenue plateaus or declines and margins shrink, organizations must determine how best to optimize cash flow and working capital. Workforce reductions are often a consideration but must be executed without putting the business at operational risk. New initiatives requiring any investment are receiving tremendous scrutiny, and most are ending up on the back burner as resources are reallocated to activities closer to the core. Expansions into new markets or products/lines of service are being deferred unless the forecasted ROI is overwhelming. There is a need for greater transparency into operations so the right optimization decisions can be made and for risk mitigation planning so the organization can develop appropriate responses to additional economic hardships that may persist through 2009.

Given these concerns and modifications in short-term strategy, the key message from respondent companies is that in the near term most companies are not planning any drastic changes in their outsourcing offshoring strategies. Exhibit 1 summarizes the changes, identified by respondents as a

result of the financial crisis, in the strategic drivers underlying offshoring decisions.I

>>

Exhibit 1: Changes in the strategic drivers of offshoring decisions

Increased emphasis on “taking out costs”The most prominent change is labor cost savings. The findings from the ORN survey conducted in November 2008 show that labor cost savings have become even more important (relative to ORN 2007/2008 findings) in the current economic situation. Follow-up interviews and comments from respondents indicate that companies are concerned about pressure on margins and declining top-line growth. Not surprisingly, a renewed and increased emphasis on “taking

Labor CostSavings

Enhancing effi ciency throughbusiness process

redesign

Part of companyglobal strategy

Increasing speed to market

Access to new markets for

products andservices

Access to qualifi edpersonnel offshore

Growth Strategy

Drivers of Offshoring

Source: Duke University/Pricewaterhouse Coopers Offshoring Research Network Focus Survey 2008

Exhibit 4

`

`

`

`

High

Low

High Low Quality of Supply

Costs

Mexico

Hungary Malaysia Philippines

S. Africa Russia

China India

Israel Ireland

Singapore

Original source McKinsey, adapted from A. B. Patel and H. Aran Exhibit 2

Types of workers being offshored

Exhibit 3

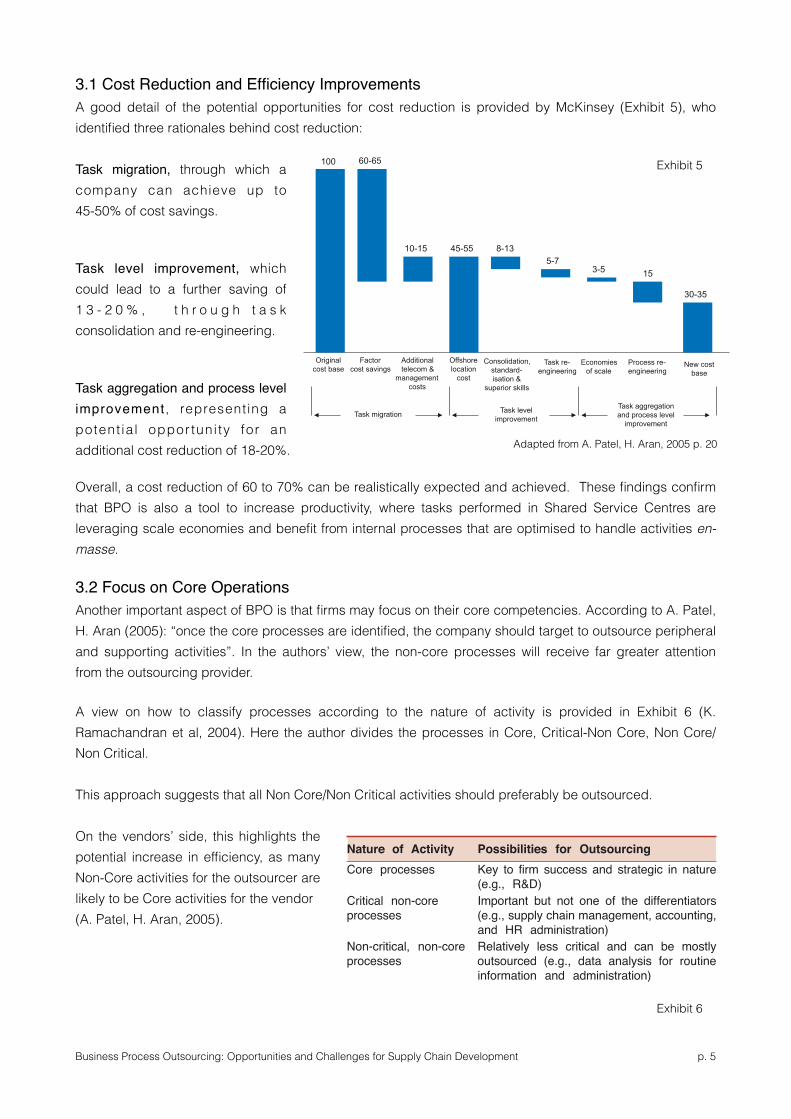

3.1 Cost Reduction and Efficiency Improvements!A good detail of the potential opportunities for cost reduction is provided by McKinsey (Exhibit 5), who identified three rationales behind cost reduction: Task migration, through which a company can achieve up to 45-50% of cost savings. !Task level improvement, which could lead to a further saving of 1 3 - 2 0 % , t h r o u g h t a s k consolidation and re-engineering. !Task aggregation and process level improvement , representing a potent ia l oppor tuni ty for an additional cost reduction of 18-20%.

Overall, a cost reduction of 60 to 70% can be realistically expected and achieved. These findings confirm that BPO is also a tool to increase productivity, where tasks performed in Shared Service Centres are leveraging scale economies and benefit from internal processes that are optimised to handle activities en-masse.

3.2 Focus on Core OperationsAnother important aspect of BPO is that firms may focus on their core competencies. According to A. Patel, H. Aran (2005): “once the core processes are identified, the company should target to outsource peripheral and supporting activities”. In the authors’ view, the non-core processes will receive far greater attention from the outsourcing provider. !A view on how to classify processes according to the nature of activity is provided in Exhibit 6 (K. Ramachandran et al, 2004). Here the author divides the processes in Core, Critical-Non Core, Non Core/Non Critical. !This approach suggests that all Non Core/Non Critical activities should preferably be outsourced. !On the vendors’ side, this highlights the potential increase in efficiency, as many Non-Core activities for the outsourcer are likely to be Core activities for the vendor (A. Patel, H. Aran, 2005).

!!

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 5

nants of outsourcing:• cost reduction• core competence focus• flexibility while retaining control• competitive advantage through strategic

outsourcing.In essence, the logic of outsourcing of services is

based on sound economic principles. Learnings from theexperiences on the manufacturing front suggest thatoutsourcing will continue to happen within or acrossgeographical boundaries.

BPO AND ITES: THE LINK

The rapid growth in ITES has often given an impressionthat it is quite independent of BPO which is not true.As the term suggests, ITES includes services that can beoutsourced using the powers of IT. The extent to whichIT can be leveraged varies under the influence ofsuitability to industry, location, time, costs, and mana-gerial perception of the risks involved. As shown inTable 2, the processes that can be outsourced can beclassified into IT-enabled and others. Similarly, all theorganizational processes can be broadly grouped intothree depending on the extent to which each is a coreprocess, critical but non-core, and non-critical and non-core. The boom in ITES is primarily in customer care,followed by administration and banking, all at the lowerend of an intellectual pyramid, but involving largenumber of people . However, the significant proportionof people involved in content development is an indi-cator of possible opportunities at the higher levels of thepyramid [Table 1(a)].

The primary resources for building execution capa-bilities are capital and technology apart from people-based resources. The building of execution capabilityrequires investment in operations infrastructure which,in turn, heavily depends on the intended or planned sizeof operations in terms of scale. The scope for variationin the complexity of the task outsourced and level of

expertise required for execution is enormous, dependingon the Functional Value Captured (FVC). For instance,Raman Roy, founder of Spectramind divided the tele-working pie into five slices in the ascending order ofvalue (The Economist, 2001) as follows:• Data entry and conversion which includes medical

transcription.• Rule-set processing in which a teleworker makes

judgements based on a set of rules set by thecustomer.

• Problem solving in which a teleworker has morediscretion; the rules here are fluid and less amenableto structuring than in the rule-set processing genre.

• Direct customer interaction in which the teleworkerhandles more elaborate interaction with the client’scustomers. Services here could include support andmaintenance and payment collections.

• Expert ‘knowledge services’ which require specialists(with the help of a database).‘Teleworking’ as described above is amenable to

any definition of ITES involving remote processingservices of information (data, voice, images, multime-dia). The Economist (2001) described the above catego-rization as extendable to ‘just any service that is deliv-erable over fibre-optic wire’ which is intuitively under-standable as well. The higher the FVC, the higher arethe entry barriers. In the normal course, returns, marketscope, and growth potential are higher for higher FVCs(Porter, 1985).

As mentioned earlier, many of the processes thatcould not be outsourced earlier are done so now thanksto the developments on the IT front globally and grow-ing level of comfort parent firms have with BPO firmsin countries such as India. It is relevant to note here thatthe relocation of business processes including ITES wasinitially intra-national, i.e., to low-cost locations withinthe same country, but significant breakthroughs indigitization technologies and data transmission withresultant savings in costs enabled development of thispractice to travel across continents. Consequently, la-bour cost, skill availability, and infrastructure qualitybecame the determinants for relocating services.

THEORY OF THE FIRM AND ITES-BPO

The implications of the theoretical discussion are al-ready evident in the Indian BPO scene. The industry,particularly the ITES sector, has grown manifold. Thenumber of BPO professionals (most of whom belong to

Table 2: IT-enabled Services Possibilities

Nature of Activity Possibilities for OutsourcingCore processes Key to firm success and strategic in nature

(e.g., R&D)Critical non-core Important but not one of the differentiatorsprocesses (e.g., supply chain management, accounting,

and HR administration)Non-critical, non-core Relatively less critical and can be mostlyprocesses outsourced (e.g., data analysis for routine

information and administration)

VIKALPA • VOLUME 29 • NO 1 • JANUARY - MARCH 2004 53Exhibit 6

Original cost base

Factor cost savings

Additional telecom &

management costs

Offshore location

cost

Consolidation, standard- isation &

superior skills

Task re- engineering

Economies of scale

Process re- engineering

New cost base

100 60-65

10-15 45-55 8-13 5-7

3-5 15

30-35

Task migration Task level improvement

Task aggregation and process level

improvement

Exhibit 5

Adapted from A. Patel, H. Aran, 2005 p. 20

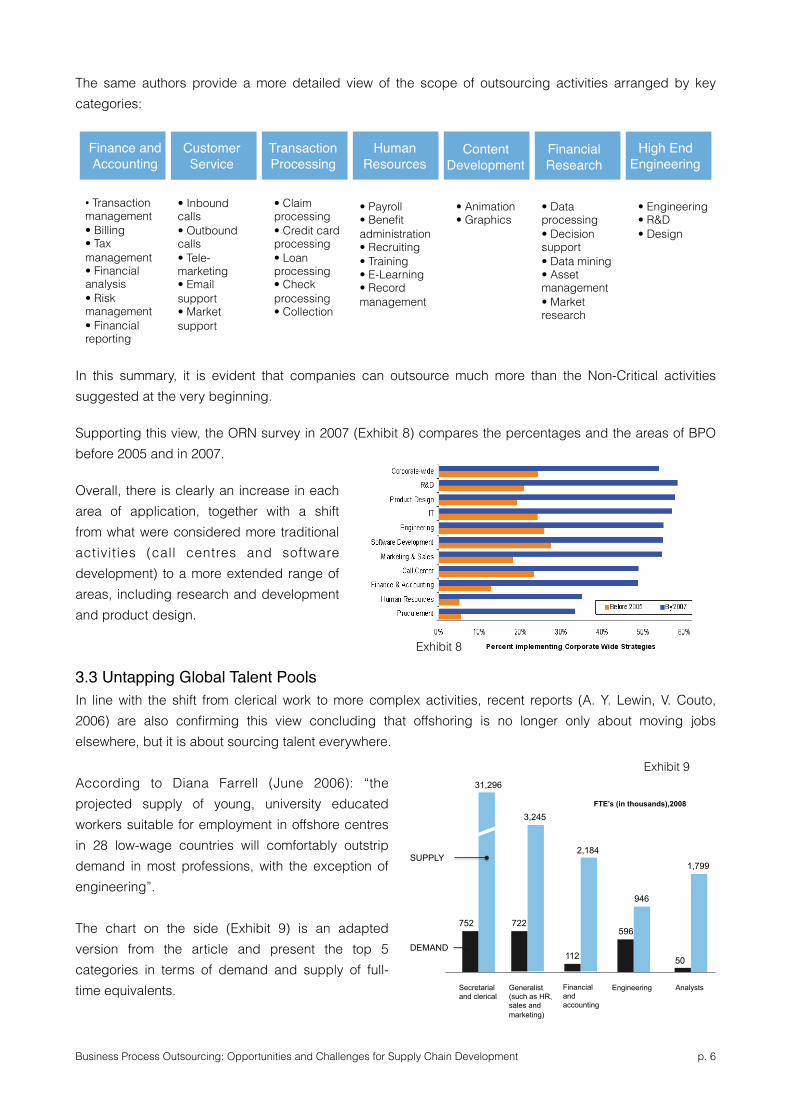

The same authors provide a more detailed view of the scope of outsourcing activities arranged by key categories:

In this summary, it is evident that companies can outsource much more than the Non-Critical activities suggested at the very beginning.

Supporting this view, the ORN survey in 2007 (Exhibit 8) compares the percentages and the areas of BPO before 2005 and in 2007.

Overall, there is clearly an increase in each area of application, together with a shift from what were considered more traditional activities (call centres and software development) to a more extended range of areas, including research and development and product design.

!3.3 Untapping Global Talent Pools!In line with the shift from clerical work to more complex activities, recent reports (A. Y. Lewin, V. Couto, 2006) are also confirming this view concluding that offshoring is no longer only about moving jobs elsewhere, but it is about sourcing talent everywhere. !According to Diana Farrell (June 2006): “the projected supply of young, university educated workers suitable for employment in offshore centres in 28 low-wage countries will comfortably outstrip demand in most professions, with the exception of engineering”. !The chart on the side (Exhibit 9) is an adapted version from the article and present the top 5 categories in terms of demand and supply of full-time equivalents. !Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 6

column / off shoring in a struggling economy (cont'd)

Moreover, as a result of the financial crisis, companies are under pressure to increase their capital base. Together, these factors pressure companies to consider a drastic move, such as selling their captive operations to third-party service providers. Theoretically, third-party outsourcing provides firms the flexibility to scale up or down quickly and help them keep the cost per trade at a minimum.

One example is Citigroup’s sell-off deal with Tata Consultancy Services (TCS). In early October 2008, TCS signed an agreement with Citigroup to acquire its Indian-based captive business processing unit for $505 million in return for a seven-year service contract. Following Citigroup’s footstep, Motorola announced a plan to sell its software development unit in Malaysia to Satyam, India’s No. 4 software service exporter. Exhibit 6 summarizes key captive acquiring deals announced in 2008.

In spite of these few examples, the results from our survey show a more conservative approach adopted by respondent companies to deal with the declining economy. While efficiency enhancement and cost reduction are at the top of the agenda, only a few companies mentioned an option of spinning off their captive operations to a provider to repatriate capital. Focused interviews with executives from respondent companies reflect two main concerns over spinning off captive operations. First, many companies indicate that such options require a significant amount of time and effort to negotiate. Second, and perhaps just as important, service providers are unlikely to have the pool of capital resources for financing the acquisition of a significant number of captives. At present, moves such as TCS’ are fairly rare. In fact, like other businesses, service providers are also tightening their budget and being conservative about any investment that affects their top-line growth, such as acquiring

22 Shared Services News/February 2009

Exhibit 3: The inefficiency trap: Potential for immediate efficiency improvements

Exhibit 4: Percentage of companies implementing corporate wide strategies before 2005 versus by end of 2007

weaker rivals or customers’ captives. In addition to the emerging trend of

captive spin-off, there are increasingly more reports in business presses about acquisitions between service providers. In one of the largest deals of this year, Hewlett-Packard (HP) signed an agreement to purchase BPO and IT giant EDS at a value of $13.9 billion. In line with the concern arising from buy-side companies, this consolidation phenomenon demonstrates service providers’ pressure for cost-cutting and their attempt to increase efficiency through achieving economies of scale. Nonetheless, the continuing financial crisis and shrinking free cash flow can be expected to slow the trend toward consolidation between service providers and acquisition of captive operations.

In response to the question about financing options under consideration (see Exhibit 7), more than 30 percent of companies noted they are considering delaying implementation of new projects because of required up-front costs. Some revealed that providers could influence a decision by offering to absorb these costs. Similarly, a few companies said they are considering spreading implementation time lines as well as cancelling or postponing discretionary projects, especially software development projects.

Exhibit 7: Financing options in consideration

SSN’S ADVISORY BOARD Comments:

Know How to Lead Shared Services in Times of Crisis In Q4 ‘08 alone we saw fi nancial meltdowns across global markets, a major terrorist attack on one of our biggest sourcing cities and turmoil on the stock exchanges as share prices roller-coaster daily. It’s hard to know what to expect.

Chris Gunning, Director Global Shared Services - Europe, India and Asia Pacifi c, Unisys puts things in perspective for us. Having been in Bangalore during the Mumbai attacks, he shares his top tips for leading from the front during a crisis—be it economic, or otherwise.

“The Dos and Don’ts of Shared Services Leadership in a Crisis”

• Do tighten up your belt.• Do get tough with expense scrutiny and management. • Don’t forget that Cash still remains King – in fact, it is more important than ever.• Don’t take your eye off the ball as far as internal controls or Sarbanes Oxley goes. • Do continue to talk to your customers more than ever – internal and external.• Do continue to publicize internally in your company, that shared services is there to save you money and generate labor arbitrage – and that it should be a more important vehicle than ever in the current challenging times. • Don’t forget your employees.• Do continue to communicate to your employees globally how important they are in terms of your overall strategy. • Don’t forget good balance sheet control.• Don’t panic. • Do market yourself to bring more work into shared services.• Do continue to look to expand your SSC portfolio to save the company even more money. • Do not be afraid of India or other global locations in the light of the recent Mumbai events. • Don’t forget most of the world is in the same boat as you and your company. • Don’t get stressed! Key Opportunities For 2009I don’t envision huge changes from what we are doing anyway—but hey, this is shared services, that could change tomorrow! • More off shoring.• More governance. • More focus on customer satisfaction. • More focus on SSC employees skills set and development. • More work moved into the SSC portfolio

Delaying projects Continuing projectfi nancing as is

Spreading theimplementation of

projects over a longerperiod

Having serviceprovider fi nance

projects

Other Soliciting 3rd partyfi nancing

Financing OptionsSource: Duke University/Pricewaterhouse Coopers Offshoring Research Network Focus Survey 2008

Exhibit 8

752

31,296

SUPPLY

DEMAND

Secretarial and clerical

3,245

2,184

946

1,799

722

112

596

50

Generalist (such as HR, sales and marketing)

Financial and accounting

Engineering Analysts

FTE’s (in thousands),2008

Exhibit 9

Finance and Accounting"

CustomerService"

Transaction"Processing"

Human Resources"

Content Development"

Financial Research"

High End Engineering"

• Transaction management • Billing • Tax management • Financial analysis • Risk management • Financial reporting

• Inbound calls • Outbound calls • Tele- marketing • Email support • Market support

• Claim processing • Credit card processing • Loan processing • Check processing • Collection

• Payroll • Benefit administration • Recruiting • Training • E-Learning • Record management

• Animation • Graphics

• Data processing • Decision support • Data mining • Asset management • Market research

• Engineering • R&D • Design

When offshoring knowledge works, firms heavily rely on the availability of technical personnel at offshore locations. In order to secure access to talent, Western firms often establish collaborative relationships with technical universities abroad and thereby customise university programmes to serve their particular needs. Examples include institutions in Shanghai, such as Tong-Ji University, where German firms and scholars co-sponsor laboratories, courses, and provide internships. Similar examples of collaborative arrangements can be found in Eastern Europe, e.g. in Romania (Wikipedia, 2011).

Comparing the results of the Offshore Research Network surveys in 2004, 2005 and 2006, a shift in the importance of offshoring as a strategic driver to access to qualified personnel is clearly visible. It rose from 42% in 2004 to 68% in 2006 (Manning et al, 2008).

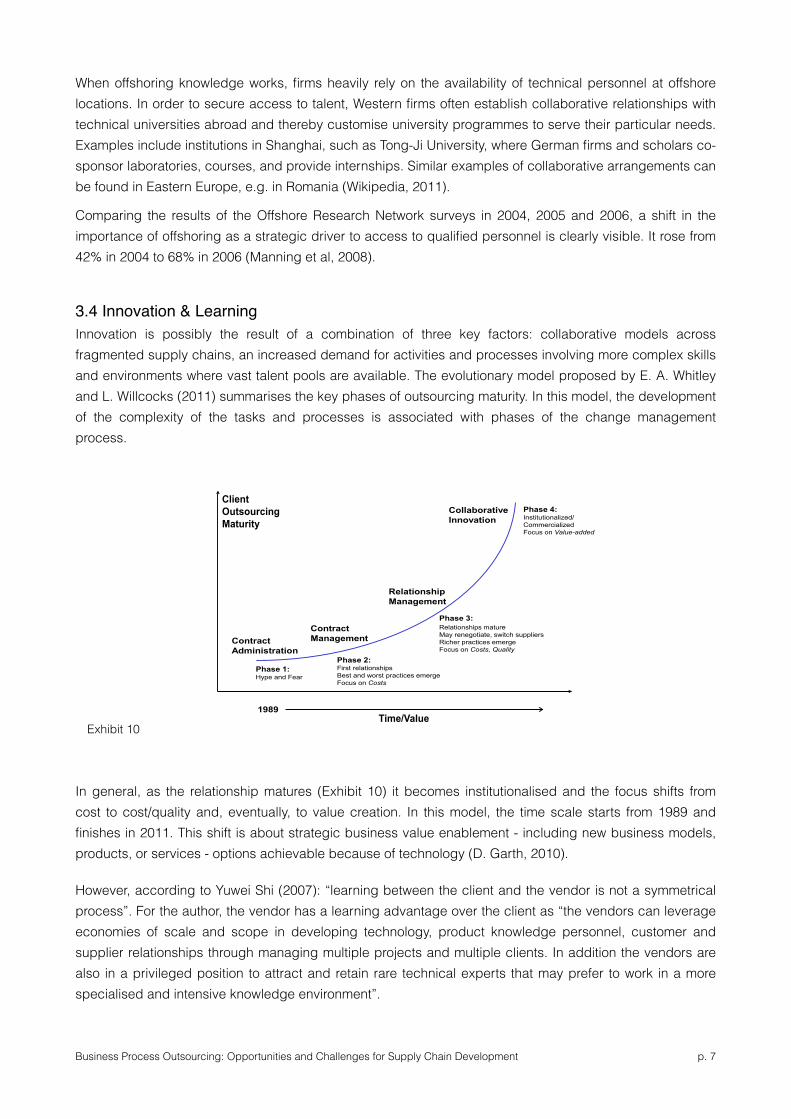

!3.4 Innovation & Learning !Innovation is possibly the result of a combination of three key factors: collaborative models across fragmented supply chains, an increased demand for activities and processes involving more complex skills and environments where vast talent pools are available. The evolutionary model proposed by E. A. Whitley and L. Willcocks (2011) summarises the key phases of outsourcing maturity. In this model, the development of the complexity of the tasks and processes is associated with phases of the change management process. !!!!!!!

!In general, as the relationship matures (Exhibit 10) it becomes institutionalised and the focus shifts from cost to cost/quality and, eventually, to value creation. In this model, the time scale starts from 1989 and finishes in 2011. This shift is about strategic business value enablement - including new business models, products, or services - options achievable because of technology (D. Garth, 2010).

However, according to Yuwei Shi (2007): “learning between the client and the vendor is not a symmetrical process”. For the author, the vendor has a learning advantage over the client as “the vendors can leverage economies of scale and scope in developing technology, product knowledge personnel, customer and supplier relationships through managing multiple projects and multiple clients. In addition the vendors are also in a privileged position to attract and retain rare technical experts that may prefer to work in a more specialised and intensive knowledge environment”.

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 7

Achieving Step-Change in Outsourcing Maturity: Toward Collaborative Innovation

© 2011 University of Minnesota MIS Quarterly Executive Vol. 10 No. 3 / Sep 2011 97

DEFINING COLLABORATIVE INNOVATION9

Studies of ITO and BPO engagements over the last 15 years have regularly reported that the rhetoric of strategic relationships, partnering, and innovation are very rarely converted into practices and superior outcomes.10 It is therefore important to understand what is meant by collaboration and innovation and how outsourcing clients see the roles of suppliers and themselves in facilitating the step-change in sourcing maturity needed for a new performance agenda.

CollaborationCollaboration is a co-operative arrangement in which two or more parties work jointly on a common enterprise toward a shared goal. In the context of business relationships, collaboration signals close partnering behaviors developed over and for the long term. These behaviors are characterized by the KLJK� WUXVW�� ÀH[LELOLW\�� ULVN� VKDULQJ�� DQG� LQYHVWPHQW� RI�

9 Figure 1 has been developed from Lacity, M. C., and Rottman, J. W. 2IIVKRUH�2XWVRXUFLQJ�RI�,7�:RUN� Palgrave Macmillan, 2008.��� 'LEEHUQ�� -��� *ROHV�� 7��� +LUVFKKHLP�� 5�� $��� DQG� %DQGXOD�� -��“Information systems outsourcing: a survey and analysis for the literature,” Database for Advances in Information Systems (34:4), 2004, pp. 6-102; Kern, T., and Blois, K. “Norm development in outsourcing relationships,” Journal of Information Technology (17:1), 2002, pp. 33-42.

resources and time essential if high performance on individual and shared goals is to be achieved.11

$OO� VXFFHVVIXO� RXWVRXUFLQJ� LV� EDVHG� RQ� D� JRRG�working relationship. But deeper, more trust-based relationships are required if external resources are to be used for more sophisticated, risk-bearing and critical services such as large-scale IT development projects, business process changes, and WHFKQRORJ\� LQQRYDWLRQV��$� VHQVH� RI� WKH� GLIIHUHQFH� LV�communicated by the following comments made by some of those we interviewed:

“The standard behavior in an organization is everybody does their job, they deliver it, and then somebody else goes and creates the same thing over and over again; but with collaboration comes leverage. In collaboration, you will be welcoming an DGYDQFH�IURP�PH�WR�EH�DEOH�WR�¿QG�RXW�KRZ�\RX�did it and to share it with me. Partnering is an ongoing relationship where you are leveraging the skills that your partner has and learn from them. Leadership is key in making progress in collaboration.” (IT Development Manager, Insure 2)

��� 2XU� GH¿QLWLRQ� RI� FROODERUDWLRQ� LV� FRQVLVWHQW� ZLWK� VWUDWHJ\�literature but not with earlier outsourcing literature. See also Kern, T., and Willcocks, L. P. The Relationship Advantage: Information Technologies, Sourcing and Management, Oxford University Press, 2000.

Figure 1: The Global Sourcing Learning Curve 1989-20119

Phase 1:Hype and Fear

Phase 2:First relationshipsBest and worst practices emergeFocus on Costs

Phase 3:Relationships matureMay renegotiate, switch suppliersRicher practices emergeFocus on Costs, Quality

Phase 4:Institutionalized/CommercializedFocus on Value-added

Contract Management

Relationship Management

Collaborative Innovation

ContractAdministration

Client Outsourcing Maturity

Time/Value1989

Exhibit 10

3.5 Other Key BPO DriversThe opportunity to use multiple time zones: for instance X-Ray scans made in US can be transmitted in India, where they are analysed and returned to US by the start of the next working day, with a substantial reduction of patient waiting time (C. W. Hill, 2011).!

Flexibility: BPO allows firms to retain their entrepreneurial speed and agility, which they would otherwise sacrifice in order to become efficient as they expanded. It avoids a premature internal transition from its informal entrepreneurial phase to a more bureaucratic mode of operation (K. Ramachandran et al, 2004).

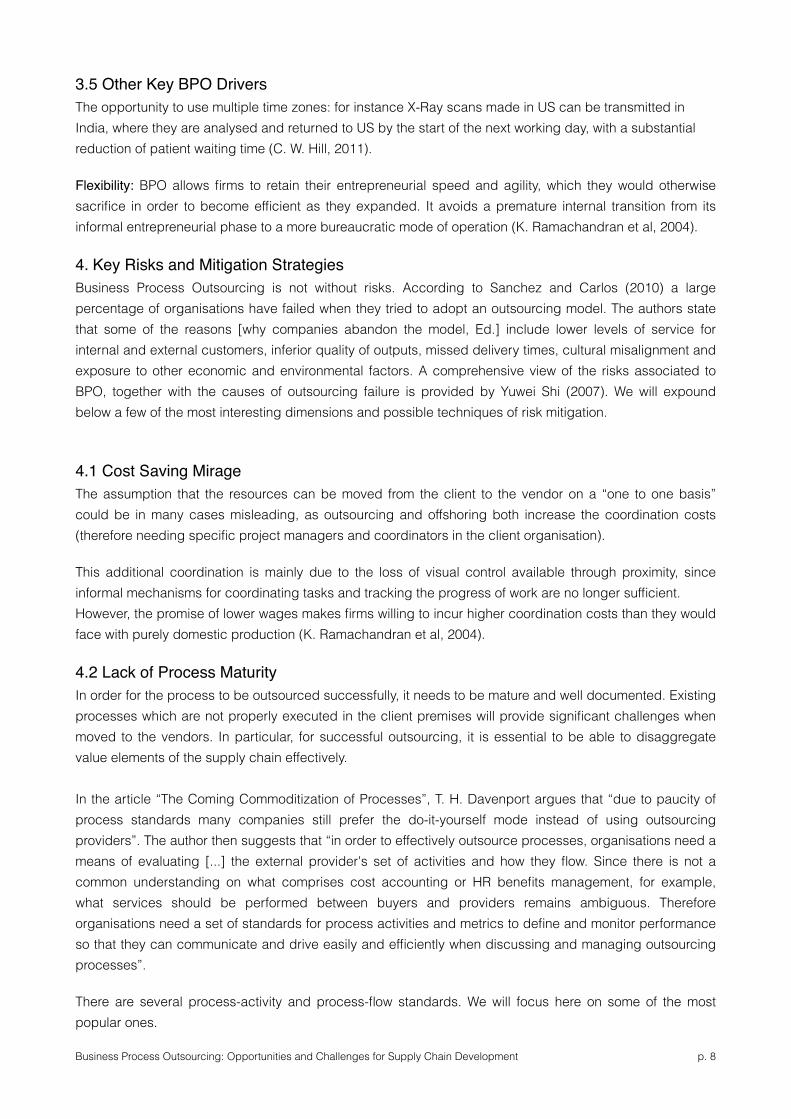

4. Key Risks and Mitigation Strategies !Business Process Outsourcing is not without risks. According to Sanchez and Carlos (2010) a large percentage of organisations have failed when they tried to adopt an outsourcing model. The authors state that some of the reasons [why companies abandon the model, Ed.] include lower levels of service for internal and external customers, inferior quality of outputs, missed delivery times, cultural misalignment and exposure to other economic and environmental factors. A comprehensive view of the risks associated to BPO, together with the causes of outsourcing failure is provided by Yuwei Shi (2007). We will expound below a few of the most interesting dimensions and possible techniques of risk mitigation. !4.1 Cost Saving Mirage The assumption that the resources can be moved from the client to the vendor on a “one to one basis” could be in many cases misleading, as outsourcing and offshoring both increase the coordination costs (therefore needing specific project managers and coordinators in the client organisation).

This additional coordination is mainly due to the loss of visual control available through proximity, since informal mechanisms for coordinating tasks and tracking the progress of work are no longer sufficient. However, the promise of lower wages makes firms willing to incur higher coordination costs than they would face with purely domestic production (K. Ramachandran et al, 2004).

4.2 Lack of Process MaturityIn order for the process to be outsourced successfully, it needs to be mature and well documented. Existing processes which are not properly executed in the client premises will provide significant challenges when moved to the vendors. In particular, for successful outsourcing, it is essential to be able to disaggregate value elements of the supply chain effectively. In the article “The Coming Commoditization of Processes”, T. H. Davenport argues that “due to paucity of process standards many companies still prefer the do-it-yourself mode instead of using outsourcing providers”. The author then suggests that “in order to effectively outsource processes, organisations need a means of evaluating [...] the external provider's set of activities and how they flow. Since there is not a common understanding on what comprises cost accounting or HR benefits management, for example, what services should be performed between buyers and providers remains ambiguous. Therefore organisations need a set of standards for process activities and metrics to define and monitor performance so that they can communicate and drive easily and efficiently when discussing and managing outsourcing processes”.

There are several process-activity and process-flow standards. We will focus here on some of the most popular ones.

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 8

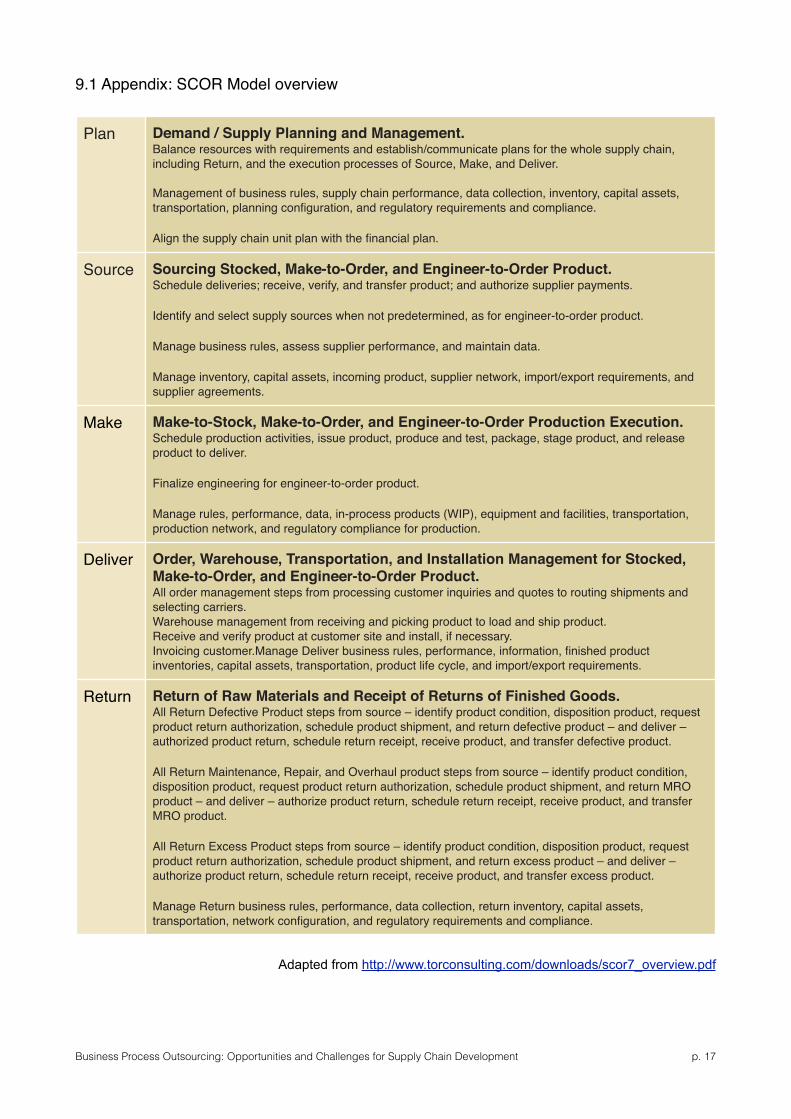

The Supply Chain Council has developed the Supply Chain Operating Reference (SCOR) model adopted by more than 800 businesses. The model is based on five key steps: Plan, Source, Make, Deliver and Return. For each of these steps the model covers 3 levels of detail specifying process elements, activities and tasks. Key Performance Indicators and measurement standards are also included in the model, providing a solid platform for process and performance definition (http://www.torconsulting.com/downloads/scor7_overview.pdf). A description of the key steps in the SCOR model can be found in appendix 9.1.

The Process Handbook is an initiative by a group of MIT researchers who has created a library describing more than 5,000 processes. In this impressive collection, the researchers focused on understanding what makes a company successfully execute its processes and how to create references (http://process.mit.edu/Info/eModels.asp).

CMMI (Capability Maturity Model Integration) is a process improvement approach that provides organisations with the essential elements of effective processes. The model defines 5 levels of execution maturity starting from a basic level 1, when a company has an initial approach towards process management and ending at level 5, when the company is constantly optimising and improving its processes (http://www.sei.cmu.edu/cmmi/). These frameworks can be applied to mitigate the risks of process outsourcing, to help understand the vendor capabilities, to define common expectations and Service Level Agreements as well as the level of process capability in the firm before making outsourcing decisions.

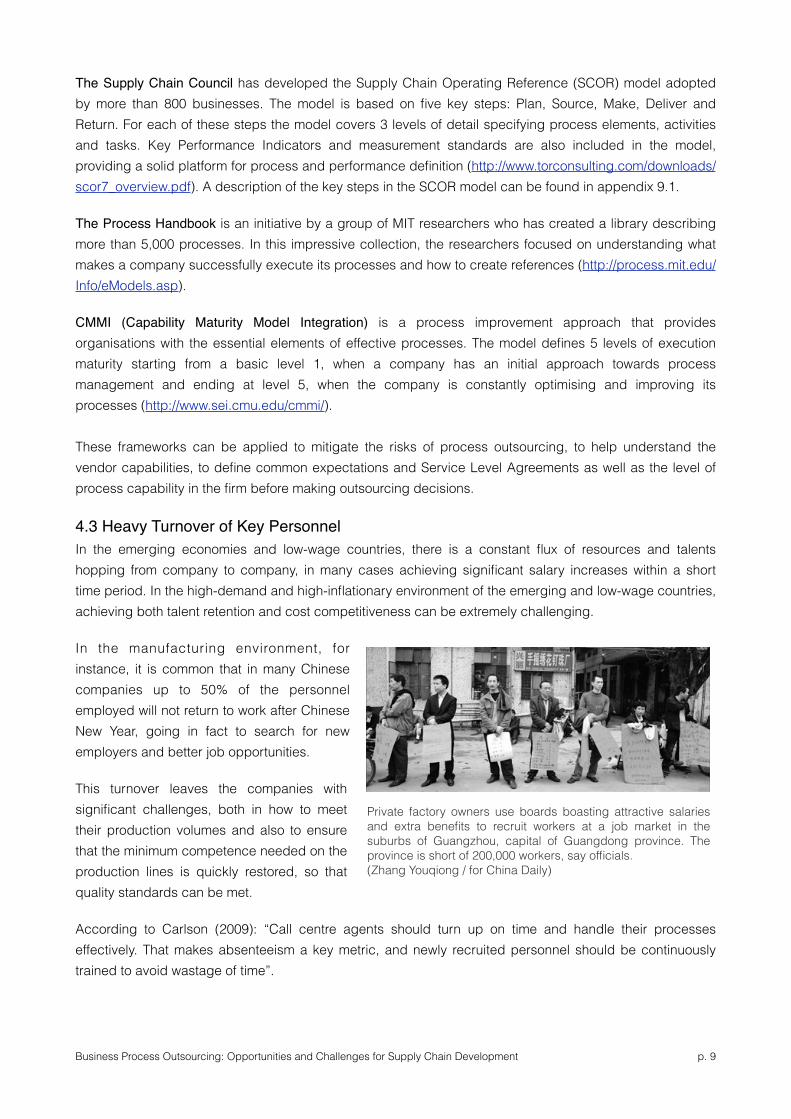

4.3 Heavy Turnover of Key Personnel In the emerging economies and low-wage countries, there is a constant flux of resources and talents hopping from company to company, in many cases achieving significant salary increases within a short time period. In the high-demand and high-inflationary environment of the emerging and low-wage countries, achieving both talent retention and cost competitiveness can be extremely challenging.

In the manufacturing environment, for instance, it is common that in many Chinese companies up to 50% of the personnel employed will not return to work after Chinese New Year, going in fact to search for new employers and better job opportunities.

This turnover leaves the companies with significant challenges, both in how to meet their production volumes and also to ensure that the minimum competence needed on the production lines is quickly restored, so that quality standards can be met.

According to Carlson (2009): “Call centre agents should turn up on time and handle their processes effectively. That makes absenteeism a key metric, and newly recruited personnel should be continuously trained to avoid wastage of time”.

!Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 9

Private factory owners use boards boasting attractive salaries and extra benefits to recruit workers at a job market in the suburbs of Guangzhou, capital of Guangdong province. The province is short of 200,000 workers, say officials. (Zhang Youqiong / for China Daily)

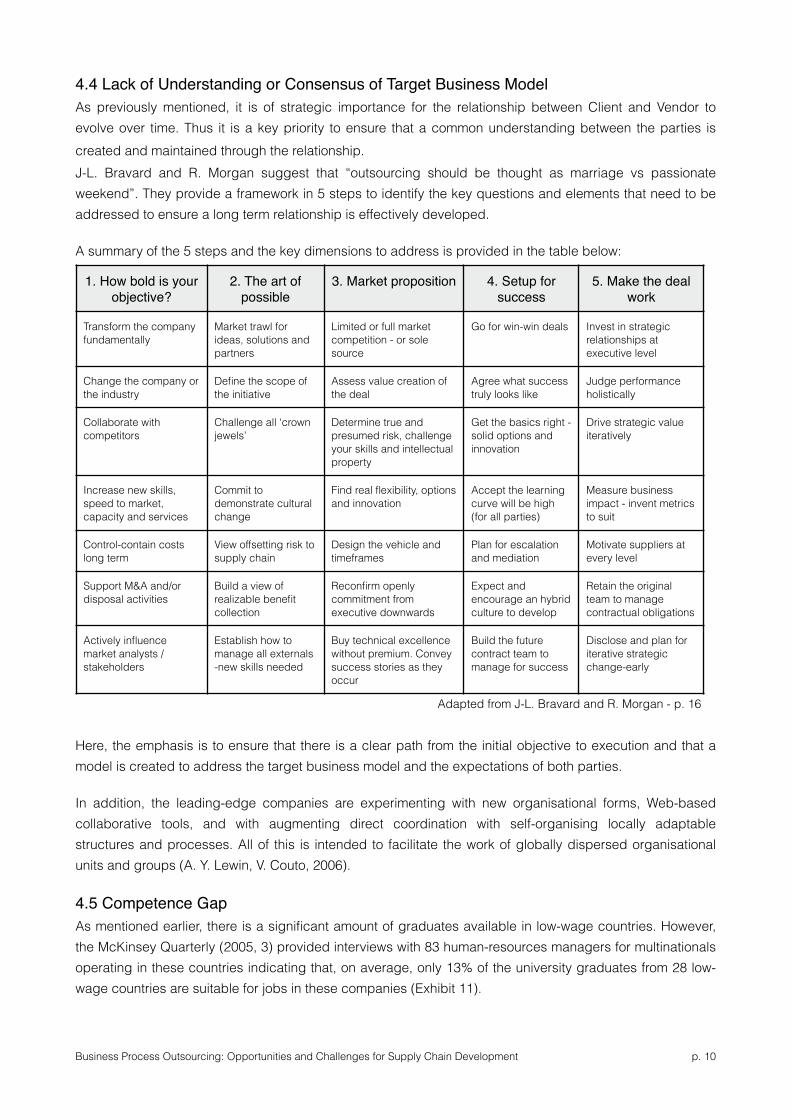

4.4 Lack of Understanding or Consensus of Target Business ModelAs previously mentioned, it is of strategic importance for the relationship between Client and Vendor to evolve over time. Thus it is a key priority to ensure that a common understanding between the parties is created and maintained through the relationship. J-L. Bravard and R. Morgan suggest that “outsourcing should be thought as marriage vs passionate weekend”. They provide a framework in 5 steps to identify the key questions and elements that need to be addressed to ensure a long term relationship is effectively developed.

A summary of the 5 steps and the key dimensions to address is provided in the table below:

Here, the emphasis is to ensure that there is a clear path from the initial objective to execution and that a model is created to address the target business model and the expectations of both parties.

In addition, the leading-edge companies are experimenting with new organisational forms, Web-based collaborative tools, and with augmenting direct coordination with self-organising locally adaptable structures and processes. All of this is intended to facilitate the work of globally dispersed organisational units and groups (A. Y. Lewin, V. Couto, 2006).

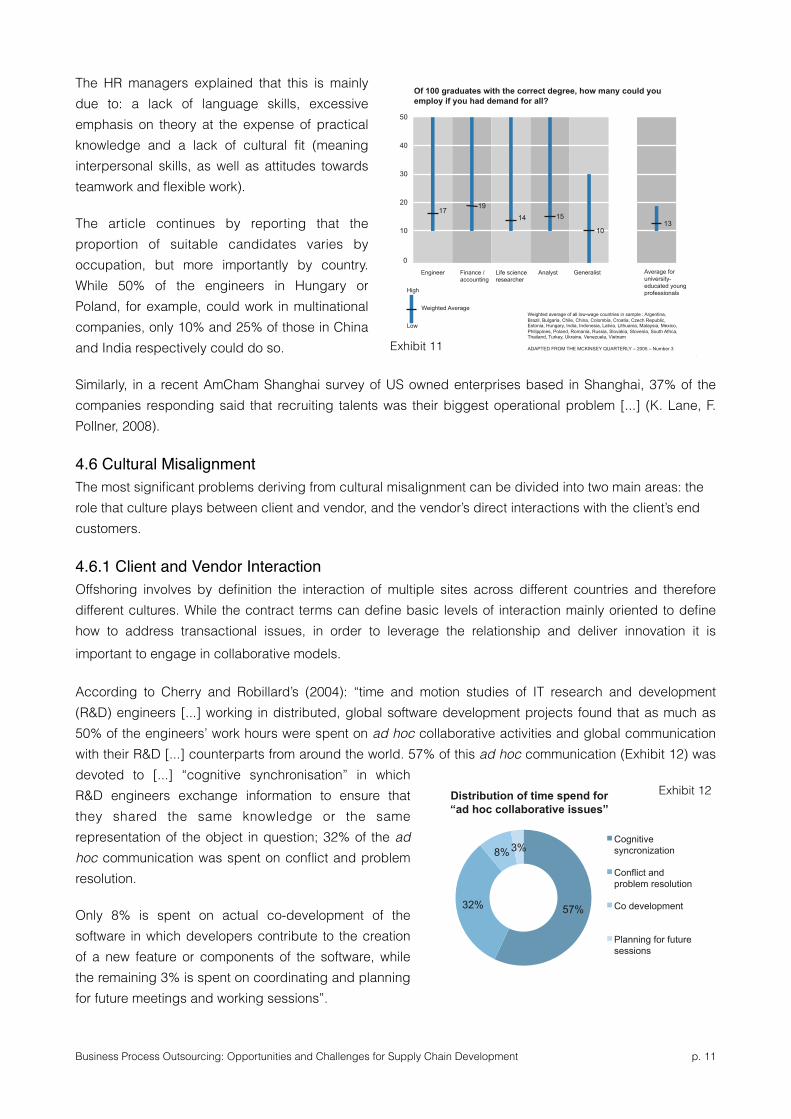

4.5 Competence Gap As mentioned earlier, there is a significant amount of graduates available in low-wage countries. However, the McKinsey Quarterly (2005, 3) provided interviews with 83 human-resources managers for multinationals operating in these countries indicating that, on average, only 13% of the university graduates from 28 low-wage countries are suitable for jobs in these companies (Exhibit 11).

1. How bold is your objective?

2. The art of possible

3. Market proposition 4. Setup for success

5. Make the deal work

Transform the company fundamentally

Market trawl for ideas, solutions and partners

Limited or full market competition - or sole source

Go for win-win deals Invest in strategic relationships at executive level

Change the company or the industry

Define the scope of the initiative

Assess value creation of the deal

Agree what success truly looks like

Judge performance holistically

Collaborate with competitors

Challenge all ‘crown jewels’

Determine true and presumed risk, challenge your skills and intellectual property

Get the basics right - solid options and innovation

Drive strategic value iteratively

Increase new skills, speed to market, capacity and services

Commit to demonstrate cultural change

Find real flexibility, options and innovation

Accept the learning curve will be high (for all parties)

Measure business impact - invent metrics to suit

Control-contain costs long term

View offsetting risk to supply chain

Design the vehicle and timeframes

Plan for escalation and mediation

Motivate suppliers at every level

Support M&A and/or disposal activities

Build a view of realizable benefit collection

Reconfirm openly commitment from executive downwards

Expect and encourage an hybrid culture to develop

Retain the original team to manage contractual obligations

Actively influence market analysts / stakeholders

Establish how to manage all externals -new skills needed

Buy technical excellence without premium. Convey success stories as they occur

Build the future contract team to manage for success

Disclose and plan for iterative strategic change-early

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 10

Adapted from J-L. Bravard and R. Morgan - p. 16

The HR managers explained that this is mainly due to: a lack of language skills, excessive emphasis on theory at the expense of practical knowledge and a lack of cultural fit (meaning interpersonal skills, as well as attitudes towards teamwork and flexible work).

The article continues by reporting that the proportion of suitable candidates varies by occupation, but more importantly by country. While 50% of the engineers in Hungary or Poland, for example, could work in multinational companies, only 10% and 25% of those in China and India respectively could do so.

Similarly, in a recent AmCham Shanghai survey of US owned enterprises based in Shanghai, 37% of the companies responding said that recruiting talents was their biggest operational problem [...] (K. Lane, F. Pollner, 2008).

4.6 Cultural MisalignmentThe most significant problems deriving from cultural misalignment can be divided into two main areas: the role that culture plays between client and vendor, and the vendor’s direct interactions with the client’s end customers. !

4.6.1 Client and Vendor Interaction Offshoring involves by definition the interaction of multiple sites across different countries and therefore different cultures. While the contract terms can define basic levels of interaction mainly oriented to define how to address transactional issues, in order to leverage the relationship and deliver innovation it is important to engage in collaborative models. !

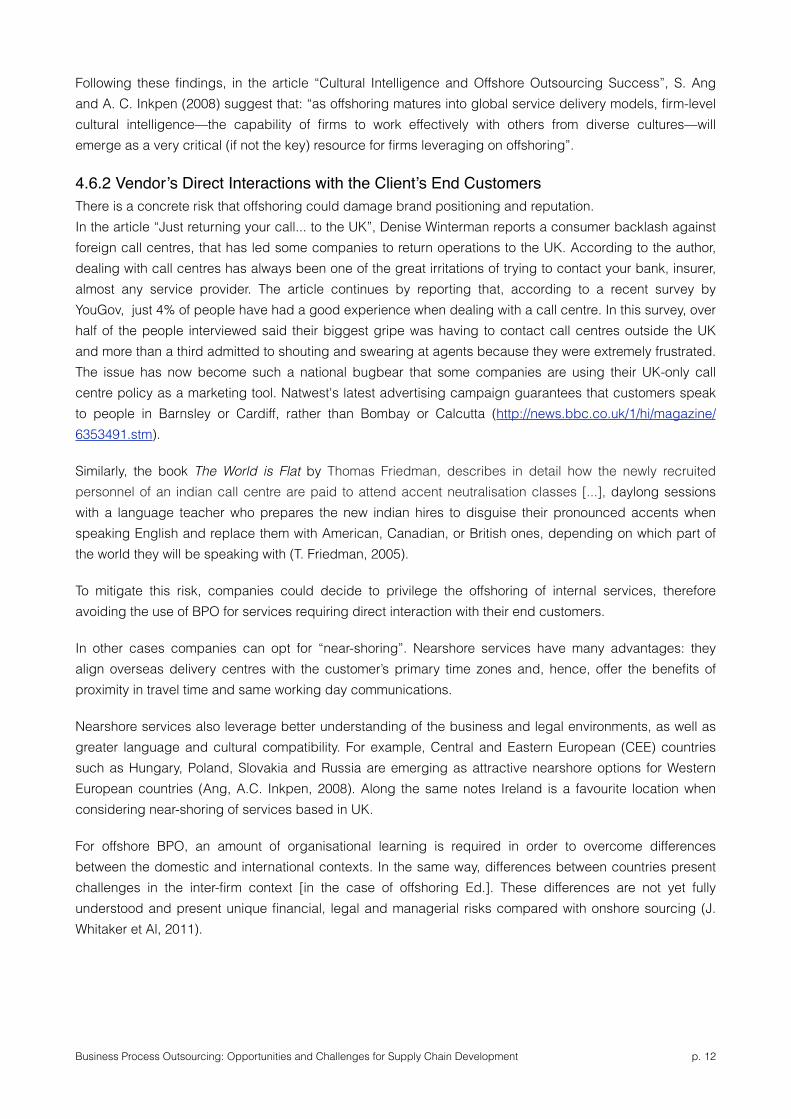

According to Cherry and Robillard’s (2004): “time and motion studies of IT research and development (R&D) engineers [...] working in distributed, global software development projects found that as much as 50% of the engineers’ work hours were spent on ad hoc collaborative activities and global communication with their R&D [...] counterparts from around the world. 57% of this ad hoc communication (Exhibit 12) was devoted to [...] “cognitive synchronisation” in which R&D engineers exchange information to ensure that they shared the same knowledge or the same representation of the object in question; 32% of the ad hoc communication was spent on conflict and problem resolution.

Only 8% is spent on actual co-development of the software in which developers contribute to the creation of a new feature or components of the software, while the remaining 3% is spent on coordinating and planning for future meetings and working sessions”.

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 11

0

10

20

30

40

50

Engineer Finance / accounting

Life science researcher

Analyst Generalist Average for university- educated young professionals

17 19

14 15

10 13

High

Low

Weighted Average Weighted average of all low-wage countries in sample : Argentina, Brazil, Bulgaria, Chile, China, Colombia, Croatia, Czech Republic, Estonia, Hungary, India, Indonesia, Latvia, Lithuania, Malaysia, Mexico, Philippines, Poland, Romania, Russia, Slovakia, Slovenia, South Africa, Thailand, Turkey, Ukraine, Venezuela, Vietnam

ADAPTED FROM THE MCKINSEY QUARTERLY – 2005 – Number 3

Of 100 graduates with the correct degree, how many could you employ if you had demand for all?

57% 32%

8% 3%

Distribution of time spend for “ad hoc collaborative issues”

Cognitive syncronization

Conflict and problem resolution

Co development

Planning for future sessions

Exhibit 12

Exhibit 11

Following these findings, in the article “Cultural Intelligence and Offshore Outsourcing Success”, S. Ang and A. C. Inkpen (2008) suggest that: “as offshoring matures into global service delivery models, firm-level cultural intelligence—the capability of firms to work effectively with others from diverse cultures—will emerge as a very critical (if not the key) resource for firms leveraging on offshoring”.

4.6.2 Vendor’s Direct Interactions with the Client’s End CustomersThere is a concrete risk that offshoring could damage brand positioning and reputation. In the article “Just returning your call... to the UK”, Denise Winterman reports a consumer backlash against foreign call centres, that has led some companies to return operations to the UK. According to the author, dealing with call centres has always been one of the great irritations of trying to contact your bank, insurer, almost any service provider. The article continues by reporting that, according to a recent survey by YouGov, just 4% of people have had a good experience when dealing with a call centre. In this survey, over half of the people interviewed said their biggest gripe was having to contact call centres outside the UK and more than a third admitted to shouting and swearing at agents because they were extremely frustrated. The issue has now become such a national bugbear that some companies are using their UK-only call centre policy as a marketing tool. Natwest's latest advertising campaign guarantees that customers speak to people in Barnsley or Cardiff, rather than Bombay or Calcutta (http://news.bbc.co.uk/1/hi/magazine/6353491.stm).!

Similarly, the book The World is Flat by Thomas Friedman, describes in detail how the newly recruited personnel of an indian call centre are paid to attend accent neutralisation classes [...], daylong sessions with a language teacher who prepares the new indian hires to disguise their pronounced accents when speaking English and replace them with American, Canadian, or British ones, depending on which part of the world they will be speaking with (T. Friedman, 2005).

To mitigate this risk, companies could decide to privilege the offshoring of internal services, therefore avoiding the use of BPO for services requiring direct interaction with their end customers.

In other cases companies can opt for “near-shoring”. Nearshore services have many advantages: they align overseas delivery centres with the customer’s primary time zones and, hence, offer the benefits of proximity in travel time and same working day communications.

Nearshore services also leverage better understanding of the business and legal environments, as well as greater language and cultural compatibility. For example, Central and Eastern European (CEE) countries such as Hungary, Poland, Slovakia and Russia are emerging as attractive nearshore options for Western European countries (Ang, A.C. Inkpen, 2008). Along the same notes Ireland is a favourite location when considering near-shoring of services based in UK.

For offshore BPO, an amount of organisational learning is required in order to overcome differences between the domestic and international contexts. In the same way, differences between countries present challenges in the inter-firm context [in the case of offshoring Ed.]. These differences are not yet fully understood and present unique financial, legal and managerial risks compared with onshore sourcing (J. Whitaker et Al, 2011).

!!Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 12

4.7 Geopolitical RisksAnother important dimension to highlight, following the recent unfortunate rise of terrorism, is that of geopolitical risk. Before venturing offshore, the company should examine any issues pertaining to border unrest, the religious makeup of the country, government policies, terrorism and other elements (A. B. Patel, H. Aran, 2005). Therefore it is important to ensure extreme scenarios can be properly managed.

A possible way to mitigate the geopolitical risks is to adopt a Business Continuity Management model (BCM). A good example of a BCM framework is provided by Financial Service Authority (FSA) in the form of a “Practice Guide” which has been based on the benchmark of 60 companies. The guide is grouped into 5 different modules: Corporate Continuity, Crisis Management, Systems, Facilities and People. For each of the modules, the framework provides an observed standard practice adopted by most of the benchmarking participants and leading practices that are observed in 20% of the benchmarking participants (Financial Service Authority, 2006).

4.8 Performance, Key Performance Indicators, Service Level AgreementsAccording to Ian S. Hayes of Clarity Consulting (2007): “Service Level Agreement (SLA) is an essential part of any outsourcing project. It defines: the boundaries of the project in terms of functions and the service that the provider will give to its clients; the volume of the work that will be accepted and delivered; the acceptance criteria for responsiveness; the quality of the deliverables. A well defined and crafted SLA correctly sets expectations for both sides of the relationship and provides targets for accurately measuring performance to those objectives”. While a well defined SLA can support a successful implementation of BPO, when the services provided become more articulate and the partnership develops from transactional to innovative, the definition of effective Key Performance Indicators can be extremely difficult and complex.

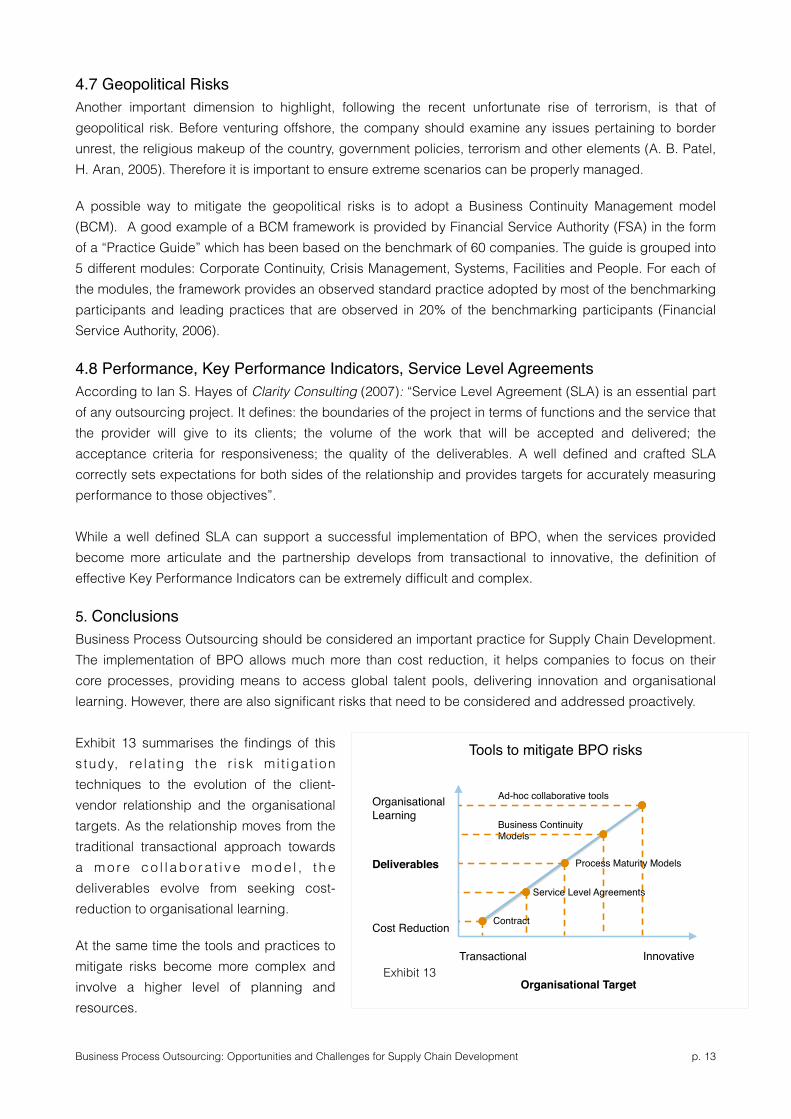

5. ConclusionsBusiness Process Outsourcing should be considered an important practice for Supply Chain Development. The implementation of BPO allows much more than cost reduction, it helps companies to focus on their core processes, providing means to access global talent pools, delivering innovation and organisational learning. However, there are also significant risks that need to be considered and addressed proactively. Exhibit 13 summarises the findings of this s tudy, re la t ing the r isk mi t igat ion techniques to the evolution of the client-vendor relationship and the organisational targets. As the relationship moves from the traditional transactional approach towards a m o re c o l l a b o r a t i v e m o d e l , t h e deliverables evolve from seeking cost-reduction to organisational learning.

At the same time the tools and practices to mitigate risks become more complex and involve a higher level of planning and resources.

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 13

Innovative!Transactional !

Cost Reduction !

Organisational !Learning!

Ad-hoc collaborative tools!

Business ContinuityModels!

Organisational Target !

Deliverables!

Contract !

Process Maturity Models!

Service Level Agreements !

Tools to mitigate BPO risks !

Exhibit 13

Business Process Outsourcing can become an integral part of the corporate strategy and provide significant Supply Chain advantages, however these opportunities can be realised only with the right level of maturity of the client and the vendor, with the adoption of the correct risk management approach.

At the same time cultural awareness plays an essential role especially when the partnership is expected to deliver innovation.

In the near future it is not difficult to imagine that globalisation will drive higher customer services expectations. For instance constant availability (24/7) of call centres could be delivered as a standard for every service. To fulfil these customer expectations within sustainable cost levels, small and medium enterprises will need to implement Business Process Outsourcing.

To compete in this new market place, companies will have to engage with a dispersed network of vertically specialised process providers, which will leverage scale economies and innovation for their customers, creating new cost structures and business models that will bring new service capabilities into the markets.

A more demanding customer will be effectively driving this revolution creating a new world of agile supply chains that will leverage their service providers.

!!!!!!!!!!!!!!Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 14

6. References!

A. Y. Lewin, V. Couto, 2006, 2006 Report, Next Generation Offshoring, The Globalization of Innovation, ORN, Duke University and Booz Allen Hamilton.

Alex Carlson, 16-Sep 2009, The Risks in BPO Services, Article Niche.

Arie Y. Lewin, Feb 2009, Getting Serious about Offshoring in a Struggling Economy, Shared Services News.

Charles W. Hill, 2011, International Business: Competing in the Global Marketplace, 8th edition McGraw Hill.

Cherry, S. and Robillard, P. N., 2004, Communication Problems in Global Software Development: Spotlight on a New Field of Investigation. In ISCE (Ed.). Proceedings of the International Workshop on Global Software Development, International Conference on Software Engineering, Edinburgh, Scotland, pp. 48–52.

Diana Farrell, June 2006, Smarter Offshoring, Harvard Business Review.

Diana Farrell, M. A. Laboissiere, and J. Rosenfeld, 2005, Sizing the Emerging Global Labour Market, The McKinsey Quarterly, Number 3.

Denise Garth, November 22/29, 2010, New Business Process Outsourcing: A Strategic Building Block for Innovation, National Underwriter, Property & Casualty, pp. 24,25.

E.A. Whitley and L. Willcocks, Sep 2011, Achieving Step-Change in Outsourcing Maturity: Toward Collaborative Innovation, MIS Quarterly executive, Vol. 10, No. 3, pp. 95-107.

Ian S. Hayes, 2007, Creating Better Service Level Agreements, Clarity Consulting.

Jean-Louis Bravard, Robert Morgan, 2006, Smarter Outsourcing, FT Prentice Hall.

Jonathan Whitaker, Sunil Mithas, and M.S. Krishnan, Winter 2010-11, Organizational Learning and Capabilities for Onshore and Offshore Business Process Outsourcing, Journal of Management Information Systems, Vol. 27, No. 3, pp. 11-42.

K.Ramachandran, Sudhir Voleti, Vikalpa, January-March 2004, Business Process Outsourcing (BPO): Emerging Scenario and Strategic Options for IT enabled services, Vol. 29, No.1.

Kevin Lane and Florian Pollner, 2008, How to Address China’s Growing Talent Shortage, The McKinsey Quarterly, Number 3.

Peter Weill, Thomas W. Malone, Victoria T. D’ Urso, George Herman and Stephanie Woerner, May 2004, Do Some Business Models Perform better than Others? A study of the 1000 largest firms, MIT 6.

Prasanna B. Tambe and Lorin M. Hitt, October 2010, How Offshoring Affects IT Workers, Communications of the ACM, Vol. 53, No.10.

Sanchez and Carlos, May / June 2010, Ivey Business Journal, 4818248, Vol. 74, Issue 3.

S. Ang and A.C. Inkpen, August 2008, Cultural Intelligence and Offshore Outsourcing Success, Decision Sciences 2008, The Author Volume 39 Number 3 Journal compilation 2008, Decision Sciences Institute.

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 15

S. Helper and Mari Sako, Management Innovation in Supply Chain: Appreciating Chandler in the Twenty-First Century, Industrial and Corporate Change, Volume 19, Number 2, pp 399-429.

Stephan Manning, Silvia Massini and Arie Y. Lewin, 2008, A Dynamic Perspective on Next-Generation Offshoring: The Global Sourcing of Science and Engineering Talent, Academy of Management Perspectives.

Thomas Friedman, Farrar, Strauss and Giroux, 2005, The World is Flat: A brief history of twenty-first century.

Thomas H. Davenport, June 2005, The Coming Commoditization of Processes, Harvard Business Review.

Vinay Couto, Mahadeva Mani, Arie Y. Lewin, Dr. Carine Peeters, The Globalization of White-Collar Work - the Facts and Fallout of Next Generation Offshoring, Booz Allen Hamilton and Offshoring Research Network.

Yuwei Shi, Spring 2007, Today’s Solution and Tomorrow’s Problem: the Business Process Outsourcing Risk Management Puzzle, California Management Review, Vol. 49, no. 3.

7. Bibliography !

A. B. Patel, H. Aran, 2005, Outsourcing Success: The Management Imperative, Palgrave.

Diana Farrell, December 2004, Beyond Offshoring Assess your Company’s Global Potential, Harvard Business Review.

Jason Amaral, Geoffrey Parker, September 2008, Preventing Disasters in Design Outsourcing, Harvard Business Review, p. 30.

(Edited by) Paul Strebel, 2000, Focused Energy: Mastering Bottom-up Organization, IMD, Wiley.

8. Websites!

Capability Maturity Model Integration - reference from http://www.sei.cmu.edu/cmmi/

D. Winterman, Just returning your call..to the UK, BBC News Magazine, http://news.bbc.co.uk/1/hi/magazine/6353491.stm Qiu Quanlin, Gao Changxin, 2010, Workers call the shots, China Daily, http://www.chinadaily.com.cn/cndy/2010-03/11/content_9570417.htm!Financial Service Authority, Business Continuity Management Practice Guide, http://www.fsa.gov.uk/pubs/other/bcm_guide.pdf

IT and Financial Service Outsourcing Lead Investment Values in Tier-2 Cities, CCID Consulting, April 2009, www.en.ccidconsulting.com/en/io/mr/mr/cs/webinfo/2010/04/1272329397146739.htm

IT Definitions and Glossary, Gartner, www.gartner.com/technology/it-glossary/#bpm Process Handbook - MIT http://process.mit.edu/Info/eModels.asp

Supply Chain Council - SCOR Model Reference http://www.torconsulting.com/downloads/scor7_overview.pdf

Wikipedia, http://www.en.wikipedia.org/wiki/Offshoring

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 16

9.1 Appendix: SCOR Model overview!

Adapted from http://www.torconsulting.com/downloads/scor7_overview.pdf

!

Plan!

!Demand / Supply Planning and Management.Balance resources with requirements and establish/communicate plans for the whole supply chain, including Return, and the execution processes of Source, Make, and Deliver. Management of business rules, supply chain performance, data collection, inventory, capital assets, transportation, planning configuration, and regulatory requirements and compliance.!

Align the supply chain unit plan with the financial plan.

Source Sourcing Stocked, Make-to-Order, and Engineer-to-Order Product.Schedule deliveries; receive, verify, and transfer product; and authorize supplier payments.!

Identify and select supply sources when not predetermined, as for engineer-to-order product.!

Manage business rules, assess supplier performance, and maintain data.!

Manage inventory, capital assets, incoming product, supplier network, import/export requirements, and supplier agreements.

Make! Make-to-Stock, Make-to-Order, and Engineer-to-Order Production Execution. Schedule production activities, issue product, produce and test, package, stage product, and release product to deliver.!

Finalize engineering for engineer-to-order product.!

Manage rules, performance, data, in-process products (WIP), equipment and facilities, transportation, production network, and regulatory compliance for production.

Deliver Order, Warehouse, Transportation, and Installation Management for Stocked, Make-to-Order, and Engineer-to-Order Product.All order management steps from processing customer inquiries and quotes to routing shipments and selecting carriers.Warehouse management from receiving and picking product to load and ship product.Receive and verify product at customer site and install, if necessary.Invoicing customer.Manage Deliver business rules, performance, information, finished product inventories, capital assets, transportation, product life cycle, and import/export requirements.

Return Return of Raw Materials and Receipt of Returns of Finished Goods.All Return Defective Product steps from source – identify product condition, disposition product, request product return authorization, schedule product shipment, and return defective product – and deliver – authorized product return, schedule return receipt, receive product, and transfer defective product.!

All Return Maintenance, Repair, and Overhaul product steps from source – identify product condition, disposition product, request product return authorization, schedule product shipment, and return MRO product – and deliver – authorize product return, schedule return receipt, receive product, and transfer MRO product.!

All Return Excess Product steps from source – identify product condition, disposition product, request product return authorization, schedule product shipment, and return excess product – and deliver – authorize product return, schedule return receipt, receive product, and transfer excess product.!

Manage Return business rules, performance, data collection, return inventory, capital assets, transportation, network configuration, and regulatory requirements and compliance.

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 17

9.2 Appendix: Factors in choosing a location

!

(Smarter Offshoring, Diana Farrell, HBR June 2006 p. 88)

instance, we project that the supplies of support staff andyoung professional generalists suitable for employmentby multinational companies in emerging markets will ex-ceed demand by 98% and 78%, respectively, in 2008. Onlythe aggregate supply of engineers in low-wage countrieslooks as though it will be a little tight. (See the exhibit“The Supply and Demand Outlook.”)

The bright outlook for the overall supply of low-wagetalent is due in large part to the robust growth in thenumber of university graduates that developing countriesare churning out: 5.5% per year, compared with an annualincrease of just 1% in developed countries. Of course, de-veloped countries have a larger base of graduates, butfaster growth in the developing world’s graduate pool isclosing the gap.

For instance, in 2003, there were about 30% fewer engi-neers in low-wage economies than in high- and mid-wagecountries. By 2008, when young professional engineersworldwide will number more than 2 million, that gap willbe 18%. The supply of suitable finance and accounting pro-fessionals from developing countries will outnumberthose from high-wage ones by that time. Growth in thesupply of graduates with qualifications that multination-als most desire is particularly rapid: In just five years, theproportion of degrees awarded in business and econom-ics has jumped from 18% to 31% of the total in Russia andfrom 16% to 36% of the total in Poland.

The huge aggregate supply of competent professionalsavailable for hire in emerging markets means that theiraverage wages will remain relatively low for the foresee-

Smarter Offshoring

88 harvard business review

FACTORS IN CHOOSING A LOCATIONTo make the right offshoring decisions, companies should assemble detailed information on a number of factors:

Cost

• Labor: current average wages for skilled workers andmanagers

• Infrastructure: unit costs for telecom networks,Internet access, and power

• Real estate: cost of class A office space

• Corporate taxes: the total tax burden or, conversely, thetax breaks and other incentives for local investment

Availability of Skills

• Skill pool: size of labor force with the required skills

• Size of offshore sector: dollar volume and share of employment in the sector, as well as share of theseservices as a percentage of total exports

• Vendor landscape: size of local sector providing IT services and other business functions

Environment

• Government support: policy on foreign investment,labor laws, bureaucratic and regulatory burden, andlevel of corruption

• Business environment: compatibility with prevailing business culture and ethics

• Living environment: overall quality of life, prevalence of HIV infection, and serious crimes per capita

• Accessibility: travel time, flight frequency, and time difference

Market Potential

• Attractiveness of local market: current GDP and GDP growth rate

• Access to nearby markets: in the host country and adjacent region

Risk Profile

• Disruptive events: risk of labor uprising, political unrest, and natural disasters

• Security: risks to personal security and property from fraud, crime, and terrorism

• Regulatory risk: stability, fairness, and efficiency of legal framework

• Macroeconomic risk: cost inflation, currency fluctuation, and capital freedom

• Intellectual-property risk: strength of data and IP protection regime

Quality of Infrastructure

• Telecom and IT: network downtime, speed of servicerestoration, connectivity

• Real estate: availability and quality

• Transportation: scale and quality of road and rail network

• Power: reliability of power supply

Business Process Outsourcing: Opportunities and Challenges for Supply Chain Development p. ! 18

Related Documents